1 Risk Based Pricing in the Credit Card Industry: Evidence from US Survey Data José Liñares-Zegarra a John O. S. Wilson b+ Abstract This paper explores the risk-based pricing strategies of banks issuing credit cards in the United States. We employ a unique database which combines both the risk of cardholders (demand side) and terms and conditions of card cards (supply side) offered in the US. Our results suggest that the annual percentage rates paid per unit of risk decrease, implying that high-risk cardholders pay lower interest rates than their low-risk counterparts. This effect is pronounced for sub-prime cardholders. These findings suggest that the risk-based pricing strategies employed by banks are ineffective in distinguishing between high- and low-risk consumers. The non-price characteristics of credit cards (such as network affiliation, issuer brand and reward program) play an important role in complementing the risk-based strategies. Keywords: Risk-based pricing, credit card plans, demand, supply. JEL Codes: D21, L8 a School of Management, University of St Andrews, The Gateway, North Haugh, St Andrews, Fife, KY16 9AJ, UK. Tel: +44 1334 462800. Email: [email protected]b School of Management, University of St Andrews, The Gateway, North Haugh, St Andrews, Fife, KY16 9AJ, UK. Tel: +44 1334 462803. Email: [email protected]+ Address for correspondence: José Liñares-Zegarra, School of Management, University of St Andrews, The Gateway, North Haugh, St Andrews, Fife KY16 9SS, UK. Tel: +44 1334 462800. Fax: +44 1334 462812. E-mail: [email protected].

Transcript

1

Risk Based Pricing in the Credit Card Industry:

Evidence from US Survey Data

José Liñares-Zegarra a

John O. S. Wilson b+

Abstract

This paper explores the risk-based pricing strategies of banks issuing credit cards

in the United States. We employ a unique database which combines both the risk of

cardholders (demand side) and terms and conditions of card cards (supply side) offered

in the US. Our results suggest that the annual percentage rates paid per unit of risk

decrease, implying that high-risk cardholders pay lower interest rates than their low-risk

counterparts. This effect is pronounced for sub-prime cardholders. These findings

suggest that the risk-based pricing strategies employed by banks are ineffective in

distinguishing between high- and low-risk consumers. The non-price characteristics of

credit cards (such as network affiliation, issuer brand and reward program) play an

important role in complementing the risk-based strategies.

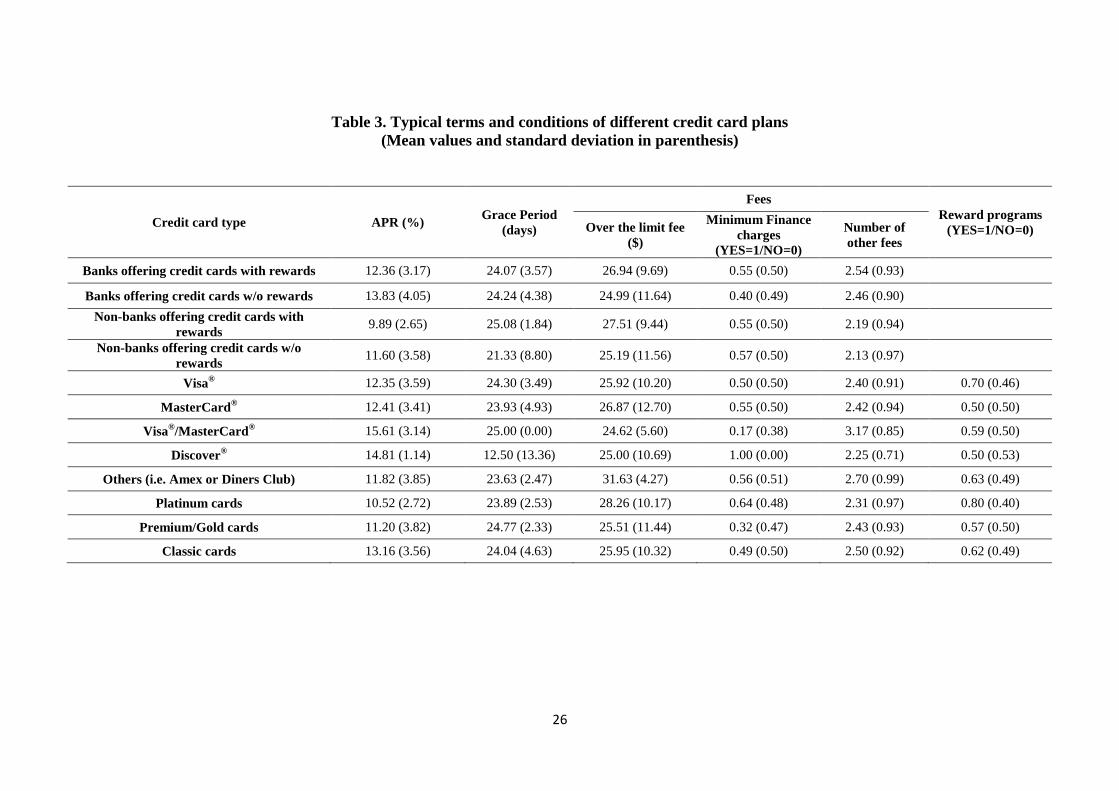

(1) *, **, *** indicate estimates statistically different from zero at the 0.10, 0.05, and 0.01 probability levels. (2) Empty cells occur when a particular variable is not included in a regression. (3)

Standard errors reported in parenthesis, they are robust to general forms of heteroscedasticity. (4) Type I comprises cardholders with both a high outstanding balance and a low FICO Score, Type

II comprises cardholders with a high outstanding balance and Type III comprises cardholders with a low FICO Score. (5) The omitted categories include (a) local banks, (b) other credit card

networks (American Express or Diners Club) and (c) Classic cards.

28

Appendix A. Sample of banks

Type of credit

card plan

Bank Class

(FDIC) Name of the bank

Headquarters’

area

NATIONAL NM 1st Summit Bank Pennsylvania

NATIONAL NM 5Star Bank Colorado

NATIONAL NM Amalgamated Bank of Chicago Illinois

LOCAL N Amegy Bank National Association Texas

NATIONAL SA American Express Bank, FSB. Utah

NATIONAL NM American Express Centurion Bank Utah

LOCAL NM American State Bank Texas

NATIONAL SA Ameriprise Bank, FSB Minnesota

NATIONAL N ANB Financial National Association Arkansas

NATIONAL NM Appalachian Community Bank Georgia

REGIONAL SM Arvest Bank Arkansas

NATIONAL NM Banamex USA California

REGIONAL NM Banamex USA California

REGIONAL SM Banco Popular North America New York

REGIONAL NM BancorpSouth Bank Mississippi

REGIONAL N Bank Midwest, National Association Missouri

NATIONAL NM Bank of Louisiana Louisiana

LOCAL N Banker's Bank of Kansas, National Association Kansas

REGIONAL N Banker's Bank of Kansas, National Association Kansas

REGIONAL NM Banner Bank Washington

LOCAL NM Bar Harbor Bank & Trust Maine

NATIONAL NM Barclays Bank Delaware Delaware

REGIONAL SA BB&T Financial, FSB Georgia

NATIONAL NM BMW Bank of North America Utah

REGIONAL NM Branch Banking and Trust Company North Carolina

NATIONAL N Capital One Bank (USA), National Association Virginia

LOCAL NM Central Bank & Trust Co. Kentucky

REGIONAL SM Centura Card Bank Georgia

NATIONAL N Citibank (South Dakota), N.A. South Dakota

LOCAL NM Citizens First Bank Florida

REGIONAL N City National Bank California

NATIONAL NM CNB Bank Pennsylvania

REGIONAL NM Columbia River Bank Oregon

REGIONAL N Commerce Bank, National Association Pennsylvania

REGIONAL N Commerce Bank, National Association Nebraska

LOCAL SM Community Bank & Trust Company Pennsylvania

LOCAL NM Community First Bank Arkansas

REGIONAL SM Compass Bank Alabama

REGIONAL NM Coppermark Bank Oklahoma

LOCAL NM CoreFirst Bank & Trust Kansas

REGIONAL NM CoreFirst Bank & Trust Kansas

NATIONAL N Credit One Bank, National Association Nevada

NATIONAL N Chase Bank USA, National Association Delaware

LOCAL SM Chemung Canal Trust Company New York

29

NATIONAL NM D. L. Evans Bank Idaho

REGIONAL N Delaware National Bank Delaware

NATIONAL NM Discover Bank Delaware

REGIONAL SA Dollar Bank, Federal Savings Bank Pennsylvania

LOCAL SA Fairfield Federal Savings and Loan Association of

Lancaster Ohio

LOCAL NM Farmers State Bank Iowa

NATIONAL N FIA Card Services, National Association Delaware

REGIONAL SM Fifth Third Bank Ohio

LOCAL NM First Bank & Trust East Texas Texas

REGIONAL NM First Citizens Bank and Trust Company, Inc. South Carolina

NATIONAL SA First Command Bank Texas

LOCAL NM First Commercial Bank Alabama

NATIONAL SM First Community Bank New Mexico

LOCAL SB First County Bank Connecticut

NATIONAL SA First Federal Savings and Loan Association of

Charleston South Carolina

REGIONAL N First Financial Bank, National Association Ohio

REGIONAL N First Financial Bank, National Association Indiana

REGIONAL SM First Interstate Bank Montana

NATIONAL N First National Bank South Dakota

LOCAL N First National Bank Texas

LOCAL N First National Bank Alaska Alaska

NATIONAL N First National Bank of Omaha Nebraska

REGIONAL N First National Bank of St. Louis Missouri

NATIONAL N First National Bank of the Mid-Cities Texas

LOCAL NM First Security Bank Arkansas

LOCAL NM First State Bank New Mexico

REGIONAL N First Tennessee Bank, National Association Tennessee

REGIONAL SM FirstBank Colorado

REGIONAL NM First-Citizens Bank & Trust Company North Carolina

LOCAL N First-Knox National Bank Ohio

REGIONAL N Firstmerit Bank, National Association Ohio

LOCAL N FNB Bank, National Association Pennsylvania

LOCAL NM FNBT.COM BANK Florida

NATIONAL SA Franklin Templeton Bank and Trust, F.S.B. Utah

NATIONAL SA GE Money Bank Utah

LOCAL N Greenville National Bank Ohio

LOCAL NM Hawthorn Bank Missouri

LOCAL SM Heartland Bank Ohio

LOCAL NM Hills Bank and Trust Company Iowa

LOCAL SA Home Federal Bank of Tennessee Tennessee

NATIONAL SM HSBC Bank USA New York

LOCAL NM Huntington State Bank Texas

NATIONAL NM Idaho Independent Bank Idaho

NATIONAL N InfiBank, National Association Nebraska

NATIONAL N Intrust Bank, National Association Kansas

REGIONAL SA IronStone Bank Florida

NATIONAL SM Johnson Bank Wisconsin

LOCAL NM Kentucky Bank Kentucky

30

LOCAL SM Lafayette Ambassador Bank Pennsylvania

NATIONAL NM Liberty Bank and Trust Company Louisiana

NATIONAL N Los Alamos National Bank New Mexico

REGIONAL SA M & I Bank FSB Nevada

LOCAL N MERCANTIL COMMERCEBANK, NATIONAL

ASSOCIATION Florida

LOCAL SA Mercer Savings Bank Ohio

NATIONAL NM Merrick Bank Utah

REGIONAL SA MFB Financial (The "Savings Bank") Indiana

NATIONAL SM Morton Community Bank Illinois

REGIONAL N National City Bank Ohio

NATIONAL SA Nationwide Bank Ohio

NATIONAL NM New Millennium Bank New Jersey

LOCAL NM NewBridge Bank North Carolina

LOCAL N Newfield National Bank New Jersey

NATIONAL SA Nordstrom fsb Arizona

REGIONAL SB Northwest Savings Bank Pennsylvania

NATIONAL NM Oak Hill Banks Ohio

LOCAL NM Palos Bank and Trust Company Illinois

NATIONAL NM Penn Security Bank and Trust Company Pennsylvania

LOCAL SA Peoples First Community Bank Florida

REGIONAL NM Pinnacle Bank Nebraska

REGIONAL NM Plains Commerce Bank South Dakota

NATIONAL SA Pocahontas Federal Savings and Loan Association Arkansas

REGIONAL SM Quad City Bank and Trust Company Illinois

NATIONAL SB Rainier Pacific Bank Washington

REGIONAL SM RBC Bank (USA) North Carolina

NATIONAL N RBS Citizens, National Association Rhode Island

LOCAL NM Republic Bank & Trust Company Kentucky

LOCAL NM S&T Bank Pennsylvania

NATIONAL N Silverton Bank, National Association Georgia

NATIONAL N Simmons First National Bank Arkansas

LOCAL SM Solvay Bank New York

LOCAL NM State Bank of Cross Plains Wisconsin

NATIONAL SA State Farm Bank, F.S.B. Illinois

NATIONAL N Sunflower Bank, National Association Kansas

REGIONAL SM SunTrust Bank Georgia

NATIONAL NM Synovus Bank Georgia

NATIONAL N TCM Bank, National Association Florida

NATIONAL N TD Bank, National Association Delaware

LOCAL NM Texas Bank and Trust Company Texas

LOCAL SM The Adirondack Trust Company New York

LOCAL NM The Bank New Jersey

LOCAL SB The Bank of Canton Massachusetts

REGIONAL NM The Bank of Kentucky, Inc. Kentucky

LOCAL SA The Bank of Maine Maine

REGIONAL N The Boone County National Bank of Columbia Missouri

REGIONAL NM The Central Trust Bank Missouri

LOCAL N The City National Bank of Taylor Texas

31

LOCAL NM The Delaware County Bank and Trust Company Ohio

NATIONAL NM The Farmers & Merchants State Bank Ohio

REGIONAL NM The Fidelity Bank North Carolina

LOCAL N The First National Bank of Fairfield Montana

NATIONAL N The First National Bank of Ipswich Massachusetts

LOCAL N The First National Bank of Litchfield Connecticut

NATIONAL N The National Bank of Blacksburg Virginia

LOCAL N The National Grand Bank of Marblehead Massachusetts

REGIONAL SM The North Side Bank and Trust Company Ohio

REGIONAL NM The Ohio Valley Bank Company Ohio

LOCAL NM The Park Bank Wisconsin

LOCAL N The Park National Bank Ohio

NATIONAL N The Randolph National Bank Vermont

LOCAL NM The Richland Trust Company Ohio

REGIONAL N The Rockport National Bank Massachusetts

LOCAL N The Security National Bank and Trust Co. Ohio

LOCAL N The Vinton County National Bank of McArthur Ohio

NATIONAL SM TIB The Independent Bankersbank Texas

NATIONAL N Town North Bank Nevada, National Association Nevada

NATIONAL NM Toyota Financial Savings Bank Nevada

REGIONAL N Trustmark National Bank Mississippi

REGIONAL N U.S. Bank National Association ND North Dakota

NATIONAL N UMB Bank, National Association Missouri

REGIONAL NM Union Bank and Trust Company Nebraska

REGIONAL SM United Bank West Virginia

LOCAL N Univest National Bank and Trust Co. Pennsylvania

NATIONAL NM USAA Savings Bank Nevada

NATIONAL N Wachovia Bank, National Association North Carolina

LOCAL NM Wallis State Bank Texas

NATIONAL SA Washington Mutual Bank California

NATIONAL SM Wayne Bank and Trust Co. Indiana

NATIONAL N Wells Fargo Bank, National Association South Dakota

REGIONAL NM Wells Fargo Financial Bank South Dakota

NATIONAL N Wells Fargo Financial National Bank Nevada

LOCAL NM West Suburban Bank Illinois

REGIONAL N Whitney National Bank Louisiana

NATIONAL SM Wilmington Trust Company Delaware

NATIONAL N World Financial Network National Bank Delaware

NATIONAL NM World's Foremost Bank Nebraska

NATIONAL NM York State Bank Nebraska

REGIONAL N Zions First National Bank Utah

Note:

Commercial Banks include: SM = commercial bank, state charter and Fed member, supervised by the Federal

Reserve (FRB), NM = commercial bank, state charter and Fed non-member, supervised by the FDIC and N =

commercial bank, national (federal) charter and Fed member, supervised by the Office of the Comptroller of

the Currency (OCC). Non-commercial banks include the following codes: SA = savings associations, state or

federal charter, supervised by the Office of Thrift Supervision (OTS) and SB = savings banks, state charter,

supervised by the FDIC.

32

Appendix B: Methodology used to build the demand and supply variables

In this Appendix, we discuss the various data sources used to build both demand

(cardholder‟s sources of risk) and supply (credit card terms and conditions) variables

needed to carry out our empirical estimations. We also explain the methodology used to

match each bank‟s credit card plan (supply side) with the risk profile of the cardholders

located in the markets where the credit cards are offered (demand side).

Supply side variables

For data related to supply of credit cards, we use the twice yearly Terms of

Credit Card Plans (TCCP) Survey undertaken by the U.S. Federal Reserve Bank. Since

demand data is only available for 2008 and 2009, we limit our sample to these years.

Each bank surveyed reports specific details of its most popular credit card plans.29

Appendix A provides a list of the banks surveyed. Credit cards vary across providers

(banks and non-banks), reward enhancements (reward and non-reward cards) and

location (US States). For each bank in the TCCP, we know specifically which of the

various U.S. states where the credit card plan is advertised and issued for each bank.

Credit card plans in our database can be issued on a nationwide (all 50 states and the

District of Columbia), regional (more than one state), or state-specific basis. Each

category is mutually exclusive; so each bank matches with only one category. In order

to guarantee that each bank is associated with a unique card plan, we follow the next

criteria: if the card plan is offered nationally, but with different terms in a few states, we

only consider the „most common terms‟ reported by the bank; if identical terms are

offered regionally, we take average values across all states in which the plan is

29

This refers to the plans that have the largest number of cards outstanding and that was available to new

cardholders as of the report date.

33

marketed while if the card is regional but with different terms in a few states, we

consider the „most common terms‟ reported by the bank. Finally, if the plan is offered

only in one state, we consider the terms applied by the bank in the specific state.30

Demand side variables

We use both the 2008 and 2009 Survey of Consumer Payment Choice (SCPC) as

a primary data source of our demand side variables. The SCPC is a nationally

representative survey data on consumer payment choices in the U.S. (Foster et al.,

2011). It is conducted online to a random sample of more than 2.000 consumers by the

RAND Corporation as a module of the American Life Panel (ALP). The survey

contains detailed information about the state of residence of credit cardholders and risk

measures such as outstanding card debt, unpaid debt information, FICO score along

with the primary financial institution of the cardholders (bank or non-bank institutions)

and information on reward programs linked to the cardholder‟s credit card. We employ

this data to compute state-level average level of risk of credit cardholders according to

the next criteria: if a cardholder has or does not have a reward programs associated to

their credit cards along with if the cardholder has or does not have a commercial bank as

her primary financial institution. 31

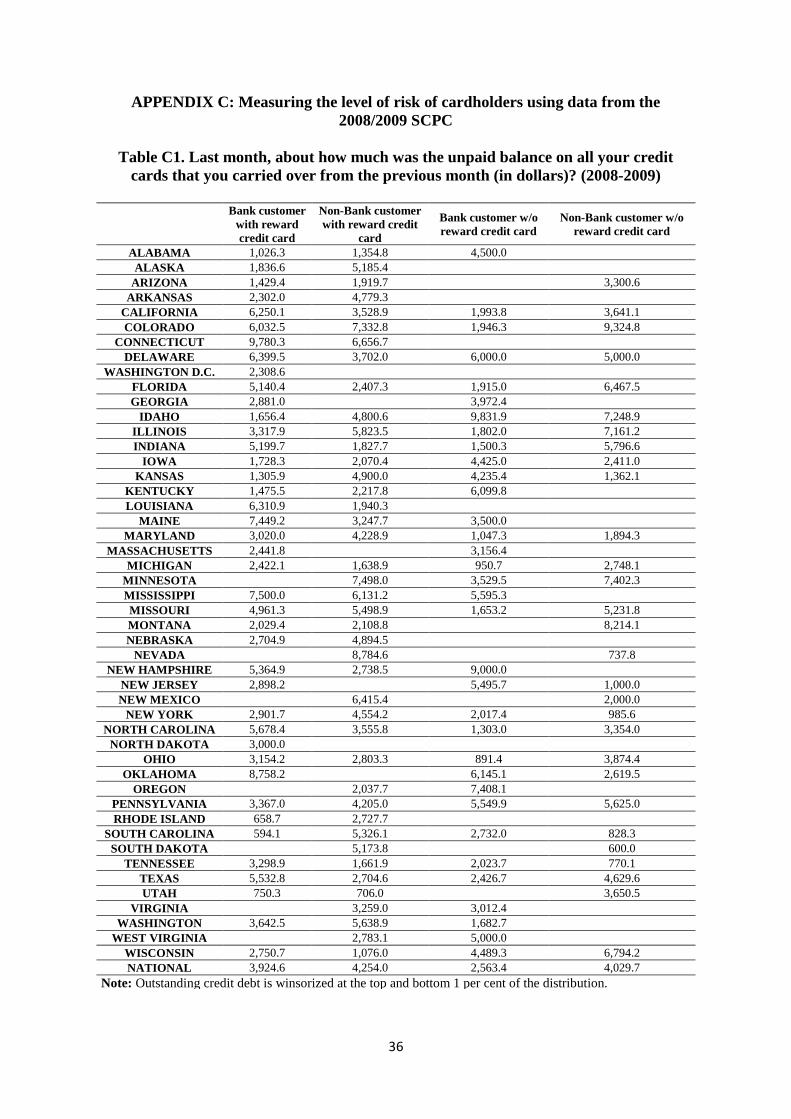

Tables C1 to C3 show the average values (2008-2009) across U.S. states of the

main financial characteristics considered in our study.32

All data are weighted to match

national population estimates from the Census Bureau‟s Current Population Survey.

Table C1 shows a considerable state-level variation in the unpaid debt of credit

30

We weight continuous variables by the branches of the bank in these states. 31

It should be noted that we restrict our analysis to consumers whom have adopted a credit card(s) and

have a positive outstanding balance in their card (revolving cardholders) since it is expected that they are

more responsive to changes in credit card plans. Because the interest rate is only relevant to those who

borrow on their credit card, respondents were filtered to include only credit card users who carry a

balance. 32

Missing values in Tables 1 to 4 are due to there is no state-level available data for cardholders who

meet these criteria in both the 2008 and 2009 SCPC.

34

cardholders. The credit card debt of bank cardholders is much lower than non-bank

cardholders. Unpaid debt is higher for reward receivers than non-reward receivers.

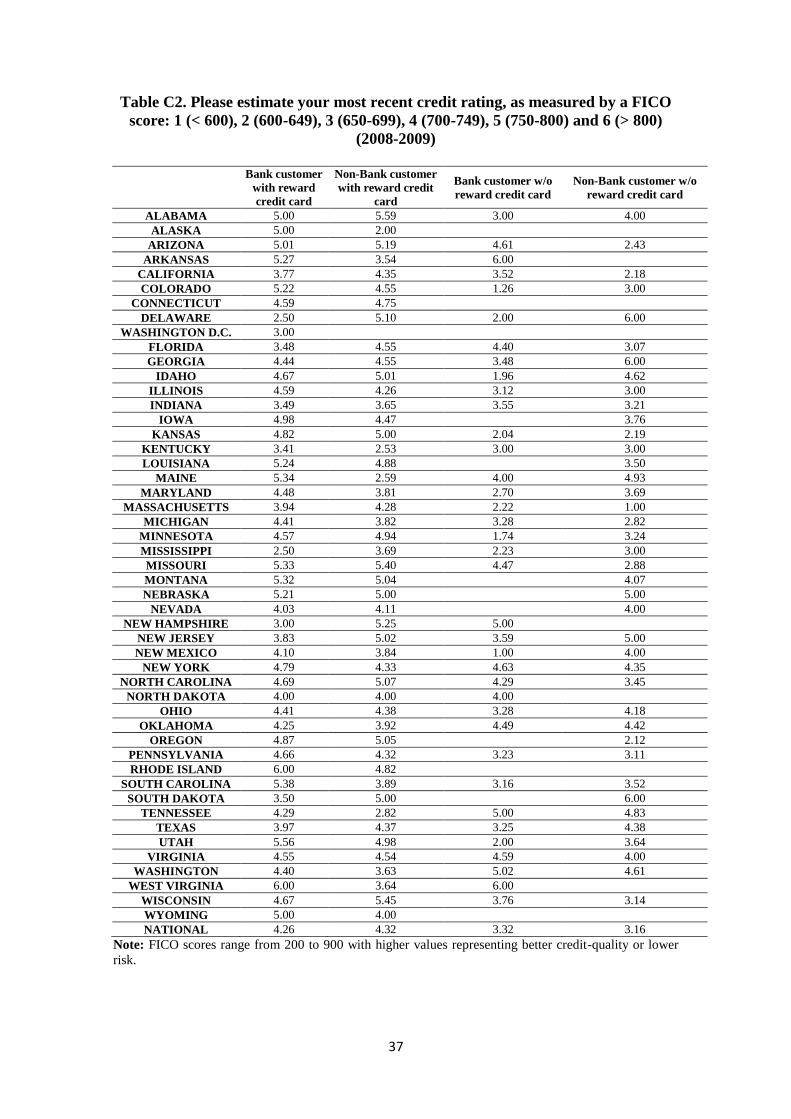

Table C2 completes this picture and provides self-reported FICO scores, ranging from 1

(<600 points) to 5 (>800 points), of the cardholders surveyed. There is substantial

variation in FICO scores across states and between consumers holding cards with

associated reward programs. Table C3 shows that, on average, the U.S. cardholders

have carried an unpaid balance on any credit card from one month to the next during the

previous 12 months. More precisely, the last row of Table C3 (national weighted

average) shows that more than 50 per cent of the cardholders in our sample have carried

an unpaid balance on any credit card from one month to the next during the previous 12

months.

Matching demand, supply and market variables

As shown in Section 3, our database contains both demand and supply side

information for the period 2008 to 2009. From the demand side, we can observe if the

cardholder is or is not a client of a commercial bank and has or does not have reward

programs associated with their credit cards. From the supply side, we can observe

whether each credit card plan is or is not marketed by a commercial bank, and if the

plan offers or does not offer reward programs. By using this information, we are able to

match each bank‟s credit card plan with the level of risk of their most likely credit

cardholder living in the regions where each bank offers its card plans. Nationally

marketed credit cards plans have been matched with national average values of the

cardholder‟s level of risk extracted from the 2008/2009 SCPC (see Tables C1-C3).

Regional card plans are matched with the weighted average value of the cardholder‟s

level of risk in the regions where the bank operates while if the card plan is offered in

35

only a single US state, we impute the cardholder‟s level of risk in this particular US

state to the card plan marketed in the same US state. 33

33

Our weighted factor is the population of the states where each credit card is offered.

36

APPENDIX C: Measuring the level of risk of cardholders using data from the

2008/2009 SCPC

Table C1. Last month, about how much was the unpaid balance on all your credit

cards that you carried over from the previous month (in dollars)? (2008-2009)

Bank customer

with reward

credit card

Non-Bank customer

with reward credit

card

Bank customer w/o

reward credit card

Non-Bank customer w/o

reward credit card

ALABAMA 1,026.3 1,354.8 4,500.0

ALASKA 1,836.6 5,185.4

ARIZONA 1,429.4 1,919.7 3,300.6

ARKANSAS 2,302.0 4,779.3

CALIFORNIA 6,250.1 3,528.9 1,993.8 3,641.1

COLORADO 6,032.5 7,332.8 1,946.3 9,324.8

CONNECTICUT 9,780.3 6,656.7

DELAWARE 6,399.5 3,702.0 6,000.0 5,000.0

WASHINGTON D.C. 2,308.6

FLORIDA 5,140.4 2,407.3 1,915.0 6,467.5

GEORGIA 2,881.0 3,972.4

IDAHO 1,656.4 4,800.6 9,831.9 7,248.9

ILLINOIS 3,317.9 5,823.5 1,802.0 7,161.2

INDIANA 5,199.7 1,827.7 1,500.3 5,796.6

IOWA 1,728.3 2,070.4 4,425.0 2,411.0

KANSAS 1,305.9 4,900.0 4,235.4 1,362.1

KENTUCKY 1,475.5 2,217.8 6,099.8

LOUISIANA 6,310.9 1,940.3

MAINE 7,449.2 3,247.7 3,500.0

MARYLAND 3,020.0 4,228.9 1,047.3 1,894.3

MASSACHUSETTS 2,441.8 3,156.4

MICHIGAN 2,422.1 1,638.9 950.7 2,748.1

MINNESOTA 7,498.0 3,529.5 7,402.3

MISSISSIPPI 7,500.0 6,131.2 5,595.3

MISSOURI 4,961.3 5,498.9 1,653.2 5,231.8

MONTANA 2,029.4 2,108.8 8,214.1

NEBRASKA 2,704.9 4,894.5

NEVADA 8,784.6 737.8

NEW HAMPSHIRE 5,364.9 2,738.5 9,000.0

NEW JERSEY 2,898.2 5,495.7 1,000.0

NEW MEXICO 6,415.4 2,000.0

NEW YORK 2,901.7 4,554.2 2,017.4 985.6

NORTH CAROLINA 5,678.4 3,555.8 1,303.0 3,354.0

NORTH DAKOTA 3,000.0

OHIO 3,154.2 2,803.3 891.4 3,874.4

OKLAHOMA 8,758.2 6,145.1 2,619.5

OREGON 2,037.7 7,408.1

PENNSYLVANIA 3,367.0 4,205.0 5,549.9 5,625.0

RHODE ISLAND 658.7 2,727.7

SOUTH CAROLINA 594.1 5,326.1 2,732.0 828.3

SOUTH DAKOTA 5,173.8 600.0

TENNESSEE 3,298.9 1,661.9 2,023.7 770.1

TEXAS 5,532.8 2,704.6 2,426.7 4,629.6

UTAH 750.3 706.0 3,650.5

VIRGINIA 3,259.0 3,012.4

WASHINGTON 3,642.5 5,638.9 1,682.7

WEST VIRGINIA 2,783.1 5,000.0

WISCONSIN 2,750.7 1,076.0 4,489.3 6,794.2

NATIONAL 3,924.6 4,254.0 2,563.4 4,029.7

Note: Outstanding credit debt is winsorized at the top and bottom 1 per cent of the distribution.

37

Table C2. Please estimate your most recent credit rating, as measured by a FICO