Page 1

HUNDRED AND SIXTY SECOND REPORT

ON

LAYING OF

ANNUAL REPORTS & AUDITED ACCOUNTS

OF

COUNCIL OF SCIENTIFIC & INDUSTRIAL RESEARCH (CSIR)

(Presented to the Rajya Sabha on 27th July, 2021)

PARLIAMENT OF INDIA

RAJYA SABHA

COMMITTEE ON

PAPERS LAID ON THE TABLE

Rajya Sabha Secretariat, New Delhi

27th

July, 2021/ Shravana 5, 1943(Saka)

REPORT NO.

162

Page 2

Website : http//rajyasabha.nic.in

E-Mail : [email protected]

Page 3

PARLIAMENT OF INDIA

RAJYA SABHA

COMMITTEE ON PAPERS LAID

ON THE TABLE

HUNDRED AND SIXTY SECOND REPORT

ON

LAYING OF

ANNUAL REPORTS & AUDITED ACCOUNTS OF

COUNCIL OF SCIENTIFIC & INDUSTRIAL RESEARCH (CSIR)

(Presented to the Rajya Sabha on 27th July, 2021)

Rajya Sabha Secretariat, New Delhi

27th

July, 2021/ Shravana 5, 1943(Saka)

Page 4

C O N T E N T S

Page No.

1. Composition of the Committee.................................................... (i)

2. Preface......................................................................................... (ii)

3. Acronyms.................................................................................... (iii)

4. Report of the Committee............................................................. 1-20

Introduction …………………………………………………… 1-3

Council of Scientific and Industrial Research (CSIR)………… 4-20

5. Summary of Observations & Recommendations........................ 21-29

6. Minutes of the Meetings of the Committee.................................. 31-35

Page 5

COMPOSITION OF THE COMMITTEE

(Constituted on 20.04.2021)

1. Shri K.C. Ramamurthy - Chairman

2. Shri Shamsher Singh Dullo

3. Shri Kanakamedala Ravindra Kumar

4. Shri Shwait Malik

5. Shri Deepak Prakash

6. Shri Sanjay Raut

7. Shri G.K. Vasan

8. Shri Harnath Singh Yadav

9. Vacant

10. Vacant

SECRETARIAT

1. Shri Jagdish Kumar, Additional Secretary

2. Shri Prem Singh, Director

3. Shri Sanjeev Chandra, Additional Director

4. Smt. Subha Chandrashekar, Under Secretary

(i)

Page 6

P R E F A C E

I, the Chairman of the Committee on Papers Laid on the Table, Rajya Sabha,

having been authorised by the Committee, present this 162nd

Report to the Rajya

Sabha.

2. The Committee considered the laying status of the Annual Reports and

Audited Accounts of Council of Scientific and Industrial Research (CSIR) and

decided to seek clarifications from the administrative Ministry and representatives of

the Organisation for the same.

3. The Committee heard the representatives of the Department of Scientific and

Industrial Research and the Council of Scientific and Industrial Research (CSIR) on

the delayed laying of Annual Report / Audited Accounts of CSIR on 11th November,

2019 and thereafter an interaction was held between the senior officials of CSIR and

the Chairman in his room in Parliament House Annexe Extension on 23rd

March,

2021.

4. The Committee considered and adopted the draft Report in its meeting held on

22nd

July, 2021.

5. The Committee has made observations/recommendations on the requirements

to be fulfilled for laying the Reports on the Table of the House, time limit for laying

of papers, extension request for laying of papers, laying of Review and Delay

statements, monitoring of the papers laid on the Table of the House by the

concerned Ministries, uploading of the papers and online availability etc. The

Recommendations/Observations of the Committee are set out in bold letters at

appropriate places in the Report.

K.C. RAMAMURTHY

New Delhi ; Chairman,

27th July, 2021 Committee on Papers Laid on the Table,

Shravana 5, 1943(Saka) Rajya Sabha

(ii)

Page 7

ACRONYMS

1 AA Audited Accounts

2 AR Annual Report

3 CSIR Council of Scientific & Industrial Research

4 R &D Research and Development

5 C&AG Comptroller and Auditor General of India

6 GFRs General Financial Rules

(iii)

Page 8

1

INTRODUCTION

1.1 The practice of laying papers on the Table is the logical corollary of

Parliament's inherent right to information as well as enforcing executive

accountability to it. In order to enforce the accountability of Public Undertakings,

it has been made mandatory for such bodies to lay their Annual reports and

Audited accounts on the Table of the two Houses of Parliament. In certain Central

Acts, therefore, specific provisions exist for the laying of certain documents on

the Table. Neither the House by itself nor its Members by themselves is/are in a

position to give a closer scrutiny to each and every document laid on the Table. It

was in that background that the need to constitute a Committee on Papers Laid on

the Table was felt and the Committee on Rules in its second report presented to

Rajya Sabha on 22 May 1979, recommended for the constitution of the

Committee on Papers Laid on the Table. The second report was agreed to by

Rajya Sabha on 24 December 1981. The Gazette notification to that effect was

made on 15 January 1982. Rules 212 H to 212 O in the Rules of Procedure and

Conduct of Business in Rajya Sabha, relate to the constitution and functions of the

Committee on Papers laid on the Table.

COMMITTEE'S MANDATE TO REVIEW THE LAYING STATUS OF

CSIR

1.2 The Committee draws its mandate to review the laying status of the

Annual Reports and Audited Accounts of CSIR from Rule 212 H Clauses (2) and

(3) which state as follows :-

1.3 After a paper is laid before the Rajya Sabha by a Minister, the

Committee considers:

(1.3.a) whether there has been compliance with the provisions of the

Constitution or the Act of Parliament or any other law, rule or

regulation in pursuance of which the paper has been so laid;

(1.3.b) whether there has been any unreasonable delay in laying the

paper before the House and if so, (i) whether a statement

explaining the reasons for such delay has also been laid before

the House along with the paper, and (ii) whether those reasons

are satisfactory; and

(1.3.c) whether the paper has been laid before the House both in

English and Hindi and if not, (i) whether a statement explaining

the reasons for not laying the paper in Hindi has also been laid

Page 9

2

before the House along with the paper, and (ii) whether those

reasons are satisfactory.

1.4 The Committee also performs such other functions in respect of the

papers laid on the Table as may be assigned to it by the Chairman from time to

time. The Committee has the power to require the evidence of persons or the

production of papers or records, if such a course is considered necessary for the

discharge of its duties.

1.5 As per the recommendations contained in Para 26 of the 1st Report of

the Committee on Papers Laid on the Table, Rajya Sabha, the Annual Report and

the Audited Accounts of the Government Companies/Organisations are required

to be laid on the Table of the House within nine months from the date of closure

of their Annual Accounts.

1.6 Rule 238 (5) of the General Financial Rules, 2017 states that in the

case of Private and Voluntary Organisations receiving recurring Grants-in-aid

from Rupees 10 lakhs to less than Rupees 50 lakh, all the Ministries or

Departments of Government of India should include in their Annual Reports a

statement showing the quantum of funds provided to each of those Organisations

and the purpose for which they were utilized, for the information of Parliament.

The Annual Reports and Accounts of Private and Voluntary Organisations

receiving recurring Grants-in-aid to the tune of Rupees 50 lakh and above should

be laid on the Table of the House within 9 months of the close of the succeeding

financial year of the Grantee Organisations. Furthermore, Rule 238(6) of the

General Financial Rules, 2017, too, mandates that in the case of organisations

receiving one-time assistance or non recurring Grants as Grants-in-aid from

Rupees ten lakhs to Rupees fifty lakhs, all Ministries or Departments of

Government of India should include in their Annual Reports, statements showing

the quantum of funds provided to each of these organisations and the purpose for

which the funds were utilized, for the information of Parliament. The Annual

Reports and Audited Accounts of Private and Voluntary Organisations or

societies registered under the Registration of Societies Act, 1860, receiving one-

time assistance/non-recurring Grants of Rupees fifty lakhs and above should also

be laid on the Table of the House, within nine months of the close of the

succeeding financial Year of the grantee Organisations.

1.7 CSIR is also mandated to lay its AR and AA by Rule 68 and 69 of

the CSIR Rules and regulation, which are reproduced below:-

Rule 68. Accounts and Audit. (i) The Society shall maintain proper accounts

and other relevant records and prepare an annual statement of accounts

including the balance sheet in such form as may be prescribed by the Central

Page 10

3

Government in consultation with Comptroller & Auditor-General of India. (ii)

The accounts of the Society shall be audited annually by the Comptroller &

Auditor-General and any expenditure incurred in connection with the audit of

accounts of the Society shall be payable by the Society. (iii) The Comptroller

& Auditor-General shall have the same rights, privileges and authorities in

connection with the audit of accounts of the Society as the Comptroller &

Auditor-General has in connection with the audit of Government Accounts and

in particular, shall have the right to demand the production of books, accounts,

connected vouchers and other documents and papers and to inspect any of the

offices of the Society.

Rule 69. Annual Report. An Annual Report of the proceedings of the Society

of all work undertaken during the Financial Year shall be prepared by the

Governing Body. A draft of the Annual Report and the yearly accounts of the

Society as certified by Comptroller and Auditor General of India together with

the Audit Report thereon, shall be placed before the Society together with the

audit report thereon for its consideration and approval. Copies of the Annual

Report and yearly accounts as approved by the Society shall be forwarded to

the Government of India who shall cause the same to be laid before the

parliament.

1.8 The Committee, thus, as part of its mandate, took up for its

consideration and examination, the case of CSIR.

Page 11

4

Council of Scientific & Industrial Research (CSIR)

BACKGROUND

The Department and CSIR, during the course of their interaction with the

Committee, on 11th November, 2019, had provided information regarding the

genesis of CSIR, its mission and achievements, extracts from which are reproduced

in the succeeding paras from 2.1 to 2.3.

2.1. The Council of Scientific & Industrial Research (CSIR) is a contemporary

R&D organization with a pan-India network of 38 national laboratories, 39 outreach

centres, 1 Innovation Complex and 3 units, 3460 active scientists supported by

about 4796 scientific and technical personnel.

2.2. CSIR covers a wide spectrum of science and technology – from radio and

space physics, oceanography, earth sciences, geophysics, chemicals, drugs,

genomics, biotechnology and nanotechnology to mining, materials, aeronautics,

instrumentation, environmental engineering and information technology. It provides

significant technological intervention in many areas which include inter-alia,

environment, health, drinking water, food, housing, energy, metals & minerals.

Pioneer of India‟s intellectual property movement, CSIR today is strengthening its

patent portfolio to carve out global niches for the country in select technology

domains. On an average CSIR files about 300 Indian patents and 250 foreign

patents per year. Amongst its peers in publicly funded research organisations in the

world, CSIR is a leader in terms of filing and securing patents worldwide.

2.3. CSIR‟s mission is to “build a new CSIR for a new India” and its vision is to

“Pursue science which strives for global impact, technology that enables innovation

– driven industry and nurture trans-disciplinary leadership thereby catalysing

inclusive economic development for the people of India”

LAYING STATUS OF ANNUAL REPORTS AND AUDITED ACCOUNTS

2.4. The laying status of CSIR for the years 1986-87 to 2017-18, as tabulated

from the Committee‟s database, reveals the following position: -

Page 12

5

Sl.

No

Year Due Date Date of

Laying

Delay Time Record Type

Year Month Day

1

1986-87 31/12/1987 08/08/1989 1

7

7 Both AR/AAs,

Review Statement

& Delay Statement

2

1987-88 31/12/1988 08/01/1991 2

0

7 Both AR/AAs,

Review Statement

& Delay Statement

3

1988-89 31/12/1989 08/01/1991 1

0

7 Both AR/AAs,

Review Statement

& Delay Statement

4

1989-90 31/12/1990 05/09/1991 0

8

4 Both AR/AAs,

Review Statement

& Delay Statement

5

1990-91 31/12/1991 30/07/1992 0

6

29 Both AR/AAs,

Review Statement

& Delay Statement

6

1991-92 31/12/1992 26/08/1993 0

7

25 Both AR/AAs,

Review Statement

& Delay Statement

7

1992-93 31/12/1993 28/04/1994 0

3

27 Both AR/AAs,

Review Statement

& Delay Statement

8

1993-94 31/12/1994 22/12/1995 0

11

21 Both AR/AAs,

Review Statement

& Delay Statement

9

1994-95 31/12/1995 28/11/1996 0

10

27 Both AR/AAs,

Review Statement

& Delay Statement

10

1995-96 31/12/1996 05/06/1998 1

5

4 Both AR/AAs,

Review Statement

& Delay Statement

11

1996-97 31/12/1997 10/12/1999 1

11

9 Both AR/AAs,

Review Statement

12

1997-98 31/12/1998 10/12/1999 0

11

9 Both AR/AAs,

Review Statement

13

1998-99 31/12/1999 15/12/2000 0

11

14 Both AR/AAs,

Review Statement

& Delay Statement

Page 13

6

Sl.

No

Year Due Date Date of

Laying

Delay Time Record Type

Year Month Day

14

1999-00 31/12/2000 10/05/2002 1

4

9 Both AR/AAs,

Review Statement

& Delay Statement

15

2000-01 31/12/2001 10/05/2002 0

4

9 Both AR/AAs,

Review Statement

& Delay Statement

16

2001-02 31/12/2002 09/05/2003 0

4

8 Both AR/AAs,

Review Statement

& Delay Statement

17

2002-03 31/12/2003 26/08/2004 0

7

25 Both AR/AAs,

Review Statement

& Delay Statement

18

2003-04 31/12/2004 04/08/2005 0

7

3 Both AR/AAs,

Review Statement

& Delay Statement

19

2004-05 31/12/2005 12/03/2007 1

2

11 Both AR/AAs,

Review Statement

& Delay Statement

20

2005-06 31/12/2006 17/12/2008 1

11

16 Both AR/AAs,

Review Statement

& Delay Statement

21

2006-07 31/12/2007 17/12/2008 0

11

16 Both AR/AAs,

Review Statement

& Delay Statement

22

2007-08 31/12/2008 06/05/2010 1

4

5 Both AR/AAs,

Review Statement

& Delay Statement

23

2008-09 31/12/2009 25/11/2010 0 10

24 Both AR/AAs,

Review Statement

& Delay Statement

24

2009-10 31/12/2010 08/08/2011 0 7

7 Both AR/AAs,

Review Statement

& Delay Statement

25

2010-11 31/12/2011 23/08/2012 0 7

22 Both AR/AAs,

Review Statement

& Delay Statement

26

2011-12 31/12/2012 09/12/2013 0 11

8 Both AR/AAs,

Review Statement

& Delay Statement

Page 14

7

Sl.

No

Year Due Date Date of

Laying

Delay Time Record Type

Year Month Day

27

2012-13 31/12/2013 04/08/2016 2 7

3 Both AR/AAs,

Review Statement

& Delay Statement

28

2013-14 31/12/2014 04/08/2016 1 7

3 Both AR/AAs,

Review Statement

& Delay Statement

29

2014-15 31/12/2015 20/09/2020 4 8

19 Both AR/AAs,

Review Statement

& Delay Statement

30

2015-16 31/12/2016 20/09/2020 3 8

19 Both AR/AAs,

Review Statement

& Delay Statement

31

2016-17 31/12/2017 20/09/2020 2 8

19 Both AR/AAs,

Review Statement

& Delay Statement

32

2017-18 31/12/2018 20/09/2020 1 8

19 Both AR/AAs,

Review Statement

& Delay Statement

DELAY IN LAYING ANNUAL REPORT AND AUDITED ACCOUNTS

2.5. The Committee observed from the information detailed in the above table

that there had been persistent delay in laying from the initial years and throughout

the last three decades. In most years the delay was of a few months interspersed

with delays ranging from 1 ½ years to nearly 2 years. In 2014-15, however, there

was an inordinate delay of 4 years, 8 months and 20 days. The Committee noted

that CSIR had laid all the ARs/AAs for the years from 2014-15 to 2017-18

simultaneously on 20th

September, 2020. The CSIR far from being able to stem the

delay in laying, had been unable to lay its AR/AAs for four consecutive years. The

AR/AAs of 2018-19 and 2019-20 were also still to be laid. The Committee noted

however that the CSIR had always been laying its ARs and AAs together, to give a

complete and fair picture of the working of the organisation, in conformity of the

Committee‟s guidelines in Para 3.17 of the 21st Report. The Committee noted that

the Review and Delay Statements had been laid together with the Reports in all the

years in bilingual form.

Page 15

8

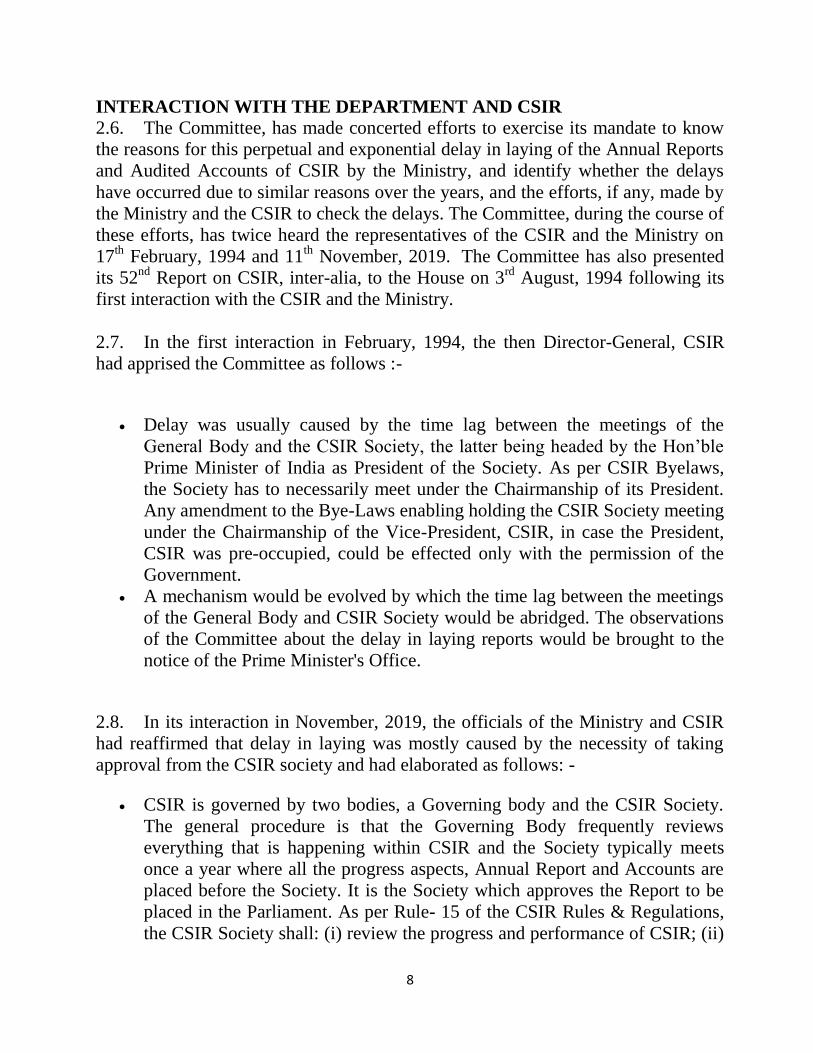

INTERACTION WITH THE DEPARTMENT AND CSIR

2.6. The Committee, has made concerted efforts to exercise its mandate to know

the reasons for this perpetual and exponential delay in laying of the Annual Reports

and Audited Accounts of CSIR by the Ministry, and identify whether the delays

have occurred due to similar reasons over the years, and the efforts, if any, made by

the Ministry and the CSIR to check the delays. The Committee, during the course of

these efforts, has twice heard the representatives of the CSIR and the Ministry on

17th February, 1994 and 11

th November, 2019. The Committee has also presented

its 52nd

Report on CSIR, inter-alia, to the House on 3rd

August, 1994 following its

first interaction with the CSIR and the Ministry.

2.7. In the first interaction in February, 1994, the then Director-General, CSIR

had apprised the Committee as follows :-

Delay was usually caused by the time lag between the meetings of the

General Body and the CSIR Society, the latter being headed by the Hon‟ble

Prime Minister of India as President of the Society. As per CSIR Byelaws,

the Society has to necessarily meet under the Chairmanship of its President.

Any amendment to the Bye-Laws enabling holding the CSIR Society meeting

under the Chairmanship of the Vice-President, CSIR, in case the President,

CSIR was pre-occupied, could be effected only with the permission of the

Government.

A mechanism would be evolved by which the time lag between the meetings

of the General Body and CSIR Society would be abridged. The observations

of the Committee about the delay in laying reports would be brought to the

notice of the Prime Minister's Office.

2.8. In its interaction in November, 2019, the officials of the Ministry and CSIR

had reaffirmed that delay in laying was mostly caused by the necessity of taking

approval from the CSIR society and had elaborated as follows: -

CSIR is governed by two bodies, a Governing body and the CSIR Society.

The general procedure is that the Governing Body frequently reviews

everything that is happening within CSIR and the Society typically meets

once a year where all the progress aspects, Annual Report and Accounts are

placed before the Society. It is the Society which approves the Report to be

placed in the Parliament. As per Rule- 15 of the CSIR Rules & Regulations,

the CSIR Society shall: (i) review the progress and performance of CSIR; (ii)

Page 16

9

give the policy direction to Governing Body; and (iii) approve the annual

report and the yearly accounts of CSIR.

The CSIR Society is chaired by the Hon. Prime Minister who is the ex-officio

President of the Society and the ex-officio Vice President of the Society is

the Minister in charge of the Ministry & Department dealing with CSIR. The

Society has about 30 odd members, including many ex-officio members,

Secretaries of many departments, Hon. Minister of Finance, Hon. Minister of

Commerce and Industry etc.

The term of the Society is 3 years after which a new Society is notified.

During the period from May, 2016- October 2019 the notification of the new

Society was delayed due to several reasons beyond the control of CSIR,

including death of a proposed member and superannuation of a few proposed

ex-officio members. However, the composition of the new Society had just

been notified on 7/11/2019 and the meeting of the new Society was expected

to be held very soon.

2.9. By oral and written submissions in the reply to questionnaire, the Department

and CSIR had apprised the Committee about the procedure involved in preparation

of AR and AA as under:

2.10. As per Rule 68 and 69 of the CSIR Rules & Regulations, “a draft of the

Annual Report and yearly accounts of the CSIR Society as certified by Comptroller

and Auditor General of India together with the Audit Report thereon shall be placed

before the Society for its consideration and approval before the same are placed on

the Table of House of the Parliament.” For Annual Reports, CSIR Laboratories

submit their inputs based on a template after a completion of a financial year. The

template covers significant achievements, activities under different Govt. Missions,

Honors & Awards, etc. These are then compiled, consolidated and then a draft

report is placed for approval of the Governing Body meeting. The complete process

takes duration of about 2-4 months.

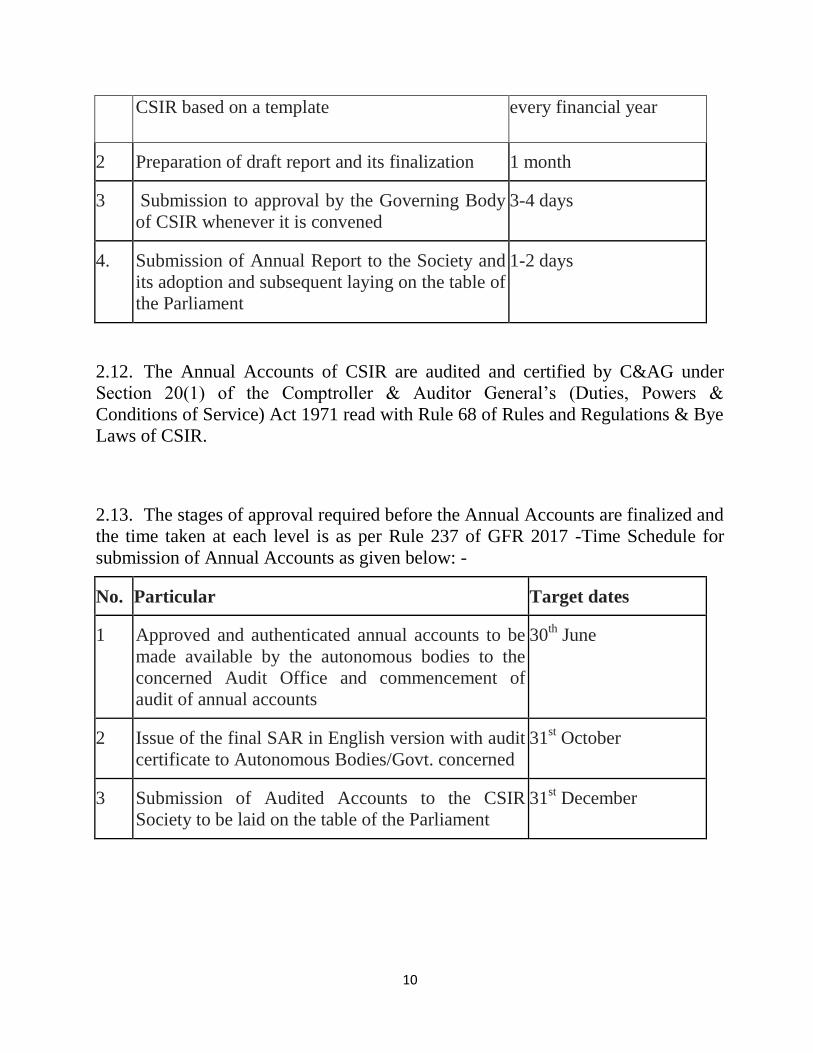

2.11. The stages of preparation of Annual Reports are as follows:

No. Particular Duration

1 Receipt and consolidation of inputs from all the

constituent laboratories and various divisions of

2-3 months from April of

Page 17

10

CSIR based on a template every financial year

2 Preparation of draft report and its finalization 1 month

3 Submission to approval by the Governing Body

of CSIR whenever it is convened

3-4 days

4. Submission of Annual Report to the Society and

its adoption and subsequent laying on the table of

the Parliament

1-2 days

2.12. The Annual Accounts of CSIR are audited and certified by C&AG under

Section 20(1) of the Comptroller & Auditor General‟s (Duties, Powers &

Conditions of Service) Act 1971 read with Rule 68 of Rules and Regulations & Bye

Laws of CSIR.

2.13. The stages of approval required before the Annual Accounts are finalized and

the time taken at each level is as per Rule 237 of GFR 2017 -Time Schedule for

submission of Annual Accounts as given below: -

No. Particular Target dates

1 Approved and authenticated annual accounts to be

made available by the autonomous bodies to the

concerned Audit Office and commencement of

audit of annual accounts

30th June

2 Issue of the final SAR in English version with audit

certificate to Autonomous Bodies/Govt. concerned

31st October

3 Submission of Audited Accounts to the CSIR

Society to be laid on the table of the Parliament

31st December

Page 18

11

2.14. The Committee was further informed that the CSIR Annual Accounts are

generally closed and submitted to Audit on time i.e., by 30th June of the following

year as per prescribed time schedule. No constraints are faced by CSIR to prepare

or finalize its Annual Reports/Audited Accounts. The Annual Report and Annual

Accounts for the financial years 2014-15, 2015-16, 2016-17 and 2017-18 had been

approved by the Governing body of CSIR in its meetings held in June, 2016,

November, 2017, December, 2018 and April, 2019 respectively but could not be

laid because they had not been approved by the CSIR Society.

2.15. Printing of Annual Reports/ Annual Accounts in CSIR is undertaken as per

need and there are no constraints related to it. CSIR also has no problem in Hindi

translation as the organisation has its Internal Hindi Cell.

2.16. The Committee was also informed that Audit paras outstanding from 1999

onwards were settled from 2014 onwards and presently no CAG paras were

outstanding as on 31st March, 2021. The reasons for the delays of about two

decades in the settlement of some of these paras were (i) delay in formulating

appropriate replies by the concerned laboratories of CSIR and its continued

improvement to the satisfaction of C&AG; (ii) In one case for compliance,

concerned laboratory was dependent upon outside agency‟s cooperation; and (iii)

Also time taken in revising guidelines/Rules to avoid recurrence of such

irregularities etc.

2.17. Since the information provided at the interaction held in November, 2019

was still unsatisfactory on some aspects, the Director-General, CSIR and two senior

officials were called for an interaction with the Chairman of the Committee on 23rd

March, 2021. Clarifications were sought from the CSIR officers mainly on the

following issues –

Whether the Society as a whole became defunct every three years or the term

of the members expired after three years.

Whether the CSIR Society could be chaired by the Vice-President in case of

absence of the President, so that delay in obtaining the approval of the

Society for the Annual Reports/Audited Accounts of CSIR could be avoided.

2.18. The officials informed that as per the Rules & Regulations and Bye-Laws of

Memorandum of Association of CSIR, 2018, only Members of the Society are re-

constituted and notified every three years. The composition of the CSIR Society

Page 19

12

was notified four times during the last 15 years. However, during the period from

May, 2016 to October, 2019 there was no reconstitution of the members of the

Society. The re-constitution of the Society had got delayed due to several reasons

beyond control of CSIR including death of a proposed member and superannuation

of few proposed ex-officio members. However, the CSIR Society has now been

reconstituted and notified on 7/11/2019.

2.19. The officials also informed that in the CSIR Society Meeting held on 14th

February, 2020, the Society has approved the proposal of CSIR to convene Society

meetings in future to be chaired by the Vice President, CSIR to approve the Annual

Reports and Annual Accounts to enable CSIR to place these on the Table of

Parliament. They briefed the Chairman about the Rules & Regulations especially

Rule 9, 14, 21 and 50 which pertain to the constitution and proceedings of the

Society.

“Rule 9. Unless their membership of the Society is terminated as provided in

Rules 10 and 11 and subject to the provisions of Rule 5, all other members of the

Society shall relinquish their membership on the expiry of three years from the

date on which they became members of the Society but shall be eligible for

reappointment. If a casual vacancy arises during the three years period, the

person appointed in the vacancy shall, subject to the provisions of Rules 5, 10

and 11, hold office only for the unexpired period of that three year period.

“Rule 14. The Society shall function notwithstanding that any person who is

entitled to be a member by reason of his office is not a member of the Society for

the time being and notwithstanding any other vacancy in its body whether by

non-appoinment or otherwise and no act or proceeding of the Society shall be

invalidated merely by reason of the happening of any of the above events or of

any defect in the appoinment of any of its members.”

“Rule 21. If the President is not present at the meeting of the Society, the

Vice-President shall be chairman of the meeting. If both the President and Vice

President are not present, any member of the Governing Body appointed by the

President in writing shall be Chairman of the meeting, but if there shall be no

member appointed as aforesaid present or willing to take the chair, the members

of the Society shall choose one of the members, present to be the Chairman of

the meeting.”

“Rule 50. The President may, in writing, delegate such of his powers as may be

necessary to the Vice-President or the Director-General.”

Page 20

13

OBSERVATIONS / RECOMMENDATIONS

DELAY IN LAYING OF AR/AAs

2.20. The Committee observes that ever since its first interaction with CSIR in

1994, the position of the CSIR and its controlling Ministry had always been

that as per the CSIR bye-laws, the CSIR Society had to necessarily meet under

the Chairmanship of its President and any amendment to the byelaws would

require the permission of the Government. The Ministry and the organization

had also always presented the necessity of obtaining the approval of the

President, CSIR Society as the main reason for delay in laying the AR/AAs of

CSIR. Now, it is apparent from a reading of the Bye-laws of CSIR that there is

a built-in provision for the Vice-President to be the Chairman of the

Committee if the President is absent. The Committee observes that both the

Ministry and CSIR seem to have had a casual approach to the issue and do not

appear to have examined their own bye-laws seriously or researched the

matter even after being called twice to give their evidence before the

Committee. The Committee notes that the CSIR had taken up the issue at a

meeting of the CSIR Society chaired by the Prime Minister on 14th

February,

2020 and had obtained the permission of the Society to convene Society

meetings in future to be chaired by the Vice-President of the Society. The

Committee appreciates the initiative however belatedly taken but the inaction

of the Ministry and CSIR for four years when the AR/AA could not be laid

from 2014-2018 cannot be overlooked. One of the functions of the CSIR

Society is to review the progress and performance of CSIR. Since the Annual

Reports are the main indicators of the progress and performance of an

institution, the Society was negligent in the performance of its functions by not

examining and approving the Reports for four years. The CAG in its Separate

Audit Report of 2017-18 has also pointed out that the ARs/AAs of CSIR had

not been laid in Parliament for the past three years yet no action was taken on

the issue. The Committee appreciates the role played by CSIR as a premier

scientific institution in the country but emphasizes that timely laying of Report

should also be given priority as it provides both Parliament and the general

public access to the activities of CSIR.

2.21. The Committee further observes that as informed by the CSIR and the

Ministry, the members of the CSIR Society are notified every 3 years but

there had been no notification for the time period between May 2016 to

October, 2019 which was the main reason for delay in getting approval of the

Society for the AR/AAs to be laid in Parliament. The Committee perceives

that as per Rule 9 of the CSIR Byelaws, the term of the members expires after

three years and the Society itself does not become defunct. Moreover, as per

Page 21

14

Rule 14, the Society continues to function despite vacancies and non-

appointment of members for any reason. Therefore, there does not seem to

any impediment for conducting meetings of the Society for approval of

ARs/AAs even if appointment of some members was in progress. The reasons

given for the delay in appointment of members proposed for the Society that

the members had either retired or were deceased are not acceptable. The

Committee is unable to accept the explanation that suitable members could not

be found for four years for appointment to the Society. The Committee notes

that the composition of the Society had been notified on 7th

November, 2019 i.e.

a few days before the interaction of the Committee with the CSIR on 11th

November, 2019 which confirms that the reasons given for delaying its

notification were baseless and irrational.

2.22. The Committee observes that the CSIR, by its own admission, faced no

constraints either in preparing ARs/AAs, or in translating or printing the

reports. The only impediments to timely laying of the ARs/AAs of CSIR as

stated by the organization and the Ministry were the time-lag between the

meetings of the Governing Body and the CSIR Society and the necessity of

taking approval of the President, CSIR for the AR/AA at the meeting of the

CSIR Society. The first reason is untenable as the Ministry and CSIR have

shown great laxity in notifying the composition of the CSIR Society by letting

more than 3 years lapse before the notification. The second reason is not valid

as the Bye-laws of the CSIR Society provide for the Vice-President to chair the

meeting of the CSIR Society in absence of the Chairman. Therefore, neither of

the reasons which were repeatedly put forward by the Ministry and CSIR over

the years to explain the delay in laying are credible. The Committee observes

that such laxity is all the more deplorable when there were Audit paras

pending which were allowed to remain outstanding because the ARs/AAs were

not being laid.

2.23. The Committee observes that there were 6 Audit paras pending since

1999 which were settled in 2016-2018, which is a delay of about two decades.

18 Audit paras pending from 2000 to 2013 were settled mostly in the years

2015-2018 with delays of more than a decade. Audit paras from the years 2015

onwards have mostly been settled after 2-3 years of delay. The Committee

observes further that there are no outstanding audit paras at present and the

delay in settlement of audit paras has been considerably reduced. While

acknowledging the organisation’s efforts towards reduction in delay of

settlement of the audit paras and the achievement of nil pendency of audit

paras, the Committee is compelled to register its displeasure in the decades

Page 22

15

long delay in settlement of earlier audit paras pending from 1999 onwards. The

reasons given for delay in settlement of the long outstanding paras are

unacceptable to the Committee. The Committee observes that formulation of

appropriate replies to audit paras to the satisfaction of C&AG or revision

guidelines to prevent recurrence of irregularities took nearly two decades is a

farcical excuse and not becoming of a premier institute like the CSIR. The fact

that Audit paras were kept pending for nearly two decades for flimsy reasons

reveals that there was no serious attempt at settlement. Taken together with

the fact that despite the backlog of pending Audit paras, the ARs/AAs for the

previous four years were not laid at all, a regrettable state of affairs was

allowed to exist with no apparent attempt by either the organisation or the

Controlling Ministry to tackle the issues with the seriousness warranted.

2.24. The Committee finds it astonishing that the Ministry, which had the duty

of monitoring the preparation and laying of AR/AAs, did not take up the

matter of the pending reports earlier and it took an interaction with a

Parliamentary Committee to spur the Ministry and the organisation to action.

2.25. The Committee notes that the schedule for preparation of Annual

Accounts is a general time schedule given in the GFR, 2017 for all

organisations. The Committee observes that CSIR has not worked out a

detailed schedule for preparation of its accounts with deadlines for compilation

and preparation of accounts for approval of the Governing Body or of

submission of replies to draft Audit reports.

2.26. The Committee recommends that action for nominating members to the

CSIR Society may be initiated a few months before the expiry of the terms of

retiring members so that the vacant seats in the Society are kept to a

minimum. Since as per the byelaws the Society continues to function

irrespective of notification of members, the CSIR and the Ministry may ensure

that there is no delay in convening meetings of the Society and obtaining the

approval for the Annual Reports and Audited Accounts.

2.27. The Committee notes that the CSIR has already taken the initiative to

obtain approval for the Vice-President to chair the Society meeting when the

President was pre-occupied. Since the byelaws also contain a provision for the

same, there is no excuse for delaying holding the meetings of the Society on the

pretext that the President, CSIR Society was unavailable to attend the

meetings. The Committee avers that both the excuses for delayed laying which

have been repeatedly tendered by the Ministry and CSIR over the years,

Page 23

16

namely non-constitution of CSIR Society and difficulty in obtaining approval

of President, CSIR for AR/AAs, have been found, upon examination, to be

indefensible and unjustified. The Committee recommends that the CSIR and

the Ministry should ensure that in future, the ARs/AAs are approved as per

schedule and there is no delay in obtaining the approval of the Society or in

laying in Parliament.

2.28. The Committee observes that the present schedule for Annual Accounts

is a reproduction of the generalized schedule given in Rule 237 of GFR, 2017

and recommends that a detailed schedule for preparation of Annual Accounts

may be drawn up, with deadlines for every stage of preparation of accounts,

submission to audit authorities, submission of draft replies to audit queries,

receipt of final audit report and forwarding to Ministry for laying in the

Parliament etc. The Committee recommends that the Audited Accounts may

be submitted to the CSIR for approval by end of November so that the

AR/AAs could be forwarded to the Ministry by mid-December for laying in the

Parliament.

2.29. The Committee also recommends that all efforts may be made to

maintain the schedule for settlement of Audit paras within a reasonable period

of time and care may be taken not to have any lapse in this matter. In future,

Audit paras kept lingering for years together as was done in the last decade for

untenable reasons would be viewed seriously and the Committee exhorts both

the organisation and the Ministry to ensure that the current momentum is

sustained.

EXTENSION OF TIME

2.30. The Committee observes that as per available record, the Ministry has

sought extensions repeatedly for the same year of Report, the average being

three extensions for every year of report from 2005-06 to 2015-16. In the years

2012-13, 2014-15 and 2015-16, extensions had been sought five times from the

Committee. On many occasions, the Reports have been laid after the last

extended date inspite of the many extensions granted by the Committee. For

example, the reports for the years 2014-15 and 2015-16 have been laid only on

20/9/20 after grant of five extensions the last one being uptill 31/7/19.

Moreover, the requests for extensions in many cases have been forwarded well

after the due date for laying. The most glaring case is of the year 2016-17,

wherein extension has been sought almost two years after the due date of

laying. It is evident that the Ministry has treated the process of obtaining

extension from the Committee in a casual way, routinely obtaining extensions

Page 24

17

with no efforts being made to comply with the extended deadline.

2.31. The Committee invites attention of the Ministry to its recommendation

in this regard made in Para No. 27 of its 1st Report, to seek extension well in

advance, as soon as it is clear that there would be a delay in laying of the

Reports: -

"In case of delay in respect of reports for periods upto 31st March,

1981, a statement explaining the reasons for delay should also be laid on

the Table of the House along with the documents. If there is likely to be a

delay in laying a paper within the stipulated period, the administrative

Ministry should approach the Committee sufficiently in advance for

extension of time by explaining the reasons for doing so. A reference

should be made to the extension given by the Committee in the paper when

laid. This procedure should be followed in respect of all reports with

accounting periods from 1st April, 1981."

The Committee also draws the attention of the Ministry to its

recommendations in Para 11 of its 136th Report regarding repeated requests

for extension:-

“The Committee, therefore, cautions the Ministry and the Company

that Parliamentary norms of seeking extension from the Committee, in the

event of delay, must be adhered to. The Ministry must give valid reasons for

seeking extension. However, seeking the extension cannot be an unending

exercise. It is upon the Ministry and the Company to resolve the issues

causing the delay, because recurrent annual extensions for similar reasons

may be taken adversely by the Committee while considering the requests for

extension. In this regard, the Committee would like that in case of repeated

delays in laying, responsibility must be fixed.”

LAYING OF DELAY STATEMENT

2.32. The Committee observes that the Ministry has been appending the Delay

Statement along with the ARs/AAs for the past few years. However, the

chronological order of events is given only after supply of the accounts to the

Audit, leaving out the events regarding the process of compilation of the

Annual Report. The Committee recommends that the Annual Report of CSIR

includes information regarding all its Research Centers and compilation of the

same takes some time, the timeline for preparation of the Annual Report

should also be given in the Statement. The Committee emphasizes its

Page 25

18

recommendation contained in Para 3.17 of its 22nd

Report wherein it is stated

that “The statements giving reasons for delay should contain information, in

chronological order setting forth the dates of compilation of accounts, their

submission to Audit, receipt of draft Audit Report, replies given to audit queries,

receipt of final Audit Report, translation and printing of Accounts and their

submission to the Ministry for laying on the Table of the House. So that the

House may identify the stages, causes and extent of delay and suggest remedial

measures wherever required.”

LAYING OF REVIEW STATEMENT

2.33. Apart from the Annual Reports and Audited Accounts, the

Ministry/Department is also required to lay a Comprehensive Review Statement.

The Review Statement by the Ministry/Department is a very important and

informative document for the legislature since it underlines the achievements made

against the targets set as well as the future plans chalked out to be achieved and

critical areas to be addressed.

2.34. The Committee notes that the CSIR covers a wide spectrum of science

and technology and has numerous achievements covered in great detail in its

Annual Reports. However, only one Review Statement has been laid for all the

four years 2014-15, 2015-16, 2016-17 and 2017-18 and this statement too is

extremely brief merely stating that since the Department is in agreement with

Annual Report, no “Review” thereon is being laid. The Committee has time

and again taken the view that mere agreement of the Ministry with the Report

of the organisation cannot be taken as an objective appraisal of the

organisation. The Committee draws the attention of the Ministry to its

recommendation in Para 3, 125th

Report :

“The Committee recommends that the Review by the Ministry should be an

objective appraisal of the performance against tangible benchmarks and a

comparative assessment of the Board’s performance vis a vis global and domestic

trends in the industry. The Committee also recommends that Ministry should give

the details of the process and methodology adopted for conducting such a

review.”

UPLOADING OF ANNUAL REPORTS / AUDITED ACCOUNTS / REVIEW

& DELAY STATEMENTS

2.35. The Committee observes that the CSIR has uploaded all the Annual

Reports and Annual Accounts since 2003-04, both English and Hindi versions

on its website. However, the Delay Statement and Review Statements have not

been uploaded. Moreover, the Annual Reports have been uploaded under a

Page 26

19

common Head instead of a separate icon. The Committee, therefore,

recommends that the Ministry should ensure that the CSIR gives complete

information on its website by uploading the Review Statements and Delay

Statements till date, alongside its Annual Reports. The Committee in this

regard emphatically reiterates its recommendation contained in Para Nos 1.21

and 1.22 of its 156th Report which is as under:

“The Committee therefore recommends that all the Ministries/

Departments should upload Annual Report/ Audited Accounts/ Review Statement/

Delay Statement, if any, of their organisations soon after laying or within 03 days

of laying of the papers in the House so that the same may be easily accessible to

the general public for their perusal and benefit. The Committee further

recommends that this leeway of 03 days is initially given so that all the papers

required to be uploaded may be placed in the public domain for viewing. Later on

all out efforts may be made to place the papers so laid on the date of laying

itself.”

(Para 1.21)

“The Committee is of the view that in the current era of ever increasing

level of internet penetration in the country, uploading of the papers on the

respective websites should be given the priority at par with the laying thereof. In

this backdrop, the Committee is of the opinion that the process of laying should

always be integrated with immediate uploading of both English and Hindi

versions of the papers on the website.”

(Para 1.22)

UPLOADING OF LIST OF GRANTEE/ AUTONOMOUS

ORGANISATIONS ON THE WEBSITE 2.36. The Committee observes that GoI has released total funds of Rs. 30295.3

crore to the CSIR during the period of 2007-08 to 2016-17. As per Rule 230 (2) of

General Financial Rules, 2017, each Ministry/Department should make available,

on the website, a list of institutions/organisations along with details of the amount

and purpose of grants given to them, in order to avoid duplication in Grants-in-aid.

But neither the details of grants/funds released to the CSIR nor of any other grantee

organization under the control of the Ministry, is available on its website. The

Committee further observes that Ministry of Finance, Department of Expenditure

had vide Office Memorandum dated 16th September, 2020, forwarded to all the

Ministries/Departments, directed them to comply with the above cited provisions of

the Rule 230 (2) of GFR, 2017, but it is seen from the website of the Ministry that

no such information is available.

Page 27

20

2.37. The Committee, therefore, recommends that the Ministry should upload

details of grants released to the CSIR and all other grantee /autonomous

organisations under its control, on its website, in compliance to Rule 230(2) of

General Financial Rules, 2017, without any delay and create a separate icon for

easy access of the same.

Page 28

21

SUMMARY OF OBSERVATIONS AND RECOMMENDATIONS

DELAY IN LAYING OF AR/AAs

1. The Committee observes that ever since its first interaction with CSIR

in 1994, the position of the CSIR and its controlling Ministry had always

been that as per the CSIR bye-laws, the CSIR Society had to necessarily

meet under the Chairmanship of its President and any amendment to

the byelaws would require the permission of the Government. The

Ministry and the organization had also always presented the necessity of

obtaining the approval of the President, CSIR Society as the main

reason for delay in laying the AR/AAs of CSIR. Now, it is apparent

from a reading of the Bye-laws of CSIR that there is a built-in provision

for the Vice-President to be the Chairman of the Committee if the

President is absent. The Committee observes that both the Ministry and

CSIR seem to have had a casual approach to the issue and do not

appear to have examined their own bye-laws seriously or researched the

matter even after being called twice to give their evidence before the

Committee. The Committee notes that the CSIR had taken up the issue

at a meeting of the CSIR Society chaired by the Prime Minister on 14th

February, 2020 and had obtained the permission of the Society to

convene Society meetings in future to be chaired by the Vice-President

of the Society. The Committee appreciates the initiative however

belatedly taken but the inaction of the Ministry and CSIR for four years

when the AR/AA could not be laid from 2014-2018 cannot be

overlooked. One of the functions of the CSIR Society is to review the

progress and performance of CSIR. Since the Annual Reports are the

main indicators of the progress and performance of an institution, the

Society was negligent in the performance of its functions by not

examining and approving the Reports for four years. The CAG in its

Separate Audit Report of 2017-18 has also pointed out that the ARs/AAs

of CSIR had not been laid in Parliament for the past three years yet no

action was taken on the issue. The Committee appreciates the role

played by CSIR as a premier scientific institution in the country but

emphasizes that timely laying of Report should also be given priority as

it provides both Parliament and the general public access to the

activities of CSIR.

(Para 2.20)

Page 29

22

2. The Committee further observes that as informed by the CSIR and the

Ministry, the members of the CSIR Society are notified every 3 years

but there had been no notification for the time period between May 2016

to October, 2019 which was the main reason for delay in getting

approval of the Society for the AR/AAs to be laid in Parliament. The

Committee perceives that as per Rule 9 of the CSIR Byelaws, the term

of the members expires after three years and the Society itself does not

become defunct. Moreover, as per Rule 14, the Society continues to

function despite vacancies and non-appointment of members for any

reason. Therefore, there does not seem to any impediment for

conducting meetings of the Society for approval of ARs/AAs even if

appointment of some members was in progress. The reasons given for

the delay in appointment of members proposed for the Society that the

members had either retired or were deceased are not acceptable. The

Committee is unable to accept the explanation that suitable members

could not be found for four years for appointment to the Society. The

Committee notes that the composition of the Society had been notified

on 7th

November, 2019 i.e. a few days before the interaction of the

Committee with the CSIR on 11th

November, 2019 which confirms that

the reasons given for delaying its notification were baseless and

irrational.

(Para 2.21)

3. The Committee observes that the CSIR, by its own admission, faced no

constraints either in preparing ARs/AAs, or in translating or printing

the reports. The only impediments to timely laying of the ARs/AAs of

CSIR as stated by the organization and the Ministry were the time-lag

between the meetings of the Governing Body and the CSIR Society and

the necessity of taking approval of the President, CSIR for the AR/AA

at the meeting of the CSIR Society. The first reason is untenable as the

Ministry and CSIR have shown great laxity in notifying the composition

of the CSIR Society by letting more than 3 years lapse before the

notification. The second reason is not valid as the Bye-laws of the CSIR

Society provide for the Vice-President to chair the meeting of the CSIR

Society in absence of the Chairman. Therefore, neither of the reasons

which were repeatedly put forward by the Ministry and CSIR over the

years to explain the delay in laying are credible. The Committee

observes that such laxity is all the more deplorable when there were

Page 30

23

Audit paras pending which were allowed to remain outstanding because

the ARs/AAs were not being laid.

( Para 2.22)

4. The Committee observes that there were 6 Audit paras pending since

1999 which were settled in 2016-2018, which is a delay of about two

decades. 18 Audit paras pending from 2000 to 2013 were settled mostly

in the years 2015-2018 with delays of more than a decade. Audit paras

from the years 2015 onwards have mostly been settled after 2-3 years of

delay. The Committee observes further that there are no outstanding

audit paras at present and the delay in settlement of audit paras has

been considerably reduced. While acknowledging the organisation’s

efforts towards reduction in delay of settlement of the audit paras and

the achievement of nil pendency of audit paras, the Committee is

compelled to register its displeasure in the decades long delay in

settlement of earlier audit paras pending from 1999 onwards. The

reasons given for delay in settlement of the long outstanding paras are

unacceptable to the Committee. The Committee observes that

formulation of appropriate replies to audit paras to the satisfaction of

C&AG or revision guidelines to prevent recurrence of irregularities

took nearly two decades is a farcical excuse and not becoming of a

premier institute like the CSIR. The fact that Audit paras were kept

pending for nearly two decades for flimsy reasons reveals that there was

no serious attempt at settlement. Taken together with the fact that

despite the backlog of pending Audit paras, the ARs/AAs for the

previous four years were not laid at all, a regrettable state of affairs was

allowed to exist with no apparent attempt by either the organisation or

the Controlling Ministry to tackle the issues with the seriousness

warranted.

( Para 2.23)

5. The Committee finds it astonishing that the Ministry, which had the

duty of monitoring the preparation and laying of AR/AAs, did not take

up the matter of the pending reports earlier and it took an interaction

with a Parliamentary Committee to spur the Ministry and the

organisation to action.

( Para 2.24)

6. The Committee notes that the schedule for preparation of Annual

Accounts is a general time schedule given in the GFR, 2017 for all

organisations. The Committee observes that CSIR has not worked out a

Page 31

24

detailed schedule for preparation of its accounts with deadlines for

compilation and preparation of accounts for approval of the Governing

Body or of submission of replies to draft Audit reports.

( Para 2.25)

7. The Committee recommends that action for nominating members to the

CSIR Society may be initiated a few months before the expiry of the

terms of retiring members so that the vacant seats in the Society are

kept to a minimum. Since as per the byelaws the Society continues to

function irrespective of notification of members, the CSIR and the

Ministry may ensure that there is no delay in convening meetings of the

Society and obtaining the approval for the Annual Reports and Audited

Accounts.

(Para 2.26)

8. The Committee notes that the CSIR has already taken the initiative to

obtain approval for the Vice-President to chair the Society meeting

when the President was pre-occupied. Since the byelaws also contain a

provision for the same, there is no excuse for delaying holding the

meetings of the Society on the pretext that the President, CSIR Society

was unavailable to attend the meetings. The Committee avers that both

the excuses for delayed laying which have been repeatedly tendered by

the Ministry and CSIR over the years, namely non-constitution of CSIR

Society and difficulty in obtaining approval of President, CSIR for

AR/AAs, have been found, upon examination, to be indefensible and

unjustified. The Committee recommends that the CSIR and the

Ministry should ensure that in future, the ARs/AAs are approved as per

schedule and there is no delay in obtaining the approval of the Society

or in laying in Parliament.

(Para 2.27)

9. The Committee observes that the present schedule for Annual Accounts

is a reproduction of the generalized schedule given in Rule 237 of GFR,

2017 and recommends that a detailed schedule for preparation of

Annual Accounts may be drawn up, with deadlines for every stage of

preparation of accounts, submission to audit authorities, submission of

draft replies to audit queries, receipt of final audit report and

forwarding to Ministry for laying in the Parliament etc. The Committee

recommends that the Audited Accounts may be submitted to the CSIR

for approval by end of November so that the AR/AAs could be

Page 32

25

forwarded to the Ministry by mid-December for laying in the

Parliament.

(Para 2.28)

10. The Committee also recommends that all efforts may be made to

maintain the schedule for settlement of Audit paras within a reasonable

period of time and care may be taken not to have any lapse in this

matter. In future, Audit paras kept lingering for years together as was

done in the last decade for untenable reasons would be viewed seriously

and the Committee exhorts both the organisation and the Ministry to

ensure that the current momentum is sustained.

(Para 2.29)

EXTENSION OF TIME

11. The Committee observes that as per available record, the Ministry has

sought extensions repeatedly for the same year of Report, the average

being three extensions for every year of report from 2005-06 to 2015-16.

In the years 2012-13, 2014-15 and 2015-16, extensions had been sought

five times from the Committee. On many occasions, the Reports have

been laid after the last extended date inspite of the many extensions

granted by the Committee. For example, the reports for the years 2014-

15 and 2015-16 have been laid only on 20/9/20 after grant of five

extensions the last one being uptill 31/7/19. Moreover, the requests for

extensions in many cases have been forwarded well after the due date

for laying. The most glaring case is of the year 2016-17, wherein

extension has been sought almost two years after the due date of laying.

It is evident that the Ministry has treated the process of obtaining

extension from the Committee in a casual way, routinely obtaining

extensions with no efforts being made to comply with the extended

deadline.

(Para 2.30)

12. The Committee invites attention of the Ministry to its recommendation

in this regard made in Para No. 27 of its 1st Report, to seek extension

well in advance, as soon as it is clear that there would be a delay in

laying of the Reports: -

"In case of delay in respect of reports for periods upto 31st March,

1981, a statement explaining the reasons for delay should also be laid on

Page 33

26

the Table of the House along with the documents. If there is likely to be a

delay in laying a paper within the stipulated period, the administrative

Ministry should approach the Committee sufficiently in advance for

extension of time by explaining the reasons for doing so. A reference

should be made to the extension given by the Committee in the paper when

laid. This procedure should be followed in respect of all reports with

accounting periods from 1st April, 1981."

The Committee also draws the attention of the Ministry to its

recommendations in Para 11 of its 136th Report regarding repeated

requests for extension:-

“The Committee, therefore, cautions the Ministry and the Company

that Parliamentary norms of seeking extension from the Committee, in the

event of delay, must be adhered to. The Ministry must give valid reasons for

seeking extension. However, seeking the extension cannot be an unending

exercise. It is upon the Ministry and the Company to resolve the issues

causing the delay, because recurrent annual extensions for similar reasons

may be taken adversely by the Committee while considering the requests for

extension. In this regard, the Committee would like that in case of repeated

delays in laying, responsibility must be fixed.”

(Para 2.31)

LAYING OF DELAY STATEMENT

13. The Committee observes that the Ministry has been appending the

Delay Statement along with the ARs/AAs for the past few years.

However, the chronological order of events is given only after supply of

the accounts to the Audit, leaving out the events regarding the process of

compilation of the Annual Report. The Committee recommends that the

Annual Report of CSIR includes information regarding all its Research

Centers and compilation of the same takes some time, the timeline for

preparation of the Annual Report should also be given in the Statement.

The Committee emphasizes its recommendation contained in Para 3.17

of its 22nd

Report wherein it is stated that “The statements giving reasons

for delay should contain information, in chronological order setting forth

the dates of compilation of accounts, their submission to Audit, receipt of

draft Audit Report, replies given to audit queries, receipt of final Audit

Report, translation and printing of Accounts and their submission to the

Ministry for laying on the Table of the House. So that the House may

Page 34

27

identify the stages, causes and extent of delay and suggest remedial

measures wherever required.”

(Para 2.32)

LAYING OF REVIEW STATEMENT

14. Apart from the Annual Reports and Audited Accounts, the

Ministry/Department is also required to lay a Comprehensive Review

Statement. The Review Statement by the Ministry/Department is a very

important and informative document for the legislature since it

underlines the achievements made against the targets set as well as the

future plans chalked out to be achieved and critical areas to be

addressed.

( Para 2.33)

15. The Committee notes that the CSIR covers a wide spectrum of science

and technology and has numerous achievements covered in great detail

in its Annual Reports. However, only one Review Statement has been

laid for all the four years 2014-15, 2015-16, 2016-17 and 2017-18 and

this statement too is extremely brief merely stating that since the

Department is in agreement with Annual Report, no “Review” thereon

is being laid. The Committee has time and again taken the view that

mere agreement of the Ministry with the Report of the organisation

cannot be taken as an objective appraisal of the organisation. The

Committee draws the attention of the Ministry to its recommendation in

Para 3, 125th

Report :

“The Committee recommends that the Review by the Ministry should

be an objective appraisal of the performance against tangible benchmarks

and a comparative assessment of the Board’s performance vis a vis global

and domestic trends in the industry. The Committee also recommends that

Ministry should give the details of the process and methodology adopted

for conducting such a review.”

(Para 2.34)

UPLOADING OF ANNUAL REPORTS / AUDITED ACCOUNTS /

REVIEW & DELAY STATEMENTS

16. The Committee observes that the CSIR has uploaded all the Annual

Reports and Annual Accounts since 2003-04, both English and Hindi

versions on its website. However, the Delay Statement and Review

Page 35

28

Statements have not been uploaded. Moreover, the Annual Reports have

been uploaded under a common Head instead of a separate icon. The

Committee, therefore, recommends that the Ministry should ensure that

the CSIR gives complete information on its website by uploading the

Review Statements and Delay Statements till date, alongside its Annual

Reports. The Committee in this regard emphatically reiterates its

recommendation contained in Para Nos 1.21 and 1.22 of its 156th

Report which is as under:

“The Committee therefore recommends that all the Ministries/

Departments should upload Annual Report/ Audited Accounts/ Review

Statement/ Delay Statement, if any, of their organisations soon after laying

or within 03 days of laying of the papers in the House so that the same may

be easily accessible to the general public for their perusal and benefit. The

Committee further recommends that this leeway of 03 days is initially given

so that all the papers required to be uploaded may be placed in the public

domain for viewing. Later on all out efforts may be made to place the

papers so laid on the date of laying itself.”

(Para 1.21)

“The Committee is of the view that in the current era of ever

increasing level of internet penetration in the country, uploading of the

papers on the respective websites should be given the priority at par with

the laying thereof. In this backdrop, the Committee is of the opinion that

the process of laying should always be integrated with immediate uploading

of both English and Hindi versions of the papers on the website.”

(Para 1.22)

(Para 2.35)

UPLOADING OF LIST OF GRANTEE/ AUTONOMOUS

ORGANISATIONS ON THE WEBSITE

17. The Committee observes that GoI has released total funds of Rs. 30295.3

crore to the CSIR during the period of 2007-08 to 2016-17. As per Rule

230 (2) of General Financial Rules, 2017, each Ministry/Department

should make available, on the website, a list of institutions/organisations

along with details of the amount and purpose of grants given to them, in

order to avoid duplication in Grants-in-aid. But neither the details of

grants/funds released to the CSIR nor of any other grantee organization

under the control of the Ministry, is available on its website. The

Committee further observes that Ministry of Finance, Department of

Expenditure had vide Office Memorandum dated 16th September, 2020,

Page 36

29

forwarded to all the Ministries/Departments, directed them to comply

with the above cited provisions of the Rule 230 (2) of GFR, 2017, but it is

seen from the website of the Ministry that no such information is

available.

( Para 2.36)

18. The Committee, therefore, recommends that the Ministry should upload

details of grants released to the CSIR and all other grantee /autonomous

organisations under its control, on its website, in compliance to Rule

230(2) of General Financial Rules, 2017, without any delay and create a

separate icon for easy access of the same.

( Para 2.37)

Page 38

31

RECORD NOTE OF DISCUSSION

The Committee met at 3.00 PM on Monday, the 11th

November, 2019 in

Committee Room „A‟, Ground Floor, Parliament House Annexe, New Delhi.

MEMBERS PRESENT

1. Dr. C. P. Thakur - Chairman

2. Shri Sushil Kumar Gupta

SECRETARIAT

1. Shri Rohtas, Additional Secretary

2. Smt. Arpana Mendiratta, Director

3. Smt. Subha Chandrashekar, Under Secretary

4. Ms. Kiran K., Research Officer

WITNESSES

Department of Scientific & Industrial Research (DSIR) and Council of

Scientific & Industrial Research (CSIR)

1. Dr. Shekhar C. Mande, Secretary, DSIR & DG, CSIR

2. Shri K.R. Vaidheeswaran, Joint Secretary (Parl.), DSIR/CSIR

3. Ms. Sumita Sarkar, Financial Advisor, DSIR/CSIR

2. The Chairman welcomed the officials of Department of Scientific &

Industrial Research (DSIR) and Council of Scientific & Industrial Research (CSIR).

The Chairman in his opening remarks, observed that there was persistent and

extraordinary delay in the laying of Annual Report and Audited Accounts of CSIR

and also observed that ARs/AAs from the year 2014-15 onwards had not been laid.

He also brought their attention to an earlier assurance given by CSIR in a previous

Page 39

32

meeting with the Committee held in 2007 wherein the erstwhile DG of CSIR had

enumerated the reasons for delay and had apprised the Committee of the remedial

measures proposed to be taken to mitigate the delays. The Chairman sought to

know reasons in the failure in arresting delay and the pendency in laying of papers

of the last five years.

3. The Secretary, DSIR began his submission by giving a brief introduction

about DSIR and the bodies under the Department. Thereafter, he informed the

Committee about the functioning about CSIR. The Secretary accepted that there

was delay in laying of ARs/AAs of CSIR. He stated that CSIR is governed by two

bodies - Governing Body and CSIR Society. The Governing Body frequently

reviews the functioning of CSIR and the Society meets once a year where it

considers the progress made by CSIR and approves the ARs/AAs. He further stated

that the ARs/AAs of the financial years 2014-15, 2015-16, 2016-17 and 2017-18

had been approved by the Governing Body but CSIR Society‟s approval of the

papers was pending.

4. The Secretary submitted that the Prime Minister is President of the

Society and Minister of Science & Technology and Earth Sciences is the Vice

President of the Society which comprises of about 30 members which includes

Ministers of Finance and Commerce & Industry, Secretaries of various

Ministries/Departments, ex-officio members, etc. The Committee was apprised that

the term of the Society had expired and the composition of the new Society had

been notified and it was expected the meeting of the Society will be held very soon

and the ARs/AAs would be placed before the Society and laid in Parliament

thereafter.

Page 40

33

5. Issues such as clearance of outstanding audit paras, efforts taken to constitute

the CSIR Society and hold the meetings, quorum required for CSIR Society

meetings, bylaws of CSIR Society regarding proceedings of Society, term of CSIR

Society, retrospective approval of ARs/AAs by CSIR Society, cost-effective

alternative methods to stubble burning, effectiveness of green crackers and air

purification equipments developed by CSIR, accessibility of Traditional Knowledge

Digital Library to the public, schemes to promote innovation, CSIR Labs and their

accessibility to students of Government schools etc. were discussed.

6. A Verbatim Record of the proceedings was kept.

7. The meeting adjourned at 4.10 P.M.

ARPANA MENDIRATTA

DIRECTOR

DATED THE 11TH

NOVEMBER, 2019 NEW DELHI

Page 41

34

MINUTES OF THE MEETING OF THE COMMITTEE

ON PAPERS LAID ON THE TABLE (COPLOT),

RAJYA SABHA

II

SECOND MEETING

The Committee met at 3.30 PM on Thursday, the 22nd July, 2021 in

Committee Room „A‟ Ground Floor, Parliament House Annexe, New Delhi.

Members Present

1. Shri K.C. Ramamurthy – Chairman

2. Shri Kanakamedala Ravindra Kumar

3. Shri Shwait Malik

4. Shri Deepak Prakash

5. Shri G.K. Vasan

6. Shri Harnath Singh Yadav

SECRETARIAT

1. Shri Jagdish Kumar, Additional Secretary

2. Sh. Prem Singh, Director

3. Shri Sanjeev Chandra, Additional Director

4. Smt. Subha Chandrashekar, Under Secretary

WITNESSES

Ministry of Education

1. Shri Amit Khare, Secretary

2. Shri Vineet Joshi, AS (CU)

3. Ms. Kamini Chauhan Ratan, JS (HE)

4. Shri Subhash Chand Sharu, Director (CU)

University Grants Commission (UGC)

1. Prof. Rajnish Jain, Secretary

2. Shri P.K. Thakur, Financial Adviser

3. Dr. Jitendra Kumar Tripathi, Joint Secretary

Page 42

35

University of Delhi (DU)

1. Prof. P.C. Joshi, Vice-Chancellor (Acting)

2. Dr. Vikas Gupta, Registrar

3. Shri Girish Ranjan, Finance Officer

2. At the outset, the Chairman welcomed the Members of the Committee. He, then,

apprised the Members regarding the first agenda of the meeting i.e to consider and

adopt the draft 162nd

Report on „Laying of Annual Reports and Audited Accounts

of Council of Scientific and Industrial Research.‟

3. The Committee adopted the draft Report and authorized the Chairman to carry

out any changes on account of any typographical/factual errors. Thereafter, the

Committee decided that the Report may be presented to the Rajya Sabha on 27th

July, 2021 and authorized the Chairman and in his absence, Shri Deepak Prakash,

and in his absence, Shri G.K. Vasan to present the Report to the House.

4. ***

5. ***

6. ***

7. ***

8. ***

9. ***

10. The verbatim record of the proceedings was kept.

11. The Committee then adjourned at 4.58 P.M.

SANJEEV CHANDRA

ADDITIONAL DIRECTOR

Dated the 22nd

July, 2021

New Delhi

*** Matter pertains to other subject

*********