ReportNo. 17554-LAC OECS Financial Sector Review May 27, 1998 Finance, Private Sector & Infrastructure Unit Caribbean Country Management Unit Latin America and the Caribbean Region U Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript

Report No. 17554-LAC

OECS Financial Sector Review

May 27, 1998

Finance, Private Sector & Infrastructure UnitCaribbean Country Management UnitLatin America and the Caribbean Region

U

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Currency Unit: Eastern Caribbean Dollar (EC)

EC 2.70 = US$ 1.00(May 20, 1998)

FISCAL YEARJanuary 1 - December 31

ACRONYMS AND ABBREVIATIONS

AEF Africa Enterprise FundAPDF Africa Project Development FacilityATM Automated Teller MachineCOOPS Cooperatives Strengthening ProjectEC Eastern CaribbeanECCB Eastern Caribbean Central BankECEF Eastern Caribbean Enterprise FundECHMB Eastern Caribbean Home Mortgage BankFDI Foreign Direct InvestmentFTC Federal Trade CommissionGDP Gross Domestic ProductIFC International Finance CorporationINDECOPI National Institute for the Defense of Competition and Intellectual Property RightsLUCELEC St. Lucia Electric Services Ltd.OECS Organization of Eastern Caribbean StatesSWOT Strengths, Weaknesses, Opportunities, Threats

Vice President Shahid Javed BurkiCountry Director Orsalia KalantzopoulosSector Director Danny LeipzigerTask Manager John Pollner

-i -

OECS FINANCIAL SECTOR REVIEW

TABLE OF CONTENTS

Executive Summary ............ Page iii

Part I General Economic Background .Page 1

Part II Overall Assessment ..................... Page 2

Research and preparation of this report was conducted by a team consisting of John Pollner(Task Manager, LCSFP), Meir Kohn (Principal Consultant), Steve Webb (Sr. Economist,LCSPR), and Isabelle Daverne (Financial Consultant). Key discussions and inputs for thispurpose, were provided by Mr. Dwight Venner, Governor of the ECCB, and Messrs. ArthurCampbell and James Fleming of ECCB's Financial and Enterprise Development Unit.

- iii -

EXECUTIVE SUMMARY

1. The Eastern Caribbean has benefited from monetary and price stability in the quartercentury in which most islands obtained independence from Britain, and has avoided the financialcrises that hobbled economies elsewhere. The Eastern Caribbean Central Bank (ECCB) and themember countries want to continue this laudable record while at the same time modernizing thefinancial sector and making it a dynamic force for economic development. This is especiallyimportant as the end of the century finds stagnation or decline in several traditional sectors.

2. Despite its avoidance of crises, the financial sector has serious problems. Most of themare in three categories - geographic fragmentation, industry fractionalization, and shortage ofinstitutions to provide long term and venture capital to the private sector:

(i) Fragmentation results from legal and regulatory obstacles that block integration withinthe Eastern Caribbean and de-link it from the international financial system.(ii) Industry fractionalization which generates diseconomies of scale in each country,results from both fragmentation of the sub-regional market, proliferation of 'transactionintermediaries' that add little to resource mobilization efforts in the industry, and highcosts of intermediation due to the scale of lending versus other financial institutions.(iii) Changes of technology and global trading patterns should be opening newopportunities for the economies to shift away from declining sectors, such as sugar andbananas. But lack of institutions to mobilize financing for private sector ventures,combined with scarcity of human resources, and regulatory barriers, hinders dynamicadaptation of the economies.

3. The ECCB has taken the lead in developing with member governments, a program tocreate a single financial space for the Eastern Caribbean and to upgrade the sector to help the sub-regional economy meet the challenges of the next century. The ECCB is seeking and should begiven support within the region and externally, to design, refine, and implement the program. Theon-going projects to improve fiscal management, public sector efficiency, and the overall climatefor business also deserve support as important complements to financial sector efforts.

Financial Sector

4. Commercial banks are and will remain the backbone of the area's financial system. Thebranches of the four foreign-owned banks, which account for roughly half of deposits, and someof the indigenous banks are sound, some are not. The problems stem in part from the dependenceof indigenous banks on the small undiversified economies of individual islands and occasionallyinappropriate political interference in lending policies.

(i) The ECCB's ongoing program of assuring provisioning for losses, strengthening bankmanagement, privatization of publicly owned banks, and merging banks across islandsshould continue.(ii) To provide safe, competitive and efficient banking services, the system will need torationalize banks on each island, each one operating branches at least throughout theEastern Caribbean in order to achieve adequate scale and diversity.

-iv -

5. Credit unions, Development Banks, and Insurance Companies are importantcomplements to the commercial banks. National governments have supervision responsibility forthem, but generally lack the capacity to do so adequately. The ECCB is working withgovernments to supervise these institutions and direct their rationalization. This program shouldcontinue, and ECCB should facilitate the standardization of regulations and supervisory practicesas an information broker and disseminator of best practice.

(i) While a combination of mergers and exits in the 1990s has substantially rationalizedthe life insurance sector, general insurance is plagued by excessive taxation, a commissionstructure which provides distorted incentives against capital reserves, and the proliferationof small insurers, which impairs efficiency and safety. All aspects of insurance need tighterstandards and supervision, supported with public education.(ii) Regulations should be changed to allow these institutions to operate freely betweenislands.

6. Contractual arrangements for long-term savings - pensions, life insurance, and socialsecurity which is currently the most important - need to be strengthened to assure adequateretirement payments for today's pool of workers, and to fund investment for sustainable growth.The design of these systems should cautiously but steadily evolve to become fully funded andpossibly contribution defined, and to take advantage of recent innovations in institutionaltechnology that allow greater transparency and responsiveness to investment preferences ofparticipants. The objectives of macroeconomic stability, assurance of minimum retirementbenefits, higher returns, greater investment in the Eastern Caribbean economy, and internationaldiversification, compete and conflict to some extent. Thus a balanced approach whichincorporates each of these elements without favoring some in the extreme, is crucial.

Securities Markets

7. Developing region-wide securities markets is an important part of the ECCB's plan forincreasing the financial sector's contribution to economic growth. Many steps are needed toreach the goal, and the ECCB plans to proceed in a sequential manner. Experience in the regionand elsewhere should be utilized, ensuring that the basic institutional infrastructures and financialinstruments which drive and provide liquidity to the capital market, are well established early on.

8. Establishing an integrated market for government securities would be the first step, as apool of assets already exists and valuation is relatively transparent. Establishing this market couldbuild up inter-island information and trading systems, which could then be utilized for othersecurities.

9. An OECS/ECCB area-wide equities market could help fill the private sector's need forlonger-term financing and venture capital. It will require:

(i) Eliminating restrictions on inter-island investment and labor mobility.(ii) Establishing rules and reliable mechanisms for payment and trading, and for disclosureof information on companies.(iii) Establishing a sub-regional institution to monitor and enforce proper securities tradingwith adequate technology to assure timely interventions, if needed.

(iv) Generating a pool of public companies to increase shares in circulation; this will bemore easily encouraged through privatized public enterprises.

10. Commercial banks would need to help handle payments for capital market transactionsand could execute trades for customers. Of course they would participate in the governmentsecurities market where they are now the major stakeholders. Their participation and capitalexposure in the equities market should be limited, however.

11. Contractual savings institutions should participate in the securities markets, but this shouldbe with clear rules on asset risks, especially for disclosure to participants, on changes in marketvaluation in the equities market.

12. The securities market should ultimately be opened up to allow for internationaldiversification in local portfolios and local diversification in international portfolios, as prudentialrisk reduction measures and to encourage participation in equity investments. This might proceedin a phased manner to assure that domestic enterprises and firms are not squeezed out of financingsources which the sub-region's envisioned capital markets are meant to support.

OECS FINANCIAL SECTOR REVIEW

PART I

GENERAL ECONOMIC BACKGROUND

The Organization of Eastern Caribbean States (OECS) consists of Anguilla, Antigua &Barbuda, Dominica, Grenada, Montserrat, St. Kitts & Nevis, St. Lucia, and St. Vincent and theGrenadines. The combined population is approximately 550,000. In 1995 combined GDP of theOECS was approximately US$1.9 billion or US$3,400 per capita. Per capita GDP variedsignificantly from territory to territory, from a high of US$6,800 for Antigua and Barbuda to alow of $2,000 in St. Vincent and the Grenadines.

Up to the 1950s the economies of the territories were overwhelmingly agricultural-mainlyspecializing in either bananas or sugar. There has since been a steady shift, accelerating in the1980s, away from agriculture and towards tourism. In general, the territories in which income hasrisen most are those in which this shift has proceeded the furthest. Overall, tourism todayaccounts for 10.8% of GDP and agriculture 9.3%. Manufacturing remains relatively small (5.5%)and consists largely of food processing and enclave industries such as garments and smallassembly plants. Construction is significant (9.8%), much of it serving the needs of tourism.

The economies of the territories are very open: imports are 56% of GDP; exports 16%,services balance 22%. Foreign direct investment of 7.4% of GDP largely balances the currentaccount deficit. A large part of trade is with other CARICOM countries. Other important tradingpartners are the U.S. and the E.U., with both of which it enjoys trade preferences. Thesepreferences are being phased out, and this is likely to shrink agriculture even further. Themembers of the OECS share a common currency (the EC dollar) issued by a joint central bank,the Eastern Caribbean Central Bank (ECCB). The EC dollar has, since 1976, been at a fixedparity against the US dollar. Consequently, the sub-region has enjoyed a stable monetaryenvironment.l

Two aspects of the OECS economies stand out - their very small size and theirvulnerability to shocks. Even taken as a whole, the OECS is a very small economy. Moreover,internal barriers prevent the territories from constituting a single market, and some of theindividual territories are quite tiny. Indivisible fixed costs are consequently a barrier to all forms ofeconomic activity: the market is so small that import is often unprofitable, let alone localproduction. The OECS economies are highly vulnerable to shocks. They are unusually exposed tonatural disasters - particularly hurricanes, and less frequently to drought and volcanic eruption.Because of their small size, the impact of a natural disaster can be far more devastating than for alarger economy where the damage is localized. Another source of potential shocks is the heavydependence on tourism, an industry that is sensitive to recessions in the tourists' countries oforigin2. The smallness of the economies and their exposure to shocks dictate two predominantconcerns: (i) the exploitation of all possible economies of scale and scope; and (ii) the greatestpossible effort to mitigate risk. These considerations, important in the real economy, should beuppermost too in considering the development of the financial system.

lIn the following, dollar means EC dollar unless otherwise indicated.2Correlations between U.S. and OECS GDP growth rates over a 15 year period bear this out. While non-tourism factors alsoimpact on OECS growth, given the substantial tourism sector as a % GDP, downturns correlated with the U.S. and Europeinvariably impact the tourist trade in the OECS, not only in service exports but capital investments as well.

-2-

PART II

OVERALL ASSESSMENT

The financial sector of the OECS/ECCB area is poised for an increased pace of change.The basic institutional infrastructure and scope of financial institutions in the area have reached acritical mass, and now stand ready to cooperate in collectively augmenting the supply of financialcapital throughout the OECS. This should be through taking advantage of economies ofintegration and opportunities for deepening the capital markets to generate long-term financingfor development opportunities in the private sector. The main institutional players in the currentstructure are the banks, the ECCB, the government securities market, pension funds, insurancecompanies, credit unions, finance companies, and the budding private enterprise sector.

The capital market instruments and institutions being utilized and/or considered to achievethese objectives, include the government bond market, the Eastern Caribbean Home MortgageBank, a Call Exchange for debt and equity trading, an Enterprise Fund, and a Unit Trust (MutualFund) to provide increased access by investors to a future capital market. All of these institutionsand mechanisms are expected to contribute to the development of a more robust market in theOECS/ECCB area. The importance of sequencing the implementation of these initiatives so as tobuild up the supporting regulatory frameworks and facilitating market mechanisms, however, willbe key factors to ensure a smooth and successful transition towards a flexible financial sectorwhich can meet the developmental and financing needs of the sub-region. In this respect, thisreport attempts to identify the constraints and existing or recommended facilitating factors whichneed to be addressed and acted on to achieve these objectives in a timely manner. This shouldpave the way for an enabling financial, legal, and regulatory environment which will provide theimpetus to the proposed institutions and structures. This should generate the envisioned resourceflows within a dynamic and modernized financial sector.

The financial system of the ECCB area, however, currently suffers from two majorconstraints -- (i) inter-territory fragmentation and (ii) intra-territoryfractionalization.Fragmentation is the result of legal and regulatory obstacles as well as infrastructure and logisticalfactors that block integration within the area and separate it from the international financialsystem. Fractionalization, partially related to fragmentation, is the result of proliferation ofnumerous operations and intermediaries within each island, particularly in the general insuranceand credit union sector but also in banking, thus leading to high aggregate fixed costs, increasedfinal costs to consumers, and less efficient generation of surplus capital in the financial sector.

FRAGMENTATION

Inter-island fragmentation of the financial system in the ECCB area is harmful in threeways. First, it is economically inefficient. Differences in interest rates and in liquidity acrossterritories and across institutions indicate that funds are not going to their most productive uses.As a result, both the level and the rate of growth of area income are lower than they might be.Second, fragmentation creates domestic financial institutions - banks, credit unions, insurancecompanies -that are localized and not well diversified. The result is also high operating costs andreduced safety.

St.Kitts & Nevis 9.50-12.00 9.50-21.60 1.50-6.00 4.00-5.00

St. Lucia 9.50-10.00 9.50-23.00 2.00-7.00 4.00-6.00

St. Vincent & Gren. 9.50-11.00 9.50-16.50 1.50-5.00 4.00-5.50

The third way in which fragmentation is harmful is that it prevents the financial systemfrom playing its essential role in spreading risk. A recent study investigated the mechanisms thatenabled residents of individual U.S. states to maintain their consumption in the face of shocks totheir state economies.3 It found that the most important mechanism (smoothing 39% of shocks tostate income) was the cross-ownership of productive assets. If households derive investmentincome mainly from productive assets in other states, a shock to one state's income has littleeffect on its own residents' investment income; the effect is spread out over other states. Thesecond most important mechanism (smoothing 23% of shocks to state income) was borrowingfrom residents of other states and the sale to them of financial assets. The federal government,through its system of taxes and transfers, smoothed only 13% of shocks to state income.

The role of the financial system in spreading risk is especially important for the economiesof the OECS, subject as they are to an unusual degree of risk. Fragmentation reduces enormouslythe ability of the financial system to fulfill this role: it places obstacles in the way of cross-ownership of productive assets; it hampers borrowing from foreigners; and it makes difficult theholding of foreign assets that can be sold to support consumption in the event of a shock toincome. It should be noted, however, that extensive foreign direct investment has led tosubstantial foreign ownership of productive assets in the OECS.

The causes of financial fragmentation within the ECCB area include the following:

(a) Risk aversion and lack of confidence by financial institutions to expand their lendingoperations outside the home territory. This is in part due to the traditional businessculture, but also due to territorial differences in business licensing, disclosure, and taxpractices.

(b) Legal restrictions such as the Alien Land Holding Acts which restrict foreign(including intra-OECS) ownership of domestic assets such as real estate and majority

3 Asdrubali, Pierfederico, Bent E. Sorensen and Oved Yosha, 'Channels of interstate risk sharing: the United States 1963-1990," 0Quarterly Journal of Economics I I 1, November 1996, 1081-1110.

-4 -

equity ownership positions in local enterprises. In the case of company equity sharestransacted in the existing private market, each territory has differing rules allowing thedegree of foreign and intra-OECS ownership.

(c) Differential tax policies: most territories have withholding taxes on the payment ofprofits, interest, etc. for non-residents and foreigners, in contrast to residents. Interest ongovernment securities and on domestic bank deposits in the majority of cases is tax-free toresidents only. ECCB however, is currently engaged in on-going initiatives to promoteharmonization and consistency in these areas and to encourage cross-border integrationand business activity.

All of these obstacles also serve to separate the financial systems of the territories from theinternational financial system. Of course, it is not only in terms of their financial systems that thearea's economies are fragmented. There is very little cross-border economic activity of any kind.Few business operate in more than one territory. Obstacles cited by businessmen include complexlegal and regulatory environments that differ from territory to territory, uncertainty about futuretreatment of outside investors, and generally a tradition of conducting business only within thehome territory.

FRACTIONALIZATION

Fractionalization results in diseconomies of scale due to the number of comparativelysmall financial institutions existent within each country/territory. In the banking sector this is theresult of two factors:

(i) due to the traditional practice for domestically owned businesses to conduct bankingwithin single territorial borders, cross-border diversification and operational efficiencies have notbeen fully achieved, as discussed above. This has resulted in less diversified portfolio 'hedging'against credit risks, proportionately higher fixed costs per institution, and thus higher overallintermediation costs. In addition, such diseconomies of size do not provide sufficient flexibility(both institutional and financial) to domestic banks, for developing much needed, new financialproducts to provide additional investment liquidity for private enterprise. Such products includethe offered fixed income instruments (e.g.: commercial paper, banker's acceptances) to investorsas well as longer-term lending products to borrowers. The institutional capabilities foraccelerating the circulation of funds in the financial sector, and facilitating secondary marketsthrough potentially dealing in government securities and equities, is also constrained by therelative size, technical infrastructure, and capital requirements of the domestic banks. This is notto say that bigger is always better, but rather to recognize that there are minimum institutional andcapital requirements needed to prepare the banking sector for a larger role in augmenting the poolof investment funds. In this regard, the additional complexity of such operations would implysome degree of capital expansion, and possibly, industry consolidation.

(ii) due to the earlier role of foreign branch banks which lent primarily to foreign businessenterprises, the indigenous banking industry grew to meet the demand for domestic needsincluding housing finance, domestic business, and public enterprise operations. This separation ofroles, while meeting emergent needs, also resulted in an increase in the number of domesticinstitutions, which, due to their independent expansion within each territory, necessarily impliedoperations of relatively small asset portfolios and thus higher operating expense / asset ratios. This

- 5 -

effect increases the spread between rates savers receive and rates borrowers pay and reduces therange and volume of financial products available to them. Further consolidation at the national(and sub-regional) level as well as further OECS-wide integration of the industry would mitigatethese diseconomies of scale and reduce the current fractionalization in the industry. This could beaccomplished more effectively through further privatization of government owned banks in orderto promhote a larger equity market while allowing the private sector to consolidate to achieve amore optimal efficiency equilibrium.

The public sector role should focus on facilitating an integrated area-wide market forgovernment securities, which would be highly beneficial for the OECS financial system. With thefixed costs of market infrastructure borne by the government securities market, the marginal costsof adding trading in other securities (such as private bonds and equities) would be much lower.Liquid T-bills would provide ideal collateral for short-term lending. Government debentureswould make an ideal safe asset for contractual savings institutions (lifes and pension funds).4 TheECCB has already started initiatives aiming to equalize the tax treatment of government securitiesin the OECS, and this should be given priority due to the benchmarking function and maturityrange which government securities offer in setting the base for the capital market.

The phenomenon of fractionalization is even more prevalent in the general insuranceindustry and in the credit union sector. A proliferation of 'market' players for property andcasualty insurance, including brokers and agents, as well as a number of primary insurancecompanies, exceed the per capita needs of the OECS. Primary companies themselves are subjectto strong commission incentives by ceding their domestic portfolio coverage to internationalreinsurers. The broker and agent businesses which primarily serve the primary companies toattract customers, are net commission driven concerns, and at current supply levels, impedeeffective capital market development and risk spreading functions of well-capitalized insuranceintermediaries. Thus, the diseconomies of intermediation caused by this fractionalized industryprevents this sector from deepening the capital market. The widespread competition for directfees discourages primary domestic insurers from accumulating reserves which could be deployedinto the financial system. This along with tax disincentives in this sector, results in a high dividendpaying industry, a high dependence on foreign reinsurance, and continued fractionalization. Withrespect to the credit union sector, this serves smaller community-based constituencies, but there issome room for economies of scale both within each territory and across the sub-region, byconsolidating institutions serving similar community groupings with common interests and/orattributes, such as government employees.

Recommendations (Also see Part III 'Financial Integration')

a. Tax Reform: To further financial sector integration and outside investment, thereshould be no tax preferences or differential treatment for specific financial assets -- in particular,tax differences in this regard within the OECS territories, mitigate against sub-regional financialintegration. Interest on government securities, on local bank deposits, and on the bonds of theECHMB should be taxed consistently and in line with other investment income. Taxes on

4However, a market for government securities would not, as has sometimes been suggested, provide "benchmark" rates forprivate borrowing. Given the monetary regime, the debt of individual governments is analogous not to federal debt in theUnited States, but to state or municipal debt: since OECS governments cannot monetize their debt it is not risk-free(conceivably, private borrowers might be able to borrow at lower rates than some governments). Again given the monetaryregime fixed to the US dollar, benchmark rates already exist - those of the US dollar market.

-6-

foreigners or foreign holdings of domestic investments should be minimized or avoided whenthese have the effect of protecting domestic concerns at the expense of a level-playing competitiveenvironment which would otherwise encourage inflows of external capital. Taxes on the transferof securities (stamp duties) should be phased out since their existence is an obstacle to creatingliquid secondary markets in tradable financial instruments.

b. Legal and Regulatory Restrictions: Alien Land Holding restrictions should be revisedand/or repealed, particularly when these affect intra-OECS transactions, but also to allow value-added foreign investment concerns to contribute to the domestic economies. Withholding taxes onforeign investment income should be phased out, when similar treatment is not applied toequivalent resident income, and when such foreign investment income is already taxed in the homecountry5 . Delays for foreign as well as domestic lenders in enforcing debt contracts in domesticcourts, should be minimized. Short of undertaking a major judicial sector reform, this could beachieved via the establishment of a trade & commerce agency which would have administrativepowers to rule on commercial disputes on a fast track basis. Such an agency (modeled along thelines of the U.S. FTC or Peru's INDECOPI6) would be staffed and guided by professionalspecialists from the private sector contributing technical/egal advice on a part-time as-neededbasis. While the judicial system could still be accessed subsequently by the litigants, theadministrative trade/commerce agency (as in other countries) would likely discourage suchappeals given its professional competence and technical backing on administrative rulings. Theagency would strive to be self-funded by charging fees for its services while minimizing the needfor formal, more costly and time consuming legal sector interventions.

c. Exchange Controls: Licensing and administrative procedures required for theacquisition of foreign financial assets should be simplified to encourage investment inflows anddiversify the savings base to assure safety and long-run stability. As discussed later in the report,regulations can be put in place to avoid merely speculative capital flows from destabilizing thefinancial system. Domestic savers and, more important, domestic financial institutions should notbe discouraged to acquire foreign financial assets -- authorization procedures for this should belimited to complying with proper monitoring of foreign exchange transactions, and this could beoptimized via ex-post rather than ex-ante reporting requirements. Small savers are unlikely topurchase foreign financial assets directly themselves. The current procedures make it difficult forthem to do so indirectly through financial institutions. It would be desirable, for example, forbanks to offer domestic savers mutual funds partially invested in foreign securities.

There may be some concern about the consequences of exchange liberalization on thebalance of payments. The purchase of foreign assets is balanced by saving (with a reduction inimports), by foreign direct investment (which is already substantial) and by foreign portfolioinvestment (which may increase with development of the capital market). In the event of a naturalcatastrophe or severe economic downturn, the sale of foreign assets would balance an increase inimports, serving to stabilize the balance of payments. Thus, while this entails transferring somecontrol of foreign exchange and foreign savings diversification to the private sector, the benefitsof such diversification and security in access to funds outweighs the risks of restricting investmentto home markets. While intra-OECS liberalization will to some extent mitigate this, it only reflects

5 While this practice varies by country, those countries with successfil FDI experience have avoided such taxes.6 In the U.S. this is the Federal Trade Commission. In Peru, INDECOPI is the Institute for the Defense of Competition andIntellectual Property.

-7 -

a first necessary step in the process of integrating the sub-regional financial system andsubsequently using it to tap the international capital markets. Under the practice of virtually fullbacking of the currency, capital flight would be counteracted by upward adjustments in domesticinterest rates due to reductions in the supply of credit. This adjustment, however, would serve tomake domestic financial investments more competitive in order for the banking system to attractadditional funds to meet borrowing demand. In any event, a phased-in regime for suchliberalization might be more adequate in the OECS context. Foreign portfolio investment limits asa percentage of total assets held by individuals or institutional investors could meet diversificationobjectives and mitigate capital flight.

- 8 -

PART HI

THE FINANCIAL SYSTEM

Eastern Caribbean Central Bank (ECCB)

The ECCB acts as a currency board, standing ready to exchange US dollars for EC dollarsat a rate of EC$2.70 = US$1.00. The ECCB is required to back at least 60% of its monetaryliabilities with foreign currency assets. Actual backing is 98%. Up to $100,000 (per transaction)may be converted into foreign currency without formality. Larger amounts require authorization.ECCB lending to member governments is strictly limited by statute.7 It provides a small amountof export credit guarantees.

The ECCB operates an interbank market for reserve deposits, and is ready to lend tobanks for reserve management at administered deposit and lending rates, for periods up to 30days. Borrowing banks must collateralize with fixed deposits, T-bills, or other acceptable paper.Banks do not take advantage of this facility: presumably the alternatives are less expensive ormore informal. The ECCB also manages what is in essence a call repo market (the secondarytreasury bill market/discount window). It makes a portion of its portfolio of domestic T-billsavailable for discount to commercial banks and stands ready to rediscount at the banks'discretion. Banks rediscount when liquidity is tight. Discount and rediscount rates areadministered. In addition, as a separate facility, banks with excess liquidity can also make depositswith the ECCB in a 24 hr./7-day call account, at a competitive interest rate. The ECCB also offersbanks fixed deposit accounts at prevailing market rates for periods of 1,2,3, and 6 months.

The ECCB is the sole supervisor and regulator of commercial banks in the memberterritories (all of which recently passed a uniform banking act). Banks must submit periodicfinancial reports and are subject to regular on-site inspection. All other financial institutions --offshore banks, insurance companies, and credit unions -- are regulated and supervised by theindividual territories, sometimes with advice and assistance from the ECCB. Banking supervisionprocedures appear to be well organized, but there seems to be a need to develop more 'crisis'contingency planning and readiness for potential systemic problems, even though at present suchthreats are not on the horizon due to the stable macroeconomic situation and the monetary regimeincludes a number of statutory safeguards (see Box 1) to maintain discipline.

Somewhat worrisome, however, is the sector's reported non-performing loan rate for thedomestic banks which on average represent about 10% of the portfolio. While such a proportionis not "critical" relative to the entire portfolio, it is significantly higher than international practice.In addition, loan loss provisions for banks with higher non-performing loans are not fullyadequate, as they have been adapting to recently implemented stricter provisioning requirementsfor non-accruing assets. Therefore, while immediate risks are not major, careful monitoring ofbank portfolios and their compliance with loss provisioning should be an on-going priority toassure the preservation of usable capital. Such capital will be essential to support the proposedcapital market's institutional infrastructure. As will be explained later, the banking sector's role inproviding liquidity to an emerging capital market will be significant.

7The ECCB has allocated credit lines to member governments based on its 60% backing requirement. It is because mostgovernments have not drawn in these credit lines that the backing ratio is so high. See also Box 1.

- 9 -

Box 1: The OECS/ECCB Monetary Regime and its Safeguards

The ECCB area is a monetary union of eight island micro-economies, which by definition ischaracterized by the issuance of a single common currency, the flow of which is unrestricted among itsmembers; a common pool of foreign exchange reserves; and the existence of a central monetary authority,which decides on monetary policy. Although a monetary union, the responsibilities and powers of theECCB are in many ways similar to those of other central bank. The ECCB has the statutory responsibilityto regulate the availability of money and credit; to promote and maintain monetary stability; to promotecredit and exchange conditions and a sound financial structure conducive to balanced growth anddevelopment.

The main central banking functions prescribed in the ECCB Charter relate to the foreign exchangecover, the limits on the amount of credit which can be extended to governments by the Bank, and theregulation and supervision of banking business. In relation to the foreign exchange cover, the ECCB isrequired at all times to maintain external reserves in an amount not less than sixty per cent of the value ofcurrency in circulation and other demand liabilities. With respect to lending to governments, the Charterstipulates that the Bank may extend a limited amount of credit to participating governments by way oftemporary advances to meet seasonal needs, and by way of holdings of Treasury Bills and governmentbonds. For the purpose of regulation and the conduct of monetary policy, the ECCB has among otherthings, the authority:

(i) to impose reserve requirements;(ii) to purchase from, sell to, discount and rediscount for financial institutions, bills of exchange

and promissory notes maturing within 91 days;(iii) to grant secured advances or loans to financial institutions for periods not exceeding 91 days.

The ECCB is therefore not a currency board, although in keeping with the limitations of its charter,its operations have broadly resembled those of a currency board. The ECCB currently maintains a foreignexchange cover of 98 per cent, and generally over the years, the cover has been maintained at a level inexcess of 80 per cent. The ECCB extends limited amounts of credit to participating governments, and onoccasions has also made secured advances to commercial banks, although in recent times this latter activityhas been rare. The ECCB also operates a repurchase arrangement, whereby it sells Treasury Bills acquiredin the primary market for its own portfolio to commercial banks on a repurchase basis, to enable the banksto better employ their excess reserves. As it pursues its efforts to develop the government securities marketon a region-wide basis, the ECCB intends to maintain the strictures that have governed its operations. Anysupport that it may provide to the market would therefore be consistent with the current limitations on theholdings of government securities as prescribed by the charter.

The ECCB is committed to the maintenance of the fixed exchange rate for the EC dollar. The ratehas been maintained unchanged since the establishment of the link in July 1976 with the US dollar. Thefixed exchange rate policy has served the currency area well, and over the years, the countries have beenable to achieve relative price and balance of payments stability, and relatively good rates of economicgrowth. This policy has generated considerable confidence in the EC dollar both within and outside thecurrency area. It has also enhanced the environment for decision-making in relation to production andpricing, and for savings and investment.

Stability in the value of the EC dollar is the primary objective of ECCB. It is recognized that this isdependent on continued strong backing for the currency. All the operations and activities of the Bank willcontinue to be made consistent with this overriding objective of monetary stability with a fixed exchangerate.

- 10-

FINANCIAL INTERMEDIARIES

Financial intermediaries as a whole hold a total of $8 billion in assets. Commercial banks,with 72% of this total ($5.8 bn.), dominate the financial system. In comparison, social securityfunds hold 16%; credit unions, 5%; insurance companies, 4%; and development banks 3%. Theratio of M2 to GDP, a standard measure of the "depth" of a financial system, is 90%, which isquite high by international standards. Non-resident deposits amount to 12% of total deposits.

MONETARY STATISTICS

(EC$ Mn.)

M2 Currency Demand Savings Time Forex M2 as %

deposits deposits deposits deposits of GDP

Anguilla 318 8 9 36 50 216 172%

Antigua & Barbuda 1,118 69 192 388 411 58 95%

Dominica 491 27 77 207 175 5 86%

Grenada 709 53 96 356 174 29 100%

Montserrat 109 12 18 55 17 7 74%

St.Kitts & Nevis 711 29 71 225 307 78 122%

St. Lucia 1,132 63 167 432 452 17 83%

St. Vincent & Gren. | 600 31 115 207 238 9 87%

Total ECCB Area 5,188 292 7 745 1,906 1,824 420 96%Data as of June 30, 1997

Commercial Banks

The five "branch" banks were operating as branches of foreign banks at the time theterritories became independent and were allowed to continue as such. Most of these branch banksoperate in more than one territory. There are eighteen domestic/indigenous banks -- government-owned, private, and subsidiaries of foreign banks. Foreign banks that have entered sinceindependence have been required to establish capitalized local subsidiaries and are included in thecategory "indigenous." With the exception of one cross-border branching operation, theindigenous/domestic banks have restricted themselves to their home territories and most are singleunit banks.

While the domestic banks have expanded aggressively in recent years and now account forover 50% of bank assets, they are individually quite small, thus fractionalized as an industry. Thelargest have assets of US $150 million to $200 million equivalent; the smallest, under US$20million equivalent. The small size of these banks places them at a disadvantage relative to theforeign branch banks. Because of fixed cost requirements at start-up, a branch operation is lesscostly to establish and to operate than an independent bank of comparable size. Moreover,branches of large banks enjoy financial economies of scale (better diversification and betterliquidity) as well as reputational advantages. The branch banks are generally perceived as beingsafer, and this may allow them to attract deposits at lower rates.

Within the ECCB area the banking market is highly fragmented. Interest rates vary widelyand differ from US dollar rates. Liquidity varies both across territories and across institutions, andfunds do not flow freely from one territory or institution to another. (The reasons for thisfragmentation are discussed further below as well as in the associated payment systems report).The geographic fragmentation of the banking market exacerbates the scale problem andfractionalization of the domestic banks, since their potential growth is limited to an individualterritory.

There is some interbank lending, although its scope is limited. The ECCB brokers amarket for interbank loans. The rate is administered and the loans, which must be collateralized,are guaranteed by the ECCB. There is also a private market for unsecured interbank loans, theterms of which are negotiated bilaterally. The foreign branch banks manage their liquidity on asubregional basis, with one branch covering the reserve requirements of another. The branchbanks tend to favor the ECCB-brokered interbank market; while the domestic banks prefer theprivate market. Banks also manage liquidity by actively soliciting time deposits in lieu ofborrowings, from large commercial and institutional customers.

The domestic banks are well aware of these problems of fractionalization, scale, andfragmentation. The 11 larger domestic banks are currently discussing a joint initiative that mightencompass (i) a jointly-owned lending subsidiary that could diversify across territories and fundloans that were too large for individual banks; (ii) an expansion of the existing joint credit cardfacility to link ATMs and to support debit cards; (iii) an investment banking subsidiary; and (iv)the joint acquisition of problem institutions both inside and outside the OECS. Such initiativessupport the objectives of the ECCB's capital market development strategy, and reflect positivesteps in mnitigating the constraints of market fractionalization and fragmentation.

The safety of the branch banks is not a major issue: each is a very small branch of a verylarge, well-capitalized multinational institution. With respect to the domestic banks, detailedinformation on problems (or their absence) were not disclosed. However, the small size of eventhe larger domestic banks and their lack of diversification leave them quite vulnerable and theirsafety as mentioned earlier, may be a cause for concern. Some consolidation of the industry wouldgenerate economies of safety, scope, and operating cost, provided that the balance sheets of bankswishing to merge were sufficiently healthy at the outset.

Local banking markets are characterized by vigorous competition. Banks compete for timedeposits with one another, with non-bank financial institutions, and even with non-financialcompanies. Banks also compete aggressively with each other and with non-bank lenders inconsumer lending-mortgages and installment loans (especially automotive), although there isconsiderably less competition in business lending. Despite this competition, spreads betweenaverage loan rates and average deposit rates remain high by international standards. Possibleexplanations include the impact of reserve requirements on financial costs of relatively smallbanks; the substantial holdings of only medium-yielding assets such as government securities; andlack of profitable loan opportunities that often keep liquidity high (with correspondingly lowerasset yields insufficient to fully cover deposit rates and pro-rated operating costs).

Complaints have been heard that lending rates, especially on business loans, seemedrelatively insensitive to excess liquidity (that they were "inflexible downwards"). This

- 12 -

phenomenon is not special to the OECS: it is well known in other countries. It is a result ofbanks' market power with respect to their business borrowers (for informational reasons, thelatter cannot easily switch lenders), as well as the perception by banks that significantly largecushions of liquidity must be maintained to safeguard against potential market and credit risks.Thus, the holding of substantial lower yielding liquid assets must be balanced by higher yieldingloans to ensure coverage of banks' borrowing and operating costs. The phenomenon may besomewhat augmented in the OECS by the rigidity in some interest rates (e.g.: ECCB lending ratesand yields on government securities), which are administered rather than market-determined.

Recommendations

a. Financial Integration: Commercial banks are, and will remain, the backbone of thefinancial system. Consequently, the efficiency and safety of the banking system is of paramountconcern. Beyond reducing regulatory and other constraints that create financial fragmentation, anurgent priority is to reduce the fractionalization of the industry via the integration and/orconsolidation of banks. ECCB should encourage any initiatives on the part of the domestic banksin this direction. Moreover, where foreign banks provide promise of sub-regional integration, thearea governments should encourage acquisition of domestic banks by sound institutions, whetherthese be sub-regional, regional, or internationally based. The domestic banks are unhappy aboutrecent acquisitions in the area by a Trinidad-based bank. However, acquisitions by foreigninstitutions are not only desirable due to economies of scale and diversification, but also becausethey apply pressure on the domestic banks to integrate sub-regionally, reduce intra-islandfractionalization, and become more competitive.

To facilitate intra-OECS bank cooperation, additional development of a repo market ingovernment securities would greatly facilitate the expansion of interbank lending and thus theintegration of the banking system. Current options for interbank lending seem limited: the ECCB-brokered market may be considered too formal for banks wishing to avoid unnecessary visibility;the bilateral 'private' banking market being unsecured, is somewhat risky. Reliable sources ofshort-term funds (with low risk to the suppliers) would not only support sub-regional bankingintegration, but also increase the stock of liquidity needed to support a flexible capital marketinfrastructure. This is particularly relevant for the envisioned cross-border purchases of companysecurities, where banks serving as payors on behalf of investors (via their deposit accounts) mayneed to request banks in the territory of the share/security issues, to advance them funds foreffecting purchases in 'real-time', while interbank settlement arrangements are being executed.

In this respect, the recommendations raised in the payment systems study, would be of apriority to begin putting in place a state-of-the-art financial infrastructure. This is particularlyrelevant in the OECS/ECCB area context given the geographical land separation among theterritories. In addition, in terms of sequencing and establishing the necessary business conditions,it is highly recommended as a first step, that the sub-region's governments in conjunction with theECCB, assure an enabling environment for a single financial space. This would be achieved bylegislating uniform/one-time procedures for the simultaneous registration and licensing of banksacross the territories without needing individual country registration/licensing procedures,especially for banks wishing to expand across territories.

b. Reserve Requirements: Current reserve requirements are based on the stock of bothsavings and time deposits, and also are used as bank clearing accounts. While in percentage terms

- 13 -

they are not excessive, given the comparatively small size of some bank's assets, this couldmarginally impact on the spread between deposit and lending rates. To provide more flexibility,the averaging period on which the level of reserves are calculated, might be extended (e.g.: to 30days) thus allowing banks additional options in their management of funds. As also recommendedin the payments systems study, more efficient technology will serve to minimize settlement delaysand thus transactions and lending costs. Banks may also be at a disadvantage in the competitionfor time deposits from non-banks not subject to reserve requirements. Rather than reduce reserverequirements to resolve this, it is recommended that close monitoring of non-bank deposit-takingoperations be continued and that these be classified as banks. Where non-bank deposit taking is inthe form of commercial paper, these instruments would be covered under proposed capitalmarkets and securities regulations which will be required under the initiatives being proposed.

c. Capital Requirements: The current capital requirement is 8% of Tier 1 and Tier 2capital combined. Currently most banks more than fulfill this requirement by holding 8% of Tier 1capital, thus exceeding Basle standards. The Basle requirements were designed with much largerand better diversified banks in mind: the smaller the bank, the higher the capital ratio required toprovide the same degree of safety. The fact that many of the indigenous banks voluntarily exceedthe requirement suggests that they understand this (as do their depositors). ECCB also requiresbanks to hold capital equivalent to 5% of their deposits. These requirements do not apply toforeign branches of banks which are required to submit to ECCB a 'comfort letter' from theparent banks, guaranteeing the requisite capital backing for their OECS operations. As mentionedearlier, a priority issue does not pertain to useable capital but rather to banks' loan loss reserves.As a safety and prudential measure (and to mitigate against growth in the non-performingportfolio of the banking sector), ECCB should continue reinforcing this area of monitoring andwork with the area governments to assure full compliance with minimum provisions. This isparticularly important to assure the banking sector's solvency once the capital market (and thusthe opportunities for enterprise financing) begins expanding.

d. Equity Holdings: While current law restricts banks to hold no more than 10% of anindividual company's equity, it does not restrict the total amount of equity holdings (i.e.,diversified across companies) that a bank may hold as a percentage of its capital. Currently,however, OECS banks restrict their equity holdings, but with the development of the sub-region'scapital markets, banks are likely to participate as institutional investors and thus wish to increasesuch holdings to achieve capital growth. Holding of equity stakes by banks would support futurecapital market depth and allow banks to perform a role in corporate governance in the assessmentand disclosure of traded securities. However, due to the riskiness to the banking sector ofallowing it unlimited equity holdings, limitations on their asset portfolios (e.g. 15%-30% of totalearning assets), might be considered, as a prudential safeguard under an integrated banking andsecurities framework.

Since commercial banks have a well developed financial infrastructure to broker andpurchase or sell securities to individual investors not able to access a formal exchange, they mightalso serve to facilitate the trading function within an over-the-counter market. Given the proposedrestrictions on their own equity holdings, they would not function as typical 'investment banks'.Rather they would reflect a hybrid set-up combining the U.S.-style separation betweencommercial and investment banks, and the German/French style universal banks. They would beallowed a minimal equity stake in the market as well as brokering functions, but would primarilyfunction as commercial (lending) banks. The OECS/ECCB proposal also envisions utilizing

- 14 -

development banks as a nexus in each island, for investors to obtain information on securities andto trade them at those locations. While a role for development banks as information centers mightbe useful, there are some limitations in terms of operationalizing this approach, as discussedfurther below. These limitations pertain to the nature of development banks as non-deposit-takinginstitutions, given that deposit-taking would be a necessary function for capital market brokeragents to perform, in order to expedite payment and settlement procedures in an active securitiesmarket.

e. Government-Owned Financial Institutions: In the ECCB area, governments own orhave controlling interests in four commercial banks. In order to facilitate the availability of anattractive equity market, governments should privatize through public sale, their controllinginterests in banks, insurance companies, and other financial institutions that they now own. Somedevelopment banks or the high performing portions of their portfolios should also be consideredfor privatization and placing on a commercial basis (including perhaps merging with some of thenational commercial banks and sold as one package). Governments might also wish to considerthe privatization of the social security system (as discussed below). While conversion to acontribution defined system might also be considered under public sector management, the risksof this are potentially greater if such funds end up restricting a large portion of their investmentsto government fixed income securities. While privatization of national commercial banks is beingconsidered, management of public enterprise bank accounts held by such banks, should also besubject to competitive bidding by the rest of the private commercial banking sector.

f Offshore Banking and Other Issues: The OECS/ECCB area governments are keen ondeveloping and expanding the offshore banking business. There are three major configurationsavailable in developing this sector. These include the institutional and regulatory set-up ofoffshore accounts under of the following alternatives and/or their combinations: (i)Accounting/legal brass-plate banks / trust accounts, (ii) Deposit centers in OECS, holding foreigncurrencies only, and (iii) Domestic or branch banks managing offshore and domestic accounts. Inthe latter case, legislative/regulatory provisions and their strict enforcement are needed to fullysegregate domestic and offshore business as separate industries. This is also key in order to avoid' system leakages' which would open the door for money laundering activities. In addition,budding offshore banking markets in the OECS should be segregated from domestic bankingactivity to avoid 'cross-sector' flows which could undermine the stability and integrity of thebanking system.

The offshore banking industry typically does not provide services to residents in theterritories in which such operations are established. Nor does this industry use or invest fundsfrom the local market. As mentioned above, in the simplest form, the offshore industry isrepresented by 'paper' operations which generally consist of a local legal/accounting office whichbooks the offshore accounts. These offices generally take the legal form of trust or limited liabilitycompanies and do not conduct any business on the domestic market. The advantages to the clientsof these services, are tax benefits, and confidentiality. Invested instruments are generally from theexternal foreign market, as are the trading agents which execute these. More complexarrangements involve the above set-up but also include limited local operations. Examples ofthese are captive insurance companies which are proprietary in that they only service clients whichhave controlling interests. The most challenging to regulate, however, are those operations whichhave local banking, insurance, and other services, as well as offshore accounts.

- 15 -

Offshore financial centers can offer one or more combinations of the above. In order tocreate an attractive environment for these, governments usually set out the following regulatoryparameters: (i) legislation authorizing specific vehicles such as trust companies or certain financialinstitutions to conduct offshore business; (ii) low or no taxes on income or profits from suchoperations; (iii) tax treaties allowing further advantages under the counterpart country's taxregime (e.g.: exemption from withholding tax); (iv) low stamp duties, value added, or inheritancetaxes; (v) confidentiality via restrictions on public inspection of filing, and limited disclosurerequirements; (vi) exemptions for the offshore sector from exchange controls or limits; and (vii)simplified licensing and other administrative formalities. Prudential regulatory requirements andsupervision usually apply to those operations also offering traditional services to parties in thelocal market, and is concerned mainly with capital adequacy requirements.

The development impact of offshore operations can vary substantially. The 'paper'booking companies add little value in terms of employment, which is usually limited to clericalstaff and ancillary services such as computer and telecommunications suppliers. Foreign exchangeearnings to host governments depend mainly on volume since, due to high competition, annual'maintenance' fees charged by host governments tend to be low, as are taxes. The limitedincremental employment yields little additional tax revenue from local income taxes (whereapplicable). On the other hand, the tasks of the government are relatively straightforward andessentially are limited to adopting the proper legislation and assuring and effective registry foroffshore operations. Additional development impact is achieved when such operations also havelarger local operations, albeit restricted to offshore business transactions. Local employment isincreased and higher levels of skills transfers are achieved. Related services such as auditing,accounting, as well as housing, are also generated. Income taxes may apply both to localemployees as well as to the offshore businesses.

Additional levels of employment are attained when offshore banks also cater to domesticbanking and other services. These involve much larger volumes of operations with commensuratedirect and indirect revenues to the host government. Knowledge transfer is more significant andcan have positive impacts on the domestic financial industry. The complexity of such operations,however, also increases the complexity of the government's regulatory role. More involvedsupervision and licensing procedures are required, and measures are needed to prevent moneylaundering. In addition, predictable monetary and exchange policy is crucial, given the paralleloperation of two markets which need to be segregated. In general, under all of the offshorearrangements, the government is required to enforce the somewhat artificial barriers between thelocal market and offshore operations which deny access to local entities, and to prevent financialflows between the two segments even though in practice, 'leakage' inevitably occurs to someextent.

Development of the offshore sector should proceed in parallel with measures to strengthendetection of potential money laundering. The OECS governments have already signed on tointernational money laundering monitoring agreements, and the ECCB is assisting in theimplementation of reporting formats for both domestic and offshore banks, which should providemore detailed information to monitor or detect abnormal movements in funds through the bankingsystem. Multilateral institutions and bilateral donors might assist in setting up twinningagreements for ECCB with countries with related experiences. This could include early warningmechanisms and detection techniques (including the requisite monitoring technology & links with

- 16 -

foreign regulatory authorities) and preventive measures against blossoming of illicit fundschanneling via the OECS banking system.

Currently, OECS/ECCB area offshore banking laws differ by territory, and no attempt hasbeen made to make these consistent under a uniform regulatory framework. While this isunderstandable due to the competitive pressures by each island to provide offshore investors morefavorable terms than those of other ECCB area territories, this 'go-it-alone' approach worksagainst the uniform banking framework and sub-regional integration objectives. It isrecommended that for the establishment of offshore banking, ECCB work with the sub-region'sgovernments to set out consistent requirements for supervision, for separation of these accountsfrom the domestic banking system and for verification mechanisms. This is also crucial in order toavoid the inadvertent infiltration of illicit funds, which could severely damage the reputation of anemerging industry.

g. Payment Systems in the Banking Sector: As delineated more in detail in the paymentsystems study which was conducted as part of the financial sector review, modernization of thebanking infrastructure is fundamental to the success of the anticipated reforms in the ECCB areaas well as to resolve some of the issues of fragmentation and fractionalization of the industry. Todate, only one bank in the sub-region operates in each of the eight territories. Therefore, a largeproportion of payments both inter and intra-territorially are effected via correspondent banks.Clearing inter-island cheques can sometimes take up to two weeks, and unavoidable delaysgenerate credit and liquidity exposures among banks, thus augmenting the risks to the system. Theobjective should be to reduce the cheque system to a minimum and increase the use of inter-bankcredit transfer systems, particularly for large and time-critical payments. In order to fulfill theplans for a single financial space and the development of capital markets to promote saving andinvestment, the proposed securities markets for both government bonds and equities will requirethe support of an efficient area-wide payments system.

Some of the recommended actions, elaborated in more detail in the payment systemsreport, include (a) having commercial banks establish a jointly-owned debit card switch linking anetwork of point-of-sale terminals and ATMs across the sub-region; (b) having banks establish ajoint direct debit scheme for the payment of regular bills; (c) having the ECCB establish a real-time accounting system to process and provide final settlement for credit transfers between banksthroughout the day, and to handle all payments between ECCB and individual banks includingthose arising in the securities markets; (d) having the banks explore a joint arrangement forclearing and settlement of cheques drawn in US Dollars on banks in the US, as a means ofreducing costs and delays under the current arrangements; and (e) having ECCB consider grantingsettlement accounts to non-bank intermediaries in the securities markets, to ensure adequate andreliable delivery/payment procedures.

- 17-

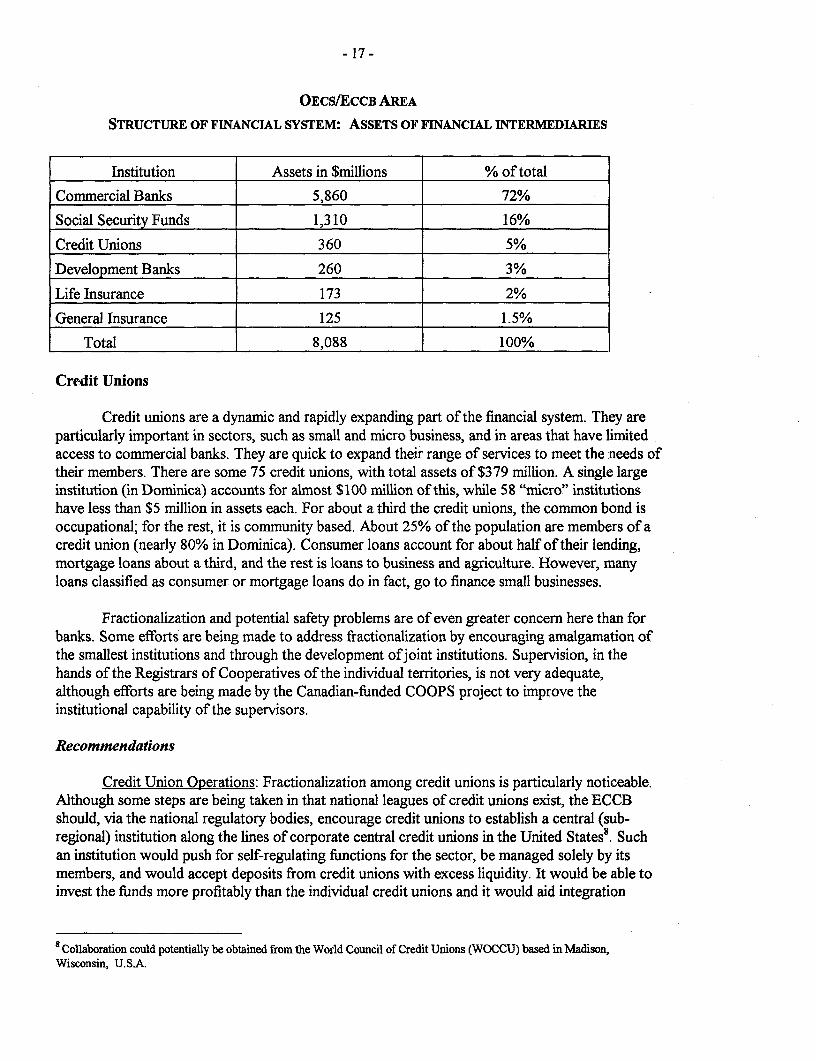

OECS/ECCB AREA

STRUCTURE OF FINANCIAL SYSTEM: ASSETS OF FINANCIAL INTERMEDIARIES

Institution Assets in $millions % of total

Commercial Banks 5,860 72%

Social Security Funds 1,310 16%

Credit Unions 360 5%

Development Banks 260 3%

Life Insurance 173 2%

General Insurance 125 1.5%

Total 8,088 100%

Credit Unions

Credit unions are a dynamic and rapidly expanding part of the financial system. They areparticularly important in sectors, such as small and micro business, and in areas that have limitedaccess to commercial banks. They are quick to expand their range of services to meet the needs oftheir members. There are some 75 credit unions, with total assets of $379 million. A single largeinstitution (in Dominica) accounts for almost $100 million of this, while 58 "micro" institutionshave less than $5 million in assets each. For about a third the credit unions, the common bond isoccupational; for the rest, it is community based. About 25% of the population are members of acredit union (nearly 80% in Dominica). Consumer loans account for about half of their lending,mortgage loans about a third, and the rest is loans to business and agriculture. However, manyloans classified as consumer or mortgage loans do in fact, go to finance small businesses.

Fractionalization and potential safety problems are of even greater concern here than forbanks. Some efforts are being made to address fractionalization by encouraging amalgamation ofthe smallest institutions and through the development ofjoint institutions. Supervision, in thehands of the Registrars of Cooperatives of the individual territories, is not very adequate,although efforts are being made by the Canadian-funded COOPS project to improve theinstitutional capability of the supervisors.

Recommendations

Credit Union Operations: Fractionalization among credit unions is particularly noticeable.Although some steps are being taken in that national leagues of credit unions exist, the ECCBshould, via the national regulatory bodies, encourage credit unions to establish a central (sub-regional) institution along the lines of corporate central credit unions in the United States'. Suchan institution would push for self-regulating functions for the sector, be managed solely by itsmembers, and would accept deposits from credit unions with excess liquidity. It would be able toinvest the funds more profitably than the individual credit unions and it would aid integration

sCollaboration could potentially be obtained from the World Council of Credit Unions (WOCCU) based in Madison,Wisconsin, U.S.A.

- 18 -

among credit unions and with the rest of the financial system. It would also provide individualcredit unions with a variety of financial services that fragmentation and scale fractionalizationprevent them from providing for themselves. These would, among others, include a central mutualaccount where members could deposit excess liquidity for the benefit of those with temporaryfunding shortages. Financial sector oversight and regulation of credit unions should becoordinated and consolidated in order to achieve supervision economies. The ECCB should assistin this effort while helping to strengthen the supervisory capacities of the area governments.

Development Banks

Seven of the territories have development banks with total assets of $284 million. Theseinstitutions, owned by governments, were traditionally a conduit for concessionary funds,channeled to them through the Caribbean Development Bank. As these funds have dried up, thedevelopment banks have turned increasingly to other sources of finance, including Social Securityfunds in a few cases. Their lending largely goes to finance projects of various kinds considered ofpriority by the government; these include housing finance, and various sectoral industry projects.About half their aggregate portfolios are in mortgage lending, both residential and commercial.

Given development banks' roles of funding priority sectors which have long gestationperiods before payback, risks can be high, and on occasion some OECS institutions of this typehave suffered from high non-performing loan rates. On balance, however, some of the majordevelopment banks in the OECS have performed satisfactorily, and loans to the housing sectorhave yielded reliable returns due to the basic incentives for borrowers to ensure repayment.ECCB's views on governance, management, funding, and regulation of development banks pointto areas which have resulted in positive restructuring of this sector in other countries. Forexample, despite the recent financial crisis, the East Asian experience shows that the followingfactors were critical for development banks to operate on a more commercialized basis andachieve solid institutions:

a. Using development banks as non-recourse/no-guarantee apex institutions for on-lending tocommercial banks at favorable terms for the development of new sectors;b. Regular and thorough external audits including periodic determinations of adequacy of thecapital base, strict limits on loan concentrations (both sectoral and client), potential equityerosion, and strict policies for full write-off of non-performing assets;c. High standards for professional management and technical staff (with competitive pay),and appointment of independent and majority apolitical Boards of Directors with heavyprivate sector representation;d. Financial accounting and lending policies including aging criteria for non-performingclassification, in-depth up-front credit analysis (and skilled staff for this purpose),conservative arrears ratios, and pro-active resource mobilization and fund raising policies.e. Linkage of loans to independent equity investments, and other financing parties,f. Observance of banking laws and prudential regulations commensurate with commercialbanking practices,g. Adequate funding against potential foreign exchange risks including forex stabilizationfunds and asset/liability currency matching to the extent possible,h. Implementation of fully modernized information systems for day-to-day loan accountmonitoring and supervision.

- 19 -

One development bank in the OECS seems to be moving in the direction ofcommercialization and possible privatization.

Recommendations

As mentioned earlier, government owned banks including development banks should, tothe extent possible, operate according to commercial standards, particularly for those projectswith rates of returns capable of repaying debt service. With respect to the proposed role ofdevelopment banks as a 'window agencies' for brokering securities of OECS/ECCB areacompanies (as part of capital market facilitation for investors), this should be carefully considered,particularly with regard to the implied operational aspects which might more optimally sharedwith the commercial banking sector. While a development bank might serve as a governmentsponsored nexus point at which to obtain over-the-counter data on securities available for trading,the function of actually transacting trades becomes more complex. In this respect, it should beconsidered that for the purchase and sale of securities, most investors, whether individual orinstitutional, will be more likely to use commercial banking services and engage in electronicaccount debiting in order to purchase securities more expeditiously. Such procedures will be evenmore invaluable as capital markets develop, and efficient real-time transactions are demanded toensure investor confidence.

If a development bank were to perform these functions, it would be required to opendeposit accounts (and thus be supervised under the Uniform Banking Act), which could lead togrowth in an area of business that they are not set up for (in terms of risk management of assetsand liabilities). While cash transactions could be possible, these proceeds would need to beeventually transmitted electronically to the recipient of the funds, which again would depend on acommercial banking communications network. Also, for safety reasons, the carrying of cash bycustomers would not be desirable, particularly if purchases of securities were of large volumes.Therefore, for the proposed function, it is recommended that at the outset, commercial banks bealso permitted to participate in brokering securities, to ensure transactional efficiencies andliquidity in the emerging capital market.

Regarding the restructuring of the OECS development banks, the ECCB has identifiedcertain criteria, particularly relating to governance, management, and regulatory aspects of suchinstitutions which would ensure their long-run sustainability. Regulation of such banks as part ofstandard banking sector supervision would formalize the prudential financial requirements ofdevelopment banks and assist in standardizing their information disclosure. Such practices wouldalso permit these banks to eventually become more independently funded (e.g.: via own bondissues), by attracting market investors relying on standardized disclosure reports which wouldprovide comparable information for making investment decisions. In this respect, the example ofthe Trinidadian Development Finance Limited bank (DFL) which issues its own bonds to funddevelopment projects, would be a an interesting successful model to examine in this context.

General Insurance

There are some 56 companies registered to transact general insurance business (roughlyone company per 2,000 households). A few are branches or subsidiaries of large foreign insurers.Some are government-sponsored or subsidiaries of government-owned financial institutions.

- 20 -

Some are subsidiaries of non-financial companies. Gross premiums were $108 million in 1992(2.5% of GDP). Assets were $125 million (mostly in the form of T-bills and time deposits).

The bulk of the business is for real and related property with linked catastrophe coverages(including fire and natural hazard perils) under comprehensive home and commercial policies --motor vehicles also constitute a significant share of the business. Typically, up to 85% of the riskis reinsured internationally. Local companies earn large commissions on reinsurance premiums.The sharp rise in these premiums in recent years has greatly increased commission income and sothe profitability of the local insurers. Rather than this leading to competition to drive down rates,it has instead led to the entry of ever smaller insurers and agents which many times do not addproductive value to the industry. The cost of catastrophe coverage is further inflated by a varietyof taxes and impositions. There is a tax on premiums, a withholding tax on reinsurance premiums,required statutory deposits bearing no interest, and purchases of government securities at belowmarket rates. This policy seems to distort industry incentives and diminish the potential role ofinsurance companies in providing much needed capital to the financial system. Governmentsshould seriously consider reducing taxes on this industry. Surely, there is a powerful publicinterest in encouraging people to insure.

The proliferation of small insurers is cause for concern regarding efficiency(fractionalization and economies of scale), but even more regarding safety. Are these smallcompanies sufficiently capitalized for the 15% of the risk that they retain? Are they sufficientlycareful in choosing reinsurers that can be relied upon to pay up their 85% share? Regulation inthis sector needs to be substantially strengthened, and specialists with underwriting and actuarialskills deployed for the supervision function. Since regulation is in the hands of the individualterritories, there are some diseconornies due to the lack of institutional, technical, andtechnological resources to effectively monitor and supervise.

Recommendations

a. Financial Reserves: Companies and households should be encouraged to establishfinancial reserves to supplement insurance or to cover losses that are uninsurable (such asinterruption of business). A possible idea is to establish tax-free savings accounts that could bedrawn upon only for casualty losses (the tax-free status of course would matter for householdsonly in those territories having a personal income tax). Financial reserves might also provide asolution to the problem of the notorious "2% deductible". Policyholders could be offered a specialcontractual savings vehicle, enabling them to put aside a certain amount each month until theyaccumulated an amount equal to the deductible. A credit line could be associated with thisaccount so that they could "overdraw" if a loss occurred before they had accumulated the fullamount. Such a solution would be less expensive for policyholders than reducing the deductible(information was received that reducing the deductible to 1% raises the premium by 15-25%).

Governments, too, might consider establishing reserve funds that they could draw uponfor infrastructure repairs. Of course, with a well-developed government securities market and areduced reliance on external debt, they would also be able to borrow more easily for this purpose,as needed. The Government of St. Kitts allows insurance companies to accumulate a "catastropheclaims equalization reserve". Each year they may set aside 20% of premiums before tax until theyhave built a fund equal to 100% of premiums. This is an excellent idea and should be extended toall territories. An added benefit of these various financial reserves, from the point of view of

- 21 -

capital market development, is that they would increase the volume of contractual savingsvehicles in the area.