24

Risk Evaluation for Investment Decisions by NHS Foundation Trusts

Risk Evaluation for Investment Decisions by NHS Foundation Trusts

Risk Evaluation for InvestmentDecisions by NHS Foundation Trusts

01

Contents

02 A. Context 04 B. Scope of this document05 C. Best practice principles in making investments06 D. Key elements of investment policy10 E. Monitor’s role in NHS foundation trust investments

12 Appendix 1:12 Appendix 1:12 Framework for evaluating, executing and monitoring proposed major investments

16 Appendix 2: Due diligence check list

17 Appendix 3:17 Appendix 3:17 Provisions of the Health and Social Care (Community Health and Standards) Act 2003 relevant to NHS foundation trust investments

Risk Evaluation for InvestmentDecisions by NHS Foundation Trusts

A. Context

NHS foundation trusts were created as new legal entities in the form of public benefi t corporations by the Health and Social Care (Community Health and Standards) Act 2003 (“the Act”). The legislation gave NHS foundation trusts new freedoms, with trust boards having more autonomy to make fi nancial and strategic decisions. In this new regime, NHS foundation trust boards are ultimately and collectively responsible for the fi nancial performance and quality of healthcare delivery of their foundation trust.

One new freedom, which fundamentally distinguishes NHS foundation trusts from NHS trusts, is the freedom to invest money for the purposes of, or in connection with, their functions. This freedom is widely drawn and needs to be exercised in keeping with the provisions of the Act and the NHS foundation trust’s terms of authorisation.

Accordingly, this document sets out governance processes for all major investments undertaken by NHS foundation trusts including those under sections 17 and 27 of the Act. Relevant sections of the Act are set out in Appendix 3 of this document.

Investments under section 17 of the Act are new endeavours for many NHS foundation trust boards and senior management teams. Experience from other countries and industries shows that entities with the freedom to invest often initially encounter common pitfalls, such as:

■ making investments which are inconsistent with the overall corporate strategy;■ forming partnerships that offer prospects of attractive returns, but have signifi cant

risk (strategic, reputational, operational or fi nancial). Unless the risks are properly evaluated and risk management arrangements are put in place, such partnerships can destabilise the organisation;

■ undertaking acquisitions that destroy value: studies show that over 50% of private sector mergers and acquisitions fail1;

■ entering into deals involving brand licensing, which may appear to carry limited fi nancial risk, but may expose the organisation to reputational damage, with potentially severe long-term fi nancial consequences;

■ making investments with funds derived from cross-subsidies that mask underlying fi nancial weaknesses; and

■ entering into transactions that appear low-risk, but create contingent liabilities, for instance, guaranteeing the debt of joint ventures.

1 Based on studies by Ernst & Young (1999), Mitchell (1996), Coopers & Lybrand (1996), McKinsey & Company (2000), A.T. Kearney (1998), and Mercer (1996). Defi nitions of failure vary from no net growth to inferior stock performance relative to industry

Given these risks, it is Monitor’s view that NHS foundation trusts should proceed cautiously when considering investments, particularly high risk investments outside the core competency of the institution, that is, outside healthcare in England. Over time, as NHS foundation trusts gain experience with such transactions, they are likely to develop a greater level of capability and capacity to evaluate them.

This document is issued as best practice advice to help NHS foundation trust boards responsibly use their freedom to invest. It is not mandatory guidance and does not seek to prescribe a specifi c approach to making investments. Instead it describes best practice governance and decision making processes for making investments (Section C, Section D, Appendices 1 and 2).

However, Monitor does have mandatory reporting requirements around NHS foundation trust investments. These requirements are set out in the Compliance Framework2 and are referred to in Section E of this document, for ease of reference.

NHS foundation trusts are strongly encouraged to take account of the best practice process described in this document, in conjunction with independent professional advice where appropriate.

Following the best practice described in this document can be expected to reduce the probability of imprudent or inappropriate investments. However, following this best practice advice cannot be construed as a guarantee for successful investments. Investment risk remains solely with NHS foundation trusts.

02 – 03

2 Monitor’s Compliance Framework was issued on 31 March 2005 and sets out the framework for monitoring compliance by Compliance Framework was issued on 31 March 2005 and sets out the framework for monitoring compliance by Compliance FrameworkNHS foundation trusts with the terms of authorisation and for intervening in the event of failure to comply

Risk Evaluation for InvestmentDecisions by NHS Foundation Trusts

B. Scope of this document

Risk Evaluation for Investment Decisions by NHS Foundation Trusts is aimed at all ‘high risk’ investments.

High risk investments are defi ned as:

■ Reportable transactions: All investments that are reportable to Monitor under the thresholds for reporting investments in the Compliance Framework.

■ Other transactions: All investments that may have any one or more of the following characteristics:

■ an equity component, which is defi ned as any participation involving shares and securities, debt instruments convertible into equity, options conferring the right to acquire equity in the future, royalties, participation in the profi ts of the enterprise, and all types of mezzanine fi nance3 where the returns exceed normal secured debt returns;

■ signifi cant reputational risk; ■ the potential to destabilise the core business; or ■ the creation of material contingent liabilities.

The types of transactions covered by this guidance include signifi cant capital expenditure, acquisitions, joint ventures, equity stakes, major property transactions, mergers and alliances (eg formal or informal agreements to work with other institutions), irrespective of how they are fi nanced. The fi nancing of such transactions could be through retained surpluses, equity, debt, sale and leaseback transactions, private fi nance initiative (PFI) and other fi nancially engineered transactions.

This document focuses on medium to long-term investments and does not apply to investment of surplus operating cash, that is, surplus cash likely to be needed within 12 months to support ongoing operations. Such investments are covered in Managing Operating Cash in NHS Foundation Trusts 4.

This document applies only to funds under the direct control of NHS foundation trusts. It does not apply to pensions, associated charities, or other funds connected with an NHS foundation trust.

Monitor’s approach to reportable investments is set out in Section E of this document, while its proposed framework for reviewing mergers under section 27 of the Act is set out in the consultation document, Merger Guide for Applicants5.

3 Mezzanine fi nance is used to describe a form of fi nance which has characteristics that place it between debt and equity (ordinary shares). It is typically used to fi nance management buyouts or expansion

4 Best practice advice issued by Monitor in December 20055 Monitor’s consultation document, dated October 2005, on applying for a merger involving an NHS foundation trust. This consultation has now closed

04 – 05

C. Best practice principles in making investments

Set out below are the key principles which Monitor regards as best practice for NHS foundation trusts proposing to make investments that fall within the scope of this paper.

1. Development of a written investment policy, which is reviewed by independent professional advisers (including legal experts as required), approved by the board, and reviewed annually.

2. Ensuring that the written investment policy addresses the following issues (discussed further in Section D):

■ investment committee functions and structure;■ investment philosophy and objectives;■ attitude to risk and process for managing risk; ■ decision rights; and■ process for evaluating and managing investments.

3. Establishment of an investment committee if major investment is being proposed. Key roles of the investment committee would be to:

■ establish the overall methodology, processes and controls which govern investments;

■ ensure that robust processes (eg evaluation of fi t with the NHS foundation trust’s overall strategy, use of appropriate independent professional advisers) are followed; and

■ evaluate, scrutinise and monitor investments.

4. Confi rmation that the NHS foundation trust has the legal power to make the proposed investment.

5. Engagement early on in the investment evaluation process of independent external advisers with demonstrated expertise in advising on transactions of the size and nature being proposed.

6. Rigorous evaluation of all proposed major investments using a thorough evaluation, execution, and monitoring process, such as the one described in Appendix 1.

Risk Evaluation for InvestmentDecisions by NHS Foundation Trusts

D. Key elements of investment policy

A best practice investment policy will contain the following elements:

(i) Investment committee functions and structureTypically the functions of the investment committee will be to approve investment and borrowing strategy and policies, approve performance benchmarks, review performance against the benchmarks, ensure proper safeguards are in place for security of the NHS foundation trust’s funds, monitor compliance with treasury policies and procedures, approve proposals for acquisition and disposal of assets above a de minimis amount and approve external funding arrangements within their delegated authority.

The investment committee will comprise executive and non-executive directors, with a majority of non-executive directors. It should be chaired by a non-executive director with relevant investment decision-making experience. It may be a committee of the board, or the board itself in the case of smaller NHS foundation trusts.

(ii) Investment philosophy and objectivesA best practice statement of investment philosophy and objectives will provide the criteria for selecting the NHS foundation trust’s investments, and address the following:

1. the statutory and principal purpose of the NHS foundation trust – the provision of goods and services for the health service in England;

2. the NHS foundation trust’s corporate strategy (including geographic and service focus);

3. target rates of return for investments and explanation of how rates of return will be calculated (eg return net of any cross-subsidies); and

4. time frame for realising the desired return on investments.

06 – 07

(iii) Attitude to risk and process for managing riskRisk refers to the probability of an adverse outcome that is different from the expected outcome and the potential impact of such an outcome. Some major categories of investment risk include:

1. Strategic: risks associated with a particular strategy, for instance, overcapacity, product or service line obsolescence, competitor reactions;

2. Financial: risks associated with the fi nancial structure of a business, the fi nancial transactions made by the business, and the fi nancial systems which are in place, for instance, interest rate risk, foreign exchange risk and credit risk;

3. Operational: risks associated with the operational and administrative procedures of a business, such as, clinical operations, supply chain management, IT systems, recruitment, labour management and post-merger integration process;

4. Regulatory and political: risks posed by potential changes in the regulatory and political environment, such as, tariff changes, policy changes and changes in healthcare targets;

5. Reputational: risks to the perceived quality or brand of an institution, for instance, through bad press resulting from association with a failed joint venture;

6. Contingent: risks that will only come into existence if a certain contingent event takes place, for instance, guarantees of a joint venture that are only payable if it defaults.

Risk management refers to the collective set of processes, working practices and tools used to minimise the probability and impact of adverse outcomes. It entails:

■ identifying potential sources of risk;■ estimating value at risk, calculated as probability of loss x severity of loss; ■ implementing controls to minimise probability and severity of loss.

It is best practice to defi ne in the investment policy the NHS foundation trust’s principles for managing risk aligned with its corporate strategy. Examples of risk management principles include:

■ guidelines on identifi cation of different types of risk;■ methodology for calculating value at risk; ■ expected returns of individual investments for a given risk level – higher risk

investments require higher expected returns;■ aggregate targeted rate of return across the portfolio of investments;■ limitations on the locations and types of investments that can be pursued. For instance,

the policy may specify that investments in overseas ventures should only be within the ‘core competence’ of the organisation and within stated risk concentrations for each geography;

■ guidelines for asset diversifi cation outside core operations. For instance, specifying that either the organisation will not diversify outside the health sector in England, or specifying limits on concentration of risk in a particular technology or sector.

A best practice investment policy will provide the criteria for categorising investments by level of risk (eg high, medium and low risk). Criteria for assessing riskiness of an investment include:

■ fi nancial magnitude of deal;■ probability of loss;■ complexity of the deal structure;■ distance from an NHS foundation trust’s core capabilities and operations;■ fi nancing arrangements, for instance, type of debt fi nance;■ geographic location, for instance, investment in a highly competitive, uncertain,

or unfamiliar territory will increase risk;■ degree of operating risk assumed, be it construction risk or cost overrun risk,

for example; ■ level of post-investment management required (eg post acquisition integration).

Best practice is to scrutinise investments in proportion to risk. For example, an NHS foundation trust board may accept ‘routine scrutiny’ for low-risk investments (eg decisions delegated to the investment committee, with a short-form business case), but require ‘special scrutiny’ for high-risk investments (eg engagement of external independent advisers for in-depth business case, and main board approval).

While it is for NHS foundation trusts to determine their own thresholds for each level of risk and associated scrutiny, the approach used by Monitor for its own risk assessment may provide a useful reference point (see Section E).

It is best practice for NHS foundation trusts to seek advice from appropriate independent external advisers (eg risk management consultants) when developing their approach to managing risk.

Risk Evaluation for InvestmentDecisions by NHS Foundation Trusts

(iv) Decision rightsA best practice investment policy will defi ne clearly the roles, responsibilities and approval limits of the various committees and individuals with investment oversight. These are likely to include the board, investment committee, fi nance director, and business development group, if one exists. For example, the board might be required to approve the written investment policy and all ‘high risk’ investments, while the investment committee might approve all other investments and ensure that investment decisions follow the guidelines laid out in the written investment policy.

(v) Process for evaluating and managing investmentsA robust investment policy will explain the internal processes for evaluating, executing, and performance managing investments. The extent of review/due diligence needs to be appropriate to the investment proposed. For example, all major investments would be expected to undergo detailed business case evaluation and challenge.

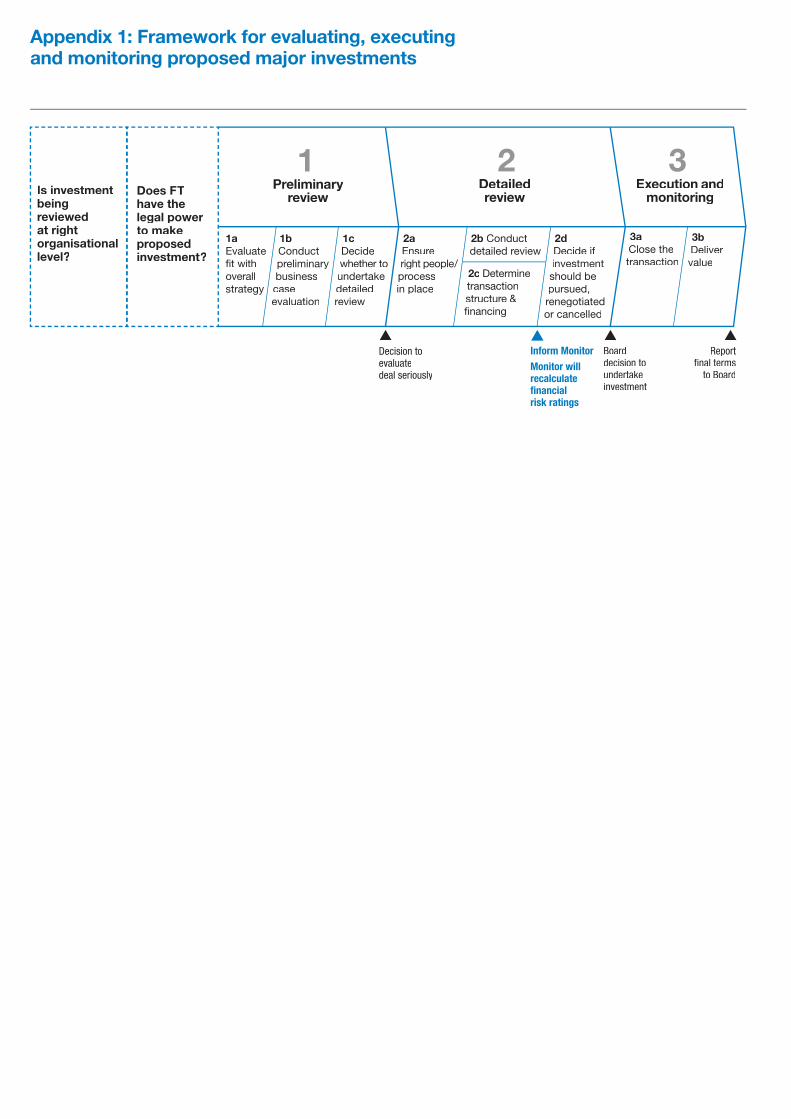

An example of a robust framework for evaluating and managing investments is set out in Appendix 1. This framework describes the key phases in making a major investment decision: preliminary review, detailed review, and execution and monitoring. For each of these phases it provides a list of key questions that board members will ask and also lists the types of external advisers that will likely be engaged.

This risk evaluation framework is an indication of the type of analysis required at each of the three stages of investment appraisal. If an NHS foundation trust is unclear about how to apply the framework to a particular investment appraisal they should seek professional advice.

08 – 09

E. Monitor’s role in NHS foundation trust investments

The Compliance Framework describes Monitor’s mandatory reporting Compliance Framework describes Monitor’s mandatory reporting Compliance Frameworkrequirements and role in NHS foundation trust investments.

Section 2.1.3 (paragraph 60) of the Compliance Framework provides the following guidance:

“ Monitor requires NHS foundation trusts to report any proposed major investments that could affect their fi nancial risk rating, as part of the annual planning process or in-year, prior to fi nancial closure. Monitor does not have any role in approving such plans but it will consider their impact on the NHS foundation trust’s fi nancial risk rating. The Board of Directors of an NHS foundation trust will need to determine when such an investment should be reported to Monitor. [The diagram below provides the detail on reporting thresholds.]”

Risk Evaluation for InvestmentDecisions by NHS Foundation Trusts

Thresholds for reporting investments to Monitor

If a transaction meets any one of these criteria, then the NHS foundation trust should report this transaction to Monitor

Reporting requirements

Non healthcare/Category Ratio Description international UK healthcare

Assets The gross assets* subject to the > 5% > 10% transaction divided by the gross assets of the NHS FT

Profi ts I The EBITDA attributable to the > 12.5% > 25% assets subject to the transactionSize assets subject to the transactionSize assets subject to the transaction

divided by the EBITDA of the NHS FT

Income The income attributable to the assets > 7.5% > 15% subject to the transaction divided by the income of the NHS FT

Consideration The gross capital† of the company > 5% > 10% to total NHS or business being acquired divided

FT capital by the total capital of the NHS FT

Profi tability Profi ts II The EBITDA margin attributable to Dilutive‡ Dilutive‡

the assets subject to the transaction

* Gross assets is the total of fi xed assets and current assets† Gross capital equals the market value of the target’s shares and debt securities, plus all other liabilities, plus the excess of current liabilities over current assets‡ Lower EBITDA margin than the NHS FT has reported in the last audited fi nancial year

{

NHS foundation trusts should inform Monitor about proposed major investments once they have completed the detailed review and before fi nalising the deal (see Appendix 1, which lays out a best practice framework for investment evaluation, execution and monitoring). However, when contemplating major investments, NHS foundation trusts may wish to inform Monitor before proceeding with the detailed review.

Monitor’s level of scrutiny towards NHS foundation trust investments will be in proportion to perceived risk. In general, the larger the investment, and the more the investment is outside an NHS foundation trust’s natural core competence ofhealthcare in England, the more risk will be associated with it.

Based on the data provided by the NHS foundation trust, Monitor will assess the impact of the proposed investment on the NHS foundation trust’s fi nancial risk rating. Given that the risk rating determines the NHS foundation trust’s borrowing power and might require renegotiation of deal terms, NHS foundation trusts should not commit to any proposed major investment until Monitor has provided the expected post-deal risk rating.

10 – 11

Appendix 1: Framework for evaluating, executing and monitoring proposed major investments

Is investment being reviewed at right organisational level?

Does FT have the legal power to make proposed investment?

Preliminary review

Detailed review

Execution andmonitoring

1 2 3

▲ ▲ ▲ ▲Decision to evaluatedeal seriously

Inform MonitorMonitor willrecalculatefi nancial risk ratings

Board decision to undertake investment

Report fi nal terms

to Board

1aEvaluate fi t with overall strategy

1b Conduct preliminarybusiness case evaluation

1c Decide whether to undertake detailed review

2a Ensure right people/ process in place

2d Decide if investment should be pursued, renegotiated or cancelled

2b Conduct detailed review

2c Determine transaction structure & fi nancing

3a Close the transaction

3b Deliver value

12 – 13

1a Evaluate fi t with overall strategy

■ What is the strategy of the FT?■ How does the proposed

investment support or confl ict with this strategy?

■ If investment involves other entities, are their strategy/goals for the proposed investment aligned with those of FT?

1b Conduct preliminary business case evaluation

■ Has project plan for investment review been agreed?

– Timetable – Resources (eg project lead,

budget)■ Have appropriate external

advisers been engaged to undertake robust preliminary review and high level due diligence?

– Commercial issues (market, business plan, synergies, operations, management, cultural fi t, key commercial terms)

– Financing and structure – Legal/regulatory requirements■ Has expected risk-return been

identifi ed?■ Are proposed transaction Are proposed transaction

terms clear?■ Have necessary skills/expertise

to make investment successful been identifi ed (eg if entering new service line or geography)?

■ Have necessary FT management resources been identifi ed?

■ Has basic business model been prepared (eg scope assumptions, available data, fi nancial impact)?

■ Has a preliminary valuation been undertaken?

1c Decide whether to undertake detailed review

■ Does the investment seem promising enough to warrant detailed review?

■ Is FT well-positioned to manage/execute the investment (ie does it have necessary skills/expertise and management capacity)?

■ Can FT afford investment (eg will required additional borrowing leave suffi cient room for contingencies under prudential borrowing limit (PBL))?

■ Is there a clear understanding of alternative opportunities (eg improving core operations)?

■ Why is the proposed investment as good as, or better, than alternatives

– Strategic fi t? – Ability to execute? – Affordability? – Likely risk-return?■ What is the value of investing

now vs. retaining the option to invest later?

■ What potential future moves would taking this decision compromise?

Key questions

External advisers ■ Possibly management consultants

■ Accounting fi rms■ Lawyers■ Corporate Finance advice

■ Possibly management consultants, accounting fi rms

Is investment being reviewed at right organisational level?

Does FT have the legal power to make proposed investment?

Preliminary review

Detailed review

Execution andmonitoring

1 2 3

▲ ▲ ▲ ▲Decision to evaluatedeal seriously

Inform MonitorMonitor willrecalculatefi nancial risk ratings

Board decision to undertake investment

Report fi nal terms

to Board

1a Evaluate fi t with overall strategy

1b Conduct preliminarybusiness case evaluation

1c Decide whether to undertake detailed review

2a Ensure right people/ process in place

2d Decide if investment should be pursued, renegotiated or cancelled

2b Conduct detailed review

2c Determine transaction structure & fi nancing

3a Close the transaction

3b Deliver value

1 Preliminary review

Appendix 1: Framework for evaluating, executing and monitoring proposed major investments

2a Ensure right people/process in place

Key questions

■ Does project plan need to be refi ned?

– Timetable (refi ned with each stage of process)

– Resources and budget – Clear roles and responsibilties,

including internal project lead■ What are the contingency plans

if personnel leave?■ Are all external advisers in place

(eg management consultants, lawyers, accounting fi rms, investment banks) for detailed review:

– Business case (including market and operational risk analysis)

– Legal issues (eg constraints on ability to repatriate foreign earnings)

– Valuation – Transaction structuring

and fi nancing■ Is communications plan agreed?

2b Conduct detailed review of business case

Key questions

■ Have all key issues been taken into account eg commercial issues (as in 1b), fi nancial, HR, IT, legal, tax, pensions? For acquisitions, see Appendix 2

■ Are risks clear and quantifi ed where possible?

■ Has business model been refi ned (eg sensitivities, data quality)?

■ Have variations to any assumptions been addressed?

■ Is there a fi nalised valuation with clear methodology?

■ Has impact on fi nancial ratios used in risk ratings been assessed?

■ Is there an integration or separation plan, if relevant?

■ Has internal management been adequately engaged in providing input to external advisors?

■ Have necessary reports from external advisors been shared with investment committee?

2c Determine transaction structure & fi nancing

Key questions

■ What are the pros and cons of various transaction structures, eg JV, alliance, majority-owned subsidiary, minority-owned subsidiary?

■ What is the optimal fi nancing structure for the venture (eg debt vs. equity mix, upfront vs. stage payments)?

■ What are the pros and cons of various sources of fi nancing for FT?

■ Has fi nancing been integrated into business model?

■ Where should the venture be headquartered (if applicable)?

■ Will FT have appropriate board representation in the venture?

■ Inform Monitor: – Provide full details – Monitor will review, challenge

and revise risk rating

2d Decide if investment should be pursued

Key questions

■ How will the investment impact risk rating and PBL?

■ If the PBL impact is negative, can the investment be renegotiated?

■ If the investment will have negative impact and cannot be renegotiated, should it be cancelled?

■ Does investment still look more favourable than others (eg is there a business plan with compelling value creation opportunity)?

■ What is expected return on investment (eg Net Present Value) and pay back period?

■ What are the associated risks and potential impact on value?

– Market (eg demand, technology changes, competition)

– Financial (eg fi nancial risk takings)

– Regulatory/political (eg tariffs, policy change)

– Execution (eg construction delay, personnel)

– Reputation■ How will organisation

manage risks, including worst case scenario?

■ What is price/investment range that willl allow creation of value?

■ Is the investment still affordable?■ Is there confi dence in any

proposed partner’s cultural fi t and management capability?

■ Is there confi dence in proposed leadership and management of venture?

■ Are there any remaining information gaps?

2 Detailed Review

External advisers■ Corporate fi nance advice ■ Lawyers

■ Accounting fi rm■ Corporate Finance advice

■ Accountancy fi rms■ Tax advisers■ Lawyers

■ Possibly managementconsultants

Is investment being reviewed at right organisational level?

Does FT have the legal power to make proposed investment?

Preliminary review

Detailed review

Execution andmonitoring

1 2 3

▲ ▲ ▲ ▲Decision to evaluatedeal seriously

Inform MonitorMonitor willrecalculatefi nancial risk ratings

Board decision to undertake investment

Report fi nal terms

to Board

1aEvaluate fi t with overall strategy

1b Conduct preliminarybusiness case evaluation

1c Decide whether to undertake detailed review

2a Ensure right people/ process in place

2d Decide if investment should be pursued, renegotiated or cancelled

2b Conduct detailed review

2c Determine transaction structure & fi nancing

3a Close the transaction

3b Deliver value

14 – 15

3a Close the transaction

■ Is agreed price/investment within range which allows creation of value?

■ Is the fi nancing structure still viable in light of any revisions to FT’s Prudential Borrowing Limit?

■ Have all key issues been agreed: – Transaction value and

funding fl ows? – Working Capital arrangements? – Governance arrangements? – Leadership structure? – Rights/responsibilities of

partners (if applicable)? – Dispute resolution process? – Exit options (eg if partner

becomes insolvent or wants to exit, are the ownership rights clear?)

– Legality of investment?■ Does contract refl ect agreed

position and protect against contingencies?

■ Is there external stakeholder support?

■ Has transaction been recorded appropriately in law and in the FT’s records

■ Has it been signed off by relevant stakeholders?

■ Have communication priorities been agreed (internal and external)?

3b Deliver value

■ Is accountability for venture’s success clear?

■ Does the person in-charge have the appropriate skills, resources, and powers to do his/her job effectively?

■ Is everything in place to ensure value is delivered (eg in case of acquisition, are post-acquisition integration plan and programme offi ce in place, have appropriate advisers been engaged, is budget agreed)?

■ How will success of the venture be measured (eg performance against EBITDA targets, utilisation)?

■ How will performance be monitored?

– Metrics

– Methodology for data collection and presentation

– Frequency of reporting

– Who reviews reports■ How will performance issues and

ongoing risk be managed (eg are there clear trigger points which call for closer senior management scrutiny)?

■ Is communications plan being implemented appropriately, both internally and externally?

Key questions

External advisers ■ Lawyers■ Accounting fi rms■ Tax advisers■ Investment Banks

■ Post-acquisition management specialists, if relevant

■ Auditors

3 Execution and monitoring

Is investment being reviewed at right organisational level?

Does FT have the legal power to make proposed investment?

Preliminary review

Detailed review

Execution andmonitoring

1 2 3

▲ ▲ ▲ ▲Decision to evaluatedeal seriously

Inform MonitorMonitor willrecalculatefi nancial risk ratings

Board decision to undertake investment

Report fi nal terms

to Board

1aEvaluate fi t with overall strategy

1b Conduct preliminarybusiness case evaluation

1c Decide whether to undertake detailed review

2a Ensure right people/ process in place

2d Decide if investment should be pursued, renegotiated or cancelled

2b Conduct detailed review

2c Determine transaction structure & fi nancing

3a Close the transaction

3b Deliver value

Risk Evaluation for InvestmentDecisions by NHS Foundation Trusts

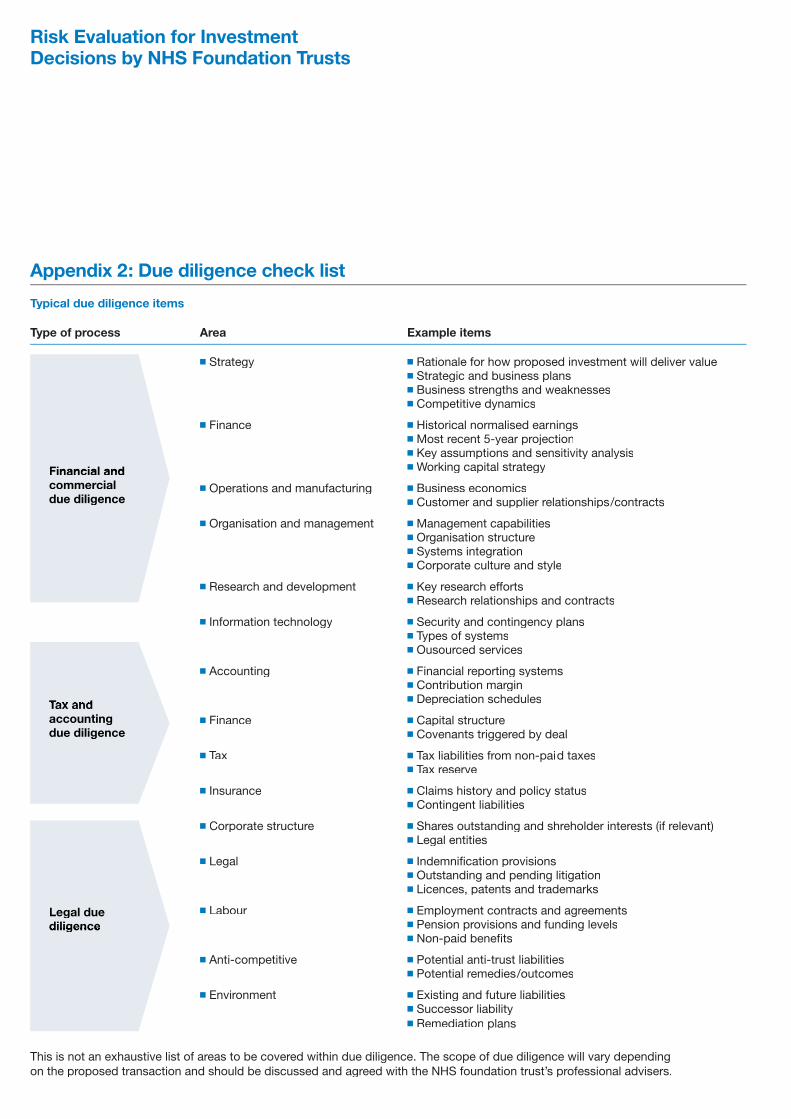

Appendix 2: Due diligence check list

Typical due diligence items

Type of process Area Example items

■ Strategy ■ Rationale for how proposed investment will deliver value ■ Strategic and business plans ■ Business strengths and weaknesses

■ Competitive dynamics

■ Finance ■ Historical normalised earnings ■ Most recent 5-year projection ■ Key assumptions and sensitivity analysis ■ Working capital strategy

■ Operations and manufacturing ■ Business economics ■ Customer and supplier relationships/contracts

■ Organisation and management ■ Management capabilities ■ Organisation structure ■ Systems integration ■ Corporate culture and style

■ Research and development ■ Key research efforts ■ Research relationships and contracts

■ Information technology ■ Security and contingency plans ■ Types of systems ■ Ousourced services

■ Accounting ■ Financial reporting systems ■ Contribution margin ■ Depreciation schedules

■ Finance ■ Capital structure ■ Covenants triggered by deal

■ Tax ■ Tax liabilities from non-pai d taxes ■ Tax reserve

■ Insurance ■ Claims history and policy status ■ Contingent liabilities

■ Corporate structure ■ Shares outstanding and shreholder interests (if relevant) ■ Legal entities

■ Legal ■ Indemnifi cation provisions ■ Outstanding and pending litigation ■ Licences, patents and trademarks

■ Labour ■ Employment contracts and agreements ■ Pension provisions and funding levels ■ Non-paid benefi ts

■ Anti-competitive ■ Potential anti-trust liabilities ■ Potential remedies/outcomes

■ Environment ■ Existing and future liabilities ■ Successor liability ■ Remediation plans

This is not an exhaustive list of areas to be covered within due diligence. The scope of due diligence will vary depending on the proposed transaction and should be discussed and agreed with the NHS foundation trust’s professional advisers.

Financial and Financial and

commercial due diligence

Tax and Tax and

accounting due diligence due diligence

Legal due diligence diligence

Appendix 3: Provisions of the Health and Social Care (Community Health and Standards) Act 2003 relevant to NHS foundation trust investments

Part 1 of the Act

14. Authorised services

(1) An authorisation must authorise the NHS foundation trust to provide goods and services for purposes related to the provision of health care.

(2) But the authorisation must secure that the principal purpose of the trust is the provision of goods and services for the purposes of the health service in England.

(3) The trust may also carry on activities other than those mentioned in subsection (1), subject to any restrictions in the authorisation, for the purpose of making additional income available in order to carry on its principal purpose better.

(4) The authorisation may require the provision, wholly or partly for the purposes of the health service in England, of goods and services by the trust.

(5) References in this part to goods and services include, in particular –

(a) education and training,

(b) accommodation and other facilities.

6. The authorisation must authorise and may require the trust –

(a) to carry out research in connection with the provision of health care,

(b) to make facilities and staff available for the purposes of education, training or research carried on by others;

and, in deciding how to exercise its functions under this subsection in a case where any of the corporation’s hospitals includes a medical or dental school provided by a university, the regulator is to have regard to the need to establish and maintain appropriate arrangements with the university.

7. In deciding whether or not to require the trust to provide, wholly or partly for the purposes of the health service in England, any goods or services the regulator is to have regard (among other things) to –

(a) the need for the provision of goods or services in the area in question,

(b) any provision of goods or services by other health service bodies in the area in question,

(c) any other provision by the trust with which the provision of the goods or services is connected,

(d) any agreement or arrangement to which the body corporate which is the trust is or was a party.

16 – 17

Risk Evaluation for InvestmentDecisions by NHS Foundation Trusts

8. Such a requirement as is mentioned in subsection (4) may be framed by reference (among other things) to –

(a) goods or services in general or of a particular description,

(b) goods or services required to meet the needs of health service bodies in general or those of a particular description,

(c) goods or services required to meet the needs of other persons of a particular description,

(d) the volume of goods or services provided,

(e) the place where goods or services are provided,

(f) the period within which goods or services are provided.

17. Financial powers

(1) An NHS foundation trust may borrow money for the purposes of or in connection with its functions.

(2) But the total amount of the trust’s borrowing is subject to the limit imposed by its authorisation.

(3) The limit must be reviewed annually by the regulator.

(4) An NHS foundation trust may invest money (other than money held by it as trustee) for the purposes of or in connection with its functions.

(5) The investment may include investment by –

(a) forming, or participating in forming, bodies corporate,

(b) otherwise acquiring membership of bodies corporate.

(6) An NHS foundation trust may give fi nancial assistance (whether by way of loan, guarantee or otherwise) to any person for the purposes of or in connection with its functions.

27. Mergers

(1) An application may be made jointly by –

(a) an NHS foundation trust, and

(b) another NHS foundation trust or an NHS trust,

to the regulator for authorisation of the dissolution of the trusts and the transfer of some or all of their property and liabilities to a new NHS foundation trust established under this section.

(2) The application must –

(a) be supported by the Secretary of State if one of the parties to it is an NHS trust,

(b) specify the property and liabilities proposed to be transferred to the new NHS foundation trust,

(c) describe the goods and services which it is proposed should be provided by the new trust, and

(d) be accompanied by a copy of the proposed constitution of the new trust;

and must give any further information which the regulator requires the applicants to give.

(3) The applicants may modify the application with the agreement of the regulator at any time before authorisation is given under this section.

(4) The regulator may –

(a) issue a certifi cate incorporating the directors of the applicants as a public benefi t corporation, and

(b) give an authorisation under this section to the corporation to become an NHS foundation trust,

if the regulator is satisfi ed as to the following matters.

(5) The matters are that –

(a) the constitution of the new trust will be in accordance with Schedule 1 and will otherwise be appropriate,

(b) the applicant has taken steps to secure that (taken as a whole) the actual membership of any public constituency, and (if there is one) of the patients’ constituency, will be representative of those eligible for such membership,

(c) the new trust will be able to provide the goods and services which the authorisation is to require it to provide, and

(d) any other requirements which the regulator considers appropriate are met.

(6) In deciding whether it is satisfi ed as to the matters referred to in subsection (5)(c), the regulator is to consider (among other things) –

(a) any report or recommendation in respect of either of the applicants made by the Commission for Healthcare Audit and Inspection,

(b) the fi nancial position of the applicants.

(7) The applicants must consult about the application in accordance with regulations.

18 – 19

Risk Evaluation for InvestmentDecisions by NHS Foundation Trusts

(8) In the course of the consultation the applicants must seek the views of –

(a) any Patients’ Forum for an applicant,

(b) the staff employed by the applicants,

(c) individuals who live in any area specifi ed in the proposed constitution as the area for a public constituency,

(d) any local authority that would be authorised by the proposed constitution to appoint a member of the board of governors,

(e) if the proposed constitution provides for a patients’ constituency, individuals who would be able to apply to become members of that constituency,

(f) any persons prescribed by regulations

(9) The regulator may not give an authorisation under this section unless it is satisfi ed that the applicants have complied with the regulations.

(10) The certifi cate is conclusive evidence of incorporation; and the authorisation is conclusive evidence that the corporation is an NHS foundation trust.

(11) On an authorisation being given under this section, the proposed constitution of the NHS foundation trust has effect, but the directors of the applicants may exercise the functions of the trust on its behalf until a board of directors is appointed in accordance with the constitution.

28. Section 27: supplementary

(1) Where an authorisation is given under section 27, the regulator is to specify the property and liabilities to be transferred to the new NHS foundation trust.

(2) Where such an authorisation is given, the Secretary of State is to make an order –

(a) dissolving the trusts in question, and

(b) transferring, or providing for the transfer of, the property and liabilities specifi ed by the regulator to the new NHS foundation trust.

(3) The order may –

(a) transfer, or provide for the transfer of, any of the remaining property or liabilities to the persons mentioned in section 25(3),

(b) include provisions corresponding to those of Schedule 3. (4) Where one of the parties to an application under section 27 is an NHS trust, the

powers conferred on the Secretary of State by Part 4 of Schedule 2 to the 1990 Act are not exercisable in relation to the trust.

(5) Section 6(4) applies to an authorisation under section 27 as it does in relation to an authorisation under that section.

39. General duty of NHS foundation trusts

An NHS foundation trust must exercise its functions effectively, effi ciently, and economically.

4 Matthew Parker StreetLondon SW1H 9NL

T: 020 7340 2400W: www.monitor-nhsft.gov.uk

IRG 01/06 © Monitor (February 2006)