Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 1 of 53 IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF COLORADO Civil Action No.: 1:14-cv-01409-MSK-CBS ROBERT OLINATZ and GEORGE SIROIS, Individually on Behalf of Themselves and All Others Similarly Situated, Plaintiffs, v. FOREST OIL CORPORATION, PATRICK R. MCDONALD, JAMES D. LIGHTNER, JAMES H. LEE, DOD A. FRASER, LOREN K. CARROLL, RAYMOND I. WILCOX, RICHARD J. CARTY, NEW FOREST OIL INC., FOREST OIL MERGER SUB INC., SABINE OIL & GAS LLC, SABINE INVESTOR HOLDINGS LLC, SABINE OIL & GAS HOLDINGS LLC, and SABINE OIL & GAS HOLDINGS II LLC., Defendants. AMENDED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY AND VIOLATIONS OF FEDERAL SECURITIES LAWS

Transcript

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 1 of 53

IN THE UNITED STATES DISTRICT COURT FOR THE DISTRICT OF COLORADO

Civil Action No.: 1:14-cv-01409-MSK-CBS

ROBERT OLINATZ and GEORGE SIROIS, Individually on Behalf of Themselves and All Others Similarly Situated,

Plaintiffs,

v.

FOREST OIL CORPORATION, PATRICK R. MCDONALD, JAMES D. LIGHTNER, JAMES H. LEE, DOD A. FRASER, LOREN K. CARROLL, RAYMOND I. WILCOX, RICHARD J. CARTY, NEW FOREST OIL INC., FOREST OIL MERGER SUB INC., SABINE OIL & GAS LLC, SABINE INVESTOR HOLDINGS LLC, SABINE OIL & GAS HOLDINGS LLC, and SABINE OIL & GAS HOLDINGS II LLC.,

Defendants.

AMENDED COMPLAINT BASED UPON SELF-DEALING AND BREACH OF FIDUCIARY DUTY AND VIOLATIONS OF FEDERAL SECURITIES LAWS

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 2 of 53

SUMMARY OF THE ACTION

1. This is an amended shareholder class action brought by plaintiffs on behalf of all

the holders of Forest Oil Corporation ("Forest Oil" or the "Company") common stock (the

"Class") against Forest Oil and its affiliates, the members of Forest Oil's Board of Directors (the

"Board" or "Individual Defendants"), and Sabine Oil & Gas LLC ("Sabine") and its affiliates.

This action seeks to enjoin defendants from violating federal securities laws and further

breaching their fiduciary duties in their pursuit of a sale of the Company at a potentially unfair

price through an unfair and self-serving process to Sabine (the "Proposed Transaction")

Defendants announced on May 6, 2014, that the Board had agreed to sell Forest Oil to Sabine, a

privately-held company, for 0.1 Sabine shares in exchange for each share of Forest Oil (the

"Proposed Consideration"). As a result of the transaction, former Sabine unit holders will own

approximately 73.5% percent and Forest Oil shareholders will own just 26.5% of the outstanding

Sabine common stock upon closing of the Proposed Transaction. Plaintiffs make the following

allegations upon knowledge as to plaintiffs and upon information and belief (including

investigation of counsel and review of publicly available information) as to all other matters, and

allege as follows.

2. Through the Proposed Transaction, Sabine is attempting to take advantage of

Forest Oil's depressed stock price, which is trading at five-year lows. The Company's recent

performance, however, indicates that a strong turnaround for Forest Oil has already begun. The

Company's production greatly increased in 2013 and it was able to reduce its net debt by more

than 50% . Moreover, the Company was able to overcome a $1.3 billion loss in 2012 to achieve

nearly $74 million in net earnings in 2013. In a call with financial analysts on February 26,

- 1 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 3 of 53

2014, defendant Patrick R. McDonald ("McDonald"), the Company's President, Chief Executive

Officer ("CEO"), and a director, touted that Forest Oil was "able to accomplish a number of the

strategic goals [management] set forth for 2013" and had a positive foundation for growth in

2014.

3. Unfortunately, the Individual Defendants are attempting to prevent plaintiffs and

the Class from realizing the benefits of the Company's strong financial results and bright future

by inexplicably deciding to sell Forest Oil now. Intent on selling the Company promptly, the

Board conducted a limited sales process, locking in on Sabine from the outset without adequately

exploring alternative transactions or other bidders. Not having to face any competition, Sabine

was ultimately able to secure a one-sided equity split for itself to the detriment of Forest Oil

shareholders. The proposed equity split in the Proposed Transaction is particularly unfair to

Forest Oil shareholders given the relative financial strength and asset positions of the two

companies.

4. The Board further breached its fiduciary duties by agreeing to preclusive deal

protection devices in connection with the Agreement and Plan of Merger the Company entered

into on May 5, 2014 (the "Merger Agreement"), which all but ensure that the inadequate

Proposed Transaction will be consummated. These provisions, which further undermine

shareholder value by precluding any competing offers for the Company from emerging, include

(i) a no-solicitation provision prohibiting the Company from properly shopping itself; (ii) a

three-business-day matching rights period during which Sabine has the option to match any

superior proposal received by the Company; and (iii) a termination fee of $15 million payable by

the Company to Sabine in the event that, among other things, an unsolicited superior offer

- 2 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 4 of 53

materializes and is accepted. Collectively, these provisions reflect an attempt by the Individual

Defendants to lock up the Proposed Transaction at a price that grossly undervalues the Company,

thereby securing for themselves the personal financial benefits they have negotiated for

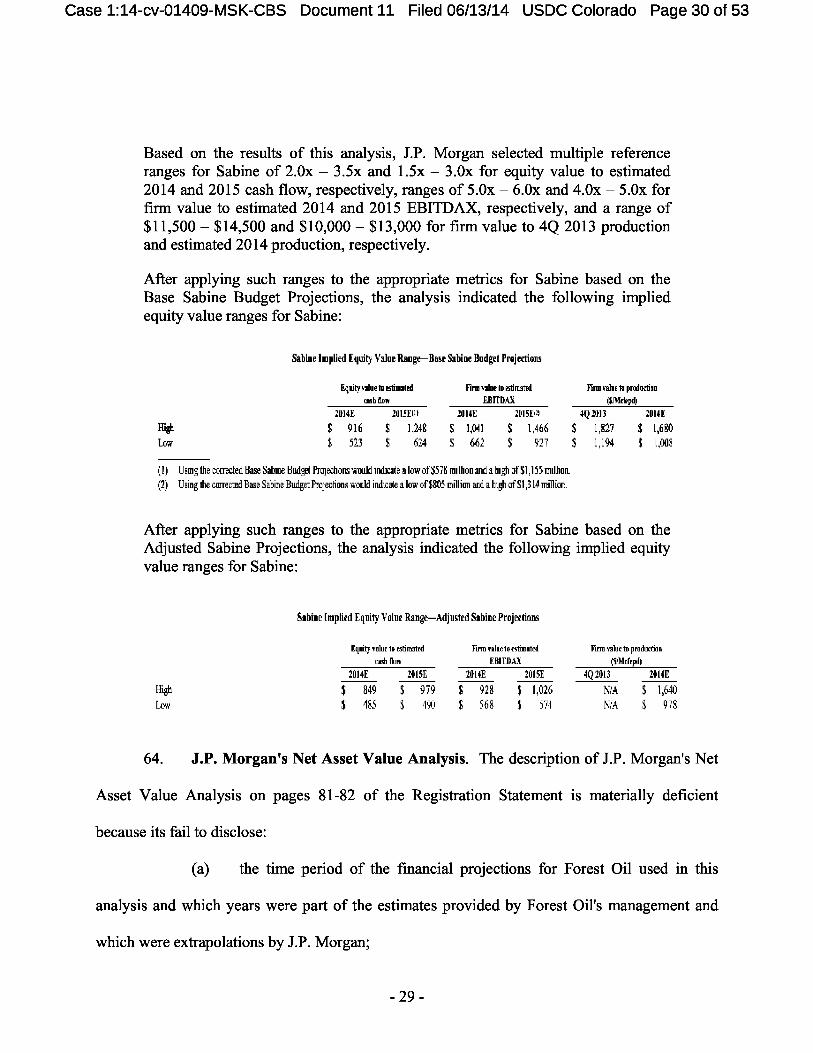

themselves in connection with the closing of the Proposed Transaction.

5. Though the Board is intent on cashing out Forest Oil shareholders at a potentially

unfair price, the Individual Defendants will receive immediate benefits upon the closing of the

Proposed Transaction. Defendant McDonald will receive the biggest windfall upon

consummation of the Proposed Transaction, including a cash severance payment equal to 2.5

times the sum of his annual salary and annual bonus and vesting of all his all outstanding stock

options, restricted stock, and cash-settled phantom stock units. The completion of the Proposed

Transaction will also trigger change-of-control provisions for holders of Forest Oil's existing

senior notes. These change-of-control provisions entitle the holders of the senior notes to receive

101% of the principal amount of the notes plus accrued interest with respect to each series of

notes. In addition, the Individual Defendants have ensured that at least two of the members of

the Board will retain their prestigious positions following completion of the Proposed

Transaction.

6. On May 29, 2014, defendants filed with the U.S. Securities and Exchange

Commission ("SEC") the materially false and misleading Form S-4 Registration Statement

("Registration Statement"). The Registration Statement, which recommends that Forest Oil

shareholders vote in favor of the Proposed Transaction, omits and/or misrepresents material

information in contravention of sections 14(a) and 20(a) of the Securities Exchange Act of 1934

("Exchange Act") and SEC Rule 14a-9 promulgated thereunder regarding (i) the sales process

- 3 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 5 of 53

leading to the Proposed Transaction; (ii) financial analyses performed by J.P. Morgan Securities

LLC ("J.P. Morgan"); and (iii) the Company's and Sabine's financial projections, which were

relied upon J.P. Morgan in the financial analyses used to support its fairness opinion.

7. In pursuing the unlawful plan to sell the Company via an unfair process and at an

inadequate price, each of the defendants has violated applicable law by directly breaching and/or

aiding and abetting the other defendants' breaches of their fiduciary duties of loyalty and due

care, among others. This action seeks to enjoin the Individual Defendants from further violating

federal securities laws and breaching their duties in connection with the Proposed Transaction.

Specifically, to remedy the defendants' legal violations as set-forth herein, plaintiffs seek, among

other things: (i) an order requiring defendants to disclose the omitted and/or misrepresented

material information concerning the value of the Proposed Consideration; (ii) injunctive relief

preventing consummation of the Proposed Transaction unless and until the Company adopts and

implements a procedure or process designed to obtain a transaction that provides the best

possible terms for shareholders; (iii) a directive to the Individual Defendants to exercise their

fiduciary duties to obtain a transaction which is in the best interests of Forest Oil's shareholders;

and (iv) rescission of, to the extent already implemented, the Merger Agreement or any of the

terms thereof.

JURISDICTION AND VENUE

8. This Court has jurisdiction over the subject matter of this action pursuant to

section 27 of the Exchange Act for violations of sections 14(a) and 20(a) of the Exchange Act

and SEC Rule 14a-9 promulgated thereunder. This Court has supplemental jurisdiction under 28

U.S.C. §1367, over the state law claims.

- 4 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 6 of 53

9. This Court has jurisdiction over each defendant named herein because each

defendant is either a corporation that conducts business in and maintains operations in this

District, or is an individual who has sufficient minimum contacts with this District so as to

render the exercise of jurisdiction by the District courts permissible under traditional notions of

fair play and substantial justice.

10. Venue is proper in this Court pursuant to 28 U.S.C. §1391(a) because (i) Forest

Oil maintains its principal place of business in this District; (ii) one or more of the defendants

either resides in or maintains executive offices in this District; (iii) a substantial portion of the

transactions and wrongs complained of herein occurred in this District; and (iv) defendants have

received substantial compensation in this District by doing business here and engaging in

numerous activities that had an effect in this District.

PARTIES

11. Plaintiff Robert Olinatz is, and at all times relevant hereto, was a shareholder of

Forest Oil.

12. Plaintiff George Sirois is, and at all times relevant hereto, was a shareholder of

Forest Oil.

13. Defendant Forest Oil is a New York corporation with principal executive offices

located at 707 17th Street, Suite 3600, Denver, Colorado. Defendant Forest Oil is an

independent oil and gas company engaged in the acquisition, exploration, development, and

production of oil, natural gas, and natural gas liquids primarily in North America. Defendant

Forest Oil recorded net earnings of $74 million in 2013 as compared to a net loss of $1.3 billion

in 2012. Upon completion of the Proposed Transaction, Forest Oil will become a wholly-owned

- 5 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 7 of 53

subsidiary of defendant New Forest Oil Inc. ("New Forest Oil"), which will be renamed Sabine

Oil & Gas Corporation.

14. Defendant McDonald is Forest Oil's President and CEO and has been since

September 2012 and a director and has been since 2004. Defendant McDonald was also Forest

Oil's Interim CEO from June 2012 to September 2012.

15. Defendant James D. Lightner is Forest Oil's non-executive Chairman of the Board

and has been since May 2008 and a director and has been since 2004.

16. Defendant James H. Lee is a Forest Oil director and has been since 1991.

17. Defendant Dod A. Fraser is a Forest Oil director and has been since 2000.

18. Defendant Loren K. Carroll is a Forest Oil director and has been since 2006.

19. Defendant Raymond I. Wilcox is a Forest Oil director and has been since 2009.

20. Defendant Richard J. Carty is a Forest Oil director and has been since October

2012.

21. Defendant New Forest Oil is a Delaware corporation and wholly-owned

subsidiary of defendant Forest Oil with principal executive offices located at 707 17th Street,

Suite 3600, Denver, Colorado. Upon completion of the Proposed Transaction, defendant New

Forest Oil will be renamed Sabine Oil & Gas Corporation and will become the ultimate parent of

Forest Oil.

22. Defendant Forest Oil Merger Sub Inc. ("Merger Sub") is a New York corporation

and wholly-owned subsidiary of defendant New Forest Oil with principal executive offices

located 707 17th Street, Suite 3600, Denver Colorado. Upon completion of the Proposed

- 6 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 8 of 53

Transaction, defendant Merger Sub will merge with and into defendant Forest Oil and cease its

separate corporate existence.

23. Defendant Sabine is a Delaware limited liability company with principal

executive offices located at 1415 Louisiana Street, Suite 1600, Houston, Texas. Defendant

Sabine is an independent energy company engaged in the acquisition, production, exploration,

and development of onshore oil and natural gas properties in the United States. During the

Proposed Transaction, defendant Sabine will merge with and into Forest Oil, and will cease its

separate existence.

24. Defendant Sabine Investor Holdings LLC ("New Sabine") is a Delaware limited

liability company with principal executive offices located at 1415 Louisiana Street, Suite 1600,

Houston, Texas. Upon closing of the Proposed Transaction, defendant New Sabine will directly

and indirectly contribute to defendant New Forest all of the outstanding equity of defendant

Sabine Oil & Gas Holdings LLC ("Sabine Holdings") in exchange for 33,013,641 shares of

defendant New Forest Oil's common stock.

25. Defendant Sabine Holdings is a Delaware limited liability company with principal

executive offices located at 1415 Louisiana Street, Suite 1600, Houston, Texas. Upon closing of

the Proposed Transaction, defendant Sabine Holdings will become a wholly owned subsidiary of

defendant New Forest Oil.

26. Defendant Sabine Oil & Gas Holdings II LLC ("SOGH II") is a Delaware limited

liability company and a wholly owned subsidiary of defendant Sabine Holdings with principal

executive offices located at 1415 Louisiana Street, Suite 1600, Houston, Texas. During the

- 7 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 9 of 53

Proposed Transaction, defendant SOGH II will merge with and into Forest Oil, and will cease its

separate existence.

THE INDIVIDUAL DEFENDANTS' FIDUCIARY DUTIES

27. Under New York law, in any situation where the directors of a publicly traded

corporation undertake a transaction that will result in either: (i) a change in corporate control; or

(ii) a breakup of the corporation's assets, the directors have an affirmative fiduciary obligation to

obtain the highest value reasonably available for the corporation's shareholders, including a

significant premium at the highest price attainable in the market. Because control of Forest Oil

is going from a large fluid market (the members of the Class) to a select, small group of affiliated

investors, the Individual Defendants' duty to attain the best possible price for shareholders is

triggered. To diligently comply with these duties, neither the directors nor the officers may take

any action that:

(a) adversely affects the value provided to the corporation's shareholders;

(b) will discourage, inhibit, or deter alternative offers to purchase control of

the corporation or its assets;

(c) contractually prohibits themselves from complying with their fiduciary

duties;

(d) will otherwise adversely affect their duty to secure the best value

reasonably available under the circumstances for the corporation's shareholders; and/or

(e) will provide the directors and/or officers with preferential treatment at the

expense of, or separate from, the public shareholders.

- 8 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 10 of 53

28. In accordance with their duties of loyalty and good faith, the Individual

Defendants, as directors and/or officers of Forest Oil, are obligated under New York law to

refrain from:

(a) participating in any transaction where the directors' or officers' loyalties

are divided;

(b) participating in any transaction where the directors or officers receive, or

are entitled to receive, a personal financial benefit not equally shared by the public shareholders

of the corporation; and/or

(c) unjustly enriching themselves at the expense or to the detriment of the

public shareholders.

29. The Individual Defendants, separately and together, in connection with the

Proposed Transaction, are knowingly or recklessly violating their fiduciary duties and aiding and

abetting such breaches, including their duties of loyalty, good faith, and independence owed to

plaintiffs and other public shareholders of Forest Oil.

30. Defendants are obtaining for themselves personal benefits, including personal

financial benefits not shared equally by plaintiffs or the Class. Accordingly, the Proposed

Transaction will benefit the Individual Defendants in significant ways not shared with Class

members. As a result of the Individual Defendants' self-dealing and divided loyalties, neither

plaintiffs nor the Class will receive adequate or fair value for their Forest Oil common stock in

the Proposed Transaction.

- 9 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 11 of 53

BACKGROUND TO MERGER

31. In 2008, Forest Oil achieved record oil and natural gas production and its stock

price soared to $83.10 per share that year. In recent years, the Company has struggled,

culminating in a billion dollar net loss in 2012. However, the Company started to rebound last

year, recording net earnings of $74 million.

32. Rather than allow its turnaround to play out, for reasons not explained in the

Registration Statement, the Board instead believed it was necessary to conduct a fire sale of the

Company's assets. After conducting a limited process, the Board sold its oil and gas positions

located in the Texas Panhandle area (the "Panhandle Assets") to Templar Energy LLC, an

affiliated company of private equity firm First Reserve Fund XI, L.P. ("First Reserve"), in

November 2013. Instead of using the substantial proceeds from the sale to boost its existing

operations, the Board inexplicably decided to sell the rest of the Company right away.

33. Sensing an opportunity to buy Forest Oil on the cheap and go public at the same

time, at the end of 2013, private oil and gas company Sabine expressed an interest in buying

Forest Oil. Through its controlling shareholder First Reserve (which is an affiliate of the entity

that bought the Panhandle Assets), Sabine was very familiar with the significant value of Forest

Oil's operations and assets. The Board appeared to be resigned to selling the Company to the

first bidder that came its way; after commencing discussions with Sabine in December 2013, it

contacted only a few additional parties and never seriously considered a transaction with any

other entity from that point forward.

34. On February 14, 2014, Sabine submitted a proposal to purchase Forest Oil for an

equity split of 70/30 between Sabine and Forest Oil shareholders. Ultimately, Sabine took

- 10 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 12 of 53

advantage of the lack of competition to lower the equity split to 73.5/26.5, which the Board

readily accepted in approving the Proposed Transaction on May 6, 2014.

THE PROPOSED TRANSACTION

35. On May 6, 2014, Forest Oil and Sabine issued a joint press release announcing the

Proposed Transaction. The press release explained that Sabine and Forest Oil will combine their

businesses in an all-stock transaction to form Sabine Oil & Gas Corporation, which is expected

to list on the New York Stock Exchange under the ticker "SABO." Notably, upon completion of

the combination transaction, Sabine unit holders (which consist almost entirely of the private

equity fund First Reserve and its affiliates) will own approximately 73.5% of the new combined

entity and Forest Oil shareholders will own approximately 26.5%. The press release stated:

Sabine Oil & Gas LLC ("Sabine") and Forest Oil Corporation (NYSE: FST) ("Forest"), today announced the signing of a definitive merger agreement under which Sabine and Forest will combine their businesses in an all-stock transaction. Sabine and Forest's highly complementary asset portfolios will create one of the industry's largest East Texas players, benefiting from drilling program optimization and economies of scale. The combination is also strengthened by a sizable collective Eagle Ford position, as well as Granite Wash, Permian and Arkoma positions that provide optionality for development and monetization.

Upon completion of the combination transaction, Sabine unit holders will own approximately 73.5 percent of the new combined entity and Forest shareholders will own approximately 26.5 percent . The combined entity, named Sabine Oil & Gas Corporation, will be a newly formed parent company expected to list on the New York Stock Exchange under the symbol "SABO". The combined entity will be headquartered in Houston, Texas, and be led by Sabine's current executive management team. The transaction is expected to be tax-free to Forest's shareholders.

* * *

TERMS OF THE TRANSACTION

Under the terms of the agreement, Sabine and Forest Oil will combine their businesses under a newly formed holding company, Sabine Oil & Gas

- 11 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 13 of 53

Corporation ("Sabine Oil & Gas"). Forest Oil will merge with a subsidiary of Sabine Oil & Gas and survive as a subsidiary of Sabine Oil & Gas. As part of the transaction, each share of Forest Oil common stock will be converted into 0.1 of a share of Sabine Oil & Gas common stock, designed to replicate a 10:1 reverse stock split . Concurrent with the merger, Sabine's parent entity will contribute all of its equity interest in Sabine to Sabine Oil & Gas, in exchange for which it will receive approximately 33 million shares of Sabine Oil & Gas common stock. As a result of the transaction, former Sabine unit holders and Forest Oil shareholders will own approximately 73.5% percent and 26.5% percent, respectively, of the outstanding Sabine Oil & Gas common stock upon closing of the combination.

The boards of directors of Sabine and Forest have each unanimously approved the transaction and Forest is recommending approval of the transaction to its shareholders . Consummation of the transaction is subject to approval by the Forest shareholders, regulatory approvals and other customary closing conditions. The transaction is expected to close in the third or fourth quarter of 2014.

Upon completion of the transaction, David Sambrooks will serve as Chairman of the Board of Directors of Sabine Oil & Gas as well as President and Chief Executive Officer. Shane Bayless will serve as Executive Vice President and Chief Financial Officer and Todd Levesque will serve as Executive Vice President and Chief Operating Officer. The Board of Directors of the combined entity will be comprised of the existing six Sabine board members, as well as two of the current Forest board members . At closing, it is expected that at least a majority of the directors will be independent under NYSE rules.

The completion of this transaction will trigger change-of-control provisions in the indentures governing Forest's existing senior notes. These change-of-control provisions entitle holders of the notes to receive 101 percent of the principal amount of the notes plus accrued interest with respect to each series of notes . Sabine expects that any of Forest's notes that are not tendered pursuant to the change of control offers will remain outstanding following the transaction, subject to any opportunistic refinancing of such notes Sabine Oil & Gas may pursue based on market conditions.

36. On May 6, 2014, the Company filed a Current Report on Form 8-K with the SEC

wherein it disclosed the Merger Agreement. Collectively, the announcement of the Proposed

Transaction and the filing of the Merger Agreement reveal that the Proposed Transaction is the

product of a flawed sale process. The Merger Agreement further reveals that the Individual

- 12 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 14 of 53

Defendants agreed to a number of draconian deal protection devices designed to preclude any

competing bids for Forest Oil from emerging in the period following the announcement of the

Proposed Transaction. As the Individual Defendants were duty bound to maximize shareholder

value in connection with the Proposed Transaction, the inclusion of these provisions, as detailed

below, constitutes a further breach of their fiduciary duties.

37. Specifically, section 6.4 of the Merger Agreement subjects Forest Oil to a strict

no-solicitation clause that prohibits the Company from seeking a superior offer for its

shareholders. Section 6.4(a) states that:

Except as expressly permitted by this Section 6.4, Forest shall, and shall cause each of its Subsidiaries and its and their respective directors and officers and shall use reasonable best efforts to cause its and their Representatives to, (i) immediately cease and terminate any solicitation, encouragement, knowing facilitation, discussions, negotiations or other similar activities with any Persons other than New Sabine Holdings and its Affiliates and its and their Representatives that may be ongoing with respect to, or that may reasonably be expected to lead to, an Acquisition Proposal ; and (ii) immediately revoke or withdraw access of any Person other than New Sabine Holdings and its Affiliates and its and their Representatives to any data room (virtual or actual) containing any non-public information with respect to Forest or its Subsidiaries previously furnished with respect to any Acquisition Proposal and request or require (to the fullest extent permitted under any confidentiality agreement or similar agreement with such Person) such Person to promptly return or destroy, as elected by Forest, all confidential information concerning Forest and its Subsidiaries.

38. Though the Merger Agreement ostensibly has a "fiduciary out" provision that

allows the Company to negotiate with other bidders, it may only do so in the rare event that the

potential acquirer first makes a "bona fide, written" acquisition proposal which the Board

determines, in good faith and after consultation with its financial and legal advisors, is "superior"

to the Proposed Transaction. Collectively, the inability of the Company to provide any non-

public information to, much less communicate with, any third-party regarding a potential

- 13 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 15 of 53

transaction—as well as the fact that section 6.4(b) of the Merger Agreement requires Forest Oil

to notify Sabine of any potentially competing inquiry or offer it receives—renders the purported

"fiduciary out" provision illusory and the likelihood of any rival bidder emerging, at best,

miniscule.

39. The likelihood of another offer emerging is even further reduced by the "matching

rights" provision contained in section 6.4(f) of the Merger Agreement. This provision requires

the Company to provide Sabine with copies of the superior proposal and affords Sabine a

remarkable three-business-day window within which to consider and match the terms of any

superior proposal received by the Company, thereby further dissuading any competing bidders

from emerging. Specifically, section 6.4(f) states that the Board of the Company shall not make

a Change of Recommendation unless:

[P]rior to taking such action (i) Forest has given New Sabine Holdings at least three (3) Business Days' prior written notice of its intention to take such action (which notice shall specify the material terms and conditions of any such Superior Proposal (including the identity of the Person making such Superior Proposal)) and has contemporaneously provided to New Sabine Holdings a copy of any proposed transaction agreements with the Person making such Superior Proposal, (ii) Forest has negotiated, and has caused its Representatives to negotiate, in good faith with New Sabine Holdings (in each case, if New Sabine Holdings seeks to negotiate with Forest) during such notice period to enable New Sabine Holdings to revise the terms of this Agreement such that it would cause such Superior Proposal to no longer constitute a Superior Proposal, (iii) following the end of such notice period, the Forest Board shall have considered in good faith any changes to this Agreement proposed in writing by New Sabine Holdings, and shall have determined in good faith, after consultation with its financial advisor and outside legal counsel, that notwithstanding such proposed changes, the third party proposal remains a Superior Proposal, and (iv) Forest has complied in all material respects with its obligations under this Section 6.4. Any amendment to the financial terms or other material terms of a Superior Proposal after delivery of a notice in respect of such Superior Proposal shall require delivery of another notice and shall commence a new three (3) Business Day notice period in respect of such Superior Proposal pursuant to this Section 6.4(f) shall commence. No Forest Recommendation Change shall change the approval of this Agreement for

- 14 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 16 of 53

purposes of Section 902 of the NYBCL, and in no event shall Forest or the Forest Board be permitted to rescind or amend the resolutions approving this Agreement as in effect on the Execution Date. No Forest Recommendation Change shall have the effect of causing any state (including New York) corporate Takeover Law or other similar statute to be applicable to the transactions contemplated by this Agreement (including the Transactions).

40. Section 8.3(b) of the Merger Agreement subjects Forest Oil to another preclusive

deal-protection provision in the form of a $15 million termination fee payable to Sabine should a

superior proposal ultimately be accepted. This additional consideration would be paid directly to

Sabine rather than Forest Oil shareholders, thereby making it even more difficult for any

competing bidder to acquire the Company.

41. Collectively, these onerous and preclusive deal protection devices operate in

conjunction to ensure that no competing offers will emerge for the Company and that the

patently inadequate Proposed Transaction is consummated, thereby guaranteeing that the

Individual Defendants (along with certain other officers of Forest Oil) will secure the personal

financial benefits they negotiated for themselves in connection with the consummation of the

Proposed Transaction. Accordingly, the Individual Defendants' efforts to put their own personal

interests before those of the Company's shareholders have resulted in the Proposed Transaction

being presented to Forest Oil shareholders at a potentially untenable and inadequate offer price

which, arguably, cannot be topped by a competing bidder.

FAILURE TO MAXIMIZE SHAREHOLDER VALUE

42. The Individual Defendants' fiduciary duties require them to maximize shareholder

value when entering into a change-in-control transaction such as the Proposed Transaction. But

they have failed to do so. Rather, Sabine is attempting to take advantage of Forest Oil's recently

depressed stock price to buy the Company on the cheap. Indeed, just prior to the announcement

- 15 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 17 of 53

of the Proposed Transaction, the Company's stock was trading at five-year lows. As recently as

late January 2014, the Company's share price was trading at $3.65 per share, and between

February and May 2014 alone, the Company's stock price fell nearly 30%.

43. The Company's rock bottom share price does not accurately reflect its improving

financial performance and strong prospects. The Company recently has begun to turnaround its

financial performance and is becoming profitable. According to Forest Oil's Annual Report on

Form 10-K filed with the SEC on February 26, 2014, the Company was able to overcome a $1.3

billion loss in 2012 to achieve nearly $74 million in net earnings in 2013. In a call with financial

analysts on February 26, 2014, defendant McDonald, the Company's President, CEO, and a

director, discussed the factors that contributed to the Company's improvement. Specifically,

defendant McDonald stated that the Company was "able to accomplish a number of the strategic

goals [management] set forth for 2013. [The Company's] objectives were to accelerate the

development of [its] oil assets, principally the Eagle Ford; improve [its] operational focus by

directing [the Company's] efforts to the assets where [it] had a confidence and resources

development, and importantly, to reduce the debt level of the company."

44. In addition, the Company's production greatly increased in 2013. As defendant

McDonald explained, "[o]il and liquids volume increased over [2013] as net oil sales volumes

grew by 55%, net liquid sales volume grew 41% compared to 2012 pro forma for divestitures.

[The Company's] oil reserves grew by 30%. [Management] believe[s] this trend will continue in

2014."

45. Defendant McDonald also discussed the progress made in developing the

Company's Eagle Ford assets through a joint development agreement. Defendant McDonald

- 16 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 18 of 53

touted the benefits of the agreement, such as "providing the capital required to increase the

drilling activity as well as access to impressive technology, which will pay benefits now and in

the future."

46. Moreover, the Company was able to significantly reduce its debt through the sale

of its Texas Panhandle and South Texas assets, which generated cash proceeds of approximately

$1.3 billion. As of the end of 2013, the Company was able to reduce its net debt by more than

50% from the end of 2012.

47. Regarding the Company's outlook for 2014, Victor A. Wind, the Company's

Executive Vice President and Chief Financial Officer stated, "[Forest Oil's] equivalent net sales

volumes are expected to increase on a quarterly basis throughout 2014, although [the Company]

should see a notable uptick in second-half volumes compared to the first half as [the Company]

benefit[s] from the increased Ark-La-Tex activity.... Carrying the growth trajectory of this

program forward into 2015, one could reasonably assume [the Company would] have robust

growth in 2015 over 2014."

48. Accordingly, Forest Oil is poised for a significant recovery despite its depressed

stock price. However, the Proposed Transaction comes at a time when Sabine can acquire the

Company at a bargain price and reap an outsized portion of the rewards of Forest Oil's recovery.

49. In addition to taking advantage of the momentum in Forest Oil's recovery, there

are substantial synergies created by the merger. Sabine and Forest Oil's highly complementary

asset portfolios will create one of the industry's largest East Texas players, benefiting from

drilling program optimization and economies of scale. The combination is also strengthened by

a sizable collective Eagle Ford position, as well as Granite Wash, Permian, and Arkoma

- 17 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 19 of 53

positions that provide opportunities for development and monetization. The considerable

overlapping in these two asset areas will result in substantial cost savings from reduced overhead

and streamlined operations. In addition, the combined company will have estimated proved

reserves of 1.50 trillion cubic feet and estimated daily production of 345 million cubic feet for

2014, giving the new company a leading position among its industry peers in production and

cash flow growth. With defendants' failure to provide financial information about the post-

closing company, there is no way to know whether members of the Class are being fairly

compensated for the synergies detailed herein.

50. As reflected by the table below, the proposed equity split is also unfair to Forest

Oil shareholders in light of the relative financial and asset strength of the two companies. Most

notably, Forest Oil's share of the proved reserves of the combined companies is approximately

43%, well in excess of the 26.5% equity share its shareholders are receiving in the Proposed

Transaction.

Pro Forma Combined Forest Oil % of

Metric Sabine Forest Oil Company Pro Forma

1Q14 Production (MBOE/Day) 30.80 17.50 48.30* 36.23%*

YE13 Proved Reserves (Bcfe) 839 625 1,464 42.69%

FY2014E Production Guidance

(Mmcfe/d) 220 125 345 36.23%

1Q14 Revenue (in millions) $112.72 $65.19 $177.91 36.64%

* Denotes approximation based on unadjusted financial and operating results reported by Sabine

and Forest Oil.

THE INSIDER BENEFITS PROVIDED BY THE PROPOSED TRANSACTION

51. In order to meet their fiduciary duties, the Individual Defendants are obligated to

explore transactions that will maximize shareholder value, and not structure a preferential deal

- 18 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 20 of 53

for themselves. Here, however, the Individual Defendants have disloyally placed their own

interests first, and tailored the terms of the Proposed Transaction so as to aggrandize their own

financial positions.

52. Defendant McDonald, the Company's CEO and a director, will receive the biggest

windfall upon consummation of the Proposed Transaction including a cash severance payment

equal to 2.5 times the sum of his annual salary and annual bonus and vesting of all his all

outstanding stock options, restricted stock, and cash-settled phantom stock units. As stated in the

Company's Schedule 14A Definitive Proxy Statement filed with the SEC on March 26, 2014,

following the Proposed Transaction, defendant McDonald will be entitled to receive:

• a cash severance payment consisting of a lump sum payment in an amount equal to 2.5 times the sum of his ... annual salary and annual bonus ;

* * *

• vesting of all outstanding stock options, restricted stock, and cash-settled phantom stock units to the extent described in the applicable award agreement;

* * *

• with respect to the performance unit awards granted prior to October 1, 2012, [defendant MacDonald] will be entitled to receive a number of shares of common stock that would have been earned based on Forest's total shareholder return in comparison to its peer companies, assuming the date of the change-of-control as the last day of the performance period [which may be settled in cash at the discretion of the Compensation Committee];

* * *

• with respect to the performance unit awards granted on or after October 1, 2012, if the successor entity does not assume or replace such awards with awards substantially similar in all material respects, [defendant MacDonald] will be entitled to receive a number of shares of common stock, or an amount of cash, that would have been earned based on

- 19 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 21 of 53

Forest's total shareholder return in comparison to its peer companies, assuming the date of change-of-control as the last day of the performance period [which may be settled in cash at the discretion of the Compensation Committee].

53. The completion of the Proposed Transaction will also trigger change-of-control

provisions for holders of Forest Oil's existing senior notes. These change-of-control provisions

entitle holders of the notes to receive 101% of the principal amount of the notes plus accrued

interest with respect to each series of notes.

54. In addition, the Board has ensured that at least two of its members will retain their

prestigious positions following completion of the Proposed Transaction. As such, the board of

directors of the combined entity will be comprised of the existing six Sabine board members, as

well as two of the current Forest Oil Board members.

55. In short, the Proposed Transaction is wrongful, unfair, and harmful to Forest Oil's

public stockholders, and represents an effort by the Individual Defendants to aggrandize their

own financial positions and interests at the expense and to the detriment of the Class.

Specifically, defendants are attempting to deny plaintiffs and the Class their shareholder rights

through the sale of Forest Oil via a potentially unfair process. Accordingly, the Proposed

Transaction will benefit the Individual Defendants at the expense of Forest Oil shareholders.

56. In order to meet their fiduciary duties, the Individual Defendants are obligated to

explore transactions that will maximize shareholder value, and not structure a preferential deal

for themselves. Due to the Individual Defendants' eagerness to enter into a transaction with

Sabine, they failed to implement a process to obtain the maximum price for Forest Oil

shareholders.

- 20 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 22 of 53

57. As a result of defendants' conduct, Forest Oil's public stockholders have been and

will continue to be denied the fair process and arm's-length negotiated terms to which they are

entitled in a sale of their Company. In light of the foregoing, the Individual Defendants must, as

their fiduciary obligations require:

• Withdraw their consent to the sale of Forest Oil and allow the shares to trade freely—without impediments such as the aforementioned no-solicitation, matching rights, and termination fee provisions;

• Act independently so that the interests of Forest Oil's public stockholders will be protected;

• Adequately ensure that no conflicts of interest exist between defendants' own interests and their fiduciary obligation to maximize stockholder value or, if such conflicts exist, to ensure that all conflicts be resolved in the best interests of Forest Oil's public stockholders; and

• Solicit competing bids to Sabine's offer without the impediments listed above to ensure that the Company's shareholders are receiving the maximum value for their shares.

THE MATERIALLY MISLEADING REGISTRATION STATEMENT

58. On May 29, 2014, defendants filed with the SEC the Registration Statement in

which they recommended that Forest Oil shareholders vote in favor of the Proposed Transaction.

The Registration Statement is materially false and misleading because, in violation of sections

14(a) and 20(a) of the Exchange Act, it fails to disclose all information that Forest Oil

shareholders would consider important in making a rational and fully-informed decision as to

whether to vote for the Proposed Transaction. Specifically, the Registration Statement fails to

provide the Company's shareholders with material information and/or provides materially

misleading information regarding (i) the process leading to the Proposed Transaction; (ii) the

- 21 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 23 of 53

financial analyses performed by the Company's financial advisor, J.P. Morgan; and (iii) the

Company's financial projections.

The Sales Process Leading to the Proposed Transaction

59. With respect to the process that led to the Proposed Transaction, the Registration

Statement is materially deficient and misleading because it fails to disclose:

(a) the number of parties with which Forest Oil engaged in discussions

regarding a sale of the Panhandle Assets and of these, the number of parties which submitted

bids and the value of any such bids;

(b) the number of parties that expressed an interest in a joint venture with

Forest Oil, which is referenced on page 70 of the Registration Statement, whether any submitted

a proposal and if so, the number of parties and the terms of any such proposals;

(c) whether Forest Oil or its advisors calculated the estimated values of

synergies expected to result from the Proposed Transaction (and in particular the synergies

resulting from related entities purchasing both the Panhandle Assets and the remaining

Company), when any such analyses were conducted and the resulting values;

(d) the number of parties Forest Oil management and J.P. Morgan identified

and contacted about a potential merger in or after November 2013 and the criteria used to select

them;

(e) the amount of First Reserve's equity interest in Sabine and whether First

Reserve also has an equity interest in the entity (Templar Energy) that purchased the Company's

Panhandle Assets and if so, how much; and

- 22 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 24 of 53

(f) the total amount of compensation received by J.P. Morgan for all services

rendered to Forest Oil, First Reserve or their respective affiliates for the two years prior to

rendering the fairness opinion for the Proposed Transaction.

60. The omission of this information makes the following statements in the

Registration Statement materially misleading:

(a) on pages 68-69 of the Registration Statement, the statements:

In June 2013, the Forest board reviewed Forest's strategic positioning and, in light of the interest in the Panhandle Assets expressed by several parties and Forest's substantial leverage, the Forest board instructed J.P. Morgan, which had been engaged effective as of May 2, 2013 as Forest's financial advisor in connection with its exploration of strategic alternatives, to commence a public sale process for the Panhandle Assets and, at the same time, to assess potential interest in a merger or sale transaction involving all of Forest. Forest and J.P. Morgan commenced the Panhandle Asset sale process on July 15, 2013. Concurrently with, and, in some cases, as part of, the Panhandle Asset sale process, from mid-July through early October 2013, J.P. Morgan contacted or was contacted by approximately 12 industry participants who were considered likely to be interested in, and capable of consummating, a merger or sale transaction involving all of Forest (or all of Forest excluding the Panhandle Assets). While some indicated some initial interest and engaged in some discussions with Forest or J.P. Morgan, ultimately, none of these 12 parties indicated interest in moving forward. During this time, Forest received bids to acquire the Panhandle Assets and, in a transaction announced on October 3, 2013 and completed on November 25, 2013, Forest sold the Panhandle Assets to Templar Energy LLC for approximately $1.0 billion in cash. Templar Energy is a portfolio company of a fund related to First Reserve. In November 2013, Forest used approximately $840 million of the sale proceeds to repurchase outstanding senior notes and to repay the outstanding balance on its revolving credit facility.

(b) on page 69 of the Registration Statement, the statements:

Following the announcement of the Panhandle Asset sale, Forest received inquiries from a few industry participants (including some of the ones previously identified or contacted as having potential interest) regarding a possible strategic transaction involving all of Forest (excluding the Panhandle Assets), and the Forest board instructed management and J.P. Morgan to contact select additional parties that could potentially be interested in such a transaction. As a result, from November 2013 through February 2014, Forest engaged in discussions and, in

- 23 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 25 of 53

some cases, due diligence with eight potentially interested parties, in addition to Sabine.

(c) on page 70 of the Registration Statement, the statements:

On February 12, 2014, the Forest board met for a regularly scheduled meeting. At this meeting, which was attended by members of management, J.P. Morgan and Wachtell, Lipton, Rosen & Katz, Forest's outside legal counsel ("Wachtell Lipton"), the Forest directors received an update on the status of ongoing discussions, which were continuing at that time with Sabine and the two other parties potentially interested in a transaction involving all of Forest, and with several parties potentially interested in a joint venture alternative. The Forest board authorized management to continue to pursue all alternatives.

* * *

On February 26 and 27, 2014, Messrs. McDonald and Sambrooks met in Denver. During these meetings, Messrs. McDonald and Sambrooks discussed synergy potential and operational and personnel matters relevant to a merger of Forest and Sabine, and confirmed to each other that their respective boards of directors remained interested in a transaction. Mr. Sambrooks conveyed the concern expressed by the Sabine board over the decrease in Forest's stock price, but did not propose a change in the sharing ratio.

(d) on page 71 of the Registration Statement, the statement:

On March 25, 2014, Messrs. McDonald and Sambrooks met in Houston to continue discussions concerning operational matters and potential synergies that might be achieved by a merger of Forest and Sabine.

(e) on page 84 of the Registration Statement, the statements:

During the two years preceding delivery of its opinion, neither J.P. Morgan nor its affiliates have had any material financial advisory or other material commercial or investment banking relationships with Sabine Investor Holdings. During the two years preceding delivery of its opinion, J.P. Morgan and its affiliates have had commercial or investment banking relationships with Forest and certain portfolio companies of First Reserve Corporation, for which J.P. Morgan and such affiliates have received customary compensation. Such services during such period have included acting as (i) joint bookrunner on an offering of Forest's debt securities in September 2012 and as Forest's financial advisor in connection with the sale of certain of its oil and gas assets to Templar Energy LLC in November 2013 and (ii) financial advisor for certain transactions, joint bookrunner on offerings of debt and equity securities and arranger on certain credit facilities for certain portfolio companies of First Reserve Corporation. In addition, J.P. Morgan's commercial

- 24 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 26 of 53

banking affiliate is an agent bank and a lender under outstanding credit facilities of Forest, for which it receives customary compensation or other financial benefits. In the ordinary course of their businesses, J.P. Morgan and its affiliates may actively trade the debt and equity securities of Forest for their own account or for the accounts of customers and, accordingly, J.P. Morgan and its affiliates may at any time hold long or short positions in such securities.

61. These statements are rendered misleading by the omissions because they give a

materially incomplete and distorted picture of the sales process.

JP Morgan's Financial Analyses

62. J.P. Morgan's Public Trading Multiples Analysis. The description of J.P.

Morgan's Public Trading Analysis on pages 79-81 of the Registration Statement is materially

deficient and misleading because it fails to disclose:

(a) The individually observed multiples for each of the selected companies

used in the analysis, including the following multiples:

(i) equity value/2014 estimated ("E") cash flow;

(ii) equity value/2015E cash flow;

(iii) firm value/2014E earnings before interest, taxes, depreciation,

amortization and exploration expenses ("EBITDAX");

(iv) firm value/2015E EBITDAX;

(v) firm value/4Q 2013 production; and

(vi) firm value/FY2014 production;

(b) the resulting implied equity value ranges for both sets of Forest Oil's

projections (base and adjusted) and both sets of Sabine's projections (base and adjusted) for each

of the above multiples; and

- 25 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 27 of 53

(c) whether, and to what extent, J.P. Morgan conducted any kind of

benchmarking analyses for Forest Oil and Sabine in relation to the selected companies.

63. The omission of this information renders the following statements in the

Registration Statement materially misleading:

(a) on pages 76-77 of the Registration Statement, the statements:

At the meeting of the Forest board on May 5, 2014, J.P. Morgan rendered its oral opinion to the Forest board that, as of such date and based upon and subject to the factors, assumptions, limitations and qualifications set forth in such opinion, the exchange ratio in the proposed transactions contemplated by the merger agreement was fair, from a financial point of view to the holders of Forest common stock. J.P. Morgan confirmed its May 5, 2014 oral opinion by delivering its written opinion to the Forest board, dated May 5, 2014, that, as of such date, the exchange ratio in the proposed transactions contemplated by the merger agreement was fair, from a financial point of view, to the holders of Forest common stock. No limitations were imposed by the Forest board upon J.P. Morgan with respect to the investigations made or procedures followed by it in rendering its opinion.

(b) on pages 79-81 of the Registration Statement, the statements:

Public Trading Multiples Analysis

Using publicly available information, J.P. Morgan compared selected financial data of Forest and Sabine with similar data for publicly traded companies engaged in businesses which J.P. Morgan judged to be sufficiently analogous to Forest's and Sabine's businesses or aspects thereof.

For Forest, the companies selected by J.P. Morgan were as follows:

• Goodrich Petroleum Corporation • Midstates Petroleum Company, Inc. • Penn Virginia Corporation • PetroQuest Energy, Inc.

For Sabine, the companies selected by J.P. Morgan were as follows:

• Forest • Goodrich Petroleum Corporation • Jones Energy, Inc.

- 26 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 28 of 53

• Midstates Petroleum Company, Inc. • Penn Virginia Corporation • PetroQuest Energy, Inc. • SandRidge Energy, Inc.

These companies were selected for each of Forest and Sabine, among other reasons, because they are publicly traded companies with operations and businesses that, for purposes of J.P. Morgan's analysis, may be considered similar to those of Forest and Sabine based on the nature of their assets and operations and the form and geographic location of their operations. However, certain of these companies may have characteristics that are materially different from those of Forest and Sabine. The analyses necessarily involve complex considerations and judgments concerning differences in financial and operational characteristics of the companies involved and other factors that could affect the companies differently than would affect Forest or Sabine.

For each company listed above, J.P. Morgan calculated and compared various financial multiples and ratios based on publicly available information as of May 2, 2014. Among other calculations, the information J.P. Morgan calculated for each of the selected companies included:

• Multiple of equity value (calculated as the market value of the company's common stock on a fully diluted basis) to research analysts' consensus estimates for cash flow (calculated as earnings before interest, taxes, depreciation, amortization and exploration expenses ("EBITDAX"), less interest expense and taxes) for the fiscal years ended December 31, 2014 and December 31, 2015;

• Multiple of firm value (calculated as equity value plus debt and other adjustments, including non-controlling interest and preferred stock, less cash) to research analysts' consensus estimates for EBITDAX for the fiscal years ended December 31, 2014 and December 31, 2015; and

• Multiple of firm value to production (in dollars per thousand cubic feet equivalents per day ("$/Mcfepd")) for the fiscal quarter ended December 31, 2013 ("4Q 2013 production") and estimated production for the fiscal year ended December 31, 2014.

Results of the analysis for Forest and Sabine, respectively, are as follows:

Forest

Mean

Mdiaji - 27 -

Pr Group Trading Multiples

Equity value to &ijiicd FLrm value to imted Lash now [BITDAX

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 29 of 53

Based on the results of this analysis, J.P. Morgan selected multiple reference ranges for Forest of 1.5x – 3.0 x and 1.0x – 2.5x for equity value to estimated 2014 and 2015 cash flow, respectively, ranges of 4.5x – 5.5x and 4.0x – 4.5x for firm value to estimated 2014 and 2015 EBITDAX, respectively, and ranges of $11,000 - $14,000 and $9,500 - $12,500 for firm value to 4Q 2013 production and estimated 2014 production, respectively.

After applying such ranges to the appropriate metrics for Forest based on the Base Forest Budget Projections, this analysis indicated the following implied equity value per share ranges for Forest shares:

Forest Implied Equity Value Per Share Rmige-Base Forest Budget Projections

High Low

Equity value to eifimated Firm valueto estimated cb flow EBITDAX

2014E 2015E 2014E 20ISE

$ 3.57 S 4.81 S 118 $ 4.87

1.78 $ 1.92 S lAS S 3.64

Firm value to prodacioui {Mefpd

4Q2.013 2014E $ 6.97 S 7.7 $ 4.07 S 3.89

After applying such ranges to the appropriate metrics for Forest based on the Adjusted Forest Projections, the analysis indicated the following implied equity value per share ranges for Forest shares:

Foresl Implied Equity Value Per Share Range-Adjusted Forest Projections

High Low

Equity value to estimated cash now

2014E 201SE $ 2 .72 $ 4.08 $ 1.36 $ 1.63

Finn value to estimated EBITDAX

OI4E 2015E

$ 1.97 $ 3.56 $ 048 S 2.4

Firm value to production ($Th1depd

4Q2013 2014E N/A $ 6.50 NA £ 346

The ranges of implied equity values per Forest share based on the Base Forest Budget Projections and the Adjusted Forest Projections were compared to Forest's closing share price of $1.77 on May 2, 2014.

Sabine

Peer Group Trading MuItipls

Mean

Median

Equity uluelo estimated Firm value to estimated cath flow EIIITDAX

2014E 10I5E

2014E 2015E

lix 2.x

5,9x 47x 3.Ox 14x

4.9x 41x

Finn vilue to priidudion (Mefpd)

4Q 2013 2014E

$

14,175 $ 11,931 $ 2,780 $ I1,06

- 28 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 30 of 53

Based on the results of this analysis, J.P. Morgan selected multiple reference ranges for Sabine of 2.0x – 3.5x and 1.5x – 3.0x for equity value to estimated 2014 and 2015 cash flow, respectively, ranges of 5.0x – 6.0x and 4.0x – 5.0x for firm value to estimated 2014 and 2015 EBITDAX, respectively, and a range of $11,500 – $14,500 and $10,000 – $13,000 for firm value to 4Q 2013 production and estimated 2014 production, respectively.

After applying such ranges to the appropriate metrics for Sabine based on the Base Sabine Budget Projections, the analysis indicated the following implied equity value ranges for Sabine:

Sabine Implied Equity Value Range—Base Sabine Budget Projection

High Low

E1ityvIIuE t hinitd Fbm value to ntimated cash flow £BITFIAX

2014E 101gE1F 2014E 201EI' 016 S 1,249 $ 1,041 $ 1,466 523 $ 624 662 S 927

Thw uhe lis prodQtiID

(MthpJ

4Q 2413 2014E

S 1,827 $ 1,680 S 1,194 $ [,OO

() Using the corrected Base Sabine Budget rediorwou]d indicate a low of$5Th million and ahigh of $1,155 (2) Using the corrected Base Sabine Budget Projeconswould indicate alaw Df $805 million and a l]igIl of $1,314 million.

After applying such ranges to the appropriate metrics for Sabine based on the Adjusted Sabine Projections, the analysis indicated the following implied equity value ranges for Sabine:

Sabine Implied Equity Value Range—Adjusted Sabine Projections

High Low

Equity VD]UC to estimated Firm value to estimated

cash flow EBITDAX 2014E2OIL 2014E 2015L

$ 849 S 979 $ 928 $ 1,026 $ 485 S 490 $ 568 574

Firm 4ue to production

(iMthpiI)

4Q2013 2014E

NIA $ 1,640

NA 978

64. J.P. Morgan's Net Asset Value Analysis . The description of J.P. Morgan's Net

Asset Value Analysis on pages 81-82 of the Registration Statement is materially deficient

because its fail to disclose:

(a) the time period of the financial projections for Forest Oil used in this

analysis and which years were part of the estimates provided by Forest Oil's management and

which were extrapolations by J.P. Morgan;

- 29 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 31 of 53

(b) whether J.P. Morgan used a terminal period calculation for Forest Oil in

this analysis (and if so, what it was) or whether the projection period was extended to the

anticipated end of Forest Oil's potential production;

(c) whether stock-based compensation for Forest Oil was included in the

general and administrative expenses for purposes of this analysis and if not, how it was

accounted for in this analysis;

(d) the specific inputs and assumptions used to determine the discount rate

range (of 10.5-12.0%) for Forest Oil applied in this analysis;

(e) the time period of the financial projections for Sabine used in this analysis

and which years were part of the estimates provided by Forest Oil's management and which were

extrapolations by J.P. Morgan;

(f) whether J.P. Morgan used a terminal period calculation for Sabine in this

analysis (and if so, what it was) or whether the projection period was extended to the anticipated

end of Forest Oil's potential production;

(g) whether stock-based compensation for Sabine was included in the general

and administrative expenses for purposes of this analysis and if not, how it was accounted for in

this analysis; and

(h) the specific inputs and assumptions used to determine the discount rate

range (of 9.0-10.5%) for Sabine applied in this analysis.

65. The omission of this information renders the following statements in the

Registration Statement materially misleading:

- 30 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 32 of 53

(a) on pages 76-77 of the Registration Statement, the statements:

At the meeting of the Forest board on May 5, 2014, J.P. Morgan rendered its oral opinion to the Forest board that, as of such date and based upon and subject to the factors, assumptions, limitations and qualifications set forth in such opinion, the exchange ratio in the proposed transactions contemplated by the merger agreement was fair, from a financial point of view to the holders of Forest common stock. J.P. Morgan confirmed its May 5, 2014 oral opinion by delivering its written opinion to the Forest board, dated May 5, 2014, that, as of such date, the exchange ratio in the proposed transactions contemplated by the merger agreement was fair, from a financial point of view, to the holders of Forest common stock. No limitations were imposed by the Forest board upon J.P. Morgan with respect to the investigations made or procedures followed by it in rendering its opinion.

(b) on pages 81-82 of the Registration Statement, the statements:

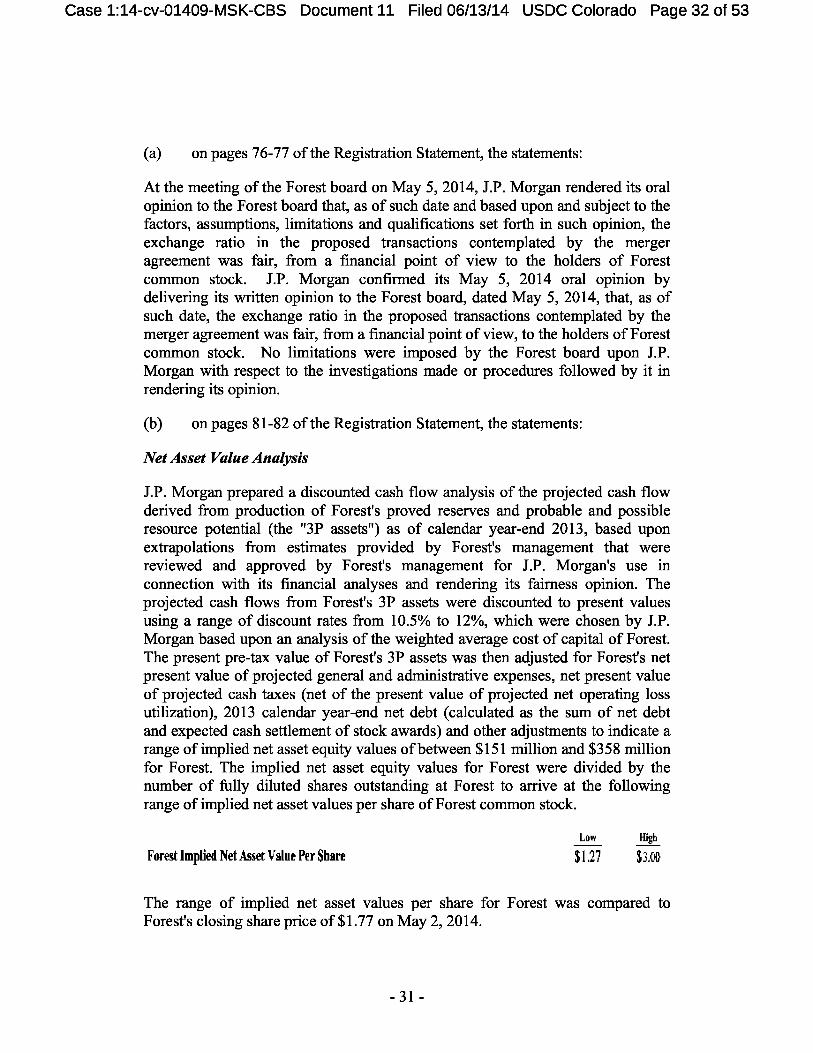

Net Asset Value Analysis

J.P. Morgan prepared a discounted cash flow analysis of the projected cash flow derived from production of Forest's proved reserves and probable and possible resource potential (the "3P assets") as of calendar year-end 2013, based upon extrapolations from estimates provided by Forest's management that were reviewed and approved by Forest's management for J.P. Morgan's use in connection with its financial analyses and rendering its fairness opinion. The projected cash flows from Forest's 3P assets were discounted to present values using a range of discount rates from 10.5% to 12%, which were chosen by J.P. Morgan based upon an analysis of the weighted average cost of capital of Forest. The present pre-tax value of Forest's 3P assets was then adjusted for Forest's net present value of projected general and administrative expenses, net present value of projected cash taxes (net of the present value of projected net operating loss utilization), 2013 calendar year-end net debt (calculated as the sum of net debt and expected cash settlement of stock awards) and other adjustments to indicate a range of implied net asset equity values of between $151 million and $358 million for Forest. The implied net asset equity values for Forest were divided by the number of fully diluted shares outstanding at Forest to arrive at the following range of implied net asset values per share of Forest common stock.

Low High Forest Implied Net Asset Value Per Share $1.27 $300

The range of implied net asset values per share for Forest was compared to Forest's closing share price of $1.77 on May 2, 2014.

- 31 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 33 of 53

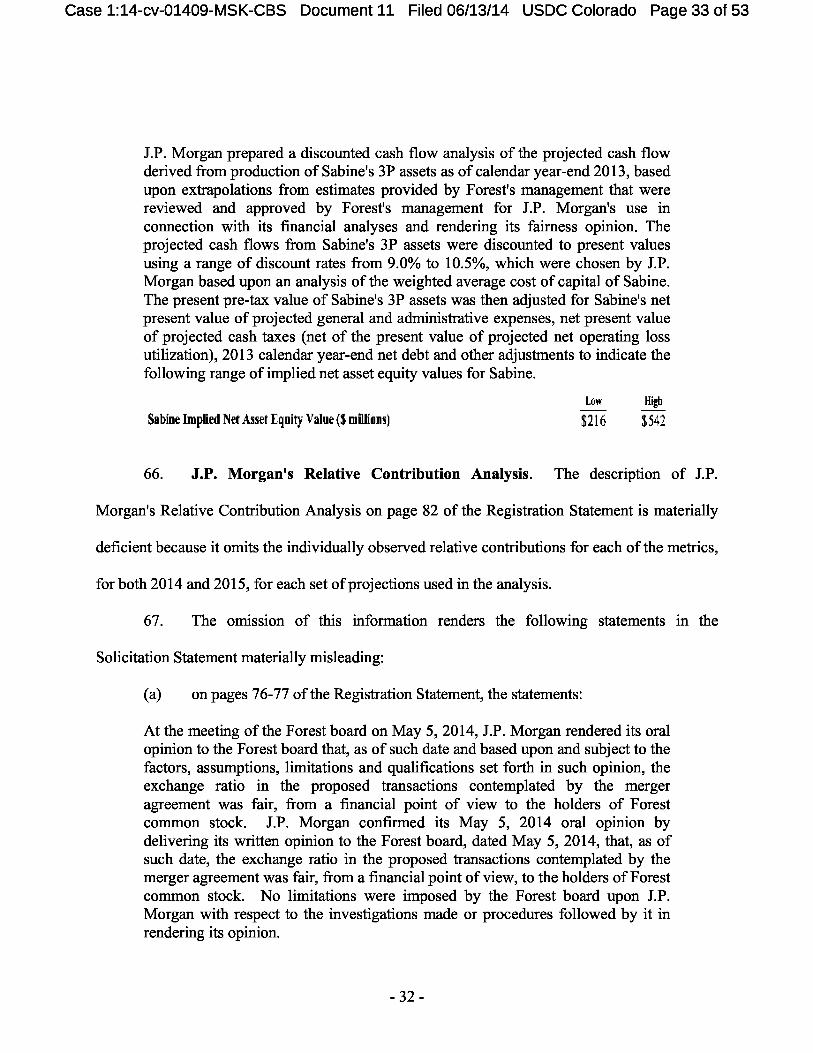

J.P. Morgan prepared a discounted cash flow analysis of the projected cash flow derived from production of Sabine's 3P assets as of calendar year-end 2013, based upon extrapolations from estimates provided by Forest's management that were reviewed and approved by Forest's management for J.P. Morgan's use in connection with its financial analyses and rendering its fairness opinion. The projected cash flows from Sabine's 3P assets were discounted to present values using a range of discount rates from 9.0% to 10.5%, which were chosen by J.P. Morgan based upon an analysis of the weighted average cost of capital of Sabine. The present pre-tax value of Sabine's 3P assets was then adjusted for Sabine's net present value of projected general and administrative expenses, net present value of projected cash taxes (net of the present value of projected net operating loss utilization), 2013 calendar year-end net debt and other adjustments to indicate the following range of implied net asset equity values for Sabine.

Low High Sabine Implied Net Asset Equity Value ( millions) $216 $542

66. J.P. Morgan's Relative Contribution Analysis . The description of J.P.

Morgan's Relative Contribution Analysis on page 82 of the Registration Statement is materially

deficient because it omits the individually observed relative contributions for each of the metrics,

for both 2014 and 2015, for each set of projections used in the analysis.

67. The omission of this information renders the following statements in the

Solicitation Statement materially misleading:

(a) on pages 76-77 of the Registration Statement, the statements:

At the meeting of the Forest board on May 5, 2014, J.P. Morgan rendered its oral opinion to the Forest board that, as of such date and based upon and subject to the factors, assumptions, limitations and qualifications set forth in such opinion, the exchange ratio in the proposed transactions contemplated by the merger agreement was fair, from a financial point of view to the holders of Forest common stock. J.P. Morgan confirmed its May 5, 2014 oral opinion by delivering its written opinion to the Forest board, dated May 5, 2014, that, as of such date, the exchange ratio in the proposed transactions contemplated by the merger agreement was fair, from a financial point of view, to the holders of Forest common stock. No limitations were imposed by the Forest board upon J.P. Morgan with respect to the investigations made or procedures followed by it in rendering its opinion.

- 32 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 34 of 53

(b) on page 82 of the Registration Statement, the statements:

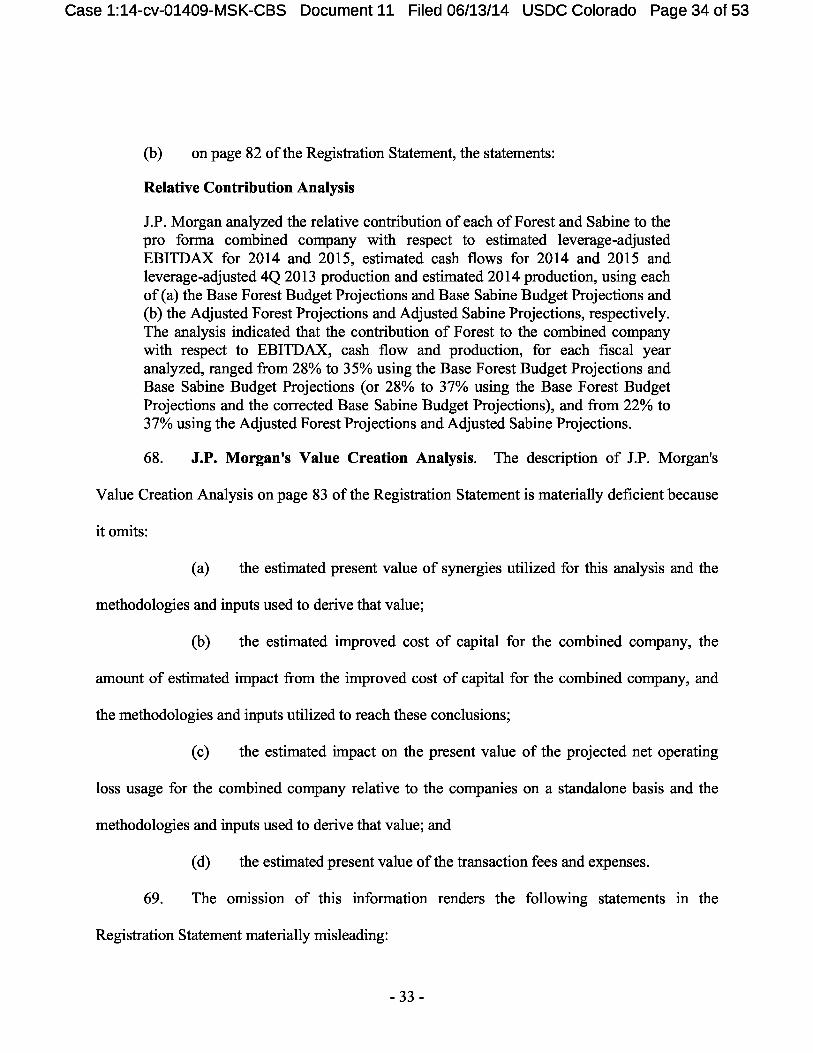

Relative Contribution Analysis

J.P. Morgan analyzed the relative contribution of each of Forest and Sabine to the pro forma combined company with respect to estimated leverage-adjusted EBITDAX for 2014 and 2015, estimated cash flows for 2014 and 2015 and leverage-adjusted 4Q 2013 production and estimated 2014 production, using each of (a) the Base Forest Budget Projections and Base Sabine Budget Projections and (b) the Adjusted Forest Projections and Adjusted Sabine Projections, respectively. The analysis indicated that the contribution of Forest to the combined company with respect to EBITDAX, cash flow and production, for each fiscal year analyzed, ranged from 28% to 35% using the Base Forest Budget Projections and Base Sabine Budget Projections (or 28% to 37% using the Base Forest Budget Projections and the corrected Base Sabine Budget Projections), and from 22% to 37% using the Adjusted Forest Projections and Adjusted Sabine Projections.

68. J.P. Morgan's Value Creation Analysis . The description of J.P. Morgan's

Value Creation Analysis on page 83 of the Registration Statement is materially deficient because

it omits:

(a) the estimated present value of synergies utilized for this analysis and the

methodologies and inputs used to derive that value;

(b) the estimated improved cost of capital for the combined company, the

amount of estimated impact from the improved cost of capital for the combined company, and

the methodologies and inputs utilized to reach these conclusions;

(c) the estimated impact on the present value of the projected net operating

loss usage for the combined company relative to the companies on a standalone basis and the

methodologies and inputs used to derive that value; and

(d) the estimated present value of the transaction fees and expenses.

69. The omission of this information renders the following statements in the

Registration Statement materially misleading:

- 33 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 35 of 53

(a) on pages 76-77 of the Registration Statement, the statements:

At the meeting of the Forest board on May 5, 2014, J.P. Morgan rendered its oral opinion to the Forest board that, as of such date and based upon and subject to the factors, assumptions, limitations and qualifications set forth in such opinion, the exchange ratio in the proposed transactions contemplated by the merger agreement was fair, from a financial point of view to the holders of Forest common stock. J.P. Morgan confirmed its May 5, 2014 oral opinion by delivering its written opinion to the Forest board, dated May 5, 2014, that, as of such date, the exchange ratio in the proposed transactions contemplated by the merger agreement was fair, from a financial point of view, to the holders of Forest common stock. No limitations were imposed by the Forest board upon J.P. Morgan with respect to the investigations made or procedures followed by it in rendering its opinion.

(b) on pages 83 of the Registration Statement, the statements:

Value Creation Analysis

J.P. Morgan conducted an analysis of the theoretical value creation to the holders of Forest common stock that compared the estimated implied equity value of Forest on a standalone basis based on the midpoint value determined in J.P. Morgan's Net Asset Value Analysis described above to the implied equity value of Forest shares pro forma for the proposed transactions contemplated by the merger agreement. J.P. Morgan calculated the pro forma implied equity value of Forest shares by (1) adding the sum of (a) the implied equity value of Forest using the midpoint value determined in J.P. Morgan's Net Asset Value Analysis described above, (b) the implied equity value of Sabine using the midpoint value determined in J.P. Morgan's Net Asset Value Analysis described above, (c) the estimated present value of the Synergies and (d) the estimated impact of improved cost of capital of the combined company relative to the estimated cost of capital for Forest on a standalone basis, (2) subtracting the sum of (a) the estimated implied impact on the present value of the projected net operating loss usage for the combined company relative to the estimated present value of the net operating loss usage of each company on a standalone basis and (b) the estimated present value of transaction fees and expenses relating to the transactions contemplated by the merger agreement, and (3) multiplying such sum of the estimated valuations described above by a factor of 26.5%, representing the approximate pro forma equity ownership of the combined company by the holders of Forest common stock. Based on the assumptions described above, this analysis implied value creation for the holders of Forest common stock of approximately 5.0%.

J.P. Morgan also conducted an analysis of the theoretical value creation to the holders of Forest common stock that compared the equity value of Forest based

- 34 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 36 of 53

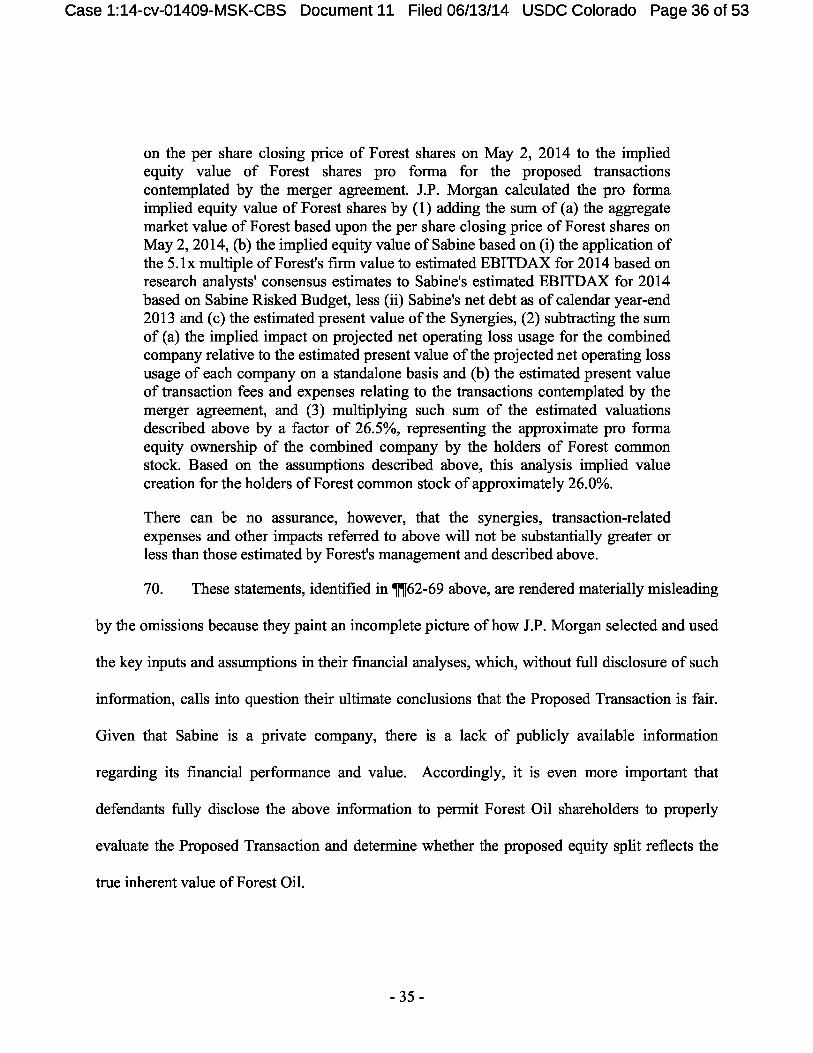

on the per share closing price of Forest shares on May 2, 2014 to the implied equity value of Forest shares pro forma for the proposed transactions contemplated by the merger agreement. J.P. Morgan calculated the pro forma implied equity value of Forest shares by (1) adding the sum of (a) the aggregate market value of Forest based upon the per share closing price of Forest shares on May 2, 2014, (b) the implied equity value of Sabine based on (i) the application of the 5.1x multiple of Forest's firm value to estimated EBITDAX for 2014 based on research analysts' consensus estimates to Sabine's estimated EBITDAX for 2014 based on Sabine Risked Budget, less (ii) Sabine's net debt as of calendar year-end 2013 and (c) the estimated present value of the Synergies, (2) subtracting the sum of (a) the implied impact on projected net operating loss usage for the combined company relative to the estimated present value of the projected net operating loss usage of each company on a standalone basis and (b) the estimated present value of transaction fees and expenses relating to the transactions contemplated by the merger agreement, and (3) multiplying such sum of the estimated valuations described above by a factor of 26.5%, representing the approximate pro forma equity ownership of the combined company by the holders of Forest common stock. Based on the assumptions described above, this analysis implied value creation for the holders of Forest common stock of approximately 26.0%.

There can be no assurance, however, that the synergies, transaction-related expenses and other impacts referred to above will not be substantially greater or less than those estimated by Forest's management and described above.

70. These statements, identified in ¶¶62-69 above, are rendered materially misleading

by the omissions because they paint an incomplete picture of how J.P. Morgan selected and used

the key inputs and assumptions in their financial analyses, which, without full disclosure of such

information, calls into question their ultimate conclusions that the Proposed Transaction is fair.

Given that Sabine is a private company, there is a lack of publicly available information

regarding its financial performance and value. Accordingly, it is even more important that

defendants fully disclose the above information to permit Forest Oil shareholders to properly

evaluate the Proposed Transaction and determine whether the proposed equity split reflects the

true inherent value of Forest Oil.

- 35 -

Case 1:14-cv-01409-MSK-CBS Document 11 Filed 06/13/14 USDC Colorado Page 37 of 53

Financial Projections

71. According to pages 76-79, 84-86 of the Registration Statement, J.P. Morgan

relied upon certain financial forecasts for the Company and Sabine in conducting its financial

analyses in support of its fairness opinion. The Registration Statement, however, does not

disclose the following:

(a) the following financial data for the Forest Oil projections used in J. P.

Morgan's Net Asset Value Analysis and other related financial analyses:

(i) projected cash flows from the 3P assets (as defined in the

Registration Statement);