PERTANIKA14(3),373-381 (1991) Returns to Bidding and Target Finns in Hostile Takeovers: Some UK Evidence SHAMSHER MOHAMAD and ANNUAR MD. NASSIR Department of Accounting and Finance Faculty ofEconomics and Management Universiti Pertanian Malaysia 43400 UPM Serdang, Selangor Darnl Ehsan, Malaysia. Key words: takeovers, bidders, targets, abnormal returns, combined gains. ABSTRAK Kajian ini mengkaji kesan pengumuman pengambilalihan terhadap pulangan firma pembidaan dan firma sasaran dan kekayaan bersama dalam bida pengambilalihan berseteruan di UK. Penemuan kajian ini menunjukkan bahawa firma bida memperolehi pulangan abnormal negatifyang signifikan manakala firma sasaran memperolehi pulangan positif yang signifikan. Penemuan ini adalah tekal dengan penemuan dari kajian yang serupa di pasaran saham Amerika Syarikat. Kekayaan kombinasi yang positifdan signifikan menyiratkan bahawa aktiviti pengambilalihan adalah pelaburan yang menguntungkan dan tekal dengan bayangan bahawa para pengurns menjalankan aktiviti pengambilalihan untuk memaksimakan kekayaan dan bukan saiz. firma. ABSTRACT This paper explores the returns to bidding and target firms in hostile takeovers and their combined wealth effects on the announcement of the offer in the UK. Thefindings reveal that bidderfirms earn negative and significant abnormal returns, whereas target firms earn positive and significant abnormal returns. The gains to target firms more than compensate the losses suffered lry bidders as the combined gains are positive and significant. Thesefindings are consistent with those documented in the US. The positive and significant combined gains imply that takeovers are wealth-creating investments, which is consistent with the notion that managers pursue takeovers to maximise wealth rather than size of theirfirm. INTRODUCTION Previous studies on acquisitions in the UK by Newbould (1970), Singh (1971), Utton (1974), Franks et al. (1977), Firth (1980), Barnes (1978, 1984) and Dodd and Quek (1985) concentrated on returns to bidders and targets in mergers rather than takeovers. This could have been due to the <;lvailabilityofdata on mergers and/ or the popularity of this technique at that time. These studies which used different methodologies on different samples of firms in different time periods concluded that mergers in general did not create any wealth for the bidder shareholders though the targer shareholders always gained. At present, hostile takeovers are as popular as mergers, but little research has been done on firms involved in takeovers. This study intends to explore the behaviour of announcement period returns and the combined wealth effects of bidders and targets involved in takeovers in the UK. Total Bidder Returns At the announcement of the bid, the bidder is expected to offer a price above the current market price of the target firm but below the bidder's estimated value for the target. If the successful bidder has a high chance of acquiring the target firm at a price below the estimated value for the target, part of the potential gains from the takeover identified by the bidder should accrue to the bidder's shareholders. The This paper is a continuation of our earlier paper entitled "Means of Payment and Bidding Firms' Returns in the UK A Test of Information Hypothesis" published in PERTANlKA 14 (1) 1991:93-100.

Transcript

PERTANIKA14(3),373-381 (1991)

Returns to Bidding and Target Finns in Hostile Takeovers:Some UK Evidence

SHAMSHER MOHAMAD and ANNUAR MD. NASSIRDepartment ofAccounting and FinanceFaculty ofEconomics and Management

Universiti Pertanian Malaysia43400 UPM Serdang, Selangor Darnl Ehsan, Malaysia.

Kajian ini mengkaji kesan pengumuman pengambilalihan terhadap pulangan firma pembidaan dan firma sasarandan kekayaan bersama dalam bida pengambilalihan berseteruan di UK. Penemuan kajian ini menunjukkan bahawafirma bida memperolehi pulangan abnormal negatifyang signifikan manakalafirma sasaran memperolehi pulanganpositifyang signifikan. Penemuan ini adalah tekal dengan penemuan dari kajian yang serupa di pasaran sahamAmerika Syarikat. Kekayaan kombinasi yang positifdan signifikan menyiratkan bahawa aktiviti pengambilalihanadalah pelaburan yang menguntungkan dan tekal dengan bayangan bahawa para pengurns menjalankan aktivitipengambilalihan untuk memaksimakan kekayaan dan bukan saiz. firma.

ABSTRACT

This paper explores the returns to bidding and target firms in hostile takeovers and their combined wealth effects on theannouncement of the offer in the UK. The findings reveal that bidderfirms earn negative and significant abnormalreturns, whereas target firms earn positive and significant abnormal returns. The gains to target firms more thancompensate the losses suffered lry bidders as the combined gains arepositive and significant. Thesefindings are consistentwith those documented in the US. The positive and significant combined gains imply that takeovers are wealth-creatinginvestments, which is consistent with the notion that managers pursue takeovers to maximise wealth rather than size oftheirfirm.

INTRODUCTION

Previous studies on acquisitions in the UK byNewbould (1970), Singh (1971), Utton (1974),Franks et al. (1977), Firth (1980), Barnes (1978,1984) and Dodd and Quek (1985) concentrated onreturns to bidders and targets in mergers ratherthan takeovers. This could have been due to the<;lvailabilityofdata on mergers and/or the popularityof this technique at that time. These studies whichused different methodologies on different samplesof firms in different time periods concluded thatmergers in general did not create any wealth for thebidder shareholders though the targershareholdersalways gained.

At present, hostile takeovers are as popular asmergers, but little research has been done on firms

involved in takeovers. This study intends toexplore the behaviour of announcement periodreturns and the combined wealth effects ofbidders and targets involved in takeovers in theUK.

Total Bidder ReturnsAt the announcement of the bid, the bidder isexpected to offer a price above the current marketprice of the target firm but below the bidder'sestimated value for the target.

If the successful bidder has a high chance ofacquiring the target firm at a price below theestimatedvalue for the target, part of the potentialgains from the takeover identified by the biddershould accrue to the bidder's shareholders. The

This paper is a continuation of our earlier paper entitled "Means of Payment and Bidding Firms' Returns in the UK A Test of InformationHypothesis" published in PERTANlKA 14 (1) 1991:93-100.

SHAMSHER MOHAMAD AND ANNUAR MD. NASSIR

expected gains should be discounted in the bidder's share price and the bidder's shareholdersshould earn positive abnormal returns at the announcement of the offer.

Finance theory predicts that firms pursue newcapitalinvestmentswhen the investments have positive effects on their market value. McConnell andMuscarella (1985) provide evidence in support ofthis view, reporting asignificant positive share pricereaction for a sample of industrial firms whichannounced an increase in planned capital expenditures. Acquisitions are also capital investmentsand if the acquisition has any wealth-creating effectfor the bidder firm, the bidder returns at the announcement of the offer should be positive.

Evidence from the US on bidder returns intakeovers show mixed results. For example,Asquith's (1983) study showed that the two-dayannouncement abnormal returns for bidders arepositive but not significantly different from zero.Dodd's (1980), and Asquith and Kim's (1982) studies showed that bidders in takeovers earn significant negative returns at the two-day announcementperiod, whereas Bradley (1980) and Bradley et ai. 's(1983) studies showed that bidders in takeoversearn significant positive abnormal returns at thetwo-day announcement period.

Generally, most findings on daily and monthlyreturns to bidders in takeovers in the US tend to beeither negative or insignificantly positive (Jensenand Ruback 1983, Rappaport 1987.

In the UK, Franks et ai. 's (1988) comparativestudy of firms involved in takeovers in the UK andUS provided some evidence with respect to theeffect ofthe form ofpayments on bidder and targetreturns in the UK, but not total returns and combined wealth effects. To fill the gap, this studyascertains the behaviour of returns to 90 bidderfirms involved in hostile takeovers in the UK at theannouncement of the offer.

Target ReturnsEvidence from the US in general has consistentlyshown that the two-day announcement abnormalreturns of target firms in hostile takeovers arepositive and statistically significant (Asquith 1983;Dodd 1980; Asquith and Kim 1982; Bradley et ai.1983; Bradley 1980 andJarrell and Poulsen 1989).

The shareholders of the target firm earnpositive abnormal returns possibly reflecting theexpected gains of the combined firm and thelarge premiums offered by the bidder at theannouncement.

In the UK, there is no published evidence'On returns to targets in hostile takeovers. Franks

et ai. 's (1988) study provides evidence on returnsto targets in takeovers classified according to themeans of payments offered to their targets but noton total returns of targets in takeovers. Thereforethis study aims to ascertain the effect of takeoverannouncements on the target firms involved inhostile bids in the UK. The returns behaviour oftarget firms involved in hostile takeovers wasobserved at the announcement of the offer.

Combined GainsAn attempt by a bidding firm to gain control of thetarget's resources and implement a higher valuedstrategy is assumed to create wealth throughsynergistic effects. Synergy is realised when anincrease in the aggregate market value of the twofirms is more than a simple sum of market value ofeach firm (Weston and Copeland 1988).

If bidder managers seek to maximise theirshareholders' wealth, their takeover activity can bejustified only if there is some form of synergypresent which will contribute towards the creationof such wealth. Synergy may manifest itself in theform of increase in market power, possession of anew technology, superior research and developmentfacilities, better ditributional facilities, skilledmanagement, production and sales economies ofscale or any other form which will help towards thecreation of more wealth.

The presence and the potential of exploitingthese expected synergies explain partly the rationale for bidders willing to pay large premiums fortheir targets.

In the UK, there is no published evidence ofcombined returns of firms in takeovers at theannouncement of the offer, but findings oncombined returns to bidders and targets inmergers have been reported by Firth (1980) and

f Franks et ai. (1977). Firth (1980) found that the; combined gains of bidders and targets in mergers

~ in the announcement month were virtually zero.However, Franks et ai. (1977) found that combinedgain~ were positive, implying the presence of synergy for firms merging within the brewing anddistil)ing sector.

In US, studies on takeovers by Dodd and Ruback(1977), Bradley (1980), Bradley etai. (1983), Schip-

. per and Thomson (1983) found large and significant positive abnormal returns for target shareholders and small but significant positive abnormalreturns to bidding firms' shareholders, implyingthat the positive combined gains are in support ofthe synergy hypothesis. Mandelker's study (1974)concluded that bidding firms earned normal returns whereas abnormal returns from mergers

374 PERTANIKAVOL. 14NO.3, 1991

RETURNS TO BIDDING AND TARGET FIRMS IN HOSTILE TAKEOVERS: SOME UK EVIDENCE

accrue to target shareholders, implying positivecombined gains.

However, when the combined gains to targetand bidding firms' shareholders are not positive, itimplies that there is merely a transfer of existingrights of ownership from target to the bidder. Roll(1986) in his analysis of successful takeovers in USsuggested that gains by targets are a simple wealthtransfer from bids that are more than their worth(also known as the Hubris Hypothesis).

Dodd (1980) found significant negative returns for bidders and positive returns to targetfirm's shareholders at the announcement of thebid and concluded that gains arising from theacquisition to the target shareholders were at theexpense of the bidding firms's shareholders.

In ascertaining the presence ofsynergy in takeovers using the abnormal returns analysis, it isdifficult to identify the particular type of synergypresent. The presence of synergy is detected if thecombined abnormal returns ofbidders and targetsin the takeover offer are significantly positive at theannouncement of the offer.

To ascertain the presence ofexpected synergyin takeovers, the combined returns to bidders andtargets at the two-day announcement period werecalculated and the results are presented in Table 3.

MATERIALSAND METHODS

DataThe data analysed in this study were drawn frompublic announcements of proposals to acquire atarget firm by means of a takeover. The samplecontains bidder and target firms engaged insuccessful takeovers for the years 1985 to 1988, forwhich daily share returnswere calculalted for elevendays surrounding the announcement day. Theannouncement day is the day of the most recentoffer for the target. The takeover offer wasconsidered successful when the bidding firmacquired the required interest in the target firm'scommon equity (i.e. equal to, or more than, 30 percent). The offers studied were not preceded by amerger attempt.

The sample was identified by a search ofvarious financial publications such as 'AcquisitionMonthly', 'Investors Chronicle'. 'Business Research Index', 'Fair and Trade Publications', 'Stock ExchangeYearbook' and financial newspapers. The sampledfirms were subjected to the following requirements:

(a) The takeover offer was considered successful ifitwas declared unconditional as to acceptances.

(b) Bidder and target firms were listed on the

London Stock Exchange and only alpha andsome beta stocks were sampled to mitigate thenon-synchronous trading problem.

(c) To filter the confounding effects of exogenousevents on bidder returns during the eleven dayssurrounding the event, the bidders and targetssampled did notexperience any major corporateevent at the time of the announcement of theoffer. Major corporate events were defined asdeath or appointment of key executives,announcement of financial reports or newinvestment programmes (except for thetakeover offer under study) for the eleven dayssurrounding the announcement.

(d) Daily share prices for each firm were availablefor at least 58 days before and 58 days after theannouncement day.

The final sample contained 90 bidder and 90target firms.

MethodologyThe research hypotheses examined were tested byapplying an event-type methodology similar to thatdescribed in Fama et al. (1969) and Travlos (1987).The ordinary-leastsquares coefficientsofthe marketmodel regression were estimated over the period n= -58 to n = - 6 and n = + 6 to n = +58 relative to theday of the initial announcement. Daily abnormalcommon stock returns were calculted for each firmi over the interval n = - 5 to n = +5.

Abnormal Return = Rio - (a + BRmn>(lz)

For a sample of N firms, daily average abnormal returns (AR) for each day n are computed by

~!iAR n £..i=1 N

or

1 N- I(Rin - a - BR mn )N i=1

n= -5, ,0, ,+ 5 N = the number of firms

where R. is the returns for common stock of firmIn

i, Rmo is return for the market approximated by theoverall market index on day n, aI'~ are ordinaryleast squares estimates of the market modelparameters (adjusted for non-synchronous tradingproblem using Dimson's (1979) aggregatedcoefficient approach). The daily returns werecalculated from stock prices after adjustment forcapital changes such as dividends and stock splits.

PERTANIKA VOL. 14 NO.3, 1991 . 375

SHAMSHER MOHAMAD AND ANNUAR MD. NASSIR

RESULTS

and

TABLE!Summary of the average abnormal returns (AR) andthe cumulative abnormal returns (CAR) of biddersin takeovers at the two-day announcement period.

The t-statistics are in parentheses.

-0.8915(-8.457)**

AR-0.1005(-0.954)

o

Event Day-1

Bidders

Bidder CAR (-1,0) -0.992(-6.65)**

~T2 - Tl + 1

** Significantly different from zero at 1%level

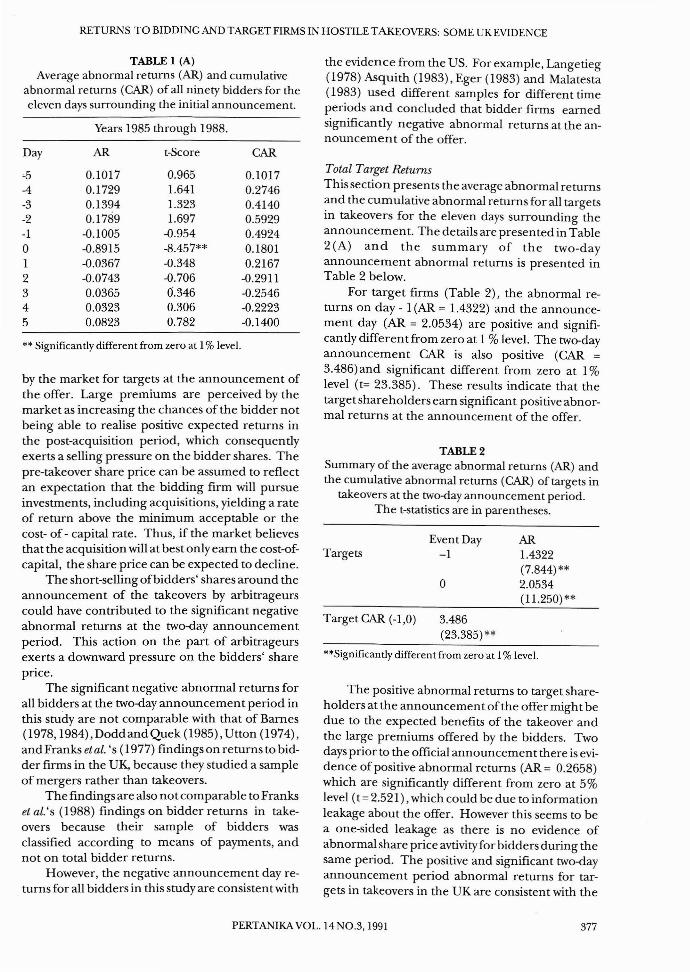

For bidders, the abnormal return on day-l isnegative (AR=-0.1005) but not significantly different from zero (t = - 0.954) at 1%level, whereas theannouncement day abnormal return is negative(AR = - 0.8915) and significantly different fromzero at 1 % level (t = - 8.457) (Table 1). The twoday announcement CAR is also negative (CAR =

-0.992) and significantly different from zero at 1 %,level (t = -6.65). The results indicate that bidders'shareholders in takeovers suffer losses at the announcement of the offer. The findings of negativeabnormal returns to bidders are apparently notconsisten twith the view that acquisitions are wealthcreating investments. However, there might beother factors dominating the positive wealth effectof acquisitions at the announcement of the offer.For example, in the enthusiasm to take over thetarget resources, the bidder management may haveoverstretched its financial and management resources result in some loss of efficiency in its current business activities, which is reflected in theshare price.

There is also a possibility that bidders offerpremiums that are higher than those expected

Total Bidder ReturnsThis section presents the average abnormal returnsand the cumulative abnormal returns for all thebidders in takeovers for the eleven days surroundingthe announcement. The details are presented inTable 1 (A) in the Appendix and the summary ofthe two-day announcement period returns formthis table is presented in Table 1 below.

The estimation period is from n= - 58 to n =

6 and n = + 6 to n = + 58 and the analysis period isfrom n =- 5 to n =+ 5. The standardizing factor Swhich takes into account the problem of nonconstant variance of the residuals in the estimationand analysis period, was computed as follows:

l ]x1 (R mn - Rm)2Sin S~ (l + L + --',-L-----'--

1(~!(Rmk_R m)2

where S~s the residual variance for security i from1

the market model regression, L is the numberof observations during the estimation period (i.e.106 days), R

mkis the return on the market index for

the k day of the estimation period, Rmn

is the returnon th~market index for day n in the analysis period,and R mis the average return of the market index(i.e. market portfolio) for the estimation period.

Assuming that individual abnormal returnsare approximately normally distributed andindependent across time and across securities, the

statistic t and ~!T2 which follow unit-normaldistribution (Dodd and Warner 1983) are used totest the hypothesis that the average standardizedabnormal returns (AR:) and average cumulative

standardized abnormal returns (C~IT2) equal

zero, where

~ *AR*t = \IN n

The returns for each firm were also adjusted for anysignificant first-order auto-correlation usingCochrane-Orcutt's (1949) quasi-first-differenceapproach before calculating the abnormal returns.

The AR for each firm were adjusted for thedifference in size of bidders and targets. Size wasmeasured in terms of the total market value of thefirms at the announcement day. Average cumula-

tive abnormal returns (~!T2)were also derivedby summing the AR over the eleven days surrounding the announcement. The expected values of

AR: and~!T2are zero in the absence ofabnormal performance.

*The test statistics of AR nand~!T2are basedon the average standardized abnormal returns andthe average standardized cumulative abnormalreturns respectively, where

AR~ = AR n = 1.- f (Rin - ex - BR mn

Sin N i=! SinT2

CARTlT2 = L AR~,t=Tl

376 PERTANlKA YOL.14NO.3, 1991

RETURNS TO BIDDING AND TARGET FIRMS IN HOSTILE TAKEOVERS: SOME UK EVIDENCE

TABLE I (A)Average abnormal returns (AR) and cumulative

abnormal returns (CAR) of all ninety bidders for theeleven days surrounding the initial announcement.

by the market for targets at the announcement ofthe offer. Large premiums are perceived by themarket as increasing the chances of the bidder notbeing able to realise positive expected returns inthe post-acquisition period, which consequentlyexerts a selling pressure on the bidder shares. Thepre-takeover share price can be assumed to reflectan expectation that the bidding firm will pursueinvestments, including acquisitions, yielding a rateof return above the minimum acceptable or thecost- of - capital rate. Thus, if the market believesthat the acquisition will at best only earn the cost-ofcapital, the share price can be expected to decline.

The short-selling ofbidders' shares around theannouncement of the takeovers by arbitrageurscould have contributed to the significant negativeabnormal returns at the tw<Hiay announcementperiod. This action on the part of arbitrageursexerts a downward pressure on the bidders' shareprice.

The significant negative abnormal returns forall bidders at the two-day announcement period inthis study are not comparable with that of Barnes(1978, 1984), Dodd and Quek (1985), Utton (1974),and Franks et at. 's (1977) findings on returns to bidder firms in the UK, because they studied a sampleof mergers rather than takeovers.

The findings are also not comparable to Frankset al.'s (1988) findings on bidder returns in takeovers because their sample of bidders wasclassified according to means of payments, andnot on total bidder returns.

However, the negative announcement day returns for all bidders in this study are consistent with

** Significantly different from zero at 1%level.

Years 1985 through 1988.

AR1.4322(7.844)**2.0534(11.250) **

o

3.486(23.385)**

Event Day-1

The positive abnormal returns to target shareholders at the announcement of the offer might bedue to the expected benefits of the takeover andthe large premiums offered by the bidders. Twodays prior to the official announcement there is evidence of positive abnormal returns (AR = 0.2658)which are significantly different from zero at 5%level (t = 2.521), which could be due to informationleakage about the offer. However this seems to bea one-sided leakage as there is no evidence ofabnormal share price avtivi tyfor bidders during thesame period. The positive and significant two-dayannouncement period abnormal returns for targets in takeovers in the UK are consistent with the

**Significantly different from zero at 1%level.

the evidence from the US. For example, Langetieg(1978) Asquith (1983), Eger (1983) and Malatesta(1983) used different samples for different timeperiods and concluded that bidder firms earnedsignificantly negative abnormal returns at the announcement of the offer.

Total Target ReturnsThis section presents the average abnormal returnsand the cumulative abnormal returns for all targetsin takeovers for the eleven days surrounding theannouncement. The details are presented in Table2 (A) and the summary of the two-dayannouncement abnormal returns is presented inTable 2 below.

For target firms (Table 2), the abnormal returns on day - 1(AR = 1.4322) and the announcement day (AR = 2.0534) are positive and significantly different from zero at 1 % level. The two-dayannouncement CAR is also positive (CAR =3.486)and significant different from zero at 1%level (t= 23.385). These results indicate that thetarget shareholders earn significant positive abnormal returns at the announcement of the offer.

TABLE 2Summary of the average abnormal returns (AR) andthe cumulative abnormal returns (CAR) of targets in

takeovers at the two-day announcement period.The t-statistics are in parentheses.

Targets

Target CAR (-1,0)

CAR

0.10170.27460.41400.59290.49240.18010.2167

-0.2911-0.2546-0.2223-0.1400

t-Score

0.9651.6411.3231.697

-0.954-8.457**-0.348-0.7060.3460.3060.782

AR

0.10170.17290.13940.1789

-0.1005-0.8915-0.0367-0.07430.03650.03230.0823

Day

"5-4-3-2-1o12345

PERTANlKA VOL. 14NO.3, 1991 377

SHAMSHERMOHAMADANDANNUARMD.NASSIR

TABLE 2 (A)Average abnormal returns (AR) and cumulative

abnormal returns (CAR) of all ninety bidders for theeleven days surrounding the initial announcement.

** Significantly different from zero at I% level* Significantly different from zero at 5% level.

findings of announcement period target returnsin takeovers in the US.

Combined Total ReturnsFor the total sample of 90 bidders and 90 targets,shareholders of bidding firms earned significantnegative abnormal returns whereas shareholdersof target firms earned significant positiveabnormal returns for the two-day announcementperiod (Table 3). The gains to target shareholdersmore than compensated the losses to biddershareholders and the combined gains were positive(AR = 2.494) and significant at I % level (t = 4.67).These findings are consistent with the notion that

the market recognises expected benefits fromtakeovers at the announcement of the offer,al though a major portion of the benefits seems toaccrue to the target shareholders. The distributionof expected benefits at the announcement of theoffer could have been influenced by a combinationof factors such as competition for the target, targetmanagement's resistance, and lack of informationabout the target firm and its industry.

It is expected that when the bidder is successful in acquiring the target resources and able toimplement a higher valued operating strategy toexploit the expected benefits from the takeover, itwill be able to earn the expected returns on its investment, which is reflected in the share price at theannouncement of the offer.

However, the positive effects ofexpected benefits might be overshadowed by the effects of otherfactors operating simultaneously such as competition, target resistance, valuation error and meansof payment.

The bidder's ability to realise the potentialsynergies in the post-takeover period will dependon how well it is able to integrate the targetresources in its own organisation which requiresexperienced and skilful management. The market,however, gauges the bidder's ability to realise theexpected benefits from the takeover from its pastexperience, which is discounted in the bidder'sshare price at the announcement of the offer.

In essence, the findings of positive combinedreturns in takeovers imply that the intense takeoveractivity in recent years is not without purpose, aswealth is created in the process which is socially andeconomically desirable. The positive combined

TABLE 3Summary ofthe two-day announcement cumulative abnormal returns (CAR) and combined returns for

targets and bidders in the cash, shares and combination offers respectively and for total targets and bidders.The t-statistics are in parentheses.

Total Cash Shares CombinationSampleN=90 N=30 N=30 N=30

** Significantly different from zero at 1 % level* Significantly different from zero at 5% level

378 PERTANIKA VOL. 14 NO.3, 199}

RETURNS TO BIDDING AND TARGET FIRMS IN HOSTILE TAKEOVERS: SOME UK EVIDENCE

returns also imply that takeovers are an effectivemeans ofemploying resources to a highervalue useand are consistent with the notion that they are aneffective tool to discipline complacent managers.

The combined returns of bidders and targetsin cash, share combination offers are positive andsignificant, implying that irrespective of the meansofpayment offered, takeovers are positive net present value investments.

Implication of Findings for Growth MaximisationHypothesisIn recent years, we observe that takeovers are morefrequent between firms in seemingly unrelated orloosely related businesses. Als~, most acquiredtargets are left to operate as autonomous divisionsrun by the same management team that controlledthem before the takeover. A probable reason forsuch behaviour on the part of active bidders is thatfirms could possibly be responding to thegovernment's tough anti-competitive rules ontakeovers.

When one firm takes over another firm in thesame industry, the other firms in the industry mayfeel insecure and resort to defensive measuressuch as pursuing takeovers of other firms, even inunrelated or loosely related businesses. Theprocess restores some sort of equilibrium in theindustry in terms of relative firm size. There is anincentive to increase size because it becomesdifficult and expensive for a potential bidder. Thetargets are usually left to manage their own businesswith minimum interference, possibly due to thebidder's lack of expertise in the target's businessand/or the bidder's management style (i.e. strategic control or financial control type of management).

Marris (1964), Mueller (1969) and Murphy(1985) suggest that bidder managers pursuegrowth rather than profit objectives because sizeprovides both pecuniary and non-pecuniary benefits to the bidder managers.

Wiedenbaum and Vogt (1987) argue thatmanagers prefer to increase the size of theircorporations because the ability ofshareholders tomonitor management decreases in larger andcomplex organisations. If most bidder managerspursue takeovers basically for growth purposes atthe expense oftheir shareholders' interest, we canexpect, on average, their combined gains to beeither zero or negative.

The findings in Table 3 are not consistent withthe growth maximisation hypothesis. The findingsare consistent with the notion that bidders pursuetakeovers with the intention of increasing wealth

rather than firm size. These findings are consistentwith the activities oflarge conglomerates in the UK,such as BTR and Hanson Trust. Their success isattributable to the strong management team whicheffectively employs a 'financial-control' type ofmanagement style and pursues an effectiverationalisation policy subsequent to taking controlofthe target resources. BTRand Hanson Trust takeover firms in unrelated business, keep the mostprofitable part of the business and sell off the otherparts which have very poor fit with their own business and are making losses. The proceeds from thesale help to recoup part of the purchase price.

In the UK, there is no published evidence ofcombined gains of bidders and targets in hostiletakeovers, though there is evidence of combinedgains of merging firms in the industrial sectorprovided by Firth (1980) and in the brewing anddistilling sector by Franks et al. (1977).

However, it is not appropriate to compare thefindings of combined gains of firms involved inhostile bids in this study with those of Firth orFranks et al. because mergers are technicallydifferent from hostile bids.

The positive significant combined gains ofbidders and targets in this research do not supportRoll's (1986) hubris hypothesis which postulatesthat takeovers are zero-sum game, that is gains totarget shareholders are offset by the losses tobidder shareholders.

CONCLUSION

The two-day announcement cumulative abnormalreturns of all bidders in the takeover sample issignificantly negative and for targets, it issignificantly positive. The negative and significantabnormal returns to bidder firms might have beendue to one or more ofthefollowingfactors: expectedloss of efficiency in the bidder's current businessoperations due to management time amI effortspent on pursuing the takeover; the takeover's lackof cormmercial or industrial logic as perceived bythe market; excessive premiums offered to target atannouncement which could have been due to theexpected resistance from the target, competitionfrom other potential bidders and lack ofinformation about the target's business and itsindustry; short-selling of bidder's shares byarbitrageurs or due to specific-bid effect whichseems not to fit into the bidder's business but is anessential part of the bidder's long-term financialstrategy.

The negative abnormal returns to bidders atannouncement, however, cannot imply that bidder

PERTANIKA VOL. 14NO.3, 1991 379

SHAMSHER MOHAMAD AND ANNUAR MD. NASSIR

management are not acting in the best interests oftheir shareholders, because the findings do notaccount for the long term effect of takeovers butjust the two-day announcement returns. There isalso no evidence to indicate that the loss to shareholders benefits the management. It is naive toassume that bidder managers are consistentlymaking irrational investment decisions, because ifthey are then they are jeopardizing own position asthey would become the target of other bidders. Itmight be that the majority of the bidders are pursuing targets merely as a long term strategy to gaina competitive advantage in their respective marketsor industries.

This view is supported by the fact that thecombined gains of bidders and targets are significantly positive implying that takeovers do createwealth for the shareholders ofthe combined firms.

ACKNOWLEDGEMENTS

The authors acknowledge the helpful comments ofProfessor Simon Keane, Department ofAccountingand Finance, University of Glasgow in thepreparation of this paper.

REFERENCES

Acquisitions MonthZ'Y Magazine. January 1985 toDecember 1988.

AsQUITH, P. and H. KIM. 1982. The Impact of MergerBids on the Participating Firms' SecurityHolders.] Finan. 37: 1209-1228.

BARNES, P. 1978. The Effect ofMergers on Share Priceof Bidding Firms. Ace. and Bus. Res. 9: 162-165.

BARNES, P. 1984. The Effectofa Merger on the SharePrice ofthe Attacker, Revisited. Ace. and Bus. Res.15: 45-49.

BRADLEY, M. 1980. Inter-firm Tender Offers and theMarket for Corporate Control. ] Bus. 53: 345375.

BRADLEY, M., A. DESAI and H.E. KIM. 1983. TheRationale Behind Interfirm Tender Offers:Information or Synergy?] Finan. Eeons. 11: 183206.

BREALEY, RA. 1979. The Efficiency of the BritishCapital Market, in City Lights: Essays on FinancialInstitutions and Markets in the City ofLondon, p 2037. London: The Institute of Economic Affairs.

BROWN, S. j. and j.B. WARNER. 1980. MeasuringSecurity Price Performance.] Finan. Eeons. 8: 205258.

BROWN, S. j. and j. B. WARNER. 1985. Using StockReturns: The Case of Event Studies. ] Finan.Eeons. 14: 3-31.

COCHRANE, D. and C. H. ORCUTI. 1949. Applicationof Least Squares Regression to RelationshipsContaining the Autocorrelated Error Terms. ]A mer. Stat. Assoc. 44: 32-61.

DIMSON, E. 1979. Risk Measurement When Shares areSubjected to InfrequentTrading.] Finan. Eeans.7: 197-226.

DODD, P. 1980. Merger Proposals, ManagementDiscretion and Shareholder Wealth. ] Finan.Eeons. 8: 105-137.

DODD,j.C. andj.P. QUEK. 1985. Effect of Mergers onthe Share Price Movement ofthe Acquring Firms:A U.K. Study.] Bus. Finan. and Ace. 12: 285-296.

DODD, P. and RUBACK, R.S. 1977. Tender Offers andStockholder Returns.] Finan. Eeans. 5: 351-373.

DODD, P. and j. WARNER. 1983. On CorporateGovernance: A Study ofProxy Contests.] Finan.Eeons. 11: 401-438.

DURBIN,j. and C.S. WATSON. 1951. Testing for SerialCorrelation in Least Squares Regressions.Biometriea38: 159-178.

EGER, C. 1983. An Empirical Test to the Redistributionin Pure Exchange Mergers. ] Finan. and Quant.Anal. 18: 547-572.

FAMA, E.F., L. FISHER, M.C.JENSEN and R ROLL. 1969.The Adjustments of Stock Prices to NewInformation. Int. Eeon. Rev. 10: 1-21.

Financial Times Newspaper. 1985 to 1988.

FiRTH, M. 1980. Takeovers, Shareholder Returns andTheory of the Firm. Qyar.] Eeons. 94: 235-260.

FRANKS, j. R., j.E. BROYLES and MJ. HECHT. 1977.Industry Study of the Profitability of Mergers inthe United Kingdom. ] Finan. 32: 1525-1531.

FRANKS,j.R , RH. HARRis and C. MAYER. 1988. Meansof Payment in Takeovers: Results from the U.K.and the U.S. Nat. Bureau ofEeon. Res. p 221-258.

GRAY, SJ. and M.C. McDERMOTI. 1989. Mega-mergerMayhem London: Paul Chapman.

HUANG, YS. and R.A. WALKING. 1987. TargetAbnormalReturns Associated with AcquisitionAnnouncements: Payment, Acquisition Form and

380 PERTANlKAVOL. 14 NO.3, 1991

RETURNS TO BIDDING AND TARGET FIRMS IN HOSTILE TAKEOVERS: SOME UK EVIDENCE

JARRELL, G.A. and A. B. POULSEN, 1989. The Returns toAcquiring Firms in Tender Offers: Evidence fromThree Decades. Finan. Mgt. 18: 12 -19.

JENSEN, M. and RS. RUBACK. 1983. The Market forCorporate Control: The Scientific Evidence. ].Finan. Econs. 11: 5-50.

UNGETIEG, T.C. 1978. An Application to MeasureThree Factor Performance Index to MeasureStockholder Gains from Mergers. ]. Finan. Econs.6: 365-383.

LIMMACK, RJ. 1989. Corporate Mergers and ShareholdersWealth Effects: 1977-1986. Draft report for theEconomic and Social Research Council, Centrefor InvestmentManagement, UniversityofStirling.

MAnDALA, G. S'. 1977. Econometrics. New York: McGrawHill.

MALATESTA, P.H. 1983. Wealth Effect of MergerActivity and the Objective Functions of MergingFirms. ]. Finan. Econs. 11: 151-181.

MANDELKER, G. 1974. Risk & Returns: the Case ofMerging Firms. ]. Finan. Econs. 1: 305-335.

MARRIs, R L. 1964. The Economic Theory ofManagerialCapitalism. London: MacMillan.

MCCONNELL,JJ. and C.]. MUSCARELLA. 1985. CorporateCapital Expenditure Decisions and the MarketValue of the Firm. ]. Finan. Econs. 14: 399-422.

MUELLER, D.C. 1969. Theory ofConglomerate Mergers.Qyar.]. Econs. 83: 643-659.

MuRPHY, K ]. 1985. Corporate Performance andManagerial Remuneration: An EmpiricalAnalysis.

]. Ace. andEcons. 7: 11-42.

NEWBOULD, C. D.1970. Management and Merger Activity.Liverpool: Guthstead.

RAPPAPORT, A. 1986. Creating Shareholder Value: TheNew Standard for Business Performance. London:Collier Macmillan Publishers.

RAPPAPORT, A. 1987. Converting Merger Benefits toShareholder Value. Mergers and Acquisitions 21:49-55.

ROLL, R. 1986. The Hubris Hypothesis of CorporateTakeovers.]. Bus. 59: 197-216.

SCHIPPER, K and RTHOMSON. 1983. Evidence onCapitalisedValue ofMergerActivity for AcquiringFirms. ]. Finan. Econs. 11: 85-119.

SINGH, A. 1971. Takeovers: Their Relevance to the StockMarket and the Theory of the Firm.. London:Cambridge University Press.

SINGH, A. 1975. Takeovers Economic Natural Selection,and the Theory of the Firm: Evidence from thePost-war United Kingdom Experience. Econ.]. 85:497-515.