26

Risk Management in Commercial Banks

| Date post: | 28-Dec-2015 |

| Category: |

Documents |

| Upload: | bryce-poole |

| View: | 215 times |

| Download: | 1 times |

Risk Management in Commercial Banks

Risk means uncertainty that may result in adverse

outcome, adverse in relation to planned objectives

Risk : Known Unknown

Uncertainty : Unknown Unknown

Classification of Banking Business

The entire Banking Business can classified under three major heads

• A) Banking Book• B) Trading Book• C) Off balance Sheet Exposures

Banking Book

All assets & liabilities in ‘banking book’ have following characteristics:

a) They are normally held till maturity.

b) Accrual System of accounting is followed

Trading Book

This book Consists of all investments and securities the bank has made, which are not held till maturity.

Mark to Market System is followed

The above book is further classified in to

a)Held to Maturity (HTM)

b)Held For Trading (HFT)

c)Available for Sale (AFS)

Off-Balance-Sheet Exposure

• Off-balance sheet exposure is contingent in nature- Guarantees, LCs, Committed or back up credit lines etc.

• A contingent exposure may become a fund-based exposure in Banking book or trading book.

Banking Book

The following are the risks involved in Banking Book

a)Liquidity Risk

b)Credit Risk

c)Interest Rate Risk

d)Operational Risk

Banking Book

As the assets and liabilities in the Banking

Book are normally held till their maturities,

they do not attract any market Risk

Trading Book

This book consists of banks` proprietary positions in financial instruments such as

a)Debt Securities

b)Equities

c)Foreign Exchange

d) Commodities

e) Derivatives held for Trading

Risks in Trading Book

Market Risk

Credit Risk

Liquidity Risk

Interest Rate Risk

Currency Risk

Operational Risk

Off Balance Sheet Exposures

All risks as applicable to Banking Book &

Trading book are applicable to this book

also

Liquidity Risk

Liquidity risk arises on account of funding long

term assets by short term liabilities.

Such risk arises, when there is a mismatch

in the maturity periods or repricing periods

of the assets and liabilities .

Example for Liquidity Risk

A Rs100 crores liability is raised for one year and the same is deployed in a two year assets

Naturally, there is a mismatch in the maturity periods of the assets and liabilities.

The liability cannot be repaid at the end of first year, as the bank would receive after two years only.

Hence the bank incurs a liquidity risk

Dimensions of Liquidity Risk

Funding Risk

Need to replace net outflows on account of unexpected withdrawals and non-renewal of deposits, due to loss of reputation or systemic risk.

Time Risk

Need to compensate for nonreceipt of expected inflow of funds on account of deterioration in asset quality or standard assets turning to NPA

Call Risk

This risk arises on account of crystallization of off balance sheet exposures or Contingent liabilities

Interest Rate Risk

When Banks` financial assets/liabilities such as

Advances and Deposits are exposed to

fluctuations in market interest rates, it will have

an impact on Net Interest Margin and the

market value of their equities.

This is called Interest Rate Risks

Dimensions of Interest Rate Risk

01. Gap or mismatch Risk

This risk arises from holding assets and liabilities

with different principal amounts, maturity dates or

repricing dates, thereby creating an exposure to

unexpected changes in the level of market interest

rates

02.Basis Risk

When interest rates of different assets and liabilities change

in different magnitude, the risk that arises is called Basis

Risk.

03.Embedded Option Risk

Significant changes in interest rates create a source of risk

to banks` profitability, by encouraging pre payment of Cash

credit /demand loan and/ or premature withdrawal of term

deposits before their slated period of maturity.

04.Yield Curve Risk

When banks take two different instruments

maturing on two different time horizon, as the

basis for pricing their assets and liabilities, any

non-parallel movement in yield curve would

affect the Net Interest Margin.

Example for Yield Curve Risk

91 days Treasury Bill8%

364 days Treasury Bill12%

Prevailing Market Rates

A liability is raised with interest rates 2% above 91 days

T-bill rate.Interest Rate on deposits 10%

Amount is deployed in advances with interest rates 2% above 364 days T-bill rate-Int rate on advances :14%

Spread 4%

91 days treasury Bill rate increases

to 10%Then, deposit rate also increases to

12%

364 days treasury bill rate does not

increase. Int rate is 14%

NII declines to

2%

Market Risk

Market Risk is the risk of adverse deviations of the mark

to market value of the trading portfolio, due to market

movements, during the period of holding. This results

from adverse movement of prices of interest rate related

instruments, equities, commodities and currencies.

Market risk is also called as Price risk

01.It is the loss in the market value of Fixed Income securities due to adverse fluctuations in their prices.

02.Risk of adverse deviations in the market to market value of a trading portfolio, due to market movements, during the period of holding.

03.Loss that occurs on account of the assets are being sold before the slated period of their maturity.

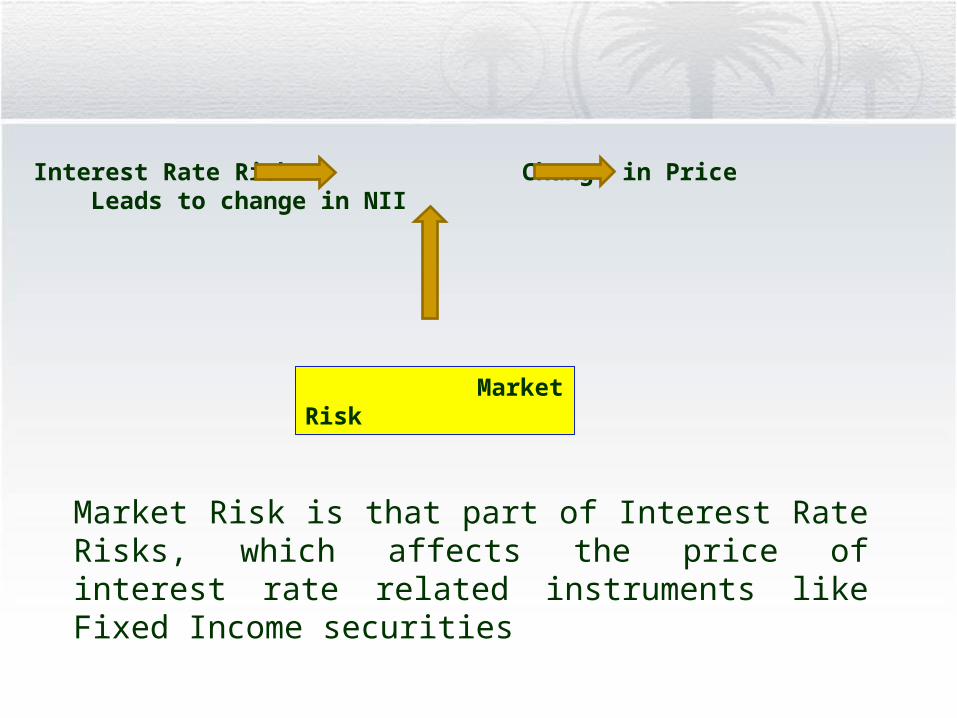

04.It is that part of Interest Rate Risks ,which affects the price of interest rate related instruments like Fixed Income securities

Interest Rate Risk Change in Price Leads to change in NII

Market Risk

Market Risk is that part of Interest Rate Risks, which affects the price of interest rate related instruments like Fixed Income securities

A fixed income security is an investment that pays regular income in the form of a coupon payment, interest payment or preferred dividend.

How it works/Example:

Fixed income securities provide periodic income payments at an interest or dividend rate known in advance by the holder. The most common fixed-income securities include Treasury bonds, corporate bonds, certificates of deposit (CDs) and preferred stock.

Operational Risk

It is the risk of loss resulting from inadequate or failed

internal processes, people and systems or from

external events.

Strategic Risk and Reputation risk are not part of

operational risk

Reputation Risk –

Reputation risk is the current or prospective indirect risk to earnings and capital from adverse perception of the image of the bank on the part of customers, shareholders and regulator.

Reputation risk may originate in lack of compliance with industry service standards and regulatory standards, failure to deliver on commitments, lack of customer friendly service and fair market practices, a service style that does not harmonize with customer expectation.

Strategic risk –

Business risk means current or prospective risk to

earnings and capital arising from changes in the business

environment and from adverse business decisions.

Reputation Risk and Strategic Risk are not coming under

operational risk.