Report No. 25805 - KE Republic of Kenya Country Financial Accountability Assessment November, 2001 Africa Region Operational Quality & Knowledge Services Unit Financial Management World Bank, Washington, D.C. Document of the World Bank Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript

Report No. 25805 - KE

Republic of KenyaCountry Financial Accountability Assessment

November, 2001

Africa RegionOperational Quality & Knowledge Services UnitFinancial ManagementWorld Bank, Washington, D.C.

Document of the World Bank

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Country Financial Accountability Assessment Republic of Kenya

REPUBLIC OF KENYA

COUNTRY FINANCIAL ACCOUNTABILITY ASSESSMENT

Table of Contents

PREFACE ..................................................... v

EXECUTIVE SUMMARY .................................................... VI

PART A: PUBLIC SECTOR ..................................................... 1

Section 1: Government Financial Planning and Budgeting ................................................ . 21.1 Review of the current system .. 2

1.1. 1 Legislative and regulatory environment .. 21.1.2 Transparency and integrity of the budgetary system and mechanism . . 51.1.3 Technical capacity and willingness to implement and promote best practice . 51.1.4 Ongoing reforns .. 6

1.2 Assessment of the current system .. 61.3 Conclusion and recommendations .. 7

Section 2: Government Accounting and Financial Reporting .......................................... . 82.1 Review of the current system .. 8

2.1 1 Legislative and regulatory environment .. 82.1.2 Transparency and integrity .. 92.1.3 Ongoing reforms .. 12

2.2 Assessment of the current system .. 132.3 Conclusion and recommendations .. 14Section 3: Public Sector Internal Control and Records Management . ....................................... 163.1 Review of the current system .. 16

3.1.1 Legislative and regulatory environment .. 163.1.2 Technical capacity and willingness to implement and promote best practice .. 173.1.3 Ongoing reforms .17

3.2 Assessment of the current system .. 183.3 Conclusion and recommendations .. 19Section 4: Public Sector Auditing .......................... 204.1 Office of the Controller and Auditor-General .. 20

4.1.1 Review of the current situatioon .............................................................................. 204.1.1.1 Legisbtive and regulatory environment ............. 204.1.1.2 Capacity and ability to promote best practices ....................... ............... . .204.1.1.3 Ongoing reforms ............. 21

4.1.2 Assessment of the current situation ............. 224.1.3 Recommendations ............. 24

4.2 Internal Audit Department (Treasury) .. 244.2.1 Review of the current situation .. 244.2.2 Assessment of the current situation .. 254.2.3 Conclusion and recommendations .. 26

- I-

Country Financial Accountability Assessment Republic of Kenya

5.1.1 Review of the current system................... ........... .......... 275.1.1.1 Regulatory environment, transparency and integrity...................275.1.1.2 Strengths and weaknesses of the oversight mechanisms............. .275.1.1.3 Conformity of local established practice with internationally recognized

5.1.2 Assessment of the current system ...... .................. ......... . . 285.1 3 Recommnendations . ........................................... .. . 29

5.2 Ethics and Integrity ...... .......... .......... .............. ........... 295.2 1 Review of the current situation..................................... 29

5.2.1.1 Legislative and regulatory environmient .......................... 295.2.1.2 Capacity and ability to implement and promote best practice ............ 305.2.1.3 Ongoing reforms ......... .............................. 30

5 2.2 Assessment of the current situation . . ..... ........................... 3 15.2.3 Recommendations............................................. .. .32

Section 6: Local Government Financial Accountability.................................33

6 2 Assessment of the current situation......................................... . . 366.3 Conclusions and recommendations .'...... ................................. 38Section 7: Public Access to Information on Public Sector Financial Management ............ 407.1 Review of the current situation.............................................. . . 40

7.1 1 Legislative and regulatory environment....................................407.1.2 International benchmarks .. ................................ ........ . . 407.1.3 Accessing informnation on government planning and spending .. .... .......... 40

7 2 Assessment of the current situation .................................... ...... . . 417.3 Conclusions and recommendations ............ .............. ................ 42

Section 8: Non-Governmental Organizations (NGOs) and Community Based Organizations(CBOs).............................................................43

8.1I Review of the current situation .............................................. . . 438.1.1 Legislative and regulatory environment............... .................. 438.1.2 Transparency and integrity............................................ . . 438.1.3 Capacity and ability to implement and promote best practice ................... 448.1.4 Current initiatives for financial accountability reformns........................ . . 44

8.2 Assessment of the current situation.................... .......................... 448.3 Conclusion and recommendations............................................ . . 46

Section 9: Government Business Enterprises........................................4 79.1 Review of the current situation............................................... . . 47

9.1.1 Legislative and regulatory environment, transparency and integrity................479.1.2 Compliance with established rules, regulations and benchmarks................... 489.1.3 Technical capacity to implement and promote best practice ..................... 48

9.2 Assessment of the current situation............................................ . . 489 3 Conclusion and recommendations ............................................ . . 49

- ii-

Country Financial Accountability Assessment Republic of Kenya

PART B: PRIVATE SECTOR ..................................................................... 50

Section 10: The Accountancy Profession and Standard Setting ................................................. 5110.1 Review of the current situation ..................................................................... 51

10.1.1 Legislative and regulatory environment .................................................................... 5110.1.2 Professional education and training ..................................................................... 5210.1.3 Established professional rules, regulations and standards ........................................... 5210.1.4 Technical capacity to implement and promote best practice ....................................... 5310.1.5 Ongoing reforms ..................................................................... 53

10.2 Assessment of the current situation ..................................................................... 5410.3 Conclusion and recommendations ..................................................................... 54

Section 11: Corporate Governance and the Corporate Business Environment . . 5611.1 Corporate Governance ..................................................................... 56

11.1.1 Review of the current situation ...................................................................... 5611.11.1. Regulatory environm ent ..................................................................... 5611.1.1.2 Willingness to implement and promote best practice and Ongoing reforms ..58

11.1.2 Assessment of the current situation ............................................. 5811.1.3 Conclusion and recommendations ..................................................................... 59

11.2 Registrar of Companies ...................................................................... 5911.2.1 Review of the current situation ..................................................................... 59

11.2.1.1 Legislative and regulatory environment ..................................................... 5911.2.1.2 Transparency and integrity ..................................................................... 6011.2.1.3 Ongoing reforms ..................................................................... 61

11.2.2 Assessment of the current situation ............................................. 6111.2.3 Conclusion and recommendations ..................................................................... 62

11.3 The Banking Sector ..................................................................... 6211.3.1 Review of the current system ..................................................................... 62

11.3.1.1 Legislative and regulatory environment ..................................................... 6211.3.1.2 Transparency and integrity ..................................................................... 6311.3.1.3 Extent and quality of compliance with established statutory requirements .... 64

11.3.2 Assessment of the current system ..................................................................... 6411.3.3 Conclusion and recommendations ..................................................................... 65

11.4 The Insurance Sector ..................................................................... 6511.4.1 Review of the current situation ..................................................................... 6511.4.2 Assessment of the current situation ..................................................................... 6611.4.3 Conclusion and recommendations ..................................................................... 66

11.5 Capital Markets ..................................................................... 6611.5.1 Review of the current situation and system ............................................................... 66

11.5.1.1 Legislative and regulatory environm ent ..................................................... 6611.5.1.2 Extent and quality of compliance with established rules or regulations ......... 6711.5.1.3 Ongoing reforms ..................................................................... 67

11.5.2 Assessment of the current situation and system ......................................................... 6811.5.3 Conclusion and recommendations ..................................................................... 68

PART C: APPENDICES ..................................................................... 69

Appendix 4: Sections of the Checklist ..................................................................... 93

- ill -

Country Financial Accountability Assessment Republic of Kenya

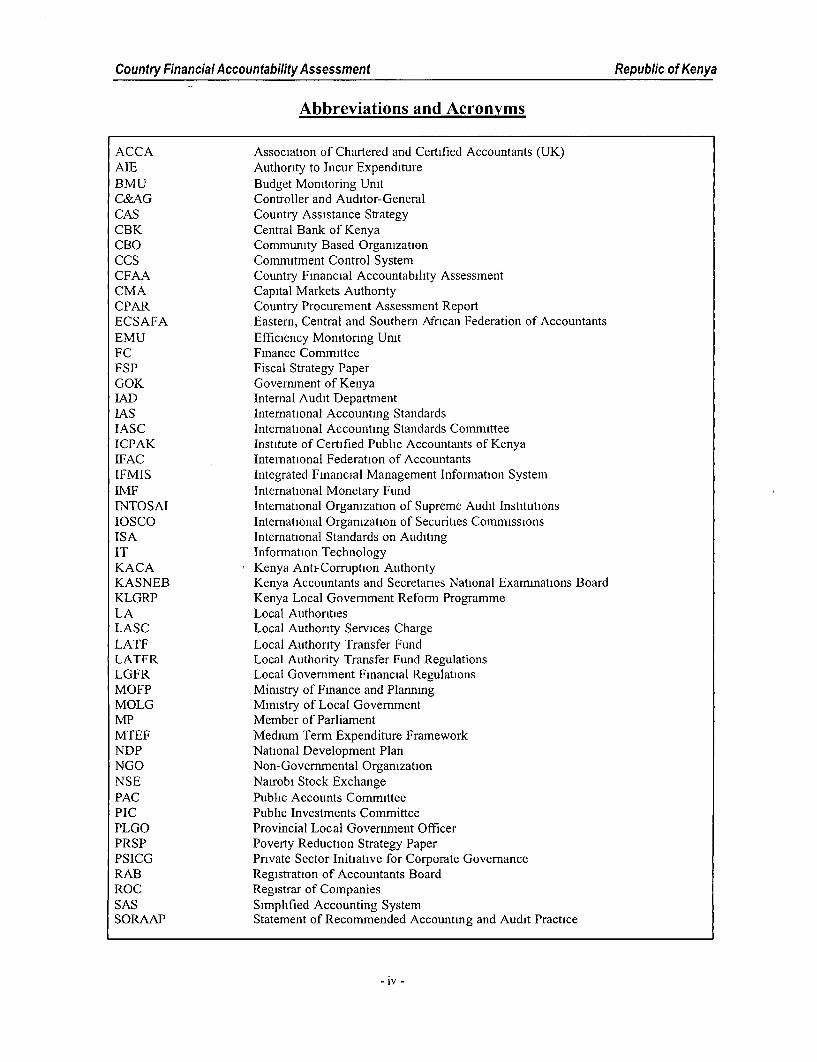

Abbreviations and Acronyms

ACCA Association of Chartered and Certified Accountants (UK)AIE Authority to Incur ExpenditureBMU Budget Monitoring UnitC&AG Controller and Auditor-GeneralCAS Country Assistance StrategyCBK Central Bank of KenyaCBO Community Based OrganizationCCS Commitment Control SystemCFAA Country Financial Accountability AssessmentCMA Capital Markets AuthorityCPAR Country Procurement Assessment ReportECSAFA Eastern, Central and Southern African Federation of AccountantsEMU Efficiency Monitoring UnitFC Finance CommitteeFSP Fiscal Strategy PaperGOK Government of KenyaTAD Internal Audit DepartmentIAS International Accounting StandardsIASC International Accounting Standards CommitteeICPAK InstitLte of Certified Public Accountanits of KenyaIFAC International Federation of Accountants[FMIS Integrated Financial Management Information SystemIMF International Monetary FundINTOSAI International Organization of Supreme Audit InstitutionsIOSCO International Organization of Securities CommissionsISA International Standards on AuditingIT Information TechnologyKACA Kenya Anti-Corruption AuthorityKASNEB Kenya Accountants and Secretaries National Exammations BoardKLGRP Kenya Local Government Reform ProgrammeLA Local AuthoritiesLASC Local Authonty Services ChargeLATF Local Authority Transfer FundLATFR Local Authority Transfer Fund RegulationsLGFR Local Government Financial RegulationsMOFP Ministry of Finance and PlanningMOLG Ministry of Local GovernmentMP Member of ParliamentMTEF Medium Term Expenditure FrameworkNDP National Development PlanNGO Non-Governmental OrganizationNSE Nairobi Stock ExchangePAC Public Accounts CommitteePTC Public Investments CommitteePLGO Provincial Local Government OfficerPRSP Poverty Reduction Strategy PaperPSICG Private Sector Initiative for Corporate GovernanceRAB Registration of Accountants BoardROC Registrar of CompaniesSAS Simplified Accounting SystemSORAAP Statement of Recommended Accounting and Audit Practice

-iv -

Country Financial Accountability Assessment Republic of Kenya

PREFACE

This Country Financial Accountability Assessment (CFAA) considers the strength of thefinancial accountability framework in Kenya's public and private sectors. It is intended to assistthe Government's own ongoing efforts and reforms to strengthen the financial accountabilityframework and build capacity to carry out financial accountability functions. The reportassesses whether the design and implementation of the framework are adequate to ensure theproper use of Governmeit and donor resources. It also measures the degree of compliance withrules and procedures; identifies areas of risk, especially where the country's formal rules,systems, and procedures fall below international benchmarks, and suggests remedial actions andmitigating measures. In addition, the assessment focuses on progress made in building capacityto perform the duties necessary to ensure financial accountability, with special concern forgovernance issues and the public interest.

A World Bank team conducted the CFAA with support by stakeholders from both the publicand private sectors. The World Bank team comprised: Marius Koen (Team Leader, AFTQK),John Nyaga (AFTQK, Country Office), John Ogallo (AFTQK, Country Office), DonaldMphande (AFTQK, Malawi Office), Margaret Olale (Disbursement Assistant, Country Office),Wanjiku Warui-Njoroge (Team Assistant, Country Office) and Lucy Karanja (DFIDConsultant: Wachira Irungu & Associates). Contributions by Peter Warutere (ExternalRelations Officer, Country Office) is also recognised.

Peer reviewers were Sanjay Vani (ECSCS), David Shand (OPCFM) and Zubaidur Rahman(LOADR). The work was completed under guidance of Brian Falconer (Regional FinancialManagement Advisor) and Melanie Marlett (Country Coordinator).

The study was done between November 2000 and April 2001 and consisted of questionnaires,written submissions, desk reviews and interviews with key personnel of GovernmentDepartments and other organizations that participated. The team would like to express theirsincere gratitude to the Ministry of Finance and Planning, and to those individuals from both thepublic and private sectors that participated and submitted comments. Also, the World Bank isgrateful to the Department for International Development (DFID) for financing the work of theconsultants.

It was envisaged to engage the major stakeholders to consider the salient recommendations ofthe CFAA at a workshop and expand on the development of an action plan that would addressthe key issues. However, by November 2001 no agreement to the proposed workshop, norconsolidated comments from the cross section of the stakeholders had been received, in view ofwhich it was decided to finalize and issue the report.

Country Financial Accountability Assessment Republic of Kenya

EXECUTIVE SUMMARY

A Country Financial Accountability Assessment (CFAA) considers the strengths of financialaccountability processes in both the public and private sectors. It is an assessment and not anaudit; its findings cannot therefore provide complete assurance on the status of financialaccountability processes, procedures or systems. A CFAA is a "snapshot" at a particular pomtin time which highlights those issues that are more directly associated with fiduciary risk. Thisreport focuses specifically on institutional arrangements and structural strengths and weaknessesin processes, procedures, and systems.

The CFAA had two key objectives, firstly to facilitate a common understanding by theGovernment of Kenya and development partners of the country's financial managementarrangements in both the public and private sectors, identifying areas for improvement andreaching agreement amongst key stakeholders on how to take this forward. Secondly, toidentify areas where accountability arrangements need to be strengthened and the nisks thatthese may pose in relation to the use of public funds.

Kenya's system of financial management in the public sector has some strengths, notably asound code of financial regulations, the existence of a core of skilled top level managers, anupdated budget framework, the computerization of a number of financial accountabilityfunctions as well as the powers and autonomy of the Controller and Auditor General (C&AG)rooted in the Constitution. In the private sector, the accountancy profession is well establishedand the Government has created an enabling environment for financial accountability through asolid legal framework. Nevertheless, the fiduciary risk in public spending is assessed as high.While a lack of compliance with established financial and procurement regulations havecompletely rendered many initiatives aimed at strengthening the control environmentineffective, issues of limited execution, inadequate monitoring, insufficient capacity and lack ofenforcement also need to be resolved. The country's financial accountability framework, andtherefore financial management, would be considerably more effective and the associatedfiduciary risk mitigated, if these areas were strengthened. Consequently, it is envisaged that anykind of adjustment or programmatic lending in the immediate future would have to go hand inhand with significant improvements in public sector financial management.

Governinient financial planning and budgeting: The budgeting process is underpinned on astrong institutional and elaborate legal framework. However, considerable fiduciary risksremain in the budgeting system in Kenya, particularly with regard to the budget executionwhich has, in practice, not adhered to government procedures, thereby compromising itspurpose for control and accountability of public resources. In this, there are obvious risksattributed to inadequate assurance that allocated resources are used economically and efficientlyfor the intended purposes and beneficiaries (value for money). This position has been cited inthe various reports of the C&AG. Although the potential gains of the Medium TermExpenditure Framework (MTEF) are yet to be fully understood, appreciated and unlocked, it ishoped that greater effort will be made to link budget inputs to outputs and outcomes/impacttaking the efficiency factor into consideration. The existence of poor linkage between policiesand budget process, has made it impossible to measure outputs from activities where resourceshave been used. Finally, falling domestic revenues against projected forecasts is underminingthe ability of government to sustain a reliable and dependable level of service delivery, whichoften tends to exert undue pressure on available resources against many demands.

- VI -

Country Financial Accountability Assessment Republic of Kenya

Government accounting and financial reporting: A number of reform initiatives are ongoingwith a view to enhancing greater financial accountability and efficiency in the governmentaccountng framework. Examples include a review of the Exchequer and Audit Act, whichseeks to improve the legal and regulatory framework for financial management in the publicsector, proposals to develop an incentive-based scheme of service for accountants ingovernment and putting in place an Integrated Financial Management Inforimtion System(IFMIS) that will help link the different and fragmented operations to form a comprehensiveframework for the accounting practice in government (inclusive of districts). Nevertheless,considerable risks remain as a result of the following weakness:o Compliance with the regulatoryframework. The 1997/8 report of the C&AG consists of

217 pages with over 900 paragraphs documenting a series of unresolved audit queries. Theyinclude instances of inadequate record keeping, non-compliance, irregularities, cases ofincompetent staff, flawed procurement procedures, irrational recruitment, poor managementand weak financial/internal controls. Although these queries do not necessarily equal fraudor corruption, it creates a substantial fiduciary risk in an environment of financial andprocedural confusion. This situation has continued unabated in view of weak capacity atTreasury to monitor compliance with internal regulations, procedures and controls by theministries and departments.

o Completeness, accuracy and reliability of government accounting and reporting: Theseattributes of financial statements are significantly hampered by the numerous examplesreported by the C&AG of expenditures that can not be supported by proper evidence as wellas transactions that are not fully captured in the accounts. In situations like these, the trueand fair view concept in accounting may be uncertain, especially where the items arematerially affecting the accounts, e.g. where state enterprises are so much indebted that theyhave negative working capital, leaving them technically insolvent, yet they continue tooperate with financial support from donors through project funding and governmentsubventions. This situation imply that fiduciary risks for reliability and accuracy of recordsin the public domain contmue to increase unabated.

o Non-attractive compensation terms: Although there is a relatively large number of supportaccounting technicians and semi-qualified accountants in the service, it's highly unlikelythat the scenario will change over the short term, to attract fully qualified accountants in thepublic sector. The poor compensation in the public sector as a whole has been the majorreason why government has often found it difficult to attract and retain some of the bestpeople after having invested so much resources in their training.

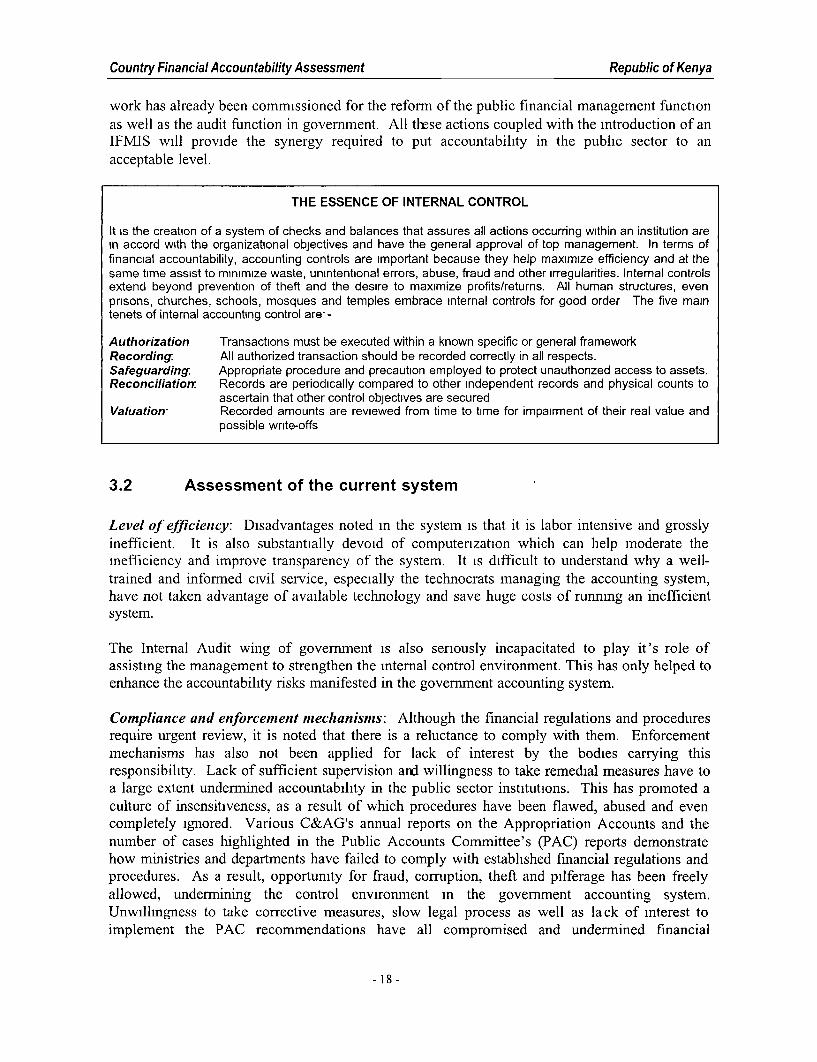

Public sector internal control and records management: Although internal control andrecords management requirements are well articulated in the financial regulations andprocedures, there is general laxity to comply with them. Disadvantages noted in the system isthat it is labor intensive and substantially devoid of computerization which makes it grosslyinefficient and laborious. As a result, opportunity for fraud, corruption, theft and pilferage hasbeen freely allowed, undermining the control environment in the government accountingsystem. Various C&AG's annual reports on the Appropriation Accounts and the number ofcases highlighted in the Public Accounts Committee's (PAC) reports demonstrate non-compliance by mimstries and departments. It is also evident that corrective action is notpreferred and supervision by management is weak or lacking.

Public sector auditing: Both the external and internal public sector audit functions are useful inmanaging public sector spending, ensuring financial accountability and curbing corruption by

-vii -

Country Financial Accountability Assessment Republic of Kenya

reinforcing legal, financial and institutional frameworks and reducing arbitrary application ofrules and laws.* External audit: The Office of the C&AG is perhaps the only known institution in the public

service where meritocracy is upheld. However, it still suffers from a shortage of qualifiedand experienced staff which leads to the application of outdated audit techniques and theinability to keep up with the changing scope and complexities of audit work. Otherweaknesses include the delay in completing audit reports to be submitted to parliament anda lack of adequate momtoring and follow-up of audit findings. Finally the proposedlegislation which is expected to bring about enhanced operational autonomy andindependence from the Executive is long overdue. The legislation will also bring back thefragmented public auditing function under one umbrella practice and control of the NationalAudit Office.

* Internal audit. The current set up of the Internal Audit Department (IAD) is very weak. Itsoperations are not specifically recognized and governed by any legislation. Lack of capacityto monitor the department's operations and follow up of its reports undermines the purposefor which it was established and makes it technically ineffective. There is need to expandthe mandate of the IAD and to have its powers explicitly embedded in legislation.

Legislative scrutinty, ethlics and integrity: The C&AG's annual reports have year after yearcited numerous instances where fraud, wastage and poor accountability and failure to reconcilerelatively huge balances in government accounts, have for many years not been attended to Inaddition, m-discipline has not been punished and suspected corruption in transactions have notbeen brought to conclusion. Although there is a willingness amongst members of PAC and PICto improve their effectiveness, their technical capacity is often low. These committees alsosuffer from a fundamental weakness m that they have no power to force the executive toimplement their recommendations - unwillingness to take corrective measures, slow legalprocess, as well as lack of interest to implement their recommendations have all compromisedand undermined financial accountability principles in government.

The Government has initiated several corruption prevention strategies and major reform effortstowards enhancing financial accountability, including (1) the establishment and strengthening ofthe Kenya Anti-Corruption Authority (KACA), (2) the establishment of the Directorate ofProcurement within the Ministry of Finance, (3) the development of a National Anti-corruptionPlan in collaboration with all the stakeholders, and (4) the tabling of the Public Service (Code ofConduct and Ethics) Bill (2000) as well as the Anti-Corruption and Economic Crimes Bill(2000) in Parliament. Sadly, the proposed legislation, on which these major reforms are based,has been stupended by parliament due to technical issues which have not been resolved by thetime of issuing this report.

Local governient financial accountability: In 1996 the Ministry of Local Government(MOLG) established the Kenya Local Government Reform Programme (KLGRP) secretariatwhich has as one of its main objectives to improve financial accountability of local authorities(LAs). Nevertheless, the public management hierarchy of LAs still allows for duplication andmultiple accountability at the levels where councils are established whereas democraticallyaccountable governance structures are lacking at the village, sub- locational, rural divisional andprovincial levels. Other weaknesses that pose significant fiduciary risk includes the following:* The lega I framework and financial requirements for financial accountability are fairly strong

but the relevant stakeholders do not adhere to them for various reasons. Also, the MOLG

Country Financial Accountability Assessment Republic of Kenya

seems unable to fulfill its functions due to insufficient resources and facilitation, but mainlydue to lack of a long tenrn strategy for the sector.

o Unrealistic budgets are enforced on LAs and are therefore, generally, ignored for thepurpose of managing performance. Some are approved long after the beginning of therelevant financial year. Also the budgeting process has not been open to public participationand consultations with other stakeholders.

O Though current rules and structures require LA political and administrative leaders to beaccountable, this is never enforced. Internal checks and balances have proved to be weakand easily ignored while procurement practices are not transparent.

o Institutional capacity is low. This has resulted in the shortage of financial managementstaff, which is expectantly more acute in rural LAs than in urban ones. Accountingdepartments are also not well facilitated with modem processing, communicating, and datamanagement equipment.

o Records are not properly maintained and reconciliations and final accounts are not prepared.Normal book-keeping of primary records, including bank reconciliation statements, is alsoin a backlog position.

o The majority of LAs do not comply with the rules and regulations and some of them havenot submitted final accounts since mception. Also, external audit is not complete as all LAsare in a backlog position.

Public access to information on public sector financial management: Even though theConstitution provides for freedom of information, the provisos to it tends to undermine itseffectiveness to a large extent. The onus has been placed on the seeker of information to showwhy information should be availed to him/her. There is need to carefully consider theincorporation m the Constitution of a specific provision on the Right to Freedom of Informationwith the eye towards maintaining the spirit of the original Constitution and InternationalConventions. Capacity of existing public institutions of financial accountability need to beimproved to enable them to facilitate access to credible and objective public information by thepublic in a timely manner. The Finance, PIC and PAC meetings should be opened up to thepublic and the media unless matters are dealt with where particular evidence needs to be heardin camera. Finally, there is need to raise the awareness of the public about their basic right offreedom to access public information.

Non-government organizations (NGOs) and community based organizations (CBOs): Therole of the fast growing NGO/CBO sector in the socio-economic development in Kenya hasbeen gaining increasing prominence, particularly the crucial contribution towards povertyalleviation. NGOs are required to prepare annual financial estimates, but there is no mechanismto ensure compliance. Accountability and transparency are also weak as a result of lack of aneffective monitoring regime. Most NGOs have low compliance with accounting standards andlimited compliance with established regulations and procedures. CBOs registered under theSocieties Act are required to submit annual returns which may or may not include financialstatements. They are under no obligation to prepare financial statements unless demanded bydonor agencies. In general, there has been little emphasis on good financial management andaccounting practices. Hence, transparency and financial accountability are often not used ascriteria for securing donor funding, thus creating situations of high fiduciary risk.

Government business enterprises: There is urgent need to harmonize the State CorporationsAct with the enabling Acts of Parliament to remove inconsistencies. Compliance with the

- lx -

Country Financial Accountability Assessment Republic of Kenya

requirements of the Act varies from low to high, depending on the quality of the Board andmanagement of a particular State Corporation. Weak accounting and internal control systemshave been retained by Boards and management of some State Corporations to perpetratefinancial indiscipline. Capacity of regulatory bodies to ensure quality is generally low. There islack of enforcement of fiduciary responsibility even by the PIC of Parliament whose pastrecommendations on punitive measures for financial impropriety have not been implemented.

The accountalicy profession and stantdard setting: Although the accountancy profession iswell established through the Institute of Certified Public Accountants of Kenya (ICPAK) andhas a solid resource base, the following issues of concern need to be addressed to provideftirther impetus to its enhancement: (1) lack of legal backing for the enforcement of Accountingand Auditing Standards, (2) need for a mechanism to monitor the quality of accountancytraining at the various training institutions, (3) the non-existence of a Quality/Peer ReviewScheme and compliance monitoring system and (4) lack of ability and capacity to providetechnical support to members of the accountancy profession. ICPAK does not have thestatutory responsibility and sole mandate to registers members and issue practicing licenses,resulting in high fiduciary nsk. On a national scale there is a need to uplift the entry standardsof students that want to register for professional training as accotntants, set up mechanisms toensure proper quality of training and upgrading education materials and facilities.

Corporate governance and the corporate business environment: In Kenya, the Governmenthas created an enabling environment for financial accountability in the prnvate sector through asolid legal framework.* Corporate governance. Corporate governance is increasingly taking centre stage in the

busmess environment due to the consistent promotion of the concept and its principles bythe Private Sector Initiative for Corporate Governance, with active support by the majorregulatory bodies in the private sector. However, there is a need for a legal frameworkwithm which corporate governance can be enforced It is also essential to raise the aware-ness of all stakeholders in the corporate environment about their right and responsibility todemand good corporate governance and financial accountability from corporate bodies.

* Registrar of companies: The Registrar's office is faced with constraints such as lack ofsufficient number of qualified staff, lack of adequate resources to meet the demands of thework program, and inadequate training opportunities - these shortcomings ncapacitatethe department's ability to fulfill its mandate. Although there is genuine willingness toimplement and promote best practice in the department, the capacity to oversee such a moveis indeed weak. Finally the Companies Act, CAP 486 (1962) needs to be updated to make itresponsive to current business and market conditions.

* Banking sector: In an effort to solve the banking crisis of the nineties, the regulatory andlegal framework for the banking sector had been strengthened in recent years. This includessignificant improvements in financial reporting and auditing compliance. However, thefollowing issues could assist in improving financial accountability in the banking sector: (1)bringing building societies within the ambit of the Central Bank's supervision framework,(2) considering the impact on the auditors' independence when also providing consultancyservices to their clients and (3) the development and implementation of a Code of Conduct

* Insurance sector: While there is adequate financial management capacity in the insuranceindustry, compliance to regulations and norms has been weak mainly because of capacityconstraints in the Insurance Commissioner's office to properly analyse the annual financialreturns and carry out its statutory mandate. Sufficient guidelines for assessing the solvency

Country Financial AccountabilityAssessment Republic of Kenya

of operators does not exist which in itself is a high fiduciary risk that the regulatory bodycould issue renewed licenses to insolvent operators.

O Capital markets: The Capital Markets Authonty is actively and efficiently promoting thedevelopment of transparent capital markets in the country. It enforces compliance by alllisted companies to prepare and present their financial statements in accordance with therequirements of International Accounting Standards. In addition, it plays an active role inthe promotion of the principles of good corporate governance in the business environment.It is worth noting that (1) there is a need for programs that promote key understanding onthe structure of the financial markets and (2) that the absence of credit rating agencies andcredit reference bureaus creates operational difficulties within the capital markets.

The most significant underlying principal of conducting a CFAA is the one of nationalownership of diagnosis and prescriptions by the country's authorities. Accordingly, thedevelopment objectives of the CFAA aims at facilitating a common understanding by the majorstakeholders in the public and private sectors of the borrower, the Bank and developmentpartners of the key issues and recommendations related to the country's financial managementarrangements and challenges. For this reason a forum was envisaged to facilitate a focuseddiscussion and reaching consensus on the findings and recommendations of the draft CFAAreport by all the stakeholders - in particular the emphasis would have been placed onpreparing a development action plan that would address the key challenges and weaknesses.Unfortunately, the workshop never took place and a:nsequently it was decided to prepare a"shadow" schedule of the salient actions that, if implemented, would make a significant impacton improving the financial accountability environment in Kenya. Should the Government ofKenya wish to revive this process in the future we will consider a follow-up workshop at thatstage.

Salient recommendations1 Government Financial Planning and Budgeting

o Improved and realistic cash revenue forecasting is imperative. The system of weekly cash rationingshould be transformed into a proper financial planning process.

o The introduction of the MTEF should be strengthened by ensuring that as far as possible all funds(including extra-budgetary funds) are managed and monitored under this mechanism.

2 Government Accounting and Financial Reportingo Urgent need for putting in place an IFMIS that will enable the integration of the current free

standing and fragmented systems and operations of financial accountmg.o The Financial Management and Accountability Bill, 2000 to be enactd by parliament.o The funds flow mechanism to the districts should be strengthened.

3 Public Sector Internal Control and Records Managemento Punitive actions should be taken to bring into existence a disciplined financial management practice

for internal control and records management in the public sector.o Implementation of recommendations made in the C&AG's reports on the state of both the intemal

control and records management practices should be ensured.4 Public Sector Auditing

o Enactment of the Kenya National Audit Office Bill to consolidate and strengthen the public auditingfunction and bring about enhanced autonomy and independence from the Executive.

o The C&AG's Annual Report on the Government Accounts should be submitted timely - thebacklog should be cleared.

o There is need to expand the mandate of the IAD. It is also suggested that the department should begiven a higher status in law by having its powers fully and explicitly embedded in legislation.

-xi-

Country Financial Accountability Assessment Republic of Kenya

5 Legislative Scrutiny, Ethics and Integrity* The National Assembly should increase its statutory authority to enforce the implementation by the

executive of the recommendations of PIC and PAC.* The issue of KACA's constitutional status should be resolved. Also, the two suspended Bills

mentioned above should be brought back to Parliament after proper re-drafting and enacted into law.* The anti-corruption bodies envisaged by the proposed new legislation should be empowered to

continuously monitor any corrupt practices and to prosecute cases of mal-practices6 Local Government Financial Accountability

* Generally the systems for budgeting, expenditure control, accounting, reporting and auditing shouldbe strengthened.

7 Public Access to Information on Public Sector Financial Management* There is need to carefully consider the incorporation in the Constitution of a specific provision on

the Right to Freedom of Infonration with the eye towards maintaining the spirit of the originalConstitution and International Conventions.

* Existing public institutions of financial accountability need to be capacitated so as to serve thepurpose of accessing credible and objective public information by the public in a timely manner.

8 NGO's & CBO's* Capacity of the regulatory bodies (NGO Board and the National Council of NGOs) should be

strengthened to ensure compliance and to promote best practice* Proper guidelines/standards of financial reporting and auditing should be furnished.

9 Government Business Enterprises* Need to harmonize the State Corporations Act with the enabling Acts of Parliament to remove

inconsistencies, reduce the number of govemment agencies to which State Corporations areaccountable, and streamline criteria and procedures for granting exemptions from the Act.

* The strengthening of financial accountability functions should be extended to State Corporationsthat have definite capacity shortcomings.

10 The Accountancy Profession and Standard Setting* ICPAK accounting and auditing pronouncements should have explicit legal backing.* ICPAK should have the statutory responsibility and sole mandate to registers members and issue

practicing licenses.* An effective compliance mechanism should be established through a Quality/Peer Review Scheme.

11 Corporate Governance and the Corporate Business Environment* There is need to support the Pnvate Sector Initiative for Corporate Governance by creating a legal

framework within which corporate governance will be enforceable. Explicit legal backing of theseprnciples by the Companies Act, Banking Act, Insurance Act and other related legislation isrequired to ensure compliance by all corporate entities.

* The capacity of the regulating authorities in the private sector to enforce compliance with rules andregulations should be strengthened through capacity building programs.

- xii -

PART A- PUBULC ECTOR

LEGAL FRAMEWORK

Kenya has a fundamentally well established legal framework for publicfinancial management and financial accountability that is underpinnedby existing laws. Specifically, sections 48 and 99- 105 of the Constitutionof Kenya together with the Exchequer and Audit Act, CAP 412 (1955), thePaymaster-General Act, CAP 413 (1960), and the Government FinancialRegulations and Procedures (1989) provide the legal basis for the controland management of government finances in Kenya. In this regard, allrevenues or other moneys raised or received (from any source) for thepurpose of the Government of Kenya, are to be paid into and from theConsolidated Fund, from which no moneys can be withdrawn except asmay be authorized by the Constitution or by an Act of Parliament(including an Appropriation Act) or by a vote on account passed by theNational Assembly. This doctrine lays the basis upon which publicresources are planned for, executed, accounted for and audited, whichare the basic pillars of financial accountability.

Country Financial Accountability Assessment Republic of Kenya

SECTION 1: GOVERNMENT FINANCIAL PLANNING AND BUDGETING

1.1 Review of the current system

1.1.1 Legislative and regulatory environment

Public sector budgeting in Kenya is an important element of Public Financial Management. It isin relative terms well established with a strong legal and institutional framework foundation,which is enshrined in Chapter VII, sections 99 to 105 of the Constitution of Kenya. The budgetsystem is fundamentally "cash based" and has over the years been improved gradually to takeinto perspective initiatives such as Commitment Control, Program Based Planning and morerecently, the Medium Term Expenditure Framework (MTEF) and the latest initiative of PovertyReduction Strategy bias in resource allocation.

The Exchequer and Audit Act, CAP 412 (1955), and the Paymaster-General Act, CAP 413(1960), provide the framework for managing the collection, issue and payment of public moneysin the government The government budget and accounting (i.e. financial) penod is annualcycles, running from July 01 to June 30. The general legal framework requires that governmentbudget should provide for the following basic features.

* Revenue/expenditure plans of government ministries/departments.* Provision for both Recurrent and Development votes.* Reflection of political, legal, social-economic policy measures of government

Budget cycle- The government budget cycle in Kenya is marked by three broad phases, i.e.budget preparation, budget execution and buclget review In between, there are a number ofinterfaces of significant importance from a process perspective. The annual estimates areprepared by the spending ministries and departments around March in readiness for submissionto the Treasury for rationalization and compilation before the national budget is presented to theNational Assembly in the month of June. While debate in Parliament over the budget is inprogress, spending ministries/departments are authonzed to implement up to one half (50%) ofthe budgeted allocation for the year ("Vote on Account") and in accordance with the Treasury'sinstructions and guidance.

Budget preparation: One of the core functions of the Ministry of Finance and Planning (MOFP)in public expenditure management is to oversee the preparation process of the budget by thespending ministries and departments. The main features of this function are:

* Initiation of the budget formulation process, giving guidance and setting the framework forthe spending ministries and departments to follow.

* Determination of the budget ceilings for the spending ministries and departments at all levelsof the budget structure.

* Issuance of the budget circular along with various useful indicators such as inflation rate, etc.that would be assist the spending ministries and departments to develop realistic forecasts.

* Facilitate thorough discussions with spending ministries and departments before finalizingeach mmistry's and department's estimates.

- 2 -

Country Financial Accountability Assessment Republic of Kenya

o Consolidation of all the agreed estimates for spending ministries and departments imreadiness for presentation to the National Assembly.

o Oversee and lead the preparation of supplementary and forward estimates by spendingministries and departments.

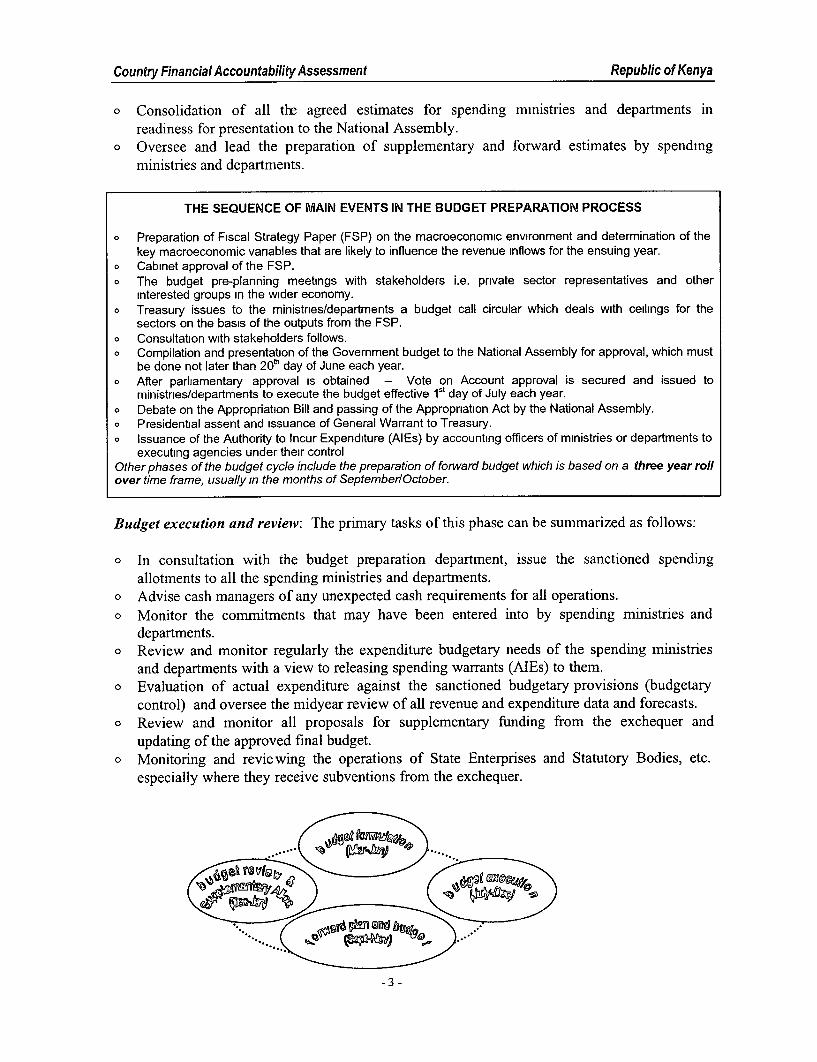

THE SEQUENCE OF MAIN EVENTS IN THE BUDGET PREPARATION PROCESS

o Preparation of Fiscal Strategy Paper (FSP) on the macroeconomic environment and determination of thekey macroeconomic variables that are likely to influence the revenue inflows for the ensuing year.

o Cabinet approval of the FSP.o The budget pre-planning meetings with stakeholders i.e. private sector representatives and other

interested groups in the wider economy.o Treasury issues to the ministries/departments a budget call circular which deals with ceilings for the

sectors on the basis of the outputs from the FSP.o Consultation with stakeholders follows.o Compilation and presentation of the Government budget to the National Assembly for approval, which must

be done not later than 20t day of June each year.o After parliamentary approval is obtained - Vote on Account approval is secured and issued to

ministries/departments to execute the budget effective lt day of July each year.o Debate on the Appropriation Bill and passing of the Appropriation Act by the National Assembly.o Presidential assent and issuance of General Warrant to Treasury.o Issuance of the Authority to Incur Expenditure (AlEs) by accounting officers of ministries or departments to

executing agencies under their controlOther phases of the budget cycle include the preparation of forward budget which is based on a three year rollover time frame, usually in the months of SeptemberlOctober.

Budget execution and review: The primary tasks of this phase can be summarized as follows:

o In consultation with the budget preparation department, issue the sanctioned spendingallotments to all the spending ministries and departments.

o Advise cash managers of any unexpected cash requirements for all operations.O Monitor the commitments that may have been entered into by spending ministries and

departments.o Review and monitor regularly the expenditure budgetary needs of the spending ministries

and departments with a view to releasing spending warrants (AIEs) to them.o Evaluation of actual expenditure against the sanctioned budgetary provisions (budgetary

control) and oversee the midyear review of all revenue and expenditure data and forecasts.o Review and monitor all proposals for supplementary funding from the exchequer and

updating of the approved final budget.o Monitoring and reviewing the operations of State Enterprises and Statutory Bodies, etc.

especially where they receive subventions from the exchequer.

-3 -

Country Financial Accountability Assessment Republic of Kenya

The figure above illustrates the budget cycle that runs throughout the government financial year(i.e. July through to June):

There has been recognition by the Kenyan authorities that government budgets were faced withsome systemic problems which compromised their effectiveness in expenditure control. As aresult, MOFP was unable to adequately monitor or control spending in ministries anddepartments. Due to weak public expenditure management and inadequate compliance withfinancial regulations there were persistent spendmg overruns and accumulation of domesticarrears. A study by the International Monetary Fund (IMF) of the public expendituremanagement in Kenya in February, 2000 indicated that unrealistic costing of policies aggravatedthe problem of poor compliance, giving rise to many irregular in-year additions to spending. Inparticular, debt service and wages were almost always crowding out operations and maintenancespendmg. 1 Effort has been made to implement some of the recommendations, geared atimproving present procedures, promote better integration and coordination, and implement morecomprehensive medium-term program of reforms. Some of the short-run actions already put inplace aim at providing a more enablmg institutional framework for public expendituremanagement, which include strengthening of Finance Officers' position in spending agencies andstreamlining operations of the District Treasuries under the purview of MOFP.

Cash based budget has the advantage that funds are only released on the basis of rations madeavailable to areas of expenditure to which the government attaches "high priority". The goodaspect of this is that there is likely to be desired results and impact from well funded activitiesrelative to the outcome of proportional distribution of the available cash thinly across all thevarious approved expenditure items. If w.ed well, this tool has demonstrated its strength forexpenditure control and in keeping creation of pending bills in check, with help from budgetmonitonng feedback. The downside of cash based budgets is that the release of funds isunpredictable and not transparent, often laced with arbitrary allocation of funds, which issometimes politically influenced. Although there is tremendous effort to improve on thepredictability of release of funds, there still remains bottlenecks in the flow of funds mechanismwhich is a major systemic problem faced by both donor supported projects as well asgovernment own funded projects. This contributes substantially to the government's inability toabsorb donor funds within the planned period2 .

One major reform initiative aimed at improving public budget structure in Kenya is theintroduction of the MTEF by the government. In broad terms, MTEF entails establishment of aframework and decision making process that permits budget resource allocation decisions to bebased on outcomes they are expected to produce, e.g. decline in poverty, healthier, better skilledand educated populace, etc. MTEF concept presents a strong tool of ensuring the best possibledelivery of public services and investment decision by the government. Year 2000/2001 budgetwas the first MTEF based budget, which already began to demonstrate the new thinking in themanner in which national priorities as articulated in policies, received adequate attention inresource allocation. Because it is still in its early stages of adoption, much remains to beachieved in both definmg the concept in the Kenya context and the strategy for itsinstitutionalization. During the first year of its adoption, it was evident that spending agencies

l IMF Fiscal Affairs Department July 2000 Report on Kenyas Agenda for Reforming Public ExpenditureManagement by J Diamond, T. Prakash, H S Jung, M Flanagan and G Hansen2 By end of March 2001, over 0.5 billion US dollars remained undisbursed under the IDA supported portfolio inKenya

-4 -

Country Financial Accountability Assessment Republic of Kenya

had not adequately been prepared for it. In this regard, training of spending agencies all relevantlevels was instituted, the effect of which will be expected to be illustrated in the quality of thenext MTEF based budget. Further gains can be achieved with its continued stewardship byMOFP. Some of the threats that will require some attention are:

o Treatment of pending bills and other commitment.o How new and old policies in budgeting are handled.O Ensuring budget prioritization is fully inclusive of all expenditure, i.e.

D Extra-budgetary fundinga Tax expenditures, etc.

It is envisaged that successive implementation of MTEF (program based budgeting) reforms willamong other things lead to greater transparency, sound and comprehensively based resourceutilization. This however, is underpinned by the need to substantially improve budgetpreparation techniques across the board.

1.1.2 Transparency and integrity of the budgetary system and mechanism

With the introduction of MTEF, government budgeting process is becoming much moreinclusive and transparent that in the past, thus reducing potential risks during budget execution.Transparency and integrity in the preparation of the next MTEF based budget will substantiallybenefit from the recently concluded consultations with stakeholders of the Poverty ReductionStrategy Paper (PRSP) which was fully driven by the government. Workshops and seminarswere held in various major centers in the entire country, where Kenyans at all levels of theeconomy were allowed to articulate their needs and priorities, which would eventually from thebasis for resource allocation at the national level, cascading down to the village level. The roleof the both public as well as private was also particularly important in the dissemination ofpolicies emerging from these prionties at the national level.

1.1.3 Technical capacity and willingness to implement and promote bestpractice

Although the concept of the MTEF has been in the policy discussions within the government forthe last three years, as a rew tool for controlling public expenditure, its fruition has remainedelusive until the year 2000/2001 budget. This is the first time the budget was prepared under theprinciples of MTEF. Even then, it was clear that most of the government agencies did notadequately understand the MTEF conceptual framework. Undoubtedly therefore, it would beacceptable to say that year 2000/2001 was just a first step in the strategy of reforming thebudgetary formulation process in the government. It is trusted that the momentum now alreadyput in place will be pursued with vigor to bring the intended improvement in the publicexpenditure management in Kenya. National priorities will be reflected conspicuously in thegovernment budget allocation, and any inevitable budget cuts will be applied selectively toensure national priorities are only affected as a last resort. Meanwhile, before the MTEFprinciples are perfectly embedded in future budgets a number of strategic areas have beenidentified and will be immediately ring- fenced against any budget cuts. These are expendituresrelated to Kenya Revenue Authority, Local Authority Transfer Fund, Maize Safety Net, CILOR,Fuel Levy and Constitutional Review operations. Other protected areas are projects and

-5-

Country Financial AccountabilityAssessment Republic of Kenya

programs that focus on poverty eradication in HIV/AIDS, Primary and Secondary Education,with special emphasis to girl child, and other social spheres.

1.1.4 Ongoing reforms

Through the Integrated Fmancial Management Information System (IFMIS)3 and with theintroduction of the MTEF it is expected that budgeting process in government will be moretransparent, and thereby enhancing accountability. MTEF will promote the need to have arealistic costing of policies which will culminate into a budget that is not only reliable but alsodependable within the country 's resource limits. In essence therefore, it will be based on nationalpriorities that are articulated by the government policies and are agreed by its people.

1.2 Assessment of the current system

Considerable fiduciary risks remam in the budgeting system in Kenya, particularly with regard tobudget execution. In this, there are obvious risks attributed to inadequate assurance thatallocated resources are used economically and efficiently for the intended purposes andbeneficiaries. There is insufficient comfort that value for money is obtained. This position hasbeen cited in the various reports of the Controller and Auditor General (C&AG). Mechanisms toensure that allocated budget resources are utilized efficiently to lead to the intended outcomes aresubstantially weak. Similarly, institutions of accountability in the public sector that underpin thefoundation financial discipline are also weak and unable to play that role reliably. Lack ofcompliance with established financial and procurement regulations have completely renderedmany initiatives aimed at strengthening the control environment ineffective. Some of the majorfactors attributing to this situation are:

* Weakness in accounting and financial reporting of public expenditures (as illustrated inchapter 2 and 4), which make the diversion of resources to unintended uses possible withoutrapid detection until long after the effect. IFMIS and better skilled internal auditors willsignificantly allow measures to mitigate against this risks to be taken and institutionalized.

* Although the potential gams of the MTEF concept are yet to be fully understood, appreciatedand unlocked, it's hoped that greater effort will be made to link budget inputs to outputs andoutcomes/impact taking the efficiency factor into consideration. This will require workingand reliable monitoring and evaluation instruments which can be complimented by IFMIS toprovide management with information for timely decision making.

* The existence of poor linkage between policies and budget process, has made it impossible tomeasure outputs from activities where resources have been used. MTEF based budgets areexpected to ensure that policies are properly linked to budgets and that outputs can bedetermined and measured.

* With greater mvolvement of stakeholders, for example the recent PRSP consultations, itsvery probable that reality check mechanisms can be built among the public, which will helpto install discipline and positive attitude in public service delivery. This should becomplimented by the institutional strengthening planned at the district level.

* Private sector participation in the public budget management system is a major area ofconcern, which weakens accountability, making it difficult to justify any support from the

3Refer to Section 2 of this report for details about this new initiative.

- 6 -

Country Financial Accountability Assessment Republic of Kenya

public sector. From the recent consultations underlying the PRSP and the last World BankCountry Assistance Strategy (CAS) process, it's evident that private sector is graduallystarting to be attracted into public sector affairs, e.g. sponsorship of social and publicprojects by some multinational and regional business conglomerates especially in theconsumer industry (e.g. tobacco and beverages).

O The budget execution has in practice not adhered to government procedures, therebycompromising its purpose for control and accountability in the management of publicresources.

o Finally, falling domestic revenues agamst projected forecasts is undermining the ability ofgovernment to sustain a reliable and dependable level of service delivery, which often tendsto exert undue pressure on available resources against many demands. Realistic costing ofpolicies and budgets cannot therefore be overemphasized as an important element of publicexpenditure management.

1.3 Conclusion and recommendations

In conclusion, it is not disputable that the budgeting process is underpinned on a stronginstitutional and elaborate legal framework. However, some improvements are still needed toperfect the practice. The government lDpes to put forward in the coming years greater effort tobuild the necessary capacity on the application of the MTEF principles in ministries, departmentsand the Treasury to improve on future budgets. The following are some key recommendationswhich would contribute towards achievmg the desired results in the medium to long term4 :

o The MTEF should be pursued to ensure it's the only frilly adopted formal mechanism ofinstilling discipline at all levels of government.

O Improved and realistic cash revenue forecasting is imperative. Appropriate tools and relevantinformation should be used to help achieve this goal. Furthermore the present system ofweekly cash rationing should be transformed into a proper financial planning process whichis based on improved channels of infornation and operates in a transparent manner.

o The use of extra-budgetary funds should only be allowed when there are strong reasons forretaining the revenues and expenditures separately. The efficient implementation of theMTEF would contribute towards this goal.

o Government Policies and Regulations must be handed down and be seen to be adhered to inaccordance with established implementation guidelines and rules. Any deviation therefromother than as prescribed by the same statutes must be remedied and appropriate actions takento punish the culprits and accomplices of the act.

4A report prepared by staff from the IMF, Fiscal Affairs Department, Kenya. An Agendafor Reforming PublicExpenditure Management contains a detailed action plan with recommendations on reforms which even goesbeyond the scope of the CFAA

-7-

Country Financial Accountability Assessment Republic of Kenya

SECTION 2: GOVERNMENT ACCOUNTING AND FINANCIALREPORTING

2.1 Review of the current system

2.1.1 Legislative and regulatory environment

Government accounting and financial reporting in Kenya is governed by the Exchequer andAudit Act, CAP 412 (1955), and the Paymaster-General Act, CAP 413 (1960). In addition,Sections 48 and 99 to 105 of the Constitution of Kenya provide the broad legal framework forthe management and control of public funds in Kenya. The Constitution grants the Minister forFinance the mandate of managmg and controllmg of government finances into and out of theConsolidated Fund. Subsequent operational guidelines are handed down by Treasury in the formof The Government Financial Regulations and Procedures (1989), which are from time to timeupdated through Treasury Circulars to the Accounting Officers in ministrnes, departments anddistricts. The Accountant General's Department in Treasury s empowered to direct and guidethe accounting function in the government and manage the cash basket, which is ideally a budgetmanagement function. The Accountant General is also responsible for ensuring there issufficient staff capacity in all ministries, departments and districts in consultation with otherrelevant departments of government5.

Historically the process of planmng, executing, accounting and reporting public resources in thegovernment has been the responsibility of the MOFP. There are elaborate and well documentedguidelines and procedures detailing how the process works, with clear separation of rolesbetween various govermnent departments, which illustrates that a high degree of integrity hasbeen in-built in the system. The MOFP is empowered by Parliament through the AppropriationAct to expend sanctioned budgeted allocations, on the basis of a Presidential Warrant (GeneralWarrant) authorizing withdrawal of funds from the Consolidated Fund. The Treasury applies tothe C&AG for Credits on the Exchequer account to meet charges expected to be mcurred by theAccounting Officers, who are the Chief Executives of spending ministries and departments TheCentral Bank of Kenya (CBK), in its role as the govermment's banker, executes its mandate onthe basis of the C&AG authority and transfer funds from the Exchequer account as directed bythe Treasury from time to time for defraying approved government expenditure. In turn, theMinister for Finance will issue Treasury Warrants granting authority to incur expenditure (AIEs)to the Accounting Officers in accordance with their approved budgets. Subsequent releases offunds within the fiscal year are henceforth made available by Treasury to the individual bankaccounts of ministnes/departments. The amounts available depend on the monthly remittance ofrevenue collected by the Kenya Revenue Authority.

5 These are the Public Service Commission of Kenya for recruitment, reward, and discipline of civil servants andthe Directorate of Personnel Management for career development and creation of new positions other than thoseestablished in the civil service Provincial Administration arm in the Office of the President is involved is placementof District Accounting staff in the districts6Kenya Revenue Authority was established in 1995 as a parastatal under the MOFP for mobilizing andconsolidating collection of government revenues

-8 -

Country Financial Accountability Assessment Republic of Kenya

2.1.2 Transparency and integrity

The historical genesis of government accounting system in Kenya can be traced way back to thepre-independent era when the country was administered by the colonial government of the day.To a large extent, the system has remained substantially the same to the present time, except forminor changes that have been made from time to time. The system is fundamentally cash basedaccounting, and substantially manual and labor intensive. It is basically simple and easy tomaintain. However, it's simplicity has been overwhelmed by the numerous and sometimecomplex transactions and demands of government. As a result, the system is no longer able toproduce reliable and complete financial information and audited accounts in a timely manner.This situation exacerbates the fiduciary risks involved and compromises the country's credibilityand accountability rating in relative terms. Salient features of the government accounting systeminclude those mentioned below.

Cash based government accounting: The budget and accounting systems are primanly cashbased. The release of funds from the Exchequer is based on the budgetary allocation, anddependent on the revenue mobilized from various sources. In practice however, funds are usuallyreleased by rationing the available funds to priority areas as determined by MOFP, and not onthe basis of proportionate distribution across the ministries and departments.

Flow offunds: The flow of funds from the Exchequer to the spending ministries, departmentsand districts, is triggered by quarterly requisition for funds from the spending units. Amountsand timeliness of the releases are incidentally dependent on the availability of revenue fundscollected at the national level by the Kenya Revenue Authority. This applies to both governmentfunds as well as donor funds that are channeled through the budget system. In essence therefore,donor funds advanced to government through the Special Accounts for projects can not beaccessed directly by the projects without being subjected to the exchequer channel. Thisrequirement is legally enshrined in section 99 of the Constitution of Kenya and further elaboratedin section 5 and 11 of the Exchequer and Audit Act. Due to this, flow of funds has for a longtime been a major impediment to timely project implementation. This has posed high fiduciaryrisk to donor assisted projects in Kenya. In view of this, it was imperative that other options hadto be explored with a longer term solution. As a result, the government recently agreed to revisitthe legal aspects that stand on the way to expediting flow of funds to projects to facilitate theirtimely implementation. Unfortunately, the proposed draft "Public Financial Management andAccountability Bill 2000" does not appear to explicitly attended to the problem.

Pending bills: The downside of the cash based system is that projected revenue targts arehardly achieved in aggregate terms. Meanwhile, budget execution on the basis of AlEs isactively ongoing. This system pose a high risk of building up huge pending bills year after year,unless sufficient resources are set aside for defraying backlog of pending bills. The governmentintroduced a Cash Management System in FY 1996/97, which was expected to mitigate againstthe risk of having any pending bills in line ministries. Although this measure initially seemed togive positive results, it was not able to prevent the emergence of pending bills altogether.

Budget monitoring: It is important to recognize and commend the government for establishing aBudget Monitoring Unit (BMU) whose objective is to analyze monthly revenue and expenditurereturns submitted by line ministries and departments. On this basis, BMU monitors and signalsareas where budget management is potentially getting out of control (risk behavior). Although

-9-

Country Financial Accountability Assessment Republic of Kenya

BMU has been in place for the last two years now, the unit admits that it's potential has not beenfully exploited to impact notable change in financial disciplme in the Treasury and other lineministries. The unit prepares monthly analytical reports with recommendations for doableactions to the management for consideration Some of the unit's recommendations have beenwell received and put under an implementation plan while others are still under consideration.

Accounting and financial reporting system: Because the entire government operates a cashbased budget and accounting system there are no accruals, receivables (debtors), prepaymentsand payables (liabilities). Inventories of all types of assets are often maintained, but at theministry level which do not form part of the accounting system. Venfication of these records isnot a regular activity, except when auditors would include it in their audit programs for testing.The conventional financial statements are not prepared, making it difficult to determine the networth of individual ministries and the entire government. However, it's important to take notethat Treasury guidelines for the preparation of Appropriation Accounts and other memorandumrecords are adequately followed by ministnes and departments. For many years, accounting forproject expenditures was subsumed in the ministry's appropriation accounts, which madetracking of donor funds used in projects impossible. This posed very high fiduciary nsk,especially to the multi- lateral donors who did not have any idea whether their funding was bemgused for intended purposes. To mitigate against this risk, various donors have tried to buildaccountability safeguards around the projects of their interest with a view to tracking theirfinancial assistance. The main down side of this approach, is that it mcks coordination andbuilds many small stand alone parallel systems scattered across the ministries, and can nottherefore be sustained beyond the project's life. Recognition of this fact, by both the governmentand development donors prompted them to work together for a mutually acceptable solution.This provided the government with an opportunity to review and modermize its accountingsystem and legislative framework. In 1995/96, the Accountant General in collaboration withdevelopment partners started to set out a strategy to diagnose the problem areas with a view tostrengthening the accounting system to suit the present day's needs. This process, evolved intoan action plan, with three phases, i.e. short tenn, medium term and longer term actions.Meanwhile, non-monetary reform actions began to be implemented almost immediately. Sincethen, useful changes have been undertaken by government which has to some extent improvedsome of the areas of concern, e.g. reduction of steps from 45 to 12 in payment procedures mdonor funded projects, thus reducing the transaction time from 150+ days to about 45-60 days onaverage. The accounting aspects of the problem have also gradually improved, especially withregard to timeliness in the preparation of draft annual accounts for audit. Some major issuessuch as the flow/tracking of funds remains outstanding which still poses some fiduciary risk. Itis envisaged that in the medium to long term, these concerns will be addressed as the governmentembarks on a project to integrate the key functional arms of Treasury through an IntegratedFinancial Management Information System (IFMIS 7).

Basis of financial reporting: In Kenya, government financial reporting and accountmg isprimarily based on the mandated scope as stipulated in the Government Financial Regulationsand Procedures backed legally by the Exchequer and Audit Act. The government preparesappropriation accounts detailing the receipts and issues of public monies from the Exchequer by

7 IFMIS was conceived from a diagnostic analysis of the Kenya Government Financial and Accounting system in1996 following the results of Country Portfolio Performance Review conducted by the World Bank and shared withother development partners In summary, it was evident that Public Expenditure Management and Flow ofBudgeted Funds through the government channels was completely clogged and constrained

- 10-

Country FinancialAccountability Assessment Republic of Kenya

each line ministry and department. Although there is an intent to move toward accrual basedaccounting system soon, in reality it will take considerable time and effort to develop anappropriate environment and capacity to a level that will be able to support accrual accounting.

Computerization and the IFMIS: Computerization of the accounting and reporting function ingovernment has been fragmented smce the early ninety's. Until recently there has been twocomputing sections in the MOFP. The Micro Computer Department dealt with the financialrecords such as the Vote Book and pensions and the Government Computer Services wasresponsible for, inter alia, the processing of the payroll system on a main frame system. Thesetwo sections have now been amalgamated. Software is mainly based on COBOL and Novell.Furthermore, accounting and reportmg functions at district level are not fully computenzed.Meanwhile, the IFMIS-project has been undertaken in the Accountant General's department toreplace the current computer systems and to develop an integrated Ledger Management Systemthat will generate more useful information to facilitate informned decision making bymanagement. Although it is estimated to take about 5 years to be completed in all phases and alllocations, installation would be done in an phased manner. This could bring about significantchanges within a two year time frame. The approach is to benefit from purchasing proven off-the-shelf software.

IFMIS aims at brnging together planning and budget preparation, budget execution and controlas well as budget monitoring on one hand with financial accounting and reporting on the otherhand into one system, where data is shared and networked. These will eventually help tointerface all the necessary linkages that are fundamental in a well structured financialmanagement system. It is envisaged that when the system is fully rolled out to encompass allministnes, departments and districts, flow of financial mformation will substantially improve andenhance transparency and mtegnty m government financial management and decision making.IFMIS will enable managers to lmk budgetary inputs to outputs and outcomes, which is presentlyan impossible task. When the system is fully implemented, the Treasury and its Finance Officersbased in line ministries will have the tools and environment to control public expenditure. Thiswould help to prevent the possibility of expenditure centers in ministnes, departments anddistricts from overrunning their budget by entering into commitments which can not be financedwhich give rise to pending bills, currently about Kshs 10 billion (US $132 million).