The Islamic law (Shariah) prohibits the charging and paying of interest. There-fore, in countries where Muslim populations constitute an important segment ofthe society, considerations for Islamic law have recently hampered the advance-ment of competent systems for monetary control (Sundararajan, Martson, &Ghiath, 1998). Hence, governments as well as corporate entities seekingresource mobilization and debt management necessitate the development ofalternatives to traditional debt markets that can be acceptable by Islamic law.

Ali Arsalan Tariq is a senior consultant with the Islamic Financial Services Group at Ernst & Youngin Bahrain. He specializes in rendering strategic advisory services to Islamic financial institutions.During his time with Ernst & Young, he has contributed to various strategic consultancy assign-ments, including preparing feasibility studies for new financial institutions as well as documentingenterprisewide strategies for existing ones. He is a graduate of McGill University in Canada and alsoholds a master’s degree from Loughborough University in the United Kingdom [[email protected][email protected]].Humayon Dar is the vice-president of Dar al Istithmar, a London-based subsidiary of Deutsche Bankand a global think tank for Islamic finance. Previously, he was a lecturer in the Department of Eco-nomics at Loughborough University and an assistant professor and head of the economics depart-ment at the Lahore College of Arts and Sciences, and a visiting lecturer at the Imperial College ofBusiness Studies, Lahore, and the Markfield Institute of Higher Education. Dr. Dar holds a BS andMS in economics from the International Islamic University, Islamabad, Pakistan, and received anM.Phil in 1992 and a PhD in 1997 from the University of Cambridge, England. He has publishedwidely in Islamic banking and finance [[email protected]].

Thunderbird International Business Review, Vol. 49(2) 203–223 • March–April 2007

Published online in Wiley InterScience (www.interscience.wiley.com).

Recently, there has been a rapid growth of a thriving multibillion-dol-lar market in Shariah-compliant sovereign and corporate Islamicstructured financial instruments known as sukuk. Generally, sukuk areasset-backed, stable income, tradable and Shariah-compatible trustcertificates. The primary condition for the issuance of sukuk is theexistence of assets on the balance sheet of the government, the mon-etary authority, the corporate body, the banking and financial institu-tion, or any entity that wants to mobilize their financial resources. Asof 2006, the total worth of sukuk in issue globally is estimated to beover $25 billion. Sovereign issuers include Bahrain, Malaysia, Qatar,and Saxony-Anhalt in Germany. Hence, the sukuk are emerging as avery important vehicle for resource mobilization. However, the min-imum investment requirements of the sukuk issues are often verylarge, and mainly institutional and high net worth investors havebeen able to participate in such investment opportunities. The effec-tiveness of sukuk as an efficient tool for resources mobilization can beenhanced, provided these can be accessible to the general public withfeasibly minimum amounts of investment requirements.

Significant ideas are covered in Haque and Abbas (1999), Kahf(1997), Elgari (1997), and Zarqa (1997) with regard to public-sec-tor financing in Islamic economies. Also, Al-Suwailem (2000) and El-Gamal (2000) scrutinize the functionality of uncertainty within therealm of Islamic finance that will become a focal point of the feasibil-ity of Islamic risk management mechanisms in this research. Theobjective of this study is to assess the sukuk structures and analyze thevarious risks underlying the Islamic sovereign and corporate sukukstructures. The article contrasts the risks underlying traditional fixed-income instruments and those underlying the sukuk structures. Wealso aim to suggest Shariah-compatible frameworks that can replicatethe functions of interest-rate swaps and derivatives in managing therisks of sukuk.

The success and popularity of the sukuk framework as an alternativeasset management platform will invariably require inbuilt mecha-nisms that can be instrumental in mitigating risks that exist in thestructures due to their fixed pricing features as well as their bench-marking with market references such as the London Interbank OfferRate (LIBOR). This phenomenon will be investigated in the light ofthe unique requirements of Islamic finance. Ultimately, the aim is toput together sukuk structures that can be competitive without uti-lizing derivatives, making sukuk an efficient channel of resourcemobilization.

Ali Arsalan Tariq ■ Humayon Dar

204 Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

The objective ofthis study is toassess thesukuk structuresand analyze thevarious risksunderlying theIslamicsovereign andcorporate sukukstructures.

EVOLUTION AND PROFILE OF SUKUK STRUCTURES ANDMARKETS

Types of SukukThe proper classification of the asset classes will also determine thetype of certificates to be issued. It is imperative to note that theseassets can be prepared for the issuance of trust certificates in a num-ber of ways conditional to the need of the issuing entity. TheAccounting and Auditing Organization for Islamic Financial Institu-tions (AAOIFI) has extensively outlined the various asset classes thatcan form the base for sukuk certificates (see AAOIFI, 2002).

Pure Ijarah SukukThese certificates are issued on stand-alone assets that are identifiedon the balance sheet. The assets can be parcels of land or fixed assetsto be leased such as aircrafts and ships. The rental rates of returns onthese sukuk can either be fixed or floating depending on the particu-lar originator.

Hybrid/Pooled SukukThe underlying pool of assets can consist of istisna, murabahah, andijarah receivables. Indeed, having a portfolio of assets composed ofdifferent classes allows for a greater mobilization of funds as previ-ously inaccessible murabahah and istisna assets can comprise a port-folio. However, at least 51% of the pool must be composed of ijarahassets. Due to the fact that the murabahah and istisna receivables arepart of the pool, the return on these certificates can only be a prede-termined fixed rate of return.

Variable Rate Redeemable SukukIn some circumstances, implementing sukuk by representing the fullstrength of an issuer’s balance sheet can prove to be beneficial. Sev-eral corporate entities refer to these sukuk as Musharakah TermFinance Certificates (MTFCs). These can be considered as an alter-native to sukuk because of their seniority to the issuer’s equity, theirredeemable nature, and their relatively stable rate as compared to div-idend payouts. MTFCs have two main advantages. First, employingmusharakah returns is preferred from the viewpoint of jurists, as suchan arrangement would strengthen the paradigm of Islamic bankingthat considers partnership contracts as the embodiment of core ide-als. Second, the floating rate of return on these certificates would notdepend on benchmarking with market references such as LIBOR butwould instead be contingent on the firm’s balance-sheet actualities.

Risks of Sukuk Structures: Implications for Resource Mobilization

205Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

In some circum-stances, imple-menting sukuk

by representingthe full strength

of an issuer’sbalance sheet

can prove to bebeneficial.

Fixed-Rate Zero-Coupon SukukAnother possible classification of sukuk structures can be createdwhere the assets to be mobilized do not yet exist. Consequently,the objective of the fund mobilization would be to create moreassets on the balance sheet of company through istisna. However,certificates of this nature would not readily be tradable because ofShariah restrictions (see Usmani, 2002). The primary asset poolsto be generated would be of a nature warranted by istisna andinstallment purchase/sale contracts that would create debt obliga-tions.

Assessment of Sukuk Structures The market for sukuk has injected a much-needed scope for liquiditymanagement in Islamic banks. Previously, such liquidity could onlybe secured through continuous murabahah transactions (Vogel &Hayes III, 1998). In a global market where conventional financedominates, liquidity could only be acquired by transactions limited tospecific Shariah-acceptable commodities such as industrial goods,metals, and oils. The process of issuing sukuk certificates allowsIslamic financial institutions to garner a much wider asset pool thatwas previously either inaccessible or inefficient.

However, some of the corporate and sovereign sukuk prospectuseshave come under increased scrutiny for their Shariah suitability. Thepredominant feature of several of the prospectuses is the floating-ratereturn distributed to the certificate holders. The market referenceused is the LIBOR, over which a competitive premium is added.However, it should be observed that in the case of the ijarah sukukarrangements, LIBOR serves as a market reference for the returns,and the intrinsic distributions arise from the rentals pertaining to theleasing arrangements with the originator and Special Purpose Vehicle(SPV).

The sukuk issuance by the Islamic Development Bank (IDB) servesas an excellent and promising example for future arrangements.The prospectus contained clear and precise Shariah considerationsoutlined by numerous leading scholars and it involved an innova-tive portfolio combination of ijarah, murabahah, and istisna pro-jects. Also, the returns on the sukuk were agreed upon a fixed rateof return on the underlying assets rather than being benchmarkedto LIBOR.

One dimension of the paradigm of Islamic finance that should not belost upon compromises for increased profitability is altruism. In this

Ali Arsalan Tariq ■ Humayon Dar

206 Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

The process ofissuing sukukcertificatesallows Islamicfinancial institu-tions to garner amuch widerasset pool thatwas previouslyeither inaccessi-ble or inefficient.

regard, the sukuk prospectuses have not only mobilized previouslyuntapped public-sector funds, but have also introduced long-soughtfunding for development projects. The Qatar issuance funded a largemedical complex (Hamad Medical City) in Doha, and the Malaysiansukuk certificates raised funds for several government-owned hospi-tals as well as offices. Most significantly, the IDB sukuk prospectusesraised funds for projects in 21 developing nations in a wide range ofschemes that included power transmissions, hospitals, steel manufac-turing, mineral water networks, livestock breeding, seaport develop-ment, pharmacology research, agricultural irrigation, telecommuni-cations projects, rural development, and colleges.

Table 1 collects a sample of recent developments in sukuk markets.

Basic Structure of Existing SukukThere are variations of the sukuk structure, but the basic arrangementis outlined in Figure 1. Fundamentally, there are three parties to asukuk arrangement: the originator of the sukuk (the obligor), theSpecial Purpose Vehicle who is the issuer of the sukuk certificates, andthe investors that buy these certificates.

The originator of the sukuk holds the assets that are intended to beleased to form the rental payments that are the basis of the returns tothe sukuk holder. He is thus obliged to guarantee these payments.The SPV is created by the originator of the certificates and is desig-nated as a separate independent legal entity. The originator sells theassets to the SPV and then leases it back under a term-specified con-tract. The SPV securitizes the assets by issuing sukuk certificates forsale to potential investors. These sukuk notes represent undividedshares in ownership of tangible assets, and the SPV takes on the func-tion of handing over the rent collected from the originator to theinvestor.

1. Originator sells assets to be leased to the SPV.2. Originator receives payment for assets sold.3. The SPV leases assets back to the originator.4. The SPV receives rent payments from the originator under a

term-specified contract.5. The SPV collects funds from the issuances of sukuk certificates

to finance the purchase of assets from the originator.6. The SPV utilizes the rent payments from the originator to dis-

burse distributions on the sukuk certificates.7. Investors (both conventional and Islamic) secure the sukuk

certificates.

Risks of Sukuk Structures: Implications for Resource Mobilization

207Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

Fundamentally,there are three

parties to asukuk arrange-

ment: the origina-tor of the sukuk(the obligor), theSpecial Purpose

Vehicle who isthe issuer of the

sukuk certifi-cates, and the

investors that buythese certificates.

Ali Arsalan Tariq ■ Humayon Dar

208 Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

Tab

le 1

. Sam

ple

Rec

ent

Dev

elop

men

ts in

Su

kuk

Mar

kets

Nam

e of

Ija

rah

Suku

kT

ype

Am

ount

M

atur

ity

Pric

ing

Gut

heri

e C

o. M

alay

sian

Glo

bal

Firs

t, M

alay

sia

Cor

pora

te

US$

150

M

5 ye

ars

Floa

ting

refe

renc

e ra

te o

n un

derl

ying

Ija

rah

Mal

aysi

an G

loba

l Ija

rah

Suku

k So

vere

ign

U.S

.$50

0 M

7

year

s Fl

oatin

g re

fere

nce

rate

on

unde

rlyi

ng I

jara

h Q

atar

Glo

bal I

jara

h Su

kuk

Sove

reig

n U

.S.$

700

M

7 ye

ars

Floa

ting

refe

renc

e ra

te o

n un

derl

ying

Ija

rah

Tab

reed

Glo

bal I

jara

h Su

kuk

Cor

pora

te

U.S

.$15

0 M

5

year

s Fl

oatin

g re

fere

nce

rate

on

unde

rlyi

ng I

jara

h Su

kuk

Al I

ntifa

a M

akka

h, S

audi

Ara

bia

Cor

pora

te

U.S

.$39

0 M

24

yea

rs

Sale

of u

sufr

uct

righ

ts a

s w

eekl

y tim

e sh

ares

Ij

arah

Suk

uk S

axon

y-A

nhal

t, G

erm

any

Sove

reig

n E

uro

100

M

5 ye

ars

Floa

ting

refe

renc

e ra

te o

n un

derl

ying

Ija

rah

Dub

ai D

epar

tmen

t of

Civ

il A

viat

ion

(DC

A)

Ijar

ah S

ukuk

C

orpo

rate

U

.S.$

1 B

5

year

s Fl

oatin

g re

fere

nce

rate

on

unde

rlyi

ng I

jara

h Si

tara

Mus

hara

kah

Ter

m F

inan

ce, P

akis

tan

Cor

pora

te

Pak

Rup

ees

360

M5

year

s Fi

xed

rate

on

prof

itsSu

dane

se G

over

nmen

t In

vest

men

t Su

kuk

Sove

reig

n SD

6

B2

year

s Fi

xed

rate

on

prof

itsSo

lidar

ity T

rust

Cer

tific

ates

Isl

amic

D

evel

opm

ent

Ban

k (I

DB

) C

orpo

rate

U

.S.$

400

M

5 ye

ars

Fixe

d-ra

te r

etur

n ID

BC

orpo

rate

U.S

.$50

0 M

5 ye

ars

Fixe

d-ra

te r

etur

nPa

kist

ani I

nter

natio

nal S

ukuk

Gov

ernm

ent

U.S

.$60

0 M

5 ye

ars

Floa

ting-

rate

ret

urn

Am

ple

Zon

e B

erha

d, M

alay

sia

Cor

pora

teR

M 1

50 M

2 to

7 y

ears

Fixe

d-ra

te r

etur

nD

ubai

Glo

bal S

ukuk

, UA

ESo

vere

ign

U.S

.$1

B5

year

sFl

oatin

g-ra

te r

etur

nSa

raw

ak G

loba

l Suk

uk, M

alay

sia

Sove

reig

nU

.S.$

350

M5

year

sFl

oatin

g-ra

te r

etur

nIn

gres

s Su

kuk

Bar

had,

Mal

aysi

aC

orpo

rate

RM

160

M3

year

sFi

xed

rate

ret

urn

Firs

t Is

lam

ic I

nves

tmen

t B

ank,

Bah

rain

Cor

pora

teE

uro

76 M

2 ye

ars

Floa

ting

rate

ret

urn

Em

aar,

UA

EC

orpo

rate

U.S

.$65

M5

year

sFl

oatin

g ra

te r

etur

nB

ahra

in M

onet

ary

Age

ncy

(BM

A),

Bah

rain

Sove

reig

nT

otal

V

ario

usM

ajor

ity is

suan

ces

fixed

rat

e re

turn

U.S

.$97

0 M

Min

3,

One

issu

ance

floa

ting

rate

ref

eren

ceM

ax 1

0 ye

ars

Sour

ce: C

alcu

late

d fr

om L

iqui

dity

Man

agem

ent

Cen

tre

Web

site

(ht

tp:/

/w

ww

.lmcb

ahra

in.c

om/

Glo

bal-

tabl

e.as

p) a

nd v

ario

us S

ukuk

pro

spec

tuse

s (s

ee, f

or e

xam

ple,

Mal

aysi

an G

loba

l Fir

st I

jara

hSu

kuk,

200

1; M

alay

sian

Glo

bal I

nc.,

2002

; Qat

ar G

loba

l Suk

uk, 2

003;

and

Tab

reed

Fin

anci

ng C

orpo

ratio

n (2

004)

.

8. The investors are reimbursed periodically by the distributionsfrom the SPV, which are funded by the originator’s rental pay-ments on the leased assets.

At the expiry of the term of the sukuk (and lease of the assets), theownership of the asset would reside with the collective sukuk holders,and they would then realize a capital gain or loss on this assetdepending on its market value at the time. It follows that the costs offinancing incurred by the originator would be higher if the assetsunder question have no viable market. Often, the originator may notbe willing to part with the assets upon maturity of the contract, andso the closure of the sukuk contract would include a stipulation stat-ing the originator’s willingness to buy back the assets at their facevalue.

The SPV is generally designated to be a stand-alone entity that isbankruptcy remote from the originator. However, there may be anotion of settlement risk involved with the SPV in that the originatorwill have to channel the payments through a clearinghouse. The cer-tificate holders will then be reimbursed through the clearinghouse.

RISKS UNDERLYING SUKUK STRUCTURES

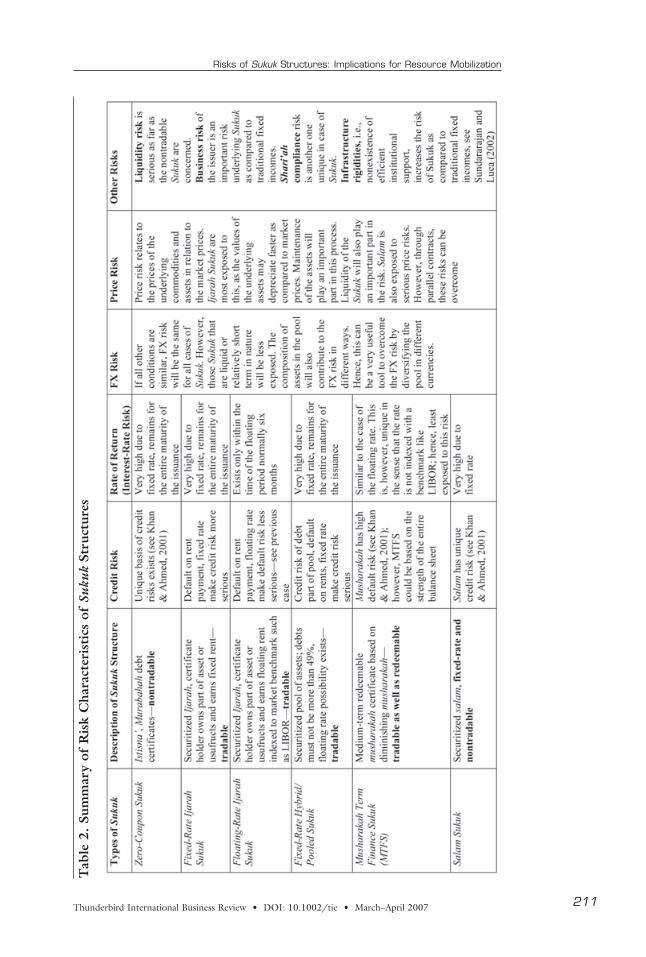

The novelty of sukuk inherently entails a higher exposure to certainmarket and financial risks. In this section, we will discuss the natureof the different risks that the sukuk arrangements are confrontedwith, as summarized in Table 2.

Risks of Sukuk Structures: Implications for Resource Mobilization

209Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

Figure 1. Generic Arrangement of Sukuk Structure

Market Risks Rate of Return Risk Sukuk based on fixed rates are exposed to this risk in the same man-ner as fixed-rate bonds are exposed to interest-rate risk. The rise inmarket interest rates leads to a fall in the value of fixed-income sukuk.There is also a dimension of reinvestment risk and the opportunitycost of investing at the new rate, particularly if the asset is not liquid,as in case of the zero-coupon nontradable sukuk.

Sukuk certificates are indirectly exposed to interest-rate fluctuationsthrough the widespread benchmarking with LIBOR in their financ-ing operations. For example, the markup is a defining characteristicof the murabahah contract that is the most popular Islamic financialinstrument on the asset side of the balance sheet (Vogel & Hayes III,1998). Every contract benchmarked with LIBOR inherits the possi-bility that in the future the LIBOR rates will rise and that the issuer,on the asset side, will not have made as much profit as future marketconditions might dictate. Interlinked is the liabilities side of theissuer’s balance sheet that has provisions for adjusting to market con-ditions. The sukuk issuers will have to respond to fluctuations inLIBOR because any increase in earnings will have to be jointly withthe investors. However, on the asset side, the repricing of muraba-hah contracts is not possible, as debts are nontradable in Islamicfinance (Usmani, 2002, pp. 17–18). Therefore, we have a situationwhere murabahah contracts expose the issuer as well as the buyer ofthe issuance to a considerable interest-rate risk, albeit indirectly.Some of the sukuk issuances, such as the IDB trust certificates, havean underlying portfolio of assets that include murabahah receivables,rendering the whole issuance indirectly exposed to an interest-raterisk.

The underlying assets of the sukuk certificates are subject to numer-ous risks as well. Primarily, there is the risk of loss of the assets. Theseare minimal with regard to ijarah assets of land parcels. However, inthe case of equipment and large-scale construction typifying some ofthe underlying IDB assets, the risk of loss may not be so negligible.Nevertheless, Islamic finance has Shariah-compliant provisions forinsurance claims in the form of takaful, and these arrangements willhave to be utilized to mitigate the risks of asset losses. Also, there isthe need to maintain the structures of the assets. Proper maintenancewill ensure adequate returns to the certificate holder. According toShariah principles, the SPV will usually be required to bear theresponsibilities on ensuring asset structure maintenance (AAOIFI,2002).

Ali Arsalan Tariq ■ Humayon Dar

210 Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

Islamic financehas Shariah-compliant provi-sions for insur-ance claims inthe form of taka-ful, and thesearrangementswill have to beutilized to miti-gate the risks ofasset losses.

Risks of Sukuk Structures: Implications for Resource Mobilization

211Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

Tab

le 2

. Sum

mar

y of

Ris

k C

hara

cter

isti

cs o

f Su

kuk

Stru

ctur

es

Foreign Exchange-Rate Risks Currency risk arises from unfavorable exchange-rate fluctuations,which will undeniably have an effect on foreign exchange positions.In the event of a divergence between the unit of currency in whichthe assets in the sukuk pool are denominated and the currency ofdenomination in which the sukuk funds are accumulated, the sukukinvestors are rendered to an exchange-rate risk. A clear manifestationof this situation arises with the IDB prospectus. The unit of accountof the IDB is an Islamic Dinar (ID), and is equivalent to one SpecialDrawing Right (SDR) of the International Monetary Fund that isweight-composed of 45% in U.S. dollars, 29% in euros, 15% inJapanese yen, and 11% in British pounds. However, the sukuk certifi-cates are denominated in U.S. dollars, and consequently there is acurrency mismatch. Although during the initial sukuk issuances, thismismatch has resulted in a profit for the IDB because of the weaknessof the U.S, dollar relative to the Islamic Dinar, any appreciation ofthe U.S. dollar against the ID will invariably result in a currency loss.

The IDB serves as a guarantor and thus protects the investors fromany exchange-rate fluctuations. Indeed, the investors in all the sukukprospectuses are shielded through similar provisions. However, thisdoes not eliminate the exchange risk faced by the originators. Intruth, exchange-rate risks are compounded with a rapidly growingindustry and increasingly multinational investment arrangements.The challenge for sukuk-issuing corporate entities and sovereignsbecomes to devise an effective exchange risk management strategycongruent to Shariah principles.

Credit and Counterparty Risk Credit risk refers to the probability that an asset or loan becomesirrecoverable due to a default or delay in settlements. Chapra andKhan (2000), Khan and Ahmed (2001), and El-Hawary, Grais, andIqbal (2004) identify various unique credit risks that are particular toIslamic finance. Sukuk prospectuses operate, for the most part, inemerging markets where counterparties possess less sophisticated riskmanagement mechanisms. The rescheduling of debt at a highermarkup rate is not existent due to the prohibition of interest. Conse-quently, counterparties would be more inclined to default on theircommitments to other parties. Also, the nature of profit-loss sharing(PLS) arrangements means that agency costs will be higher.

Default RiskEach prospectus has provisions for the termination of the certificatein the event of a default by the obligor. If the obligor fails to pay the

Ali Arsalan Tariq ■ Humayon Dar

212 Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

Sukuk prospec-tuses operate,for the mostpart, in emergingmarkets wherecounterpartiespossess lesssophisticatedrisk manage-ment mecha-nisms.

rentals on the ijarah agreements that form the coupon payments, thecertificate holder can exercise the right to nullify the contract andforce the obligor to buy back the assets. Furthermore, in the eventthat the obligor fails to reimburse the principal amount, the certifi-cate holder can exercise the right to take legal action and force theobligor to enter into debt-rescheduling proceedings.

Coupon Payment RiskThe obligor may fail to pay the required coupons on time. Anydelayed coupons will be subject to a specified payment amount thatwill be accumulated with the SPV. Nonetheless, such accumulatedfunds are recommended by Shariah boards to be donated for chari-table purposes.

Asset Redemption RiskThe originator has to buy back the underlying assets from the certifi-cate holder. The principal amount paid may not be equal to the sukukissuance amount, and, as a result, there is the risk that the assets maynot be fully redeemed.

Shariah Compliance Risks Shariah compliance risk refers to the loss of asset value as a result ofthe issuers’ breach of its fiduciary responsibilities with respect tocompliance with Shariah. The dissolution clauses of the sukukprospectus define events that will make the sukuk deed null andvoid due to Shariah noncompliance. For example, if the sukuk isbased on a hybrid of ijarah and istisna assets, ijarah must always bemore than istisna in the pool; otherwise the sukuk deed will dissolve(Usmani, 2002, p. 218). The issue then becomes that of competi-tiveness and survival in the market as a distinct Shariah-compliantasset class.

There are a number of discrepancies regarding the applicability ofIslamic financial instruments reflecting the different schools ofthought as well as the legal regimes in which the sukuk are issued.Such a theoretical ambiguity would pose further procedural risks thatthe Islamic bank might run afoul of Shariah jurisdictions. For exam-ple, the theoretical applicability of the murabahah contract variesbetween different schools of thought. Numerous jurists, such as theOrganization of the Islamic Conference (OIC) Fiqh Academy, con-cur that the murabahah contract is binding on only the seller of thecontract and not on the buyer. Other jurists hold the view that boththe parties to a contract have an equal obligation to the terms of thecontract (Vogel & Hayes III, 1998).

Risks of Sukuk Structures: Implications for Resource Mobilization

213Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

Shariah compli-ance risk refers

to the loss ofasset value as a

result of theissuers’ breachof its fiduciaryresponsibilitieswith respect to

compliance withShariah.

An additional case relates to the liquidity facility. The sukuk prospec-tuses analyzed have had stipulations for a liquidity facility to abatelags between payments to investors and returns on the underlyingasset pools. Some liquidity facilities have been formed to permit thetrustee to benefit the facility for any liquidity deficit ensuing fromdefault in the sukuk asset pools. The imbursement of the liquidity ser-vices has been provisional upon surplus funds after the distribution ofcoupon payments to the sukuk holders. The sole purpose of such aliquidity facility would be to ease out lags between investor paymentsand returns on the underlying asset pools. The importance of such aliquidity facility can most effectively be garnered where the arrange-ment had floating-rate payments, as fixed-rate returns would implythe nonexistence of interest-rate differentials.

Sukuk prospectuses are subject to the same fiduciary risks as Islamicbanks (El-Hawary et al., 2004). The reputation of the originatorwould suffer tremendously as investors would lose confidence in itsability to conform to industry regulations. Accordingly, the investormay also incur economic losses from not being able to recoup onpotential investments. In conclusion, the association of Shariahsupervisors with sukuk issuances will ensure investor confidence.However, the convenience with which the Shariah compliancerequirements can be married with the conditions of market compet-itiveness will remain a great challenge for the sukuk issuances.

Liquidity RisksThe certificate holder is rendered to several risks pertinent to sukukstructures. These are primarily regarding liquidity issues. The sukukstructures, as welcome as they are in dealing with liquidity managementissues in Islamic finance, are exposed to a liquidity risk because there cur-rently does not exist a well structured and sufficiently liquid secondarymarket. The certificates are listed on several local markets, but this alonedoes not signify their liquidity. The sukuk certificates are medium tolong term in maturity, and their continued success will largely dependon their aptitude to evolve into highly liquid means of fund investmentwith adequate risk management mechanisms. As is currently the case,most of the certificates tend to be held until maturity.

MANAGING THE FINANCIAL RISKS OF SUKUK STRUCTURES

Islamic financial markets have sequentially faced the realities of infla-tionary pressures and disintermediation owing to the inefficienciesrelated to the dearth of adequate market-based government mone-

Ali Arsalan Tariq ■ Humayon Dar

214 Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

…the conve-nience withwhich theShariah compli-ance require-ments can bemarried with theconditions ofmarket competi-tiveness willremain a greatchallenge for thesukuk issuances.

tary policy instruments compatible with Shariah (see Sundararajan &Luca, 2002; Sundararajan et al., 1998). Sukuk certificates aim tobridge this gap and serve to replicate the functions of conventionalbonds and tradable securities to effectively mobilize resources intothe markets and inject liquidity into enterprises or governments.Moreover, they provide a stable source of income for investors inIslamic markets. However, there are some stark differences betweensukuk and bonds. The legitimacy of sukuk structures within Shariahlies in the fact that they do not take advantage of interest-rate move-ments. Also, investing in sukuk issuances involves the funding of tradeor production of tangible assets. Furthermore, sukuk investors havean inherent right to information on the use of their investments,nature of underlying assets, and other particulars that would other-wise be redundant in conventional investments.

In the next section, we discuss some aspects of enhancing the competi-tiveness of sukuk structures by overcoming some of the undesirableunderlying risks. In this regard, we discuss some aspects of institutionalreform and some possible mechanisms of financial engineering.

SUKUK AND THE CHALLENGE OF DERIVATIVES

The nonexistence of interest rates in Islamic finance ostensibly makesthe need for derivative instruments redundant in Islamic markets.However, we need to note some important qualifiers. First, the pro-hibition of interest and gharar should not categorically close the doorfor financial engineering in compliance with the Shariah. Second,sukuk cannot avoid being competitive in those conventional marketsin which they operate. Finally, the positive aspects of derivative mar-kets can be valuable for developing capital markets if replicated inemerging economies.

An impending concern for the managers and investors in sukuk is theirability to protect themselves from different types of risks. The nextlogical step in the evolution of Islamic finance is the provision of riskmanagement mechanisms that replicate the functions of conventionalinstruments in a way compliant with Islamic law. Shariah does not rec-ognize financial options as a form of wealth. Hence, these options can-not be traded (see Usmani, 2002; Vogel & Hayes III, 1998).

Embedded Options and GhararThe previously cited position on derivatives has been with regard tothe applicability of stand-alone contracts such as call and put options.

Risks of Sukuk Structures: Implications for Resource Mobilization

215Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

The legitimacy ofsukuk structures

within Shariahlies in the fact

that they do nottake advantageof interest-rate

movements.

Embedded options are not detachable and are not traded, but insteadthese form part of the initial issuance contract. As such, embeddedoptions can create callable or puttable bonds. A callable bond con-tains provisions allowing the issuing firm to buy back the bond at apredetermined price at a certain time in the future. Such bonds nor-mally cannot be recalled within the first few years of the issuance.Conversely, the puttable bond allows the holder to demand an earlyredemption at a predetermined price at a certain time in the future.A puttable bond commonly has lower yields than option-free bondsbecause it is more attractive to the buyer. Similarly, the callable bondwill have higher yields than noncallable bonds as it is deemed lessvaluable to the holder.

Merton (1995) identifies that puttable bonds are equivalent to aportfolio of discount bonds and a short-term bond at the risk-freerate. The put option is exercised when the discount prices fall, andthis reduces interest-rate risk faced by the holder of the bond.Accordingly, it is concluded that when prices of discount bonds fall,the prices of embedded options on these bonds fall less. Embeddedoptions, therefore, help to stabilize the prices of these instruments.

The applicability of embedded options can be analyzed through thesuggestive framework developed by Al-Suwailem (2000). To analyzethe term gharar in a conventional sense, it is compared to the idealsof zero-sum games. Shariah dictates the prohibition of gharar as itrenders a financial contract unfair to the extent that one party willwholly benefit at the expense of the counterparty (Al-Suwailem,2000). This is the situation that prevails in zero-sum games. Fur-thermore, it is determined that all zero-sum games are not compati-ble with Shariah principles.

It will be argued that embedded options do not strictly take theshape of zero-sum games that tradable option contracts take. Non-zero-sum games can have a different spectrum of “win-win,” “lose-lose,” and “win-lose” payoff structures. Shariah considerations donot reproach contracts that embody risk but rather when this risk isan avenue for one party to entirely benefit at the expense of thecounterparty. Al-Suwailem discusses the Shariah guidelines bywhich risk can be tolerated in non-zero-sum games before itbecomes gharar. These criteria are that the risk must be: (1) negli-gible in that the probability of loss must be small enough to beacceptable, (2) inevitable such that a mutually beneficial outcomecan be garnered, and (3) unintentional in that the participantsshould avoid zero-sum games.

Ali Arsalan Tariq ■ Humayon Dar

216 Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

Shariah dictatesthe prohibition ofgharar as it ren-ders a financialcontract unfair tothe extent thatone party willwholly benefit atthe expense ofthe counterparty.

Scrutinizing the functions of embedded options under these threecriteria we can make a case for their Shariah acceptability. Anyeagerness by Shariah jurists to accept embedded options may beundermined by the underlying uncertainty associated with the exer-cising of the option. The concern is whether this uncertaintyamounts to gharar or can be accepted within the boundaries ofIslamic jurisdiction.

First, we can try to classify this uncertainty as negligible. The embed-ded option in conventional bonds is usually not exercised before 2–3years after the issuance of the bond. Even then, it is only exercisedsubject to economic developments and interest-rate movements per-taining to the value of the bond. Also, with embedded call options,the buyer of the bond is not left “empty-handed” if the option isexercised. Rather, the originator buys back the bond at a predeter-mined price, and throughout the life of the bond the buyer enjoys astream of coupon payments. Conversely, a tradable option contract isnot bought back but becomes void if markets move against theexpectations of the option holder. Consequently, the premium on thecontract is lost, and the buyer is left with a financial loss. Therefore,we can move to classify the uncertainty as significantly less in magni-tude and possibly less probable for two reasons. First, if the calloption is exercised, the buyer is compensated and the bond is boughtback at a previously agreed-upon price. Second, the likelihood of thebond option being exercised is only possible several years after theissuance.

Second, the dimension of inevitability states that “win-win” out-comes should be possible. The results of embedded options may notbe considered to be totally “win-win.” After all, the option is exer-cised when circumstances make it profitable to do so. However,because callable bonds are less valuable to the buyer, the coupon pay-ments are higher to reflect this. The buyer also gets reimbursed forthe bond that is bought back. Therefore, the overall payoffs to boththe parties can be measured to not follow a zero-sum pattern. Whatis observed are circumstances where both parties to the contract areleft better off than had the investment not been undertaken. Thebuyer of the bond would not have received the coupon payments,and the issuer may not have benefited from the liquidity profits of thebond issuance.

Finally, the intentionality dimension is tied closely to the presence ofa zero-sum structure. The embedded option arrangements do notembody such payoff structures that typify tradable call and put option

Risks of Sukuk Structures: Implications for Resource Mobilization

217Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

The results ofembedded

options may notbe considered to

be totally “win-win.”

contracts. Therefore, the upshot from these considerations is thatthere is scope for embedded options to be considered within thesphere of Islamic finance. The modus operandi of the provisions forembedded options in sukuk structures must be formulated to bespecifically tailored for the purposes of Islamic finance. Instead oftying to interest-rate movements that are typical of conventionalbonds, sukuk options can be related to the value of the underlyingassets and their continued viability and profitability with respect toexisting economic conditions.

Embedded Options as a Risk Management Tool Conventional investors have a wide range of financial instruments toselect from through which to construct different investment strategies.Bonds with embedded options are one of a myriad of such instruments.Neftci and Santos (2003) identify three opportunities to expand thescope for analyzing embedded bond options. First, these bonds can beevaluated for their price-stabilizing properties. Second, they can beimplemented in replicating interest-rate derivative markets. Finally,embedded option bonds traditionally have been popular among private-sector issuers in developed markets and less so among governments ofboth developed and emerging markets. Their use by governments canbe warranted by the bonds’ accomplishments in private-sector issuances.

The price-stabilizing properties identified by Merton (1995) andNeftci and Santos (2003) can be implemented to reap the convexitygains of trading in highly volatile emerging markets. It is against thegovernment’s interests if a puttable sukuk certificate is exercised.Thus, another advantage of puttable structures is that after theissuance of such certificates the government will ensure that theireconomic position is sound so as to be able to honor future commit-ments in the event that such a put option is exercised. However, put-table and callable structures inherit the possibility that traders of suchcertificates will try to exploit the price volatility of the underlyingbond so as to increase their likelihood of exercising the options.

Previously, we introduced the structure of zero-coupon sukuk as aShariah-compatible debt finance instrument. Unlike traditional zero-coupons, the limitation of the zero-coupon sukuk is that these are nottradable in Islamic secondary markets. Consequently, these instrumentsface serious liquidity issues and cannot be adjusted to the variations inmarket conditions such as prices, interest rates, and exchange rates.Hence, investors in these assets are exposed to serious market risks.Unless these market risks are mitigated efficiently, the sukuk marketswill face stark challenges in competing with traditional bond markets.

Ali Arsalan Tariq ■ Humayon Dar

218 Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

…puttable andcallable struc-tures inherit thepossibility thattraders of suchcertificates willtry to exploit theprice volatility ofthe underlyingbond so as toincrease theirlikelihood ofexercising theoptions.

The impending issue is how to manage these market risks inherent inthe zero-coupon sukuk. In conventional financial markets, embeddedcall and put option features of bonds as well as fixed-floating–rateswaps play an important role in mitigating market risks of debt instru-ments in two important respects. First, these ensure a wider flexibil-ity of financial instruments to market conditions and, hence, improveliquidity of assets by enhancing the prospects of repricing from theperspective of the issuing companies. The ability of an asset to repricefacilitates its protection against price risks. Second, investors obtain asafeguard against risks when they purchase any of these bonds. If themarket price of the issuer’s stock grows, the value of the embeddedconvertible bond also increases. If the market price of the stock goesdown, owners of the convertibles lose nothing, as the downsides ofthese assets are protected by the debts.

Islamic Embedded OptionsShariah guidelines do not allow the sale of debts but they allow theexchange of debts for real assets, goods, and services (Usmani, 2002,pp. 18–19). Thus, the opportunity of an exchange of debts againstreal assets and usufructs can be added to the debt certificates as anembedded option for the settlement of debts. Practically, the enter-prise that would implement the funds would write the embeddedoption. Such an option would not be binding on the financier but, ifutilized, the user of the funds is bound by the promise.

Suppose that a firm needs funds for the construction of a new apart-ment complex. A financier provides funding for construction on thebasis of istisna at a 6% markup. Also, assume that the total amount ofdebts amounts to $100 million. These can then be divided into onemillion zero-coupon sukuk of $100 each. A zero-coupon certificatewill accordingly represent $94 of the principal amount and $6 of themarkup. Suppose the zero-coupons are issued for ten years.

This financial asset that is a debt has no Islamic secondary market.The zero-coupon needs to be kept for ten years before it can becashed for $100. Hence, this financial asset is bundled with a num-ber of financial risks such as liquidity risks, reinvestment risks dueto the highly illiquid nature of the issued certificates, credit risksdue to the long term to maturity, interest-rate risks, and foreignexchange risks.

An embedded option will interestingly transform the risk scenario ofthis zero-coupon sukuk certificate. Suppose the constructor writes anoption on the certificate that if the holders of the certificate wish,

Risks of Sukuk Structures: Implications for Resource Mobilization

219Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

Shariah guide-lines do not

allow the sale ofdebts but they

allow theexchange of

debts for realassets, goods,and services.

commencing in the second year (the completion of the construc-tion), the holders can purchase apartments or acquire apartments onleases utilizing their zero-coupons. For example, the rent of an apart-ment of this building may be $3,000 per year. An investor holdingzero-coupons worth $3,000 can acquire an apartment on a one-yearrent after two years instead of waiting for ten years to cash the zero-coupons.

It should be noted that the embedded feature in this case is a calloption on the new assets of the construction company. This calloption cannot be detached and sold independently. Therefore, noderivative is created.

However, the embedded call option alters the nature of all the aboverisks that were previously bundled with the zero-coupons. The down-side of the investments is, by default, protected by the fixed markupof 6%. Additionally, the entire nature of the certificates changesdepending on the performance of the new construction. Thesebecome more attractive, as anyone holding zero-coupons will bene-fit from the call option. The zero-coupons can easily be liquidated attheir face value. Once the call option is utilized, the interest-rate risk,reinvestment risk, credit risk, and exchange-rate risk are all isolated.Indeed, the financial asset is transformed into a real asset with differ-ent risk characteristics.

The embedded options can be additional with most Islamic financialcontracts like leasing, installment sale, and salam contracts. More-over, different varieties of options can be added with the differentcontracts. For example:

• The zero-coupon holders may be given the option to exchangetheir certificate for a suitable amount of output of the com-pany. This is contingent on the nature of the company andoutput or on the common stocks of the company, if the com-pany or its subsidiaries are listed.

• The certificate holders can put back the certificate and rescindfrom the contract during a specified time period prior to matu-rity and the company can call back the certificate during aspecified time period prior to maturity.

Floating- to Fixed-Rate Swaps of SukukA swap is an exchange of liabilities and obligations. The issue of thepermissibility of swaps within the realm of Shariah has not beenaddressed thus far.

Ali Arsalan Tariq ■ Humayon Dar

220 Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

The embeddedoptions can beadditional withmost Islamicfinancial con-tracts like leas-ing, installmentsale, and salamcontracts.

Previously, we described the floating rate sukuk (FRS) and the fixed-rate zero-coupon embedded sukuk (ZCES) based on leasing andistisna transactions, respectively. We know that the FRSs representownership in rented assets and/or of usufructs of assets. They are, thus,tradable in secondary markets. The ZCESs, on the other hand, are debtinstruments that cannot be traded on secondary markets. However, theZCESs are exchangeable with real assets, goods, services, and stocks ofcompanies. Hence, the ZCESs are exchangeable with the FRSs giventhat they are of identical face values. If the face values of the FRSs andSCESs are not identical, the discrepancies will have to be adjusted bycash payments. For example, an FRS with face value of $100 isexchangeable with a ZCES worth $105 under the condition that theadditional $5 is adjusted by cash payments. Accordingly, this can estab-lish a basis for a Shariah-compliant fixed- and floating-rate swap.

CONCLUSION

In this research, we discussed and analyzed a number of issues relatedto the evolution, underlying principles, structures, risks, and compet-itiveness of sukuk as Shariah-compliant substitutes to traditionalfinancial assets. It is expected that sukuk will encourage many Mus-lims worldwide to participate in financial markets and, thus, will beinstrumental in expanding and deepening these markets, particularlyin emerging countries. There are other benefits of sukuk for theeconomies and financial markets such as heightened discipline andincreased financial stability.

Sukuk are an indispensable vehicle for resource mobilization, whetherin the public or private sector. Through Shariah-compatible financialengineering, sukuk can also become highly competitive in the marketand accessible to the general public as an investment opportunity. Inthe absence of such a stable-income, Shariah-compatible channel forinvestment, the public has on one hand no incentive to save and onthe other hand no possibility to invest.

Investors in conventional markets have also garnered the positiveeffects of swaps in differing interest rates, exchange rates, andbetween floating and fixed rates. The emergence of sukuk certificatesas mechanisms of liquidity management presents a novel asset-backedsecurities structure that can set the foundation for supporting risk-management derivative instruments. Our discussion centered on theviability of a swap between floating-rate sukuk (FRS) and fixed-ratezero-coupon-embedded sukuk (ZCES).

Risks of Sukuk Structures: Implications for Resource Mobilization

221Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

The emergenceof sukuk certifi-

cates as mecha-nisms of liquidity

managementpresents a novel

asset-backedsecurities struc-ture that can set

the foundationfor supportingrisk-manage-

ment derivativeinstruments.

Sukuk markets will only continue to grow and they have generatedthe first truly global convergence between conventional finance andIslamic finance. A greater pool of investors is attracted to this com-ponent of Islamic finance because of the relative similarity betweenconventional fixed-income securities and sukuk certificates. Adequaterisk management techniques will foster this growth and enable thesatisfaction of a greater variety of investment appetites. The early suc-cess of sovereign sukuk issues has encouraged corporate placementsto the extent that corporate issues now comprise over 90% of the totalvolume of global sukuk issuances. To Islamic institutions, sukuk pro-vides for enhanced liquidity and balance-sheet mechanisms. Previ-ously untapped funds are now mobilized. For conventional investors,sukuk certificates are another avenue to reap global diversificationbenefits and recycle previously idle Islamic assets and funds. Movingforward, the challenge for the industry lies in the development ofefficient secondary markets for sukuk certificates to support thegrowth in primary issues.”

In this study, we made an effort to identify the risks underlying sukukstructures and suggest some possible methods of mitigating suchrisks. Indeed, the subject is an emerging one and offers rich potentialfor further research.

REFERENCES

Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI). (2002).Investment sukuk (Shar’iah Standard No. 18). Manama: Author.Al-Suwailem, S. (2000). Towards an objective measure of gharar in exchange. Islamic Eco-nomic Studies, 7(1), 61–98.Chapra, M. U., & Khan, T. (2000). Regulation and supervision of Islamic banks. OccasionalPaper No. 3. Jeddah: Islamic Research and Training Institute, Islamic Development Bank. El-Gamal, M. (2000). An economic explication of the prohibition of gharar in classical Islamicjurisprudence. In Islamic finance: Challenges and opportunities in the twenty first century(Conference Papers). Loughborough: Fourth International Conference on Islamic Economicsand Banking, U.K.Elgari, M. A. (1997). Short term financial instruments based on salam contracts. In A. Ahmed& T. Khan (Eds.), Islamic financial instruments for public sector resource mobilization (pp.249–266). Jeddah: Islamic Research and Training Institute, Islamic Development Bank.El-Hawary, D., Grais, W., & Iqbal, Z. (2004). Regulating Islamic financial institutions: Thenature of the regulated. World Bank Policy Research Working Paper 3227. Haque, N., & Abbas, M. (1999). The design of instruments for government finance in anIslamic economy. Islamic Economic Studies, 6(2), 27–43.Kahf, M. (1997). The use of assets ijarah bonds for bridging the budget gap. In A. Ahmed &T. Khan (Eds.), Islamic financial instruments for public sector resource mobilization (pp.265–316). Jeddah: Islamic Research and Training Institute, Islamic Development Bank.Khan, T., & Ahmed, H. (2001). Risk management: An analysis of issues in the Islamic finan-cial industry. Occasional Paper No. 5. Jeddah: Islamic Research and Training Institute, IslamicDevelopment Bank. Malaysian Global First Ijarah Sukuk. (2001). Guthrie Plantation’s Issuance Prospectus

Ali Arsalan Tariq ■ Humayon Dar

222 Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

Malaysian Global Inc. (2002). Issuance prospectus of ijarah trust certificates.Merton, R. C. (1995). Financial innovation and the management and regulation of financialinstitutions. Journal of Banking & Finance, 19, 461–481.Neftci, S. N., & Santos, A. O. (2003). Puttable and extendable bonds: Developing interest-ratederivatives for developing countries. IMF Working Paper, WP/03/201.Qatar global sukuk. (2003). Issue prospectus of ijarah sukuk.Sundararajan, V., & Luca, E. (2002). Islamic financial institutions and products in the globalfinancial system: Key issues in risk management and challenges ahead. IMF Working Paper,WP/02/192Sundararajan, V., Martson, D., & Ghiath, S. (1998). Monetary operations and governmentdebt management under Islamic banking. IMF Working Paper, WP/98/144.Tabreed Financing Corporation. (2004). Issuance prospectus for Tabreed Global Istisna’ cumIjarah Sukuk.Usmani, M. T. (2002). An introduction to Islamic finance. The Hague: Kluwer Law Interna-tional.Vogel, F. E., & Hayes, S. L., III. (1998). Islamic law and finance: Religion, risk, and return.The Hague: Kluwer Law International. Zarqa, M. A. (1997). Istisna’ financing of infrastructure projects. In A. Ahmed & T. Khan(Eds.), Islamic financial instruments for public sector resource mobilization (pp. 231–248).Jeddah: Islamic Research and Training Institute, Islamic Development Bank.

Risks of Sukuk Structures: Implications for Resource Mobilization

223Thunderbird International Business Review • DOI: 10.1002/tie • March–April 2007

![The Perception-Distortion Tradeoff - Technion · dence of the advantages of GANs in image restoration [22,38,35,51,36,15,55]. The perception-distortion tradeoff has major implica-tions](https://static.documents.pub/doc/80x56/5f8601fca5440344c22b082a/the-perception-distortion-tradeoff-technion-dence-of-the-advantages-of-gans-in.jpg)