26

ROLE OF REGIONAL ECONOMIC COMMUNITIES IN PROMOTING ECONOMIC INCLUSIVENESS THE SADC LA, Cape Town, 18‐19 th August 2016 By Daniel Njiwa

| Date post: | 24-Jun-2018 |

| Category: |

Documents |

| Upload: | nguyenphuc |

| View: | 214 times |

| Download: | 0 times |

ROLE OF REGIONAL ECONOMIC COMMUNITIES IN PROMOTING ECONOMIC

INCLUSIVENESS

THE SADC LA, Cape Town, 18‐19th August 2016

By Daniel Njiwa

Introductory facts The concept of inclusiveness Existing frameworks Discussion on key sectors & how they impact

economic inclusiveness Examples of regional initiatives that promote

economic inclusiveness: STR, FoodTrade ESA, Industrial Clusters, CAADP…

The gaps ‐ what can be done.

Sources: Africa Development Bank; Africa Investment Report; World Bank; ERA 2016; African Union; TNO/Excelsoir Firm

Demographic dividend [~0.5 billion 25‐64yrs ‐

2015]

65% worlds arable land; most

mineral resources

Share of mobile tel. penetration is significant; tech. transfer

10 of the fastest growing

economies

FDI growth over 10 years > world

average

Middle class more than

tripled over past 30 years

Poverty decline by proportion (56‐48% ‐ ‘90‐

2000)

Integration (trade) structural reforms, private sector focus

Democracy

Diaspora remittances

increasing > ODA & FDI in cases

Tertiary education

enrolment ^ 21% y.o.y from 2000

Econ. growth @least 4.5% over

10 years

Africa today

Sources: Africa Development Bank; Africa Investment Report; World Bank; ERA 2016; African Union; TNO/Excelsoir Firm

Women far more disadvantaged (access/culture)

ICT penetration below par

Infrastructure challenges

[roads, energy, rail]

At least half a billion live below

poverty line ($1.25)

Urbanisation (~3%) & Unemployment (>7% SSA)

Access to tertiary education & vocational skills limited

Imports $35bn of food every year

WHY?

HIV and AIDS remains a big challenge

11 million Africans enter the labour force

annually

Declining commodity prices

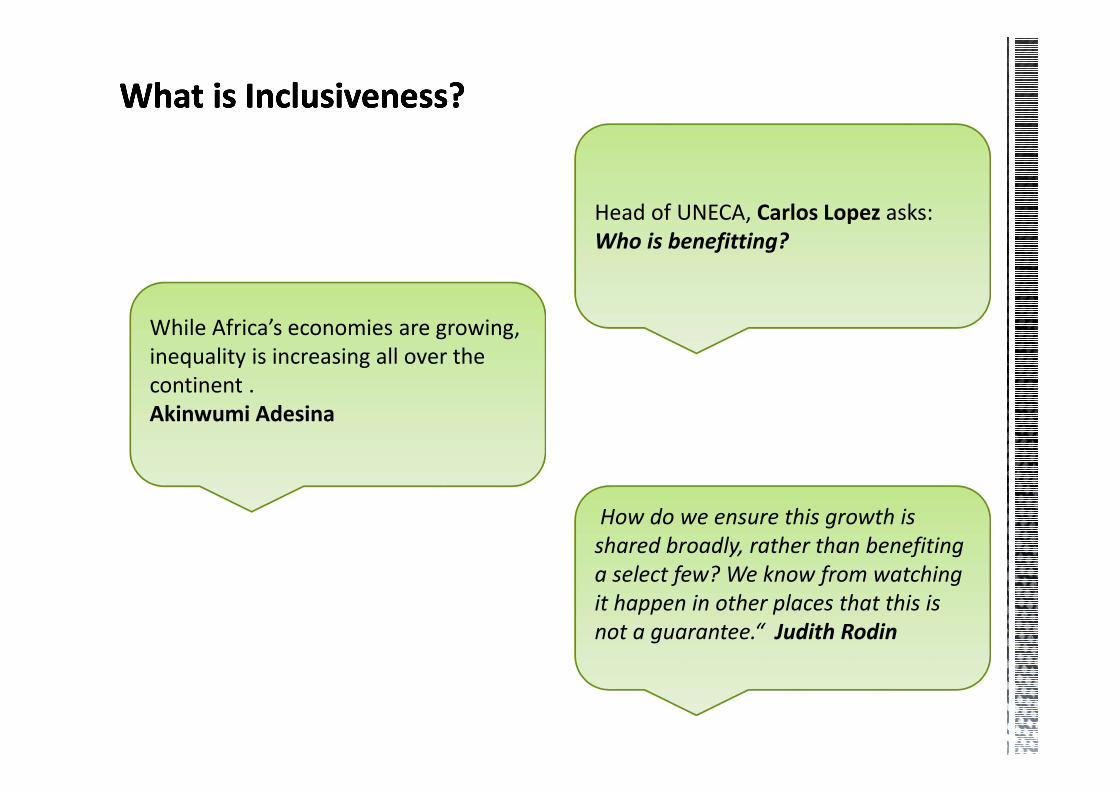

Head of UNECA, Carlos Lopez asks: Who is benefitting?

How do we ensure this growth is shared broadly, rather than benefiting a select few? We know from watching it happen in other places that this is not a guarantee.“ Judith Rodin

While Africa’s economies are growing, inequality is increasing all over the continent .Akinwumi Adesina

Income equality (still a significant challenge in Africa)Gender balance – equal participation of women, youth and othersAccess to natural resources Access to social amenities (clean water, housing, energy, education, roads, security, health etc.)Equitable formal employment (>70% are in informal employment; mostly agro‐based)For these: protection of assets and rights is non‐existentParticipation in policy and developmentCorruption breeds inequality (governance institutions still have work)

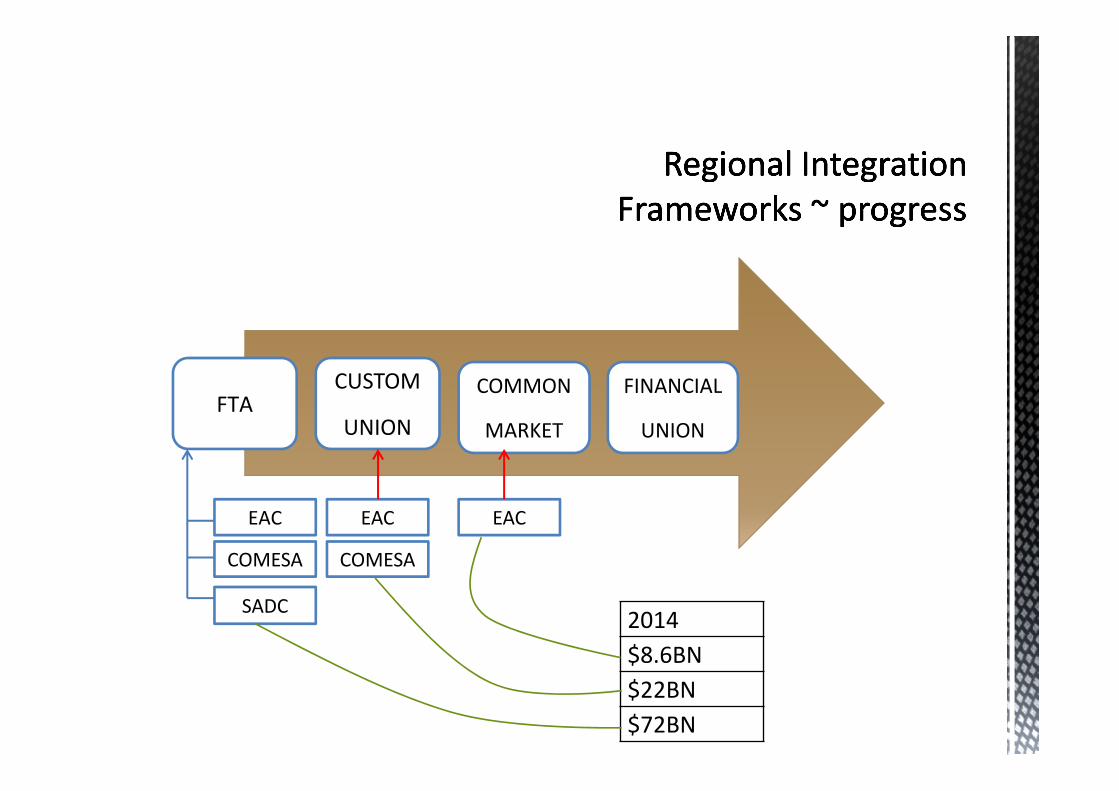

FTAFINANCIAL

UNION

COMMON

MARKET

CUSTOM

UNION

EAC

COMESA

SADC

EACEAC

COMESA

2014$8.6BN$22BN$72BN

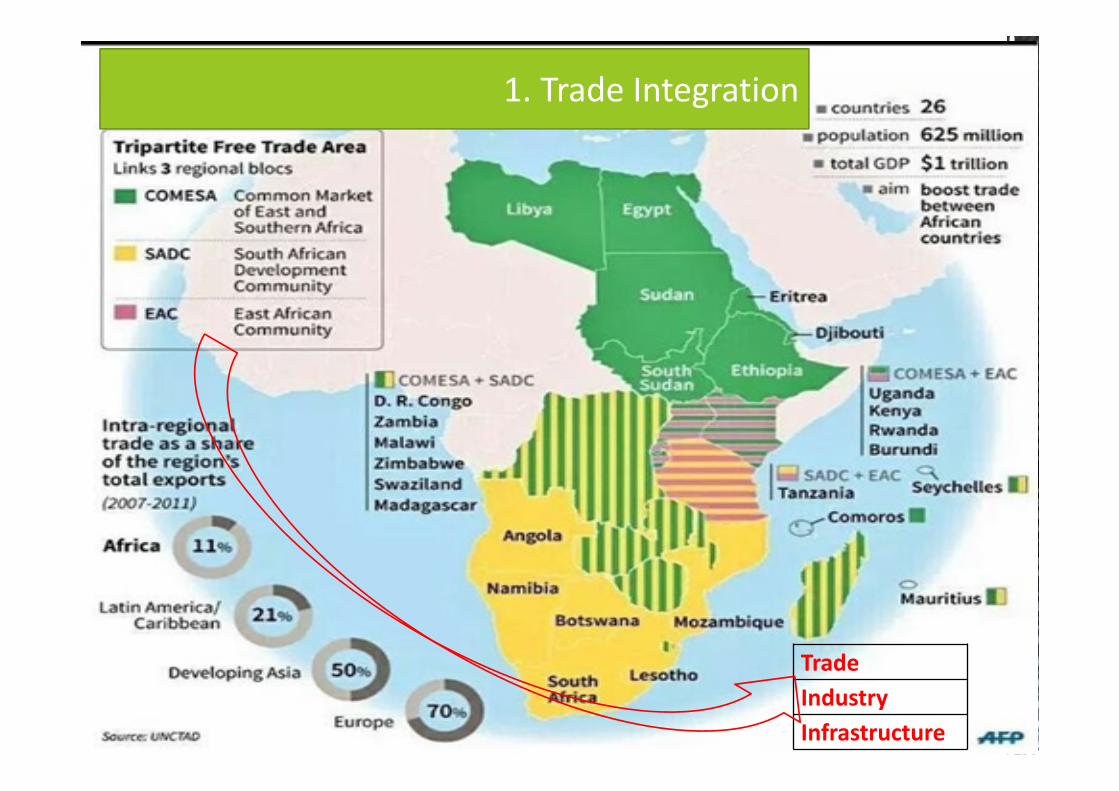

1. Trade Integration

TradeIndustryInfrastructure

Sources: UNECA, 2016

Single customs territoryRegional customs transit systemCargo tracking systemsInteragency coordinationOne‐stop border postsCorridor monitoring,Dwell time at port reduced by days (e.g. Chirundu or Malaba); border clearance to under 8hrs; Cost of Doing Business reduced by 50%. This Boosts investments, productivity, welfare (but to what extent?)

commercial

Question: How many citizens/local SMEs are benefiting from these arrangements?

COMESA, EAC Simplified trade regime STR:‐ Refers to Simplified Trade Regime: simplification of procedures and documentation of trade/customs in order to encourage utilization by millions of small/informal traders. Prerequisites: ‐ Functional FTA; Legal‐Amended Customs Act; Simplified customs documentation; Issuance of COO at border (or Common list of products agreed bilaterally or regionally); training and awareness creation by both traders and customs and border authorities

Agreement on volumes and values Agreement on other procedures such as SPS controls, immigration procedures, etc Regional Cross Border Traders Association formed Mwami, Livingstone[30,000 monthly]; Malaba, Busia [>50,000 monthly]

Source: COMESA Secretariat

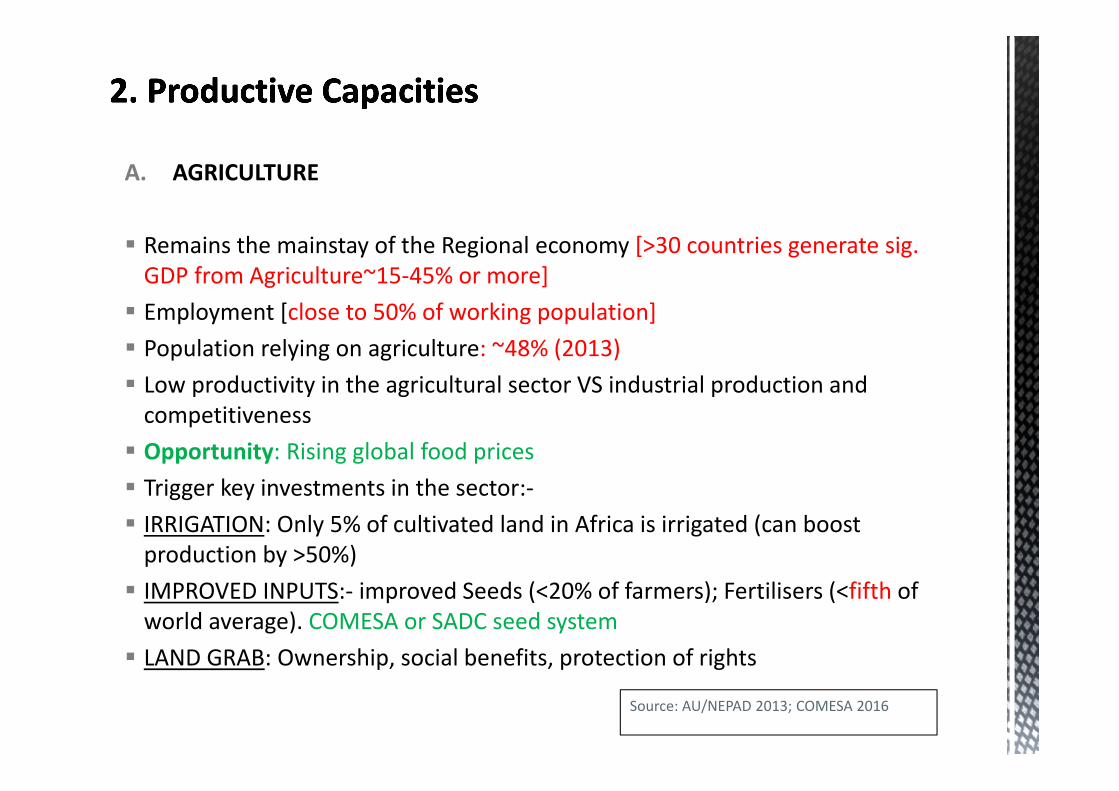

A. AGRICULTURE

Remains the mainstay of the Regional economy [>30 countries generate sig. GDP from Agriculture~15‐45% or more] Employment [close to 50% of working population] Population relying on agriculture: ~48% (2013) Low productivity in the agricultural sector VS industrial production and competitiveness Opportunity: Rising global food prices Trigger key investments in the sector:‐ IRRIGATION: Only 5% of cultivated land in Africa is irrigated (can boost production by >50%) IMPROVED INPUTS:‐ improved Seeds (<20% of farmers); Fertilisers (<fifth of world average). COMESA or SADC seed system LAND GRAB: Ownership, social benefits, protection of rights

Source: AU/NEPAD 2013; COMESA 2016

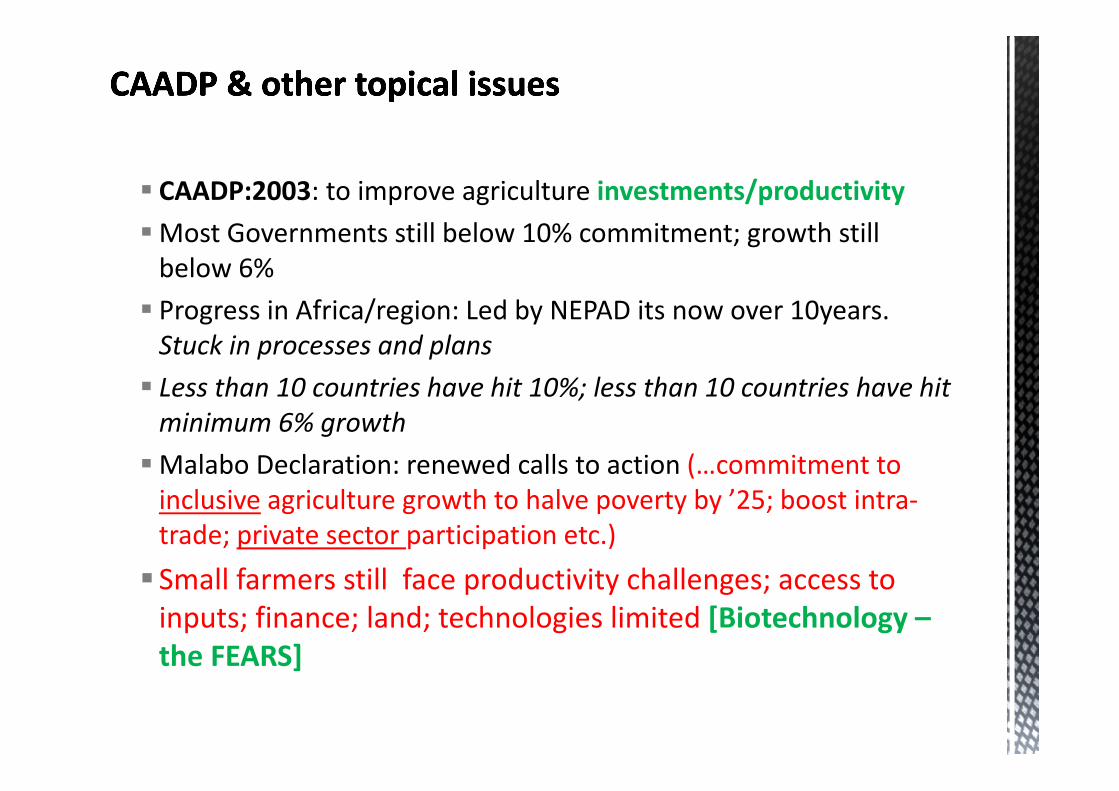

CAADP:2003: to improve agriculture investments/productivityMost Governments still below 10% commitment; growth still below 6% Progress in Africa/region: Led by NEPAD its now over 10years. Stuck in processes and plans Less than 10 countries have hit 10%; less than 10 countries have hit minimum 6% growthMalabo Declaration: renewed calls to action (…commitment to inclusive agriculture growth to halve poverty by ’25; boost intra‐trade; private sector participation etc.) Small farmers still face productivity challenges; access to inputs; finance; land; technologies limited [Biotechnology –the FEARS]

Food Trade East & Southern Africa

16

1) To stimulate innovative business models that deliver commercial benefits & solutions to market failures;2) Deliver jobs, income & market access for the poor & smallholder farmers; 3) Grants up to $ 1.5 million; 4) 14 contracts currently signed.

1) Facilitate dialogue & actionaround key barriers in regional staple food markets 2) Fund targeted interventions to strengthen these markets.3) Support to non‐profits,agencies, NGOs. 4) 5 contracts currently signed (incl. the PPP with the WFP)

FoodTrade ESA Challenge Fund

17

Extraction PlantMt. Meru (Tanzania & Zambia) Grant $ 1.5 million ‐ company multi

million £ investment 4,000 new soya farmers Produc on ↑ 50% with minimum

price New products: soy oil and cakes

Joseph Initiative Uganda Grant $ 1.5 million ‐ company £ 9

million 90 new village aggregation centres Inputs and loans 57,000 farmers, incomes ↑ 150% Trade volumes ↑ 30%

18

East Africa Grain Council To develop a private sector‐driven, market platform

(G‐Soko) to link buyers & sellers in staple foods trade in Eastern Africa.

The new G‐Soko Platform will bring structure and consistency to trade in grains.

Millions of farmers in East Africa Grant: £ 3.5M

Alliance for Commodity Trade ESA To facilitate the domestication of harmonised seed

trade regulations in east and southern Africa (7 countries)

Issues include: complex national regulations, a lack of common regional standards for production, seed quality, certification and release.

Grant: £ 1.2M

FoodTrade ESA Development Fund

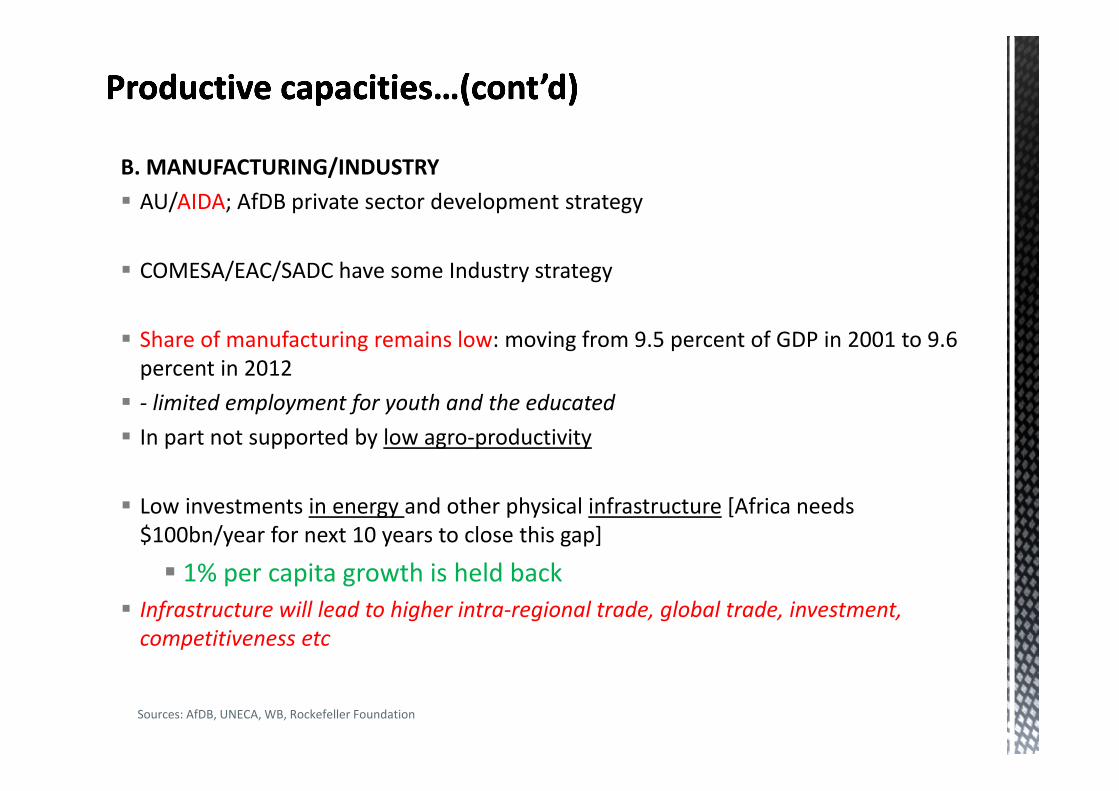

B. MANUFACTURING/INDUSTRY AU/AIDA; AfDB private sector development strategy

COMESA/EAC/SADC have some Industry strategy

Share of manufacturing remains low: moving from 9.5 percent of GDP in 2001 to 9.6 percent in 2012 ‐ limited employment for youth and the educated In part not supported by low agro‐productivity

Low investments in energy and other physical infrastructure [Africa needs $100bn/year for next 10 years to close this gap]

1% per capita growth is held back Infrastructure will lead to higher intra‐regional trade, global trade, investment, competitiveness etc

Sources: AfDB, UNECA, WB, Rockefeller Foundation

9/19 member states of COMESA: Regional strategy Programme implementation led by the COMESA Leather and Leather Products Institute based in Ethiopia Currently supported about 6 country strategies: Uganda, Sudan, Malawi, Ethiopia, Eritrea, Burundi Focus is:‐ Policy and regulatory environment improved Capacity building of SMEs in leather and leather products [skills development] Access to technology and financing Business skills and information access Establishment of industrial clusters, technology hubs for leather and leather products

Currently…..

C. MINING AU/UNECA: African Mining Vision 2009 SADC : 1997 Protocol on Mining; Framework and Implementation plan for Harmonisation of Mining Policies, Standards, Legislative and Regulatory frameworks EAC: Harmonize their mineral laws and policies; joint exploration; information exchange; among others COMESA: A harmonized mineral sector policy framework. To what extent these frameworks have translated into better livelihoods for common people needs interrogation

CHALLENGES still exist for the SMEs- policy framework limited (deal making. corruption); limited access to

technology and capacity; lack of markets; conflict minerals; lack of financing; - women and child labour issues

AU/NEPAD 2013: Extractive industries spur growth but have little impact on employment and revenue

Productive Capacities...(cont’d)

SADC Protocol Facilitating Movement of Persons 2005 Only 4 MS have ratified against 2/3 to put it in force

Transposition into National laws also a Challenge COMESA: Also has a protocol of free movement of persons which has not been fully signed by all its Member States.

EAC is by far ahead of all other RECs in ESA: Free movement of persons is in force with the ‘Coalition of the Willing’ – Rwanda, Kenya, Uganda leading. Labour freely moves, no passport/visa required on travel

UNECA 2016: Less than 50% of MS in all these RECs are categorised as high‐performers RSA, Zambia are examples in the southern region: But ASK, what does it take? $500,000….how many of us has this amount? Critical for extending economic benefits of regional integration to the majority of the citizens of the region. ONUS ON US

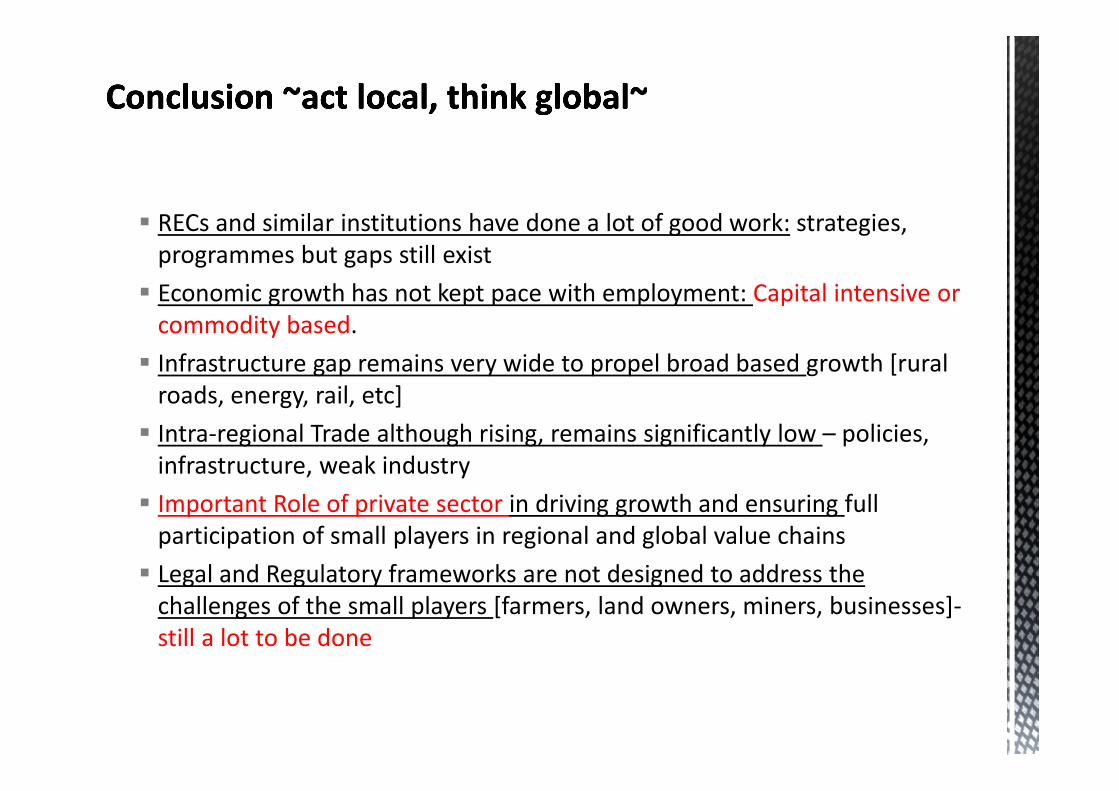

RECs and similar institutions have done a lot of good work: strategies, programmes but gaps still exist Economic growth has not kept pace with employment: Capital intensive or commodity based. Infrastructure gap remains very wide to propel broad based growth [rural roads, energy, rail, etc] Intra‐regional Trade although rising, remains significantly low – policies, infrastructure, weak industry Important Role of private sector in driving growth and ensuring full participation of small players in regional and global value chains Legal and Regulatory frameworks are not designed to address the challenges of the small players [farmers, land owners, miners, businesses]‐still a lot to be done

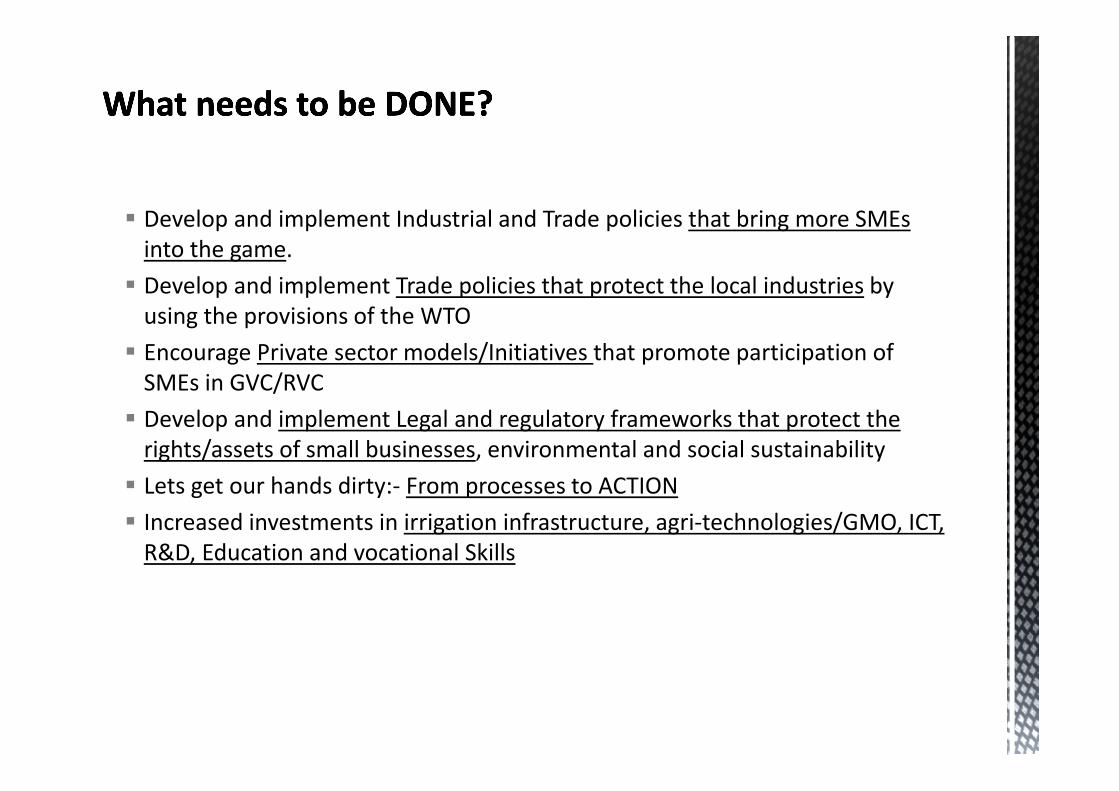

Develop and implement Industrial and Trade policies that bring more SMEs into the game. Develop and implement Trade policies that protect the local industries by using the provisions of the WTO Encourage Private sector models/Initiatives that promote participation of SMEs in GVC/RVC Develop and implement Legal and regulatory frameworks that protect the rights/assets of small businesses, environmental and social sustainability Lets get our hands dirty:‐ From processes to ACTION Increased investments in irrigation infrastructure, agri‐technologies/GMO, ICT, R&D, Education and vocational Skills

“We need to invest in expanding opportunities and unlocking potential ‐ for the poor, for the private

sector, for countries, for the continent, and especially for women and young people.”

Akinwumi Adesina, 2015