12 June 2008 • Park Hyatt • Johannesburg, South Africa Risks and Opportunities in the Emerging Economic Landscape of Africa Karanta Kalley Regional Managing Director, Africa Group Global Insight

Transcript

12 June 2008 • Park Hyatt • Johannesburg, South Africa

Risks and Opportunities in theEmerging Economic Landscape of Africa

Karanta KalleyRegional Managing Director, Africa Group

Remittances Rose Sharply in 2006• Sub-Saharan Africa received US$20 billion (UN)

• Surge in growth was largely the result of:– Globalization spurred by economic liberalization

– Reduction in average transmission costs

• Boosted migrants’ disposable incomes and their incentive to remit

• Macro level: remittances are more stable than FDI, official aid or export revenues

• Remittances have a multiplier effect through increased household consumption and investment in human capital, such as education, in healthcare and better nutrition

• Main role: Stimulate consumption and investment and contribute to poverty alleviation

...But there are Risks at the Regional Level As Well• Risks:

– Poor infrastructure– Growth, though increasing, still remains insufficient– Excessive reliance on primary commodity exports– External debt still remains high and private capital flows

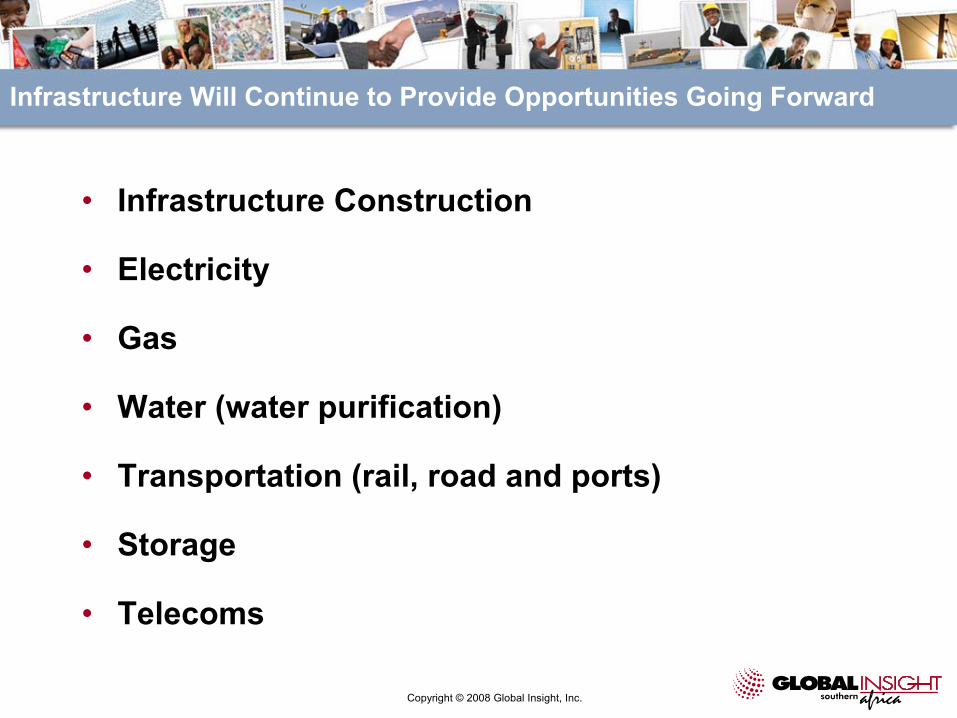

are insufficient– Disbursements of external development financing fall

short of commitments– Domestic savings as a percent of GDP remains low– Political risk, though declining, remains high– HIV-Aids, both an immediate crisis and a long-term

systemic challenge with profound consequences for the region

• However, some major developments point to a positive direction

• A favorable global environment, prudent economic policies, good governance and political stability will bode well for socio-economic development, going forward

• We are beginning to see some light at the end of the tunnel. If Africa and its partners do not take constructive advantage of this situation, the light we see will just be another flicker in the tunnel