22

A future for the Demand Side in Western Australia? Richard Wilson – WA Power and Gas Conference 2016

| Date post: | 20-Jan-2017 |

| Category: |

Presentations & Public Speaking |

| Upload: | informa-australia |

| View: | 1,732 times |

| Download: | 3 times |

A future for the Demand Side in

Western Australia?Richard Wilson – WA Power and Gas Conference 2016

2

About EnerNOC

Proven Customer Track Record

• Over 80,000 enterprise (C&I) customer sites and 6,000+ demand response customers

• Over 50 utility and grid operator customers

• Over $1 billion in customer payments/savings to date

• Simple, risk-free commercial agreements

Full Value and Technology Offering

• Energy intelligence application platform addresses demand and supply side, connects energy usage

to spend

• Combines technology, managed services, and market access

• Nearly $200 million invested to date in technology

• 24/7/365 Network Operations Center, real-time metering and web-based monitoring from any device

World-Class Team and Resources

• Over 1,300 employees and growing fast – multiple “top places to work” awards

• Publicly traded on the U.S. NASDAQ (ENOC)

• $400 million in 2015 revenues

• $138 million in cash and cash equivalents on balance sheet

Updated 03.2016

Leading SaaS provider of energy intelligence software (EIS) for enterprises and utilities

3

About EnerNOC

Proven Customer Track

Record

• Thousands of enterprise

customers across over 80,000

sites

• Over $1B in customer savings

delivered to date

• Market leader in demand

response

To learn more, visit http://www.enernoc.com

Strong Financial Profile

• 2015 Revenues: $400M

• $138M in cash/cash equivalents on

balance sheet

• Publicly traded on the NASDAQ)

(ENOC)

• Over 1,300 employees and growing

fast; multiple “top places to work”

awards

Full Value and Technology

Offering

• Energy intelligence software = ~$5B

market in U.S. alone

• Energy intelligence application

platform addresses demand and

supply-side, connects energy usage

to currency

• Combines technology, managed

services, and market access

• ~$200M invested to date in

technology

Updated 11.2015

4

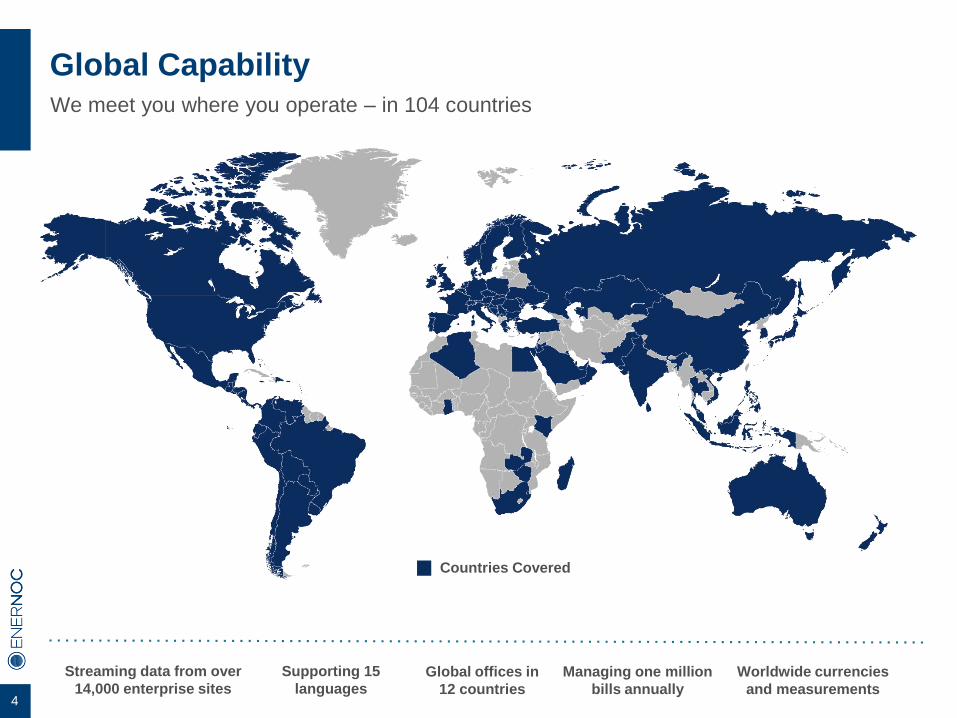

We meet you where you operate – in 104 countries

Global Capability

Supporting 15

languagesManaging one million

bills annually

Worldwide currencies

and measurements

Countries Covered

Global offices in

12 countries

Streaming data from over

14,000 enterprise sites

5

A Global Demand Response Footprint

6

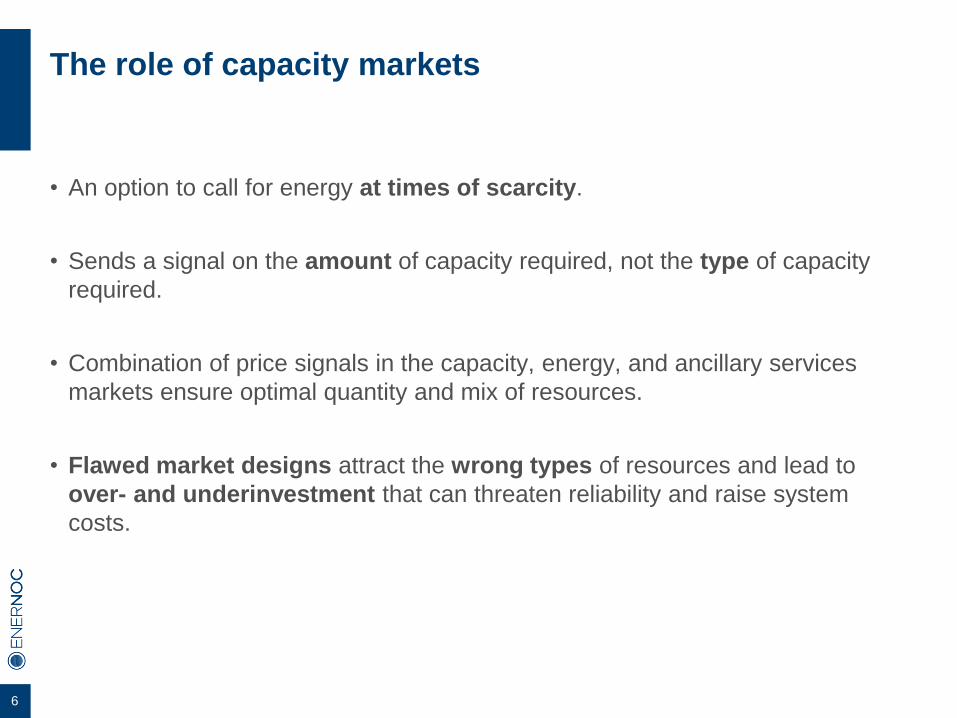

The role of capacity markets

• An option to call for energy at times of scarcity.

• Sends a signal on the amount of capacity required, not the type of capacity

required.

• Combination of price signals in the capacity, energy, and ancillary services

markets ensure optimal quantity and mix of resources.

• Flawed market designs attract the wrong types of resources and lead to

over- and underinvestment that can threaten reliability and raise system

costs.

7

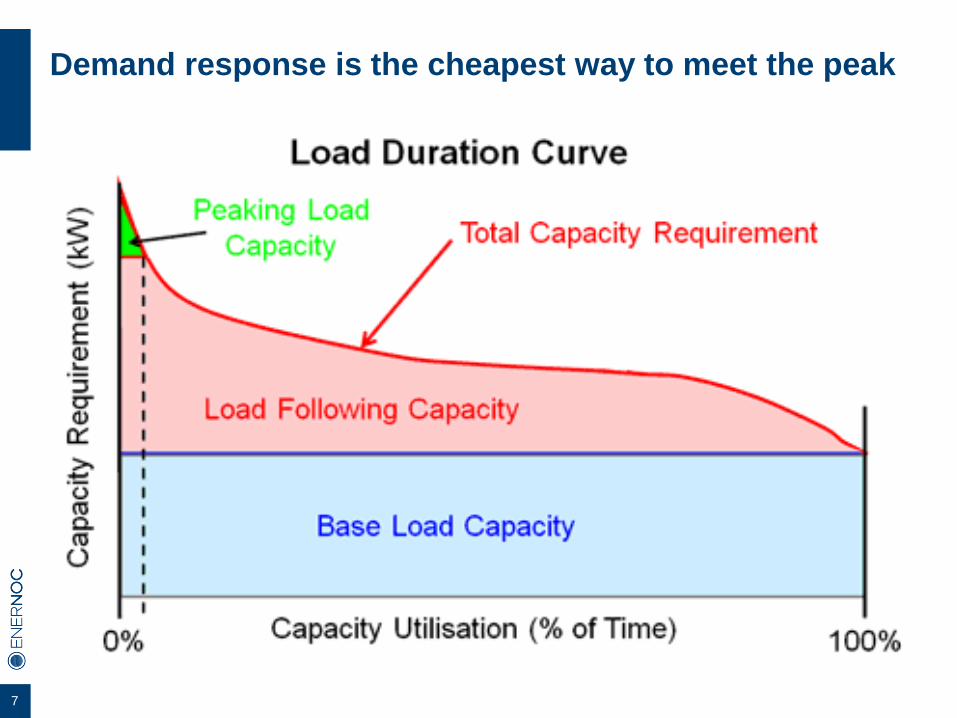

Demand response is the cheapest way to meet the peak

8

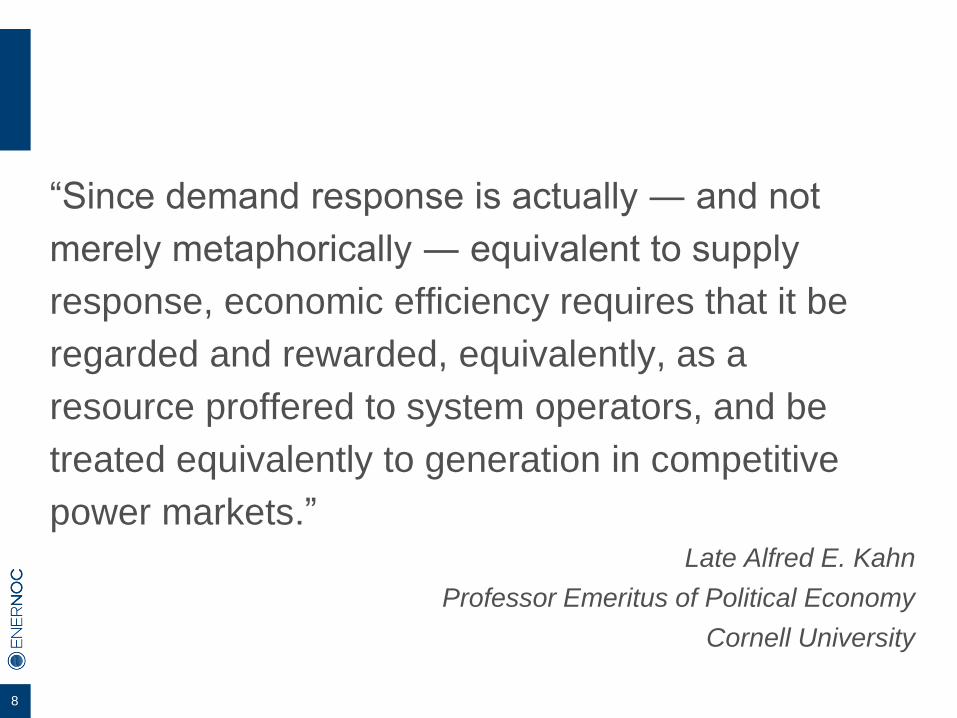

“Since demand response is actually ― and not

merely metaphorically ― equivalent to supply

response, economic efficiency requires that it be

regarded and rewarded, equivalently, as a

resource proffered to system operators, and be

treated equivalently to generation in competitive

power markets.”Late Alfred E. Kahn

Professor Emeritus of Political Economy

Cornell University

9

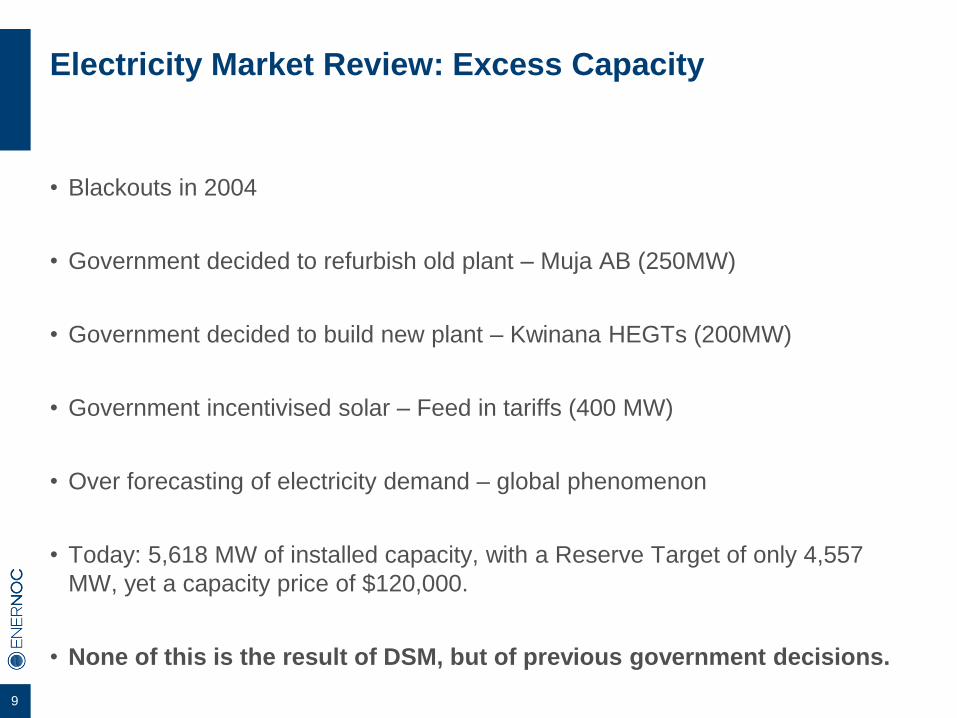

Electricity Market Review: Excess Capacity

• Blackouts in 2004

• Government decided to refurbish old plant – Muja AB (250MW)

• Government decided to build new plant – Kwinana HEGTs (200MW)

• Government incentivised solar – Feed in tariffs (400 MW)

• Over forecasting of electricity demand – global phenomenon

• Today: 5,618 MW of installed capacity, with a Reserve Target of only 4,557

MW, yet a capacity price of $120,000.

• None of this is the result of DSM, but of previous government decisions.

10

11

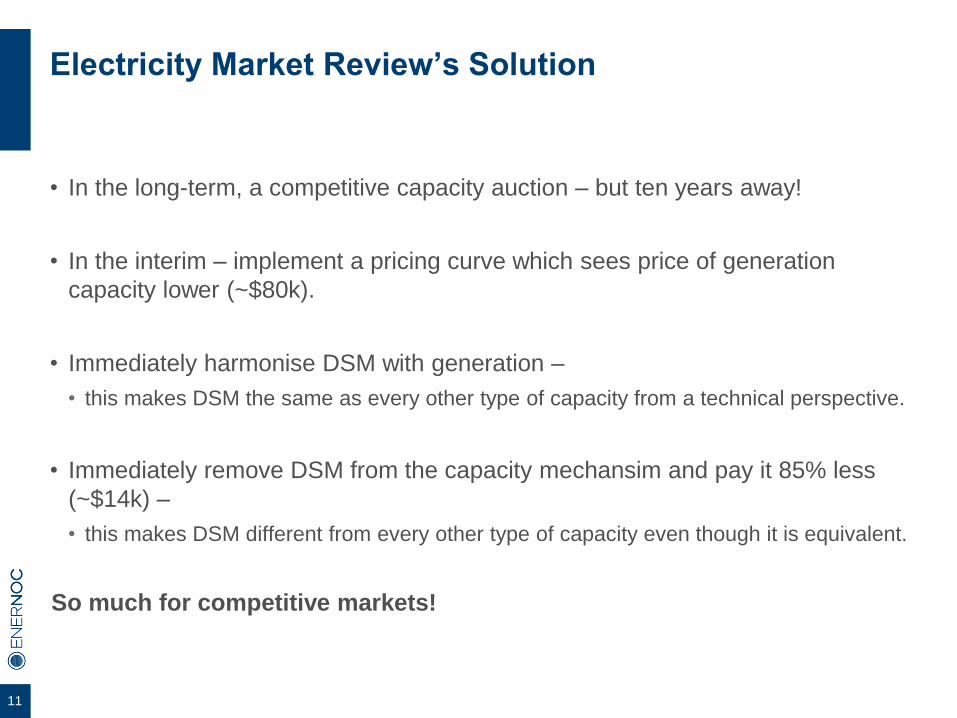

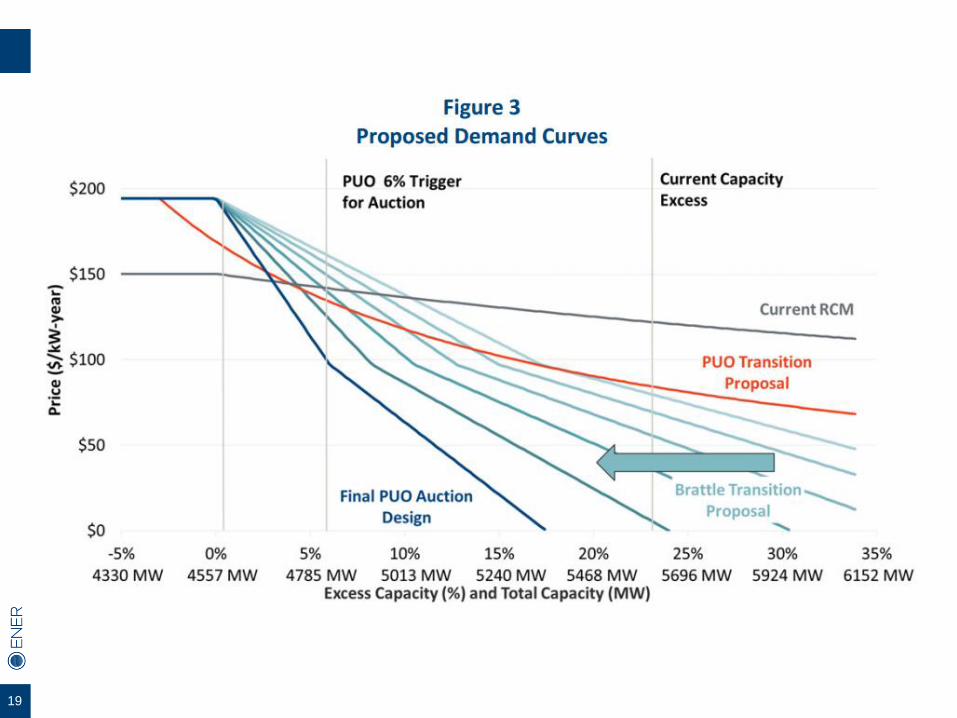

Electricity Market Review’s Solution

• In the long-term, a competitive capacity auction – but ten years away!

• In the interim – implement a pricing curve which sees price of generation

capacity lower (~$80k).

• Immediately harmonise DSM with generation –

• this makes DSM the same as every other type of capacity from a technical perspective.

• Immediately remove DSM from the capacity mechansim and pay it 85% less

(~$14k) –

• this makes DSM different from every other type of capacity even though it is equivalent.

So much for competitive markets!

12

“To fully restore appropriate incentives to market

participants, the demand side of the market should be

treated symmetrically with the supply side. Demand

response resources that are compatible with the system

operator’s reliability criteria should be compensated at levels

equivalent to what is paid to generators to make capacity

available during capacity constrained periods.”

Professor Paul Joskow

Massachusetts Institute of Technology

13

Why price discrimination is bad policy

• During times of scarcity, all forms of capacity – baseload, mid-merit, and

peaking, including DSM – provide the same value to the system.

• Will create a bias in suppliers’ overall costs of operation and impact the bids

suppliers will submit in the energy and ancillary services markets.

• Sets a precedent for treating emerging technologies differently (batteries,

baseload solar).

• Will lead to total exit of DSM from the market.

• Treating the top end of the load-duration curve on an energy-only basis

would be akin to attempting to buy insurance only after you have been

robbed but expecting to pay the same price as prior to the burglary.

14

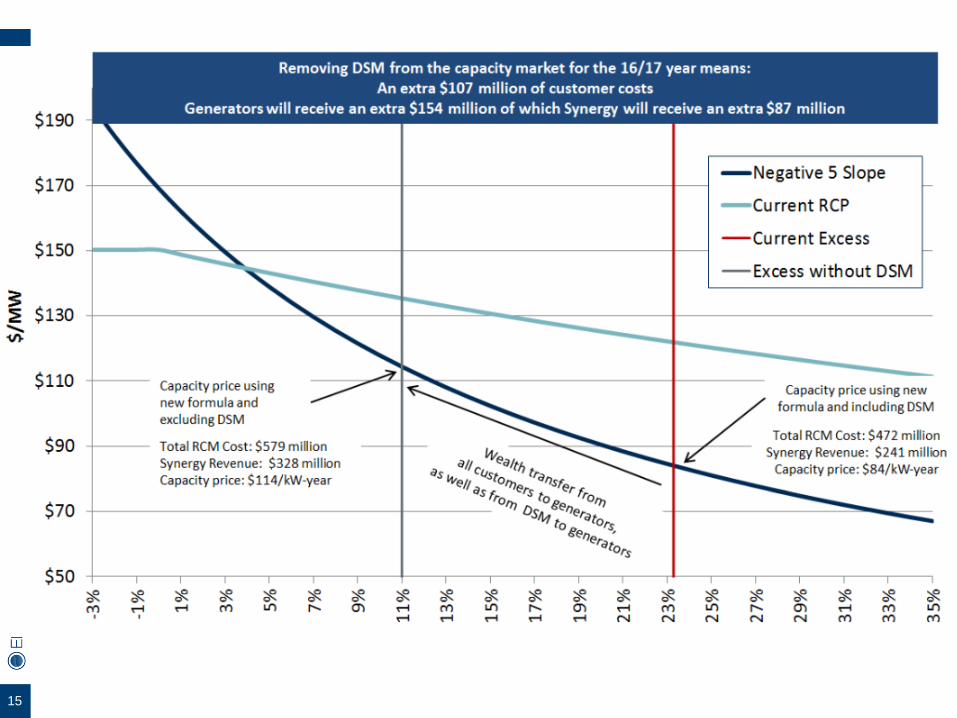

Winners and losers

Winners

• Generators - benefit from a higher

capacity price

• Synergy – currently subsidised

$500m

Losers

• 300+ DSM businesses

• Consumers - $107 million

• Energy efficiency – DR provides

capital for EE measures

• State Government – delays

introduction of capacity auction due

to generator decisions to refurbish

and prop up the price.

15

16

Technology neutrality has wide support everywhere

except government and generators

Supporters

• DSM businesses

• CCIWA

• CMEWA

• WA Independent Power Association

• Australian Energy Market Operator

• Energy Efficiency Council

• Major Energy Users Group

• Brattle (Government’s own

consultants on capacity market

design)

Detractors

• Synergy, Alinta, Perth Energy (ie

generators that stand to benefit)

• Generator’s financiers (CBA)

• State owned monopolies (Western

Power) – can’t go against Minister

17

The biggest myth: DSM is never used, and is not needed

• 2011: Cyclone Carlos – 100% of DSM dispatched across the state for

consecutive days

• Excess capacity was 8.7% above the reserve margin.

• If DSM had instead been gas fired peakers, the grid would have blacked out.

• 2014: Muja transformer failure – Great Southern region at risk

• Excess capacity was 23.7%.

• Shows flexibility of DSM – locational dispatch. Why get rid of this?

• The reserve target is based on the probability of a one-in-ten-year excedence.

• Yet we have used DSM twice in five years.

• Do we really want to get rid of it? Even temporarily?

18

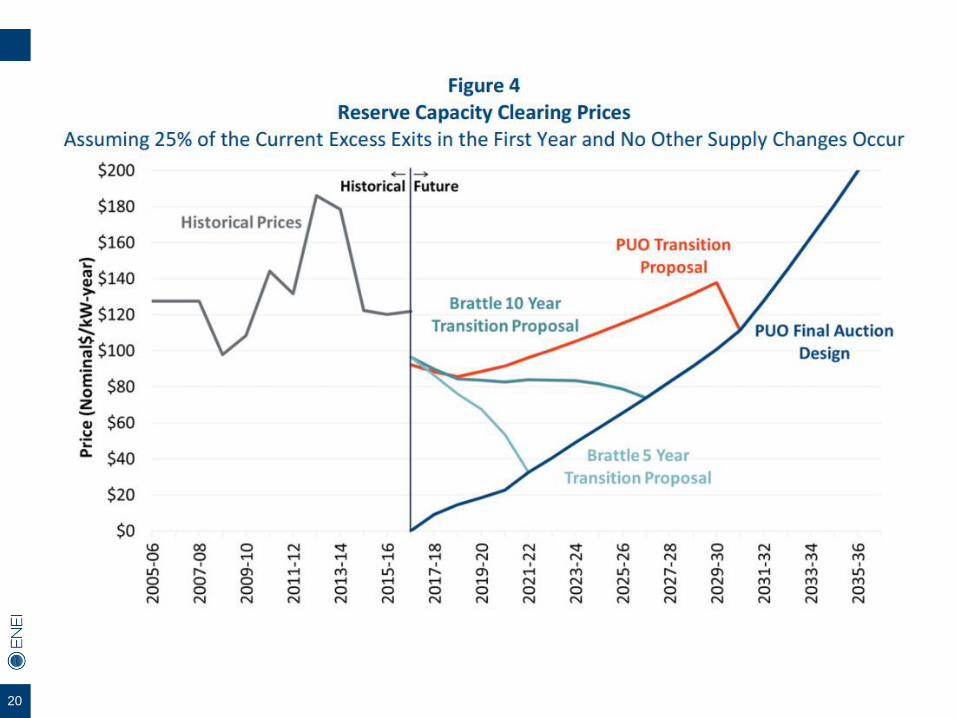

A better way – competitive markets

• Level playing field for all resource types

• Introduce an auction now

• Flat initial demand curve, as per PUO proposal

• Steepen the demand curve over time

• Institute a fixed timetable for the final design, reducing incentive for generators

to delay

19

20

21

A better way – Reform Synergy

• EMR hopelessly conflicted – Synergy’s Chairman is on Steering Committee.

• Underwater contracts

• High costs due to inefficient and ageing plant

• Lack of competition

• Effects of government ownership

• Solution: Restructure and privatise

22

Conclusion

• Blatant discrimination violates best practice and the WEM’s own objectives.

• Consumers and businesses lose while generators win.

• Government ownership is contaminating the policy process.

• There is a better way – competitive markets, now.