Page 1

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 1/28

swap Page 1

SWAP

Introduction

The implacable wave of credit crisis casualties has financial institutions

scrambling to protect their bottom line. In these uncertain times, once

solid investment vehicles are now looked upon as carrying great risk. A

derivative is a financial instrument that allocates the risks and price

exposures associated with a designated asset between the parties to an

instrument. Derivatives can provide price exposure or price insulation to

changes in the price or level of an open-ended range of assets, including

stocks, interest rates, currencies, bonds, commodities, insured risks, credit

risks, investment funds, property, the weather and more. Derivatives are

used in an infinite variety of ways by commercial, eleemosynary and

governmental entities to manage the commercial and financial risks they

confront. As the breadth and complexity of derivatives evolve, so too does

the complexity of associated documentation and legal issues.

Page 2

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 2/28

swap Page 2

Meaning

In finance, a swap is a derivative in which counterparties exchange certain

benefits of one party's financial instrument for those of the other party's

financial instrument. The benefits in question depend on the type of

financial instruments involved. For example, in the case of a swap

involving two bonds, the benefits in question can be the periodic interest

(or coupon) payments associated with the bonds. Specifically, the two

counterparties agree to exchange one stream of cash flows against another

stream. These streams are called the legs of the swap. The swap

agreement defines the dates when the cash flows are to be paid and the

way they are calculated. Usually at the time when the contract is initiated

at least one of these series of cash flows is determined by a random or

uncertain variable such as an interest rate, foreign exchange rate, equity

price or commodity price.

The cash flows are calculated over a notional principal amount, which is

usually not exchanged between counterparties. Consequently, swaps can

be in cash or collateral. Swaps can be used to hedge certain risks such as

interest rate risk, or to speculate on changes in the expected direction of

underlying prices.

Swaps can be used to hedge certain risks such as interest rate risk, or to

speculate on changes in the expected direction of underlying prices.

Traditionally, the exchange of one security for another to change the

Page 3

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 3/28

swap Page 3

maturity (bonds), quality of issues (stocks or bonds), or because

investment objectives have changed. If firms in separate countries have

comparative advantages on interest rates, then a swap could benefit both

firms. For example, one firm may have a lower fixed interest rate, while

another has access to a lower floating interest rate. These firms could

swap to take advantage of the lower rates

The first swaps were negotiated in the early 1980s.David Swensen, a Yale

Ph.D. at Salomon Brothers, engineered the first swap transaction

according to "When Genius Failed: The Rise and Fall of Long-Term

Capital Management" by Roger Lowenstein. Today, swaps are among the

most heavily traded financial contracts in the world: the total amount of

interest rates and currency swaps outstanding is more thn $426.7 trillion

in 2009, according to International Swaps and Derivatives Association.

Page 4

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 4/28

swap Page 4

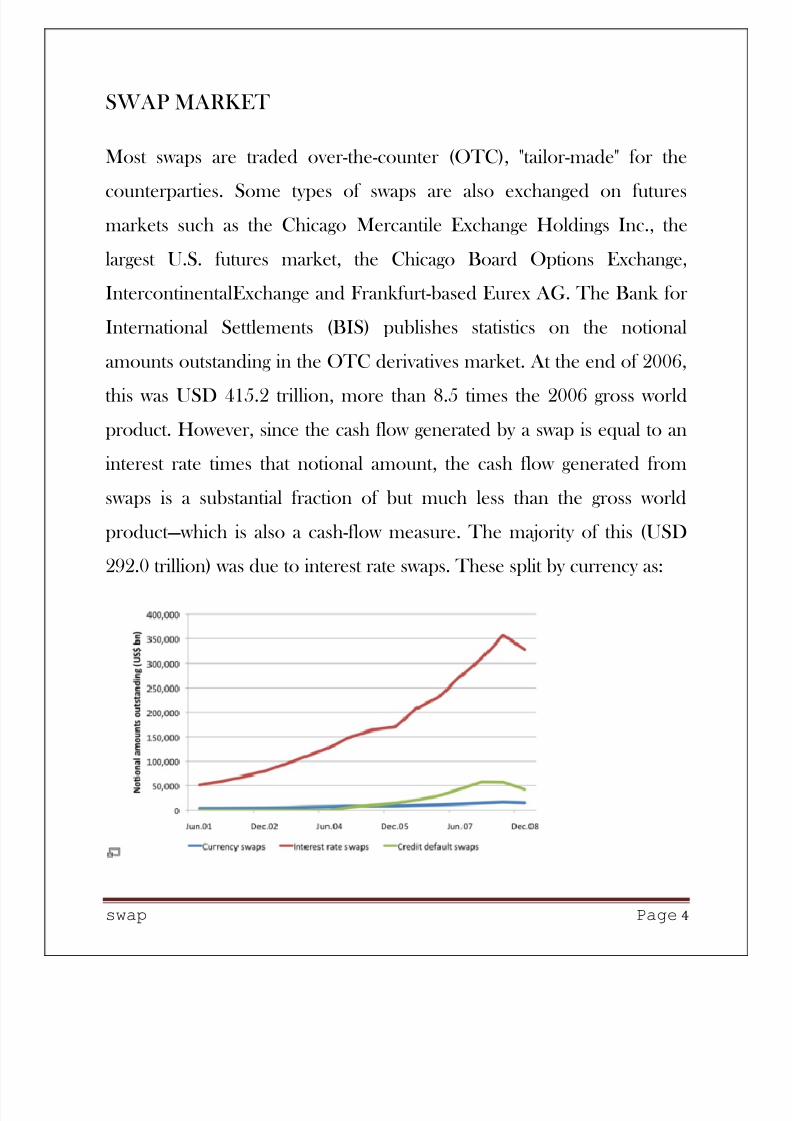

SWAPMARKET

Most swaps are traded over-the-counter (OTC), "tailor-made" for the

counterparties. Some types of swaps are also exchanged on futures

markets such as the Chicago Mercantile Exchange Holdings Inc., the

largest U.S. futures market, the Chicago Board Options Exchange,

IntercontinentalExchange and Frankfurt-based Eurex AG. The Bank for

International Settlements (BIS) publishes statistics on the notional

amounts outstanding in the OTC derivatives market. At the end of 2006,

this was USD 415.2 trillion, more than 8.5 times the 2006 gross world

product. However, since the cash flow generated by a swap is equal to an

interest rate times that notional amount, the cash flow generated from

swaps is a substantial fraction of but much less than the gross world

product³which is also a cash-flow measure. The majority of this (USD

292.0 trillion) was due to interest rate swaps. These split by currency as:

Page 5

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 5/28

swap Page 5

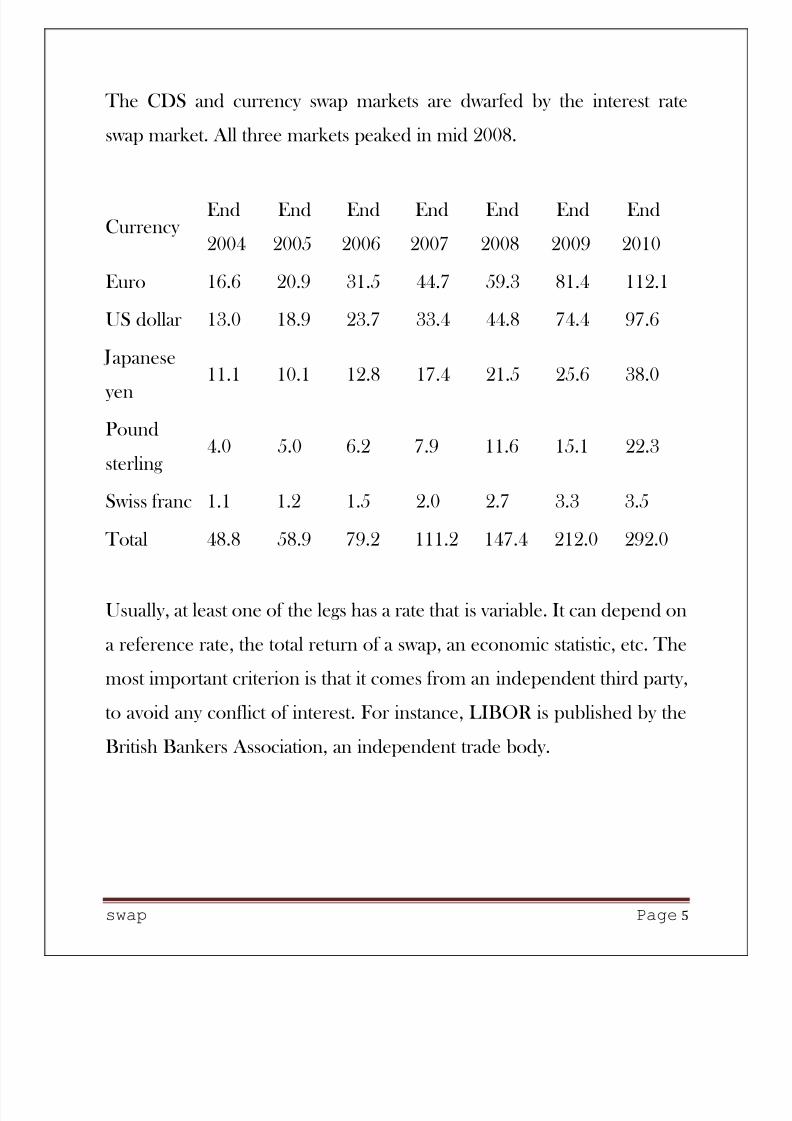

The CDS and currency swap markets are dwarfed by the interest rate

swap market. All three markets peaked in mid 2008.

Currency End

2004

End

2005

End

2006

End

2007

End

2008

End

2009

End

2010

Euro 16.6 20.9 31.5 44.7 59.3 81.4 112.1

US dollar 13.0 18.9 23.7 33.4 44.8 74.4 97.6

apanese

yen

11.1 10.1 12.8 17.4 21.5 25.6 38.0

Pound

sterling 4.0 5.0 6.2 7.9 11.6 15.1 22.3

Swiss franc 1.1 1.2 1.5 2.0 2.7 3.3 3.5

Total 48.8 58.9 79.2 111.2 147.4 212.0 292.0

Usually, at least one of the legs has a rate that is variable. It can depend on

a reference rate, the total return of a swap, an economic statistic, etc. The

most important criterion is that it comes from an independent third party,

to avoid any conflict of interest. For instance, LIBOR is published by the

British Bankers Association, an independent trade body.

Page 6

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 6/28

swap Page 6

Need for swap?

The motivations for using swap contracts fall into two basic categories:

commercial needs and comparative advantage. The normal business

operations of some firms lead to certain types of interest rate or currency

exposures that swaps can alleviate. For example, consider a bank, which

pays a floating rate of interest on deposits (i.e., liabilities) and earns a fixed

rate of interest on loans (i.e., assets). This mismatch between assets and

liabilities can cause tremendous difficulties. The bank could use a fixed-

pay swap (pay a fixed rate and receive a floating rate) to convert its fixed-

rate assets into floating-rate assets, which would match up well with its

floating-rate liabilities.

Some companies have a comparative advantage in acquiring certain types

of financing. However, this comparative advantage may not be for the type

of financing desired. In this case, the company may acquire the financing

for which it has a comparative advantage, then use a swap to convert it to

the desired type of financing.

Page 7

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 7/28

swap Page 7

For example, consider a well-known U.S. firm that wants to expand its

operations into Europe, where it is less well known. It will likely receive

more favorable financing terms in the US. By then using a currency swap,

the firm ends with the euros it needs to fund its expansion.

Page 8

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 8/28

swap Page 8

Types of Swaps

The five generic types of swaps, in order of their quantitative importance,

are:

i. Interest Rate Swaps

ii. Currency Swaps

iii. Credit Swaps

iv. Commodity Swaps And

v. Equity Swaps

Interest rate swaps

An interest rate swap is an exchange between two counter parties of interest obligations (payments of interest) or receipts (investment income),in the same currency on an agreed amount of notional principal for anagreed period of time. The agreed amount is called "notional principal"because, since it is not a loan or investment. The principal amount isneither exchanged at the outset nor rapid at maturity. The most commoninterest-rate swaps involve the exchange of interest from a fixed to a floating basis or vice versa.

Page 9

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 9/28

swap Page 9

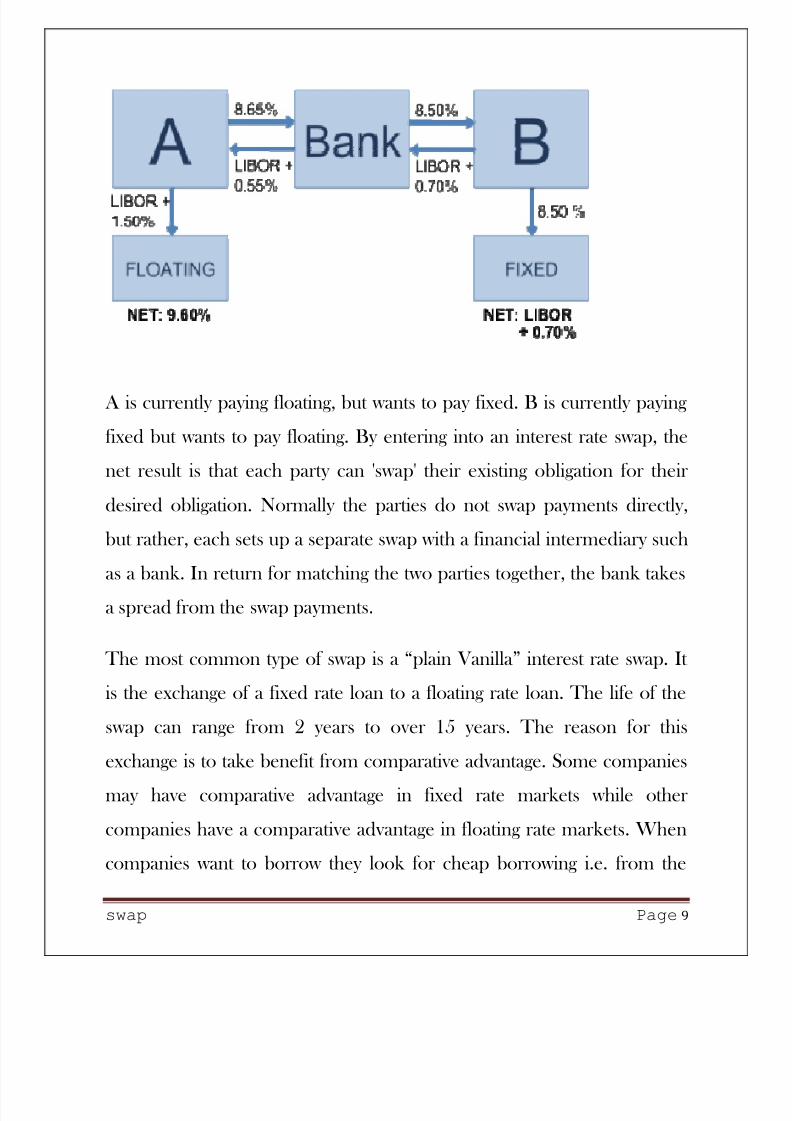

A is currently paying floating, but wants to pay fixed. B is currently paying

fixed but wants to pay floating. By entering into an interest rate swap, the

net result is that each party can 'swap' their existing obligation for their

desired obligation. Normally the parties do not swap payments directly,

but rather, each sets up a separate swap with a financial intermediary such

as a bank. In return for matching the two parties together, the bank takes

a spread from the swap payments.

The most common type of swap is a ´plain Vanillaµ interest rate swap. It

is the exchange of a fixed rate loan to a floating rate loan. The life of the

swap can range from 2 years to over 15 years. The reason for this

exchange is to take benefit from comparative advantage. Some companies

may have comparative advantage in fixed rate markets while other

companies have a comparative advantage in floating rate markets. When

companies want to borrow they look for cheap borrowing i.e. from the

Page 10

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 10/28

swap Page 10

market where they have comparative advantage. However this may lead to

a company borrowing fixed when it wants floating or borrowing floating

when it wants fixed. This is where a swap comes in. A swap has the effect

of transforming a fixed rate loan into a floating rate loan or vice versa.

For example, party B makes periodic interest payments to party A based

on a variable interest rate of LIBOR +70 basis points. Party A in return

makes periodic interest payments based on a fixed rate of 8.65%. The

payments are calculated over the notional amount. The first rate is called

variable, because it is reset at the beginning of each interest calculation

period to the then current reference rate, such as LIBOR. In reality, the

actual rate received by A and B is slightly lower due to a bank taking a

spread.

Page 11

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 11/28

swap Page 11

Currency Swaps

It is a swap that involves the exchange of principal and interest in one

currency for the same in another currency. It is considered to be a foreign

exchange transaction and is not required by law to be shown on the

balance sheet. Just like interest rate swaps, the currency swaps also are

motivated by comparative advantage.

Example

Suppose a U.S.-based company needs to acquire Swiss francs and a

Swiss-based company needs to acquire U.S. dollars. These two companies

could arrange to swap currencies by establishing an interest rate, an agreed

upon amount and a common maturity date for the exchange. Currency

swap maturities are negotiable for at least 10 years, making them a very

flexible method of foreign exchange.

Working

A currency swap agreement specifies the principal amount to be swapped,

a common maturity period and the interest and exchange rates

determined at the commencement of the contract. The two parties would

continue to exchange the interest payment at the predetermined rate until

Page 12

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 12/28

swap Page 12

the maturity period is reached. On the date of maturity, the two parties

swap the principal amount specified in the contract.

The equivalent amount of the loan value in another currency is calculatedby using the net present value (NPV). This implies that the exchange of

the principal amount is carried out at market rates during the inception

and maturity periods of the agreement.

Uses

Currency swaps have two main uses:

y To secure cheaper debt (by borrowing at the best available rateregardless of currency and then swapping for debt in desiredcurrency using a back-to-back-loan)

y To hedge against (reduce exposure to) exchange rate fluctuations.

Benefits of Currency Swap

The benefits of currency swaps are:

Help portfolio managers regulate their exposure to interest rates.

Speculators can benefit from a favorable change in interest rates.

Reduce uncertainty associated with future cash flows as it enablescompanies to modify their debt conditions.

Reduce costs and risks associated with currency exchange.

Page 13

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 13/28

swap Page 13

Companies having fixed rate liabilities can capitalize on floating-rate

swaps and vise versa, based on the prevailing economic scenario.

Currency swaps can be used to exploit inefficiencies in international

debt markets.

Limitations of Currency Swap

The drawbacks of currency swaps are:

Exposed to credit risk as either one or both the parties could

default on interest and principal payments.

Vulnerable to the central government·s intervention in the

exchange markets. This happens when the government of a

country acquires huge foreign debts to temporarily support a

declining currency. This leads to a huge downturn in the value of

the domestic currency.

Page 14

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 14/28

swap Page 14

Commodity Swap

A commodity swap is an agreement whereby a floating (or market or spot)

price is exchanged for a fixed price over a specified period. It is a swap

where exchanged cash flows are dependent on the price of an underlying

commodity. This is usually used to hedge against the price of a

commodity. In this swap, the user of a commodity would secure a

maximum price and agree to pay a financial institution this fixed price.

Then in return, the user would get payments based on the market price

for the commodity involved. The vast majority of commodity swaps

involve oil.

Equity Swap

It is basically a strategy in which an investor sells a bond and at the same

time purchases a different bond with the proceeds from the sale. There

are several reasons why people use a bond swap: to seek tax benefits, to

change investment objectives, to upgrade a portfolio's credit quality or to

speculate on the performance of a particular bond.

An equity swap is a special type of total return swap, where the underlying

asset is a stock, a basket of stocks, or a stock index. Compared to actually

owning the stock, in this case you do not have to pay anything up front,

but you do not have any voting or other rights that stock holders do have.

Page 15

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 15/28

swap Page 15

Equity Swaps also provide the following benefits over plain vanilla equity

investing:

1. An investor in a physical holding of shares loses possession on theshares once he sells his position. However, using an equity swap the

investor can pass on the negative returns on equity position without losing

the possession of the shares and hence voting rights. For example, let's say

A holds 100 shares of a Petroleum Company. As the price of crude falls

the investor believes the stock would start giving him negative returns in

the short run. However, his holding gives him a strategic voting right in the

board which he does not want to lose. Hence, he enters into an equity

swap deal wherein he agrees to pay Party B the return on his shares

against LIBOR+25bps on a notional amt. If A is proven right, he will get

money from B on account of the negative return on the stock as well as

LIBOR+25bps on the notional. Hence, he mitigates the negative returnson the stock without losing on voting rights.

2. It allows an investor to receive the return on a security which is listed in

such a market where he cannot invest due to legal issues. For example,

let's say A wants to invest on script X listed in Country C. However, A is

not allowed to invest in Country C due to capital control regulations. He

can however, enter into a contract with B, who is a resident of C, and ask

him to buy the shares of company X and provide him with the return on

share X and he agrees to pay him a fixed / floating rate of return.

Page 16

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 16/28

swap Page 16

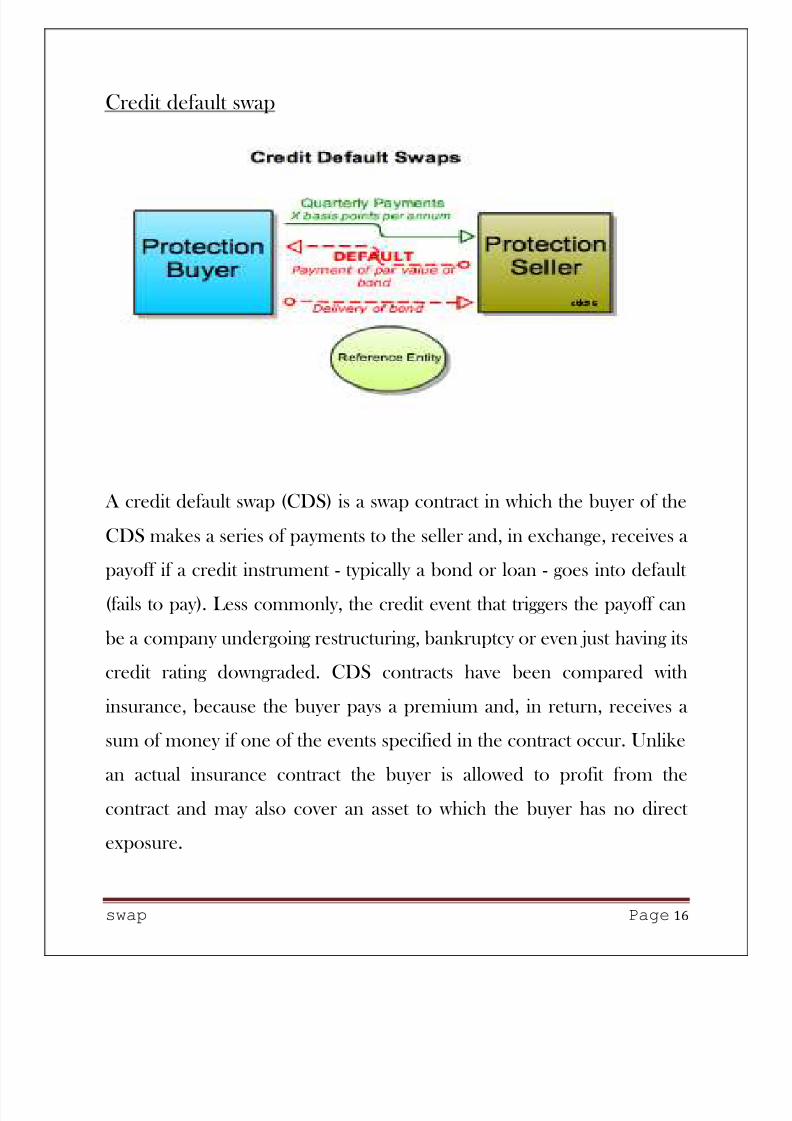

Credit default swap

A credit default swap (CDS) is a swap contract in which the buyer of the

CDS makes a series of payments to the seller and, in exchange, receives a

payoff if a credit instrument - typically a bond or loan - goes into default

(fails to pay). Less commonly, the credit event that triggers the payoff can

be a company undergoing restructuring, bankruptcy or even just having its

credit rating downgraded. CDS contracts have been compared with

insurance, because the buyer pays a premium and, in return, receives a

sum of money if one of the events specified in the contract occur. Unlike

an actual insurance contract the buyer is allowed to profit from the

contract and may also cover an asset to which the buyer has no direct

exposure.

Page 17

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 17/28

swap Page 17

Uses

Credit default swaps can be used by investors for speculation, hedging and

arbitrage.

y Speculation

Credit default swaps allow investors to speculate on changes in CDS

spreads of single names or of market indices such as the North American

CDX index or the European iTraxx index. An investor might believe that

an entity's CDS spreads are too high or too low, relative to the entity's

bond yields, and attempt to profit from that view by entering into a trade,

known as a basis trade, that combines a CDS with a cash bond and an

interest-rate swap.

y Hedging

Credit default swaps are often used to manage the risk of default which

arises from holding debt. A bank, for example, may hedge its risk that a

borrower may default on a loan by entering into a CDS contract as the

buyer of protection. If the loan goes into default, the proceeds from the

CDS contract will cancel out the losses on the underlying debt.

Page 18

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 18/28

swap Page 18

y Arbitrage

Capital Structure Arbitrage is an example of an arbitrage strategy that

utilizes CDS transactions.This technique relies on the fact that a

company's stock price and its CDS spread should exhibit negative

correlation; i.e. if the outlook for a company improves then its share price

should go up and its CDS spread should tighten, since it is less likely to

default on its debt. However if its outlook worsens then its CDS spread

should widen and its stock price should fall. Techniques reliant on this

are known as capital structure arbitrage because they exploit market

inefficiencies between different parts of the same company's capital

structure; i.e. mis-pricings between a company's debt and equity. An

arbitrageur will attempt to exploit the spread between a company's CDS

and its equity in certain situations.

Page 19

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 19/28

swap Page 19

Naked credit default swaps

In the examples above, the hedge fund did not own debt of Risky Corp. A

CDS in which the buyer does not own the underlying debt is referred to

as a naked credit default swap, estimated to be up to 80% of the credit

default swap market. There is currently a debate in the United States and

Europe about whether speculative uses of credit default swaps should be

banned. Legislation is under consideration by Congress as part of

financial reform.

Critics assert that naked CDS should be banned, comparing them to

buying fire insurance on your neighbor·s house, which creates a huge

incentive for arson. Analogizing to the concept of insurable interest, critics

say you should not be able to buy a CDS-insurance against default when

you do not own the bond. Short selling is also viewed as gambling and the

CDS market as a casino. Another concern is the size of CDS market.

Because naked credit default swaps are synthetic, there is no limit to how

many can be sold. The gross amount of CDS far exceeds all ´realµ

corporate bonds and loans outstanding. As a result, the risk of default is

magnified leading to concerns about systemic risk.

Page 20

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 20/28

swap Page 20

Forex swap

In finance, a forex swap (or FX swap) is a simultaneous purchase and sale

of identical amounts of one currency for another with two different value

dates (normally spot to forward).

Structure

A forex swap consists of two legs:

y a spot foreign exchange transaction, and

y a forward foreign exchange transaction.

Constant maturity swap

A constant maturity swap, also known as a CMS, is a swap that allows the

purchaser to fix the duration of received flows on a swap.

The floating leg of an interest rate swap typically resets against a published

index. The floating leg of a constant maturity swap fixes against a point on

the swap curve on a periodic basis.

A constant maturity swap is an interest rate swap where the interest rate

on one leg is reset periodically, but with reference to a market swap rate

rather than LIBOR. The other leg of the swap is generally LIBOR, but

may be a fixed rate or potentially another constant maturity rate. Constant

maturity swaps can either be single currency or cross currency swaps.

Page 21

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 21/28

swap Page 21

Therefore, the prime factor for a constant maturity swap is the shape of

the forward implied yield curves. A single currency constant maturity swap

versus LIBOR is similar to a series of differential interest rate fix (or

"DIRF") in the same way that an interest rate swap is similar to a series of

forward rate agreements. Valuation of constant maturity swaps depends

on volatilities and correlations of different forward rates and therefore

requires an interest rate model or some approximated methodology like a

convexity adjustment, see for example Brigo andMercurio (2001).

Example

A customer believes that the difference between the six-month LIBOR

rate will fall relative to the three-year swap rate for a given currency. To

take advantage of this, he buys a constant maturity swap paying the six-

month LIBOR rate and receiving the three-year swap rate.

Page 22

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 22/28

swap Page 22

Other variations

There are myriad different variations on the vanilla swap structure, which

are limited only by the imagination of financial engineers and the desire of

corporate treasurers and fund managers for exotic structures.

y A total return swap is a swap in which party A pays the total return

of an asset, and party B makes periodic interest payments. The total

return is the capital gain or loss, plus any interest or dividend

payments. Note that if the total return is negative, then party A

receives this amount from party B. The parties have exposure to the

return of the underlying stock or index, without having to hold the

underlying assets. The profit or loss of party B is the same for him

as actually owning the underlying asset.

y An option on a swap is called a swaption. These provide one party

with the right but not the obligation at a future time to enter into a

swap.

y A variance swap is an over-the-counter instrument that allows one to

speculate on or hedge risks associated with the magnitude of

movement, a CMS, is a swap that allows the purchaser to fix the

duration of received flows on a swap.y An Amortising swap is usually an interest rate swap in which the

notional principal for the interest payments declines during the life

Page 23

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 23/28

swap Page 23

of the swap, perhaps at a rate tied to the prepayment of a mortgage

or to an interest rate benchmark such as the LIBOR.

Valuation

The value of a swap is the net present value (NPV) of all estimated future

cash flows. A swap is worth zero when it is first initiated, however after this

time its value may become positive or negative. There are two ways to

value swaps: in terms of bond prices, or as a portfolio of forward

contracts.

a) Using bond prices

While principal payments are not exchanged in an interest rate swap,

assuming that these are received and paid at the end of the swap does not

change its value. Thus, from the point of view of the floating-rate payer, a

swap can be regarded as a long position in a fixed-rate bond (i.e. receiving

fixed interest payments), and a short position in a floating rate note (i.e.

making floating interest payments):

Page 24

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 24/28

swap Page 24

V swap = Bfixed Bfloating

From the point of view of the fixed-rate payer, the swap can be viewed as

having the opposite positions. That is,

V swap = Bfloating Bfixed

Similarly, currency swaps can be regarded as having positions in bonds

whose cash flows correspond to those in the swap. Thus, the home

currency value is:

V swap = Bdomestic S0Bforeign, where Bdomestic is the domestic cash flows of the

swap, Bforeign is the foreign cash flows of the swap, and S0 is the spot

exchange rate.

b) Using forward rate agreements

Consider a three year interest rate swap with semiannual payments. The

first cash flow is known at the time the swap is initiated, however the other

five exchanges can be regarded as forward rate agreements. The payment

for these other exchanges is the 6 month rate observed in the market 6

months earlier. Assuming that forward interest rates are realised, this

method values the swap by firstly calculating the required forward ratesusing the LIBOR/swap curve, then calculating the swap cash flows using

these rates, and then finally discounting these cash flows back to today.

Page 25

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 25/28

swap Page 25

c) London Interbank Offered Rate (LIBOR)

LIBOR is the rate of interest offered by banks on deposit from other

banks in the eurocurrency market. One-month LIBOR is the rate offeredfor 1-month deposits, 3-month LIBOR for three months deposits, etc.

LIBOR rates are determined by trading between banks and change

continuously as economic conditions change. Just like the prime rate of

interest quoted in the domestic market, LIBOR is a reference rate of

interest in the InternationalMarket.

d) Arbitrage arguments

As mentioned, to be arbitrage free, the terms of a swap contract are such

that, initially, the NPV of these future cash flows is equal to zero. Where

this is not the case, arbitrage would be possible.

For example, consider a plain vanilla fixed-to-floating interest rate swap

where Party A pays a fixed rate, and Party B pays a floating rate. In such

an agreement the fixed rate would be such that the present value of future

fixed rate payments by Party A are equal to the present value of the

expected future floating rate payments (i.e. the NPV is zero). Where this

is not the case, an Arbitrageur, C, could:

1. assume the position with the lower present value of payments, and

borrow funds equal to this present value

Page 26

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 26/28

swap Page 26

2. meet the cash flow obligations on the position by using the

borrowed funds, and receive the corresponding payments - which

have a higher present value

3. use the received payments to repay the debt on the borrowed funds

4. pocket the difference - where the difference between the present

value of the loan and the present value of the inflows is the arbitrage

profit.

Exiting a Swap Agreement

Sometimes one of the swap parties needs to exit the swap prior to the

agreed-upon termination date. This is similar to an investor selling an

exchange-traded futures or option contract before expiration. There are

four basic ways to do this.

1) Buy Out the Counterparty

Just like an option or futures contract, a swap has a calculable

market value, so one party may terminate the contract by paying the

other this market value. However, this is not an automatic feature,

so either it must be specified in the swaps contract in advance, or the

party who wants out must secure the counterparty·s concent

Page 27

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 27/28

swap Page 27

2) Enter an Offsetting Swap

For example, Company A from the interest rate swap example

above could enter into a second swap, this time receiving a fixed rate

and paying a floating rate.

3) Sell the Swap to Someone Else

Because swaps have calculable value, one party may sell the contract

to a third party. As with Strategy 1, this requires the permission of

the counterparty.

4) Use a Swaption

A swaption is an option on a swap. Purchasing a swaption would

allow a party to set up, but not enter into, a potentially offsetting

swap at the time they execute the original swap. This would reduce

some of the market risks associated with Strategy 2..

Page 28

8/7/2019 risk management project swap

http://slidepdf.com/reader/full/risk-management-project-swap 28/28