18

Ron Harbour President Harbour Consulting

| Date post: | 29-Dec-2015 |

| Category: |

Documents |

| Upload: | denis-stewart |

| View: | 222 times |

| Download: | 1 times |

Ron HarbourPresident

Harbour Consulting

Flexible Manufacturing

© 2005 Harbour Consulting. All Rights Reserved

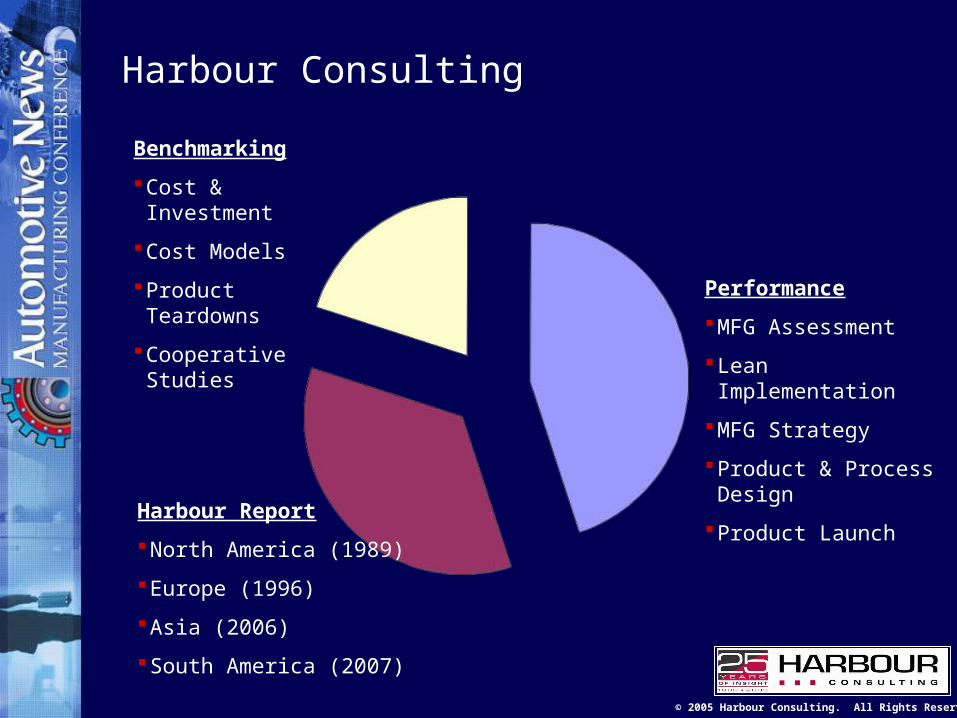

Harbour Consulting

Benchmarking

Cost & Investment

Cost Models

Product Teardowns

Cooperative Studies

Harbour Report

North America (1989)

Europe (1996)

Asia (2006)

South America (2007)

Performance

MFG Assessment

Lean Implementation

MFG Strategy

Product & Process Design

Product Launch

© 2005 Harbour Consulting. All Rights Reserved

Recent Clients

© 2005 Harbour Consulting. All Rights Reserved

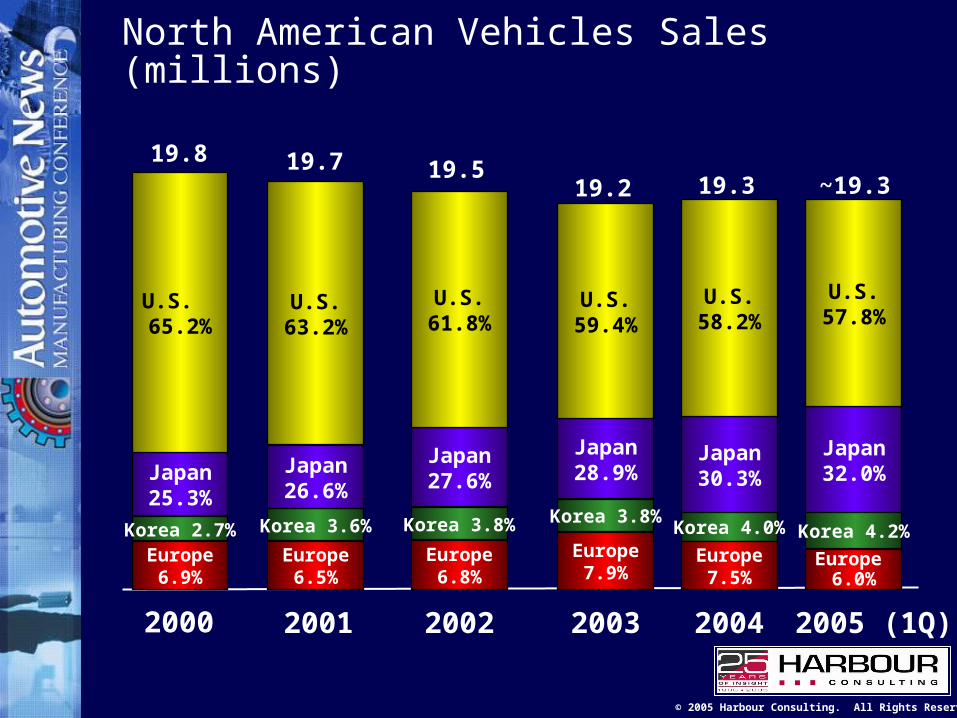

2000

Korea 2.7% Korea 3.6%

19.8 19.7

Europe6.9%

Japan25.3%

U.S. 65.2%

Europe6.5%

Japan26.6%

U.S.63.2%

Korea 3.8%

Europe6.8%

Japan27.6%

U.S.61.8%

19.5

2001 2002

Korea 3.8%

Europe7.9%

Japan28.9%

U.S.59.4%

19.2

2003 2005 (1Q)

North American Vehicles Sales (millions)

Korea 4.0%

Europe7.5%

Japan30.3%

U.S.58.2%

19.3

2004

Korea 4.2%

Europe 6.0%

Japan32.0%

U.S.57.8%

~19.3

© 2005 Harbour Consulting. All Rights Reserved

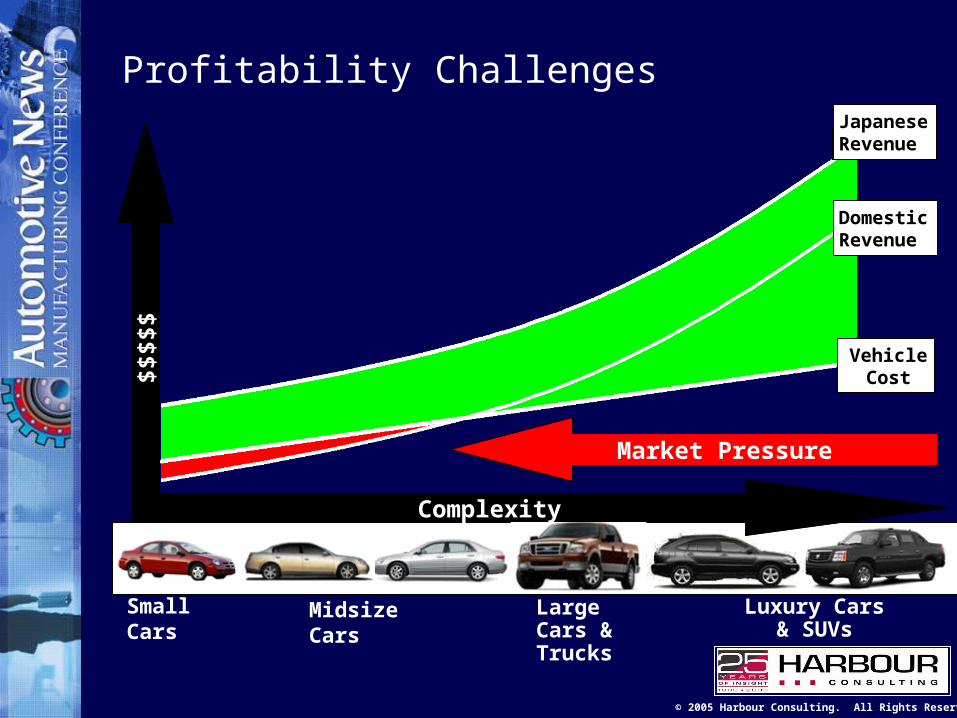

VehicleCost

Revenue

Domestic Revenue

Japanese Revenue

Market Pressure

Small Cars Midsize Cars Large Cars & Trucks

Luxury Cars & SUVs

$$$$

$

Complexity

Profitability Challenges

© 2005 Harbour Consulting. All Rights Reserved

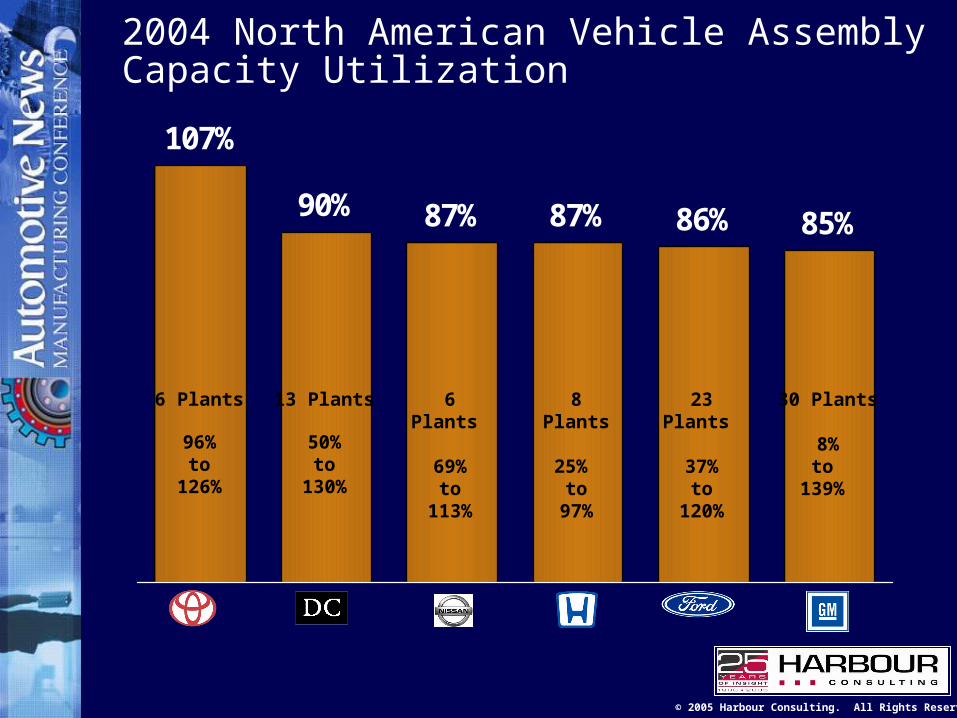

2004 North American Vehicle Assembly Capacity Utilization

107%

90% 87% 87% 86% 85%

8 Plants

25% to

97%

6 Plants

69%to

113%

23 Plants

37%to

120%

30 Plants

8%to

139%

6 Plants

96%to

126%

13 Plants

50%to

130%

© 2005 Harbour Consulting. All Rights Reserved

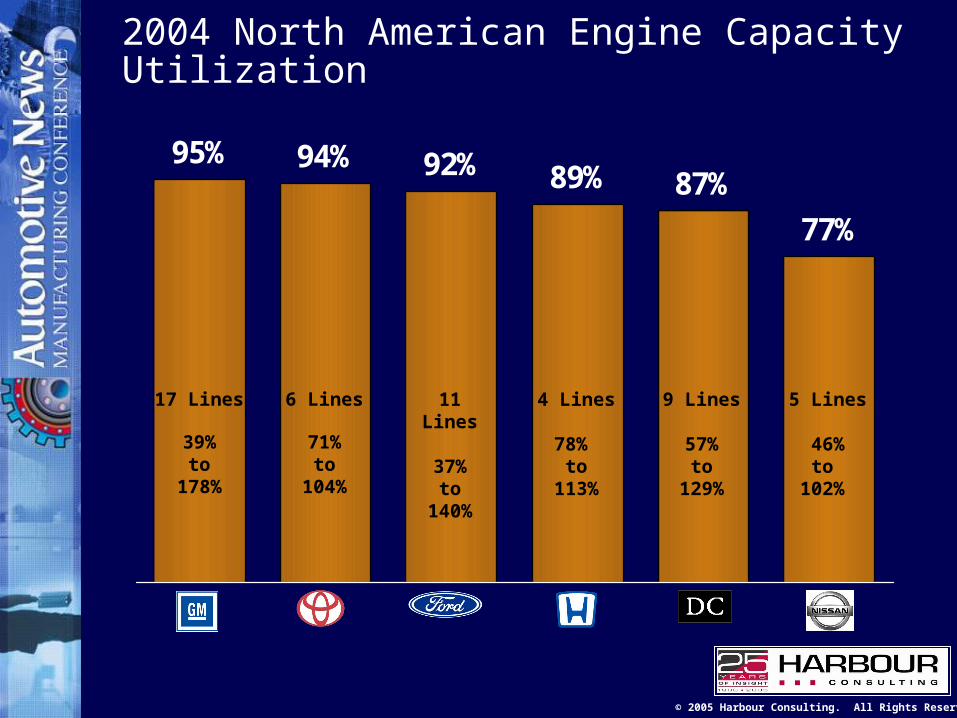

2004 North American Engine Capacity Utilization

95% 94% 92% 89% 87%

77%

4 Lines

78% to

113%

11 Lines

37%to

140%

9 Lines

57%to

129%

5 Lines

46%to

102%

17 Lines

39%to

178%

6 Lines

71%to

104%

© 2005 Harbour Consulting. All Rights Reserved

The Capacity /Flexibility Dilemma

Products/Models are increasing, volume per model is decreasing

GM, Ford market share loss has left numerous plants underutilized

Union labor agreements limit plant closings

Foreign brand growth paced by available capacity

Concurrent Impact on Powertrain, Stamping

Suppliers that aren’t diverse or flexible hurt the most

© 2005 Harbour Consulting. All Rights Reserved

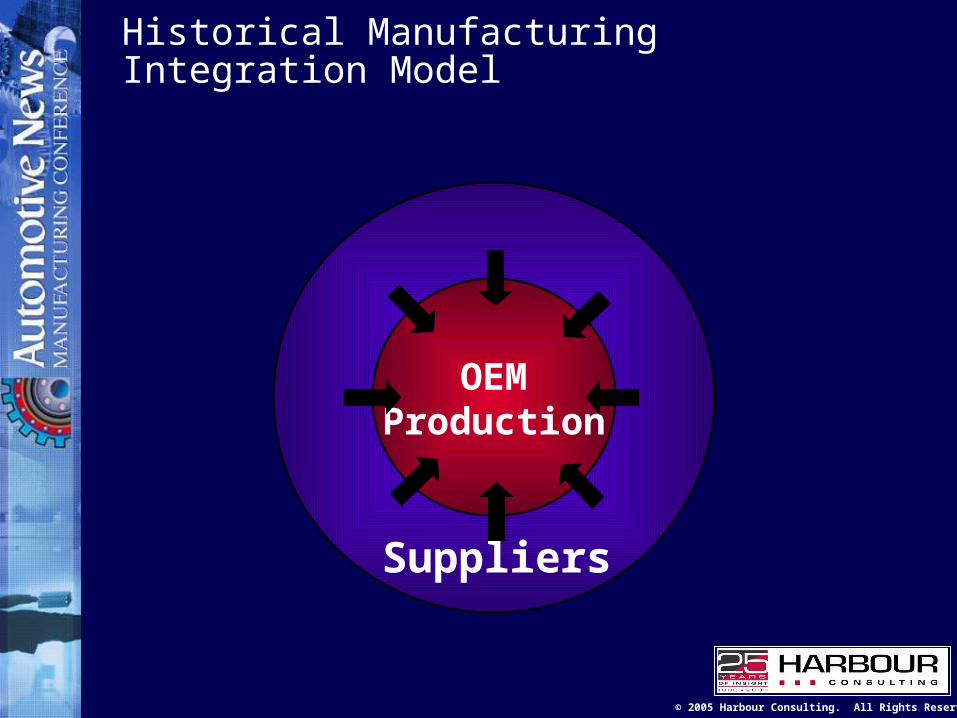

Historical ManufacturingIntegration Model

OEMProduction

Suppliers

© 2005 Harbour Consulting. All Rights Reserved

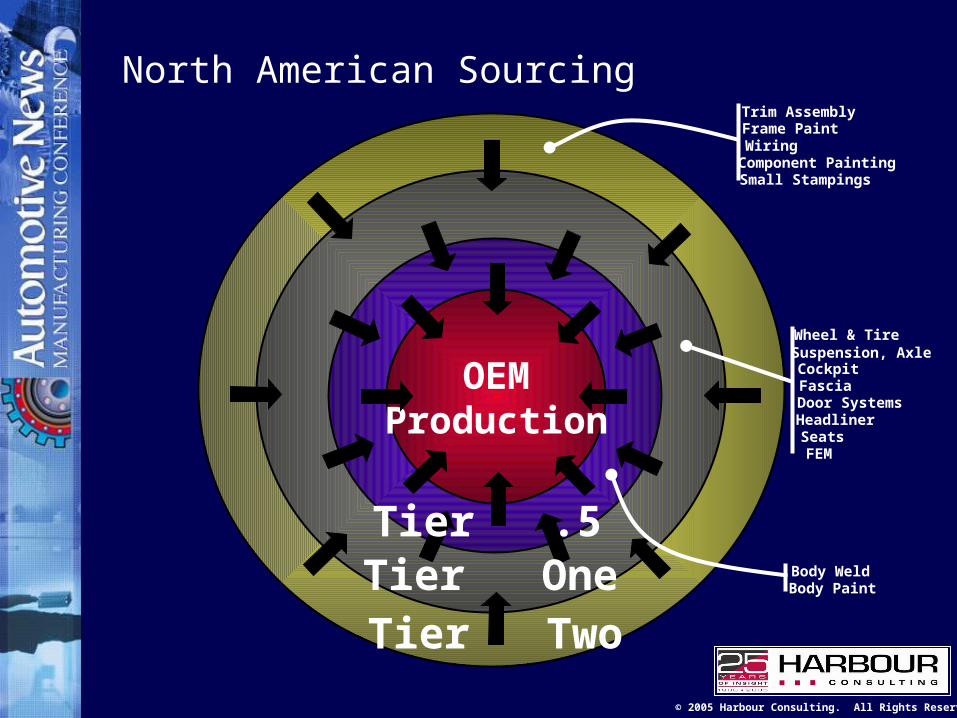

North American Sourcing

OEMProduction

Tier .5

Tier TwoTier One

Trim AssemblyFrame PaintWiringComponent PaintingSmall Stampings

Wheel & TireSuspension, AxleCockpitFasciaDoor SystemsHeadlinerSeatsFEM

Body Weld Body Paint

© 2005 Harbour Consulting. All Rights Reserved

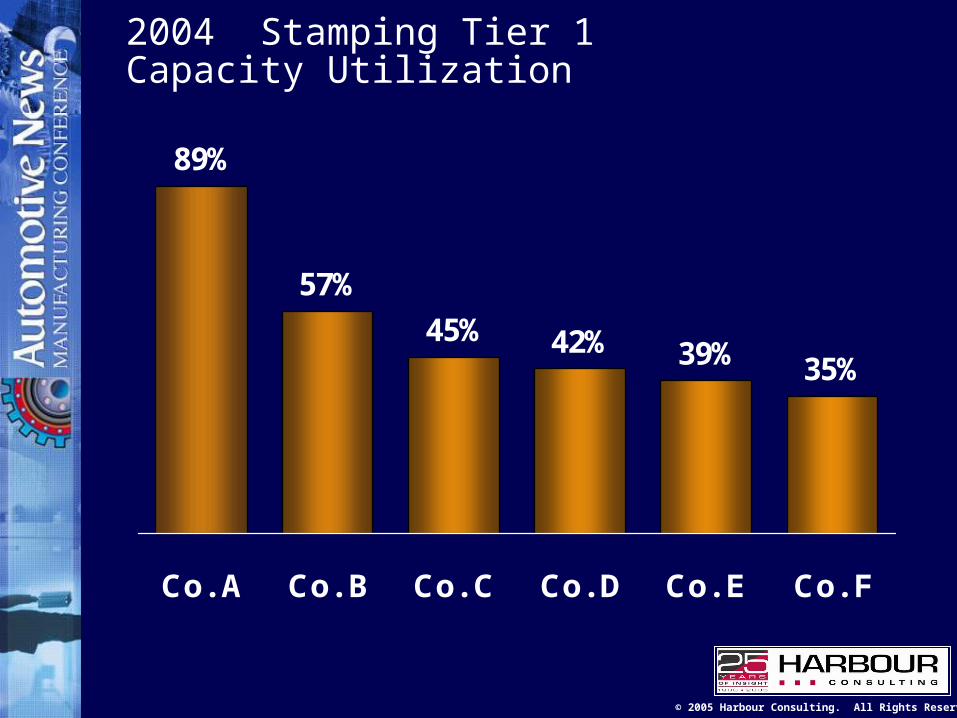

2004 Stamping Tier 1 Capacity Utilization

89%

57%

45% 42% 39% 35%

Co. A Co. B Co. C Co. D Co. E Co. F

© 2005 Harbour Consulting. All Rights Reserved

What is Manufacturing Flexibility?

Capable of Building numerous models in one process

Capable of producing multiple architectures/platforms all in a single process

Ability to add a product with minimal disruption, cost, and time

Rapid product mix change Quick new product launch

© 2005 Harbour Consulting. All Rights Reserved

Flexibility Enablers

Similar architecture Common build sequence Layout for “flex” manning Well trained, rotating workforce Quick part switch Responsive Suppliers

Capacity must be generic

© 2005 Harbour Consulting. All Rights Reserved

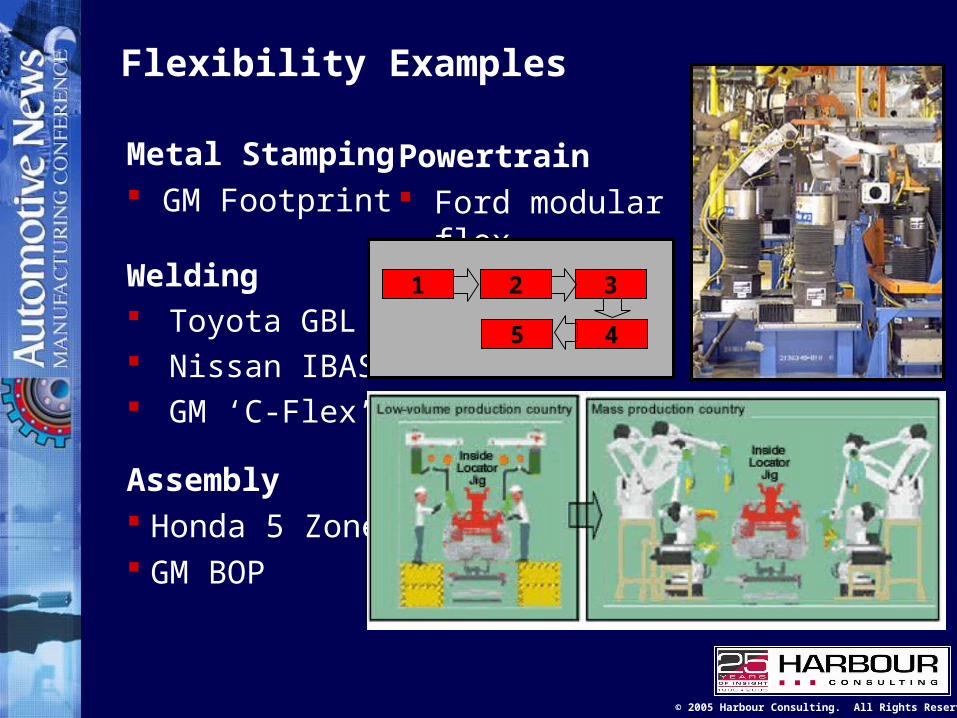

Flexibility Examples

Welding Toyota GBL Nissan IBAS GM ‘C-Flex’

Metal Stamping GM Footprint

Powertrain Ford modular flex

Assembly Honda 5 Zone GM BOP

1 2 3

45

© 2005 Harbour Consulting. All Rights Reserved

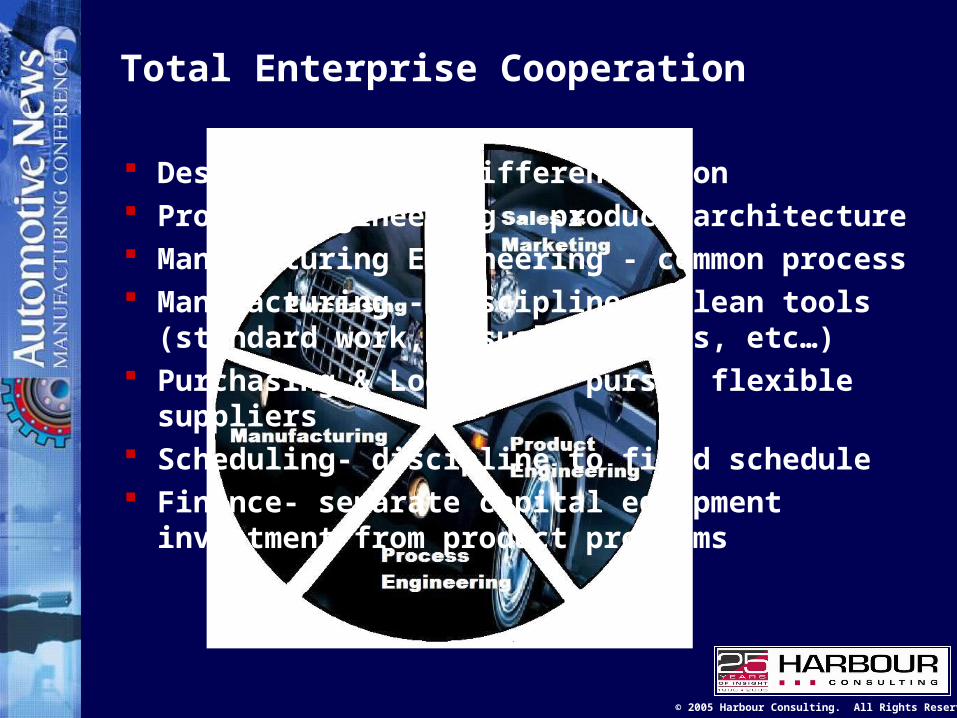

Total Enterprise Cooperation

Design- focus on differentiation Product Engineering - product architecture Manufacturing Engineering - common process Manufacturing - discipline to lean tools (standard

work, visual controls, etc…) Purchasing & Logistics- pursue flexible suppliers Scheduling- discipline to fixed schedule Finance- separate capital equipment investment

from product programs

© 2005 Harbour Consulting. All Rights Reserved

The Bottom Line

Flexibility is important for all plants but even more critical for suppliers

Some manufacturers are more effective at low cost flexibility than others- a significant competitive differentiator

Flexibility does not have to cost more money The winners will be the plants that can handle

variety and change quickly from old to new

Ron HarbourPresident

Harbour Consulting