April 1, 2009 Document of the World Bank Report No. 44744-TN Republic of Tunisia Water and Sanitation Strategy Sustainable Development Department Middle East and North Africa Region Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript

April 1, 2009

Document of the World Bank

Report N

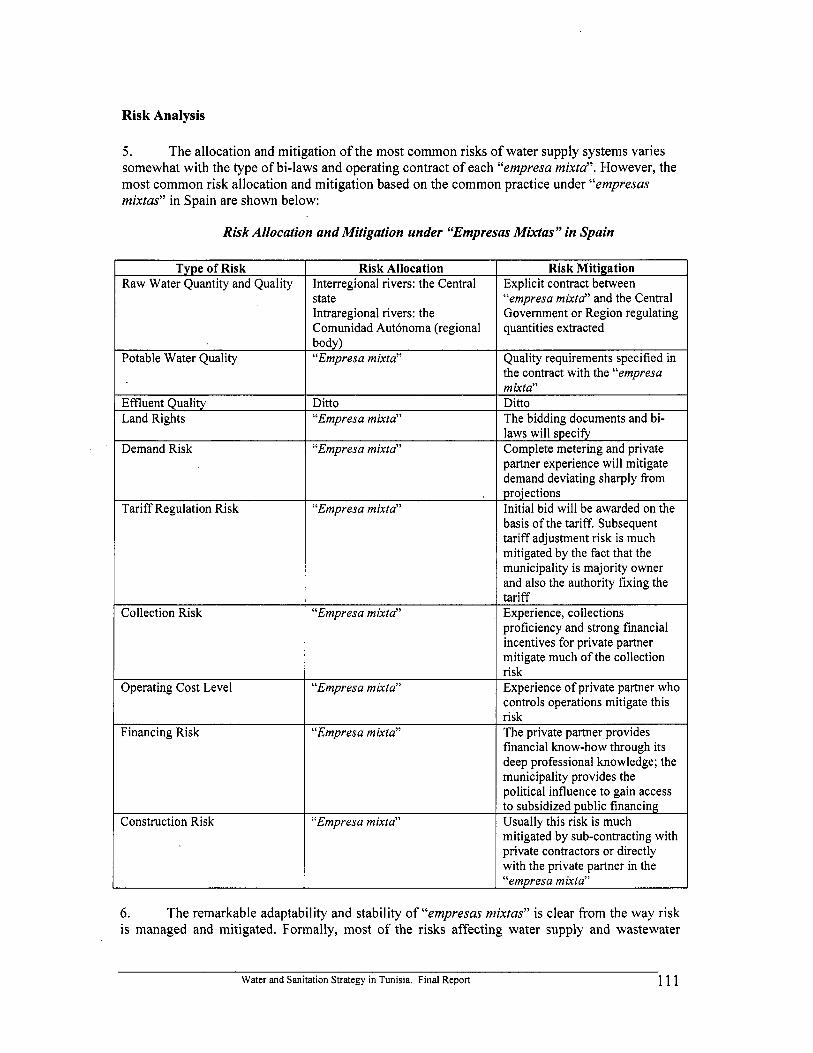

o. 44744-TN

Republic of Tunisia

Water and Sanitation Strategy

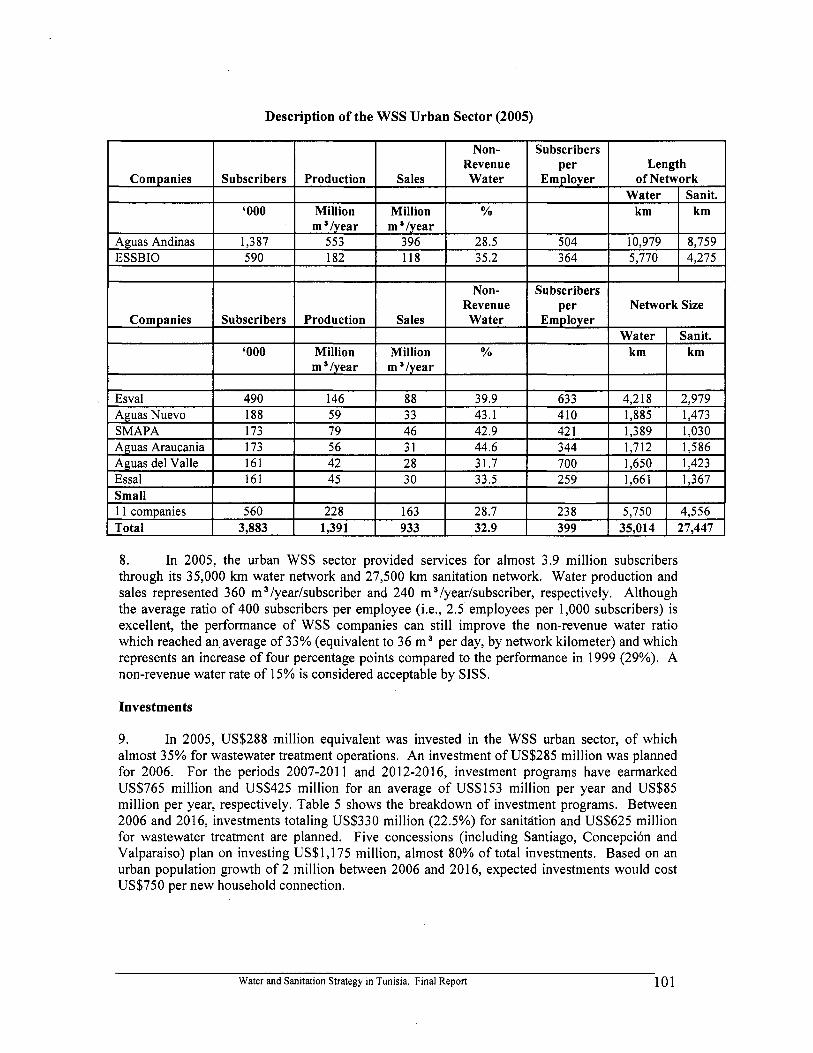

Report No. 44744-TN

Republic of TunisiaWater and Sanitation Strategy

Sustainable Development DepartmentMiddle East and North Africa Region

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

TABLE OF CONTENTS

Executive Summary

I1 Tunisia‘s water resources and allocation principles ......................................................... 12 I11 Water sector achievements and success factors ................................................................ 14

I Preamble ............................................................................................................................... 12

Drinking water and sanitation performance: Main indicators ....................................... 15 Impacts on the population.. ............................................................................................ 16

A specific system for rural areas ........................................................................................... 19 Economic factors: the role o f sustained growth ............................................................ 20

commercial nature supported by the state ............................................................................. 22 Relationships with donors ..................................................................................................... 22 Relationships with customers ................................................................................................ 23

The sector operators ....................................................................................................... 24 Internalization o f Tunisia’s national vision and objectives ................................................... 24 Capacity Building .................................................................................................................. 24 Beneficiaries’ involvement in management activities in rural areas ..................................... 26

111.1 111.2

IV . 1 I V Institutional and economic factors o f success ................................................................... 16

A centralized and de-centralized system for urban areas ...................................................... 18

IV.3 V

Urban and rural systems managed by public institutions o f industrial and

V.2

V I Current system limits and emergent deficiencies ............................................................. 27 Various services limits and emergent deficiencies ........................................................ 27

Limits and deficiencies in urban drinking water supply ........................................................ 27 Limits and deficiencies with regard to rural drinking water supply ...................................... 31 Limits and deficiencies in urban sanitation ........................................................................... 32 Limits and deficiencies in rural sanitation .............................................................................. 40

Common limits and deficiencies ................................................................................... 41 Synergy between various drinking water supply operators and sanitation ........................... 41 Cost recovery and tar i f fs in urban areas ............................................................................... -42 Cost recovery & tar i f fs in rural areas (AIC/GIC/GDA) ....................................................... -48 Regulation. autonomy and operators performance incentives ............................................... 50

Limited participation o f the private sector ........................................................................... -51 Strengthening customer relationships ................................................................................... -53

VI1 Sector challenges and the need for reform ........................................................................ 53 Challenges for the drinking water sector (managed by SONEDE) ........................................... 53 VI1 . 1 Challenges for the sanitation sector (managed by ONAS) ............................................ 54 VII.2 Drinking water and sanitation challenges in rural areas ................................................ 57 VII.3 The need for reforms ..................................................................................................... 58

VI11 Options for institutional reform for urban drinking water and sanitation ................... 59 VI11 . 1 Regional water and sanitation companies with a national company for production and supply ............................................................................................................... 59

V I . 1

VI.2

Constraints and limits in SONEDE and ONAS management autonomy .............................. 50

VIII.2 Merging SONEDE and the ONAS i s possible and makes more sense than regrouping electricity and gas in the same company ................................................................. 60 VIII.3 Maintaining the two enterprises but with more thorough decentralization, improved management efficiency and increased private sector participation ........................... 61 VIII.4 The concession .............................................................................................................. 63 VIII.5 Water and sanitation holding company ......................................................................... 64

I X Common reforms to all options for urban drinking water ............................................. 65 and sanitation ............................................................................................................................... 65

Creation o f a regulatory entity ....................................................................................... 65

Common reform actions to all institutional options ..................................................... -71 Common actions to drinking water and sanitation ................................................................ 71 Actions specific to drinking water (managed by SONEDE) ................................................. 72 Actions specific to urban sanitatlon ....................................................................................... 72 Need for reform in rural areas drinking water and sanitation ....................................... 73

Institutional aspects for rural drinking water ................................................................. 73

X I Financing: possible reforms ................................................................................................ 75 XI1 Conclusions and recommendations .................................................................................... 78

X . 1 X.2 Institutional aspects o f rural sanitation. ........................................................................ -75

TABLES

3 Table 1 : Water resource allocation (million m ) ........................................................................... 13 Table 2: Water Supply vs . Demand (million m ) ......................................................................... 13

Table 4: Investments in the water and sanitation sector (1 992-2005) ........................................... 21 Table 5: Connection to sanitation indicators ................................................................................. 33 Table 6: Used water purification .................................................................................................. -34 Table 7: Average quality o f the water treated in water treatment stations .................................... 35 Table 8: ONAS staff in 2006 ......................................................................................................... 38

3

Table 3 : Water resources allocation (%) ....................................................................................... 14

GRAPHS

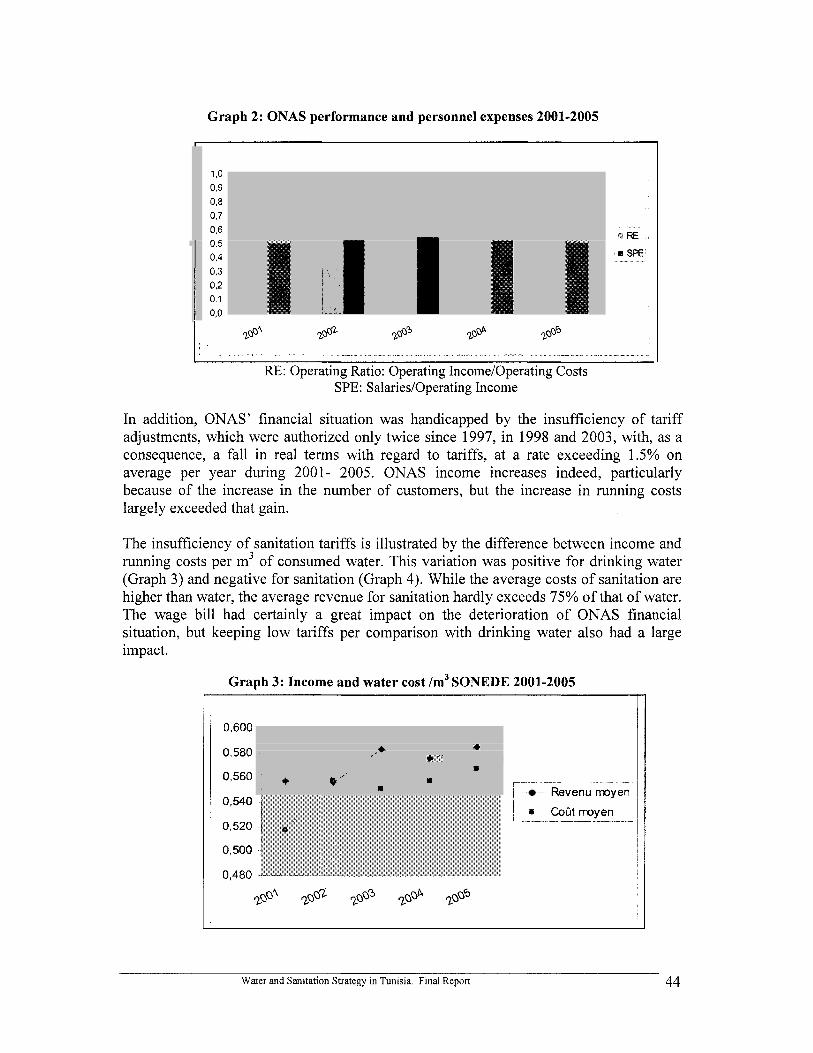

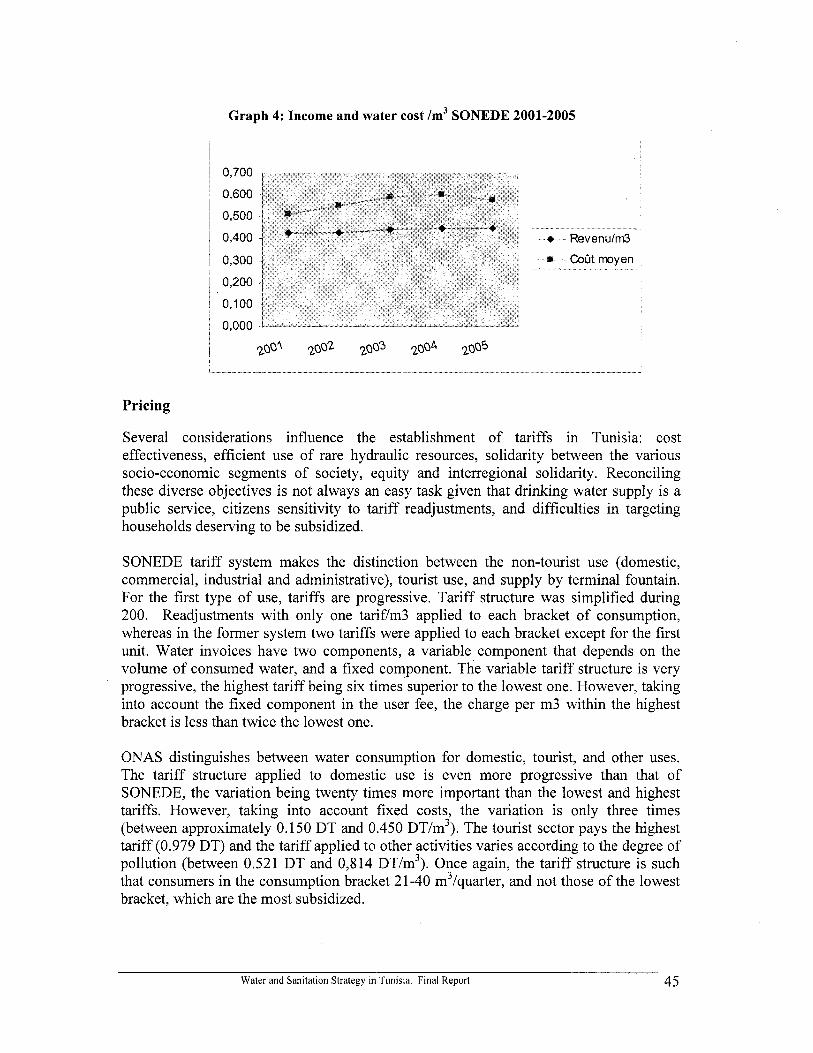

Graph 1 : SONEDE performance and personnel expenses (2001 -2005) ...................................... -43 Graph 2: ONAS performance and personnel expenses 200 1-2005 ............................................... 44 Graph 3: Income and water cost /m3 SONEDE 2001 -2005 ........................................................... 44 Graph 4: Income and water cost /m SONEDE 2001-2005 .......................................................... 45 3

Water and Sanitation Strategy in Tunisia . Final Report

Acknowledgements

This report was prepared by a team led by Mohammed Benouahi (Lead Water Supply and Sanitation Specialist). Major authors to the report were Mohamed Larbi Khrouf (Consultant, Water and Sanitation Engineer), Mohammed Lahouel (Consultant, Economist), Ameur Horchani (Consultant, Water Resource) and Klas Ringskog (Consultant, Institutional Specialist). Vijay Jagannathan (Sector Manager), Julia Bucknall (Lead Water Resources Specialist), and Claire Kfouri (Water and Sanitation Specialist) also provided input to the report. Administrative support was provided by Zakia Chummun and Angeline Mani.

A draft o f this report was formally reviewed in Tunis on April 3, 2007 and in Washington D.C. on October 17, 2007, chaired by Ms. Cecile Fruman (Acting Country Director). The peer reviewers were: Alex Kremer (Senior Sector Economist), Nabil Chaherli (Senior Sector Economist), Ndiame Diop (Senior Economist) and Philippe Huc (Senior Water and Sanitation Specialist).

Republic of Tunisia

Strategy for Water Supply and Sanitation in Tunisia

Executive Summary

1. At the request o f the Tunisian Government, the World Bank mobilized a team o f multidisciplinary specialists to prepare a strategy for the water supply and sanitation sector in Tunisia.

2. This strategy i s a comprehensive overview o f the institutional, organizational and economic aspects o f the sector. Based on an analysis o f the current situation, this strategy wi l l examine the strengths and weaknesses o f the sector and review reform options o f reform that address upcoming challenges and provide the highest level o f service at the lowest possible cost for urban and rural beneficiaries, while guaranteeing the widest and most sustainable service coverage.

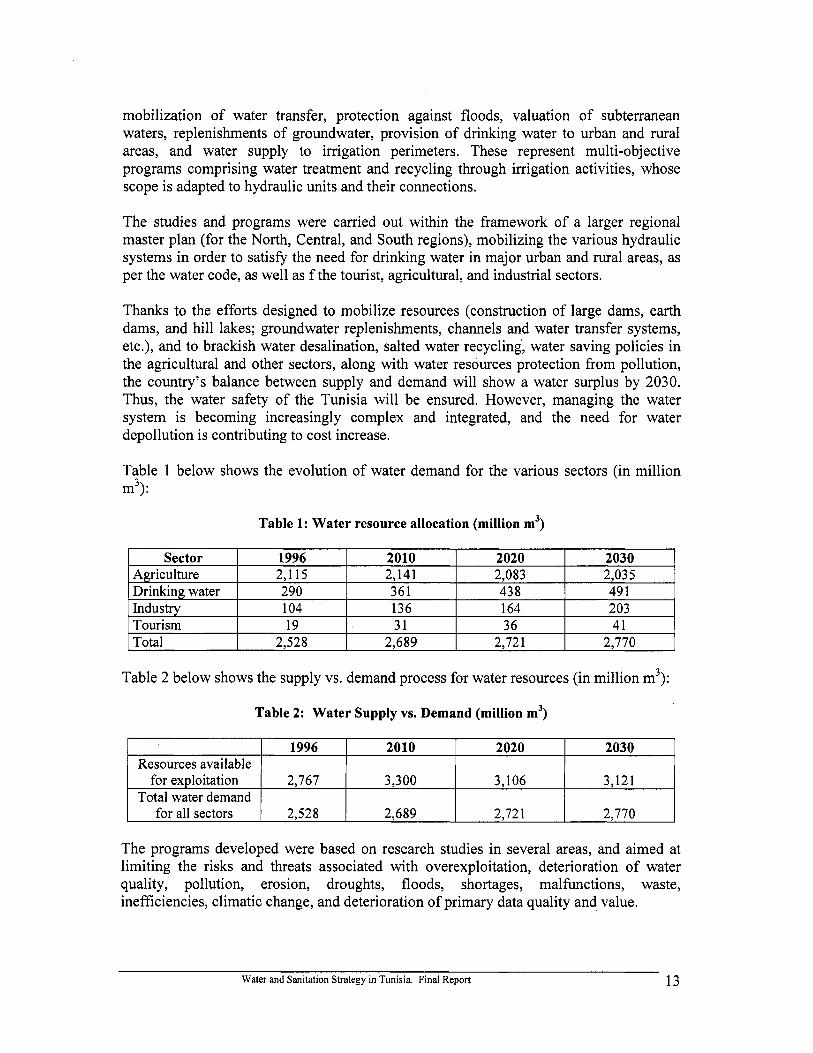

3. Tunisia i s a Mediterranean country with limited water resources o f 4,860 million m3/year o f which 610 million m3are rarely renewable, 1,550 million m3/year are renewable and 2,100 million m3/year are surface water flowing into rivers that can be mobilized at a rate o f up to 95%. The Water Code governs water resource allocations and gives priority to fulfil l ing the demand for potable water in the urban and rural sectors, with secondary attention given to the requirements o f the industrial, tourist trade and agricultural sectors. The projected water balance between available resources and demand between different sectors shows a slight increase by the year 2030, provided that: (a) water resource mobilization efforts are maintained; (b) desalination o f brackish water and recycling o f salt water are pursued; (c) water savings policies are implemented in agriculture and other sectors; and (d) water pollution control measures are supported. Agriculture uses the majority o f the water resource base, although the potable water share o f these resources will slightly increase from 13.4% in 2010 to 17.7% by 2030. The industry and tourist sectors are expected to maintain limited usage o f water resources.

4. Even if the anticipated water balance between available resources and demand remains positive by 2030, the margin will s t i l l represent an incentive for improved management efficiency o f water resources across all sectors.

5. conclusions:

The diagnosis and evolution o f the water sector have lead to he following

6. sanitation with highly positive impacts on the quality o f l i f e and economic development.

The sector has achieved remarkable results in the areas o f water supply and

7. The continued improvements o f water and sanitation services have always been priority areas in the national economic and social development plans. Sector leaders,

Water and Sanitation Strategy in Tunisia. Final Report 1

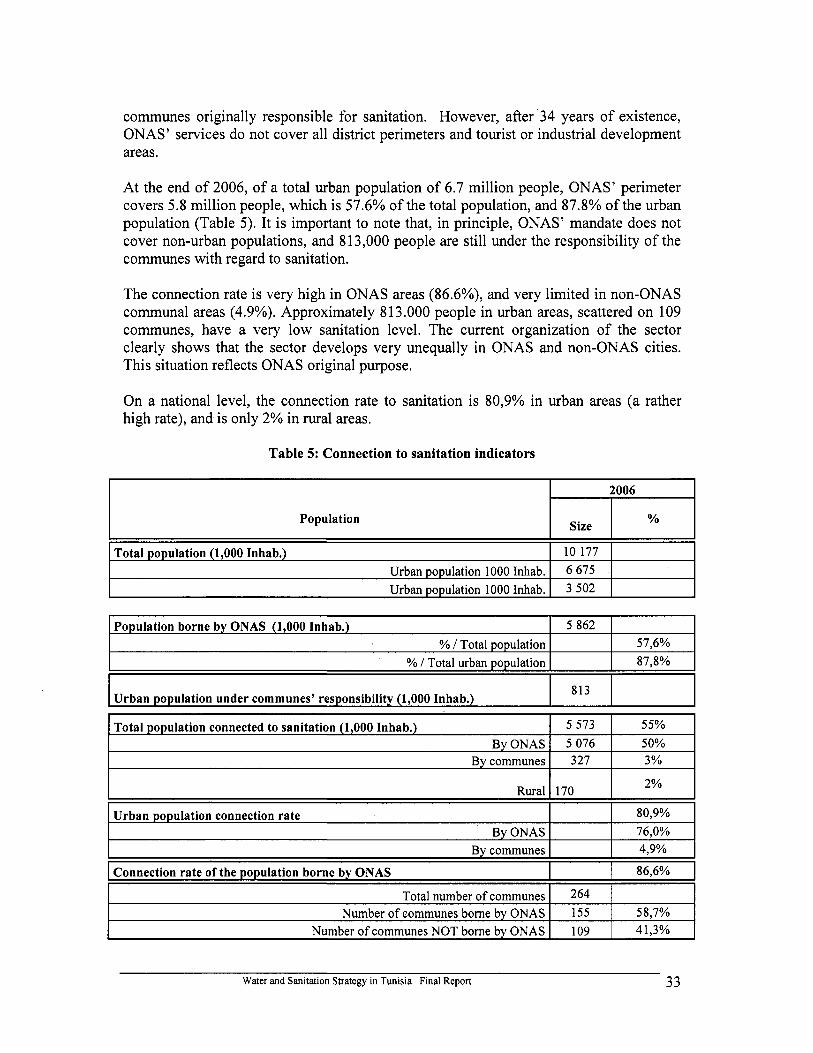

more importantly SONEDE and ONAS , have addressed these priorities with very satisfactory results. Access to potable water has become permanent throughout the country, including in marginal areas, and a large percentage o f the population now has access to sanitation services. Currently, the entire urban population has access to potable water and over 90% o f the rural population is supplied through SONEDE and other associations (GIC/GDA). Moreover, 80% o f the urban population now has access to sanitation services. This achievement i s even more remarkable given that water resources are limited, the climate i s arid, the ecosystems are fragile, and the required financial investments are high.

8. (a) a marked improvement in quality o f l i fe and economic development; and (b) improved health as shown by a net decrease in the occurrences o f diarrhea among children. Potable water service delivery has also had a positive impact on integrated development, and the urbanization o f rural areas has strengthened the community spirit and stimulated the development o f small operation and maintenance facilities.

This performance has provided notable advantages, such as:

9. The sector’s strong performance is due to the vision and experience o f the operators, to the institutional framework which has been implemented, and to the sustained growth o f the Tunisian economy over the past several decades.

10. The sector has made advances on the basis o f national Development Plan in coordination with the national strategy for water resource development. The operators and the General Directorate o f Rural Works and Water Resources (DGGREE) have identified regional water demands and have encouraged the development o f long-and medium-term measures to ensure a clear vision o f the sector’s future. Through the establishment o f successive five-year plans, the DGGREE and operators has also improved the targeting o f quantifiable objectives, water resource mobilization and investment optimization.

1 1. The Operators have gained technical experience by merging proven technologies, while adapting these to country specifics (i.e., handling iron in rural areas, adapting water treatment techniques in desalination plants, pipeline corrosion control, odor control in treatment plants and ventilation in activation basins).

12. The existing institutional framework has facilitated sector development, although it encourages urban water supply and sanitation monopolies at the national level. The lack o f adequate water service delivery and specialized sk i l ls 1960 to 1970 was remedied by the training o f competent operators on a national scale. Moreover, SONEDE and ONAS were created as industrial and commercial entities governed by legislation tailored to their respective mandates. The main actors also participate in these organizations’ board o f directors. Oversight is carried out by the responsible ministry, as well as by other specialized ministries, i.e., the Prime Minister’s office, the Ministry o f Finance, the Procurement Commission, the Accounting Commission (Cow des Comptes), etc. This oversight exerts strict control over operators, ensuring the required financial and administrative discipline.

Water and Sanitation Strategy in Tunisia. Final Report 2

13. As regards the populations o f remote rural areas or those without SONEDE assistance, a participative approach was developed through the creation o f Collective Interest Groups (AICs) which have today become Agricultural Development Groups (GDAs). This type o f success in a complex sector that includes numerous projects throughout the country, at times in remote and rugged areas, i s due to the strategy adopted by DGGREE. Their strategy was thus able to harmonize and synchronize activities among different actors, Le., consulting firms to develop studies, entrepreneurs to handle works, and IACs/GICs/GDAs for water production.

14. The Tunisian economy’s strong growth during the past four decades, at over 5% per annum, enabled the government to mobilize substantial internal and external resources to finance sector investments. The increase in public revenue parallel to this growth was also instrumental in ensuring sustainable project funding. Moreover, this economic growth greatly stimulated household incomes, thus access to water supply and sanitation services.

15. In addition to improving economic growth and improvement in the quality o f life, relatively l o w cost, service delivery to low cost for low-income households has helped increase overall ’service delivery to the majority o f the population. The implementation o f an efficient cost recovery system has also played an important role in sector development by providing a large portion o f required financial resources. Thus, a relatively high cost recovery for expenditures demonstrates the overall efficiency o f the water sector.

Emerging Issues and Future Challenges

16. SONEDE and ONAS have increased their operations through the development nationwide o f activities throughout the country. Their staff complements are very high, perhaps overly so compared to the amount o f works and relative to international criteria for good performance.

17. The implementation o f investment projects and modernization o f management systems are progressing at a relatively slow pace for several reasons, directly related - but not always - t o the operators.

18. The issue o f infrastructure rehabilitation and upgrading i s becoming problematic for the sector. Financial constraints are impeding the rate o f infrastructure upgrades. Also at risk i s the quality o f service provided, especially for the sanitation sector.

19. SONEDE i s not benefitting from increased revenues from the implementation o f important investments in sustainable potable water supply, i.e., as regards quality improvement, which could increase i t s expenditures and jeopardize i t s financial viability. Also, the development o f water resources and transfers, including desalination facilities in the south o f the country, will be more costly in future, especially without clear policies on optimized cost recovery. The transfer o f potable water and sanitation services to SONEDE and ONAS could also undermine these institutions’ financial situation.

Water and Sanitation Strategy in Tunisia. Final Report 3

20. Cost recovery issues are crucial for ONAS whose production deficit has lasted for the past several years and whose investments are almost exclusively financed by the government. Subsequent reductions in expenditure were implemented to forestall these financial constraints, but the quality o f sanitation services was negatively affected.

2 1. Tariff adjustment uncertainties preclude operators from preparing reliable financial projections and undermine planning for current investment expenditures.

22. since collaboration and pooling o f funds could help to reduce costs.

A lack o f synergy between these two activities i s an important issue, especially

23, For the potable water sector, the major challenges include:

Increasing costs o f water resources due to longer transfer periods; The introduction o f desalination facilities to increase the volume of water resources and improve water quality; Ensuring the sustainability o f water supply, especially for large urban areas; Management of extreme climate variations, especially drought; Water supply for rural and peri-urban areas; Demand o f an increasingly well-informed population for water quality Over-staffing issues need to be addressed as well as management o f human resources; Demand management; Modernization o f institution management (SONEDE); Lower cost service provision at a lower cost; Tariffs, cost recovery and associated regulations; Upgrading/rehabilitation and expansion o f existing infrastructure; Future sector financing; Autonomy and management tools; Delays in project implementation periods; and Compensation for implementation delays for new information technology methods (NTIC) and new management tools.

24. For the sanitation sector, the major challenges include:

Expanding the service delivery area to small towns where costs are higher than revenues; Rehabilitation and expansion o f sanitation infrastructure, e.g., wastewater treatment plants and pumping stations; Over-staffing issues; Delays in project implementation, hindering closer project phasing which would ensure better use o f financial resources; Modernization o f facility management (ONAS); Tariff/cost recovery and their oversight; Service delivery at a lower cost;

Water and Sanitation Strategy in Tunisia. Final Report 4

Compensation for delays in implementation o f new information technology methods (NTIC) and new management tools; Rural sanitation institutional issues; Industrial pollution in water treatment plants (STEP) hindering their operations; Quality demands from a better informed population (regarding odors, mosquitoes, and spillage); Management o f extreme climate variations, especially floods; Increasing the rate o f treated waste water reuse to avoid costly spillage; Protection o f economically viable activities, i.e., tourism area preservation; Identification o f technical solutions to avoid waste water treatment waste (i.e., sludge, gases, etc.); Wider scope o f sanitation infrastructure to areas lacking services and follow- up o f urban development; National subsidies and solidarity, and subsidy targeting; and Future sector financing.

25. The major challenges in rural areas, are:

Potable Water Supply

Limited level o f financial resources for AICs/GICs/GDAs; . Weak management o f AICs/IGCs/GDAs;

Service provision should be in line with SONEDE standards;

Water distribution methods not in line with beneficiary expectations; and Potable water supply in rural areas i s a burden for SONEDE.

Sanitation

Financial constraints in water production and collective installation

Individual household connections will create hygiene problems; Institutional weakness o f rural water sanitation services;

maintenance; and Identification and adoption o f technical solutions for the rural areas.

26. These challenges require global reforms to promote the efficiency o f the potable water supply and sanitation sectors. The strategy addresses possible reforms, showing the advantages and disadvantages o f each scenario. The strategy also presents the option o f developing a regulatory framework for the potable water supply and sanitations sectors.

27. The objectives o f these reforms are as follows:

Create a forward-looking development framework focusing on an overall sector strategy;

Water and Sanitation Strategy in Tunisia. Final Report 5

28.

29.

Ensure better coordination between potable water and sanitation sectors; Develop a beneficial synergy between the two activities; Create incentives for private sector participation, combining potable water and sanitation; Establish transparent relations between government and operators through delegation o f responsibility to the relevant entities; Develop an incentive program based on good performance and a more modern management system; and Provide sustainable resources, taking into consideration the interests o f marginalized social groups.

The institutional options for the urban sector are as follows:

Creation o f regional water and sanitation entities linked to a national

Maintaining both entities with better decentralization, more efficient

Creation o f concessions;

organization for water production and supply and treatment Merging o f SONEDE and SONAS;

management, and increased private sector participation;

Creation o f a national water and sanitation holding company; and Multi-sectoral integration o f potable water, sanitation, electricity and gas.

Since SONEDE and ONAS activities are primarily concentrated in the southern part o f the country, the option o f regional water and sanitation entities would entail the creation o f one o f the largest organization serving the Tunis region, medium-sized entities for the regions o f Sousse and Sfax, and smaller entities for the other areas. Aside from the Tunis area, the viability o f this new structure would require substantial tar i f f increases in other regions which would be contradictory to the objective o f national solidarity. Moreover, regional entities would be more likely to experience social pressures. However, this option would entail additional expenditures for the creation o f these new entities and would deprive the country o f knowledge sharing on regional endeavors. Moreover, the sector would require staff with a high level o f competency, which i s not currently available, nor would these skills be used efficiently in view o f some regional activities. However, this option may be better suited to the development o f concessions. International experience has shown that proposals made by private companies to oversee these services are o f a higher caliber if water and sanitation are jo int ly managed.

30. The other option would be to merge the two national entities, SONEDE and ONAS, however, this scenario i s not recommended due to the large number o f staff concerned, currently 12,000 persons. The merge could also create social and management problems because o f status issues between the two institutions. Also, the only way to improve efficiency and reduce costs would be through reorganization and reduction in staffing costs, which would greatly reducing staff complements. This would be dif f icult under the current conditions.

Water and Sanitation Strategy in Tunisia. Final Report 6

31. Long-term concessions to private companies for water supply and sanitation services would not be the best solution for Tunisia since the two public enterprises are currently operating efficiently. This management system would better suit a country where public services are not performing satisfactorily. Moreover, this type o f concession could imply higher tariffs for water supply and sanitation since the private sector would be unable to mobilize the required financial resources at a better rate than SONEDE and ONAS. In fact, the private sector would not be able to benefit from increased revenue through a lower rate o f technical and commercial losses since the latter are weak compared to international standards.

32. The option o f maintaining the existing two-entity structure would require greater decentralization and implementation o f reforms for better efficiency in order to facilitate decision-making and improve service delivery to users. This option would also need a modern administrative and technical management system, as wel l as a sound analytical accounting system employed as a management tool. The creation o f a dual ONAS- SONEDE entity would provide the opportunity to explore possible synergies between water and sanitation and for them to coordinate their policies accordingly.

33. The holding company scenario would have the advantage o f providing better coordination between water and sanitation services by developing their jo int synergies. I t would also provide a strong tar i f f pol icy beneficial to the two entities, as wel l as to beneficiaries. The current scenario would also stimulate the development o f strategic options for services, particularly by encouraging new technologies, private sector development, optimization o f financial conditions, provide required services for mega- project development, and support technical and financial planning. Finally, the holding would require a simplified and coherent structure and l imited expenditures.

34. In many countries, power and gas distribution i s managed by the potable water and sanitation provider. This multi-sectoral approach could be useful as a means to developing trade synergies, i.e., as regards client relations as wel l as technical interventions in the field. The dual responsibility o f this joint sector approach could also be appealing to the private sector.

35. In addition to institutional restructuring, the two existing entities would need to develop decentralization measures and implement certain reforms to ensure better overall efficiency. Moreover, efficient decentralization would require the delegation o f certain responsibilities to facilitate decision-making and improve service delivery for users. Priority actions can be summarized as follows:

Lower Staffing Costs. Assistance would be required to align the number o f staff with ongoing activities. A satisfactory solution would need to be identified by negotiations with both parties. Private Sector Participation in Activities of Both Entities. This action could be taken in conjunction with staff reductions, and would be an incentive for private sector participation.

Water and Sanitation Strategy in Tunisia. Final Report 7

Modernization of Facilities Management, N e w information and communication technologies (NTIC) would need to be incorporated into the management systems o f both entities to ensure modernization and upgrading.

Institutional Elements o f the Rural Areas

36. I t i s recommended that the current participatory approach and management of potable water systems by GDAs be maintained. However, i t would be beneficial to consolidate these elements and to modify their collective distribution system into an individual scheme. The participatory approach remains fragile and would require government assistance. Appropriate measures would be required such as tari f f modifications, production subsidies for potable water supply similar to those in place for investments, etc. Remote and sparsely populated areas would continue to be supplied through individual connections (individual water sources, water tanks, etc.).

37. Rural sanitation services should not be managed by ONAS since this would deplete i t s financial resources. I t would be more advisable to implement a specific financial and institutional system based on rural potable water services. The approach o f a “Strategic Sector Study o f Sanitation Services in Rural Areas” would be more realistic, even though upgrading and detailed studies would be required. This study would allocate tasks among GDAs, DGGREE and ONAS. I t would be useful to further develop this scheme and implement it on a pi lot basis. The technical findings o f pi lot schemes have recently been applied, whereas institutional applications have not been implemented.

Development of Regulatory Statutes as a Priority

3 8. Sector regulations are currently implemented at different levels o f oversight. Staff recruitment and new positions are handled by the government and are based on the needs o f both operators. Expenses are submitted to the Internal Procurement Commission for specific amounts; expenses in excess o f the threshold are reviewed by the Superior Procurement Commission. Water and sanitation services must also be in line with national health and environmental standards. Water tar i f fs are established by the government fol lowing a review o f cost and tar i f f adjustment requests f rom operators. Following the amendment o f legislation on contractual agreements, partnership activities with the private sector are controlled through contracts signed by the public operator and his private partner. Finally, performance monitoring is carried out under five-year program contracts which outline the objectives o f water service delivery, production, and other service quality indicators.

39. This regulatory arrangement has facilitated sector development through the allocation o f additional responsibilities for operators in control o f national monopolies. However, these regulations have reached the limits o f political and administrative standards inherent to important decision-making. However, quality and service demands are very high and thus more expensive and a new institutional framework will need to be developed to ensure coherence between these requirements and cost recovery. The creation o f a legal regulatory system could resolve the information imbalance between

Water and Sanitation Strategy in Tunisia. Final Report 8

government and operators and the new institutional and independent framework would also ensure better performance monitoring o f operators. Transparent terms o f reference will be prepared to alleviate sector bottlenecks and giving operators a better vision o f the methodology needed to achieve government’s goals. Indeed, the creation o f a regulatory body would improve the current disconnect between the legal authorities and the entities regarding tariffs for water and sanitation services. Both entities have expressed concerns regarding the lack o f tar i f f adjustments needed to ensure their level o f operation, often over several years (such as the case o f ONAS) and the Government also believes that management systems for entities could be improved and that costs could be reduced.

40. A legal Regulatory Commission would ensure a better balance between the demand o f quality services and cost recovery, and facilitate decision-making on tariff and subsidy levels. This Commission would also establish regulations for tariffs, monitor the quality o f service, and create more transparent relations between operators and government on the basis o f objective data and regular monitoring. Additionally, the Commission would have the authority to oversee the power sector, and eventually the transport sector, although its role would not be identical to a structure managed by the private sector. The proposed Commission will have no decision-making power over tariffs and subsidies, which will remain under government oversight. I t s role would solely be to provide objective information to government on the entities’ management efficiency and on their required funding to achieve government goals. The Commission will be independent and will incite more transparency in data provided. It will be staffed by qualified individuals and will control performance indicators. Since it will have no decision-making authority to set tariffs, this will guarantee i t s independence. If government does not deem it advisable to raise tariffs, the Commission can then recommend alternative measures such as limiting the investment programs. Proposals put forth by the Commission would carry more weight with government and will encourage entities to adopt management tools and performance indicator monitoring systems.

41. In view o f the sector’s current situation, establishing the Commission i s considered a priority, regardless o f the institutional framework selected.

Financing and Cost Recovery

42. Tunisia’s tariff system focuses on cost recovery, efficiency, and solidarity between budget lines and inter-regional issues. In light o f these objectives, tar i f f scales have become national and progressive. Although tar i f fs ensure cost recovery for water, they have been lagging for sanitation.

43. Subsidies established for water consumption and the regions have helped to achieve social objectives, in spite o f insufficient targeting. The ideal policy would be to make direct transfers to disadvantaged households instead o f imposing the lowest tar i f fs with unreliable targeting. Certain countries have been successful with the direct transfer method, but the required conditions for this system do not yet exist in Tunisia.

Water and Sanitation Strategy in Tunisia. Final Report 9

44. The current water tariff system does not distinguish between domestic water consumption and economic uses, except for the tourism sector which enjoys the same tariff as the highest domestic segment o f the population. Thousands o f retailers, small- scale industrialists and art isans thus benefit from reduced tariffs.

45. recommended since the amount o f revenue generated would be low.

However, the application o f new tariffs for this specific group o f users i s not

46. SONEDE finances activities through i t s own resources, except rural investments which are funded by government. Future tariff policies should focus on the financial stability o f SONEDE. The creation o f an official Regulatory Commission would allow a more thorough review o f tariff adjustment cases and could provide an incentive for better cost reflection resulting in improved oversight.

47. For the sanitation sector, accumulated deficits have hindered i ts development and the quality o f i t s service delivery. Sanitation i s as important as potable water, especially in view o f the fragile state o f the environment which i s critical for quality o f l i fe and economic activity. Although government has financed the majority o f ONAS’ investments and a portion o f sector development, the institution must also develop i t s independent financing capacity through user contributions for the following reasons: (a) even if beneficiaries living in healthier environments are dispersed, pollution i s essentially due to potable water consumption. As a result, the application o f the polluter- pays principal implies that the latter will be charged for pollution control efforts; and (b) financing o f this activity must be separate from public finances and macroeconomic issues. In the long term, sanitation should be financed by the users. This goal will only be achieved progressively, however, since tar i f fs w i l l require readjustment to avoid financial problems within ONAS and to give this institution a degree o f financial capacity.

48. In rural areas managed by AICs/GICs/GDAs, investments are entirely financed by government. Operation and maintenance expenses are financed through potable water tar i f fs paid to AICs/GICs/GDAs. However, even if these tar i f fs are higher than those for SONEDE (with a comparable consumption rate) and they adequately cover operating costs, they do not meet the demands o f maintenance nor upgrading expenditures. When AICs/GICs/GDAs face breakdowns due to lack o f maintenance, they will not have the required funding for large-scale repairs and upgrades o f equipment and works. It i s therefore recommended that Government cover maintenance and upgrading costs through the creation o f a maintenance fund for AICs/GICs/GDAs.

49. Some collective sanitation pilot projects implemented by ONAS for government are financed by the State. Individual sanitation installations are financed by the owners. I t i s recommended that operating costs for collective works be financed partly through sanitation charges, and the balance by a state subsidy which would cover operating costs for wastewater treatment plants and pumping stations.

Water and Sanitation Strategy in Tunisia. Final Report 10

50. Tunisia has now established higher service delivery standards for the quality o f potable water and sanitation. Accordingly, financial assistance should support this trend, whether collections are made from the users (Le,, the urban sector for water) or divided between users and the state (i-e., sanitation). Tariff policies must ensure that urban water activities can financially support their own operations and that cost recovery for water production i s sustainable in the sanitation sector. The creation o f an official Regulatory Commission would be useful to better assess costs in view o f targeted objectives, especially for quality issues, and to prepare the tariff adjustments with more transparency.

5 1. Finally, it i s recommended that a detailed study on the option o f an “urban water and sanitation holding” be prepared to better formulate i t s context and implications for all sectors. The merging o f SONEDE and ONAS scenario would be worth assessing in the context o f this study to identify the best possible option. The creation o f an official and independent Regulatory Commission is, however, crucial at this point and should be a priority. Pending the results o f the study, reforms can be implemented to ensure the efficiency o f both operators.

Water and Sanitation Strategy in Tunisia. Final Report 11

Strategy on Drinking Water and Sanitation in Tunisia

DIAGNOSIS

At the request o f the Tunisian Government, the World Bank has mobilized a team o f multidisciplinary experts to undertake a strategy o f Tunisia's drinking water and sanitation sectors.

This comprehensive strategy specifically focuses on the sectors' institutional, organizational and economic aspects. It includes an analysis o f the current situation and identifies reforms that would contribute to tackling. upcoming challenges and deliver the best service at least cost to beneficiaries in urban and rural areas, while guaranteeing wide water and sanitation service coverage and sustainability.

The present document does not aim to be an exhaustive study o f the issues at hand, or attempt to provide answers to all the challenges reform will present for these two sectors. Rather, it i s a strategic analysis meant to identify the main axes o f reforms that should be implemented based on the results o f this reflection.

11 Tunkia 's water resources and allocation principles

Tunisia i s a Mediterranean country with limited water resources not exceeding 4,860 mill ion m3 / year, among which 610 million m3 / year are not easily renewable. 1,550 million m3 / year i s renewable groundwater, and 2,100 million m3 / year i s surface water flowing into oueds (rivers) and mobilizable at 95 %. Flow variations observed during the 1985-2006 period are between 7 and 8 billion m3.

The annual average precipitation i s estimated at 36 billion m3, with a variation between 7 and 90 billion m3, as observed during the last century.

Since 1970, several research studies for planning and simulation have been conducted using basic data from hydrological and hydro-geologic analyses obtained from measurement stations that are dispatched throughout the country.

The objective o f these studies and other related projects i s to mobilize the potential in variable surface water as well as in fragile groundwater resources, in order to satisfy fast- growing water needs while limiting the negative effect o f pollution, and ensuring water resources sustainability.

This research and analysis lead to the implementation o f several programs, including integrated developments in all the regions o f the country, according to a chronogram o f

Water and Sanitation Strategy in Tunisia. Final Report 12

mobilization o f water transfer, protection against floods, valuation o f subterranean waters, replenishments o f groundwater, provision o f drinking water to urban and rural areas, and water supply to irrigation perimeters. These represent multi-objective programs comprising water treatment and recycling through irrigation activities, whose scope i s adapted to hydraulic units and their connections.

- Resources available

for exploitation Total water demand

for all sectors

The studies and programs were carried out within the framework o f a larger regional master plan (for the North, Central, and South regions), mobilizing the various hydraulic systems in order to satisfy the need for drinking water in major urban and rural areas, as per the water code, as well as f the tourist, agricultural, and industrial sectors.

1996 2010 2020 2030

2,767 3,300 3,106 3,121

2,528 2,689 2,72 1 2,770

Thanks to the efforts designed to mobilize resources (construction o f large dams, earth dams, and hill lakes; groundwater replenishments, channels and water transfer systems, etc.), and to brackish water desalination, salted water recycling, water saving policies in the agricultural and other sectors, along with water resources protection from pollution, the country’s balance between supply and demand wi l l show a water surplus by 2030. Thus, the water safety o f the Tunisia will be ensured. However, managing the water system i s becoming increasingly complex and integrated, and the need for water depollution i s contributing to cost increase.

Table 1 below shows the evolution o f water demand for the various sectors (in million m3>:

Table 1 : Water resource allocation (million m3)

Table 2 below shows the supply vs. demand process for water resources (in million m3):

Table 2: Water Supply vs. Demand (million m3)

The programs developed were based on research studies in several areas, and aimed at limiting the r isks and threats associated with overexploitation, deterioration o f water quality, pollution, erosion, droughts, floods, shortages, malfunctions, waste, inefficiencies, climatic change, and deterioration o f primary data quality and value.

Water and Sanitation Strategy in Tunisia. Final Report 13

For example, the PISEAU I project for 200 1-2007 included components dealing with participative management o f water demand, integrated management o f water resources, conservation o f water resources and environmental protection against pollution. The project also provided for creating a modern storage information data processing system for water resources (SINEAU).

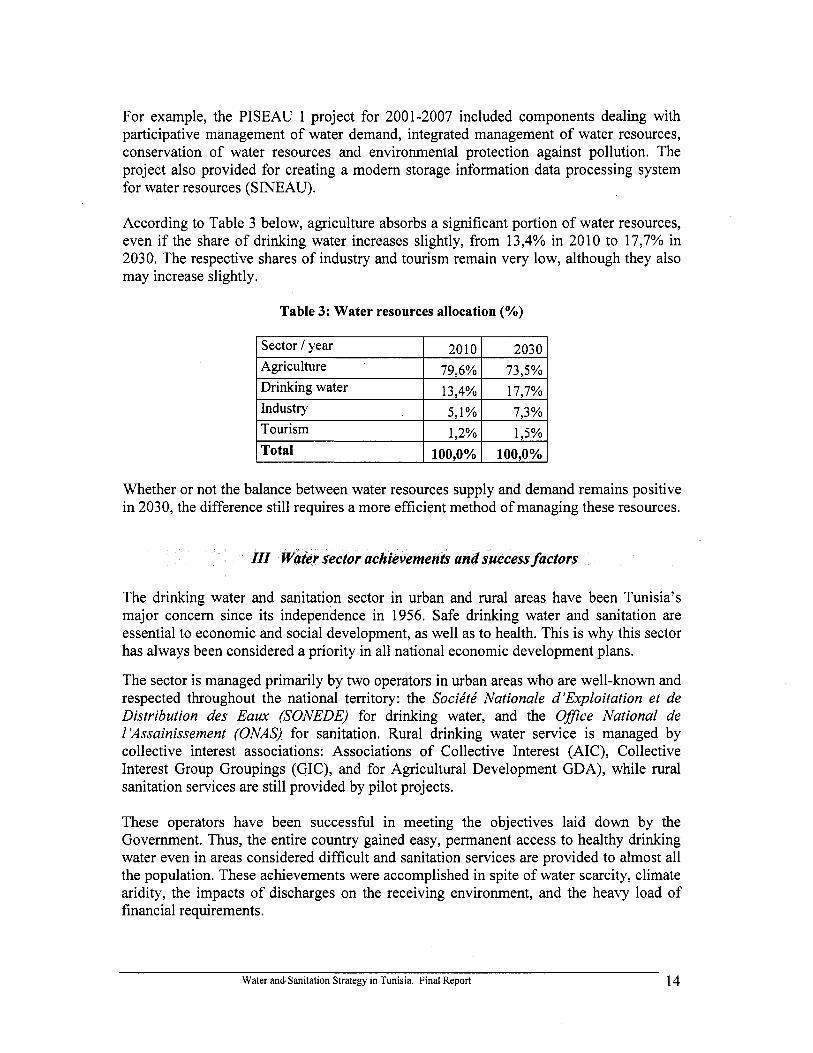

According to Table 3 below, agriculture absorbs a significant portion o f water resources, even if the share o f drinking water increases slightly, from 13,4% in 2010 to 17,7% in 2030. The respective shares o f industry and tourism remain very low, although they also may increase slightly.

Table 3: Water resources allocation (%)

Whether or not the balance between water resources supply and demand remains positive in 2030, the difference s t i l l requires a more efficient method o f managing these resources.

se cc

The drinking water and sanitation sector in urban and rural areas have been Tunisia's major concern since i t s independence in 1956. Safe drinking water and sanitation are essential to economic and social development, as well as to health. This is why this sector has always been considered a priority in al l national economic development plans.

The sector is managed primarily by two operators in urban areas who are well-known and respected throughout the national territory: the Socie'te' Nationale d 'Exploitation et de Distribution des Eaux (SONEDE) for drinking water, and the Ofjce National de 1 'Assainissement (ONAS) for sanitation. Rural drinking water service i s managed by collective interest associations: Associations o f Collective Interest (AIC), Collective Interest Group Groupings (GIC), and for Agricultural Development GDA), while rural sanitation services are s t i l l provided by pi lot projects.

These operators have been successful in meeting the objectives laid down by the Government. Thus, the entire country gained easy, permanent access to healthy drinking water even in areas considered difficult and sanitation services are provided to almost al l the population. These achievements were accomplished in spite o f water scarcity, climate aridity, the impacts o f discharges on the receiving environment, and the heavy load o f financial requirements.

Water and Sanitation Strategy in Tunisia. Final Report 14

However, the reforms implemented since the creation o f these two large operators have been limited, dealing primarily with organizational adaptations without addressing the institutional aspects. In addition, efforts were developed to economize on water usage, and adopt new technologies. On the other hand, private sector participation in the water sector i s considered modest, and limited to a few functions.

III. 1 Drinking water and sanitation performance: Main indicators

Some indicators showing these operators performance are mentioned below:

In 2006, urban water, rural water, and urban sanitation coverage rates, have reached respectively 100 %, 9 1 YO, and 80,9 YO.

The number o f SONEDE services users i s over 2 million, and 1.27 million for ONAS, while AIC / GIC / DGA have extended their services to more than 2.55 million. This broad coverage was made easier thanks to a progressive tariff structure that has allowed low-income households to access drinking water.

Access to healthy water and adequate sanitation services are basic human needs, essential to health, on the same level as medicines and vaccines. Infections by hydrous transmission have dropped significantly in Tunisia. The National Institute o f Public Health indicated that infectious and parasitic diseases account for only 3.5% o f the total causes o f death, and that there was a downward trend in the frequency o f children with diarrhea, from 15.6% in 1987 to 3.6% in 2002. On the other hand, the last case o f cholera reported in Tunisia goes back to 1986.

Service providers deliver a continuous, permanent, secure, and relatively uniform service throughout the entire country. SONEDE laboratories analyze the quality o f drinking water (in 2004, SONEDE took 53.938 samples, analyzed regularly by public health system services).

In the same way, the quality o f water treated by purification plants, and the impact on the receiving environment are analyzed by ONAS laboratories, under the control o f the Public Health System and the National Agency for Environmental Protection (ANPE);

Drinking water operators, other than SONEDE, DGGREE or GDA have responded to demand by providing water in sufficient quantity and in a continuous manner. Drinking water supply to SONEDE customers i s insured 24 hours a day, and every day o f the year. Cutoffs are very rare, due to certain management requirements and not to system failures. The number o f breakages i s 12.364 in 2004, that i s a breakage every 3.2 km. Breakages are found in the outdated water supply networks.

The improvement o f sanitary conditions was facilitated by the development o f drinking water and sanitation projects in rural and peri-urban areas.

Water and Sanitation Strategy in Tunisia. Final Report 15

In addition, ONAS had to respond to a tremendous increase in drinking water demand, control nuisance situations and potential health hazards, and protect sensitive ecosystems.

However, the direct and indirect economic impact o f drinking water and sanitation services extension, which i s considered an important growth factor, has not been studied.

111.2 Impacts on the population

The beneficiaries’ perception o f the operators i s generally positive. The services provided are appreciated, and the migration towards other providers doesn’t appear to have been considered, in spite o f tari f f increases.

Connection to the SONEDE and ONAS networks i s usually considered an achievement, and an indication o f moving up on the social ladder. Accessing the service seems relatively easy, and it i s available to low-income people. Anomalies are usually reported to the SONEDE and the ONAS as wel l as to the concerned Ministries. The beneficiaries’ reaction to system failures is fast and rather energetic, which stimulates the operators’ promptness to deal with issues. Complaints are thus taken into account and dealt with diligently.

The continuous provision o f services and the operators’ diligent and effective interventions to deal with the consequences o f breakdowns and floods, have greatly contributed to the ONAS and SONEDE positive image among consumers.

The quality o f the service and the pricing pol icy are generally the same everywhere in the country. Nonpublic users pay their invoices normally, and the water cutoff rate for nonpayment doesn’t appear to be excessive.

The coverage o f drinking water services in rural areas (91%) had a very positive impact on health, integrated rural development, as well as more generally the development o f these areas. In addition, a population cluster develops around each water supply facility. Moreover, the collective management o f the service has strengthened communal spirit and encouraged the creation o f micro-enterprises for maintenance purposes in rural areas.

I K l Vision, choice, policy, and planning

Drinking water supply and sanitation services were developed within the framework o f a clear long-term vision, supported by an unambiguous political will based on popular support for the various National Development Plans. The average annual investments within the 10th and 1 lth plans are 100 mi l l ion Dinars (MD) for SONEDE, 100 MD for ONAS and 30 MD for A I C / GIC / GIC.

16 Water and Sanitation Strategy in Tunisia. Final Report

O n the other hand, rigorous management, the development o f the required skills, and a planning process connecting the development o f water resources on national scale with a rational classification o f priorities, has resulted in a harmonious approach to project design and more efficiency in implementation. In addition, project design and implementation benefited from an extended database, and was based on feasibility studies. This has resulted in the access to drinking water for the majority o f the population, and to wastewater treatment in most urban areas.

SONEDE, ONAS, and A I C / GIC / GDA were able to generate significant knowledge throughout their history, and to use it appropriately. In addition, they combined certified and safe technologies, and adapted new technologies to the country’s specificities (iron treatment in rural areas, adaptation o f pretreatment techniques in desalination plants, water pipes corrosion control, odor treatment in water treatment stations, aeration system o f sludges tanks, etc.). These efforts are testimony to the assimilation capacity o f new technologies by public operators.

Timely climate, drought and f lood control efforts in sensitive and vulnerable areas have allowed the operators to develop short-term solutions integrated within a long-term vision for drinking water supply and hydrous pollution management. The success o f this approach has provided enough time to develop adequate long-term solutions, and to raise the required funds, without depriving consumers o f minimum service.

Finally, SONEDE, and AIC/GIC/GDA tari f f adjustments are made fairly regularly, with the active and positive participation o f al l the concerned actors within the sector and constitutes significant success factors for drinking water operators. The introduction o f a sewerage tariff, which hasn’t been readjusted regularly during the last decade, made it possible, however, to finance a large share o f operating costs. On the other hand, consumers’ payment capacity for the services was strengthened thanks to the past decades o f sustained economic growth;

IV.2 Institutional factors

Even if the institutional structure confers a monopoly on water and sanitation to SONEDE and ONAS in urban areas, the two public institutions, o f industrial and commercial nature, are governed by rules that clearly specify their respective missions. Their contract specifies in detail their respective five-year objectives. SONEDE and ONAS have an investment program included in the five-year plan, and a budget determined in consultation with the relevant Ministry, the Ministry o f Finance and the Ministry o f Economic Development.

The main parties are represented by the board o f directors o f SONEDE and ONAS, and their activities are monitored by the relevant ministries, the Prime Minister’s Office, the Ministry o f Finance, the Commission Supe‘rieure des Marche‘s (procurement committee), and the Court o f Audit, etc. Thus, recruitments are subject to prior approval, and

Water and Sanitation Strategy in Tunisia. Final Report 17

procurement activities are regulated and submitted to relevant procurement committees that also include outside members. In addition, external auditors regularly audit SONEDE and ONAS accounts, and the Court o f Audit i s entitled to conduct management controls.

In the absence o f an independent regulatory body, tariffs are determined after consultation and discussion with supervisory authorities, and are even discussed within inter-ministerial councils. Tariffs are published in the form o f ministerial decrees in the Official Journal fol lowing a transparent process. In the case o f nonpayment, SONEDE discontinues the provision o f drinking water.

SONEDE and ONAS have contributed to the creation o f sk i l ls and competences, and in the improvement o f human resources in their respective sector, thanks to their training and retraining policies.

In order to improve the re-use rate o f treated water in agriculture, a f i rs t step has been taken to form an appropriate institution through the creation o f a commission within the Ministry o f Agriculture to ensure efficient coordination.

Rural drinking water supply differs when dealing with agglomerated rural areas; semi- dispersed rural areas, or dispersed rural areas. Agglomerated rural areas are considered similar to urban areas and are supplied by SONEDE, even if that becomes an increasingly heavy load to carry. For dispersed rural areas, a participative approach was set up through the creation o f Associations o f Collective Interest “AIC” and Groupings for Agricultural Development “GDA”. Though these structures possess some weaknesses, they are appreciated because they supply dispersed rural areas with drinking water without direct intervention from the SONEDE.

O n the other hand, there i s an institutional vacuum with regard to sanitation in rural areas. This can sometimes become an issue when drinking water consumption increases and rural areas become agglomerated.

A centralized and de-centralized system for urban areas

The institutional system for urban areas i s centralized with some level on decentralization.

At the time o f SONEDE and ONAS inception, there was an obvious lack o f drinking water and sanitation services. Moreover, professional competences in these two areas were scarce. This explains the creation o f operators to operate on a national scale able to develop a comprehensive national approach in terms o f planning and priorities, and to facilitate relationships with the various donors and mobilize external resources for projects implementation. The geographical size o f the country made it possible to benefit from the advantages o f a centralized approach.

At the time o f the creation o f these public utilities, centralization made it possible for al l cities to benefit from scarce competences. It also allowed to capitalize on experiences,

Water and Sanitation Strategy in Tunisia. Final Report 18

coordination as well as cross subsidies between regions, without which it would have been impossible to supply drinking water and provide sanitation to some cities.

While being centralized, the institutional system i s also decentralized, since both SONEDE and ONAS have regional and even local representations. This type o f organization brings them closer to customers, to local and regional authorities, and to infrastructures.

Both operators are represented in regional councils, which allows them to take into account the regions needs, and to ensure a certain regional and social equity by providing uniform services.

A specific system for rural areas

With the development o f drinking water projects in rural areas, starting in 1980, there has been a burgeoning o f AIC/GIC/GDA destined to ensure the sustainability o f infrastructures built in these areas.

The operators in charge o f developing drinking water supply infrastructures in rural areas are SONEDE and DGGREE. These infrastructures are operated by SONEDE and the AIC/GIC/GDA groupings. The number o f AIC/GIC/GDA groupings has increased from 100 in 1987 to 2809 in 2005, including 16 10 for drinking water, 1075 for irrigation, and 124 for both (drinking water and irrigation). AIC/GIC/GDA groupings supply drinking water to more than two million consumers.

The success o f the rural drinking water supply sector, a complex sector given the multitude o f very diversified projects scattered throughout the country and often in difficult areas, i s explained by the strategy adopted by the DGGREE. This strategy made it possible to harmonize and synchronize the activities o f the various actors (consulting f i rms, construction companies, and AIC/GIC/GDA groupings for operational activities. The DGGREE played a key role in the creation o f AICS/GIC/GDA groupings.

Several consulting f i r m s and other small services f i r m s were created under the impulse o f the DGGREE, and established at the time o f the starting o f the rural drinking water supply projects. They all contributed to improve living conditions in rural areas.

In 2005, there were 932 water points for rural drinking water projects, including 284 deep wells, and 114 shallow wells, with the remaining ones being tapping on SONEDE or DGGREE networks from natural springs.

The poorly suppiied areas are mainly located in mountainous regions in the North Wes. This i s due to the insufficient hydrous potential o f local water tables, or to the frequent drying up o f local springs in summer or during years o f drought. This situation requires the use o f large water storage tanks ‘in wintertime, or long distance water transfer as well as pumping. In both cases, water treatment proves to be essential.

Water and Sanitation Strategy in Tunisia. Final Report 19

SONEDE has built large axes through mountainous regions Nor th o f Jendouba, Beja and Bizerte, connecting the dams located in the North o f the country, in order to ensure the supply o f the entire rural population o f one mi l l ion inhabitants, scattered in these areas without sufficient hydraulic resources.

Some regions located in the South, the Center and the Cap Bon are endowed with water resources loaded with i ron or salt, requiring specific treatments to reduce salinity and ferric concentrations. The SONEDE and DGGREE carried out several pilot projects to solve the problems linked to water supply to these areas.

To tackle constraints in terms o f water resources in difficult regions, DGGREE carried out hydro-geologic prospecting activities that contributed to identifying exploitable tables and provide for the needs o f the various projects.

The revision o f the AIC/GIC/GDA status on several occasions resulted in increased accountability on the part o f the management boards, and in improving the coverage rate as well as operational effectiveness.

State funding o f important repairs (replacing drilling equipment, electric pumps, etc.) contributed to AIC/GIC/GDA groupings positive image by the beneficiaries. In addition, DGGREE assistance and supervision constituted insurance and a protection for these groupings.

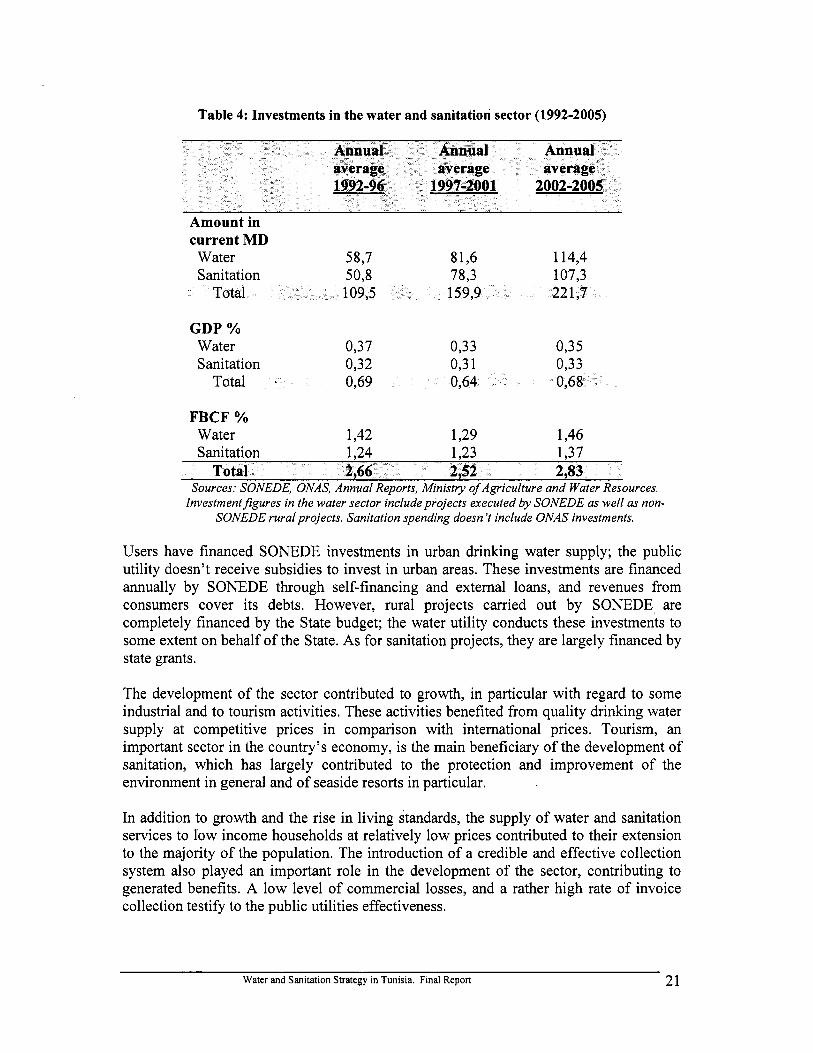

IV.3 Economic factors: the role of sustained growth

Economic growth has contributed to provide the necessary resources to finance the water and sanitation sector.

Robust growth that characterized the Tunisian economy during the past four decades, on average more than 5% per year, made it possible for the Government to mobilize internal and external re2ources to finance investments in water and sanitation in a sustainable manner. Moreover, economic growth led to improvements in household incomes, making it possible for them to afford water and sanitation services. Thus, progress in this sector would not have been possible with a l o w rate o f economic growth.

Water and sanitation services developed thanks to sustained investment efforts. These investments have doubled during the period between the 8th and 10th Development Plans, increasing from less than 110 MD a year to more than 221 MD a year (see Table 1). These investments increased in relation to total gross fixed capital formation, exceeding 2.8%. This upward trend concerned both water and sanitation. Thus, resources allocated to this sector increased at a pace even more sustained than macroeconomic growth and total investment.

Water and Sanitation Strategy in Tunisia. Final Report 20

Table 4: Investments in the water and sanitation sector (1992-2005)

Annual Annual Annual average average average 1992-96 1997-2001 2002-2005

Amount in current MD

Water 58,7 81,6 114,4 Sanitation 50,8 78,3 107,3

21

GDP Yo Water 0,37 0,33 0,35 Sanitation 0,32 0,3 1 0,33

Total 0,69 0,64 096

FBCF Yo Water 1,42 1,29 1,46 Sanitation 1,24 1,23 1,37

Sources: SONEDE, ONAS, Annual Reports, Ministry of Agriculture and Water Resources. .~ ~

Investmentfigures in the water sector include projects executed by SONEDE as well as non- SONEDE rural projects. Sanitation spending doesn ’t include ONAS investments.

Users have financed SONEDE investments in urban drinking water supply; the public utility doesn’t receive subsidies to invest in urban areas. These investments are financed annually by SONEDE through self-financing and external loans, and revenues from consumers cover its debts. However, rural projects carried out by SONEDE are completely financed by the State budget; the water utility conducts these investments to some extent on behalf o f the State. As for sanitation projects, they are largely financed by state grants.

The development o f the sector contributed to growth, in particular with regard to some industrial and to tourism activities. These activities benefited f rom quality drinking water supply at competitive prices in comparison with international prices. Tourism, an important sector in the country’s economy, i s the main beneficiary o f the development o f sanitation, which has largely contributed to the protection and improvement o f the environment in general and o f seaside resorts in particular.

In addition to growth and the rise in living standards, the supply o f water and sanitation services to l o w income households at relatively l o w prices contributed to their extension to the majority o f the population. The introduction o f a credible and effective collection system also played an important role in the development o f the sector, contributing to generated benefits. A l o w level o f commercial losses, and a rather high rate o f invoice collection test i fy to the public utilities effectiveness.

Water and Sanitation Strategy in Tunisia. Final Report 21

V.1 Governance

Urban and rural systems managed by public institutions o f industrial and commercial nature supported by the state

The sector benefited from a sound organizational and governance system in spite o f some deficiencies. The operators are institutions o f industrial and commercial nature with financial autonomy, clear statutes, and objectives to fulfill, and are responsible for the supply o f services in their respective fields, while maintaining financial balance.

The operators’ mode o f organization allowed the inclusion o f the main partners representatives in the board o f directors, and to subject the sector to rigorous rules o f management. Contract programs were later developed to better define the relationship between the state and the two operators, SONEDE and ONAS. Monitoring projects cost and implementation was ensured thanks to a series o f tools and methods that certainly limited the operators’ autonomy but imposed a certain rigor in terms o f management. These tools and methods include: management control, monitoring o f procurement activities, external audit, contract-program, and, more recently, prior approval and monitoring for recruitments. Some o f these methods maybe less usefu l today, and should be replaced by a posteriori control.

The State has always provided support to the sector through investment subsidies for sanitation and drinking water in rural areas, and through a tar i f f policy that facilitated access o f low-income consumers to these services. The organization o f the sector that allowed commercial companies to operate, and the support provided by the state, in particular through subsidies or guarantees for foreign loans, facilitated the sector regular development,

Relationships with donors

Operators usually use loans from multilateral and bilateral donors to finance a substantial share o f their investments. It i s worth noticing here that the World Bank contributed to SONEDE and ONAS initiation.

Loan terms are generally advantageous (low interest rates, repayments over a long time frame, etc.). Some donors have also provided grants for specific activities.

Loans are granted with state guarantees, when they are not contracted directly by the Government o f Tunisia and transferred to operators (as was the case o f some loans that benefited ONAS).

Water and Sanitation Strategy in Tunisia. Final Report 22

Donors took part in the financing o f rural drinking water supply projects through the provision o f loans to the Government. These projects are usually carried out either by SONEDE, DGGREE, or by the CRDA.

Some donors have also provided assistance for AIC/GIC/GDA design and implementation.

Bilateral cooperation agencies have provided meaningful assistance for the operators’ development activities.

In addition to their financial support, donors often provide assistance in terms o f technical, management, strategic development, and capacity building activities.

Generally, loan contracts include conditions for project implementation, and sometimes the implementation o f management reforms (on the part o f the operators).

Donors also make recommendations for tariff readjustments.

Operators must provide donors with project implementation reports o n a regular basis (semi-annually or quarterly).

Projects financed by loans above a certain amount (specified in loan agreements), require the donor no objection with respect to specific allocation.

Issues that have arisen between operators and donors stemmed from the fact that Tunisian and donors’ procurement procedures may be different and even contradictory at times. Moreover, donors’ procedures are not uniform, which may have added to the problem.

Relationships with customers

The relationships o f SONEDE and ONAS with c’ustomers relate primarily to requests for connection, invoicing, and collection operations, as well as to complaints. Consumers’ complaints may be filed by phone, or on ONAS Website. O n the other hand, some communications activities have been especially designed to encourage the public to save water.

AIC/GIC/GDA managers’ relationships with the beneficiaries are direct with regard to daily problems, and through the annual general meeting for other issues. The beneficiaries elect these managers.

Water and Sanitation Strategy in Tunisia. Final Report 23

V.2 The sector operators

Operators have played a key role in the sector’s success.

Internalization o f Tunisia’s national vision and objectives

For a long time, Economic and Social Development Plans have been very useful frameworks to set objectives and determine investment plans for water and sanitation. The operators involved in this process made medium-term commitments for which they were held accountable during and after implementation periods. They participated actively in the planning process; taking into account local and regional needs for water and sanitation services in their investment programs. These operators have accumulated substantial experience over several national plans. This experience has been subsequently very useful in project and program design and implementation, and in progressively extending water and sanitation services to the population.

Capacity Building

The creation o f SONEDE (1968) and ONAS (1974) resulted in a new approach and dynamics, as wel l as in a more propitious climate in terms o f investments, and know-how and technological development. In addition, the adoption o f modern management techniques made it possible to reach 100% drinking water coverage in the country’s urban areas, and 80.9% with regard to sanitation. This performance has allowed SONEDE and ONAS personnel to improve their know-how by using various technical and management methods in the drinking water and sanitation sector.

The two companies have accumulated substantial know-how based on national traditions and on other countries knowledge systems in the areas o f exploitation and management o f drinking water resources and sanitation. This knowledge covers the entire water circuit, from water mobilization upstream to water treatment downstream.

In addition, this know-how was developed through adaptation to the specific conditions o f the country’s each region, and thanks to the two companies’ executives and other member o f the personnel assimilation and creative capacity, whose sk i l ls improved thanks to the development o f professional training.

Technical Capacity

The drinking water and sanitation sector has emerged as a major source o f jobs for a variety o f activities.

SONEDE, ONAS took advantage o f the realization o f many projects throughout the country to improve capacity and competence.

Technology transfer and international cooperation in projects and programs design,

Water and Sanitation Strategy in Tunisia. Final Report 24

implementation, and management have also contributed toward improving knowledge.

SONEDE, ONAS and the other structures responsible for drinking water supply in rural areas have succeeded in capitalizing on know-how accumulated through years o f experience.

- Training competent executives

The two organizations benefited fully from the teaching and professional training system, and obtained additional training when necessary to meet their specific needs. Retraining in various specialized areas was also available to them.

SONEDE and ONAS have developed their own training programs that they carried out or that were provided by independent consultants. These programs are based on competence requirements for .the personnel to fulfill i t s mission and to learn new technologies.

The 513 training cycles in 2005 for SONEDE related to computer engineering and management. Thus, 2,473 agents o f a total o f 6,93 1 agents attended the training sessions, including 50% supervisory staff members and 16% operation agents. For ONAS, training was centered on the use o f new purification technologies, networks, and management. Overall, for the two companies, an average 40% o f the personnel participated in the training and retraining sessions.

- Managerial quality

For SONEDE and ONAS, supervisor-to-staff ratio remains low for two main reasons. The f i rs t relates to the low subcontracting rate, particularly for routine tasks. The second has to do with the fact that the two companies are overstaffed, after many temporary jobs have been made permanent.

In 2005, the supervisor-to-staff ratio reached 8.2% for SONEDE and 11% for ONAS. A Quality Unit was created in 2004 with the purpose o f optimizing the use o f human and technical resources.

SONEDE and ONAS’ contract program for each National Development Plan comprises a clause relating to the obligation to improve the supervisor-to-staff ratio.

Man agemen t

Recently, the two companies have manifested a keen interest in improving management and governance. In the past, the operators’ focus was essentially on technical issues, but they became lately more aware o f the need for qualified management personnel and to introduce modern management methods. The increase in the number o f consumers, the scarcity o f financial resources, and a more regular management control explain this trend. However, computerization and efficiency require that efforts deployed be more constant in order to improve management effectiveness and the use o f New Information and

Water and Sanitation Strategy in Tunisia. Final Report 25

Communications Technologies (NICT) tools. Thus, SONEDE and ONAS have started a large management modernization program, with regard €0 methods and training.

Recruitment Discipline

Profiles selection and recruitment are programmed for each development plan and are monitored by the supervisory entities. Recruitment i s carried out by way o f entrance examination in accordance with established standards. The recruitment and regularization o f temporary employees are carried out in accordance with a calendar agreed upon with union delegates.

- External audit

External audit i s carried out in accordance with the regulations in force that apply to al l public enterprises. The annual audit i s carried out by known competent entities selected through a tender process.

Computerization

SONEDE and ONAS maintain information systems used for basic management needs such as accounting and financial management, procurement and stock management, personnel management and a common commercial system based at the SONEDE.

ONAS has developed, by subcontracting to consulting f i rms, some applications (operating budget, purchase, maintenance, rol l ing stock fleet management, etc.).

The two companies have programs to widen the scope o f their respective information systems.

Both companies plan to joint ly acquire a modern commercial information system (SIC) adapted to water and sanitation activities. In spite o f similarities in their activities, there i s no other program designed joint ly apart from the commercial system in project. It seems that systems are developed with a l o w level o f integration, and also that some o f them provide only basic information pertaining to personnel management.