1 FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION. FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION. Rethinking Fixed Income in Defined Contribution Plans

Transcript

1

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION. FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Rethinking Fixed Income in Defined Contribution Plans

2

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Agenda

Rationalizing Your Plan’s Fixed Income LineupAligning Participant Expectations with Your Plan’s Core Plus Manager Janus Fixed Income Capabilities

2

3

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION. FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Rationalizing Your Plan’s Fixed Income Lineup

4

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Fixed Income Is Often Underrepresented In Menus

According to the nonprofit Plan Sponsor Council of America (PSCA), the average DC plan has 18 offerings in its investment menu, but only two or three are fixed-income fundsLimiting choice of fixed income funds may pose significant fiduciary and retirement readiness risks including the inability to properly diversify the fixed income portion of a participant’s portfolio

4

5

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Too Many Options Leads to “Choice Overload”

Several academic studies have concluded that too many options within a Defined Contribution plan confuses participants and leads to sub-optimal behavior:• Procrastination

• Low levels of participation

• Naïve diversification strategies

5

6

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

A Framework for Fixed Income Menu Construction

Assuming a lineup of 18 options and a target-date series of 5 to 6 funds, a fixed income lineup of 5 funds offering distinct risk and reward characteristics will leave 7 to 8 funds for equity options

The 5 fixed income funds can be selected beginning with the most conservative option

6

7

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

A Framework for Fixed Income Menu Construction

7

Step 1: Capital Preservation

Lower HigherRisk/Return Tradeoff

Money Market/Stable Value

Primary objective is to preserve principal

8

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

A Framework for Fixed Income Menu Construction

On July 23, 2014, the SEC finalized its ruling on money market mutual fund reform. The new rules, which must be in place within two years, include:• Prime Funds that service institutions must move to a floating NAV;

• Prime Funds that service “only” retail shareholders can continue to use stable NAV accounting;

• US Government and Treasury Funds are exempt from rule changes;

• In times of stress, a fund’s Board can halt redemption activity for up to 10 days and/or impose a 2% redemption fee; and

• Funds will be required to make public their 7-day and 30-day liquidity positions on a daily basis

8

9

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

A Framework for Fixed Income Menu Construction

9

Step 2: US Short-Term Investment Grade

Lower HigherRisk/Return Tradeoff

Short-Term/Low-Duration

May provide slightly higher yield than the capital preservation option but principal is not “guaranteed”

10

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Average Annual Return

Standard Deviation 2008 Return

US Money Market-Taxable 1.46% 0.51% 2.01%

US Short-Term Bond 2.48% 1.87% -4.61%

10

Money Market vs. Short-Term Bond Managers (1/1/04-12/31/13)

A Framework for Fixed Income Menu Construction

Source: Category average returns for period 1/1/04-12/31/13, Morningstar

11

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

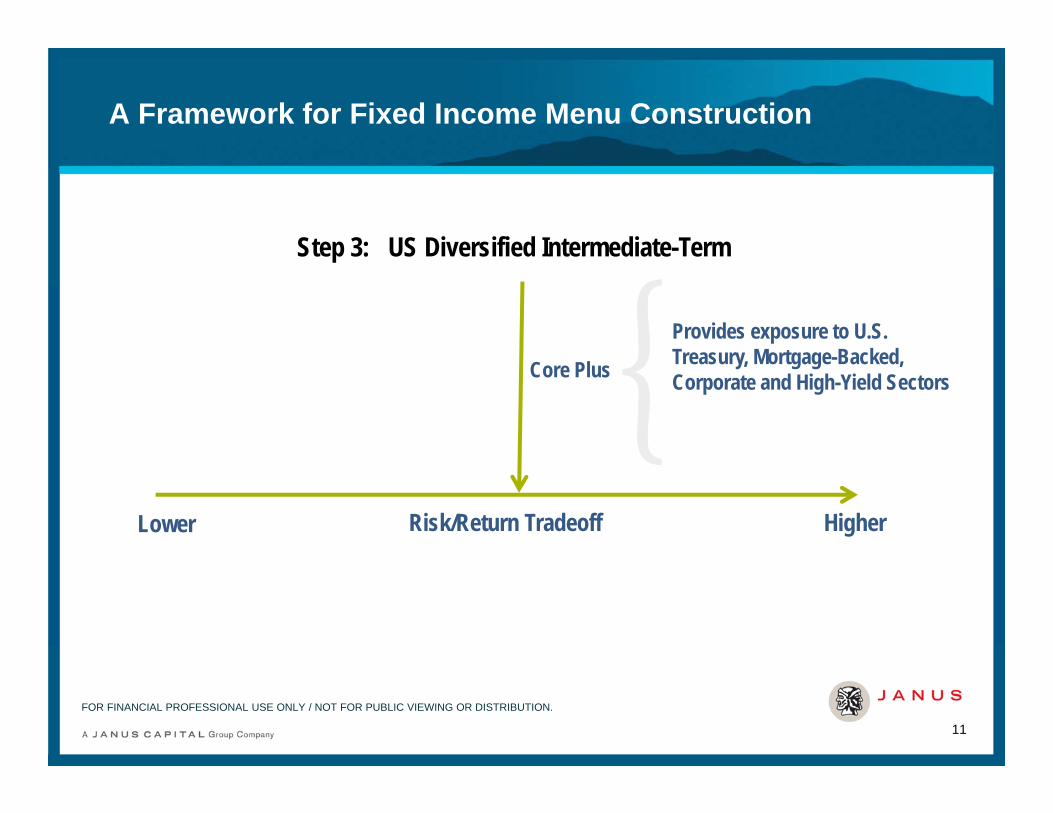

A Framework for Fixed Income Menu Construction

11

Step 3: US Diversified Intermediate-Term

Lower HigherRisk/Return Tradeoff

Core Plus

Provides exposure to U.S. Treasury, Mortgage-Backed, Corporate and High-Yield Sectors

12

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

A Framework for Fixed Income Menu Construction

12

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

High-Yield

11.13%

US Treasury2.79%

High-Yield

11.85%

USTreasury9.01%

US Treasury13.74%

High-Yield

58.21%

High-Yield

15.12%

US Treasury9.81%

High-Yield

15.81%

High-Yield

7.44%

Corporate5.24%

High-Yield

2.74%

MBS5.22%

MBS6.90%

MBS8.34%

Corporate16.04%

Corporate8.47%

Corporate8.35%

Corporate9.37%

MBS-1.41%

MBS4.70%

MBS2.61%

Corporate4.26%

Corporate5.11%

Corporate-3.08%

MBS5.89%

USTreasury5.87%

MBS6.23%

MBS2.59%

Corporate-2.01%

US Treasury3.54%

Corporate1.96%

US Treasury3.08%

High-Yield

1.87%

High-Yield

-26.16%

US Treasury-3.57%

MBS5.37%

High-Yield

4.98%

US Treasury1.99%

USTreasury-2.75%

Core Plus Offers Broad Diversification – Four Categories in One

Source: Barclays U.S. Aggregate Corporate – High Yield (High Yield), Government – Treasury (US Treasury), Credit – Mortgage (MBS), Corporate AAA (Corporate); Morningstar

13

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

A Framework for Fixed Income Menu Construction

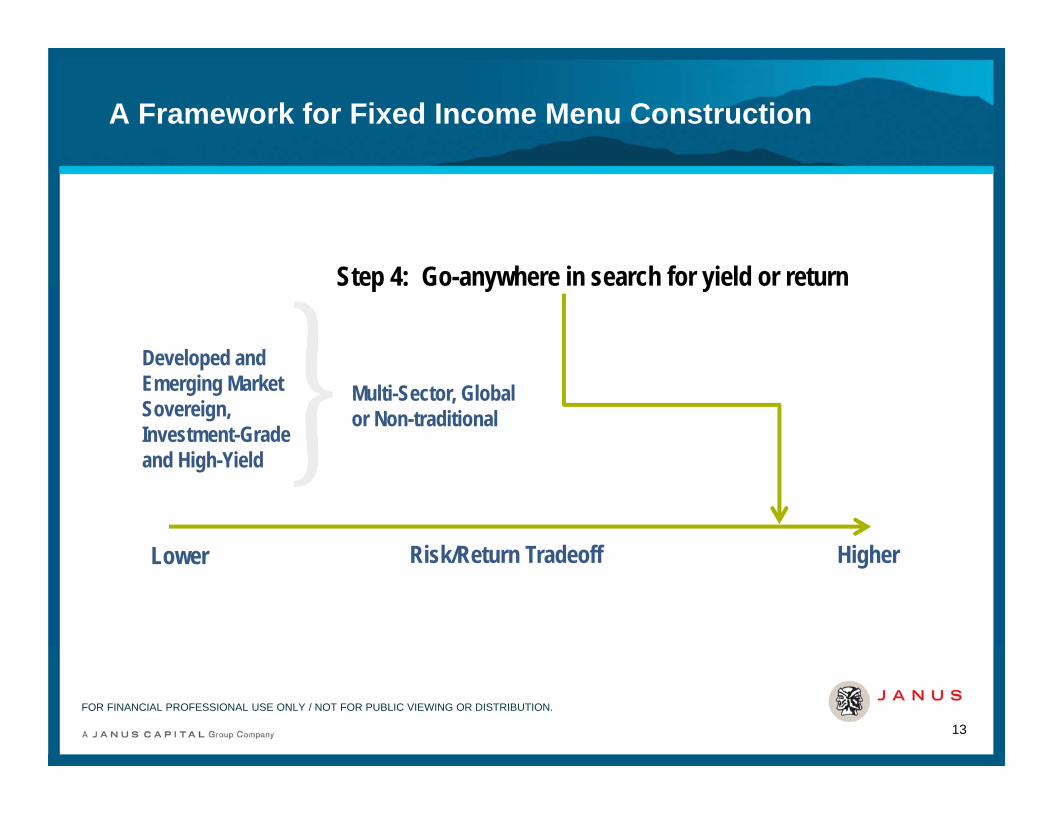

13

Step 4: Go-anywhere in search for yield or return

Lower HigherRisk/Return Tradeoff

Multi-Sector, Global or Non-traditional

Developed and Emerging Market Sovereign,Investment-Grade and High-Yield

14

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

US Intermediate-Term vs. Go-Anywhere Fixed Income Managers

Source: Category average returns, Morningstar

15

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

A Framework for Fixed Income Menu Construction

15

Step 5: Inflation Protection

Real Return

Hedges for inflation through the use of TIPS, Real Estate, Commodities, Gold, Natural Resources, etc.

16

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

A Framework for Fixed Income Menu Construction

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

S&P Global REIT

31.97%

S&P Global Natural

Resources26.79%

FTSE EPRA/NAREIT

Global REITs39.20%

S&P Global Natural

Resources41.73%

S&P GSCI Gold Spot

5.53%

S&P GlobalNatural

Resources36.14%

S&P GSCI Gold Spot29.67%

Barclays U.S. Treasury U.S. TIPS13.56%

FTSE EPRA/NAREIT

Global REITs22.97%

FTSE EPRA/NAREIT

Global REITs2.32%

S&P Global Natural

Resources 24.38%

BloombergCommodity

21.36%

S&P Global Natural

Resources29.78%

S&P GSCI Gold Spot31.35%

Barclays U.S. Treasury U.S. TIPS

-2.35%

FTSE EPRA/NAREIT

Global REITs32.60%

FTSE EPRA/NAREIT

Global REITs22.83%

S&P GSCI Gold Spot10.23%

S&P Global Natural

Resources7.15%

S&P Global Natural

Resources1.55%

BloombergCommodity

9.15%

S&P GSCI Gold Spot18.36%

S&P GSCI Gold Spot22.95%

BloombergCommodity

16.23%

BloombergCommodity

-35.65%

S&P GSCI Gold Spot23.96%

Bloomberg Commodity

16.83%

FTSE EPRA/NAREIT

Global REITs2.26%

Barclays U.S. Treasury U.S. TIPS

6.98%

Barclays U.S. Treasury U.S. TIPS

-8.61%

Barclays U.S.

Treasury U.S. TIPS

8.46%

S&P GlobalREIT9.13%

BloombergCommodity

2.07%

Barclays U.S. Treasury U.S. TIPS11.64%

S&P Global Natural

Resources-38.29%

BloombergCommodity

18.91%

S&P Global Natural

Resources10.97%

BloombergCommodity

-13.32%

S&P GSCI Gold Spot

6.96%

Bloomberg Commodity

-9.52%

S&P GSCI Gold Spot

5.36%

Barclays U.S. Treasury U.S. TIPS

2.84%

Barclays U.S. Treasury U.S.

TIPS0.41%

FTSE EPRA/NAREIT

Global REITs-10.84%

FTSE EPRA/NAREIT

Global REITs-44.43%

Barclays U.S. Treasury U.S. TIPS11.41%

Barclays U.S. Treasury U.S. TIPS

6.31%

S&P Global Natural

Resources-14.86%

Bloomberg Commodity

-1.06%

S&P GSCI Gold Spot-28.26%

Real Return Offers Broad Diversification

Source: Index returns, Morningstar

16

17

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

A Framework for Fixed Income Menu Construction

In summary, we consider using 5 fixed-income asset strategies with distinct risk and reward characteristics

17

Lower HigherRisk/Return Tradeoff

Money Market/ Short-Term/ Core Plus Multi-Sector, Real Stable Value Low-Duration Global or Non- Return

Traditional

InflationHedge

18

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION. FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Aligning Participant Expectations with Your Plan’s Core Plus Manager

19

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

What Are Your Participant’s Expectations?

19

Preserve principalReduce or dampen volatility during times of market stressGenerate a modest or reasonable amount of income

20

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

Jan-

08M

ar-0

8M

ay-0

8Ju

l-08

Sep

-08

Nov

-08

Jan-

09M

ar-0

9M

ay-0

9Ju

l-09

Sep

-09

Nov

-09

Jan-

10M

ar-1

0M

ay-1

0Ju

l-10

Sep

-10

Nov

-10

Jan-

11M

ar-1

1M

ay-1

1Ju

l-11

Sep

-11

Nov

-11

Jan-

12M

ar-1

2M

ay-1

2Ju

l-12

Sep

-12

Nov

-12

Jan-

13M

ar-1

3M

ay-1

3Ju

l-13

Sep

-13

Nov

-13

Jan-

14M

ar-1

4M

ay-1

4

10-Year Treasury2008-2014

20

History of Interest Rates Since 2008

Source: Federal Reserve Bank of St. Louis

21

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

A Secular Bear Market May Actually Create Opportunity

21

Despite the inverse relationship between interest rates and bond prices, a secular bear market may create opportunities if properly managed:• Historically, long-term interest rate trends do not move in a perfectly

linear direction and• Maturing bonds can be reinvested into higher-coupon bonds offsetting

the decline in price

22

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Interest Rate Movements Are Not Linear

Time Period of Rising Rates* 10-year Treasury (Start) 10-Year Treasury (End) Yield Change (bp)Nov 1981-Feb 1982 12.92 14.95 +203

May 1982-Jun 1982 13.46 14.76 +130

May 1983-May 1984 10.12 13.95 +383

Apr 1986-Jun 1986 6.95 8.31 +136

Dec 1986-Oct 1987 6.92 10.23 +331

Mar 1988-Mar 1989 8.11 9.54 +143

Dec 1991-Mar 1992 6.69 7.69 +100

Oct 1993-Nov 1994 5.17 8.03 +286

Jan 1996-Jun 1996 5.52 7.06 +154

Oct 1998-Jan 2000 4.16 6.79 +263

Oct 2001-Apr 2002 4.18 5.43 +125

Jun 2003-Jun 2004 3.11 4.88 +177

Jun 2005-Jun 2006 3.88 5.24 +136

Dec 2008-Jun 2009 2.06 3.95 +189

Oct 2010-Feb 2011 2.38 3.74 +136

May 2013-Dec 2013 1.63 3.03 +140

22

Source: Bloomberg, FactSet. Data presented reflects past performance, which is no guarantee of future results.*From first day of beginning month of the period to final day of ending month of the period.

23

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Reinvesting at Higher Rates Could Yield Positive Returns

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

Total Return

23

The Last Long-Term Rising Rate Environment• Total Return of U.S. Intermediate-Term Government Bond Index vs. 10-Year Treasury Rate

10-Yr. Treas. Rate

Int.-Term Govt. Bond Index

KEY

Source: Barclays

24

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Passive Doesn’t Mean “Safe”

24

5.55

2.48

0

1

2

3

4

5

6

Barclays U.S. Aggregate Index Duration Barclays U.S. Aggregrate Index Yield to Worst

Yield Duration of the Barclays U.S. Aggregate Bond Index

Source: Bloomberg, Barclays (as of 12/31/2013)

25

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

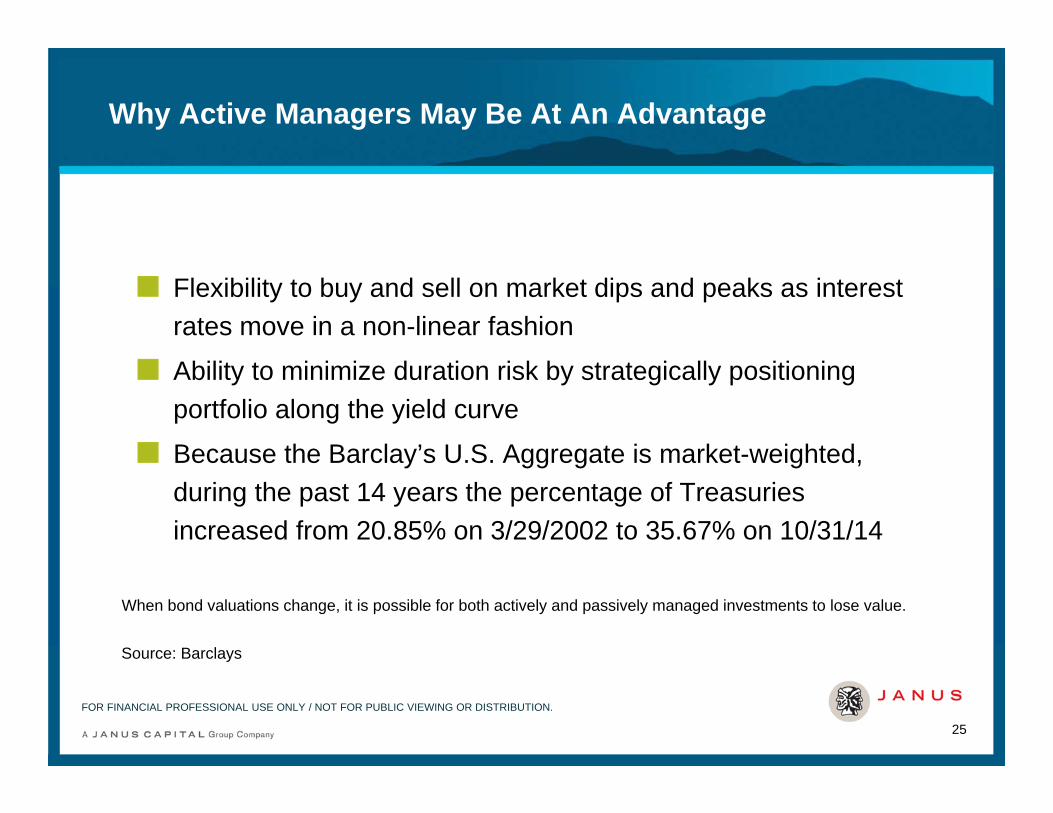

Why Active Managers May Be At An Advantage

Flexibility to buy and sell on market dips and peaks as interest rates move in a non-linear fashion

Ability to minimize duration risk by strategically positioning portfolio along the yield curve

Because the Barclay’s U.S. Aggregate is market-weighted, during the past 14 years the percentage of Treasuries increased from 20.85% on 3/29/2002 to 35.67% on 10/31/14

25

When bond valuations change, it is possible for both actively and passively managed investments to lose value.

Source: Barclays

26

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

What Are Your Participant’s Expectations?

Preserve principalReduce or dampen volatility during times of market stressGenerate a modest or reasonable amount of income

26

27

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION. FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Pre-Crises Correlations to Equities – as of September 2007

27

0

50

100

150

200

Freq

uenc

y

Distribution of 7-Year Correlation to the S&P 500 IndexMorningstar Intermediate-Term Bond Funds

Barclays U.S. Aggregate Index: -0.31 correlationFund Average: -0.22 correlation

CorrelationSource: Morningstar

28

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION. FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Post-Crises Correlations to Equities – as of June 2014

28

Distribution of 7-Year Correlation to the S&P 500 IndexMorningstar Intermediate-Term Bond Funds

0

20

40

60

80

100

120

140

Freq

uenc

y

Barclays U.S. Aggregate Index: .07 correlationFund Average: .32 correlation

CorrelationSource: Morningstar

29

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION. FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Equity Correlation and Max Drawdown – as of June 2014

29

Distribution of 7-Year Correlation to the S&P 500 Index vs. Max DrawdownMorningstar Intermediate-Term Bond Funds

-45

-40

-35

-30

-25

-20

-15

-10

-5

-.3 -.2 -.1 .0 .1 .2 .3 .4 .5 .6 .7 .8 .9

Max

Dra

wdo

wn

(%)

Correlation

Source: Morningstar

30

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Is Your Core Plus Manager a Downside Volatility Dampener or Contributor?

2008 Return 2008 Maximum Drawdown

3rdQ 2011 Return

3rdQ 2011 MaximumDrawdown

S&P 500 -37.00% -13.87%

1st Percentile Core Plus Manager 11.19% -.56% 7.40% -.01%

20th Percentile Core Plus Manager 3.76% -3.31% 3.22% -.17%

Average Core Plus Manager -3.30% -4.05% 1.84% -1.01%

80th Percentile Core Plus Manager -9.59% -4.65% .87% -1.82%

100th Percentile Core Plus Manager -36.24% -17.83% -6.86% -6.86%

30

Source: Morningstar

31

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

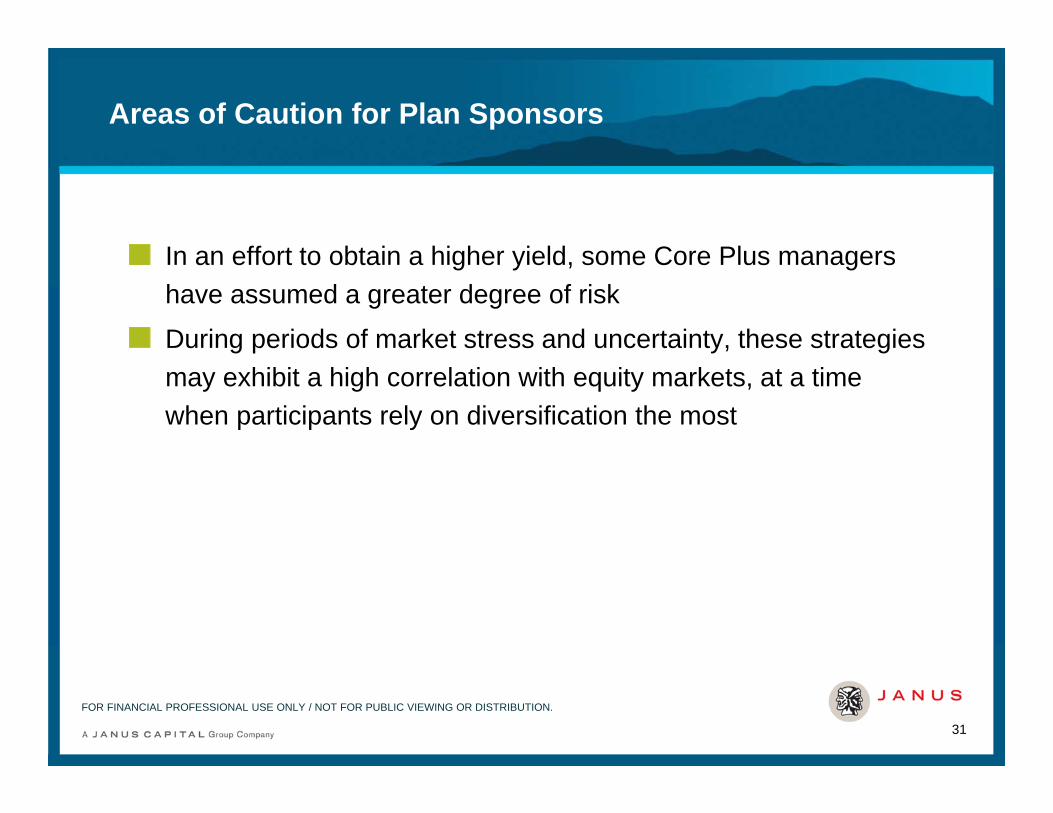

Areas of Caution for Plan Sponsors

In an effort to obtain a higher yield, some Core Plus managers have assumed a greater degree of risk

During periods of market stress and uncertainty, these strategies may exhibit a high correlation with equity markets, at a time when participants rely on diversification the most

31

32

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

What Are Your Participant’s Expectations?

Preserve principalReduce or dampen volatility during times of market stressGenerate a modest or reasonable amount of income

32

33

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Yields Above 5% are Difficult to Find

5.29% 5.20%

2.86% 2.76%2.17% 2.11%

1.38% 1.29%

0%

1%

2%

3%

4%

5%

6%

Yield-to-Worst as of 8/29/2014

33

Source: Barclays Live Index Returns

34

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Low Yields May Mean Limited Price Appreciation

34

0

5

10

15

20

25

1/1/

1987

10/1

/198

77/

1/19

884/

1/19

891/

1/19

9010

/1/1

990

7/1/

1991

4/1/

1992

1/1/

1993

10/1

/199

37/

1/19

944/

1/19

951/

1/19

9610

/1/1

996

7/1/

1997

4/1/

1998

1/1/

1999

10/1

/199

97/

1/20

004/

1/20

011/

1/20

0210

/1/2

002

7/1/

2003

4/1/

2004

1/1/

2005

10/1

/200

57/

1/20

064/

1/20

071/

1/20

0810

/1/2

008

7/1/

2009

4/1/

2010

1/1/

2011

10/1

/201

17/

1/20

124/

1/20

131/

1/20

14

Barclays U.S. Corporate High Yield Bond Index Yield-to-Worst

Source: Barclays

35

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Tale of Two Companies: Ford

35

Ford’s credit was rated BB+ in early 2013

Research suggests:• The company made improvements to its business model in recent

years, including reducing costs, improving liquidity and providing a better product mix and

• The improving US economy, replacement demand and low interest rates provided a positive business climate for the auto industry

In September 2013, S&P raised its credit rating from BB+ to BBB-

Despite higher rates in 2013, the Ford 3% 2017 closed at $104.04, up from $102.74

36

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Tale of Two Companies: Dell

36

An A-rated issue in early 2013, with spreads trading close to the A-rated index

Research suggests:• PC Market in decline as tablets like the iPad took significant

market share;

• Management was focused on friendly equity shareholder activities such as debt-funded acquisitions and share repurchases; and

• Concerned about a potential leveraged-buyout given the bonds lacked a protective change of control covenant

When a LBO was announced in 2013, the 5.4% 2040 bonds troughed at a low of $68 compared to trading at $100 earlier in the year

37

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Important Lessons About Credit Risk

Managers must be able to discern between attractively priced corporate bonds and those of ailing companies with a justified depressed market valuation

Security avoidance can be as important as security selection

37

38

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION. FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Janus Fixed Income Capabilities

39

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Fixed Income Background at Janus

39

Janus Fixed Income manages $31.3 billion (as of 9/30/14) for clients globally in multi-sector investingHistory dates back to 1987 with the inception of the Janus Flexible Bond FundPortfolio managers average more than 25 years of investment experienceTwo distinct and separate fixed income investing platforms:• Bottom-up, fundamental fixed income• Top-down, global macro fixed income

40

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Shared Strategies of Equity and Fixed Income

40

Shared focus on fundamental research integrates our equity and fixed income teamResearch and business contacts for accessing management are shared between investment teams to form a collective opinion regarding management’s intentionsA deep understanding of potential catalysts and more data points is acquired as a result of shared research for a particular company

41

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Fixed Income Strategies

41

Bottom-up, Fundamental Fixed IncomeJanus Core Plus/Flexible Bond

• Employs a bottom-up fundamentally driven investment process that focuses on credit-oriented investments• Fundamental credit research is used to build a mosaic of information in an effort to identify macro trends

and inform allocations across fixed income sectors• Credit research emphasizes free cash flow generation, quality of management and security valuation

Janus Global Multi-Sector• Flexibility to deviate significantly from the index on a sector, country, currency and duration basis, seeking

risk-adjusted returns and capital preservation• Fundamental corporate and sovereign credit research drives portfolio allocation and security selection• Sophisticated, proprietary fixed income portfolio and risk-management system, Quantum Global

Janus Short Duration• Employs a bottom-up fundamentally driven investment process that focuses on credit-oriented investments• Fundamental credit research is used to build a mosaic of information in an effort to identify macro trends

and inform allocations to corporate and government fixed income securities• Credit research emphasizes free cash flow generation, quality of management and security valuation

Janus High Yield• Moderate beta approach, driven by a bottom-up, fundamentally based investment process• Designed to serve as a long-term strategic allocation, not a tactical allocation• Credit research emphasizes free cash flow generation, quality of management and security valuation

42

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Fixed Income Strategies

42

Top-down, Global Macro Fixed IncomeJanus Global Unconstrained Bond

• Seeks to achieve long-term positive returns in diverse market environments over full market cycles• Invests broadly across global fixed income markets and is not constrained by benchmark-specific guidelines• Managed by world-renowned fixed income investor Bill Gross

There is no assurance that the investment process will consistently lead to successful investing. There is no assurance the stated objective(s) will be met. Diversification neither assures a profit nor eliminates the risk of experiencing investment losses.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

High-yield/high-risk bonds, also known as "junk" bonds, involve a greater risk of default and price volatility than U.S. Government and other high quality bonds. High-yield/high-risk bonds can experience sudden and sharp price swings which will affect net asset value.

Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility and differing financial and information reporting standards, all of which are magnified in emerging markets.

Sovereign debt securities are subject to the additional risk that, under some political, diplomatic, social or economic circumstances, some developing countries that issue lower quality debt securities may be unable or unwilling to make principal or interest payments as they come due.

No investment strategy, including an absolute return strategy, can ensure a profit or protect against loss. Additionally, investing in an absolute return strategy may result in underperformance during a bull market.

43

FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Thank You

43

For more information contact your Janus Sales Director at 877.33JANUSPast performance is no guarantee of future results.

This presentation is for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any security. There is no guarantee that the information supplied is accurate, complete, or timely, nor does it make any warranties with regards to the results obtained from its use. It is not intended to indicate or imply in any manner that current or past results are indicative of future profitability or expectations. As with all investments, there are inherent risks that individuals would need to consider.

Please consider the charges, risk, expenses and investment objectives carefully before investing or recommending to clients for investment. For a prospectus containing this and other information, please call Janus at 877.33JANUS (52687) or download the file from janus.com/info. Read it carefully before you invest or send money.

This document is not intended to be legal or fiduciary advice or a full representation of all responsibilities of plan sponsors and advisors. In preparing this document, Janus has relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources.

![GOVERNMENTAL DEFINED CONTRIBUTION … DEFINED CONTRIBUTION VOLUME SUBMITTER PLAN AND TRUST BASIC PLAN DOCUMENT [DC-BPD #05] © Copyright 2014 Governmental Defined Contribution Basic](https://static.documents.pub/doc/80x56/5b0419f67f8b9a4e538d36ff/governmental-defined-contribution-defined-contribution-volume-submitter-plan.jpg)