24

Russian hydrocarbon sectors Andrei V Belyi, CEURUS, Tartu

| Date post: | 22-Dec-2015 |

| Category: |

Documents |

| Upload: | derick-jennings |

| View: | 227 times |

| Download: | 0 times |

Russian hydrocarbon sectors

Andrei V Belyi, CEURUS, Tartu

structurestructure

1. Historical and institutional specificities 2. Reserves, production and exports 3. Dynamics in oil sector4. Oil pipelines5. Gas sector: domestic issues6. Gas Export dimension State-owned companies7. Gazprom and Rosneft: new policy

dimensions

1. Historical and institutional specificities

Soviet legacies of energy sectors

In addition, Russia’s political strategy remains in scope of disputes

Regulation of hydrocarbon• No energy-specific regulator

– Federal Anti-Monopoly Service (FAS) covering issues of competition, anti-trust and consumer protection (remains very liberal)

– Federal Tariff Service (FTS) covering price regulation in natural monopolies; also responsible for monitoring of price

– Ministries: (1) Economic development, (2) Energy and (3) Natural Resources

• Oil sector was restructured since 1992 – No monopoly on export but a growing concentration on production – Oil pipelines are unbundled from production, private pipelines are possible

• Gas sector exempted from restructuring– But legislation is set for a wholesale market, issues with implementation– Gazprom owns MRG, the pipeline operator– Export monopoly, de-jure since 2005

Before 1917 First drilling in Baku in 1846 (second drilling after US in 1814)

Volga region develomment since 1864

1917-1955 Large exploration and production works started in North Caucasus, Volga-Ural regions

1955-1991 Negative prospects for further oil discoveries proven to be wrong: with Timan Pichora and Western Siberia oil reserves Russian production boosted

1991- to date New discoveries provide even larger production potential in the short-term production increase: North Caspian, East Siberia Sakhalin,

Exploration ongoing Russian and Siberian North still has an important estimated resource potential

Arctic Shelf

Kamch

atka

Sakhalin

Barents Sea

Timan Pichora

Baku

Volga

N. CaucasusN. Caspian

Urals

Vast reserves allowed an energy intensive economy but access to new fields in EasternRegions is more difficult hence requires a new approach

2. Reserves, production and exports

West Siberia

Source: IEA, 2002 , TEK, 2008 and BBVA, 2008

East Siberia

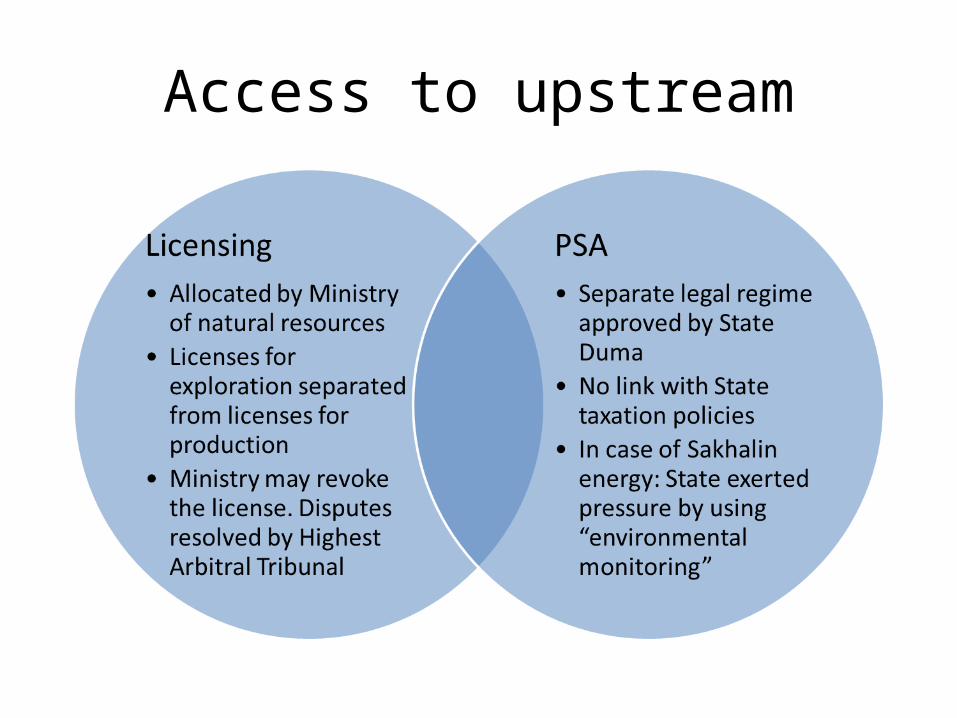

Access to upstream

Russia is the first world gas producer, But gas consumption close to the EU level

Up to 70% of gas production is consumed Domestically

Production

Domestic consumption

BCM

258262260230

190164144

481470459

421

380348

323

0

100

200

300

400

500

600

2000 2001 2002 2003 2004 2005 2006 2007

Production

Export

Mln

ton

s

Mln tons

Mln tons

Oil Export growth with the production, but half of oil goes for Russian internal market

Russia is the world largest oil and gas producerRussia is the world largest oil and gas producerBut also a large hydrocarbon consumerBut also a large hydrocarbon consumer

How to accommodate domestic demand and export ambitions?How to accommodate domestic demand and export ambitions?

Russia’s oil and gas production since 2000

Exports historically oriented to Europe (outdated map shows that by 2001 no exports to Asia)

2001-2003 2003-20101992-2000

VSNK(3-5%)

Gazprom(7-8%)

Yukos(12-13%)

Rosneft(5-6%)

Onako(1-2%)

Sidanko(8-9%)

TNK(9-10%)

Sibneft(7-8%)

Tatneft(7-8%)

SurgutNG(11-12%)

Lukoil (19%)

Slavneft(5-7%)

Yukos acquires VSNK(20-21%)

SurgutNG(15%)

Rosneft(5-6%)

TNK acquires Sidanko, Onako(12%)

Slavneft(4%)

Sibneft(9-10%)

Gazprom(7%)

Tatneft(5-6%)

Lukoil(19%)

Rosneft(28%)

state-owned

TNK-British Petroleum Holding (16-17%) private

Gazpromneft (8%)State-owned

Tatneft(6%) regionally owned

SurgutNG(16-17%)private

Lukoil(22%)private

Reasons for concentration:

– Political:

- Concentration of the control over strategic state resources

- Easier conditions to conclude profitable concessions

– Economic/financial:

- Larger profits stimulated by the high world oil prices

- Attraction of external capital to invest into the sector

– Technical:

- Better capability to exploit difficult areas of resources

Russian oil companiesApprox. Production share in brakets

With purchase of TNK-BP (2012), Rosneft can be defined as a new NOC

3. Dynamics in oil sector

• Transition from command to market economy in the 1990s lead to a decrease in production. In 1998 oil production represented 59% of its 1990 level

• After 1999: oil sector regained its strength with the economic stabilization and world price increase

• In 2004 Largest production subsidiary Yuganskenftegaz was taken over by the state owned company Rosneft from Yukos

• Stagnation after 2007 mainly due to inefficient taxation system (Royalty is linked to world oil price)

• Tax relief since 2009 for greenfields but limited effect

• In 2013 production rate reached the level of 1988 but average marginal costs are high

• Regulation on access to small fields is stalled

• Transition from command to market economy in the 1990s lead to a decrease in production. In 1998 oil production represented 59% of its 1990 level

• After 1999: oil sector regained its strength with the economic stabilization and world price increase

• In 2004 Largest production subsidiary Yuganskenftegaz was taken over by the state owned company Rosneft from Yukos

• Stagnation after 2007 mainly due to inefficient taxation system (Royalty is linked to world oil price)

• Tax relief since 2009 for greenfields but limited effect

• In 2013 production rate reached the level of 1988 but average marginal costs are high

• Regulation on access to small fields is stalled

Source: Oil & Capital

1995-99: lowest production level

Oil production decline after Break-down of the USSR (1991) Due to under-Investments

1992: private and state-owned oil companies start operating Russian oil sector

Mln tons

Oil Production and export: historical trends

Profits decline unwillingness to change classification to avoid decrease in capitalization

Oil products

Refineries are concentrated on the western part of RussiaLevels of price vary from 0.6 Eur to 1 Eur per l.Yakutia and Far East have the highest levels (low market fragmentation)

Source: Russian Energy Agency, 2013

Página 14

Transneft pipelinesSpecificities:

– Telescope down effect: built to supply former satellite countries, the pipeline capacity is small on export points due to the low demand in Eastern Europe.

– Different heavy and light oil sorts are commingled in Druzhba pipeline within one flow (so called Urals), Ministry of Energy constantly delayed quality banking

– Pro rata regulation is applied: all oil producers get a quota according to the production level

Constructed during Soviet era, pipeline sector needs to be reshaped in order to meet world market structure

World longest oil pipeline networkSource: TEK, 2008

Length: 50 000 kmAverage shipment length: 3000 kmDruzhba pipeline: 5500km

crude oiloil products

Baltic terminals

Black sea

terminals(

Druzhba

Druzhba

0%

20%

40%

60%

80%

100%

Before1992

2001-2005 2005-2008 2010 2012

Druzhba To Black Sea To Baltic Sea To Pacif ic

Geography of Transneft oil shipments in timeSource: TEK, 2008 Oil shipment via Druzhba and

Black sea terminals decreasesProportionally to an increased use of Baltic terminals and of the Pacific in future.

Effects: decrease of shipment to Baltic branches (LV and LT)

Geography of export by pipeline: decrease of Druzhba and increase of terminals

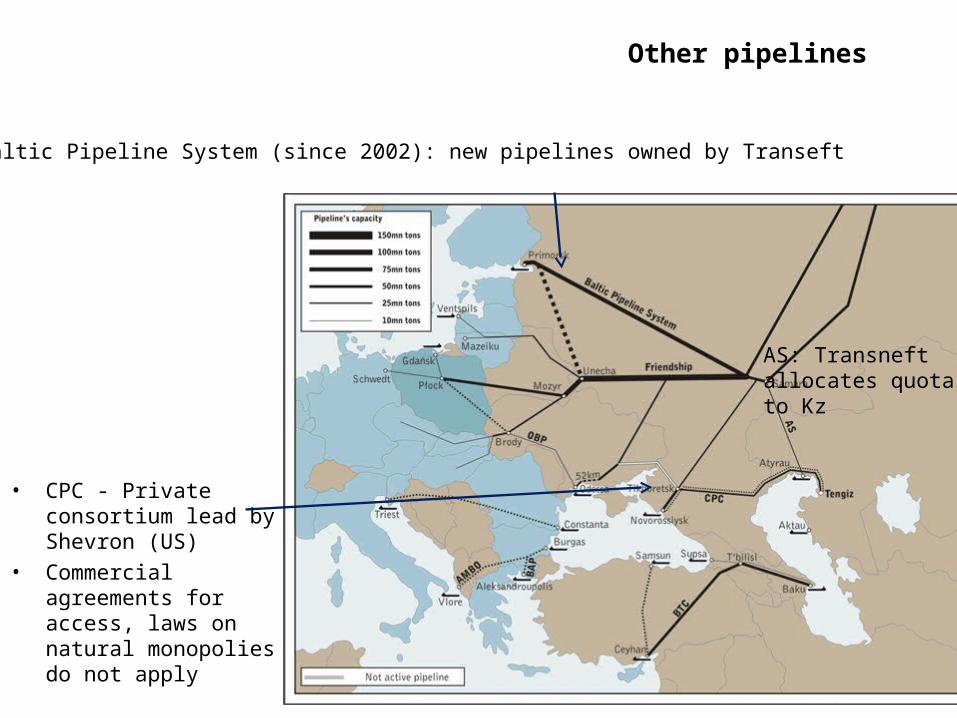

Other pipelines

• CPC - Private consortium lead by Shevron (US)

• Commercial agreements for access, laws on natural monopolies do not apply

Baltic Pipeline System (since 2002): new pipelines owned by Transeft

AS: Transneft allocates quotas to Kz

5. Russian gas sector: domestic issues

Russia is the first world gas producer

Russia is the world leading gas consumer:Up to 70% of gas production is consumed Domestically need to reduce gas flaring

Production

Domestic consumptionBCM

Export is monopolized by GazpromOil companies and independents sell gas domestically

EU oriented export, East direction is underdeveloped

1992-2010

Novatek aims at producing 115-120 bcm by 2020

Gazprom would allocate an internal market, but price is uncompetitive Pressure on exports Oct 2012 Novatek concludes 10 yrs agreement to supply German costumer EnBV with 2 bcm annually

Institutional setting

Towards wholesale market?

Gazprom’s gas deliveries to Europe 2007-2011

Source: T. Vehrs, Gazprom Germania presentation, Tallinn 14.11.2012

Most of gas is delivered under long term contracts, long term upstream Most of gas is delivered under long term contracts, long term upstream investments needed:investments needed:- Development of upstream: Northern Yamal, South East Nadym Pur Taz; Far East; Eastern Siberia- Largest investment plans: 40 billion USD till 2020 (mostly transport infrastructure) need for long term contracts with take-or-pay

Gazprom participates in the spot, and increases competition for the European Gazprom participates in the spot, and increases competition for the European retailers retailers ground for disputes ground for disputes

2007 2008 2009 2010 2011Export in bcm 153 160 148 139 150Other (incl. Hub trade) in bcm 16 8 7 10 9Price in USD per MMBTU 7.6 11.6 7.3 8.5 10.8

6. Export dimension6. Export dimension

EU-Russia gas trade issuesEU-Russia gas trade issues

EstoniaEstonia LatviaLatvia LithuaniLithuaniaa

Eesti Eesti Gaas Ltd.Gaas Ltd.

JSC JSC Latvijas Latvijas GazeGaze

JSC JSC Lietuvos Lietuvos DujosDujos

GazpromGazprom - - 37% 37%

IteraItera Latvia-Latvia- 9.85%9.85%

GazpromGazprom - - 25%25%

IteraItera Latvia-Latvia- 25%25%

GazpromGazprom - - 37.1%37.1%

Gazprom and Baltic States: area of difficulty

Most difficulties are with Baltic states, where Gazprom has stakes in distributionEE and LT decided to implement full ownership unbundling disputes

7. State-owned companies:Gazprom and Rosneft

• Both Rosneft and Gazprom are state-owned but dynamic of influence is different– Gazprom is a VIC which is in path to a decentralization (without losing

the institutional structure)– Rosneft became a China-type NOC

• Financial differences:– Since 2000s oil export revenue is higher (reaching 172 bln USD in

2012) then of gas (58 bln USD for gas)– Rosneft is less dependent on exports– Rosneft was successful in dealing with China– Level of securitization of oil imports from Russia is much less

significant