76

RISK MANAGEMENT REPORT BANCO DO BRASIL S.A.

2nd quarter of 2011

Risk Management Report

Banco do Brasil S.A. 2

Summary List of Tables ......................................................................................................................... 3

List of Figures ........................................................................................................................ 5

1. Introduction ........................................................................................................................ 6

2. CEO’s Message ................................................................................................................. 7

3. Governance ....................................................................................................................... 8

Risk Exposure........................................................................................................................ 8

Types of Risks ....................................................................................................................... 8

Corporate Risk Governance ................................................................................................. 10

Risk Management Process .................................................................................................. 11

Reports ................................................................................................................................ 11

4. Regulation ....................................................................................................................... 12

Basel Accord ....................................................................................................................... 12

Background ...................................................................................................................... 12

Basel I .............................................................................................................................. 12

1996 Market Risk Amendment ......................................................................................... 13

Basel II ............................................................................................................................. 13

Basel III ............................................................................................................................ 17

5. Basel II at Banco do Brasil ............................................................................................... 19

6. Regulations ...................................................................................................................... 21

7. Financial Conglomerate ................................................................................................... 22

8.1 Financial Conglomerate .............................................................................................. 23

8.1.1 Credit Risk ........................................................................................................... 23

8.1.2 Market and Liquidity Risks .................................................................................. 43

8.1.3 Operational Risk .................................................................................................. 54

8.2 Non-financial Companies ........................................................................................... 59

9. Capital ............................................................................................................................. 60

9.1 Regulatory Capital ...................................................................................................... 60

9.1.1 Referential Equity (PR) ........................................................................................ 60

9.1.2 Required Referential Equity (PRE) ....................................................................... 68

9.1.3 Basel Index (IB) ................................................................................................... 71

9.2 Economic Capital ....................................................................................................... 73

Risk Management Report

Banco do Brasil S.A. 3

List of Tables Table 1. Timetable for Basel III Implementation in Brazil ...................................................... 19

Table 2. Credit-risk exposure by Risk Weights ..................................................................... 30

Table 3. Average credit-risk exposure in each quarter ......................................................... 30

Table 4. Credit-risk exposure by geographic region and country .......................................... 31

Table 5. Credit-risk exposure of the financial conglomerate by economic sector .................. 32

Table 6. Credit-risk exposure of the economic-financial consolidated group by economic sector: .................................................................................................................................. 33

Table 7. Amount of transactions in arrears ........................................................................... 33

Table 8. Concentration levels of the ten biggest clients in relation to the total from lending transactions. ........................................................................................................................ 34

Table 9. Flow of transactions written-off ............................................................................... 34

Table 10. Stock of allowances for doubtful accounts ............................................................ 34

Table 11. Loss operations assigned, with substantial transfer of risks and benefits ............. 35

Table 12. Value of the exposures derived from acquiring FIDC and CRI .............................. 36

Table 13. Notional value of contracts to be liquidated in clearing house liquidation systems, in which the house acts as central counterparty ...................................................................... 38

Table 14. Notional value of contracts subject to counterparty credit risks in which clearing houses do not act as central counterparty. ........................................................................... 38

Table 15. Notional value of contracts where clearing houses did not act as central counterparty, and which do not have guarantees. ................................................................ 39

Table 16. Notional value of contracts where clearing houses did not act as central counterparty, and which do have guarantees. ...................................................................... 39

Table 17. Positive gross value of contracts subject to counterparty credit risks, not taking into account the positive values from compensation agreements, as set forth in CMN Resolution 3.263/05. .............................................................................................................................. 40

Table 18. The value of guarantees which cumulatively meet the requirements of paragraph VI, Article 8, of Bacen Circular 3.477/09:.............................................................................. 41

Table 19. Notional value of credit derivatives ....................................................................... 41

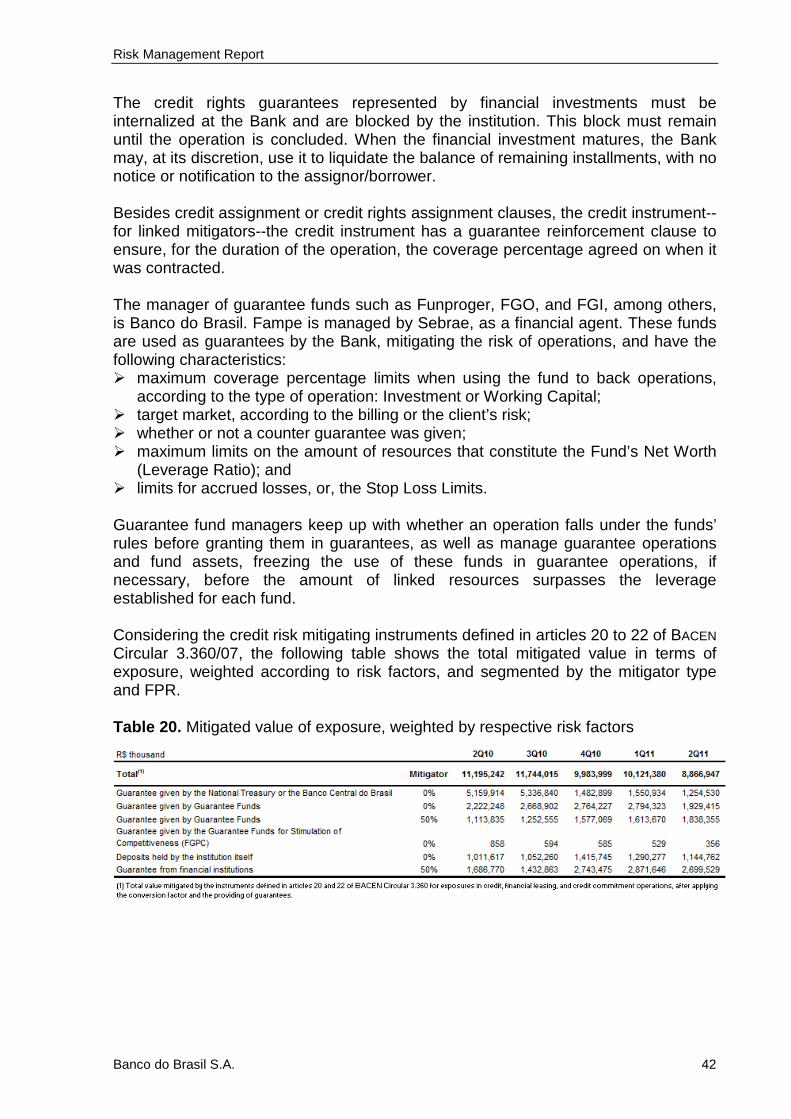

Table 20. Mitigated value of exposure, weighted by respective risk factors .......................... 42

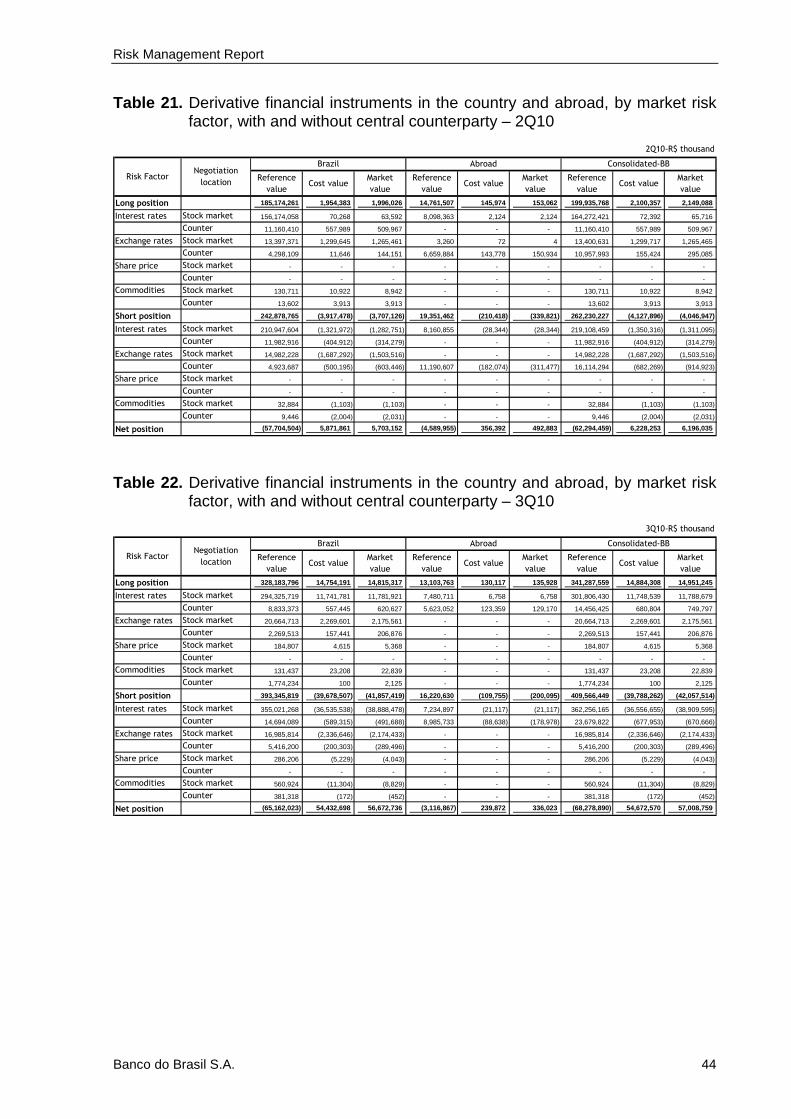

Table 21. Derivative financial instruments in the country and abroad, by market risk factor, with and without central counterparty – 2Q10 ...................................................................... 44

Table 22. Derivative financial instruments in the country and abroad, by market risk factor, with and without central counterparty – 3Q10 ...................................................................... 44

Table 23. Derivative financial instruments in the country and abroad, by market risk factor, with and without central counterparty – 4Q10 ...................................................................... 45

Table 24. Derivative financial instruments in the country and abroad, by market risk factor, with and without central counterparty – 1Q11 ...................................................................... 45

Table 25. Derivative financial instruments in the country and abroad, by market risk factor, with and without central counterparty – 2Q11 ...................................................................... 46

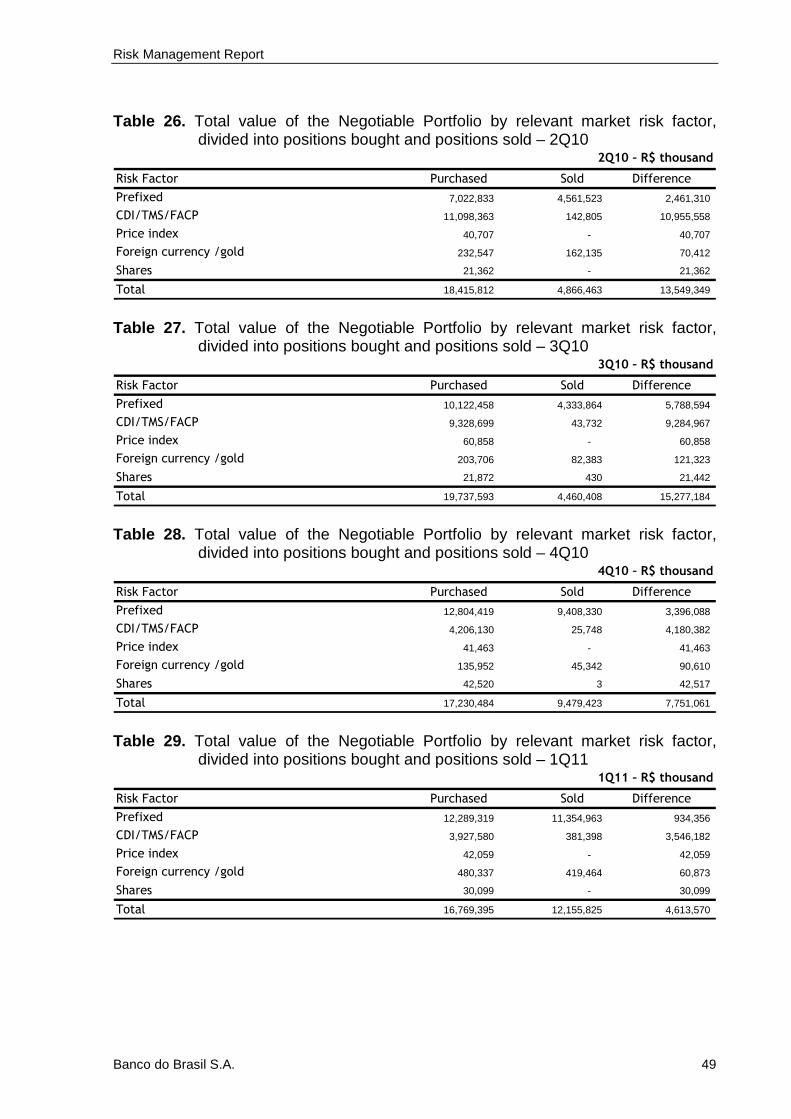

Table 26. Total value of the Negotiable Portfolio by relevant market risk factor, divided into positions bought and positions sold – 2Q10 .................................................................. 49

Table 27. Total value of the Negotiable Portfolio by relevant market risk factor, divided into positions bought and positions sold – 3Q10 ......................................................................... 49

Table 28. Total value of the Negotiable Portfolio by relevant market risk factor, divided into positions bought and positions sold – 4Q10 ......................................................................... 49

Risk Management Report

Banco do Brasil S.A. 4

Table 29. Total value of the Negotiable Portfolio by relevant market risk factor, divided into positions bought and positions sold – 1Q11 ......................................................................... 49

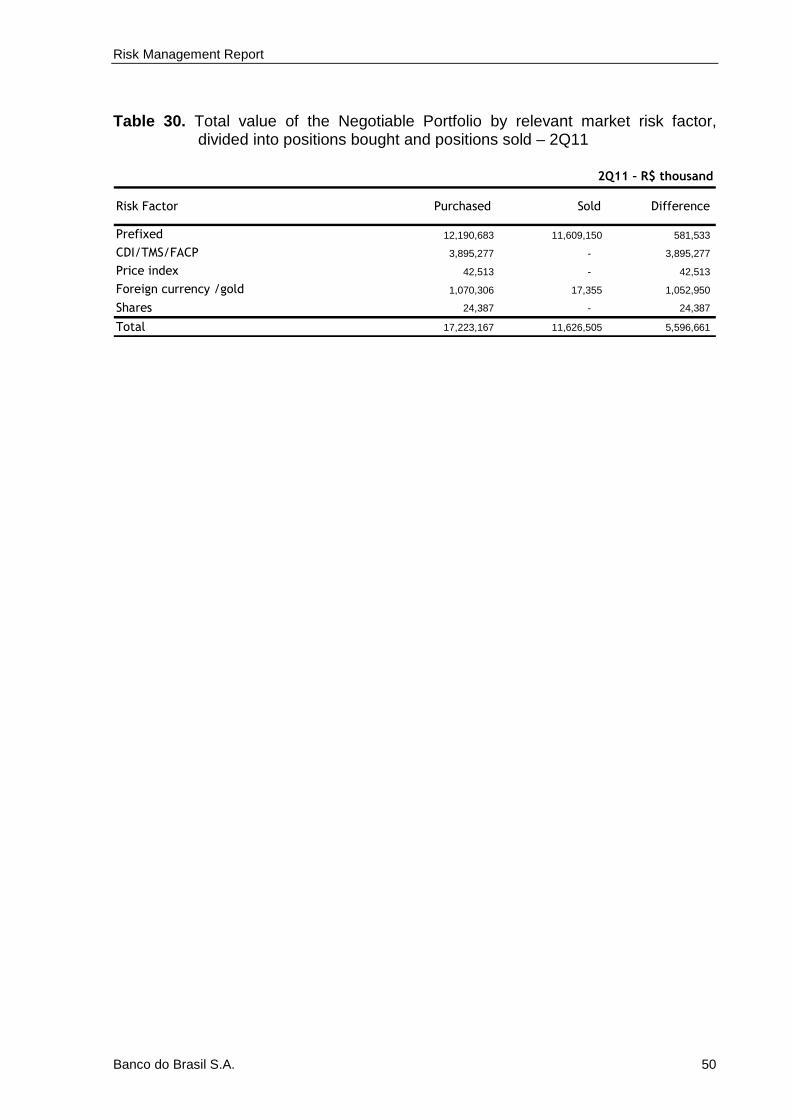

Table 30. Total value of the Negotiable Portfolio by relevant market risk factor, divided into positions bought and positions sold – 2Q11 ......................................................................... 50

Table 31. Phases of the operational risk management process ........................................... 55

Table 32. Monitoring of operating losses.............................................................................. 58

Table 33. Referential Equity ................................................................................................. 61

Table 34. Capital and Retained Earnings ............................................................................. 62

Table 35. Equity valuation adjustments ................................................................................ 62

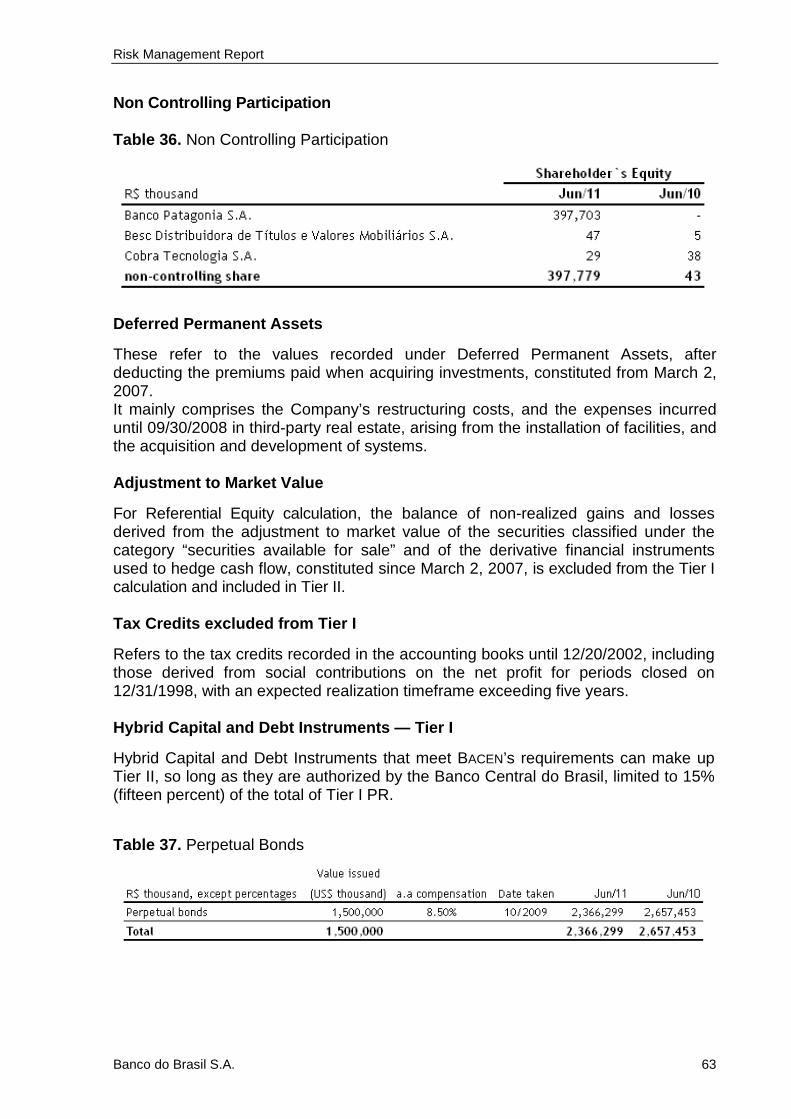

Table 36. Non Controlling Participation ................................................................................ 63

Table 37. Perpetual Bonds .................................................................................................. 63

Table 38. Subordinated Debt ............................................................................................... 65

Table 39. Subordinated Debt Eligible as Capital .................................................................. 65

Table 40. Perpetual Bonds .................................................................................................. 65

Table 41. Financial Instruments excluded from the PR ........................................................ 67

Table 42. PR historical series – Financial Conglomerate ..................................................... 67

Table 43. PR historical series – Consolidated Economic and Financial ............................... 67

Table 44. Required Referential Equity for the Financial Conglomerate ................................ 69

Table 45. Required Referential Equity for the Consolidated Economic – Financial .............. 70

Table 46. The Basel ratio and capital margin — Financial Conglomerate. ........................... 72

Table 47. The Basel ratio and capital margin — Consolidated Economic and Financial ....... 72

Table 48. Economic Capital ................................................................................................. 73

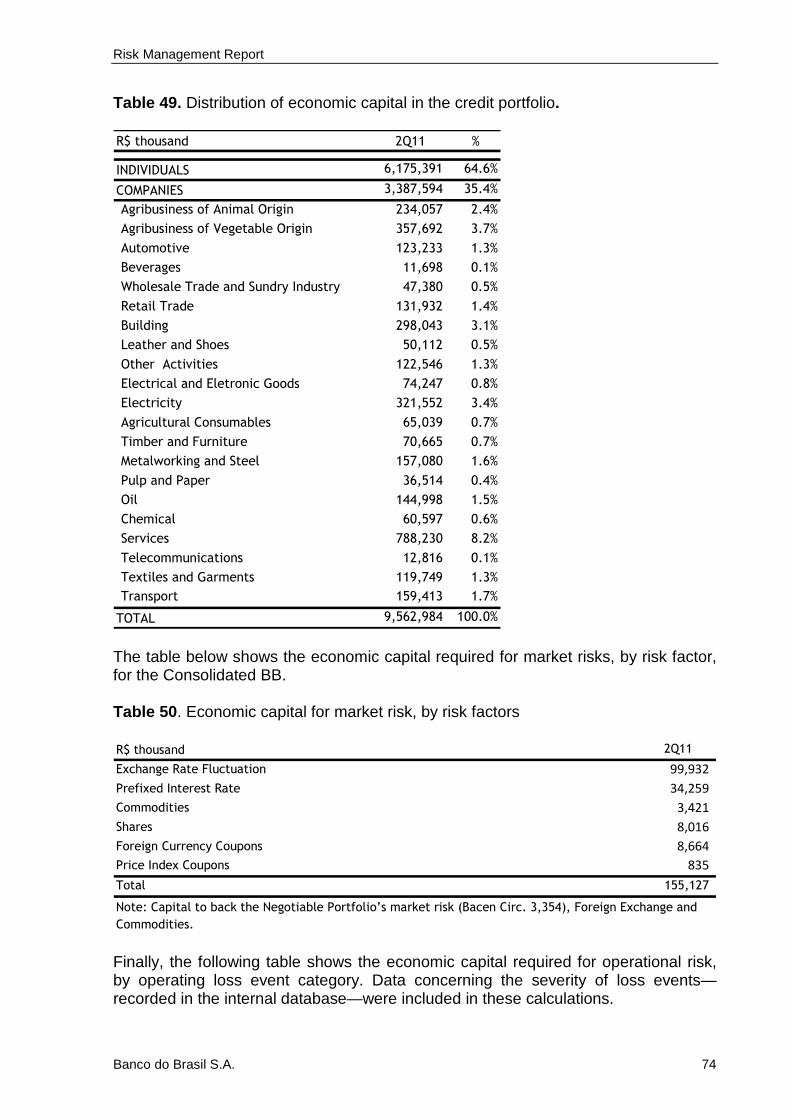

Table 49. Distribution of economic capital in the credit portfolio. .......................................... 74

Table 50. Economic capital for market risk, by risk factors ................................................... 74

Table 51. Economic capital for operational risk, by loss event category ............................... 75

Risk Management Report

Banco do Brasil S.A. 5

List of Figures Figure 1. Governance Structure ........................................................................................... 10

Figure 2. Management Structure and Process ..................................................................... 11

Figure 3. Basel II Pillars ....................................................................................................... 14

Figure 4. Capital allocation................................................................................................... 14

Figure 5. Pillar III Structure .................................................................................................. 16

Figure 6. Credit-risk management ........................................................................................ 23

Figure 7. Credit-risk management structure ......................................................................... 26

Figure 8. Operational risk management structure ................................................................ 54

Risk Management Report

Banco do Brasil S.A. 6

1. Introduction BB considers risk and capital management as its fundamental vectors for decision-making, providing greater stability, better capital allocation, and optimization of the risk-return ratio. The objective of this section is to inform shareholders and interested parties of the management practices and policies that comprise risk management at BB.

Risk Management Report

Banco do Brasil S.A. 7

2. CEO’s Message Participation by the country’s representative in the Basel Committee on Banking Supervision in Switzerland is a source of pride for Brazilians, reaffirming the new level of stability achieved by Brazil’s financial system. As is well-known, banking system sustainability is indissolubly linked with risk-management policies and mechanisms. The methods of identifying, measuring, assessing, monitoring, and controlling risk safeguard financial institutions in adverse situations and provide support for positive, recurring earnings over time. The expectation of smaller bank spreads reinforces that conviction. Just as important as increasing the volume of business is the consistency of a company’s risk governance and the efficiency of its management processes. Institutions that are able to transcend mere compliance with regulatory requirements and take risk into account in a quick and accurate way when making decisions are the ones that will rise to the challenge. Brazil’s participation in the Basel Committee on Banking Supervision will encourage broader, timelier adoption of international prudential standards. These new frontiers of the regulatory environment will require Brazilian financial institutions to become more agile and adaptable. In these aspects the bank is mature and conscious of its commitment to its clients, shareholders, investors, and society. Banco do Brasil continually seeks to keep pace with best management practices, including its risk-management architecture, which has a multidimensional scope to address credit, liquidity, market, and operational risks. The specifics are described in this space. Aldemir Bendine

Risk Management Report

Banco do Brasil S.A. 8

3. Governance Risk Exposure

Changes to the global financial environment, such as market integration through globalization, the emergence of new transactions and products, increasing technological sophistication, and new regulations, have made financial activities and processes - and their risks - ever more complex. Additionally, the lessons learned from financial disasters, such as those of the Metallgesellschatt Group and Barings, have helped show the essential need for risk management in the banking industry. These factors have influenced regulatory agencies and financial institutions to invest in risk management, seeking to strengthen the financial health of banks and to prevent detrimental effects on the financial system. In concert with this outlook, BB has invested in the continual improvement of its risk-management process and practices, in accordance with international market benchmarks and the New Basel Accord, known as Basel II, and by the fine-tuning provided by Basel III. Types of Risks

The main risks to which BB is exposed in its business are: Situational Risk: arises from the possibility of losses caused by changes to political, cultural, social, economic, or financial conditions in Brazil and other countries. It includes the following risks: a) Strategic Risk – risk of losses from adopting unsuccessful strategies, taking into

account the dynamics of business and competition, political changes in the country and abroad, and changes in the domestic and global economy;

b) Country Risk – understood as the possibility of losses associated with non-fulfillment of financial obligations according to negotiated terms by a borrower or counterparty located outside of the country, resulting from actions taken by the government of the country where the borrower or counterparty is located; and transfer risk, understood as the possibility of difficulties occurring during currency conversion of funds received; and

c) Systemic Risk – Possibility of losses due to the financial difficulties of one or more institutions that cause substantial damage to others, or a disruption of normal operations of the national financial system.

Credit Risk: defined as the possibility of losses associated with non-fulfillment by a buyer or a counterparty of their respective financial obligations according to negotiated terms, the devaluation of a loan agreement due to a drop in the borrower’s risk rating, a decline in gains or earnings, advantages offered during renegotiation, and recovery costs. Among other things, credit risk is defined as including:

Risk Management Report

Banco do Brasil S.A. 9

− counterparty credit risk, understood as the possibility of a given counterparty not fulfilling its obligations related to settlement of transactions that involve trading financial assets, including those related to the settlement of financial derivatives;

− country risk – understood as the possibility of losses associated with non-fulfillment of financial obligations according to negotiated terms by a borrower or counterparty located outside of the country, resulting from actions taken by the government of the country where the borrower or counterparty is located; and transfer risk, understood as the possibility of difficulties occurring during currency conversion of funds received;

− the possibility of having to make disbursements to honor guarantees, bonds, co-obligations, credit commitments, or other transactions of a similar nature; and

− the possibility of losses associated with a loan broker or intervening party not fulfilling their financial obligations according to negotiated terms.

Image Risk: possibility of losses from the institution having its name sullied on the market or with authorities, as a result of negative publicity, whether true or not. Market Risk: the possibility of losses from fluctuations of the market value of positions held by a financial institution. It includes the risks of transactions subject to fluctuations of exchange rates, interest rates, share prices, and commodity prices. Legal Risk: this can be defined as the possibility of losses due to fines, penalties or indemnities arising from actions by regulators, and losses due to unfavorable rulings in lawsuits and administrative actions. Liquidity Risk: is the occurrence of imbalances between tradable assets and liabilities payable - "mismatches" between payments and receipts - which can affect the institution’s payment ability, taking into account the various currencies and settlement terms of its rights and obligations.

Operational Risk: possibility of losses due to failures, deficiencies, or improper internal processes, people and systems or external events. This definition includes the legal risk associated with improper or deficient contracts signed by the institution, as well as sanctions resulting from noncompliance with legal provisions and compensation for damages to third parties resulting from activities engaged in by the institution.

Risk Management Report

Banco do Brasil S.A. 10

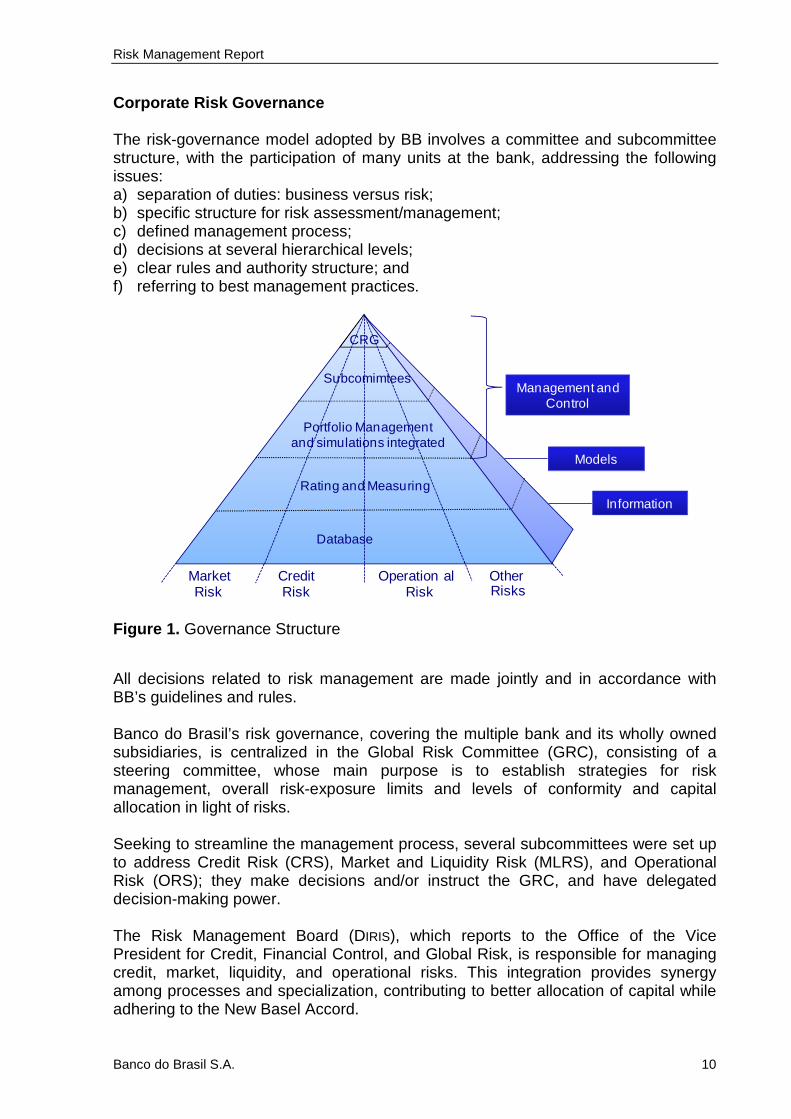

Corporate Risk Governance

The risk-governance model adopted by BB involves a committee and subcommittee structure, with the participation of many units at the bank, addressing the following issues: a) separation of duties: business versus risk; b) specific structure for risk assessment/management; c) defined management process; d) decisions at several hierarchical levels; e) clear rules and authority structure; and f) referring to best management practices.

CRG

MarketRisk

CreditRisk

Operation alRisk

OtherRisks

Database

Rating and Measuring

Portfolio Managementand simulations integrated

SubcomimteesManagement and

Control

Models

Information

Figure 1. Governance Structure

All decisions related to risk management are made jointly and in accordance with BB’s guidelines and rules. Banco do Brasil’s risk governance, covering the multiple bank and its wholly owned subsidiaries, is centralized in the Global Risk Committee (GRC), consisting of a steering committee, whose main purpose is to establish strategies for risk management, overall risk-exposure limits and levels of conformity and capital allocation in light of risks. Seeking to streamline the management process, several subcommittees were set up to address Credit Risk (CRS), Market and Liquidity Risk (MLRS), and Operational Risk (ORS); they make decisions and/or instruct the GRC, and have delegated decision-making power. The Risk Management Board (DIRIS), which reports to the Office of the Vice President for Credit, Financial Control, and Global Risk, is responsible for managing credit, market, liquidity, and operational risks. This integration provides synergy among processes and specialization, contributing to better allocation of capital while adhering to the New Basel Accord.

Risk Management Report

Banco do Brasil S.A. 11

Figure 2. Management Structure and Process Decisions are reported to intervening units through decisions that objectively express the position taken by executive management, guaranteeing application throughout the bank. Risk Management Process

The risk-management process involves a continuous flow of information, abiding by the following phases: a) preparation: data gathering and analysis phase. During this stage, risk measures

are analyzed and proposed for discussion and deliberation in the subcommittees, and if necessary, for later discussion and deliberation in the GRC;

b) decision: decisions are made jointly at the appropriate levels and reported to the intervening units;

c) execution: the intervening units implement the decisions made; and d) monitoring/management: the Risk Management Board oversees the process,

evaluating compliance with deliberations and their impacts on BB, reporting the status of these actions to the appropriate forum (subcommittee or GRC). Oversight of these decisions and reporting to subcommittees/GRC allows for improvement of the management process.

Reports

Risk-management reports provide support for risk-related decisions in the subcommittees, the Global Risk Committee, the Board of Officers, and the Board of Directors. They are prepared every month and have qualitative and quantitative managerial information about the bank’s exposure to risk. They support the

Aréas de Negócio

Aréas de Negócio

SRML SRC SRO

Risk Management Board

Global Risk Committee

Boards

Officers

President &

Vice-

Presidents

CRG Decision

Business Units

Monitoring Units

Risk Management Report

Banco do Brasil S.A. 12

information disclosed to the market in the Management Report and the Performance Analysis Report.

4. Regulation Basel Accord The rules established by the Basel Committee, from the outset, have always sought to create an international standard that regulators could use to defend the market against risks specific to the financial industry. Background In 1973, the global financial market was undergoing a period of intense volatility with the end of the International Monetary System based on fixed exchange rates. Liberalization of rates required measures to minimize the system’s risk. The fragility reached a critical level in 1974 with the occurrence of disruptions on international markets, such as the failure to settle currency contracts due to the insolvency of Germany’s Bankhaus Herstatt. At the end of that year, those in charge of banking oversight in the G-10 countries decided to create the Committee on Banking Regulation and Supervision of Practices, headquartered at the Bank of International Settlements (BIS) in Basel, Switzerland. Thus the name, the Basel Committee. The Committee consists of representatives from central banks and authorities with formal responsibility for banking oversight in the G-10 member countries. This Committee discusses issues related to the banking industry, seeking to improve the quality of banking supervision and to strengthen the security of the international banking system. The Committee does not have formal authority for supranational supervision, but it has the goal of inducing behavior in countries that are not members of the G-10. By following committee guidelines, those countries will contribute to improving practices on the international financial market. Basel I In July 1988, after an intense debate, the Basel Accord was executed, defining the mechanisms for measuring credit risk and establishing the minimum-capital requirements to endure risks. This accord is now known as Basel I. The accord’s objectives were to strengthen the health and the stability of the international banking system and to minimize the competitive inequalities among internationally active banks. These inequalities were the result of different minimum-capital requirement rules by national regulators. The 1988 Basel Accord defined three concepts:

Risk Management Report

Banco do Brasil S.A. 13

� Regulatory Capital - the amount of own capital allocated to cover risks, considering the parameters defined by the regulator;

� Asset Risk Weighting Factors - the exposure of assets (on and off balance sheet) to credit risk is adjusted by varying weights based primarily on the borrower’s profile; and

� Minimum Capital Index to Cover Credit Risk (Basel Index or BIS Ratio) - quotient between risk-bearing capital and risk-weighted assets (on and off balance sheet). If the amount calculated is equal to or greater than 8%, the bank’s capital level is sufficient to cover credit risk.

1996 Market Risk Amendment The advance made with Basel I, in terms of regulations and capital requirements to cover credit risk, was undeniable. However, a few criticisms emerged, making it necessary to improve upon that document within the Basel Committee. Among the adjustments was the need to set aside capital to cover market risks. Thus, in January 1996, an addendum to Basel I was published, called the Market Risk Amendment, whose main features are: � expansion of controls over risks incurred by banks; � extension of requirements to define minimum (or regulatory) capital, incorporating

market risk; and � possibility of using internal risk-measurement models, provided that they are

approved by local regulators. Basel II Since the Basel Committee’s creation in 1975, banking regulation has made significant strides. Thus, in June 2004, the Committee published the New Capital Accord, commonly known as Basel II, with the following objectives: � to promote financial stability; � to strengthen the capital structure of institutions; � to favor the adoption of best risk-management practices; and � to encourage greater transparency and market discipline. Basel II proposes a focus that is more flexible for capital requirements and more robust in terms of strengthening banking supervision and stimulating greater transparency in disclosing information to the market, based on three major premises: � Pillar I - strengthening the capital structure of institutions; � Pillar II - encouraging the adoption of best risk-management practices; and � Pillar III - reducing the asymmetry of information while favoring market discipline.

Risk Management Report

Banco do Brasil S.A. 14

Management of the national financial

system and financial information

Lessen asymmetry of information

Assessment in how banks are adjusting

needs to risks incurred

PILAR IIBanking Supervision

and Governance

Disclosure of relevant information

to the market

PILAR IIIMarket Discipline

System Stability

Solidity

Risks

- Credit

- Market

- Operational

PILAR IMinimum

Capital Requirements

Figure 3. Basel II Pillars

Pillar I defines the treatment to be given to determine capital requirements in light of risks incurred in the activities engaged in by financial institutions. In relation to the 1988 Accord, Basel II introduces a capital requirement for operational risk and refines the discussion of credit risk.

Market RiskCredit Risk Operational Risk

Modified Maintened Added

IRB Models�Standard�Advanced

Standard Aproach�Standard�StandardSimplified

**********

IRB Model

Standard Aproach

**********

IRB Model�Advanced

Standard Aproach�Standard�StandardAlternative

Basic

Figure 4 . Capital allocation

Basel II encourages the adoption of proprietary models to measure risks (credit, market, and operational), with differing degrees of complexity, subject to regulatory approval, and the possibility of benefits from lower capital requirements by adopting internal approaches. Pillar II reaffirms and strengthens the participation and role of the regulator in the banking supervision process and evaluation of risk governance at institutions, and how they manage capital to deal with the risks that they incur.

Risk Management Report

Banco do Brasil S.A. 15

Pillar III recommends the creation of instruments and conditions to lower systemic risk caused by asymmetric information, encouraging and favoring market discipline and transparency of information about risk-management practices. The combination of these three major elements on which the entire Basel II philosophy is based can be defined, in short, as the pursuit of refining risk-management and control practices. Pillar I Minimum Capital Requirements Under Pillar I, various alternatives are proposed to determine capital requirements in keeping with the financial institution’s size, complexity, and technical capacity, in order to measure risk. It sought to include a variety of measurement approaches, considering the use of (advanced) internal models as well. The main changes with respect to the first accord are: � the sophistication of credit-risk measurement methods; and � the inclusion of metrics for operational risk. Even though the internal models to calculate capital allocation require a greater degree of complexity, sophistication and investment, they allow for reducing the capital to be set aside in better reflecting the bank’s internal structure. Pillar II Governance and Supervision Process The supervision process establishes rules for risk management. The Committee established four essential principles of supervisory review that demonstrate the need for banks to evaluate capital adequacy in relation to risks assumed and for supervisors to review their strategies and to adopt relevant attitudes in light of these assessments. They are: 1. First Principle: banks must have a process to estimate their capital adequacy in

relation to their risk profile and have a strategy to maintain sufficient levels of capital;

2. Second Principle: supervisors should assess the banks’ strategies, adequacy estimates, and ability to monitor and to guarantee their compliance with minimum capital requirements;

3. Third Principle: supervisors expect, and may require, banks to operate over the minimum capital requirements; and

4. Fourth Principle: supervisors may intervene in advance and require banks to take prompt actions if their capital level falls below the minimum level.

Risk Management Report

Banco do Brasil S.A. 16

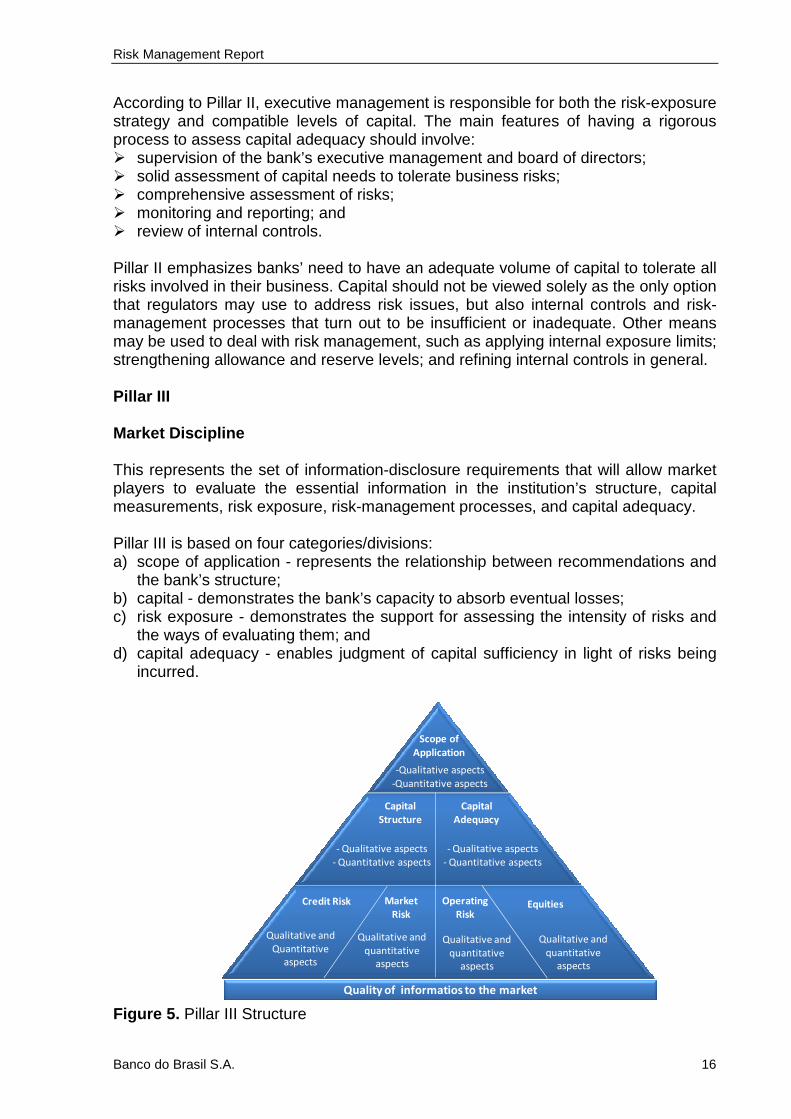

According to Pillar II, executive management is responsible for both the risk-exposure strategy and compatible levels of capital. The main features of having a rigorous process to assess capital adequacy should involve: � supervision of the bank’s executive management and board of directors; � solid assessment of capital needs to tolerate business risks; � comprehensive assessment of risks; � monitoring and reporting; and � review of internal controls. Pillar II emphasizes banks’ need to have an adequate volume of capital to tolerate all risks involved in their business. Capital should not be viewed solely as the only option that regulators may use to address risk issues, but also internal controls and risk-management processes that turn out to be insufficient or inadequate. Other means may be used to deal with risk management, such as applying internal exposure limits; strengthening allowance and reserve levels; and refining internal controls in general. Pillar III Market Discipline This represents the set of information-disclosure requirements that will allow market players to evaluate the essential information in the institution’s structure, capital measurements, risk exposure, risk-management processes, and capital adequacy. Pillar III is based on four categories/divisions: a) scope of application - represents the relationship between recommendations and

the bank’s structure; b) capital - demonstrates the bank’s capacity to absorb eventual losses; c) risk exposure - demonstrates the support for assessing the intensity of risks and

the ways of evaluating them; and d) capital adequacy - enables judgment of capital sufficiency in light of risks being

incurred.

Credit Risk

Qualitative and

Quantitative

aspects

Market

Risk

Qualitative and

quantitative

aspects

Operating

RiskEquities

Capital

Structure

- Qualitative aspects

- Quantitative aspects

Capital

Adequacy

- Qualitative aspects

- Quantitative aspects

Scope of

Application

-Qualitative aspects

-Quantitative aspects

Quality of informatios to the market

Qualitative and

quantitative

aspects

Qualitative and

quantitative

aspects

Figure 5. Pillar III Structure

Risk Management Report

Banco do Brasil S.A. 17

The rationale for creating this third pillar is to complement minimum capital requirements (Pillar I) and the supervisory review process (Pillar II). This means that with the development of rules that encourage and require more open information about banks’ risk profiles and capitalization levels, market players will feel encouraged to exercise discipline on this market. The use of certain transparency levels will be the benchmark for recognition and qualification of a financial institution in a specific capital-measurement approach. Examples include disclosing qualitative information about the structure of internal rating systems and the process to manage and to recognize the mitigation of credit risk. To guarantee compliance with transparency, Basel II calls for supervisors to have a greater number of persuasive instruments, ranging from dialogue with the bank’s management to financial fines, depending on the disclosure deficiency in question. With this format, the role of regulators grows in the sense of accessing and evaluating banks’ positions, given their risk exposures, with an emphasis on their supervisory role. By encouraging open information, the New Accord seeks to potentialize market players’ power of evaluation and action. Basel III Given the guidelines from the Basel Banking Supervision Committee, the Central Bank of Brazil (BACEN) published Notice 20,615 on 2/17/2011, which set out preliminary guidelines and a timetable for implementation in Brazil of the capital structure, leverage, and liquidity requirements known as Basel III. The main definitions and guidelines of this notice are presented below: a) New definition of capital: Tier I Capital of Referential Equity (PR) will consist of

two parts: Principal and Additional Capital;

b) Principal: will essentially consist of capital stock and retained earnings, after deduction of following items from Common Equity Tier 1 (CET1): � deferred tax assets from temporary differences; � deferred tax assets from tax losses and a negative basis for the social

contribution on net income; � premiums paid in acquiring investments based on the expectation of future

profitability and payroll rights, constituted starting on 01/01/2012; � deferred permanent assets and other intangible assets; � assets related to defined-benefit pension funds to which the financial institution

does not have unrestricted access; � holdings of non-controlled insurance firms; � investments in own shares (treasury stocks); � minority holdings that exceed the minimum required of CET1 and Capital

Conservation Buffer, defined in paragraph 16 of the notice, recorded at financial institutions that are part of a financial conglomerate or in the consolidated economic/financial group; and

� funding instruments issued by other financial institutions.

Risk Management Report

Banco do Brasil S.A. 18

Deferred tax assets from temporary differences and significant investments in non-controlled insurance firms may be recognized in the capital structure up to an individual limit of 10% of Common Equity Tier 1, and in the aggregate, along with other capital adjustments cited in paragraph 4 of the notice, up to 15% of Common Principal. These deductions shall occur progressively between 07/01/2012 and 01/01/2018.

c) Additional Capital: the trend is for it to consist of authorized hybrid capital and debt instruments that meet the requirements of loss-absorption during a financial institution’s operation; of subordination; of perpetuity; and of non-cumulative dividends;

d) Tier II Capital: it will likely consist of hybrid capital and debt instruments that do not qualify to be part of Additional Capital, along with subordinated debt instruments. For instruments that do not meet the eligibility requirements set out in Basel III, including the conversion clauses disclosed in the Basel Committee press release on 01/13/2011 (BIS, Press Release 03/2011), a gradual timetable for deductions will be defined, initially forecast as follows: 10% deduction of the nominal value of ineligible instruments, on 01/01/2013, adding 10% a year, so as to be completely excluded by 01/01/2022. The rule states that the BACEN shall publish a new referential equity definition by December 2011;

e) New minimum capital indices: two new indices were created: i) the Minimum

CET1, consisting of the ratio of CET1 to risk-weighted assets (RWA); and ii) Minimum Tier I Capital Index, consisting of the ratio of Tier 1 Capital and RWA;

f) Counterparty credit risk: modifications are anticipated to the capital requirements for counterparty credit risk, both for the standard approach and for internal risk rating (IRR) based approaches, to guarantee the inclusion of relevant risks in the capital structure;

g) Conservation Capital: this amount will complement the minimum regulatory requirements and will consist of elements accepted to comprise CET1;

h) Countercyclical Capita: this should also consist of elements accepted in the

CET1 and will be required in the event of excessive growth of credit associated with the potential accumulation of systemic risk. The established timetable notwithstanding, any increases to the percent of Countercyclical Capital will be published by the BACEN at least 12 months in advance;

i) Leverage Index: Basel III recommends implementation of a Leverage Index as a

complementary capital measure, determined by dividing Tier I Capital by the amount of total exposure. As of 01/01/2018, the minimum required amount for the Leverage Index is scheduled to begin, initially forecast at 3%; and

j) Liquidity measures: two liquidity indices are proposed, one short-term and the

other long-term, as described below: � Short-Term Liquidity Index (LCR): the purpose is to demonstrate that

institutions have highly liquid funds to make it through a scenario of acute

Risk Management Report

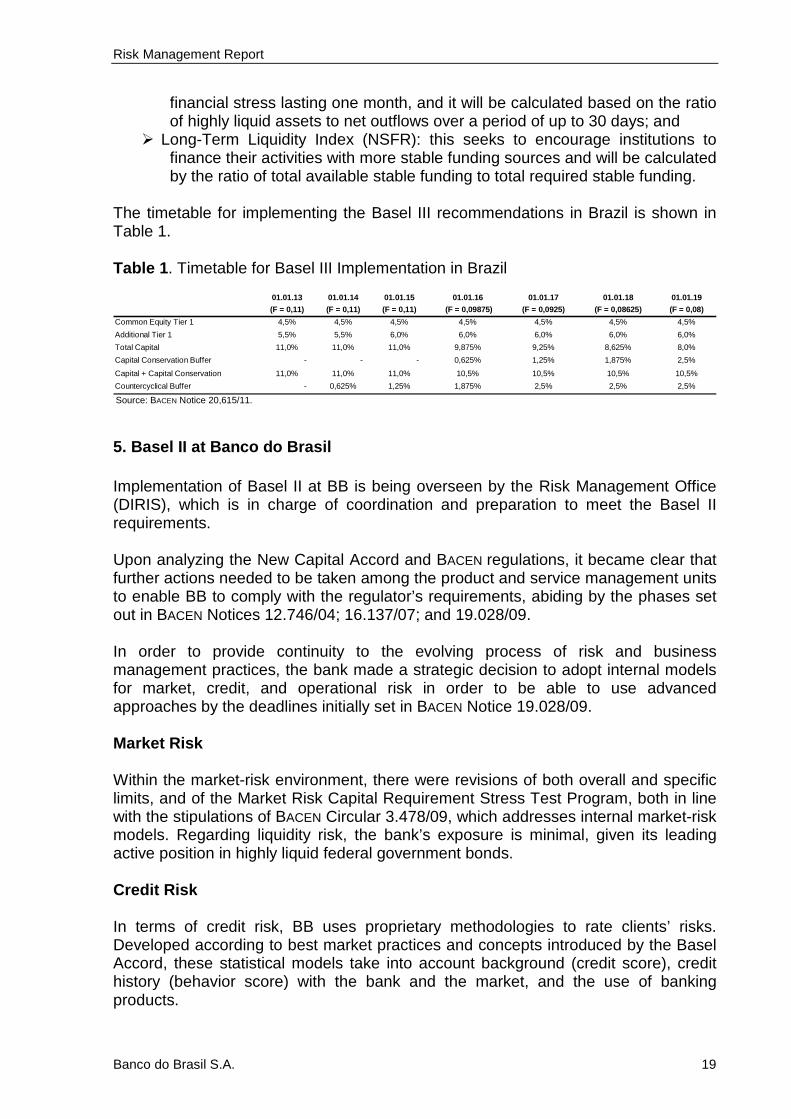

Banco do Brasil S.A. 19

financial stress lasting one month, and it will be calculated based on the ratio of highly liquid assets to net outflows over a period of up to 30 days; and

� Long-Term Liquidity Index (NSFR): this seeks to encourage institutions to finance their activities with more stable funding sources and will be calculated by the ratio of total available stable funding to total required stable funding.

The timetable for implementing the Basel III recommendations in Brazil is shown in Table 1. Table 1 . Timetable for Basel III Implementation in Brazil

01.01.13 01.01.14 01.01.15 01.01.16 01.01.17 01.01.18 01.01.19

(F = 0,11) (F = 0,11) (F = 0,11) (F = 0,09875) (F = 0,0925) (F = 0,08625) (F = 0,08)

Common Equity Tier 1 4,5% 4,5% 4,5% 4,5% 4,5% 4,5% 4,5%

Additional Tier 1 5,5% 5,5% 6,0% 6,0% 6,0% 6,0% 6,0%

Total Capital 11,0% 11,0% 11,0% 9,875% 9,25% 8,625% 8,0%

Capital Conservation Buffer - - - 0,625% 1,25% 1,875% 2,5%

Capital + Capital Conservation 11,0% 11,0% 11,0% 10,5% 10,5% 10,5% 10,5%

Countercyclical Buffer - 0,625% 1,25% 1,875% 2,5% 2,5% 2,5% Source: BACEN Notice 20,615/11.

5. Basel II at Banco do Brasil Implementation of Basel II at BB is being overseen by the Risk Management Office (DIRIS), which is in charge of coordination and preparation to meet the Basel II requirements. Upon analyzing the New Capital Accord and BACEN regulations, it became clear that further actions needed to be taken among the product and service management units to enable BB to comply with the regulator’s requirements, abiding by the phases set out in BACEN Notices 12.746/04; 16.137/07; and 19.028/09. In order to provide continuity to the evolving process of risk and business management practices, the bank made a strategic decision to adopt internal models for market, credit, and operational risk in order to be able to use advanced approaches by the deadlines initially set in BACEN Notice 19.028/09. Market Risk Within the market-risk environment, there were revisions of both overall and specific limits, and of the Market Risk Capital Requirement Stress Test Program, both in line with the stipulations of BACEN Circular 3.478/09, which addresses internal market-risk models. Regarding liquidity risk, the bank’s exposure is minimal, given its leading active position in highly liquid federal government bonds. Credit Risk In terms of credit risk, BB uses proprietary methodologies to rate clients’ risks. Developed according to best market practices and concepts introduced by the Basel Accord, these statistical models take into account background (credit score), credit history (behavior score) with the bank and the market, and the use of banking products.

Risk Management Report

Banco do Brasil S.A. 20

Operational Risk To manage operational risk, Banco do Brasil - adhering to best market practices - monitors operational losses by making use of systematized internal databases, exposure limits, and key risk indicators, in addition to risk matrices to evaluate relevant outsourced services. Seeking continual improvement of the operational-risk management process, in 2010 BB implemented specific limits for operational losses related to “Labor Issues”, “Business Failures”, “Process Failures” and “External Fraud and Theft”, with the goal of providing more flexibility when proposing mitigation actions. Particularly important was the work done to adjust to the guidelines published by the BACEN in Notice 19.217/09, which involved using four essential elements in the internal model for measuring operational risk: Internal Database, External Database, Scenario Analysis, Internal Control Factors, and Business Environment. To prevent, correct, or inhibit weaknesses that might cause risks to BB, and to reduce losses and to strengthen the risk culture, the Technical Risk Recommendation was created, issued to units that manage processes or products when a need is identified to take a loss-mitigation action, and to guarantee compliance with the responsibilities defined in the risk-management phases.

Risk Management Report

Banco do Brasil S.A. 21

6. Regulations The BACEN, in concert with the procedures of regulators in developed countries, has issued a series of prudential regulations. Current regulations can be consulted on its website.

Risk Management Report

Banco do Brasil S.A. 22

7. Financial Conglomerate Risk management in the Banco do Brasil financial conglomerate is comprehensive and covers credit, market, liquidity, and operational risks. Management activities are performed by specific, specialized structures, pursuant to objectives, policies, strategies, processes, and systems described in each of these risks. Even though activities focus on credit, market, liquidity, and operational risk, the bank uses mechanisms to guarantee capital sufficiency to cover other risks incurred.

Risk Management Report

Banco do Brasil S.A. 23

8. Risk Management 8.1 Financial Conglomerate 8.1.1 Credit Risk Management Objectives Exposures subject to credit risk are a big part of Banco doBrasil’s assets. That is why risk management of these exposures is fundamental for the bank to achieve its objectives. Banco do Brasil’s credit risk is managed according to best market practices and following banking supervision and regulatory rules. It seeks to identify, measure, control, and mitigate the risk of exposure, contribute to maintaining the bank’s health and solvency, and guarantee that shareholders’ interests are being met. Credit-risk management at the financial conglomerate involves credit policy, management strategies, management processes, operational procedures, and management systems, as shown in the figure below:

CREDIT POLICY

MANAGEMENT PROCESSES

OPERATIONAL PROCEDURES

MANAGEMENT SYSTEMS

MANAGEMENT STRATEGY

CA

CRG

DICRE

DIRAO

DIRIS

STRATEGIC LEVEL

RISK MANAGEMENT STRUCTUREOPERATIONAL LEVEL

SRC

TATICAL LEVEL

Figure 6. Credit-risk management Note: CA = Board of Directors; CRG = Global Risk Committee; SRC = Credit Risk Subcommittee; DICRE = Credit Board; DIRAO = Asset Restructuring Board; DIRIS = Risk Management Board.

Risk Management Report

Banco do Brasil S.A. 24

In accordance with CMN Decision 3.721/09, the Board of Directors (CA) approved the credit-risk management structure of Banco do Brasil, consisting of the Global Risk Committee (CRG), Credit Risk Subcommittee (SRC), Credit Board (DICRE), Operational Asset Restructuring Board (DIRAO), and Risk Management Board (DIRIS). Given that the DIRIS is the unit at the bank in charge of overall risk management and does not have any ties to the management of third-party funds or to performing transactions subject to credit risk, the CA appointed the Director of Risk Management as the person in charge of BB’s credit-risk management with respect to the BACEN. This credit-risk management structure is compatible with the nature of transactions, the complexity of products and services, and in proportion to the size of the credit-risk exposure incurred by Banco do Brasil. Credit Policy Banco do Brasil’s credit policy contains strategic guidelines to direct credit-risk management actions at the financial conglomerate. It is approved by the Board of Directors and reviewed every year. It is available to all employees, and applies to all business that involves credit risk. The policy is divided up into four blocks: General Aspects, Assuming Credit Risk, Collections and Credit Recovery, and Credit Risk Management. Each block has a broad set of statements that encompass all stages of credit-risk management at Banco do Brasil. Listed below are a few of the topics addressed in Banco do Brasil’s credit policy: � concept of credit risk; � conditions for assuming risk; � separation of duties; � guidelines for collections and credit

recovery; � joint decisions; � expected loss, economic and regulatory

capital; � risk appetite; � allowance and capital levels; � risk limits; � stress tests and sensitivity analysis; and � client rating; � capital planning

Risk Management Report

Banco do Brasil S.A. 25

Management Strategies Management strategies are established by the CA and the CRG, and implemented tactically by the SRC, all in accordance with the credit-risk management objectives and credit policy of Banco do Brasil. The CRG consists of the President and Vice Presidents of the units involved with credit-risk management. The Committee sets strategies for credit-risk management, defines overall exposure limits, and approves capital allocation. The SRC was created to make faster decisions about credit-risk management. It is a tactical structure, subordinated to the CRG, which has delegated decision-making authority to deliberate on certain issues, instructing the CRG on other issues. The SRC consists of officers from the units involved in credit-risk management, coordinated by the Director of the Risk Management Board. Credit-risk management strategies guide actions at the operational level. Strategic decisions include: � materializing the risk appetite of Banco do Brasil; � approving credit-risk management models; � setting goals for fulfillment, recovery, maximum loss, and quality of the credit

portfolio; � setting risk and concentration limits; � keeping adequate levels of allowances and capital; and � management of the risk-return ratio Management Processes According to Banco do Brasil’s credit-risk management structure, the Credit (DICRE), Operational Asset Restructuring (DIRAO) and Risk Management (DIRIS) units are responsible for implementing strategic decisions approved by the CA, CRG and SRC, keeping exposure at the risk levels set by the executive management. The DICRE focuses on clients and operations. Its main products are: registration, marketing studies and information on economic sectors, methodologies (risk, risk components, and credit limits), risk analysis (clients, operations, projects, economic sectors, countries, and projects), pre-validation and monitoring of risk methodology and credit-risk components, study of investment and leasing transactions, economic/financial evaluation and diagnosis of businesses/business groups, monitoring the credit portfolio, and producing inputs to price credit risk. The DIRAO deals with, collects, and recovers problem credits. Its main products are: models to rate clients under collections and recovery, collection and recovery strategies, recovery quality indicators, management of collections and recovery channels, rescheduling debt, restructuring transactions, setting negotiating floors and methodologies for dealing with problem credits and/or defaults. The DIRIS focuses on managing the credit risk of aggregate positions. Its main products are: policies, risk limits, credit risk models, information on credit risk,

Risk Management Report

Banco do Brasil S.A. 26

indicators of credit portfolio quality, capital allocation as a function of risk, management of the credit portfolio’s risk, and monitoring of risk versus return.

DICRE DIRAO DIRIS Prepare sector studies and a panorama

Manage default portfolio

Control risk limits for aggregate exposure

Analyze clients and set limits

Develop models and strategies to deal with, collect, and recover problem credits

Determine regulatory capital for credit risk

Analyze credit risk of transactions

Manage collection and recovery channels

Determine economic capital for credit risk

Create and monitor credit-risk methodologies

Propose strategies to pursue debts in higher courts

Manage credit portfolio

Figure 7. Credit-risk management structure

The processes and procedures of the credit-risk management structure are validated and evaluated by two internal units at different points in time, a fact that ensures adequate separation of duties and the independence of work. The Internal Control Board (DICOI) is responsible for validating the financial conglomerate’s risk determination and measurement models and the bank’s internal control system. Internal Audit (AUDIT) periodically evaluates credit-risk management processes to verify whether they are consistent with the strategic guidelines, credit policy, and internal rules. In addition to the units above, independent auditors analyze some of the processes and procedures of credit-risk management, helping to verify whether they are in accordance with regulatory requirements and internal definitions. Communication and Information Processes Disclosure of credit-risk information is a continual and ongoing process. The premises considered when selecting and disclosing information include: best practices, banking laws, user needs, the bank’s interests, confidentiality, and the relevance of the information. The communication and information on credit-risk management is provided to internal and external clients, pursuant to the following processes:

Risk Management Report

Banco do Brasil S.A. 27

Communication process for internal clients The operational units of the credit-risk management structure always communicate with upper management about risk exposure in order to monitor management actions and for executive management to make decisions. The communication process involves several reports on credit-risk management. These documents are produced periodically and are the result of analyses done by professionals from the units. They demonstrate the credit risk of all exposure or in certain portfolios, such as: � Credit Risk Exposure Portfolio Report; � BB vs. SFN Comparison Report (BACEN data); � Bank Comparison Report (accounting data from banks); � Capital Management Report; � Risk-Return Analysis of the Credit Portfolio; � Stress Monitoring Report; and � Risk Panel. Communication process for external clients The operational units of the credit-risk management structure produce information for external users and send it to the Investor Relations Unit (IRU). The IRU discloses this information to the market, as a transparent governance practice, allowing investors and interested parties to monitor risk-management actions and the evolution of credit risk, and to prove the bank’s capital adequacy to cover all of the risks that it has assumed. Information for external users is provided on a publicly accessible location, easily found on the bank’s website. The following documents are published: � Performance Analysis Report; � Notes to the Financial Statements; and � Annual Report.

Measurement Systems Credit risk is measured in many ways: by default, arrears, portfolio quality, allowance for doubtful accounts, concentration, expected losses, and regulatory and economic capital requirements, among others. The quantity and nature of our operations, the diversity and complexity of our products and services, and the volume exposed to credit risk require systematic measurement of credit risk at Banco do Brasil. The bank has enough databases and corporate-system infrastructure to ensure comprehensive measurement of credit risk. Some of these risk measures are highlighted below.

Risk Management Report

Banco do Brasil S.A. 28

Concentration The bank developed and implemented a system to measure and monitor credit-risk concentration in the corporate portfolio. The model is based on the Herfindahl Index. It evaluates concentration based on borrowers’ credit risk, and it considers the interrelationship of the various economic sectors that comprise the corporate credit portfolio. Expected Loss The bank also developed specific methodologies and proprietary systems to determine risk components1 that are used to determine expected loss and economic capital. Expected loss is used in numerous processes and procedures, such as: pricing products and services, verifying allowance levels, and calculating risk-adjusted return on capital (RAROC). In addition, an analysis of historic expected loss provides important information about the behavior of credit risk. Regulatory and Economic Capital Requirements The bank measures the regulatory capital requirements for credit risk through a standard simplified approach, whose procedures for calculating Risk-Weighted Exposure were published by the BACEN in Circular 3.360/07, and updates. These procedures were implemented in a proprietary system that determines the capital requirements quickly and securely, allowing for timely verification of the bank’s solvency under the regulator’s rules. The bank uses regulatory-capital information to assess the efficiency of capital allocation and planning. The bank developed an internal model to measure economic capital whose theoretical foundation is based on an actuarial approach that is now very widely used in the banking industry. Because it was modeled internally, this measure better reflects the risk profile of exposure, which is why it is used managerially in calculating RAROC and in measuring the Herfindahl concentration index. Additionally, the analysis of the historic evolution of economic capital provides important information on capital consumption resulting from exposure of certain clients and/or segments of clients.

1 It is in the refining stage, to comply with regulatory requirements.

Risk Management Report

Banco do Brasil S.A. 29

Mitigation Policy Banco do Brasil has a conservative attitude toward credit risk. When doing any business subject to credit risk, the bank’s general rule is to tie it to a mechanism that will provide partial or complete hedging of the risk incurred. In managing credit risk on the aggregate level, to keep exposure within the risk levels determined by executive management, the bank seeks to transfer or to share credit risk. The use of credit-risk mitigating instruments is stated in the credit policy, present in strategic decisions, and formalized in credit rules, affecting all levels of the organization and covering all stages of credit-risk management. Credit rules provide clear, comprehensive guidelines for the operational units. Among other aspects, the rules address ratings, requirements, choices, assessments, formalization, control, and reinforcement of guarantees, assuring the adequacy and sufficiency of the mitigator throughout the transaction’s cycle. Strategies to Monitor the Effectiveness of Mitigato rs Strategies that monitor the effectiveness of credit-risk mitigation consist of: � continually monitoring credit-risk exposure and comparing the default index with

the level of allowances for exposure, with and without related guarantees; � constantly managing capital and comparing regulatory capital requirements with

economic capital consumption of exposure, with and without related guarantees; and

� periodically evaluating information from collection and recovery of credits and determining which mitigators contribute effectively to exercising the bank’s rights.

Processes for Monitoring the Effectiveness of Mitig ators Monitoring the effectiveness of mitigators is part of the bank’s credit-risk management processes. For example, there are the processes to monitor credit-risk exposure, the risk ratings of credit transactions, capital management, and collections and recovery of credits. The processes of monitoring credit-risk exposure and rating credit-transaction risks produce important information for verifying the effectiveness of mitigating instruments. A low default index in certain segments of the credit portfolio and a low level of allowances in certain transactions may mean that the existence of guarantees tied to exposure is lowering credit risk. The capital management process allows for verifying whether a lower regulatory capital requirement and/or less consumption of economic capital in a given product or service is related to the existence of guarantees tied to exposure to credit risk, lowering the bank’s exposure to credit risk. The process of collecting and recovering credits generates information that enables the bank to verify which mitigating factors were the most important for receiving credits in default and for recovering problem credits, allowing for a revision of the criteria for choosing guarantees, allowances, and capital allocation.

Risk Management Report

Banco do Brasil S.A. 30

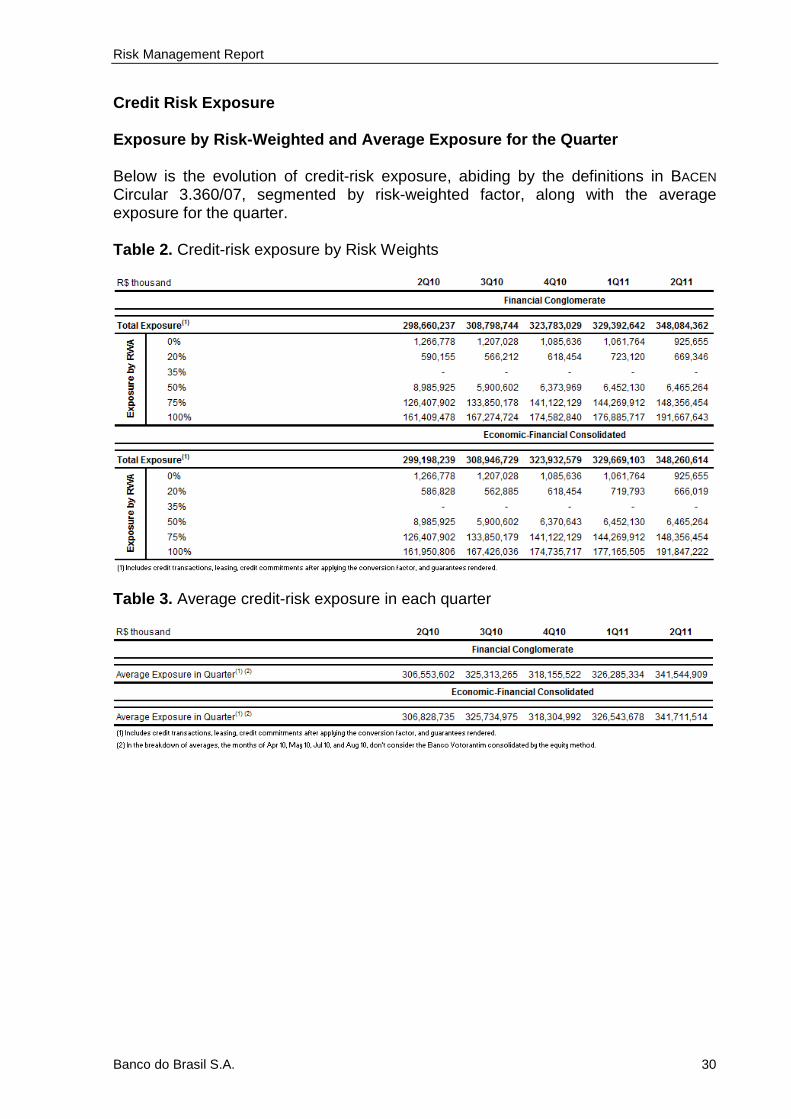

Credit Risk Exposure Exposure by Risk-Weighted and Average Exposure for the Quarter Below is the evolution of credit-risk exposure, abiding by the definitions in BACEN Circular 3.360/07, segmented by risk-weighted factor, along with the average exposure for the quarter. Table 2. Credit-risk exposure by Risk Weights

Table 3. Average credit-risk exposure in each quarter

Risk Management Report

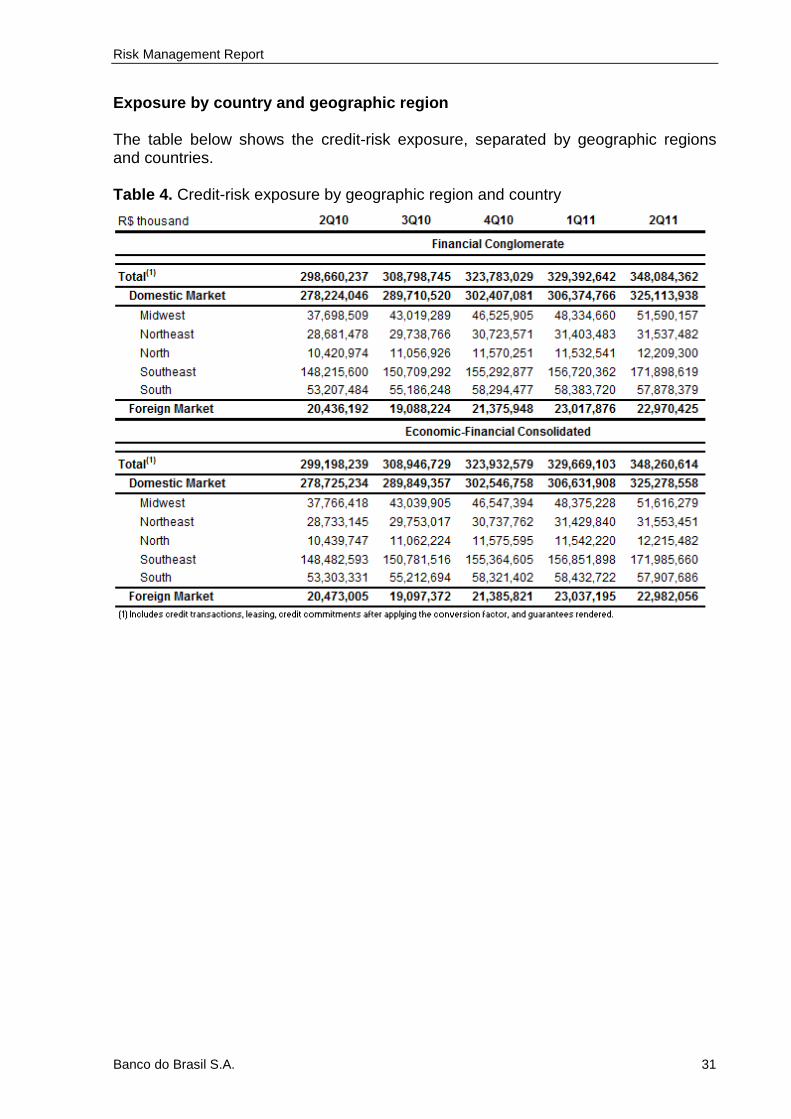

Banco do Brasil S.A. 31

Exposure by country and geographic region The table below shows the credit-risk exposure, separated by geographic regions and countries. Table 4. Credit-risk exposure by geographic region and country

Risk Management Report

Banco do Brasil S.A. 32

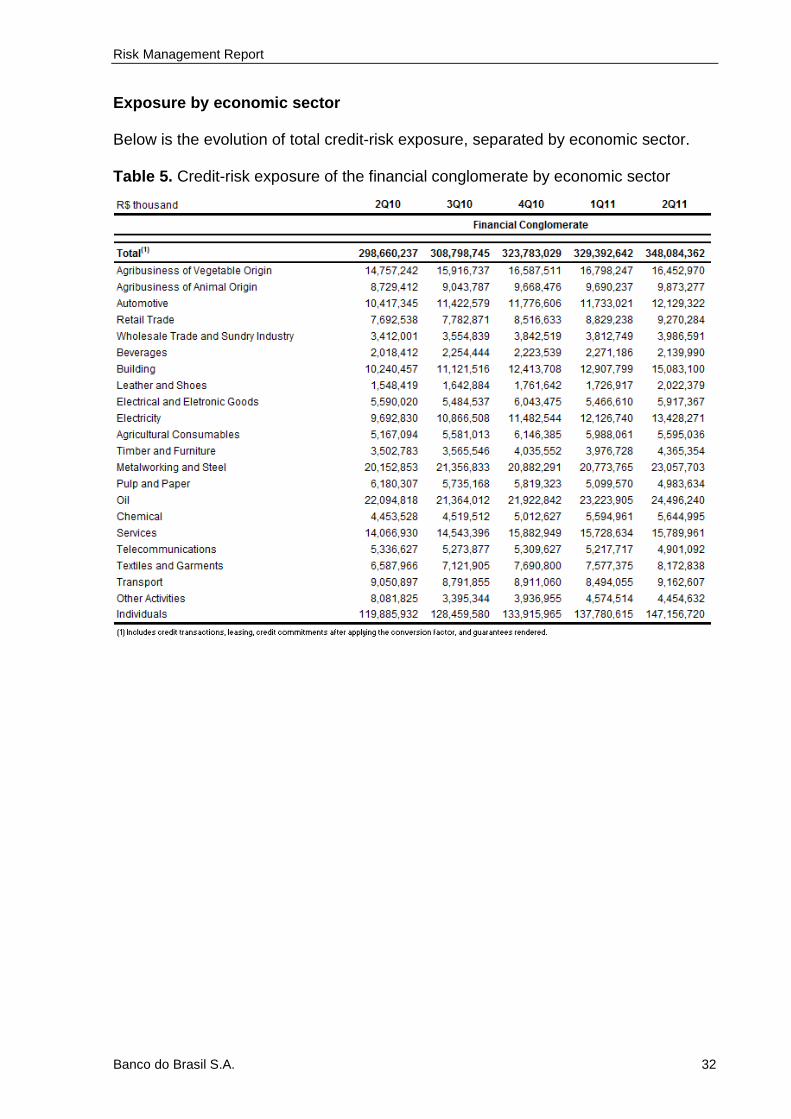

Exposure by economic sector Below is the evolution of total credit-risk exposure, separated by economic sector. Table 5. Credit-risk exposure of the financial conglomerate by economic sector

Risk Management Report

Banco do Brasil S.A. 33

Table 6. Credit-risk exposure of the economic-financial consolidated group by economic sector:

Credit-risk exposure by arrears period The table below shows the portfolio, by arrears period. Table 7. Amount of transactions in arrears

R$ thousand Up to 60 days From 61 to 90 days From 91 to 180 days Over 180 days

2Q10 6,669,589 1,164,539 2,811,537 5,255,302

3Q10 6,275,003 1,347,684 2,894,201 5,407,058

4Q10 5,969,969 1,144,144 3,231,475 4,146,733

1Q11 6,253,704 1,210,927 2,688,850 4,312,166

2Q11 6,081,696 1,293,508 2,961,151 3,883,726

Note: This information covers the branches of BB in Brazil and abroad (BB-Multiple Bank).

Risk Management Report

Banco do Brasil S.A. 34

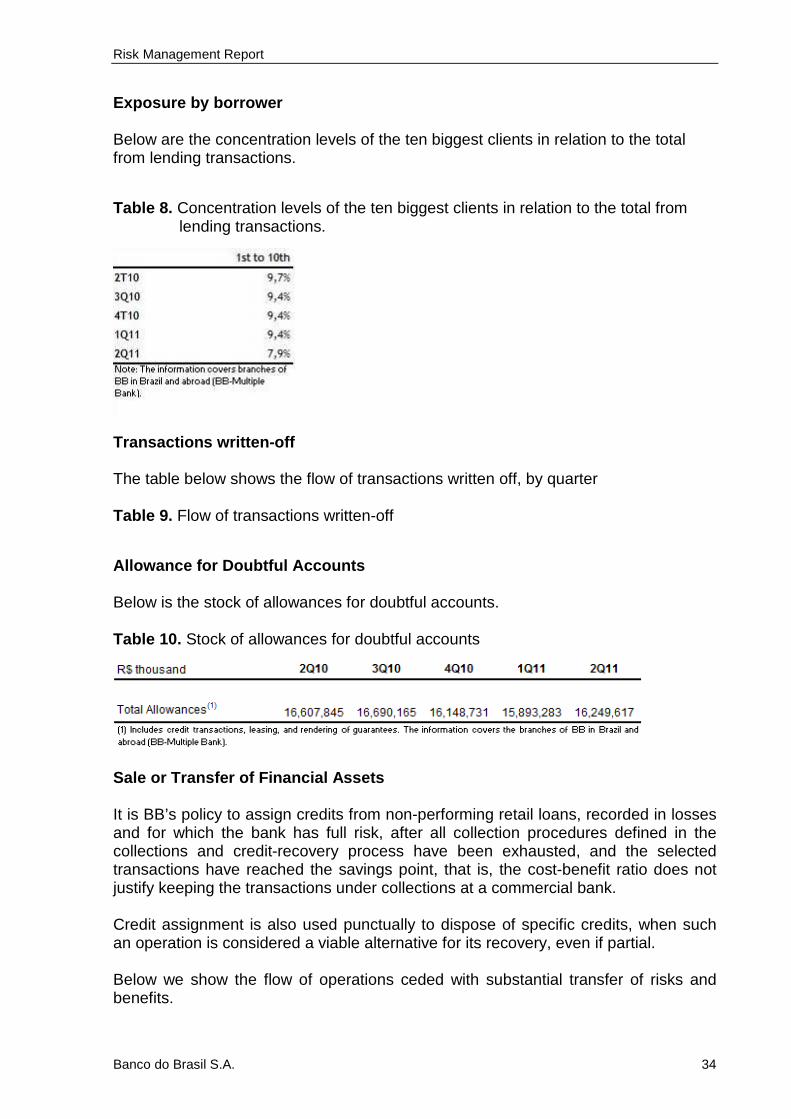

Exposure by borrower Below are the concentration levels of the ten biggest clients in relation to the total from lending transactions.

Table 8. Concentration levels of the ten biggest clients in relation to the total from lending transactions.

Transactions written-off The table below shows the flow of transactions written off, by quarter Table 9. Flow of transactions written-off

Allowance for Doubtful Accounts Below is the stock of allowances for doubtful accounts. Table 10. Stock of allowances for doubtful accounts

Sale or Transfer of Financial Assets It is BB’s policy to assign credits from non-performing retail loans, recorded in losses and for which the bank has full risk, after all collection procedures defined in the collections and credit-recovery process have been exhausted, and the selected transactions have reached the savings point, that is, the cost-benefit ratio does not justify keeping the transactions under collections at a commercial bank. Credit assignment is also used punctually to dispose of specific credits, when such an operation is considered a viable alternative for its recovery, even if partial. Below we show the flow of operations ceded with substantial transfer of risks and benefits.

Risk Management Report

Banco do Brasil S.A. 35

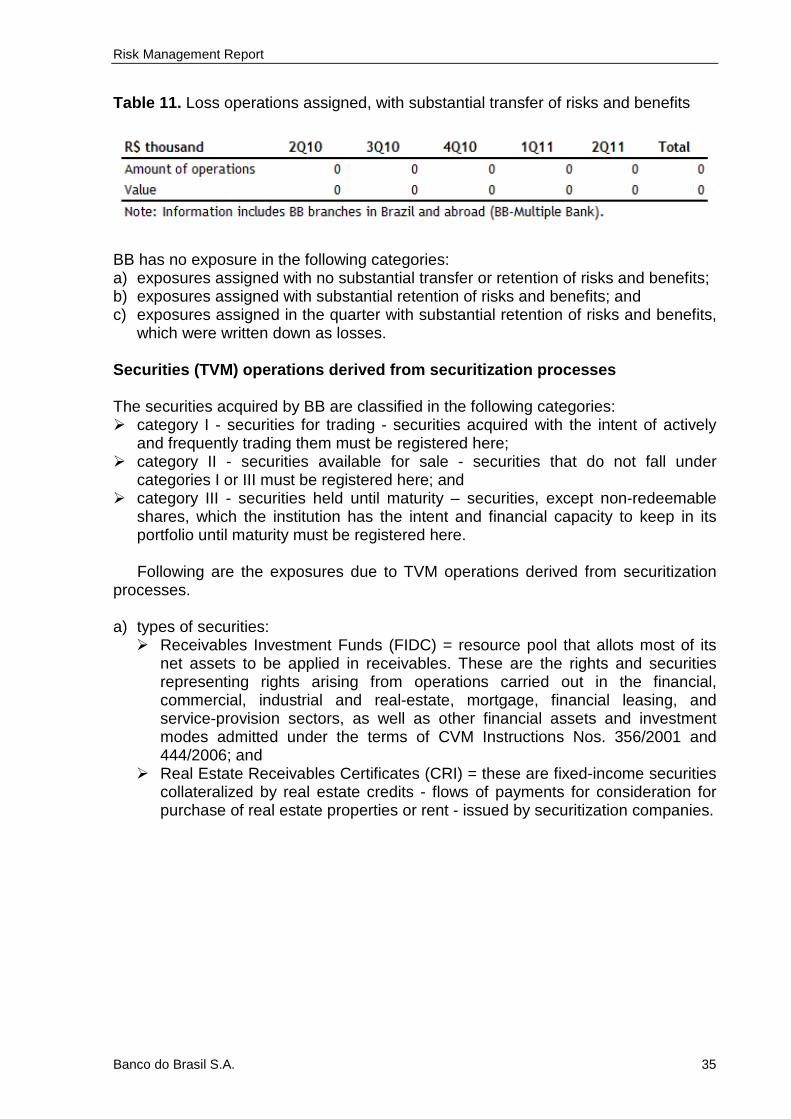

Table 11. Loss operations assigned, with substantial transfer of risks and benefits

BB has no exposure in the following categories: a) exposures assigned with no substantial transfer or retention of risks and benefits; b) exposures assigned with substantial retention of risks and benefits; and c) exposures assigned in the quarter with substantial retention of risks and benefits,

which were written down as losses. Securities (TVM) operations derived from securitiza tion processes The securities acquired by BB are classified in the following categories: � category I - securities for trading - securities acquired with the intent of actively

and frequently trading them must be registered here; � category II - securities available for sale - securities that do not fall under

categories I or III must be registered here; and � category III - securities held until maturity – securities, except non-redeemable

shares, which the institution has the intent and financial capacity to keep in its portfolio until maturity must be registered here.

Following are the exposures due to TVM operations derived from securitization

processes. a) types of securities:

� Receivables Investment Funds (FIDC) = resource pool that allots most of its net assets to be applied in receivables. These are the rights and securities representing rights arising from operations carried out in the financial, commercial, industrial and real-estate, mortgage, financial leasing, and service-provision sectors, as well as other financial assets and investment modes admitted under the terms of CVM Instructions Nos. 356/2001 and 444/2006; and

� Real Estate Receivables Certificates (CRI) = these are fixed-income securities collateralized by real estate credits - flows of payments for consideration for purchase of real estate properties or rent - issued by securitization companies.

Risk Management Report

Banco do Brasil S.A. 36

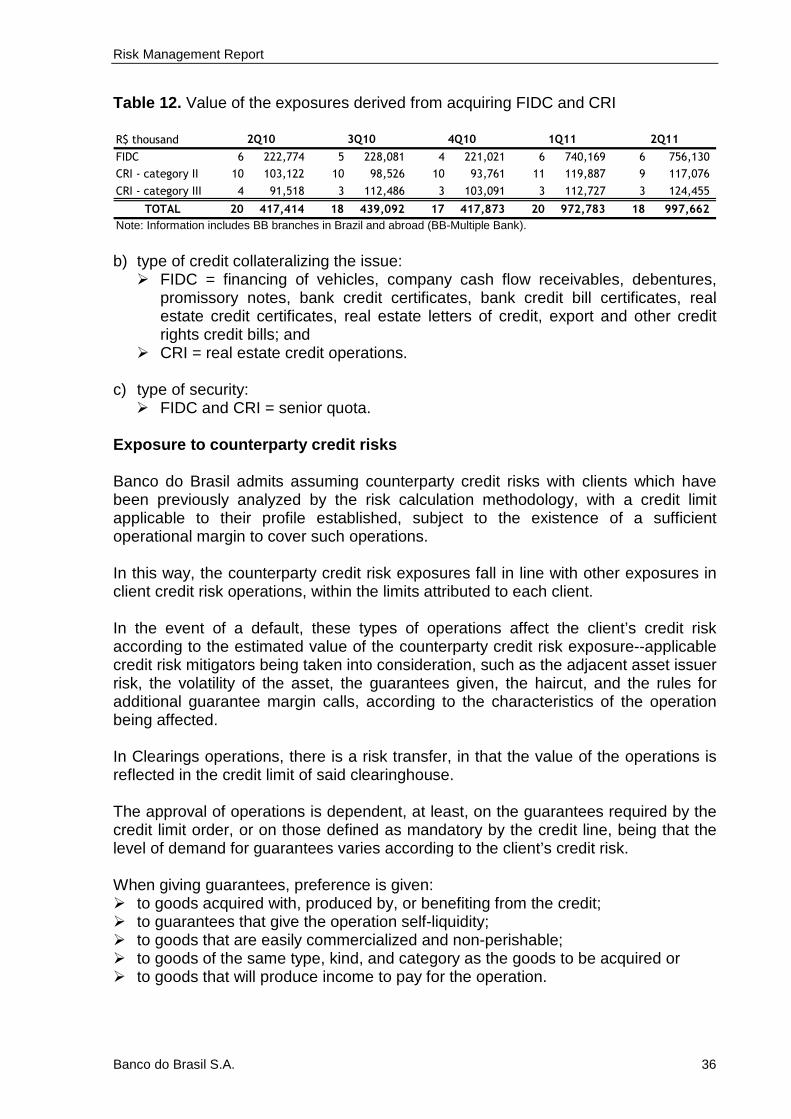

Table 12. Value of the exposures derived from acquiring FIDC and CRI R$ thousand

FIDC 6 222,774 5 228,081 4 221,021 6 740,169 6 756,130

CRI - category II 10 103,122 10 98,526 10 93,761 11 119,887 9 117,076

CRI - category III 4 91,518 3 112,486 3 103,091 3 112,727 3 124,455

TOTAL 20 417,414 18 439,092 17 417,873 20 972,783 18 997,662

Note: Information includes BB branches in Brazil and abroad (BB-Multiple Bank).

4Q10 1Q11 2Q112Q10 3Q10

b) type of credit collateralizing the issue: � FIDC = financing of vehicles, company cash flow receivables, debentures,

promissory notes, bank credit certificates, bank credit bill certificates, real estate credit certificates, real estate letters of credit, export and other credit rights credit bills; and

� CRI = real estate credit operations. c) type of security:

� FIDC and CRI = senior quota. Exposure to counterparty credit risks Banco do Brasil admits assuming counterparty credit risks with clients which have been previously analyzed by the risk calculation methodology, with a credit limit applicable to their profile established, subject to the existence of a sufficient operational margin to cover such operations. In this way, the counterparty credit risk exposures fall in line with other exposures in client credit risk operations, within the limits attributed to each client. In the event of a default, these types of operations affect the client’s credit risk according to the estimated value of the counterparty credit risk exposure--applicable credit risk mitigators being taken into consideration, such as the adjacent asset issuer risk, the volatility of the asset, the guarantees given, the haircut, and the rules for additional guarantee margin calls, according to the characteristics of the operation being affected. In Clearings operations, there is a risk transfer, in that the value of the operations is reflected in the credit limit of said clearinghouse. The approval of operations is dependent, at least, on the guarantees required by the credit limit order, or on those defined as mandatory by the credit line, being that the level of demand for guarantees varies according to the client’s credit risk. When giving guarantees, preference is given: � to goods acquired with, produced by, or benefiting from the credit; � to guarantees that give the operation self-liquidity; � to goods that are easily commercialized and non-perishable; � to goods of the same type, kind, and category as the goods to be acquired or � to goods that will produce income to pay for the operation.

Risk Management Report

Banco do Brasil S.A. 37

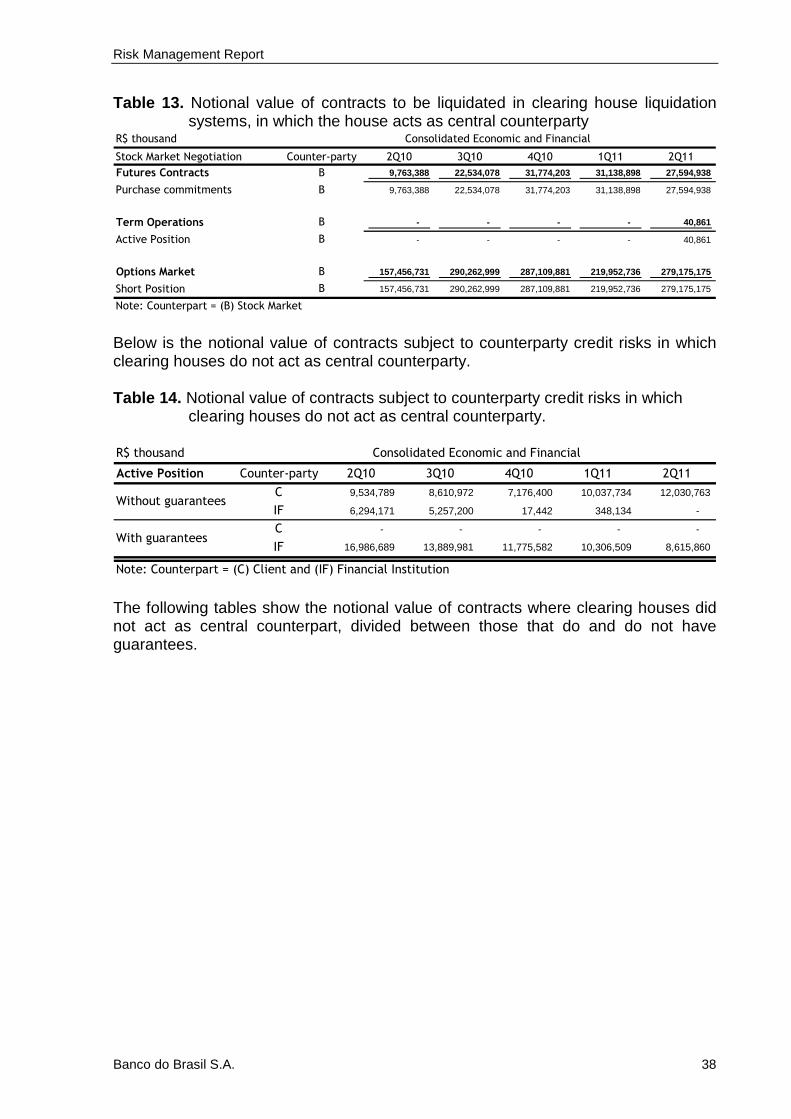

In order to earmark goods as a guaranty, they are valued by a technical appraisal or by an opinion of value, the validity of which is up to twelve months. In the case of a personal guaranty, the economic-financial situation of guarantors or sureties is analyzed, as are the Bank’s direct and indirect liabilities, with debts to third parties being taken into account, especially tax, social welfare, and labor debts. When accepting a good or right as guaranty, the maximum value considered is reached by applying a percentage on the value of said good or right, according to the type and kind of good. In the case of a trade bill or check in custody, the maximum value is obtained by applying the percentage of advance corresponding to the Annual Liquidity Ratio (ILA) of the client’s portfolio on the amount given as a guaranty. Goods received as guaranty in credit operations must be backed until the operation is concluded, or, in the case of funds given as guaranty, remain frozen until the operation is concluded. Guarantees linked to credit operations are registered on a corporate basis, which allows automatic control of the linked goods and rights, and the generation of administrative information, such as the guaranty sufficiency analysis, and an adequacy analysis. For operations subject to counterparty credit risks, Banco do Brasil follows the provisions of BACEN Circular 3,068/01, using such risks as a parameter when adjusting the market value of such exposures, which affects the profit/loss for the period, or a Net Worth highlighted account, subject to the exposure’s classification. Below is the notional value of contracts subject to counterparty credit risks to be liquidated in clearing house liquidation systems, in which the house acts as central counterparty.

Risk Management Report

Banco do Brasil S.A. 38

Table 13. Notional value of contracts to be liquidated in clearing house liquidation systems, in which the house acts as central counterparty

R$ thousand

Stock Market Negotiation Counter-party 2Q10 3Q10 4Q10 1Q11 2Q11

Futures Contracts B 9,763,388 22,534,078 31,774,203 31,138,898 27,594,938

Purchase commitments B 9,763,388 22,534,078 31,774,203 31,138,898 27,594,938

Term Operations B - - - - 40,861

Active Position B - - - - 40,861

Options Market B 157,456,731 290,262,999 287,109,881 219,952,736 279,175,175

Short Position B 157,456,731 290,262,999 287,109,881 219,952,736 279,175,175

Consolidated Economic and Financial

Note: Counterpart = (B) Stock Market Below is the notional value of contracts subject to counterparty credit risks in which clearing houses do not act as central counterparty. Table 14. Notional value of contracts subject to counterparty credit risks in which

clearing houses do not act as central counterparty. R$ thousand

Active Position Counter-party 2Q10 3Q10 4Q10 1Q11 2Q11

C 9,534,789 8,610,972 7,176,400 10,037,734 12,030,763

IF 6,294,171 5,257,200 17,442 348,134 -

C - - - - -

IF 16,986,689 13,889,981 11,775,582 10,306,509 8,615,860

Note: Counterpart = (C) Client and (IF) Financial Institution

Consolidated Economic and Financial

Without guarantees

With guarantees

The following tables show the notional value of contracts where clearing houses did not act as central counterpart, divided between those that do and do not have guarantees.

Risk Management Report

Banco do Brasil S.A. 39

Table 15. Notional value of contracts where clearing houses did not act as central counterparty, and which do not have guarantees.

R$ thousand 2Q10 3Q10 4Q10 1Q11 2Q11

Active Position 25,230,043 26,438,635 23,016,639 22,099,886 25,625,395

22,984,196 22,248,987 21,149,157 20,319,074 21,411,855

Inter-bank deposits 22,242,243 19,453,846 16,428,027 15,323,033 16,619,367

Foreign Currency Investments 741,953 2,795,141 4,721,130 4,996,041 4,792,488

Operations to liquidate in the purchase

and sale of foreign currency, securities,

and gold no in the spot market

1,666,810 2,212,787 86,576 67,421 2,031,195

Currency arbitrage 1,507,810 1,464,881 86,576 67,421 54,163

Inter-bank exchange 159,001 747,906 - - 1,977,032

Operations to liquidate in the purchase

and sale of foreign currency, securities,

and gold in the spot market 579,037 1,976,860 1,780,906 1,713,391 2,182,345

Currency arbitrage 295,486 617,701 610,517 224,719 111,669

Inter-bank exchange 283,551 1,359,159 1,170,389 1,488,672 2,070,676

Financial Conglomerate

Table 16. Notional value of contracts where clearing houses did not act as central

counterparty, and which do have guarantees.

R$ thousand 2Q10 3Q10 4Q10 1Q11 2Q11

Long position 101,515,736 101,781,289 78,507,871 117,081,032 115,395,029

Repos donated 101,515,736 101,781,289 78,507,871 117,081,032 115,395,029

Short position – without brokerage 246,617,835 244,919,234 198,978,917 276,706,385 283,758,964

Repos taken – own and third-party portfolios 146,723,571 144,939,574 120,614,973 159,780,091 166,064,996

Repurchase agreements “repos” (Brokerage) 99,894,264 99,979,660 78,363,944 116,926,294 117,693,968

Operations to liquidate in the purchase and sale

of foreign currency, securities, and gold no in

the spot market - - - - 15,230

Inter-bank exchange - - - - 15,230

Operations to liquidate in the purchase and sale

of foreign currency, securities, and gold in the

spot market 1,205,551 212,973 502,200 3,583,018 207,049

Inter-bank exchange 1,205,551 212,973 502,200 3,583,018 207,049

Financial Conglomerate

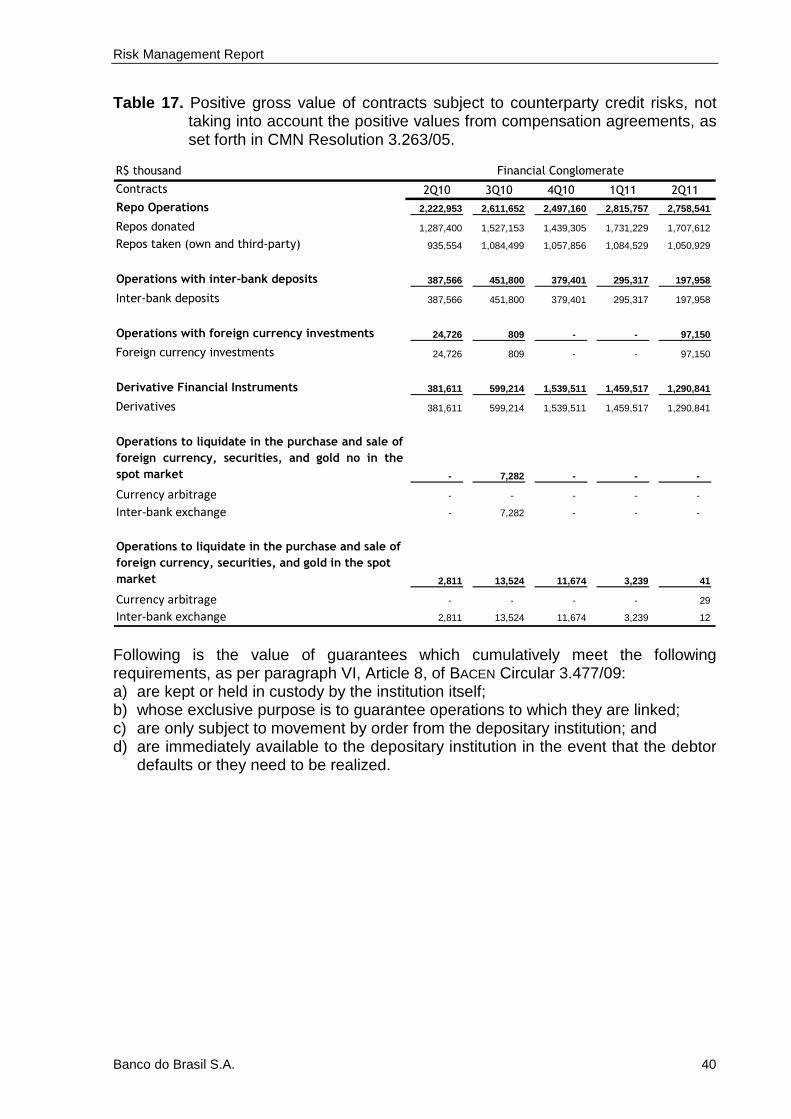

The following table shows the positive gross value of contracts subject to counterparty credit risks, including derivatives, outstanding operations, asset loans and repo transactions, not taking into account the positive values from compensation agreements, as set forth in CMN Resolution 3.263/05.

Risk Management Report

Banco do Brasil S.A. 40

Table 17. Positive gross value of contracts subject to counterparty credit risks, not taking into account the positive values from compensation agreements, as set forth in CMN Resolution 3.263/05.

R$ thousand

Contracts 2Q10 3Q10 4Q10 1Q11 2Q11

Repo Operations 2,222,953 2,611,652 2,497,160 2,815,757 2,758,541

Repos donated 1,287,400 1,527,153 1,439,305 1,731,229 1,707,612

Repos taken (own and third-party) 935,554 1,084,499 1,057,856 1,084,529 1,050,929

Operations with inter-bank deposits 387,566 451,800 379,401 295,317 197,958

Inter-bank deposits 387,566 451,800 379,401 295,317 197,958

Operations with foreign currency investments 24,726 809 - - 97,150

Foreign currency investments 24,726 809 - - 97,150

Derivative Financial Instruments 381,611 599,214 1,539,511 1,459,517 1,290,841

Derivatives 381,611 599,214 1,539,511 1,459,517 1,290,841

Operations to liquidate in the purchase and sale of

foreign currency, securities, and gold no in the

spot market - 7,282 - - -

Currency arbitrage - - - - -

Inter-bank exchange - 7,282 - - -

Operations to liquidate in the purchase and sale of

foreign currency, securities, and gold in the spot

market 2,811 13,524 11,674 3,239 41

Currency arbitrage - - - - 29

Inter-bank exchange 2,811 13,524 11,674 3,239 12

Financial Conglomerate

Following is the value of guarantees which cumulatively meet the following requirements, as per paragraph VI, Article 8, of BACEN Circular 3.477/09: a) are kept or held in custody by the institution itself; b) whose exclusive purpose is to guarantee operations to which they are linked; c) are only subject to movement by order from the depositary institution; and d) are immediately available to the depositary institution in the event that the debtor

defaults or they need to be realized.

Risk Management Report

Banco do Brasil S.A. 41

Table 18. The value of guarantees which cumulatively meet the requirements of paragraph VI, Article 8, of Bacen Circular 3.477/09:

R$ thousand 2Q10 3Q10 4Q10 1Q11 2Q11

Financial investments – fixed-income Checks 3,062,957 2,953,887 3,340,184 3,219,978 3,402,271

Checks 423,334 537,538 616,925 630,871 702,033

Agricultural products – with warrant 97,610 87,897 81,524 86,972 56,206

Financial investments – variable yield 137 130 875 926 155

TOTAL 3,584,039 3,579,451 4,039,509 3,938,746 4,160,666

Note: Information includes BB branches in Brazil and abroad (BB-Multiple Bank). According to the classification of types of guarantees adopted by the BACEN, we have identified those which cumulatively meet the conditions established in BACEN Circular 3.477/09, being that for this calculation we have considered the value committed as guaranty to the linked operation. BB has no compensation and liquidation of obligations agreements, as defined in CMN Resolution 3.263/05. The table below shows the notional value of credit derivatives, divided by type of operation. Table 19. Notional value of credit derivatives

R$ thousand 2Q10 3Q10 4Q10 1Q11 2Q11

Active Position – Transferred Risk 1,582,618 1,392,181 1,012,217 2,524,485 1,789,802

Credit swaps – derivatives with banks 1,582,618 1,392,181 1,012,217 2,524,485 1,646,961

Others - - - - 142,841

Passive Position – Risk Received 4,229,514 2,911,541 1,759,596 2,524,485 723,188

Credit swaps – derivatives with banks 4,229,514 2,911,541 1,759,596 2,524,485 655,662

Others - - - - 67,526

Consolidated Economic and Financial