A REPORT ON “To find out a methodology of ranking Debt Mutual Fund Schemes that can be adopted by ITC Limited to invest its surplus cash”. By Ankit Dhanuka O r ga n i z a tion RUSSELL CREDIT LIMITED

Transcript

A REPORT

ON

“To find out a methodology of ranking Debt Mutual Fund Schemes that

can be adopted by ITC Limited to invest its surplus cash”.

By

Ankit Dhanuka

O r ga n i z a tion

RUSSELL CREDIT LIMITED

(WHOLLY OWNED SUBSIDIARY OF ITC LTD)

VIRGINIA HOUSE

37 J L NEHRU ROAD

KOLKATA-700071

PROJECT COMPLETION CERTIFICATE

ACKNOWLEDGEMENT

Success is not a destination but a journey- it is often said. I realized it even better during my Internship program. When I completed this journey, I may not have come this far without help, guidance and support of certain people who acted as guide, friend and torchbearers along the way.

Words often fail to express one's inner feeling of gratitude and indebtedness to one' s benefactor but then it is only readily available medium through which the undersigned can express his sincere thanks to all those who are associated with his work in one way or the other.

I take this opportunity to express my sincere gratitude to Mr. Jagdish Singh, (Head- Corporate Treasury, ITC Limited) who provided me this great opportunity to work in the Corporate Treasury of ITC Limited and gave me such a challenging project.

I feel it my profound privilege to express my most sincere gratitude and indebtedness to my mentor, Mr. Bishnu Agrawal, (Assistant Manager, Corporate Treasury, ITC Ltd) who has been instrumental in providing me direction, constant encouragement and cooperation in an attempt to take this project to a logical conclusion.

I would also like to thank Mr. Suresh Kumar, (Front Office Manager, Corporate Treasury, ITC Ltd), Mr. Abhishek Kumar, (Back Office Manager, Corporate Treasury, ITC Ltd) & Ms. Aanchal Dhawan, (Assistant Manager, Corporate Treasury, ITC Ltd) for their constant help and co-operation.

Apart from the people at ITC, I would like to thank Mr. Sandipan Ray, Institutional Sales, Principal Mutual Fund and Mr. Vijay Kumar, Business Development Manager, CRISIL for their help, co-operation and invaluable time.

I wish to thank my Faculty Mentor Prof. Subir Srimani for his constant support and encouragement.

Last but not the least; I would like to thank my fellow trainees at ITC, for making my stay at ITC a memorable one.

My 12 weeks at ITC Ltd have been a great learning experience. Apart from knowledge enrichment, it has provided value addition in terms of corporate culture and corporate conduct.

- Ankit Dhanuka

TABLE OF CONTENTS1. Company Profile 1-12

1.1 Brief History 1

1.2 ITC's Core Values 2

1.3 Corporate Strategy of ITC 3

1.4 Major Business Divisions 3-10

1.5 Porter's Five Forces Model 10-12

1.6 BCG Matrix (Industry Analysis) 12

2. Abstract 13-14

3. Introduction 15-18

3.1 Objectives 15

3.2 Methodology & Limitations 16

3.3 Gtnews Survey 17

3.4 Ernst & Young Survey 18

4. Main Text 19-84

4.1 Stage 1

4.1.1 ABC of Mutual Funds

20-46

20-36

4.1.1.1 Types 21-34

4.1.1.2 Advantages Of Investing in MF 35

4.1.1.3 Disadvantages Of Investing in MF 36

4.1.2 Investment alternatives for Surplus Cash 36-44

4.1.3 Risk-Return Matrix 44

4.1.4 Comparison of MF with other instruments 44-46

4.2 Stage 2 47-56

4.2.1 CRISIL-CPR 47-50

4.2.2 ICRA-Methodology 50-53

4.2.3 Value Research Fund Rating 53-55

4.2.4 Asset Management Companies 56

4.3 Stage 3 57-58

4.4 Stage 4 59-71

4.4.1 Why Ranking only for Liquid & Liquid Plus 60-61

4.4.2 Selection of AMC 62

4.4.3 Ranking Methodology 63-66

4.4.3.1 Corpus Size 63

4.4.3.2 Investment in AAA 64

4.4.3.3 Investment in GOI securities 64

4.4.3.4 Average Maturity 64-65

4.4.3.5 Point To Point Returns 65-66

4.4.4 Ratio for Performance Evaluation 66-71

4.4.4.1 Alpha Ratio 66-67

4.4.4.2 Information Ratio 67-68

4.4.4.3 Sharpe Ratio 68-69

4.4.4.4 Sortino Ratio 69-70

4.5 Stage 5

4.4.4.5 Treynor Ratio 70-71

72-84

4.5.1 Steps Involved in Final Analysis 72-73

4.5.2 Final Analysis 73-80

4.5.3 Comparison 80-81

5. Findings 82

6. Conclusion 83

7. Recommendations 84

8. References 85-86

Page 1

1. COMPANY PROFILE

ITC is one of India's foremost private sector companies with a market capitalisation of

FMCG-Cigarettes: ITC is the market leader in cigarettes in India. With its wide range of

invaluable brands, it has a leadership position in every segment of the market. It's highly

popular portfolio of brands includes Insignia, India Kings, Classic, Gold Flake, Silk Cut,

Navy Cut, Scissors, Capstan, Berkeley, Bristol and Flake.

FMCG-Foods: ITC made its entry into the branded & packaged Foods business in

August 2001 with the launch of the Kitchens of India brand. A more broad-based entry

has been made since June 2002 with brand launches in the Confectionery, Staples and

Snack Foods segments.

The Foods business is today represented in 4 categories in the market. These are:

Ready To Eat FoodsStaplesConfectionerySnack Foods

FMCG-Lifestyle Retailing: ITC‘s Lifestyle Retailing Business Division has established

a nationwide retailing presence through its Wills Lifestyle chain of exclusive specialty

stores. Wills Lifestyle, the fashion destination, offers a tempting choice of Wills Classic

work wear, Wills Sport relaxed wear, Wills Clublife evening wear, fashion accessories

and Essenza Di Wills – an exclusive range of fine fragrances and bath & body careproducts and Fiama Di Wills - a range of premium shampoos and shower gels. Wills

Lifestyle has also introduced Wills Signature designer wear, designed by the leading

designers of the country.

With a distinctive presence across segments at the premium end, ITC has also established

John Players as a brand that offers a complete fashion wardrobe to the male youth of

today. The recent launch of Miss Players with its range of trendy fashion wear for young

women has been a successful addition to the youthful offering. With its brands, ITC is

committed to build a dominant presence in the apparel market through a robust portfolio

of offerings.

FMCG-Personal Care: In line with ITC's aspiration to be India's premier FMCG

company, recognised for its world-class quality and enduring consumer trust, ITC

forayed into the Personal Care business in July 2005. In the short period since its entry,

ITC has already launched an array of brands, each of which offers a unique and superior

value proposition to discerning consumers. Anchored on extensive consumer research

and product development, ITC's personal care portfolio brings world-class products with

clearly differentiated benefits to quality-seeking consumers.

ITC's Personal Care portfolio under the 'Essenza Di Wills', 'Fiama Di Wills', 'Vivel Di

Wills' 'Vivel UltraPro', 'Vivel' and 'Superia' brands has received encouraging consumer

response and is being progressively extended nationally.

FMCG-Education & Stationery: ITC made its entry into the stationery business in the

year 2002 with its premium range of notebooks, followed in the year 2003 with the more

popular range to augment its offering.

Today, ITC continues to blend its core capabilities to market a growing range of

education and stationery products. These capabilities include,

1. Manufacturer of India‘s first Ozone treated environment friendly Elemental

Chlorine Free (ECF) pulp, paper and paperboard.

2. Knowledge of image processing, printing & conversion garnered from its

Packaging & Printing Business.

3. Brand Building & Trade Marketing & Distribution strengths resident in its FMCG

Business.

ITC‘s stationary Brands are marketed as ―Classmate and ―Paperkraft, with Classmate

addressing the needs of students and Paperkraft targeted towards college students and

executives.

FMCG-Safety Matches: As part of its strategic initiative to create multiple drivers of

growth in the FMCG sector, ITC commenced marketing safety matches sourced from the

small-scale sector. The Matches business leverages the core strengths of ITC in

.

Page 5

marketing and distribution, brand building, supply chain management and paperboard &

packaging to offer Indian consumers high quality safety matches.

ITC‘s range of Safety matches includes popular brands like i Kno, Mangaldeep, Aim, Aim

Mega and Aim Metro. With differentiated product features and innovative value

additions, these brands effectively address the needs of different consumer segments. The

Aim brand is the largest selling brand of Safety Matches in India. ITC also exports

regular and premium safety matches brands to markets such as Middle East, Africa and

the USA. The successful acquisition of Wimco Limited by Russell Credit Limited, a

wholly owned subsidiary of ITC has consolidated the market standing of the Company's

Matches business through synergy benefits derived through combined portfolio of

offerings, improved servicing of proximal markets and freight optimization. Through its

participation, ITC aims to enhance the competitiveness of the small and medium scale

sectors through its complementary R&D based product development and marketing

strengths, especially the breadth and depth of the Company's trade marketing and

distribution.

FMCG-Agarbattis: As part of ITC's business strategy of creating multiple drivers of

growth in the FMCG sector, the Company commenced marketing Agarbattis (incense

sticks) sourced from small-scale and cottage units in 2003. This business leverages the

core strengths of ITC in nation-wide distribution and marketing, brand building, supply

chain management, manufacture of high quality paperboards and the creation of

innovative packaging solutions to offer Indian consumers high quality Agarbattis. With

its participation in the business, ITC aims to enhance the competitiveness of the small

and medium scale sectors through its complementary R&D based product development

and strengths in trade marketing and distribution.

Mangaldeep Agarbattis are available in a wide range of fragrances like Rose, Jasmine,

Bouquet, Sandalwood, Madhur, Durbar, Tarangini, Anushri, Ananth and Mogra.

Page 6

B. HOTELS

ITC entered the hotels business in 1975 with the acquisition of a hotel in Chennai, which

was then rechristened ITC Chola. Since then the ITC-Welcomgroup brand has become

synonymous with Indian hospitality. With over 100 hotels in more than 75 destinations,

ITC-Welcomgroup has set new standards of excellence in the hotel industry in

Accommodation, Cuisine, Environment and Guest Safety. ITC's Hotels business is one of

India's finest and fastest growing hospitality chains. ITC Hotels' commitment to

delivering globally benchmarked services, embedded in a culture deeply rooted in India's

rich tradition of hospitality, gives it a unique and distinct identity.

C. Paperboards Paper & Packaging

Paperboards & Speciality Paper Division: ITC‘s Paperboards and Specialty Papers Division is India‘s largest and most technologically advanced paper and paperboards business. ITC caters to a wide spectrum of packaging, graphic, communication, writing,

printing and specialty paper requirements through its four world-class mills in India.

Having pioneered many speciality applications like cigarette tissues, packaging boards,

aseptic cartons and gypsum liners, ITC‘s Paperboards and Specialty papers businessenjoys market leadership in the value-added paperboards segment, and also has a

significant share of the Indian paperboards market. It is also the largest Indian exporter of

coated boards.

Page 7

The product range includes:

Packaging & Printing: ITC's Packaging & Printing Business is the country's largest

convertor of paperboard into packaging. It converts over 50,000 tonnes of paper and

paperboard per annum into a variety of value-added packaging solutions for the food &

beverage, personal products, cigarette, liquor, cellular phone and IT packaging industries.

It has also entered the Flexibles and Corrugated Cartons business.

The Division, which was set up in 1925 as a strategic backward integration for ITC's

Cigarettes business, is today India's most sophisticated packaging house. State-of-the-art

technology, world-class quality and a highly skilled and dedicated team have combined

to position ITC as the first-choice supplier of high value added packaging.

Page 8

D. Agri Business

Agri Commodities & Rural Services: ITC's pre-eminent position as one of India's

leading corporates in the agricultural sector is based on strong and enduring farmer

partnerships, that has revolutionized and transformed the rural agricultural sector. A

unique rural digital infrastructure network, coupled with deep understanding of

agricultural practices and intensive research, has built a competitive and efficient supply

chain that creates and delivers immense value across the agricultural value chain. One of

the largest exporters of agri products from the country, ITC sources the finest of Indian

5. Processed Fruits - Fruit Purees/Concentrates, IQF/Frozen Fruits, Organic Fruit

Products, Fresh Fruits

6. Coffee & Spices - Coffee, Black Pepper, Chilly, Turmeric, Ginger, Celery and

other Seed Spices

Cigarette Leaf Tobacco: ITC pioneered the cultivation and development of Leaf

Tobaccos in India. Nearly a century of creating customer delight ensures that

globally, ITC's Leaf Tobacco business is synonymous with being "The One Stop Shop

for Quality Indian Tobaccos". The Leaf Tobacco business' partnership with the farmer is

also almost

100 years old. In a spirit that truly embodies the Company's "commitment beyond the

market", ITC has helped the Indian farmer grow quality leaf tobaccos and linked him to

global markets.

Page 9

ITC is the largest buyer, processor and exporter of leaf tobaccos in India - creating a

global benchmark as the single largest integrated source of quality tobaccos. Serving

customers in 50 countries across more than 70 destinations, ITC co-creates and delivers

value at every stage of the leaf tobacco value chain.

1.5. Porters Five Forces Model –ITC Limited

ITC is diversified in its businesses and this makes an overall analysis with regard to its

individual business units highly complex. The company‘s diversified status originates

from its corporate strategy aimed at creating multiple drivers of growth, anchored on its

time-tested core competencies:

1. Unmatched distribution reach

2. Superior brand-building capabilities

3. Effective supply chain management

4. Acknowledged service skills in hotel business.

Over the years, ITC has diversified its business risk by diversifying its product categories

into multi-businesses, which are different in nature, yet, draws from competencies of

existing businesses to fructify into a strategic business unit. E.g., matches business draws

strength from the distribution and branding competencies of the tobacco business and has

already taken over more than 40% of the branded matches segment in the country.

Its businesses are spread over a wide spectrum, ranging from FMCG to hotels, packaging,

paper and paperboards and international commodities trading. Each of these businesses is

vastly different from the other in its type, the state of its evolution and the basic nature of

its activity, all of which influence the choice of the form of governance. The challenge of

governance for ITC therefore lies in fashioning a model that addresses the uniqueness of

each of its businesses and yet strengthens the unity of purpose of the company as a

whole.

Page 10

ITC’s Five Forces Model

A comprehensive analysis for ITC is difficult owing to its diversified presence in several

sectors of the industry. An attempt is being made to provide a brief overview of the same.

1. ITC has an immensely strong presence in all the sectors it caters to. A large-

scale business like that of ITC is hard to compete with. ITC has carved a niche

in the market in all the segments that it is present in. It is far ahead of its age-

old competitors as well as potential entrants owing to its focus on value

creation for the consumer through significant investments in product design,

innovation, manufacturing technology, quality, marketing and distribution.

2. With such a powerful presence in its business sectors, it is threatened by

substitutes, however, to a much lesser extent as compared to businesses with a

similar profile. Some SBUs of ITC are faced with stiff competition owing to

their late entry in to the same

3. Bargaining power of buyers is moderate, in fact, low as far as most of the

businesses of ITC are concerned. This is primarily owing to the fact that ITC

believes in unadulterated quality and strives to achieve the same in all its

endeavors

4. Bargaining power of suppliers is low due to the overpowering presence of ITC

as far as all the divisions are concerned. Long-term relationships with

suppliers are beneficial for the company as well as the suppliers. Suppliers

abide by ITC‘s terms, again owing to the trust and quality that ITC stands for

and look forward to longer contracts leading to the establishment of standard

sources of supply

5. Rivalry among the existing players within all the sectors in the industry is

strong. Well-established and big companies desire to get bigger and the

smaller, growing companies desire to reach the performance levels

of the leading players in the market. ITC has been consistently

outperforming its competitors in some of the sectors where it has

had a long presence. It has several close competitors in certain other

segments and it has yet to reach the benchmark levels in other

segments where it is a relatively new player in the Markets

Page 11

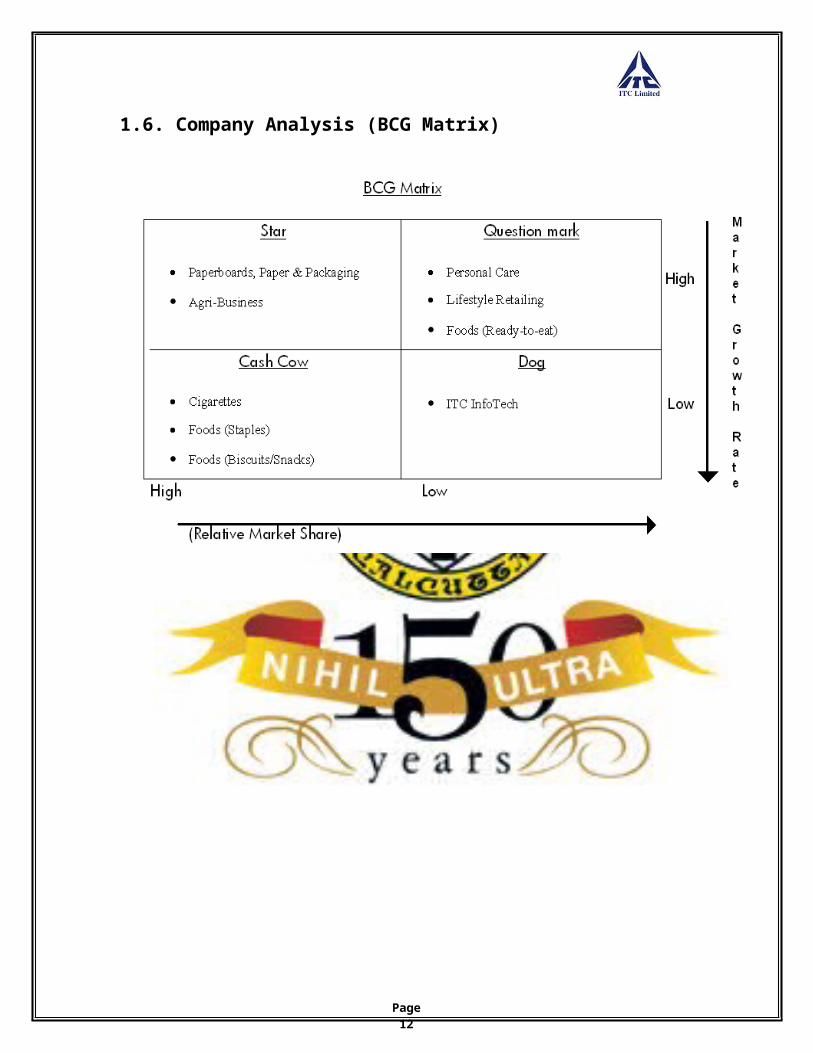

1.6. Company Analysis (BCG Matrix)

Page 12

2. ABSTRACT

The role of the Treasury as a strategic business unit has become more pronounced as

Indian corporate stride confidently towards newer geographic to expand their global

footprints. The role of the Treasury in India has evolved from pure fund management to

cover strategic hedging, risk management and more recently fund raising and balance

sheet management.

The Indian Corporate Treasury has evolved over a period of time. The focus is now

pivoted around centralization of activities and enhancing efficiencies through better

negotiation with banks and capitalization of opportunities presented through

liberalization.

Corporate Treasury was earlier expected to display efficiency through banking

negotiations and the execution of sacrosanct strategies. Today, their role has become

more holistic and involves more decision-making and strategy development as compared

to overall risk philosophy of companies. As competencies develop and the focus shifts to

superior performance delivery, Indian treasuries are likely to evolve into ―Strategic

Business units‖ focused on adding value to other business units.

The main objective of this project is to study the debt schemes of various Asset

Management Companies (AMCs) under Liquid & Liquid Plus or Ultra Short Term

(Treasury Advantage) categories and then suggest a methodology that can be used by

ITC Limited for deployment of surplus cash. The project also covers the overview of

Mutual Fund Industry and parameters involved in selecting the right scheme under the

said category.

In ITC Limited, the deployment of temporary liquidity of the company is guided by the

twin objective – ―Capital Protection & Return Optimization‖. The investments are mainly

made in Liquid, Treasury Plus, Floating Rate, Fixed Maturity Plans, Short Term

Funds and Income Schemes of Debt Mutual Funds.

Page 13

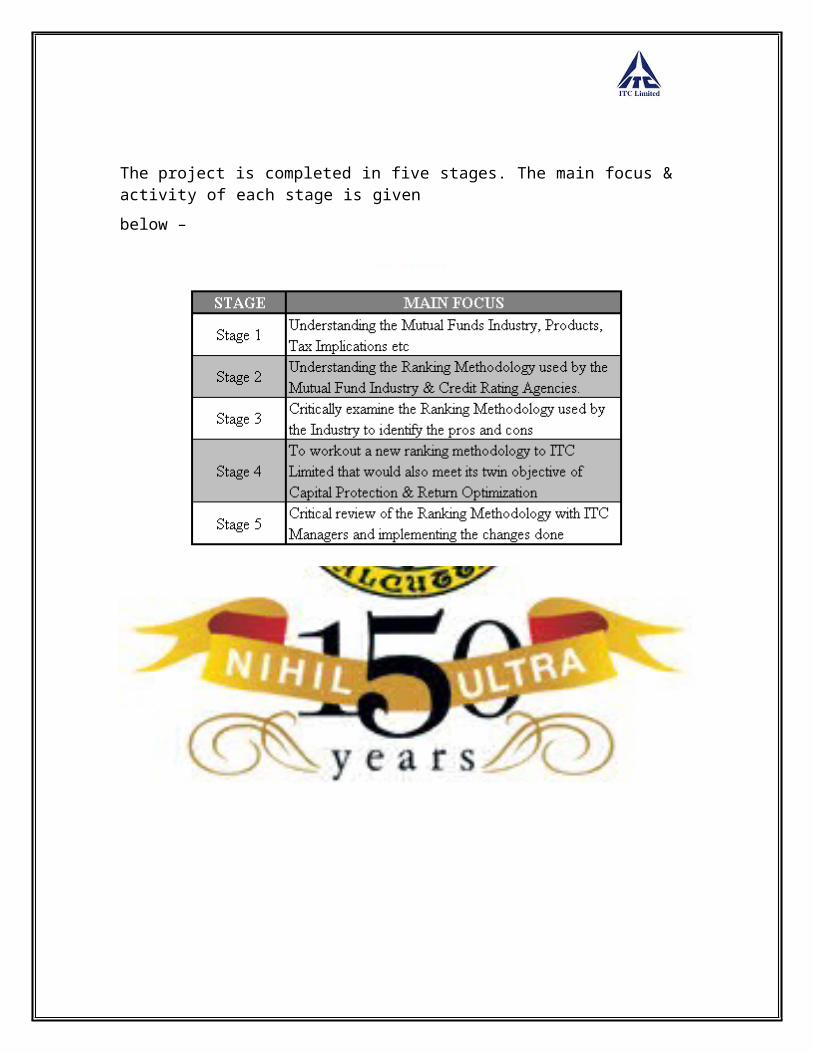

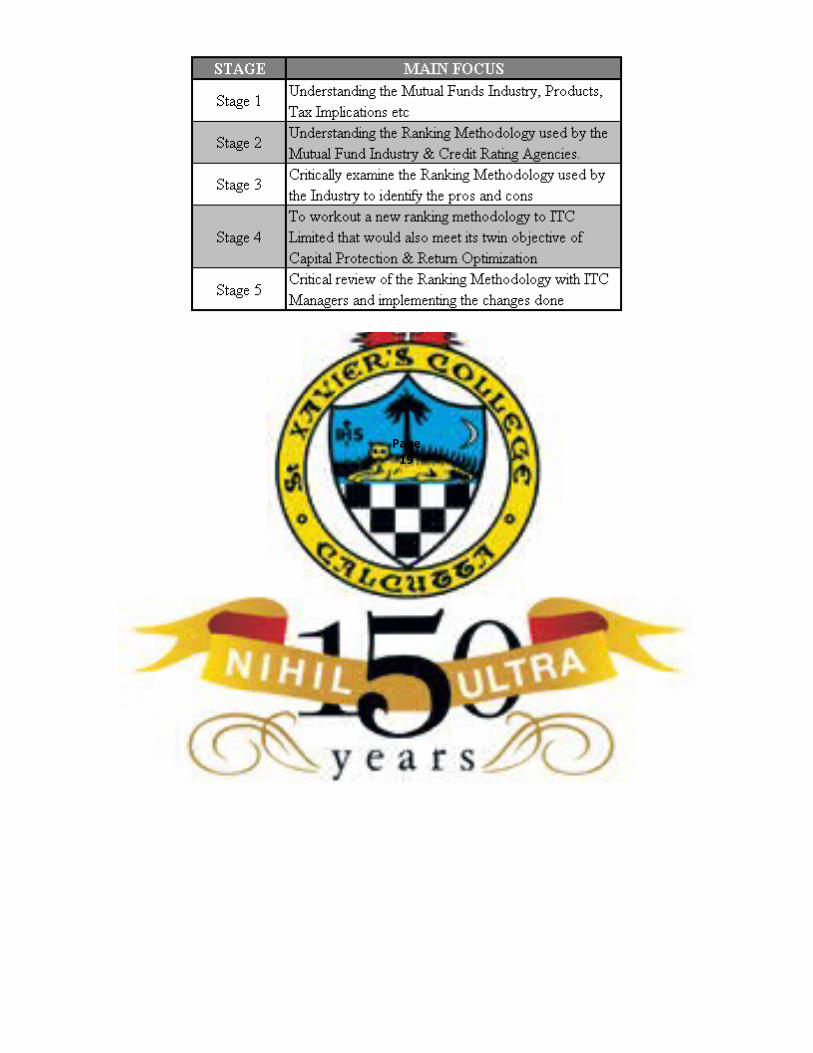

The project is completed in five stages. The main focus & activity of each stage is given

below –

Page 14

3. INTRODUCTION

The main objective of the project is to study the methodology used in the mutual fund

industry to Rank debt schemes of various Asset Management Companies (AMCs) under

Liquid & Ultra Short Term (Treasury Advantage) categories and then suggest a

methodology, which can be used by ITC Limited for deployment of surplus cash. This

project report is primarily an insight in to the area of investment management, as a part,

of the Treasury operations that are carried out in ITC Limited.

It involves a thorough and in-depth understanding of the importance of investment

decisions for corporate houses, the investment process, the various criteria for making the

process more effective and the relevance of those criteria depending on the varied

investment objectives. It also involves a deep understanding of the financial markets in

terms of the several classifications within them as well as a detailed insight into the

various investment alternatives that are available to the corporate houses.

The project also discusses the concept of mutual funds in great detail, including their

types, as well as the several benefits associated with them. It also provides an overview

of the various classifications of mutual funds and the criteria for selecting the appropriate

investment opportunity.

3.1 Objectives of the Project:

To understand the Mutual Fund Industry and the factors affecting it.

To understand the Ranking Methodology used in the Industry.

To critically examine the Ranking Methodology used by the Industry. This is to

identify the pros and cons of the ranking methodology that would help in

developing a new methodology of ranking mutual fund schemes.

To suggest a ranking methodology to ITC Limited that would also meet its twin

objective of Capital Protection & Return Optimization.

Page 15

3.2 Methodology:

Visit Mutual Fund houses to understand:

o Various Categories of Debt Mutual Fund Schemes

o The perspective of various Mutual Fund Schemes on the Mutual Funds

industry as a whole

o The sensitivity of various Mutual Fund Schemes to the market conditions.

o The methodology of Portfolio Creation.

Refer Textbooks, Research Papers, Fact Sheets of Mutual Funds, presentations

available within the organization and Internet for secondary data and latest

happenings in Mutual Fund industry.

Study the ranking methodology used by the Industry and critically analyzing it.

Discuss ideas with the managers of Corporate Treasury and identifying crucial

areas within ranking of mutual fund schemes.

3.2 Limitations of the study:

Comparison with peers is not possible as the investment methodology of parking

temporary cash is not publicly available.

As Kolkata is the marketing hub for mutual fund houses and financial decisions

are taken at their head offices in Mumbai, discussion with fund managers about

their mode of portfolio selection could not be feasible.

Since the company invests only in Debt Mutual Funds, the methodology for

Equity Mutual Funds was not done as would not meet the objective of the

Company.

The study would be limited to Liquid, Ultra Short Term Schemes as these are

most suited for Cash Management. Also, all other categories of Debt Mutual

Funds are very sensitive to interest rates movements and investments in these

schemes are based on the existing market conditions.

Page 16

Methods of collecting data:

The NAVs of the mutual Fund schemes were obtained from AMFI website

(www.amfiindia.com).

The data related to debt market were obtained from FIMMDA website

(w w w. f i m mda. c o m ) & databases such as Prowess and Bloomberg.

The portfolio and the average maturity of the debt mutual fund schemes were

provided on a weekly basis by CRISIL.

Surveys – GTnews and Ernst & Young survey:

The main objective of the project was Surplus Cash Management and hence Internet was

referred to obtain the trend in the corporate world. The two surveys, which are

summarized here, show the pattern in India as well as in the Western World.

3.3. Gtnews.com is the home for treasurers around the world for key speeches and

information. The survey presented here was conducted between March & April 2008 in

association with SEB. The corporate that participated in the survey where mostly from

Europe & America.

The key findings of this survey was –

60% (last year 63%) of the corporate use bank deposits to allocate their surplus

cash.

52% (last year 51%) of the corporate use money market mutual funds to allocate

their surplus cash.

(* Source: htt p:/ /www.gt news.com/ feature/287.c f m )

Page 17

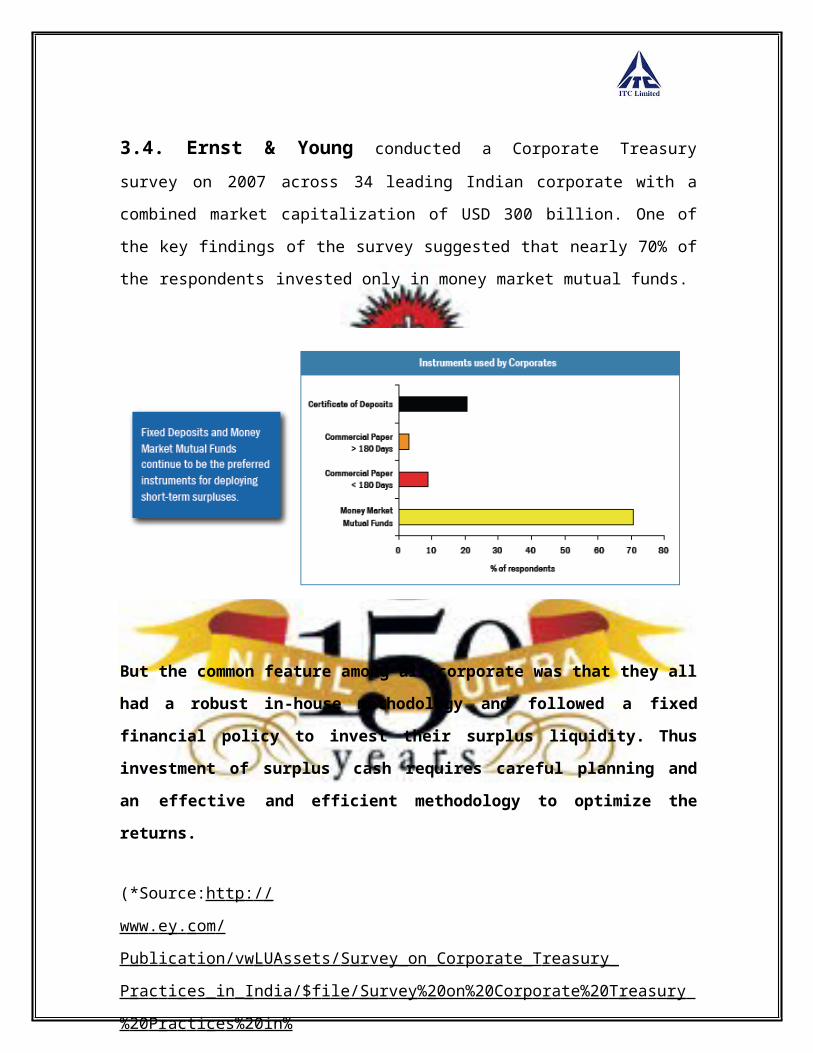

3.4. Ernst & Young conducted a Corporate Treasury survey on 2007 across 34

leading Indian corporate with a combined market capitalization of USD 300 billion. One

of the key findings of the survey suggested that nearly 70% of the respondents invested

only in money market mutual funds.

But the common feature among all corporate was that they all had a robust in-house

methodology and followed a fixed financial policy to invest their surplus liquidity.

Thus investment of surplus cash requires careful planning and an effective and

efficient methodology to optimize the returns.

(*Source:ht t p: / /ww w . e y . c om /P ubl i ca t i on/v w L U A ssets/ S u r v e y _on_Co r po r a te_T r e a su r y _

P r a c t i ce s_in _ I ndia/$ f i l e / S u r v e y % 20on % 20Corp o r a te % 20 T r e a s u r y % 20 P ra c t i ce s%20in%

20 India.p df)

Page 18

4. MAIN TEXT

As already mentioned, this project focuses on the Surplus Cash Management of Treasury

Operations at ITC Limited. The project focuses on the debt schemes of Mutual Funds

under Liquid & Liquid Plus (or Ultra Short Term) category. ITC Ltd invest its Surplus

Cash in the following instruments –

1. Debt schemes of Mutual Funds.

2. Fixed Maturity Plans of Mutual Funds.

3. Bank Fixed Deposits.

4. Tax Free Bonds.

The main objective of the project is to understand the Mutual Funds industry and come

out with a Ranking Methodology to invest in Liquid & Liquid plus category, as this is the

only category where a pre-defined ranking methodology can be set. Moreover interest

rate movements least affect these schemes.

Thus keeping the objective in mind, the whole project was divided into five stages –

Page 19

4.1 Stage 1

In this stage of the project, I have understood the Mutual Fund Industry and its various

products. I am really indebted to managers of Corporate Treasury who spared their

invaluable time to explain the practical aspects of the theoretical concepts.

The following is my understanding of concepts involved in Mutual Funds & the industry

as a whole –

4.1.1. ABC of Mutual Funds

A mutual fund represents a vehicle for collective investment. It pools money from

investors, with a promise that professional managers who are expected to honor the

promise would invest the money in a particular manner. On participating in a mutual fund

scheme, investors become part owners of the investments held under that scheme.

The idea behind a mutual fund is that investors lack the time or the inclination or the

skills to manage their investments. Professional managers, acting on behalf of the mutual

fund, manage the investments for the benefit of investors, in return for a management fee.

The organization that manages the investment is the Asset Management Company

(AMC). Individuals within the AMC who perform this role of managing investments are

the fund managers. Each mutual fund unit represents an investor's proportionate

ownership of the fund's holdings and the income those holdings generate.

Investors have their individual

preferences on how they would

like their money to be invested

and how much risk they would

be willing to take. Professional

managers can choose to

manage each individual

investor‘s money as per the

Page 20

investor‘s preferences. Such personal treatment is referred to as Portfolio

Management

Scheme (PMS) in India. This scheme is economically feasible only for investment

portfolios above a particular value. The breakeven asset size, which depends on the cost

structure of the manager, is rarely below Rs.10, 00,000. The Asset Under Management

(As On 31.03.2009) shows that bulk of investment is in income fund, which is a preferred

investment destination for corporate to park their surplus cash.

The main characteristics of Mutual Funds can be shown as –

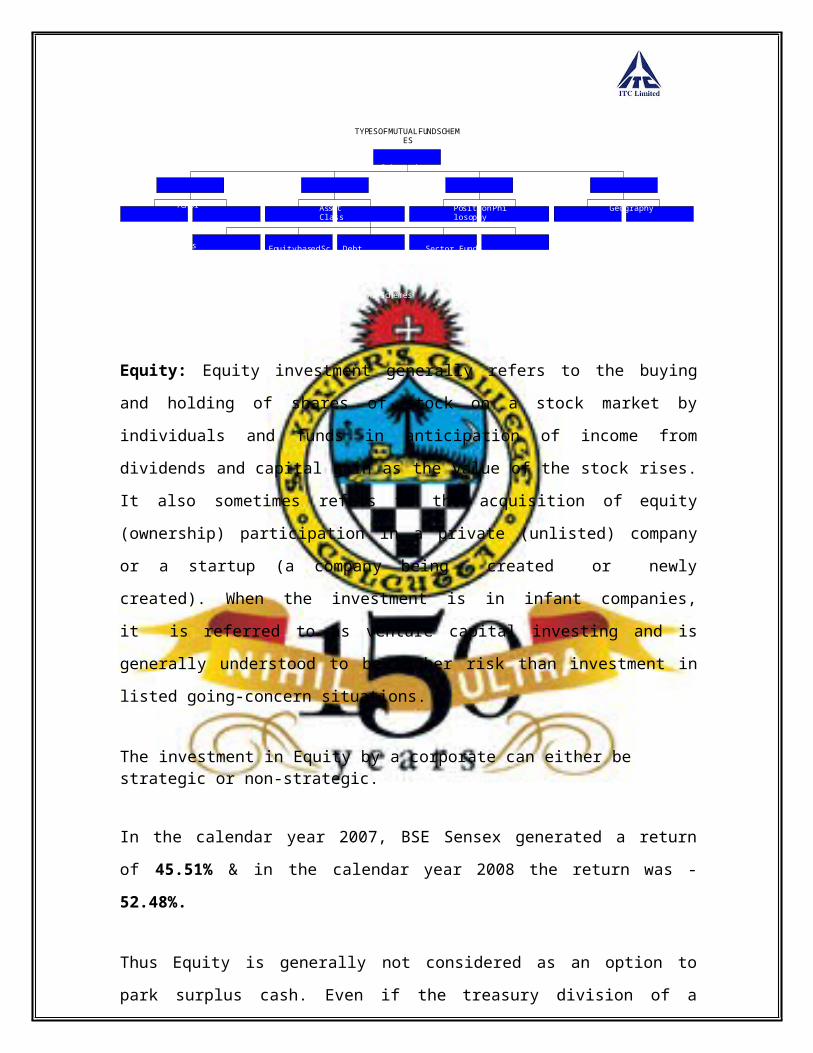

4.1.1.1. Types of Schemes

MF schemes can be offered with any of a range of investment objectives, each

corresponding to a certain point in the risk-return matrix. In a broad sense, they can be

classified on the basis of –

Tenor Asset Class Position Philosophy Geography

Page 21

Classification on Time Basis

a. Open-End Schemes - These are schemes that do not have a fixed maturity. The

MF ensures liquidity by announcing sale and repurchase price for the units of an

open-end scheme on an ongoing basis. Investors who wish to exit from an open-

end scheme can offer their units to the MF for redemption, generally called

repurchase. Similarly, the MF can sell new units to investors desirous of

participating in the scheme, generally called sale. Every such transaction goes to

change the unit capital of the scheme.

Additionally, the MF can choose to provide liquidity through listing of the

scheme in the stock market. In such a scenario, investors can either trade in the

market or opt for the sale and repurchase route.

Open mutual funds generally do not deploy in illiquid investments, as they are

liable to redeem the investors‘ money at a very short notice. Also, the average

maturity of the portfolio of an open mutual fund is also very low which makes it

easy for the fund to liquidate its assets at a very short notice without any

appreciable losses.

b. Closed-End Schemes - A closed mutual fund, as the name suggests, has

restrictions on the minimum holding period and the investor is required to pay a

penalty in the form of load if he wants to redeem his investment without fulfilling

the minimum holding period criteria. As a closed mutual fund invests in securities

which are susceptible to market risk, entry / exit in securities is planned by the

fund manager based on the minimum time period committed by the investor.

Since a fund may suffer losses if the investor redeems his investment prematurely,

there is a need to put restrictions on free entry / exit by investors in the scheme.

Page 22

Generally, such funds offer better returns than open-ended funds as they can

deploy in relatively risky instruments and also in instruments, which have higher

average maturity and enjoy the steepness of the yield curve. Occasionally,

closed-end schemes provide a repurchase option to investors, either for a specified

period or after a specified period, normally up to a total limit for all investors

together, or a limit per investor.

Classification on Asset Class Basis

a. Equity Schemes – Equity schemes invest primarily in equities. While mutual

funds most often invest in the stock market, fund managers do not just buy any

old stock they find attractive. Some funds specialize in investing in large-cap

stocks; others in small-cap stocks, and still others invest in what has left - mid-cap

stocks. Equity schemes invest the bulk of their corpus in equity shares or equity

linked instruments and the balance in cash.

Depending on the scheme objective, investments could be in growth stocks where

earnings growth is expected to be attractive, or momentum stocks that go up or

down in line with the market, or value stocks where the fund manager is of the

view that current valuations in the market do not reflect intrinsic value, or income

stocks that earn high returns through dividends.

b. Debt/Income Schemes – Debt instruments invest in debt instruments, i.e., bonds

and cash. They are of the following types:

1. Gilt Schemes – A gilt scheme or a government securities scheme invests

only in government bonds, which may typically account for 80-85 percent

of the corpus, and cash that may account for the balance. Gilt schemes

may be dedicated to gilts of varying maturities – long-term, medium-term

and short-term.

Page 23

2. Bond Schemes - These securities invest in bond securities issued by the

Government or any other issuer.

3. Junk Bond Schemes – These invest in securities that are below the

investment grade. However, attractive returns in such poor quality

investments would more than make up for the higher risk of losing the

entire investment in some cases.

4. Money Market/Liquid Schemes – These schemes invest in short term

debt instruments. Money market funds have relatively low risks, compared

to other mutual funds (and most other investments). By law, they can

invest in only certain high-quality, short-term investments.

Money market funds pay dividends that generally reflect short-term

interest rates, and historically the returns for money market funds have

been lower than for either bond or stock funds. That's why "inflation risks"

— the risk that inflation will outpace and erode investment returns over

time — can be a potential concern for investors in money market funds.

5. Balanced Schemes - Balanced schemes invest in a mix of equity and debt.

The debt instruments ensure a basic interest income, which the fund

manager hopes to top up with capital gains on the investment portfolio.

However, losses can eat into the basic interest income and capital.

The greatest benefit of a balanced investment program is that it makes risk

more palatable. An allocation to bonds moderates the short-term volatility

of stocks, giving the risk-averse long-term investor the confidence to

sustain a heavy allocation to equities.

Page 24

Classification on Position Philosophy Basis

a. Sector Funds – Regular equity funds invest in a mix of equities that are spread across

different sectors. Thus they are often referred to as Diversified Equity Funds. Sector

funds, on the other hand, are expected to invest only in a specific sector. For instance, an

energy fund would only invest in energy companies.

b. Index Funds – These funds seek to have a position that replicates an identified index,

BSE Sensex or NSE Nifty. Such a position can be created using either of the two

methods given below.

Maintaining an investment portfolio that replicates the composition of

a chosen index can do it. Thus, the stocks in such a fund‘s portfolio

would be the same as are used in calculating the index. The proportion

of each stock in the portfolio too would be the same as the weight of

the stock in the calculation of that index. This replicating style of

investment is called ‗passive investment‘. Index funds are thus oftencalled passive funds. Funds that are not passive are managed funds.

Index schemes are also referred to as unmanaged schemes or tracker

schemes since they seek to track a specific index. Passive investment

places lower demands on the time and efforts of the AMC. All that is

required is a good system that would integrate the valuation of

securities from the market and information of sales and repurchases of

units as well as generate the requisite buy/sell orders. Thus,

management fees are lower for index funds as compared to managed

schemes.

Alternately, a mutual fund, through its research can identify a basket

of securities and/or derivatives whose movement is similar to that of

the index. Schemes that invest in such baskets can be viewed as active

index funds.

Page 25

seeks to beat the performance of its benchmark index by at least 0.1 percent, but no more

than 2 percent.

d. Exchange Traded Funds – These are open-end funds that can be traded on the

exchange at any time throughout the course of the day. Like index funds, they are

benchmarked to a stock exchange index. Though, the legal structure and makeup vary

around the world, the major common features include:

An exchange listing and ability to trade continually.

They are index-linked rather than actively managed.

Through dynamic and quantitative strategies, these can be dynamic

rather than static indexing strategies.

The ability to handle contributions and redemptions on an in-kind

basis (typically in large blocks of shares only).

Their 'value' (but not necessarily the price at which they trade—they

can trade at a 'premium' or 'discount' to the 'underlying' assets' value)

derives from the value of the 'underlying' assets comprising the fund.

These qualities provide ETFs with some significant advantages compared with traditional

open-ended collective investments. The ETF structure allows for a diversified, low cost,

low turnover index investment. This appeals to both institutional and retail investors both

for long-term holding and for selling short and hedging strategies

e. Fixed Maturity Plans/Serial Schemes – Investors in debt securities get their expected

yield if they hold fixed coupon debt securities until maturity. But, if they sell their

securities earlier, then what they recover would depend on the market situation at the

time of sale. They could end up with either a capital gain or a capital loss.

Fixed maturity plans (FMPs) seek to eliminate the risk of such capital loss by investing

exclusively in a pre-specified debt security. On maturity, the scheme would redeem the

security and pay the investor. The investor, however, can exit earlier. But the investor‘srecovery would depend on the market situation at the time of his/her exit. Thus, investors

Page 26

are assured of a fixed return, if they stay invested in the scheme for the period originally

envisaged. They also have an earlier exit option, in case they invest in an FMP that is

structured as an open-ended scheme.

When a series of FMPs are issued for different maturities, they are called Serial Funds.

These can choose to invest exclusively in government securities, in which case they

become Serial Gilts. Alternatively, they can invest in non-government securities, in

which case they become Serial Bond Schemes.

f. Hedge/Leveraged Funds - A hedge fund is a fund that can take both long and short

positions, use arbitrage, buy and sell undervalued securities, trade options or bonds, and

invest in almost any opportunity in any market where it foresees impressive gains at

reduced risk. Hedge fund strategies vary enormously -- many hedge against downturns in

the markets -- especially important today with volatility and anticipation of corrections in

overheated stock markets. The primary aim of most hedge funds is to reduce volatility

and risk while attempting to preserve capital and deliver positive returns under all market

conditions.

Key Characteristics of Hedge Funds

Hedge funds utilize a variety of financial instruments to reduce risk, enhance

returns and minimize the correlation with equity and bond markets. Many hedge

funds are flexible in their investment options (can use short selling, leverage,

derivatives such as puts, calls, options, futures, etc.).

Hedge funds vary enormously in terms of investment returns, volatility and risk.

Many, but not all, hedge fund strategies tend to hedge against downturns in the

markets being traded.

Many hedge funds have the ability to deliver non-market correlated returns.

Many hedge funds have as an objective consistency of returns and

capital preservation rather than magnitude of returns.

Page 27

Experienced investment professionals who are generally disciplined and

diligent manage most hedge funds.

Pension funds, endowments, insurance companies, private banks and high net

worth individuals and families invest in hedge funds to minimize overall portfolio

volatility and enhance returns.

Most hedge fund managers are highly specialized and trade only within their area

of expertise and competitive advantage.

Hedge funds benefit by heavily weighting hedge fund managers‘ remuneration

towards performance incentives, thus attracting the best brains in the investment

business. In addition, hedge fund managers usually have their own money

invested in their fund.

While the name hedge funds‘ gives a psychological comfort of a fund being on low risk,

the truth is very different from it. Hedge funds are leveraged funds where the fund

manager invests a mix of funds belonging to its investors (unit capital and reserves) and

funds from lenders (borrowed funds). A leveraging of 2 would imply that for every Re.1

of unit capital, an additional Rs.2 is borrowed, thus investing Rs.3 in the market.

Borrowed funds have interest and repayment obligations that are independent of how the

market performs. Thus, in adverse market conditions, a non-leveraged fund only needs to

bear a loss. However, a leveraged fund would also need to generate additional resources

to meet the interest and repayment obligations on borrowed funds. Thus, hedge funds are

extremely risky funds, the level of risk being a function of the extent of leveraging.

a. Option Income Fund – This refers to a type of mutual fund, which attempts to

increase current income through continual option writing. There are two

implications for an option writer:

If the stock of a company rises above the price, the investor would

exercise his/her option in which case the option writer would lose out on

the opportunity of gaining from that appreciation (opportunity loss

Page 28

If the option writer operates on a fully hedged basis, then he/she will retain

the shares of the company in the portfolio, so that they can be offered if

the investor exercises his/her option. During the period that the option

writer holds the share, the dividend would belong to him/her (holding

income).

Classification on Geography Basis

a. Country/Region Funds – These funds invest in securities from a specific country or

region. The underlying belief is that the chosen country or region is expected to

demonstrate superior performance, which in turn, would be favorable for the securities of

that country. The returns on country funds are affected not only by the performance of the

market where they are invested but also by the changes in exchange rates.

b. Offshore Funds – These funds mobilize moneys from investors for investment outside

the country.

Classification on Investment Objective Basisa. Aggressive Growth Funds – This means that investors will be buying into stocks that

have a chance for dramatic growth and may gain value rapidly. This type of investing

carries a high element of risk with it since stocks with dramatic price appreciation

potential often lose value quickly during downturns in the economy. It is a great option

for investors who do not need their money within the next 5 years, but have a more long-

term perspective. This option should not be chosen if capital conservation is being looked

at. Instead, it should be chosen when one could afford to potentially lose the value of

one‘s investment.

b. Growth Funds – As with aggressive growth, growth seeks to achieve high returns.

However, the portfolios will consist of large, medium and small sized companies. The

fund portfolio chooses to invest in stable, well established, blue-chip companies together

with a small portion in small and new businesses. The fund manager would pick growth

stocks, which will use their profits to grow rather than to pay out dividends. It is a

Page 29

medium to long-term commitment. However, they are perhaps more beneficial in the

long-term.

c. Growth and Income Funds – A combination of growth and income funds, also

known as balanced funds, is that which has a mix of goals. They seek to provide investors

with current income while still offering the potential for growth. Some funds buy stocks

and bonds so that the portfolio will generate income whilst still keeping ahead of

inflation. They are able to achieve multiple objectives desirable to the investors. They

have a low to moderate stability along with a moderate potential for current income and

growth.

d. Income Funds – These funds will generally invest in a number of fixed income

securities. This will provide investors with regular income. The fund manager would

choose to buy debentures, company fixed deposits, etc. in order to provide investors with

a steady income. Despite being a stable option, it has some risk components. As interest

rates go up or down, the prices of income fund shares, particularly bonds, move in the

opposite direction. This makes income funds, interest rate sensitive.

e. Money Market Mutual Fund – The most cautious investor should opt for this type,

which aims at maintaining capital preservation. This indicates that gains would not be an

option even though the interest rates given on these funds could be higher than that of

bank deposits. These funds pose very little risk but at the same time would not protect the

investors‘ initial investments‘ buying power. They are highly liquid enabling investors to

alter their investment strategies.

Since the whole project revolves around Liquid & Liquid Plus schemes, this two schemes

require more explanation.

Liquid & Liquid Plus or Ultra Short Term (or Treasury Advantage)

Liquid Fund: Liquid funds are used primarily as an alternative to short-term fix deposits.

Liquid funds invest with minimal risk (like money market funds). Most funds have a

Page 30

lock-in period of a maximum of three days to protect against procedural (primarily

banking) glitches, and offer redemption proceeds within 24 hours.

Liquid funds score over short term fix deposits. Banks give a fixed rate in the range 5%-

5.5% p.a. for a term of 15-30 days. Returns from deposits are taxable depending on the

tax bracket of the investor, which considerably pulls down the actual return. Dividends

from liquid funds are tax-free in the hands of investor, which is why they are more

attractive than deposits.

Liquid Plus or Ultra Short Term (or Treasury Advantage): The Mutual Fund industry

has created an Income Scheme, where lower Dividend Distribution Tax (DDT) is

applicable called Liquid Plus Scheme. These schemes are positioned between the liquid

scheme and the Short Term Income scheme with respect to the risk return matrix. The

focus of these schemes is to optimize portfolio yield through a judicious mix of short

duration and MTM assets. Average portfolio maturity of these schemes is around 6 to 12

months. They maintain MTM portion at around 5-10%.

The differences between this two schemes are-

1. Investment tenure

This is the major differentiating factor between liquid and Ultra Short Term funds. The

debt instruments held by Ultra Short Term funds have a longer tenure than liquid funds

i.e. the portfolios of Ultra Short Term funds have a higher average maturity than those of

liquid funds. In effect, while investors can invest in liquid funds for as briefly as one day,

the holding period for Ultra Short Term funds should be higher than that.

2. Exit load

Both liquid and Ultra Short Term funds can be redeemed within a day. However, if Ultra

Short Term funds are redeemed within a specified period, there can be an exit load (the

minimum investment tenure and the exit load varies across fund houses). On the other

hand, there is no exit load on liquid funds.

Page 31

Page 32

In order to generate higher yields, some of these Ultra Short Term Schemes have exit

loads ranging from 0.05% - 0.25% and a lock-in period of 5-15 days. This is to

discourage investors having 1-5 day’s surplus from entering these schemes that may

impact the overall returns.

3. Dividend distribution tax

Ultra Short Term funds are more tax efficient than liquid funds. In terms of tax

implications, a dividend distribution tax of 28.3250% is charged on liquid funds, whereas

it‘s 22.6600% for Ultra Short Term funds.

4. Risk

Ultra Short Term funds are riskier vis-a -vis liquid funds. This is mainly due to two

reasons a) Ultra Short Term funds hold investments that have a higher maturity and b)

there is no limit on the mark-to-market (MTM) component of Ultra Short Term funds as

opposed to a maximum of 10% MTM limit on liquid funds.

Since Ultra Short Term Schemes take exposure in longer maturity papers, they carry an

additional amount of risk while generating higher returns. However, since the proportion

of MTM element is generally in between 10-15% in the entire portfolio, there shall not be

any major impact on the returns and are expected to deliver returns at least equal to that

of Liquid Schemes on a consistent basis.

Holiday NAV

Traditional Liquid Schemes have the concept of previous day NAV, which implies that

the funds get invested on a day before actual investment letter along-with fund transfer

advice is given to Mutual Fund AMC. Hence funds can be deployed on the basis of actual

surplus in the banks on a particular day.

However, Ultra Short Term Schemes have same day NAV that implies that investments

made on any business day before the normal cut-off timings shall get NAV of the

Page 33

investment date and the actual outflow of funds will take place on the next working day.

Also, there is no Holiday NAV for these schemes. In this case the funds needs to be

deployed based upon the estimated surplus collections for next day by means of a cheque,

which shall be banked on the next working day. Further, the funds may be switched from

Liquid/Short Term Floater Schemes for deployment in Ultra Short Term Schemes.

Additionally, the days on which Ultra Short Term Schemes don‘t declare NAV (i.e.

Holiday NAV), the surplus collection for those days be first deployed in Liquid/Short

Term Floater Schemes and subsequently switched to Ultra Short Term Schemes.

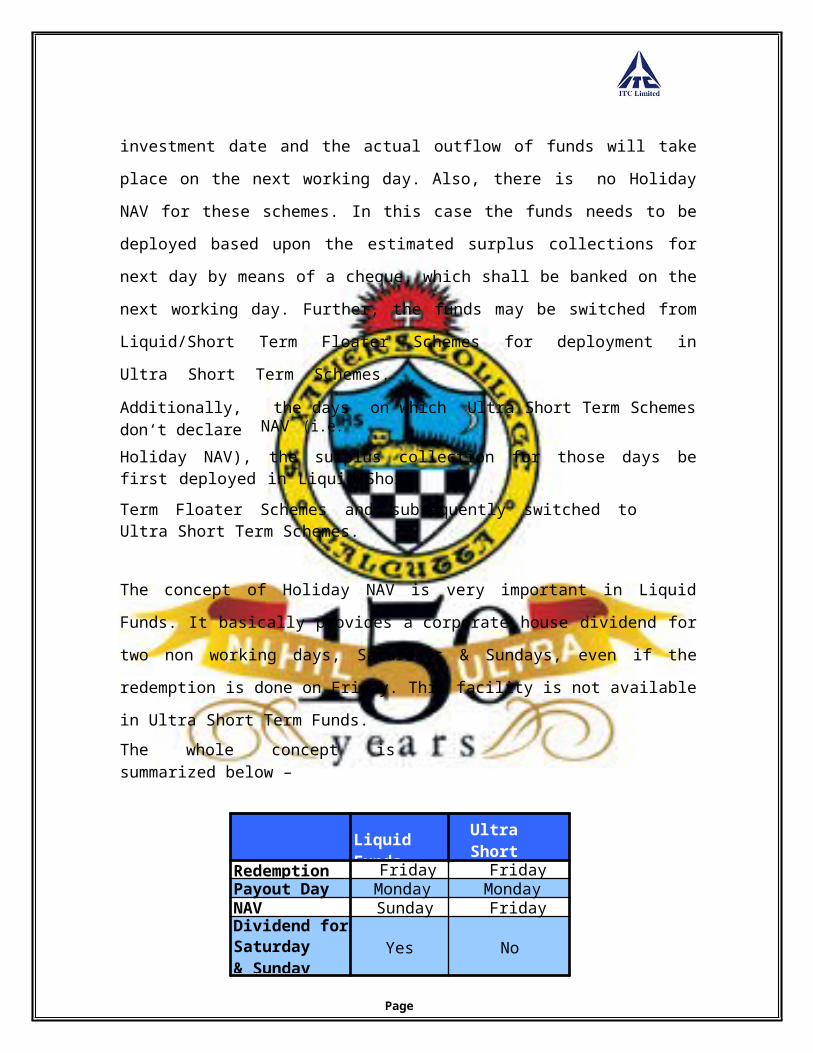

The concept of Holiday NAV is very important in Liquid Funds. It basically provides a

corporate house dividend for two non working days, Saturdays & Sundays, even if the

redemption is done on Friday. This facility is not available in Ultra Short Term Funds.

The whole concept is summarized below –

Liquid FundsUltra ShortTerm Funds

Redemption Day Friday FridayPayout Day Monday MondayNAV Applicable Sunday FridayDividend forSaturday & Sunday

Yes No

Page 34

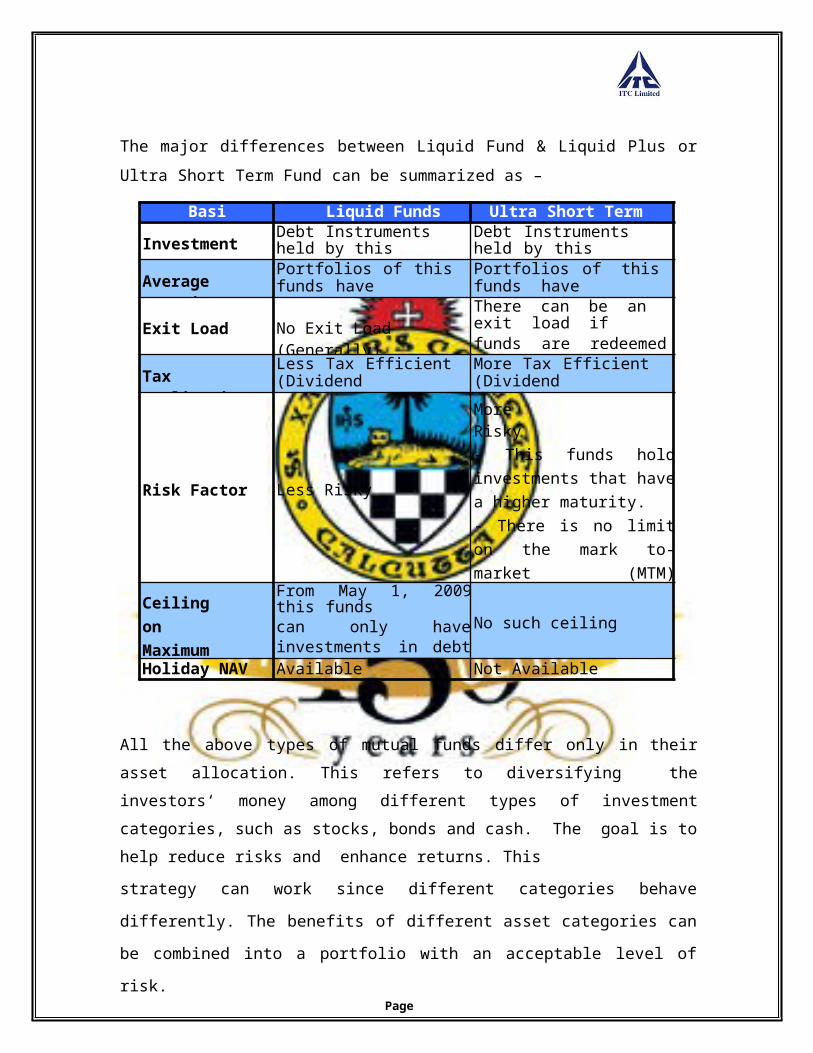

The major differences between Liquid Fund & Liquid Plus or Ultra Short Term Fund can

be summarized as –

Basis Liquid Funds Ultra Short Term Funds

Investment TenureDebt Instruments held by thisfunds have shorter tenure

Debt Instruments held by thisfunds have Longer tenure

Average MaturityPortfolios of this funds havelower average maturity

Portfolios of this funds havehigher average maturity

Exit Load No Exit Load (Generally)There can be an exit load iffunds are redeemed within a specified time (Generally)

Tax ImplicationsLess Tax Efficient (DividendDistribution Tax of 28.325%)

More Tax Efficient (DividendDistribution Tax of 22.66%)

Risk Factor Less Risky

More Risky- This funds hold investments that have a higher maturity.- There is no limit on the mark to-market (MTM) component of liquid plus funds as opposed to the 10% MTM limit on liquid funds.

Ceiling on Maximum maturity

From May 1, 2009 this fundscan only have investments in debt instruments of three months tenure

No such ceiling

Holiday NAV Available Not Available

All the above types of mutual funds differ only in their asset allocation. This refers to

diversifying the investors‘ money among different types of investment categories, such as

stocks, bonds and cash. The goal is to help reduce risks and enhance returns. This

strategy can work since different categories behave differently. The benefits of different

asset categories can be combined into a portfolio with an acceptable level of risk.

Page 35

4.1.1.2. Advantages

1. Portfolio Diversification: Mutual Funds leads to diversification of risks. As

corporate can choose schemes based on the risk appetite. When the market is

volatile Mutual Funds gives huge options to investors. There are index funds,

which capture the return of entire index. There are also sector-based schemes,

which invest, only in that particular sector like banking sector, FMCG etc.

2. Professional management: Qualified investment professionals who seek to

maximize returns and minimize risk monitor investor's money. It is the Fund

Manager's job to (a) find the best securities for the fund, given the fund's stated

investment objectives; and (b) keep track of investments and changes in market

conditions and adjust the mix of the portfolio, as and when required.

3. Reduction in transaction costs: It reduces the overall transaction fee for the

corporate. As they normally invest in liquid funds for their daily cash

management, there are many investments, redemptions and sweep into other

schemes from the existing one on a daily basis. If the investments are done

directly on the underlying security there will be huge costs involved and hence

less returns.

4. Liquidity: Normally corporate investors invest in open-ended schemes with no

lock in period. Investments are mainly done keeping in mind their working capital

needs. Thus normally those schemes are chosen which are liquid and on

redemptions can sell their underlying securities easily.

5. Tax Benefits: Corporate investors choose the mutual fund route to invest their

surplus cash because it is tax efficient. The tax rate on Liquid schemes is 28.325%

and on Liquid Plus it is 22.66%. Thus in both the cases it is less than the 33.33%,

which is corporate tax rate for profits earned.

4.1.1.3. Disadvantages

1. No control over costs: A corporate investor pays less expense compared to retail

investors. But the rate remains same how ever large the investment is. Fund

managers charge a hefty fee for his professional management and that is not

dependent on the kind of returns, which the scheme is generating.

2. No tailor made portfolios: The schemes which are there in the market cannot be

customized based on the risk appetite of the corporate. A corporate might invest

in a scheme, which has a high percentage of AA papers in the portfolio to increase

their return whereas another corporate might not invest in those schemes

considering them volatile and hence risky.

3. No say on the management: A corporate investor has no say on the management

of mutual fund schemes even if he owns the maximum permissible 20% of the

asset under management.

4.1.2. Investment Alternatives for Surplus Cash

When corporate invests their temporary cash, the main emphasis lies on

Capital preservation &

Return optimization.

Keeping these two factors in mind the major alternatives could be –

Bank fixed deposits

Corporate fixed deposits

Corporate bonds

Mutual Funds

Equity

Real Estate

Bullion

Financial Derivatives

Page 36

Bank fixed deposits: It is a money deposit at a banking institution that normally cannot

be withdrawn before a certain "term" or period of time. When the term is over it can be

withdrawn or it can be held for another term. Generally speaking, the longer the term the

better the yield on the money. A certificate of deposit is a time-deposit product.

These deposits are stringently regulated and banks operate under stricter requirements

regarding Stuatory Liquidity Ratio (SLR) & Cash reserve Ratio (CRR).

Bank Deposits up to Rs 1,00,000 are protected by the Deposit Insurance and Credit

Guarantee Corporation (DICGC), as long as bank has paid the requisite insurance

premium of 5 paise per annum for every Rs 100 of deposits.

The factors to consider while investing in Bank Fixed Deposits are –

Prevailing Interest rate and hence CRR.

Inflation

Tax Rate.

Currently the interest rates for a 15 day Fixed Deposit hovers between 3.00-3.50% per

annum and for a 30-45 days Fixed Deposit, it ranges between 4-5%.

The tenure for which a company parks its surplus cash primarily depends upon the

working capital requirements and the prevailing interest rate scenario.

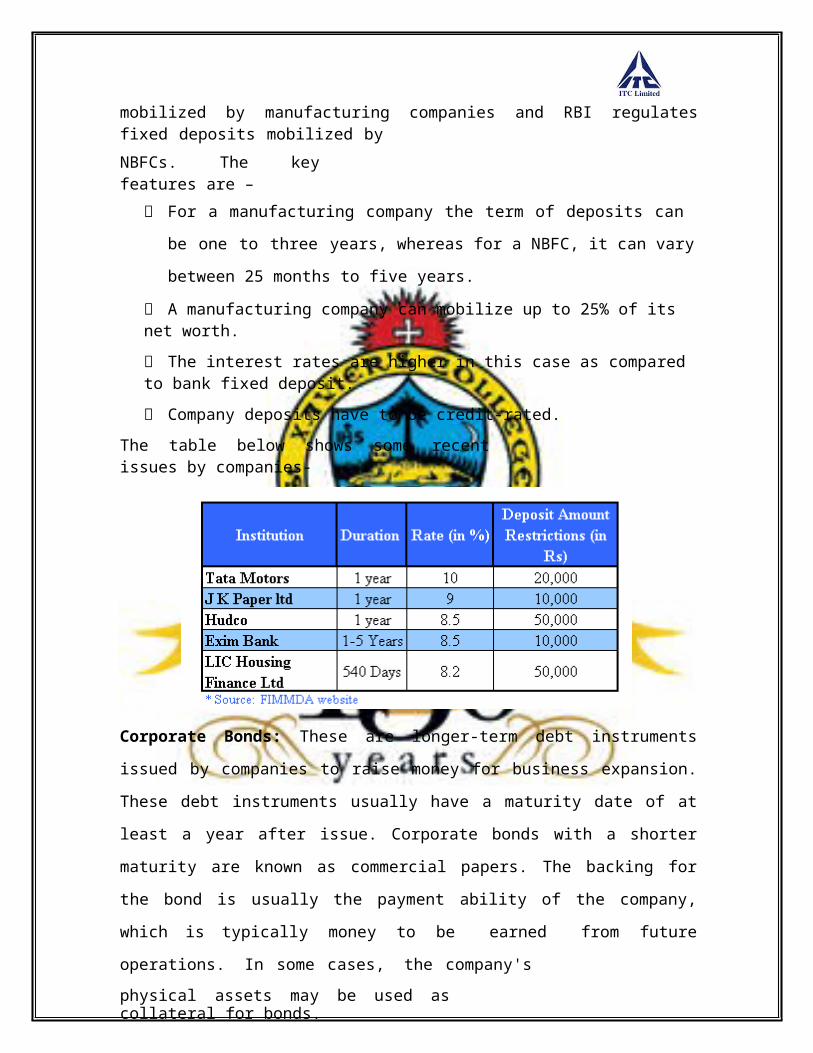

Corporate Fixed Deposits: Fixed deposits are unsecured borrowings by the company

accepting the deposit. The Company Law Board (CLB) regulates fixed deposits

Page 37

mobilized by manufacturing companies and RBI regulates fixed deposits mobilized by

NBFCs. The key features are –

For a manufacturing company the term of deposits can be one to three years,

whereas for a NBFC, it can vary between 25 months to five years.

A manufacturing company can mobilize up to 25% of its net worth.

The interest rates are higher in this case as compared to bank fixed deposit.

Company deposits have to be credit-rated.

The table below shows some recent issues by companies-

Corporate Bonds: These are longer-term debt instruments issued by companies to raise

money for business expansion. These debt instruments usually have a maturity date of at

least a year after issue. Corporate bonds with a shorter maturity are known as commercial

papers. The backing for the bond is usually the payment ability of the company, which is

typically money to be earned from future operations. In some cases, the company's

physical assets may be used as collateral for bonds.

Page 38

Some of the AAA bonds are presented below –

* Source: FIMMDA website

Corporate bonds are considered higher risk than government bonds. As a result, interest

rates are almost always higher, even for top-flight credit quality companies.

Here are some benefits of corporate bonds:

1. Attractive yields: Corporations generally offer higher yields than government

bonds of the same maturity.

2. Dependable income: Corporate bonds offer investors the opportunity of a steady

income, while preserving the principal.

3. Safety: Credit rating agencies, like S&P and Moody, rate corporate bonds

according to associated risk and rewards. Ratings reflect the capability of the

issuing authority to deliver timely returns. The higher the rating, the safer the

investment.

4. Diversity: An investor can choose from a variety of sectors and credit-quality

characteristics.

5. Marketability: Most corporate bonds sell easily and quickly due to the market‘s

size and liquidity.

Page 39

6. Put Benefit: When interest rate rises in the market, the subscriber to the issue

would not like to stick with the bond paying lower coupon rate. In this scenario

investors dump the bonds with lower coupon rate and subscribe to the issue with

higher returns.

While corporate bonds offer a higher yield than some other investments, they are also

accompanied by higher risks. These include:

1. Interest Rate Risk: Interest rate movements can significantly reduce the value of

the bond.

2. Credit Risk: Corporate bonds are not secured by collateral. Thus an investor

faces the risk of a corporation failing to meet the debt obligation.

3. Event Risk: Corporate bonds have exposure to event-based risks. Corporate

reshuffles, takeovers or restructuring have far reaching consequences on the credit

rating and price of such bonds.

4. Call Risk: Callable corporate bonds can be a nightmare when the issuer declares

the purchase of bonds after a stipulated time period. Corporations usually call off

a high-yielding bond when interest rates plummet. This gives the company a

chance to reissue bonds at lower interest rates. In such cases, an investor receives

only the par value of the bond.

Mutual Funds: Instead of directly buying equity shares and/or fixed income instruments,

one can participate in various schemes floated by mutual funds, which, in turn, invest in

equity shares and fixed income securities. There are three broad types of mutual fund

schemes:

Equity Schemes

Debt Schemes

Balanced Schemes

MF schemes can be offered with any of a range of investment objectives, each

corresponding to a certain point in the risk-return matrix. In a broad sense, they can be

classified on the basis of –

Page 40

TYPESOFMUTUALFUNDSCHE

MES

Schemesbasedo

n

Tenor Asset Class

PositionPhilosophy

Geography

OpenEndSchemes

CloseEndSchemes

EquitybasedSchemes

Debt basedSchemes

Sector Funds

IndexFunds

OffshoreFund RegionFund

Gilt Schemes BondSchemes JunkBondSchemes MoneyMarket Schemes BalancedSchemes

Equity: Equity investment generally refers to the buying and holding of shares of stock

on a stock market by individuals and funds in anticipation of income from dividends and

capital gain as the value of the stock rises. It also sometimes refers to the acquisition of

equity (ownership) participation in a private (unlisted) company or a startup (a company

being created or newly created). When the investment is in infant companies, it is

referred to as venture capital investing and is generally understood to be higher risk than

investment in listed going-concern situations.

The investment in Equity by a corporate can either be strategic or non-strategic.

In the calendar year 2007, BSE Sensex generated a return of 45.51% & in the calendar

year 2008 the return was -52.48%.

Thus Equity is generally not considered as an option to park surplus cash. Even if the

treasury division of a corporate house invests in Equity, it is merely for the purpose of

return maximization or the investment in strategic in nature. The quantum of investment

in equity compared to debt market is very less for surplus cash management.

Page 41

The movement of sensex in both Bull & Bear phase is shown for highlighting the

volatility in the market –

Page 42

Real Estate: Real estate is basically defined as immovable property such as land and

buildings. The investment in real estate essentially depends on the risks associated with

it, that is to say, even if the venture succeeds when the future stream of income will

accrue to the investor and the alternative investment opportunities. Real estate investment

can be attractive if viewed as a business opportunity; it can generate rental income, using

it as collateral to secure a loan for a business venture, to offset otherwise taxable income

through cash savings on tax-deductible interest rate losses, or simply from the profits

garnered from its resale. Notable, in this context is the gains reaped by real estate

speculators who trade in real estate futures (by buying and selling purchase options).

Precious Objects: Precious objects are items that are generally small in size but highly

valuable in monetary terms. Today, many investors use precious metals, or their stocks,

as a hedge against massive inflation. The important precious objects are:

Gold and silver

Precious stones

Art objects

The advantages of Precious Metals as an investment are –

Precious metals are an excellent hedge against inflation. Historically, gold, silver,

and platinum have been accepted as standards of value. During periods of

hyperinflation, their prices rise accordingly to keep pace.

Precious metal stocks, like other stocks, can be easily bought and sold on major

stock exchanges, giving them a high measure of liquidity.

Owning shares in a precious metal company is an easy way to invest in precious

metals without having to physically buy and hold the actual commodities.

The disadvantages of Precious Metals as an investment are –

Like collectibles, precious metals do not earn interest.

Precious metal prices are greatly influenced by the actions of governments. For

example, if Russia (the world's major producer of platinum) were to decide to sell

off its stockpiles of the metal in order to raise capital, the price of platinum

worldwide would drop.

Page 43

Financial Derivatives: A financial derivative is an instrument whose value is derived

from the value of an underlying asset. It may be viewed as a side bet on the asset. Options

and futures are the most important financial derivatives from the point of view of

investors.

Based on the basic knowledge of several investment avenues as mentioned above, it is

possible to compare them in terms of the key investment attributes, namely, rate of

return, risk, marketability, tax shelter. A summarized table is being given below –

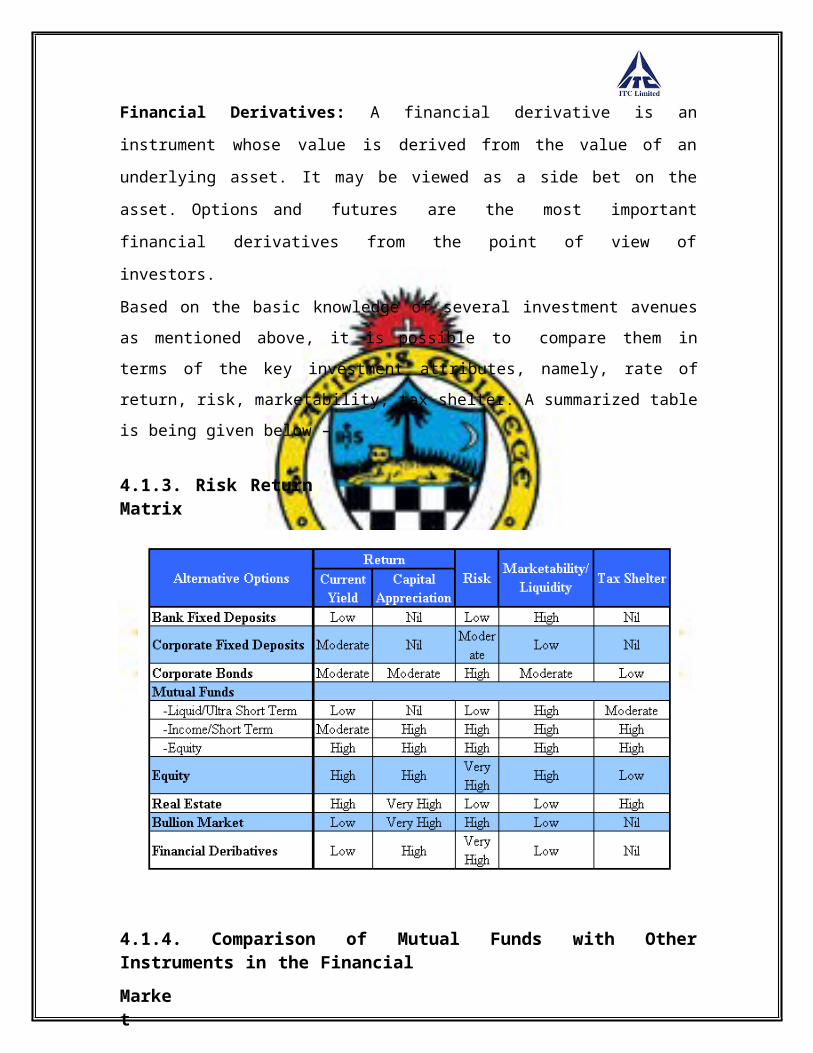

4.1.3. Risk Return Matrix

4.1.4. Comparison of Mutual Funds with Other Instruments in the Financial

Market

Company Fixed Deposits Vs Mutual Funds – Fixed deposits are unsecured borrowings

by the company accepting the deposit. Credit rating of the fixed deposit instrument is an

indication of the inherent default risk in the investment.

The moneys of investors in a mutual fund scheme are invested by the AMC in specific

investments under that scheme. These investments are held and managed in-trust for the

Page 44

benefit of the scheme‘s investors. On the other hand, there is no direct correlation

between a company‘s fixed deposit mobilization, and the avenues where these resources

are deployed.

A corollary of such linkage between mobilization and investment is that the gains and

losses from the mutual fund scheme entirely flow through to the investors. Therefore,

there can be no certainty of yield, unless a named guarantor assures a return, or, to a

lesser extent, if the investment is in a serial gilt scheme. On the other hand, the return

under a fixed deposit is certain, subject only to the default risk of the borrower.

Both fixed deposits and mutual funds offer liquidity, but subject to certain differences as

given below:

The provider of liquidity in the case of fixed deposits is the borrowing company.

In mutual funds, the liquidity provider is the scheme itself as in the case of open-

end schemes, or the market as in the case of closed-end schemes.

The basic value at which fixed deposits are en cashed is not subject to market risk.

However, the value at which units of a scheme are redeemed entirely depends on

the market. If securities have gained in value during the period, then the investor

can even earn a return that is higher than what he/she anticipated at the time of

investment. Conversely, a loss could also result.

Early encashment of fixed deposits is always subject to a penalty charged by the

company that accepted the fixed deposit. Mutual fund schemes also have the

option of charging a penalty on early redemption of units by way of an exit load.

If the NAV appreciates adequately, then despite the exit load, the investor could

earn a capital gain on the investment.

Bank Fixed Deposits Vs Mutual Funds – Bank fixed deposits are similar to company

fixed deposits. The major difference is that banks are more stringently regulated than are

companies. They even operate under stricter requirements as far as statutory liquidity

ratio (SLR) and cash reserve ratio (CRR) are concerned.

While the above causes a lot of comfort, bank deposits are also subject to default risk.

However, given the political and economic impact of bank defaults, the Government as

well as the Reserve Bank of India (RBI) tries to ensure that banks do not fail.

Page 45

Bonds and Debentures Vs Mutual Funds – As in the case of fixed deposits, credit

rating of the bond/debenture is an indication of the inherent default risk in the investment.

However, unlike fixed deposits, bonds and debentures are transferable securities. While

an investor may have an early encashment option from the issuer, generally liquidity is

through a listing in the market. Its implications are :

If the security does not get traded in the market, then the liquidity remains on

paper. In this respect, an open-end scheme offering continuous sale/repurchase

option is superior.

The value that the investor would realize in an early exit is subject to market risk.

The investor could have a capital gain or a capital loss. This aspect is similar to

that of a mutual fund scheme.

It is possible for an astute investor to earn attractive returns by directly investing in the

debt market, and actively managing the positions. Given the market realities in India, it is

difficult for most investors to actively manage their debt portfolio. Further, at times, it is

difficult to execute trades in the debt market even when the transaction size is as high as

Rs.1 crore. In this respect, investment in a debt scheme would be beneficial.

Debt securities could be backed by a hypothecation or a mortgage of an identified fixed

and/or current assets (secured bonds/debentures). In such a case, if there is a default, the

identified assets become available for meeting redemption requirements. An unsecured

bond/debenture is for all practical purposes like a fixed deposit, as far as the access to

assets is concerned.

A custodian for the benefit of the investors in the scheme holds the investments of a

mutual fund scheme. Thus, the securities that relate to a scheme are ring-fenced for the

benefit of its investors.

Equity Vs Mutual Funds – Investment in both equity and mutual funds are subject to

market risk. An investor holding an equity security that is not traded in the market place

has a problem realizing value from it. But investment in an open-end mutual fund

eliminates this direct risk of not being able to sell the investment in the market. An

indirect risk remains, because the scheme has to realize its investments to pay investors.

The AMC is however in a better position to handle the situation.

Page 46

4.2. Stage 2

After understanding the Mutual Fund Industry and the major players involved in the

market. The second stage of the project was to study the methodology of ranking Mutual

Fund schemes used by the Credit Rating Agencies (CRISIL & ICRA), Internet site

It basically benchmarks a mutual fund scheme vis-à-vis its peers.

It serves as a guide to investors in selecting schemes for asset allocation.

It takes into account both NAV & the portfolio of the schemes.

The ranking is done at the end of each quarter and displayed in the website

(w w w. c risi l . c o m ).

Methodology

Since the analysis was related only to the Liquid & Liquid plus schemes of the Mutual

Funds. The same was only studied for the CRISIL-CPR. The salient points are presented

below-

Only those schemes are included in the ranking which satisfies the following –

o Full portfolio disclosure for the preceding three months.

o One year NAV for the Liquid & Liquid plus category of Mutual Funds.

o Average Asset Under Management (AUM) is calculated based on the last

months average from the date of ranking. For the Liquid and Liquid plus

the cut off set is – Liquid (Institutional) – 100 crores

Liquid (Super Institutional) – 150 crores Liquid Plus or Ultra Short Term (Institutional) – 100 crores Liquid Plus or Ultra Short Term (Super Institutional) – 150 crores

For consistent CRISIL-CPR category a scheme has to consistently feature in all

quarterly rankings for the last 5 years time frame.

Page 47

The performance of a scheme is judged on the following parameters –

o Superior Returns Score: It gives the relative measure of the return & the

risk for the schemes within a peer group. For Liquid & Liquid plus

category, the SRS is calculated for one year, though normally SRS is

calculated for non-debt schemes of Mutual Funds. The steps involved in

calculation are-

Daily return of the scheme within the peer group is calculated for

the period of analysis.

The daily average of this return is the peer average return for this

scheme.

The difference between daily peer average and the scheme daily

return is calculated, this is the differential return series for the

scheme.

The average return divided by the standard deviation of the

differential return is the Superior Return Score.

The tope performer gets the rank of 1 while others are ranked in

descending order.

o Mean return & Volatility: It is mostly calculated for debt schemes of

Mutual funds as they show less volatility. It is calculated as follows-

Mean return is calculated for the period of I year for each of the

schemes.

Standard Deviation of daily return is considered as volatility.

One-year period is broken down into 4 periods of three months; the

recent 3 months are given the maximum weightage.

o Portfolio Concentration: Portfolio of the funds are analysed in detail as

the Indian Debt Market is still evolving.

Securities belonging to companies in the Manufacturing, Banks,

Deposits & Securitized papers will have an individual issuer

Page 48

specific threshold. The rationale behind doing this is to penalize

the additional risk being taken by investing higher proportions in

an individual company‘s debt security over and above the specifiedthreshold.

o Liquidity: Liquidity measures the ease with which an investor can convert

an investment to cash without a material adverse impact on either capital

or return. All corporate bonds in the portfolio are divided into three

categories based on CRISIL Fixed Income Research Team.

Liquid

Semi-Liquid

Illiquid

o Asset Quality: In the case of debt portfolio, asset quality plays an

important role driving the probability of an investor getting repayments on

principal and interest in full and in time. Asset quality is evaluated as – Based on its 20-year history of rating default and statistics

maintained by it.

Based on its rating and when it is not available, a view is taken

based on the available information.

o Average Maturity: The CRISIL-CPR is silent on this.

o Downside Risk Probability: It measures the probability of the investment

getting lower returns then short tenure risk free securities. Risk free return

as taken as the 91-day T bill yield over the period.

o Asset Size: Anything above the cut off is better.

o Historic Performance in the CRISIL-CPR: It is important to judge a

consistent performer.

Page 49

CRISIL-CPR Category Definitions –

4.2.2. ICRA online methodology for ranking mutual fund schemes

ICRA ONLINE Mutual Fund (MF) Rankings seek to inform investors and MF

intermediaries of the category-wise relative performance of MF schemes. The rankings,

covering the two time horizons of one and three years, have been arrived at following an

in-depth analysis of critical parameters, including: risk-adjusted performance; portfolio

concentration characteristics; liquidity; corpus size; average maturity; and portfolio

turnove

Eligibility Criteria for Ranking

The Net Asset Value (NAV) of the MF scheme should have been disclosed daily

during the period covered by the ranking.

In the case of one-year ranking, complete disclosure of monthly portfolio should