72

Report of the Tax Forecasting Methodology Review Group February 2008

Report of the Tax Forecasting Methodology Review Group

February 2008

2

Contents

Page

Executive Summary 3

1. Introduction 9

2. Main Developments in Tax Revenue 1999 – 2006 11

3. Tax Revenue Forecasting Process 17

4. Tax Revenue Forecasting Performance 31

5. Controlling for Economic Forecasting Errors 40

6. Retrospective Forecasting using Alternative Methodologies 47

- Incorporates Controlling for the Impact of the Property Market

7. Conclusions 60

Appendices 62

- Long-run Aggregate Tax Elasticity 63

- Composition of the Forecasting Errors 66

- An Examination of Data Revisions in the Quarterly National Accounts 68

- ESRI QEC Tax Revenue Forecasting Model 72

3

Executive Summary

Objective

The primary objective of this report is to examine the tax revenue forecasting

methodology currently employed by the Department of Finance in light of the actual

experience over the period 1999 - 2006. The motivation for conducting a review is

two-fold. Firstly, a considerable period of time has lapsed since the last review was

undertaken, and an update is therefore timely. Secondly, on a headline basis, there has

been considerable overshooting of tax revenue over the last three years. A detailed

analysis of the tax forecasting performance over a longer timeframe is therefore

required.

Aggregate Performance

At an aggregate level, the analysis finds that, on a headline basis, there has been a

significant divergence between forecast tax revenue and the actual outturn over the

period 1999 – 2006; the overall root mean squared (forecast) error (RMSE) is found

to be 6.1 per cent of the actual tax revenue outturn.

Developments on a purely headline basis are subject to a number of important

caveats. For instance, various one-off factors (both positive and negative) which are

difficult to quantify ex ante will impact on the accuracy or otherwise of the tax

forecasts. In addition, forecasts of macro-economic variables are a key input into the

tax forecasting process, and economic forecasting ‘errors’ will contribute to

inaccuracies in the tax revenue projections.

Therefore, in order to quantify the underlying tax forecasting error, the analysis

controls for these factors. This is undertaken through retrospectively forecasting tax

revenue on the basis of actual economic developments and by applying the actual

revenue generated from the various one-off factors over this period. The result is a

decline in the RMSE to 4.0 per cent, suggesting that economic forecasting errors and

one-off factors had some impact on the accuracy of the tax forecasts.

In terms of the direction of error, tax revenue has, for the most part, tended to exceed

forecasts, possibly suggesting a prudent bias in the forecasts. In terms of comparison

with the previous report, the scale of the error is larger over the later period,

4

suggesting a deterioration in the forecasting performance in more recent years. The

direction of the error is unchanged vis-à-vis the earlier report.

Performance of Individual Tax Heads

Developments for the individual tax heads are also analysed. On average over the

period, the four largest tax heads accounted for almost 90 per cent of total tax

revenue, so that developments in these deserve special mention. On an underlying

basis (i.e. having controlled for economic forecasting errors and one-off factors), the

following results emerge:

the average error for income tax over the period was found to be 3.9 per cent,

with revenue from this source undershooting forecasts in five of the last six years.

However, there were fundamental changes to the income tax system over this

period, namely the introduction of tax credits and partial individualisation.

VAT forecasts were found to be the most accurate of all the tax heads, with a

RMSE of 3.3 per cent. Revenues have overshot forecasts in each of the last three

years.

Corporation tax receipts recorded the largest error of the four largest tax heads,

with an error of 7.5 per cent over the period. Given the scale of multinational

operations relative to the size of the domestic economy together with a number of

important changes to the corporation tax regime in recent years it is perhaps not

surprising that this tax head has proved to be difficult to forecast with any degree

of accuracy. Moreover, Ireland is not unique in recording significant forecasting

error for this tax head; broadly similar developments have been evident in the UK

for instance.

The RMSE of the excise duty forecasts over the period was 3.8 per cent.

However, this is due in large part to the scale of the error in 2001, when excise

duties were 18 per cent below target. Excluding this one year from the analysis

reduces the RMSE to 2.8 per cent.

Considered in aggregate, the underlying forecast error of the four largest tax heads is

3.2 per cent. This suggests that smaller tax heads have had an important role in the

divergence between forecasts and outturn.

5

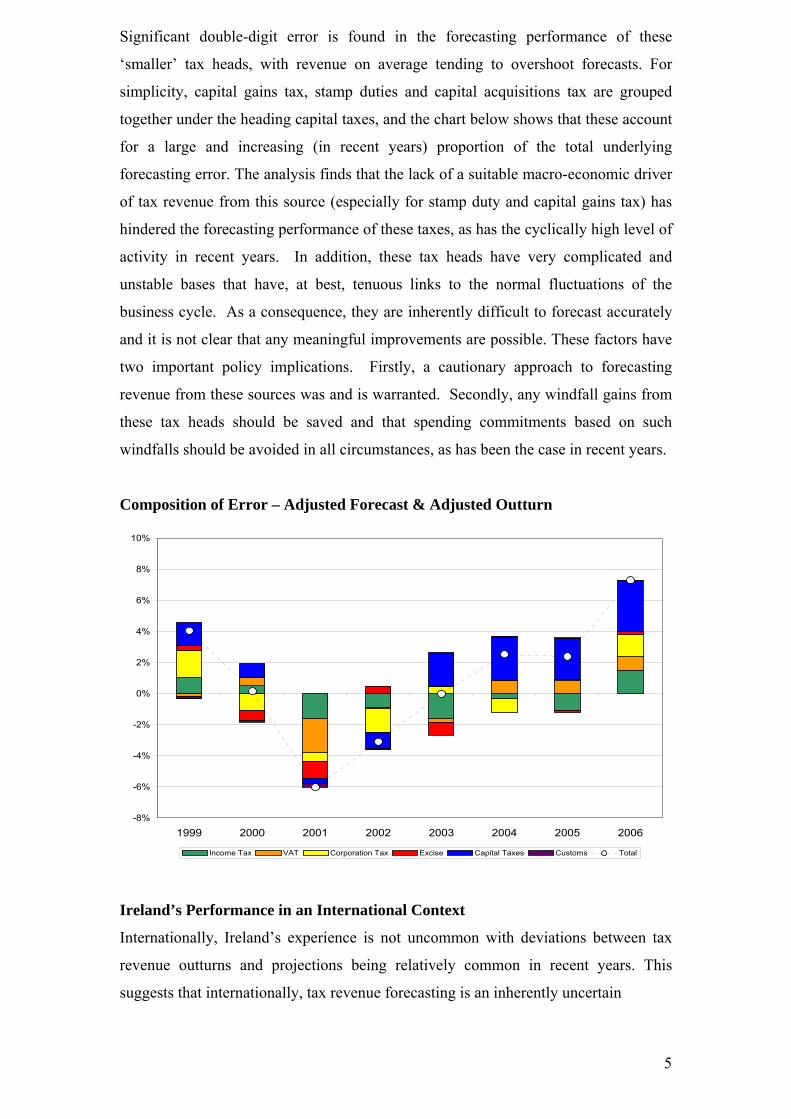

Significant double-digit error is found in the forecasting performance of these

‘smaller’ tax heads, with revenue on average tending to overshoot forecasts. For

simplicity, capital gains tax, stamp duties and capital acquisitions tax are grouped

together under the heading capital taxes, and the chart below shows that these account

for a large and increasing (in recent years) proportion of the total underlying

forecasting error. The analysis finds that the lack of a suitable macro-economic driver

of tax revenue from this source (especially for stamp duty and capital gains tax) has

hindered the forecasting performance of these taxes, as has the cyclically high level of

activity in recent years. In addition, these tax heads have very complicated and

unstable bases that have, at best, tenuous links to the normal fluctuations of the

business cycle. As a consequence, they are inherently difficult to forecast accurately

and it is not clear that any meaningful improvements are possible. These factors have

two important policy implications. Firstly, a cautionary approach to forecasting

revenue from these sources was and is warranted. Secondly, any windfall gains from

these tax heads should be saved and that spending commitments based on such

windfalls should be avoided in all circumstances, as has been the case in recent years.

Composition of Error – Adjusted Forecast & Adjusted Outturn

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

1999 2000 2001 2002 2003 2004 2005 2006

Income Tax VAT Corporation Tax Excise Capital Taxes Customs Total

Ireland’s Performance in an International Context

Internationally, Ireland’s experience is not uncommon with deviations between tax

revenue outturns and projections being relatively common in recent years. This

suggests that internationally, tax revenue forecasting is an inherently uncertain

6

process, and some error is inevitable. The international approach to forecasting tax

revenue is generally similar to that in Ireland, namely a “bottom-up” disaggregated

tax head approach supplemented by a “top-down” check.

The scale of deviation in Ireland is nevertheless found to be high by international

standards. There are a number of exceptional factors, however, that have contributed

to this. Firstly, the period dealt with in this report (1999 – 2006) was a transitional one

for the Irish economy. Substantial structural changes within the economy and within

the tax system meant that the relationship between the relevant tax bases and their

economic drivers may have changed over time. Unfortunately, pinning down a

steady-state relationship during a transitional period of deep structural change is

highly problematic. The residential property market is perhaps the most obvious

example. In Ireland, the residential property market has been among the most

dynamic in the OECD, with significant increases in both prices and turnover. As a

result, it is estimated that housing-related tax revenue has risen from around 3½ per

cent of total tax revenue in 1999 to 9 per cent in 2006. It is also worth noting that

stamp duty and capital gains tax receipts emanating from activity in the non-

residential/commercial property market have contributed significantly to the excesses

over target in tax revenues in recent years

Secondly, the Irish economy remains amongst the smallest and most open within the

OECD, with output concentrated in a relatively small number of sectors. As a result,

overall economic activity – and the tax revenue that this generates – is potentially

more volatile than in larger, more sectorally-diversified countries. For instance, the

global ICT shock in 2000/01 had a very sharp, almost instantaneous impact on

economic activity in Ireland, with noticeable tax revenue undershooting occurring as a

consequence. This experience illustrates the volatility of tax revenue in Ireland to

extraneous factors and provides a strong justification for a cautionary approach.

Tax-GDP Elasticity

Over the 1996-2006 period, the implied aggregate tax-to-GDP elasticity was found to

average 1.11. This figure must be interpreted with caution however. There has been

considerable year-to-year variance, with, for instance, an implied elasticity of around

0.3 in 2002, while in 2006 the implied elasticity was almost 2.0.

1 In simple terms, this means that for every 1 per cent rise in GDP, tax revenues rise by 1.1 per cent. See Appendix 1 for details of elasticity calculations.

7

Recommendations

On the basis of the analysis contained in the report, the following recommendations

are made under three main headings; namely methodological refinements, data

improvements and transparency.

Methodological Refinements

Maintain an aggregate tax-to-GDP elasticity of 1.0 as a “top-down” check on the

“bottom-up” approach. This recommendation was put forward in the previous

report of the Tax Forecasting Methodology Review Group. Despite the short-

term variance evident at the aggregate level in recent years, the tax-to-GDP

elasticity should still be viewed as an important check of the overall tax forecast.

The current approach to forecasting VAT receipts should be complemented by

an alternative approach which projects VAT receipts from new housing

separately from other VAT receipts. In theory, the alternative approach would

appear to be a more methodologically robust approach. However, retrospective

analysis shows no improvement over the entire period in question, although

significant improvements are evident in later years. Hence, there is a need for

the two approaches to be undertaken in tandem and for the relative merits of

both to be examined on an ongoing basis. This, of course injects an element of

subjectivity into the forecasts, although this is not seen as a major issue.

Using the macro-economic variable Gross Operating Surplus (defined as GDP

minus compensation of employees) as a driver of corporation tax receipts could

be considered. For most years the use of this variable leads to an improvement

in the tax forecasting performance. However, because there is a deterioration in

two of the years considered, it is recommended that this approach be used in

conjunction with the current approach.

Maintain the disaggregated approach to forecasting stamp duty that was first

used in Budget 2006, namely using forecasts of new housing output and prices

as a loose proxy to project receipts from residential property and using the

nominal increase in other building and construction investment excluding roads

to project receipts from non-residential property.

8

Given that the excess property-related tax revenue in recent years would appear

to be cyclical rather than structural, a cautious approach to forecasting property-

related tax revenue is prudent and should be continued.

Improved Data

Given the increased importance of receipts emanating from the housing market

in recent years, a more detailed breakdown of the actual VAT yield is desirable.

This would allow the actual receipts from new housing to be identified. At

present only estimates of the VAT yield from this sector can be obtained,

through the Post-Budget VAT base. While a breakdown of actual receipts is

desirable, it must be recognised that obtaining such data would involve drawing

on significant resources of the Revenue Commissioners. Therefore it is

recommended that this issue be investigated further.

More timely data on the nature of property market transactions giving rise to

stamp duty and capital gains tax receipts would also be useful although there

must be acknowledgement of the recent improvements in this area and

acceptance of the structural difficulties involved in going further.

Transparency

In light of the fact that the Irish economy has effectively been in a transitional

phase over the period in which this analysis was undertaken, it is recommended

to undertake more regular analysis of the tax forecasting performance. The

results of such analysis could be published by the Department of Finance on an

annual basis. This could also contain analysis of significant one-off factors

which are considered important.

9

1. Introduction

1.1 The last full review of the Department of Finance’s tax forecasting methodology

was carried out in 1998.

1.2 In light of the increasingly large variations which have arisen between tax

revenue forecasts and outturns in recent years in particular, it was decided to

carry out a further review of the tax forecasting methodology.

1.3 The Tax Forecasting Methodology Review Group (TFMRG) was established in

December 2006. The focus of the Group’s work was to carry out an evaluation

of the tax forecast methodologies currently used by the Department of Finance.

1.4 The formal terms of the reference for the Group were as follows:

To review the existing tax forecasting methodologies;

To examine the reason for divergences between tax revenue outturns and

forecasts;

To analyse the information bases on which forecasts are made;

To review the structural parameters of tax elasticities;

To look at the tax forecasting experience in other relevant jurisdictions;

To make recommendations for methodological changes, where

appropriate.

1.5 The Group was chaired by a Senior Economist on secondment to the

Department of Finance from the Central Bank and was comprised of other

representatives from the Department, the Revenue Commissioners, the Central

Bank, the Economic and Social Research Institute and the European

Commission.

1.6 The following were the members of the working group:

10

John McCarthy (Department of Finance, on secondment from the Central

Bank) – Chairperson

Paddy Molloy and Gerard Moran (Revenue Commissioners)

Ide Kearney and Adele Bergin (ESRI)

Diarmaid Smyth (Central Bank)

Brian Finn, Emma Cunningham and Aideen Foley (Department of Finance)

Martin Larch (European Commission) – participated fully by e-mail and

provided useful analysis and insight in relation to the international

experience in the tax forecasting area.

Alan Mahon (Department of Finance) – Secretariat

11

2. Main Developments in Tax Revenue: 1999 - 2006

2.1 This section of the report details the changing composition of tax revenue since

1999. The main developments in relation to the tax forecasting process since the

previous report of the TFMRG are also outlined.

Structure of Tax Revenue

2.2 Chart 2.1 shows the share of Exchequer tax revenue accounted for by each tax

head in 1999 and in 2006.

2.3 The tax heads are ranked in descending order according to their respective share

of total revenue in 2006. The data illustrate that in 1999, aggregate tax revenue

was concentrated in the four largest tax heads – VAT, income tax, corporation

tax and excise duties – which together accounted for €21.7 billion or 92 per cent

of total tax revenue. This concentration has declined over the period, with the

proportion accounted for by these tax heads falling to 84 per cent in 2006 -

€38.1 billion of a total €45.5 billion. This reflects the growth of stamp duties and

capital gains tax (CGT) over this period. When these two latter tax heads are

included, the six largest tax heads account for 99 per cent of total tax revenue. It

is clear, therefore, that in terms of forecasting tax revenue, focusing on these

particular tax heads is sufficient.

Chart 2.1: Tax Receipts - % of Total in 1999 and 2006

1999

■ VAT ■ Income tax ■ Corporation tax ■ Excise duty ■ Stamp duty ■ CGT ■ CAT ■ Customs

2006

12

VAT

2.4 VAT receipts accounted for 29.5 per cent of total tax revenue in 2006, 3.2

percentage points more than the equivalent figure in 1999. As a result, VAT has

overtaken income tax as the largest source of tax revenue in Ireland (this

occurred for the first time in 2003, and has been consistently the case ever

since).

Income Tax

2.5 In 1999, income tax was the largest source of tax revenue, accounting for 34.1

per cent of total tax revenue. By 2006, this share had fallen to 27.2 per cent. The

decline in the share partly reflects a number of changes to the income tax

regime, including a decline in tax rates and a widening of the bands. The

revenue take from this source in recent years has been negatively affected by the

significant Exchequer cost arising from the popularity of the SSIA scheme (the

tax credits paid to SSIA holders were essentially treated as income tax

repayments) but also positively impacted upon by the yields from the various

Revenue Commissioners’ special investigations. The decline in the share also

reflects the growth in other sources of tax revenue.

2.6 Income tax comprises separate PAYE and non-PAYE components. Non-PAYE

consists, amongst other things, of Schedule D (paid by farmers and the self-

employed), Deposit Interest Retention Tax (DIRT), Withholding Tax (WHT)

and Dividend Withholding Tax (DWHT). PAYE receipts have historically

tended to account for approximately 80 per cent of total income tax. The extent

of receipts from Revenue’s special investigations, the majority of which are paid

over as non-PAYE income tax have “artificially” boosted receipts from this

subhead in recent years. Table 2.1 gives a Revenue net receipts2 breakdown of

income tax between PAYE and non-PAYE.

2 Net receipts (accounting concept) differ from Exchequer receipts (cash concept) mainly because of timing and accounting differences.

13

Table 2.1: Income Tax – Revenue Net Receipts Breakdown 1999-2006

Income Tax €m PAYE % Non-PAYE %

1999 8,028 83 17

2000 9,113 78 22

2001 9,347 78 22

2002 9,063 74 26

2003 9,162 79 21

2004 10,651 76 24

2005 11,266 77 23

2006 12,390 76 24

Corporation Tax

2.7 Corporation tax, as a share of total tax revenue has remained relatively constant

over the period, rising slightly from 14.6 per cent to 14.7 per cent over the

period, although it did reach a peak of 16.4 per cent in 2002. There have been a

number of important changes to the corporation tax regime over this period,

most notably the phased reduction to a standard 12½ per cent tax rate for trading

income generally but also the decision to bring forward the payment date for

preliminary corporation tax by seven months, effectively to a current year

payment basis.

2.8 The 5 year transition period for the gradual move to a current year payment

basis for corporation tax ended in 2006. The transition arrangements – whereby

1/5th of the amount due was brought forward in each year – generated cash-flow

gains in each of the transitional years but from 2007 this cash-flow gain is lost.

This cash-flow loss broadly offsets the benefit to the Exchequer arising from the

ending of the SSIA scheme.

Excise Duty

2.9 Excise duties as a percentage of total tax revenue have declined from 17.2 per

cent in 1999 to 12.3 per cent in 2006.

Stamp Duty

2.10 Stamp duty as a percentage of total tax revenue has more than doubled since

1999, rising from 3.9 per cent to 8.2 per cent in 2006. Stamp duty receipts are

mainly levied upon equity and property (residential and commercial)

14

transactions. The large increase in property prices – together with the high level

of activity in the market – is primarily responsible for the increase in the share

of revenue attributable to this source.

Capital Gains Tax (CGT)

2.11 Receipts from CGT have increased significantly since 1999, from 1.9 per cent of

total receipts to 6.8 per cent in 2006. While the yields from residential and

commercial property transactions have undoubtedly played an important role in

driving the increase in revenues from this tax head since 1999, other sources of

CGT such as from the disposal of quoted and unquoted shares and agricultural

and development land have also contributed significantly (see table 2.2 below).

Table 2.2: CGT by Consideration Value of Asset Type Disposal3

% of Total 2002 2003 2004 2005

Quoted Shares 21 23 26 20

Unquoted Shares 15 15 14 13

Residential Property 19 19 18 18

Commercial Property 13 12 15 17

Agricultural Land 13 13 11 12

Development Land 11 12 11 16

Other 8 6 6 5

Total 100 100 100 100

*Figures may not add to 100 per cent due to rounding of individual categories.

Other Tax Receipts

2.12 The data also illustrate that the revenue from other tax heads (capital

acquisitions tax, customs and levies) are relatively small. In aggregate terms,

receipts under these tax heads totalled to 1.3 per cent of total tax revenue in

2006, a decline from the 2.1 per cent share in 1999.

3 Table 2.2 contains details of CGT by consideration value of disposals by asset type and as such is no more than indicative of the actual CGT yield. The 2002 – 2004 figures are derived from CGT returns filed via the Revenue Online System (ROS) version and the paper version of Form 11 (the Pay & File tax return form). The 2005 figures are derived from CGT returns filed to early January 2007 via the ROS version of the Form 11 only. CGT returns can be made via other Forms but these figures capture the majority of returns.

15

Main Developments since the 1998 TFMRG Report

(i) Direct Tax Base Working Group

2.13 The Direct Tax Base Working Group (DTBWG) is an informal group set up

with the approval of the Minister for Finance in mid-2002 and is made up of

officials of the Department of Finance and the Revenue Commissioners. It was

established in order to analyse the reasons for the shortfall in direct taxes around

2001/2002 and to examine issues which may have had an impact on the tax

yield from direct taxes, including income tax, for the purpose of improving the

tax forecasting methodology. While the work of this Group is ongoing, the

Group has identified a number of areas where improvements can be made.

2.14 The Group examined issues related to the sampling of the Revenue

Commissioners income tax data files with a view to using more up-to-date but

not fully complete information to improve the forecasting of income tax (in

particular PAYE) receipts. The aim would be to cross-check and verify

employment and earnings elasticity coefficients calculated on the existing

historical basis using more up-to-date though partially incomplete Revenue

taxpayer data. In a rapidly changing economy such as Ireland the hope would be

to use a more up-to-date representative though incomplete sample rather than

using an older although more complete sample.

2.15 The Group has also considered ways to improve the forecasting of stamp duties

and CGT. In the area of stamp duty, a difficulty is the absence of timely data on

the underlying transactions giving rise to stamp duty yields. Detailed current

data (details of the residential and non-residential stamp duty tax yield for a

particular month available by the middle of the following month) on the

numbers and values of transactions in the residential and non-residential

property area, from which the majority of the stamp duty yield is derived, has

not been available. Similarly for CGT, the legislative processes operating mean

that it is systematically not possible to obtain relevant information on the

underlying transactions giving rise to current tax yields. For example, while the

payment of CGT on transactions giving rise to liability in the first 9 months of

2006 was due on 31 October 2006, details of the transactions themselves are not

required to be returned until one year later at end-October 2007. Some progress

has been made on this issue (see Table 3.2 for details of CGT by consideration

value of disposal by asset type for the years 2002-2005).

16

2.16 The work of the DTBWG is still ongoing and it would be unwise to draw any

conclusions at this time regarding the possible usefulness of its work for

forecasting purposes.

(ii) IMF Article on Ireland’s Fiscal Forecasting Record

2.17 In October 2005, the International Monetary Fund (IMF) published an analysis

of Ireland’s track record on forecasting the fiscal balance.4 On the revenue side

(which is of most importance in the context of this Report), the research found

that stronger-than-expected economic growth and buoyant asset price

developments were the main reasons for the overshooting of tax revenue. In

terms of economic growth forecasts, Department of Finance forecasts were

found to be similar to those of other institutions, and the difficulty in forecasting

economic growth in a period of strong economic growth was highlighted.

4 Favourable Fiscal Outturns: Is It Just the Luck of the Irish? – IMF Country Report No. 05/370

17

3. Tax Revenue Forecasting Process

3.1 Tax revenues are forecast by the Department of Finance on a disaggregated

individual tax head basis using relevant macroeconomic drivers supplied by the

Economic Forecasting Unit of the Department of Finance and, where

appropriate, certain elasticity factors.

3.2 There are eight main individual taxes, namely:

VAT

Income tax

Corporation tax

Excise duties

Stamp duties

CGT

Capital acquisitions tax

Customs duties – forecast by the Revenue Commissioners

The Department of Finance forecasts all of the taxes bar customs duties, which

are forecast by the Revenue Commissioners, on the basis of the available macros

provided by Department of Finance. In addition, in some instances (e.g., most of

the non-PAYE income tax) the Revenue forecast figures are used.

3.3 As the first six of these tax heads are forecast to account for 99 per cent of total

tax revenue in 2007, this Report focuses on them. The methodologies for

forecasting capital acquisitions tax (CAT) and customs duties are not discussed

in detail.

3.4 There are three tax forecasting rounds each year:

May/June for the Budget Strategy Memorandum (BSM). This is for the

information of the Government only and the forecasts are not made available

publicly.

18

September/October for the Pre Budget Outlook (PBO).5 An estimate of the

aggregate tax revenue outturn for the current year6 together with forecasts

for the following two years is provided in the PBO.

November/December for the Budget. An estimate of the tax revenue outturn,

on a disaggregated basis, for the current year together with forecasts for the

following three years is provided at Budget time.

3.5 As a “top-down” check on the validity of the overall tax forecast, in line with

the key recommendation in the 1998 Report of the TFMRG, the forecast change

in the level of nominal GDP is compared to the total tax revenue forecast growth

rate constructed on an individual tax head or “bottom-up” basis, i.e. the

elasticity of overall tax revenue growth with respect to nominal economic

growth is checked. In general, this particular elasticity factor is likely to be close

to one (see Appendix 1). However, this one to one relationship need not hold

from year to year and can be influenced by factors such as the composition of

economic growth and the impact of Budget changes.

3.6 There are a number of factors that effect tax forecasts:

Budget tax forecasts are made at a time when final economic data for the

current or forecast year are not available. In addition, most economic data

published by the CSO are subject to revision. A recent Central Bank

technical paper7 examining national accounts data published by the CSO

shows how initial estimates of GDP and its components can differ quite

significantly from final estimates, which creates problems for economic

forecasting purposes and hence for tax forecasting purposes. The paper

found that the final revision to the growth rate of GDP was 1½ per cent,

almost 20 per cent of average GDP growth over the sample. The average

5 This was first published in October 2006. 6 The Department of Finance constantly monitors in-year tax revenue performance and has often given estimates of the current year aggregate tax revenue outturn at its end-Q2 and end-Q3 Exchequer Returns Press Conferences. 7 Research Technical Paper 10/RT/06 by Colin Bermingham. This paper is summarised in Appendix 3.

19

revision was positive indicating that initial estimates of GDP tend to be too

low.

The composition of economic growth has a significant bearing on the actual

tax yield. This has been particularly applicable in recent years when the

composition of growth in Ireland has been heavily driven by domestic

demand.

At Budget time, the base year actual tax outturn is not known and therefore

the outturn is merely an estimate.

The impact of “one-off” or extraneous factors from year to year can be

significant. In recent years, the impact of Revenue’s special investigations

receipts has far exceeded expectations. These receipts cannot, by their

nature, be forecast with any degree of certainty.

The effect of structural changes (e.g. changes in the due date for payment) in

the tax system can sometimes impact on taxpayer behaviour with

unforeseeable results on tax revenues in the short term.

Receipts from some taxes such as CGT and stamp duties, which have

become increasingly significant in recent years, do not have as consistent a

relationship with economic growth as, say, income tax or VAT, and are

more difficult to forecast. These particular taxes are more dependent on

activity in the asset markets (property and shares). Activity in asset markets

is prone to more pronounced movements in volume and price than in the

wider economy and is therefore less predictable.

Corporation tax receipts from export profits are affected by international

trading conditions and are known to be highly volatile, particularly in small

open economies such as Ireland.

20

3.7 For all tax heads, the estimated impact of one-off or other factors expected to

affect tax collection in the forecast year is added to or subtracted from the

forecast.

Value Added Tax (VAT)

3.8 VAT is forecast by reference to growth in the nominal level of personal

consumption expenditure (PCE) including cars.

An estimate of the base year outturn for VAT is made.

This projected outturn is adjusted to take account of any known one-off

factors, both negative and positive, likely to impact on the yield in the

forecast year and also the effects of previous Budgets, which have been

carried forward.

This adjusted outturn figure is then grown by the forecast rate of increase in

nominal PCE, i.e. PCE (including cars) volume multiplied by a PCE deflator

and an elasticity factor, which has been 1 in recent years.

The figures are then refined to take account of the impact of Budget

measures, if any.

3.9 The bulk of VAT is due for payment in January and every second month

thereafter on the basis of trading turnover in the two months prior to each due

month.

Income Tax

3.10 Although income tax appears as a single tax head in the Budget Booklet, it

actually comprises separate PAYE and non-PAYE components. PAYE

represents around 80% of income tax and is forecast by the Department of

Finance. Non-PAYE consists mainly of Schedule D (paid by farmers and the

21

self-employed), Professional Services Withholding Tax (PSWT), Deposit

Interest Retention Tax (DIRT), Back Duty (special investigations monies) and

Dividend Withholding Tax (DWHT). With the exception of DIRT, which is

forecast by the Department of Finance, the other non-PAYE income tax

elements are forecast by the Revenue Commissioners.

3.11 There has been a major programme of structural reform to the income tax

regime in recent years. The standard and marginal tax rates have both been cut,

the standard rate band has been widened significantly, a system of tax credits

has replaced the tax free allowances and an element of individualisation has

been introduced. All of these changes coupled with the huge surge in

employment and the composition of employment have made the job of

forecasting income tax more difficult.

PAYE

3.12 To produce the PAYE forecast:

An estimate of the base year outturn for PAYE is made.

The projected outturn is adjusted to take account of any known one-off

factors, both negative and positive, likely to impact on the yield in the

forecast year and also the effects of previous Budgets, which have been

carried forward (in recent years relevant “one-off” factors have included the

impact of the SSIA scheme).

The adjusted outturn figure is then multiplied by an aggregate multiplier.

This multiplier is a combination of the forecast increase in non-agricultural

earnings together with an earnings elasticity factor and the forecast increase

in non-agricultural employment together with an employment elasticity

factor. The earnings and employment elasticity factors estimate the

sensitivity of PAYE taxes to changes in numbers employed and in the level

of earnings. For the Budget 2007 income tax forecasts, the elasticity factors

used for non-agricultural employment and non-agricultural earnings were

1.0 and 2.1 respectively. The aggregate multiplier is calculated by applying

22

the earnings elasticity to the earnings macro and the employment elasticity to

the employment macro. This is then applied to the cleaned PAYE base.

The figures are then refined to take account of the impact of Budget

measures, if any.

Calculation of Elasticity Factors

3.13 The elasticity factors take account of the fact that new and existing employees

are likely to pay tax at different marginal tax rates. In effect, the elasticity is a

measure of the tax increase arising from the shift of taxpayers from a lower to a

higher tax rate in the event of an income increase. The lower employment

elasticity factor represents the understanding that new jobs do not initially

generate as much in tax revenue as increases in the earnings of existing

employees. This is because the employment elasticity relates to new employees

and as the question of moving from one tax rate to another does not generally

apply in the first year of employment, a “flat” increase in tax equal to the

projected growth in numbers employed is therefore assumed.

3.14 The elasticity factors for any tax year t are derived from a projected taxpayer

income and tax model for the tax year t based on historical Revenue taxpayer

data for the tax year t-4. While “lookback” revisions of the elasticity factors tend

to confirm the projected versions of the elasticity factors first used (see 3.15

below), it is now considered appropriate that future projections be supported by

more recent information. An examination is underway to explore ways of basing

future forecasts on more up-to-date but less complete sample data for the year t-

2 (see work of Direct Tax Base Working Group in Chapter 3 for more detail).

3.15 A retrospective look back at the actual 2003 non-agricultural earnings elasticity

factor, carried out by the Revenue Commissioners, gave a figure of 2.0. The

figure used in the Budget 2003 PAYE income tax forecast, which was based on

1999 data was also 2.0, meaning that using more up-to-date information may not

necessarily prove more accurate. The analysis was carried out for one year only

and caution must be taken when drawing conclusions for other years.

Theoretically however, it would make more sense to use the most up-to-date

23

data available, provided of course it is fully representative of the complete data

series.

Non-PAYE Income Tax

3.16 Revenue’s forecast process for the main component of non-PAYE income tax,

Schedule D/Farmers, follows the same principles as PAYE but with some

differences such as:

estimating preliminary tax separately from “balances”. Preliminary tax for

the current tax year must be paid on or before the 31 October each year and

must be at least 90 per cent of the final taxable liability for that year (or

alternatively 100 per cent of the previous year’s liability). Any balance of

tax due for the previous tax year must also be paid on or before 31 October.

computing Revenue’s own income growth “macro” using historical trends of

tax yields.

adding in a separate estimate for the yield from normal audit activity. In

recent years, estimates of receipts from Revenue’s special investigations

would also have been included.

adjusting downwards to offset for higher withholding tax credits that arise

from an increase in that tax.

using a lower elasticity factor than is used for PAYE (income increases are

less likely to be reflected in tax payments).

monitoring trends of take-up on tax reliefs in case Revenue need to provide

for higher tax repayments.

3.17 Forecasting non-PAYE income taxes has proven difficult in recent times. [There

is no appropriate macroeconomic driver available to use in the forecasting of

these taxes and so Revenue compute their estimates using a growth “macro”

based on historical trends of tax yields]. Other issues such as the popularity of

24

tax incentives, most notably property based incentives which act as a legal tax

shelter but the take-up of which is difficult to predict and compliance issues on

foot of Revenue’s special investigations have also added to the difficulty in

forecasting non-PAYE income taxes.

Corporation Tax

3.18 Budget 2002 began the process, on a 5 year transitional basis, of bringing

forward the payment date for preliminary corporation tax by seven months,

effectively to a current from a preceding year basis. Therefore, with the payment

arrangements for corporation tax having undergone significant changes over the

last five years coupled with the phased reduction to a standard 12½ per cent tax

rate for trading income generally, the methodology for forecasting corporation

tax was made more difficult during this period.

3.19 The 5 year transition period for the gradual move to a current year payment

basis for corporation tax ended in 2006. The transition arrangements – where

1/5th of the amount due was brought forward in each year – generated cash-flow

gains in each of the transitional years but from 2007 this cash-flow gain will be

lost. It is estimated that corporation tax revenues in 2007 will be approximately

€700 million - €800 million less than they would otherwise have been as a result

of this cash-flow reduction.

3.20 In an effort to improve forecasting methods, the top 50 companies have been

contacted by way of a questionnaire from Revenue’s Large Cases Division

(LCD) in each of the last two years to see if they could forecast the expected

growth in the corporation tax they were likely to pay in year t+1.

3.21 Corporation tax is forecast in the following way:

An estimate of the base year outturn is made.

This projected outturn is then adjusted to take account of any known one-off

factors (LCD survey based or other known factors) likely to impact on the

25

yield in the forecast year and also the effects of changes in previous Budgets

which have been carried forward.

This figure is then multiplied by the growth in nominal GDP in the forecast

year and an elasticity factor, which has tended to be 1 in recent years.

A particular problem with corporation tax however is that just over half of

all corporation tax is due for payment in November. Collection performance

in the preceding months of the year is thus not a reliable guide on the

November outcome.

The figures are then refined to take account of the impact of Budget

measures, if any.

3.22 For the Budget 2007 forecasting round, approximately 25 of the top corporation

tax paying companies made an estimate in mid to late 2006 in relation to their

2007 profits with some of these indicating expected negative growth in their

2007 tax (most of these as a result of once-off factors). In the 2005 survey for

use in Budget 2006 forecasts, those companies that did respond forecast zero

growth in tax payments in 2006 which obviously did not happen. Nevertheless,

the results of the 2006 survey were found useful in helping to determine the tax

forecast for 2007 and were used to enhance Revenue’s forecast methodology,

largely by increasing their knowledge of one-off factors.

Excise Duty

3.23 Vehicle Registration Tax (VRT) is included in excise duty. However, this

component of excise duty is forecast separately. The process involved in

forecasting these separate components is outlined below:

Estimates of the base year outturns for excise duties (less VRT) and for VRT

itself are made.

26

These projected outturns are then adjusted to take account of any known

one-off factors likely to impact on the yield in the forecast year and also the

effects of previous Budgets which have been carried forward.

The base year outturn for excises (excluding VRT but including the €168

million Health Tobacco Levy paid to the Department of Health and

Children) is then multiplied by the forecast increase in the volume of PCE

(excluding cars). The €168m Health Tobacco Levy payment is then stripped

out as it is not classified as an Exchequer tax receipt.

The Revenue Commissioners favour a different approach in respect of

excises other than VRT. Their estimates are usually compiled on the basis of

expected trends in the consumption of goods liable to excise. The

Department of Finance also analyses the Revenue’s trend based excise duty

forecasts thoroughly and has been known to adopt a combination of both

methodologies if it feels it will produce the most reliable forecast.

For VRT, the expected base year outturn is multiplied by the forecast

increase in the price and volume of new car sales.

Both the VRT and excise less VRT figures are then refined to take account

of the impact of any Budget measures.

Stamp Duty

3.24 Stamp duties are charged in respect of legal and financial transactions for which

there is a corresponding document. Most stamp duties are charged ad valorem

(at a certain percentage) of the value underlying the transaction in question.

Where it is not feasible to determine a value on which to base an ad valorem

charge, for example in the case of cheques, drafts and ATM cards, a fixed duty

is levied.

3.25 Table 3.1 shows the percentage breakdown of stamp duty receipts for each of

the years 1999-2006, using Revenue net receipts as the basis for calculation. It is

27

worth noting the increasing percentage of total stamp duty receipts accounted

for by property and within property related transactions, the increasing

importance of receipts from non-residential property transactions.

Table 3.1: Stamp Duty – Percentage Breakdown of Receipts 1999-2006

% of Total Stamp Duty From: 1999 2000 2001 2002 2003 2004 2005 2006

Land & Property

- Residential Property

- Non-Residential Property

60

29

31

62

26

36

55

22

33

58

31

27

65

32

33

71

36

35

75

35

40

82

36

46

Stocks & Shares 25 21 28 27 15 13 12 11

Companies Capital Duty 2 4 6 2 1 1 1 -

Cheques/Bills of Exchange etc 4 4 4 4 6 5 4 3

Insurance & Miscellaneous 9 9 7 8 7 5 4 3

Levy on Financial Institutions - - - - 6 5 4 -

Total 100 100 100 100 100 100 100 100

3.26 For the forecasting exercise, stamp duties are broken down into the following

sub-heads:

Residential Property

Non-Residential/Commercial Property

Stocks and Shares

Insurance Levy

Others (including non-life insurance levy, credit etc. cards & cheques)

3.27 Forecasts of stamp duty receipts attempt primarily to model movements in the

value and turnover of residential and non-residential property market

transactions. However, the available economic indicators are not entirely

satisfactory for predicting movements in property prices and turnover in the

second-hand market, from which the majority of residential property market

stamp duty receipts are derived.

28

3.28 Therefore, the following methodology is used to produce the stamp duty

forecast:

Estimates of the base year outturns for each component are made.

These projected outturns are then adjusted to take account of any known

one-off factors likely to impact on the yield in the forecast year and also the

impact of changes in previous Budgets which have been carried forward.

For residential property, the estimated change for the forecast year in the

volume and price of new house activity is used as a loose proxy for the

change in the level and value of stamp duty-liable transactions; this is

augmented by an (upward) adjustment for the consequential movement into

higher stamp duty bands brought about by the projected increase in house

prices.

On the non-residential8 side the nominal growth in investment in non-

residential construction excluding roads is used to forecast the increase in

yield from this source.

The shares category9 is increased in line with nominal GDP in the forecast

year.

The insurance levy is assumed to remain at the base year level (unless where

otherwise indicated by Revenue).

The others category is grown in line with projected consumer price inflation.

The figures are then refined to take account of the impact of Budget

measures, if any.

8 Revenue use an average growth rate derived from Stamp duty receipts from non-residential property over the past 5 years. 9 Consumer Price Index used by Revenue.

29

Capital Gains Tax (CGT)

3.29 CGT is chargeable on the gains arising from the disposal of assets. Any form of

property, including an interest in a property (lease) is an asset for CGT purposes.

The tax payment is liable once the asset is disposed of. Liabilities arising in the

first 9 months of the year are payable by the end of October that year. Liabilities

arising in the last three months of the year are payable by the end of the

following January.

3.30 There is no agreed methodology for forecasting receipts from CGT. The forecast

difficulties are compounded by the administrative structures under which the tax

operates and under which tax receipts are received at two points in the year

followed significantly later by the returns detailing the reasons for the

underlying liabilities.

3.31 The following approach to forecasting CGT is currently undertaken:

An estimate of the base year outturn for CGT is made.

This projected outturn is then adjusted to take account of any known one-off

factors likely to impact on the yield in the forecast year and also the impact

of changes in previous Budgets which have been carried forward.

This figure is then grown by the forecast rate of increase in nominal GNP in

the forecast year.

The figures are then refined to take account of the impact of Budget

measures, if any.

Capital Acquisitions Tax (CAT)

3.32 CAT comprises gift tax, inheritance tax, discretionary trust tax and probate tax

and very minor amounts in respect of residential property tax and is forecast

using the rate of increase in nominal GNP in the forecast year. In years prior to

Budget 2007, the CPI was used as the multiplier but the Department of Finance

considers that GNP is now a more appropriate growth factor.

30

Customs Duty

3.33 Customs duties are collected on a wide range of goods imported from non-EU

countries. While all customs duties collected are paid into the Exchequer, 75 per

cent of the amount collected is subsequently paid out of non-voted central fund

expenditure to the EU as part of Ireland’s EU budget contribution known as

‘traditional own resources’. The remaining 25 per cent is retained as collection

expenses.

3.34 The forecasting of this tax head is undertaken by the Revenue Commissioners,

with the Department of Finance generally accepting Revenue’s estimate.

However, the Department supplies Revenue with a macro-economic forecast of

the nominal (value) increase in merchandise imports. Forecasting customs duties

has become more difficult in recent years with the introduction of Single

European Authorisation (SEA) arrangements. This allows a company with

branches in different Member States to transact all of their customs business in

one Member State. The Member State which issues the SEA acts as the

Supervising Customs Authority for all Member States in respect of that

authorisation and collects the customs duties in respect of imports into the

various Member States. It then pays over an agreed amount of collection costs

(up to 25 per cent) to the various Member States into which non-EU goods have

been imported. For example, included in the customs receipts figure for 2006

was an amount of €44 million (around 17 per cent of total customs duties

collected in 2006) under an SEA collected on behalf of another Member State.

31

4. Tax Revenue Forecasting Performance

4.1 This section of the report analyses the tax revenue forecasts produced by the

Department of Finance over the period 1999 – 2006. The tax revenue forecasts

are the Budget day projections produced in December of each year for the

following year.

4.2 While tax revenue has outperformed Budget day projections in six of the last

eight years – significantly so in each of the last three years – it is clear that a

number of extraneous factors have had a sometimes significant impact on tax

revenue collection during that time. Such factors are often difficult – if not

impossible – to forecast with any degree of accuracy. In the analysis below,

therefore, the forecasting performance is shown, firstly, on an unadjusted basis

(i.e. no allowance is made for extraneous factors) and secondly, on an adjusted

basis (i.e. after making allowance for exceptional factors). This approach

enables a broad quantification of forecast errors.

Methodology

4.3 In terms of assessing the forecast performance, the approach taken below is to

formally examine the Budget day one-year ahead tax revenue forecasting

accuracy over the 1999 – 2006 period using the following statistical tools:

Mean (forecast) error, where: ME = 1/T*(Σet)

Root mean squared (forecast) error, where: RMSE = [1/T*(Σet2)]½

4.4 The error term for each year is defined as the difference between the outturn and

the forecast, expressed as a percentage of the actual outturn. The ME is the

simple average of forecast errors over the period. This provides an indication of

the direction of forecast errors. However, because but it is affected by both

positive and negative errors, it is not an appropriate tool to quantify the

magnitude of errors. On the other hand, the RMSE – defined as the square root

of the mean of the errors squared – is independent of the error sign and can

therefore be used to quantify the magnitude of the forecast errors. In line with

most of the recent international literature, the analysis below concentrates on the

RMSE measure.

32

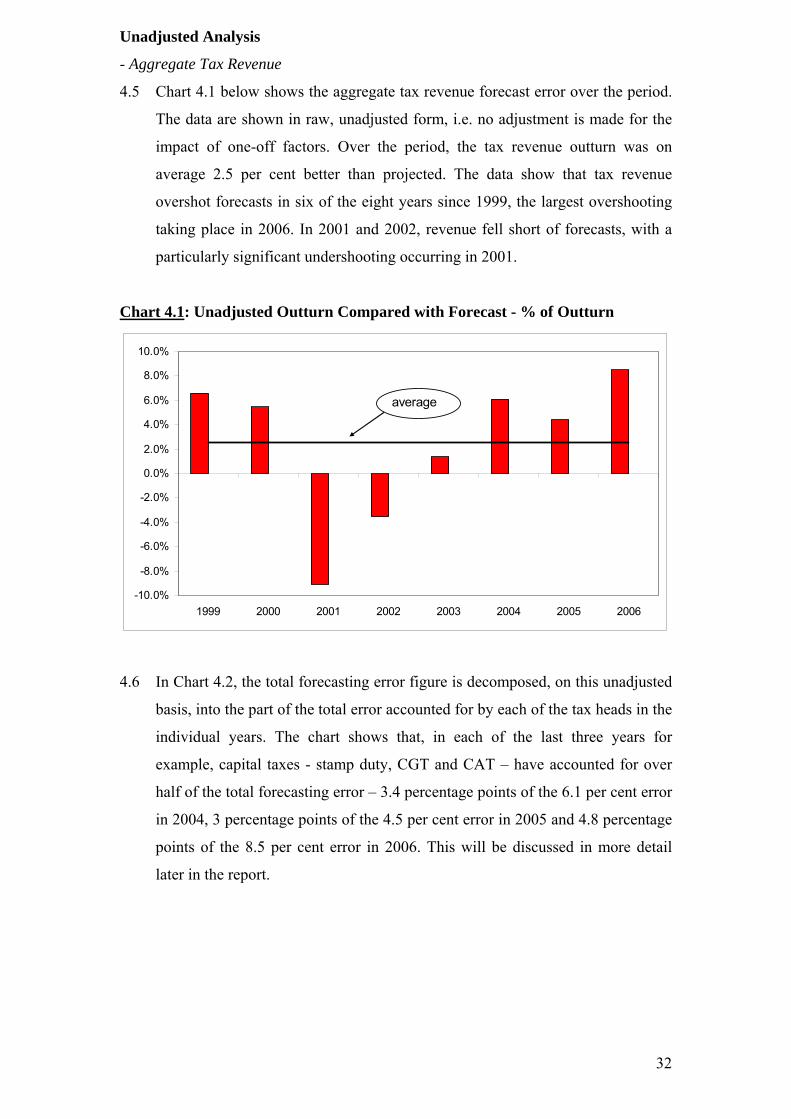

Unadjusted Analysis

- Aggregate Tax Revenue

4.5 Chart 4.1 below shows the aggregate tax revenue forecast error over the period.

The data are shown in raw, unadjusted form, i.e. no adjustment is made for the

impact of one-off factors. Over the period, the tax revenue outturn was on

average 2.5 per cent better than projected. The data show that tax revenue

overshot forecasts in six of the eight years since 1999, the largest overshooting

taking place in 2006. In 2001 and 2002, revenue fell short of forecasts, with a

particularly significant undershooting occurring in 2001.

Chart 4.1: Unadjusted Outturn Compared with Forecast - % of Outturn

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

1999 2000 2001 2002 2003 2004 2005 2006

average

4.6 In Chart 4.2, the total forecasting error figure is decomposed, on this unadjusted

basis, into the part of the total error accounted for by each of the tax heads in the

individual years. The chart shows that, in each of the last three years for

example, capital taxes - stamp duty, CGT and CAT – have accounted for over

half of the total forecasting error – 3.4 percentage points of the 6.1 per cent error

in 2004, 3 percentage points of the 4.5 per cent error in 2005 and 4.8 percentage

points of the 8.5 per cent error in 2006. This will be discussed in more detail

later in the report.

33

Chart 4.2: Composition of Forecast Error – Unadjusted Outturn & Forecast

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

1999 2000 2001 2002 2003 2004 2005 2006

Income Tax VAT Corporation Tax Excise Capital Taxes Customs Total

4.7 The forecasting error, as measured by the RMSE, was 6.1 per cent of the actual

outturn on this unadjusted basis. To put that 6.1 per cent overall RMSE in

context, a paper10 comparing Canadian Budget forecasts with those of other

industrial countries shows that the overall RMSE for tax revenues in Canada

over the nine year period 1995-2003 was 5.7 per cent. In the Netherlands, the

RMSE was 5.4 per cent while in Germany it was 5.1 per cent.

4.8 As mentioned above, capital taxes have become increasingly significant. This is

evidenced by the fact that the RMSE falls to 4.3 per cent, if it is assumed that

capital taxes were on target each year over the period.

4.9 The previous report of the TFMRG showed an average (mean) error of 3.3 per

cent of forecast tax revenue over the 10 year period 1988 – 1997.11

Significantly, tax revenues outperformed their targets in nine of those ten years

while in 1991 tax revenues were exactly on target. This is somewhat at odds

with the period since 1999. The extent of the overall average (mean) errors in

more recent years has generally been greater than over the 1988 – 1997 period

10 IMF Working Paper 05/66 - How do Canadian Budget forecasts compare with those of other Industrial countries? 11 Whereas the previous TFMRG report expressed errors as a percentage of the tax forecasts, this report expresses the errors as a percentage of the actual tax revenue outturns.

34

while tax revenues came in below target in 2001 and 2002, by 9.1 per cent and

3.5 per cent respectively.

- Disaggregate Tax Revenue

4.10 The forecasting performance of each of the individual tax heads over the period

is illustrated in table 4.1. With the exception of PAYE income tax, excise duties

and customs duties, tax revenues from all tax heads have exceeded forecasts.

The largest overshooting occurred in the CGT, stamp duty and non-PAYE

income tax heads (CAT and customs also recorded significant overshooting but

as outlined earlier, these are relatively insignificant in terms of overall tax

revenue).

Table 4.1: Individual Tax Head Percentage Errors (Unadjusted) 1999 – 2006

ME RMSE

Income Tax 1.9 5.4

- PAYE -1.5 5.7

- non PAYE 12.9 17.2

VAT 0.5 4.7

Corporation Tax 0.5 8.1

Excise Duty -1.6 6.8

Stamp Duty 12.6 17.5

CGT 23.3 33.5

CAT 15.3 22.0

Customs Duty -2.5 21.2

Total 2.5 6.1

Total excluding Capital12 Taxes 0.6 4.3

4.11 Ireland is not alone in having such large forecasting errors. For example, in the

case of Canada13, in seven of the eight years from 1996-97 to 2003-04, total

revenues came in ahead of projections, significantly so in the years 1997-98,

1999-00 and 2000-01. The errors – surplus tax revenue as a percentage of actual

tax revenue – in each of those years was 10.1 per cent, 5.4 per cent and 9.3 per

cent respectively and of the main components of total revenue in Canada, both

12 Assuming zero forecast error for CGT, CAT and stamp duty i.e. receipts from these tax heads were on target. 13 Review of Canadian Federal Fiscal Forecasting – Processes and Systems, June 2005

35

personal income tax and corporate tax revenues came in ahead of target in six of

the eight years.

Adjusted Analysis

4.12 The raw data presented above do not take into account extraneous factors which

can impact on tax collection and contribute ex post to a divergence between

forecast and outturn. Over the period concerned, such one-off factors have, in

general, tended to ‘surprise’ on the upside, imparting an upward bias to forecast

errors. The analysis below sets out the main identifiable one-off factors. It

should be noted, of course, that the classification of some factors as one-offs can

be somewhat arbitrary.

4.13 It is worth noting also that there have been significant payment date changes for

a number of tax heads, which have also impacted on tax revenues in recent

years.

4.14 On the basis of best judgement, table 4.2 sets out the main one-off factors

which, when excluded, enable a more accurate like-for-like comparison between

forecast revenue and outturn over the period 2000 – 2006. There were no major

one-off items in 1999.

36

Table 4.2: Total One-off Adjustments One-Off Factors €m

Income tax

Unadjusted

Outturn

€m PAYE Non-

PAYE CT VAT CAT

Stamp

Duty CGT Customs

Adjusted

Outturn

€m

2000 27,072 216 26,856

2001 27,925 227 27,698

2002 29,294 -133 69 38 29,320

2003 32,103 238 63 28 15 31,759

2004 35,581 523 98 21 11 7 76 34,845

2005 39,254 313 -196 16 38 33 39,050

2006 45,539 -66 -37 63 22 52 45,505

*A positive one-off figure in table 4.2 indicates an unexpected or one-off yield which is subtracted

from the unadjusted outturn to get the adjusted outturn figure. Likewise a negative (-) figure indicates

an unexpected loss which is added back to the unadjusted outturn to get the adjusted outturn figure.

4.15 It should be noted that no allowance is made in the analysis below for ongoing

improvements in compliance or for stronger than expected take-up of various

legal tax shelters (such as in property) that pertained over the period. These

factors are difficult to quantify ex ante and have undoubtedly had an impact on

the revenue outturn over the period in question (ceteris paribus contributing to

overshooting in the case of improved compliance and to undershooting in the

case of increased take-up of legitimate tax shelters).

- Aggregate Tax Revenue

4.16 Chart 4.3 below shows the forecast and outturn once the identifiable one-off

factors are taken into account. The mean error declines to 1.9 per cent while the

RMSE declines to 5.9 per cent of actual tax revenue, suggesting some marginal

improvement in the forecasting accuracy.

37

Chart 4.3: Forecast Compared with Adjusted Outturn - % of Outturn

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

1999 2000 2001 2002 2003 2004 2005 2006

average

4.17 Chart 4.4 combines charts 4.1 and 4.3 so that the improvement in the RMSE,

arising from the factoring in of the adjusted outturn figures, can be easily seen.

The blue bars represent the unadjusted outturns while the red bars represent the

adjusted outturns. 2001 is the only year in which adjusting for one-off factors

worsens the RMSE.

Chart 4.4: Improvement in RMSE with Adjusted Outturn

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

1999 2000 2001 2002 2003 2004 2005 2006

unadjustedaverage

adjusted average

Blue = Unadjusted Red = Adjusted

38

- Disaggregate Tax Revenue

4.18 The forecasting performance of each of the individual tax heads on the adjusted

basis is illustrated in table 4.3. The results show that even allowing for one-off

factors, there was still overshooting for most tax heads. Of the larger tax heads,

the most noticeable improvement (i.e. lowering of the RMSE) occurs in non-

PAYE income tax, owing to the exclusion of special investigations receipts.

Table 4.3: Individual Tax Head Percentage Errors (Adjusted Outturn) 1999 – 2006

ME RMSE

Income Tax 0.2 5.2

- PAYE -1.2 5.2

- non PAYE 4.4 15.5

VAT 0.4 4.6

Corporation Tax 0.8 8.1

Excise Duty -1.6 6.8

Stamp Duty 11.7 17.1

CGT 22.8 32.9

CAT 9.9 16.9

Customs Duty -4.1 19.8

Total 1.9 5.9

Total excluding Capital Taxes 0.0 4.3

4.19 In summary, there has been a significant overshooting of revenue vis-à-vis

forecasts over the period 1999 – 2006. On an unadjusted basis, the aggregate

forecasting error as measured by the RMSE was 6.1%. This period has seen a

substantial number of exceptional factors which have impacted on tax revenue.

Controlling for these factors – which itself is subject to considerable uncertainty

– results in a slight improvement in the overall forecasting accuracy, with the

RMSE declining to 5.9%. Other factors, such as improved compliance, would

also appear to have had an impact on revenue but these are difficult to quantify.

Chart 1 in Appendix 2 provides details of the composition of the forecast error

on this adjusted outturn basis.

4.20 The 1998 report of the TFMRG concluded that the main reason for the

divergence of the actual tax revenue outturns from the Budget day forecasts was

39

the stronger than expected economic performance. Given the continued strength

of the economy in the years since the 1998 report, controlling for economic

factors was viewed as the next step in attempting to explain the divergence of

tax revenues from forecast in recent years.

40

5. Controlling for Economic Forecasting Errors

5.1 Projections for key macro-economic variables are a key input into the tax

forecasting process (VAT is a function of the nominal growth of consumption;

income tax is a function of employment and earnings growth, etc). Therefore,

economic forecasting errors will have a knock-on impact on the tax forecasts.

5.2 In order to analyse the accuracy of tax forecasting, therefore, it is important to

isolate the impact of economic forecasting errors. This is done through

producing retrospective tax forecasts by application of the most up-to-date

macroeconomic data.14

5.3 A priori it is to be expected that these revised tax forecasts would be closer to

the adjusted outturns for each of the tax heads than the original Budget day

forecasts, i.e. the gap between forecast and outturn would be narrowed and a

proportion of the forecast error could be explained.

5.4 The reasons underlying economic forecasting error, can in broad terms, be

categorised under the following headings:

Changes in Key Exogenous Variables

Economic developments in Ireland are heavily dependent on developments

elsewhere in the global economy (particularly on developments in the OECD

area). Thus, in preparing national economic forecasts key assumptions are made

in relation to key external developments, such as economic growth and trade in

our major trading partners. In Ireland, these assumptions are based on the

forecasts of various international institutions such as the European Commission,

the OECD and the IMF. In framing the Budget forecasts, the assumptions of the

European Commission are particularly important. In these circumstances,

forecasting errors in key exogenous variables will generate errors in the

domestic economic forecasts. As Ireland has become more globally integrated

in recent years, these exogenous variables have become relatively more

important in explaining growth developments in Ireland.

14 It should be noted that further revisions to the currently available economic data are possible.

41

Domestic Policy Assumptions

In Ireland, the Department’s economic forecasts are underpinned by the

conventional no policy change assumptions in relation to a broad range of

economic and social policies. To the extent that actual policies diverge from the

no policy change benchmark, the divergence in the national forecast will be

greater.

Model Error

Medium-term economic forecasting requires assumptions to be made regarding

the economy’s estimated trend or potential growth rate. In other words, once

short-term demand-side fluctuations evaporate, an economy is assumed to grow

in line with its potential, which in turn is determined by assumed increases in the

factors of production together with assumptions regarding the efficiency with

which these factors are used in the production process (total factor productivity).

In these circumstances, an important source of the forecast error relates to

assumptions regarding the economy’s trend or potential rate of growth which

have been incorrect. In an Irish context, there is considerably uncertainty

regarding the potential growth rate of the economy, mainly related to the

openness of the economy together with the extent of structural change that has

occurred over the last decade or so.

Economic Shocks

Economic shocks – both internally and externally generated – can affect the

forecasting performance. Given the size of the Irish economy, together with

fairly concentrated sectoral economic activity (somewhat inevitable for a small

economy), shocks can have a significant impact on overall activity. For

example, the global ICT shock in 2000/2001 had a large unforeseen impact on

the economic performance of the Irish economy over this period, with growth in

2001 being 3.0 percentage points below that forecast in the December 2000

Budget.

Data Revisions

Very often economic forecasts are based on preliminary estimates of macro-

economic variables which are subsequently subject to – in some cases –

significant revisions.

42

5.5 Budget 2006 presented a review of the track record of the Department of

Finance’s Budget economic forecasts against those of other forecasting

agencies. In late 2005 both the IMF and the ESRI15 concluded that all

forecasters of the Irish economy have, particularly in the 1990’s, consistently

underestimated economic growth, mainly due to upside growth surprises. This

was most clearly the case for external demand, which is particularly difficult to

forecast in a globally-integrated economy like Ireland.

Table 5.1 shows the average divergence between the outturn as measured by the

CSO and the annual forecasts for the 1997 to 2004 period produced by a number

of agencies, including the Department of Finance. The results, as measured by

the error level across the different agencies, are very similar. The spread may

well be explained, at least in part, by the timing of publication and the

availability of up-to-date information. Information availability constrains all

forecasts, particularly as short-term forecasting does not readily lend itself to the

application of econometric or model-based analysis. The main conclusion from

this analysis is that performance of the official Department of Finance forecasts

published on Budget day compare well against those of other forecasting

institutions.

Table 5.1 – Economic Forecast Performance 1997-2004

Forecaster Publication Divergence from Outturn16

Central Bank

ESRI

EU Commission

IMF

OECD

Winter Bulletin

Winter QEC

Autumn Forecast

WEO – Sept/Oct

Outlook – Nov/Dec

2.66%

2.92%

2.57%

2.80%

2.62%

Dept. of Finance Budget 2.59%

Methodology

5.6 In order to produce revised tax forecasts for the period 1999-2006, based on the

most up-to-date macroeconomic data available; the following approach was

taken for each of the individual tax heads. 15 The Quarterly Economic Commentary Forecasting Record 1994 to 2004, QEC Autumn 2005. Ireland: Selected Issues, IMF Country Report No. 05/370, October 2005 16 Divergence from the CSO outturn is measured using Root Mean Squared Forecast Error.

43

5.7 When producing the Budget year tax forecasts in December of each year, the

base year outturn – essentially the starting point for the forecast – is not known

and must therefore be estimated. In producing the revised tax forecasts, the

actual base year outturn is used as the starting point.

5.8 The Budget year tax forecasts are based on projections of macroeconomic

activity or what are known as “tax macros” for the forthcoming year. Economic

data can be subject to regular revision for a number of years after the end of the

forecast year and the revised tax forecasts are based on the most recently

available estimates of the actual outturns for these tax macros. A recent Central

Bank technical paper17 shows how initial estimates of GDP and its components

can differ quite significantly from final estimates. The paper found that the final

revision to the growth rate of GDP was 1.5 per cent, almost 20 per cent of

average GDP growth over the sample. The average revision was positive

indicating that initial estimates of GDP tend to be too low. Such revisions create

problems for economic forecasting purposes and hence for tax forecasting

purposes.

5.9 The actual base year outturns and the revised tax macros were then inserted into

the Budget tax forecasting spreadsheets for each of the years to produce revised

tax forecasts.

5.10 The actual base year outturns and the revised tax macros were the only variables

that were updated in the context of producing these revised tax forecasts. Other

issues which may have had an impact on the accuracy of the Budget day tax

forecasts such as the employment and elasticity factors for income tax and the

cost of the Budget day tax packages were not updated. This is because the aim

of the process is simply to control for the base year outturn and the latest

available macroeconomic data to see the impact this would have on the tax

forecasts.

Results

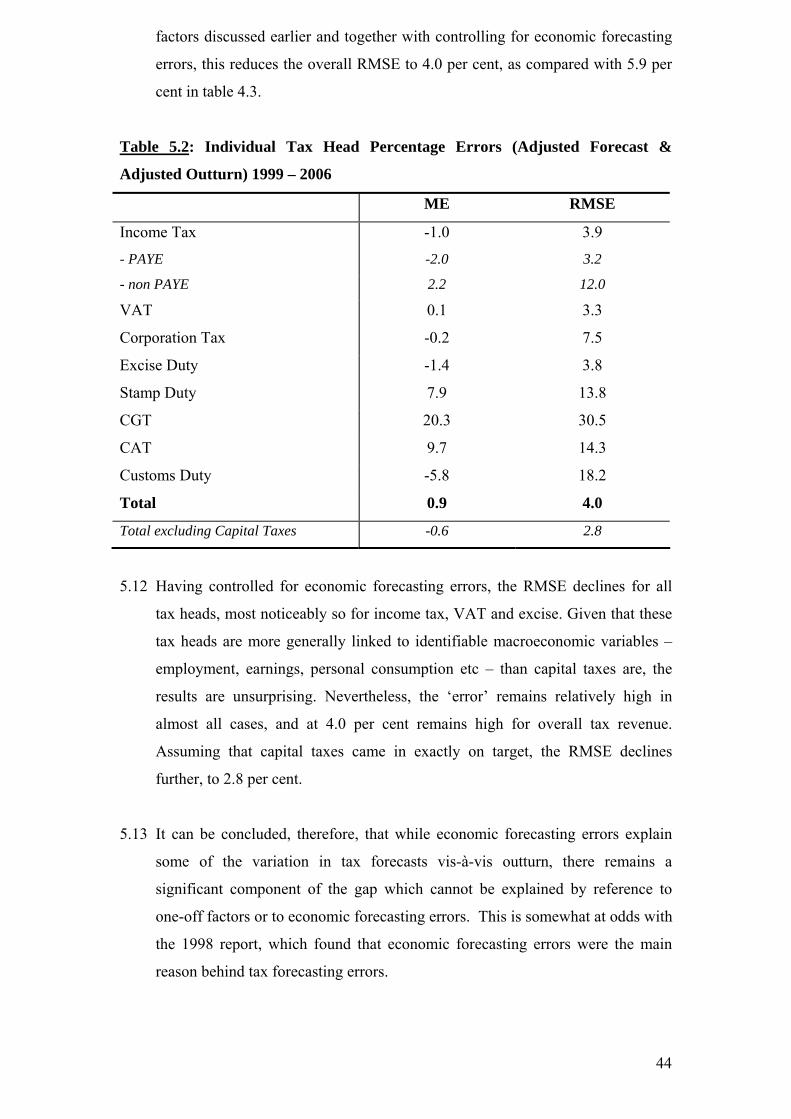

5.11 The results are set out in the table 5.2, which shows the RMSE for each tax head

and for overall tax revenue. These figures include adjustments for once-off

17 Research Technical Paper 10/RT/06 by Colin Bermingham – see Appendix 2 for summary of this paper.

44

factors discussed earlier and together with controlling for economic forecasting

errors, this reduces the overall RMSE to 4.0 per cent, as compared with 5.9 per

cent in table 4.3.

Table 5.2: Individual Tax Head Percentage Errors (Adjusted Forecast &

Adjusted Outturn) 1999 – 2006

ME RMSE

Income Tax -1.0 3.9

- PAYE -2.0 3.2

- non PAYE 2.2 12.0

VAT 0.1 3.3

Corporation Tax -0.2 7.5

Excise Duty -1.4 3.8

Stamp Duty 7.9 13.8

CGT 20.3 30.5

CAT 9.7 14.3

Customs Duty -5.8 18.2

Total 0.9 4.0

Total excluding Capital Taxes -0.6 2.8

5.12 Having controlled for economic forecasting errors, the RMSE declines for all

tax heads, most noticeably so for income tax, VAT and excise. Given that these

tax heads are more generally linked to identifiable macroeconomic variables –

employment, earnings, personal consumption etc – than capital taxes are, the

results are unsurprising. Nevertheless, the ‘error’ remains relatively high in

almost all cases, and at 4.0 per cent remains high for overall tax revenue.

Assuming that capital taxes came in exactly on target, the RMSE declines

further, to 2.8 per cent.

5.13 It can be concluded, therefore, that while economic forecasting errors explain

some of the variation in tax forecasts vis-à-vis outturn, there remains a

significant component of the gap which cannot be explained by reference to

one-off factors or to economic forecasting errors. This is somewhat at odds with

the 1998 report, which found that economic forecasting errors were the main

reason behind tax forecasting errors.

45

5.14 Of the main tax heads, the largest errors – in RMSE terms – are to be found in

CGT and stamp duty. Even after controlling for one-off factors and stronger

than expected economic performance, the respective RMSEs are 30.5 per cent

and 13.8 per cent. In the previous report of the TFMRG, which covered the

period from the late 1980s to 1997, the performance of CGT and stamp duty was

not analysed to any great extent, given the share of total tax revenue each

accounted for and the fact that any divergence from accuracy in the forecasting

of these tax heads was minor in overall terms. In 1999, for example, these two

tax heads combined accounted for less than 6 per cent of total tax revenue. In

2006 that figure was 15 per cent. One possible reason for the larger errors in

these particular tax heads is the performance of the property market in recent

years and the large increase in tax revenues attributable to that particular sector

of economic activity. Chart 5.1 below shows the composition of the forecast

error on this adjusted forecast and adjusted outturn basis. The chart highlights

the fact that capital taxes account for a large and rising (in recent years)

proportion of the total forecasting error.

Chart 5.1: Composition of Error – Adjusted Forecast & Adjusted Outturn

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

1999 2000 2001 2002 2003 2004 2005 2006

Income Tax VAT Corporation Tax Excise Capital Taxes Customs Total

5.15 It is worth noting that the Irish economy has gone through a period of significant

structural change in the last decade. Up until the early years of this decade,

economic growth was characterised by large increases in manufacturing output

46

and employment as well as by a large contribution from net exports. However,