43

REVIEW GUIDE FOR NON PROFIT ORGANIZATION’S INDIRECT COST PROPOSALS U.S. DEPARTMENT OF HEALTH AND HUMAN SERVICES PROGRAM SUPPORT CENTER DIVISION OF COST ALLOCATION 2003

| Date post: | 23-Apr-2018 |

| Category: |

Documents |

| Upload: | nguyenkhanh |

| View: | 223 times |

| Download: | 1 times |

REVIEW GUIDE FORNON PROFIT ORGANIZATION’SINDIRECT COST PROPOSALS

U.S. DEPARTMENT OF HEALTH AND HUMAN SERVICESPROGRAM SUPPORT CENTER

DIVISION OF COST ALLOCATION2003

2

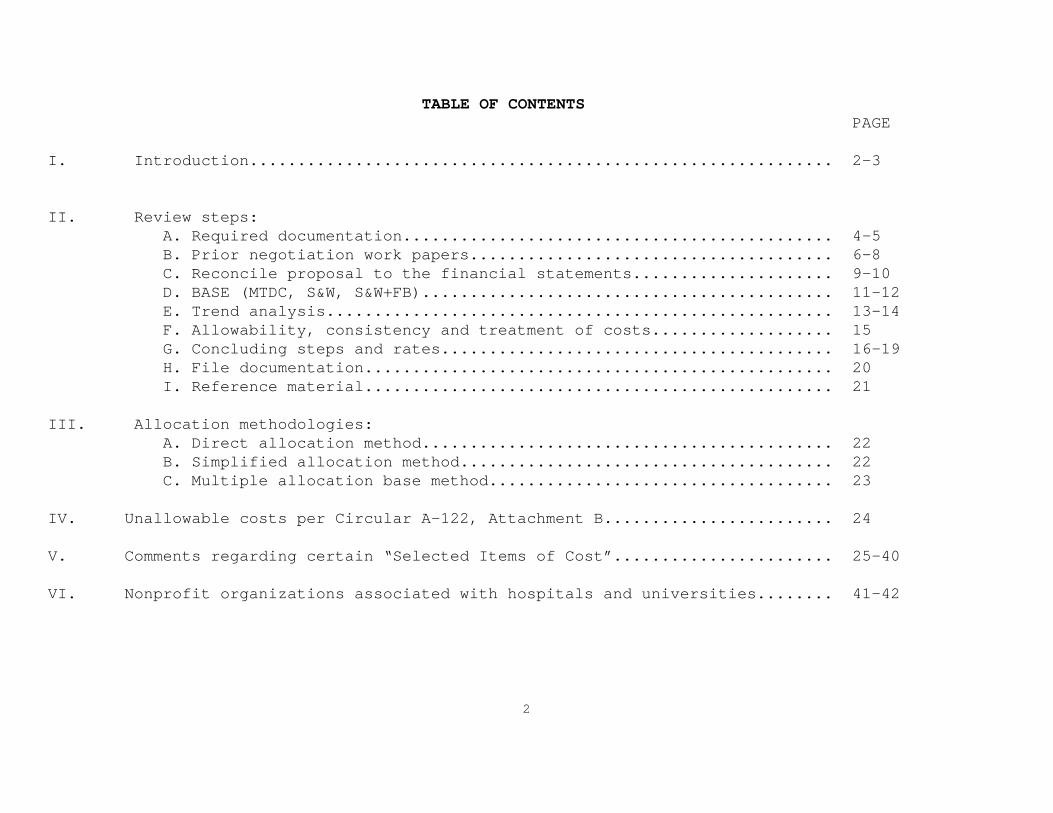

TABLE OF CONTENTS PAGE I. Introduction............................................................. 2-3

II. Review steps:A. Required documentation............................................. 4-5 B. Prior negotiation work papers...................................... 6-8 C. Reconcile proposal to the financial statements..................... 9-10 D. BASE (MTDC, S&W, S&W+FB)........................................... 11-12E. Trend analysis..................................................... 13-14 F. Allowability, consistency and treatment of costs................... 15G. Concluding steps and rates......................................... 16-19H. File documentation................................................. 20I. Reference material................................................. 21

III. Allocation methodologies:A. Direct allocation method........................................... 22B. Simplified allocation method....................................... 22C. Multiple allocation base method.................................... 23

IV. Unallowable costs per Circular A-122, Attachment B........................ 24

V. Comments regarding certain “Selected Items of Cost”....................... 25-40

VI. Nonprofit organizations associated with hospitals and universities........ 41-42

3

REVIEW GUIDE FOR

NONPROFIT ORGANIZATIONS

INDIRECT COST RATE PROPOSALS

I. INTRODUCTION:

This review guide was developed to assist Division of Cost Allocation (DCA) staff in reviewing andnegotiating indirect cost proposals for nonprofit organizations. The guide presents a number ofideas, facts and concerns that should be considered during the review of indirect cost proposals.Alternative approaches and allocation methods, including their strong and weak points are presentedand discussed in detail. While this guide is reasonably detailed and comprehensive, it is notintended to be a substitute for professional experience and judgement.

The Office of Management and Budget (OMB) issues cost principles for all Federal agencies thatsponsor research, training and other work at nonprofit organizations. OMB Circular A-122 establishesprinciples for determining costs applicable to grants and contracts with nonprofit organizations.The principles deal with the subject of cost determination and are designed to provide that theFederal Government bear its fair share of total allowable and allocable costs, except whererestricted or prohibited by law. In general, the Circular defines the attributes associated with anonprofit organization. It also provides general definitions regarding the applicability, allowability and reasonableness of different types of costs. The Circular describes the differentallocation bases that can be used by nonprofit organizations. Attachment B of Circular A-122provides a list of “selected items of cost” and how these costs should be treated. There have beenseveral revisions to the Circular since its inception on June 27, 1980. Prior to its inception,individual agencies issued their own cost principles with regard to nonprofit organizations. The most recent update of the Circular is dated June 1, 1998. Revisions also were made to CircularA-122 in the years 1984, 1987, 1995 and 1997. These revisions were widely disseminated to thenonprofit community and are considered Department policy. DCA staff should therefore be familiarwith the revisions.

4

Indirect costs are those expenses that benefit common activities and therefore cannot be readilyassigned to a specific cost objective or project. At nonprofit organizations, such costs normallyare classified into one overall pool of costs. This pool is then divided by the allocation base the nonprofit organization has chosen in order to calculate a rate.The preparation of an indirect cost proposal can be a significant undertaking for a nonprofitorganization, that generally has to be done on an annual basis.

The decision that a cost proposal needs a more in-depth review and analysis by the DCA will beinfluenced by many factors. One purpose of this review guide is to help a negotiator identifyfactors that will help determine what type of review is necessary.

5

II. REVIEW STEPS:

A. REQUIRED DOCUMENTATION

STEPS COMMENTS

1. Determine whether the proposal package iscomplete, in sufficient detail to permit anadequate review, and is in a format thatcan be readily followed by the negotiator.

2. Make sure that any information specificallyrequested by the DCA in prior correspondence or in advanced agreementsestablished in previous negotiations isincluded in the proposal package.

The proposal package should include:

o The proposal itself. A separate columnshould be used for each direct activity(Federal grants, non-Federal grants, fundraising, etc.) of the organization. A separate column should also be used forindirect costs. These columns should showthe type (e.g., labor, travel, supplies,etc.) and amount of costs incurred by eachactivity.

o Audited financial statements.

o A detailed and understandablereconciliation between the proposal andfinancial statements, showing eachreclassification and adjustment to thefinancial statement accounts.

6

STEPS COMMENTS

o A “notice of grant award” or a “financialassistance award document” that shows thenonprofit organization has a currentFederal award that is eligible to receiveindirect costs. Training grants or grantswhere the amount of indirect costs isfixed (e.g., Dept. of Education, 8%training grant, etc.) do not meet thisrequirement. Also, DCA is not required toissue a rate that will be used strictlyfor “matching requirements” on grants.

7

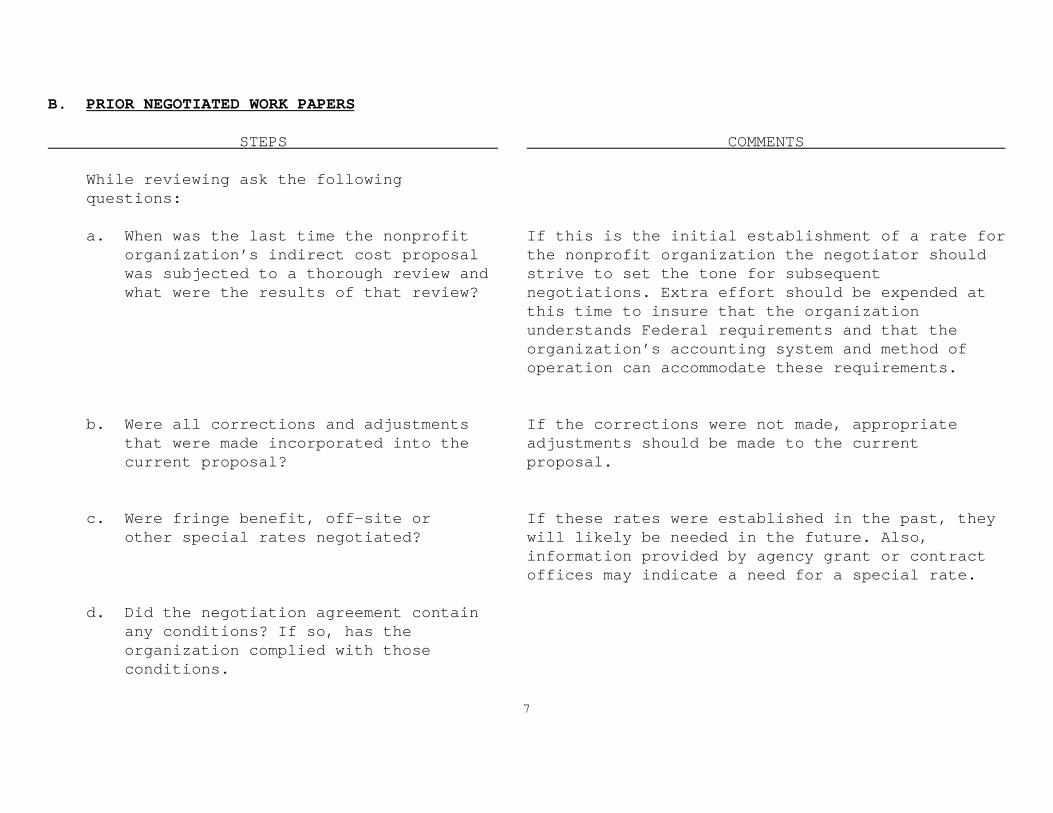

B. PRIOR NEGOTIATED WORK PAPERS

STEPS

While reviewing ask the followingquestions:

a. When was the last time the nonprofitorganization’s indirect cost proposalwas subjected to a thorough review andwhat were the results of that review?

b. Were all corrections and adjustmentsthat were made incorporated into thecurrent proposal?

c. Were fringe benefit, off-site orother special rates negotiated?

d. Did the negotiation agreement containany conditions? If so, has theorganization complied with thoseconditions.

COMMENTS

If this is the initial establishment of a rate forthe nonprofit organization the negotiator shouldstrive to set the tone for subsequentnegotiations. Extra effort should be expended atthis time to insure that the organizationunderstands Federal requirements and that theorganization’s accounting system and method ofoperation can accommodate these requirements.

If the corrections were not made, appropriateadjustments should be made to the currentproposal.

If these rates were established in the past, theywill likely be needed in the future. Also,information provided by agency grant or contractoffices may indicate a need for a special rate.

8

STEPS

e. If fixed rates were negotiated, doesthe carry-forward amount in the currentproposal agree with the prior writtencarry-forward agreement?

f. Compare the submission with priornegotiations and identify any items inthe proposal which appear unusual andare not discussed in the proposalpackage.

g. Determine whether the proposal requiresan extensive review and/or site visit.

h. Perform a “math check” to ensure theaccuracy of the organization’scomputations.

COMMENTS

See the Trend Analysis section of this guide formore details regarding this requirement.

Normally a review of a nonprofit organization canbe achieved without performing a site visit.Exceptions to this could be if the organizationhas multiple rates applicable to differentfunctions or significant specialized servicefacilities,etc.

9

STEPS

i. Determine the type of rates to benegotiated.

COMMENTS

A significant number of nonprofit organizationswill have their rates negotiated on an annualbasis using provisional/final type rates. However, nonprofit organizations can alsonegotiate predetermined rates when facts aresufficient for both parties to reach an informedjudgement as to future rates.Note: An organization that has any Federalcontracts cannot be given a predetermined rate(per an 11/10/82 GAO ruling).

10

C. RECONCILE PROPOSAL TO THE FINANCIAL STATEMENTS

Costs included on the proposal must be reconciled to the financial statements. A brief review of thefinancial statement itself can provide the negotiator with some insight regarding the nonprofitsorganizational structure, accounting system and costing methodologies. This can be helpful in theproposal review process. The reconciliation should be completed by the organization and submittedwith their proposal. If the proposal has not been reconciled to the financial statements thenonprofit should be notified immediately. A review of the proposal should be delayed until this stepis completed.

STEPS

1. Reconcile the cost proposal to the auditedfinancial statements.

COMMENTS

The first step is to reconcile total costs, bothallowable and unallowable, to the total costsshown on the audited financial statements.

2. Once the negotiator is assured that thetotal costs, direct and indirect, includedin the indirect cost proposal agree withthe audited financial statements, analyzethe adjustments for unallowable andextraneous costs that should be excludedfrom the proposal, and those that should beallocated their share of indirect costs.

Unallowable and un-allocable costs (e.g., baddebts, fines, penalties, etc.) should always beeliminated from the indirect cost pool before thepool is allocated to each direct program. However,unallowable functions (e.g., fund raising, etc.)and non-reimbursable activities (e.g., donatedlabor or services that meet Circular A-122requirements) should be treated as directfunctions and receive their proper distribution ofindirect costs. Indirect costs allocated to thesefunctions are not reimbursed by the federalprograms. To do this would dilute requiredmatching ratios.

11

STEPS

3. Analyze and verify the accuracy andnecessity for adjustments andreclassifications.

COMMENTS

The negotiator must understand every substantialreclassification and why it is taking place.Understanding this process is an important part ofthe proposal review.

12

D. ACCEPTABLE BASE (MTDC, SW, SW+FB) STEPS

1. Determine that the proposed base results in an equitable distribution of indirectcosts.

The three most common bases used bynonprofit organizations are as follows:

a) Modified Total Direct Cost (MTDC): This base includes all direct costs incurred by the organization with the exception of distorting items such as, capital expenditures, subcontracts, flow through funds, etc.

b) Salaries and Wages (SW): This base includes only the direct salaries and wages incurred by the organization.

c) Salaries and Wages plus Fringe Benefits (SW+FB): This base includes only the direct salary and wages and the direct fringe benefits incurred by the organization.

2. Analyze and verify that the base theorganization is proposing is consistentwith the base they’ve used in previoussubmissions and on the rate agreement.

COMMENTS

Generally, if the proposed base conforms to thesuggested or required bases they should beaccepted. However, there may be circumstanceswhich indicates that an inequity will result if asuggested base is used. For example, anorganization uses a modified total direct costbase, however, they have one grant that has adisproportionate amount of “other direct costs.”This could distort the amount of indirect coststhat are allocated to that program. Therefore, asalary and wage base might be more equitable.

Below are a few examples of possibleinconsistencies a negotiator could encounter whenreviewing a nonprofit organization’s base:

- The organizations’s previous rate agreementshowed a base of salaries & wages including paidabsences. However, the organization’s proposalsubmission shows paid absences as part of thefringe benefit pool.

- The organization’s previous rate agreementshowed a base of salaries & wages including fringebenefits. However, the organization’s proposalsubmission does not include fringe benefits in thebase.

13

STEPS COMMENTS

- The organizations’s previous rate agreementshowed a base of modified total direct costs thatincluded the first $25,000 of sub-awards in thebase. However, the organization’s proposalsubmission does not include any subcontractorcosts in the base.

14

E. TREND ANALYSIS

A trend analysis of the nonprofit organization’s indirect costs, rates, and allocation baseshould be performed during the preliminary review of each cost proposal. A trend analysis canbe completed in a short period of time and frequently provides the negotiator with an insightinto the areas of the proposal needing a more detailed review.

STEPS

COMMENTS

1. Perform a detailed trend analysis of thenonprofit organization’s indirect costs,rates, and allocation base for the lastthree years, including the proposal year.

A basic trend analysis is simply plotting the rawrate value of each indirect cost along with theapplicable base involved. This provides thenegotiator not only with a idea of where the rateis changing (e.g., increasing or decreasing), butshould also indicate what items of costs anegotiator should spend time reviewing.

It is very important for a negotiator to comparehow much certain indirect costs are increasingwhen compared to the increases in the nonprofitorganization’s direct base.

Here are a couple of examples regarding what mightbe discovered through trend analysis:

- An organization’s direct cost base has increasedby 5%, however, their indirect travel hasincreased by 40%. In this case it would be prudentfor the negotiator to inquire about the largeindirect travel increase.

15

STEPS COMMENTS

- An organization’s indirect supplies hasincreased 25% but its base has increased 30%. In this case although the indirect supplies haveincreased considerably they are still increasingat a slower rate than the base. This is a fairlynormal occurrence and probably would not requireany further inquiry by the negotiator.

16

F. ALLOWABILITY, CONSISTENCY AND TREATMENT OFCOSTS

STEPS

1. Determine whether the proposed costs benefitFederal awards.

2. Determine if the types of costs included inthe indirect cost pool are consistently treatedas indirect costs.

3. Review the proposal and financial statementsto determine whether the indirect cost poolincludes any unallowable costs.

4. Review the financial statements to determineif there are any applicable off-sets.

COMMENTS

Generally an expense that is necessary to theoverall operation of the nonprofit organization is allocable to Federal awards. When there is amulti-tier distribution involving more than onepool, the criteria is; does the expense benefitall activities included in the particulardistribution base?

The nonprofit organization should be queried todetermine whether any costs included in theindirect cost pool have also been charged to anyFederal awards as direct costs. Where such costsare charged directly, they should be removed fromthe indirect cost pool except to the extent thatthey apply to indirect activities.

Some examples of unallowable costs would include,alcoholic beverages, bad debts, contingencies,contributions and donations, entertainment, finesand penalties, fund raising, lobbying, etc.

Income generated by the activities in the indirectcost pool and certain negative expenditure typesof transactions should be used to off-set orreduce expenses in the indirect cost pool (e.g.,parking fees, purchase discounts, etc.).

17

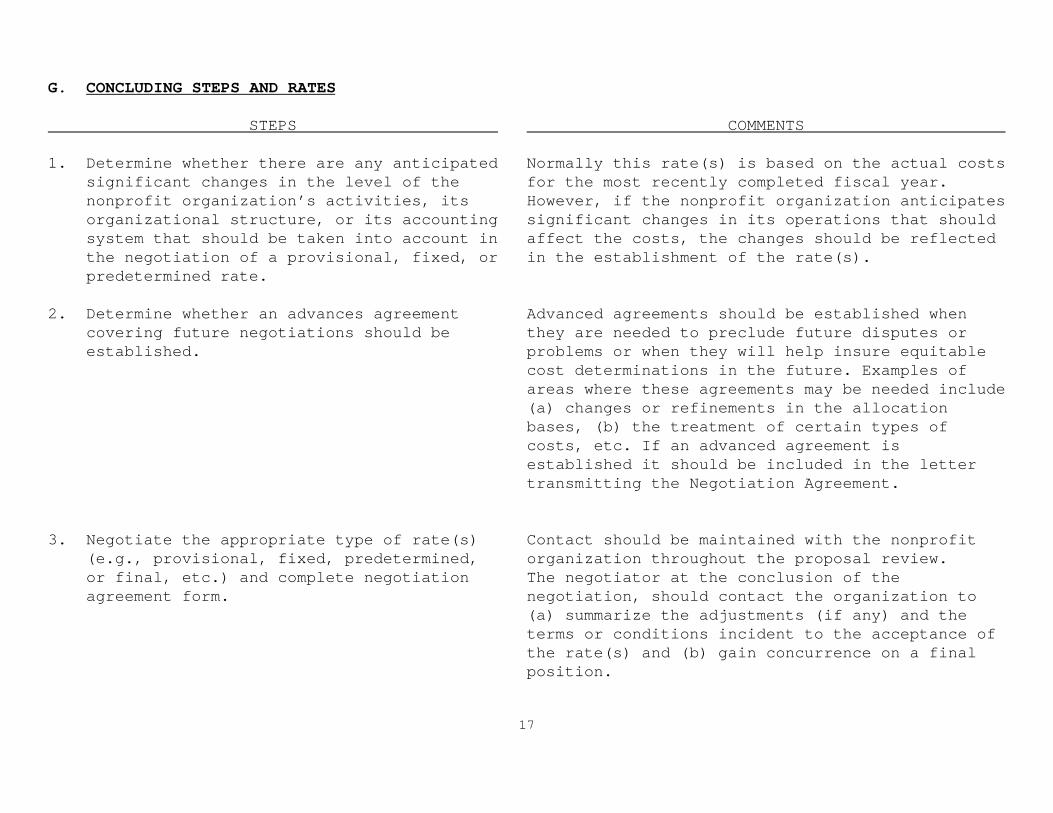

G. CONCLUDING STEPS AND RATES

STEPS

1. Determine whether there are any anticipatedsignificant changes in the level of thenonprofit organization’s activities, itsorganizational structure, or its accountingsystem that should be taken into account inthe negotiation of a provisional, fixed, orpredetermined rate.

2. Determine whether an advances agreementcovering future negotiations should beestablished.

3. Negotiate the appropriate type of rate(s)(e.g., provisional, fixed, predetermined,or final, etc.) and complete negotiationagreement form.

COMMENTS

Normally this rate(s) is based on the actual costsfor the most recently completed fiscal year.However, if the nonprofit organization anticipatessignificant changes in its operations that shouldaffect the costs, the changes should be reflectedin the establishment of the rate(s).

Advanced agreements should be established whenthey are needed to preclude future disputes orproblems or when they will help insure equitablecost determinations in the future. Examples ofareas where these agreements may be needed include(a) changes or refinements in the allocationbases, (b) the treatment of certain types ofcosts, etc. If an advanced agreement isestablished it should be included in the lettertransmitting the Negotiation Agreement.

Contact should be maintained with the nonprofitorganization throughout the proposal review. The negotiator at the conclusion of thenegotiation, should contact the organization to(a) summarize the adjustments (if any) and theterms or conditions incident to the acceptance ofthe rate(s) and (b) gain concurrence on a finalposition.

18

STEPS COMMENTS

Guidance on the circumstances under which costsshould be negotiated on a provisional, final,fixed, or predetermined basis are as follows:

- Provisional rates will be used only in thosesituations in which the negotiator has littleconfidence in the rate proposed and cannotnegotiate a rate which will fairly reflect theorganization’s operations during the period towhich the rate applies. Provisional rates shouldalso be used when (i) the propriety of the ratesare contingent upon the occurrence of a futureevent which is uncertain at the time ofnegotiation or (ii) the organization plans toreorganize or otherwise substantially change itsoperations in the future. When a provisional rateis established, a final rate must be negotiatedwhen the actual costs for the period become known.

- Predetermined rates may only be negotiated inthose situations where there is a high probabilitythat the rate negotiated will result in a dollarrecovery to the organization not in excess of theamount that would have been recovered had the ratebeen established on an “after the fact” basis. Predetermined rates are not authorized if thereare Federal contracts awarded to the organization.

19

STEPS COMMENTS

- Fixed rates with carry forward provisions may beused except where the carry forward adjustmentwould be difficult or impossible to make because:

(i) the organization is unlikely to have activeawards in future periods to affect thecarryforward adjustment,(ii) the mix of Federal/non-Federal work performedby the organization from year to year is tooerratic to permit a fair carry-forward adjustment,(iii) the operating activities of the organizationare unstable,(iv) the negotiator is not satisfied that the rateproposed will approximate the actual rate.

The negotiator should avoid setting fixed rateswhich result in major carry-forward adjustments.Consider setting limitations on the amount ofpermissible adjustments (e.g., spread over morethan one fiscal year, etc.).

If a fixed, final or predetermined rate is used, aprovisional rate would normally be established tocover the period subsequent to the period coveredby the fixed, final or predetermined rate. Thiswill preclude potential problems in fundingawards made after the expiration of the fixed,final, or predetermined rate.

20

STEPS

4. Complete Summary of Negotiations

COMMENTS

A summary of negotiations should be prepared whichshows the amounts negotiated that are differentfrom the amounts submitted, and the reasons forthe negotiated differences. The summary should besufficiently detailed to permit an independentreviewer to quickly see and understand how thenegotiated rates were computed.

21

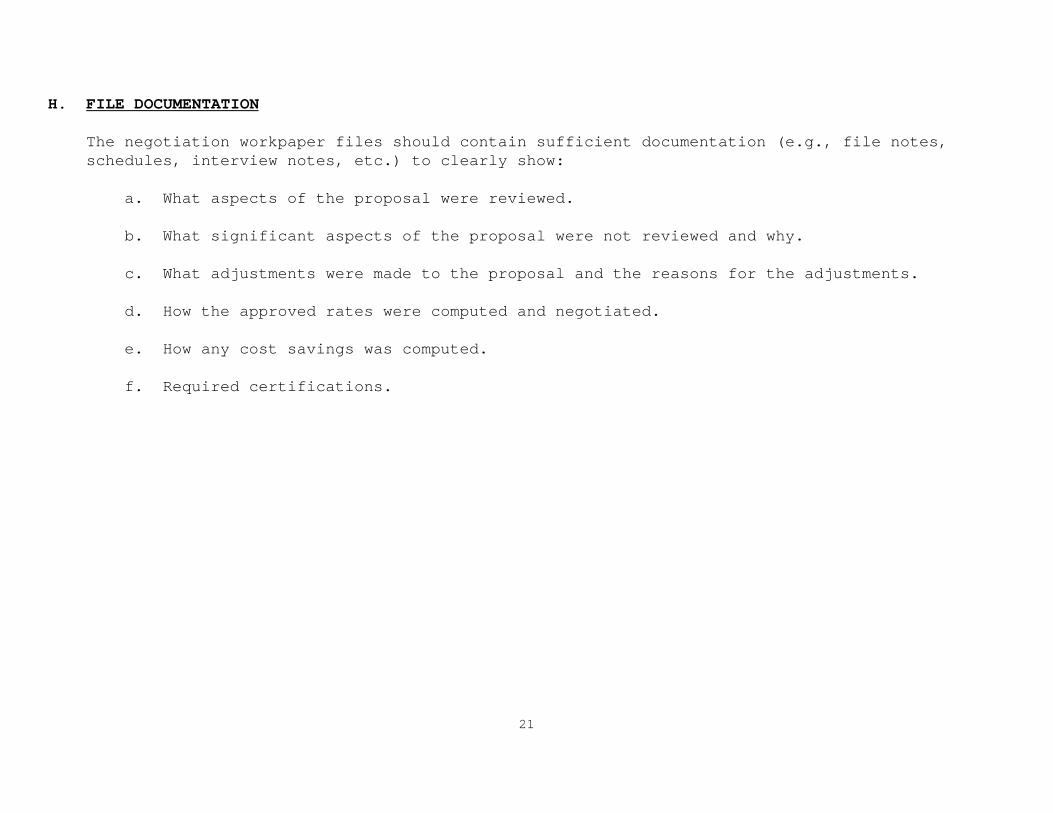

H. FILE DOCUMENTATION

The negotiation workpaper files should contain sufficient documentation (e.g., file notes,schedules, interview notes, etc.) to clearly show:

a. What aspects of the proposal were reviewed.

b. What significant aspects of the proposal were not reviewed and why.

c. What adjustments were made to the proposal and the reasons for the adjustments.

d. How the approved rates were computed and negotiated.

e. How any cost savings was computed.

f. Required certifications.

22

I. REFERENCE MATERIAL

- OMB Circular A-122, “Cost Principles for Non-Profit Organization.”

- OMB Circular A-110, “Uniform Administrative Requirements for Grants and Agreements withInstitutions of Higher Education, Hospitals, and Other Non-profit Organizations.”

- OMB Circular A-133, “Audits of States, Local Governments, and Non-Profit Organization.”

- ASMB C-5, “A Guide for Nonprofits.”

- Grants Administration Manual/Grants Policy Directives.

- 45 CFR Part 16, “Procedures of the Departmental Grants Appeals Board.”

- 45 CFR Part 74, “Uniform Administrative Requirements for Awards and Subawards toInstitutions of Higher Education, Hospitals, Other Nonprofit Organizations, andCommercial Organizations; And Certain Grants and Agreements with States, LocalGovernments and Indian Tribal Governments” - Departmental Implementing Regulations for OMB A-110.

- Internet Sites:

- OMB Circulars - www.whitehouse.gov/omb/grants/index.html- GASB Statements - www.rutgers.edu/Accounting/raw/gasb/st/summary- FASB Statements - www.rutgers.edu/Accounting/raw/fasb/st/summary- HHS Cost Policy Issuances (including ASMB C-5) - www.hhs.gov/progorg/grantsnet- CFR Sections - www.access.gpo.gov/nara/cfr/index.html- DAB Decisions - www.hhs.gov/dab/index.html- Actuarial Standards of Practice - www.actuary.org/standard.htm

23

III. ALLOCATION METHODOLOGIES:

There are three common allocation methodologies that a nonprofit organization can use to allocatecosts. They are the “direct allocation method,” the “simplified allocation method,” and the“multiple allocation base method.” These methods are defined as follows:

A. DIRECT ALLOCATION METHOD

This method should be used by nonprofit organizations that elect to charge their programs(e.g.,grants) directly for all costs except those identified as “support services” costs. These nonprofit organizations usually separate their costs into two basic categories:

(1) Program services - these include direct functions such as community service activities, research, education and training.

(2) Supporting services - these include general administration and general expenses.

Joint costs such as depreciation, operation and maintenance, utilities, are prorated individually toeach program (grant) or activity and to the supporting services (management and general) function.These costs will be allocated using an appropriate distribution base. The direct allocationmethodology is acceptable provided each joint cost is prorated on a distribution base which isestablished in accordance with reasonable and consistently applied criteria, adequately supported bycurrent data of the organization and, based on the benefits received. Examples of appropriatedistribution bases along with how to employ this methodology are shown in document ASMB C-5 “A GuideFor Nonprofits.”

B. SIMPLIFIED ALLOCATION METHOD

This method should be used when all of the nonprofit organizations major functions benefit from aparticular indirect cost expense by approximately the same degree. This method should also be usedwhen a nonprofit organization has only one major function encompassing a number of individualprojects (grants) or activities. Examples of appropriate distribution bases along with how to employthis methodology are shown in document ASMB C-5 “A Guide For Nonprofits.”

24

C. MULTIPLE ALLOCATION BASE METHOD

This method should be used when a nonprofit organization has several major functions which benefitfrom its indirect costs in varying degrees. Indirect costs are accumulated into separate costgroupings, such as groupings for general and administrative expenses, and a grouping fordepreciation and other facility expenses. Each grouping should contain a pool of expenses that areof like character in terms of the functions they benefit and the allocation base which best measuresthe relative benefits provided to each function. Each grouping is then allocated individually to thebenefitting functions by means of a base which best measures the relative benefits to each function.The number of separate groupings should be held within practical limits, taking into considerationthe materiality of the amount involved and the degree of precision desired. Indirect cost allocatedto each function are then distributed to individual awards and other direct activities included inthat function by means of an indirect cost rate. Examples of appropriate distribution bases alongwith how to employ this methodology are shown in document ASMB C-5 “A Guide For Nonprofits.”

It should be noted that most nonprofit organizations use either the “direct allocation method” orthe “simplified allocation method.”

25

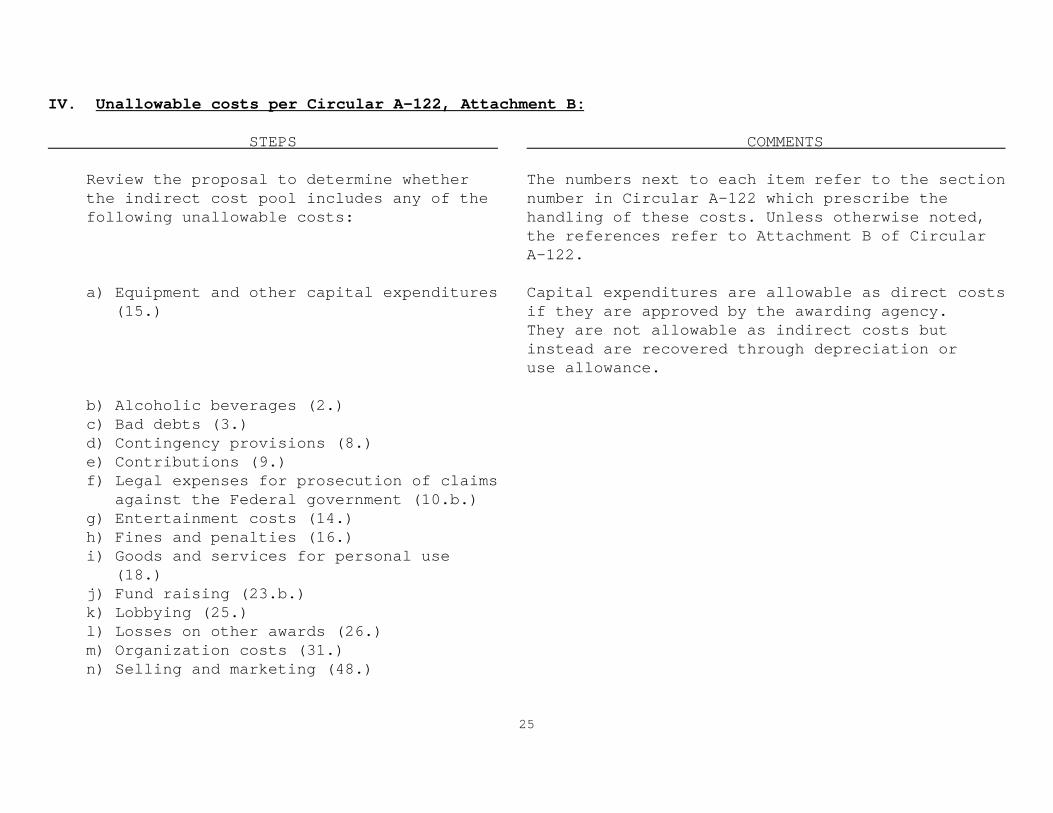

IV. Unallowable costs per Circular A-122, Attachment B:

STEPS COMMENTS

Review the proposal to determine whetherthe indirect cost pool includes any of thefollowing unallowable costs:

a) Equipment and other capital expenditures (15.)

b) Alcoholic beverages (2.)c) Bad debts (3.) d) Contingency provisions (8.) e) Contributions (9.)f) Legal expenses for prosecution of claims against the Federal government (10.b.) g) Entertainment costs (14.)h) Fines and penalties (16.)i) Goods and services for personal use (18.)j) Fund raising (23.b.)k) Lobbying (25.)l) Losses on other awards (26.)m) Organization costs (31.)n) Selling and marketing (48.)

The numbers next to each item refer to the sectionnumber in Circular A-122 which prescribe thehandling of these costs. Unless otherwise noted,the references refer to Attachment B of CircularA-122.

Capital expenditures are allowable as direct costsif they are approved by the awarding agency. They are not allowable as indirect costs butinstead are recovered through depreciation or use allowance.

26

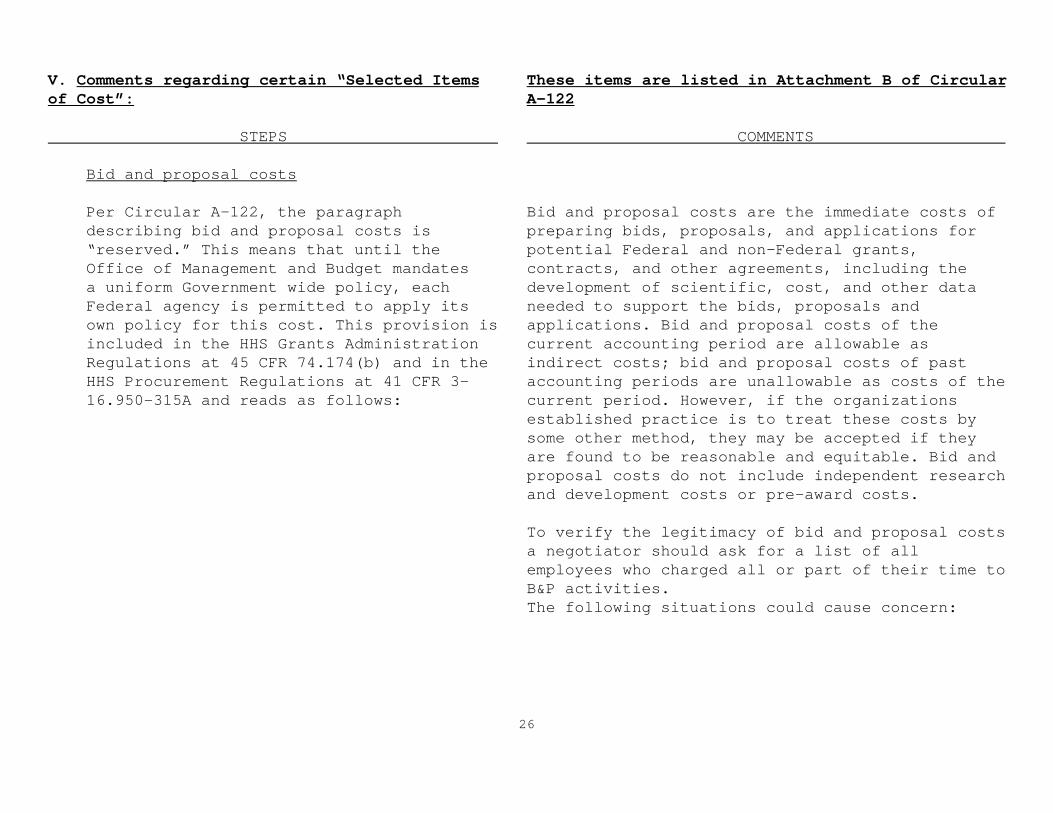

V. Comments regarding certain “Selected Itemsof Cost”:

STEPS

Bid and proposal costs

Per Circular A-122, the paragraphdescribing bid and proposal costs is“reserved.” This means that until theOffice of Management and Budget mandates a uniform Government wide policy, eachFederal agency is permitted to apply itsown policy for this cost. This provision isincluded in the HHS Grants AdministrationRegulations at 45 CFR 74.174(b) and in theHHS Procurement Regulations at 41 CFR 3-16.950-315A and reads as follows:

These items are listed in Attachment B of CircularA-122

COMMENTS

Bid and proposal costs are the immediate costs ofpreparing bids, proposals, and applications forpotential Federal and non-Federal grants,contracts, and other agreements, including thedevelopment of scientific, cost, and other dataneeded to support the bids, proposals andapplications. Bid and proposal costs of thecurrent accounting period are allowable asindirect costs; bid and proposal costs of pastaccounting periods are unallowable as costs of thecurrent period. However, if the organizationsestablished practice is to treat these costs bysome other method, they may be accepted if theyare found to be reasonable and equitable. Bid andproposal costs do not include independent researchand development costs or pre-award costs.

To verify the legitimacy of bid and proposal costsa negotiator should ask for a list of allemployees who charged all or part of their time toB&P activities. The following situations could cause concern:

27

STEPS COMMENTS

a) Employee(s) who charge most of their time to adirect project and a small portion to B&P and/oremployee(s) who charged most of their time in the previous year to a direct project are now chargingmost of their time to B&P.

b) The nonprofit organization cannot document theactual B&P projects that the employees worked on.

28

STEPS

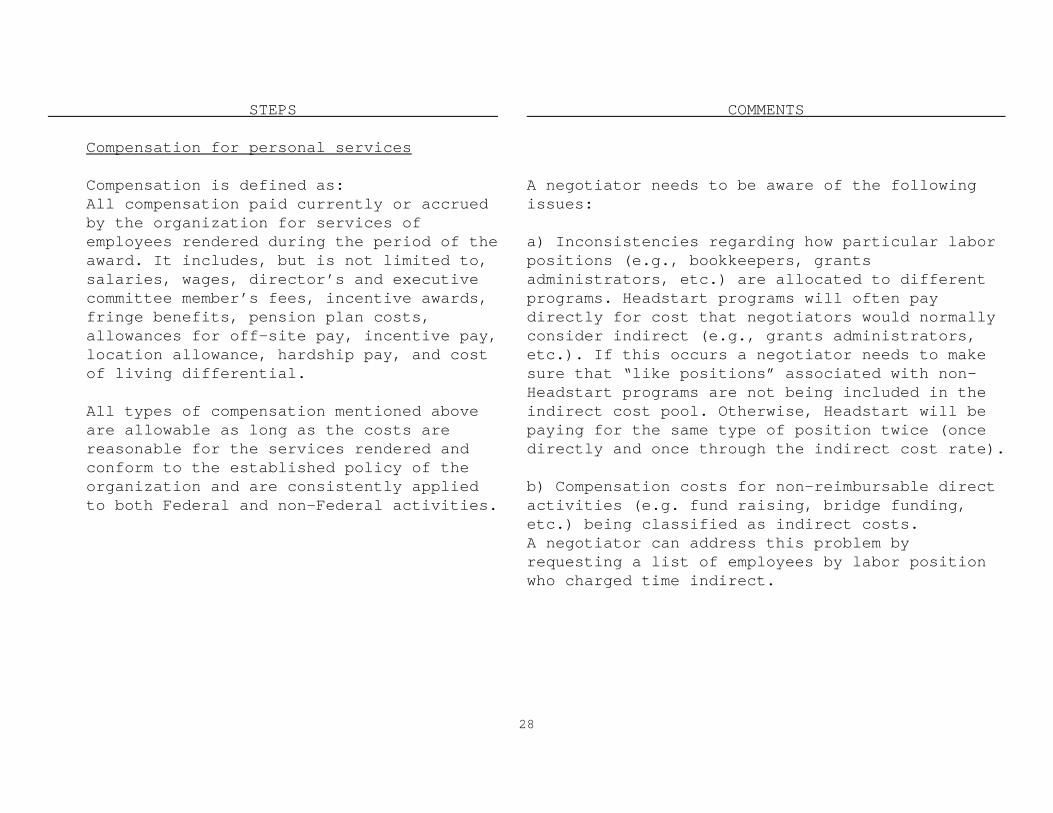

Compensation for personal services

Compensation is defined as:All compensation paid currently or accruedby the organization for services ofemployees rendered during the period of theaward. It includes, but is not limited to,salaries, wages, director’s and executivecommittee member’s fees, incentive awards,fringe benefits, pension plan costs,allowances for off-site pay, incentive pay,location allowance, hardship pay, and costof living differential.

All types of compensation mentioned aboveare allowable as long as the costs arereasonable for the services rendered andconform to the established policy of theorganization and are consistently appliedto both Federal and non-Federal activities.

COMMENTS

A negotiator needs to be aware of the followingissues: a) Inconsistencies regarding how particular laborpositions (e.g., bookkeepers, grantsadministrators, etc.) are allocated to differentprograms. Headstart programs will often paydirectly for cost that negotiators would normallyconsider indirect (e.g., grants administrators,etc.). If this occurs a negotiator needs to makesure that “like positions” associated with non-Headstart programs are not being included in theindirect cost pool. Otherwise, Headstart will bepaying for the same type of position twice (oncedirectly and once through the indirect cost rate).

b) Compensation costs for non-reimbursable directactivities (e.g. fund raising, bridge funding,etc.) being classified as indirect costs. A negotiator can address this problem byrequesting a list of employees by labor positionwho charged time indirect.

29

STEPS

Depreciation and use allowances

Depreciation or use allowance is anallowable costs as long as certain criteriaare met. See Circular A-122 for a list ofthe criteria.

COMMENTS

A negotiator should be aware of the followingthings with regard to this item of cost:

a) Make sure that no depreciation applicable toassets bought with Federal sponsored program fundsor non-Federal (private industry, state grants,etc.) sponsored program funds are included in theproposal.

b) Make sure no depreciation or use allowance isincluded in the proposal that is applicable toidle facilities.

c) The unamortized portion of any equipmentwritten off as a result of a change incapitalization levels may be recovered bycontinuing to claim the otherwise allowable useallowances or depreciation on the equipment, or by amortizing the amount to be written off over a period of years as negotiated with the Federalcognizant agency.

30

STEPS

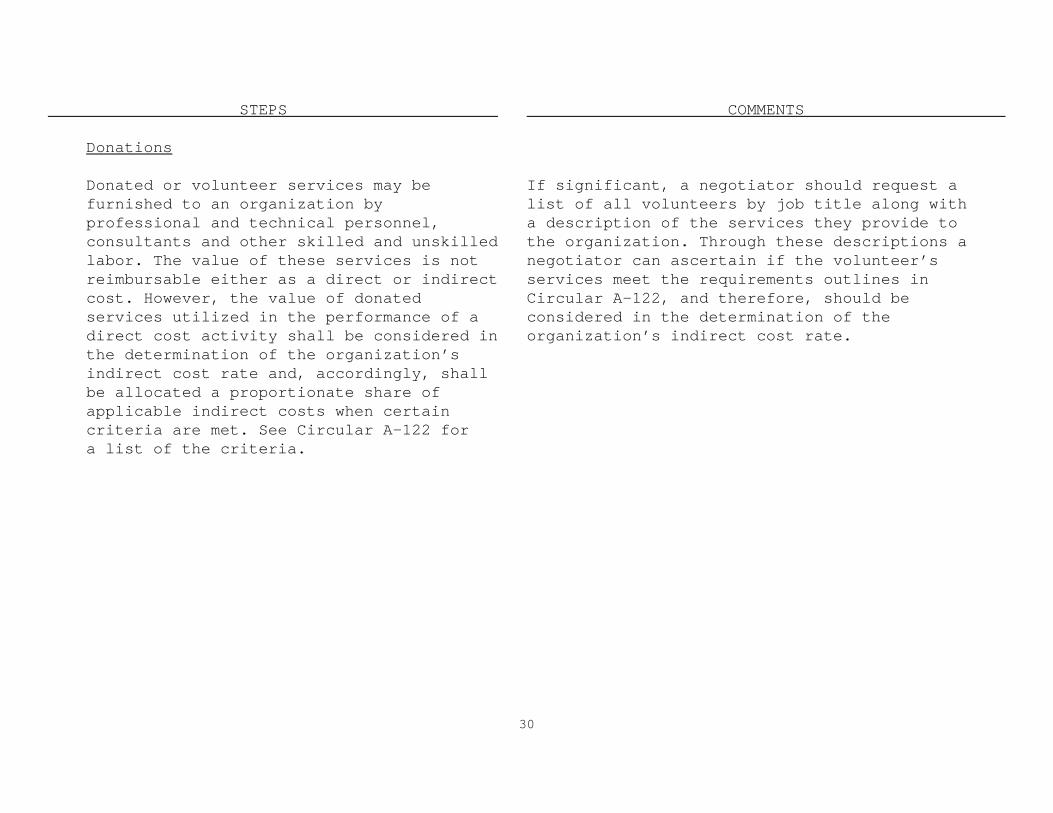

Donations

Donated or volunteer services may befurnished to an organization byprofessional and technical personnel,consultants and other skilled and unskilledlabor. The value of these services is notreimbursable either as a direct or indirectcost. However, the value of donatedservices utilized in the performance of adirect cost activity shall be considered inthe determination of the organization’sindirect cost rate and, accordingly, shallbe allocated a proportionate share ofapplicable indirect costs when certaincriteria are met. See Circular A-122 for a list of the criteria.

COMMENTS

If significant, a negotiator should request a list of all volunteers by job title along with a description of the services they provide to the organization. Through these descriptions anegotiator can ascertain if the volunteer’sservices meet the requirements outlines inCircular A-122, and therefore, should beconsidered in the determination of theorganization’s indirect cost rate.

31

STEPS

Fringe benefits

1) Fringe benefits in the form of regularcompensation paid to employees duringperiods of authorized absences from thejob, such as vacation leave, sick leave,military leave, and the like, areallowable, provided such costs are absorbedby all organization activities inproportion to the relative amount of timeor effort actually devoted to each.

2) Fringe benefits in the form of employercontributions or expenses for socialsecurity, employee insurance, workmen’scompensation insurance, pension plan costs,and the like, are allowable, provided suchbenefits are granted in accordance withestablished written organization policies.Such benefits whether treated as indirectcosts or as direct costs, shall bedistributed to particular awards and otheractivities in a manner consistent with thepattern of benefits accruing to theindividuals or group of employees whosesalaries and wages are chargeable to suchawards and other activities.

COMMENTS

There are two different methods an organizationcan use to allocate fringe benefit costs. They are as follows:

Specific identification method: This method involves “specifically assigning” the actual fringe benefit costs incurred by a “particular employee” to that “particularemployee.”

Fringe benefit rate(s):This method involves developing a rate(s) for allemployees in the organization. The rate could bethe same for everyone or there could be severaldifferent rates depending on the employees jobclassification (e.g., professional, clerical,etc.).The rate is calculated by taking the total fringebenefit costs incurred and dividing that amount bythe total salary and wage costs incurred for thetotal organization or the class of employees forwhich you are developing a rate.

32

STEPS

3) Provisions for a reserve under a selfinsurance program for unemploymentcompensation or workers’ compensation areallowable to the extent that the provisionsrepresent reasonable estimates of theliabilities for such compensation, and thetypes of coverage, extent of coverage, andrates and premiums would have beenallowable had insurance been purchased tocover the risks. However, provisions forself-insured liabilities which do notbecome payable for more than one year afterthe provision is made shall not exceed thepresent value of the liability.

4) Where an organization follows aconsistent policy of expensing actualpayments to, or on behalf of employees or former employees for unemploymentcompensation or workers’ compensation, such payments are allowable in the year of payment with the prior approval of the awarding agency, provided they areallocated to all activities of theorganization.

COMMENTS

33

STEPS

5) Costs of insurance on the lives oftrustees, officers, or other employeesholding positions of similar responsibilityare allowable only to the extent that theinsurance represents additionalcompensation. The costs of such insurancewhen the organization is named asbeneficiary are unallowable.

6) Organization furnished automobiles. That portion of the cost of organizationfurnished automobiles that relates topersonal use by employees (includingtransportation to and from work) isunallowable as fringe benefit or indirectcosts regardless of whether the cost isreported as taxable income to theemployees. These costs are allowable asdirect costs to sponsored awards whennecessary for the performance of thesponsored award and approved by theawarding agency.

COMMENTS

34

STEPS

Idle facilities and idle capacity

For this particular item of cost, thefollowing terms have the meanings set forthbelow:

Facilities means land and buildings or anyportion thereof, equipments individually orcollectively, or any other tangible capitalasset, wherever located, and whether ownedor leased by the organization.

Idle facilities means completely unusedfacilities that are in excess to theorganization’s current needs.

Idle capacity means the unused capacity ofpartially used facilities.

Costs of idle facilities or idle capacitymeans costs such as maintenance, repair,housing, rent, and other related costs,e.g., property taxes, insurance, anddepreciation or use allowance.

COMMENTS

If a negotiator identifies idle facilities theyshould inform the grantee of the requirementsunder Circular A-122. The negotiator should then set a time frameregarding when the organization would need tovacate the space if it remains unoccupied.

When making this determination the negotiatorneeds to understand that the cost of idlefacilities is unallowable except to the extentthat:

1) They are necessary to meet fluctuations in workload.

2) They were necessary when acquired and are nowidle because of changes in work requirements andefforts to achieve economical operations could notbe foreseen. General speaking with regard to this situation theorganization will be given a reasonable period oftime, ordinarily not to exceed one year to disposeof such facilities.

35

STEPS

Independent research and development

Per Circular A-122, the paragraphdescribing Independent research anddevelopment cost is “reserved.” This meansthat until the Office of Management andBudget mandates a uniform Government widepolicy, each federal agency is permitted toapply its own policy in this area. DHHS haselected to continue its long standingpolicy for this cost. This provision isincluded in the HHS Grants AdministrationRegulations at 45 CFR 74.174(b) and in theHHS Procurement Regulations at 41 CFR 3-16.950-315A.

COMMENTS

Independent research and development is researchand development that is not sponsored by Federalor non-Federal grants, contracts, or otheragreements. Independent research and developmentshall be allocated its proportionate share ofindirect costs on the same basis as the allocationof indirect costs to sponsored research anddevelopment. The costs of independent research anddevelopment, including its proportionate share ofindirect costs, are unallowable.

36

STEPS

Interest

Interest costs are allowable (subject tospecific conditions listed in Circular A-122) if they relate to debt incurred afterSeptember 29, 1995, to acquire or replacecapital assets acquired after this date andused in support of sponsored agreements.

COMMENTS

If an organization is claiming significantinterest expense the negotiator should determineif the interest is allowable per Circular A-122,also, the negotiator should determine ifadditional provisions mentioned in Attachment B,Paragraph 23.a., of Circular A-122, areapplicable.

It should be noted that costs incurred forinterest on borrowed capital or temporary use of endowment funds, however represented, areunallowable.

37

STEPS

Fund raising

Fund raising costs include financialcampaigns, endowment drives, solicitationof gifts and bequests, and similar expensesincurred solely to raise capital or obtaincontributions. These costs are unallowableas indirect costs.

COMMENTS

Nonprofit organizations may have separate anddistinct fund raising departments. These separatedepartments are often shown on the financialstatements and make it easier for a negotiator toidentify fund raising costs. When a negotiatorsees salaries and wages associated with fundraising they need to make sure that an appropriateamount of ”other costs” (e.g., telephone ,postage, etc.) associated with fund raising havealso been identified.

Other nonprofit organizations may not haveseparate and distinct fund raising departments.However, employees such as the Executive Directormay devote part of their time to fund raising. A negotiator may want to request positiondescriptions of various employees to ensure thatfund raising activities are classified properly,and where applicable, allocated an appropriateshare of indirect costs. Note: For purposes of computing an indirect costrate, fund raising costs must be included in thebase if they:(1)include salaries of personnel,(2) occupy space,and (3) benefit from indirect costs.

38

STEPS

Investment management costs

Investment management costs include costsof investment counsel and staff and similarexpenses incurred solely to enhance incomefrom investments. These costs areunallowable as indirect costs.

COMMENTS

A negotiator should review the balance sheet ofthe organization and see what types of investmentsare disclosed. If the organization has a largeinvestment portfolio, yet shows no investmentmanagement costs in their proposal, the negotiatormay want to inquire further regarding theclassification of these costs. Note: For purposes of computing an indirect costrate, investment management costs must beincluded in the base if they: (1) include salaries of personnel (2)occupy space,and (3) benefit from indirect costs.

39

STEPS

Participant support costs

Participant support costs are direct costsfor items such as stipends or subsistenceallowances, travel allowances, andregistration fees paid to or on behalf ofparticipants or trainees (but notemployees) in connection with meetings,conferences, symposia, or trainingprojects.These costs are allowable with the priorapproval of the awarding agency.

COMMENTS

Participant support costs are generally excludedfrom the base because these costs normally do notgenerate a significant amount of administrativecosts and normally do not generate any facilitiescosts such as building maintenance and operations.However, if participant support costs incurredrelate to training or other projects performed atthe site of the nonprofit organization and utilizeeither owned or rental facilities, a negotiatorshould determine whether or not the participantsupport costs should be excluded from the base.

40

STEPS

Rental costs

Rental costs are allowable, however, they are subject to several conditions. A brief description of these conditions are as follows:

a) Rental costs should be reasonable andconsistent with that of comparableproperties fair market value.

b) Rental costs under sale leaseback arrangements are allowable only up to the amount that would be allowed had the organization continued to own the property.

c) Rental costs under less than arms lengthleases are allowable only up to the amount that would be allowed had title to the property vested in the organization.

COMMENTS

Rental costs are allowable both as direct orindirect costs for reimbursement on Federalawards. However, great care should be exercised to ensure that rental cost incurred by theorganization are comparable to existing facilitiesin that general locale.

Negotiators need to be aware of less common rentalarrangements. Examples of these are “sale andleaseback” or rental costs that create materialequity in the leased property, both would besubject to ownership cost if:a) an organization that owns a facility/buildingsells to a related/unrelated entity and thenrents/leases back that same facility, or b) if the lease arrangement creates a materialequity such as a noncancellable lease with abargain purchase option, one in which a lowerpurchase price (e.g., below market value) is fixedat the inception of the lease or the lease termexceeds 75% of the economic life of the facility.

41

STEPS

d) Rental costs under leases which arerequired to be treated as capital leasesunder GAAP, are allowable only to theamount that would be allowed had theorganization purchased the property on thedate the lease agreement was executed(e.g., to the amount that minimally wouldpay for depreciation or use allowance,maintenance, taxes, and insurance). See Circular A-122 for a more expansivedefinition of this condition.

COMMENTS

A negotiator needs to verify if an organizationenters into a lease that is considered to be lessthan an arms length transaction, per Circular A-122 definition, such as, one with common boardmember(s), or officer(s), or between subsidiaryand parent company.These types of arrangements represent joint/commonownership the purpose of which could be toexercise control over the lessor in fixing theoccupancy/rental charge.Negotiators must ensure that the lessor/lesseerelationship is independent of one another byasking questions relative to occupancy/rentalcosts.

For all of the above cited conditions, ifownership is established then ownership costs,such as depreciation/use allowance, maintenance,taxes, insurance and qualifying interest expensewould be allowed and any rental cost included inthe indirect cost proposal that is in excess ofownership costs would be disallowed.

42

VI. OTHER AREAS:

Nonprofit organizations associated with hospitals and universities

Nonprofit organizations can be affiliated with other types of organizations. These affiliationscould be in the form of space being occupied on the premises of an affiliate, administrative costsof a nonprofit organization being handled by the affiliate or other types of arrangements. Below are some issues that a negotiator should be aware of when negotiating with nonprofitorganizations affiliated with hospitals and universities.

1) If a nonprofit organization is affiliated with a hospital the following issues need to beaddressed regarding space and administrative costs.

- SPACE If a nonprofit organization is occupying space owned by the hospital the negotiator needs todetermine who is paying for the space costs that the nonprofit organization is occupying.If the nonprofit organization is claiming space costs (e.g., rent expense, etc.) in their proposalthe negotiator needs to request a copy of the hospitals medicare cost report. This report shouldshow an adjustment for space costs claimed by the hospital to take into account the space occupiedby the nonprofit organization. If the negotiator does not see an adjustment in the medicare costreport then the space costs related to the nonprofit organization could be getting reimbursed twice.Once by medicare and once through the nonprofit organization’s indirect cost rate.

- ADMINISTRATION If a nonprofit organization includes costs in their proposal that they paid to the hospital tohandle administrative functions of the nonprofit (e.g., payroll, etc.) the negotiator needs torequest a copy of the hospitals medicare cost report. This report should show an adjustment foradministrative costs claimed by the hospital to take into account the reimbursement foradministrative services paid to the hospital by the nonprofit organization. If the negotiator doesnot see an adjustment in the medicare cost report then the administrative costs relating to thenonprofit organization could be getting reimbursed twice. Once by medicare and once through theindirect cost rate.

43

Nonprofit organizations associated with hospitals and universities (continued)

2) If a nonprofit organization is affiliated with a university the following issues need to beaddressed regarding space and administrative costs.

- SPACEIf a nonprofit organization is occupying space owned by the university the negotiator needs todetermine who is paying for the space costs that the nonprofit organization is occupying.If the nonprofit organization is claiming space costs (e.g., rent expense, etc.) in their proposalthe negotiator needs to contact an official of the university to see how the university isclassifying the space. If DCA negotiates rates with the university the negotiator should review theuniversities previous indirect cost proposal submission. The proposal submission should show anadjustment for space costs claimed by the university to take into account the space occupied by thenonprofit organization. If the negotiator does not see an adjustment in the universities proposalthen the space costs associated with the nonprofit organization could be getting reimbursed twice.Once through the universities indirect cost rate and once through the nonprofit organization’sindirect cost rate.

- ADMINISTRATION If a nonprofit organization includes costs in their proposal that they paid to the university tohandle administrative functions of the nonprofit (e.g., payroll etc.) the negotiator needs tocontact an official of the university to see if the university is offsetting their administrativecosts by the amount paid to them by the nonprofit organization. If DCA negotiated rates with the university the negotiator should review the universities previousindirect cost proposal. The proposal should show an adjustment which takes into account thereimbursement for administrative services paid to the university by the nonprofit organization. If the negotiator does not see an adjustment in the universities indirect cost proposal then theadministrative costs relating to the nonprofit organization could be getting reimbursed twice. Once through the universities indirect cost rate and once through the nonprofit organization’sindirect cost rate.