29

Role of the Customer in Energy Efficiency and Conservation Lisa Wood Montana’s Energy Future Helena, Montana January 7-8, 2011

Role of the Customer in Energy Efficiency and

Conservation

Lisa Wood

Montana’s Energy Future

Helena, Montana

January 7-8, 2011

Today’s breakfast talking points

What’s achievable with energy efficiency and

demand response?

– EE potential estimates

– DR potential estimates

What about low income customers?

Engaging the customer – what’s new?

Are we on cusp of the 2nd electric revolution?

2

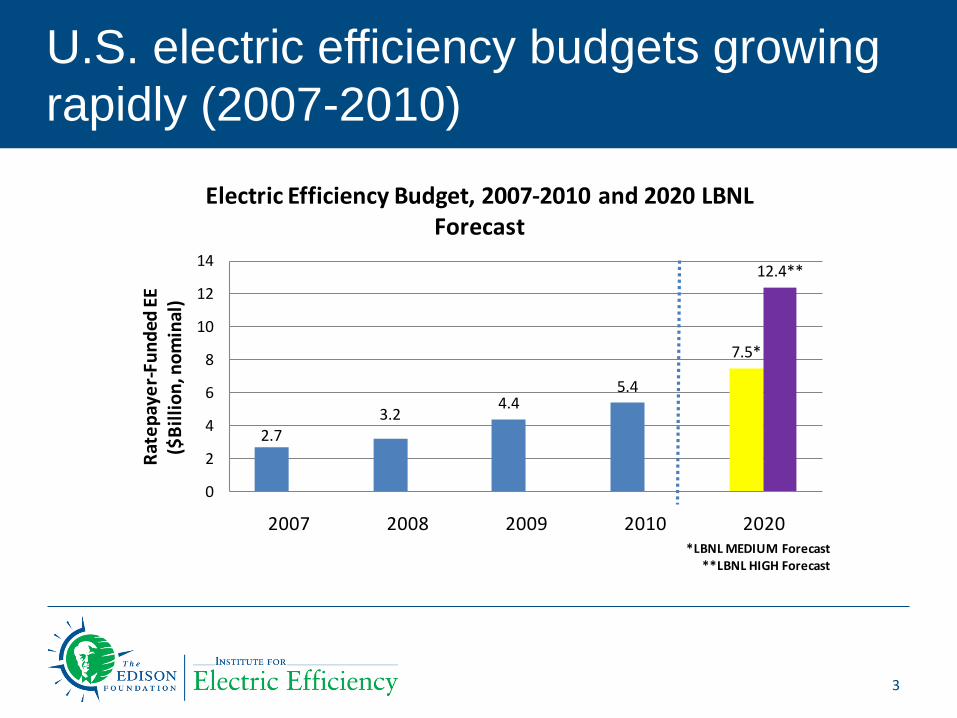

U.S. electric efficiency budgets growing

rapidly (2007-2010)

3

2.73.2

4.45.4

7.5*

12.4**

0

2

4

6

8

10

12

14

2007 2008 2009 2010 2020

Rat

ep

aye

r-Fu

nd

ed E

E($

Bil

lio

n, n

om

inal

)

*LBNL MEDIUM Forecast **LBNL HIGH Forecast

Electric Efficiency Budget, 2007-2010 and 2020 LBNL Forecast

Utilities play major role in ratepayer-funded

electric efficiency budgets in U.S.

4

Utility Non-Utility

Utility

Share of

Total

Percent

Increase

2007 $2,722,788,884 $2,413,639,443 $309,149,441 89%

2008 $3,165,329,920 $2,704,072,429 $461,257,491 85% 16%

2009 $4,370,445,097 $3,796,110,308 $574,334,789 87% 38%

2010 $5,433,087,642 $4,789,681,107 $643,406,535 88% 24%

Electric Efficiency 2007-2010 U.S. Budgets

Total

Source: IEE Brief. Summary of ratepayer-funded electric

efficiency impacts, expenditures, and budgets. January 2011.

U.S. electric efficiency savings projected to

exceed 100 TWh in 2010

5

69.2

85.3 92.6 100+*

0

20

40

60

80

100

120

2007 2008 2009 2010

TWh

* IEE Projection

U.S. Electric Efficiency Impacts (2007-2009 & 2010 Forecast)

Source: IEE Brief. Summary of ratepayer-funded electric

efficiency impacts, expenditures, and budgets. January 2011.

6

Energy efficiency

potential – programs

plus codes & standards

Energy efficiency savings growing rapidly but

significant potential for much more savings

7

85 TWh

represented

about 2% of

total usage in

2008.

293

CEE(Actual

Achieved)

85.3

372

1080

0

200

400

600

800

1000

1200

2008 2020

Ene

rgy

Effi

cie

ncy

Sav

ings

TWh

IEE (Codes and Standards Aggressive) - 2009EPRI (Maximum Achievable) - 2009McKinsey - 2009

How much EE can we expect by 2020?

Energy efficiency potential forecasts cover wide range – exact

number doesn’t really matter because there is so much left to do!

– EPRI predicts 372 TWh (maximum achievable potential) by 2020 (Jan. 2009)

– McKinsey: predicts 1,080 TWh “saved” by 2020 (July 2009)

In 2008, electric efficiency programs saved 85.3 billion kWh (CEE)

– Enough to power 7.4 million homes for one year

– 58 million metric tons of CO2 avoided

In 2009, electric efficiency programs save 92.6 billion kWh (CEE)

– Enough to power 8 million homes for one year

– 66 million tons of CO2 avoided

Plus – the potential savings due to codes and standards is huge

and very cost effective!

8

9

A few words on

demand response

Utility scale smart meter deployments, plans, and proposals –

about 65 million meters will be deployed (50% of US

households over next 5-7 years). Will this drive retail DR?

10

*This map represents smart meter deployments, planned deployments, and proposals by investor-

owned utilities and large public power utilities.

Deployment for

>50% of end-users

Deployment for

<50% of end-users

IEE: September 2010 update

Potential peak demand reduction due to demand

response – wide range of estimates. Expanded BAU

and MAP realistic in my view!

11

Baseline Forecast (NERC): 950 GW by 2019Baseline Forecast: 964 GW by 2020

(951 GW by 2019)

0

20

40

60

80

100

120

140

160

180

200

BAU Expanded BAU

Achievable Potential

Full Participation

38

82

138

188

GW

Sa

ve

d

FERC (June 2009): Peak Demand Savings due to Demand Response

0

20

40

60

80

100

120

140

160

180

200

RAP MAP Technical Potential

44

66

163

GW

Sa

ve

d

EPRI (January 2009): Summer Peak Demand Savings due to Demand Response

(4%) (9%) (14%) (20%) (4.6%) (6.8%) (16.9%)

Portfolio of DR sources for peak demand

savings

12

- 5,000 10,000 15,000 20,000 25,000

DLC-Cooling

Direct Control-Lighting

DLC-Other

Interruptible Demand

Price-Response

DLC-Process

Interruptible Demand

Price-Response

DLC-Central AC

DLC-Water Heating

Price-Response

Cumulative Summer Peak Demand Savings (MW)

2030

2020

2010

Co

mm

erc

ial

Ind

us

tria

l R

es

ide

nti

al

Source: EPRI Report #1016987. January 2009

We know customers respond to prices;

response even greater with technology

13

0%

10%

20%

30%

40%

50%

60%

1 2 3 4 5 6 7 8 9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

Pricing Pilot

% R

ed

ucti

on

in

Pea

k L

oa

d

TOU TOU w/

TechPTR CPP CPP w/

Tech

RTP

RTP

w/

Tech

PTR

w/

Tech

Source: Ahmad Faruqui, Brattle.

Historical vs. projected U.S. summer peak load

reduction (GW) due to energy efficiency and demand

response (EIA and EPRI Report #1016987)

14

0

20

40

60

80

100

120

140

160

2007 2020 2030

30 GW

79 GW

157 GW

GW

Total U.S. Summer Peak Load Reduction due to EE and DRSources: EIA Form 861, EPRI, "Assessment of Achievable Potential from EE and DR Programs in

the U.S." (2009)

Actual Realistically Achievable Potential (EPRI, 2009)

Source: EPRI Report #1016987. January 2009

EPRI: EE and DR programs together can reduce 8% (RAP) to

15% (MAP) U.S. summer peak demand in 2020

15

2010

2020

2030

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

Maximum Achievable Potential Realistic Achievable

Potential

4.9%

2.2%

15.3%

8.2%

19.5%

14.0%

Pe

rce

nt o

f S

um

me

r P

ea

k D

em

an

d

Split 7% from

DR and 7%

from EE

Source: EPRI Report #1016987. January 2009

16

What about impact on

low income customers?

Low income customers and dynamic pricing –

Two viewpoints

Low income customers have flatter load shapes than

average residential customers so would immediately

benefit from dynamic pricing.

Low income customers use less energy and therefore

have limited ability to shift load from peak to off peak

hours so would be harmed from dynamic pricing.

Empirical evidence from five studies shows the following:

– Many low income customers can benefit from dynamic prices

even without shifting load

– Low income customers do shift their energy usage in response

to price signals

17

Source: IEE Whitepaper, “The Impact of Dynamic

Pricing on Low Income Customers, September 2010

www.edisonfoundation.net/IEE

Low income customers benefit from smart

prices even without shifting load

18

51%

61%65%

79%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

CPP Rate Design #1 CPP Rate Design #2

Per

cen

t o

f C

ust

om

ers

in S

am

ple

Percent of Sample with Immediate Bill Decreases on CPP Rates

(Even with No Load Shifting – i.e., No Demand Response)

Residential Low Income

Source: IEE Whitepaper, “The Impact of Dynamic

Pricing on Low Income Customers, September 2010

www.edisonfoundation.net/IEE

Low income customers do respond to smart prices –

the same as or less than other customers

19

Note: For the PepcoDC pilot, the average residential response excludes

low income customers that qualify for the RAD program

Program ResultsLow Income Peak

Reduction

Average Peak

Reduction

Low Income

vs. Average

BGE 2008: Known Low Income vs. Known

Average Customer

Varies depending on rate type; low income

customers respond similarly to average customer100%

CL&P's PWEP Program: Known Low Income

vs. Known Average Customer

Varies depending on rate type; low income

customers respond similarly to average customer100%

CL&P's PWEP Program (PTP high): Hardship

vs. Average 13% 20% 67%

Pepco DC (price only): Low Income vs.

Average Residential1 11% 13% 85%

PG&E SmartRate 2008: CARE vs. Average 11% 17% 66%

PG&E SmartRate 2009: CARE vs. Average 8% 15% 50%

California SPP: Low Income vs. Average 11% 13% 84%

California SPP: CARE vs. Average 3% 13% 22%

How do dynamic prices affect low income customers:

Conclusions based on 5 studies plus a load research

sample

Dynamic prices are not harmful to low income customers. In fact, just the opposite is true

– 65-79% are instant winners even without load shifting due to flatter-than-average load shapes.

– All five studies cited found that low income customers do respond to dynamic prices; evidence on the magnitude of their responsiveness is mixed.

The vast majority of low income customers are likely to benefit from dynamic pricing. Restricting access to dynamic rates may, in fact, be harmful to a large percentage of low income customers.

20

Source: IEE Whitepaper, “The Impact of Dynamic Pricing

on Low Income Customers, September 2010

www.edisonfoundation.net/IEE

21

Engaging the customer

What’s new in the EE space? Focus on

the customer

22

Educating and engaging the customer

23

Utilities are partnering with vendors and using home

energy reporting, goal setting, and rewards as

motivators to save

24

Large-Scale Customer

Engagement

Flagship Product –

Home Energy Report™

Efficiency Portal

Utility Partners:

Utilities send out monthly “Energy

Reports” to motivate customer action.

Make comparisons to neighbors

Results are measured and accepted as

an efficiency resource (average cost is

$0.03 per kWh saved).

Customers save energy (2-3%). Could

save a lot more if coupled with

technology.

Example: Commonwealth Edison launched major AMI

and rate pilot with customer centric design (2010)

Customer education innovations– Web energy management tools including

comparisons; educational modules; monthly updates

– In home displays, programmable communicating

thermostats

– Community support

Customer energy management assistance– Via bill comparisons, web tools, call center, monthly educational meetings

About 131,000 customers – 8,500 smart rates responders

– 120,000 smart energy managers

25

The customer’s energy management options

Demand response - smart rates– Many pilots but few smart (dynamic) rate “opt out” deployments

– In US, state regulators moving toward peak time rebate (PTR).

Demand response – direct load control – Decades of experience

– Move to measurable and verifiable DLC – DLC 2.0

Information induced conservation– Info alone or information with technology

PHEVs

Distributed generation

26

Big question: How will we motivate customers

to be smart energy managers?

We know customers benefit from smart rates on smart

meters

But, for those customers with smart meters but no smart

rates (i.e., the vast majority right now) or those without

smart meters, empowering customers to be smart

energy managers is the key

– Consumers are ready to be smart energy managers.

– Need to educate and engage the customer

– Technology can make a big difference

27

Smart meter platform will take EE and DR to

new levels – 2nd electric revolution!

28

HAN communication

SmartMeter communication

…It’s all about giving

customers the tools and

the know-how to be

smarter energy

consumers. Educate,

educate, educate!

For more information, contact:

Lisa Wood

Executive Director

Institute for Electric Efficiency

701 Pennsylvania Ave., N.W.

Washington, D.C. 20004-2696

202.508.5550

www.edisonfoundation.net/IEE