131

REPORT ON ICT INDUSTRY IN INDIA

REPORT ON

ICT INDUSTRY IN INDIA

SECTION A: ICT SECTOR ANALYSIS PART 1 SECTOR ANALYSIS FOR IT & TELECOM

• 1.1 Introduction • 1.2 Market overview • 1.3 Demand dynamics • 1.4 Range of service offerings • 1.5 Sourcing models • 1.6 The India advantage

• 1.6.1 Vast Access to Skill base: • 1.6.2 Strong quality orientation • 1.6.3 Availability of high quality infrastructure • 1.6.4 Cost advantage • 1.6.5 Enabling policy environment • 1.6.6 Mature industry eco-system • 1.6.7 Availability of private equity • 1.6.8 Commitment of address security concerns • 1.6.8 Prominent IT services & ITES locations within India

• 1.7 The Indian IT services & ITES industry- The road ahead • 1.8 IT for development • 1.9 R&D services & software products • 1.10 Offshore product development • 1.11 Embedded software & systems • 1.12 Offshore product development exports • 1.13 Global product engineering market • 1.14 Telecommunications

• 1.14.1 Background • 1.14.2 Organizational structure in telecommunication

• 1.15 Capacities, capabilities & Trends in the telecommunication sector • 1.15.1 Telecom equipment manufacturing sector • 1.15.2 Switching • 1.15.3 Transmission • 1.15.4 Terminal Equipment • 1.15.5 Research & Development

• 1.16 Noteworthy development in policies & activities in ICT field new telecom policy, 1999

• 1.17 C-Dot Technologies • 1.18 Broadband integrated services digital network switching platform • 1.19 Intelligent network solution • 1.20 Network management system • 1.21 C-Dots billing & operations support system

• 1.22 Rural wireless access & broadband solution • 1.23 Another R&D laboratory by Telecordia technologies • 1.24 Other supporting technologies & R&D • 1.25 Optical communication • 1.26 Electronics material

PART 2 OPPORTUNITIES • 2.1 Opportunities in the Indian IT services & ITES industry

• 2.1.1 IT services • 2.1.2 Opportunity segments within IT services

• 2.2 Customer Interaction Services • 2.3 Transaction Processing • 2.4 Content development • 2.5 Knowledge services • 2.6 Engineering design • 2.7 Key emerging trends impacting the Indian IT services & ITES industry

• 2.7.1 Demand related • 2.7.2 Supply related

• 2.8 Future Opportunities • 2.8.1 Outsourcing or off shoring product development activities • 2.8.2 Embedded software • 2.8.3 Shrink wrapped product development

• 2.9 Some major MNC’s undertaking R&D in India • 2.9.1 Siemens • 2.9.2 SAI • 2.9.3 Schneider • 2.9.4 Texas Instruments • 2.9.5 Sun Microsystems & Cadence design • 2.9.6 Intel • 2.9.7 Samsung • 2.9.8 Motorola • 2.9.9 Philips • 2.9.10 Delphi • 2.9.11 Daimler • 2.9.12 Bosch

• 2.10 Emerging Areas • 2.11 Hardware: Current status & key opportunities • 2.12 Performance in the Xth plan • 2.13 Technology status • 2.14 Future trends • 2.15 Status of investments & investment needed to meet the targets • 2.16 Thrust areas for optical development & opportunities • 2.17 Thrust areas in electronic materials for research & opportunities

• 2.18 Areas of opportunity in the Telecom sector • 2.19 Opportunities for investment in Telecom PART 3 SELECT CASE STUDIES • 3.1 GE • 3.2 American Express • 3.3 Citigroup • 3.4 EDS • 3.5 Cisco • 3.6 Intel • 3.7 Samsung PART 4 OBSTACLES • 4.1 Introduction • 4.2 Types of obstacles

• 4.21 High investment • 4.2.2 Absence of focused product shops in India • 4.2.3 Distance from clients • 4.2.4 Poor past records

PART 5 PARAMETERS OF COMPETITION • 5.1 Leading Indian software product companies • 5.2 Key success factors

• 5.2.1 Skilled manpower • 5.2.2 Research & Development • 5.2.3 Domain Enterprise • 5.2.4 Sales & Marketing • 5.2.5 Business Predictability

• 5.3 Trends PART 6 COMMUNICATION AND PROMOTION PART 7 PENETRATIONS IN THE MARKET • 7.1 A typical sourcing programme- risks,roadmap & timelines • 7.2 Entry strategies for IT & Telecom companies • 7.3 Forms of Enterprise

• 7.3.1 Introduction • 7.4 Major types of corporation

• 7.4.1 Private corporation • 7.4.2 Public corporation • 7.4.3 Foreign corporation

• 7.5 Structures typically used by foreign investors

• 7.5.1 Subsidiary companies • 7.5.2 Branch office • 7.5.3 Liason office • 7.5.4 Project office • 7.5.5 Joint Venture • 7.5.6 Appointing agent or distributor • 7.5.7 Third party arrangement for maintenance & servicing of products • 7.5.8 Franchising • 7.5.9 Direct Selling

• 7.6 Regulations for presence in India for a foreign company PART 8 PRECAUTIONS TO BE TAKEN BY ITALIAN EXPORTERS SECTION B: GENERAL OVERVIEW PART 9 INFORMATION SOURCES PART 10 IMPORT LEGISLATION • 10.1 How to start import • 10.2 Principal law & import export policy • 10.3 Mode of pricing & INCO terms • 10.4 Ex-work • 10.5 Free on rail/Free on truck • 10.6 Free alongside ship • 10.7 Free on board • 10.8 Cost & Freight • 10.9 Cost insurance freight • 10.10 Customs clearance services for import consignments • 10.11 Customs Duty PART 11 BANKING SYSTEM & EXCHANGE POLICIES • 11.1 Reserve Bank of India • 11.2 Types of institutions

• 11.2.1 Public sector banks • 11.2.2 Private sector banks • 11.2.3 Foreign banks • 11.2.4 Recent developments

• 11.3 Currency • 11.4 Foreign exchange controls

• 10.4.1 Current account transactions

• 10.4.2 Capital account transactions

• 11.5 Foreign Exchange Management Act • 11.6 General Permission under FEMA PART 12 METHODS OF PAYMENT • 12.1 Payment against imports • 12.2 LC Vs Bank guarantee • 12.3 LC • 12.4 Parties to a LC

• 12.4.1 Beneficiary • 12.4.2 Issuing bank • 12.4.3 Confirming bank

• 12.5 Mode of payment • 12.6 Postal Imports PART 12 LOCAL JUDICIAL SYSTEM PART 13 NAMES OF EVENTUAL PARTNERS PART 14 RISK ANALYSIS • 14.1 Country • 14.2 Non-collection of goods & Non-payment PART 15 LEGISLATION ON INTELLECTUAL PROPERTY PART 16 LABELLING & PACKAGING RULES PART 17 MAIN EXHIBITIONS PART 18 LOGISTICS • 18.1 Overview • 18.2 Metro • 18.3 Buses • 18.4 Highways • 18.5 Waterways • 18.6 Pipelines • 18.7 Ports & harbours • 18.8 Merchant marine • 18.9 Air travel • 18.10 Airports & seaports • 18.11 Airport

EXECUTIVE SUMMARY

The idea of India is gradually changing as number of countries showing interest to invest in India is increasing. According to an AT Kearney’s FDI Confidence index, India has displaced the US as the second most favored destination in the world after China. India attracted FDI at US$7.96 billion during the first half of FY06, as against US$2.38 billion during the same period in FY05, more than 3 times growth. India’s economy is predicted to be growing over 8% in 2006 and with a billion plus population India has its wings of varied culture and business/industry scenario across the country. At the backdrop of such characteristics prospective investors in any foreign countries will be interested to know ‘Doing business in India in wine industry’. The study aimed at highlighting macro-economic indicators of the country with its risk analysis in terms of currency, non-collection of goods and non-payment. It also discusses obstacles that the prospective investors may face and appropriate marketing strategies that they should adopt to ensure smooth landing in the country which requires a good understanding of its geographies and associated culture and business environment, least but not the last the market dynamics. Approach taken for this study was to collect information/data from various authentic sources like industry associations, trade agencies and respective ministries wherever applicable. As far as policy/regulations are concerned respective ministries’ reports and guidelines have been referred and an attempt has been made to explain them appropriately as relevant they may be. Salient points which are key findings in this report are given below.

Challenges in the market is still to find the right partner, knowledgeable about local market and procedural issues for foreign industries investment in India and can formulate the right strategies with solid foundation for setting up manufacturing base as JVs as the FDI policy may stipulate in respective sectors

Tariffs (although tariff structure has been reduced considerably since economic reforms but issues still remain in some specific sectors) and poor infrastructure still poses a serious challenge to FDI.

In addition, heavily bureaucratic investment processes, poor IPR enforcement,

government inefficiency, and corruption have also discouraged foreign investors.

Winning strategy overcoming the market entry barriers for setting up an establishment- a solid regional plan analyzing the local market demand and economics that work out to be feasible in producing in India and exporting to other countries in the world leveraging conducive economic factors that otherwise become an impediment in future growth.

While marketing products distribution strategy can really make the difference;

however merit has to be given after due diligence is done and a meticulous plan should be in place. Small distributors can really make a drastic improvement in sales growth where flexible marketing strategies play an important role.

A joint venture company is generally formed under the Indian Companies Act of

1956 and is jointly owned by an Indian company and a foreign company. This type of arrangement is quite common because India encourages foreign collaborations to facilitate capital investments, import of capital goods and transfer of technology.

All industrial undertakings are exempt from obtaining an industrial license to

manufacture, except for (i) industries reserved for the Public Sector, (ii) industries retained under compulsory licensing, (iii) items of manufacture reserved for the small scale sector and (iv) if the proposal attracts location restriction.

Being a buyer’s market from seller’s market promotion of products matters much. The key to gaining rural market share is increased brand awareness, complemented by a wide distribution network. Rural markets are best covered by mass media - India’s vast geographical expanse and poor infrastructure pose serious challenge for communication and hence emphasis must be given in communication problems to be really effective in selling to rural market.

India is still not holding its laws high for protecting copyright issues. As a result cases of counterfeiting and violation of copyright act happens and probably judicial system is still not being able to curb the menace. Adjudication of cases is extremely slow.

Logistics play an important role in distributing products to all corners of the country. Due to its vast territory challenges in implementing a smooth supply chain model is really challenging and hence outsourcing to third parties is very common and an useful and effective strategy to reach market place just in time.

SECTION A: ICT SECTOR ANALYSIS

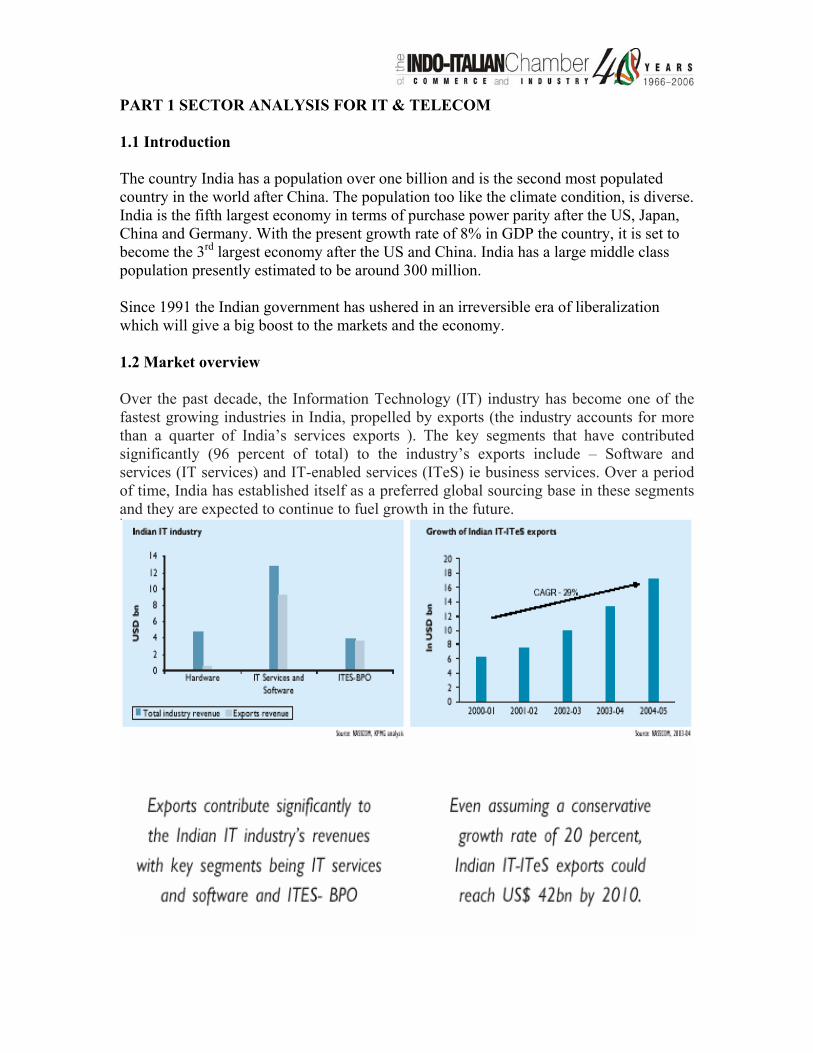

PART 1 SECTOR ANALYSIS FOR IT & TELECOM 1.1 Introduction The country India has a population over one billion and is the second most populated country in the world after China. The population too like the climate condition, is diverse. India is the fifth largest economy in terms of purchase power parity after the US, Japan, China and Germany. With the present growth rate of 8% in GDP the country, it is set to become the 3rd largest economy after the US and China. India has a large middle class population presently estimated to be around 300 million. Since 1991 the Indian government has ushered in an irreversible era of liberalization which will give a big boost to the markets and the economy. 1.2 Market overview Over the past decade, the Information Technology (IT) industry has become one of the fastest growing industries in India, propelled by exports (the industry accounts for more than a quarter of India’s services exports ). The key segments that have contributed significantly (96 percent of total) to the industry’s exports include – Software and services (IT services) and IT-enabled services (ITeS) ie business services. Over a period of time, India has established itself as a preferred global sourcing base in these segments and they are expected to continue to fuel growth in the future.

These segments have been evolving over the years into a sophisticated model of operations. Indian IT and ITES companies have created global delivery models (onsite-near shore-offshore), entered into long term engagements with customers, expanded their portfolio of services offerings, built scale, extended service propositions beyond cost savings to quality and innovation, evolved their pricing models and have tried to find sustainable solutions to various issues such as risk management, human capital attraction and retention and cost management. 1.3 Demand dynamics A key demand driver for the Indian IT services and ITeS industry has been the changing global business landscape which has exerted performance pressures on multinational enterprises.

While companies initially sourced from the Indian IT and ITeS industry for cost, quality and enhanced competitiveness have induced them to continue and expand. Some companies have also viewed sourcing differently (beyond cost and quality) and achieved non-traditional benefits of sourcing from India.

1.4 Range of service offerings The range of services offered by the Indian IT services and ITeS industry to these global corporations range from simple tasks to increasingly complex activities and span across the entire value chain of a typical organisation

Source: News reports, IBEF study of Fortune 500 companies inIndia, IBEF study of successful US and UK companies in India: Illustrative and not exhaustive

1.5 Sourcing models A wide range of sourcing models have evolved for sourcing IT and ITeS services from India based on the required capabilities as well as risk profiles.

There is an increasing trend towards a global delivery model (higher proportion of offshore in the onsite – near shore – offshore mix) as well as a preference for captives and co-sourcing arrangements, though mature captives are gradually tending towards becoming third party service providers.

1.6 The India advantage Various country comparison studies have established the attractiveness of the Indian IT services and ITeS industry.

The key attributes that have enabled India to establish itself as a preferred sourcing base include: 1.6.1 Vast Access to Skill base: • Large pool of resources for IT and ITeS operations - 14 million graduates, 1 million technical resources, one of the largest English speaking manpower in the world. • Availability of quality delivery management talent from international banks and consulting firms. In the future, while the increasing demand for resources may put pressure on the resource base, initiatives are currently underway to enhance the supply of quality human capital in the country.

1.6.2 Strong quality orientation • ISO9001, COPC, 6 sigma are some of the established quality initiatives. • 80 out of the world’s 117 SEI CMM Level 5 companies are from India. 1.6.3 Availability of high quality infrastructure • Concerted efforts to provide dedicated, international quality, cost effective real estate at software parks, Special Economic Zones (SEZ) and knowledge sector industrial estates. • Availability of high quality international and national dedicated telecom infrastructure with high level of redundancies insulating centres from Public Switched Telephone Network (PSTN) quality. • Availability of multiple levels of backups providing insulation from public system issues, if any. 1.6.4 Cost advantage The cost impact of sourcing from the Indian IT and ITeS industry can be significant due to the lower wages and lower cost of living.

While the increasing demand for resources is gradually adding pressure on labour costs, companies within the industry are attempting to sustain cost competitiveness through appropriate location choices and revamped human resource management practices.

1.6.5 Enabling policy environment The Government of India is taking proactive measures to encourage investments in this sector. Significant measures and incentives include a liberalised FDI regime, single-window clearance facility, income tax holiday and customs duty exemptions. State governments too are demonstrating a proactive approach towards attracting and facilitating investments and are providing support for the development of specialised infrastructure, focusing on development of a larger base of cities/towns to meet the needs of the industry and undertaking measures to continually enhance the supply and quality of manpower. 1.6.6 Mature industry eco-system The support infrastructure for the Indian IT and ITeS industry which includes specialised firms for functions such as recruitment, training, property management, security, fleet management, book-keeping and payroll as well as industry associations has evolved over the years. 1.6.7 Availability of private equity Presence of a mature private equity industry to support local entrepreneurs (organisations such as Warburg Pincus, General Atlantic, CDC). 1.6.8 Commitment to address security concerns Indian companies as well as the government have been active in adhering to international security standards such as ISO 17799, BS7799, COBIT and ITSM. The required legal framework has been laid down by the government and a revamp of the country’s Information Technology Act, 2000 is expected in the near future. The revised legal framework is likely to include provisions against a new range of computer crimes to cover areas like privacy, information protection and harming computer systems through viruses.

1.6.9 Prominent IT services and ITeS locations within India A majority of IT / ITeS activity in India is concentrated in seven cities /clusters in India. With concerted development efforts of a wider base of cities / towns, the geographical spread of IT / ITeS activity is gradually expanding to cover cities such as Ahmedabad, Jaipur, Coimbatore, Kochi, Trivandrum, Chandigarh, Mysore, Mangalore, Madurai and Bhubhaneswar.

Various companies have chosen to locate their operations in one or more of these seven clusters based on parameters such as: • Leveraging local experience and assets • Spreading to reach right skills at right costs • Business continuity requirements.

1.7 The Indian IT services and ITeS Industry – The road ahead The Indian IT services and ITeS industry is poised for rapid growth over the next few years by offering a wider services portfolio, catering to a larger set of industry verticals and evolving / adapting to suit the service delivery preferences of global customers. Key challenges that the industry faces include the need to sustain competitiveness in the face of alternative emerging locations and enhancing supply of quality human capital to cater to increasing demand. Efforts in this direction are already underway and continuous emphasis on the same is imperative to ensure that the industry’s future growth is undeterred.

1.8 IT for development The contribution of IT in the development of the rural areas is critical and efforts are underway to enhance the awareness and penetration of IT in rural areas. Attempts to increase the depth of IT services in rural areas range from small initiatives like single computer information kiosks to the “Wired Village Project” where dozens of villages are provided high speed internet connectivity. The government as well as the private sector has been actively involved in the dispersion of IT and IT based services to rural India. Some models include: • ITC Limited has set up an initiative called “e-chaupal” which aims at facilitating productivity enhancement by offering services and information on subjects like weather, market prices, scientific farm practices etc. The venture has proved to be successful and the number of e-chaupals have risen to 2,700 which cover a population of 1.2 million in five states. ITC plans to expand to 20,000 e-chaupals in the next few years. • TARAhaat Information and Marketing Services Development Alternatives (Technology Action for Rural Advancements), a wellknown Indian NGO, is focused on using technology for providing sustainable livelihood in villages. The strategy deployed is to evolve a commercially viable IT-based enterprise and to deliver public benefits by satisfying private needs. The services provided are education, egovernance, insurance, mini-credit financing, rolling out development packages made by NGOs and e-communications. • A private Indian IT company, Aksh Broadband, has executed the Gramdoot programme in Jaipur district (in the state of Rajasthan) in western India. The model is based on fibre optic technology laid through the district to carry voice, data and graphics. The optic fibre cable runs for 3000 kms and benefits a population of 6 million people. All government records are online - from land records to revenue collected – and health and education services are provided real time in Jaipur district. It is in fact the first time anywhere in the world that land deeds are offered to the villager in real time. To help sustain this model commercially, a small charge is administered for the services provided. The model is cost effective, has rapid deployability, and has demonstrated ease of operation and maintenance. • The “Param” project by Ogilvy and Mather aims to improve rural connectivity in backward areas. • “Drishtee” has focussed on provision of e-governance facilities and information services to the rural community. • Attempts to impart IT education to students from rural areas are pursued by Microsoft and the Azim Premji foundation. Some players in the Indian IT and ITeS industry have also included rural India in their capability sourcing models. Select examples include:

• Lason India, an end to end outsourcing company is promoting village BPO’s where functions like data entry and data processing are carried out from rural areas. • Datamation group is a Public Private Partnership where NGO’s train individuals from under-privileged sections of the society and employ them in BPO’s owned and run by them. Source: The source of this report is IBEF and NASSCOM 1.9 R&D services and software products Indian R&D services and software product exports, though at a nascent stage, is expected to grow rapidly (growth forecasts are US$ 8-11 bn by 2008-10: Source – NASSCOM). The key opportunity areas within R&D services and software products include embedded software and systems and offshore product development. A number of large multinational corporations source a part of their embedded system requirements from India either through captive design centres or through vendors. Some of these companies include Samsung, Texas Instruments, Delphi, STMicroelectronics, Motorola, Intel, Analog Devices and National Semiconductor (Illustrative and not exhaustive; Source- NASSCOM). Apart from multinational corporations sourcing requirements from India, there are over a 100 Indian companies operating in the embedded software solutions domain. Also, in addition to the export of products developed by the offshore units on behalf of MNCs, a few Indian vendors (e.g. Infosys, I-Flex Solutions) have successfully expanded their revenue streams to include their own software products. 1.10 Offshore Product Development India is one of the key centres for outsourcing IT services for global IT vendors. Some Indian companies have leveraged the India advantage and gone a step further to set up centres for product development and R&D services. These centres perform product development activities for ISVs. ISVs have the following benefits in outsourcing product development functions to India: • Match lower return activities with lower cost resources • Refocus the in-house team on more higher value-adding activities • Rapidly enhance the product's relevance in a wider market. For Instance, Wipro partners with Ericsson for product development. According to the deal signed in 2002, Wipro will take over the product development life cycle activities performed at three Ericsson centres in India. The deal will involve Wipro taking up assets, including personnel, at Ericsson’s R&D centres in Bangalore, Hyderabad and New Delhi.

Indian companies outsourcing product development activities include large players such as Wipro, TCS, Infosys, etc., and small niche players with domain expertise in particular verticals, such as Sasken (telecom domain), Mindtree (IP creation), etc. The major clients for this industry have changed over the last couple of years. In 2001, Nortel, Lucent and Cisco were the largest clients for Indian companies. While, the main clients in 2002 were Cisco and HP. Intel, Alcatel, Texas Instruments and Sony could potentially increase outsourcing to India. Apart from Indian companies, many global ISVs are also eyeing India as a location for establishing a captive centre for their R&D activities. Since the beginning of 2001, about 230 multinationals have opened offices in India. The market for outsourced R&D activities in India amounted to about US$ 800 million to US$1 billion a year in 2003, and is expected to reach US$11 billion by 2008 . Examples of major global players setting up captive centres in India include Microsoft, Oracle, IBM, Texas Instruments, Adobe, Novell, SAP, Intel, Cisco, etc. 1.2.3 Software Products (Shrink-wrapped and enterprise products) Developing software products and selling them to a mass clientele is one of the most difficult tasks in the software industry. Only a few companies in the world have succeeded in reaching a mass clientele for their products. An indicator of this is that only a dozen or more companies have succeeded in crossing the critical US$ 1 billion mark in turnover (in 2000). Pure product play requires proximity to the client in order to understand its needs, deep domain knowledge and skill-set to make specific products, and a product mind and focus on R&D activities. In context of the challenge, the disadvantages India faces in the global market are: • Distance from most key markets and customers • Lack of critical mass in necessary skill sets Some Indian companies that have achieved significant success despite these disadvantages are i-flex, Talisma, TCS, Infosys, Ramco Systems, Polaris, Nucleus Pramati Technologies, and smaller players such as Eastern Software, who have made a mark in the domestic market. 1.11 Embedded Software and Systems

The worldwide market for embedded software and systems is currently valued at USD 25 billion, and is estimated to be growing at an annual rate of 16 percent. Rapidly increasing global demand has helped Indian exports of embedded systems and software to reach USD 1.58 billion in FY 2003-04 – a growth of 44 percent over the previous fiscal. The high levels of growth in segment revenues is expected to continue as increasing levels of convergence and digitization and declining costs increase the global adoption of

electronic devices – and manufacturers are forced to seek technically superior / low cost sourcing destinations to remain competitive. Over 60 percent of the worlds leading companies, including Samsung, Texas Instruments, Delphi and Honeywell Industrial Controls, etc, source a part of their embedded system requirements from India. Further a number of large MNCs such as Texas Instruments, STMicroelectronics, Motorola, Intel, Cadence Design Synopsys, Analog Devices and National Semiconductor have set up their captive design centres in the country.

Apart from many MNCs doing R&D in India, there are over a 100 Indian companies operating in the embedded software solutions domain.

1.12 Offshore Product Development Exports

The value of offshore product development exports (includes the export of software products made by Indian companies) sourced from India is estimated to have increased from USD 560 million in FY 2002-03 to USD 710 million in FY 2003-04. Many global ISVs are eyeing India as a location for establishing captive centres for R&D activities. Since the beginning of 2001, approximately 230 multinationals have opened offices in India. The market for outsourced R&D activities in India reached USD 800 million to USD 1 billion in 2003, and is expected to reach USD 11 billion by 2008.

Offshore product development is not a new phenomenon in global IT services trade. A number of MNC product based companies have been sourcing a part of their product development activities from Indian vendors and their own India based development centres for several years. However, in most cases, the key driver for these companies was often the significant cost arbitrage opportunity offered by the India based vendors. As a result most of the work offshored to India was restricted to the lower-end activities of coding and testing. Over time, the demonstrated success of India-based development centres in delivering not only on cost, but also on quality and technological superiority has attracted an increasing level of interest in offshore product development to India.

Unlike large IT services organizations, product-centric firms are often small set-ups typically funded through the venture capital route. As a result the pressure to deliver on financial profitability metrics is very high. Offshore product development has proven to be an effective means of extracting more value out of every dollar of funding raised.

Analysts believe that, as in services, global sourcing of product development will become an integral part of most product-centric strategies over the next few years. The key drivers fuelling the growth in offshore product development include: Increasing pressures on product companies for faster time-to-market, coupled with the need to introduce new products and new technologies to expand geographic reach Economics of open source software is forcing companies to pare down development costs to remain profitable

US-based venture capitalist firms are encouraging their clients to use/investigate offshore facilities in India, and other countries such as China. India's lower costs (it generally costs around USD 2 million to develop a modest software product in India, as against USD 5 million in the US), means that venture capitalists are not risking as much money on a given start-up India’s emphasis on improving information security and IP protection In addition to the export of products developed by the offshore units (captive and third-party-service-providers (3PSPs)) on behalf of the MNCs, a few Indian vendors have successfully expanded their revenue streams beyond service revenues to include earnings from exporting their own software products. The following table provides the key details about the key software products being exported by Indian companies. Source: NASSCOM’s Strategic Review 2005 1.13 Global Product Engineering market Global Product Engineering market (USD bn) Product engineering Worldwide IT-ITES 2004 22.1 1,384.2 2005 27.3 1,479.3 2006 32.8 1,585.9 2007 38.8 1,696.8 2008 45.4 1,822.3 2009 53.0 1,963.7 Source: IDC From being a cost reduction centre, India is slowly but steadily proving its mettle as a thriving market for innovative ideas and new product development

1.14 TELECOMMUNICATIONS 1.14.1 Background The Communications sector covers the areas of Network Infrastructure, Services, Technology and Equipment production and thrust was on improving accessibility, reliability and provision of basic and value added services to address the growing needs of the urban and rural areas alike. With the deregulation and privatization of basic telephone and value added services the growth of both mobile communication and broadband services touched unprecedented levels. The FDI in the telecom services sector was increased to 74% from the earlier limit of 49% and up to 100% in telecom manufacturing sector. The policies in telecom have brought significant net gains to the country. These have led to drastic reduction in tariffs. New and innovative services with

better quality and reliability are now available to every user. Foreign Direct Investment in this sector has been significant and encouraging with more than US $ 2 billion already invested in the sector. It has led to increased user access and the country is now fully geared to deploy more affordable universal access. The country today has an independent, strong and effective telecom regulator with the relevant Act passed by Indian Parliament. A separate dispute settlement mechanism in the form of an Appellate Tribunal is also in place. India today ranks amongst the top 10 telecom networks in the world and the second largest in Asia. It has more than 150 million telephone network with a tele-density of around 13.09. Telecom sector has been declared as one of the key infrastructure sectors for the country and this will lead to rapid growth of Indian economy. The current installed base of communication network in India comprises of about 47.5 million wire line phones, 106 million cellular phones, 7.5 million Internet subscribers, 110 million TV households, 18.0 million PCs, 500,000 route kms of optical fiber network and 25,000 VSATs.

1.14.2 Organizational Structure in Telecommunication Telecommunications is now accepted as a basic infrastructure along with power and transportation for growth of the national economy. Telecommunications is also recognized as the means of accelerating the distribution of the fruits of economic growth to all regions, including remote and inaccessible areas in the country. Telecom in the modern world is expected to usher in a concept of a global economy and a single world marketplace. The Indian Telecom network must therefore become part of the modern global network providing access to anyone in the country for transporting information in the form of voice, data, or video to anywhere in the world. India's 47million fixed line telephone network is among the top ten largest networks in the world and second largest among the emerging economies after China with a growth rate of an average 20 percent for the last four years. The total number of lines added to the network over the last five years is 1.5 times the total number of lines added over the preceding five decades. The Department of Telecom (DoT) and Bharat Sanchar Nigam Limited (BSNL) are Government of India Departments under the aegis of the Ministry of Communications. The Department of Telecom (DoT) has its role in policy making, licensing, and coordination matters relating to telegraphs, telephones, wireless, data, facsimile, telematic services, and other like forms of communications. In addition, DoT is responsible for frequency management in the field of radio communication in close coordination with international bodies. It also enforces wireless regulatory measures for wireless transmission by users in the country. Bharat Sanchar Nigam Limited (BSNL) is the premier telecom service provider of

India. BSNL has a presence throughout the length and breadth of India. The main functions of BSNL include planning, engineering, installation, maintenance, management, and operation of voice and non-voice telecommunications services all over the country. MTNL is the other public sector telecom service provider in the country.

1.15 Capacities, Capabilities and Trends in the Telecommunications Sector

1.15.1 Telecom Equipment Manufacturing Sector

The Indian telecom equipment manufacturing industry manufactures a complete range of telecom equipment using state-of-the-art technologies designed specially to match the diverse terrain and climatic conditions.

Details of production and export of telecom equipment during X th Plan are as follows:-

Production Export

Rs. in crore US $ In million Rs. in crore US $ In million

2002-03 14,400 3,200 402 89.3

2003-04 14,000 3,111 250 55.5

2004-05 16,090* 3,575 400 88.8

2005-06 17,833* 3,963 1,500** 333

2006-07

(estmates)

20,000 4,444 1,800 400

* include Rs. 2,800 crore (2004-05) and 3000 (2005-06) crores for turnkey services

** include Rs. 950 (2005-06) crore for turnkey services

Imports, on the other hand had steep rise during the last 5 years, as per estimates shown

below:-

Year Import of Telecom Equipment (In Rs. Crore) US $ In million

2001-02 1, 672 372

2002-03 7,694 1,710

2003-04 20,000 4,444

2004-05 20,560 4,569

2005-06 26,166 5815

The targets for Telecom Sector will be a bench mark for the potential investors in telecom equipment manufacturing.

March 2007 In millions

March 2012 in millions

Net Addition in 11th Plan

Telephone connections Wire line 41 66 25 Mobile 154 584 430 Total 195 650 455 Broadband connections Wire line 10 50 40 Wire less 0 100 100 Total 10 135 140

Year 1 Mn

Year 2 Mn

Year 3 Mn

Year 4 Mn

Year 5 Mn

Total Mn

Wire line Telephone

3 4 5 6 7 25

Mobile Telephone 70 80 90 95 95 430 Wire line Broadband

7 7 8 9 9 40

Wire less Broadband

10 15 20 25 30 100

Demand for telecom equipment: It is expected that there will be requirement of telecom equipment worth US $ 73 billion during the 11th Plan in India.

Domestic Requirement of Telecom Products:

Year 1 Mn US$

Year 2 Mn US$

Year 3 Mn US$

Year 4 Mn US$

Year 5 Mn US$

Total Mn US$

Wire line Telephone CPE 30 40 50 60 70 250 Active Infrastructure 300 400 500 600 700 2500 Mobile Telephone Handset (New Connection)

2800 3200 3600 3800 3800 17200

Handset (Replacement) 2000 2800 3600 4800 6000 7200

Active Infrastructure 2250 2550 2850 3000 3000 13650 Wire line Broadband CPE (Modems) 2100 2100 2400 2700 2700 12000 Active Infrastructure 1400 1400 1600 1800 1800 8000 PC Card 300 450 600 750 900 3000

Active Infrastructure 500 750 1000 1250 1500 5000

Optical Fiber Cable 120 140 160 180 200 800

E-Governance initiatives

Defense - Telecom 400 400 600 800 1000 3200

Total Requirement 12200 14300 16960 19740 21670 72800

Export Targets : The Asia Pacific region offers a huge export opportunity since it is one of the fastest growing regions for telecom services. The following targets for exports of telecom equipments may be kept:

The present production level of telecom equipment is around US$ 2.8 Bn with a value addition of about US$ 0.3 Bn . India has to position itself as a 'Regional Hub' for telecom equipment manufacturing as domestic and export volumes offers a tremendous potential. Considering 75% of the Indian demand of telecom equipment & handsets worth US $ 73 billion to be met through indigenous manufacturing and an export potential of US $ 12 billion, the total telecom equipment production target could be US$ 67 billion for 11th five year plan and 40% value addition in the high value telecom equipment to be achieved at the end of 11th five year plan.

Important factors for growth of indigenous manufacturing of telecom equipments in India

1. Potential 650Mn telecom subscriber base in India by March 2012. 2. Encouraging Government policies. 3. Competent & Experienced management workforce with experience in

production management, supply chain management, working capital management, Flexible Manufacturing systems, etc., available in the country.

Year 1 Mn US$

Year 2 Mn US$

Year 3 Mn US$

Year 4 Mn US$

Year 5 Mn US$

Total Mn US$

400 1000 2000 3600 5000 12000

4. Strong auxiliary component manufacturing base like cables, electronic

packaging like cabinets, shelves, power electronics, tooling, bare PCBs up to 8 layers, etc.

5. Skilled & trained shop floor workforce for electronics circuit assembly, testing and integration from widely available resources from Industrial Training Institutes and Polytechnics.

6. Competitiveness in labour costs. 7. MNCs willingness to invest in India driven by demand of regional SAARC

countries as well as moderately developed ASEAN countries like Indonesia, Philippines, etc.

8. Indian Telecom Operators market base with huge investment plans. 9. Lower Manufacturing plant establishment cost in India. 10. Current major drivers of National Economy – ITeS and BPO – totally rely on

Telecom Infrastructure.

Under the New Telecom Policy, 1999, with the provision of affordable and effective communication as its core vision and goal, the telecommunication sector in India has achie-ved a lot in recent years. With rapid growth, tele-density levels have surpassed the targets set. The total number of telephones (basic and mobile) rose from 22.8 million in 1999 to more than 150 million at the end of September 2006. While 21.83 million telephones were added during 12 months of 2004-05, the first nine months of 2005-06 saw an addition of 27.47 million phones. Overall, tele-density has risen from a mere 2.32 in 1999 to 13.09 in September 2006. Table 9.9 : Growth of

telephonesover the years

SI. No.

Year Fixed in million Per cent of PSUs

Mobile (including WLL), in million

Per cent of PSUs

PSUs Pvt. Total PSUs Pvt. Total 1. 2001-02 37.90 0.52 38.42 98.65 0.26 6.28 6.54 3.98 2. 2002-03 40.53 1.10 41.63 97.36 2.64 10.35 12.99 20.32 3. 2003-04 40.49 2.36 42.85 94.49 5.99 27.70 33.69 17.78

4. 2004-05 41.11 5.09 46.20 88.98 10.97 41.20 52.17 21.03

5. 2005-06 (first 9 months)

40.70 7.01 47.71 85.31 16.48 61.60 78.08 21.11

Although India's 150 million strong telephone network, including mobile phones, is one of the largest in the world, the telephone penetration rate continues to be low at about 13.09 phones per hundred population. The country offers vast avenues for growth, and by the end of 2007 the total number of phones are targeted to reach 250 million.

The drivers of telecom growth have undergone a significant change in terms of mobile versus fixed phones, as well as public versus private service providers. During 1999, both mobile phones and the private sector separately accounted for only 5 per cent of the total number of phones. However, in December 2005, the shares of mobile phones and the private sector in total phones were 61.97 per cent and 54.45 per cent, respectively. Mobile phones are increasingly being regarded as an effective tool of empowerment of the common man. It is no longer considered a luxury item and, in recent years, with lower capital expenses of mobile technology, it has become the technology of choice for low-priced telephony. The two PSUs in the telecom sector Bharat Sanchar Nigam Limited (BSNL) and MahanagarTelephone Nigam Ltd. (MTNL) have been losing their market shares in fixed telephony. From 98.65 percent in 2001- 02, their combined share declined to 85.31 per cent in December 2005 (Table 9.9). In the past two years, PSUs have actually seen a decline in the number of fixed lines, while such lines have grown in the private sector. However, they have improved their share in mobile telephony from 3.98 per cent to 21.11 per cent of the market.

1.15.2 Switching

Digital switching system technologies of foreign companies (Alcatel, Siemens, Fujitsu, AT&T, GPT, Ericsson, and NEC) have been validated and approved by DoT for introduction in the Indian network. Manufacturing facilities based on these technologies (except GPT) have been set up, and a vast capacity based on foreign and indigenous technologies now exists in the country.

1.15.3 Transmission

With the introduction of value-added services, demand for a radio transmission system has undergone a major change. A large number of public and private sector manufacturers, in collaboration with telecom giants such as Lucent, Fujitsu, and Siemens, have set up manufacturing facilities in India for digital transmission equipment. Digital microwave radio equipment has the potential for large investments and high returns since most of the radio equipment frequency spectrum in microwave is still available for deployment. 1.15.4 Terminal Equipment

With rapid growth in basic and value-added services, the need for a wide variety of terminal equipment, including telephone instruments ranging from normal pushbutton to multi-line feature phones, is bound to grow. Production of telephone answering machines, key telephone systems, cordless telephones, pagers, cellular phones, handsets for radio trunk services, pay phones, fax machines, ISDN terminals, line jack units, data terminals, and modem, and so on provides excellent opportunities to prospective investors.

1.15.5 Research and Development

Research and development activities are being carried out at various manufacturing units of India-based MNCs, and notable R&D is also being carried out at C-DoT, whose rural exchanges are very successful in the world market, apart from IIT Chennai, who have developed COREDECT technology. Application-oriented R&D is also being carried out at ITI Bangalore, IIT Chennai, BEL, Bangalore, Shyam, and HFCL at New Delhi. DoT currently has a number of training centers all over India apart from IITs and other technical institutes all over India. Apart from this, Indian companies engaged in the telecom sector are also venturing into telecommunication training to fulfill the ever growing need for expert professionals in this sector.

1.15.6 The Telecom Equipment - Manufacturing Sector – 10th Plan

The main objective of the 10th five-year plan is to make available reliable telecom services on demand even in rural areas at reasonable prices and to improve the teledensity in tune with NTP-99. NTP-99 emphasizes the importance of convergence and the desirability of encouraging all technologies to achieve these objectives. A substantial part of the telecom equipment deployed in the network is still imported. The post-liberalization scenario posed many challenges to the telecom R&D and manufacturing sectors.

1.16 Noteworthy Developments in Policies and Activities in the Electronics and Telecommunications Field - New Telecom Policy, 1999

The New Telecom Policy (NTP), 1999 was introduced to:

• Create a modern and efficient telecommunication infrastructure by bringing about a greater competitive environment

• Protect the defense and security interests of the country • Strengthen R&D efforts in the telecom sector and enable Indian companies to

become global players • Achieve efficiency and transparency in spectrum management • Convert PCOs into public teleinfo centers • Encourage development of telecommunication in rural areas by making it more

affordable

The new policy framework is meant to put a special emphasis on creating an environment that enables continued attraction of investment in the sector to create the required infrastructure by leveraging technological development.

Other significant developments in the area of telecom are under:

• The Telecom Regulatory Authority of India (TRAI) was set up as per the TRAI Act 1997 as an independent and autonomous regulator of telecom services in the country and matters connected thereto.

• There has been rapid progress in telecom services, particularly in the area of value-added services through private participation.

Furthermore, the entry of private operators in the VSAT arena in 1994 has encouraged corporate users to start relying on this technology. This has emerged as a potent weapon for diverse applications such as data access, voice, and multimedia connectivity even in remote locations. There are about 25,000 VSATs in the country. The Ku-band has been opened up for the existing VSAT licensees. In this area, higher bandwidth support will be a crucial development. Source: Global Communications Newsletter 1.17 C-DOT TECHNOLOGIES C-DOT was established in 1984 by the Government of India as a national centre of excellence in telecom technology research. It was vested with full authority and total flexibility to develop state-of-the art telecommunication technologies to meet the needs of the Indian telecommunications network. It is headquartered in New Delhi. Recently, in March 2005, C-Dot signed and MoU with Alcatel for research, development and marketing of wireless technologies for Indian and global markets. The scope includes setting up a global research centre for wireless technologies with its first project based on WIMAX technologies. C-Dot and Vanu Inc, the leader developer of software radio solutions have signed an MoU to trial the Vanu Anywave TM Software Radio GSM Base Station technology as an integral component in wireless access and broadband solutions for the Indian rural communications market. C-Dot has signed and MoU with Communication Research Centre, Canada for joint development of fixed wireless broadband access systems. C-Dot and XALTED Information Systems Pvt. Ltd. have joined hands for the development of GPON based solution for delivery of broadband services over fibre.

1.18 Broadband Integrated Services Digital Network Switching Platform C-Dot has built over the years a broadband integrated services digital network switching platform. The series covers a wide range of products for small wide area networks to large public networks carrying integrated voice, video, data and multimedia traffic. Products in the series range from multi-service access network units, through network multiplexers to carrier class core switches for establishing wide area backbone networks. C-Dot has thus brought out new state-of-the-art versions of rural as well as urban digital switches of variable capacities from over 200 subscribers to 100,000 subscribers both in stand-alone versions and multiple-module versions respectively. 1.19 Intelligent Network Solution C-Dot has also developed a scalable, cost-effective and versatile integrated Intelligent Network Solution comprising SP, IP, SCP and SMP. It can be used for quick deployment of feature-rich-value-added telecommunication services for the fixed and mobile network and the Internet. Each node is individually scalable to meet the growing demand for services in a cost-effective manner. The solution is compliant to ITU-t, ETSI and IETF standards and is ready for multi-vender multi-service networks. C-Dot’s Fixed Line SMS Technology brings all the benefits of messaging services, hitherto available to cellular mobile users only, to the fixed line users. Fixed line subscribers can send-receive short messages to/from POTS, CDMA, WLL and GSM and CDMA cellular mobile subscribers. While the fixed line services providers can use the FSMS for adding value to their service offerings, this technology opens up a plethora of opportunities for third-party content providers and marketers. It is also a very powerful tool for government sector initiatives such as e-governance. 1.20 Network Management System The C-Dot Network Management System (CNMS) is part of the range from network management solutions from C-Dot. The CNMS provides a scalable software solution to manage, monitor, control and maintain the performance of any network element online in real time from one or more network control centres. Each network control centre can monitor and control a group of network elements to it. 1.21 C-Dot’s Billing and Operations Support System C-Dot has developed this system as a convergent, customer care, billing and accounting platform for a competitive multi-service, multi-technology and multi-vendor telecommunications network It is a one-stop solution for managing a wide range of basic and value added services over a fixed line (PSTN, ISDN, Leased lines), mobile (WLL, 2G, GPRS and 3G), ATM and internet protocol networks.

In optical areas, C-Dot is able to offer compact and cost effective STM-1 system of the SDH hierarchy and optical booster amplifier for long range broad band optical fibre backbone networks. The development of dense and coarse wavelength multiplexing systems is in an advanced state of completion. 1.22 Rural Wireless Access and Broadband Solution This system provides value-added features for support of integrated voice, multimedia and broadband services. It also enables faster rollout of services. The solution is based on a combination of cost-effective WIMAX and WIFI technologies for providing services in scattered, low population density areas. 1.23 Another R&D Laboratory by Telecordia Technologies

Telcordia Technologies Inc, a $1 billion US-based provider of telecom software solutions, has established a research and development lab in Chennai, its first such facility outside the US. located in Tidel Park.

The company also established its India entity, Telcordia Technologies India Pvt Ltd, to provide dedicated resources for mobile, fixed line and cable operators throughout the country. The new entity will be headquartered in Gurgaon with programme delivery in Hyderabad.

The lab in Chennai would work on telecom solutions relevant to India and for the company's global operations. The company has been in India for the last few years working through partners and reported a turnover of $ 30 million (Rs 135 crore) last year.

Its clients included Tata Teleservices, Idea, Reliance Infocomm, Telecom Regulatory Authority of India and Department of Telecommunication.

Telcordia is looking at implementing the wireless number portability in India, and is in talks with various government authorities on this, according to Mr Naveen Suri, Vice-President, Telcordia Global Services. Once there is a Government regulation, service providers would form a consortium to introduce the service, which the company facilitates in eight countries, including the US, he said.

1.24 OTHER SUPPORTING TECHNOLOGIES & R&D

Indian Scenario

Recognising the importance of Nanotechnology, DIT initiated the Nanotechnology

Development Programme in the year 2004 with the objective of creating infrastructure

for research in Nanoelectronics and nanometrology at the national level and also to fund

small & medium level research projects in specific areas such as, nanomaterials,

nanodevices, carbon nano tubes (CNT), nanosystems etc.

Ten projects with a total budget outlay of over Rs. 126 crore have been initiated. These include two major research infrastructure projects at the national level : (i) Nanoelectronics Centres – a joint project of IISc Bangalore & IIT Bombay with an outlay of Rs.99.80 crore for a duration of 5 years; and (ii) the Nanometrology Centre at NPL, New Delhi with an outlay of Rs.11.308 crore for a duration of 4 years. The Nanoelectronics Centres at IIT Bombay & IISc Bangalore are a unique experience of two leading academic institutions involving 55 multidisciplinary faculty working together on different components of the project. The project also includes teaching and research at PhD, M.Tech and B.Tech level. The Nanometrology Centre at NPL, New Delhi will provide calibration & traceability for line width, step height, surface texture measurement; and calibration of low voltage (nV), low current (pA) and electric charge(fC). The centre will participate in international inter-comparisons and round-robin tests. The facilities available at these Centres would also be available to other researchers, institutions and industry

1.25 Optical Communication 1. To sustain the growth of I.T. in the country it is now well recognized that the

provision of sufficient bandwidth is essential. These bandwidth requirements can only be met through Fiber Optic communication. With the opening up of the country, fiber has been laid across the country by public and private companies. The capacity requirements for the connectivity visualized have been possible and can be substantially increased only through innovative use of optical communication technologies supported by Wavelength Division Multiplexing, Optical Amplification etc.

2. Recognizing the need for bandwidth many companies are putting up High

bandwidth networks, however there is not much clarity on the essential needs and on the methodology for this. Each of this is a vendor driven activity and each vendor tries to ensure his own systems and related (proprietary) components are used so that the service provider is bound to the vendor. This also leads to a

difficulty of the different Optical systems “Talking to each other”. At times this can only be overcome at the Electronic interfaces.

3. Today there is considerable fibre laid in the backbone network and optical

technology such as WDM and Optical Amplification have led to large bandwidth availability. The picture is not as good in the access and the access network (The part of the network closest to the individual user) is acting as a bottleneck for real growth of high data connectivity. Penetration can only increase through increased bandwidth for access and low access charges. Supply of large bandwidth up to each computer will need to precede demand.

4. With this large growth of bandwidth and the plans for deployment of new

network to satisfy this need the demand for optical fibre and Photonic-based systems will be very large. A major part of the expenditure by the service providers goes into the Photonics systems, which in turn consist of the sub systems, components and technology. Except for some of the fibres the other equipment, sub systems components are being imported.

5. It is important that a thrust should be provided in the Eleventh Plan to use this

opportunity so that India has a presence as an Optical Communication Technology Developer rather than just a Market.

1.26 Electronics Materials In today's highly competitive electronic & IT industry, manufacturers are constantly challenged to find ways to cost-effectively make faster and smaller electronic devices. One of the most important aspect of achieving these challenges is dependent on the development of advanced materials and technology. Nowhere is the ability to produce new materials more crucial than in the electronics & IT industry. Electronic and IT materials are the key elements of continued scientific and technological advances in the 21st century. Electronics Materials are the core for the components production. It constitutes approximately 50% of the total components cost. The electronic and IT materials include;

• Semiconductors • Superconductors • Ferroelectrics • Liquid crystals • Conducting polymers • Organic and superconductors • Conductors • Nonlinear optical and opto-electronic materials • Electro-chromic materials • Laser materials • Photoconductors • Photovoltaic

• Electro-luminescent materials • Dielectric materials • Nano-structured materials • Silicon and glasses, • Photosynthetic and respiratory proteins

Some of these materials have already been used and will be the most important components of the semiconductors and photonics industries, computers, internet, information processing and storage, telecommunications, satellite communications, integrated circuits, photocopiers, solar cells, batteries, light-emitting diodes, liquid crystal displays, magneto-optic memories, audio and video systems, recordable compact discs, video cameras, colour imaging, printing, flat-panel displays, optical waveguides, cable televisions, computer chips, molecular-sized transistors and switches, as well as other emerging cutting edge technologies. Electronics and photonics materials are expected to grow to a trillion-dollar industry in the new millennium and will be the most dominating forces in the emerging new technologies in the fields of science and engineering. The rapid progress in the area of development of materials has entered an era of designed materials. The combination of sophisticated and accurate processing equipment and fundamental understanding of materials enable synthesis of materials especially created to have properties required by the design engineer. Moreover, recent developments in materials science and engineering have not only made it evident that the traditional division to metals, ceramics, polymers etc. is becoming obsolete, but also that the ties of physics, chemistry and process engineering are becoming stronger than ever. The development of multi-functional and adaptable material’s new technologies is finding ways to reduce energy, and material inputs. Effective advanced semiconductor and printing circuit board manufacturing requires a long list of specialized and high purity materials. New materials such as superconducting ceramics and diamond films are likely to shape the electronics industry in the coming decade. As these improved materials are synthesized atom by atom, there will be multiple combinations of atomic assemblies. This will create the possibility of achieving several new structures and properties, enabling new electronic applications. Nanostructures based on inorganic and organic semiconductors, coupled with other complex materials such as polymers, will form the building blocks for many future devices and systems. Researchers are working on a wide range of technologies and sorting out difficulties, which will have a positive impact on the industry. These include elaboration and characterization of very thin dielectrics for gate control, reliance on fewer electron memories, lithographic techniques, and the possibility of optical interconnects. New developments such as holographic data storage and doped conjugated polymers are poised to revolutionize the industry.

PART 2 OPPORTUNITIES 2.1 Opportunities in the Indian IT services and ITeS industry The opportunities in the Indian IT services and ITeS industry can be classified along the following broad categories:

2.1.1 IT services The range and depth of capabilities have enabled the Indian IT services industry to gain a respectable position in the global IT services market (Indian industry expected to achieve market share of almost 30 percent by 2008 in key segments such as application development and application outsourcing as per NASSCOM-McKinsey estimates). The key factors that have enabled the industry’s success are end-to-end solutions capability, focus on stringent processes and quality of execution, global delivery model (combination of onshore and offshore with an increasing offshore component), high-end, mission critical service capabilities and strong project management methodologies and expertise. 2.1.2 Opportunity segments within IT services

Some multinational corporations who have leveraged the India advantage for IT services (either through a captive unit or through outsourcing include Siemens, Citigroup, Microsoft, Cisco, Hewlett Packard, Nortel, Boeing, Airbus. (Illustrative and not exhaustive; Source-News reports)

2.2 Customer interaction services Customer interaction services is one of the largest segments within the Indian ITeS industry. The predominance of customer interaction services is gradually decreasing due to pricing pressures as well as increasing depth of sourcing relationships which have include a new range of service offerings. However, while the share in the total pie may be decreasing, the outlook for this segment is still favourable due to strong demand from customers who have not sourced customer interaction services in the past as well as expansion of the customer care service offering to include more complex activities such as higher-end technical support. Select multinational corporations who have leveraged the Indian advantage for business process outsourcing services include Citigroup, American Express, General Electric and Hewlett Packard. (Illustrative and not exhaustive; Source-News reports). 2.3 Transaction processing Cost advantage, access to an abundant skill pool and commitment to quality of delivery have enabled the rapid growth of this segment. The range of capabilities sourced from India in business process outsourcing has been illustrated below:

Select multinational corporations who have leveraged the Indian advantage for business process outsourcing services include General Electric, Citigroup, Standard Chartered Bank, ABN Amro, Bank of America, American Express, British Airways and IBM (Illustrative and not exhaustive; Source-News reports).

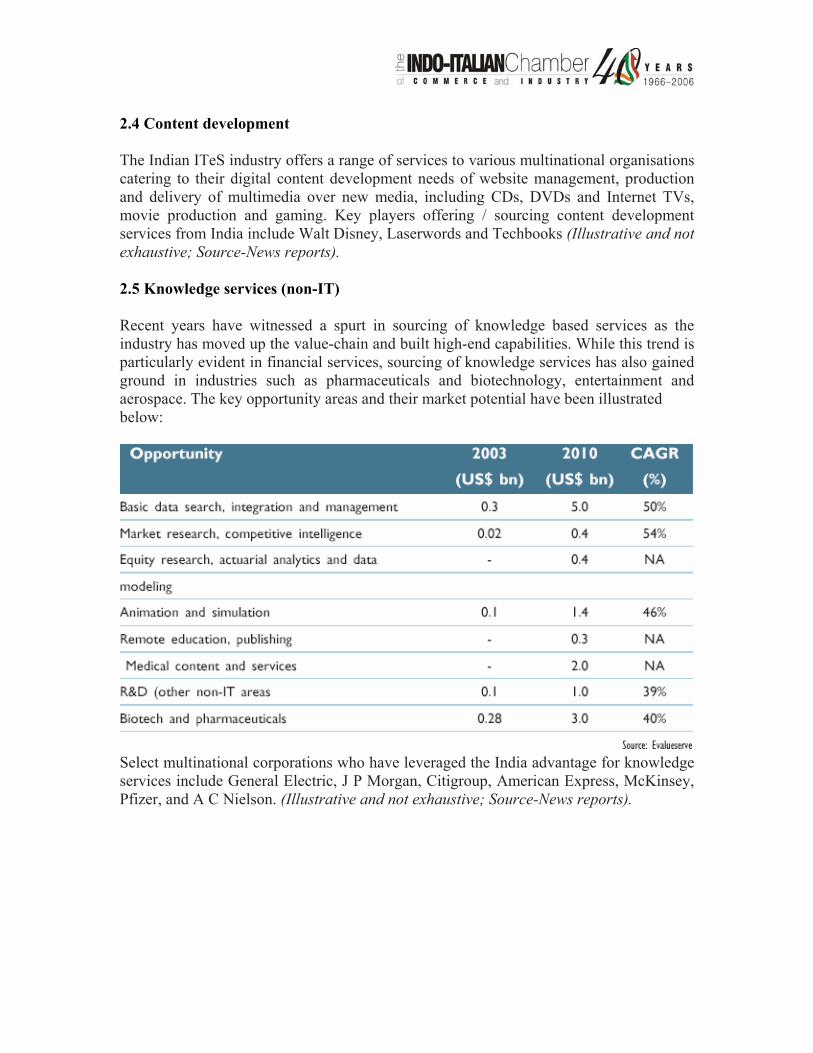

2.4 Content development The Indian ITeS industry offers a range of services to various multinational organisations catering to their digital content development needs of website management, production and delivery of multimedia over new media, including CDs, DVDs and Internet TVs, movie production and gaming. Key players offering / sourcing content development services from India include Walt Disney, Laserwords and Techbooks (Illustrative and not exhaustive; Source-News reports). 2.5 Knowledge services (non-IT) Recent years have witnessed a spurt in sourcing of knowledge based services as the industry has moved up the value-chain and built high-end capabilities. While this trend is particularly evident in financial services, sourcing of knowledge services has also gained ground in industries such as pharmaceuticals and biotechnology, entertainment and aerospace. The key opportunity areas and their market potential have been illustrated below:

Select multinational corporations who have leveraged the India advantage for knowledge services include General Electric, J P Morgan, Citigroup, American Express, McKinsey, Pfizer, and A C Nielson. (Illustrative and not exhaustive; Source-News reports).

2.6 Engineering design A significant emerging opportunity for the Indian ITeS industry is in the realm of engineering design which is expected to grow to US$ 4 bn by 2010 (Source: Evalueserve). While the scope of engineering design covers a broad spectrum of complexity levels, different players have emerged across the spectrum by building the requisite capabilities.

Key players offering / sourcing engineering design services from India include Bechtel, Ford Motor Company, General Electric, General Motors and Datamatics (Illustrative and not exhaustive; Source-News reports) 2.7 Key emerging trends impacting the Indian IT services and ITeS industry While the Indian IT services and ITeS industry is poised for rapid growth over the next few years, there are emerging trends which are likely to impact their operating models and the industry players would have to appropriately adjust their operations to capitalise upon / manage these trends. Some key emerging trends include: 2.7.1 Demand related • Offshoring is now mainstream and increasingly an integrated approach is being adopted across service types. Also, with more experience with the concept, offshoring projects are

moving beyond pilots and there is better and coordinated planning, execution and monitoring of offshoring projects. • Transaction processing is growing faster than customer interaction services and is likely to dominate future growth. Key segments which have contributed to this growth include finance and HR processing. • Demand for offshoring has extended beyond the banking and financial services industry and other key verticals that are likely to be demand drivers in the future include telecom, healthcare and entertainment / media. • While a range of sourcing models exist and continue to evolve, the preferred models are captives and hybrid options. • There is likely to be greater focus on risk, compliance and information security issues and therefore risk management is likely to be the dominant theme (both offshore and on-shore). 2.7.2 Supply related • Evolving market structure with consolidations, IPOs and other transactions. • Emergence of other competing countries and need to appropriately manage people, telecommunications and infrastructure costs to ward of competition from the same as cost arbitrage is still a significant driver for offshoring. • Possible demand-supply gap for trained manpower in the medium to long term and therefore need to invest in enhancing supply of trained manpower. • Development of a larger base of locations for IT and ITeS with supporting ecosystems. 2.8 Future Opportunities 2.8.1 Outsourcing or offshoring product development activities: Globally companies are attempting to enhance and maintain legacy products, while keeping costs low. This presents the following opportunities for Indian firms:

o Provide functions such as legacy product maintenance, development of patches and upgradation of core product, and support of multiple platform versions of core products.

o Form partnerships with global ISVs and develop new products in close

conjunction with them. The Indian team can perform functions such as development of specific modules, and testing and integration of modules with the larger product.

2.8.2 Embedded software: India has a pool of professionals skilled enough to work in

this domain. The market for embedded software products is expected to increase as OEMs and suppliers, especially in "smoke stack" industries, are struggling to build software competencies. This has created a void, which can be filled by Indian companies.

2.8.3 Shrink- Wrapped product development: Only a few Indian companies such as

i-Flex have succeeded in developing shrink-wrapped products for mass markets. This market is accessible only to companies who can compete at par with the global ISVs. Indian companies can take advantage of cost benefits and highly skilled manpower available in India, to develop software products. However, they lack experience in identifying product opportunities, and do not focus on the branding and sales strategies required to succeed in the product arena.

2.9 Some Major MNCs Undertaking R&D in India 2.9.1 The Corporate Technology Department of Siemens has set up a research centre in

Bangalore, which will focus on high-end R&D in software engineering technologies for multi-site global product line developments, client-server technologies for next-generation medical imaging solutions, and embedded software for security and automotive applications.

2.9.2 Snecma Aerospace India (SAI), the R&D centre of Snecma in India is involved in

the development of components of aero-engines and aircraft equipment, and embedded software to cater to its worldwide operations.

2.9.3 Schneider in partnership with Tata Elxsi: The global R&D centre of Schneider

Electric in Bangalore and the Indian product design company Tata Elxsi have announced the creation of a dedicated software competency centre that will be involved in the development and testing of embedded software applications offered by Schneider Electric.

2.9.4 Texas Instruments: Develops embedded software for Broadband, DSP, Wireless

terminal and OMAP applications, Device drivers and operating systems, Multimedia CODECS, Integrated software development environment

2.9.5 Sun Microsytems and Cadence Design have teamed up with Veda Institute of

Information Technology, Hyderabad to start India’s first nodal centre of competency for R&D in VLSI engineering, design automation and embedded system engineering.

2.9.6 Intel: In October 2004, Intel opened its first test lab- Enterprise Platform Group

(EPG) – thereby having end-to-end product development capability - for generating innovative, cost-effective debug and test solutions for all products coming out of India.

2.9.7 Samsung: The company has about 850 engineers in India at its two R&D centres -

Bangalore and Noida (UP) – that work on cutting edge technologies like embedded software, home network, IPV6, etc.

2.9.8 Motorola: Over 900 engineers work at Motorola’s Global Software Group (GSG)

at Bangalore and Hyderabad centres for creating cutting edge technological solutions for wireless products and infrastructure, providing embedded solutions and services for 3G Phones, UMTS and Cable Modem systems.

2.9.9 Philips: The company’s R&D centre in Bangalore - Philips Innovation Campus -

supports its global research on medical systems, semiconductors and mobile phone operating systems. The centre currently employs around 1,500 engineers and the number is expected to reach 3,000 in the next two years.

2.9.10 Delphi: Delphi’s Technical Centre India in Bangalore, meets the global needs for

vehicle software engineering, math based applications and product development particularly in software development, engineering analysis and CAD. The centre employs over 350 engineers working to develop embedded software technologies. The centre is also slated to become a centre of expertise for development of web based tools to automated engineering, modelling and business processes at Delphi electronics and safety division.

2.9.11 Daimler: The company through its Research and Tech group in Bangalore runs

alliances with 10 IT majors in the country. Besides the 100 seater centre in Bangalore also carries out dedicated research for DaimlerChrysler's global operations.

2.9.12 Bosch: The software division develops software solutions for Bosch units in many

countries including USA, Europe and Asia-Pacific. It is developing embedded software for control units, tools and diagnostics, besides mechanical design services and shared service centre accounting for Bosch operations worldwide.

2.10 EMERGING AREAS Software products can be classified in many ways and all of them offer opportunities for Indian offshore product development companies There is the consumer software product, which includes products like MS Word, software games and software for personal financial planning. Then there are the enterprise software products which include products like enterprise planning (SAP, PeopleSoft), financial management ( Tally, I-flex), supply chain ( 12, Manugistics) CAD/CAM ( Autodesk, Primavera). Yet another category is the embedded software products- software used in hardware devices such as medical devices and consumer electronics Nasscom’s Market Intelligence Service has identified certain mainly U.S. based companies with offices in India as key players in Offshore Product Development. Aditi Technologies has developed turnkey solutions for start-ups, designed a Tornado solution to augment products that are on the high growth stage and a legacy solution designed for “sunset” products that are on their way to retirement.

Aztec Software is another company that offers a gamut of services for application development, testing and QA, maintenance and support and migration and porting across application servers, databases and platforms. Ness Technolgies (India) is an offshore-centric technology solution group with five solution centres in Bangalore and Mumbai. Ness India has developed specific solution methodologies to enable independent software vendors to set up R&D transformation labs offshore for significant value and time-to-market advantages. Persistent Systems, with an office in Pune, India has over the past 13 years successfully executed over 700 release cycles, and software developed by Persistent’s team is an integral part of over 200 industry leading commercial software applications. Another company, Symphony Services, with an office in Bangalore, India specializes in product development. It helps clients to achieve effective and efficient management of the entire product lifecycle. Its product extension solutions include porting and integration.

2.11 Hardware: Current Status and Key Opportunities The global electronics (CE) industry clocked USD 1.27 trillion in CY 2005. The computer industry accounted for USD 218 billion registering an annual growth of 9%. A total of 218 million computers were shipped worldwide registering a growth of 15%. China accounted for 19.3 million units of the PC consumption in 2005 registering a growth of 29%. As manufacturers seek to reduce costs, there has been a marked shift in electronics output worldwide, including that of computers and peripherals, from high-cost to low-cost locations. Although Asia/Pacific—in particular, China—has been the main beneficiary, Central and Eastern Europe, Mexico and Brazil have also benefited from significant inward investment. In the longer term, many of today's low-cost locations will also offer significant market opportunities, creating the need for further investment in local manufacturing. The opportunity is knocking at India’s door as well. The size of the computers and peripherals market in India in 2005-06 (including printers, UPS and networking products) was around USD 5 billion (Rs. 22,000 Crores). The consumption of computers was 5.13 million units with a growth of 32% over the previous fiscal. Desktops accounted for 4.6 million units growing 28%, while notebooks accounted for 0.5 million units growing 144%. In value terms, the computers and notebooks market was USD 2.5 billion (Rs. 11,000 Crores) registering a growth of 28% over FY 2004-05, the growth in desktops being 18% and in notebooks 107%.

Computers & Peripherals Market: 2004-05 & 2005-06

Total Market Total Revenue (in Rs Crores)

Product 2005-06 2004-05 % Growth 2005-06 2004-05 % Growth

Computers Desktop PCs

4,614,724 3,632,619 27% 8,884 7,520 18%

Notebooks 431,834 177,105 144% 2,027 978 107% Servers 89,161 49,165 81% 1,545 916 69% Printers Dot matrix 472,074 399,580 18% 430 379 13% Inkjet 717,001 636,619 13% 241 223 8% Laser 325,109 142,555 128% 554 286 94% Line 4,914 4,675 5% 122 116 5% Other Peripherals

Key boards 4,639,156 3,669,441 33% * * *

Monitors 4,637,787 3,642,204 34% 2,301 1,903 21%

UPS systems

1,208,413 954,260 27% * * *

Networking Products

NICs 3,646,145 1,801,854 117% * * *

Hubs 144,117 113,894 27% * * * (Source: Manufacturers’ Association for Information Technology) * wide variations in price in product categories IT Products being manufactured in the country include personal computers, servers, workstations, supercomputers, data processing equipment, Dot-matrix printers, digitizers, networking products such as modems, hubs, etc. and add-on cards. The production in the PC segment is dominated by P-4 Processors. Other processors are gradually entering the market reflecting, perhaps, the need for low-cost computing solutions.