22

To prepare a sell side pitch-book for a chemical company in North American region by Varun Baxi 15P055 Management Development Institute Gurgaon 122 007 June 2016 1 | Page

| Date post: | 07-Jul-2016 |

| Category: |

Documents |

| Upload: | varun-baxi |

| View: | 215 times |

| Download: | 0 times |

To prepare a sell side pitch-book for a chemical company in North American region

by

Varun Baxi

15P055

Management Development InstituteGurgaon 122 007

June 2016

1 | P a g e

To prepare a sell side pitch-book for a chemical company in North American region

byVarun Baxi

15P055

Under the guidance of

Mayank KumarVice President,

JP Morgan

Management Development InstituteGurgaon 122 007

June 2016

2 | P a g e

Certificate of Approval

Name: Varun BaxiRoll No: 15P055

Table of Contents3 | P a g e

Certificate of Approval ..................................................................FOREWARD...................................................................................ACKNOWLEDGEMENT.....................................................................EXECUTIVE SUMMARY....................................................................LIST OF ABBREVIATIONS:...............................................................SPECIALTY CHEMICALS SECTOR- AN OVERVIEW...............................TARGET SELECTION......................................................................11BUYERS’ UNIVERSE......................................................................13VALUATIONS................................................................................14FOOTBALL FIELD ESTIMATES........................................................15DEAL STRUCTURE........................................................................16ACCRETION/ DILUTION ANALYSIS..................................................17REFERENCES...............................................................................18

4 | P a g e

FOREWARD

The project attempts to understand the specialty Chemical sector in NA markets region and

thereby leverage the knowledge in finding consolidation opportunities in this space. Specialty

chemicals industry varies in terms of sophistication as we move around the globe. Some

regions like USA, China witness a lot of fragmentation in the specialty chemicals. Specialty

chemicals is a diversified space with chemicals having a spectrum of end market usage.

Given the huge addressable market, strong long term tailwinds favoring technology

development and quality control, uncertainty about the global outlook and chemical sector

being heavily export oriented the best way of reaping maximum profits from specialty

chemicals industry is via consolidation. The focus of my study was to find a player in

specialty chemicals industry whose shareholders could gain by being a part of a bigger

company in similar space. The player that I finally identified is a market leader in bromine

and bromine affiliated industry. 96% of the shares in the listed entity are held by institutional

share holders making it a easily salable company. management has been reiterating their

intentions of being a part of the larger entity to unlock the share holders value. The project

deals with identifying the most suitable targets for our client, the strategic rationale,

preliminary valuations and combination analysis.

5 | P a g e

ACKNOWLEDGEMENT

First and foremost I would like to thank J.P. Morgan for giving me an opportunity to intern in investment banking division. The internship gave me an opportunity to interact with some of the brightest minds in the industry. I got a fairly good exposure to the US markets and to the Metals, Mining and Chemicals sector of Europe and North America thanks to the internship. I would like to thank my organizational guide, Mr. Mayank Kumar, VP and sector head, Metals, Mining and Chemicals at CRG Division, JP Morgan Chase & Co., for helping me out throughout the project at various junctures. His valuable insights helped me in coming up with quality output in minimum time. I would also like to thank Mr. Sanil Chaudhari(project mentor), Mr. Atul Sehgal(Analyst, MMC), Mr. Shridhar Jadhav (Analyst, MMC), Mr. Anirudh Mittal (Analyst, MMC), Mr. Ankit Pai(JA, MMC) for their incessant support during the internship. I would also like to thank Mr. Ankur Jain, Ms Snehankita Bose from the HR department for arranging a well-planned internship schedule which involved quality training sessions and interaction with the industry veterans.

I thank faculty members of finance, marketing, operations and strategy for helping us widen our horizons and come out of the proverbial shell.

Finally, I would like to thank MDI peers and alumni members for their constant support and guidance that helped me clear my confusions and doubts regarding maneuvering through the investment banking industry.

EXECUTIVE SUMMARY

6 | P a g e

My project involved finding suitable targets in the chemicals sector on the sell side and then finding suitable buyers for them. In the beginning of my project, I studied extensively about the specialty chemical industry in the world identifying the key markets, the key growth areas, the different sub-divisions of the industry, major players in the global specialty chemicals industry and also in the key geographies, the entire value chain of the industry, and the financials of the players including top line, bottom line, margins etc.

After careful analysis of the sector, I identified a very prevalent theme in the specialty chemicals sector in North America. Companies are in the process of value chain integration and portfolio diversification amidst sustained downward pricing pressure and gap in valuation expectations. To survive the global uncertainty and to diversify the risk given the prevailing uncertainty regarding oil prices and global growth companies in the chemical space are diversifying their product portfolio.

After careful consideration, I identified a US based specialty chemical player in bromine and fuel additive space, with high leverage, subscale operations, low valuation and management’s willingness to be the part of bigger group.

Key considerations for the seller was high leverage, oligopolistic industry nature, low valuations, and subscale operations and unattractive product portfolio. The declining margins from bromine business in the past few years and untapped growth potential and lack of insider ownership – making an easy target. Also there has been a recent uptick in acquisition activities of specialty chemical players.

Key considerations for the buyer was product portfolio diversification, Market leadership in the bromine market and vertical downstream integration in the fuel additive business

LIST OF ABBREVIATIONS:

MMC: Metals. Mining and Chemicals

7 | P a g e

CRG: Centralized Research Group NA: North America EMEA: Europe, Middle East and AsiaDCF: Discounted Cash Flow WACC: Weighted average cost of capital GDP: Gross domestic product

SPECIALTY CHEMICALS SECTOR- AN OVERVIEW

8 | P a g e

Specialty chemicals are produced by a complex, interlinked industry. In the strictest sense, specialty chemicals are chemical products that are sold on the basis of their performance or function, rather than for their composition. They can be single-chemical entities or formulations (combinations of several chemicals) whose composition sharply influences the performance and processing of the customer’s product. Products and services in the specialty chemicals industry require intensive knowledge and ongoing innovation.Commodity chemicals are sold strictly on the basis of their chemical composition. They are single-chemical entities. The commodity chemical product of one supplier is generally readily interchangeable with that of any other.

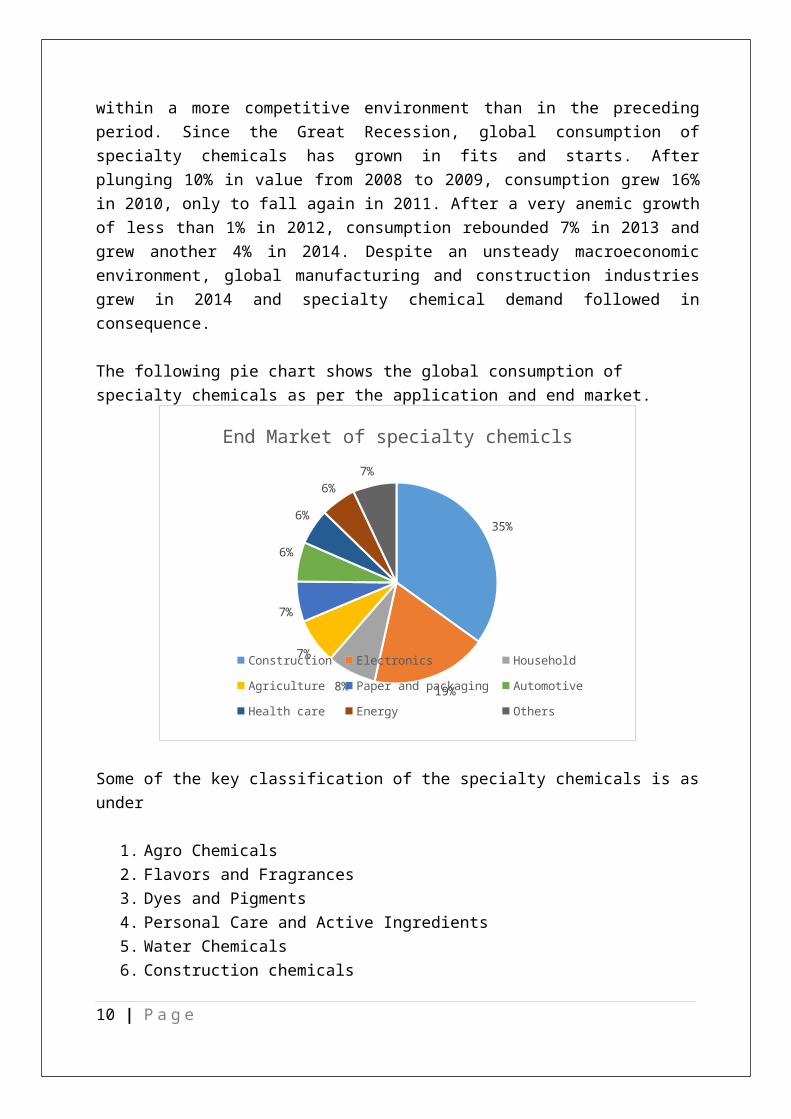

During the last 10 years, the specialty chemicals industry has experienced slower growth and lower overall profitability within a more competitive environment than in the preceding period. Since the Great Recession, global consumption of specialty chemicals has grown in fits and starts. After plunging 10% in value from 2008 to 2009, consumption grew 16% in 2010, only to fall again in 2011. After a very anemic growth of less than 1% in 2012, consumption rebounded 7% in 2013 and grew another 4% in 2014. Despite an unsteady macroeconomic environment, global manufacturing and construction industries grew in 2014 and specialty chemical demand followed in consequence.

The following pie chart shows the global consumption of specialty chemicals as per the application and end market.

35%

19%8%

7%

7%

6%

6%

6%7%

End Market of specialty chemicls

Construction Electronics Household Agriculture

Paper and packaging Automotive Health care Energy

Others

Some of the key classification of the specialty chemicals is as under

9 | P a g e

1. Agro Chemicals2. Flavors and Fragrances3. Dyes and Pigments4. Personal Care and Active Ingredients5. Water Chemicals6. Construction chemicals 7. Surfactants8. Textile chemicals 9. Polymer additives

10 | P a g e

TARGET SELECTION

After having obtained the sectorial outlook, I decided to zero in on the key attributes of potential sell side target. Some of the attributes of specialty chemicals industry like product portfolio, geographical footprint, leverage ratios and valuations were worth an attention. If opportunities of any landmark consolidation would help in increasing the total addressable market of the newly formed entity was also a key consideration. Also I considered the opportunity if the smaller entity could benefit from being a part of larger distribution network, given the extreme consolidation in the industry.

One of the key pre-requisites of identifying suitable sell side target is the willingness of the existing shareholders to let an outsider acquire the company. So, I decided to focus on management discussion and analysis with regards to potential sell side opportunities. It is worthless to pitch to an unwilling client. Also I considered the feasibility of the acquisition by looking at the current share holding pattern in the listed entity. High institutional holding makes it easy for the company to get acquired as the institutional share holders will be easily willing to go off their holding for better value

Regulatory barriers that arise as a result of potential antitrust violations have potential to break landmark acquisitions. Hence, merger of 2 companies with dominant market position would be unfeasible and was ruled out in the first go.

I used internal database of JP Morgan to sift through the management commentaries of various companies in the specialty chemicals sector. Most of the companies searched were currently in an inorganic development stage. Given the high consolidation phase that specialty chemical sector is currently undergoing. Given the growth and development the sector is undergoing it was initially difficult to find the company that would be willing to sell itself, In fact many companies were in an acquisition mode, thereby giving strong signals against potential sell side opportunities.

During my search for potential targets, I came across one of the market leader in bromine and bromine affiliate business, ABC which had 96% of institutional shareholding in the firm and had recovered from the bankruptcy in 2011. The Chairman and CEO made public proclamation of his willingness to be a part of a bigger entity by either a sell or an acquisition, However given a high debt on its balance sheet the prospects of acquisition looked bleak. The subscale operations and unattractive product portfolio has been a main hindrance for the company in unlocking the share holder’s value. Given the market leadership in the bromine business and the ongoing theme of inorganic growth prevalent in the industry there would be an ample number of buyers willing to acquire this company.

Some of the key positives of this company are as follows: Market leadership in bromine and affiliate business Broad global reach with robust supply and distribution network Strong and efficient management Strong industry position

11 | P a g e

I decided to pursue this company as the sell-side opportunity and thereby prepare a pitchbook for the same.

12 | P a g e

BUYERS’ UNIVERSE

After having decided on the sell side opportunity, I decided to finalize the list of potential buyers.Some of the factors considered while arriving at Buyers universe were:

1. Management willingness to pursue inorganic growth opportunities

2. Market leadership in the oligopolistic market

3. Financials of buyer and its credit ratings must resonate with management willingness to pursue inorganic growth

4. Potential synergies that arise as a result of merger

5. Accretive/ dilutive effects of merger

Apart from this I considered following factors for the potential suitors:

1. Strategic fit: There should be significant convergence in the long term strategies of the potential pair

2. Action-ability of the deal: The deal must successfully clear the regulatory hurdles in all jurisdictions and close in foreseeable period

I shortlisted players in specialty chemicals division having the significant presence in the product category offered by the sell side target. Players who intended to make inroads into the product categories of bromine and affiliate markets, Fuel additives and organometallics. Players who would like to integrate their value chain giving them the strong synergies and strategic advantage. We applied various criteria as listed above and arrived at final shortlist of potential suitors. In the end I arrived at the cumulative score based on the affordability, action-ability and applicability to finally arrive at a buyer.

Some of the characteristics of the firm XYZ which make it a potential suitor are as follows:

1. Second largest player in the bromine business and acquisition would make it the largest player in the bromine and affiliate business globally.

2. Strategic fit and added synergies from other businesses of our sell side target through vertical integration

3. Significant track record of successful closures of acquisition deals4. Managements willingness to make an acquisition5. Strong balance sheet and high debt capacity6. Accretive effect of the potential merger would deliver straight boost to the stock price

with immediate effect

13 | P a g e

VALUATIONS

To justify the sell side opportunity to the management of ABC, we needed to show them detailed valuations of ABC and thereby justify the price being paid.

We performed following analysis of the financials of ABC.

1. Discounted Cash Flows2. Analysis at various prices3. Preceding Transaction Comparables (EV Multiples and P/E multiples)4. Trading comparables of related companies (EV Multiples and P/E multiples) 5. Market valuation

A football field of the above valuation estimates indicated that the deal was happening at a fair price.Due to confidential nature of the above project, the detailed valuations cannot be shared across in hard copy based format.

14 | P a g e

FOOTBALL FIELD ESTIMATES

Football field is a summary of the results of valuations arrived at using various methodologies like DCF, transaction comparables, trading comparables, analyst estimates and so on.

We witnessed the following during football field estimates.

o DCF valuation of the company indicated a premium that was fairly in sync with the price offered in the sale side pitch. For DCF valuation we arrived at WACC using beta estimates, country risk premium estimates and target D/E ratio estimates from in-house research sources

o Trading comparables indicated a premium to the current price at which the company was trading

o Transaction comparables showed that the price being offered to the company was well within the range of comparable transactions in the industry in the past

o Thus currently our sells target company was trading at the considerable discount as compared to its peers, its intrinsic value and should be offered a considerable premium in the transaction

We plotted the final estimates of football field using Enterprise value as the metric for valuation. Exact numbers cannot be shared because of the confidentiality clause.

15 | P a g e

DEAL STRUCTURE

As a part of the project, I was also required to undertake the deal structure for the acquirer and undergo combination analysis. After analyzing the financials of the buyer and analyzing the past deals undertaken by the buyer, we arrived at an optimum capital structure for funding the deal.

The deal structure including the amount of debt issued and the equity used was clearly shown. The fund usage was also shown including the equity value purchase price and the retirement of previous debt and the M&A and financing fees paid.

The deal structure also took into the consideration maximum debt the buyer could issue without the credit rating downgrade

Deal structure was finalized by taking into account the accretive and dilutive effect on the EPS

Due to the confidential nature of the project, the above valuations cannot be shared across hard copy.

16 | P a g e

ACCRETION/ DILUTION ANALYSIS

The accretion/ dilution analysis of the potential deal was undertaken at various mixes of debt and equity.

The analysis showcased an immediate spike in the EPS estimates of the buyer. Due to sudden surge in the EPS, the deal had a potential to make the buyer an over performer in the stock markets in the immediate term.

The pro-forma EPS of the combined entity was considered for this purpose. We assumed synergies to be 0 in initial years.

Due to confidential nature of the project, we cannot share the analysis in hard copy.

17 | P a g e

REFERENCES

1. Bloomberg2. www.bamsec.com 3. Internal databases and research reports of JP Morgan4. Company filings5. Public news sources

18 | P a g e