Examination of Certain Policies, Procedures, Controls, and Financial Activity of the Former Administration of the Kentucky Department of Agriculture ADAM H. EDELEN AUDITOR OF PUBLIC ACCOUNTS www.auditor.ky.gov 209 ST. CLAIR STREET FRANKFORT, KY 40601-1817 TELEPHONE (502) 564-5841 FACSIMILE (502) 564-2912 Embargo until 10am April 30, 2012

The Auditor Of Public Accounts Ensures That Public Resources AreProtected, Accurately Valued, Properly Accounted For, AndEffectively Employed To Raise The Quality Of Life Of Kentuckians.

EXECUTIVE SUMMARY............................................................................ i

Chapter 1 Introduction and Background...................................................................... 1

Chapter 2 Findings and Recommendations ................................................................ 18

Exhibits 1. 2008 SASDA Conference Giveaways ............................................... 1212. Rifles Returned By Former Commissioner..................................... 1243. KY Proud Logo Engraved On Rifles ............................................... 1254. Firearms Transaction Record .......................................................... 1265. 2008 SASDA Conference Wooden Hat and Stand Gift To Former

6. KY Proud Basket Request Form ..................................................... 1347. Motor Fuel Stations In Each Kentucky County ............................. 1368. Motor Fuel Samples Taken By County ........................................... 1409. State Fair Small Inventory Check Out Form ................................. 14410. Route Taken To Perform Inspection In Winchester, Kentucky ... 145

Kentucky Department of Agriculture Response ................................................................................... 146

James Comer, CommissionerKentucky Department of Agriculture111 Corporate DriveFrankfort, Kentucky 40601

RE: Examination of Certain Policies, Procedures, Controls, and Financial Activity of the FormerAdministration of the Kentucky Department of Agriculture

Dear Commissioner Comer:

We have completed our examination of the Examination of Certain Policies, Procedures,Controls, and Financial Activity of the Former Administration of the Kentucky Department of Agriculture. The enclosed report presents, in total, 41 findings and offers approximately 126recommendations to strengthen KDA controls and management oversight procedures.

As requested, the objectives of this audit were “thorough and sweeping” andencompassed a broad review of the administrative practices and fiscal management of theDepartment of Agriculture under the administration of the former KDA Commissioner.Procedures performed during the examination include interviews with over 50 individuals,including current and former KDA staff and others. To complete this examination, the APAreviewed thousands of documents, including emails, invoices, reports, policies, timesheets, travelvouchers, and personnel files. These and other items were analyzed relative to the objectives of this examination. The scope of this examination includes a review of certain policies, records,activities, and information for the period of January 1, 2004 through December 31, 2011, with anemphasis on the last four years; however, the time periods used in the report vary due to the dateof various issues reviewed and the availability of the information.

The purpose of this examination was not to provide an opinion on the financialstatements or activities, but to ensure processes are in place to provide strong oversight of financial activity and programs and to review specific issues brought to the attention of thisoffice.

Due to the nature of certain findings discussed within this report, we are referring issueswithin the report to the Kentucky Office of the Attorney General, Kentucky Executive BranchEthics Commission, Kentucky Personnel Board, Kentucky Department of Revenue, KentuckyDepartment of Fish and Wildlife, Kentucky Agricultural Development Board, Internal RevenueService, and the United States Department of the Interior Office of Inspector General.

The Auditor of Public Accounts requests a report from KDA on the implementation of the examination recommendations within (60) days of the completion of the final report. If youwish to discuss this report further, please contact me or Brian Lykins, Executive Director of theOffice of Technology and Special Audits.

Performance and Examination Audits BranchExecutive Summary

April 30, 2012

Examination of Certain Policies, Procedures, Controls, and Financial Activitof the Former Administration of the Kentucky Department of Agriculture

Examination ObjectivesOn January 11, 2012, the Commissioner of theKentucky Department of Agriculture (KDA) formallyrequested that the Auditor of Public Accounts (APA)conduct a special examination of the KDA that would

be “thorough and sweeping.” The Commissioner indicated to the press that in his first five days on the

job, employees came forward with “several potentiallytroubling allegations” involving the administration of his predecessor. At a joint press conference later that

day with the Agriculture Commissioner, the StateAuditor agreed to take a broad look into the“administrative practices and fiscal management of theDepartment of Agriculture” under the two terms of thelast KDA Commissioner (former Commissioner).

The scope of this examination includes records,activities, and information for the period of January 1,2004 through December 31, 2011, with an emphasis onthe last four years; however, the time periods used inthe report vary due to the dates of the issues and theavailability of the information. Thousands of

documents, including emails, invoices, reports, policies,timesheets, travel vouchers, and personnel files, weresupplied by KDA staff, former staff, and other entities.These and other items were analyzed in relation to theobjectives of this examination.

The APA conducted interviews with over 50individuals, often following up on the initial interviewswith phone conversations, emails, and additionalmeetings. The APA attempted to interview the formerCommissioner; however, the former Commissionerdeclined to be interviewed.

Background

Organization At the end of the examination period, KDA had 302personnel positions, 36 of which were vacant. KDA isorganized into five executive offices including theOffice of the Commissioner, the Office for Consumerand Environmental Protection, the Office of AgricultureMarketing and Product Promotion, the Office of the

State Veterinarian, and the Office for StrategPlanning and Administration.

The Office for Consumer and Environmental Protectioversees the regulation and inspection of a variety industries, as well as, acting as a distribution agent fUSDA commodities to eligible recipient agencieStaff within the office provide regulation ainspections of items such as pesticides, amusemerides, motor fuel and motor fuel dispensers, ret

scanners and scales, and grain dealers.

The Office of Agriculture Marketing and ProduPromotion assists farmers, agricultural businesses, acommodity groups in promoting and marketing thproducts by expanding existing markets, as well developing domestic and international markeSpecific services provided by staff include farm safecourses, gathering and reporting agriculture markinformation, promoting products through the KentucProud (KY Proud) program, and sponsoring over 1livestock shows.

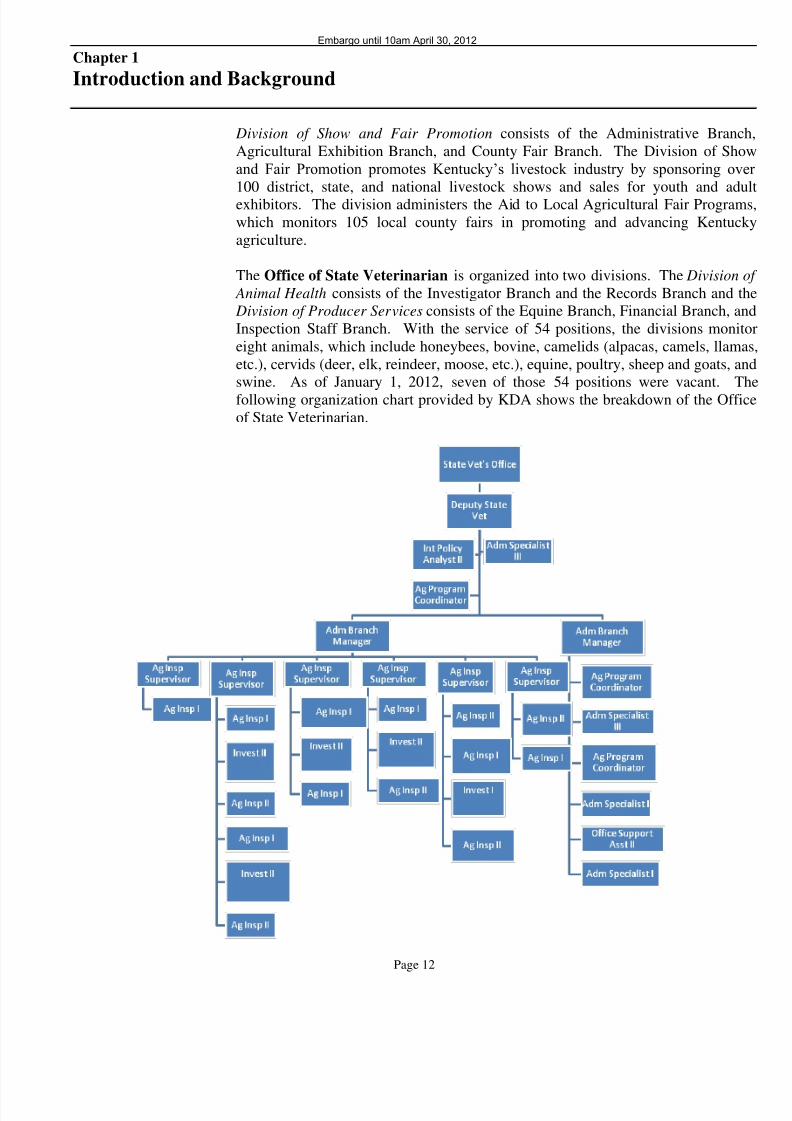

The Office of the State Veterinarian is organized intwo divisions. The Division of Animal Health consiof the Investigator Branch and the Records Branch athe Division of Producer Services consists of tEquine Branch, Financial Branch, and Inspection StaBranch. The divisions monitor eight animals, whiinclude honeybees, bovine, camelids, cervids, equinpoultry, sheep and goats, and swine.

The Office for Strategic Planning and Administratiprovides the administrative support structure of t

agency through internal human resources oversiginformation technology support, budgetary oversigand financial processing.

In addition to the many areas of day-to-dresponsibilities, KDA routinely plans and/participates in many conferences, shows, and specevents held annually in Kentucky. Such activitiinclude the Kentucky State Fair, the Incredible FoShow, Kentucky Crafted: The Market, the NorAmerican International Livestock Exposition, and t

Kentucky High School Athletic Association SweetSixteen State Basketball Tournaments.

During the period audited, KDA also provided atremendous amount of staff time and other resources tothe 2010 Alltech FEI World Equestrian Games (WEG)and the 2008 Annual Meeting of the SouthernAssociation of State Departments of Agriculture(SASDA), both of which were hosted by Kentucky in

the years noted.

KDA is also responsible for the oversight of orparticipation on seven different agriculture relatedboards and councils.

KDA FundingKDA receives funding from three primary sources,including General Fund appropriations, federal funding,and restricted funds stemming from agency collectedrevenues such as licensure fees. While an economicdownturn has caused General Funds to become a

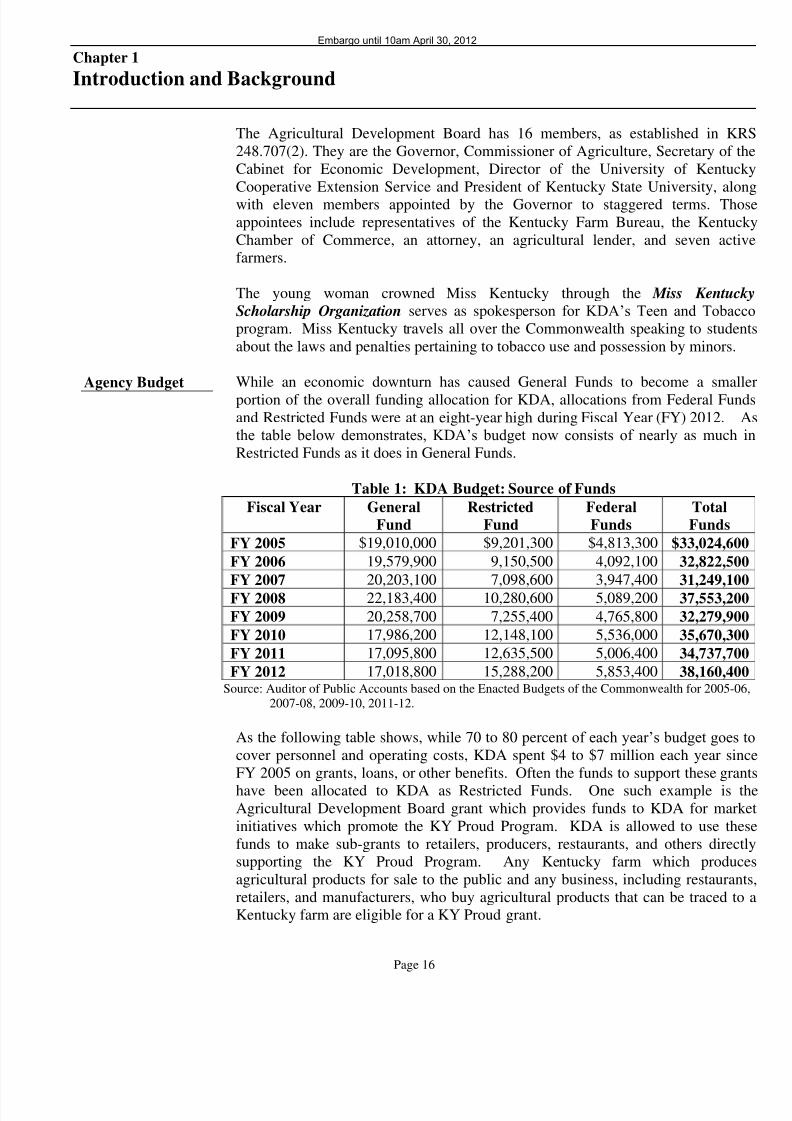

smaller portion of the overall funding allocation forKDA, allocations from Federal Funds and RestrictedFunds were at an eight-year high during Fiscal Year(FY) 2012. Total General Fund appropriations in FY2012 were $17,018,800, lower than the $19,010,000 inFY 2005. Restricted funding is $15,288,200 in FY2012, which is an increase from the $9,201,300 in FY2005. Federal funding revenue in FY 2012 is$5,853,400, an increase from the $4,813,300 in FY2005. In total, the FY 2012 budget for KDA is$38,160,400, which is an increase from the$33,024,600 in FY 2005.

Approximately 70 to 80 percent the KDA budgetedrevenue is expended on personnel and operating costseach year. Total budgeted expenses for these categoriesare $24,295,700 in FY 2012. In addition, KDA spent$4 to $7 million each year since FY 2005 on grants,loans, or other benefits, with a budgeted amount of $4,857,400 in FY 2012.

2008 Southern Association of StateDepartments of Agriculture Annual ConferenceThe Southern Association of State Departments of

Agriculture (SASDA) is an organization comprised of the commissioners and secretaries of the departments of agriculture for 17 states, including Kentucky. In 2008,the former Commissioner was the President of SASDA,making Kentucky the host state for the annualconference.

According to the accounting records, revenues andexpenditures for the 2008 conference were each$208,851, once the checking account was closed out.

Sponsorships and attendee registrations made up tmajority of the revenues for the conference, totali$194,650. Sponsorships for the conference total$164,450, comprised primarily of donations froagriculture-related vendors and associations. Recorindicate that at least seven of the sponsoring vendoare regulated by KDA, but since KDA did not retaany documentation showing whether or how thevendors were solicited for the sponsorship, it is n

possible to determine if there was any conflict interest. Registrations accounted for $30,200 of t2008 conference revenues, with the 53 registratiopaid for by KDA accounting for approximately half that amount collected due to many of the attendereceiving registrations as part of a sponsorship.

The majority of the expenditures for the 2008 annumeeting went toward hotel expenses, tripentertainment, gifts, and food. Hotel expenses were tgreatest single expense, costing $67,730 for roorentals of attendees, conference space, and dinne

Gifts for commissioners, spouses, and other attendeaccounted for approximately $61,085 in expenseExpenses for activities and taking attendees on trips various locations around the state cost approximate$46,597. Costs for entertainment, additional food, asupplies were a cumulative $15,264.

In addition to the expenses recorded through the 20SASDA annual meeting checking account, KDincurred other costs in hosting the event. KDincurred over $13,000 in direct expenditures for horooms of employees working and attending t

meeting, van rentals, and printing services. KDincurred an estimated $52,310 in costs for 39 KDemployees to provide staffing for the conferencCombined with over $30,000 expended by KDA eiththrough direct payments to SASDA or through a grato an agriculture association, the annual conferenresulted in an estimated cost to the state of $96,221.is unclear what overall benefit Kentucky received frothese expenses.

Findings and RecommendationsFinding 1: KDA expended approximately $30,0

of state funds to offset the cost of the 2008 SASDconference.KDA expended approximately $30,000 of KDAGeneral Fund money to offset the costs of the 20SASDA conference hosted by KDA when the formCommissioner was the SASDA PresideApproximately 50 percent of the funding provided bKDA in support of the conference was made throutwo grants it awarded to two organizations. KDA mathe grants with the understanding that a portion of t

funds would subsequently be used to offset conferencecosts. In addition, KDA paid a “registration fee” for dozens of KDA employees, the majority of whom didnot attend conference sessions but rather worked theconference performing various tasks, including drivingconference attendees around town, providing childcare,and distributing gifts to attendees’ hotel rooms. KDAnot only funded approximately $30,000 of the 2008SASDA conference costs with public funds, but did so

in a questionable and non-transparent manner.Recommendations: We recommend KDA refrainfrom using grant funds to subsidize its conferences orgeneral administrative expenses. Grant funds awardedby KDA should be awarded without stipulations, andused strictly in compliance with the written grant terms.We recommend KDA pay the registration fees toconferences only for a reasonable number of employees, who will actually be attending conferencesessions, and ensure that registrants are clearly notifiedof their registration and the expectation to attend.Further, KDA should ensure a reasonable number of

employees are authorized to work a conference whenhosting an event.

Finding 2: KDA incurred direct expenditures for2008 SASDA conference.KDA incurred over $13,000 in direct expenditures forthe 2008 SASDA conference, in addition to the statefunds paid to other organizations to offset conferencecosts and the cost of employees’ wages and overtime asdiscussed in Finding 1. These expenditures, paid fromthe KDA General Fund, include costs for KDAemployee hotel rooms, van rentals to transport

conference attendees during the week of theconference, pocket schedule cards for attendees, andtwo banner signs to be displayed during the conference.Recommendations: We recommend KDA scrutinizethe use of the agency’s General Fund and other publicfunds to pay the expenses for conferences it may host toensure that the expenditure of public funds are forpublic purposes only, and that the expenditure providesa direct benefit to KDA or its programs. We furtherrecommend that any non-public source of fundsdedicated to host a conference be used to pay theexpenses of the conference.

Finding 3: KDA purchased an excessive number of gifts in association with the 2008 SASDA conferenceand failed to formally track the final distribution of the excess purchases.In association with the 2008 SASDA conference, KDApurchased an excessive number of items reportedlyintended as gifts for visiting state commissioners,spouses, guests, and KDA employees. Throughdocumentation provided by KDA and interviews withcurrent and former KDA personnel and others, it is our

understanding that the excess orders were made at tdirection of the former Commissioner with the majoriof the excess items reportedly taken to the formCommissioner’s home after the conference. KDA dnot formally track the final distribution of any of texcess items purchased or of those items donated.Recommendations: We recommend KDA moclosely scrutinize its purchasing orders to ensure ththe orders are reflective of actual needs. The agen

should refrain from purchasing items in excess of tnumber required. We also recommend KDA createsystem to track items purchased for events it hosts coordinates. KDA should ensure that the findistribution of purchased gift items are documented writing and accurately reflect the final distribution each item, including the name of the individual wreceived the item, the date the item was transferred their possession, and the business purpose associatwith providing the gift.

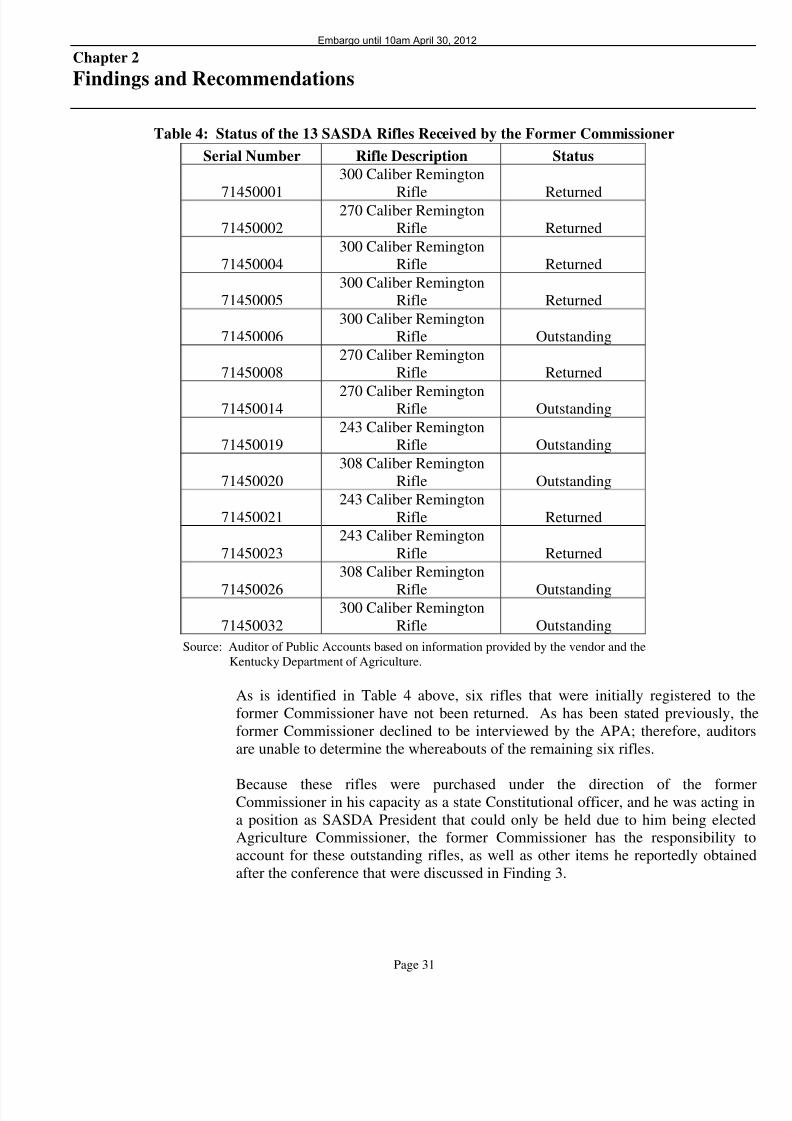

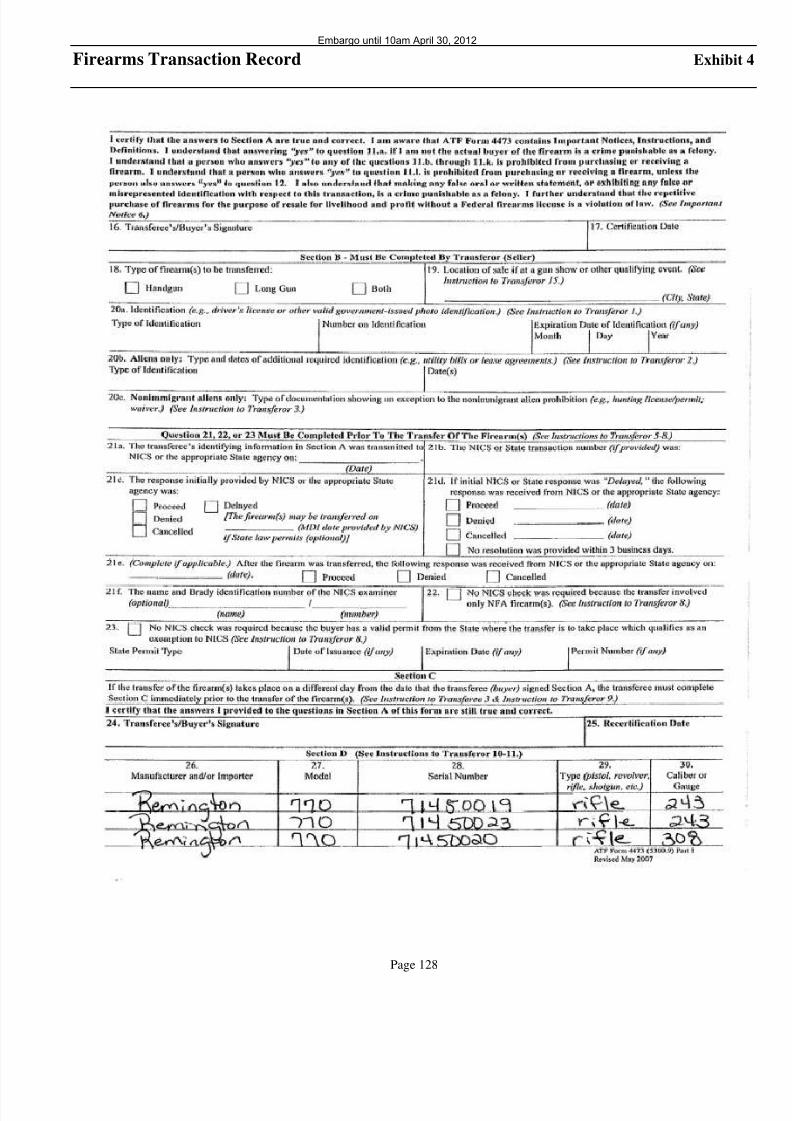

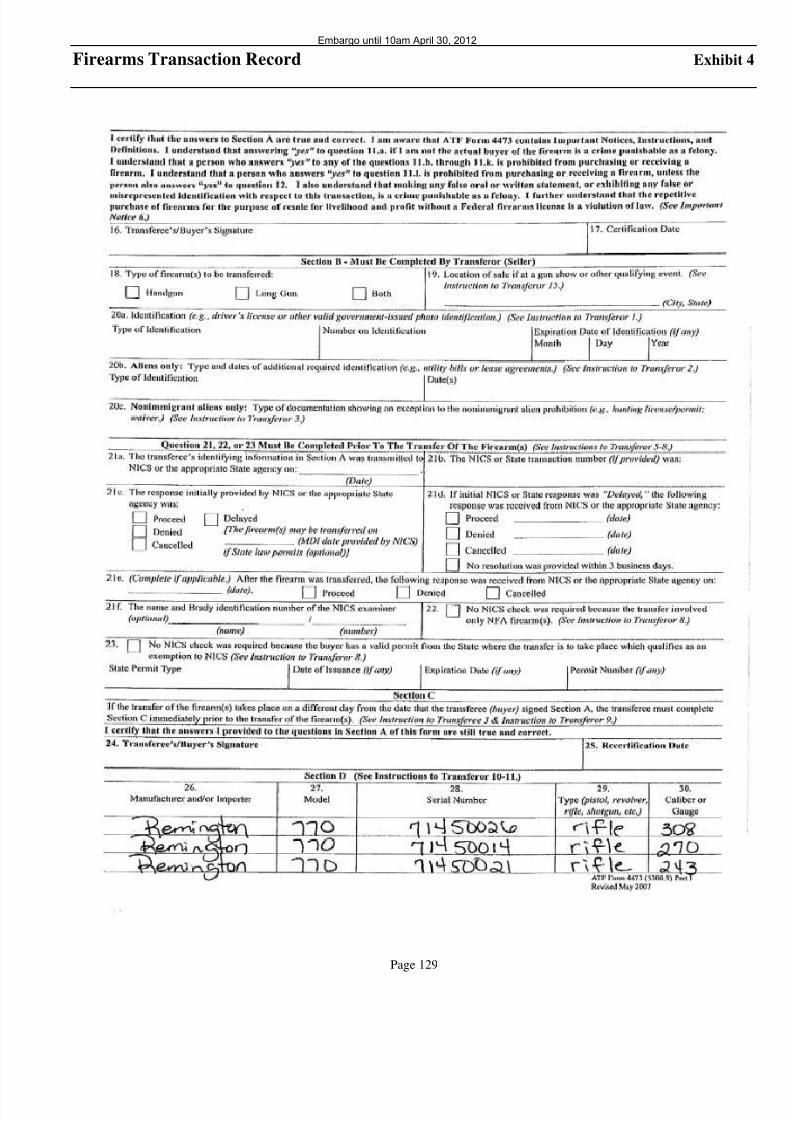

Finding 4: Former Commissioner took possession

13 rifles purchased with SASDA funds and returnonly seven, leaving six rifles unaccounted for.On June 4, 2008, five days before the 2008 SASDconference hosted by the former Commissioner, tformer Commissioner went to a local vendor and topossession of 13 Remington rifles purchased wSASDA funds. In order to take possession of tfirearms, the former Commissioner was required complete and sign an OMB No. 1140-0020 FirearmTransaction Record indicating that he was the actubuyer of these 13 rifles. On January 17, 2012, tformer Commissioner returned seven of these 13 rifl

to KDA, leaving six additional rifles unaccounted for.Recommendations: We recommend the KDadministration attempt to discuss with the formCommissioner the return of the six outstandiRemington rifles and, upon their return, ensure trifles are used or disposed of for the best benefit to thpublic.

Finding 5: KDA employees were used extensively the staff for the 2008 SASDA conference resulting at least $52,310 in estimated costs to the state.As host of the 2008 SASDA conference, KDA utiliz

numerous staff to carry out nearly all duties necessato plan, organize, and produce the event. Based onstaff work assignment listing produced by the KDstaff that was in charge of organizing the conferencthe APA has calculated that at least 39 employecontributed significantly to the SASDA-related worwith duties such as transporting conference attendeeescorting tour groups, conducting children’s programand acting as general support staff. In total, the 39 stworked an estimated 2,015 regular, compensato

(comp), and paid overtime hours with an estimated totalcost to KDA of $52,310.Recommendations: We recommend that KDA ensurethat agency resources, including employees, are used inthe best interests of the public and that an actual publicbenefit can be realized. In the future, KDA shouldensure that any conferences hosted by the agency aredone so with a reasonable and justifiable cost.

Finding 6: SASDA Hotel expenses used to benefitformer Commissioner and his family.On June 6, 2008, the KDA Administrative BranchManager responsible for organizing the 2008 SASDAconference contacted a hotel representative andrequested that additional rooms for the formerCommissioner’s extended family be billed to theSASDA account. The total cost for these additionalrooms on the SASDA account was $1,380.30. Inaddition to this expense, the former Commissionerreceived over 55,000 hotel reward points, with apurchase value of approximately $688, on his personal

hotel awards account for holding the conference at thatvenue. These points can also be exchanged for ameeting credit certificate valued at approximately $250.Recommendations: We recommend KDA refrainfrom expending SASDA or other conference funds forpersonal benefit when hosting or organizing futureconferences. KDA should ensure that the fundsdedicated to a conference or other activity are expendedfor the intended public purpose. We furtherrecommend that hotel reward points resulting fromhosting or organizing a conference or event be used tooffset future hotels costs for conferences or events and

not be used to provide a personal benefit.

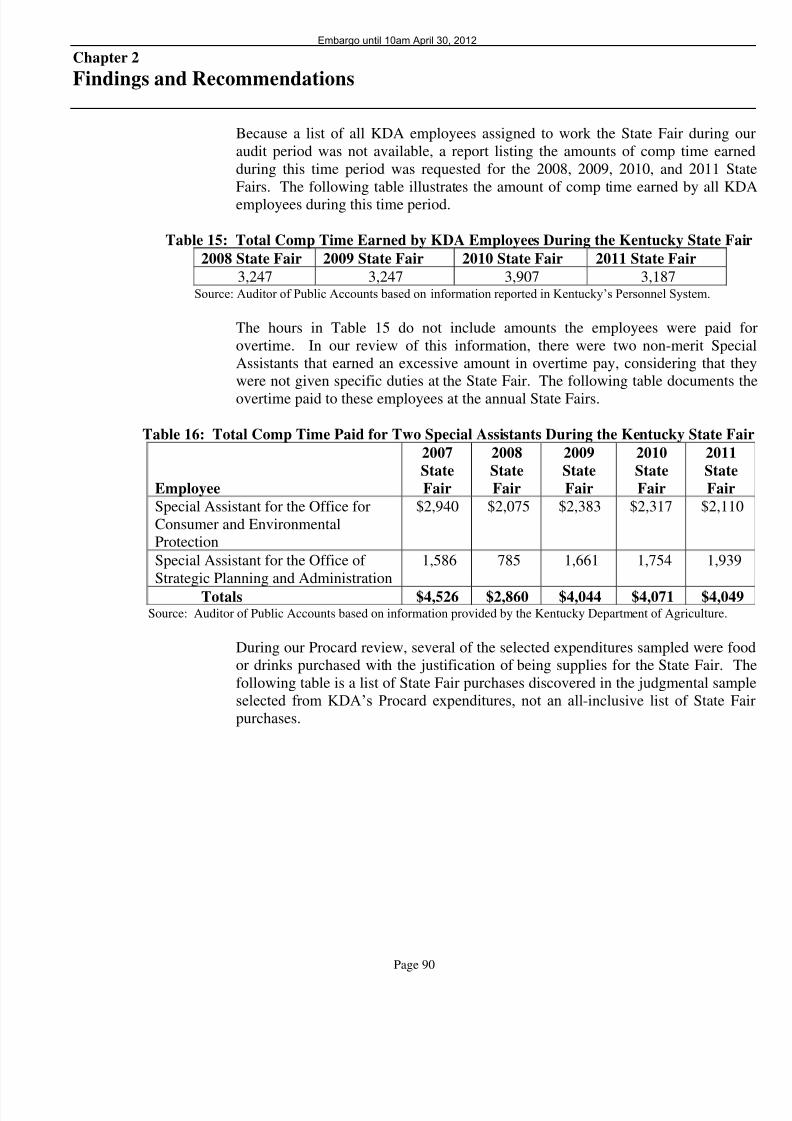

Finding 7: Additional hotel rooms were reserved atthe Kentucky State Fair for KDA employees whowere known not to be staying overnight, so theformer Commissioner could have extra rooms at hisdisposal.During the 2009 and 2010 Kentucky State Fairs, theformer Personnel Director reserved rooms in the namesof two KDA employees who she knew would not bestaying overnight during the fair. According to theformer Personnel Director, she reserved the additional

rooms at the request of the former Director of Outreachand Development, because the former Commissionerhad told him that he needed extra rooms. The formerPersonnel Director stated she was told by this Directorto determine what employees would not be stayingovernight at the fair and reserve the rooms under theirnames. While the purpose of the rooms wasunspecified in the request made to the former PersonnelDirector, interviews with KDA staff and others indicatethat the rooms were used for and occupied by theformer Commissioner’s family members.

Recommendations: We recommend that KDA follothe established approval and oversight process for travel arrangements, including reservation of horooms, regardless of the merit status of the employeWe further recommend that, through the establishapproval process, KDA ensure that state funds are nused to provide travel for the personal benefit employees, employees’ family members, or otheThe misuse of state funds or attempts to misuse fun

should be reported to agency management. management is the source of the misuse, KDA stashould report such issues to an outside source such the APA, Executive Branch Ethics Commission, Attorney General’s Office.

Finding 8: KDA reimbursed the formCommissioner for costs incurred at the Boys’ Swe

Sixteen State Basketball Tournament although tnecessity of the overnight travel was questionable.During the former Commissioner’s tenure with tKDA, Kentucky spent $8,843 to fund an annual tr

taken by the former Commissioner to the Boys’ SweSixteen State Basketball Tournament (Boys’ SweSixteen) in Lexington, KY. Due to his status as elected constitutional officer, reimbursement expenses are not based on the requirement that an eveis 40 miles from the employee’s residence, as required for other state employees, but it is requirthat the reimbursement be for a necessary expenincurred in connection with official business travThe fact that KDA advertises its KY Proud prograand maintains a booth at this event does not makenecessary for the KDA Commissioner to incur lodgi

expense by staying overnight to perform officbusiness.Recommendations: We recommend that KDA ensuthat travel expenses requested by the KDCommissioner are incurred for official business. Wfurther recommend the cost of overnight travel reimbursed only if it is necessary and provides a pubbenefit. Due to scarce public resources, every effshould be made to minimize travel cost, including cosassociated with the Commissioner’s travel.

Finding 9: Former Commissioner appears to ha

used his official position to obtain items for personbenefit. The former Commissioner appears to have used hofficial position to obtain certain items for his personbenefit that were either donated to KDA by KY Prouvendors for promotional purposes, or were paid for wKDA general funds. This, in part, was able to occdue to lax controls over accounting for lower coitems, as no items under $500 are inventoried, abecause of the authority of his position. This includgift baskets of KY Proud items, wooden hats from

KY Proud vendor, refrigerators, file cabinets, shirts,and laptops.Recommendations: As stated in the recommendationsfor Finding 29, we recommend that KDA create,document, and implement a process to account for allKY Proud products held for promotional purposes. Wealso recommend that KDA evaluate the variousclothing items purchased for staff to ensure the itemsare necessary, serve a public purpose, and are

reasonable in amount. We further recommend thatKDA tag and maintain an internal inventory of certainitems that have been assigned to individuals, have auseful life of one year, and have a value of less than$500. Such items may include monitors, dockingstations, monitor stands, printers, or cell phones.

Finding 10: Former Commissioner of Agriculturedid not report numerous gifts given to him asrequired by the Executive Branch Code of Ethics.Through the examination of KDA, auditors determinedthat the former Commissioner received numerous gifts

from various sources during his tenure. According tothe Executive Branch Code of Ethics, all publicservants, such as the Commissioner of Agriculture,must report any gifts they have received that exceed$200 when filing the required Statement of FinancialDisclosure form with the Executive Branch EthicsCommission. A review of the former Commissioner’sStatement of Financial Disclosure forms for years 2004through 2011 show that no gifts were ever reportedsince taking the position of Commissioner of Agriculture.Recommendations: We recommend all officers and

public servants, as defined by KRS 11A.010, submit aStatement of Financial Disclosure form to theExecutive Branch Ethics Commission that includes allgifts received with a value over $200, as required byKRS 11A.050(3)(k).

Finding 11: KDA employees performed work at theformer Commissioner’s personal residence during a

workday.During the former KDA administration, KDApersonnel worked to build a basketball court andretaining wall at the former Commissioner’s residence.

KDA personnel also moved a gun safe from the formerCommissioner’s garage into his basement, reportedlyduring work hours.Recommendations: We recommend state personnelnot be asked, or used, to perform personal errands fortheir state employer, or to move the employer’spersonal effects. Employees should not be placed in aposition, in performing such actions, that they feel theiremployment could be jeopardized if they failed to doso.

Finding 12: KDA employees were directed to drithe former Commissioner on personal excursions.During the examination, auditors received multipreports from current and former KDA personnel aothers regarding trips where the former Commissiondirected employees to either drive him or to accompahim in the Commissioner’s KDA-assigned vehicKDA personnel questioned the appropriateness performing these tasks, but often stated that they we

doing what they were told to do. Some indicated thfelt if they declined to travel with the formCommissioner, their employment with KDA would jeopardized.Recommendations: We recommend KDA personnbe trained as to the appropriate use of state time aresources. In light of KRS 11A.020, we recommeKDA seek training on this matter from the KentucExecutive Branch Ethics Commission, as it authorized, under that KRS 11A.060, to administer aenforce the provisions of the state’s Executive Brancode of ethics.

Finding 13: KDA used proceeds from ginseng sainconsistent with federal requirements.Approximately six months after collecting ov$241,000 from the surplus sale of wild Americginseng, KDA expended $43,000 of that amount towathe purchase of eight Ford Explorer vehicles for Animal Enforcement Officers. As Animal EnforcemeOfficers do not perform duties associated with tginseng program, this $43,000 expenditure did not methe requirements set forth by the United States Fish anWildlife Service (USFWS), which stated in an Octob

25, 2007 letter to KDA, “[t]he proceeds from the sale this legally acquired ginseng shall be used by KDexclusively for the purposes of promoting aeducating all parties involved with the recordinharvest, purchase, sale, and transfer of ginseng.” Recommendations: We recommend KDA use tginseng surplus proceeds solely for purposes thcomply with USFWS criteria for the use of these fundwhich states, “[t]he proceeds from the sale of thlegally acquired ginseng shall be used by KDexclusively for the purposes of promoting aeducating all parties involved with the recordin

harvest, purchase, sale, and transfer of ginseng.” Walso recommend KDA discuss this matter with tUSFWS to determine how this issue may best resolved. We further recommend that if proceeds arealized when fleet vehicles are disposed of, KDshould consider using these funds to restore the $43,0to the ginseng account that was used toward tpurchase of vehicles.

Finding 14: KDA paid a grant recipient the fullgrant amount without requiring the recipient tomeet grant requirements.On March 8, 2010, a KDA Staff Assistant with theKDA Office of Agriculture Marketing and ProductPromotion emailed the former Commissioner to informhim of concerns he had with a grant recipient’sperformance involving a $15,000 matching grant. Inthis same email, the Staff Assistant suggested that KDA

hold the remaining amount of the grant, $7,500, untilKDA could “see actual purchases and performancecoming closer in line with their promises.” Three dayslater, the KDA employee authorized the release of theremainder of these grant funds to the grantee noting thathe did so at the direction of the former Commissioner.Recommendations: We recommend KDA requirecompliance with its grant agreements. KDA shouldensure that tobacco settlement funds, for which it hasoversight responsibility, are used solely for the intendedpurposes and that grant recipients are all held to thesame performance standards.

Finding 15: KDA purchased two 60-inch televisionswith questionable necessity to the agency.In March 2010, KDA purchased two 60-inchtelevisions and the corresponding wall mountingbrackets for a total cost of $4,192.75. One is mountedin an executive conference room, while the other ismounted in the Commissioner’s office. The cost for each television was $1,971.99, and the cost for themounting brackets was $124. The amount of $124.77was paid for the expedited shipping charges of themounting brackets, doubling the cost of the brackets.

No official need or justification for such large andexpensive televisions was provided by any KDA staff.Various staff stated in interviews that the expeditedshipping charge for the brackets was to ensure that thetelevisions would be available in time for the formerCommissioner to watch the NCAA basketballtournament.Recommendations: We recommend KDA ensure thatall purchases have a legitimate business purpose thatcan be justified as necessary expenses to carry out themission of the agency. While agencies such as KDAshould have discretion in the items purchased, they

should be able to clearly demonstrate, when requested,the necessity of the purchase and how the expensebenefitted the mission of the organization.

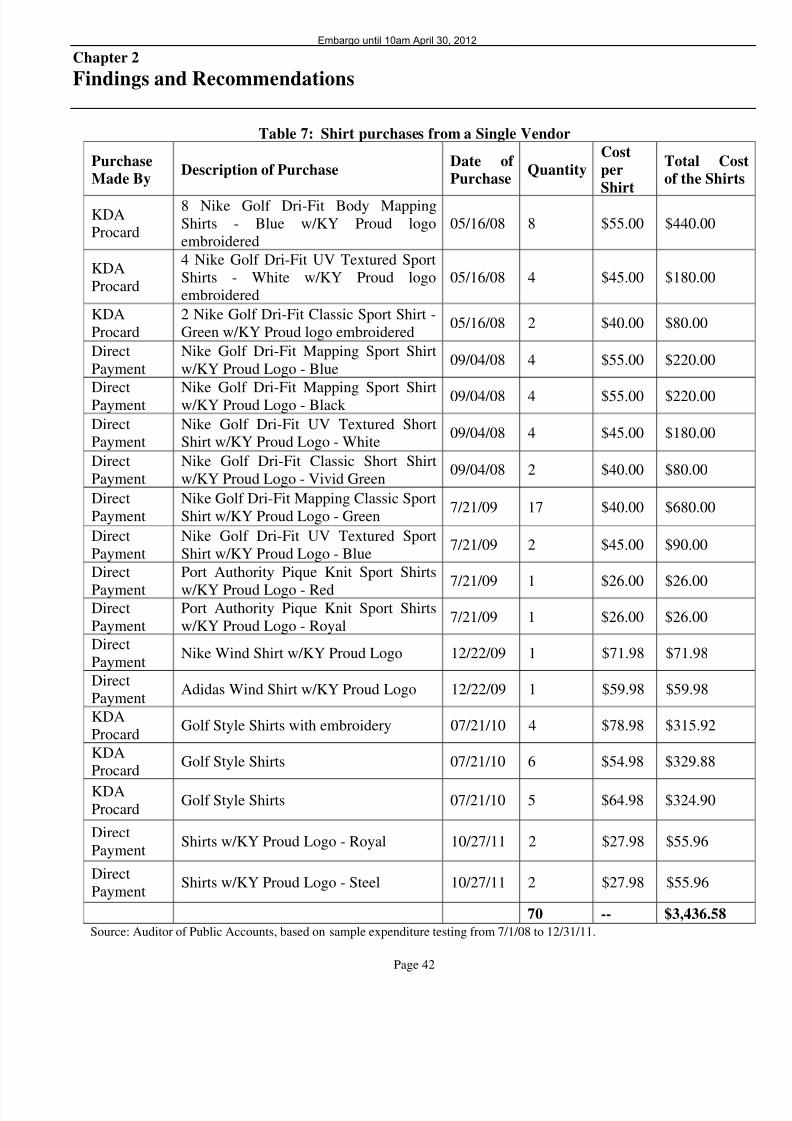

Finding 16: KDA reimbursed the former KDACommissioner and other non-merit employees forquestionable expenditures.Questionable reimbursements were found in our judgmental sample of employee reimbursements.While reimbursement guidelines for elected officialsdiffer from those for other state employees, only

expenditures necessary for official business should reimbursed. In certain instances, reimbursemedocumentation auditors reviewed did not identify tbusiness purpose for the expenditure, and a few itemfor the former KDA Commissioner were placed another employee’s travel voucher. Requests freimbursement were made for computer and cell phoequipment, as well as for gasoline purchases when temployee was reportedly driving a state vehicle.

Recommendations: We recommend KDA ensurequests for reimbursement are consistently supportby documentation that shows a necessary businepurpose for the expenditure. We also recommend threquested reimbursements that may be questionable nbe paid until documentation supporting the necessabusiness purpose of the expenditure is provided.

Finding 17: A former KDA employee received estimated $70,457 in payments for work and mileareimbursement where he did not appear to haproduced any work product.

A former KDA employee appears to have been paid fwork hours claimed that he did not work areimbursement for mileage he did not incur on behalf KDA. Based on a review of the former employeetimesheets, travel vouchers, and other documents fthe time period of June 2007 through December 201it appears the former employee received payment ftime claimed at unassigned work locations, when he dnot produce required market reports, claiming perform unknown work from home, and claiming motime than assigned duties required. The review alindicates that the employee received reimbursement f

mileage for travel that appears to have either noccurred or was not incurred on the behalf of KDA. total, the APA calculated that, at a minimum, tformer employee was paid for 3,108 work hours a11,958 travel miles where apparently no known wowas produced. Total costs for these payments aestimated at $70,457.Recommendations: We recommend KDA ensure employees are properly assigned sufficient duties create a full work schedule. We recommend all fiestaff, regardless of merit status, be assigned a diresupervisor that has the opportunity and capacity

attest that work duties are being completed and a finwork product submitted when required. The field stsupervisors should be responsible for signing temployees’ timesheets and travel vouchers. For thoemployees whose work time is segregated betwevarious supervisors, all supervisors should sitimesheets and travel vouchers or otherwise documecommunication to a primary supervisor that temployee’s work can be confirmed. KDA should avoa conflict of interest by not allowing one immediafamily member to supervise another. Immediate fam

members should not be allowed to sign the timesheetsor travel vouchers of another family member. We alsorecommend KDA seek the assistance of the ExecutiveBranch Ethics Commission to provide training to allKDA employees on the requirements of the ExecutiveBranch Code of Ethics.

Finding 18: No significant work can be confirmedfor a non-merit employee who had a personal

relationship with the former Commissioner.At the direction of the former Commissioner of Agriculture, a non-merit Staff Assistant with whom hehad a prior personal relationship was hired and startedemployment on October 31, 2011 at a salary of $5,000per month. According to interviews with KDA staff,the daily duties of the new Staff Assistant were notknown and they rarely saw her at the KDA officesperforming any work. Employees interviewed statedthey seldom saw the new Staff Assistant in the officeon work days, though two employees stated theywitnessed her at the former Commissioner’s home on at

least two work days. While the Staff Assistant did takeleave without pay for a total of 29.5 hours during hertenure at KDA, it does not appear to account for thesignificant amount of time staff members have statedshe was missing from the office.Recommendations: We recommend that KDA ensureall employees are accountable to perform their assignedduties and that those duties benefit the public throughthe mission of the agency. Supervisors should havedirect knowledge and oversight of the employees’activities before signing timesheets. If a conflict of interest arises due to close personal relationships

between the supervisor and employee, a separatesupervisor should be assigned to sign the timesheet thatwill also have direct knowledge of the employee’sactivities.

Finding 19: A KDA Amusement Safety InspectorSupervisor appears to have received pay and the useof a state vehicle when no KDA-related work wasperformed.Between June 10, 2011 and June 26, 2011, a GPStracking unit was attached to a KDA vehicle issued toan Amusement Safety Inspector Supervisor. A

comparison of the reports generated from the GPSdevice, the employee’s timesheets, and the employee’ssubmitted ride inspection forms indicates that theemployee was paid for work days when no inspectionswere performed. The comparison also indicates that theemployee charged more work hours than should havebeen required for the days that inspections wereperformed. Finally, the GPS report shows that theKDA-issued vehicle was used on days that theemployee did not report any work hours, indicating thatthe vehicle was used for personal use. Only seventeen

days of this employee’s activity could be reviewed dto the GPS unit failing, which, according to certaKDA employees interviewed, may have been due

intentional tampering with the unit.

Recommendations: We recommend that KDA ensuthat all information indicating that an employee is nproperly executing their assigned duties be properreported to all appropriate supervisors in a timemanner. We recommend the information be acted upin a manner commensurate with the determinviolation or infraction of state personnel law regardleof the relationship an employee may have with supervisor or agency official. We also recommeKDA seek the assistance of the Executive BranEthics Commission to provide training to all KDemployees on the requirements of the Executive BranCode of Ethics.

Finding 20: KDA appears to have preselectcandidates for merit employment.Auditors found evidence indicating the former KDadministration preselected candidates for appointmeninto KDA merit positions. This activity reportedoccurred at the direction of the former Commissionwho had the final appointing authority at KDA.Recommendations: We recommend that KDA contathe State Personnel Cabinet to determine what trainiopportunities exist related to the best practices fhiring state employees. We recommend KDA ensustaff involved in the personnel process, including thoinvolved in the interview and hiring process, receiadequate training to ensure their knowledge of prop

personnel processes. We also recommend KDinterview panel members document in writing threcommended candidate, and that this documentatibe filed and maintained in the individual interview filWe further recommend the appointing authority giserious consideration to the recommendations made the interview panels. We further recommend that if tappointing authority chooses a candidate other ththose recommended by the interview panel, that tappointing authority consider discussing the mattfurther with the interview panel members and documethe decision in writing with an explanation

accompany the final decision.

Finding 21: The former KDA administration issumonetary awards, and at least one reclassificatiowithout a recommendation from employee

supervisors.According to former KDA management, the formKDA Commissioner, in certain instances, determinwhich employees received ACE awards or jreclassifications. Auditors were informed that t

determinations were made without input fromemployees’ supervisors, and that the former PersonnelDirector would then create a justification to support theaction.

Recommendations: We recommend KDA create aformal written process by which its personnel actionsinvolving ACE awards and reclassifications will beawarded. KDA should ensure that the process includes

input at the beginning of the process from immediatesupervisors so that the justification for a personnelaction is based on the quality of work andaccomplishments of the employee.

Finding 22: A merit employee’s job responsibilities

were eliminated, but the action is not documented inhis personnel file.Numerous KDA staff interviewed by auditors statedthat the job duties were taken away from the AssistantDirector of the Regulation and Inspection Division.Employees were instructed not to assign any tasks or

send telephone calls to or ask questions of theemployee. This directive included taking away theemployee’s access to KDA computer databases.According to the Executive Director of the Office forConsumer and Environmental Protection, he wasinstructed to “put him in a corner” by the former Commissioner. No specific reason was provided as towhy this action was warranted, nor did the employee’spersonnel evaluations support that this type of actionwas taken or that the employee was counseled aboutperformance issues. Recommendations: We recommend that KDA ensure

that all employees are provided with specific job dutiesand responsibilities that reflect an employee’s jobclassification within the agency’s personnel structure.We further recommend that an employee’s personnelrecord and performance evaluations documentsignificant actions taken by management involving anemployee.

Finding 23: KDA interview file documentation forhiring employees was incomplete.In response to allegations received by auditors duringmultiple interviews with current and former KDA

personnel, auditors examined various KDA interviewfiles maintained by KDA’s Division of Personnel andBudget related to hiring employees, and found that filedocumentation maintained by KDA was inconsistent,and in one case missing altogether.Recommendations: We recommend KDA requesttraining from the Personnel Cabinet regarding theproper documentation to maintain and process to followwhen hiring an employee. We recommend that all KDAemployees who are involved in the hiring processattend the training. After the training, we recommend

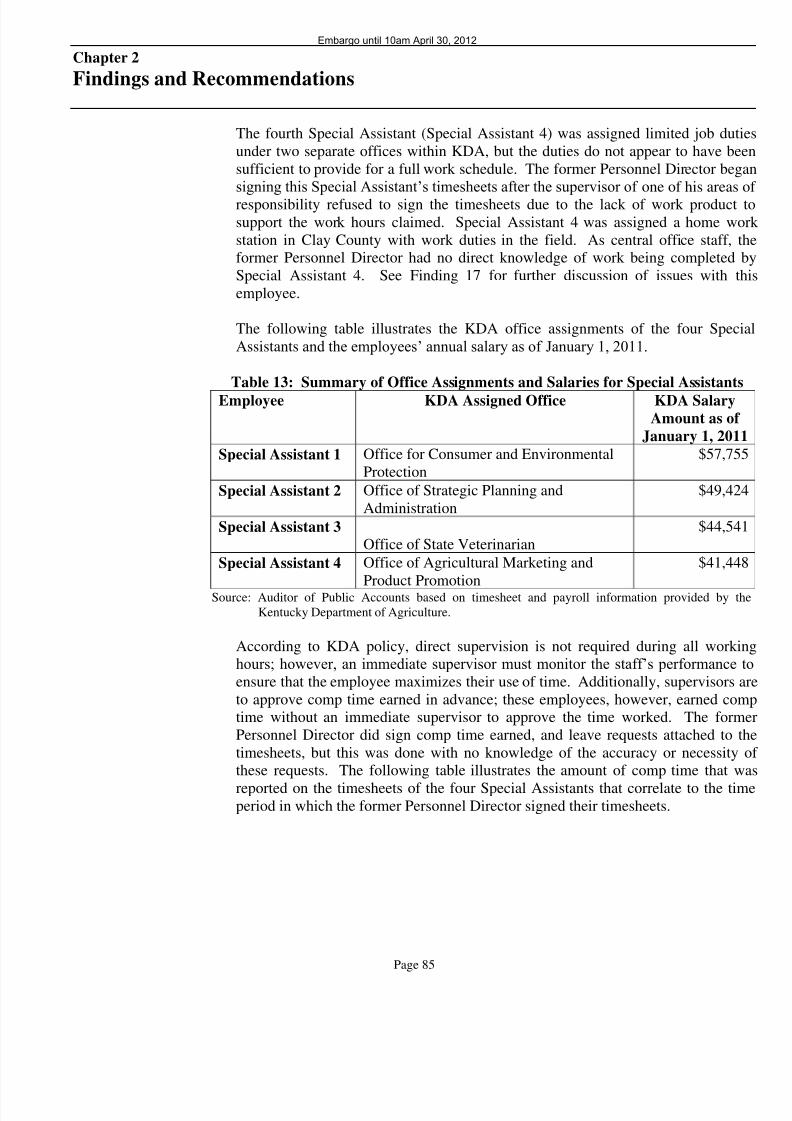

KDA establish a written policy detailing the procethat will be followed, documentation required to retained, the documentation retention period, and toffice responsible for retaining the information.Finding 24: The timesheets of four KDA non-meemployees were signed by the former PersonnDirector and not by a supervisor with direoversight of the employees’ work. During the period under review, the timesheets of fo

non-merit Special Assistants within four KDA officwere signed by the former Personnel Director instead officials within the four employees’ assigned officwith direct oversight of the employees’ work. addition, the four employees were given either limitor no specific job duties. Without a supervisor directly monitor employee activity and to approve thetimesheets, an employee’s performance and use of timcannot be accurately determined, regardless of wheththe employee has merit or non-merit status. Also, tvalidity and necessity of these positions is questionabif there are either no assigned or limited duties for t

employees to perform.Recommendations: We recommend all field staregardless of merit status, be assigned a diresupervisor who has the opportunity and capacity attest that work duties are being performed acompleted. We also recommend that KDA only creaemployment positions that have specifically defined jduties and that are a necessary and justifiable expenof public funds. We also recommend KDA considabolishing positions if the job tasks are not necessarythe daily functions of these offices. We furthrecommend that the Personnel Director only sign t

timesheets of the employees directly supervised by tPersonnel Director.

Finding 25: No entry level class exists for KDamusement park inspectors.During interviews with KDA personnel, auditors fouthat amusement park safety inspections were performby employees working for KDA in a general sericlassification that requires no mechanical backgrouneducation, or experience. Given the mechanicequipment involved in amusement park rides, tpopularity of such attractions, and the human safe

risks associated with these rides, it seems reasonabthat the job classification require some level associated mechanical knowledge or experience.Recommendations: We recommend KDA considreviewing the Agriculture Inspector series to determiwhether it would be reasonable to create an entry levposition specific to the amusement ride inspections threquires some level of associated mechanicknowledge or experience, and, for at least an inititime period, inspections by entry level employees arebe performed under the direct oversight of a superviso

We further recommend KDA consider requiringinspector supervisors to be certified to performamusement devise inspections.

Finding 26: A former Director was the soleemployee in the “Division of Outreach and

Development,” which was not a legally recognized

unit of KDA.During an interview with the current Deputy

Commissioner of Agriculture, he stated that he servedas the Director of Outreach and Development under theprevious KDA administration, and in that position hewas a “division of one” with no other employeesworking in the division. While auditors confirmed theDirector acted as a “division of one,” personneldocumentation indicated that the position of “Director of Outreach and Development” did not actually exist inKDA’s official organizational structure, and that theemployee’s position was actually funded as part of theDivision of Value-Added Animal and AquacultureProduction.

Recommendations: We recommend KDA review andreconcile its formal organizational structure to theactual structure under which KDA operates. KDAshould ensure that its Master Position report properlyreflects the duties, job functions, and responsibilitiesperformed. We also recommend KDA ensure that asupervisory position is necessary, justified, and meetsthe requirements for such a position before placing anemployee in the position. We further recommend KDAensure that employees’ duties properly reflect the jobclassification duties and responsibilities performed bythe employee.

Finding 27: KDA staff incurred a significantamount of overtime and expenses for staffing theState Fair.A significant amount of overtime was earned by KDAstaff when working at the Kentucky State Fair. Inaddition, our Procard review found several expendituresfor food and drinks incurred for the purpose of ahospitality room at the State Fair. While KDA has avery important role in this statewide event, KDA’smanagement should control staff time and extra costs tokeep these at a minimum.

Recommendations: We recommend KDA ensure onlystaff with specific responsibilities are used in support of the Kentucky State Fair. We also recommend that foodand drink expenditures be reimbursed only if they arereasonable and necessary.

Finding 28: The operation of KDA’s fuel and

pesticide testing laboratory (Fuel Lab) cost KDA$903,389 in FY 2011, yet it has not reached theanticipated test sampling goals publicized whenconstructed at a cost of $1.65 million in FY 2008.

A new Fuel Lab, constructed for KDA in FY 2008, coKentucky $1.65 million and continues to incsignificant costs to operate without having reached anticipated test sampling goals. While the goal testing 20,000 fuel samples was publicized to reached during the Fuel Lab’s first full year operations, the Fuel Lab tested only 3,786 fuel samplthat year. It is questionable whether enough researinto the Fuel Lab’s feasibility was conducted prior

KDA’s request for its construction. If a feasibilstudy was conducted, the study and associatdocumentation was not maintained by KDA. Tconcept to increase test sampling and the desire conduct these tests internally at KDA rather thpaying an outside vendor is beneficial and importabut the publicized goals do not appear to have berealistic, and they have not been accomplished.Recommendations: We recommend that KDevaluate all aspects of the Fuel Lab to maximize the uof this facility and increase the testing of Kentuckymotor fuels and other types of fuel and pesticide

Efforts should be increased to contract with other statto assist KDA in funding the expenditures incurred fthis testing now that the Fuel Lab has been establishand meeting in compliance with the regulations testing organizations.

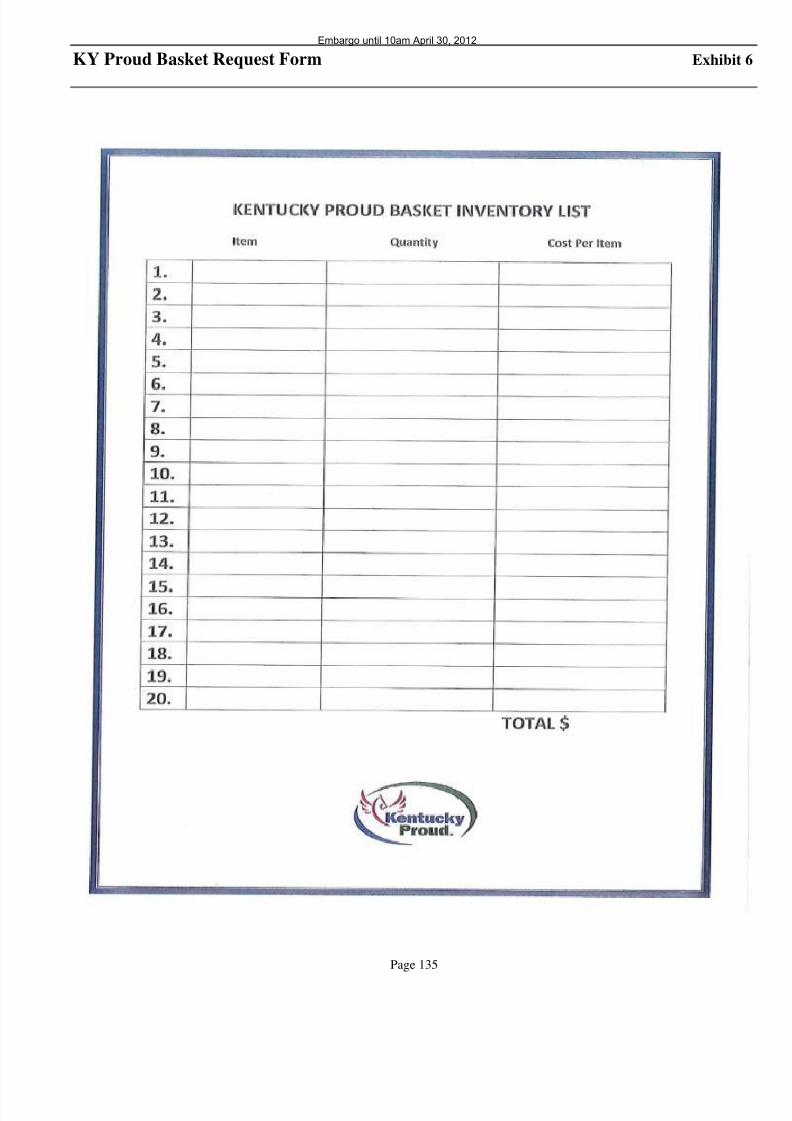

Finding 29: During the audit period, KDA did naccount for the disposition of promotional KProud products bought by KDA or received donations from KY Proud vendors.During the audit period, KDA tracked the use of KProud items with the KY Proud logo such as ha

pencils, and other items. In addition, KDA hestablished a system for staff members to request theitems for events or other circumstances. HowevKDA did not document the use of KY Proud producnor did it have a process in place to ensure personnwere not accessing the products for their personal usKY Proud products should be used to fulfill the purpoof the program, which is to promote the KY Provendors, and are not intended to be used for personbenefit.Recommendations: We recommend that KDA creadocument, and implement a process to account for

KY Proud products held for promotional purposeRelevant information, including the cost, source, abusiness use of the products should be appropriatedocumented when the items are received adistributed. We further recommend that KDA continto document and implement the process related to tnewly created KY Proud Basket Request Form. KDexecutive staff should use these forms to review tquantity and cost of the gift baskets to document thbaskets are appropriately valued for each occasion a

to determine whether the cost of the gift baskets is aneffective method to achieve promotional objectives.

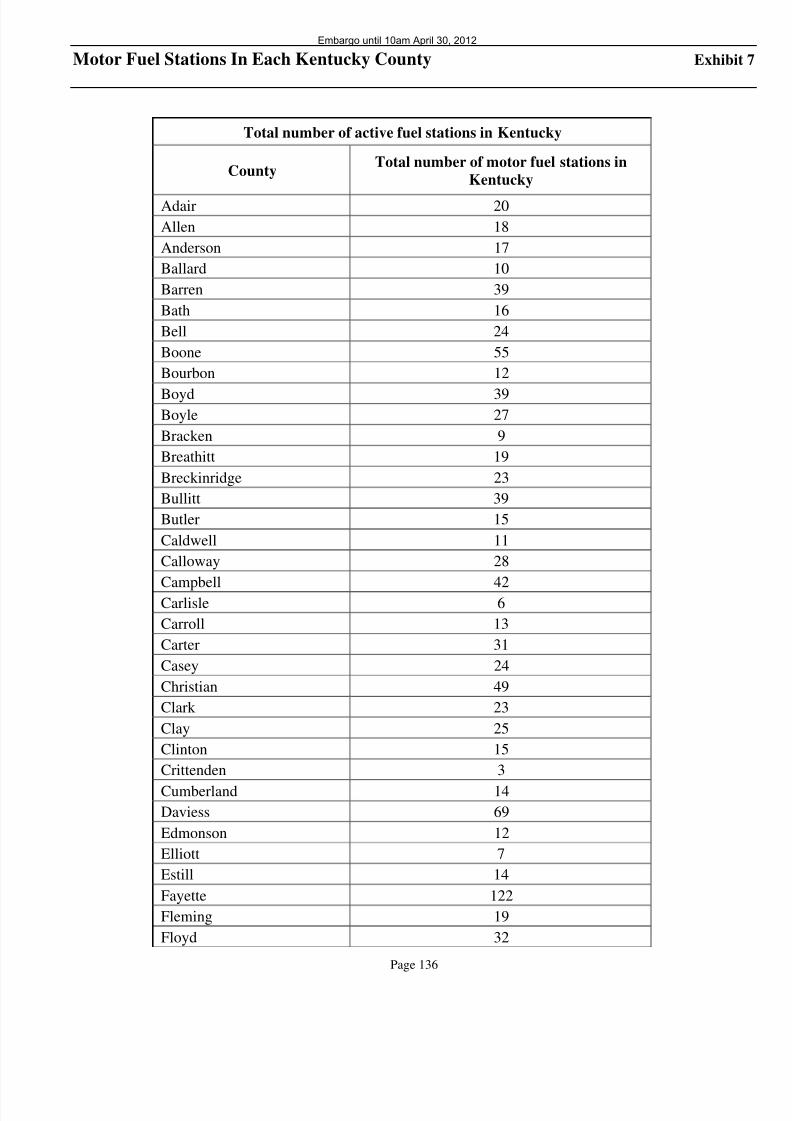

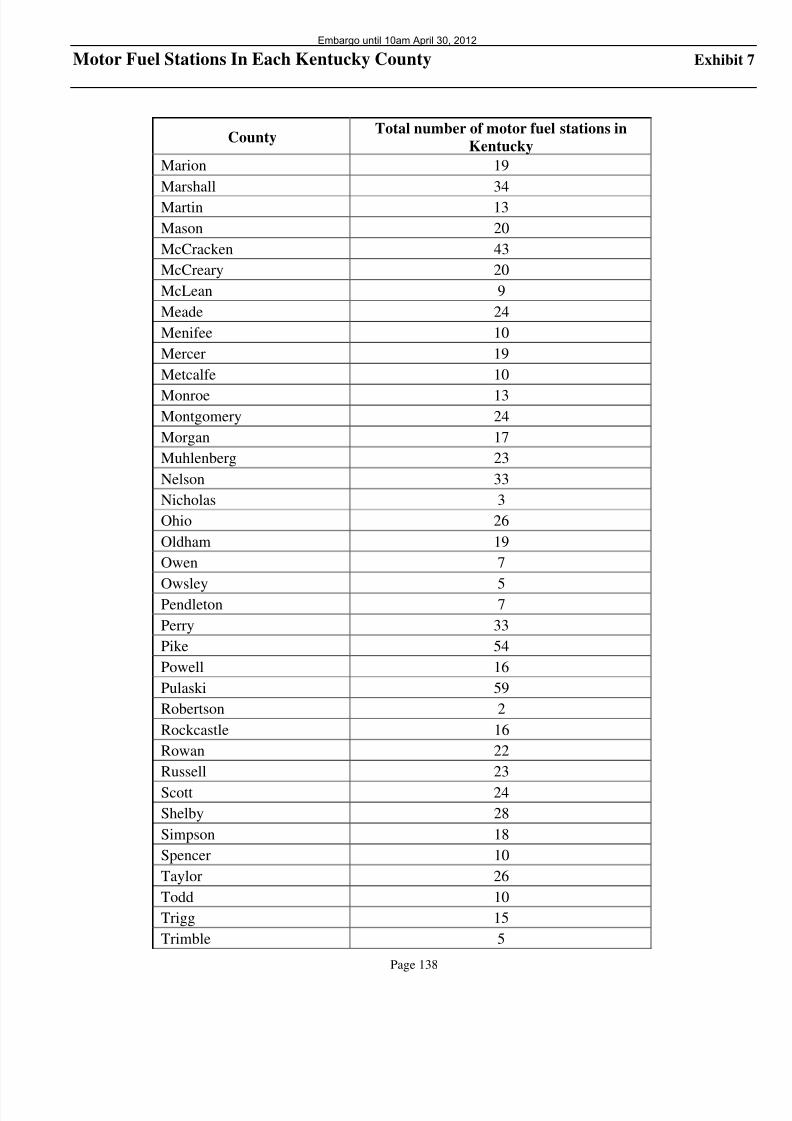

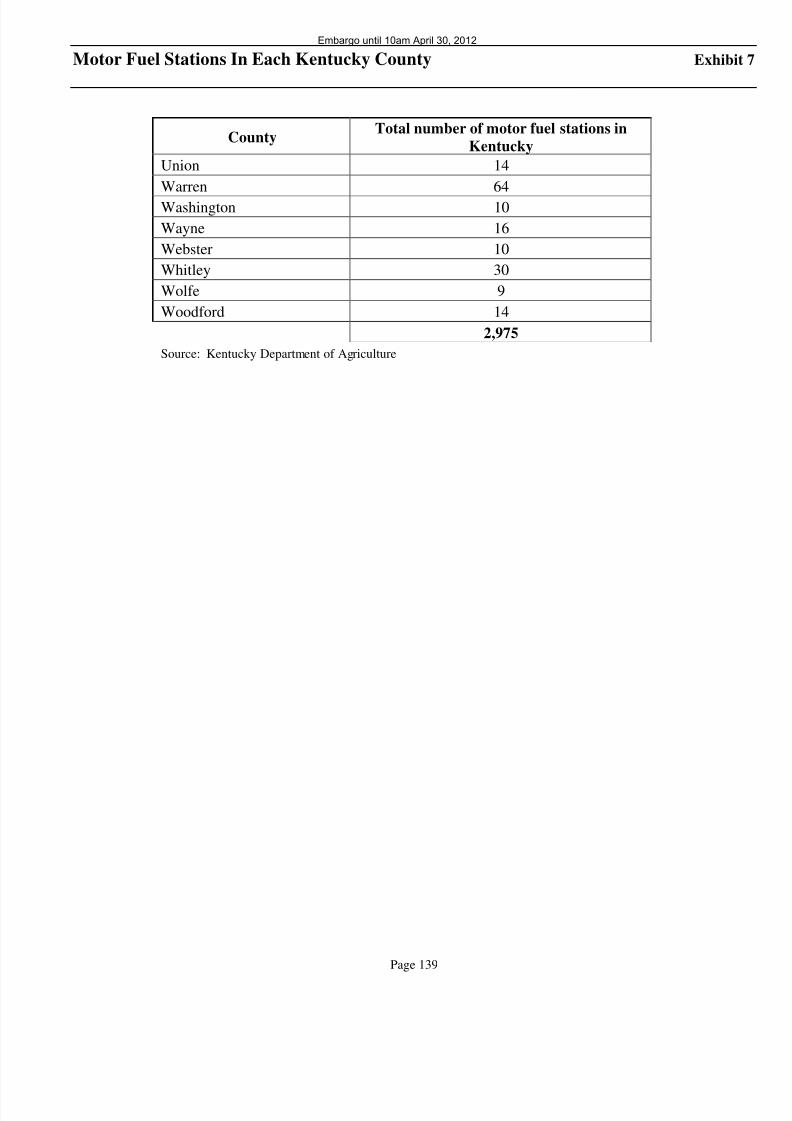

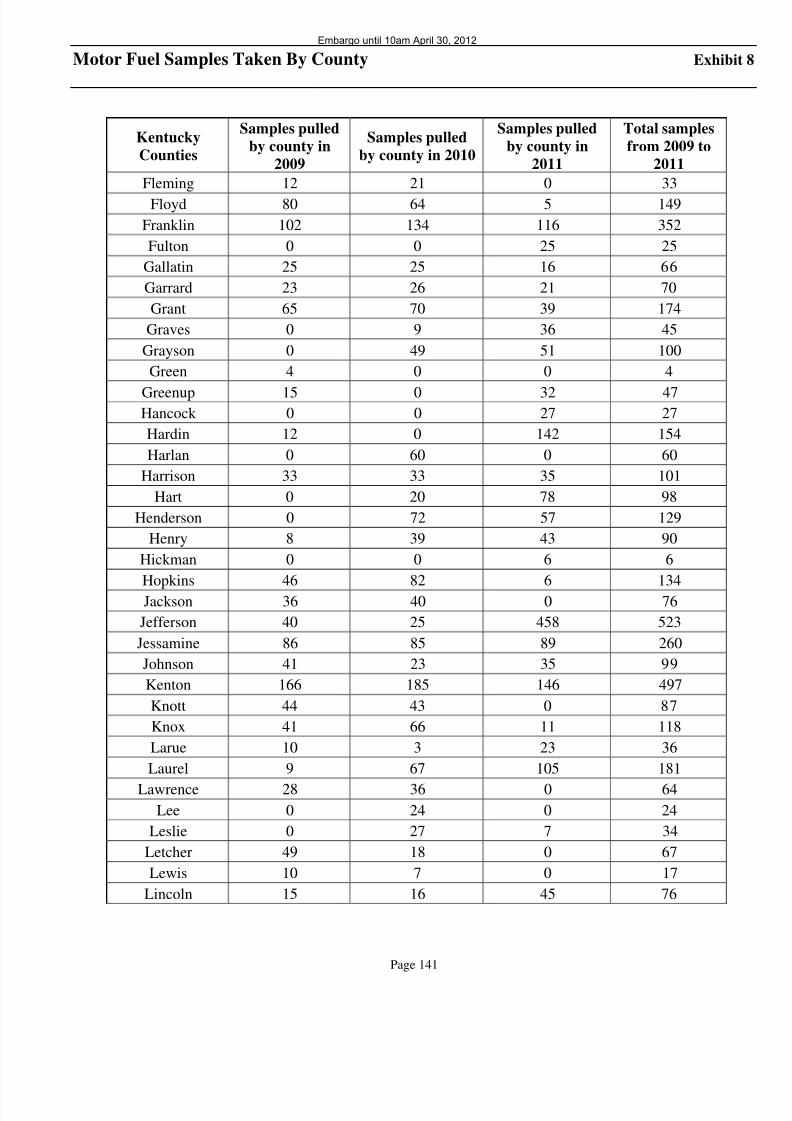

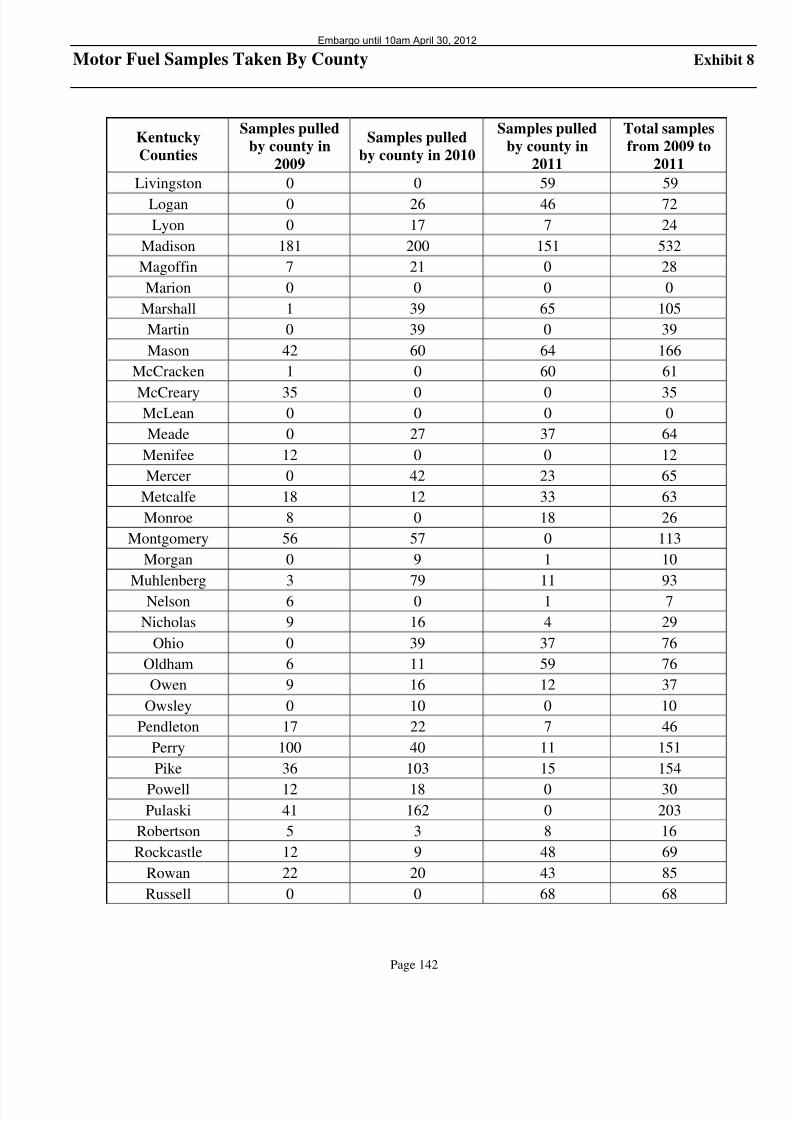

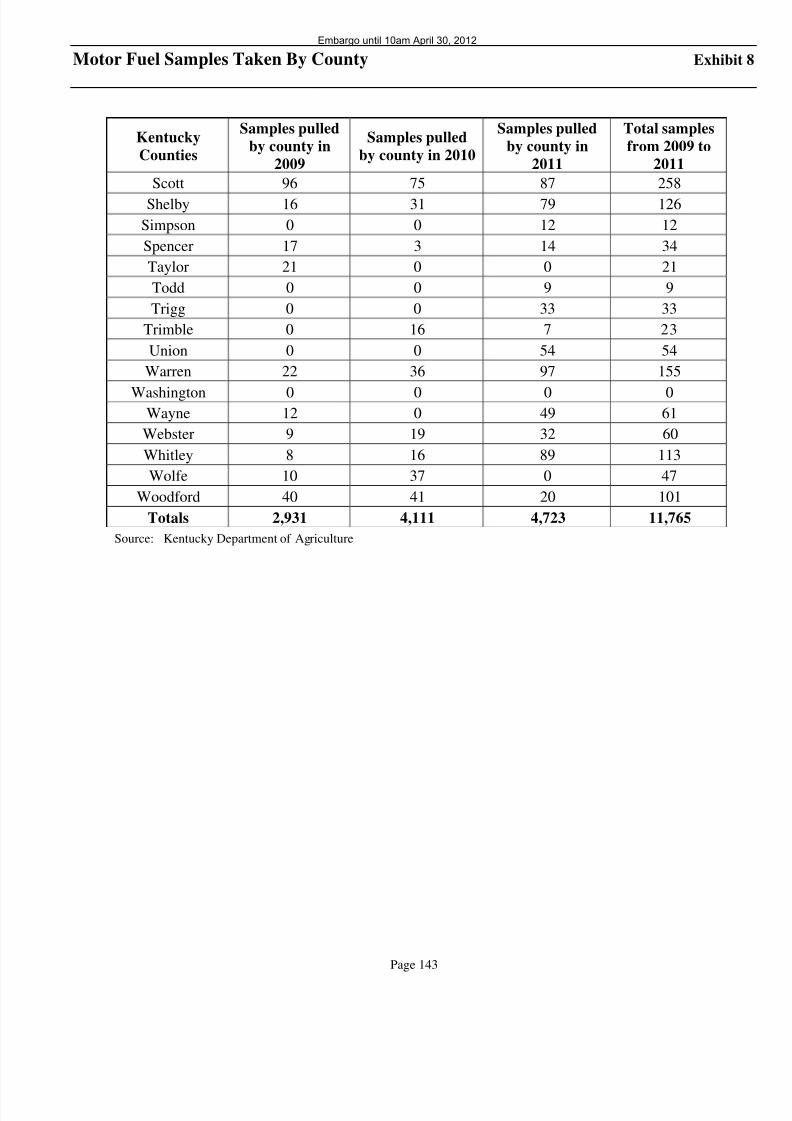

Finding 30: KDA had not established a regularinspection plan for testing motor fuel quality.Under the former KDA administration, the KDADivision of Regulation and Inspection had notestablished an inspection plan for the testing of motorfuel quality, testing that they are statutorily required to

perform. The number of motor fuels tested inKentucky counties varied from 2009 to 2011. Auditorsfound KDA’s inspectors performed inconsistent testing,as they did not sample motor fuels in some counties inKentucky for two or three of the past five consecutiveyears. Additionally, stations in some counties whosemotor fuel quality was tested failed the tests, but thestations were permitted to continue selling motor fuelswithout follow-up testing.Recommendations: We recommend that KDAestablish a systematic fuel inspection plan, whichshould include, at a minimum, a schedule to test motor

fuel in each Kentucky county within a given timeperiod. The plan should take into consideration thenumber of fuel stations in each county. KDAmanagement should determine the best course of actionto take in order to perform this testing and work into theplan the ability to inspect complaints with the staff available. Once testing of all stations is complete,KDA should start the cycle of inspection and testingagain. We also recommend KDA develop a process toensure that any and all motor fuel stations with anyfailures be re-tested before the station is permitted tocontinue selling their motor fuels.

Finding 31: KDA did not reimburse employees forhome internet connections in a consistent or uniformmanner.KDA reimbursed up to 70 employees for home internetconnections with individual monthly costs that variedfrom $14.95 per month to $97.64 per month for a totalmonthly expense to KDA of $2,352. These varied costsencompass both partial and full monthly costs for high-speed internet, and in at least one instance, it appearsthe cost may include the bundled costs of telephoneservices. The rate at which an employee gets

reimbursed appears to depend on the supervisor thatoversees an employee and the geographic location of the employee’s workstation. The process was notadministered in a uniform manner and there are nopolicies specifying the criteria for an employee toreceive the reimbursement, the allowablereimbursement amount, or the services that may beincluded for reimbursement.Recommendations: We recommend KDA conduct athorough review to determine whether reimbursementfor home internet service of certain field staff is a

necessary expense to ensure that employees are able effectively and efficiently carry out their assignduties, or if other cost effective methods are availabIf it is determined that such an expense is necessary a justified, we also recommend KDA develop a writtpolicy that establishes the process for requesting aapproving home internet reimbursement for field staThe policy should establish clearly defined criteria fdetermining which employment positions shou

receive reimbursement to ensure personal prejudices not come into play in the decision-making proceFinal approval should be centralized with a singexecutive officer to ensure a consistent process followed. The policy should also establish standardized limit on the amount that may reimbursed for all employees, based on the expectusage of the service for work purposes.

Finding 32: KDA inventory records weincomplete and not adequately maintained.According to one KDA Executive Director, during t

current Administration, KDA employees began express concern that KDA did not have adequainternal controls to properly monitor inventory. Afconducting several employee interviews and examinithe inventory records for items valued between $5and $5,000, auditors found that most items on tinventory list were over ten years old, and that tagency has struggled for years to maintain accurainventory records.Recommendations: We recommend KDA review current inventory process to ensure adequate recokeeping of its inventory items. If KDA maintains

separate inventory system outside of the stateaccounting system, the agency should ensure there isreasonable methodology by which to reconcile records with the state’s system so that the items cproperly be accounted for during physical inventocounts. Finally, we recommend KDA assiappropriate personnel to maintain and monitor tinventory process and routinely perform spot checks inventory items to ensure they are properly recordand accounted for.

Finding 33: KDA tracking of Sweet Sixte

basketball tournament tickets.During our examination period, a contract was enterinto between the Kentucky High School AthleAssociation (KHSAA) and KDA. According to tcontract, KDA agreed to buy a merchandising packafor the Boys’ and Girls’ Sweet Sixteen basketbtournaments. The merchandising package providKDA with four Boys’ Sweet Sixteen tickets in Secti30, Row AA, and four tickets in Sections 16 or 12 at charge. KDA and KHSAA continued this annuagreement thru 2011. From 2007 through 2011, t

cost of the agreement ranged from $33,100 to $36,750per year.Recommendations: We recommend that KDAdevelop a policy that stipulates who is to receivesporting event tickets or other items received by KDAwhen entering into promotional or other contracts oractivities. We recommend the policy requiredocumentation be maintained to identify the number of tickets or other items that may be received, who

initially received the tickets or other items, whoultimately received and used the tickets or other items,and the business purpose related to the use of the ticketsor other items.

Finding 34: A KDA executive director and formerdirector told staff to delay action regarding a graindealer because it was an election year and may causea negative political outcome for the formerCommissioner.The former Executive Director of the Officer of Consumer and Environmental Protection told the

supervisor of inspectors for licensed grain dealers toavoid taking action on a licensee that, according to agrain inspection report, was in violation of the suretybond requirement under KRS 251.720(6).Recommendations: KDA should not allow politicalconsiderations to interfere with the inspection andlicensing process. Any such instances of interferenceshould be reported to the Executive Branch EthicsCommission.

Finding 35: KDA is not adequately tracking fines ithas issued and has no policy relating to probating

those fines.KDA, however, cannot accurately determine theamount of unpaid fines due to database system designlimitations. The amount of unpaid fines is maintainedprimarily in the database system, but this system wasdesigned for licensing purposes and not for trackingfines. The database system reports are in PDF formatand the data is difficult to obtain in an electronicspreadsheet. Without a user-friendly data format tocalculate outstanding fines, the data is difficult to usefor managing outstanding fines, and the databasesystem is inefficient for collecting fines. Also, the data

within the database system has to be manually updated,and these manual changes have not always beenupdated in a timely manner. KDA does not have anywritten policies and procedures relating to the finecollection process. Recommendations: We recommend that KDAdevelop and implement detailed policies andprocedures for recording and collecting outstandingfines. We also recommend KDA develop aspreadsheet, or purchase software, that will capture finehistory, allow for fine adjustments to be recorded, and

generate detailed reports. KDA should provide trainiin tracking and collecting outstanding fines. KDshould routinely update, monitor, and test the validiof outstanding fine data.

Finding 36: KDA cannot determine whethmaintaining its fleet of vehicles is the most coefficient method and vehicle assignments compwith Finance Cabinet guidelines.

KDA manages its own fleet of vehicles but must follothe same guidelines established by Finance Cabinet fall other state vehicles. KDA currently owns 183 stavehicles with 132 staff having an assigned take homvehicles. While cost savings have been claimed for tinternal management of the KDA fleet, these numbewere based on estimates instead of actual numbeKDA is not required to justify their entire fleet vehicles, but KDA is required to justify, at leaannually, the assignment of take home vehicles. Bason these guidelines and KDA’s 2011 justificatireport, 24 of the take-home assignments a

questionable. In addition, from 2010 to 2011, 11 stwere removed from the list of having state vehicles dto concerns that they did not meet the criteria of tFinance Cabinet Recommendations: We recommend that KDA ensuthat a comparison of the cost to operate an agency flerather than lease vehicles through the Finance Cabinbe based on available actual data to ensure a fair anaccurate evaluation of the KDA fleet’s necessity. Walso recommend KDA only request permanentassigned vehicles for those employees who fall withthe permanently assigned vehicle requirements as s

forth by the Finance Cabinet. KDA should review thcurrent permanently assigned vehicle listing and ensuall of the Finance Cabinet’s criteria are met and thatis necessary and reasonable for an employee to permanently assigned a vehicle. KDA should ensuthat the mileage for each employee is maintainaccurately in the system so that this review is based complete mileage information. We further recommeKDA maintain a complete history of permanentassigned vehicles and the justifications that asubmitted to the Finance Cabinet for approval. T justification for a permanent vehicle assignment shou

be sufficiently detailed for the Finance Cabinet to maan informed decision whether to approve the requeThe information maintained should include information pertinent to the employee, their jdescription, and work county, at a minimum. Thinformation should be consolidated into a singsearchable database.

Finding 37: KDA exceeded its small purchaauthority without initiating a contract.

KRS 45A.100(3) states that the Finance Cabinet maygrant to any state agency a small purchase authority inaccordance with regulations promulgated by theFinance Cabinet. In 2007, KDA was granted anincrease in its small purchase authority from $1,000 to$5,000 that allowed KDA to purchase items or services,up to $5,000, without having to competitively bid forthose goods or services costing less than $5,000.However, KDA procured services from a mobile car

wash vendor that included services for hand washingcars, vans, sport utility vehicles, pick- up trucks,trailers, and other KDA vehicles and machinery. KDApaid the car wash vendor $5,855 in FY 2010 and$5,390 in FY 2011, which exceeded the KDA smallpurchase limit of $5,000.Recommendations: We recommend that KDA followall applicable statues and regulations concerning thepurchase of goods and non-professional services. Werecommend that KDA monitor all small purchases,whether through direct pay or Procard purchases, toensure that they are not exceeding their small purchase

authority by parceling, splitting, dividing, or schedulingpayments over a period of time that may cause the$5,000 small purchase limit to be exceeded. If purchases exceed the $5,000 small purchase authoritylimit of KDA, the Finance Cabinet should be contactedto initiate a Master Agreement for solicitation.

Finding 38: KDA did not consistently reporttaxable income for the use of state vehicles, nor wasany additional taxable income reported foremployee benefits such as internet and cell phonecosts.

The amounts reported by the KDA to the IRS asadditional income to employees for employee benefitsdo not appear to be consistently or fully reported basedon the employee benefits provided. KDA did not havepolicies related to employee benefit reporting eventhough KDA employees receive benefits related tovehicles, home internet costs, and the use of cellphones. Improper reporting of taxable income preventsKDA from fully complying with IRS reportingrequirements.Recommendations: We recommend that KDAestablish a policy to address how the personal use of

state vehicles will be tracked so that all KDAemployees with state vehicles will be expected to reporta taxable benefit. A consistent reporting method shouldbe adopted to ensure that all employees are incompliance with IRS regulations. We also recommendthat a method of reporting the taxable benefit related toother employee benefits, such as internet services andcell phones, be developed and documented for eachperson receiving this benefit. The reporting methodshould be explained to each employee so that each isaware of the issues when receiving this benefit. The

amount reported as additional taxable income should reviewed to ensure that all applicable employees areporting for benefits consistently. We furthrecommend that KDA’s elected Commissioner compwith the IRS and Kentucky Personnel Cabinet to trathe business use of assigned vehicles so that the annulease valuation rule can be used to determine tamount of additional income to be reported.

Finding 39: Procard procedures should strengthened.A state-issued credit card, called a Procard, is providto state agency employees authorized to have oissued to them, based on their need to purchabusiness-related goods and services for the agencAlthough the card is issued in the name of temployee, it is considered state property and should used for agency purchases only. Cardholders aexpected to comply with internal control procedures fProcard use established by their agency and with tpolicies and procedures of the Finance Cabinet f

Procard use. While the overall conclusion of threview was that, for the period under examination, tKDA procurement process generally operated in adequate manner, the auditors did find four areas fpotential improvement.Recommendations: We recommend that KDA eithrequire the items entered on the Procard Certificatiform to be described with more specificity, or modithe process for pre-approving items to be purchased. addition, we recommend that KDA limit the use blanket approvals in an effort to better monitor tamounts spent at each special event. We al

recommend that KDA staff always provide detaildocumentation for all purchases. When tdocumentation provided by the vendor lacks detaistaff should provide additional descriptions and provi justification for the purchase. We further recommethat KDA list and tag the items maintained in inventofor special events, such as the state fair. KDA shouconsider moving all the items into one location fbetter control. KDA should also fully implement th

plans to use the “State Fair Small Inventory Check OForm” to monitor who has possession of the items.

Finding 40: KDA lacked a written policy regardidocumentation for livestock show payments ancertain administrative processes.KDA had no written policy for processing prize monand judge fees for livestock shows. KDA did nmaintain application/registration forms of livestoshow judges or for show participants. AdditionalKDA had no payment documentation to support fepayable to the judges for their services or for tlivestock show winners.

Recommendations: We recommend KDA develop apolicy that, at a minimum, requires uniform livestock application/registration forms to be completed by all judges of and participants in livestock shows. Wefurther recommend a schedule be developed specifying

judges’ fees and the prize amounts paid to winningparticipants. If there is a need to deviate from the feeand prize money schedule, the payments should besubmitted and approved by KDA prior to the show. In

addition, we recommend the judge’s application bereviewed prior to a show, if feasible, to ensure the judges are qualified and free of conflicts of interest.The judge’s application form should include astatement stating that by signing the application the judge is free of conflicts of interest, or will disclose inwriting any potential conflict prior to the event.

Finding 41: KDA did not maintain records todocument the disposal of returned cell phones incompliance with Surplus Property regulations.KDA did not have a policy or a documented method for

disposing of returned cell phones. KDA staff statedthat no records were maintained because the phoneswere obsolete. However, the Division of SurplusProperty within the Finance Cabinet should have beencontacted to approve the disposal of state property.According to FAP 220-19-00, the Division of SurplusProperty has the authority to declare and dispose of surplus property. KDA is working to improve themanagement of cell phones and should determinewhich of the allowable methods the agency will use todispose of cell phones to comply with this policy. Recommendations: We recommend that KDA

comply with FAP 220-19-00 and maintaindocumentation related to cell phones returned due todamage, termination of employment, or obsolescence,and request approval for disposing of the propertythrough one of Finance Cabinet’s prescribed methods.If donation to a charity is the desired method fordisposal, KDA should request the approval of thismethod and ensure that the selected charity is anapproved nonprofit charity according to establishedFinance Cabinet policies.

Report Referrals

Due to the nature of certain findings discussed withinthis report, we are referring issues within the report tothe Kentucky Office of the Attorney General, KentuckyExecutive Branch Ethics Commission, KentuckyPersonnel Board, Kentucky Department of Revenue,Kentucky Department of Fish and Wildlife, KentuckyAgricultural Development Board, Internal RevenueService, and the United States Department of theInterior Office of Inspector General.

On January 11, 2012, the Commissioner of the Kentucky Department Agriculture (KDA) formally requested that the Auditor of Public Accounts (APAconduct a special examination of the KDA that would be “thorough and sweepingThe Commissioner indicated to the press that in his first five days on the joemployees came forward with “several potentially troubling allegations” involvinthe administration of his predecessor. At a joint press conference later that dwith the Agriculture Commissioner, the State Auditor agreed to take a broad loointo the “administrative practices and fiscal management of the Department Agriculture” under the two terms of the last KDA Commissioner (formCommissioner).

Scope of andMethodology forExamination

The scope of this examination includes records, activities, and information for thperiod of January 1, 2004 through December 31, 2011, with an emphasis on the lafour years; however, the time periods used in the report vary due to the dates of thissues and the availability of the information.

To complete this examination, the APA reviewed documents, conducted interviewand tested expenditures. Thousands of documents, including emails, invoicereports, policies, timesheets, travel vouchers, and personnel files, were supplied bKDA staff, former staff, and other entities. These and other items were analyzed relation to the objectives of this examination. The findings, or results, from thexamination are discussed in detail in Chapter 2.

The APA conducted interviews with over 50 individuals, often following up on tinitial interviews with phone conversations, emails, and additional meetings. Tfollowing were among the many interviewed:

Current and former KDA staff members;

Kentucky Proud (KY Proud) vendors;

Finance and Administration Cabinet staff;

Personnel Cabinet staff;

Executive Director of the Executive Branch Ethics Commission; and the

Former spouse of the former KDA Commissioner.

The APA attempted to interview the former Commissioner; however, the formCommissioner declined to be interviewed.

Auditors selected a judgmental sample and reviewed certain types of expenditurfrom the examination period to determine the presence of required documentatioreasonableness of expenditures, and compliance with KDA policies. Suinformation included travel vouchers, timesheets, Procurement Card (Procarexpenditures, direct payments, and checks. The findings from these reviews aalso discussed, when applicable, in Chapter 2.

Agency History The Agriculture Commissioner is a state-level position in all 50 states. The dutiof the position vary from state to state, but their general role is regulation of variofacets of the agriculture industry, as well as promotion of state agribusiness. Whthe vast majority of the states that do have the statewide governmental positioauthorize the governor to appoint an individual to the office, there are at least others which have opted to have citizens vote to select the office holders. Thestates include Alabama, Florida, Georgia, Iowa, Kentucky, Louisiana, MississippNorth Carolina, North Dakota, South Carolina, Texas, and West Virginia.

The Fourth Constitution of Kentucky in 1891 established the Commissioner Agriculture as a state-level position publicly elected by the people of the stathrough the primary/general election process to serve a four-year term. The generrole of the Commissioner has remained much the same as when it was first create – to promote the interests of Kentucky agriculture and horticulture.

At the end of the examination period, KDA had 302 personnel positions, 36 which were vacant. KDA was organized into five executive offices including tOffice of the Commissioner, the Office for Consumer and EnvironmentProtection, the Office of Agriculture Marketing and Product Promotion, the Offi

of the State Veterinarian, and the Office for Strategic Planning and Administration

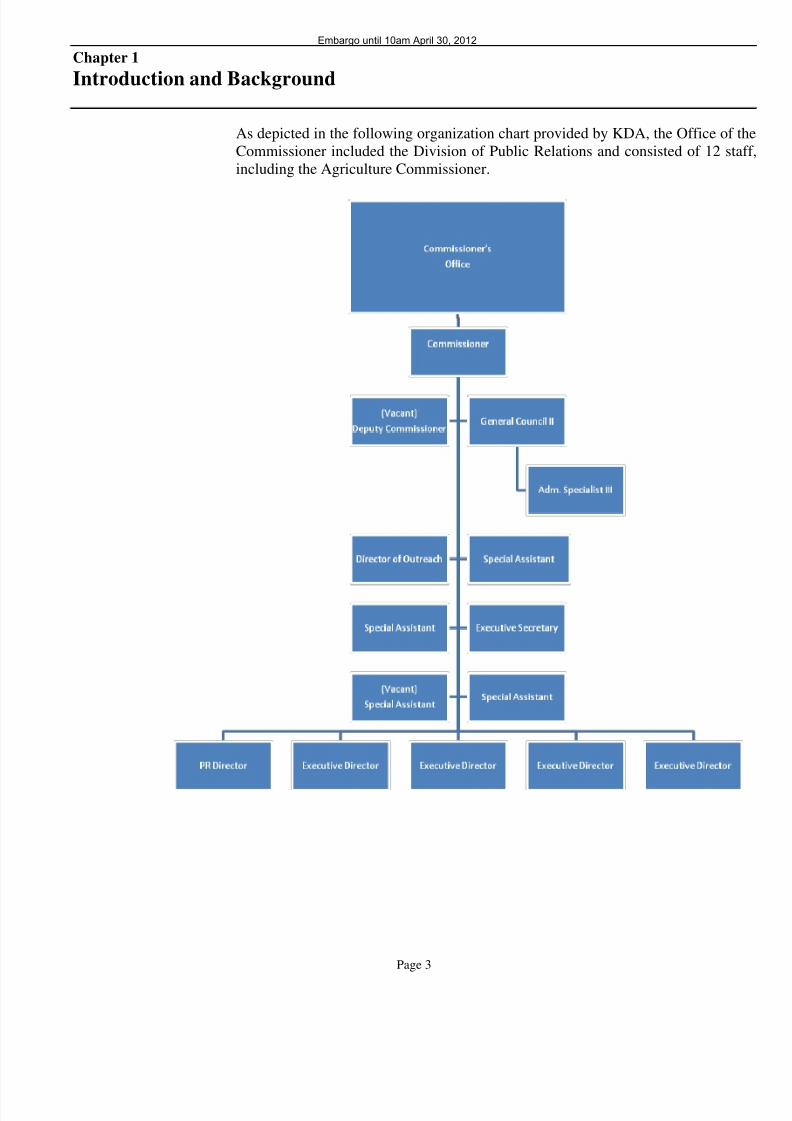

As depicted in the following organization chart provided by KDA, the Office of thCommissioner included the Division of Public Relations and consisted of 12 staincluding the Agriculture Commissioner.

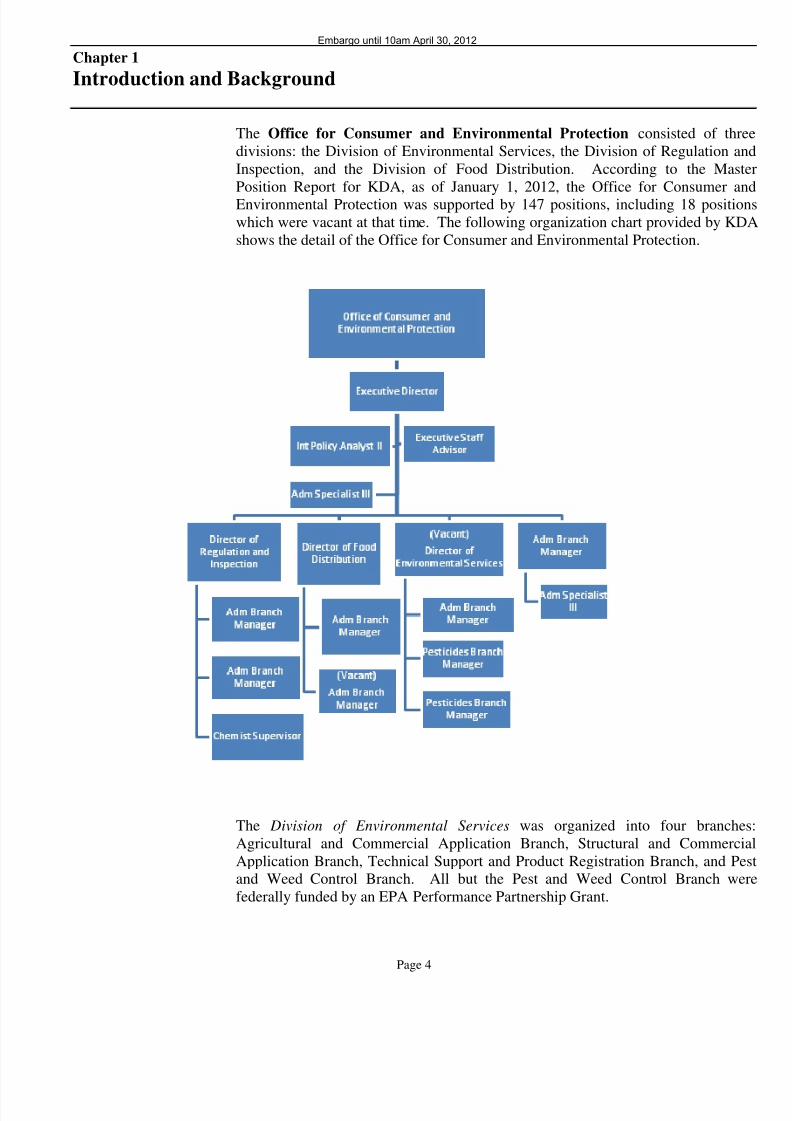

The Office for Consumer and Environmental Protection consisted of thrdivisions: the Division of Environmental Services, the Division of Regulation anInspection, and the Division of Food Distribution. According to the MastPosition Report for KDA, as of January 1, 2012, the Office for Consumer anEnvironmental Protection was supported by 147 positions, including 18 positiowhich were vacant at that time. The following organization chart provided by KDshows the detail of the Office for Consumer and Environmental Protection.

The Division of Environmental Services was organized into four brancheAgricultural and Commercial Application Branch, Structural and CommerciApplication Branch, Technical Support and Product Registration Branch, and Peand Weed Control Branch. All but the Pest and Weed Control Branch wefederally funded by an EPA Performance Partnership Grant.

The Agricultural Branch is funded by the USDA Cooperative Pesticide RecoKeeping Program. Field inspectors from both sides of this branch continuousreview records and inspect facilities of the businesses which sell and/or apppesticides within the state. The inspectors have the authority to impose fines businesses and/or individuals who neglect to follow federal and state lawconcerning the proper storage, containment, sale, distribution, application, recokeeping, or disposal of federally registered pesticides.

The Structural and Commercial Application Branch is responsible for the licensinof pest control companies and individuals applying pesticides on or withinstructure in the state. Structural pesticide inspectors investigate consumcomplaints or situations involving pesticides applied by, or services provided blicensed or unlicensed individuals.

In addition to funds from the USDA Cooperative Pesticide RecordkeepinProgram, the Technical Support and Product Registration Branch is funded by “3Grants.” The purpose of a 319 Grant is to educate those who use pesticiagriculturally of the precautions they need to take to prevent pesticides frocontaminating surface and ground water in order to preserve water quality. Thbranch also reviews the safety and effectiveness of all pesticides allowed to be soand used in Kentucky. The employees also spend a great amount of effort educate the public on Best Management Practices (BMP’s). The Rinse and RetuProgram is actively collecting old pesticide containers for recycling and educatinthe public on proper disposal of containers on the farm. Members of the team aalso called upon in the Collection and Disposal Program to perform the collectioand disposal of potentially hazardous pesticides which have been abandoned b

their owners or are no longer allowed to be used.

The Product Registration Program is responsible for the registration of each anevery pesticide product sold and/or distributed in Kentucky. A $250 fee is assessfor each new pesticide registration (prior to sale or distribution) and the renewal each pesticide registration. Product registrations expire December 31st of evecalendar year.

The Pest and Weed Branch is mandated by Kentucky Revised Statutes to providpest control services to combat major pests in the Commonwealth. The pestargeted by this branch include: mosquitoes, black flies, buffalo gnats, bull a

musk thistles. These pests are not only a terrible nuisance to people and livestocbut also pose a serious health risk with the possibility of spreading diseases, such the West Nile Virus.

The Division of Regulation and Inspection consists of four branchesAdministrative Branch, Amusement Ride Safety Branch, Motor Fuel/PesticiLaboratory Branch, and Weights and Measures Branch – but is responsible ffifteen programs.

The main responsibility of the Administrative Branch is to oversee the fleet vehicles maintained by KDA, as the agency took over its own fleet services frothe Finance and Administration Cabinet (Finance Cabinet) on January 1, 200While KDA employees within this branch do not perform the actual maintenance repair of these vehicles, the employees do oversee the assignment and proper usagof the vehicles, in addition to monitoring the maintenance needs of the vehicles anscheduling service.

The Amusement Rides and Attractions Program provides for the inspection of aamusement rides and attractions to ensure the safety of the equipment. Thincludes, for example, amusement parks, mobile carnivals, go-cart tracks, restauraplay courts, and water parks. Each company/operator must submit an annuapplication and payment for a permit in order to operate their business and compwith state laws.

The Egg Marketing Program provides for the random inspection of eggs at alevels to ensure consumer safety. Under the Kentucky Egg Marketing Law, retail businesses, distributorships, or plants must be licensed to sell shell eggs, egproducts, or specialty egg products within the Commonwealth. Others included asmall producers that sell more than 60 dozen per week or who distribute their eggfor resale. KDA strictly enforces quality, labeling, and refrigeration.

The Retail Gas Dispensers/Meter Inspection Program is responsible for the testinof retail motor fuel dispensers to ensure that the quantity delivered is accurate anthat the total price is computed correctly. Inspectors serve both consumers abusinesses by assuring equity in the marketplace.

The Grain Regulation Program is responsible for administering inspections ensure that producer grain and contractual agreements are secured and stable. Tlicensed grain business’s financial and accounting records are audited to ensure ththe farmers of the Commonwealth are being paid for the grain commoditieAnyone who buys or stores grain from producers is required to be licensed. Tlicensee is required to deduct one-fourth percent (0.0025) of the value of grapurchased from producers. This assessment is paid to the Kentucky GraInsurance Fund, which provides insurance coverage to the participating producein the case of a failure. At present, this fund is above the required $4 million, so tone-fourth percent is not being collected.

The Agricultural Limestone Program provides analysis of agricultural gralimestone. Limestone is used as a neutralizing agent for soil acidity and is tested the later parts of summer and winter so results are available before the spring anfall dustings. Samples are laboratory-tested for particle fineness and their CalciuCarbonate Equivalent. Any owner who conducts a business for the purpose offering or exposing limestone for sale must be licensed with the KDA annually.

The Meter Program inspects meters to ensure accuracy of delivery of product. Ttypes of meters inspected include liquid propane, vehicle tank, terminal, and farmilk tanks.

The Kentucky Metrology Laboratories provide calibration services and technicguidance for private industries, scale and meter repair companies, other staagencies, and weights and measures inspectors within the division. Weighvolumetric test measures and provers, and liquid propane provers are all calibrateby the metrology laboratories. These calibrations check and maintain the accuraof the equipment used to set up, monitor, inspect, and repair all types of scales anmeters throughout the Commonwealth.

The Motor Fuel Quality Testing Laboratory is responsible for the inspection antesting of gasoline, gasoline-alcohol blends, diesel, and biodiesel fuels to ensuthat the quality of the product complies with Kentucky state law and the AmericSociety for Testing and Materials standards and specifications. Kentucky’s MotFuel Quality Law requires that each retail business that sells motor fuel registered. Retail facility owners and operators are required to pay an annual fee $50 for the purpose of funding the program. Inspections are conducted routineacross the state and in response to consumer complaints.

The Retail and Wholesale Package Program uses inspectors to check the net conteof consumer packages based on weight and volume. These inspections are for consumer products with a declaration of weight or volume.

The Scale Program inspects point of sale weighing devices for accuracy. The

include large industrial scales that are used by industry; large vehicle scales founat weigh stations, power plants, coal mines, grain warehouses, and other similbusinesses; and livestock scales used to determine market weights for livestock.

Inspectors from the Scanner Program check retail pricing devices that utilize UPcodes to ensure consumers pay posted prices.