27

M E T A L S Research and Consulting MetalsPlus Sample Research Project Slides

M E T A L SResearch and Consulting

MetalsPlus

Sample Research Project Slides

M E T A L SResearch and Consulting

Database Profile of Major Metals Users

M E T A L SResearch and Consulting

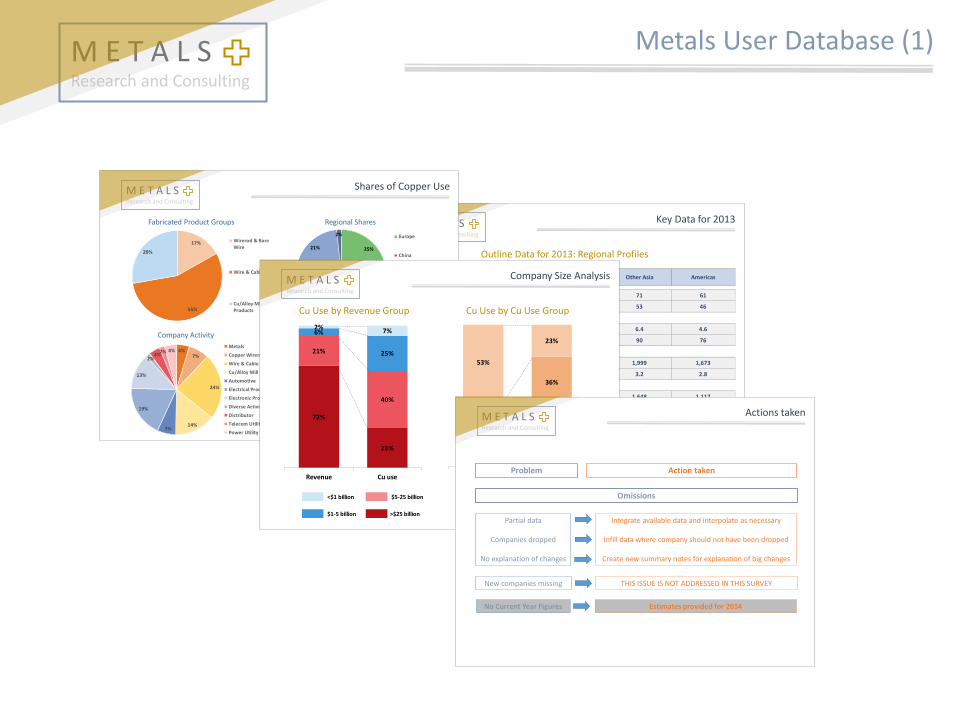

Metals User Database (1)

M E T A L SResearch and Consulting

Key Data for 2013

Outline Data for 2013: Regional Profiles

Europe & Africa China Other Asia Americas

Number of Companies 51 36 71 61

Companies with Financials 38 18 53 46

Copper Use (Mt) 5.2 6.6 6.4 4.6

Average Cu Use (kt) 103 185 90 76

Net Sales ($ billion) 1,771 141 1,999 1,673

Cu kg per $ million 3.0 47.2 3.2 2.8

Cost of Sales 1,413 123 1,648 1,117

Cu % of Cost of Sales 2.7% 39.5% 2.8% 3.0%

Operating Profit 114 7 127 228

Ratio Cu Value / Op. Profit 33.6% 738.8% 37.0% 14.8%

M E T A L SResearch and Consulting

17%

55%

28%

Wirerod & BareWire

Wire & Cable

Cu/Alloy MillProducts

25%

32%

20%

21%

2% Europe

China

Other Asia

North America

Latin America

4%7%

24%

14%7%

19%

13%

2%4%

2% 4%Metals

Copper Wirerod

Wire & Cable

Cu/Alloy Mill

Automotive

Electrical Products

Electronic Products

Diverse Activity

Distributor

Telecom Utility

Power Utility

23%

36%

32%

9% <75 kt Cu

75-200 kt Cu

200-500 kt Cu

Over 500 kt Cu

Shares of Copper Use

Fabricated Product Groups Regional Shares

Company Activity Company Copper Use

M E T A L SResearch and Consulting

Company Size Analysis

Cu Use by Revenue Group Cu Use by Cu Use Group

<$1 billion $5-25 billion

$1-5 billion >$25 billion

<75 kt 200-500 kt

75-200 kt >500 kt

72%

28%

21%

40%

6%

25%

2%7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Revenue Cu use

0%9%3%

32%44%

36%

53%

23%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Revenue Cu use

M E T A L SResearch and Consulting

Actions taken

Problem Action taken

Partial data

Companies dropped

No explanation of changes

Integrate available data and interpolate as necessary

Infill data where company should not have been dropped

Create new summary notes for explanation of big changes

Omissions

New companies missing THIS ISSUE IS NOT ADDRESSED IN THIS SURVEY

No Current Year Figures Estimates provided for 2014

M E T A L SResearch and Consulting

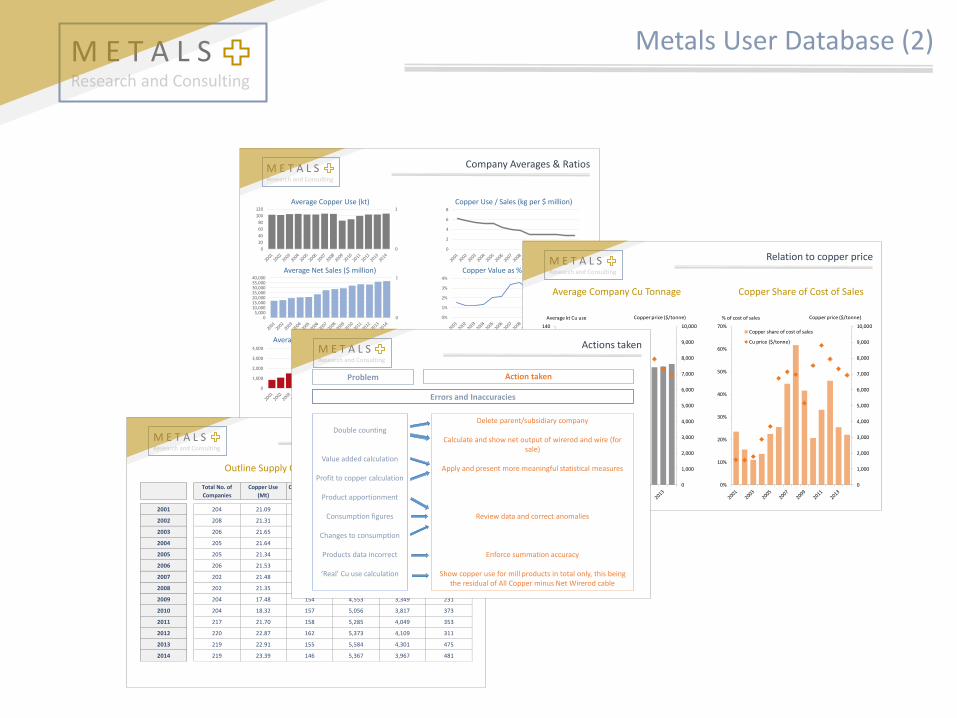

Metals User Database (2)

M E T A L SResearch and Consulting

Key data: All companies

Outline Supply Chain Database Figures

Total No. of

Companies

Copper Use

(Mt)

Companies with

Financials

Net Sales

($ bn)

Cost of Sales

($ bn)

Operating Profit

($ bn)

2001 204 21.09 179 3,044 2,260 147

2002 208 21.31 181 3,198 2,343 188

2003 206 21.65 177 3,482 2,510 264

2004 205 21.64 187 3,812 2,805 261

2005 205 21.34 185 3,798 2,759 249

2006 206 21.53 177 4,165 3,109 262

2007 202 21.48 172 4,742 3,750 278

2008 202 21.35 173 4,949 3,678 212

2009 204 17.48 154 4,553 3,349 231

2010 204 18.32 157 5,056 3,817 373

2011 217 21.70 158 5,285 4,049 353

2012 220 22.87 162 5,373 4,109 311

2013 219 22.91 155 5,584 4,301 475

2014 219 23.39 146 5,367 3,967 481

M E T A L SResearch and Consulting

0

1

0

20

40

60

80

100

120

0

1

05,000

10,00015,00020,00025,00030,00035,00040,000

0

1

0

1,000

2,000

3,000

4,000

0

2

4

6

8

0%

1%

2%

3%

4%

0%

20%

40%

60%

80%

Company Averages & Ratios

Copper Use / Sales (kg per $ million)

Copper Value as % Cost of Sales

Ratio Copper Value / Operating Profit

Average Copper Use (kt)

Average Net Sales ($ million)

Average Operating Profit ($ million)

M E T A L SResearch and Consulting

Relation to copper price

Average Company Cu Tonnage Copper Share of Cost of Sales

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

0%

10%

20%

30%

40%

50%

60%

70%Copper share of cost of sales

Cu price ($/tonne)

Copper price ($/tonne)% of cost of sales

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

0

20

40

60

80

100

120

140Average kt Cu use

Cu price ($/tonne)

Copper price ($/tonne)Average kt Cu use

M E T A L SResearch and Consulting

Actions taken

Problem Action taken

Errors and Inaccuracies

Double counting

Value added calculation

Profit to copper calculation

Product apportionment

Consumption figures

Changes to consumption

Products data incorrect

‘Real’ Cu use calculation

Delete parent/subsidiary company

Calculate and show net output of wirerod and wire (for sale)

Apply and present more meaningful statistical measures

Review data and correct anomalies

Enforce summation accuracy

Show copper use for mill products in total only, this being the residual of All Copper minus Net Wirerod cable

M E T A L SResearch and Consulting

Transformers

M E T A L SResearch and Consulting

Transformers (1)

M E T A L SResearch and Consulting

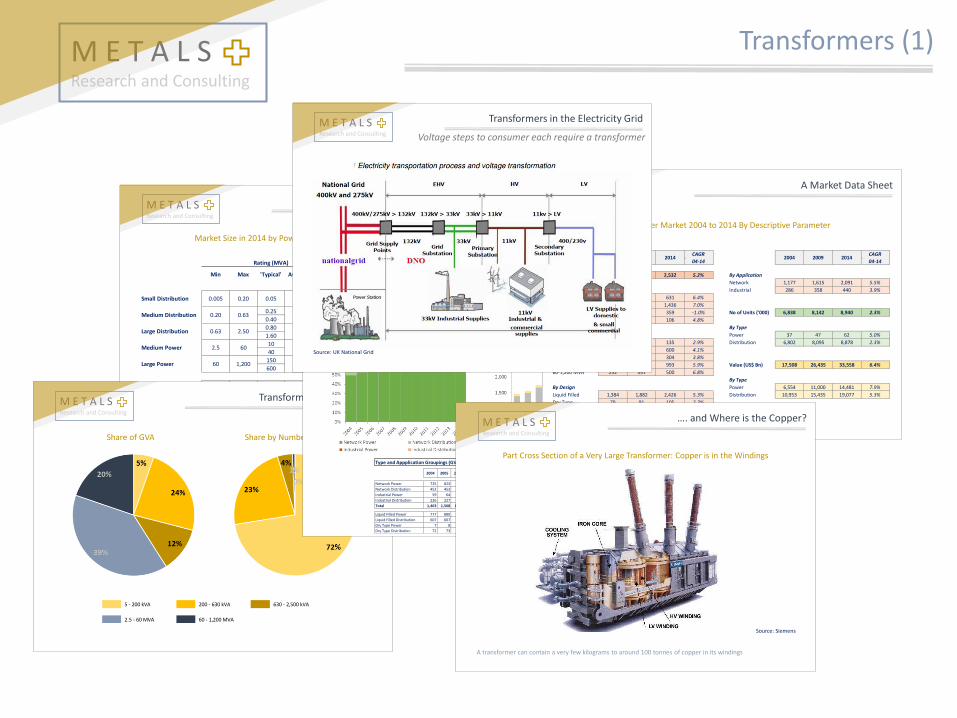

Global Market for Transformers

Market Size in 2014 by Power, Number of Units and Value

Note: Market value estimates are based on manufacturers’ selling prices

0.25

0.40

0.80

1.60

10

40

150

600

Total 0.283 2,532 100.00% 8,940 13.3 33,558

Distribution 0.117 1,039 99.03% 8,878 18.4 19,077

Power 24.149 1,493 0.97% 62 9.7 14,481

Average

$/kVA

Value

Small Distribution 0.005 0.20 0.05 0.02 135 72.4% 6,476 28.5 3,846

Total

GVAUnits %

Units

('000)

Rating (MVA) Units Sales

($ mn)

Medium Distribution 0.20 0.63 0.29 600 22.9%

Min Max 'Typical' Average

Large Distribution 0.63 2.50 0.85 304

2,047 18.3 10,981

4.0% 355 14.0 4,250

0.04% 4Large Power 60 1,200 141 500

58Medium Power 2.5 60 17.0 993 0.7% 10.2 10,132

8.7 4,349

M E T A L SResearch and Consulting

Transformer Market in 2014

Share of GVA Share by Number of Units

5 - 200 kVA 200 - 630 kVA 630 - 2,500 kVA

2.5 - 60 MVA 60 - 1,200 MVA

M E T A L SResearch and Consulting

Types & Applications Trend

Network and Industrial Applications Shares Transformer Type Trend

Type and Appplication Groupings (GVA)

04-14

Network Power 725 823 922 1,042 1,151 1,056 1,157 1,267 1,306 1,334 1,390 6.3%

Network Distribution 452 453 503 548 583 559 603 651 653 669 702 4.0%

Industrial Power 59 64 71 80 87 81 87 95 97 99 103 5.3%

Industrial Distribution 226 227 250 273 291 277 292 313 312 321 337 3.6%

Total 1,463 1,568 1,746 1,942 2,112 1,973 2,139 2,326 2,368 2,423 2,532 5.2%

Liquid Filled Power 777 880 984 1,112 1,228 1,127 1,234 1,351 1,392 1,421 1,481 6.2%

Liquid Filled Distribution 607 607 676 739 786 755 817 880 880 903 945 4.0%

Dry Type Power 7 8 9 10 11 10 10 11 11 12 12 4.5%

Dry Type Distribution 72 73 77 81 88 81 78 84 85 88 93 2.0%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014CAGR

M E T A L SResearch and Consulting

A Market Data Sheet

Transformer Market 2004 to 2014 By Descriptive Parameter

CAGR CAGR

04-14 04-14

Volume (GVA) 1,463 1,973 2,532 5.2% By Application

Network 1,177 1,615 2,091 5.5%

By Region Industrial 286 358 440 3.9%

Europe 337 465 631 6.4%

Asia 691 1,009 1,436 7.0%

North America 373 416 359 -1.0% No of Units ('000) 6,838 8,142 8,940 2.3%

Latin America 61 82 106 4.8%

By Type

By Power Rating Power 37 47 62 5.0%

5 - 200 kVA 96 115 135 2.9% Distribution 6,802 8,095 8,878 2.3%

200 - 630 kVA 382 478 600 4.1%

630 kVA - 2.5 MVA 200 243 304 3.8%

2.5 - 60 MVA 532 745 993 5.9% Value (US$ Bn) 17,508 26,435 33,558 6.4%

60-1,200 MVA 252 391 500 6.8%

By Type

By Design Power 6,554 11,000 14,481 7.9%

Liquid Filled 1,384 1,882 2,426 5.3% Distribution 10,953 15,435 19,077 5.3%

Dry Type 79 91 105 2.3%

20142004 2009 2014 2004 2009

M E T A L SResearch and Consulting

Transformers in the Electricity Grid

Voltage steps to consumer each require a transformer

Source: UK National Grid

M E T A L SResearch and Consulting

…. and Where is the Copper?

Part Cross Section of a Very Large Transformer: Copper is in the Windings

A transformer can contain a very few kilograms to around 100 tonnes of copper in its windings

Source: Siemens

M E T A L SResearch and Consulting

Transformers (2)

M E T A L SResearch and Consulting

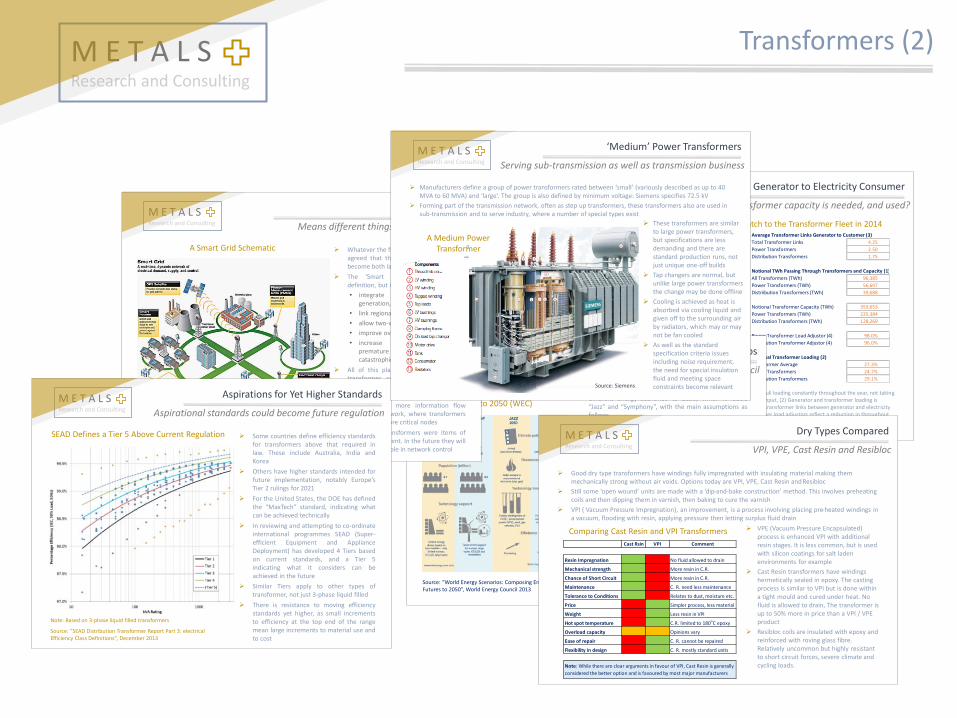

Generator to Electricity Consumer

How much transformer capacity is needed, and used?

Electricity Generation and Consumption Average Transformer Links Generator to Customer (3)

Electricity Consumption (TWh) 20,743 Total Transformer Links 4.25

Generating Capacity (GVA) 5,764 Power Transformers 2.50

Notional Generating Capacity (TWh) (1) 50,489 Distribution Transformers 1.75

Electricity Generated (TWh) 22,679

Calculated Loading % (2) 44.9% Notional TWh Passing Through Transformers and Capacity (1)

All Transformers (TWh) 96,385

Stock of Transformers in Place (GVA) Power Transformers (TWh) 56,697

Total GVA 40,371 Distriibution Transformers (TWh) 39,688

Power Transformers GVA 25,729

Distribution Transformers GVA 14,643 Notional Transformer Capacity (TWh) 353,653

Power Transformers (TWh) 225,384

Stock of Transformers in Place ('000 Units) Distribution Transformers (TWh) 128,269

Total Units ('000) 100,515

Power Transformers ('000) 1,054 Power Transformer Load Adjustor (4) 98.0%

Distribution Transformers ('000) 99,461 Distribution Transformer Adjustor (4) 96.0%

Average Transformer Size Notional Transformer Loading (2)

Average Power Rating (MVA) 0.40 Transformer Average 27.3%

Average Power Transformer (MVA) 19.40 Power Transformers 24.7%

Average Distribbution Transformer (MVA) 0.14 Distribution Transformers 29.1%

Global Requirement for Transformers and Match to the Transformer Fleet in 2014

Notes: (1) Generator and transformer notional capacity is calculated assuming full loading constantly throughout the year, not taking into account Power Factor, Harmonic or other effects limiting real-world throughput, (2) Generator and transformer loading is calculated dividing throughput by notional capacity, (3) The average number of transformer links between generator and electricity customer is estimated, and intended to represent global averages, (4) Transformer load adjustors reflect a reduction in throughput resulting from losses in the network before the transformer is reached.

Conclusion: Calculated loadings of transformers of 24.7% for power and 29.1% for distribution transformers match industry estimates.

M E T A L SResearch and Consulting

Alternative Energy Scenarios

“Jazz” and “Symphony” paths of the World Energy Council

The World Energy Council has looked at two verydifferent energy scenarios to 2050, which it labels“Jazz” and “Symphony”, with the main assumptions asfollows

Jazz: A world where there is a consumer focus onachieving energy access, affordability, and quality ofsupply with the use of best available energy sources

Symphony: A world where there is a voter consensuson driving environmental sustainability and energysecurity through corresponding practices and policies

Jazz is the higher wealth scenario, but one where thepolicy drive to create a sustainable energy future iscomparatively weak

Interestingly, while the lower wealth “Symphony”scenario shows smaller electricity increments it shows arise in its share of total energy, with an electricityinfrastructure very different from that we see today

“Jazz” & “Symphony”: Two Energy Scenarios to 2050 (WEC)

Source: “World Energy Scenarios: Composing Energy Futures to 2050”, World Energy Council 2013

M E T A L SResearch and Consulting

The Smart Grid

Means different things to different people

Source: Utility Products .Com

A Smart Grid Schematic Whatever the future energy scenario, it isagreed that the electricity network willbecome both larger and smarter

The ‘Smart Grid’, has no precisedefinition, but it is likely to:

• integrate sources of distributedgeneration, based on renewables

• link regional and national grids

• allow two-way flow of electricity

• improve overall network efficiency

• increase system security, avoidpremature equipment ageing andcatastrophic failure

All of this places specific demands ontransformer construction (reviewed inthe next Section), especially if there isstill no effective means of energy storage

It also means more information flowwithin the network, where transformerswill become more critical nodes

In the past transformers were items ofpassive equipment. In the future they willplay an active role in network control

M E T A L SResearch and Consulting

Aspirations for Yet Higher Standards

Aspirational standards could become future regulation

SEAD Defines a Tier 5 Above Current Regulation

Note: Based on 3-phase liquid filled transformers

Source: “SEAD Distribution Transformer Report Part 3: electrical Efficiency Class Definitions”, December 2013

Some countries define efficiency standardsfor transformers above that required inlaw. These include Australia, India andKorea

Others have higher standards intended forfuture implementation, notably Europe’sTier 2 rulings for 2021

For the United States, the DOE has definedthe “MaxTech” standard, indicating whatcan be achieved technically

In reviewing and attempting to co-ordinateinternational programmes SEAD (Super-efficient Equipment and ApplianceDeployment) has developed 4 Tiers basedon current standards, and a Tier 5indicating what it considers can beachieved in the future

Similar Tiers apply to other types oftransformer, not just 3-phase liquid filled

There is resistance to moving efficiencystandards yet higher, as small incrementsto efficiency at the top end of the rangemean large increments to material use andto cost

M E T A L SResearch and Consulting

‘Medium’ Power Transformers

A Medium Power Transformer

Source: Siemens

Manufacturers define a group of power transformers rated between ‘small’ (variously described as up to 40 MVA to 60 MVA) and ‘large’. The group is also defined by minimum voltage: Siemens specifies 72.5 kV

Forming part of the transmission network, often as step up transformers, these transformers also are used in sub-transmission and to serve industry, where a number of special types exist

These transformers are similar to large power transformers, but specifications are less demanding and there are standard production runs, not just unique one-off builds

Tap changers are normal, but unlike large power transformers the change may be done offline

Cooling is achieved as heat is absorbed via cooling liquid and given off to the surrounding air by radiators, which may or may not be fan cooled

As well as the standard specification criteria issues including noise requirement, the need for special insulation fluid and meeting space constraints become relevant

Serving sub-transmission as well as transmission business

M E T A L SResearch and Consulting

Dry Types Compared

VPI, VPE, Cast Resin and Resibloc

Good dry type transformers have windings fully impregnated with insulating material making them mechanically strong without air voids. Options today are VPI, VPE, Cast Resin and Resibloc

Still some ‘open wound’ units are made with a ‘dip-and-bake construction’ method. This involves preheating coils and then dipping them in varnish, then baking to cure the varnish

VPI ( Vacuum Pressure Impregnation), an improvement, is a process involving placing pre-heated windings in a vacuum, flooding with resin, applying pressure then letting surplus fluid drain

Comparing Cast Resin and VPI Transformers

Cast Rsin VPI Comment

Resin Impregnation No fluid allowed to drain

Mechanical strength More resin in C.R.

Chance of Short Circuit More resin in C.R.

Maintenance C. R. need less maintenance

Tolerance to Conditions Relates to dust, moisture etc.

Price Simpler process, less material

Weight Less resin in VPI

Hot spot temperature C.R. limited to 180oC epoxy

Overload capacity Opinions vary

Ease of repair C. R. cannot be repaired

Flexibility in design C. R. mostly standard units

Note: While there are clear arguments in favour of VPI, Cast Resin is generally

considered the better option and is favoured by most major manufacturers

VPE (Vacuum Pressure Encapsulated) process is enhanced VPI with additional resin stages. It is less common, but is used with silicon coatings for salt laden environments for example

Cast Resin transformers have windings hermetically sealed in epoxy. The casting process is similar to VPI but is done within a tight mould and cured under heat. No fluid is allowed to drain, The transformer is up to 50% more in price than a VPI / VPE product

Resibloc coils are insulated with epoxy and reinforced with roving glass fibre. Relatively uncommon but highly resistant to short circuit forces, severe climate and cycling loads.

M E T A L SResearch and Consulting

Transformers (3)

M E T A L SResearch and Consulting

Efficiency Standards Also Matter (3)

… materials use may change in ways not entirely expected

Comparing S9, S11 and S13 Standard Transformers in China

Comparing Stacked and 3-D Core Designs Electrical Steel / Copper Ratios (Stacked Core)

Source: Data based on feedback to a Chinese transformer equipment making manufacturer

Note: Example shows material saving by alternative core design and a relative decrease of Cu use between S11 and S13

M E T A L SResearch and Consulting

North America (1)

Market Shares (MVA)

Conductor (Cu Equiv.)

200 - 630 kVA

5 - 200 kVA

200 - 630 kVA

630 - 2,500 kVA

2.5 - 60 MVA

60 - 1,200 MVA

North America Market Profile

CAGR

04-14

Electriciity Generation and Use (TWh)

Generation 4,774 4,794 5,093 0.4%

Use 4,436 4,453 4,731 0.4%

Transformer Market (GVA)

5 - 200 kVA 38 40 36 -1.5%

200 - 630 kVA 95 96 86 -1.8%

630 kVA - 2.5 MVA 32 32 29 -2.0%

2.5 - 60 MVA 140 162 139 -0.6%

60-1,200 MVA 68 87 70 -0.1%

Total 373 416 359 -1.0%

Sources of Demand (GVA)

Incremental 185 227 133 -4.4%

Replacement 188 189 227 1.5%

Network 296 335 287 -0.9%

Industry 77 82 72 -1.4%

Liquid Filled 330 373 320 -0.9%

Dry Type 43 44 40 -1.7%

Material Use (kt)

Electrical Steel 283 329 324 0.6%

Copper 107 92 76 -3.9%

Aluminium 90 116 122 2.1%

Note: Aluminium in Cu equivalent

2004 2009 2014

M E T A L SResearch and Consulting

Forecasts (3)

Long Term Transformer Development

90-00 00-10 10-20 20-30 30-40 40-50

Fleet of Transformers ('000 GVA)

Europe & Africa 7.96 9.96 11.49 13.97 16.81 20.25 24.29 2.3% 1.4% 2.0% 1.9% 1.9% 1.8%

Asia & Ocenaia 3.59 6.70 13.23 25.86 34.67 45.76 59.21 6.4% 7.0% 6.9% 3.0% 2.8% 2.6%

Anericas 4.98 6.81 9.38 11.47 14.38 17.38 19.73 3.2% 3.3% 2.0% 2.3% 1.9% 1.3%

Total 16.53 23.47 34.10 51.31 65.86 83.39 103.23 3.6% 3.8% 4.2% 2.5% 2.4% 2.2%

Installation of Transformers (GVA)

Europe & Africa 361 409 530 585 744 1,074 1,217 1.3% 2.6% 1.0% 2.4% 3.7% 1.3%

Asia & Ocenaia 274 439 1,109 1,472 1,392 2,604 2,710 4.8% 9.7% 2.9% -0.6% 6.5% 0.4%

Anericas 274 386 373 538 693 860 838 3.5% -0.3% 3.7% 2.6% 2.2% -0.3%

Total 909 1,234 2,013 2,595 2,828 4,539 4,765 3.1% 5.0% 2.6% 0.9% 4.8% 0.5%

% Increment 68.8% 65.7% 68.1% 66.1% 50.2% 43.2% 41.6% -0.5% 0.4% -0.3% -2.7% -1.5% -0.4%

2050CAGR

20402020 20301990 2000 2010

Long term trends in transformers

Long Term Transformer Fleet Trend ….. Annual Market

M E T A L SResearch and Consulting

Efficiency Standards Also Matter (1)

Early expectations of huge impact on materials content

Materials Content of Alternative 400 kVA Oil Filled Transformers – Absolute and Relative Values

Data taken from Targosz, R., Fassbinder, S. and Baggini, A. (2012) “Power Transformers”

Transformer Codes: The transformer codes are based current voluntary European classifications. The first part in each (“Do” to Ao”) indicates no load losses, “Ao” being the lowest. The latter (“Ck” to Ak”) show load losses, “Ak” being most efficient

Inferences: 1) Materials content differentials are high, with a maximum difference of 64% between highest and lowest. Content differences are greatest at the top of the range. 2) Price (not shown) also varies, in this case estimated at 42% maximum differential. 3) All major materials are affected, but the highest rated product is shown to have a higher rise in copper than other materials. For copper, the maximum range variation is 107%. While the proportionate value rise in steel is less, grade is higher in the more efficient transformers.

M E T A L SResearch and Consulting

Types of Winding

Alternative techniques are employed

Layer Winding

Disc Winding Close Up Showing Coolant Ducts

A Made Up Power Transformer Winding

Alternative winding techniques have been developed to ensure low manufacturing cost, high density of winding, good mechanical strength, good overload capacity, freedom from hot spots and low stray losses. The latter is achieved in higher quality transformers by transposing wires to achieve a low contact length between adjacent wires

The simplest technique is layer winding, often used with strip or foil. Layer winding can be used with made up CTC, lowering production cost

Disc winding is preferred for higher capacity transformers (over 25 kV). Here single or multiple strands are wound in discs, connected at cross-over points

M E T A L SResearch and Consulting

Alternative Core Types: 3-D

The triangular transformer

Source: ABB

A Close Up of the Cores

A Triangular (or 3-D) Core Dry Type Distribution Transformer

Source: ABB

An alternative core form for dry type distribution transformers is the ‘3-D’ or triangular type. It is another wound core design

The 3-D core was developed in its current form in the 1990s, but has recently been gaining ground in China. ABB offers this type in China and elsewhere under the ‘”Tri-Dry” brand, up to 2.5 MVA

The triangular core configuration restores symmetry to three-phase AC systems. Phases have a circular arrangement rather than being arranged side by side. This eliminates differences between middle and outer phases and as a result there is better utilisation of core material

Chinese equipment supplier Midworld claims a 20% saving in silicon steel and a 3% saving in conductor material compared with laminated cores, making the transformers cheap to produce

It also claims very low no load losses and also low noise transformers

M E T A L SResearch and Consulting

Nickel Company Strategies

M E T A L SResearch and Consulting

Nickel Strategies (1)

M E T A L SResearch and Consulting

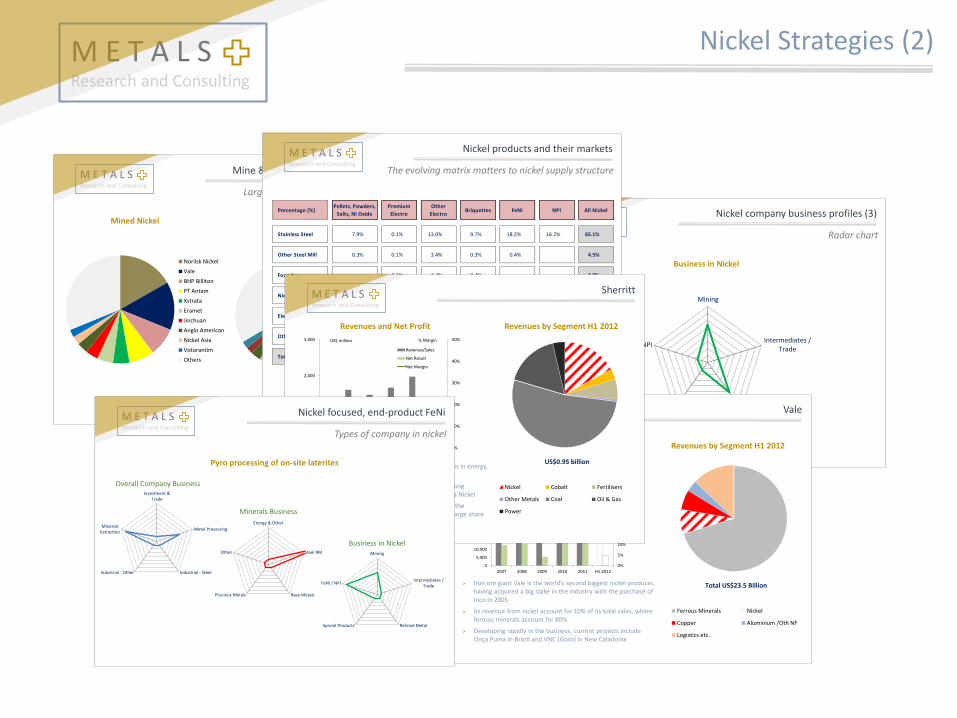

Leaders’ share eroded by growing presence of NPI

Company BaseOutput 2011 (kt

Ni)Share 2011

Rank

2011Share 2007

Rank

2007

Norilsk Nickel Russia 283 17.4% 1 20.2% 1

Vale Brazil 242 14.9% 2 18.7% 2

Jinchuan China 127 7.8% 3 8.0% 4

Xstrata Switerland 106 6.5% 4 8.8% 3

BHP Billiton UK/Ausralia 85 5.2% 5 7.3% 5

Sumitomo Japan 62 3.8% 6 4.3% 6

Eramet France 54 3.3% 7 4.2% 7

Anglo American United Kingdom 49 3.0% 8 3.4% 8

QNI Australia 35 2.2% 9 2.2% 12

Sherritt Canada 35 2.1% 10 2.4% 11

Minera (Glencore) Switerland 30 1.9% 11 2.1% 13

Cubaniquel Cuba 30 1.8% 12 3.2% 9

Cunico Macedonia 29 1.8% 13 1.1% 15

Pacific Metals Co Ltd Japan 28 1.7% 14 2.5% 10

Votorantim Brazil 21 1.3% 15 1.6% 14

Other Refined Ni & FeNi Producers 100 6.1% 11.8%

Nickel Pig Iron Producers 260 16.0% 0.6%

Total 1575 100.0% 100.0%

The Finished Nickel Producers

Quite stable in the recent past

M E T A L SResearch and Consulting

Who are the nickel companies?

What is their strategy towards nickel?

How does nickel fit within an overall business profile?

How does nickel fit within companies’ minerals business profile?

What groups of companies apply to nickel?

….. and what can we say about them?

How is the nickel company profile evolving?

Can we spot winners and losers looking forward?

This presentation is intended to help answer:

Outline

M E T A L SResearch and Consulting

Strategic Positioning of the Major Players

Bubble sizes indicate output of finished Ni in 2011. “Focus on Ni” indicates share of revenue accounted for. “Diversity in Ni” reflects product, market and geographical range of the company

Nickel companies vary in their approach to the business

M E T A L SResearch and Consulting

Anglo American

Revenues and Net Profit Revenues by Segment H1 2012

Although nickel represents a small part of its revenues, the size of the company makes it important in the global market, set to become more so with output from Barro Alto

Business associated with steel, base metals and precious metals & diamonds each from a big portion of Anglo’s overall business portfolio

0%

10%

20%

30%

40%

50%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2007 2008 2009 2010 2011 H1 2012

Revenues / Sales

Net Profit

Net Profit Margin

% Margin

Anglo American Revenues and Net Profit

US$ million

Iron Ore etc. Met Coal Thermal Coal

Copper Nickel Platinum

Diamonds Other

Anglo Revenue in H1 2011

US$16.4 billion

M E T A L SResearch and Consulting

Nickel company business profiles (2)

Business in Minerals

-10.0%

0.0 %

10. 0%

20. 0%

30. 0%

40. 0%

50. 0%

60. 0%

70. 0%

Energy & Other

Steel RM

Base MetalsPrecious Metals

Other

Radar chart

M E T A L SResearch and Consulting

Nickel Strategies (2)

M E T A L SResearch and Consulting

Nickel company business profiles (3)

Business in Nickel

-10.0%

0.0 %

10. 0%

20. 0%

30. 0%

40. 0%

50. 0%

60. 0%

70. 0%

Mining

Intermediates /Trade

Refined MetalSpecial Products

FeNi / NPI

Radar chart

M E T A L SResearch and Consulting

Mine & finished Ni product companies

Mined Nickel Finished Nickel

Norilsk Nickel

Vale

BHP Billiton

PT Antam

Xstrata

Eramet

Jinchuan

Anglo American

Nickel Asia

Votorantim

Others

Shares of Nickel Mine Output in 2011

Norilsk Nickel

Vale

Jinchuan

Xstrata

BHP Billiton

Sumitomo

Eramet

Anglo American

QNI

Sherritt

Others Processed

Chinese NPI

Shares of Finished Nickel Output in 2011

Largely the same, some key diffeences

M E T A L SResearch and Consulting

Vale

Revenues and Net Profit Revenues by Segment H1 2012

Iron ore giant Vale is the world’s second biggest nickel producer, having acquired a big stake in the industry with the purchase of Inco in 2005

Its revenue from nickel account for 10% of its total sales, where ferrous minerals account for 80%

Developing rapidly in the business, current projects include Onça Puma in Brazil and VNC (Goro) in New Caladonia

Ferrous Minerals Nickel

Copper Aluminium /Oth NF

Logistics etc.

Vale Revenues H1 2012

Total US$23.5 Billion

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

65,000

2007 2008 2009 2010 2011 H1 2012

Revenue/Sales

Net Result

Net Margin

% Margin

Vale Revenues and Net Profit

US$ million

M E T A L SResearch and Consulting

Nickel products and their markets

Percentage (%)Pellets, Powders,

Salts, Ni Oxide

Premium

Electro

Other

ElectroBriquettes FeNi NPI All Nickel

Stainless Steel 7.9% 0.1% 13.0% 9.7% 18.2% 16.2% 65.1%

Other Steel Mill 0.3% 0.1% 3.4% 0.3% 0.4% 4.5%

Foundry 0.1% 3.4% 0.4% 3.9%

Nickel Alloy 2.8% 4.5% 2.5% 9.8%

Electoplating 2.5% 4.1% 3.3% 9.9%

Other Uses 2.1% 2.0% 2.7% 6.8%

Total 15.6% 10.9% 28.3% 10.4% 18.6% 16.2% 100.0%

The evolving matrix matters to nickel supply structure

M E T A L SResearch and Consulting

Sherritt

Revenues and Net Profit Revenues by Segment H1 2012

A relatively small company, Sherritt’s main business is in energy, mostly at the extraction stage

Sherritt’s presence in nickel and cobalt is tied to its long association with State interests in Cuba through Moa Nickel

The company is transforming itself in nickel through the Ambatovy project in Madagascar. It also acquired a large share in the Sulawesi project in Indonesia. From Rio Tinto

0%

10%

20%

30%

40%

50%

0

1,000

2,000

3,000

2007 2008 2009 2010 2011 H1 2012

Revenue/Sales

Net Result

Net Margin

% Margin

Sherritt Revenues and Net Profit

US$ million

Nickel Cobalt Fertilisers

Other Metals Coal Oil & Gas

Power

Sherritt Revenue in H1 2012

US$0.95 billion

M E T A L SResearch and Consulting

Nickel focused, end-product FeNi

Pyro processing of on-site laterites

Overall Company Business

Minerals Business

Business in Nickel-10.0%

0.0 %

10. 0%

20. 0%

30. 0%

40. 0%

50. 0%

60. 0%

70. 0%

Investment &Trade

Metal Processing

Industrial - SteelIndustrial - Other

MineralsExtraction

-10.0%

0.0 %

10. 0%

20. 0%

30. 0%

40. 0%

50. 0%

60. 0%

70. 0%

Energy & Other

Steel RM

Base MetalsPrecious Metals

Other

-10.0%

0.0 %

10. 0%

20. 0%

30. 0%

40. 0%

50. 0%

60. 0%

70. 0%

Mining

Intermediates /Trade

Refined MetalSpecial Products

FeNi / NPI

Types of company in nickel

M E T A L SResearch and Consulting

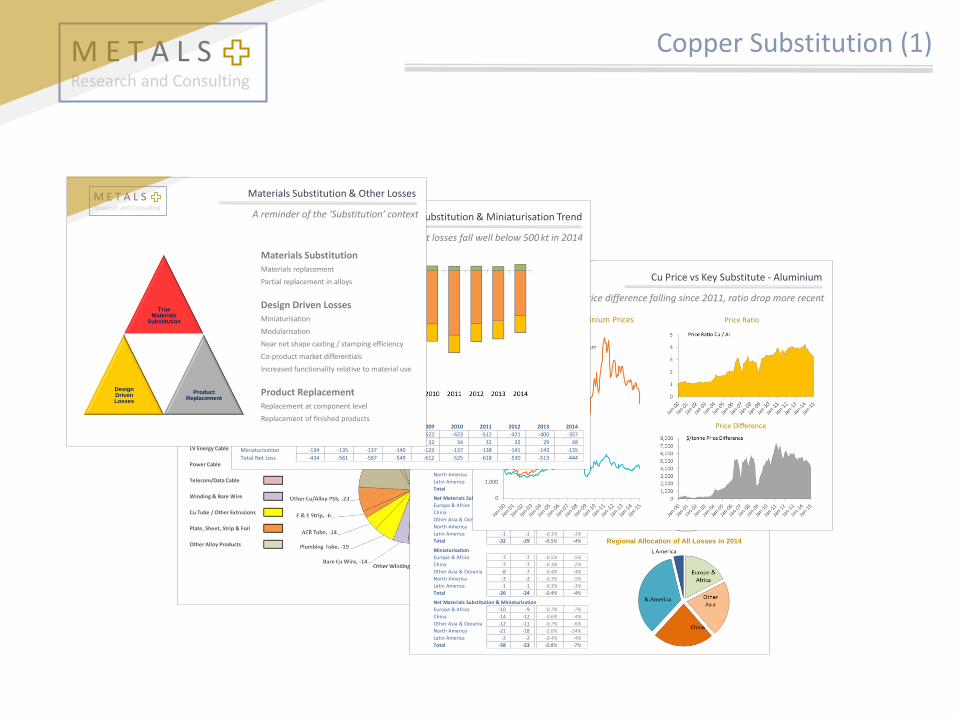

Copper Substitution & Miniaturisation

M E T A L SResearch and Consulting

Copper Substitution (1)

M E T A L SResearch and Consulting

Allocation by product group in 2014, net figures

Materials Substitution in 2014 (1)

KEY

LV Energy Cable

Power Cable

Telecom/Data Cable

Winding & Bare Wire

Cu Tube / Other Extrusions

Plate, Sheet, Strip & Foil

Other Alloy Products

M E T A L SResearch and Consulting

LV Energy Cable (1)

Product Share of All Losses in 2014

Regional Allocation of All Losses in 2014

2013 2014 2014 05-14

Market Size

Europe & Africa 1,303 1,315 1.0% 19%

China 2,017 2,170 7.6% 240%

Other Asia & Oceania 1,665 1,714 2.9% 125%

North America 678 700 3.2% -37%

Latin America 453 457 0.8% 32%

Total 6,116 6,356 3.9% 39%

Net Materials Substitution

Europe & Africa -2 -3 -0.2% -1%

China -7 -6 -0.3% -2%

Other Asia & Oceania -4 -4 -0.3% -2%

North America -18 -16 -2.3% -19%

Latin America -1 -1 -0.1% -1%

Total -32 -29 -0.5% -4%

Miniaturisation

Europe & Africa -7 -7 -0.5% -5%

China -7 -7 -0.3% -2%

Other Asia & Oceania -8 -7 -0.4% -4%

North America -3 -2 -0.3% -5%

Latin America -1 -1 -0.3% -3%

Total -26 -24 -0.4% -4%

Net Materials Substitution & Miniaturisation

Europe & Africa -10 -9 -0.7% -7%

China -14 -12 -0.6% -4%

Other Asia & Oceania -12 -11 -0.7% -6%

North America -21 -18 -2.6% -24%

Latin America -2 -2 -0.4% -4%

Total -58 -53 -0.8% -7%

% Loss / GainData

M E T A L SResearch and Consulting

Cu Price vs Key Substitute - Aluminium

Copper and Aluminium Prices Price Ratio

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

Copper Aluminium

$/tonne

Price Difference

Price difference falling since 2011, ratio drop more recent

M E T A L SResearch and Consulting

Total net losses fall well below 500 kt in 2014

Substitution & Miniaturisation Trend

Annual Net Substitution and Miniaturisation Losses (kt Cu)

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Substitution Loss -315 -450 -479 -433 -522 -423 -512 -421 -400 -357

Substitution Gain 15 24 29 25 32 34 32 32 29 48

Miniaturisation -134 -135 -137 -140 -123 -137 -138 -141 -143 -135

Total Net Loss -434 -561 -587 -549 -612 -525 -618 -530 -513 -444

M E T A L SResearch and Consulting

A reminder of the ‘Substitution’ context

Materials Substitution & Other Losses

True Materials

Substitution

Design Driven Losses

Product Replacement

Materials SubstitutionMaterials replacement

Partial replacement in alloys

Design Driven LossesMiniaturisation

Modularisation

Near net shape casting / stamping efficiency

Co-product market differentials

Increased functionality relative to material use

Product ReplacementReplacement at component level

Replacement of finished products

M E T A L SResearch and Consulting

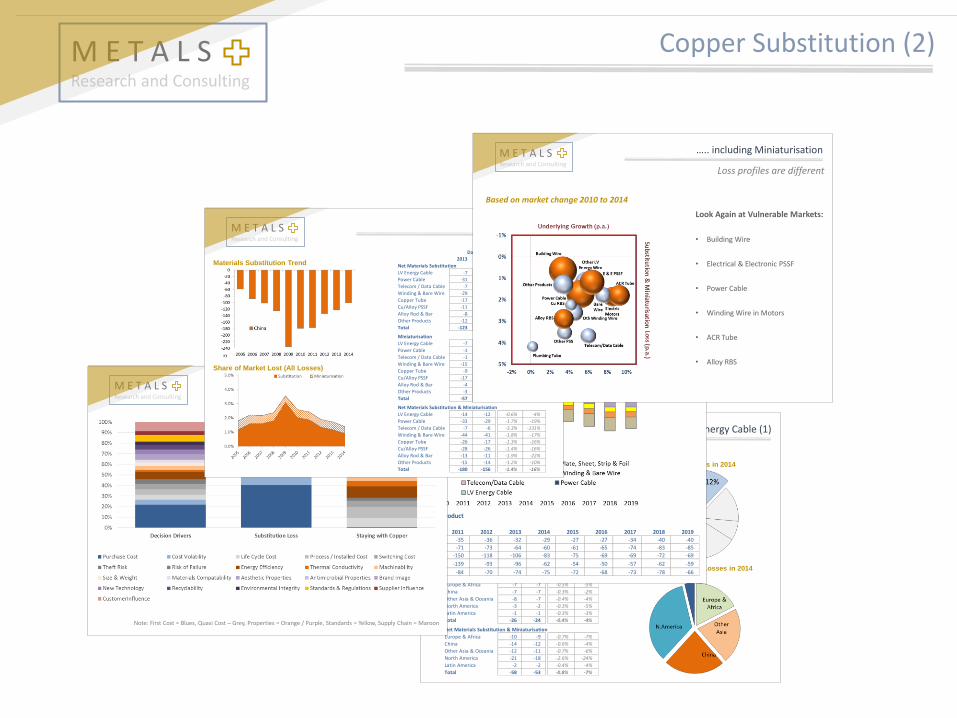

Copper Substitution (2)

M E T A L SResearch and Consulting

LV Energy Cable (1)

Product Share of All Losses in 2014

Regional Allocation of All Losses in 2014

2013 2014 2014 05-14

Market Size

Europe & Africa 1,303 1,315 1.0% 19%

China 2,017 2,170 7.6% 240%

Other Asia & Oceania 1,665 1,714 2.9% 125%

North America 678 700 3.2% -37%

Latin America 453 457 0.8% 32%

Total 6,116 6,356 3.9% 39%

Net Materials Substitution

Europe & Africa -2 -3 -0.2% -1%

China -7 -6 -0.3% -2%

Other Asia & Oceania -4 -4 -0.3% -2%

North America -18 -16 -2.3% -19%

Latin America -1 -1 -0.1% -1%

Total -32 -29 -0.5% -4%

Miniaturisation

Europe & Africa -7 -7 -0.5% -5%

China -7 -7 -0.3% -2%

Other Asia & Oceania -8 -7 -0.4% -4%

North America -3 -2 -0.3% -5%

Latin America -1 -1 -0.3% -3%

Total -26 -24 -0.4% -4%

Net Materials Substitution & Miniaturisation

Europe & Africa -10 -9 -0.7% -7%

China -14 -12 -0.6% -4%

Other Asia & Oceania -12 -11 -0.7% -6%

North America -21 -18 -2.6% -24%

Latin America -2 -2 -0.4% -4%

Total -58 -53 -0.8% -7%

% Loss / GainData

M E T A L SResearch and Consulting

Materials substitution net losses by product

Forecasts to 2019 (1)

Net Materials Substitution by Product

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

LV Energy Cable -11 -35 -36 -32 -29 -27 -27 -34 -40 -40

Power Cable -89 -71 -73 -64 -60 -61 -65 -74 -83 -85

Other Wire & Cable -137 -150 -118 -106 -83 -75 -69 -69 -72 -69

Cu Tube & C/Alloy PSSF -108 -139 -93 -96 -62 -54 -50 -57 -62 -59

Other Products -44 -84 -70 -74 -75 -72 -68 -73 -78 -66

M E T A L SResearch and Consulting

Match reasons for staying with Cu & buyer priorities?

Drivers and Substitution Illustrated

Note: First Cost = Blues, Quasi Cost – Grey, Properties = Orange / Purple, Standards = Yellow, Supply Chain = Maroon

M E T A L SResearch and Consulting

China (1)

Materials Substitution Trend

Share of Market Lost (All Losses)

2013 2014 2014 05-14

Net Materials Substitution

LV Energy Cable -7 -6 -0.3% -2%

Power Cable -31 -28 -1.6% -18%

Telecom / Data Cable -7 -5 -2.9% -128%

Winding & Bare Wire -29 -27 -1.2% -11%

Copper Tube -17 -7 -0.6% -13%

Cu/Alloy PSSF -11 -10 -0.5% -8%

Alloy Rod & Bar -8 -7 -1.2% -14%

Other Products -12 -11 -1.0% -8%

Total -123 -101 -0.9% -12%

Miniaturisation

LV Energy Cable -7 -7 -0.3% -2%

Power Cable -1 -2 -0.1% -1%

Telecom / Data Cable -1 -1 -0.4% -3%

Winding & Bare Wire -15 -15 -0.7% -5%

Copper Tube -9 -9 -0.7% -3%

Cu/Alloy PSSF -17 -16 -0.8% -8%

Alloy Rod & Bar -4 -4 -0.7% -8%

Other Products -3 -3 -0.2% -2%

Total -57 -55 -0.5% -4%

Net Materials Substitution & Miniaturisation

LV Energy Cable -14 -12 -0.6% -4%

Power Cable -33 -29 -1.7% -19%

Telecom / Data Cable -7 -6 -3.3% -131%

Winding & Bare Wire -44 -41 -1.8% -17%

Copper Tube -26 -17 -1.3% -16%

Cu/Alloy PSSF -28 -26 -1.4% -16%

Alloy Rod & Bar -13 -11 -1.9% -22%

Other Products -15 -14 -1.2% -10%

Total -180 -156 -1.4% -16%

% LossData

M E T A L SResearch and Consulting

Loss profiles are different

….. including Miniaturisation

Look Again at Vulnerable Markets:

• Building Wire

• Electrical & Electronic PSSF

• Power Cable

• Winding Wire in Motors

• ACR Tube

• Alloy RBS

Based on market change 2010 to 2014

M E T A L SResearch and Consulting

Electrical Steel & Copper

M E T A L SResearch and Consulting

Electrical Steel & Copper (1)

M E T A L SResearch and Consulting

The two types of electrical steel

GOES (Grain-oriented)

Static machines like transformers, powerreactors and hydro-generators require thegreatest magnetic properties in one favoureddirection (anisotropy).

NOES (Non-oriented)

Rotary and electrostatic machines need goodmagnetic properties in every given direction(isotropy).

NOES is mainly used for motors, generators,small transformers and other electromagneticapplications.

M E T A L SResearch and Consulting

World demand - Generic product types

Total Market = 13.13 MtNOES79%

GOES21%

Non grain oriented products (NOES) account for nearly 80% of the global market by volume

Electrical Steel Demand by Main Product Type (2013)

M E T A L SResearch and Consulting

Electricity losses in the global economy

From the point of electricity generation, losses in transmission and distribution amount to around 17% and motor driven systems around 16%. In each the copper and electrical steel containing component (transformers and motors) play an important and identifiable role but, in each case, account for less than 30% of the loss recorded.

Major Areas of

Loss – Motors and

Transformers

Easily Identified

M E T A L SResearch and Consulting

Motors and transformers market trends

0

500

1,000

1,500

2,000

2,500

3,000

Distribution Transmission & Other

MVA

0

500

1,000

1,500

2,000

2,500

Up to 0.75 kW 0.75 - 75 kW

75 - 375 kW Over 375 kW

GWTransformer Market Growth Motor Market Growth

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

TRANSFORMERS (MVA)

Europe 257 273 351 371 409 352 441 490 491 475 482 495 514 536

Asia 575 562 686 789 854 848 971 1,060 1,091 1,148 1,219 1,291 1,381 1,474

Americas 319 424 371 399 426 381 306 322 328 335 360 383 408 413

World 1,151 1,259 1,409 1,559 1,689 1,581 1,718 1,872 1,910 1,959 2,062 2,169 2,303 2,422

Growth 0.0% 9.4% 11.9% 10.7% 8.3% -6.4% 8.7% 9.0% 2.0% 2.5% 5.3% 5.2% 6.2% 5.2%

MOTORS (GW)

Europe 162 166 194 202 208 165 184 200 193 193 198 205 212 215

Asia 639 722 802 944 1,058 1,031 1,154 1,248 1,322 1,386 1,496 1,611 1,723 1,836

Americas 161 167 174 167 183 151 127 153 159 164 175 186 196 196

World 962 1,055 1,170 1,313 1,449 1,347 1,466 1,601 1,674 1,743 1,869 2,002 2,131 2,247

Growth 0.0% 9.6% 10.8% 12.2% 10.3% -7.0% 8.9% 9.2% 4.6% 4.1% 7.2% 7.1% 6.4% 5.5%

M E T A L SResearch and Consulting

The price issue

The relative price of copper has increased greatly since 2009. Saving on the amount of copper or usingaluminium for a given equipment efficiency by using better electrical steel can make economic sense.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

HR Coil SteelNOES 1NOES 2NOES 3GOES 1GOES 2GOES 3GOES 4SA1 (Amorphous)COPPER

$/tonne

Note: Prices based on the following EN grades: GOES 1 -M 165 35 S , GOES 2 - M 140 23 S, GOES 3 - M 120 23 S, GOES 4 - M 100 20 S, NOES 1 -M 400 50 A , NOES 2 - M 330 50 A , NOES 3 -M250 35 A .

M E T A L SResearch and Consulting

GOES and NOES under the microscope

ISOTROPIC MAGNETIC PROPERTIES ANISOTROPIC MAGNETIC PROPERTIES

Source: TKES

M E T A L SResearch and Consulting

Electrical Steel & Copper (2)

M E T A L SResearch and Consulting

World electrical steel demand - charts

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Europe & Africa China

Other Asia & Oceania North America

Latin America

kt

0

500

1,000

1,500

2,000

2,500

3,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Europe & Africa China

Other Asia & Oceania North America

Latin America

kt

0

2,000

4,000

6,000

8,000

10,000

12,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Europe & Africa China

Other Asia & Oceania North America

Latin America

kt

All Electrical Steel GOES

NOES

M E T A L SResearch and Consulting

Alternative types of transformer core

C or U cores, with windings put on one or

both legs

Toroidal cores, with the coil wound

through the hole in the torus and

around the outside.

Stacked/laminated cores made out by thin sheets of metal sealed together.

The lamination reduces the eddy current losses. “EI” cores are the most common

laminated cores.

M E T A L SResearch and Consulting

73

GOES grade development over time

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Amorphous Mat. High Permeability Moderate Grade Low Grade / NOES

Share

High Permeability rated at Max 100 Watt/kg loss for 0.20 mm material at 1.7 Tesla and 50 Hz.Low Grade rated at Min 130 Watt/kg loss for 0.30 mm material at 1.7 Tesla and 50 Hz. It includes NOES used in transformers.Moderate grade is in between these ratings..

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Amorphous Mat. 14 19 29 38 51 56 75 86 91 98 106

High Permeability 221 250 306 375 445 418 521 610 678 749 860

Moderate Grade 475 572 657 771 911 843 988 1,152 1,263 1,368 1,445

Low Grade / NOES 1,179 1,192 1,230 1,293 1,371 1,126 1,104 1,063 953 828 804

World 1,889 2,033 2,222 2,477 2,778 2,442 2,688 2,911 2,985 3,043 3,215

Growth 7.6% 9.3% 11.5% 12.1% -12.1% 10.1% 8.3% 2.6% 1.9% 5.7%

Amorphous Mat. 0.8% 0.9% 1.3% 1.5% 1.8% 2.3% 2.8% 2.9% 3.0% 3.2% 3.3%

High Permeability 11.7% 12.3% 13.8% 15.1% 16.0% 17.1% 19.4% 21.0% 22.7% 24.6% 26.8%

Moderate Grade 25.1% 28.1% 29.6% 31.1% 32.8% 34.5% 36.8% 39.6% 42.3% 45.0% 44.9%

Low Grade / NOES 62.4% 58.6% 55.4% 52.2% 49.4% 46.1% 41.1% 36.5% 31.9% 27.2% 25.0%

M E T A L SResearch and Consulting

Motor driven system loss gets more focus

Legislators are now looking more at motor driven systems as a whole. Motor function always forms part of a larger process, often complex in industrial applications.

Motor loss in itself may form a small

part of overall energy loss in motor

driven system. The share of loss is falling

with stiffer motor standards.

M E T A L SResearch and Consulting

Global Market Profile

Region Shares E. Steel

Transformer & Motor MarketsCopper in Relevant MarketsGOES & NOES Use

Ratios Between Copper and Electrical Steel Use

-50

150

350

550

750

950

1,150

1,350

1,550

1,750

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Transformer Market (MVA)

Motors Market (GW)

Transformer MVA Motor GW

-1,000

1,000

3,000

5,000

7,000

9,000

11,000

13,000

15,000

Grain Oriented

Non Grain Oriented

Electrical Steel kt

0

500

1,000

1,500

2,000

2,500

3,000

Transformers Motors & Generators

kt Cu

0

1

2

3

4

5

6

7

8

9

10

NOES (t) / Cu in Motors etc. (t) GOES (t) / Cu in Transformers(t)

Electrical Steel / Copper Tonnage

Europe & Africa17%

China58%

Other Asia &

Oceania18%

North America

3%

Latin America

4%

Total = 13.13 MT

M E T A L SResearch and Consulting

Electrical Steel & Copper (3)

M E T A L SResearch and Consulting

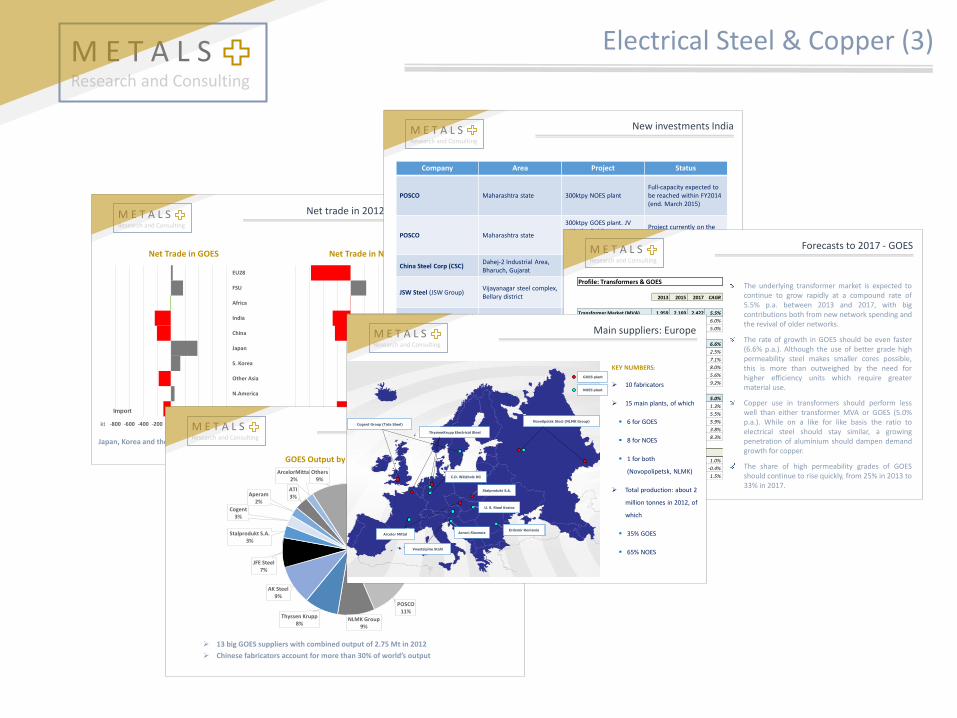

Net trade in 2012 - Geography

-800 -600 -400 -200 0 200 400 600 800

L.America

N.America

Other Asia

S. Korea

Japan

China

India

Africa

FSU

EU28

Net Trade in GOES

Import Export

-800 -600 -400 -200 0 200 400 600 800

L.America

N.America

Other Asia

S. Korea

Japan

China

India

Africa

FSU

EU28

Net Trade in NOES

ExportImport

kt kt

Japan, Korea and the FSU the big exporters, while China, India and Latin America are the main importers of all material. EU28 is a big importer of NOES

M E T A L SResearch and Consulting

GOES main suppliers

GOES Output by Supplier (2012)

WISCO16%

Baosteel Group Corporation

5%

NSSC11%

POSCO11%

NLMK Group9%

Thyssen Krupp8%

AK Steel9%

JFE Steel7%

Stalprodukt S.A.3%

Cogent 3%

Aperam2%

ATI3%

ArcelorMittal 2%

Others9%

13 big GOES suppliers with combined output of 2.75 Mt in 2012

Chinese fabricators account for more than 30% of world’s output

M E T A L SResearch and Consulting

New investments India

Company Area Project Status

POSCO Maharashtra state 300ktpy NOES plantFull-capacity expected to be reached within FY2014 (end. March 2015)

POSCO Maharashtra state

300ktpy GOES plant. JV with the Public sector Steel Authority of India (SAIL)

Project currently on the rocks over the ownership share

China Steel Corp (CSC)Dahej-2 Industrial Area, Bharuch, Gujarat

200ktpy NOES plant Operations starting in June 2014

JSW Steel (JSW Group)Vijayanagar steel complex, Bellary district

200ktpy NOES plant in collaboration with JFE Steel

To be completed within FY 2015

Rashtriya Ispat Nigam Ltd (Indian state-owned company)

Andhra Pradesh State200/400ktpy GOES plant in technological cooperation with NLMK

Under evaluation

Bhushan Steel Ltd. (BSL) Odisha 350ktoy NOES plant Under evaluation

M E T A L SResearch and Consulting

Forecasts to 2017 - GOES

The underlying transformer market is expected tocontinue to grow rapidly at a compound rate of5.5% p.a. between 2013 and 2017, with bigcontributions both from new network spending andthe revival of older networks.

The rate of growth in GOES should be even faster(6.6% p.a.). Although the use of better grade highpermeability steel makes smaller cores possible,this is more than outweighed by the need forhigher efficiency units which require greatermaterial use.

Copper use in transformers should perform lesswell than either transformer MVA or GOES (5.0%p.a.). While on a like for like basis the ratio toelectrical steel should stay similar, a growingpenetration of aluminium should dampen demandgrowth for copper.

The share of high permeability grades of GOESshould continue to rise quickly, from 25% in 2013 to33% in 2017.

Profile: Transformers & GOES

2013 2015 2017 CAGR

Transformer Market (MVA) 1,959 2,169 2,422 5.5%

Distribution 862 966 1,088 6.0%

Transmission & Other 1,097 1,203 1,334 5.0%

GOES Use (kt) 2,791 3,148 3,599 6.6%

Europe 517 536 571 2.5%

China 1,126 1,281 1,482 7.1%

Other Asia 758 873 1,029 8.0%

North America 217 252 270 5.6%

Latin America 173 206 246 9.2%

Copper Use (kt) 1,000 1,092 1,217 5.0%

Europe 156 156 164 1.3%

China 487 542 603 5.5%

Other Asia 261 285 328 5.9%

North America 53 59 62 3.8%

Latin America 44 50 60 8.3%

Key Ratios

GOES (t)/ MVA 1.43 1.45 1.49 1.0%

Transformer Cu (t) / MVA 0.51 0.50 0.50 -0.4%

GOES (t) / Cu in Transformers(t) 2.79 2.88 2.96 1.5%

M E T A L SResearch and Consulting

Main suppliers: Europe

KEY NUMBERS:

10 fabricators

15 main plants, of which

6 for GOES

8 for NOES

1 for both

(Novopolipetsk, NLMK)

Total production: about 2

million tonnes in 2012, of

which

35% GOES

65% NOES

Acroni SloveniaErdemir Romania

U. S. Steel Kosice

Cogent Group (Tata Steel)

Erdemir RomaniaArcelor Mittal

C.D. Wälzholz KG

Stalprodukt S.A.

Voestalpine Stahl

ThyssenKrupp Electrical Steel

Novolipetsk Steel (NLMK Group)

GOES plant

NOES plant

M E T A L SResearch and Consulting

Building Wire

M E T A L SResearch and Consulting

Building Wire (1)

M E T A L SResearch and Consulting

Building Wire Market Trend

Building Wire Market Development 1999-2014

Building Wire Market Development (kt Cu Equivalent)

99-14

Copper Wire 2,370 2,377 2,395 2,400 2,569 2,780 2,856 2,930 3,069 3,113 3,044 3,111 3,211 3,389 3,476 3,625 2.9%

Aluminium Wire 71 74 79 88 102 122 157 192 195 195 182 194 204 228 244 260 9.0%

Total Cu Equivalent 2,441 2,451 2,474 2,488 2,671 2,902 3,013 3,122 3,264 3,308 3,227 3,305 3,415 3,616 3,719 3,885 3.1%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Note: All aluminium figures in this report are quoted as copper equivalents, calculated at 2.077 to 1

M E T A L SResearch and Consulting

Regional Trends in Building Wire

2014 Regional Shares ….. Trend 1999-2014

European Union 490 489 476 468 -0.3%

Other Europe & FSU 53 74 81 93 3.8%

Africa 65 75 90 112 3.7%

India 54 72 109 144 6.7%

Middle East / Other S. Asia 130 151 169 228 3.8%

China 268 457 892 1,310 11.2%

Japan 160 160 160 148 -0.5%

ASEAN 95 120 131 204 5.2%

Other Asia & Oceania 173 202 183 206 1.2%

North America 740 881 685 682 -0.5%

Latin America 214 222 251 291 2.1%

Total Cu Equivalent 2,441 2,902 3,227 3,885 3.1%

CAGR

99-1420141999 2004 2009

M E T A L SResearch and Consulting

The Four Market Segments

856 kt

24.0%

Other Asia & Oceania North America Latin America

China

Europe & AfricaGlobal Market Apportionment

304 kt

35.3%

216 kt

25.2%

145 kt

16.9%

194 kt

22.6%

1,051 kt

29.5%

653 kt

18.3%

53 kt

20.4%

51 kt

19.5%

117 kt

18.1%

166 kt

25.6%

147 kt

22.7%

217 kt

33.6%

413 kt

34.9%

437 kt

37.0%

127 kt

10.8%

205 kt

17.3%

79 kt

30.4%

77 kt

29.8%

139 kt

22.4%

109 kt

17.6%

182 kt

29.3%

190 kt

30.7%

1,005 kt

28.2%

Global Market Apportionment

Cu Equiv. Tonnage and Percent Share(excluding losses)

Residential

Newbuild

Non-residential

Newbuild

Residential

Refurbishment

Non-residential

Refurbishment

M E T A L SResearch and Consulting

Copper Market Interfaces

3.6 Mt Cu of building wire is part of a 6.3 Mt market

Building Wire

Other Low Voltage Wire

Power Cable

Bare Wire

Data Cable

Copper Rod, Bar & Section

Other Mill Products

Building Wire and All Electrical / Data Copper Installation in Buildings in 2014

European Union 20 364 6 35 36 31 493 479 49%

Other Europe & Africa 5 148 2 10 12 7 184 181 50%

China 39 674 15 43 70 42 883 1,245 58%

Other Asia & Oceania 26 589 6 61 59 29 770 906 54%

North America 6 110 6 50 27 9 208 540 72%

Latin America 3 111 2 6 3 0 125 274 69%

Segment Total 100 1,996 36 206 207 118 2,663 3,625 58%

L. V.

Wire

Power

Cable

Bare

Wire

Data

Cable

Cu

RBS

Other

Mill

All Non

Build Wire

Building

Wire

%

Share

M E T A L SResearch and Consulting

Service Entrance Cable

The service entrance often sees aluminium conductor cable

Copper XLPE Insulation

Service Entrance Wire Types

SEU

SER

USE-2

The service entrance is a special location within residential buildings as the cables are larger and there may be additional requirements in terms of moisture, abrasion and cut through resistance

The economics of larger cable sizes and allowance in the codes means that the service entrance is the prime source of aluminium conductor use in the residential sector

SEU usually has two type XHHW insulated conductors with an overall PVC jacket. The cable is rated for 90 C in dry, 75 C in wet locations. It is used above-ground from the service drop to the meter base, and from the meter base to the distribution panel board

SER is of similar in construction and use to SEU but is round, and has more than two conductors

For underground service entrances, alternative conductor types are used. USE-2 is quite common

SEU and SER may be used in branch circuits for major appliances, while USE-2 has wide application in demanding non-residential environments

M E T A L SResearch and Consulting

IEC and NEC Based Wiring Standards

NEC

IEC

IEC & NEC

IEC - International Electricity Standards is the dominant code for low voltage installations. The safety principles of IEC 60364 series, IEC 61140, 60479 series and IEC 61201 are the fundamentals of most electrical standards in the world

NEC – National Electrical Code also contains installation rules for electrical products, primarily for North American markets

The dual adaptation of IEC and NEC standards is not widespread

Source: Legrand, International electrical standards & regulations

M E T A L SResearch and Consulting

Building Wire (2)

M E T A L SResearch and Consulting

Copper vs Aluminium Conductors (3)

Aluminium’s role in practice

Aluminium’s main foothold is in North America, where it has nearly 20% share on a copper equivalent basis

Elsewhere, the share is low. While growth may have been substantial in percentage, in volume it remains quite small

Installation in the US is exclusively 8000 series product, whereas elsewhere 1000 series alloys are still used in some locations

Up to eight major suppliers are thought to be selling 8000 series cables in China, and standards are being developed. Most product sold is power cable rather than building wire

In the United States, the main penetration of aluminium is in non-residential markets, although it is installed in the residential market in the service entrance and in the core of high rise multi-family dwellings

Cable economics determine that aluminium is most used in larger sized single core cables, where the additional cost of insulation (and jacketing) is proportionately less

In the US, as elsewhere, it is generally believed that there is little advantage installing aluminium building wires of less than 10 mm2 (8 AWG)

In practice, there is little used less than 16 mm2 (6 AWG), most cables being considerably larger. This effectively bars aluminium use in residential branch circuit wiring

99-14

Europe & Africa 11 9 11 12 0.7%

China 9 14 40 65 14.5%

Other Asia & Oceania 6 8 16 24 9.3%

North America 41 81 104 142 8.6%

Latin America 4 9 12 17 10.1%

Total 71 122 182 260 9.0%

% Aluminium 2.9% 4.2% 5.6% 6.7% 5.7%

2014200920041999CAGR

Aluminium Building Wire Trend

M E T A L SResearch and Consulting

The Building Wire Market and Wealth

A clear relationship, but China use looks high

Bubble sizes indicate the size od the building wire market. GDP shown on a 2010 Purchasing Power Parity (PPP) adjusted basis

Building Wire Use and GDP per Head by Region in 2014

M E T A L SResearch and Consulting

The Stock, Newbuild & Economic Stage

Newbuild focus emerging markets, existing stock mature

The Existing Stock and GDP per Head in 2014 ….. Newbuild

Bubble sizes indicate floorspace in place and installed. GDP shown on a 2010 Purchasing Power Parity (PPP) adjusted basis

M E T A L SResearch and Consulting

Floorspace in Place & Refurb. Wire

Wire in refurbishment is growing quickly in non-residential

Buildings in Place and Refurbishment Wire ….. Region Profiles 1999

….. Region Profiles 2014

Floorspace = x10 billion sq. m, Building Wire = Mt Cu equivalent

M E T A L SResearch and Consulting

Wire Use in New & Existing Buildings

Refurbishment share for wire more than for all construction

Building Wire Shares by End Use in 2014 ….. Trend 1999-2014

The Building Wire Market (kt Cu equiv.)

99-14

Residential Newbuild 694 692 706 727 776 865 898 934 927 893 845 883 922 984 1,009 1,053 2.8%

Residential Refurbishment 479 474 470 467 511 574 594 585 594 592 601 599 602 612 634 655 2.1%

Non-residential Newbuild 557 562 555 531 590 639 663 719 806 866 836 851 877 940 961 1,006 4.0%

Non-residential Refurbishment 535 542 561 578 598 607 632 642 683 699 694 714 745 788 814 859 3.2%

Building Wire Losses 176 181 182 186 197 216 226 242 254 257 251 258 270 293 301 312 3.9%

All Building Wire 2,441 2,451 2,474 2,488 2,671 2,902 3,013 3,122 3,264 3,308 3,227 3,305 3,415 3,616 3,719 3,885 3.1%

Copper 2,370 2,377 2,395 2,400 2,569 2,780 2,856 2,930 3,069 3,113 3,044 3,111 3,211 3,389 3,476 3,625 2.9%

Aluminium 71 74 79 88 102 122 157 192 195 195 182 194 204 228 244 260 9.0%

CAGR1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

M E T A L SResearch and Consulting

A simplified cable sizing procedure is as follows:

1. Take the total load in the circuit(s) concerned in Watts

2. Add 20% for future proofing

3. Multiply by Voltage to give Amps

4. LOOKUP next highest cable size for this Amp rating

5. LOOKUP ambient temperature factor and apply

6. LOOKUP method of installation factors and apply

7. STILL OK, go to 8); NOT OK, choose next cable size up

8. LOOKUP Voltage Drop factor and apply

9. STILL OK, correct sizing, NOT OK, choose next size up

Tables give de-rating factors for each cable type and each parameter

Voltage drop calculations are based on circuit length, the longer the circuit the higher than voltage drop

Voltage drop per unit length is as much as 8 times higher for a 120v system as for a 230v system

The IEC recommends a voltage drop maximum of 3% for lighting systems and 5% for other circuits in most cases

Where the consumer supply through its own MV/LV transformer, 6% and 8% voltage drop is permissible

In the US, the NEC only recommends 5% max drop in normal consumer supply. 8-10% drop is considered dangerous

The Calculation of Cable Sizing

WHY THIS MATTERS

Choice of cable type affects conductor size

Choice of installation method can make (big) differences to allowable

conductor size

As voltage drop relates to circuit length, the length of circuit also

affects conductor size

If the number of circuits is increased to reduce voltage drop, the length of cable rather than conductor size

is increased

Meaning Higher Cu Use If…..

Low cable type ratings

Low installation method ratings

Length or number of circuits increased

…. and implications for copper

M E T A L SResearch and Consulting

Building Wire (3)

M E T A L SResearch and Consulting

Conclusions

Building wire is essentially a low value commodity product, where metal cost matters

Copper use in building wire in 2014 was 3.62 Mt, part of a 6.29 Mt market for copper in fixed wiring systems in which power cable and busbar (using Cu RBS) also feature

Between 1999 and 2014 the building wire market grew at 3.1% p.a., less than GDP but more than the addition to floorspace through construction, indicating a marginal rise in use intensity

Copper use growth, at 2.9% p.a. was less, reflecting a 9.0% p.a. growth in aluminium use

Aluminium’s share is still modest (6.7%), and is focussed on non-residential and North America

By use, the market is split between residential (47.8%) and non-residential (52.2%)

It is also split between new build (57.7%) and refurbishment (42.3%), the latter being biased towards non-residential and towards mature markets

China growth has driven the building wire market, with strong new building and a growing wire density. Its share in 2014 was 34%

Intensity of use is very high in North America. This reflects 120v consumer supply of electricity, high floorspace rates, high electricity consumption and also the classification of an unusually high proportion of fixed wiring as building wire rather than power cable

IEC and NEC guidelines set the basis for most electrical regulation and installation practice

Wiring is most often carried out at or near the minimum standard required

Interest in enhanced safety, the potential for energy saving and comfort offer room for improvement in wiring practice. This should benefit both cable sizes and cable length

M E T A L SResearch and Consulting

Recommendations (2)

Ensure Compliance with Electrical Installation Codes (continued)

Support a tougher stance on the inspection of electrical work in refurbishment

Support more regular and thorough inspection of existing electrical installations

Address Sub-Optimal and Illegal Installation Practice

Address substandard installation in new buildings where illegal through enforcement

Address substandard installation in new buildings where not illegal by education / publicity

Address substandard installation in refurbishment as above, through appropriate channels

Address the manufacture, import and sale of products specified below their labelling

Promote Higher Amp Rating of Electrical Supply

Ensure that new buildings have an electrical supply suitably future proofed without cost penalty

Ensure that supply to existing buildings can be upgraded without a cost penalty

Apply ‘Green’ Arguments Where There is an Advantage for Copper

Larger cable sizes are more energy efficient and safer – thus ’green’

If advantageous, support moves to limit or ban harmful materials in insulating / jacketing

Assess cable de-rating values and consider a) changes to PVC composition, b) limits to PVC use altogether, c) wider application of LSZF, d) requiring both LSZF and better flame retardants

Active involvement in regulatory / standard initiatives on overall energy performance of buildings

Deal With Manufacturer / Consumer Concerns Over Metal Market Dynamics

Deep concerns exist over copper price volatility: Can pricing mechanisms ameliorate this?

Make more of harmful differentials in aluminium price (with premia / rod charge) and also differences in metal quality and specification (8000 series alloys?)

…. continued

M E T A L SResearch and Consulting

Building Stock and Wire Balances

Each year stock is added, raising future refurbishment

Global Building Stock and Wire Balances in 2014

Residential StockHousing Units

(million)

Floor Space

(bn. sq. m.)Non-residential Stock

Floor Space

(bn. sq. m.)

Stock in 2013 2,022.5 146.1 Stock in 2013 70.5

New Building 39.9 3.6 New Building 1.9

Addition in Refurbishment 0.0 0.3 Addition in Refurbishment 0.2

Demolition & Abandonment -10.2 -0.9 Demolition & Abandonment -0.4

Stock in 2014 2,052.2 149.1 Stock in 2014 72.1

Residential Wirekt Cu

equivalent

kt Cu equiv.

per 100 sq.m.Non-residential Wire

kt Cu

equivalent

kt Cu equiv.

per 100 sq.m.

Newbuilds 1,053 29.3 Newbuilds 1,006 52.9

Refurb. Space Addition 82 29.3 Refurb. Space Addition 108 52.9

Other Refurbishment 573 Other Refurbishment 751

Total Wire Added 1,709 Total Wire Added 1,865

Wire Removed in Refurbishment -390 Wire Removed in Refurbishment -470

Demolition & Abandonment -220 24.8 Demolition & Abandonment -171 40.1

Net Wire Added 1,099 Net Wire Added 1,223

Floorspace addition in the building stock comes from extension in refurbishment as well as newbuilds

Losses to the building stock result from demolition and abandonment. This is typically less than 1% of the building stock, but more where there is active urban renewal

Active wiring stock additions reflect floorspace addition and loss, with wire intensity per unit space typically higher in the new installation than that preceding it

M E T A L SResearch and Consulting

China (1)

Region charts

Wire Installed & GDP Per Head Building Construction in 2014 Floorspace Development

Construction Value & Wire Market Wire End Market Trends Wire End Markets in 2014

M E T A L SResearch and Consulting

Winding Wire

M E T A L SResearch and Consulting

Winding Wire (1)

M E T A L SResearch and Consulting

Types of winding wire

CLASS

Temperature Rating 155 / 180 155 / 180 155 / 180 180 180 180 180

Base Coat Polyurethane Polyurethane Polyurethane Polyester Polyester Polyesterimide Polyesterimide

Overcoat Polyurethane Polyamide Polyamide Polyamide

Bonding Coat

CLASS GENERAL

Temperature Rating 105 / 120 130 155 180 180 180 210 / 220

Base Coat Polyvinyl Acetal Polyurethane Polyurethane Polyamideimide Mod. Polyesterimide Polyester Mod. Polyesterimide

Overcoat Polyamideimide Polyamideimide

Bonding Coat Polyvinyl Polyamide Polyamide Polyamide Polyamide Polyamide

CLASS HIGH TEMP

Temperature Rating 220 / 240 180 / 220 180 / 220 180 / 220 180 / 220 n/a n/a

Base Coat Polyamide Modified Polyester Modified Polyester Mod. Polyesterimide Mod. Polyesterimide

Overcoat Polyamide Polyamide

Bonding Coat Epoxy

HIGH TEMPERATURE / FLAT WIRE COVERED FLAT WIRE

Special PapersMica / Glass Tape or

Yarn

SOLDERABLE

BONDABLE

Groups of winding wire products

Insulating material helps to determine temperature rating and solderability

Other key characteristics include abrasion and stress resistance, resistance to solvents and transformer oil

Characteristics and performance can be enhanced by the application of an overcoat

An additional coat is applied if the coating is to bond, either at low temperature or with chemicals

Special covered constructions apply to large flat wires used mainly in transformers

These special constructions can include the use of paper (kraft, crepe, aramide) or glass (mica, fibreglass)

M E T A L SResearch and Consulting

Cu winding wire – basic segmentation

344

9044

301

1,380

133

117

299

173126

EU Oth. Europe / FSU Africa

India China Japan

S. Korea Other Asia Pacific North America

Latin America

880

1,525

121

481

Transformers Motors

Generators Other Applications

Allocation by end market group - 2013 Geographical splits - 2013

COPPER WINDING WIRE USE BY APPLICATION (KT)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 04-13

Transformers 555 573 619 689 777 742 813 869 858 880 915 5.3%

Motors 992 1,069 1,123 1,196 1,225 1,160 1,275 1,375 1,452 1,525 1,647 4.9%

Generators 111 128 141 136 127 137 144 147 129 121 121 1.0%

Other Applications 597 637 643 614 529 453 521 506 483 481 496 -2.4%

Total 2,255 2,407 2,524 2,635 2,658 2,493 2,753 2,897 2,922 3,007 3,180 3.3%

M E T A L SResearch and Consulting

An overview of winding wire types

WINDING WIRE MAY BE DEFINED BY:

Conductor material• Copper

• Aluminium

Shape• Round

• Flat (or shaped)

Temperature rating (degrees centigrade)• Ranges from 105 degrees to 240 degrees plus

• Most product is 155 or 180 degree rating

Diameter (or dimensions for flat wire)• Fine wire range 0.01 to 0.2 mm

• Mainstream market 0.2 – 2.0 mm

• Large sizes 2.0 to 6.0 mm

Insulating material (see next slide)

Special characteristics

• Solderability

• Self bonding capability

• Resistance to mechanical or chemical stress

M E T A L SResearch and Consulting

Cu winding wire, substitutes & co-products

Auminium

Other

Permanent

Magnets

ELECTRICAL STEELELECTRICAL STEEL IMPACTS ON THE

ROTOR AND STATOR MARKETS

Copper

Strip

Copper

Winding

Copper

Other

Aluminium

Winding

Aluminium

Strip

Transformers

Transformers

Other Applications

Motors & Generators

Motors & Generators

M E T A L SResearch and Consulting

Brief overview of transformer market

The power and distribution transformer market is a huge consumer of winding material, copper having the largest share

Power transformers are used in the utility transmission network, distribution transformers in the utility distribution network and by industry

In total, we estimate that in 2013 the transformer market took 880 kt of copper winding wire, and an additional 176 kt of copper strip

Aluminium is a significant contender in this market

In 2013, we estimate that aluminium use in transformers amounted to 447 kt on a copper equivalent basis

In transformers, it is appropriate to consider winding wire alongside strip

Not only is strip a large part of the copper winding market, it is an even segment of the aluminium business

Energy losses in the transmission and distribution network have been of prime concern for many years, with onerous standards due to come up to 2020

This is generally good for copper, but also spurs alternative technology development

M E T A L SResearch and Consulting

Winding Wire (2)

M E T A L SResearch and Consulting

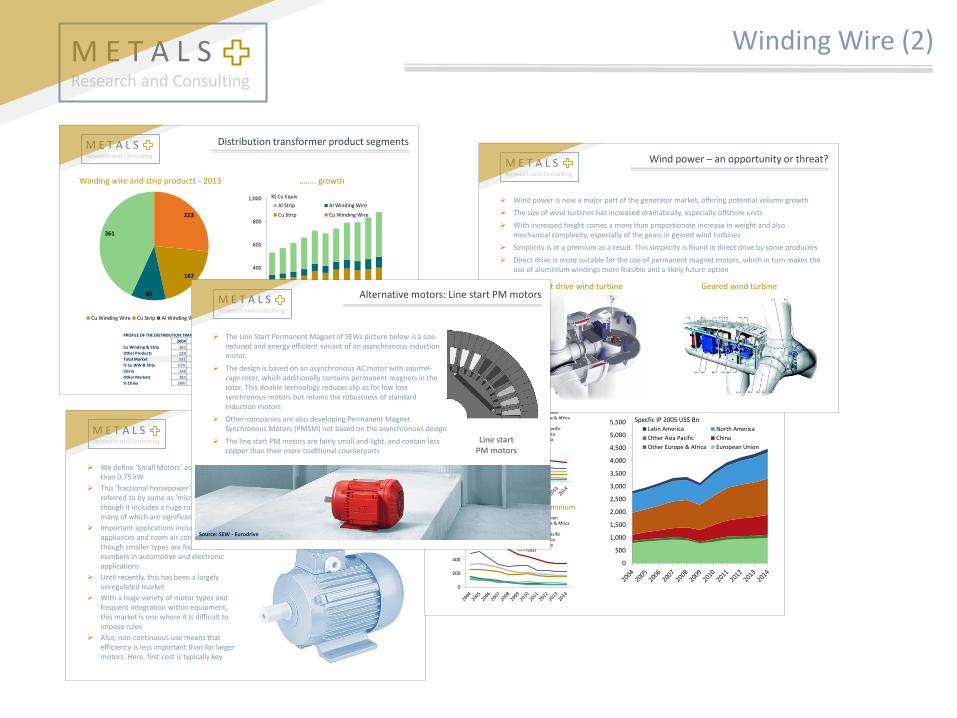

Distribution transformer product segments

223

167

87

361

Cu Winding Wire Cu Strip Al Winding Wire Al Strip0

200

400

600

800

1,000Al Strip Al Winding Wire

Cu Strip Cu Winding Wire

Kt Cu Equiv

PROFILE OF THE DISTRIBUTION TRANSFORMER MARKET (KT CU EQUIV.)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 04-13

Cu Winding & Strip 303 311 318 331 372 357 388 397 381 393 405 2.9%

Other Products 228 261 298 330 351 343 358 398 418 447 481 7.8%

Total Market 531 572 616 661 723 700 746 795 799 840 886 5.2%

% Cu WW & Strip 57% 54% 52% 50% 51% 51% 52% 50% 48% 47% 46%

China 148 150 169 200 246 248 277 298 300 323 338 9.0%

Other Markets 383 421 446 461 478 452 468 497 500 517 548 3.4%

% China 28% 26% 27% 30% 34% 35% 37% 37% 38% 38% 38%

Winding wire and strip products - 2013 …….. growth

M E T A L SResearch and Consulting

Small motor market basics

We define ‘Small Motors’ as those of less than 0.75 kW

This ‘fractional horsepower’ category is referred to by some as ‘micro-motors’, though it includes a huge range of motors many of which are significant in size

Important applications include home appliances and room air conditioners, though smaller types are found in vast numbers in automotive and electronic applications

Until recently, this has been a largely unregulated market

With a huge variety of motor types and frequent integration within equipment, this market is one where it is difficult to impose rules

Also, non-continuous use means that efficiency is less important than for larger motors. Here, first cost is typically key

Permanent magnets have gained a large slice of the rotor section of this market, as rotor material

Penetration of PMs would be greater but for uncertainty over price and availability of rare earth materials used in them

Aluminium has gained against copper in stators

M E T A L SResearch and Consulting

Cu share & intensity of use in small markets

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500Latin America North America

Other Asia Pacific China

Other Europe & Africa European Union

Specfic IP 2005 US$ Bn

0

200

400

600

800

1,000 European UnionOther Europe & AfricaChinaOther Asia PacificNorth AmericaLatin AmericaTotal

T Cu per $ bn IP

0

200

400

600

800

1,000 European UnionOther Europe & AfricaChinaOther Asia PacificNorth AmericaLatin AmericaTotal

T Cu Equiv. per $ bn IP

Market driver: Electrical & machinery IPIntensity of use: Copper

Intensity of use: Copper & Aluminium

M E T A L SResearch and Consulting

Wind power – an opportunity or threat?

Wind power is now a major part of the generator market, offering potential volume growth

The size of wind turbines has increased dramatically, especially offshore units

With increased height comes a more than proportionate increase in weight and also mechanical complexity, especially of the gears in geared wind turbines

Simplicity is at a premium as a result. This simplicity is found in direct drive by some producers

Direct drive is more suitable for the use of permanent magnet motors, which in turn makes the use of aluminium windings more feasible and a likely future option

Direct drive wind turbine Geared wind turbine

M E T A L SResearch and Consulting

Alternative motors: Line start PM motors

57

The Line Start Permanent Magnet of SEWs picture below is a size-reduced and energy efficient variant of an asynchronous induction motor.

The design is based on an asynchronous AC motor with squirrel-cage rotor, which additionally contains permanent magnets in the rotor. This double technology reduces slip as for low loss synchronous motors but retains the robustness of standard induction motors

Other companies are also developing Permanent Magnet Synchronous Motors (PMSM) not based on the asynchronous design

The line start PM motors are fairly small and light, and contain less copper than their more traditional counterparts

Line startPM motors

Source: SEW - Eurodrive

M E T A L SResearch and Consulting

Winding Wire (3)

M E T A L SResearch and Consulting

Permanent magnets in motors

34%

6%

6%4%

3%

14%

7%

11%

3%

12%

Motors & Generators Drives, Clutches & BrakingTransducers Relays, Sensore & SwitchesWaveguides HDD, CD & DVDEnergy Prodn. & Storage TransportationAppliances Other

0

50

100

150

200

250

300

350

Latin America North America

Other Asia China

Europe & Africa

Kt Magnet Weight

PERMANENT MAGNETS IN MOTORS BY LOCATION (KT)

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

China 96 127 150 172 135 121 135 140 149 159 170 182 199 210