31

1 Russian VC market overview VTB Capital’s perspective Zurich, July 11, 2013 www.vtbcapital-im.com

1

Russian VC market overview

VTB Capital’s perspective

Zurich, July 11, 2013

www.vtbcapital-im.com

2

Table of contents

Venture Capital Business of VTB Capital 3

Our Market 6

Our Strategy and Investments 16

Our War Chest 22

3

Venture capital business of VTB Capital

Geography of investments

Co-investments with top-tier venture capital firms

Global geographic coverage

Established in 2006

US$350 million in AuM

9 investment professionals

6 full-time finance, legal and administrative professionals

First venture-backed IPO in Russia (MICEX:RNAV)

Partnership with Draper Fisher Jurvetson (DFJ)

35 portfolio companies in IT, Internet, e-commerce,

material science, energy efficiency and other industries

Co-investments with Sequoia Capital, Bessemer Venture

Partners, Andreessen Horowitz, Qualcomm Ventures,

Atomico, Menlo Ventures, Asahi Glass, Amadeus,

eVenture, Mangrove Capital Partners and Ventech

44% CAGR of portfolio revenue in 2008-2012

Market leader of venture capital industry in Russia & CIS*

Offices: Moscow, Astana and Silicon Valley

*CIS - The Commonwealth of Independent States includes most of the former Soviet Union Republics: Russia, Ukraine, Belarus, Armenia, Azerbaijan, Kazakhstan, Kyrgyzstan,

Moldova, Turkmenistan, Tajikistan and Uzbekistan

4

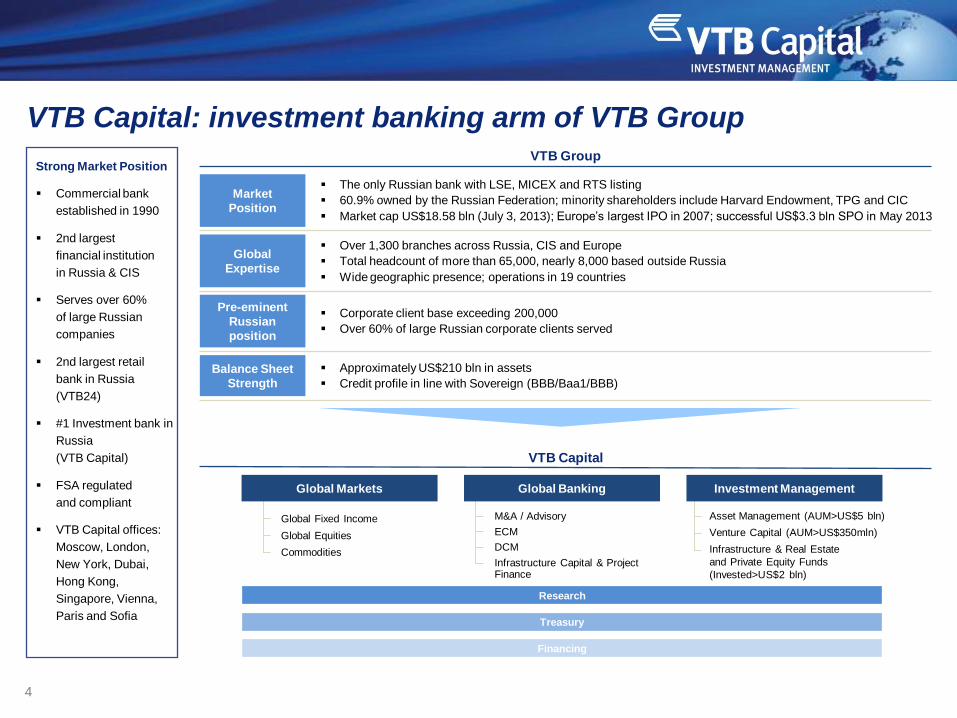

VTB Capital: investment banking arm of VTB Group

Global Fixed Income

Global Equities

Commodities

Asset Management (AUM>US$5 bln)

Venture Capital (AUM>US$350mln)

Infrastructure & Real Estate

and Private Equity Funds

(Invested>US$2 bln)

M&A / Advisory

ECM

DCM

Infrastructure Capital & Project Finance

Research

Treasury

Financing

Global Markets Global Banking Investment Management

Strong Market Position

Commercial bank

established in 1990

2nd largest

financial institution

in Russia & CIS

Serves over 60%

of large Russian

companies

2nd largest retail

bank in Russia

(VTB24)

#1 Investment bank in

Russia

(VTB Capital)

FSA regulated

and compliant

VTB Capital offices:

Moscow, London,

New York, Dubai,

Hong Kong,

Singapore, Vienna,

Paris and Sofia

Market

Position

The only Russian bank with LSE, MICEX and RTS listing

60.9% owned by the Russian Federation; minority shareholders include Harvard Endowment, TPG and CIC

Market cap US$18.58 bln (July 3, 2013); Europe’s largest IPO in 2007; successful US$3.3 bln SPO in May 2013

Global

Expertise

Over 1,300 branches across Russia, CIS and Europe

Total headcount of more than 65,000, nearly 8,000 based outside Russia

Wide geographic presence; operations in 19 countries

Pre-eminent

Russian

position

Corporate client base exceeding 200,000

Over 60% of large Russian corporate clients served

Balance Sheet

Strength

Approximately US$210 bln in assets

Credit profile in line with Sovereign (BBB/Baa1/BBB)

VTB Group

VTB Capital

5

Table of contents

Venture Capital Business of VTB Capital 3

Our Market 6

Our Strategy and Investments 16

Our War Chest 22

6

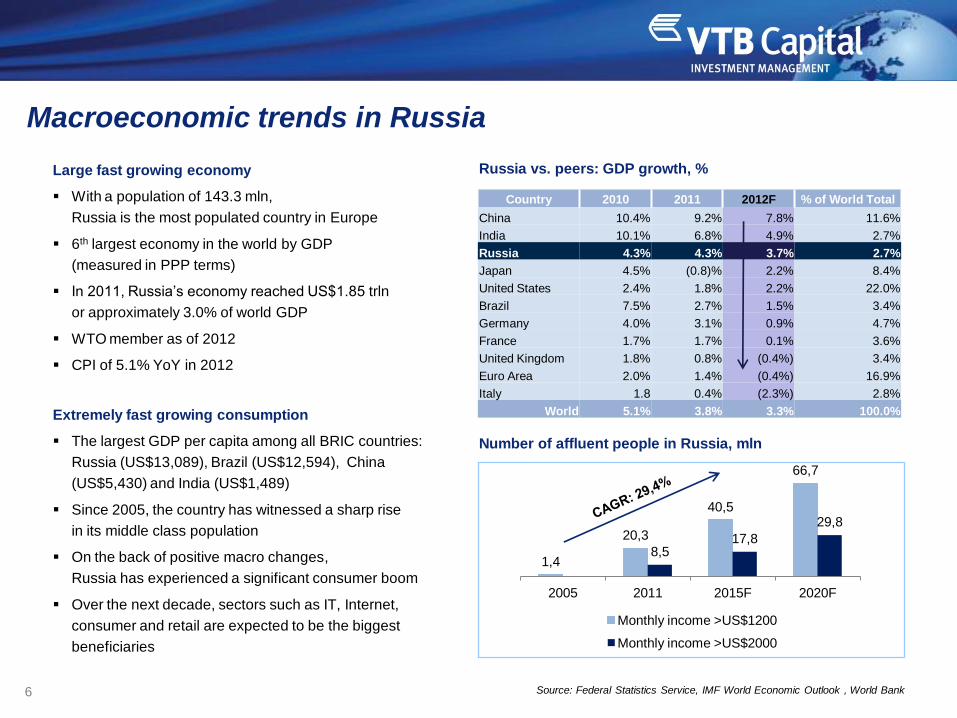

Macroeconomic trends in Russia

Large fast growing economy

With a population of 143.3 mln,

Russia is the most populated country in Europe

6th largest economy in the world by GDP

(measured in PPP terms)

In 2011, Russia’s economy reached US$1.85 trln

or approximately 3.0% of world GDP

WTO member as of 2012

CPI of 5.1% YoY in 2012

Source: Federal Statistics Service, IMF World Economic Outlook , World Bank

Number of affluent people in Russia, mln

Russia vs. peers: GDP growth, %

Extremely fast growing consumption

The largest GDP per capita among all BRIC countries:

Russia (US$13,089), Brazil (US$12,594), China

(US$5,430) and India (US$1,489)

Since 2005, the country has witnessed a sharp rise

in its middle class population

On the back of positive macro changes,

Russia has experienced a significant consumer boom

Over the next decade, sectors such as IT, Internet,

consumer and retail are expected to be the biggest

beneficiaries

1,4

20,3

40,5

66,7

8,5 17,8

29,8

2005 2011 2015F 2020F

Monthly income >US$1200

Monthly income >US$2000

Country 2010 2011 2012F % of World Total

China 10.4% 9.2% 7.8% 11.6%

India 10.1% 6.8% 4.9% 2.7%

Russia 4.3% 4.3% 3.7% 2.7%

Japan 4.5% (0.8)% 2.2% 8.4%

United States 2.4% 1.8% 2.2% 22.0%

Brazil 7.5% 2.7% 1.5% 3.4%

Germany 4.0% 3.1% 0.9% 4.7%

France 1.7% 1.7% 0.1% 3.6%

United Kingdom 1.8% 0.8% (0.4%) 3.4%

Euro Area 2.0% 1.4% (0.4%) 16.9%

Italy 1.8 0.4% (2.3%) 2.8%

World 5.1% 3.8% 3.3% 100.0%

7

Russian Internet: opportunity impossible to ignore

One of the biggest Internet markets in the world

Russian internet audience is one of the largest in

Europe, having approached Germany’s level in 2012

A total of 80 million Russian language

internet users worldwide constitutes the 5th largest

language group (after English, Chinese,

Japanese and Spanish)

European online audience (mln) – June 2012

Source: FOM, TNS Gallup, BofA Merill Lynch

Internet users as % of population: Russia vs. World – June 2012 Room to grow

Russia’s current Internet penetration level (52%)

is still behind developed countries and it is projected

to grow up to 82% in the long run (2018)

61 67

52 53

36 32

0

10

20

30

40

50

60

70

80

Russia Germany France UK Italy Spain

84%

83%

80%

80%

78%

67%

58%

52%

40%

39%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

UK

Germany

France

Japan

USA

Spain

Italy

Russia

China

Brazil

8

Russian e-commerce: the next big thing

Key facts

In 2011, the e-commerce sector reached US$9.1 billion a year

According to Morgan Stanley Research, Russian e-commerce is expected to grow at 44% CAGR in 2012-2014

E-trade represents only 1.6% of total retail turnover, which leaves huge room to grow compared to USA (4.4%) and China

(3.7%), while it is similar to the US and Chinese ratios in 2000 and 2007, respectively

Source: Data Insight 2012, GP Bullhound, June 2012

E-commerce market in Russia (2008-2015F), US$ bln E-commerce share of total retail in Europe

5 6 8

9,1

18

30

0

5

10

15

20

25

30

35

2008 2009 2010 2011 2015F 2020F

9

0

2

4

6

8

10

12

14

16

18

20

2011 2012 2013 2014 2015

Wire transfers* Terminals E-money, virtual cards, mobile banking

E-payment industry in Russia Market size, bln USD

7,8

10,0

12,4

15,5

19,0

Source: BCG, Industry Analytics, Euro Monitor, Central Bank of Russia, FOM

* Card payments

92% 87%

62% 60%

28%

8% 13%

38% 40%

72%

Russia Eastern Europe

Latin America

Asia Developed countries

Cash Non-cash

Breakdown of payments by region

10

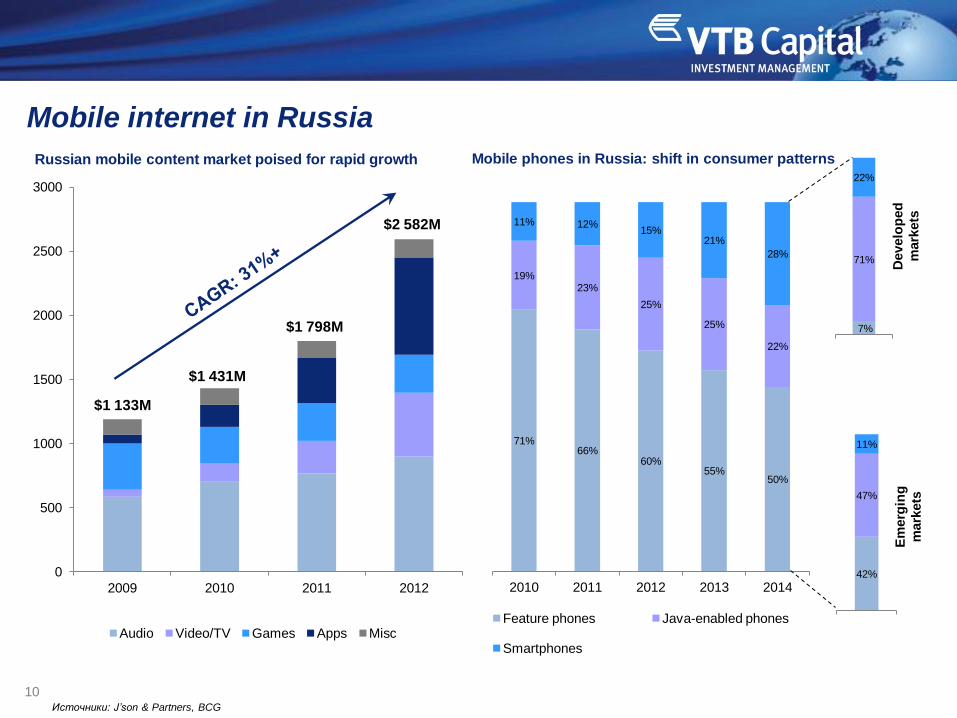

Mobile internet in Russia

71% 66%

60% 55%

50%

19% 23%

25%

25%

22%

11% 12% 15%

21%

28%

2010 2011 2012 2013 2014

Feature phones Java-enabled phones

Smartphones

7%

71%

22%

42%

47%

11%

Mobile phones in Russia: shift in consumer patterns

Develo

ped

mark

ets

E

merg

ing

mark

ets

0

500

1000

1500

2000

2500

3000

2009 2010 2011 2012

Audio Video/TV Games Apps Misc

$1 133M

$1 431M

$1 798M

$2 582M

Источники: J’son & Partners, BCG

Russian mobile content market poised for rapid growth

11

Russian Internet: local leaders dominate the market

Local start-ups have substantial advantages in winning and retaining market share over global leaders.

To conquer the market companies need to be local

International companies are likely to acquire successful local start-ups rather than build from scratch,

creating exit opportunities for start-ups

Russian Internet market

remains largely dominated by local players

Russian companies are leaders in their respective categories

Language complexities

Similar to China, Japan and South Korea, language is one of the

key barriers to entry in the Russian Internet market

Marketing specifics

Effective marketing campaigns require a specific understanding

of consumer preferences and behavioral habits

Logistics Impacting Profitability

The vast size of the country and shortage of fast, cheap

and reliable logistical systems is a natural barrier for many global e-

tailers. Local players like Ozon and KupiVIP have been able

to successfully solve this problem by building their own logistics.

Category Global Leader Russian Leader

Search engine

Electronics

retail

Social network

Online

classifieds

Genealogy

network

Mobile

payments

12

Russian Internet: VC landscape

9

18

35

16

0

5

10

15

20

25

30

35

40

2009 2010 2011 1H2012

52$ 69$

163$

228$

0

50

100

150

200

250

2009 2010 2011 1H2012

Capital raised, mln USD

Most active international players

Leading local investors

Number of deals

Source: GP Bullhound

13

Russian start-ups: stories of huge success and more to come

… and that is just the top of the iceberg: other success stories include ABBYY, Sapato, Darberry …

ParaGraph

3D Internet software

Founded in 1989 in

Moscow

Acquired by Silicon

Graphics (SGI) in

1997 for $200 mln

IPG Photonics

Provider of high power and

high performance fiber

lasers and amplifiers

Founded in 1989 in

Moscow

IPO on NASDAQ in Dec

2006

Current market cap: $3,2B

Mail.Ru Group

Russian major online

portal and Internet

holding

IPO on LSE in Nov 2010

at $5.7B

Yandex

Russian Google

Founded in 2000 in

Moscow

IPO on NASDAQ in May

2011 at $8.4B

Qiwi

Russian major e-

payment system

IPO on NASDAQ in

May 2013

$1.0B market cap

Evernote

Popular note-taking

service founded by

Stepan Pachikov

Over $40 mln users

worldwide

Over $1.0B current

evaluation

Kaspersky Labs

World’s largest privately-

held vendor of software

security

Founded in Moscow in

1997

General Atlantic acquired

20% in secondaries for

$200M in January 2011

Parallels

One of the worlds leading

providers of virtualization

software

Founded in 1999 by

Sergey Beloussov

Backed by Bessemer,

Insight, Intel, Siguler Guff,

Cisco and Almaz

Ozon

Russian Amazon

Founded in Moscow in

1998

Backed by Baring Vostok,

Index, Alpha Associates

Now preparing for IPO

1997 2006 2011 2010 2013 … … …

14

Hi-tech opportunity: products and markets

Hi-tech today represents multibillion markets with tremendous growth rates

Clean Energy

Market in 2017: US$114,7 bln

CAGR: 12,5%+*

Huge market with growth

based on exponential increase

of energy demand

Market in 2017: US$329,1 bln

CAGR: 5,4%+*

The industry is already

operating at nanoscale,

driven by Moore’s Law

Market in 2017: US$13,1 bln

CAGR: 54,9%+*

Fast growing market based

on opportunity to operate

with molecules and

nano ‘building blocks’

Market in 2017: US$3,4 bln

CAGR: 100%+**

Perspective industry due

to the fundamental advantages

of photons in comparison

with electrons

* Source: VTB Capital research

** Source: marketsandmarkets.com

Materials

Electronics

Nanooptics

15

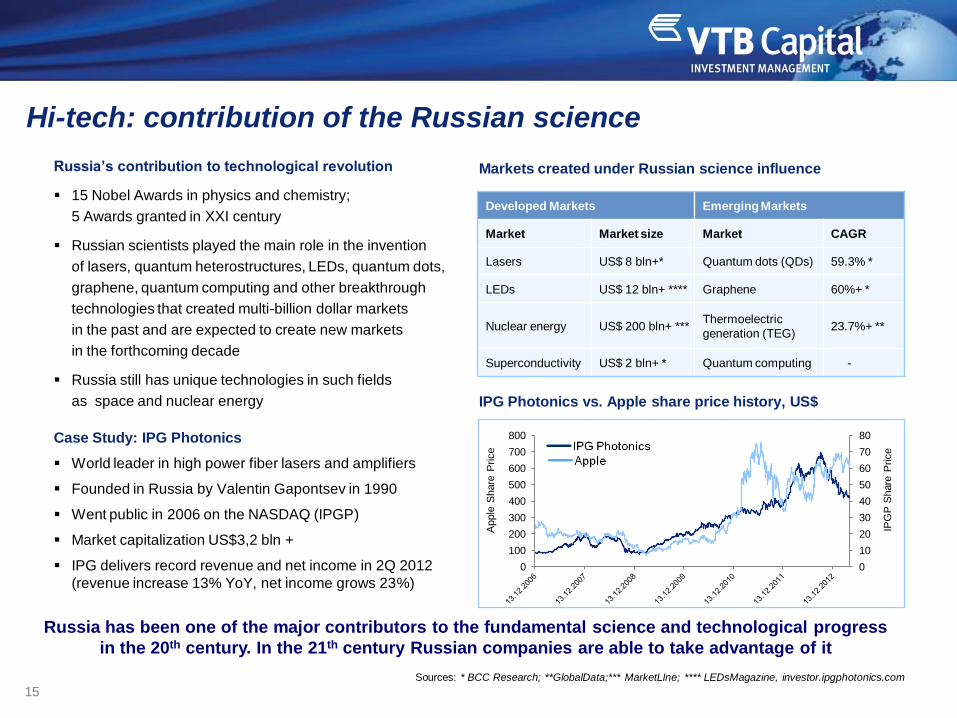

Russia’s contribution to technological revolution

15 Nobel Awards in physics and chemistry;

5 Awards granted in XXI century

Russian scientists played the main role in the invention

of lasers, quantum heterostructures, LEDs, quantum dots,

graphene, quantum computing and other breakthrough

technologies that created multi-billion dollar markets

in the past and are expected to create new markets

in the forthcoming decade

Russia still has unique technologies in such fields

as space and nuclear energy

Hi-tech: contribution of the Russian science

Developed Markets Emerging Markets

Market Market size Market CAGR

Lasers US$ 8 bln+* Quantum dots (QDs) 59.3% *

LEDs US$ 12 bln+ **** Graphene 60%+ *

Nuclear energy US$ 200 bln+ *** Thermoelectric

generation (TEG) 23.7%+ **

Superconductivity US$ 2 bln+ * Quantum computing -

Markets created under Russian science influence

Sources: * BCC Research; **GlobalData;*** MarketLIne; **** LEDsMagazine, investor.ipgphotonics.com

Russia has been one of the major contributors to the fundamental science and technological progress

in the 20th century. In the 21th century Russian companies are able to take advantage of it

Case Study: IPG Photonics

World leader in high power fiber lasers and amplifiers

Founded in Russia by Valentin Gapontsev in 1990

Went public in 2006 on the NASDAQ (IPGP)

Market capitalization US$3,2 bln +

IPG delivers record revenue and net income in 2Q 2012

(revenue increase 13% YoY, net income grows 23%)

IPG Photonics vs. Apple share price history, US$

0

10

20

30

40

50

60

70

80

0

100

200

300

400

500

600

700

800

IPG

P S

hare

Price

Apple

Share

Price

16

* Source: Ministry of Economic Development of the Russian Federation

** Source: EIU, UNESCO, Eurostat as of May 2012

Russia as a major market for new technologies

Government share in national expenditure on R&D**

Russian state-owned

companies

Expenditures on Innovations

as % of Revenue* Foreign peer

2010 2011 2012F

RusHydro 0.0% 3.2% 3.0% Fortum (0.5%)

Federal Grid Company 1.2% 2.4% 3.2% EdF (0.7%)

Rosneft 0.2% 0.4% 0.4% Petroleo Brasiliero (0.8%)

Space Corp. Energia 1.4% 3.9% 7.0% Alliant Techsystems (6.2%)

ALROSA 0.1% 0.2% 0.3% De Beers (0.2%)

Russian Technologies 0.4% 0.9% 1.1% United Technologies (3.1%)

Rostelecom 0.0% 0.2% 0.6% France Telecom (1.7%)

Growth of expenditures on innovation technologies stemming

from state-owned companies

Russia votes for modernization

Recently, Russia has taken a new course towards

modernization. The plan is to radically increase

penetration of innovative products in the Russian

market and spend more on foreign technology and

transfer of best practices to Russia.

The total budget for the Innovative Development

Program (designed to modernize manufacturing and

business infrastructures) for all Russian state-owned

companies, over next 3 years, is approximately

US$30 bln.

The Russian market represents

a huge opportunity for foreign

high-tech companies and startups

17

Table of contents

Venture Capital Business of VTB Capital 3

Our Market 6

Our Strategy and Investments 16

Our War Chest 22

18

Global Markets

Taking global technologies to Russia Taking Russian technologies global

Silicon Valley start-ups with potential to penetrate the

Russian market

(later stage: rounds from C to pre-IPO)

Russian-origin start-ups developing and commercializing

products with unrevealed potential in the global markets

(early stage: rounds A and B)

Hi-tech, new materials, nanoelectronics,

nanophotonics, energy efficiency,

biopharmaceuticals

Enterprise software, cloud, big data and hi-tech

including space, nuclear technologies, new

materials, nanophotonics, quantum computing, etc.

Investment in local leaders

Technological enterprises – leaders and pioneers of their segment

inside Russia and CIS (early stage: rounds A and B)

Drivers of Growth

Fast growing middle class, healthy macroeconomics

Natural barriers for entry for foreign enterprises (language,

regulations, etc.)

Second largest internet audience in Europe, growing at 15% YoY

Global markets opportunity

Commercialization of Russian-originated IT

technologies leveraging Russia software expertise

Access to global technological companies,

involvement of foreign business executives and

investors, access to the developed innovative

infrastructure outside Russia

Direct access to one of the largest consumer

markets in Europe

Hugely underpenetrated market for innovative

technologies

VTB as strong local partner with direct access to all

major businesses and institutions inside Russia

Opportunity in Russia and CIS

E-commerce, e-payments, mobile, social, technology

Our investment strategy: leveraging Russia

Russia and CIS

40%

30% 30%

19

Leading developer of Internet

companies in Russia

Leading Russian online hotel

booking company

#1 genealogical social network

in Russia

Leading company in Russia & CIS

web-conferencing market

#1 company in mobile payments

in Russia

Leading company in Russian

NFC mobile payment market

Advanced technology platform

for large-scale eCommerce

PaaS provider of Dynamic Case

Management solutions

#1 Russian manufacturer of

laser cutting equipment

Pioneer manufacturer of skin

antiseptic in Russia

Our portfolio

#1 Russian vehicle-tracking

(GPS/GLONASS) company

Russian manufacturer of novel

microchannel plates

20

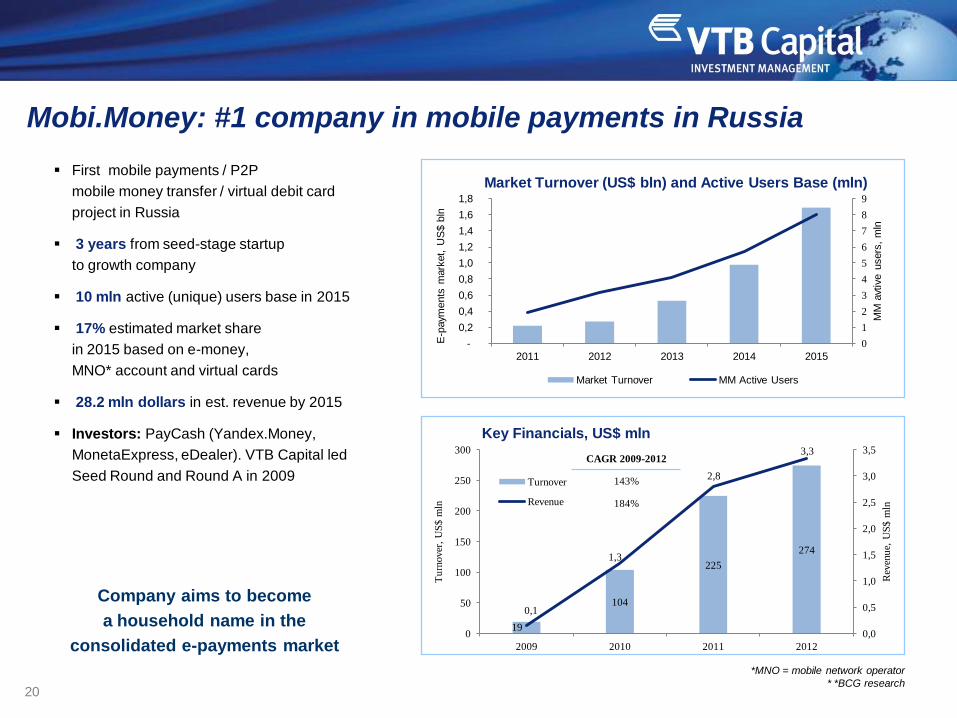

Mobi.Money: #1 company in mobile payments in Russia

First mobile payments / P2P

mobile money transfer / virtual debit card

project in Russia

3 years from seed-stage startup

to growth company

10 mln active (unique) users base in 2015

17% estimated market share

in 2015 based on e-money,

MNO* account and virtual cards

28.2 mln dollars in est. revenue by 2015

Investors: PayCash (Yandex.Money,

MonetaExpress, eDealer). VTB Capital led

Seed Round and Round A in 2009

Company aims to become

a household name in the

consolidated e-payments market

*MNO = mobile network operator

* *BCG research

Market Turnover (US$ bln) and Active Users Base (mln)

19

104

225

274

0,1

1,3

2,8

3,3

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

0

50

100

150

200

250

300

2009 2010 2011 2012

Rev

enu

e, U

S$

mln

Tu

rnover

, U

S$

mln

Key Financials, US$ mln

Turnover

Revenue

CAGR 2009-2012

143%

184%

0

1

2

3

4

5

6

7

8

9

-

0,2

0,4

0,6

0,8

1,0

1,2

1,4

1,6

1,8

2011 2012 2013 2014 2015

MM

avt

ive u

sers

, m

ln

E-p

aym

ents

mark

et, U

S$ b

ln

Market Turnover MM Active Users

21

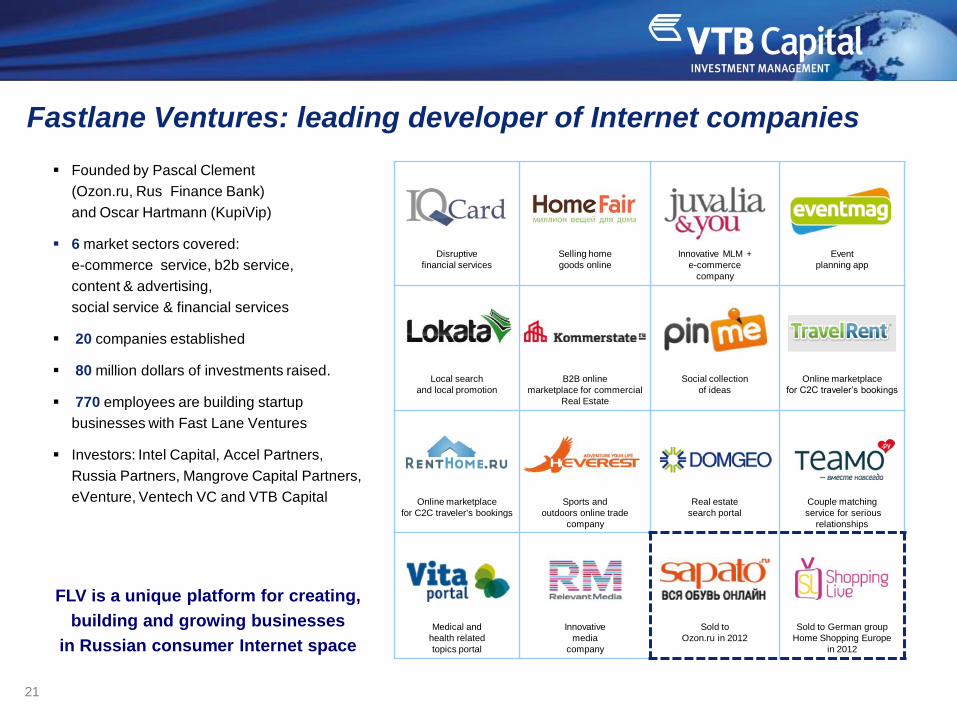

Fastlane Ventures: leading developer of Internet companies

Founded by Pascal Clement

(Ozon.ru, Rus Finance Bank)

and Oscar Hartmann (KupiVip)

6 market sectors covered:

e-commerce service, b2b service,

content & advertising,

social service & financial services

20 companies established

80 million dollars of investments raised.

770 employees are building startup

businesses with Fast Lane Ventures

Investors: Intel Capital, Accel Partners,

Russia Partners, Mangrove Capital Partners,

eVenture, Ventech VC and VTB Capital

FLV is a unique platform for creating,

building and growing businesses

in Russian consumer Internet space

Disruptive

financial services

Selling home

goods online

Innovative MLM +

e-commerce

company

Event

planning app

Local search

and local promotion

B2B online

marketplace for commercial

Real Estate

Social collection

of ideas

Online marketplace

for C2C traveler’s bookings

Online marketplace

for C2C traveler's bookings

Sports and

outdoors online trade

company

Real estate

search portal

Couple matching

service for serious

relationships

Medical and

health related

topics portal

Innovative

media

company

Sold to

Ozon.ru in 2012

Sold to German group

Home Shopping Europe

in 2012

22

RNT: pioneer in GLONASS and GPS smart fleet management

solutions

The first venture-backed IPO in Russia

(MICEX:RNAV, July 2010)

28% of the Russian market for vehicle tracking

solutions by number of installed units of

equipment

34%+ revenue CAGR during the last 4 years.

500+ investors, including institutional investors

and funds

4000+ clients in 9 countries of operations,

more than 92 dealers in 55 Russian regions

VTB Capital led round A in 2008

Company is expected to grow

by 50% during next 3 years

Installed Equipment, thousand units

Revenue, RUR mln

141 210

446

665

458

0

100

200

300

400

500

600

700

2008 2009 2010 2011 2012

60

101

170 190

0

20

40

60

80

100

120

140

160

180

200

2009 2010 2011 2012

* Company’s estimates

23

Table of contents

Venture Capital Business of VTB Capital 3

Our Market 6

Our Strategy and Investments 16

Our War Chest 22

24

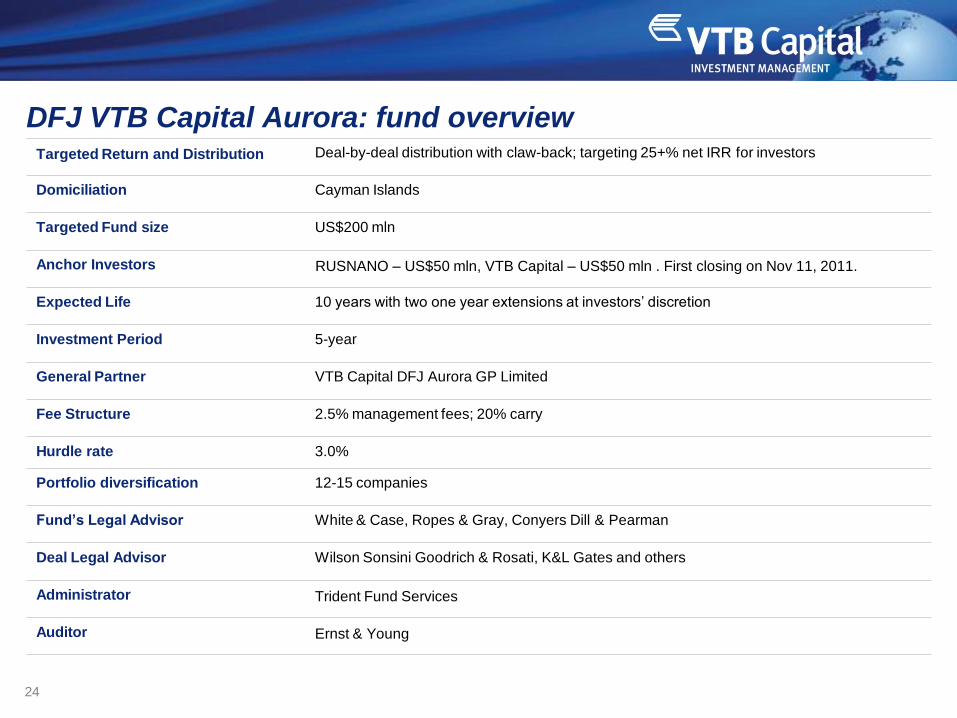

DFJ VTB Capital Aurora: fund overview

Targeted Return and Distribution Deal-by-deal distribution with claw-back; targeting 25+% net IRR for investors

Domiciliation Cayman Islands

Targeted Fund size US$200 mln

Anchor Investors RUSNANO – US$50 mln, VTB Capital – US$50 mln . First closing on Nov 11, 2011.

Expected Life 10 years with two one year extensions at investors’ discretion

Investment Period 5-year

General Partner VTB Capital DFJ Aurora GP Limited

Fee Structure 2.5% management fees; 20% carry

Hurdle rate 3.0%

Portfolio diversification 12-15 companies

Fund’s Legal Advisor White & Case, Ropes & Gray, Conyers Dill & Pearman

Deal Legal Advisor Wilson Sonsini Goodrich & Rosati, K&L Gates and others

Administrator Trident Fund Services

Auditor Ernst & Young

25

Partnerships

Asahi Glass Co (AGC):

Glass application development / Investor

SUSS Microtec AG:

Nanolithography equipment development

University of Michigan:

Mask fabrication materials & process technology Market

Rolith applications: nanostructured coatings for solar sells,

architectural glass and displays. Nanostructured coatings market:

US$1.1 bln – in 2009, US$3.5 bln – in 2015

Team

Boris Kobrin, CEO & Founder:

25 years experience in lithography and semiconductors industry

(Applied Microstructures, Onix Microsystems etc.)

Qualified technological team

Leading scientists from Stanford, University of Michigan,

Univ. of Illinois Urbana-Champaign are involved

Investors

DFJ VTB Capital Aurora: Round A lead (US$3 mln).

Asahi Glass Co (AGC): Seed (US$350k) + Round A

follow-up (US$2mln)

Technology

Near-field/soft lithography + cylindrical masks = sub-wavelength

resolution / scalability / low cost

“Rolling mask” specs: resolution ~ 10 nm; cost ~ US$2/m2;

throughput ~ 3 m2/min

Development Status

Prototype of “rolling mask” lithography

system is up and running

Nanopatterning technology

Is demonstrated on 300 mm wafers Intellectual Property

10+ Patents already filed (US and worldwide) & “know-how”

Rolith, Inc. is developing advanced technology and equipment for nanostructured coatings (anti-reflective, self-cleaning) for the solar panel,

display, and architectural glass markets using a proprietary nanolithography technology. Rolith is capable of making nanostructures cheaper,

faster, and over larger surface areas than currently existing technologies (Nanoimprint lithography, PVD, Sol-gel etc.)

Nature (mm2) Labs (cm2) Rolith (m2)

‘Scaling Nature’ Approach

Portfolio: Rolith

26

Samarium-Sulphide

Unique semiconductor rare earth material with phase transition

“semiconductor-metal” at 6.5 kBar

High levels of electron concentration in conduction band up to 1021

cм3 provide low sensitivity to impurity contamination

Isotropy of physical properties – polycrystalline material makes it

possible to use

SmS films deposited on different materials/substrates (metal, glass,

ceramic, silicon) have a suitable linear temperature expansion

coefficient

Products portfolio

Tenzosensors (Production stage)

Linear and high voltage output signal

High stability against radiation and strong magnetic fields

Wide temperature range -200 to +400°С

Thermoelectric generators, TEGs (R&D stage)

Generation without additional cooling and high efficiency

Can be designed as thin films

Portfolio: SmS Tenzotherm

SmS Tenzotherm GmbH is commercializing 30+ years experience of R&D in the field of the rare-earth Samarium Sulphide (SmS) semiconductors.

Unique properties of SmS open a path to advanced breakthrough products (Tenzosensors, Thermoelectrical generators).

Heat source

Seebek TEG

Heat source

SmS TEG

Cooling

Market

Sensors: US$6.3+ bln market in 2010

Application fields: Construction, oil & gas production, etc.

TEGs: US$1.3 bln market in 2012, CAGR >30%

Application example: Increasing solar panels efficiency by 100%,

cost savings of 25%

Russian-German collaboration

Ioffe Institute (Russia)

Transfer of developed IP to Germany, continuing R&D

MST Factory (Germany)

Manufacturing facilities for SmS products in Germany

Technical University of Dortmund (Germany)

Detailed characterization and fundamental studies of SmS

Intellectual property

Broad portfolio of “know-how” based on 30+ years experience

in Samaruim-Sulphide

Team

The world leading team in Samarium-Sulphide R&D, 30+ years

experience

Professional business team with successful exits in

semiconductor industry (Innolume, OptoGan)

Investors

Russian angel-investors: US$ 1mln (seed round)

DFJ VTB Capital Aurora: US$6 mln (Round A)

Russia’s Top 20

Best Start-ups 2013

27

Portfolio: Avalanche Technology

Avalanche is revolutionizing the US$ 70 bln computer memory market by developing a spin programmable memory (SPMEM) technology that by

itself, delivers on a number of key functional attributes found today only in separate memory technologies such as DRAM, SRAM, NOR and Flash

Technology

Proprietary Spin Programmable Memory (SPMEM)

Cell is 1/5th the size of any current memory device

Scalable beyond 10nm

Technology partners: US and Asian CMOS fabs

Team

Petro Estakhri (co-founder, CEO) took Lexar Media from a start-up

to $1B evaluation in less than 5 years including a successful IPO

and later acquisition by Micron

Dr. Rajiv Ranjan (co-founder, CTO)

former executive at Seagate and Komag

Dr. Yiming Huai (VP Technology), former CTO and co-founder

of Grandis, Inc., one of the pioneer in spin transfer torque magnetic

memory (STT-RAM), acquired by Samsung in 2011

Markets

Market #1: stand alone SPI & DDR end-products replacing current

NOR & HDD/SSD DRAM cache memory. Segment size: US$6+ bln.

Market #2: embedded STT MRAM solution for leading SOC

providers (BRCM, QCOM, NVIDIA) and large fabs (SMIC, Global,

TSMC, IBM, UMC). Segment size: US$10+ bln.

Market #3: STT MRAM enabled SSD’s. Segment size: US$10 bln.

Other Investors: The Fund co-invested US$8 mln in Round D

with US$22 mln from Sequoia Capital, Bessemer Venture Partners,

Vulcan Capital, Thomvest Ventures, and Qualcomm Ventures

Top 10 Most Promising

Storage Start-Ups in 2013

28

Portfolio: Fab.com

Social commerce platform, which allows people all over the globe to access everyday design objects from the world’s largest network of

designers. Fab is the fastest growing e-commerce company ever, having 600 employees in New York, Berlin and Pune (India) and selling

products in 26 countries all over the world.

0

500

1000

1500

2000

2500

2011 2012 2013 2014 2015

Turkey

India/Brazil/Russia

Japan

Europe

USA

New Design Discovery Paradigm in E-shopping Industry

Revenue Projections by Regions (2011-2015), US$ mln

Fab.com has raised over US$150mln from:

Andreessen Horowitz, Atomico, Baroda Ventures, Docomo, First Round

Capital, Mayfield Fund, Menlo Ventures, Pinnacle Ventures, RTP

Ventures, SoftTech VC, SV Angel, VTB Capital (US$7mln), Times

Internet, The Washington Post Company, Zelkova Ventures

verticals

Furniture & Art

Home ware

Home

accessories

Gifts

Fashion

accessories

Fashion

clothes

low price discovery

Today Fab sells 15,000 unique products

Fab sold US$25mln in the past 30 days

Fab’s gross margins are 40%+

11 million members

The average shipping time is 2 days across USA

Fab sells 23 products per minute

2012 sales will reach US$1113mln and will exceed US$247mln

in 2013

30% of sales come from Europe

(in 2011 100% of sales were from US customers)

56% of sales made via mobile devices on Christmas’12

50% of members come from social networks

65% are repeat buyers

Fab is after a US$70bln market (USA only)

The site was launched on 9 June, 2011 and just 18 months later:

Best E-Commerce

Application

29

DFJ Global Network

DFJ VTB Capital Aurora is the first and only DFJ Global Network fund in Russia and CIS

The DFJ Global Network is a unique global venture capital model encompassing a network of Network Partner

funds with operations in the US, China, India, Korea, Vietnam, Russia, Europe, Israel, Brazil, and Japan

representing over $7 billion in capital commitments and 600 funded portfolio companies.

Together, DFJ and the DFJ Network are the most active investors in the world.

30

Four reasons to invest

Why Russia?

World’s 6th largest economy (by GDP in PPP terms)

The most populated country in Europe

Rapidly growing middle class

Highest quality human capital in BRIC

One of the largest European Internet communities

Strong GR support of innovation policy

Why Venture Capital?

Counter-cycle asset class

Added value created by new technologies

Russia’s strong background in science

Investment to a better future

Why VTB Capital?

One of the most experienced Russian venture

capital firms

#1 Investment bank in Russia and CIS

Member of the DFJ Global Network

Part of VTB Group, the second largest financial group in

Russia and CIS

Why Now?

Russian Internet growth potential

First big exits achieved (Yandex, Mail.ru, Qiwi) with more

to come

Developed infrastructure for nanotechnology

commercialization

Multibillion markets for nanotech products

* See Catching Russian media with RuNet’, VTB Capital Research: March 27, 2012

31

Disclaimer

This is a marketing communication. It is not a research report. This document has been prepared by VTB Capital plc and/or one of its affiliates (“VTB Capital"), for information purposes only and is solely intended for the use of the intended

recipient(s). This document may include an indicative summary of the terms and conditions of the securities/transaction described herein and may be amended, superseded or replaced without notice. The conditions of the

securities/transaction will be set out in full in the applicable binding transaction document(s).

Not an offer: This document does not constitute an underwriting commitment, an offer of financing, an offer to sell, or the solicitation of an offer to buy or sell any securities described herein, which shall be subject to VTB Capital internal

approvals.

Not advice: VTB Capital is acting solely as principal and not as advisor or fiduciary. You must independently determine, with your own professional advisors, the appropriateness of any contemplated transaction or investment. No part of this

material constitutes tax, legal, accounting, financial or investment advice and should not be construed as such.VTB Capital accepts no liability whatsoever for any consequential losses arising from the use of this document or reliance on the

information contained herein.

Accuracy: Whilst every care has been taken in preparing this material, VTB Capital does not guarantee the accuracy or completeness of information which is contained in this document and which may have been obtained from or is based

upon data from third party sources. All information contained herein is subject to change without any notice. VTB Capital assumes no duty to update any of the content.

Opinions: Information and opinions contained herein have been compiled or arrived at by VTB Capital from publicly available information and sources that VTB Capital believes to be reliable. Any views expressed represent the personal

assessment of the author(s) only and do not necessarily reflect the views of VTB Capital and/or any of its worldwide affiliates (collectively, the “VTB Group”). All opinions and estimates are given as of the date hereof and are subject to

change.

Past performance: The value of any investment may fluctuate as a result of market changes. Past performance is not indicative of future performance. The information in this document is not intended to predict actual results and no

assurances are given with respect thereto.

Risks: Certain transactions, including futures, options and other derivatives, involve significant risk, and may not be suitable for all investors. Many persons, physical and legal, may be restricted from dealing in the securities

markets. Investors should perform their own due diligence before investing. Importantly, securities and financial instruments denominated in foreign currencies and ADRs and other investments are subject to exchange rate fluctuations that

may adversely affect the value of the investment. The value of investments may fall as well as rise and investors may not get back the amount invested.

Conflicts: The VTB Group may and may seek to do business with any companies covered in this material. Thus, investors should be aware that the VTB Group may have a conflict of interest that could affect the objectivity of this material.

The VTB Group, its officers, directors, and employees may from time to time have long or short positions in, act as principal in, and buy or sell, the securities or derivatives, if any, referred to in this material, and other divisions of the VTB

Group outside of the sales and trading division may perform investment banking or other services for any companies mentioned herein.

Professional Investors only: This material is intended only for persons regarded as investment professionals as defined in Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion Order) 2001 or those that would be

classified as Eligible Counterparties or Professional Clients/Investors under the Financial Services Authority’s Conduct of Business rules (or equivalent outside of the UK) and is not intended to be distributed directly or indirectly to any other

class of person. It is not available to any retail investor. This material is intended for Institutional Investors only in connection with its distribution in the US.

THIS DOCUMENT DOES NOT DISCLOSE ALL THE RISKS AND OTHER ISSUES RELATED TO AN OR POTENTIAL INVESTMENT IN THE SECURITIES/TRANSACTION. PRIOR TO TRANSACTING, POTENTIAL INVESTORS SHOULD

ENSURE THAT THEY FULLY UNDERSTAND THE TERMS OF THE SECURITIES/TRANSACTION AND ANY RISKS ASSOCIATED THEREWITH. THIS DOCUMENT IS NOT A PROSPECTUS. INVESTORS SHOULD ONLY SUBSCRIBE

FOR ANY TRANSFERABLE SECURITIES DESCRIBED HEREIN ON THE BASIS OF INFORMATION IN THE LEGALLY BINDING TRANSACTION DOCUMENT(S) AND NOT ON THE BASIS OF ANY INFORMATION PROVIDED HEREIN.

VTB Capital plc is authorized and regulated in the United Kingdom by the Financial Services Authority, in Dubai by the Dubai Financial Services Authority, in Singapore by the Monetary Authority of Singapore and VTB Capital Hong Kong

Limited is licensed by the Securities and Futures Commission in Hong Kong. VTB Capital plc is a bank incorporated in England & Wales (registration no. 159752). VTB Capital Inc. is licensed and regulated in the United States by the

Financial Services Regulatory Authority (“FINRA”) and by the US Securities and Exchange Commission (“SEC”). VTB Capital plc and its affiliates are part of the investment business of JSC VTB Bank. This document is confidential, and no

part of it may be reproduced, distributed or transmitted without the prior written permission of VTB Capital.

Copyright VTB Capital 2012 (all rights reserved).

Alexander Pankov

Director

E-mail: [email protected]

Telephone: +7 (495) 725 55 40

Aidar Kaliev

Global Head of Venture Capital

E-mail: [email protected]

Telephone: +7 (495) 725 55 40

www.vtbcapital-im.com

Contact information