UNITED STATES OF AMERICA DEPARTMENT OF TRANSPORTATION OFFICE OF THE SECRETARY STAR MARIANAS AIR, INC., Complainant, v. COMMONWEALTH PORTS AUTHORITY, Respondent. Docket DOT-OST-2021-0138 RESPONDENT'S APPENDIX OF EVIDENCE Please serve: Scott P. Lewis Timothy J. Roskelley Mina S. Makarious Paul M. Kominers Ezra Dunkle-Polier ANDERSON & KREIGER LLP 50 Milk Street, 21 st Floor Boston, Massachusetts 02109 T: 617.621.6500 F: 617.621.6639 [email protected][email protected][email protected][email protected][email protected]Counsel for Commonwealth Ports Authority The Robert T. Torres TORRES LAW GROUP Plata Drive Whispering Palms (Chalan Kiya) P.O. Box 50375 CK Saipan, MP 96950 T: 670.234.7859 F: 670.234.5749 [email protected]November 5, 2021 SMA App. 001

Exh. CPA-4 — Email attaching 2016 Rate Study SMA App. 045

Exh. CPA-5 — Form of Operating Agreement SMA App. 047

Exh. CPA-6 — 9.2.17 BOD Minutes SMA App. 189

Exh. CPA-7 — Director’s Determination SMA App. 194

Exh. CPA-8 — 2015 Rate Study SMA App. 223

Exh. CPA-9 — Associate Administrator’s Final Agency

Decision

SMA App. 252

Exh. CPA-10 — Board Resolution No. 2021-05 SMA App. 268

Exh. CPA-11 — 6.28.21 NPRM SMA App. 271

Exh. CPA-12 — Termination Notice SMA App. 369

Exh. CPA-13 — AUA SMA App. 395

Exh. CPA-14 — Notice of Final Regulations SMA App. 460

Exh. CPA-15 — Letter to FAA re OPA SMA App. 467

Exh. CPA-16 — SMA AR Summary SMA App. 470

Declaration of Bonnie Ossege

SMA App. 474

Exh. CPA-17 — 2022 Rate Study SMA App. 486

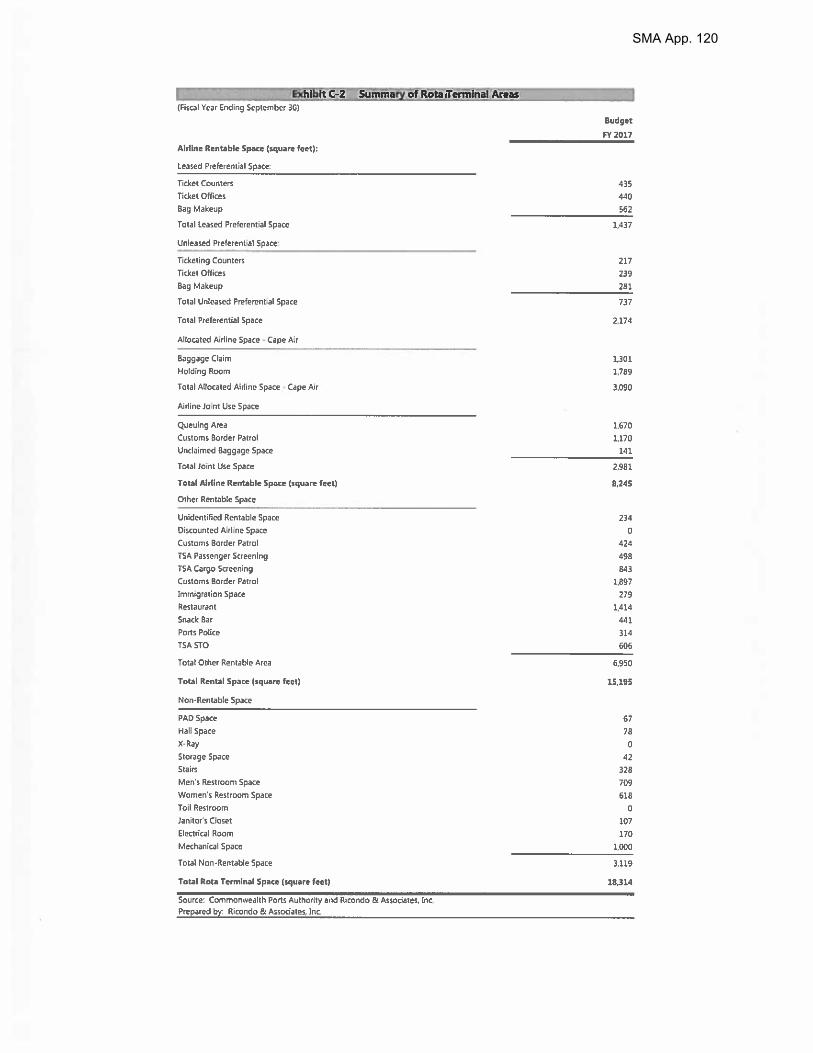

Exh. CPA-18 — Rota Space Drawing SMA App. 514

SMA App. 002

1

UNITED STATES OF AMERICA

DEPARTMENT OF TRANSPORTATION

OFFICE OF THE SECRETARY

STAR MARIANAS AIR, INC.,

Complainant,

v.

COMMONWEALTH PORTS AUTHORITY,

Respondent.

Docket DOT-OST-2021-0138

DECLARATION OF SKYE HOFSCHNEIDER

I, Skye Hofschneider, declare as follows under the pains and penalties of perjury:

1. I have read the Complaint by Star Marianas Airlines, Inc. (“SMA”) in this

proceeding and offer this testimony in support of the Commonwealth Ports Authority (the

“Authority” or “CPA”). This testimony is based upon my personal knowledge.

2. I am the Comptroller at CPA. I have worked in this capacity for CPA for the past

eight years. In this role, I am responsible for the management and supervision of all phases of

CPA’s accounting. With respect to setting rates for the three airports in CPA’s airport system –

Saipan International Airport, Rota International Airport and Tinian International Airport

(collectively, the “Airports”) – my duties include managing our relationship with our outside

financial consultants, Ricondo & Associates (“Ricondo”), providing the information Ricondo

needs to calculate our airport rates and charges and reviewing their rate calculations. Before

being named Comptroller, I was the Accountant III for CPA. In my role as Accountant III, I was

responsible for performing accounting procedures involving specific phases of the accounting

function, including recording and reconciling expenditures, monitoring budgets, issuing check

payments, and processing purchase orders. I worked in this capacity for CPA from 2012 to

SMA App. 003

2

2013. I hold a Bachelor of Science degree in Accounting and a Master in Business

Administration degree with a concentration in Accounting.

3. SMA began offering air transportation to and from the Airports in 2009.

Currently, SMA operates commuter flights at all three airports. Saipan International Airport has

two passenger terminals, the “Main Terminal,” used by international carriers, and the

“Commuter Terminal,” which SMA uses. Rota and Tinian both have single terminals that are

utilized by SMA. Aircraft rescue and fire-fighting (“ARFF”) facilities are located at each

airport. All ARFF facilities are active, functional and available to provide calls and rescues to all

aeronautical users of the Airports, including SMA.

4. In 2015, CPA began to develop a new rate methodology for charging air carriers

for the use of the Airports. The impetus for the new rate methodology was an unsuccessful effort

by SMA to establish that the terminal fees that were being charged by CPA were excessive and

constituted an illegal “head tax” under the Anti-Head Tax Act (“AHTA”) because they were

assessed on a per-passenger basis – even though they were established in accordance with an

Airline Use Agreement & Lease of Premises (the “AUA”) between each of the air carriers,

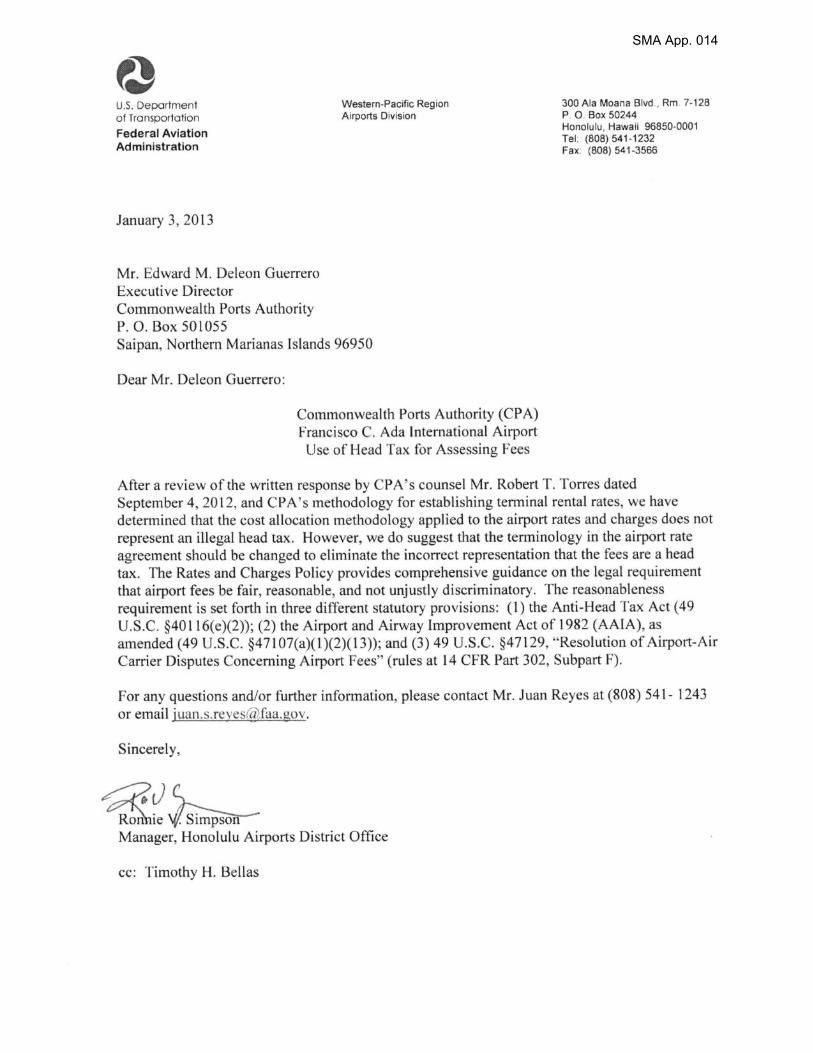

including SMA, and CPA. SMA’s allegations were reviewed by the local Airports Division

Office (“ADO”) of the Federal Aviation Administration (“FAA”). On January 3, 2013, the ADO

rejected SMA’s excessive fees claim, finding that “the facilities of the airport are made available

to the public on reasonable terms without unjust discrimination” and “[t]herefore, CPA has not

violated the requirements of Grant Assurance 22 with regard to its access fee.” A true copy of

the ADO’s January 3, 2013 letter to CPA addressing “Excessive Fees for Use of Airport Space”

is attached to this Declaration as Ex. CPA-1. On the same day, FAA wrote separately to address

the AHTA allegations, finding that “the cost allocation methodology applied to the airport rates

and charges does not represent an illegal head tax,” but recommending that CPA change its rate-

setting terminology to avoid confusion in the future. A true copy of the ADO’s January 3, 2013

letter to CPA addressing “Use of Head Tax for Assessing Fees” is attached to this Declaration as

Ex. CPA-2.

SMA App. 004

3

5. Even though FAA rejected SMA’s claims, SMA continued to dispute the fees

charged to SMA under the AUA. As a result, in 2015 CPA contracted with Ricondo, a well-

respected national aviation consulting firm that had advised CPA on airport finance since 1999.

We asked Ricondo to develop a new compensatory rate methodology that would fairly distribute

costs among the air carriers serving the Airports in accordance with applicable FAA

requirements and compute terminal charges on the basis of square footage rather than passenger

head-counts. CPA also asked Ricondo to develop a new form of airline agreement, a short-term

operating agreement (the “Operating Agreement”), to implement the new rate methodology.

6. In 2015 and 2016, Ricondo developed a new compensatory rate methodology and

a new Operating Agreement to replace the existing AUA between CPA and the air carriers

serving the Airports, including SMA.

7. During July and November 2016, CPA and Ricondo representatives met with the

air carriers serving the Airports to explain the new rate methodology and the new Operating

Agreement. We had at least two meetings with SMA: one on July 19, 2016 and a later one on

November 17, 2016.

8. Prior to the July 19 meeting, CPA provided SMA with a detailed written

explanation of the new rate methodology developed by Ricondo titled “Projected Airline Rates

and Charges Methodology for Commonwealth Ports Authority” dated July 13, 2016 (the “2016

Rate Study”). A true copy of the 2016 Rate Study is attached to this Declaration as Ex. CPA-3.

A true copy of an email dated July 15, transmitting the 2016 Rate Study to SMA, is attached to

this Declaration as Ex. CPA-4.

9. When we met with SMA on July 19, 2016, CPA and Ricondo presented the new

rate methodology and answered whatever questions SMA asked. I attended this meeting with

my colleagues Joy Deleon Guerrero, Edward Mendiola and Christopher Tenorio from CPA and

our financial consultant, Bonnie Ossege, from Ricondo. Shaun Christian and Rowena Advincula

represented SMA at this meeting.

SMA App. 005

4

10. I also attended the November 17, 2016 meeting with SMA, with Joy Deleon

Guerrero and Brian Flaherty (one of our lawyers) from CPA and Bonnie Ossege from Ricondo

(remotely). This time SMA was represented by Robert Christian, Shaun Christian and their

lawyer, Timothy Bellas. During this meeting, CPA presented the new form of “Operating

Agreement.” The new rate methodology, as well as projected rates for Fiscal Year 2017

calculated using the new rate methodology, were displayed in Exhibit E to the form of Operating

Agreement we shared with SMA at that time. A true copy of the form of Operating Agreement

we provided to SMA is attached to this Declaration as Ex. CPA-5. We again answered whatever

questions SMA asked.

11. It was apparent during our November 17 meeting that SMA had carefully

reviewed the 2016 Rate Study. SMA raised two primary objections to the new rate

methodology: (1) that the allowance for ARFF facilities should be based on fair market value

instead of actual costs; and (2) that SMA should not be charged for security screening and

circulation space that was not used by SMA’s passengers. SMA requested that, instead of

moving forward with the new rate methodology, CPA work with SMA and the Commonwealth

of the Northern Mariana Islands Legislature to develop a rate methodology that would further

reduce the costs of commuting between the islands, thereby advancing local interests.

12. SMA was the only air carrier serving the Airports that refused to accept the new

rate methodology and execute the form of Operating Agreement we had proposed. SMA stated

to me and others at CPA that they would provide a letter explaining their objections, but no such

letter was ever received by CPA.

13. Nevertheless, in response to SMA’s refusal to sign the Operating Agreement, the

Authority’s Board of Directors delayed the implementation of the Operating Agreement and new

rate methodology.

14. On August 22, 2017, Robert Christian, Board Chair at SMA, made a presentation

to the Authority’s Board of Directors. I attended the meeting and witnessed his presentation. A

true copy of an excerpt of the minutes from the August 22, 2017 Board of Directors meeting with

SMA App. 006

5

Mr. Christian’s presentation is attached to this Declaration as Ex. CPA-6. During his

presentation, SMA’s Board Chair admitted that CPA has the right to charge new fees calculated

using the compensatory rate methodology Ricondo developed and documented in the 2016 Rate

Study. Mr. Christian urged, however, that CPA should instead develop a rate methodology that

would further reduce the costs for airlines, such as SMA, that operate commuter flights to and

from Tinian Island and Rota Island. Ex. CPA-6 at 11.

15. Following that meeting, the Authority’s Board of Directors continued for four

years to delay implementation of the new rate methodology and the Operating Agreement as a

result of objections SMA raised to the Legislature over the impact of the new rate methodology

on commuter airfares. Throughout this time, SMA pursued a relentless, but unsuccessful legal

campaign to challenge the rates and fees charged by CPA for its use of our Airports. SMA has

filed rate challenges in federal court, in our local court and with the FAA. These efforts have all

failed, including SMA’s formal complaint to the FAA under 49 C.F.R. Part 16. In May 2020,

the FAA’s Director of Airport Compliance and Management Analysis (the “Director”) dismissed

every allegation in SMA’s Part 16 complaint. A true copy of the Director’s Determination is

attached to this Declaration as Ex. CPA-7. The Director’s findings included a review of

Ricondo’s rate methodology which led the Director to conclude that “nothing in these documents

appears to conflict with acceptable methodologies for establishing airport rates and charges with

airlines” and that the “Ports Authority’s compensatory methodology used to establish the

airport’s rates and charges, and fees is fair and reasonable.” Ex. CPA-7 at 13. A true copy of the

Ricondo rate study reviewed by the Director is attached to this Declaration as Ex. CPA-8. The

compensatory rate-setting methodology described by Ricondo in the rate study reviewed by the

FAA is essentially the same as the method Ricondo used to calculate the fees that are in dispute

in this proceeding. The Director’s Determination was upheld by the Associate Administrator for

Airports. A true copy of Associate Administrator’s Final Agency Decision is attached to this

Declaration as Ex. CPA-9.

SMA App. 007

6

16. Before it brought the present proceeding before the Department, SMA’s most

recent lawsuit against CPA challenging our rate-setting was filed in the Superior Court of

Commonwealth on the Northern Mariana Islands in December 2020. CPA has moved to dismiss

SMA’s complaint and a decision on that motion is pending.

17. On May 27, 2021, the Authority’s Board of Directors decided to move forward

with the new rate methodology and adopted Board Resolution No. 2021-05. This resolution

authorized the implementation of Ricondo’s new rate methodology “through the termination of

the existing Airline Use Agreements, the promulgation of amendments to the Authority's Airport

Rules and Regulations, and the issuance of new Operating Permits.” Resolution 2021-05

required CPA to provide the public 30 days’ notice to comment on the proposed amendments to

the Airport Rules and Regulations and, after considering any comments, “on October 1, 2021,

the Authority shall terminate any existing Airline Use Agreement, make effective the Authority's

amendments to the Airport Rules and Regulations, and proceed to issue Operating Permits to

airlines operating at its Airports.” A true copy of Board Resolution No. 2021-05 is attached to

this Declaration as Ex. CPA-10.

18. On June 28, 2021, notice of the proposed amendments to the Airport Rules and

Regulations was published in the Commonwealth Register. A true copy of the published notice

of the proposed amendments is attached to this Declaration as Ex. CPA-11.

19. On August 25, 2021, CPA sent written notice to SMA by hand delivery,

terminating the AUA and instituting the new rate methodology through regulation, effective

October 1, 2021. A true copy of the notice given to SMA on August 25, 2021 is attached to this

Declaration as Ex. CPA-12.

20. Termination of the AUA was consistent with and permitted by Section 6.01 of the

AUA. Section 6.01 provides: “This Agreement may be terminated as of September 30th in each

year by written notice from either party to the other given on or before August 31st of the year.”

A true copy of the AUA between CPA and SMA is attached to this Declaration as Ex. CPA-13.

SMA App. 008

7

21. On August 28, 2021, notice of certification and adoption of the proposed

amendments to the Airport Rules and Regulations was published in the Commonwealth Register.

A true copy of the August 28, 2021 notice is attached to this Declaration as Ex. CPA-14.

22. On September 3, 2021, at SMA’s request, CPA sent SMA a detailed breakdown

of the airfield and terminal costs used in calculating the rates for all three Airports.

23. In ¶ 55 of its Complaint, SMA alleges that CPA is unlawfully diverting airport

revenue to the Commonwealth Treasurer by paying one percent (1%) of the Authority’s

operating budget to the CNMI Office of the Public Auditor (“OPA”). I am not a lawyer and

offer no opinion on whether or not such payments, if they were made, would constitute unlawful

airport revenue diversion. The Authority has been communicating with regional officials of the

FAA to resolve any concerns about the propriety of such payments. A true copy of a letter from

CPA to the FAA seeking FAA’s guidance is attached to this Declaration as Ex. CPA-15. The

Authority has not actually made any such payments to the OPA for at least the past 15 years and

does not plan to make such a payment to OPA in FY 2022 unless the FAA advises that it would

be lawful to do so. The budget that Ricondo used to calculate the Fiscal Year 2022 rates

contained an allowance for such a payment to the OPA of $126,239 in the event that the FAA

advises such a payment is lawful. If the FAA advises such a payment is not lawful, a credit to

the airlines will be included in the year-end reconciliation of budgeted to actual costs for the

year. With respect to alleged payments to the OPA in Fiscal Years 2018-2021, the OPA

contribution was budgeted as an expense, but CPA has not made any such payments to the OPA.

If the FAA advises that payments under our local legislation are not lawful, CPA will reconcile

historical budgeted OPA expenses with the airlines, as appropriate.

24. As of the date of this declaration, SMA has not paid CPA any fees (other than

Passenger Facility Fees or “PFCs”) for its use of the terminals at the Airports since March 2015,

and SMA has not paid CPA any landing fees for its use of the airfields at the Airports since May

2015. As of November 1, SMA’s outstanding balance is $2,606,428.09 for use of the airfields

SMA App. 009

SMA App. 010

Exhibit CPA-1

SMA App. 011

SMA App. 012

Exhibit CPA-2

SMA App. 013

SMA App. 014

Exhibit CPA-3

SMA App. 015

Ricondo & Associates, Inc. (R&A) prepared this document for the stated purposes as expressly set forth herein and for the sole use of the Commonwealth Ports Authority and its intended recipients. The techniques and methodologies used in preparing this document are consistent with industry practices at the time of preparation. Ricondo & Associates, Inc. is not registered as a municipal advisor under Section 15B of the Securities Exchange Act of 1934 and R&A does not provide financial advisory services within the meaning of such Act.

Projected Airline Rates and Charges Methodology for Commonwealth Ports Authority Saipan Internat ional A i rport , Rota Internat iona l A i rport , T in ian Internat iona l A i rport

PREPARED BY :

RICONDO & ASSOCIATES, INC. Scr ipps Center |312 Walnut Street |Suite 3310, Suite 1700

4. Terminal Space ......................................................................................................................................... 4

6. Debt Service .............................................................................................................................................. 6

8. Airline Rates and Charges ....................................................................................................................... 8

Page 2 of 29 PREPARED ON 07/13/2016

SMA App. 017

1.1 Introduction

This document has been created to summarize the rate-making methodology to be utilized by the Commonwealth Ports Authority (the Authority) for the airlines serving Saipan International Airport, Rota International Airport, and Tinian International Airport (collectively known as “the Airport System”). This document is for discussion purposes only. Neither the Authority nor any of the airlines will be bound by any of the provisions of this document until an Operating Agreement has been fully executed. This document presents projected airlines rates and charges resulting from the operation of the Airport System by the Authority. The projected airline rates and charges methodology presented herein is based on the provisions and articles in the Operating Agreement and incorporates the estimated rates and charges impacts associated with both the day-to-day operations of the Airports, as well as undertaking capital projects during the time period covered in this document.

Included in this document are revenues and expenses for Fiscal Year (FY) 2016 Budget and Projected FY 2017 through FY 2020 (the Projection Period). The Authority’s FY is the twelve-month period ending September 30th in each year. These projections are based on a review of historical financial operations, estimated future aviation activity levels, discussions with Authority staff and the impacts of the projected Capital Improvement Program (CIP). This report also includes estimated airlines rates and charges, airline cost per enplanement, Airport cash flow, and debt service coverage for the Series A 1998 bonds.

The Authority has developed a rate-making methodology that is primarily compensatory in nature. It is recognized by the Authority that, with the current financial circumstances in which the Airlines are operating, along with transitioning to operating and maintaining a new airport facility, the business arrangement should reflect the fact that both the Airlines and the Authority are working together to provide adequate facilities at the Airports that do not create an unreasonable burden to the Airlines financially. The proposed business arrangement includes the following key elements.

A “cost center residual” landing fee rate for the Airfield Cost Center using total landed weight as the divisor.

A “cost center compensatory” average terminal rental rate for the Terminal Cost Center using total rentable square feet as the divisor.

Cost centers have been developed that are consistent with industry practices.

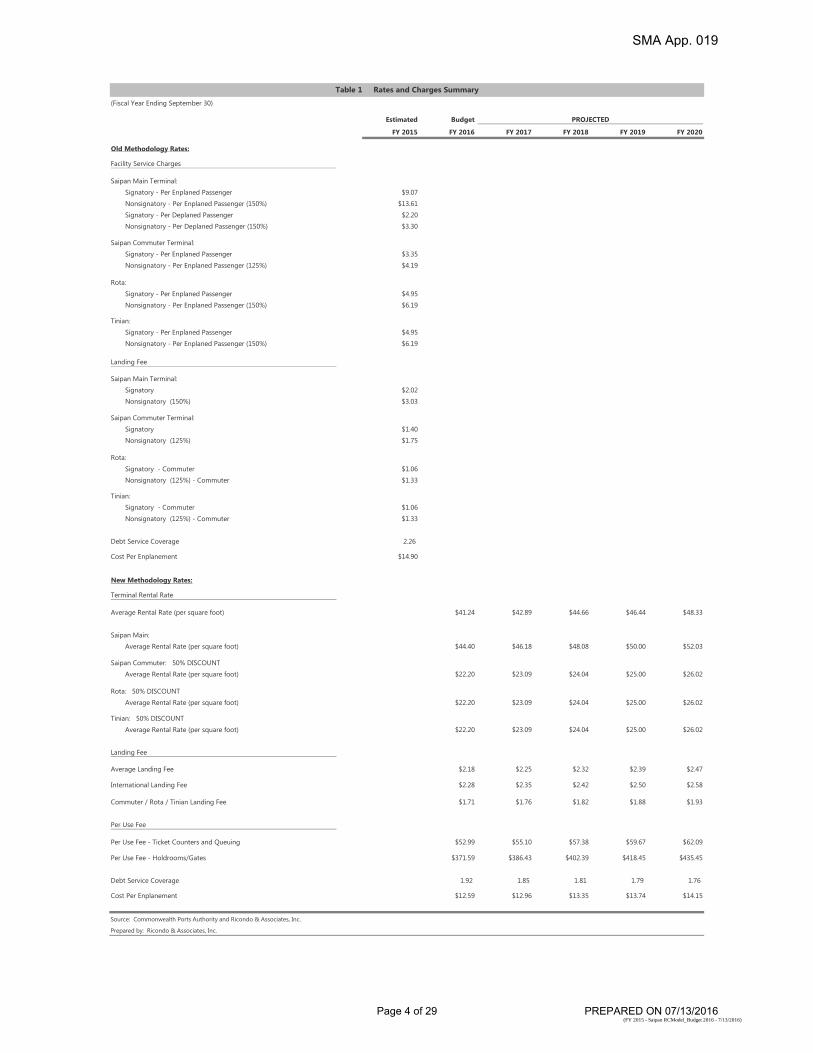

As a result of these assumptions and other described later in this report, the projected impacts to the Airlines for Budget FY 2016 and the Projection Period under the Operating Agreement are shown in Table 1.

Page 3 of 29 PREPARED ON 07/13/2016

SMA App. 018

(Fiscal Year Ending September 30)

Estimated Budget

FY 2015 FY 2016 FY 2017 FY 2018 FY 2019 FY 2020

Old Methodology Rates:

Facility Service Charges

Saipan Main Terminal:

Signatory - Per Enplaned Passenger $9.07

Nonsignatory - Per Enplaned Passenger (150%) $13.61

Signatory - Per Deplaned Passenger $2.20

Nonsignatory - Per Deplaned Passenger (150%) $3.30

Saipan Commuter Terminal:

Signatory - Per Enplaned Passenger $3.35

Nonsignatory - Per Enplaned Passenger (125%) $4.19

Rota:

Signatory - Per Enplaned Passenger $4.95

Nonsignatory - Per Enplaned Passenger (150%) $6.19

Tinian:

Signatory - Per Enplaned Passenger $4.95

Nonsignatory - Per Enplaned Passenger (150%) $6.19

Per Use Fee - Ticket Counters and Queuing $52.99 $55.10 $57.38 $59.67 $62.09

Per Use Fee - Holdrooms/Gates $371.59 $386.43 $402.39 $418.45 $435.45

Debt Service Coverage 1.92 1.85 1.81 1.79 1.76

Cost Per Enplanement $12.59 $12.96 $13.35 $13.74 $14.15

Source: Commonwealth Ports Authority and Ricondo & Associates, Inc.

Prepared by: Ricondo & Associates, Inc.

Table 1 Rates and Charges Summary

PROJECTED

(FY 2015 - Saipan RCModel_Budget 2016 - 7/13/2016)Page 4 of 29 PREPARED ON 07/13/2016

SMA App. 019

The remainder of this document is presented under the following headings:

Financial Structure Activity Projections Terminal Space Debt Service PFC Revenue Operating Expenses Non-Aviation Revenues Airline Rates and Charges

1.2 Financial Structure

Expenses, Debt Service and Capital Expenditures of the Authority are categorized into Cost Centers. The Authority utilizes the cost center structure described below, which is consistent with industry standards.

The Authority has identified the following Direct Cost Centers:

Airfield. The Airfield cost center includes the portion of the Airports provided for the landing, taking off, and taxiing of aircraft, including runways, taxiways, approach and runway protection zones, safety areas, infield areas, landing and navigational aids, and land areas required by or related to aeronautical use of the Airports.

Main Terminal. The Main Terminal cost center includes the Saipan International Airport main terminal passenger building and associated curbside entrance areas and adjoining landscaped areas. This cost center also includes the aircraft aprons at the Main Terminal.

Commuter Terminal. The Commuter Terminal cost center includes the Commuter Terminal building and associated curbside entrance areas, and aircraft aprons at the Commuter Terminal.

Rota Terminal. The Rota Terminal cost center includes the Rota Terminal building, associated curbside entrance areas, and aircraft aprons at the Rota Terminal.

Tinian Terminal. The Tinian Terminal cost center includes the Tinian Terminal building, associated curbside entrance areas, and aircraft aprons at the Tinian Terminal.

Indirect Cost Centers have expenditures that will be allocated to Direct Cost Centers:

ARFF. The ARFF cost center includes all aircraft rescue and firefighting functions of the Airport System.

Security. The Security cost center includes all functions of the Airport System related to security. Administrative. The Administrative cost center includes the administrative functions of the Airport

System.

Page 5 of 29 PREPARED ON 07/13/2016

SMA App. 020

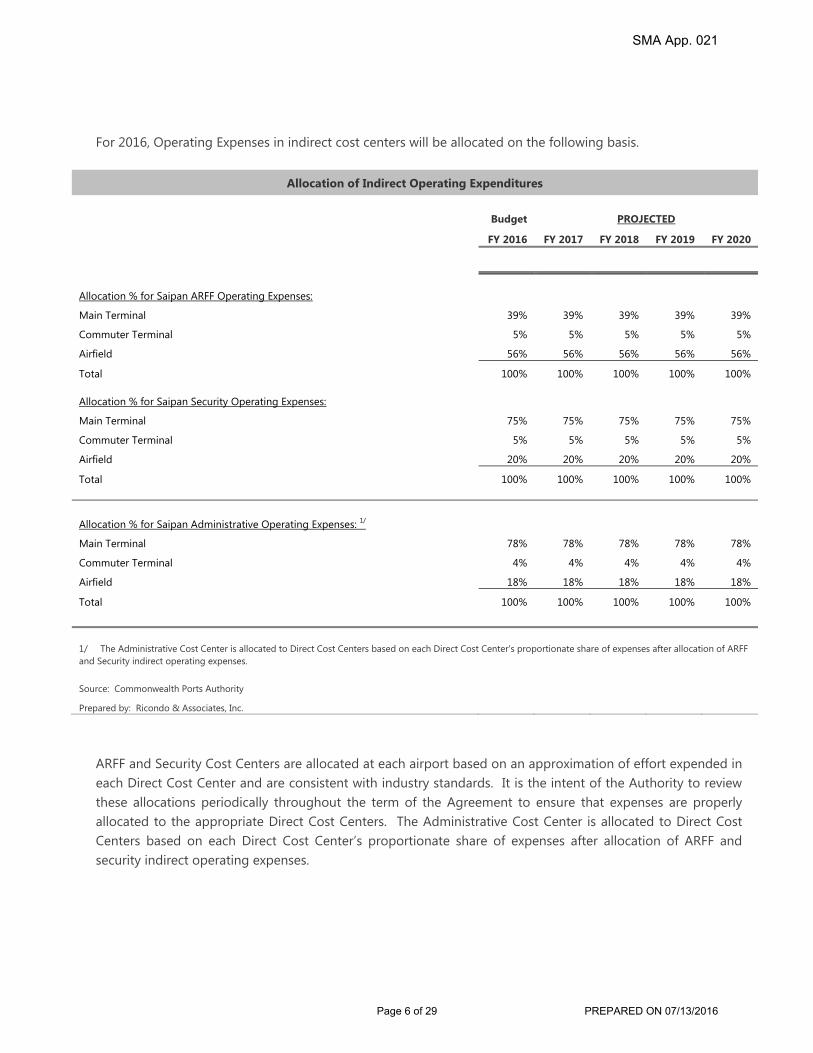

For 2016, Operating Expenses in indirect cost centers will be allocated on the following basis.

Allocation of Indirect Operating Expenditures

Budget PROJECTED

FY 2016 FY 2017 FY 2018 FY 2019 FY 2020

Allocation % for Saipan ARFF Operating Expenses:

Main Terminal 39% 39% 39% 39% 39%

Commuter Terminal 5% 5% 5% 5% 5%

Airfield 56% 56% 56% 56% 56%

Total 100% 100% 100% 100% 100%

Allocation % for Saipan Security Operating Expenses:

Main Terminal 75% 75% 75% 75% 75%

Commuter Terminal 5% 5% 5% 5% 5%

Airfield 20% 20% 20% 20% 20%

Total 100% 100% 100% 100% 100%

Allocation % for Saipan Administrative Operating Expenses: 1/

Main Terminal 78% 78% 78% 78% 78%

Commuter Terminal 4% 4% 4% 4% 4%

Airfield 18% 18% 18% 18% 18%

Total 100% 100% 100% 100% 100%

1/ The Administrative Cost Center is allocated to Direct Cost Centers based on each Direct Cost Center's proportionate share of expenses after allocation of ARFF and Security indirect operating expenses.

Source: Commonwealth Ports Authority

Prepared by: Ricondo & Associates, Inc.

ARFF and Security Cost Centers are allocated at each airport based on an approximation of effort expended in each Direct Cost Center and are consistent with industry standards. It is the intent of the Authority to review these allocations periodically throughout the term of the Agreement to ensure that expenses are properly allocated to the appropriate Direct Cost Centers. The Administrative Cost Center is allocated to Direct Cost Centers based on each Direct Cost Center’s proportionate share of expenses after allocation of ARFF and security indirect operating expenses.

Page 6 of 29 PREPARED ON 07/13/2016

SMA App. 021

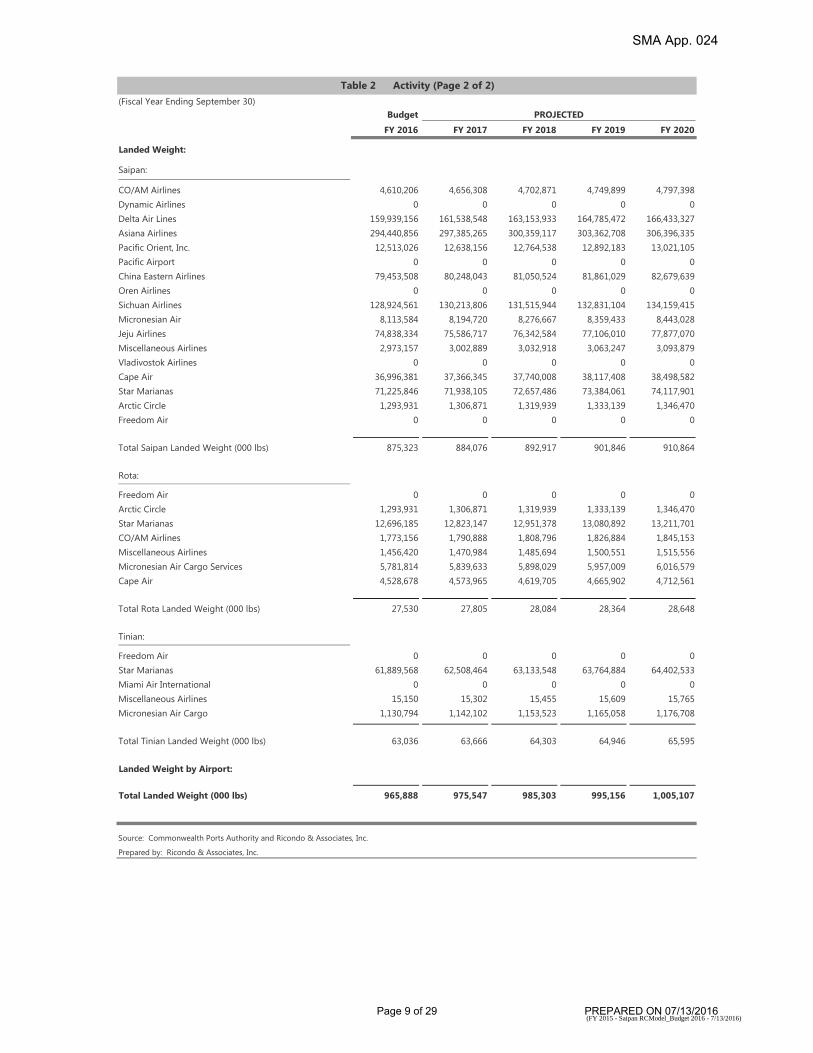

1.3 Activity Projections

Table 2 presents projected enplanements and landed weights for the Airports for the Projection Period.

The activity projections have been developed for all airlines and the main assumptions are:

Enplanements. The enplanements are projected to grow by 1.0 percent annually throughout the Projection Period.

Landed Weights. The landed weights are projected to grow by 1.0 percent annually throughout the Projection Period.

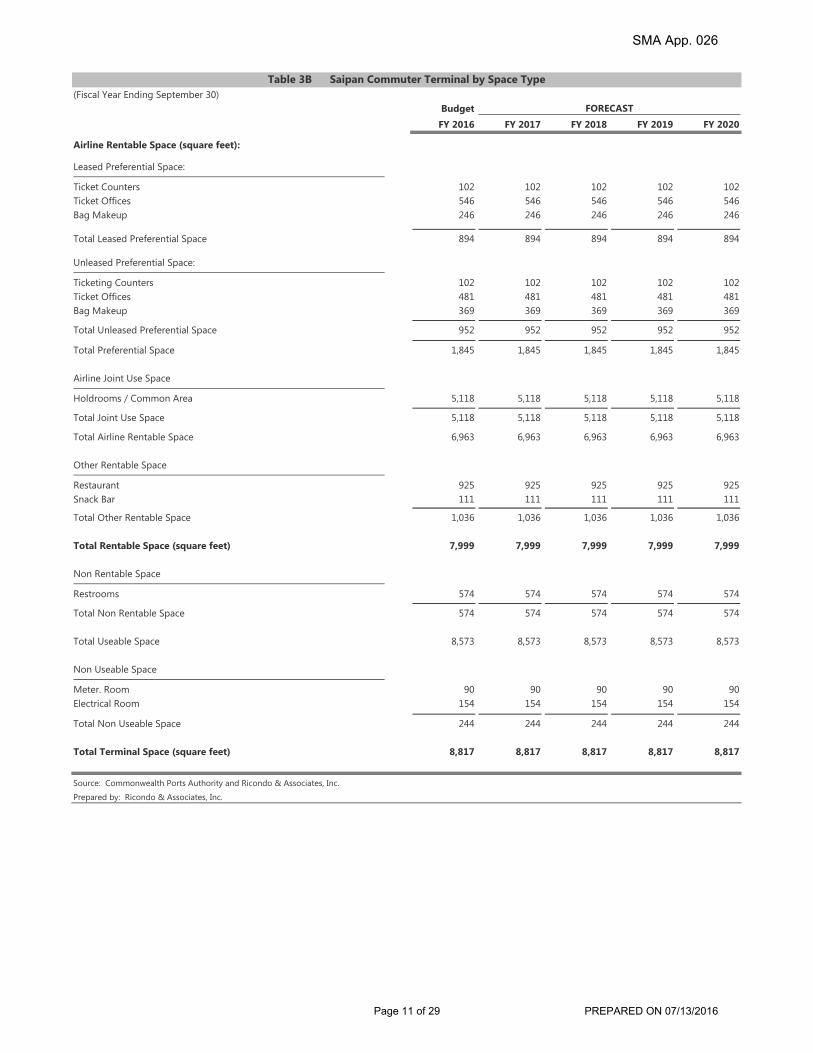

1.4 Terminal Space

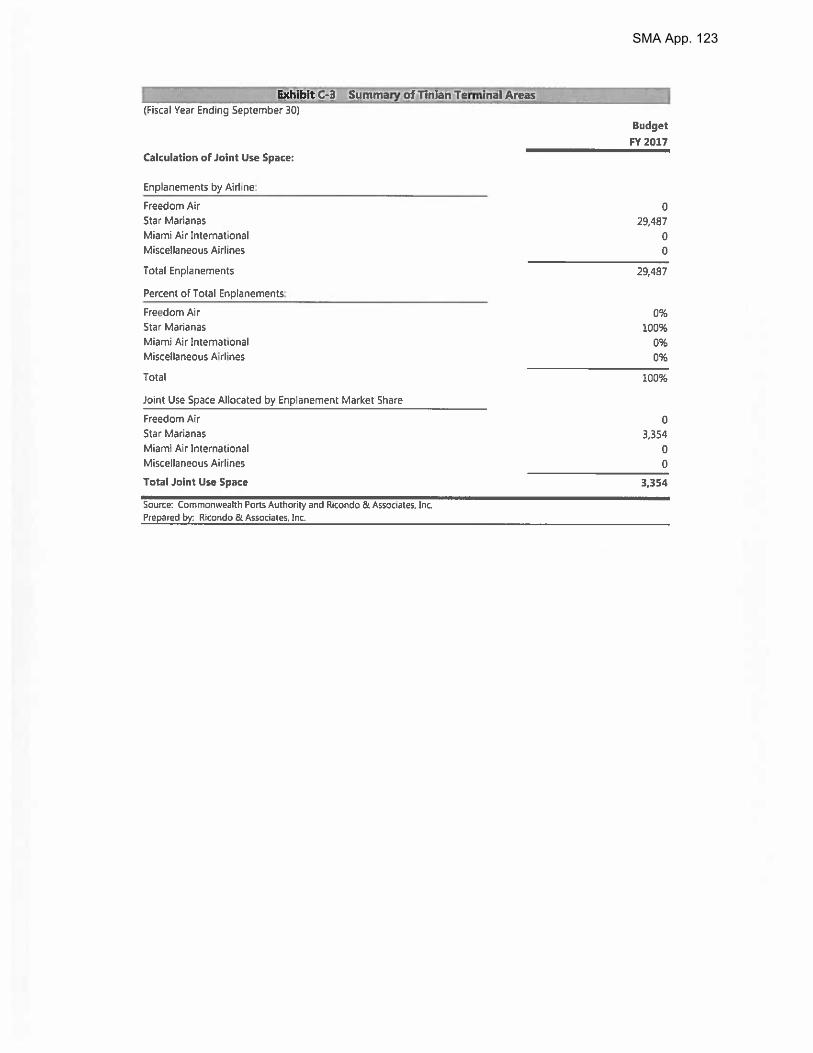

Total terminal space differentiated into airline preferential space, airline joint use space, other rentable space and non-rentable space for each airport.

The other rentable space includes concessions, Federal Inspections Services (FIS), Transportation Security Administration (TSA), U.S. Customs and Border Protection (CBP), other miscellaneous rentable and Authority administrative space. Joint Use space is allocated to Airlines based on each Airline’s percentage of enplanements.

The following Tables 3A-3D present terminal space for the Airport System:

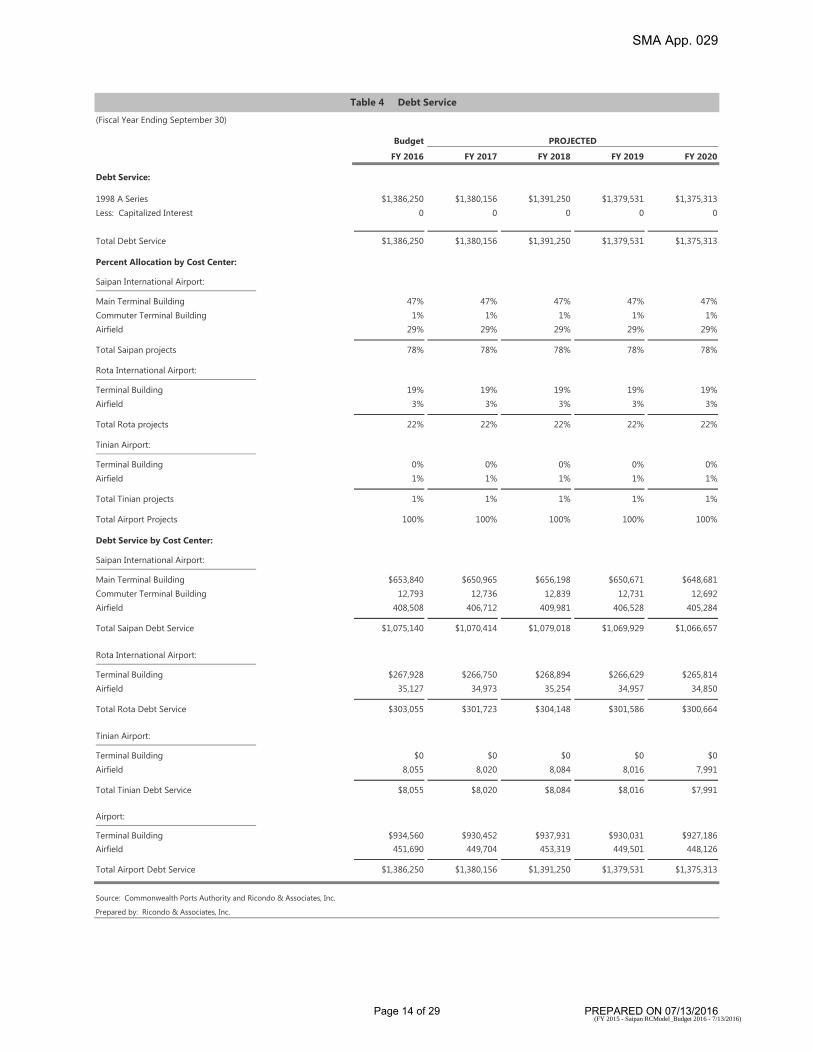

1.5 Debt Service

Debt service consists of projected debt service on the Airport’s Series A 1998 bond. Table 4 presents the projected debt service at the Airports from FY 2016 throughout the Projection Period. Debt service at the Airports is expected to remain level at approximately $1.4 million throughout the Projection Period.

1.6 Passenger Facility Charge (PFC) Revenue

Table 5 presents estimated PFC Revenue at the Airport System for the Projection Period. The Authority collects the maximum rate of $4.50 per enplanement and under FAA regulation is able to keep $4.39 per enplaned passenger after a $0.11 per enplanement administrative fee is paid. Historically, the Airport System has eligible enplanements of approximately 90.0 percent of total enplanements.

CPA has authority to pay 30.2 percent of annual Debt Service and coverage payments from PFC revenues based on 1998 PFC-eligible projects. Total PFC Revenue to be used for debt service between FY 2016 and FY

Reimburse CPA for PAYG Projects 1,898,444 1,924,962 1,945,234 1,974,362 2,000,906

Ending Balance $0 $0 $0 $0 $0

Source: Commonwealth Ports Authority and Ricondo & Associates, Inc.

Prepared by: Ricondo & Associates, Inc.

PROJECTED

Table 5 PFC Revenues

(FY 2015 - Saipan RCModel_Budget 2016 - 7/13/2016)Page 16 of 29 PREPARED ON 07/13/2016

SMA App. 031

2020 is approximately $500 thousand per year. The remaining PFC revenues received annually reimburse CPA for PFC-eligible projects originally funded with CPA funds.

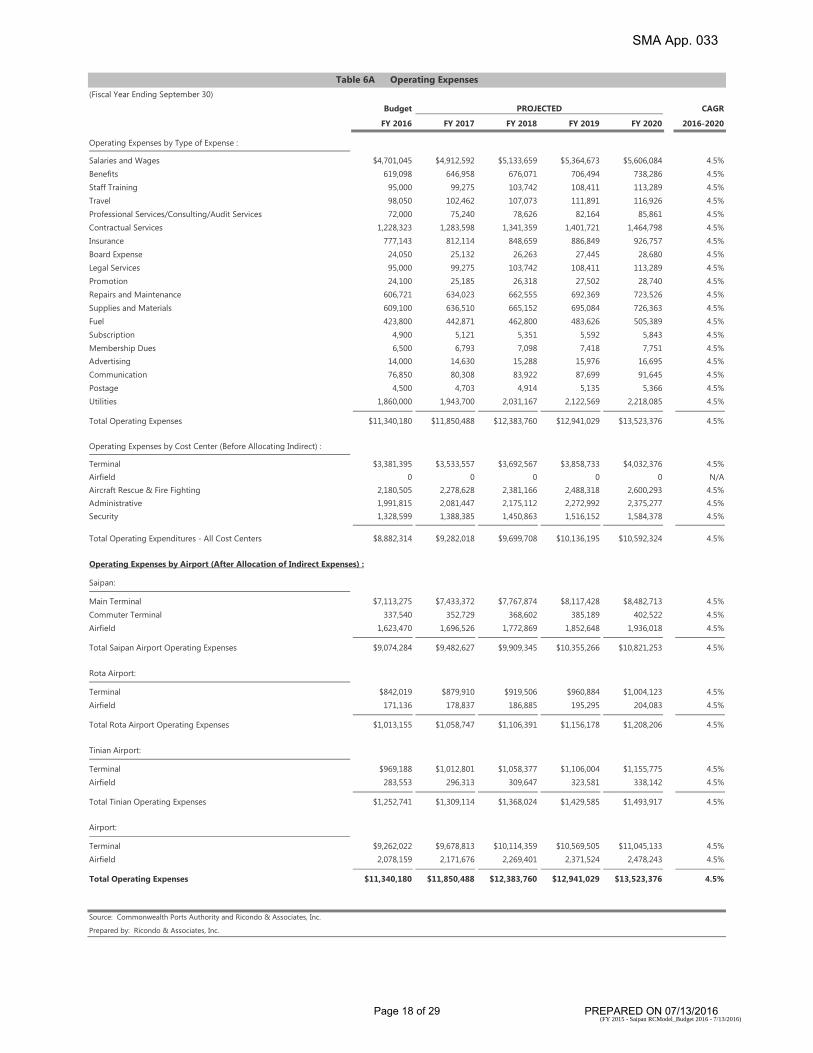

1.7 Operating Expenses and Capital Expenditures

Tables 6A and 6B present Operating Expenses and Capital Expenditures at the Airport System for the Projection Period. Operating Expenses at the Airport System are expected to increase at a compound annual growth rate of 4.5 percent through the Projection Period. Capital Expenditures at the Airport System are expected to increase at a compound annual growth rate of 3.0 percent through the Projection Period.

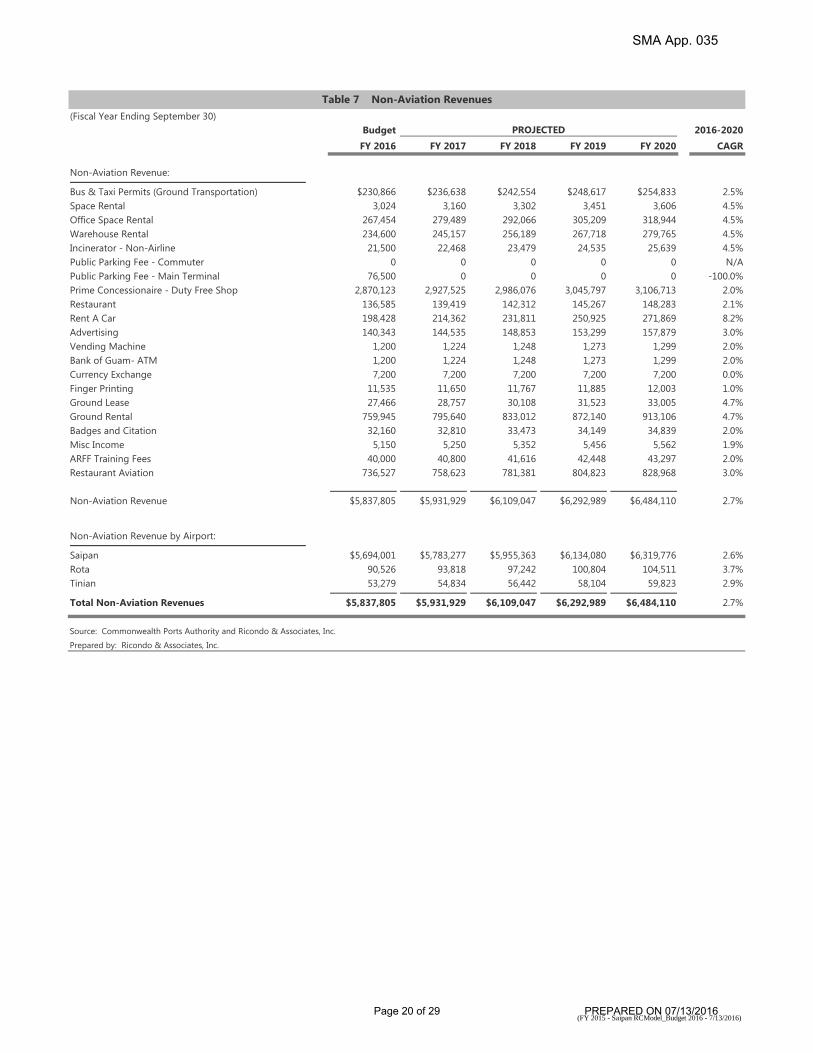

1.8 Non-Aviation Revenues

Table 7 presents Non-Aviation Revenue at the Airport System for the Projection Period. Non-Aviation Revenue includes revenues from cargo landing fees and facility rentals, hangers rentals, fuel flowage fees, FBO rentals, rental car contracts, concessions, other ground transportation fees, investments earnings, and miscellaneous other revenues.

Non-Aviation Revenue at the Airport System is expected to increase at a compound annual growth rate of 2.7 percent through the Projection Period, based on inflationary impacts and enplanement growth.

1.9 Airline Rates and Charges

Rates will be calculated for the Terminal and Airfield at the Airports. The airlines rates and charges presented in these analyses for FY 2016 though the Projection Period reflect the proposed methodology described earlier in this report. The proposed methodology is described in more detail below.

The components of the total requirement for the terminal rental rate and landing fee include the following:

Operating Expenses. Includes the Operating Expenses (direct and allocated indirect) attributable to the specific rate-setting area.

Debt Service. Includes the portion of Total Debt Service attributable to the specific rate-setting area. Debt Service Coverage. Includes 25 percent of Total Debt Service attributable to the specific rate-

setting area. Capital Equipment. Includes the capital Equipment attributable to the specific rate-setting area.

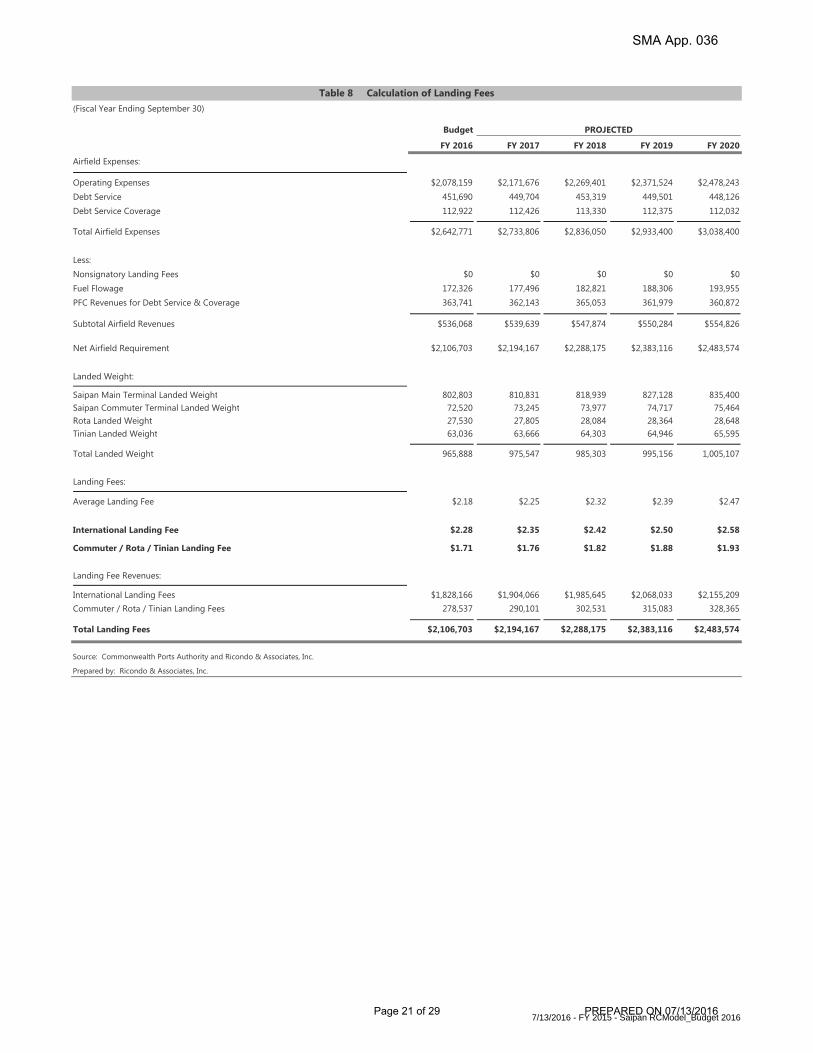

1.9.1 LANDING FEE

A residual calculation for the Landing Fee is presented in Table 8. The Total Airfield Requirement is equal to the sum of the previously described components for the Airfield Cost Center. Fuel flowage revenues, and PFC revenues eligible for Debt Service and Coverage attributable to the Airfield are deducted to yield the Airfield

Total Landing Fees $2,106,703 $2,194,167 $2,288,175 $2,383,116 $2,483,574

Source: Commonwealth Ports Authority and Ricondo & Associates, Inc.

Prepared by: Ricondo & Associates, Inc.

PROJECTED

Table 8 Calculation of Landing Fees

7/13/2016 - FY 2015 - Saipan RCModel_Budget 2016Page 21 of 29 PREPARED ON 07/13/2016

SMA App. 036

Requirement. Dividing the Airfield requirement by the total landed weight yields the Average Landing Fee. The Landing Fee is differentiated so that the Landing Fee for the Commuter Airfield, Rota Airfield, and Tinian Airfield are 50 percent less than the landing fee for the Main Terminal.

1.9.2 TERMINAL RENTAL RATE

A compensatory calculation for the Terminal Rental Rates is presented in Table 9A. The Terminal Requirement is equal to the sum of the previously described components for the Main Terminal Cost Center, Commuter Terminal Cost Center, Rota Terminal Cost Center and Tinian Terminal Cost Center less PFC revenues eligible for Debt Service and Coverage attributable in the Main Terminal Cost Center, Commuter Terminal Cost Center Rota Terminal Cost Center and Tinian Terminal Cost Center. Dividing the Terminal Requirement by the total rentable space in the terminal building yields the Average Terminal Rental Rate. The Average Terminal Rental Rate is then differentiated so that the terminal rental rate for the Commuter Terminal, Rota Terminal and Tinian Terminal is 50 percent less than the terminal rental rate for Saipan Main Terminal.

Tables 9B-9E provide detail of joint use space at the Airport System allocated based on airlines proportionate enplanements.

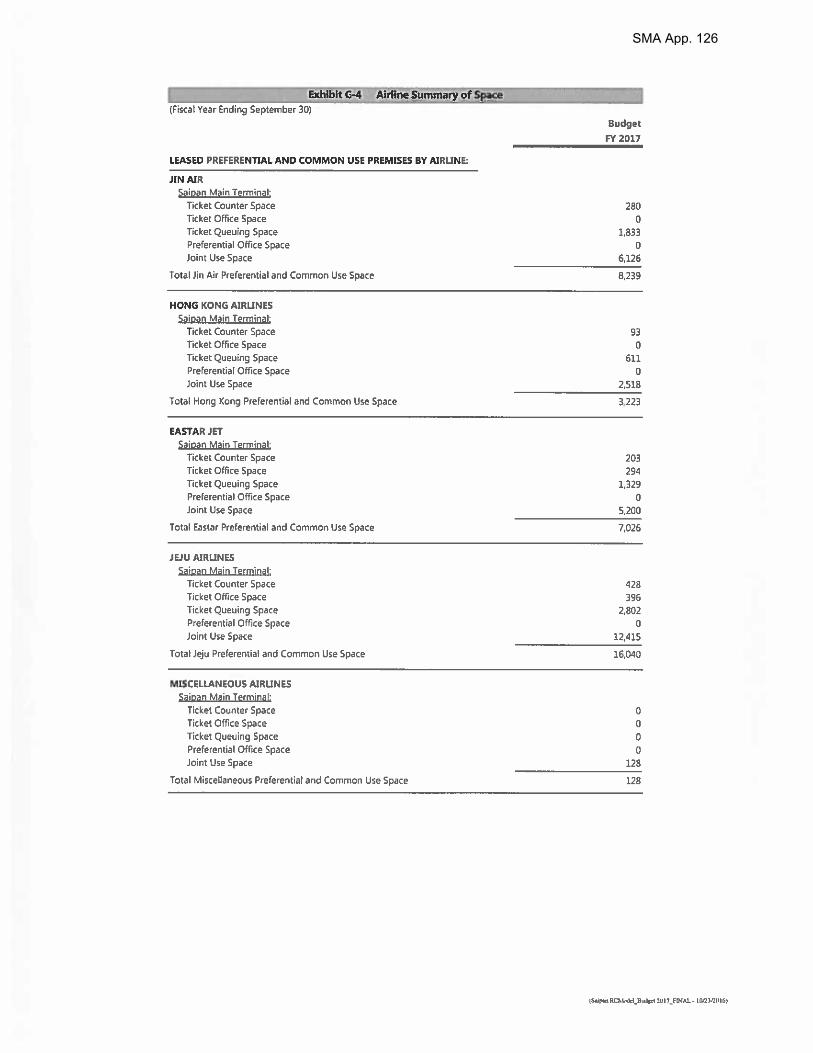

1.9.3 PER USE FEES

A Per Use Fee has been developed for Saipan Main Terminal to charge airlines utilizing shared space within the Main Terminal Building. Specifically, certain Ticket Counters/Queuing Space and Holdrooms/Gates are used by more than one airline and often on a less than daily basis. Airlines will be charged for this space based on the number of times the airline uses the space. A calculation for the Per Use Fees at the Saipan Main Terminal is presented in Table 10.

The average leased airline space used for the Ticket Counters/Queuing Space - Per Use Fee is the sum of the total ticket counters space and the total queuing space (ticketing lobby area) divided by the total number of ticket counters in the terminal building. The Average Terminal Rental Rate is applied to the Average Leased Ticket Counter/Queuing Space to calculate the annual cost of average ticket counter/queuing space. The Per Use Fee is equal to the annual cost of average ticket counter/queuing space divided by the days of the year, divided by the average turns per day.

The Holdrooms/Gates – Per Use Fee equals the average holdroom gate size multiplied by the Average Terminal Rental Rate, divided by the days of the year and the average usage per day.

1.9.4 CASH FLOW AND COST PER ENPLANEMENT

Table 11 presents the Cash Flow, Coverage Calculation and Cost Per Enplanement for the Airport System.

Total Aviation Revenues $7,626,360 $7,927,200 $8,249,641 $8,575,149 $8,918,838

Total Enplanements 605,765 611,822 617,941 624,120 630,361

Cost Per Enplanement $12.59 $12.96 $13.35 $13.74 $14.15

Source: Commonwealth Ports AuthorityPrepared by: Ricondo & Associates, Inc.

Table 11 Cash Flow, Coverage Calculation, Cost Per Enplanement

PROJECTED

(FY 2015 - Saipan RCModel_Budget 2016 - 7/13/2016)Page 29 of 29 PREPARED ON 07/13/2016

SMA App. 044

Exhibit CPA-4

SMA App. 045

1

From: CPA Receptionist [mailto:[email protected]] Sent: Friday, July 15, 2016 4:28 PM To: 'Shawn Christian' <[email protected]> Subject: RE: Airline Meeting Good afternoon, Attached is the meeting materials for the rate methodology meeting on Tuesday, July 19 at 1:00pm. For your perusal, thank you. Christine Santiago Pulido Receptionist/Secretary Commonwealth Ports Authority P.O. Box 501055 Saipan, MP 96950 Tel: (670) 237‐6500 | Fax: (670) 234‐5962

From: CPA Receptionist [mailto:[email protected]] Sent: Friday, July 01, 2016 4:28 PM To: 'Shawn Christian' <[email protected]> Subject: Airline Meeting Dear Star Marianas Air, Good afternoon, the Commonwealth Ports Authority would like to schedule a meeting for July 19 at 3:00PM at the CPA Conference Room. The meeting is to discuss about the new rate methodology. Because your presence is important, we request that you confirm your attendance at your earliest convenience. We look forward to your favorable response, thank you. Christine Santiago Pulido Receptionist/Secretary Commonwealth Ports Authority P.O. Box 501055 Saipan, MP 96950 Tel: (670) 237‐6500 | Fax: (670) 234‐5962

SMA App. 046

Exhibit CPA-5

SMA App. 047

SMA App. 048

SMA App. 049

SMA App. 050

SMA App. 051

SMA App. 052

SMA App. 053

SMA App. 054

SMA App. 055

SMA App. 056

SMA App. 057

SMA App. 058

SMA App. 059

SMA App. 060

SMA App. 061

SMA App. 062

SMA App. 063

SMA App. 064

SMA App. 065

SMA App. 066

SMA App. 067

SMA App. 068

SMA App. 069

SMA App. 070

SMA App. 071

SMA App. 072

SMA App. 073

SMA App. 074

SMA App. 075

SMA App. 076

SMA App. 077

SMA App. 078

SMA App. 079

SMA App. 080

SMA App. 081

SMA App. 082

SMA App. 083

SMA App. 084

SMA App. 085

SMA App. 086

SMA App. 087

SMA App. 088

SMA App. 089

SMA App. 090

SMA App. 091

SMA App. 092

SMA App. 093

SMA App. 094

SMA App. 095

SMA App. 096

SMA App. 097

SMA App. 098

SMA App. 099

SMA App. 100

SMA App. 101

SMA App. 102

SMA App. 103

SMA App. 104

SMA App. 105

SMA App. 106

SMA App. 107

SMA App. 108

SMA App. 109

SMA App. 110

SMA App. 111

SMA App. 112

SMA App. 113

SMA App. 114

SMA App. 115

SMA App. 116

SMA App. 117

SMA App. 118

SMA App. 119

SMA App. 120

SMA App. 121

SMA App. 122

SMA App. 123

SMA App. 124

SMA App. 125

SMA App. 126

SMA App. 127

SMA App. 128

SMA App. 129

SMA App. 130

SMA App. 131

SMA App. 132

SMA App. 133

SMA App. 134

SMA App. 135

SMA App. 136

SMA App. 137

SMA App. 138

SMA App. 139

SMA App. 140

SMA App. 141

SMA App. 142

SMA App. 143

SMA App. 144

SMA App. 145

SMA App. 146

SMA App. 147

SMA App. 148

SMA App. 149

SMA App. 150

SMA App. 151

SMA App. 152

SMA App. 153

SMA App. 154

SMA App. 155

SMA App. 156

SMA App. 157

SMA App. 158

SMA App. 159

SMA App. 160

SMA App. 161

SMA App. 162

SMA App. 163

SMA App. 164

SMA App. 165

SMA App. 166

SMA App. 167

SMA App. 168

SMA App. 169

SMA App. 170

SMA App. 171

SMA App. 172

SMA App. 173

SMA App. 174

SMA App. 175

SMA App. 176

SMA App. 177

SMA App. 178

SMA App. 179

SMA App. 180

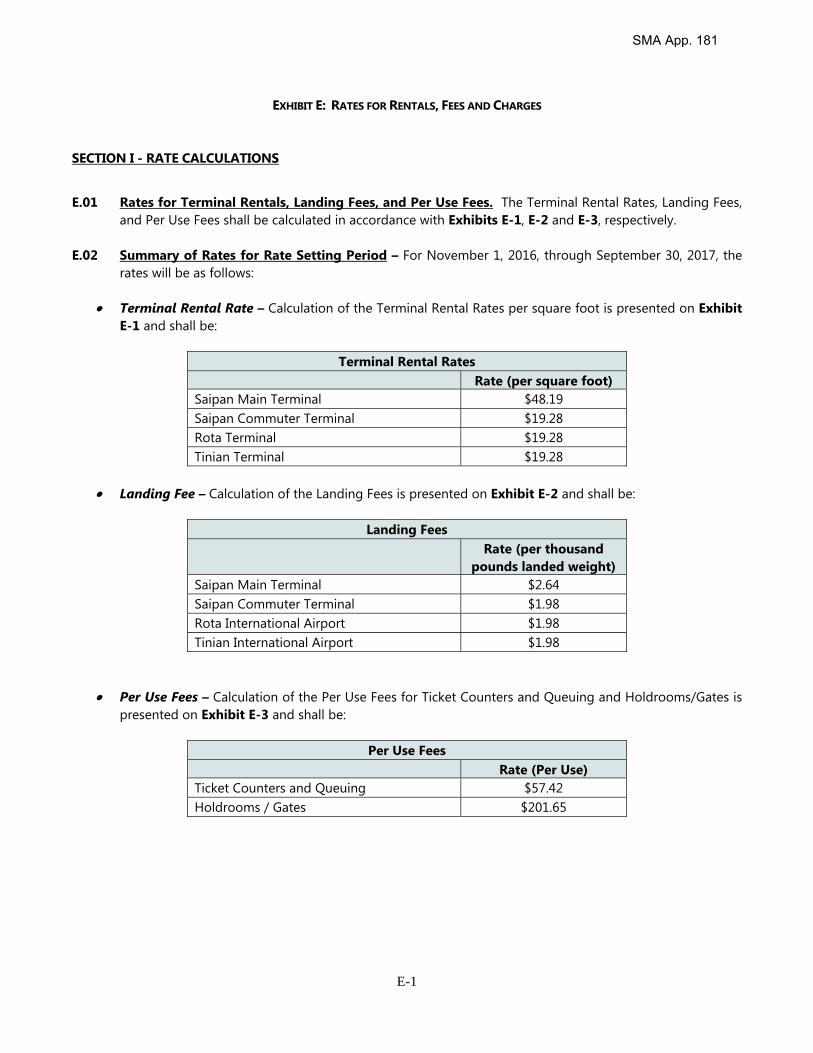

E-1

EXHIBIT E: RATES FOR RENTALS, FEES AND CHARGES

SECTION I - RATE CALCULATIONS

E.01 Rates for Terminal Rentals, Landing Fees, and Per Use Fees. The Terminal Rental Rates, Landing Fees,

and Per Use Fees shall be calculated in accordance with Exhibits E-1, E-2 and E-3, respectively. E.02 Summary of Rates for Rate Setting Period – For November 1, 2016, through September 30, 2017, the

rates will be as follows:

Terminal Rental Rate – Calculation of the Terminal Rental Rates per square foot is presented on Exhibit E-1 and shall be:

Source: Commonwealth Ports Authority and Ricondo & Associates, Inc.

Prepared by: Ricondo & Associates, Inc.

Exhibit E-1 Line Items

A. Maintenance and Operating Expenses - the current expenses, paid or accrued, of operation, maintenance, and ordinary current repairs related to the Terminal Cost and Revenue Center.

B. Debt Service – shall mean with respect to any series of Bonds or Subordinated Bonds the total, as of any

particular date of computation and for any particular period or year, of the aggregate amount required pursuant to the Resolution to be deposited during such period or year in the Bond Fund, attributable to the Terminal Cost and Revenue Center.

C. Debt Service Coverage – twenty-five percent (25%) of the Debt Service payable for Bonds in each Fiscal

Year (adjusted as may be permitted under the Bond Resolution), attributable to the Terminal Cost and Revenue Center.

SMA App. 182

E-3

D. Capital Equipment – expenditures for acquisition of moveable equipment consisting of, but not limited to, firefighting equipment, trucks, tractors, mowers, and other maintenance equipment, and automotive equipment and other similar moveable equipment and for the purpose of paying the cost of rebuilding, reconstructing, altering, maintaining, replacing and renewing the moveable equipment of the Airport System, attributable to the Terminal Cost and Revenue Center.

E. TOTAL TERMINAL MAINTENANCE AND OPERATING EXPENSES – sum of A through D.

F. PFC Revenues for Debt Service & Coverage - total amount of PFC Revenue eligible for contribution

to annual Debt Service and Debt Service Coverage in current Fiscal Year, attributable to the Terminal Cost and Revenue Center.

G. NET TERMINAL REQUIREMENT – Sum of E minus F.

H. Total Airport System Terminal Rentable Space (per square foot) – total Terminal Square Fee available

to be leased by Airport System users.

I. AVERAGE TERMINAL RENTAL RATE (per square foot) – G divided by H.

J. Saipan Main Terminal Rental Rate (per square foot) – the Terminal Rental Rate to be charged to Airport users leasing space within the Saipan Main Terminal, after 40 percent (40%) differentiation is applied between Saipan Main Terminal and Saipan Commuter Terminal, Rota Terminal, and Tinian Terminal. The Saipan Main Terminal Rental Rate (per square foot) is an iterative calculation forcing a 40 percent (40%) differential between Saipan Main Terminal and Saipan Commuter Terminal, Rota Terminal, and Tinian Terminal while simultaneously generating the Net Terminal Requirement based on Airline leased terminal space.

foot), and Tinian Terminal Rental Rate (per square foot) – the Terminal Rental Rate to be charged to Airport users leasing space within the Saipan Commuter Terminal, after 40 percent (40%) differentiation is applied between Saipan Main Terminal and Saipan Commuter Terminal, Rota Terminal, and Tinian Terminal. The Saipan Commuter Terminal Rental Rate (per square foot), Rota Terminal Rental Rate (per square foot), and Tinian Terminal Rental Rate (per square foot) is an iterative calculation forcing a 40 percent (40%) differential between Saipan Main Terminal and Saipan Commuter Terminal, Rota Terminal, and Tinian Terminal while simultaneously generating the Net Terminal Requirement based on Airline leased terminal space.

SMA App. 183

E-4

E.04 Calculation of Landing Fee Rate – Exhibit E-2

Exhibit E-2 Calculation of Landing Fees

(Fiscal Year Ending September 30)

Budget

FY 2017

Airfield Expenses:

Maintenance and Operating Expenses [A] $2,572,466

Debt Service [B] 449,704

Debt Service Coverage [C] 112,426

Total Airfield Maintenance and Operating Expenses [D] = [A+B+C] $3,134,597

Less:

Fuel Flowage [E] $177,496

PFC Revenues for Debt Service & Coverage [F] 362,143

Source: Commonwealth Ports Authority and Ricondo & Associates, Inc.

Prepared by: Ricondo & Associates, Inc.

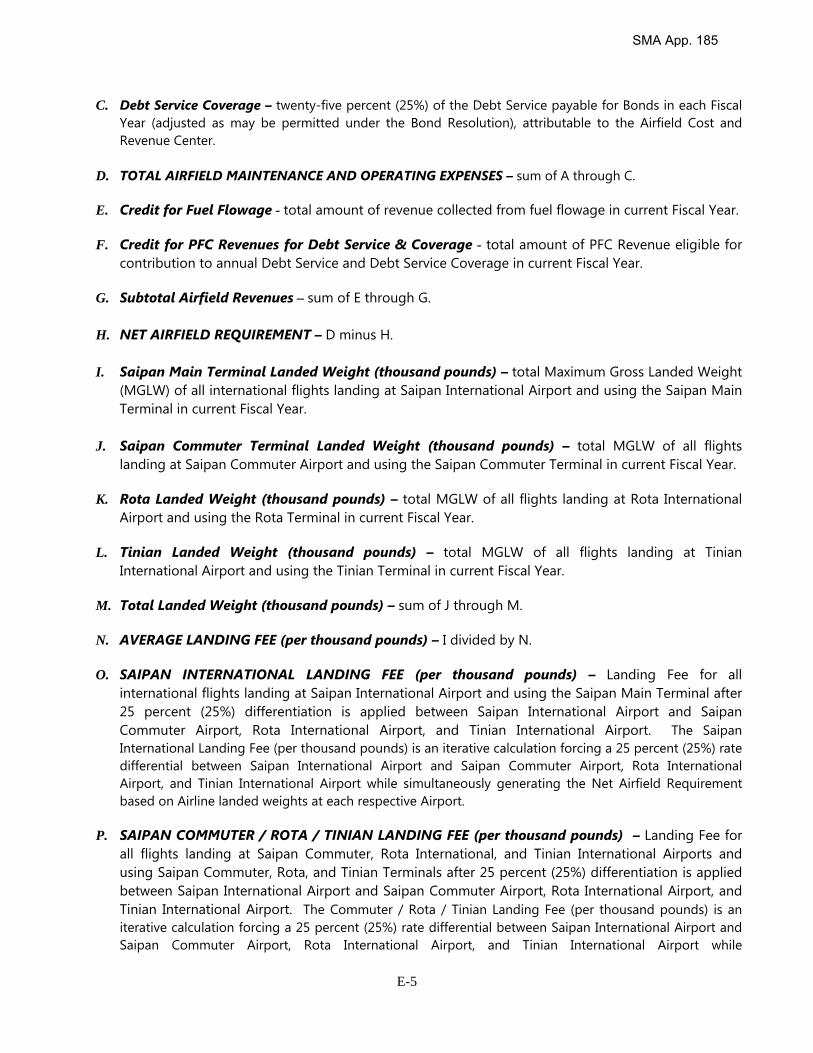

Exhibit E-2 Line Items:

A. Maintenance and Operating Expenses - the current expenses, paid or accrued, of operation, maintenance, and ordinary current repairs related to the Airfield Cost and Revenue Center.

B. Debt Service – with respect to any series of Bonds or Subordinated Bonds the total, as of any particular

date of computation and for any particular period or year, of the aggregate amount required pursuant to the Resolution to be deposited during such period or year in the Bond Fund, attributable to the Airfield Cost and Revenue Center.

SMA App. 184

E-5

C. Debt Service Coverage – twenty-five percent (25%) of the Debt Service payable for Bonds in each Fiscal Year (adjusted as may be permitted under the Bond Resolution), attributable to the Airfield Cost and Revenue Center.

D. TOTAL AIRFIELD MAINTENANCE AND OPERATING EXPENSES – sum of A through C.

E. Credit for Fuel Flowage - total amount of revenue collected from fuel flowage in current Fiscal Year.

F. Credit for PFC Revenues for Debt Service & Coverage - total amount of PFC Revenue eligible for

contribution to annual Debt Service and Debt Service Coverage in current Fiscal Year.

G. Subtotal Airfield Revenues – sum of E through G.

H. NET AIRFIELD REQUIREMENT – D minus H.

I. Saipan Main Terminal Landed Weight (thousand pounds) – total Maximum Gross Landed Weight (MGLW) of all international flights landing at Saipan International Airport and using the Saipan Main Terminal in current Fiscal Year.

J. Saipan Commuter Terminal Landed Weight (thousand pounds) – total MGLW of all flights

landing at Saipan Commuter Airport and using the Saipan Commuter Terminal in current Fiscal Year.

K. Rota Landed Weight (thousand pounds) – total MGLW of all flights landing at Rota International Airport and using the Rota Terminal in current Fiscal Year.

L. Tinian Landed Weight (thousand pounds) – total MGLW of all flights landing at Tinian

International Airport and using the Tinian Terminal in current Fiscal Year.

M. Total Landed Weight (thousand pounds) – sum of J through M.

N. AVERAGE LANDING FEE (per thousand pounds) – I divided by N.

O. SAIPAN INTERNATIONAL LANDING FEE (per thousand pounds) – Landing Fee for all international flights landing at Saipan International Airport and using the Saipan Main Terminal after 25 percent (25%) differentiation is applied between Saipan International Airport and Saipan Commuter Airport, Rota International Airport, and Tinian International Airport. The Saipan International Landing Fee (per thousand pounds) is an iterative calculation forcing a 25 percent (25%) rate differential between Saipan International Airport and Saipan Commuter Airport, Rota International Airport, and Tinian International Airport while simultaneously generating the Net Airfield Requirement based on Airline landed weights at each respective Airport.

P. SAIPAN COMMUTER / ROTA / TINIAN LANDING FEE (per thousand pounds) – Landing Fee for

all flights landing at Saipan Commuter, Rota International, and Tinian International Airports and using Saipan Commuter, Rota, and Tinian Terminals after 25 percent (25%) differentiation is applied between Saipan International Airport and Saipan Commuter Airport, Rota International Airport, and Tinian International Airport. The Commuter / Rota / Tinian Landing Fee (per thousand pounds) is an iterative calculation forcing a 25 percent (25%) rate differential between Saipan International Airport and Saipan Commuter Airport, Rota International Airport, and Tinian International Airport while

SMA App. 185

E-6

simultaneously generating the Net Airfield Requirement based on Airline landed weights at each respective Airport.

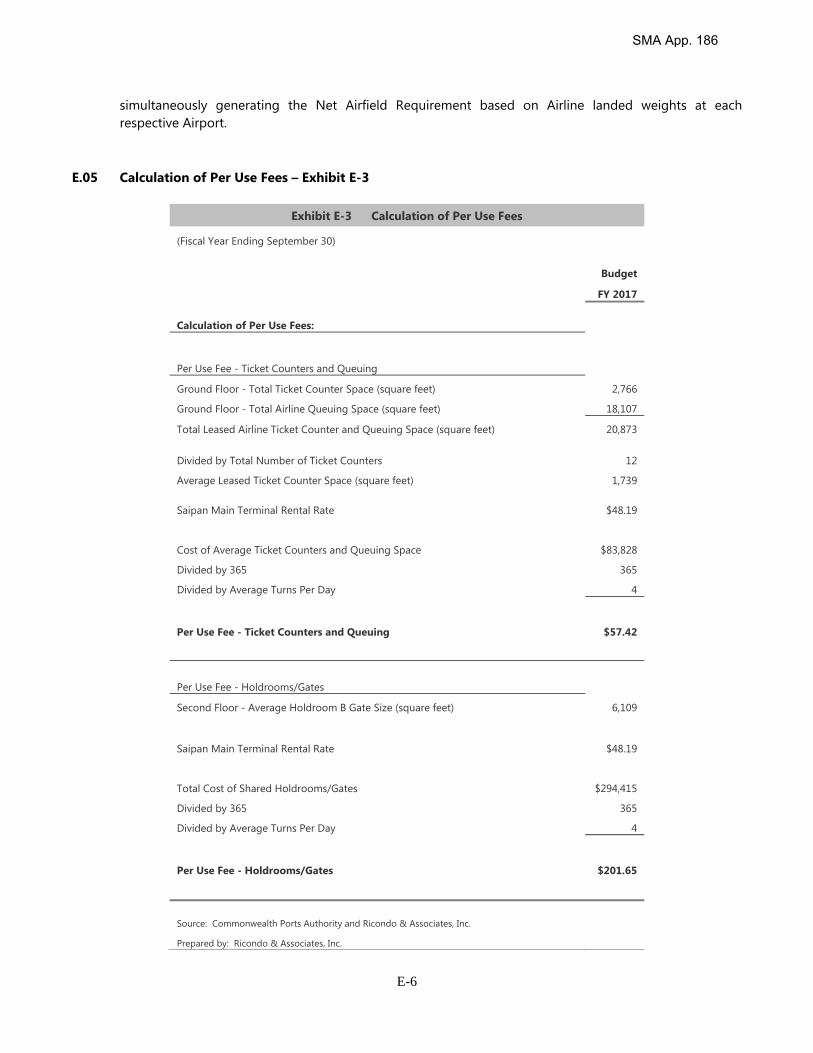

E.05 Calculation of Per Use Fees – Exhibit E-3

Exhibit E-3 Calculation of Per Use Fees

(Fiscal Year Ending September 30)

Budget

FY 2017

Calculation of Per Use Fees:

Per Use Fee - Ticket Counters and Queuing

Ground Floor - Total Ticket Counter Space (square feet) 2,766

Ground Floor - Total Airline Queuing Space (square feet) 18,107

Total Leased Airline Ticket Counter and Queuing Space (square feet) 20,873

Divided by Total Number of Ticket Counters 12

Average Leased Ticket Counter Space (square feet) 1,739

Saipan Main Terminal Rental Rate $48.19

Cost of Average Ticket Counters and Queuing Space $83,828

Divided by 365 365

Divided by Average Turns Per Day 4

Per Use Fee - Ticket Counters and Queuing $57.42

Per Use Fee - Holdrooms/Gates

Second Floor - Average Holdroom B Gate Size (square feet) 6,109

Saipan Main Terminal Rental Rate $48.19

Total Cost of Shared Holdrooms/Gates $294,415

Divided by 365 365

Divided by Average Turns Per Day 4

Per Use Fee - Holdrooms/Gates $201.65

Source: Commonwealth Ports Authority and Ricondo & Associates, Inc.

Prepared by: Ricondo & Associates, Inc.

SMA App. 186

E-7

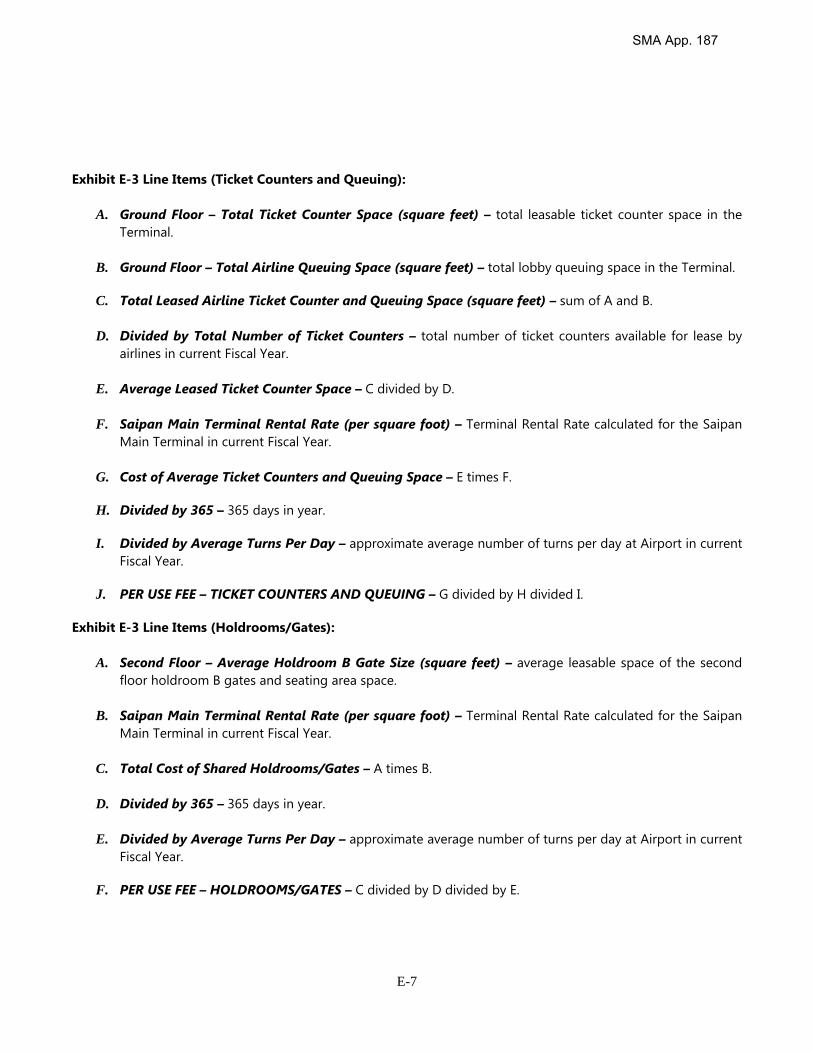

Exhibit E-3 Line Items (Ticket Counters and Queuing):

A. Ground Floor – Total Ticket Counter Space (square feet) – total leasable ticket counter space in the Terminal.

B. Ground Floor – Total Airline Queuing Space (square feet) – total lobby queuing space in the Terminal.

C. Total Leased Airline Ticket Counter and Queuing Space (square feet) – sum of A and B.

D. Divided by Total Number of Ticket Counters – total number of ticket counters available for lease by

airlines in current Fiscal Year.

E. Average Leased Ticket Counter Space – C divided by D.

F. Saipan Main Terminal Rental Rate (per square foot) – Terminal Rental Rate calculated for the Saipan Main Terminal in current Fiscal Year.

G. Cost of Average Ticket Counters and Queuing Space – E times F.

H. Divided by 365 – 365 days in year.

I. Divided by Average Turns Per Day – approximate average number of turns per day at Airport in current

Fiscal Year.

J. PER USE FEE – TICKET COUNTERS AND QUEUING – G divided by H divided I. Exhibit E-3 Line Items (Holdrooms/Gates):

A. Second Floor – Average Holdroom B Gate Size (square feet) – average leasable space of the second floor holdroom B gates and seating area space.

B. Saipan Main Terminal Rental Rate (per square foot) – Terminal Rental Rate calculated for the Saipan

Main Terminal in current Fiscal Year.

C. Total Cost of Shared Holdrooms/Gates – A times B.

D. Divided by 365 – 365 days in year.

E. Divided by Average Turns Per Day – approximate average number of turns per day at Airport in current Fiscal Year.

F. PER USE FEE – HOLDROOMS/GATES – C divided by D divided by E.

SMA App. 187

E-8

SECTION II – COST CENTERS E.6 Direct Cost and Revenue Centers. The Direct Cost and Revenue Centers include, but are not limited to, those Cost and Revenue Centers listed in Exhibit E-4 below.

Exhibit E-4. Direct Cost and Revenue Centers Cost and Revenue Center Description of Area Included or Functional Activity

Airfield All Capital Charges, all direct and indirect Operation and Maintenance Expenses, and Revenues for those portions of the Airport System provided for the landing, taking off, and taxiing of aircraft, including without limitation, approach and turning zones, aviation or other easements, runways, taxiways, runway and taxiway light, and other appurtenances in connection therewith and the aircraft parking and maneuvering areas adjacent to the Terminal and within its boundaries of areas designated for the parking of passenger aircraft and support vehicles as may be revised from time to time.

Terminal All Capital Charges, all direct, indirect, and general administrative Operation and Maintenance Expenses, and Revenues for the Commuter Terminal Building, Main Terminal Building, Rota Terminal Building, and Tinian Terminal Building and appending structures, law enforcement and security activities, paging systems, multi-user flight information display systems, and the terminal roadway systems including entrance/exit/recirculating roadways, terminal curb front, and taxi/bus/staging areas, but excluding roadways exclusively serving the public parking areas.

E.7 Indirect Cost Centers. The Indirect Cost Centers are Cost Centers to which only Operation and

Maintenance Expenses are assigned; no Revenues are attributable to the Indirect Cost Centers. The Indirect Cost Centers include, but are not limited to, those Cost Centers listed in Exhibit E-5 below.

Exhibit E-5. Indirect Cost Centers

Cost Centers Description of Area Included or Functional Activity Administrative Functions and activities associated with the general

administrative, accounting, and weather observer services of the Airport System.

Aircraft Rescue and Fire Fighting (ARFF) Functions and activities associated with emergency medical services and crash, fire and rescue operations the Airport System.

Operations Functions and activities associated with the general operations of the Airport System.

Security Functions and activities associated with security and police of the Airport System.

Indirect Cost Centers are allocated to Direct Cost and Revenue Centers based on an equitable distribution of costs.

SMA App. 188

Exhibit CPA-6

SMA App. 189

Regular Board of Directors Meeting August 22, 2017 - Minutes Page 8

In that regard, she was approached by Docomo Pacific for havin& free Wi~Fi service at the airport. So she asked a timeline as to when we could engage in the companies to discuss this with IT&E and Docomo. This will be an added benefit for the visitors.

There is currently free Wi-Fi in the Arrival Corridor by IT&E. Chair Tudela added that it is in the works and all we have to do locate space. Director Teves asked to always include Tinian and Rota in their discussions. Director Kim stated that the company mentioned the other airports too. They know that their airports are small and operations are low, but we want tourists to enjoy the other islands too.

Director Reyes asked why it was only proposed for the Arrival Area and not the Departure. Chris stated that the presentations will cover the entire airport terminals. Director Kim looks forward to those presentations.

Agenda No. VII OLD BUSINESS

Old Bus. Item I Echo Dock Request for Proposal (RFP)

The issue that they had that include public lands has been taken out. Director Reyes then made a motion to approve the RFP. Director Villagomez seconded it.

This area includes the former Seaman's restaurant. Since Kosa Fisheries vacated the area, Phoenix has been leasing it on a month-to-month. So the committee drafted the RFP that will solicit proposals that will include restaurants, berth space for luxury vessels. More nonindustrial and more for personal use vessels. The RFP solicit proposals to have them develop that area, including the dock plus berthing. Originally CPA was thinking that a collateral benefit was to improve the lower base beach between our facilities here and echo dock which is under DPL, but we crossed that out. The developer will need to comply with a whole bunch of regulations and work with D LNR, but that is all stated on the RFP. We look up to the proposers to come up with a robust plan.

The Board was then ready to vote and since there were no objections, the motion carried.

Agenda No. VIII New Business

New Bus. Item I Presentation by Robert Christian/Star Marianas

Mr. Christian first thanked the Board and announced that this is his first time ever to talk to the Board. He went over his history since he got here back in 1985. He reported that he brought Continental Airlines here and started Island Air in Hawaii. He teaches airline and airport management. His projects are airlines. He was asked by DOT to assist flight service to Rota and it was then when he started Pacific Island Aviation (PIA).

SMA App. 190

Regular Board of Directors Meeting August 22, 2017 - Minutes Page 9

Mr. Christian went over his mission statement because he feels that theirs is similar to CPA's. After they tried to retire, they were asked by the Tinian Dynasty in 2008 to come out and assist them. So they had a discussion with Taga Air and negotiated for them to surrender their certificate. This made Freedom Air the sole provider between Saipan and Tinian. He recommended that the Dynasty work with Freedom Air because they aware not interested in taking on another airline project. But that did not work.

In August 1008, they submitted documents to FAA and were granted certificate for Star Marianas Air. In February 2009, they signed the Signatory Agreement with CPA and flew between Saipan and Tinian using a single-engine carrier. They did not advertise and were solely here for the purpose of dragging Tinian Dynasty's customers back and forth. The Tinian Dynasty continued to rely on ferry.

From December 1009 to March 1010, in anticipation of the Dynasty's plan to discontinue the ferry, they acquired three (3) more Cherokees. Then in March 2010, the Tinian Dynasty suspended the ferry service. In August 2010, the military wanted to put live fire ranges on Tinian. That would have restricted airspace between Tinian and Saipan for single-engine aircrafts. So that made them purchase twin-engine aircrafts.

In May 2on, at the request of the Rota Mayor's Office, they started cargo service for them between Saipan, Rota and Guam. Freedom Air had already suspended their service for a month or so. So in May 2on, they signed an agreement with CPA for space on Rota. They paid $301 with utilities with no access to the back so all the cargo had to be processed, collected and taken to the west end of the building where they had access to the ramp. That is still the case today.

In August lOU, because of suspension of regular ferry service, they had to store fuel on Saipan. Before that, they were storing on Tinian. And after several months of discussion, they were at the point where they had to stop flying if they could not come to an agreement with CPA. So SMA was eventually allowed to store fuel that they flew in from the states in 6,ooo gallon isotainers on Saipan. He noted that they have eight to nine isotainers at any one time to make sure that they do not run out of gas. It costs about $40,000 to $6o,ooo and are subject to landing fees, etc. They also had to write a secondary spill program and get the berms up because there is no suitable facility on any of the islands. So it created operational problems because they were not allowed to park it on the tarmac thus were situated at the long-term parking area at the Saipan Airport. There were some safety and other issues which is what they were discussing with CPA, but after three years, they are now allowed to store them on the Airside Operation Area (AOA).

At the request of the Tinian Mayor's Office in December 1on, SMA started allowing residents to fly on their "repo" flights. They flew a whole bunch of flights to Tinian even during late hours. Then they are forced to bring the planes to Saipan back empty. So the Mayor's Office asked again for help to fly customers, but they did not want to give times of when they were flying because that would require publishing a schedule and they were not doing that. So the locals started coming and everyone was charged a $10 service charge.

SMA App. 191

Regular Board of Directors Meeting August 22, 2017- Minutes Page 10

They loved it. But on December Z-41 they received a letter from CPA that we were supposed to be collecting Passenger Facility Charges (PFC} on these flights, but we were never given notice. He stated that they were not revenue flights but just repo flights. Mr. Christian did not think that they should not have been subjected even if they were qualifying and required to do the PFC's. But CPA said that SMA owed them $350,ooo with no notice. So they met with CPA to try to resolve the issue, namely former Comptroller Derek Sasamoto, but that did not go well because CPA legal counsel informed them on April 12, if they did not pay $42.710001 they were going to evict SMA. So they raised that issue. It eventually went to the FAA and the FAA came back saying that notice was given and was not correct. The CPA then took a hostile position which basically said that they are of view that SMA does not think they need to collect PFC's and disclaim responsibility, SMA has a duty to collect PFCs and remit only by its own backwards self·serving logic, because they said that if they did not collect it, then SMA does not owe CPA. But the CPA legal counsel says that they chose humorous logic and that they will pursue it to its conclusion along with Freedom Air. He added that when CPA pursued Freedom Air, Freedom Air actually collected the $6oo,ooo PFC's which were not remitted to CPA. So this is where it took a turn.

They then raised the issue of having been assessed Head Charges, Facility Service Charges on per head charges when it was not being tied back to the other requirements on Section 7 of the AUA. This has been ongoing since 2.012.. They did not talk to CPA about it because they hoped that they could resolve it. So they were again threatened with the eviction on June 13. They then contacted the FAA Regional Office because SMA was not making progress. So on July 31 20121 the DOT found that they were fit, willing and able meaning that their management, financials and compliance with federal laws were looked at to do scheduled flights. It was then when they became a regional carrier to do scheduled flights. So on February 2.013, they started doing passenger charter service to Rota. They were again assessed $4·95 for the rental space for each person that they took to Rota on those chartered flights and still had no access to the ramps and take their passengers through the Arrival Area. So the customers check in at the counters in the Departure Area and then go to the Arrival Area. When Cape Air is there, they have to wait. At that time, Freedom Air was still operating so they had airside access.

On March 2.013, CPA informed them that FAA agreed with their position of the PFCs that CPA will not pursue the $42.01ooo that CPA demanded they pay. So in July 2.013, they began writing on every check that they were submitting to CPA that they were writing this "under protest" because CPA has not addressed the requirement to determine cost and adjust the cost annually.

In September 2.013, Freedom Air filed bankruptcy and CPA was a major creditor for the $6o9,ooo PFCs collected from the passengers. In August 2.014, they started scheduled flight service to Rota. SMA was denied access to Guam which made them take on Guam. Eventually the FAA intervened and required that the Guam International Airport Authority (GIAA) build something for them, so they built the Light Aircraft Terminal Facility. For 4oo,ooo square feet, they are charged $500 a month, with no PFCs. After March 2.015, with no progress on their contention that they are being overcharged for the landing fees, they stopped paying. They turned over the PFCs and still do because it is the public's money. So

SMA App. 192

Regular Board of Directors Meeting August 22, 2017- Minutes Page 11

they start the Guam flight to Rota. He then went on about the charges that the CPA was assessing: For the month of February 2016, they were charged $U.J,ooo ($531000 for the PFC's but another $7o,ooo for space).

So on March 2016, The Dynasty stopped its operation and saw a huge economic consequence to the people of Tinian, so they boosted their Discovery flights for the Chinese to subsidize some of the overhead cost associated with the operations and managed to keep the prices the same as when they started in zooS ($42 one way).

Finally, in July 2016, after several meetings with CPA and Ricondo, Ricondo informed that CPA is changing their methodology for assessing the fees. CPA is now going per square foot charge for preferential space assessing common use space based on a percentage of enplaned. And they are eliminating signatory rates for landing fees. They were presented with a letter on August 216, wherein Ricondo said that they used this methodology and computed from 2009 what could have been charged and determined that CPA overcharged SMA. But in July 2017, they get another letter wherein they used the new methodology, that they undercharged by $11200. He understands that there are good and bad days. So he wants to know how it got to this point when they are supposed to be on the same boat.

He pointed out Chapter u is good because it is appropriate in charging for different airlines. Then they look at Ricondo's methodology referring to the Commercial Compensatory Rate and compare it and it looks consistent with Chapter n. Ricondo also used an equalized methodology of taking all of the costs of the airports, wrapping it into one and using the percentage of what the commuter should be. SMA did not dispute from the get go that the AU A was absolutely ok. They only disputed that it was not being followed. They also do not dispute that Ricondo's methodology is something you can do, but they do look at something that CPA should do. There is a broad range of opportunities to assess charges and if we go back to our mission statements, he questioned if we using Ricondo to really develop transportation to its fullest. He welcomes Ricondo to look at an alternative method that would result in lower fees and compare. CPA has a lot of other revenues from other activities going on here from the Chinese flights coming in. SMA has more revenue because of their Discover flights. They are willing to use the money from those flights to help subsidize to Tinian and Rota to keep those prices stable. He suggests that if we all do not look at ways to keep our rates stable, he will need to make adjustments accordingly. If we could take another look to see what could he done to take the burden off of transportation to and from these outer islands, he pleads to let us make our money that way, but just keep the cost low. Because if not, we have minimum wage increases coming up, insurance costs, legal fees, etc. He again asked to work together to keep the costs low. He is only interested in seeing if this is something you would do. He then thanked the Board for their time.

Normally, because this falls under his committee, Director Teves makes dosing remarks, but this time because SMA has filed a case against CPA, he is reserving his comments. In response to that, Mr. Christian stated that they actually asked CPA to sue SMA first. SMA was thanked for their comments. Mr. Christian ended by saying that he hopes to meet [with the Board] more often rather than once every zo years.

SMA App. 193

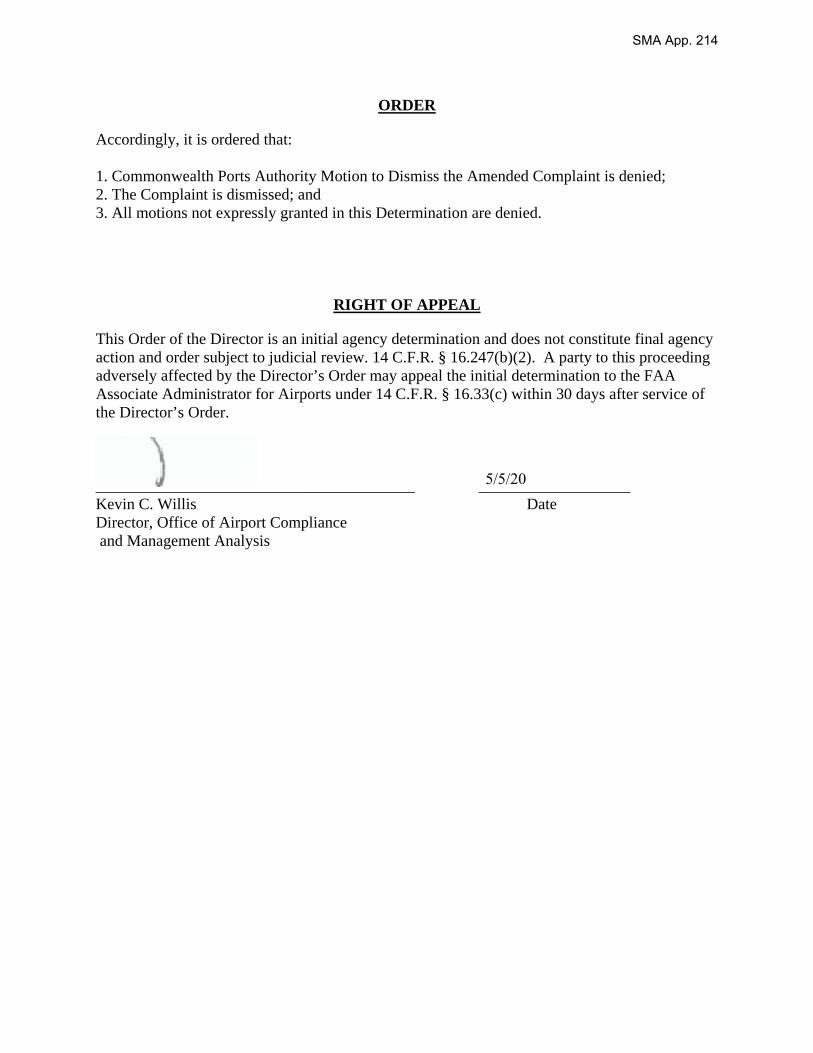

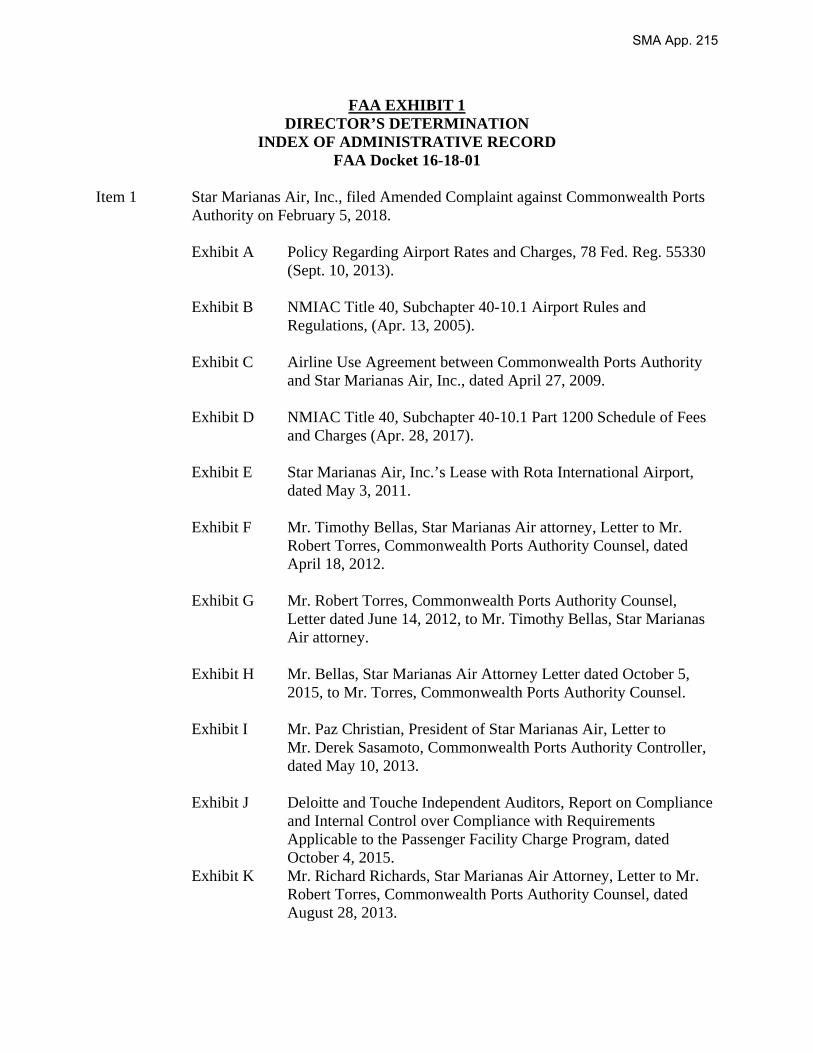

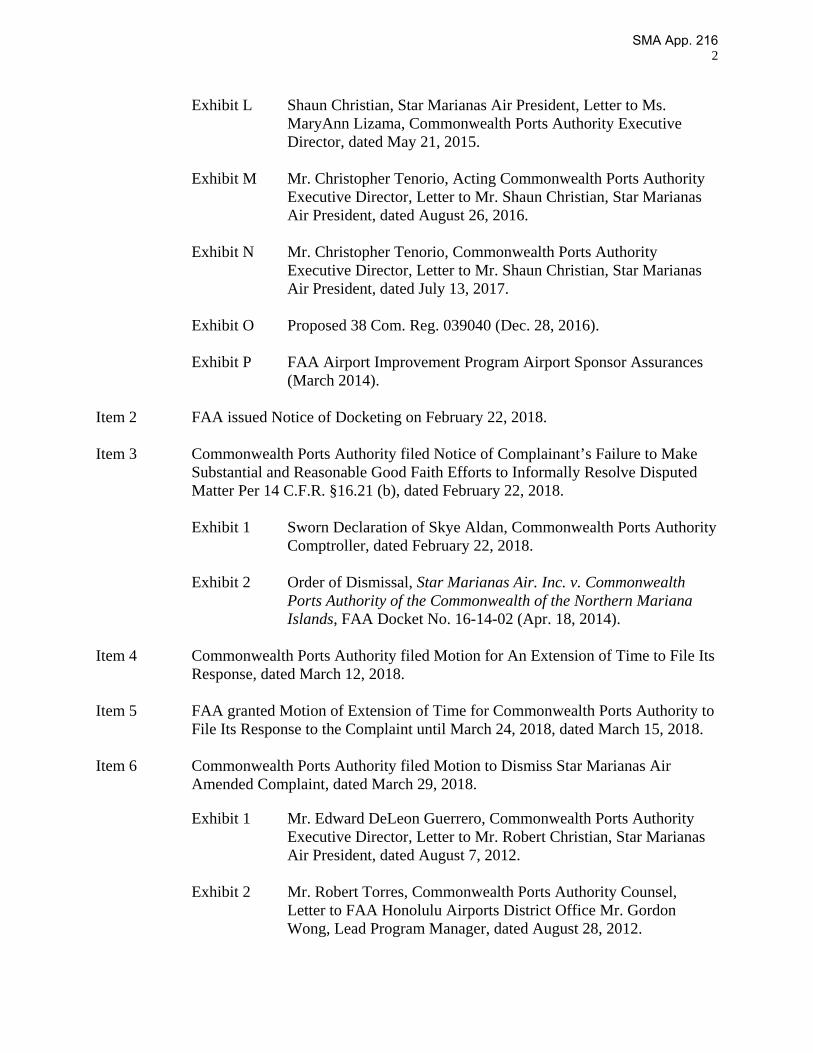

Exhibit CPA-7

SMA App. 194

Office of Airport Compliance and Management Analysis

800 Independence Ave, SW. Washington, DC 20591

Mr. Richard L. Richards Jason Goldstein Richards Goldstein LLP 55 Miracle Mile, Suite 310 Coral Gables, Florida 33134 [email protected][email protected] Mr. Robert T. Torres, Esq. Law Offices of Robert T. Torres Plata Drive, Whispering Palms (Chalan Kiya) P.O. Box 503758 CK Saipan, MP 96950 [email protected] Dear Messrs. Richards, Goldstein, and Torres: Re: Star Marianas Air, Inc. v. Commonwealth Ports Authority, Commonwealth of the

Northern Marianas Islands, FAA Docket No. 16-18-01 Enclosed is a copy of the Order of the Director issued in the above-referenced matter. The complaint is dismissed, and the reason for dismissal are set forth in the enclosed Order. This Order is an initial agency determination and does not constitute a final decision, and this Order is subject to judicial review. 14 CFR § 16.247(b)(2). A party adversely affected by the Director’s Order may appeal the initial determination to the FAA Associate Administrator for Airports under 14 CFR § 16.33(c) within 30 days after the service of the Director’s Order. Sincerely, Kevin C. Willis Director, Office of Airport Compliance and Management Analysis Enclosure

SMA App. 195

Viola E-CTR Cijntje

Stamp

UNITED STATES DEPARTMENT OF TRANSPORTATION FEDERAL AVIATION ADMINISTRATION

WASHINGTON, DC ____________________________________________ Star Marianas Air, Inc.,

Complainant, v. FAA Docket No. 16-18-01 Commonwealth Ports Authority,

This matter is before the Federal Aviation Administration (FAA) on the complaint filed by Star Marianas Air, Inc., against the Commonwealth Ports Authority, under the FAA’s Rules of Practice for Federally Assisted Airport Enforcement Proceedings, 14 C.F.R. part 16. Star Marianas Air, Inc., (Complainant or Star Marianas) filed a Complaint under part 16 against the Commonwealth Ports Authority (Respondent or Ports Authority), owner and operator of the airports in the Commonwealth of the Northern Marianas Islands (CNMI or Commonwealth).

Star Marianas contended that Ports Authority is operating CNMI airports in a discriminatory manner by imposing excessive, unreasonable, and discriminatory charges, including head taxes without any basis or support (FAA Exhibit 1, Item 1, pp. 1-6). Star Marianas further stated that these charges do not relate to the Ports Authority's costs and result in revenue surpluses (FAA Exhibit 1, Item 1, pp. 1-2). Finally, Star Marianas alleged that the Ports Authority permits airside access at one of the Ports Authority terminals (Rota Airport) to Star Marianas' competitors, while denying Star Marianas the same or similar access (FAA Exhibit 1, Item 1, p. 6).

Ports Authority denied the allegations (FAA Exhibit 1, Item 6, and FAA Exhibit 1, Item 10). Ports Authority responded that it applied the ratemaking methodology consistently to all airlines operating at the three airports, in conformance with the Department of Transportation Rates and Charges Policy (78 Fed. Reg. 55330 (Sept. 10, 2013)), and it consults with the airlines on the proposed rates and charges, and fees (FAA Exhibit 1, Item 10, p. 37). Ports Authority differentiated the rates so that the airlines with fewer passengers and smaller aircraft, operating at the Saipan Commuter, Rota, and Tinian terminals, pay less than the airlines in the Saipan International Terminal Building (FAA Exhibit 1, Item 10, p. 30). Ports Authority admitted that final rates and charges calculations for fiscal years 2009-2014 were reconciled in 2016, and it provided refunds to individual airlines (FAA Exhibit 1, Item 10, p. 37).

As discussed below, the Director dismisses the Complaint. The Director also denies all motions.

SMA App. 196

2

II. PARTIES

Complainant

Star Marianas is a CNMI corporation. It operates as a FAA certificated air carrier conducting scheduled and on-demand passenger and cargo operations between the islands of Tinian, Rota, Saipan, and Guam (FAA Exhibit 1, Item 1, pp. 6-7). Star Marianas operates twelve aircraft – 7 single engine and 5 multi-engine aircraft (FAA Exhibit 1, Item 19).

Airport

Ports Authority is an autonomous, public, CNMI corporation. It is the owner, operator, and sponsor of the CNMI public airports, including Saipan International Airport, Rota International Airport, and Tinian International Airport (FAA Exhibit 1, Item 1, pp. 2-3). These airports were developed using FAA Airport Improvement Program (AIP) grants, authorized by the Airport and Airway Improvement Act of 1982, as amended, Title 49 U.S.C. § 47101, et seq. Since 1982, Ports Authority has accepted more than $246,470,368. The most recent AIP grants were in 2019 (FAA Exhibit 1, Item 24, and FAA Exhibit 1, Item 25, and FAA Exhibit 1, Item 26).

III. PROCEDURAL HISTORY AND BACKGROUND

A. Procedural History

See Index of Administrative Record.

B. Background

April 27, 2009 Star Marianas and Ports Authority executed an Airline Use Agreement (AUA) (FAA Exhibit 1, Item 1, p. 7, and FAA Exhibit 1, Item 1, Exhibit C).

May 2011 Star Marianas signed a lease with Ports Authority for use of 344 square feet of preferential use premises at Rota Airport and 233 square feet at Tinian Airport (FAA Exhibit 1, Item 1, p. 8, and FAA Exhibit 1, Item 1, Exhibit C). Star Marianas paid $302 in monthly rent, which included utilities. The preferential use premises did not have direct access to the ramp, so all the cargo had to be processed, collected, and taken to the west end of the Rota terminal where Star Marianas could access the ramp (FAA Exhibit 1, Item 7, Exhibit 25, p. 9).

December 2011 Star Marianas allowed residents to fly on their reposition flights between Tinian and Rota Airports at the request of the Tinian Mayor’s office. This request was due to the limited access to fast transportation between the two islands. Star Marianas charged a $10 service charge to the passengers (Exhibit 1, Item 7, Exhibit 25, p. 10).

SMA App. 197

3

December 4, 2011 Ports Authority notified Star Marianas for failure to remit $350,000 in Passenger Facility Charges (PFCs) to Ports Authority (FAA Exhibit 1, Item 1, p. 12).

July 31, 2012 FAA certified Star Marianas as a regional carrier to conduct scheduled

flights (Exhibit 1, Item 7, Exhibit 25, p. 10).

September 4, 2012 Ports Authority requested Honolulu Airports District Office (HON ADO) to review whether the methodology of assessing charges on a per-passenger basis for the use of the airport facility rental and facility charges violated the Anti-Head Tax Act (FAA Exhibit 1, Item 6, Exhibit 3).

January 3, 2013 HON ADO responded to a Ports Authority written request. HON ADO informed Ports Authority that its methodology of establishing terminal rents does not represent an illegal head tax. However, HON ADO suggested that Ports Authority change the terminology in the airport rate agreement to avoid the incorrect representation that the fees are a head tax (FAA Exhibit 1, FAA Item 6, Exhibit 5).

February 19, 2013 HON ADO responded to a Ports Authority letter concerning Star Marianas alleged failure to remit Passenger Facility Charges (PFCs). HON ADO informed Ports Authority that the airline use agreement was insufficient to provide the required notice under 14 C.F.R. part 158 (FAA Exhibit 1, Item 7, Exhibit 6).

February 20, 2013 Star Marianas began passenger service to Rota. Ports Authority claims that it notified Star Marianas of a $4.95 departure facility charge imposed on each ticket originating at Rota (Exhibit 1, Item 7, Exhibit 25, p. 10; NMIAC § 40-10.1-1215). Star Marianas passengers check in at the departure area and then moved to the arrival area to board the aircraft (Exhibit 1, Item 7, Exhibit 25, p. 10).

March 8, 2013 Star Marianas claimed that Ports Authority informed Star Marianas that FAA agreed with Star Marianas’ position regarding the lack of PFC public notice, and Star Marianas did not have to remit $427,919 in unremitted PFCs to Ports Authority (FAA Exhibit 1, Item 1, p. 13).

July 2013 Star Marianas began writing “under protest” on every check submitted to Ports Authority because Star Marianas claimed Ports Authority had not addressed the requirements to determine costs and to adjust the costs annually (FAA Exhibit 1, Item 7, Exhibit 25, p. 10).

October 2, 2013 HON ADO informed Ports Authority that the FAA was aware that Ports Authority had failed to comply with requirements related to PFC collection and that, as a result, an airline had failed to remit PFCs and airline use fees for two years. The FAA stated that Ports Authority needed

SMA App. 198

4

to address its noncompliance within 30 days (FAA Exhibit 1, Item 6, Exhibit 7).

November 18, 2013 Ports Authority responded to HON ADO’s letter of October 2, 2013 (FAA

Exhibit 1, FAA Item 6, Exhibit 9). Ports Authority detailed several corrective actions already taken and under consideration including updating the rate study for the PFCs, and the retention of Ricondo and Associates (Ricondo) to help answer specific questions or concerns by tenants (FAA Exhibit 1, Item 6, Exhibit 9).

December 6, 2014 Ricondo entered into a Professional Services Contract with Ports Authority. Ricondo contractually agreed to provide Ports Authority an updated airports rates and charges study, and conduct rates and charges training to Ports Authority accounting staff (FAA Exhibit 1, Item 6, Exhibit 12).

July 19, 2016 Ports Authority and Ricondo met with Star Marianas to discuss Ports Authority changing their rates and charges methodology for assessing the fees (FAA Exhibit 1, Item 6, Exhibit 16).

August 26, 2016 Ports Authority presented Star Marianas with a letter. In the letter, Ricondo wrote that they used Ports Authority’s new airport rates and charges methodology and reconciled Star Marianas rates and charges between fiscal years 2009 - 2014. That letter claimed Ports Authority overcharged Star Marianas by $101,729 (FAA Exhibit 1, Item 1, Exhibit M, and FAA Exhibit 1, Item 6, Exhibit 17).

December 28, 2016 Ports Authority published proposed amendments in the Commonwealth Register to update the existing Airport Rules and Regulations governing the establishment of its Airport fees. The proposed revisions removed Fees for Non-Signatory Carriers; updated the Landing Fees; revised Departure Facility Service Charges to the Terminal Rental Rate; revised the International Arrival Facility Service Charge to Per Use Fees; and updated the Public Parking Fees (FAA Exhibit 1, Item 1, Exhibit O).

July 13, 2017 Star Marianas received a letter from Ports Authority stating Star Marianas owed Ports Authority $12,708 for FY 2015. Ports Authority offered Star Marianas to use its credit of $101,729. Ports Authority also requested that Star Marianas provide direction to Ports Authority as to how to handle its balance of $89,021 (FAA Exhibit 1, Item 1, Exhibit N).

August 1, 2017 Star Marianas filed a civil complaint, Docket No. 17-00012, in the U.S. District Court for the Northern Marianas Islands against Ports Authority. Star Marianas accused Ports Authority of breach of contract, violating the Anti-Head Tax Act (49 U.S.C. § 40116), and establishing unreasonable user fees for Star Marianas. Star Marianas alleged that the user fees were

SMA App. 199

5

not related to the requirements in Section 7 of the AUA (Exhibit 1, Item 7, Exhibit 25, p. 9).

February 21, 2018 Star Marianas received a letter from Ports Authority that stated Star

Marianas owed $117,061 to Ports Authority for FY 2016. Ports Authority deducted $117,061 from Star Marianas’ remaining balance of $89,021 from FY 2009-2014, resulting in Star Marianas owing $27,994 for FY 2016 (FAA Exhibit 1, Item 14, Exhibit 1).

IV. FAA POLICY AND GUIDANCE

A. The Airport Improvement Program