55

Table of Contents 1 | Page

| Date post: | 26-Dec-2015 |

| Category: |

Documents |

| Upload: | vubon-minu |

| View: | 1,034 times |

| Download: | 2 times |

Table of Contents

1 | P a g e

Executive Summary

The case ‘The Timken Company’ is about the acquisition of the Torrington from ‘Ingersoll-Rand’ by the

Timken Company. Torrington produces the best quality bearing while the Timken has many wings where

bearing is an important division of their business. Both these companies has 5% of product and 80% of

customers redundancy. After the acquisition Timken will be world’s third largest bearing company.

The main point of this case is how the payment for this acquisition will be made. Expected value of this

acquisition is estimated $800 million. How Timken will pay this large amount is the main question here.

Timken can borrow or can issue stock for this amount. But this large debt will affect Timken’s leverage

ratio, as well as Timken’s investment grading in the market. Another option for Timken is to offer stock

in exchange for the purchase. But still Timken will be needing cash for this acquisition to be complete.

However we have found several circumstances of the financing opportunities for this acquisition which

will affect the value of Timken. we analyzed various risk related to these financing like Interest Rate Risk,

Overall Business Risk, Financial Risk, Degree of Financial Leverage, and Bankruptcy Risk, Du point ratio.

After calculating the NPV of the financing options we have run simulation technique for the potential

investment. We have tried to focus on the best option for the acquisition that will increase the value of

the firm most.

2 | P a g e

Introduction

Objective of the study

Usually we gather theoretical knowledge from course material. But it is also very much important to

relate that theoretical knowledge with practical situation. The basic objective of conducting this case

analysis is applying our theoretical knowledge in practical situation. The objective behind conducting this

study is as follows:

To analyze the ‘The Timken Company’ scenario

To analyze the acquisition of Torrington from Ingersoll Rand

Analyze the financing of the acquisition

Finding out the synergy of the acquisition

Scope of the study

The study topic allows us to analyze the cases named “The Timken Company” We have gone through

the case thoroughly, analyzed the problems of this company and tried to find out solutions of these

problems. Finally we have reached recommendations that will help to take the decision. Some external

information has been used for lack of information provided.

Methodology

For preparing our report we went through the text and information collected from case and applied our

sense of finance which we gained from different course especially from corporate finance and capital

budgeting to evaluate and justify our assigned topic. All the data used in this report have been gathered

from the case. Financial techniques taught in our BBA and MBA courses have been used here. Some

reasonable assumptions have been made because of lack of information provided.

3 | P a g e

To analyze and solving the problem Free cash flow method.

Crystal ball software is to complete the simulation analysis

Limitations of the study

The limitations of the study are defined by the extensive of the facts covered by the study and those

that left out. Learning all functions, moods of business, risk factors and protective covenants were quite

tough within specified time framework. There was also time constraint. While attempting to solve the

problem we have to assume some factors. The analysis could have been better if those data were

provided

Case Briefing

The Timken Company is one of the largest bearing companies in the industry. The company was

established in 1898 by Henry Timken. During the long life of the company the company faced many ups

and downs in the life cycle. In 1982 the company suffered its first loss since depression for the increasing

amount of competition. During the year followed the company engaged in joint venture. In 2002 the

company decided to acquire ‘Torrington’ Company from ‘Ingersoll-Rand’. This acquisition would make

The Timken Company world’s third largest bearing company.

Through the acquisition the Timken Company would be able to produce bearing with lower cost,

Timken’s worldwide brand value and world class distribution will produce high quality bearing with

lowest possible cost. Potential annual cost saving from the consolidating manufacturing facilities is

expected to be $80 million.

4 | P a g e

The main challenge for The Timken Company is how the acquisition will be paid. Timken has two options

for the financing of this acquisition:

1. Issuing debt; but this debt issue will affect the Timken’s leverage ratio enough to virtually

guarantee that Timken would lose its investment grade rating.

Equity issuance; Timken’s last issuance occurred in 1987,for this huge analysis is needed for the

issuance and the no. of share issuance will have to be double since it’s last issuance to raise the

amount needed.

Both this for the cash payment or they can

2. Offer stock along with the cash payment for this acquisition

Participators of the Acquisition

The Timken Company

As a global industrial technology leader, Timken apply deep knowledge of metallurgy, friction

management and power transmission to improve the reliability and efficiency of machinery all around

the world.

They engineer, manufacture and market mechanical components and high-performance steel. Their

bearings, engineered-steel bars and tubes -- as well as transmissions, gearboxes, chain and related

products and services -- support diversified markets worldwide.

With $4.3 billion sales in 2013 and approximately 19,000 people operating from 28 countries, Timken

makes the world more productive and keeps industry in motion.

5 | P a g e

The Ingersoll Rand

With a history dating back to 1871, Ingersoll Rand and its family of brands represents a proven history in

construction and mining, industrial and commercial markets.

Through acquisitions, innovations and customer focus, today's Ingersoll Rand offers market-leading

solutions and services that enable customers to create progress through a variety of industries and

markets that touch everyday life.

Ingersoll Rand (NYSE:IR) advances the quality of life by creating comfortable, sustainable and efficient

environments. Their people and their family of brands—including Club Car®, Ingersoll Rand®, Thermo

King® and Trane®—work together to enhance the quality and comfort of air in homes and buildings;

transport and protect food and perishables; and increase industrial productivity and efficiency. They are

a global business committed to a world of sustainable progress and enduring results.

Torrington

Torrington is best known for its Torrington needle bearings and Torrington thrust bearings. All

Torrington bearings are made using special lubrication and duplex cutting in order to ensure that they

are all the same size, which helps reduce friction and makes the bearing assembly last much longer.

Torrington is somewhat more expensive than some of its competitors, however, none of them compare

in quality and longevity to Torrington

6 | P a g e

Economic Analysis:

Like a battered champion in a heavyweight boxing match, the U.S. economy rose, staggered, took a knee

then resumed fighting in 2002. The roaring recovery of early January gave way to fear of a ‘doubledip’

recession by midsummer. But by fall it appeared the U.S. economy had weathered a second recession

GDP

GDP growth in the first quarter of 2002 caught everyone by surprise. GDP jumped a staggering 5% in the

first quarter after a respectable 2.7% in 2001:4. Coming out of the 1990 recession the U.S. conomy grew

2.3%, 1.0% and 2.2% in the first three quarters after the recession ended. While large growth rates are

not uncommon after a severe recession such as 1981, 5% growth is unusual coming out of such a

shallow recession as we had in 2001. The massive interest rate cuts enacted by the Federal Reserve

during 2001 were finally showing up in the data in the form of spending.

Stock Market

After the recession of late 2001, the U.S. stock market appeared to recover its legs in early 2002. In early

March, the Dow Jones Industrial Average was at 10,700 –only 7% lower than its all-time peak.

The massive flight to safety drove up prices on bonds and drove down bond yields. Suddenly, earning 1-

2% on a savings account didn’t look too bad. Savings deposits at banks jumped a staggering 22% from

2001:10-2002:10 as households moved assets out of the equity markets into safe, liquid assets. This

provided the funds in the banking system to finance consumer durables and housing in the second half

of 2002.

Consumption

If historians look back at 2002 and try to explain how the U.S. recovered from the 2001 recession they

will clearly see that it was on the backs of the U.S. consumer. Fueled by low interest rates and the

mortgage-refinancing boom during the summer, consumer spending grew at impressive quarterly rates

7 | P a g e

(annualized) of 4%, 2.2%, 1.22% and 2.95% over the past year. Quarter to quarter, real personal

consumption expenditures increased 4.2 percent in the third quarter, compared with an increase of 1.8

percent in the second quarter. Durable goods boom waned by the end of the year raising concerns that

whatever consumption growth we saw in 2002 could disappear as we move into 2003.

Investment

After six consecutive quarters of negative growth, gross private investment finally showed some life in

the first half of the year but turned negative again in the third quarter. Non-residential investment

contracted during the first half the year. Residential investment grew respectably in the first half but fell

off during the third quarter. Inventories jumped 2.6% and 1.3% in the first half of the year after six

quarters of contraction as businesses rebuilt good stocks in the belief that the recession was over.

Government expending & Taxes

Standard economic wisdom suggests that the federal government should increase spending during a

recession to dampen the decline in output. From 2001:3-2002:3, the U.S. government clearly did its part

(due also in no small part to the war on terrorism). Real federal government spending increased from

$568.9 billion in 2001:3 to $613.1 billion in 2002:3 – a 7.7% increase for the period. However, almost

80% of that ($35 billion) went to national defense. Whether or not defense spending aimed at fighting

terrorism stimulates the U.S. economy is an open question. Transfer payments increased 9.8% during

the same period as more people relied on welfare and unemployment compensation to get them

through tough economic times.

Inflation & Unemployment

Inflation remained well under control in 2002. The Consumer Price Index increased a mere 1.5% from

2001:9-2002:9. The GDP deflator, a broader measure of inflation increased a mere 1% over 2002. As a

result, low inflation gives the monetary and fiscal authorities substantial room to pursue expansionary

policies if need be. The unemployment rate increased through the first half of 2002 hitting 6% for the

first time since 1994. However, by the fall of 2002, the unemployment rate began dropping and was at

5.7% by October 2002. The median duration of unemployment also climbed in the first half of the year

8 | P a g e

to 11.7 weeks before falling to 9.6 in October. This is nearly double the 6 weeks duration observed in the

last year of the nineties expansion

Industry Analysis

Porter’s 5 forces Analysis

Porters five forces model is a helpful tool to assess the relative attractiveness and risks inherent in an

industry. So with porters five forces model it will be attempted to analyze different components of

riskiness of this industry.

Figure: Porter’s five forces Bearing Industry

9 | P a g e

Threat of new entrants: Low

Rivalry among existing competitor:

High

Threat of substitute products:

Low

Bargaining power of buyers:

Moderate

Bargaining power of sellers: Moderate

Threats of new entrants: Low

Market is segmented to large companies. These company comprise of majority of the total

market

Required huge capital investment

Brand image is required

Rivalry among existing firms: High

There are some major competitors exists in the market

Severe economic and competitive pressure

Increasing demand of the existing firms

Threat of substitute products: Low

No proper substitute products exist; bearing is very important elements for automotive &

mechanical industry; substitute is not a strong option for this industries.

Bargaining power of buyers: Moderate

High switching cost

Low cost products available in the market

Threat of dumping by foreign producers

Bargaining power of suppliers: Moderate

Availability of suppliers in the market

No scope for forward integration

High maintenance of raw materials are required

10 | P a g e

Company Analysis

The company was founded by Henry Timken in St. Louis in 1899 and incorporated as The Timken Roller

Bearing Axle Company. In 1898, Henry Timken obtained a patent for the tapered roller bearing. Timken

influences the fundamentals of motion through the creation, transfer and control of power. Imagine the

possibilities and multitude of applications where power must be generated, transferred or monitored.

For more than 100 years, Timken has refined the science of managing friction. From Ploeisti, Romania to

Bangalore, India and beyond, Timken operates 9 technology and engineering centers dedicated to

developing solutions for customers’ toughest application problems.

Market Segments

Timken serve many diverse market segments, including aerospace, automotive, construction, consumer,

defense, energy, industrial equipment, health, heavy industry, machine tool, positioning control, power

generation and rail.

Joint Ventures

o CoLinx, LLC – Greenville, SC, U.S.A. (PTplace.com)

o S.E. SETCO Service Co. – Norcross, GA, U.S.A.

o Timken XEMC (Hunan) Bearings Co., Ltd. – Xiangtan, China

11 | P a g e

Strategic Analysis

The Timken team will continue to transform business and

create unparalleled value for customers, investors,

communities and other stakeholders. They:

Applying Knowledge

Using knowledge of metallurgy, friction management and

mechanical power transmission to create unique solutions

used in demanding applications

Differentiate Products

offering a broad array of mechanical power transmission components, high-performance steel and

related solutions and services

Expanding Reach

Extending knowledge, products, services and channels to meet customer needs, wherever they are in

the world

Perform with Excellence

Delivering exceptional results with a passion for superior execution

SWOT Analysis

12 | P a g e

Strength

Custom-Made products for the buyers

Sharing 80% customer with Torrington

Familiar industry of both the acquirer and acquired firm

Acquisition will reduce the production cost

Weakness

Issuing debt for acquisition will affect the leverage ratio of Timken

High debt to equity ratio

Higher price of Torrington’s products relative to market

Opportunity

Strong brand value in the market

Acquisition will set the stage for international growth

International distribution network

Market leadership will give the opportunity to negotiate with suppliers and sellers

13 | P a g e

Threat

Non-favorable bearing industry policy

Threat of dumping by foreign producers

Highly competitive market

14 | P a g e

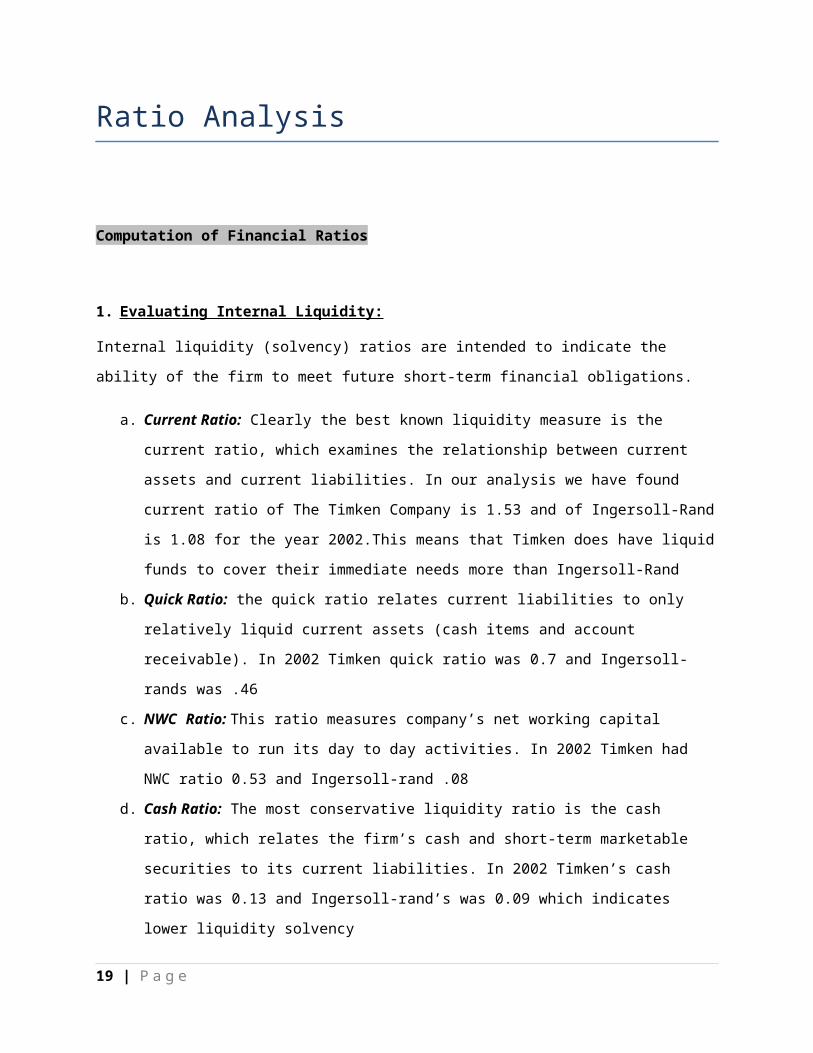

Ratio Analysis

Computation of Financial Ratios

1. Evaluating Internal Liquidity:

Internal liquidity (solvency) ratios are intended to indicate the ability of the firm to meet future short-

term financial obligations.

a. Current Ratio: Clearly the best known liquidity measure is the current ratio, which examines the

relationship between current assets and current liabilities. In our analysis we have found current

ratio of The Timken Company is 1.53 and of Ingersoll-Rand is 1.08 for the year 2002.This means

that Timken does have liquid funds to cover their immediate needs more than Ingersoll-Rand

b. Quick Ratio: the quick ratio relates current liabilities to only relatively liquid current assets (cash

items and account receivable). In 2002 Timken quick ratio was 0.7 and Ingersoll-rands was .46

c. NWC Ratio: This ratio measures company’s net working capital available to run its day to day

activities. In 2002 Timken had NWC ratio 0.53 and Ingersoll-rand .08

d. Cash Ratio: The most conservative liquidity ratio is the cash ratio, which relates the firm’s cash

and short-term marketable securities to its current liabilities. In 2002 Timken’s cash ratio was

0.13 and Ingersoll-rand’s was 0.09 which indicates lower liquidity solvency

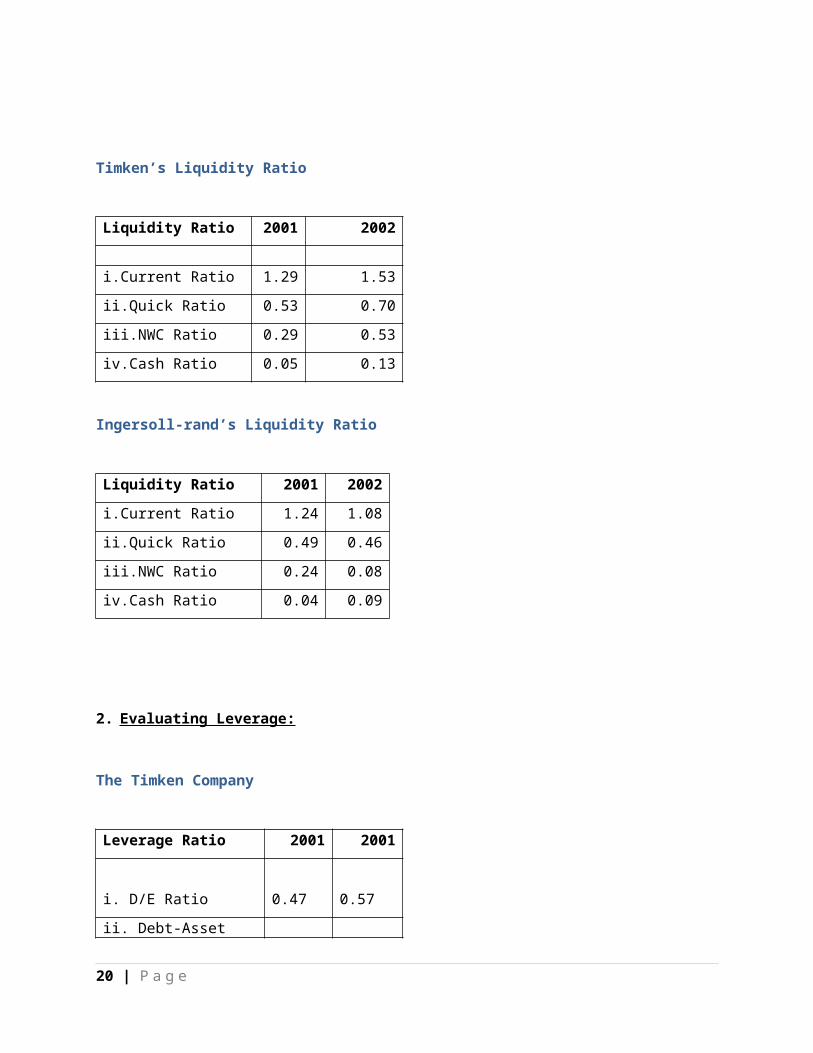

Timken’s Liquidity Ratio

Liquidity Ratio 2001 2002

i.Current Ratio 1.29 1.53

ii.Quick Ratio 0.53 0.70

iii.NWC Ratio 0.29 0.53

iv.Cash Ratio 0.05 0.13

15 | P a g e

Ingersoll-rand’s Liquidity Ratio

Liquidity Ratio 2001 2002

i.Current Ratio 1.24 1.08

ii.Quick Ratio 0.49 0.46

iii.NWC Ratio 0.24 0.08

iv.Cash Ratio 0.04 0.09

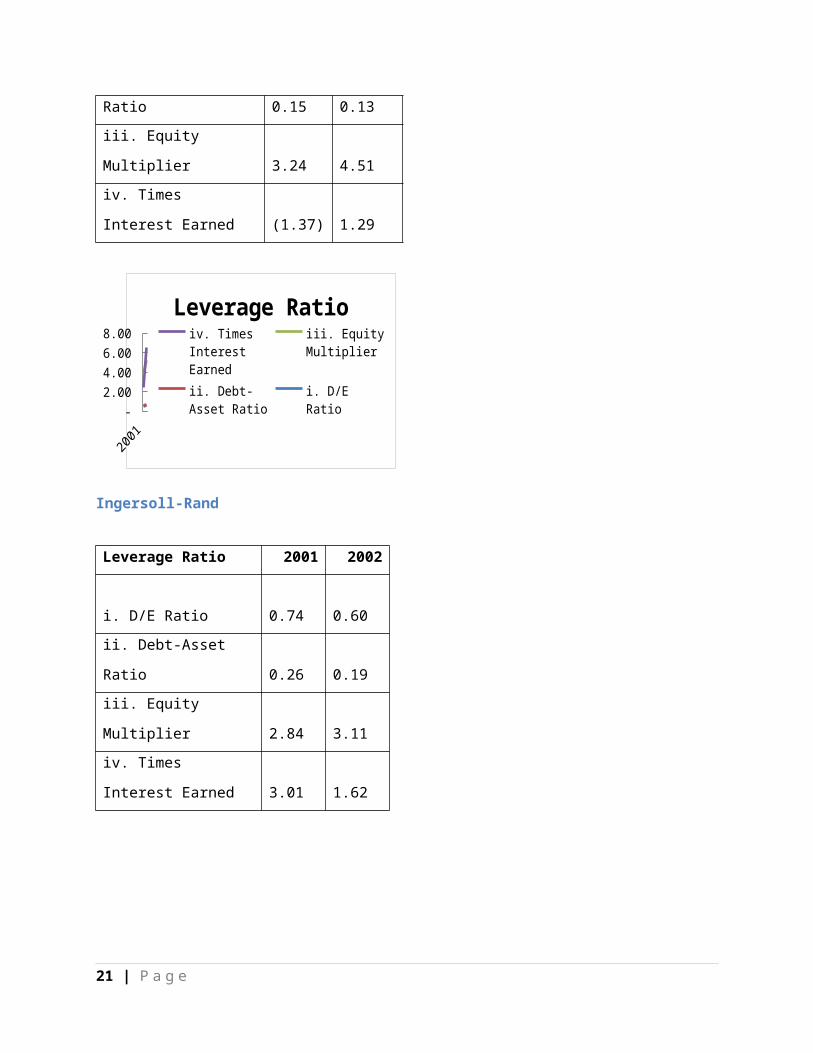

2. Evaluating Leverage:

The Timken Company

Leverage Ratio 2001 2001

i. D/E Ratio

0.47

0.57

ii. Debt-Asset Ratio

0.15

0.13

iii. Equity Multiplier

3.24

4.51

iv. Times Interest Earned

(1.37)

1.29

2001 2001 -

1.00 2.00 3.00 4.00 5.00 6.00 7.00

Leverage Ratioiv. Times Interest Earnediii. Equity Mul-tiplierii. Debt-Asset Ra-tioi. D/E Ratio

16 | P a g e

Ingersoll-Rand

Leverage Ratio 2001 2002

i. D/E Ratio

0.74

0.60

ii. Debt-Asset Ratio

0.26

0.19

iii. Equity Multiplier

2.84

3.11

iv. Times Interest Earned

3.01

1.62

- 2.00 4.00 6.00 8.00

Leverage Ratioiv. Times In-terest Earned

iii. Equity Mul-tiplier

ii. Debt-Asset Ratio

i. D/E Ratio

3. Profitability Ratios:

The Timken Company

Profitability Ratio 2001 2002

i. Net Profit Margin -0.02 0.02

ii. ROE -0.05 0.06

iii. ROA -0.02 0.01

17 | P a g e

2001 2002

-0.10

-0.05

0.00

0.05

0.10

Profitability Ratio

i. Net Profit Marginii. ROEiii. ROA

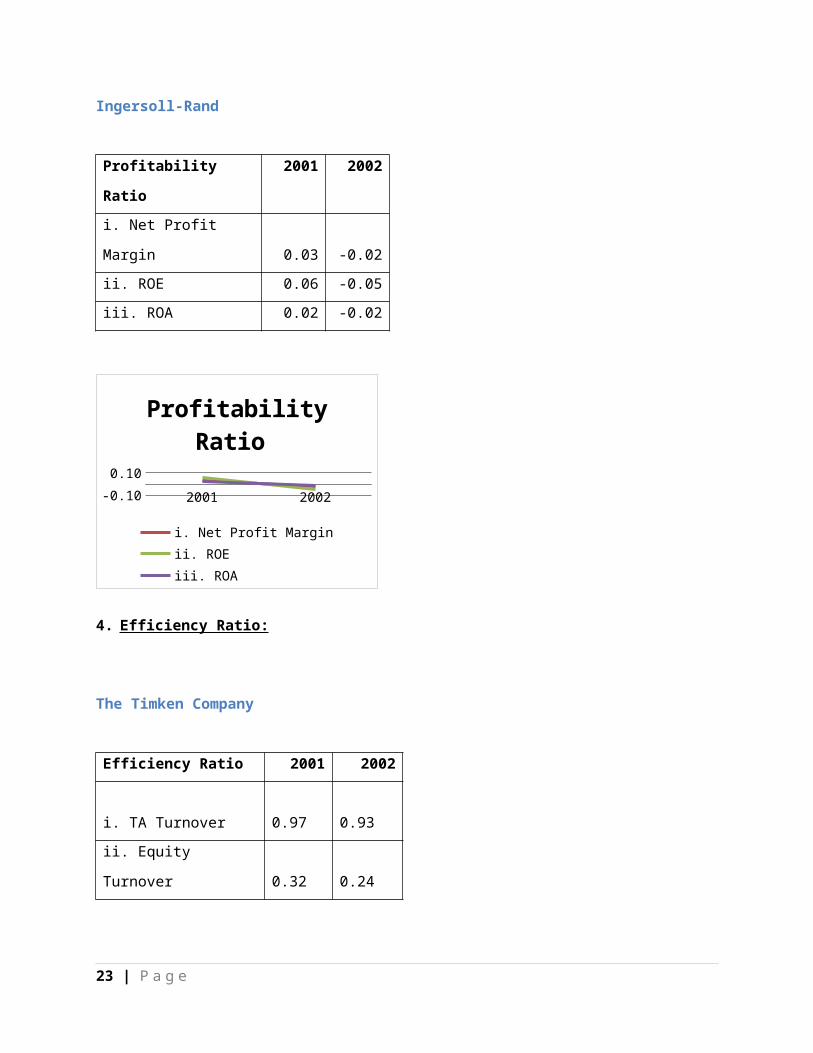

Ingersoll-Rand

Profitability Ratio 2001 2002

i. Net Profit Margin 0.03 -0.02

ii. ROE 0.06 -0.05

iii. ROA 0.02 -0.02

2001 2002

-0.10

-0.05

0.00

0.05

0.10

Profitability Ratio

i. Net Profit Marginii. ROEiii. ROA

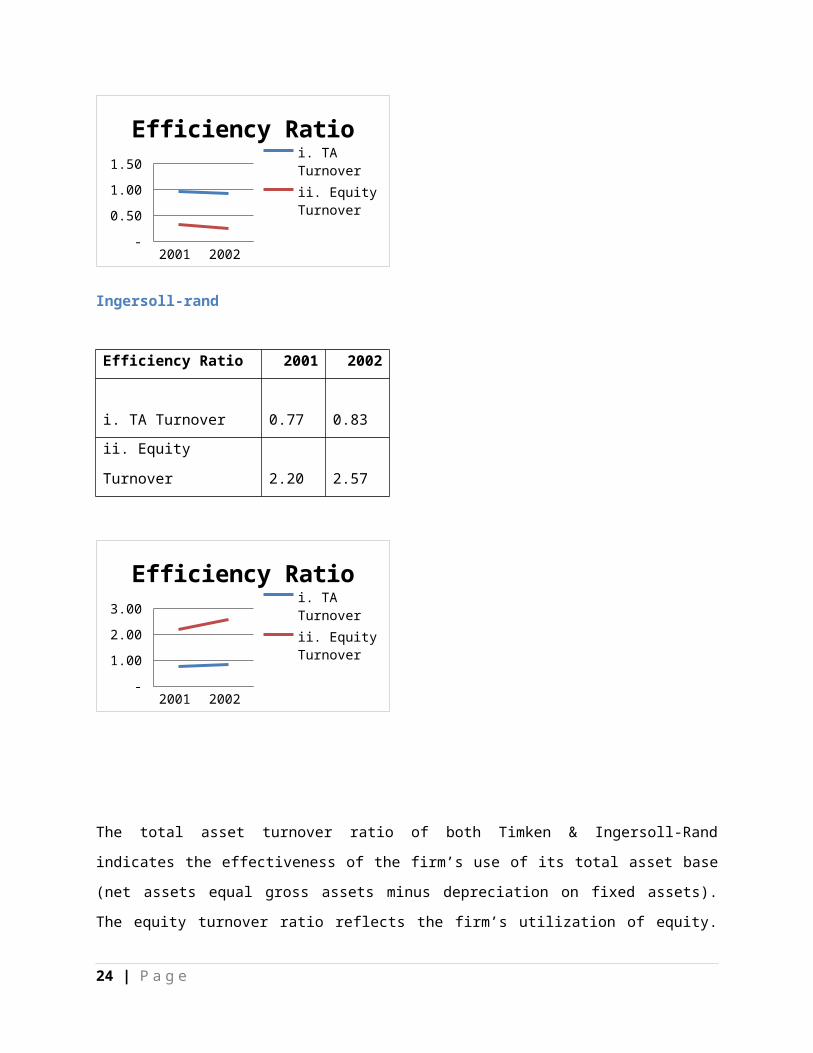

4. Efficiency Ratio:

The Timken Company

18 | P a g e

Efficiency Ratio 2001 2002

i. TA Turnover

0.97

0.93

ii. Equity Turnover

0.32

0.24

2001 2002 -

0.20 0.40 0.60 0.80 1.00 1.20

Efficiency Ratio

i. TA Turnoverii. Equity Turnover

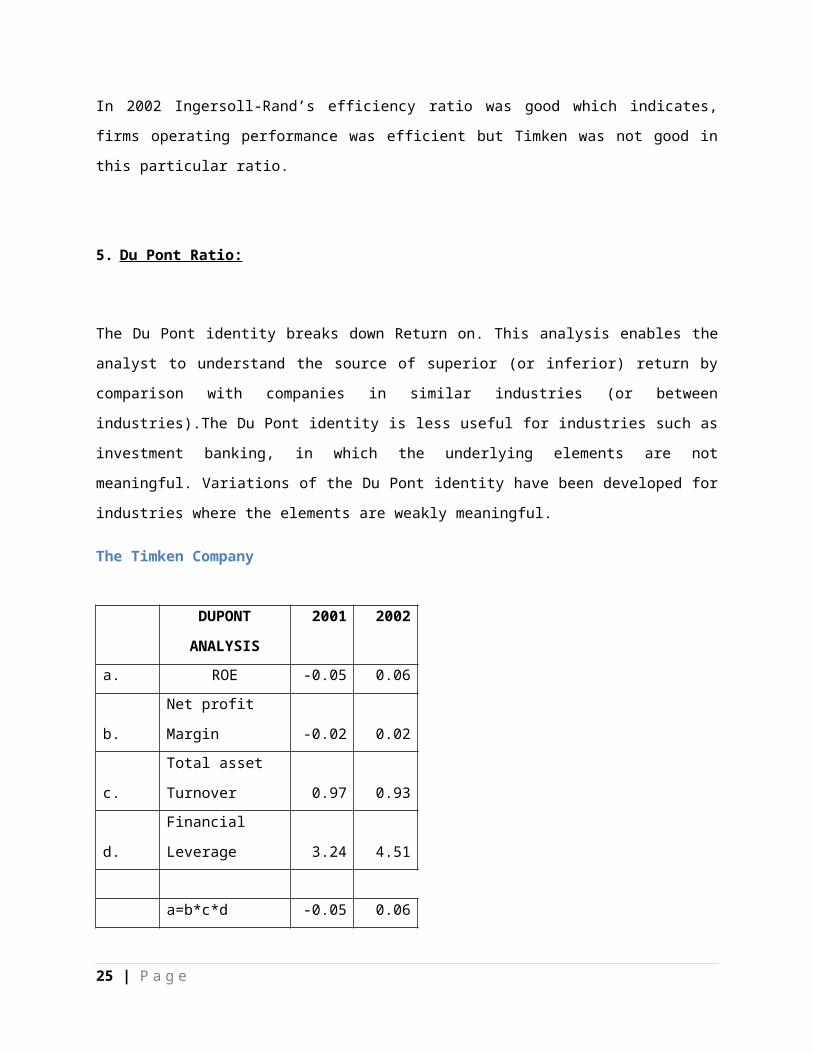

Ingersoll-rand

Efficiency Ratio 2001 2002

i. TA Turnover

0.77

0.83

ii. Equity Turnover

2.20

2.57

2001 2002 -

0.50 1.00 1.50 2.00 2.50 3.00

Efficiency Ratio

i. TA Turnoverii. Equity Turnover

19 | P a g e

The total asset turnover ratio of both Timken & Ingersoll-Rand indicates the effectiveness of the firm’s

use of its total asset base (net assets equal gross assets minus depreciation on fixed assets). The equity

turnover ratio reflects the firm’s utilization of equity. In 2002 Ingersoll-Rand’s efficiency ratio was good

which indicates, firms operating performance was efficient but Timken was not good in this particular

ratio.

5. Du Pont Ratio:

The Du Pont identity breaks down Return on. This analysis enables the analyst to understand the source

of superior (or inferior) return by comparison with companies in similar industries (or between

industries).The Du Pont identity is less useful for industries such as investment banking, in which the

underlying elements are not meaningful. Variations of the Du Pont identity have been developed for

industries where the elements are weakly meaningful.

The Timken Company

DUPONT ANALYSIS 2001 2002

a. ROE -0.05 0.06

b. Net profit Margin -0.02 0.02

c.

Total asset

Turnover 0.97 0.93

d. Financial Leverage 3.24 4.51

a=b*c*d -0.05 0.06

20 | P a g e

2001 2002

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

Dupont ratio

ROENet profit MarginTotal asset TurnoverFinancial LeverageSeries5a=b*c*d

Ingersoll-Rand

DUPONT ANALYSIS 2001 2002

a. ROE 0.06 -0.05

b. Net profit Margin 0.03 -0.02

c.

Total asset

Turnover 0.77 0.83

d. Financial Leverage 2.84 3.11

a=b*c*d 0.06 -0.05

2001 2002 -0.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Dupont ratio

ROENet profit MarginTotal asset TurnoverFinancial LeverageSeries5a=b*c*d

21 | P a g e

6. ALTMAN Z Score Analysis:

The Z-score formula for predicting bankruptcy can be used to predict the probability that a firm will go

into bankruptcy within two years. Z-scores are used to predict corporate defaults and an easy-to-

calculate control measure for the financial distress status of companies in academic studies. The Z-score

uses multiple corporate income and balance sheet values to measure the financial health of a company.

As Zoot is a private equity firm so we have used Z score estimation for private firms. Here

Z score Bankruptcy Model:

Z = 0.717T1 + 0.847T2 + 3.107T3 + 0.420T4 + 0.998T5

The Timken Company

ALTMAN Z Score

Timken

2001 2002

Coefficien

t

2001 2002

Working Capital /Total Asset 0.29 0.53 1.2 0.35 0.63

Retained Earning /Total Asset 0.00 0.00 1.4 0.00 0.00

EBIT/Total Asset 0.01 0.04 3.3 0.05 0.13

Book value of Equity/Book value of total

debt 2.12 1.74 0.6 1.27 1.04

Sales/TA 0.97 0.93 1 0.97 0.93

Score 2.64 2.73709

Z<3 Z<3

Possibility of Default

Grey

Zone

Safe

Zone

Z <1.81 1.81<Z Z>3

22 | P a g e

<3

Ingersoll-Rand

ALTMAN Z Score

Ingersoll-rand

2001 2002

Coefficien

t

2001 2002

Working Capital /Total Asset 0.06 0.03 1.2 0.08 0.03

Retained Earning /Total Asset 0.00 0.00 1.4 0.00 0.00

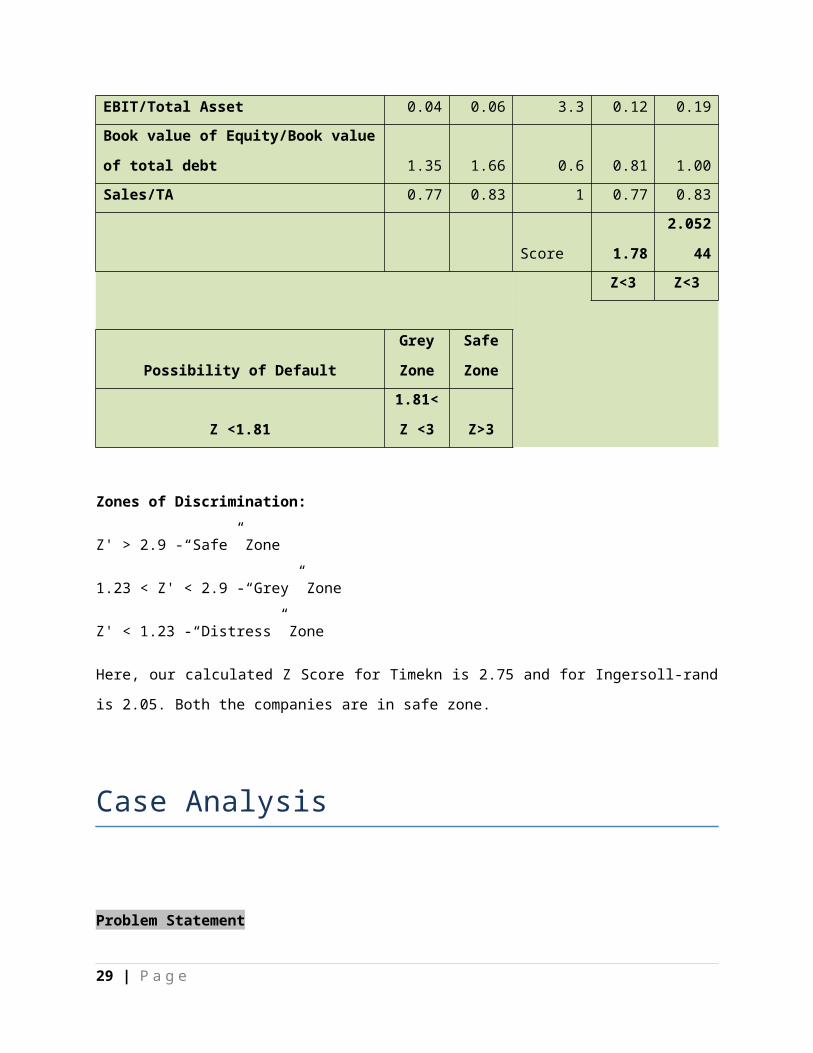

EBIT/Total Asset 0.04 0.06 3.3 0.12 0.19

Book value of Equity/Book value of total

debt 1.35 1.66 0.6 0.81 1.00

Sales/TA 0.77 0.83 1 0.77 0.83

Score 1.78 2.05244

Z<3 Z<3

Possibility of Default

Grey

Zone

Safe

Zone

Z <1.81

1.81<Z

<3 Z>3

Zones of Discrimination:

Z' > 2.9 -“Safe” Zone

1.23 < Z' < 2.9 -“Grey” Zone

Z' < 1.23 -“Distress” Zone

23 | P a g e

Here, our calculated Z Score for Timekn is 2.75 and for Ingersoll-rand is 2.05. Both the companies are in

safe zone.

Case Analysis

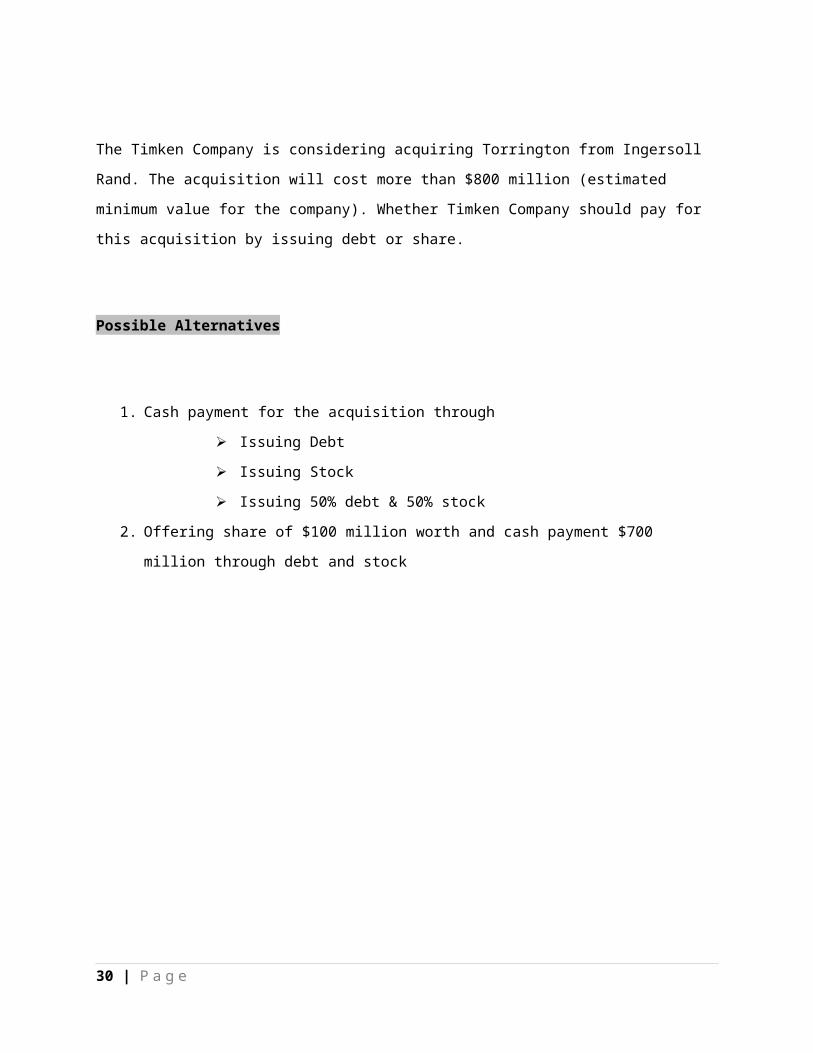

Problem Statement

The Timken Company is considering acquiring Torrington from Ingersoll Rand. The acquisition will cost

more than $800 million (estimated minimum value for the company). Whether Timken Company should

pay for this acquisition by issuing debt or share.

Possible Alternatives

1. Cash payment for the acquisition through

Issuing Debt

Issuing Stock

Issuing 50% debt & 50% stock

2. Offering share of $100 million worth and cash payment $700 million through debt and stock

24 | P a g e

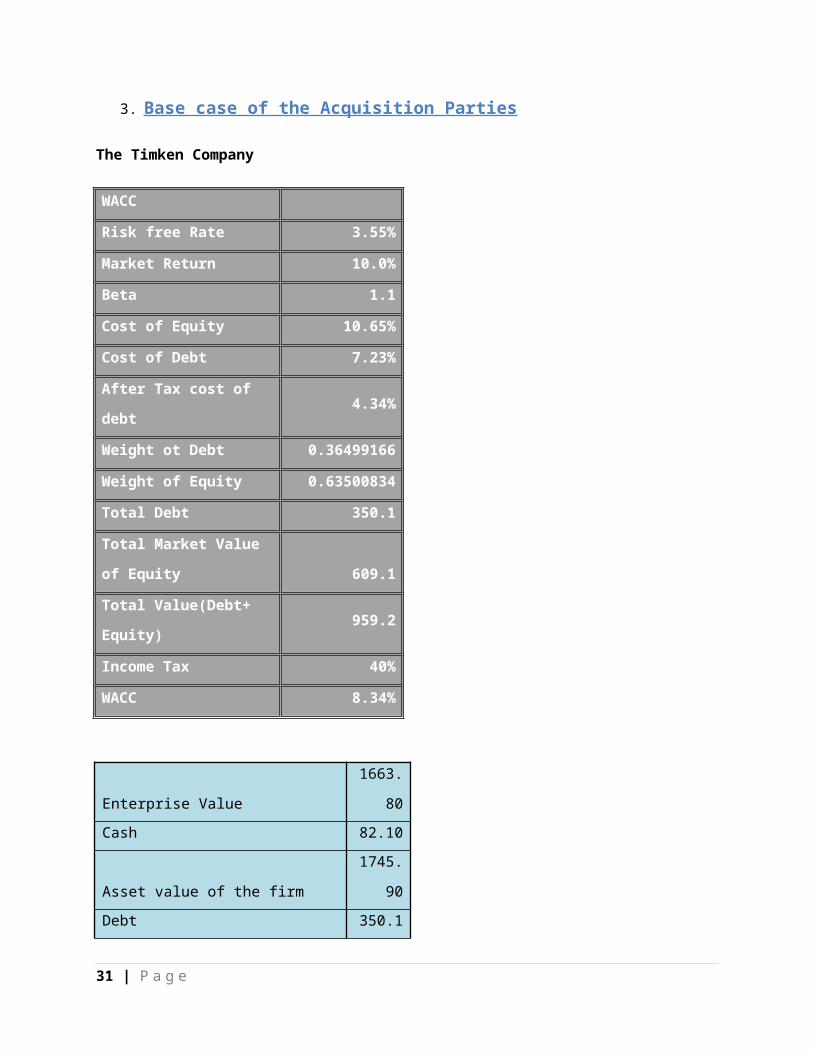

3. Base case of the Acquisition Parties

The Timken Company

WACC

Risk free Rate 3.55%

Market Return 10.0%

Beta 1.1

Cost of Equity 10.65%

Cost of Debt 7.23%

After Tax cost of debt 4.34%

Weight ot Debt 0.36499166

Weight of Equity 0.63500834

Total Debt 350.1

Total Market Value of

Equity 609.1

Total Value(Debt+ Equity) 959.2

Income Tax 40%

WACC 8.34%

Enterprise Value 1663.80

Cash 82.10

Asset value of the firm 1745.90

Debt 350.10

Equity value of the firm 1395.80

No of shares outstanding 63.40

Equity Value Per Share 22.02

Ingersoll-Rand Company

25 | P a g e

WACC

Risk free Rate 3.55%

Market Return 10.0%

Beta 1.2

Cost of Equity 11.29%

Cost of Debt 5.84%

After Tax cost of debt 3.50%

Weight ot Debt 0.375581207

Weight of Equity 0.624418793

Total Debt 2092.10

Total Market Value of Equity 3478.2

Total Value(Debt+ Equity) 5570.30

Income Tax 40%

WACC 8.37%

Enterprise Value 9339.57

Cash 342.20

Asset value of the firm 9681.77

Debt 2092.10

Equity value of the firm 7589.67

Shares outstanding 216.85

Equity value per share 35.00

% of torrington shares outstanding 29.17

Torrington

26 | P a g e

WACC

Risk free Rate 3.55%

Market Return 10.0%

Beta 0.9

Cost of Equity 9.36%

Cost of Debt 5.84%

After Tax cost of debt 3.50%

Weight ot Debt 0.375581207

Weight of Equity 0.624418793

Total Debt 281.39

Total Market Value of Equity 467.8179

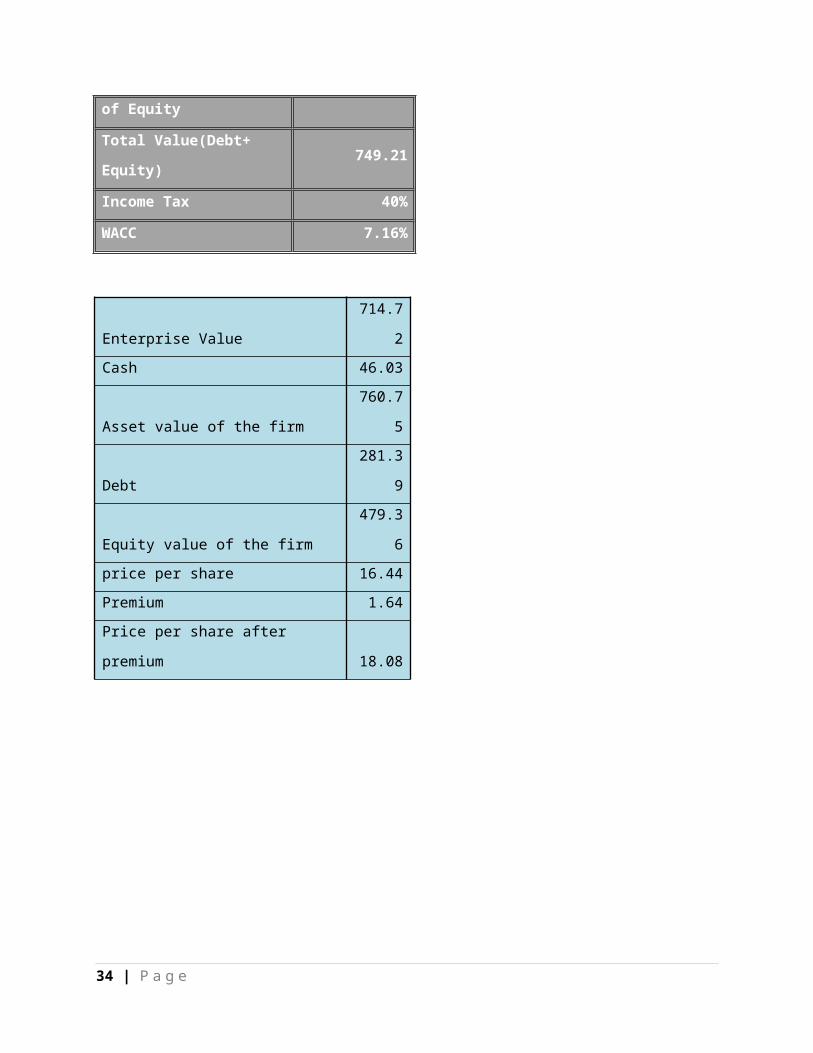

Total Value(Debt+ Equity) 749.21

Income Tax 40%

WACC 7.16%

Enterprise Value 714.72

Cash 46.03

Asset value of the firm 760.75

Debt 281.39

Equity value of the firm 479.36

price per share 16.44

Premium 1.64

Price per share after premium 18.08

27 | P a g e

Synergy

Synergy is the combined value of the acquired and acquire firm. There are four sources of synergy

1. Revenue enhancement

2. Cost savings

3. Operating expense savings

4. Capital expenditure savings

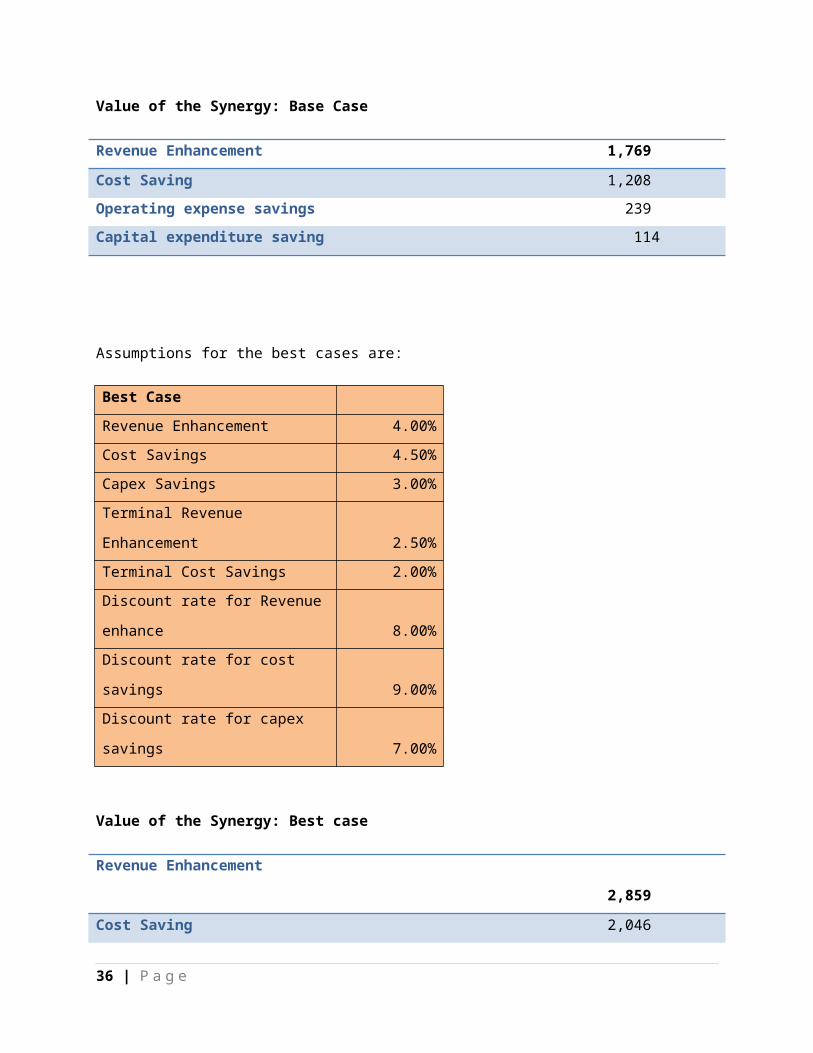

Synergy of the acquisition in three situations; a) Base b) Best & c) Worst are given below

Assumptions for the base cases are:

Base Case

Revenue Enhancement 3.00%

Cost Savings 3.85%

Capex Savings 2.00%

Terminal Revenue Enhancement 2.00%

Terminal Cost Savings 1.50%

Discount rate for Revenue enhance 9.00%

Discount rate for cost savings 10.00%

Discount rate for capex savings 8.00%

Value of the Synergy: Base Case

Revenue Enhancement 1,769

Cost Saving 1,208

Operating expense savings 239

Capital expenditure saving 114

28 | P a g e

Assumptions for the best cases are:

Best Case

Revenue Enhancement 4.00%

Cost Savings 4.50%

Capex Savings 3.00%

Terminal Revenue Enhancement 2.50%

Terminal Cost Savings 2.00%

Discount rate for Revenue enhance 8.00%

Discount rate for cost savings 9.00%

Discount rate for capex savings 7.00%

Value of the Synergy: Best case

Revenue Enhancement

2,859

Cost Saving 2,046

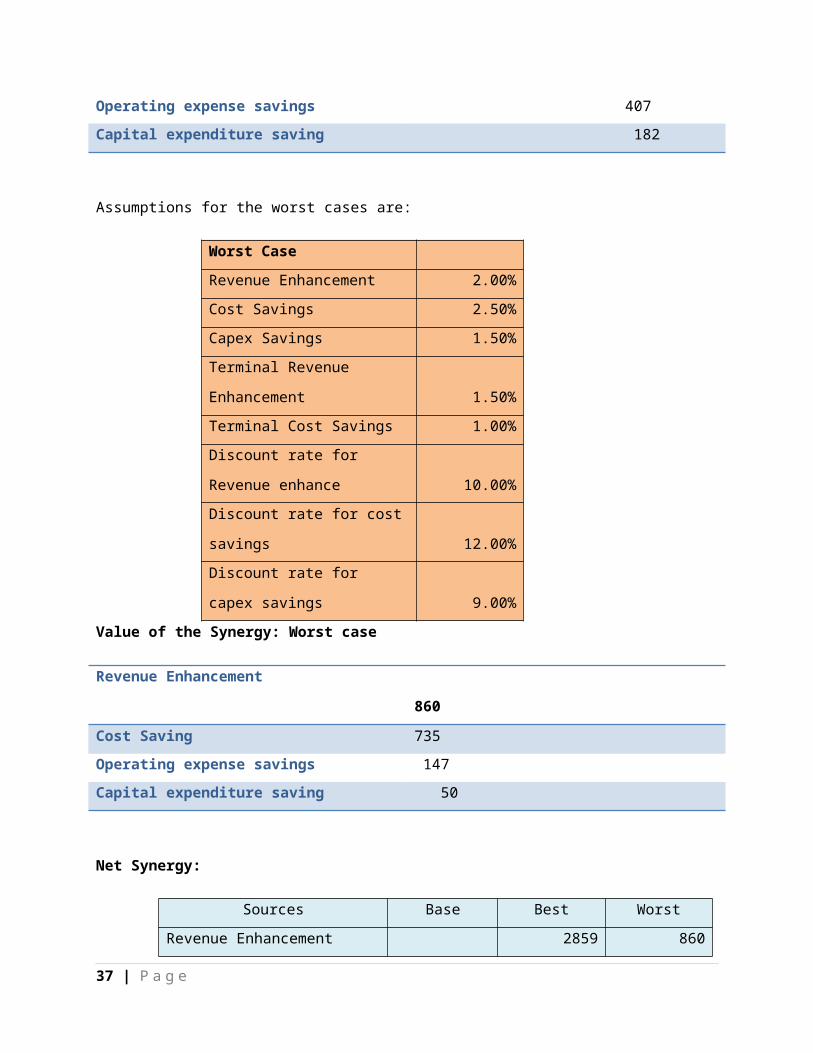

Operating expense savings 407

Capital expenditure saving 182

Assumptions for the worst cases are:

Worst Case

Revenue Enhancement 2.00%

Cost Savings 2.50%

Capex Savings 1.50%

Terminal Revenue Enhancement 1.50%

Terminal Cost Savings 1.00%

Discount rate for Revenue

enhance 10.00%

Discount rate for cost savings 12.00%

Discount rate for capex savings 9.00%

29 | P a g e

Value of the Synergy: Worst case

Revenue Enhancement

860

Cost Saving 735

Operating expense savings 147

Capital expenditure saving 50

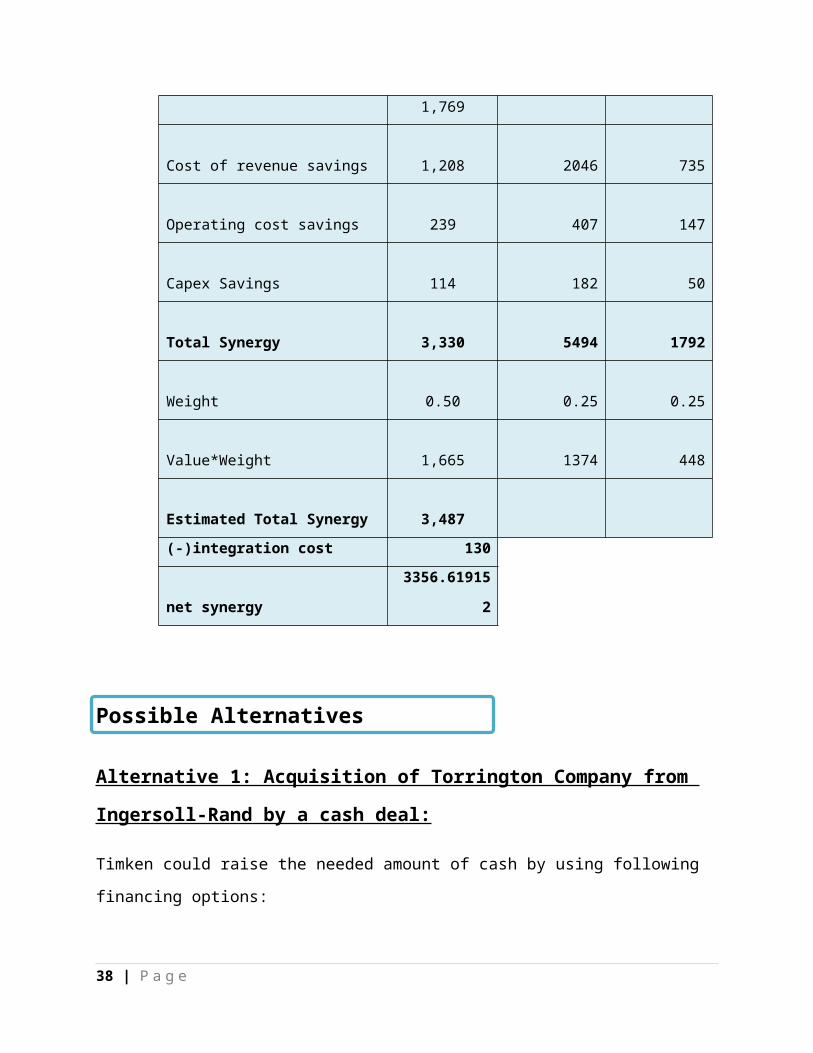

Net Synergy:

Sources Base Best Worst

Revenue Enhancement

1,7

69 2859 860

Cost of revenue savings

1,2

08 2046 735

Operating cost savings

2

39 407 147

Capex Savings

1

14 182 50

Total Synergy

3,3

30 5494 1792

Weight

0.

50

0.

25

0.

25

Value*Weight

1,6

65 1374 448

Estimated Total Synergy

3,4

87

(-)integration cost 130

net synergy 3356.619152

30 | P a g e

Alternative 1: Acquisition of Torrington Company from Ingersoll-Rand by a cash

deal:

Timken could raise the needed amount of cash by using following financing options:

Financing Options:

a) Raising $800 million for the cash deal by issuing shares to the public

b) Raising $800 million for the cash deal with a debt offering

c) Raising $800 million with a combination of debt and equity financing(50:50 ratio)

By using these three alternatives Timken could raise its needed amount of cash for the

acquisition. In each of the cases, Timken’s capital structure will be altered. The optimal capital

structure will ensure Timken with highest amount of Net Acquisition Value (NAV) and highest

equity value per share.

31 | P a g e

Possible Alternatives

WACC Calculation

for the combined

firm:

32 | P a g e

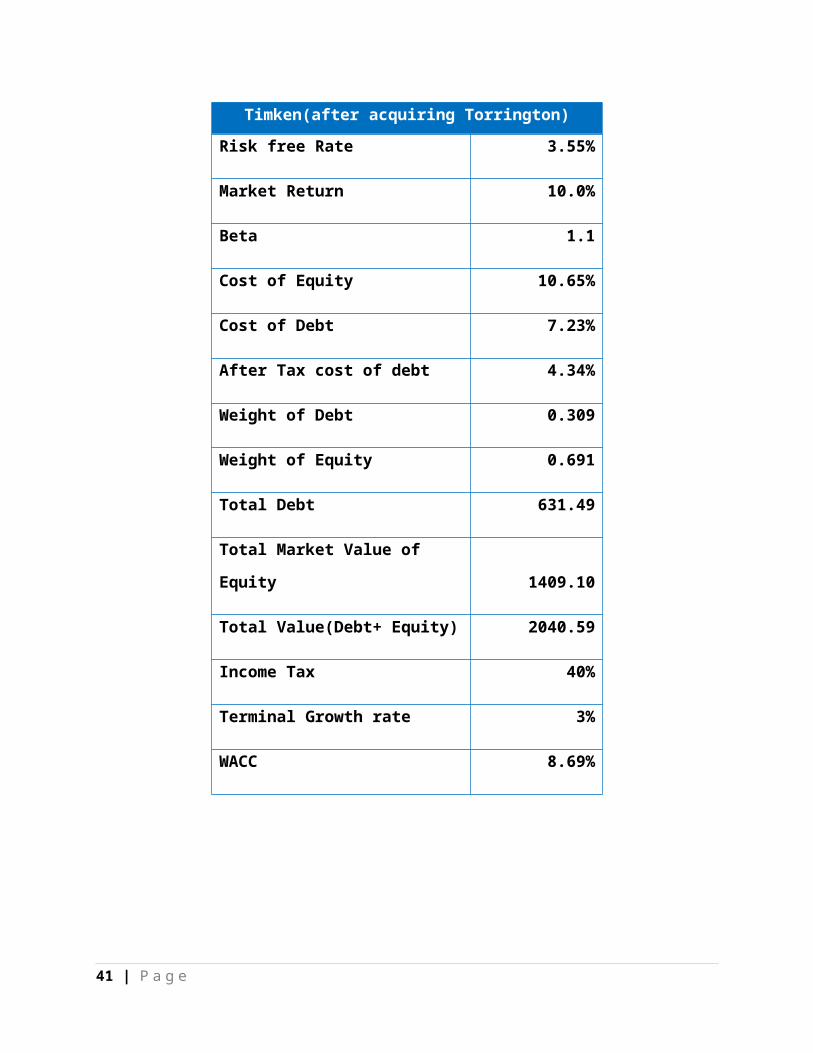

Financing Option A: Raising $800 million for the cash deal by issuing shares to the public

Timken(after acquiring Torrington)

Risk free Rate 3.55%

Market Return 10.0%

Beta 1.1

Cost of Equity 10.65%

Cost of Debt 7.23%

After Tax cost of debt 4.34%

Weight of Debt 0.309

Weight of Equity 0.691

Total Debt 631.49

Total Market Value of Equity 1409.10

Total Value(Debt+ Equity) 2040.59

Income Tax 40%

Terminal Growth rate 3%

WACC 8.69%

Here, Timken will raise $800 million by issuing shares to the public. So they will issue 42.11 new shares

at current market price which is 19 to raise $800 for the cash deal. As a result, Timken’s numbers of

outstanding shares will become 105.51 (64.2+42.11).

By adding the values of Timken and Torrington we can get combined value of Timken after aquiring

Torrington.

33 | P a g e

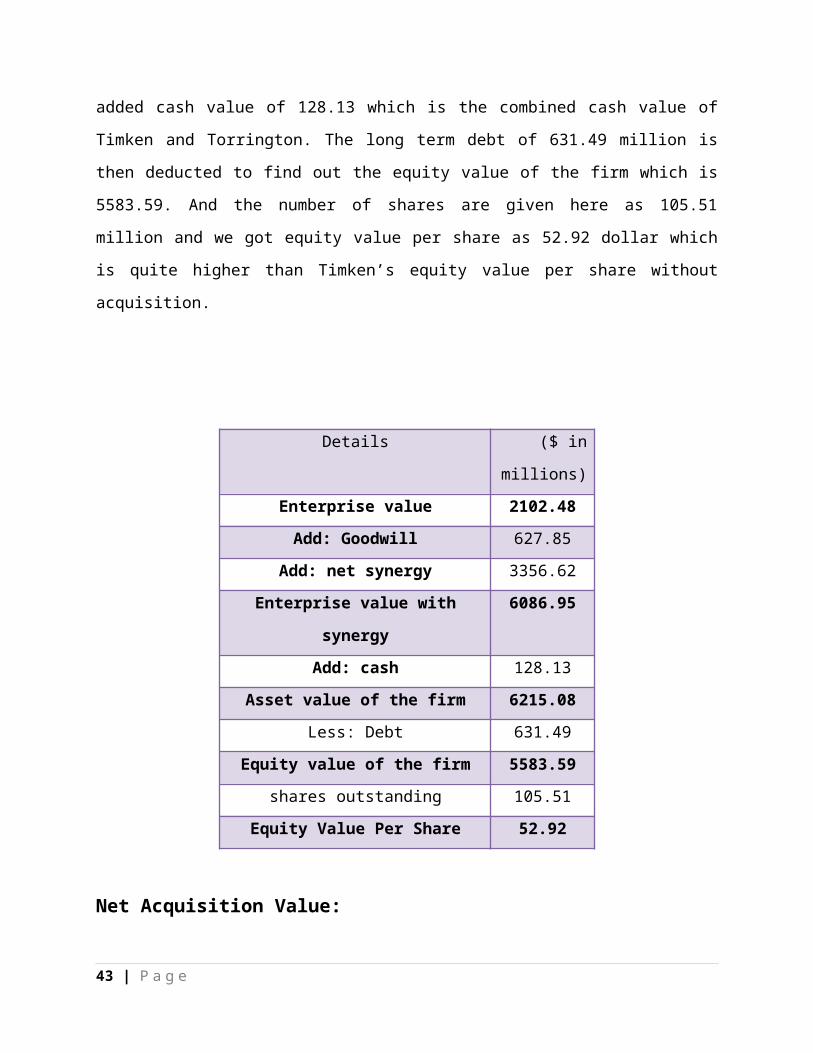

Here we get enterprise value as 2102.48 million and after adding goodwill and net synergy

value we get 6086.95. Here goodwill is determined by deducting the market value of land and

property of Torrington from purchase price (800-172.15=627.85).Then we have added cash

value of 128.13 which is the combined cash value of Timken and Torrington. The long term debt

of 631.49 million is then deducted to find out the equity value of the firm which is 5583.59. And

the number of shares are given here as 105.51 million and we got equity value per share as

52.92 dollar which is quite higher than Timken’s equity value per share without acquisition.

Details ($ in millions)

Enterprise value 2102.48

Add: Goodwill 627.85

Add: net synergy 3356.62

Enterprise value with synergy 6086.95

Add: cash 128.13

Asset value of the firm 6215.08

Less: Debt 631.49

Equity value of the firm 5583.59

shares outstanding 105.51

Equity Value Per Share 52.92

34 | P a g e

Net Acquisition Value:

It is calculated by using following formula:

NAV = Value of combined firm adjusted with synergy and integration cost - (value of Timken +

value of Torrington) - premium paid

Net Acquisition Value for the combined firm for this financing option is $3535.02 million

35 | P a g e

Financing Option B: Raising $800 million for the cash deal with a debt offering

WACC Calculation for the combined firm:

Here, Timken will raise $800 million with a debt offering. So their total debt will increase by 800 million

and will become 1431.49 million. By adding the values of Timken and Torrington we can get combined

value of Timken after aquiring Torrington.

36 | P a g e

Timken(after acquiring Torrington)

Risk free Rate 3.55%

Market Return 12.0%

Beta 1.2

Cost of Equity 13.69%

Cost of Debt 10.84%

After Tax cost of debt 6.50%

Weight of Debt 0.702

Weight of Equity 0.298

Total Debt 1431.49

Total Market Value of Equity 609.10

Total Value(Debt+ Equity) 2040.59

Income Tax 40%

Terminal Growth rate 3%

WACC 11.65%

Here we get enterprise value as 1407.216 million and after adding goodwill and net synergy

value we get 5391.68. Here goodwill is determined by deducting the market value of land and

property of Torrington from purchase price (800-172.15=627.85).Then we have added cash

value of 128.13 which is the combined cash value of Timken and Torrington. The long term debt

of 1431.49 million is then deducted to find out the equity value of the firm which is 4088.328.

And the number of shares are given here as 63.4 million and we got equity value per share as

64.48 dollar which is quite higher than Timken’s equity value per share without acquisition and

financing option A. But in this option, Timken will be forced to borrow the money at “high-

yield” rates which will lead to non- investment grade rating and that is not good for the

company.

Details ($ in millions)

Enterprise value 1407.216

Add: Goodwill 627.8535

Add: net synergy 3356.619

Enterprise value with synergy 5391.688

Add: cash 128.13

Asset value of the firm 5519.816

Less: Debt 1431.49

Equity value of the firm 4088.328

shares outstanding 63.4

Equity Value Per Share 64.48468

37 | P a g e

Net Acquisition Value:

NAV = Value of combined firm adjusted with synergy and integration cost - (value of Timken +

value of Torrington) - premium paid

Net Acquisition Value for the combined firm for this financing option is $2109 million which

is lower than the previous financing option. So it will not maximize Timken’s value

WACC Calculation

for the combined

firm:

Here, Timken will raise $800

million with a combination of

debt and equity financing where

they will issue shares worth of

38 | P a g e

Financing Option C: Raising $800 million with a combination of debt and equity financing (50:50 ratio)

Timken(after acquiring Torrington)

Risk free Rate 3.55%

Market Return 10.0%

Beta 1.1

Cost of Equity 10.65%

Cost of Debt 7.69%

After Tax cost of debt 4.61%

Weight of Debt 0.505

Weight of Equity 0.495

Total Debt 1031.49

Total Market Value of Equity 1009.10

Total Value(Debt+ Equity) 2040.59

Income Tax 40%

Terminal Growth rate 3%

WACC 7.60%

400 million with a debt offering of 400 million. So their total debt will increase by 400 million and will

become 1031.49 million. Equity will also increase by 400 million and will become 1009.10. For raising

400 million Timken will issue new shares of 21.05 at current market price which is 19. By adding the

values of Timken and Torrington we can get combined value of Timken after aquiring Torrington.

Here we get enterprise value as 2587.49 million and after adding goodwill and net synergy

value we get 6571.97. Here goodwill is determined by deducting the market value of land and

property of Torrington from purchase price (800-172.15=627.85).Then we have added cash

value of 128.13 which is the combined cash value of Timken and Torrington. The long term debt

of 1031.49 million is then deducted to find out the equity value of the firm which is 5668.607.

And the number of shares are given here as 84.45 million and we got equity value per share as

67.12 dollar which is quite higher than Timken’s equity value per share without acquisition and

financing option A as well as B.

Details ($ in millions)

Enterprise value 2587.494

Add: Goodwill 627.8535

Add: net synergy 3356.619

Enterprise value with synergy 6571.966

Add: cash 128.13

Asset value of the firm 6700.094

Less: Debt 1031.49

Equity value of the firm 5668.607

shares outstanding 84.45263

Equity Value Per Share 67.12173

39 | P a g e

Net Acquisition Value:

NAV = Value of combined firm adjusted with synergy and integration cost - (value of Timken +

value of Torrington) - premium paid

Net Acquisition Value for the combined firm for this financing option is $3655 million which

is higher than previous financing options.

Alternative 2: Acquisition of Torrington Company from Ingersoll-Rand by stock offering to Ingersoll-

Rand:

Timken could acquire Torrington by offering its stocks to Ingersoll. For this purpose Timken could issue

$400 million equity and $300 million debt and could make the payment of $700 million in cash. As well

as it can offer its stocks worth $100 million. In our case study analysis the new shares that Torrington

would get have been calculated through exchange ratio.

Exchange ratio:

New shares of target firm = α × Old shares of acquiring firm

(1-α)

Exchange ratio = New shares of target firm

Old shares of target firm

40 | P a g e

Here α has been calculated by dividing the purchase price $800 million of Torrington by the after

acquisition equity value of the firm with stock and cash offering of $5770.58 million. New shares

exchanged for existing shares of Timken Company to Ingersoll would be $1.11805204. Total shares

outstanding would be the addition of new shares with the old shares by 63.4+1.11= 64.52 shares.

Exchange ratio comes from the new shares 1.11 divided by the existing shares of Torrington of 29.17.

Here Torrington’s shares have been calculated assuming the accordance with the sales percentage of

13.45% of Ingersoll Company. Thus 29.17 shares have been calculated by the percentage of Torrington’s

sales of Ingersoll company out of Ingersoll’s share outstanding shares of 216.85.

Assumptions for the combined firm:

Timken(after

acquiring Torrington)

Terminal Growth rate 3%

WACC 7.59%

Risk free Rate 3.55%

Market Return 10.0%

Beta 1%

Cost of Debt 7.69%

Income Tax 40%

WACC Calculation for the combined firm:

WACC

Risk free Rate 3.55%

Market Return 10.0%

Beta 1

41 | P a g e

Cost of Equity 10.00%

Cost of Debt 7.69%

After Tax cost of debt 4.61%

Weight ot Debt 0.5060816

Weight of Equity 0.4939184

Total Debt 931.49

Total Market Value of Equity 909.10

Total Value(Debt+ Equity) 1840.59

Income Tax 40%

WACC 7.27%

Here additional $300 million debt has been added with existing $631.49 million debt. As well as new

equity has been added by $400 million shares with existing equity of Timken of $609.1 million. As $100

million worth shares would be given to Ingersoll equivalent amount would be deducted from the total

value of equity.

Here we get enterprise value as $2777.21 million and after adding goodwill and net synergy value we

get $3356.619. Here goodwill is determined by deducting the market value of land and property of

Torrington from purchase price ($800-$172.15=$627.85).Then we have added cash value of $128.13

which is the combined cash value of Timken and Torrington. The long term debt of $931.49 million is

then deducted to find out the equity value of the firm which is $5770.58. And the number of shares are

given here as 63.4 million plus the new shares found from equity issuing worth of ($400/19=21.05)

million and we got equity value per share as $69.6596 which is quite highest than Timken’s equity value

per share without acquisition and cash financing options. In this option, Timken will be able to borrow

the money at “lower-yield” rates which will enable Timken to keep its existing investment grade rating

and that is good for the company.

42 | P a g e

Enterprise Value 2777.21

(+)Goodwill 627.8535

(+)net synergy 3356.619

Enterprise value with synergy 6761.683

(+)cash 128.13

Asset value of the firm 6889.81

(-)Debt 931.49

Equity value of the firm 5958.32

shares outstanding 85.53485

Equity Value Per Share 69.6596

Recommendation

At the last of our analysis we would like to recommend that Timken should acquire Torrington

form Ingersoll-Rand.

Positives:

It will increase market share within Global Industry from 7% to 11%

Will become 3rd largest producer of Bearings in the World

5 % overlap in product offerings and 80% consumer overlap

Expected annual cost savings of $80 million annually by 2007

Financing method:

Optimal capital structure is the combination of debt and equity. Timken should acquire

Torrington by a cash deal of $700 million and the additional $100 million worth of shares

will be issued directly to Ingersoll-Rand as consideration for Torrington with an exchange

ratio of .038:1 where 1.12 shares will be issued as new shares.

43 | P a g e

Equity value per share will be $89.44 and Net Acquisition value will be $3755 million which

is the highest among all other alternatives.

Cash deal of $700 million will be financed by raising equity of $400 million and a debt deal

of $300 million

44 | P a g e