27

Walgreens vs CVS Caremark Financial Analysis By: Sunil Motwani

| Date post: | 15-Apr-2017 |

| Category: |

Documents |

| Upload: | sunny-motwani |

| View: | 218 times |

| Download: | 0 times |

Walgreens vs CVS Caremark Financial Analysis

By: Sunil Motwani

Introduction

The two corporations I will be comparing in this financial analysis are the two

largest pharmacy retailers in the drug store industry, Walgreens (WAG) and CVS

Caremark (CVS). Both companies provide high quality pharmacy health care while

serving as a convince store for everyday items. The main goal for each business is to

help their patients and customers by enhancing access to care, lowering costs, and

improving overall health outcomes. They do this by having a store on every corner to

succeed in making sure all customers can conveniently and easily get the medication

needed for their health.

The analysis will first look at the history, as well as any recent news stories for

each company. Next, a table will be shown of the Income Statement and Balance Sheet

for each company in order to show the real difference in how each company allocates

their money. This will also illustrate to us which of the two companies has more revenue

and net profit within the drug store industry. Line graphs of the most recent five year

stock prices will also be shown as well as each companies returns compared to the S&P

500 index. The true financial analysis of whether or not the company is worth investing

in comes next with the financial ratios. The ratios will include liquidity ratios, debt

management ratios, asset management ratios, profitability ratios, and market valuation

ratios. After the ratios, we will close up with the DuPont analysis which helps determine

how well each company creates value and makes it simple for an analyst, and even a

simple investor, to compare the valuation and returns with each other and within the

industry as a whole.

CVS Common Size Analysis – Income Statement

Walgreens Common Size Analysis – Income Statement

12 months ended Aug 31, 2013 Aug 31, 2012 Aug 31, 2011

Net sales 100.00% 100.00% 100.00%

Cost of sales -70.76% -71.60% -71.61%

Gross profit 29.24% 28.40% 28.39%

Selling, general and administrative expenses -24.29% -23.56% -22.94%

Gain on sale of business 0.03% – 0.60%

Equity earnings in Alliance Boots 0.48% – –

Operating income 5.46% 4.84% 6.05%

Interest expense, net -0.23% -0.12% -0.10%

Other income 0.17% – –

Earnings before income tax provision 5.39% 4.71% 5.95%

Income tax provision -2.00% -1.74% -2.19%

Net earnings 3.39% 2.97% 3.76%

12 months ended Dec 31, 2013

Dec 31, 2012

Dec 31, 2011

2013 (CS)

2012 (CS)

2011 (CS)

Net revenues 126,761 123,133 107,100 100% 100% Cost of revenues -102,978 -100,627 -86,539 -81.24% -81.72% -80.80%

Gross profit 23,783 22,506 20,561 18.76% 18.28% 19.20% Operating expenses -15,746 -15,278 -14,231 -12.42% -12.41% -13.29%

Operating profit 8,037 7,228 6,330 6.34% 5.87% 5.91% Interest expense -517 -561 -588 -0.41% -0.46% -0.55% Interest income 8 4 4 0.01% 0.00% 0.00%

Interest expense, net -509 -557 -584 -0.40% -0.45% -0.55% Loss on early extinguishment of debt – -348 –

-0.28% Income before income tax

provision 7,528 6,323 5,746 5.94% 5.14% 5.37% Income tax provision -2,928 -2,441 -2,258 -2.31% -1.98% -2.11%

Income from continuing operations 4,600 3,882 3,488 3.63% 3.15% 3.26% Loss from discontinued operations, net of tax -8 -7 -31 -0.01% -0.01% -0.03%

Net income 4,592 3,875 3,457 3.62% 3.15% 3.23% Net loss attributable to noncontrolling interest – 2 4

0.00% 0.00%

Net income attributable to CVS Caremark 4,592 3,877 3,461 3.62% 3.15% 3.23%

Source: CVS Caremark Corp., Annual

Reports

Walgreens History

Beginning in 1901, Walgreens opened its first store in the city of Chicago on the

intersection of Bowen Avenue and Cottage Grove. The store was run by Charles R.

Walgreen and about 15 years later in 1915, the city had five stores with more every year.

The 1920s was a very busy time for the chain as hundreds of locations were being built

all over the United States. Popularity increased tremendously when Walgreen invented

the malted milkshake. Another reason the 20s was a very successful year for the

company is due to the fact that in 1927 Walgreen Co. stock went public and by 1930 they

had about 400 locations with annual sales above $4,000,000. As more stores were being

built, in 1950 the company began to build self-service stores and by 1953 they were the

largest self-service retailer in the country. The 60s were a proud decade for Walgreens,

by the beginning of the decade they entered into the Puerto Rican market and filled their

100 millionth prescription. They also became the first major drug chain to put the

prescriptions into child resistant containers even though it wasn't required by the federal

government yet. In the year 1975, the company reached a milestone of $1 billion in

sales. With the 80s and 90s being so focused on computer technology, they started to

install intercom computers in all Walgreens so they could connect to every pharmacy via

satellite. They even offered next day photofinishing by 1982 and by 1984 they opened

their 1000th store. The 90s brought more technology to the company when they added

point of sale scanning to speed checkouts. Due to this they even opened a drive-thru

pharmacy by 1992. By 1994 the company had reached 2000 stores. Walgreens was

ahead of the game with the .com boom in the 2000s and by 1999 they launched

walgreens.com allowing customers to view their prescriptions safely online. 10 years

later they made a presence in all 50 states when opening their first pharmacy in Alaska.

Today, Walgreens has over 7,000 stores nationwide and to keep up with government

regulations and their social responsibility, they have started putting solar panels on the

roofs of their stores and are planning to add thousands of charging stations for electric

cars.

CVS Caremark History

CVS was and currently still is the fasted growing pharmacy retailer to exist. Even though

Walgreens has been around for over 100 years, CVS has a little over 40 years in the business and

with the same amount of stores. The first store opened in 1963 in the city of Lowell, MA. In the

year 1996 the company Melville Corporation took the CVS Caremark symbol to the stock

market and made it public. From the 80s till today it has been buying over local small pharmacy

chains in order to build its name and value. By 2000, CVS had over 4000 stores nationwide.

2006 was a big year for the company as they announced their MinuteClinic. This made CVS the

first ever retail store to offer certified doctors to customers for a routine checkup and they could

be prescribed their medication right in the store. CVS has been a big game changer ever since it

first started and they have no signs of disappearing. With over 7,400 stores the chain has grew

and taken over all competitions expect Walgreens and a little bit of Rite Aid. This pharmacy

retailer is also a big seller in cosmetics and in 2008 they started another store which they have

been putting right next to all CVS’s as part of their beauty campaign.

Walgreens Recent Developments

In March of 2008 Walgreens had to settle a lawsuit with the Equal Employment

Opportunity Commission due to the alleged accusations that the company discriminated against

African Americans. The settlement was for $24 Million and was split among 10,000 Afrian

American employees of the company. Walgreens did not plead guilty. In the same year in June,

Walgreens was accused of switching the dosage forms on three medications prescribed for

Medicaid patients without doctor approvals in order to boost profits. The company had to pay

$35 million to the federal government because all the Medicaid programs nationwide had to pay

much more than they normally would have to. In 2012, Walgreens was in trouble with the DEA

for not following the rules of transportation of Oxycodone. The retailer caused thousands of pills

to be misplaced causing the DEA and public to fear they are now being sold on the streets of the

black market. Finally, Walgreens would not stop the sale of Tabacco products as they made a

big profit from it while their competitor CVS banned tabcacco products from their stores.

CVS Recent Developments

CVS has had their shares of trouble. From 2000-2003 CVS execs were charged with

bribery by the federal grand jury for paying a state senator to act as a consultant for the company

and paid him $1000 a month which he would spend on his travel and golf outings. Like every

company nowadays, CVS was sued in 2007 for illegally dumping confidential patient

information and settled with $315,000 to the state. The biggest lawsuit came in 2008 for

deceptive business practices when the company tried telling insurance companies to cover the

brand name medications which would bring almost double the money to CVS while costing the

consumer the same amount. They settled for a whopping $39 million. But that’s not their

biggest, CVS had to pay up $77.6 million in fines due to the improper control in the sale of an

ingredient used to make methamphetamine. Lastly some good news, CVS announced in 2014

they will not sell any more tobacco products which takes away $1.5 billion in revenue a year for

the company.

Appendix: Return/Price Data

Date CVS Stock

Price Walgreens Stock

Price CVS Returns

Walgreens Returns

S&P Adj Close

S&P Returns

6/2/14 76.32 73.73 1949.98

5/1/14 78.32 71.91 2.62% -2.47% 1923.57 -1.35%

4/1/14 72.72 67.58 -7.15% -6.02% 1883.95 -2.06%

3/3/14 74.58 65.72 2.56% -2.75% 1872.34 -0.62%

2/3/14 72.87 67.63 -2.29% 2.91% 1859.45 -0.69%

1/2/14 67.47 56.81 -7.41% -16.00% 1782.59 -4.13%

12/2/13 71.02 56.9 5.26% 0.16% 1848.36 3.69%

11/1/13 66.44 58.64 -6.45% 3.06% 1805.81 -2.30%

10/1/13 61.78 58.38 -7.01% -0.44% 1756.54 -2.73%

9/3/13 56.1 53.02 -9.19% -9.18% 1681.55 -4.27%

8/1/13 57.38 47.37 2.28% -10.66% 1632.97 -2.89%

7/1/13 60.78 49.2 5.93% 3.86% 1685.73 3.23%

6/3/13 56.31 43.28 -7.35% -12.03% 1606.28 -4.71%

5/1/13 56.71 46.76 0.71% 8.04% 1630.74 1.52%

4/1/13 57.3 48.2 1.04% 3.08% 1597.57 -2.03%

3/1/13 53.94 46.42 -5.86% -3.69% 1569.19 -1.78%

2/1/13 50.15 39.86 -7.03% -14.13% 1514.68 -3.47%

1/2/13 50.22 38.65 0.14% -3.04% 1498.11 -1.09%

12/3/12 47.22 35.8 -5.97% -7.37% 1426.19 -4.80%

11/1/12 45.43 32.8 -3.79% -8.38% 1416.18 -0.70%

10/1/12 45.32 33.8 -0.24% 3.05% 1412.16 -0.28%

9/4/12 47.13 34.96 3.99% 3.43% 1440.67 2.02%

8/1/12 44.33 34.31 -5.94% -1.86% 1406.58 -2.37%

7/2/12 44.04 34.62 -0.65% 0.90% 1379.32 -1.94%

6/1/12 45.33 28.16 2.93% -18.66% 1362.16 -1.24%

5/1/12 43.59 29.06 -3.84% 3.20% 1310.33 -3.80%

4/2/12 43.28 33.15 -0.71% 14.07% 1397.91 6.68%

3/1/12 43.29 31.66 0.02% -4.49% 1408.47 0.76%

2/1/12 43.58 31.35 0.67% -0.98% 1365.68 -3.04%

1/3/12 40.35 31.34 -7.41% -0.03% 1312.41 -3.90%

12/1/11 39.26 31.05 -2.70% -0.93% 1257.6 -4.18%

11/1/11 37.39 31.67 -4.76% 2.00% 1246.96 -0.85%

10/3/11 34.98 30.98 -6.45% -2.18% 1253.3 0.51%

9/1/11 32.22 30.69 -7.89% -0.94% 1131.42 -9.72%

8/1/11 34.45 32.85 6.92% 7.04% 1218.89 7.73%

7/1/11 34.87 36.2 1.22% 10.20% 1292.28 6.02%

6/1/11 35.93 39.38 3.04% 8.78% 1320.64 2.19%

5/2/11 36.99 40.46 2.95% 2.74% 1345.2 1.86%

4/1/11 34.63 39.46 -6.38% -2.47% 1363.61 1.37%

3/1/11 32.7 37.08 -5.57% -6.03% 1325.83 -2.77%

2/1/11 31.5 40.03 -3.67% 7.96% 1327.22 0.10%

1/3/11 32.58 37.2 3.43% -7.07% 1286.12 -3.10%

12/1/10 33.01 35.84 1.32% -3.66% 1257.64 -2.21%

11/1/10 29.43 32.06 -10.85% -10.55% 1180.55 -6.13%

10/1/10 28.6 31.01 -2.82% -3.28% 1183.26 0.23%

9/1/10 29.79 30.66 4.16% -1.13% 1141.2 -3.55%

8/2/10 25.54 24.6 -14.27% -19.77% 1049.33 -8.05%

7/1/10 29.05 25.97 13.74% 5.57% 1101.6 4.98%

6/1/10 27.67 24.29 -4.75% -6.47% 1030.71 -6.44%

5/3/10 32.69 29.14 18.14% 19.97% 1089.41 5.70%

4/1/10 34.85 31.85 6.61% 9.30% 1186.69 8.93%

3/1/10 34.43 33.61 -1.21% 5.53% 1169.43 -1.45%

2/1/10 31.78 31.93 -7.70% -5.00% 1104.49 -5.55%

1/4/10 30.48 32.53 -4.09% 1.88% 1073.87 -2.77%

12/1/09 30.25 33.14 -0.75% 1.88% 1115.1 3.84%

11/2/09 29.12 35.09 -3.74% 5.88% 1095.63 -1.75%

10/1/09 33.15 34.02 13.84% -3.05% 1036.19 -5.43%

9/1/09 33.5 33.69 1.06% -0.97% 1057.08 2.02%

8/3/09 35.17 30.47 4.99% -9.56% 1020.62 -3.45%

7/1/09 31.38 27.8 -10.78% -8.76% 987.48 -3.25%

6/22/09 29.8 26.32 -5.04% -5.32% 919.32 -6.90%

Liquidity Ratios *All $ in Thousands

CURRRENT RATIO = Current Assets/ Current Liabilities

Current Assets Current Liabilities Current Ratio

CVS

2013 $25,325,000 $15,425,000 1.64

2012 $20,161,000 $14,150,000 1.42

Walgreens

2013 $ 11,874,000 $8,883.00 1.34

2012 $10,760,000 $8,722.00 1.23

Industry 1.26

The first ratio one usually looks at when making the decision of whether or not to invest

in a certain company is the current ratio. The ratio is found by taking the companies current

assets and dividing them by its current liabilities. This ratio helps investors determine if the

company is capable to pay back their short-term assets. When the current ratio is higher, it

means that the company is in a better shape to pay off the assets. On average, it would be

considered financially unhealthy if the current ratio was less than 1 however, it varies from

industry to industry.

The current ratio table above shows CVS & Walgreens both have current ratios greater than

one, which means both companies are capable of paying back their short-term liabilities with

their short-term assets. They both have $ higher than the industry average as well which means

they are averagely doing better than the industry.

If the current ratio fell below one this would mean that the corporation’s current liabilities are

greater than their current assets. The current ratio can give a sense of the efficiency of a

company's operating cycle or its ability to turn its product into cash.

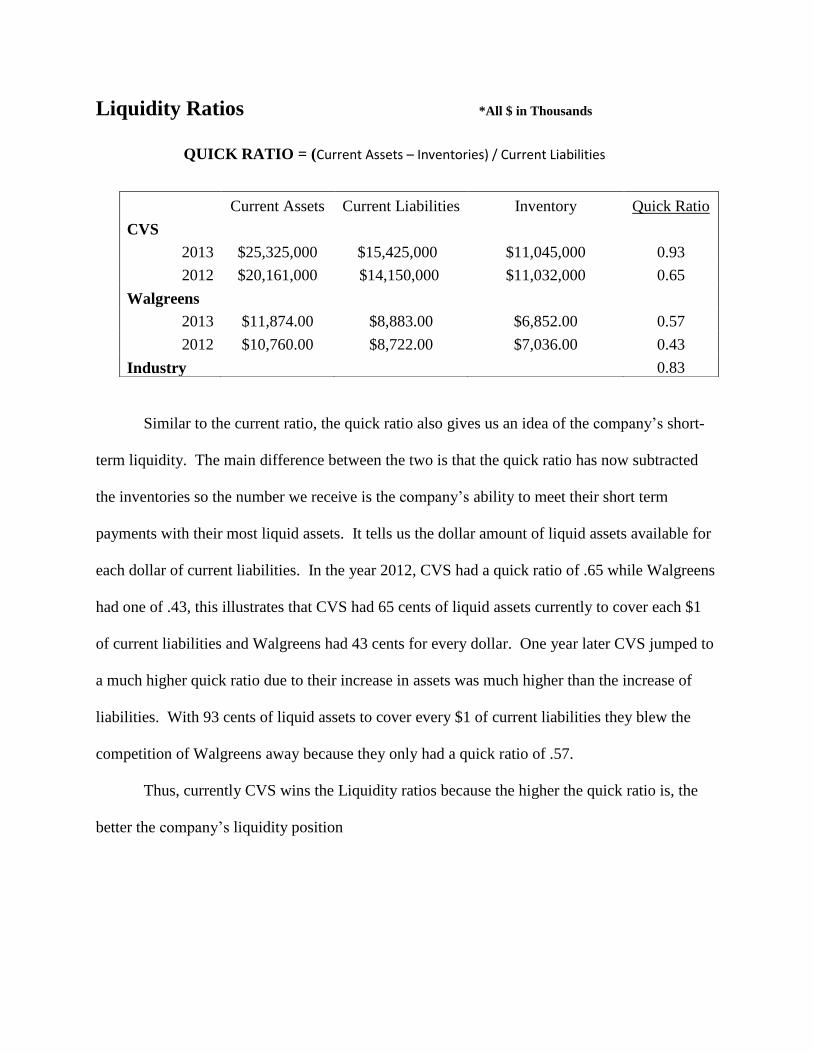

Liquidity Ratios *All $ in Thousands

QUICK RATIO = (Current Assets – Inventories) / Current Liabilities

Similar to the current ratio, the quick ratio also gives us an idea of the company’s short-

term liquidity. The main difference between the two is that the quick ratio has now subtracted

the inventories so the number we receive is the company’s ability to meet their short term

payments with their most liquid assets. It tells us the dollar amount of liquid assets available for

each dollar of current liabilities. In the year 2012, CVS had a quick ratio of .65 while Walgreens

had one of .43, this illustrates that CVS had 65 cents of liquid assets currently to cover each $1

of current liabilities and Walgreens had 43 cents for every dollar. One year later CVS jumped to

a much higher quick ratio due to their increase in assets was much higher than the increase of

liabilities. With 93 cents of liquid assets to cover every $1 of current liabilities they blew the

competition of Walgreens away because they only had a quick ratio of .57.

Thus, currently CVS wins the Liquidity ratios because the higher the quick ratio is, the

better the company’s liquidity position

Current Assets Current Liabilities Inventory Quick Ratio

CVS

2013 $25,325,000 $15,425,000 $11,045,000 0.93

2012 $20,161,000 $14,150,000 $11,032,000 0.65

Walgreens

2013 $11,874.00 $8,883.00 $6,852.00 0.57

2012 $10,760.00 $8,722.00 $7,036.00 0.43

Industry 0.83

Debt Management Ratios *All $ in Thousands

Total Debt to Asset Ratio = Total Liabilities / Total Assets

Total Liabilities Total Assets Total Debt

Ratio (%)

CVS

2013 $33,588,000 $71,526,000 46.97%

2012 $28,568,000 $66,221,000 43.14%

Walgreens

2013 $16,027,000 $35,481.00 45.17%

2012 $15,226,000 $33,462.00 45.50%

Industry 45%

This financial ratio measures the extent of a company’s financial leverage. The total

amount of debt or liabilities the company has divided by their total assets will give us the total

debt to asset ratio. This ratio indicates what portion of debt a company has relative to its assets.

This number can be sometimes misleading as many of the assets can be valued from historical

data and sometimes do not include inflation.

Both companies are in pretty good standings under this ratio. There is no dramatic

change from 2012 to 2013 in either company but if we had to choose, CVS would be the winner

due to the fact that they have a much larger business worth and their percentage for 2013 is a bit

higher than that of Walgreens.

Debt Management Ratios *All $ in Thousands

Debt-to-Equity = Total long term Debt / Total Equity

The next ratio is the debt-to-equity ratio, a great measure of a company’s financial

leverage and is found by dividing its debt by total stockholder’s equity. The ratio indicates what

proportion of equity and debt the company is using to finance its assets. If the earnings are

increased to cover the shareholders then everyone benefits. The bad side comes when the cost

of financing the debt is higher than the return which is indicating the company is on its way

down in the market.

The winner again is CVS due to having a higher Debt-to-Equity ratio both years, which

means that the value of the company is higher, especially in the last year. Even though CVS has

higher Debt their equity is much higher than Walgreens. Walgreens is still in great shape so that

doesn’t mean it isn’t a good investment but as for now CVS would be the smarter investment in

my opinion.

Total Long Term

Debt Total Equity Debt-to-Equity Ratio

CVS

2013 $12,841,000 $37,938,000 .3385=33.85%

2012 $9,133,000 $37,653,000 .2426=24.26%

Walgreens

2013 $4,477,000 $19,454.00 .2301=23.01%

2012 $4,073,000 $18,236.00 .2233=22.33%

Industry 18.4%

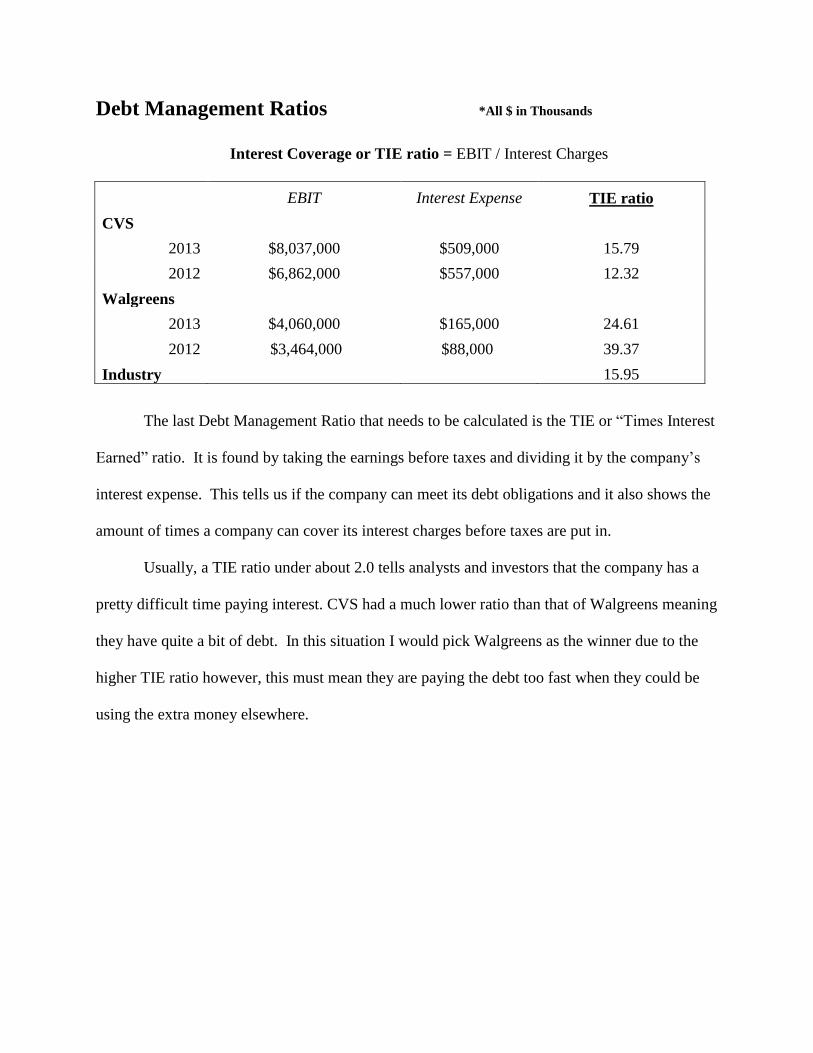

Debt Management Ratios *All $ in Thousands

Interest Coverage or TIE ratio = EBIT / Interest Charges

EBIT Interest Expense TIE ratio

CVS

2013 $8,037,000 $509,000 15.79

2012 $6,862,000 $557,000 12.32

Walgreens

2013 $4,060,000 $165,000 24.61

2012 $3,464,000 $88,000 39.37

Industry 15.95

The last Debt Management Ratio that needs to be calculated is the TIE or “Times Interest

Earned” ratio. It is found by taking the earnings before taxes and dividing it by the company’s

interest expense. This tells us if the company can meet its debt obligations and it also shows the

amount of times a company can cover its interest charges before taxes are put in.

Usually, a TIE ratio under about 2.0 tells analysts and investors that the company has a

pretty difficult time paying interest. CVS had a much lower ratio than that of Walgreens meaning

they have quite a bit of debt. In this situation I would pick Walgreens as the winner due to the

higher TIE ratio however, this must mean they are paying the debt too fast when they could be

using the extra money elsewhere.

Asset Management Ratios *All $ in Thousands

Inventory Turnover = COGS/Inventory

Costs of Goods Sold Inventory Inventory Turnover

CVS

2013 $102,978,000 $11,045,000 9.32

2012 $100,632,000 $11,032,000 9.12

Walgreens

2013 $51,098.00 $6,852.00 7.46

2012 $51,291.00 $7,036.00 7.29

Industry 10.11

To start the Asset management ratios we look at the Inventory Turnover ratio. This shows

how many times a company's inventory is sold and replaced over a period of time. The higher

the turnover rate the better the company is doing at selling their inventory. This number varies a

lot from industry to industry. For example, an automobile dealership probably has a much lower

inventory turnover because they are selling an item that lasts years.

Both CVS and Walgreens are doing a great job with turning their inventory but this could

also be because they sell many perishable items. The winner here is of course CVS due to the

fact they are in the same industry and they sell at a level much higher than Walgreens.

Asset Management Ratios *All $ in Thousands

Accounts Receivable Days = Accounts Receivable / (Sales/365)

The next Asset Management ratio we look at is calculated by taking the total value

of accounts receivable divided by the average daily sales. In order to find the daily sales

you take the revenue and divide it by 365. This shows us how many days it takes to pay

and accounts receivable. This is useful for determining how efficient the company is at

receiving whatever short-term payments it is owed.

In 2012 and 2013 CVS is the leader. Even though their bills owed on credit is

about 4 times higher than Walgreens in 2013, the average daily sales is much higher

which covers most of the credit bills.

Accounts Receivable Average Daily Sales Accounts Receivable

Days

CVS

2013 $ 9,631,000 $346,290 27.81

2012 $ 7,172,000 $337,315 21.26

Walgreens

2013 $2,632,000 $197,854 13.30

2012 $2,167,000 $196,250 11.04

Industry 13.63

Asset Management Ratios *All $ in Thousands

Total Asset Turnover = Sales / Total Assets

Sales Total Assets Total Assets Turnover

CVS

2013 $ 126,761,000 $ 71,526,000 1.77

2012 $ 123,120,000 $ 66,221,000 1.86

Walgreens

2013 $72,217,000 $35,481,000 2.04

2012 $71,633,000 $33,462,000 2.14

Industry 2.18

The last Asset Management Ratio is the Total asset turnover ratio. It is defined as the

amount of sales generated per $1 of assets. This can show an investor the level of efficiency a

company has. The reason CVS has a lower ratio number is because they more than double the

worth of assets compared to Walgreens.

Walgreens is the winner here because according to the numbers their total asset turnover

is higher for both years and that is most likely due to the conservative space and management in

each chain.

Profitability Ratios *All $ in Thousands

Net Profit Margin = Net Income / Sales

Net Income Sales Profit Margin

CVS

2013 $4,592,000 $126,761,000 3.62%

2012 $3,864,000 $123,120,000 3.14%

Walgreens

2013 $2,450,000 $72,217,000 3.39%

2012 $2,127,000 $71,633,000 2.97%

Industry 2.19%

The first profitability ratio to be analyzed is the Profit margin. This is a measure of

the percentage of profitability within a given year. It is calculated by dividing net income by

sales. In 2012 and in 2013 CVS has a higher profit margin, which means from the sales they

incurred, they made a higher percentage in profit than Walgreens did. Thus in this situation

CVS is the winner yet again. This is a great ratio to use just to be sure that a company isn’t

losing money at the end of the year.

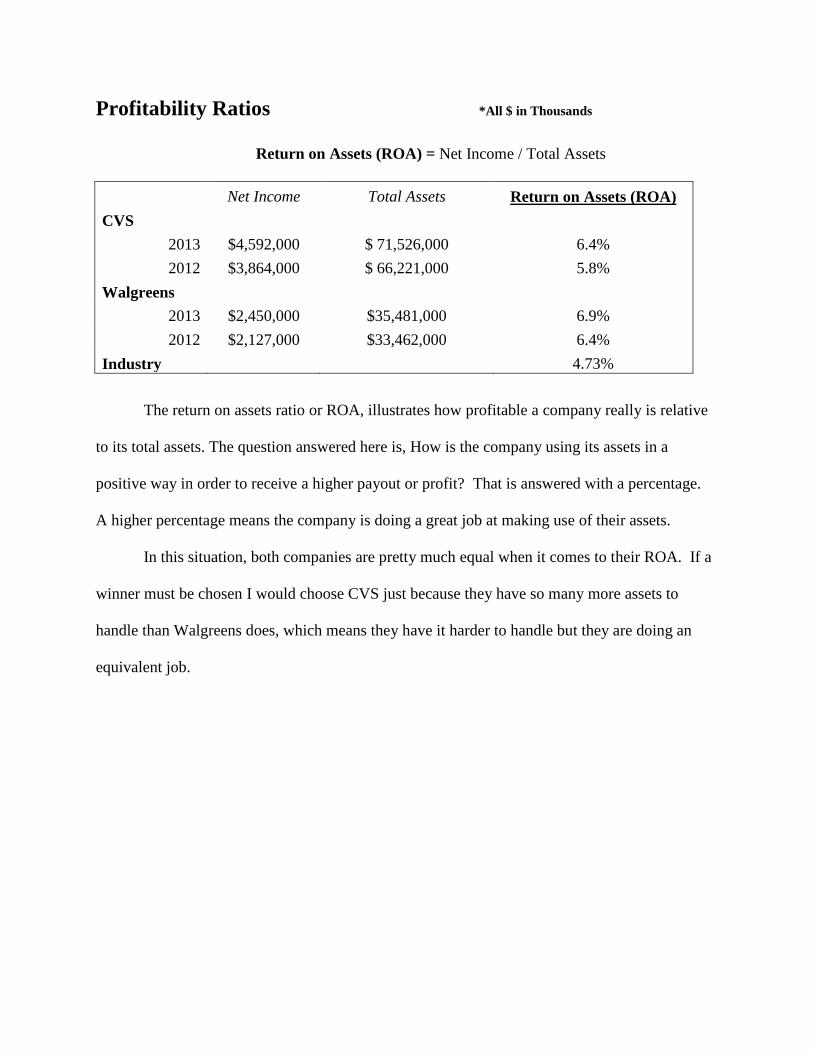

Profitability Ratios *All $ in Thousands

Return on Assets (ROA) = Net Income / Total Assets

Net Income Total Assets Return on Assets (ROA)

CVS

2013 $4,592,000 $ 71,526,000 6.4%

2012 $3,864,000 $ 66,221,000 5.8%

Walgreens

2013 $2,450,000 $35,481,000 6.9%

2012 $2,127,000 $33,462,000 6.4%

Industry 4.73%

The return on assets ratio or ROA, illustrates how profitable a company really is relative

to its total assets. The question answered here is, How is the company using its assets in a

positive way in order to receive a higher payout or profit? That is answered with a percentage.

A higher percentage means the company is doing a great job at making use of their assets.

In this situation, both companies are pretty much equal when it comes to their ROA. If a

winner must be chosen I would choose CVS just because they have so many more assets to

handle than Walgreens does, which means they have it harder to handle but they are doing an

equivalent job.

Profitability Ratios *All $ in Thousands

Return on Equity (ROE) = Net Income / Shareholder Equity

Return on equity (ROE) is Net Income divided by book value of equity. It measures the

rate of return as a percentage of shareholders' equity. The industry average is a very solid return

with above 11%. On a long term return this is about the same as the market has performed from

year to year on average. There are much higher ROE’s but that varies from industry to industry.

This shows that investing within this industry would get you an average return of 11%

Both CVS and Walgreens are between 10%-12% ROE which in my opinion is great.

Both companies are worth investing in and buying stock is a great way to make some easy

money as long as nothing bad happens to the company. I would choose to invest with Walgreens

for the short term because they have more room for growth but CVS would be a safer bet most

likely.

Net Income Book Value of Equity Return on Equity (ROE)

CVS

2013 $4,592,000 $37,938,000 12.10%

2012 $3,864,000 $37,653,000 10.26%

Walgreens

2013 $2,450,000 $19,454,000 12.60%

2012 $2,127,000 $18,236,000 11.66%

Industry 11.16

Market Valuation Ratios *All $ in Thousands

Price-To-Earnings Ratio (P/E) = Market Price Per Share / Earnings Per Share

The Price-Earnings ration or P/E Ratio, is calculated by market cap divided by net

income. It can also be calculated by taking the Market Price per share and dividing it by

Earnings per share. Usually, a higher P/E ratio shows that predictions being made expect a

higher earnings growth in the future compared to that with a lower one.

In 2013 Walgreens market cap skyrocketed and the P/E ratio went up with it.

Having a higher P/E ratio than CVS investors might now sell their shares in CVS and start

buying Walgreens as people might see more room for growth and higher earnings in the

future.

Market Cap Net Income P/E Ratio

CVS

2013 $75,510,000 $4,592,000 16.43

2012 $61,204,960 $3,864,000 15.82

Walgreens

2013 $68,080,000 $2,450,000 27.78

2012 $29,473,750 $2,127,000 13.85

Industry 16.93

Market Valuation Ratios *All $ in Thousands

The last ratio in the financial analysis is the market-to-book ratio. This is calculated to

see if the stock is over or under valued. It is determined through market capitalization. Usually if

the ratio is above 1 the stock is undervalued which is where companies want to be so more

people buy their stock.

Both companies are below the industry average however this doesn’t necessarily mean

they are bad investments. This is only one ratio when looking at a financial analysis and you

must compare them all if you want to invest in a orderly fashion and in a successful way. CVS is

the winner in my opinion due to the ratio numbers given.

Book Value (Historical Cost

basis)

Market Value (Market

Cap) Market to Book Ratio

CVS

2013 $37,938,000 $75,510,000 .5024

2012 $37,653,000 $61,204,960 .6152

Walgreens

2013 $19,454.00 $68,080,000 .2860

2012 $18,236.00 $29,473,750 .6188

Industry .81

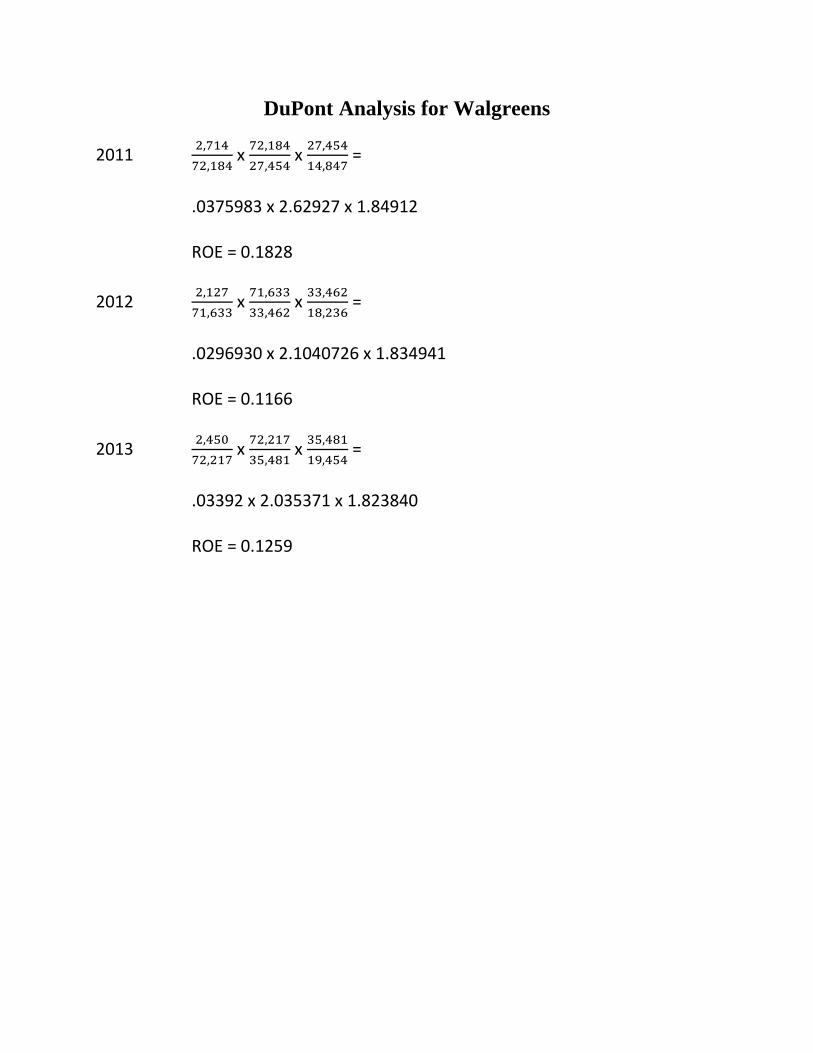

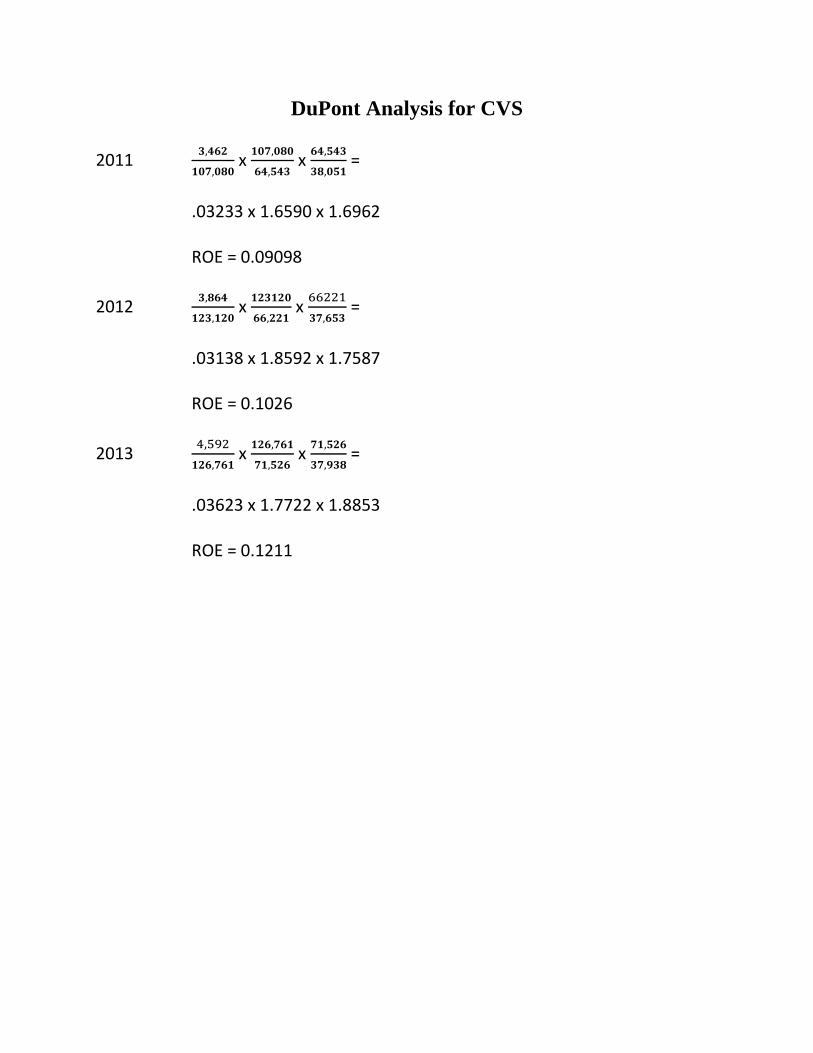

DuPont Analysis

DuPont Analysis is a performance measurement that started in the 1920s and it looks the

gross book value rather than at the net book value so a higher ROE is compounded.

ROE = (Net Income / Sales) x (Sales / Assets) x (Assets / Equity)

C.

1. Operating Efficiency is measured by Profit Margin

2. Asset use efficiency is measured by Total Asset Turnover

3. Financial Leverage is measured by Equity Multiplier

DuPont Analysis for Walgreens

2011 2,714

72,184 x

72,184

27,454 x

27,454

14,847 =

.0375983 x 2.62927 x 1.84912

ROE = 0.1828

2012 2,127

71,633 x

71,633

33,462 x

33,462

18,236 =

.0296930 x 2.1040726 x 1.834941

ROE = 0.1166

2013 2,450

72,217 x

72,217

35,481 x

35,481

19,454 =

.03392 x 2.035371 x 1.823840

ROE = 0.1259

DuPont Analysis for CVS

2011 𝟑,𝟒𝟔𝟐

𝟏𝟎𝟕,𝟎𝟖𝟎 x

𝟏𝟎𝟕,𝟎𝟖𝟎

𝟔𝟒,𝟓𝟒𝟑 x

𝟔𝟒,𝟓𝟒𝟑

𝟑𝟖,𝟎𝟓𝟏 =

.03233 x 1.6590 x 1.6962

ROE = 0.09098

2012 𝟑,𝟖𝟔𝟒

𝟏𝟐𝟑,𝟏𝟐𝟎 x

𝟏𝟐𝟑𝟏𝟐𝟎

𝟔𝟔,𝟐𝟐𝟏 x

66221

𝟑𝟕,𝟔𝟓𝟑 =

.03138 x 1.8592 x 1.7587

ROE = 0.1026

2013 4,592

𝟏𝟐𝟔,𝟕𝟔𝟏 x

𝟏𝟐𝟔,𝟕𝟔𝟏

𝟕𝟏,𝟓𝟐𝟔 x

𝟕𝟏,𝟓𝟐𝟔

𝟑𝟕,𝟗𝟑𝟖 =

.03623 x 1.7722 x 1.8853

ROE = 0.1211

0

0.005

0.01

0.015

0.02

0.025

0.03

0.035

0.04

CVS Profit Margin Walgreens Profit Margin

Profit Margin

2011 2012 2013

DuPont Analysis Graphs

This graph shows the return on equity for both CVS and Walgreens. Each color represents

a different year from 2011-2013. Something that really standsout is the year 2011 for

Walgreens. They had an ROE of above 18% which is considered a very high return. - - - - -

- - - - - - INDUSTRY ROE – About 12.98%

This bar graph shows the Profit Margin differences between CVS and Walgreens Each color

represents a different year from 2011-2013. As you may realize the year 2011 was great for

Walgreens and as time went on to today, CVS is doing much better.

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

CVS ROE Walgreens ROE

Return on Equity (ROE)

2011 2012 2013

1.6

1.65

1.7

1.75

1.8

1.85

1.9

CVS Equity Multiplier Walgreens Equity Multiplier

Equity Multiplier

2011 2012 2013

This graph is showing the Total Asset Turnover for CVS & Walgreens. Each color represents a

different year ranging from 2011-2013. The total asset turnover for Walgreens in 2011 is the

highest on the chart! In that year Walgreens topped CVS in every category but has fell slightly

since.

The graph above is of the Equity Multiplier, which is a measure of each company’s financial

leverage. As you can see as time has passed over the years CVS has started to pay their assets

with the shareholders equity while Walgreens has actually declined in their equity used on assets.

CVS does have more to pay off however so this could be the explanation of 2013.

0

0.5

1

1.5

2

2.5

3

CVS Total Asset Turnover Walgreens Total Asset Turnover

Total Asset Turnover

2011 2012 2013

References

1. http://finance.yahoo.com/q/is?s=WBA+Income+Statement&annual

2. http://www.walgreens.com/topic/about/companyhistory.jsp

3. http://finance.yahoo.com/q/is?s=CVS+Income+Statement&annual

4. https://cvshealth.com/about/company-history