SAP AG 1999 SAP AG $&&RVW2EMHFW&RQWUROOLQJIRU6DOHV2UGHUV $& $& &RVW2EMHFW&RQWUROOLQJ IRU6DOHV2UGHUV &RVW2EMHFW&RQWUROOLQJ IRU6DOHV2UGHUV n R/3 System n Release 4.6C n December 2000 n Material Number 5004 3573

7UDGHPDUNV�n Some software products marketed by SAP AG and its distributors contain proprietary software

components of other software vendors.

n Microsoft®, WINDOWS®, NT®, EXCEL®, Word® and SQL Server® are registered trademarks ofMicrosoft Corporation.

n IBM®, DB2®, OS/2®, DB2/6000®, Parallel Sysplex®, MVS/ESA®, RS/6000®, AIX®, S/390®,AS/400®, OS/390®, and OS/400® are registered trademarks of IBM Corporation.

n ORACLE® is a registered trademark of ORACLE Corporation, California, USA.

n INFORMIX®-OnLine for SAP and Informix® Dynamic ServerTM are registered trademarks ofInformix Software Incorporated.

n UNIX®, X/Open®, OSF/1®, and Motif® are registered trademarks of The Open Group.

n HTML, DHTML, XML, XHTML are trademarks or registered trademarks of W3C®, World WideWeb Consortium, Laboratory for Computer Science NE43-358, Massachusetts Institute ofTechnology, 545 Technology Square, Cambridge, MA 02139.

n JAVA® is a registered trademark of Sun Microsystems, Inc. , 901 San Antonio Road, Palo Alto, CA94303 USA.

n JAVASCRIPT® is a registered trademark of Sun Microsystems, Inc., used under license fortechnology invented and implemented by Netscape.

n SAP, SAP Logo, mySAP.com, mySAP.com Marketplace, mySAP.com Workplace, mySAP.comBusiness Scenarios, mySAP.com Application Hosting, WebFlow, R/2, R/3, RIVA, ABAP™, SAPBusiness Workflow, SAP EarlyWatch, SAP ArchiveLink, BAPI, SAPPHIRE, Management Cockpit,SEM, are trademarks or registered trademarks of SAP AG in Germany and in several other countriesall over the world. All other products mentioned are trademarks or registered trademarks of theirrespective companies.

l <RX�DUH�LQ�WKH�&RVW�$FFRXQWLQJ�GHSDUWPHQW�RI�WKH,'(6�*URXS��,'(6��ZLWK�WKH�KHOS�RI�H[WHUQDOFRQVXOWDQWV��KDV�LPSOHPHQWHG�WKH�6$3�5���6\VWHP�LQFOXGLQJ�&RVW�2EMHFW�&RQWUROOLQJ�E\�6DOHV�2UGHU�

l ,QLWLDOO\��\RX�DUH�WHPSRUDULO\�DVVLJQHG�WR�WKH�SURMHFWWHDP�WR�UHYLHZ�WKH�FXVWRPL]DWLRQ�RI�&RVW�2EMHFW&RQWUROOLQJ�E\�6DOHV�2UGHU��<RX�ZLOO�QRW�RQO\�YHULI\WKH�FRQILJXUDWLRQ�FKRLFHV��EXW�ZLOO�DOVR�DVVLVW�WKHFRQVXOWDQWV�LQ�PDNLQJ�FKDQJHV�DQG�FRPSOHWLQJ�WKHV\VWHP�VHW�XS�

l 2QFH�WKH�V\VWHP�LV�SURGXFWLYH��\RX�ZLOO�EH�RQH�RIWKH�SULPDU\�XVHUV�RI�&RVW�2EMHFW�&RQWUROOLQJ�E\6DOHV�2UGHU�

l <RX�DUH�LQ�WKH�&RVW�$FFRXQWLQJ�GHSDUWPHQW�RI�WKH,'(6�*URXS��,'(6��ZLWK�WKH�KHOS�RI�H[WHUQDOFRQVXOWDQWV��KDV�LPSOHPHQWHG�WKH�6$3�5���6\VWHP�LQFOXGLQJ�&RVW�2EMHFW�&RQWUROOLQJ�E\�6DOHV�2UGHU�

l :H�DUH�LQ�WKH�VLWXDWLRQ�WR�DQDO\]H�ZKLFK�EXVLQHVVSURFHVVHV�LQ�RXU�SODQW�ZLOO�XWLOL]H�&RVW�2EMHFW&RQWUROOLQJ�

l :H�PXVW�DQDO\]H�ZKDW�SURGXFWLRQ�W\SHV�DUH�XVHGDQG�ZKDW�WKH�PDLQ�UHTXLUHPHQWV�LQ&RVW�2EMHFW�&RQWUROOLQJ�DUH�

l %HFDXVH�RI�WKLV��ZH�PXVW�NQRZ�ZKDW�FRQWUROOLQJPHWKRGV�DUH�VXSSRUWHG�E\�&RVW�2EMHFW�&RQWUROOLQJLQ�WKH�5���V\VWHP�

n How do we rein in our overhead costs? In many organizations, overhead costs have taken a hugeupward jump, including costs which the organization cannot assign directly to either products orservices. While production areas often display great progress in controlling costs and optimizingprocesses, overhead continues to display little cost transparency. Overviews and allocations ofoverhead costs are supported by the following three application components in Overhead CostControlling (CO-OM).

n Are our responsibility areas actually working efficiently? Cost Center Accounting (CO-OM-CCA)examines where overhead costs arise within the organization. You can assign the costs fromorganizational sub-areas to their exact causes, with a wide variety of allocation methods to choosefrom when allocating amounts and quantities. In particular, activity accounting permits allocation ofa great many of those costs which would not be normally assigned to products.

n How high are the costs of our organizational measures? Do they remain within their budgets?Overhead Orders (CO-OM-OPA) gather and control costs according to the measures taken in theorganization. You can assign budgets and arrange that their requirements are monitored by the R/3System.

n How can we optimize processes within our organization? Optimizing business processes treats notonly the goals of individual divisions, but those of the entire organization. In recent years,monitoring of functions and products has been joined by control of business processes spanningorganizational boundaries. The functional view on your organization is complemented by a cross-functional, process-oriented view. CO-ABC gives you both a powerful management tool forimproving your business process performance as well as an information base for your strategicdecision making process.

n What costs occur within our organization? Cost Element Accounting (CO-OM-CEL) indicates whichcosts and revenues have occurred and is used for reconciliation of cost controlling with the FinancialAccounting (FI) module.

n Evaluate the effectiveness of your production system.• set meaningful standards to measure performance• use variance analysis to compare• report by plant, product group, product or even order

n Strategic decisions• (primary) cost component split, cost component splits by organizational unit• scrap costs, full integration of Activity Based Costing

n Inventory valuation• alternative valuations (legal, group, profit center)• three parallel currencies• standard costs• actual costs

n Semi finished and finished goods valuation• standard prices provided by cost estimates• creation of alternative cost estimates for balance sheet purposes as closing activities

n Value Work-in-Process at the close of period end

n Provisions for losses• used in a make-to-order environment• update balance sheet and profit-and-loss statements accordingly

n Product Cost Planning refers to the creation of cost estimates for the production of goods or services.There is no reference to a production order (the cost estimate is independent of any given productionorder). If a quantity structure (bill of material and routing) is available in the PP (ProductionPlanning) module of the R/3 system, you can create a cost estimate automatically using the PP data.If no quantity structure is available in R/3, the costing items can be entered manually by means ofunit costing, or can be transferred automatically from a non-SAP system using batch input.

n In Cost Object Controlling, the costs incurred in the production of a product or service are collectedon a cost object (such as a production order). Which cost object is used depends on your controllingrequirements. It may be a sales order, a production order, a process order or a production costcollector. Cost Object Controlling is used to calculate work in process, scrap costs and variances atperiod close.

n Actual Costing is used to calculate actual product costs at period close. The result may be transferredto the material master as a weighted average price for the closed period. As of Release 4.5 thequantity structure is derived dynamically using the materials movements in the R/3 system.The values connected with these movements are collected in the Material Ledger. Single-levelsettlement functions to calculate the actual material costs at period close are available in Release4.0A. Multi-level settlement functions are available in Release 4.5.

n Product costing uses the data in Logistics to determine the material consumption (BOM) and theactivities used (routing). This data forms the quantity structure.

n Product costing valuates this quantity structure with the following information:

é prices for materials

é prices for activities

é overhead on the direct costs for these materials and activities

é overhead for sales and administration costs

é processes by evaluating the process template

n The results are saved in various forms, and are also used by other applications.

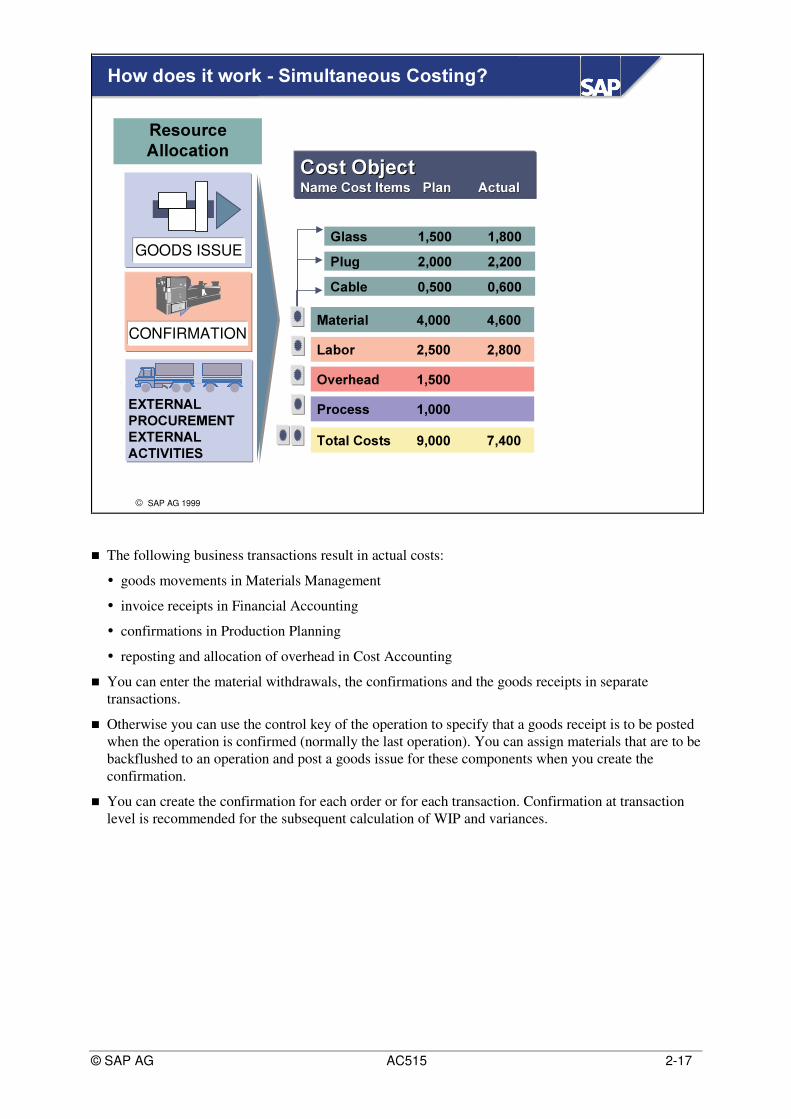

n The following business transactions result in actual costs:

é goods movements in Materials Management

é invoice receipts in Financial Accounting

é confirmations in Production Planning

é reposting and allocation of overhead in Cost Accounting

n You can enter the material withdrawals, the confirmations and the goods receipts in separatetransactions.

n Otherwise you can use the control key of the operation to specify that a goods receipt is to be postedwhen the operation is confirmed (normally the last operation). You can assign materials that are to bebackflushed to an operation and post a goods issue for these components when you create theconfirmation.

n You can create the confirmation for each order or for each transaction. Confirmation at transactionlevel is recommended for the subsequent calculation of WIP and variances.

n Template Allocation includes process costs and activities.

n Calculating work in process will calculate your WIP either at actual costs (when using fullsettlement) or at target costs (when using periodic settlement).

n Variance calculation calculates not only variances, but also target scrap and target costs as the basisfor the target/actual comparison and scrap variances.

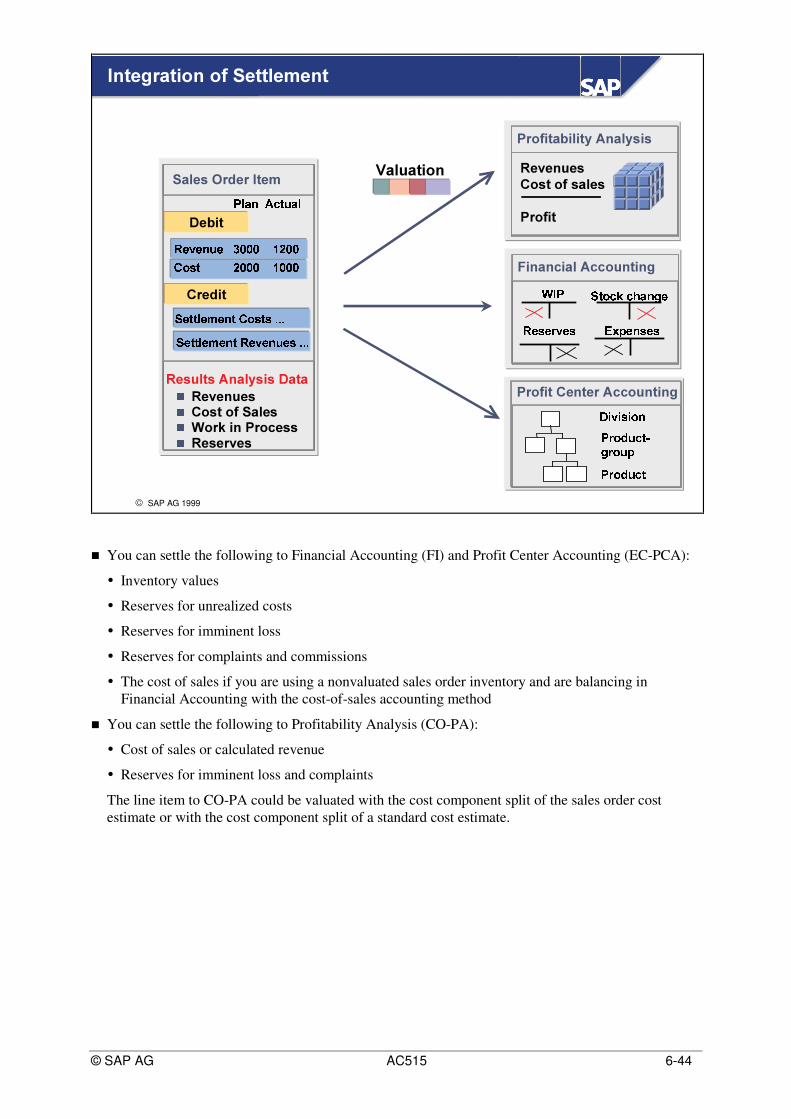

n Settlement is the last step in period-end closing in Cost Object Controlling.The necessary accountingdocuments are posted in Financial Accounting and in the Material-Ledger and data passed on toother components such as Profitability Analysis and Profit-Center Accounting.

n In this case the costs posted onto the process order via goods issues, confirmations and goodsreceipts are stored on a CO-object, which has a one-to-one relationship to the process order.

n In this example process orders have the settlement type FULL.

n As long the process order is not fully delivered or flagged technical complete the remaining orderbalance is treated as WIP. Otherwise the order balance shows up in variance calculation.

Partially Delivered Delivered or Technically Completed

��� �!�" �$# "&%'!(

�

�

35(/5(/ 3'/

9'/97(&

2

�)# "*%+!�( ��,- " - �)# "*%+!( ��,- " -

�)# "*%+!�( ��,- " -

�.�/�!�" �)# "*%+!�(

0 !�1*2 !�3 #�4 -

564 (72 8 4 1 90 !�(7% 4

5�4 (72 8 4 1:90 !(7% 4

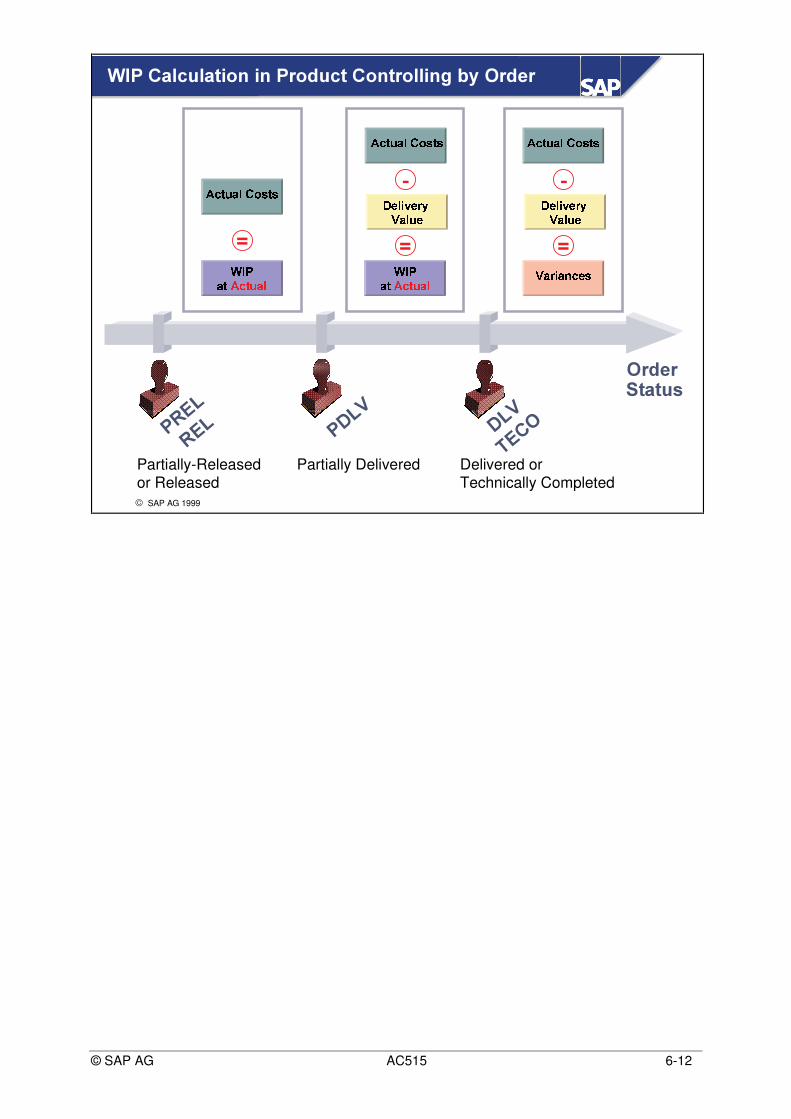

n In the Product Cost by Order component, work in process is valuated at actual costs. The work inprocess is calculated as the difference between the debit and credit of an order as long as the orderdoes not have the status DLV (delivered).

n In the Product Cost by Order component, the variances are not calculated until the order has thestatus DLV (delivered). This means that when the order has this status, the system no longerinterprets the difference between the debit and the credit as work in process but as a variance. InProduct Cost by Order, orders never have work in process and variances at the same time.

n In this case the costs posted onto the process order via goods issues, confirmations and goodsreceipts are stored on a product cost collector. A product cost collector may exist per productionversion of a product and collects all costs, which are posted to the logistic object of the accordingproduction version.

n Product Cost Collectors always have the settlement type PER.

n With period-end closing, Work in Process at Target Costs as well as Variances can be calculated onthe product cost collector.

n In Product Cost by Period the work in process is calculated at target costs. For repetitivemanufacturing you must enter reporting point backflushes for the operation, and for manufacturingorders you must enter confirmations for the operation. Confirmed quantities that are not scrap arevaluated in WIP calculation at target costs in accordance with the valuation variant for work inprocess and scrap defined in Customizing for Product Cost by Period.

n In the Product Cost by Period component, variances are calculated by period. Variance calculationcompares the confirmed actual values with the target values. The variances are determined as thedifference between the actual costs, less the delivery values, less the WIP at target values.

n Effective sales order processing ties all activity to customer demand in a series of tightly integratedprocesses. R/3 Sales and Distribution gives you precisely this kind of sales order processing using aseries of linked documents to generate a workflow for sales and distribution. Sales and Distributionbegins with pre-sales processing and ends with customer payment for goods received and servicesrendered. Sales Distribution represents each of these processes with electronic documents, eachlinked both to preceding and subsequent electronic documents.

n The Customer Order Management cycle can begin with Pre-Sales Activities. For example: Inresponse to a Request for Quotation (RFQ) from your customer, you create and send a quotation.

n As part of Sales Order Processing, you create a sales document.

n During Inventory Sourcing, R/3 determines the supplier of the inventory, based on data that youcreate and control. Is the supplier one of your plants? If so, which one? Is the supplier a third-partyvendor? If so, which one?

n As a part of Delivery, you create a delivery document.

n During Billing, you create a billing document.

n In the Customer Payment process, you receive monies and post these monies in FinancialAccounting (FI).

n In R/3, the documents defined in Sales and Distribution help you manage the Customer OrderManagement cycle for you and your customer.

n Order cycles sometimes begin with a sales query such as an inquiry or request for quotation. Salesqueries help you enter and store important, sales-related information you can use later during orderprocessing.

n Use this pre-sales information to plan sales strategies or help build a long-term relationship with thecustomer.

n Using sales queries provide data that can have great value for you later, particularly when:

é tracking lost sales

é recording pre-sales data to help negotiate large contracts

é selling to large organizations that must require documentation of the entire process

n Any one of the activities listed above can begin the sales process.

n A sales order is an electronic document that captures and records your customer’s request for goodsor services.

n The sales order contains all pertinent information to process the customer’s request throughout theCustomer Order Management cycle.

n Sales and Distribution automatically proposes appropriate existing data from relevant master recordsin order to minimize errors and redundant effort in order processing.

n You can enter a sales order with many items in a single screen, or place a complex order using anexpanded order view.

n Creating the delivery document signals the start of all shipping activities for your sales order.

n Creating a delivery document includes copying information from the sales order, such as thematerials and the quantities, onto the delivery document.

n The delivery document is the electronic means to help you manage all the activities of deliveryprocessing, including efficiently picking product, packing, planning and monitoring shipments,preparing shipping papers, and posting goods issue.

n Creating a transfer order includes copying information from the delivery document to the transferorder for processing within the warehouse.

n The transfer order is essential for controlling the movement of goods within your warehouse. Thetransfer order is based on a simple principle: where are you taking goods from and where are youtaking goods to, within your warehouse. There is a source location and a destination location forevery transfer order.

n When you post goods issue, you see the automatic update to the general ledger. R/3 affects thegeneral ledger by debiting the Cost-of-Goods Sold account and crediting the Inventory account.Inventory, both stock counts and valuation, goes down; cost-of-goods sold goes up.

n Creating a billing document includes copying information from the sales order and the deliverydocument onto the billing document.

n The billing document serves several important functions:

é The billing document is the electronic means to help you prepare invoices, which are consideredoutput of Billing.

é The billing document serves as a source to Financial Accounting (FI) to help you in themonitoring and management of customer payment.

é When you create a billing document, you see the automatic update to the general ledger. R/3affects the general ledger by debiting the customer’s Accounts Receivable account and creditingthe Revenue account.

n When you post a customer payment, you see the automatic update to the general ledger. R/3 affectsthe general ledger by debiting the Cash account and crediting the customer’s Accounts Receivableaccount.

l $�SURGXFW�DQG�VXE�DVVHPEOLHV�DUHLQGLYLGXDOO\�PDQXIDFWXUHG�IRU�D�SDUWLFXODUFXVWRPHU

l 6WRFNV�DUH�PDQDJHG�LQ�LQGLYLGXDOFXVWRPHU�VHJPHQWV���VDOHV�RUGHU�VWRFN

l 4XDQWLWLHV�SURGXFHG�IRU�D�SDUWLFXODU�VDOHVRUGHU�FDQQRW�WKHQ�EH�XVHG�WR�FRYHUDQRWKHU�VDOHV�RUGHUV�GHPDQG

l &RPSRQHQWV�FDQ�EH�SURFXUHG�VSHFLDOO\IRU�DQ�LQGLYLGXDO�VDOHV�RUGHU

n A make-to-order product is planned as a requirement for production using the sales order itemnumber. A separate segment is created in the planning run for this requirement. In the planningsegment, the requirements and stocks of the sales order item are managed separately. Thus, variouscustomer-specific variants of a product can be managed using only one material number.

n Starting from the sales order, single-item planning can be carried out for any level of the BOMstructure. Therefore, it is also possible to procure assemblies and components specifically for thesales order and manage this stock individually for the sales order. This is of particular importance ifcomponents can also be configured for the production of the individual customer product.

l :LWK�6DOHV�2UGHU&RQWUROOLQJ�SURYLGHVDGGLWLRQDO�IXQFWLRQV

�

�

6DOHV�2UGHU&RVW�(VWLPDWH

0DW� /DERU2+ 3URFHVV

n A similar handling of make-to-order production in comparison with make-to-stock production isenabled with the new R3/4.0 functionality of valuated sales order stock.

n This enables you

é to calculate production variances of related production orders

é to settle these variances to Profitability Analysis

é to provide a cost component split for Cost of Goods sold

n Moreover the sales order costing provides a basis for:

é sales and pricing decisions

é planned costs

é methods of results analysis (percentage of completion)

n Sales order costing supports different cost component views, delivers a costed BOM structure, costelement, and cost itemization information.

n Material movements are made via individual sales order stock.

n In Release 3.0/3.1 this stock is not valuated. As of Release 4.0 you can choose whether you managethis stock as unvaluated or valuated sales order stock.

Material Management0DWHULDO������3URGXFW�;6DOHV�2UGHU���������'HELWV�

&UHGLWV�

n Because the inventories assigned to sales orders and projects carry costs as well as quantities, goodsmovements for these inventories generate postings in Financial Accounting. The costs of thematerials can be determined in a cost estimate for the sales order or production order. The inventoryvalue can therefore be shown immediately in Financial Accounting - costing in the Controllingmodule is not necessary. The valuated goods movements result in debits and credits to the affectedobjects.

n The goods receipt is valuated using a predefined valuation strategy sequence.

n The first goods receipt results in valuation on the basis of one of the subsequent strategies in thespecified sequence. A standard price selected through one of the subsequent strategies is copied intostrategy and serves as the valuation basis from this point onwards.

é The system calculates the standard price on the basis of your customer exit COPCP002 Materialvaluation for valuated sales order stock.

é The system calculates the standard price in a sales order cost estimate. This sales order costestimate can be based on a unit cost estimate or on a product cost estimate.

é The system determines the standard price using the production order cost estimate or the plannedcosts for the WBS element. If there are multiple production orders for the same sales order item,the system uses the standard price that results from the production order that delivers first (seestrategy 1).

l ,Q�\RXU�SODQW�������\RX�WULJJHU�VDOHV�RUGHUUHODWHG�UHSHWLWLYH�PDQXIDFWXULQJ�XVLQJ�DVLQJOH�SURGXFWLRQ�OLQH�ZKHQ�D�VDOHV�RUGHU�LVUHFHLYHG�IRU�WKH�DXWRPRELOH�7�)$����LQRULJLQDO�,'(6�XVH�DP��JW��

l <RX�PXVW�QRZ�PDLQWDLQ�WKH�QHFHVVDU\PDVWHU�GDWD�LQ�WKH�5���V\VWHP�

l 7KHQ�\RX�KDYH�WR�FDUU\�RXW�WKH�QHFHVVDU\SRVWLQJV�LQ�WKH�5���V\VWHP�

n In repetitive manufacturing, the same product is usually produced over a longer period of time onone production line. Instead of being manufactured in restricted production lots, a total quantity ofthe product is manufactured over a specific period of time, with a specific production rate per partialperiod. Products generally go through production in a relatively steady flow. Semi-finished productsare often processed further directly, without being placed in interim storage.

n Make-to-stock repetitive manufacturing: one alternative is to use repetitive manufacturing in make-to-stock production. This means that you produce products with no direct reference to sales orders.Depending on your production strategy, you can settle planned independent requirements fromDemand Management against sales orders.The same product is produced repeatedly over a substantial period of time. Instead of beingmanufactured in restricted production lots, a total quantity of the product is manufactured over aspecific period of time, with a specific production rate per partial period. Products go throughproduction in a relatively steady flow. Sales orders are delivered from stock.

n Order-oriented repetitive manufacturing: the other alternative is to use repetitive manufacturing fororder-oriented production. Sales orders can be processed separately and planned orders are createdwith direct reference to sales orders. Production is therefore controlled via sales orders. Thequantities you produce cannot be swapped between the individual sales orders, the finished productsare stocked specifically for individual sales orders (sales order stock). Sales order stock is reducedvia goods issue for sales order.

n The system generates a planned order for the material listed in the sales order item. This plannedorder contains all the material components necessary for the manufacture of the finished product.The planned order can be created in the following ways:

é In requirement planning

é When the sales order is saved

n In order to generate the planned order generated when the sales order is saved, you must enterassembly type 1 (planned order: static processing) or 4 (planned order: dynamic processing) in therequirements class.

MotorMotor Cycles CyclesFreight vehiclesFreight vehiclesCars Cars Sport Sport cars cars Convertibles Convertibles Limousines Limousines Class Class A A Class Class B B

&2�&2�3&3&

n If you are in a sales-order-related production environment and using a valuated sales order inventorywith repetitive manufacturing, you can collect the costs for a configurable material on a product costcollector for the material.

n If you have to process a high volume of data, you can significantly improve performance byseparating the backflushing processes.

n For this purpose, the backflushing processes are split into critical and uncritical partial processes. Inthe standard system backflushing includes the following partial functions:

é Goods receipt posting

é Goods issue of the material components

é Calculation of actual costs in production activity posting

é Reduction of the production quantities

é Adjustment of the dependent requirements of the components in the reporting point backflush

é Adjustment of the capacity requirements

n By separating the backflushing processes, you can instruct the system to post the goods receipts, andreduce the production requirement quantities and capacity requirements immediately. The partialfunctions that can be carried out later (uncritical functions) are collected in a work list and processedin a background job sometime later. These uncritical functions include, for example, BOMexplosion, posting goods issues, reduction of the dependent requirements and posting the productionactivities. Before posting the goods issues the single component requirements are aggregated, so thatthe number of material documents are decreased dramatically.

n For make-to-order repetitive manufacturing, you must maintain the following logistics master data:material master, bill of materials, production line and routing. As of Release 4.0, you must alsocreate a product cost collector. If you are prepared not to use capacity planning and to carry outsimplified cost accounting (for example, not posting production activities for materials with a highmaterial cost share), it is not absolutely necessary to maintain a routing for repetitive manufacturing.

n You should not use materials of standard material type KMAT. Instead, you should use a materialthat is not material type KMAT and for which you select the ‘Material is configurable' indicator inthe Basic data view.

n In the material master (MRP view), the indicator Repetitive manufacturing authorizes the materialfor repetitive manufacturing. This enables the use of various repetitive manufacturing functions (forexample, using various backflushing transactions).In the views Costing and Financial accounting , you define the price of the material and the pricecontrol to be used (standard price, moving average price) to valuate the material in backflushing.

n The repetitive manufacturing profile contains control parameters for repetitive manufacturing. Youdefine the repetitive manufacturing profile in Customizing for Repetitive Manufacturing and assignit to a material in the material master record. Various standard profiles for typical procedures areshipped with the standard system. They define, for example:

é whether, in backflushing, the system posts goods issues for the components simultaneously withgoods receipt of the assembly, or only posts a goods receipt (field GR and GI). If you set thesystem to only post goods receipts, the goods issue for the components must be posted later in aseparate transaction.

é whether, in backflushing, the system posts production activities simultaneously with goods receiptof the assembly, or only posts a goods receipt (field Activities). If you set the system to only postgoods receipts, the production activities must be posted later in a separate transaction (if you wantto post production activities).

é whether, when the backflushing processes are separated at final backflush, the system does notpost the goods issues for the components and/or the production activities in a separate transaction,but automatically as a background job at a later point in time (field Process control).

é which movement types are to be used for the goods movements.

n The BOM defines planned material consumption for the components.

n In the status/long text of the BOM item (field production storage location), you can define whichissue storage location is used to backflush the components in the repetitive manufacturing backflush.

n Simple production lines, often consisting of one work center, are created in the R/3 system as workcenters with work center category 0007 (WkCtr on prod. line).Other work center categories can also be used in repetitive manufacturing. The work center categoryWkCtr on prod. line is simply there to separate repetitive manufacturing work centers from otherwork centers, for organizational purposes.

n The work center defines the available capacity (standard or shift sequence). Various capacitycategories can be stored.

n The formulas the system uses to calculate capacity requirements are defined in the work center.

n You make the assignment to a cost center for valuation of internal activities in the work center.

n It makes sense to use the standard value key SAP3 (Production line planning) in the work center. Forthis standard value key, you can set the production time to must be entered and the setup andteardown times to should not be entered (for the times in the routing).

n The routing is often used in repetitive manufacturing simply as a basis for scheduling/capacityrequirements determination, since it defines the production rate (quantity per time unit). Rateroutings therefore often have only one operation and do not describe the operations which areactually to be carried out.The operations which are actually to be carried out by personnel are often described in externallycreated work center instructions. These are for the information of work center personnel and are keptdirectly at the production line.You could, however, use a printout of the routing as an alternative to work center instructions.

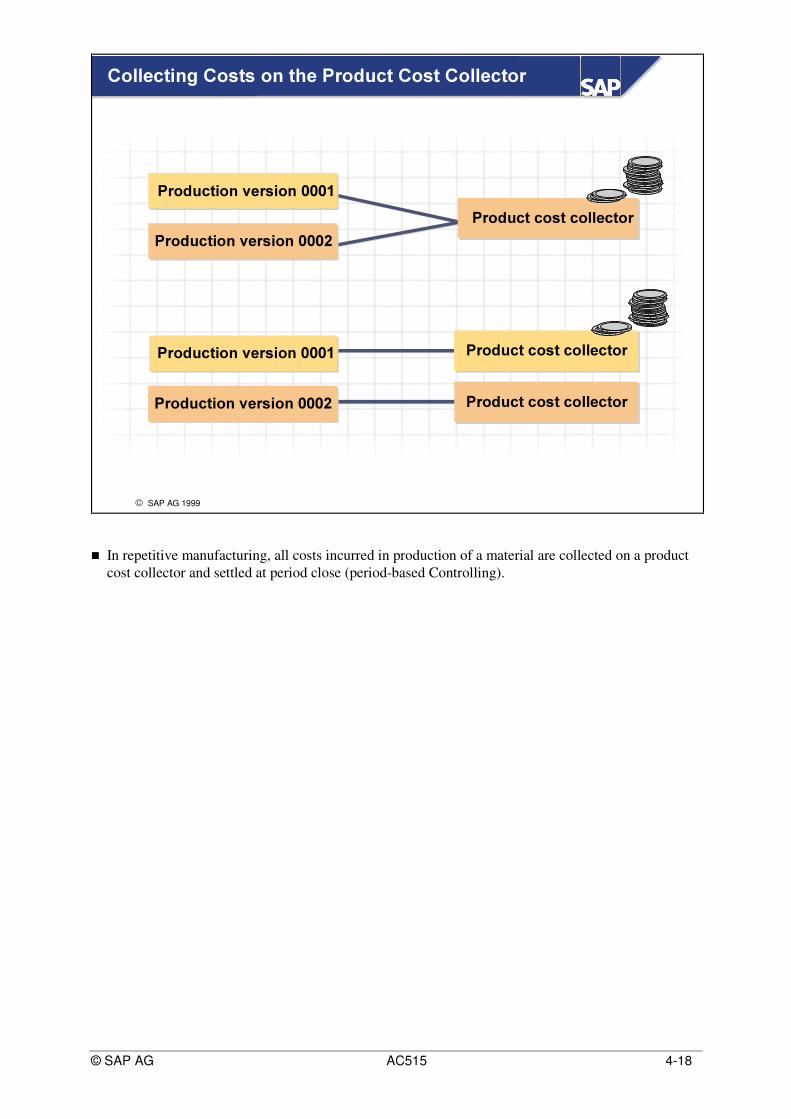

n In repetitive manufacturing, all costs incurred in production of a material are collected on a productcost collector and settled at period close (period-based Controlling).

n With the creation of the sales order a product cost estimate could be created automatically to cost theorder specific quantity structure. This cost estimate assigns the planned costs for material, labor andso on to the cost components.

n The system generates a planned order for the material listed in the sales order item. This plannedorder contains all material components necessary for manufacture of the finished product. Theplanned order can be created in the following ways:

é In requirement planning

é When the sales order is saved (assembly processing)

n Once you have manufactured the material, you enter a goods receipt for the planned order. To dothis, access the menu of Repetitive Manufacturing and enter a goods receipt for the sales order.

n The sales order stock is valuated on the basis of the sales order cost estimate.

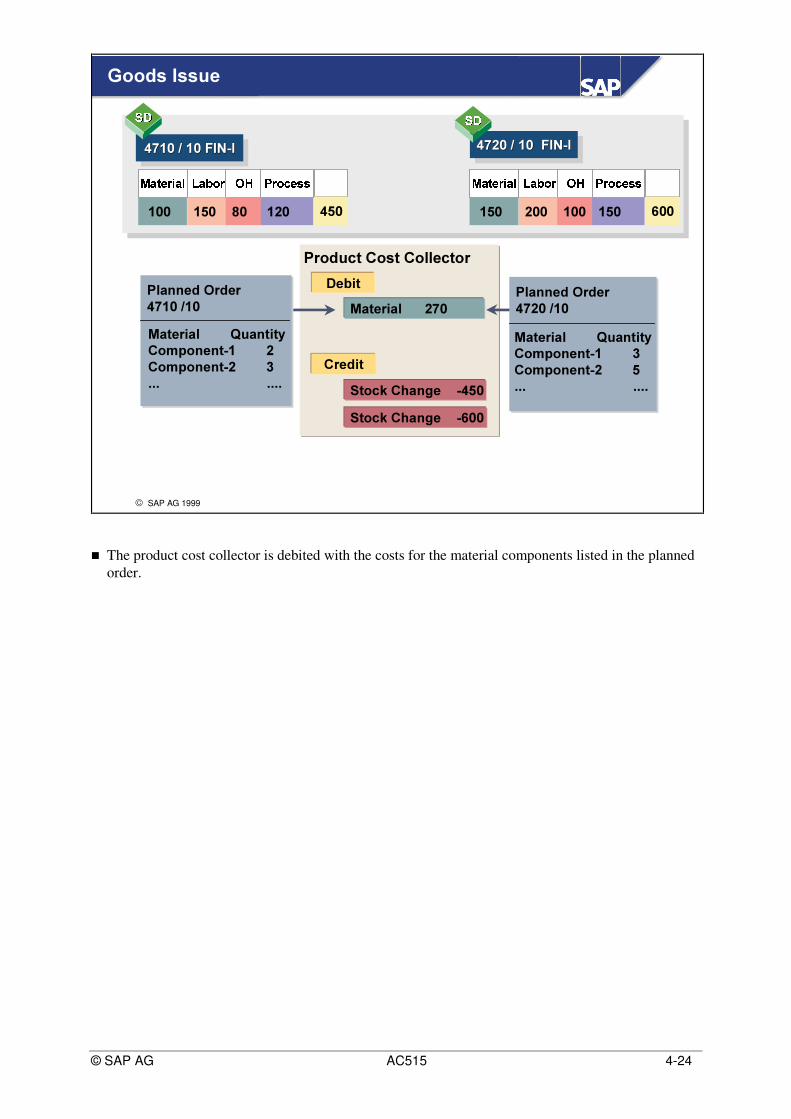

n Automatic posting of the product cost collector with the activities used only takes place if you havecreated a standard cost estimate for the configurable material. If you have created a standard costestimate for the configurable material and if you have specified in the repetitive manufacturingprofile that activities should be posted, then when the goods receipt is posted in the menu ofrepetitive manufacturing the product cost collector is debited with the activities according to thestandard cost estimate. The debit with direct material costs is still made in accordance with thematerial components listed in the planned order.

n If you have not created a standard cost estimate for the configurable material but you still want todebit the product cost collector for the activities used, carry out an internal activity allocation in theProduct Cost by Period menu.

n At billing, the R/3 System will debit the customer’s Accounts Receivable account and credit theRevenue account.

n Please note: In your implementation of the R/3 System, there may be automatic update to otheraccounting components, if implemented. For example: Controlling (CO), Profitability Analysis(CO-PA), and Legal Consolidation (FI-LC). In your implementation of the R/3 System, there maybe additional updates to the general ledger if you implement Warehouse Management or if youaccept multiple methods of payment, in addition to Credit Management.

n You can summarize the data according to the derived characteristics and then drill down interactivelyin reporting. At each level of the report, you can display the drilldown list (overview) or detailedinformation (margin analysis).

n In a CO-PA contribution margin report value fields containing process costs can now be included fora more realistic profitability analysis on product families, customers, distribution channels etc. TheCO-PA reporting functionality allows a ‘Turn and Twist' through all the dimensions of CO-PA toeven drill down to the profitability of single products.

n It depends on your business scenario if a variance calculation is usefull for the analysis of productioncosts.

n To settle the price differences to CO-PA, you can

é process variance calculation and settle the variance categories. In case that you do not want toanalyse the variance categories, use only variance category “remaining variances”.

é Define the price difference account as a cost element and enter a default account assignment toprofitability segment.

n Settlement dynamically distributes the variance to the different individual requirements stocksegments according to the delivery values of the delivered quantities. Dynamic distribution toindividual stock segments and to stock segments of make-to-stock materials is also possible.

Õ The header contains customer-relateddata for the entire order, such as currencyand term of payment

Õ Item contain data about the material andquantities ordered

Õ Schedule lines inform you as to when andin what quantity the individual items will bedelivered

n A sales document can contain as many items as you require. Items contain information such as:

é Conditions

é Texts

é Partner

n Each item may contain several schedule lines. The requested delivery date appears in the firstschedule line. If the order quantity cannot be confirmed for the requested delivery date, the R/3System proposes delivery dates and confirmed quantities in the following lines. Schedule linescontain the following information:

n You can select the requirements type through the MRP group or the strategy group in the MRP 1view in the material master record.

n Strategy for Determining the Requirements Type:

• First, an attempt is made to find a requirements type using the strategy group in the materialmaster.

• If the strategy group has not been maintained, the system will determine it using the MRPgroup.

• If the MRP group has not been defined, the system uses the material type instead of the MRPgroupwhen accessing the corresponding control tables.

• If no requirements type is found here, the system assumes a special rule and attempts to find arequirements type with the aid of the item category and the MRP type.

• If this is not possible, a last attempt is made to find a requirements type with the item categoryonly.

• If the last attempt fails, the system declares the transaction as not relevant for the availabilitycheck or transfer of requirements.

MRP Group Item UsageItem Category Group Document Type

n Another possibility is to select the requirement type through the item category group (sales viewmaterial master record) and the order type of the SD document (inquiry, quotation, sales order)

n You can select an alternative search strategy in the customizing step ‘Check Control ofRequirements Type Determination'. If the field ‘Source' field contains the value 1 or 2 therequirement type is selected through the item category group and order type.

Account Assignement Sales Order Stock Product Cost byCategory Sales Order

E Yes Yes M Yes No B No Yes

n To enable goods movements to take place through the sales order stock, you must select arequirements class that specifies an account assignment category that specifies that goodsmovements take place through the sales order stock ( Special stock field). Goods movements takeplace through the sales order stock if the entry in the Special stock field is "E" (order stock).

n To be able to collect costs on a sales order item, you must select a requirements class that specifiesan account assignment category that allows costs and revenues to be collected on a sales order item(Consumption posting field). Collecting costs and revenues on the sales order item is allowed whenthe entry in the Consumption posting field is "E" (settlement through sales order).

n Collecting costs and revenues on the sales order item is recommended in complex make-to-orderproduction. In the standard system, the account assignment category is "E" (individual customerrequirements with controlling by sales order).

n You make no entry in the Consumption posting field if you are using a valuated sales order stock anddo not want to flag the sales order item (item in an inquiry, quotation, or sales order) as carryingcosts and revenues. This is especially recommended in mass production on the basis of sales orders.In the standard system, the account assignment category is "M" (individual customer requirementswithout controlling by sales order).

n You can also carry materials from make-to-stock production in a sales order item that carries costsand revenues. This is recommended for replacement parts that are delivered for a material of thesales order stock and are withdrawn from the non-customer inventory. Here you enter "E" in theconsumption posting field (settlement through sales order). In the standard system the accountassignment category is "B".

- SPACE: No stock valuation- M: Separate valuation with ref. to sales document/project- A: Valuation without reference to sales document

n The special stock indicator in the sales order item determines how the sales order stock for that SDdocument item is to be valuated. For dependent requirements that are controlled by individualrequirements, the valuation approach is taken from the SD document item assigned to thecomponent.

Already existing Price inSales Order Stock Segment

Already existing Price inSales Order Stock Segment

Customer ExitCustomer Exit

Sales Order CostingSales Order Costing

Production OrderPlanned Costs

Production OrderPlanned Costs

Standard Price(Standard Cost Estimate)

Standard Price(Standard Cost Estimate)

l 9DOXDWLRQ�6WUDWHJ\l *RRGV�,VVXHV�'HELW

RUGHUV FRVW�FROOHFWRUV VDOHV�RUGHU�LWHP

l *RRGV�5HFHLSW�&UHGLWV RUGHUV FRVW�FROOHFWRUV

n The goods receipt is valuated using a predefined valuation strategy sequence.

é The first goods receipt results in valuation on the basis of one of the subsequent strategies in thespecified sequence. A standard price selected through one of the subsequent strategies is copiedinto strategy and serves as the valuation basis from this point onwards.

é The system calculates the standard price on the basis of your customer exit COPCP002 Materialvaluation for valuated sales order stock.

é The system calculates the standard price in a sales order cost estimate. This sales order costestimate can be based on a unit cost estimate or on a product cost estimate or a mixture of the two.

é The system determines the standard price using the production order cost estimate or the plannedcosts for the WBS element. If there are multiple production orders for the same sales order item,the system uses the standard price that results from the production order that delivers first (seestrategy 1).

é If you created the same material as a collective requirements material, the system reads thematerial master record of the collective requirements material. The standard price in the masterrecord of the collective requirements material may have been calculated in different ways, such asin a standard cost estimate.

At the conclusion of this exercise, you will be able to:

• Understand the quantity and value in make-to-order without salesorder controlling using repetitive manufacturing.

• Maintain the master data required for make-to-order repetitivemanufacturing.

• Check the control data of the sales order item.

• Create a planned order to fulfill the sales orders requirement.

• Carry out back-flushing in sales order-oriented repetitivemanufacturing.

• Create a delivery and invoice for a sales order.

• Analyze the relevant accounting and controlling documents for themake-to-order process.

In your plant 1000, the finished product T-FA## can be produced onproduction line T-LA##. The master data has already been maintained butis to be verified. You create a sales order, check the control data of thesales order and back-flush the quantity produced in the R/3 system. At theend of this exercise you create a delivery to the customer and an invoicefor the delivery.

1-1 The master data for the production of assembly 7�)$�� has already been prepared.In the following exercise, you will check that the entries for the repetitivemanufacturing process are correct.

1-1-1 Is the material authorized for repetitive manufacturing? (use MRP4 view inthe material master record)

1-1-2 According to the repetitive manufacturing profile, are production activitiesautomatically posted to the product cost collector at final back-flush for thismaterial?

Menu path:7RROV��$FFHOHUDWHG6$3��&XVWRPL]LQJ�Š3URMHFW�0DQDJHPHQW

1-1-3 Does a product cost collector exist for material T-FA##?

Menu path:$FFRXQWLQJ�Å�&RQWUROOLQJ�Å�3URGXFW�&RVW�&RQWUROOLQJ�Å &RVW�REMHFW�FRQWUROOLQJ�Å�3URGXFW�&RVW�E\�3HULRG�Å�0DVWHU�'DWD�Å3URGXFW�&RVW�&ROOHFWRU�Å�(GLW

Now enter the following data:Material: 7�)$��Plant: ����Choose (QWHU

1-2 Start by creating a sales order for the finished product T-FA##.

1-2-1 Create a sales order for one piece:

Menu path:/RJLVWLFV�Å�6DOHV�DQG�'LVWULEXWLRQ�Å�6DOHV�Å2UGHU�Å�&UHDWH

Order type:� 25���6WDQGDUG�2UGHU�Sales organization: ����Distribution channel: ��Division: ��Choose (QWHU.

Now enter the following data:Sold-to party: ����PO number: ����Req.deliv. date: LQ����GD\VMaterial: 7�)$��Order quantity: � pieceChoose (QWHU�

1-3 Now create planned orders for the sales orders.

1-3-1 To do this, execute an MRP run for the finished product T-FA## in plant1000:

Menu path:/RJLVWLFV�Å�3URGXFWLRQ�Å�053�Å3ODQQLQJ�Å�6LQJOH�,WHP��0XOWL�/HYHO

Material: 7�)$��Plant: ����Confirm by choosing (QWHU�WZLFH.

1-3-2 Check the planning results in the MRP list for the material:

Menu path:/RJLVWLFV�Å�3URGXFWLRQ�Å�053�Å(YDOXDWLRQV�Å�053�OLVW

Material: 7�)$��Plant: ����Confirm with (QWHU.

1-4 You have produced 1 finished product T-FA##. for your sales order.

1-4-1 Carry out the final back-flush in Repetitive Manufacturing:

Menu path:/RJLVWLFV�Å�3URGXFWLRQ�Å�5HSHWLWLYH�PDQXIDFWXULQJ�Å %DFNIOXVK�Å5(0�EDFNIOXVK

Select the tabstrip 0DNH�WR�RUGHU.Now enter the following data:

Backflush qty: 1

Sales order: \RXU�VDOHV�RUGHU�QXPEHUSales order item: ������Plant: ����To location: ����

Confirm with (QWHU and VDYH the final back-flush.

In the subsequent dialog box for serial number processing, select &UHDWHVHULDO�QR��DXWRPDWLFDOO\ and leave the dialog box with the pushbutton&RQWLQXH�(QWHU.

1-5-2 Display the goods issue document and determine if any financial accountingor cost accounting documents were created for the goods issue

Form delivery processing: 2XWERXQG�GHOLYHU\��Å�'LVSOD\��enter thedelivery document, press (QWHU, select item 10, then (QYLURQPHQW�Å'RFXPHQW�IORZ��Choose the *'�JRRGV�LVVXHV��then, (QYLURQPHQW�Å'LVSOD\�GRFXPHQW� Select $FFRXQWLQJ�GRFXPHQWV�

1-6 Create an invoice for delivery. Display the billing document that was created, Displaythe financial accounting document and the cost accounting document.

Menu path:/RJLVWLFV�Å�6DOHV�DQG�'LVWULEXWLRQ�Å�6DOHV�Å�2UGHU�Å�6XEVHTXHQW�IXQFWLRQV�Å%LOOLQJ�GRFXPHQW

Save the billing document.

To display the invoice: %LOOLQJ�GRFXPHQW��'LVSOD\��Enter the billing documentnumber, then enter. To view the accounting documents, press button $FFRXQWLQJ�toanalyze the FI- and CO- Documents.

1-1 The master data for the production of assembly 7�)$�� has already been prepared.In the following exercise, you will check that the entries for the repetitivemanufacturing process are correct.

1-1-1 Is the material authorized for repetitive manufacturing?

1-1-2 According to the repetitive manufacturing profile, are production activitiesautomatically posted to the product cost collector at final back-flush for thismaterial?

Menu path:7RROV��$FFHOHUDWHG6$3��&XVWRPL]LQJ�Š3URMHFW�0DQDJHPHQW

1-1-3 Does a product cost collector exist for material T-FA##?

Menu path:$FFRXQWLQJ�Å�&RQWUROOLQJ�Å�3URGXFW�&RVW�&RQWUROOLQJ�Å &RVW�REMHFW�FRQWUROOLQJ�Å�3URGXFW�&RVW�E\�3HULRG�Å�0DVWHU�'DWD�Å3URGXFW�&RVW�&ROOHFWRU�Å�(GLW

Now enter the following data:Material: 7�)$��Plant: ����Choose (QWHU

1-2 Start by creating a sales order for the finished product T-FA##.

1-2-1 Create a sales order for one piece:

Menu path:/RJLVWLFV�Å�6DOHV�DQG�'LVWULEXWLRQ�Å�6DOHV�Å2UGHU�Å�&UHDWH

Order type: 25���6WDQGDUG�2UGHU�Sales organization: ����Distribution channel: ��Division: ��Choose (QWHU.

Now enter the following data:Sold-to party: ����PO number: ����Req.deliv. date: LQ����GD\VMaterial: 7�)$��Order quantity: � pieceChoose (QWHU.In the following characteristic valuation, valuate the material characteristics asfollows:

In the subsequent dialog box for serial number processing, select &UHDWHVHULDO�QR��DXWRPDWLFDOO\ and leave the dialog box with the pushbutton ([LWZLQGRZ�(QWHU.

1-5 The car ordered is now available for delivery.

1-5-1 Create a sales delivery for the car.

Menu path:/RJLVWLFV�Å�6DOHV�DQG�'LVWULEXWLRQ�Å�6DOHV�Å�2UGHU��Å6XEVHTXHQWIXQFWLRQV�Å�2XWERXQG�'HOLYHU\

Enter the following data:Shipping Point: ����Delivery Date: WRGD\¶V�GDWH�SOXV����GD\VSales Order: QXPEHU�RI�\RXU�VDOHV�RUGHUChoose Button� (QWHU

You need to specify the serial number for your car.Menu path:([WUDV��6HULDO�QXPEHUV

Now enter the following data:Serial Number: \RXU�VHULDO�QXPEHU�IURP�WKH�EDFNIOXVK�*5�

Leave the dialog box with the pushbutton�&RQWLQXH�(QWHU.�

Proceed with the steps for picking.

Select tabstrip 3LFNLQJ.

Enter the following data:Storage Location: ����Pick quantity: �

Post the goods issue with the pushbutton 3RVW�*RRGV�,VVXH.

1-5-2 Display the goods issue document and determine if any financial accountingor cost accounting documents were created for the goods issue

Form delivery processing: 2XWERXQG�GHOLYHU\��Å�'LVSOD\��enter thedelivery document, press (QWHU, select item 10, then (QYLURQPHQW�Å'RFXPHQW�IORZ��Choose the *'�JRRGV�LVVXHV��then, (QYLURQPHQW�Å'LVSOD\�GRFXPHQW� Select $FFRXQWLQJ�GRFXPHQWV�

1-6 Create an invoice for delivery. Display the billing document that was created, displaythe financial accounting document and the cost accounting document.

Menu path:/RJLVWLFV�Å�6DOHV�DQG�'LVWULEXWLRQ�Å�6DOHV�Å�2UGHU�Å�6XEVHTXHQW�IXQFWLRQV�Å%LOOLQJ�GRFXPHQW

Save the billing document.

To display the invoice: %LOOLQJ�GRFXPHQW��'LVSOD\��Enter the billing documentnumber, then enter. To view the accounting documents, press button $FFRXQWLQJ�toanalyze the FI- and CO- Documents.

l 6LQFH�\RX�KDYH�PDQDJHPHQW�UHVSRQVLELOLW\�IRU�WKLVDSSOLFDWLRQ��\RX�QHHG�WR�XQGHUVWDQG�WKH�IORZ�RI�FRVWVRQWR�VDOHV�RUGHUV�DQG�SURGXFWLRQ�RUGHUV��ZKLFK�DUHDVVLJQHG�WR�WKH�VDOHV�RUGHUV�

l 6LQFH�WKH�HQWHUSULVH�XVHV�DOO�RI�WKH�6$3�LQWHJUDWHGDSSOLFDWLRQ�FRPSRQHQWV��\RX�ZLOO�H[DPLQH�KRZEXVLQHVV�HYHQWV�UHFRUGHG�LQ�RWKHU�DSSOLFDWLRQV�DIIHFW\RXU�VDOHV�RUGHU�

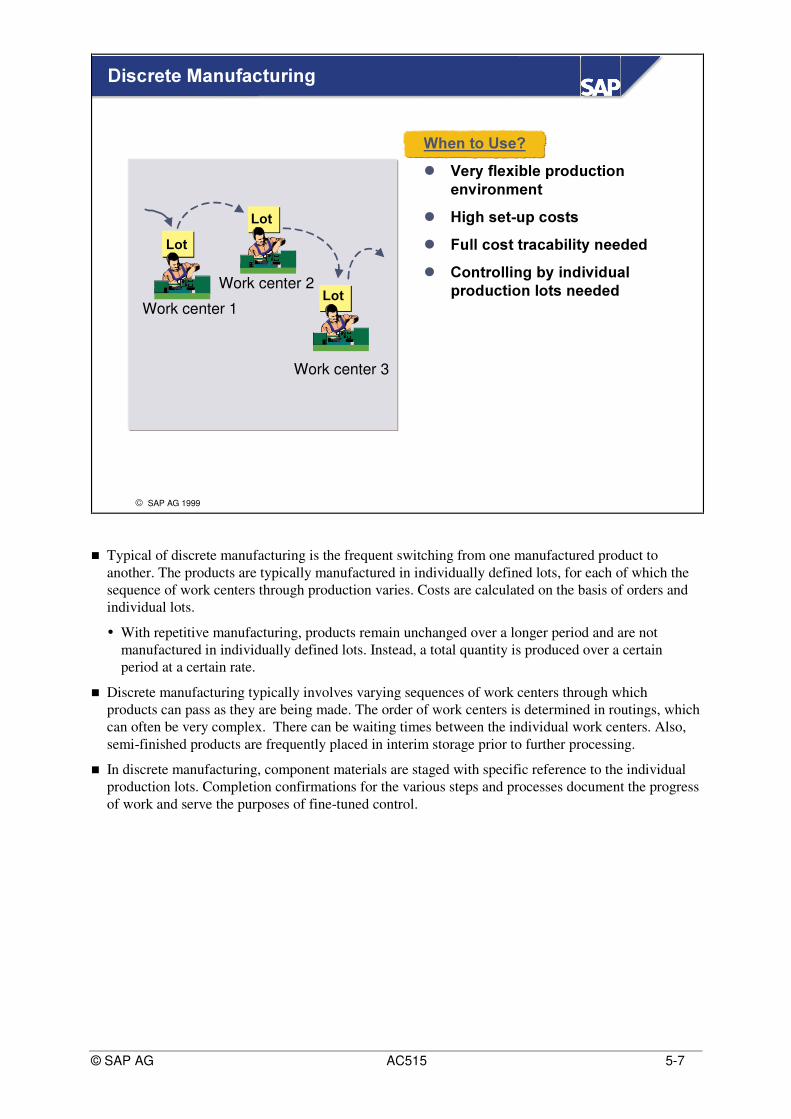

n Typical of discrete manufacturing is the frequent switching from one manufactured product toanother. The products are typically manufactured in individually defined lots, for each of which thesequence of work centers through production varies. Costs are calculated on the basis of orders andindividual lots.

é With repetitive manufacturing, products remain unchanged over a longer period and are notmanufactured in individually defined lots. Instead, a total quantity is produced over a certainperiod at a certain rate.

n Discrete manufacturing typically involves varying sequences of work centers through whichproducts can pass as they are being made. The order of work centers is determined in routings, whichcan often be very complex. There can be waiting times between the individual work centers. Also,semi-finished products are frequently placed in interim storage prior to further processing.

n In discrete manufacturing, component materials are staged with specific reference to the individualproduction lots. Completion confirmations for the various steps and processes document the progressof work and serve the purposes of fine-tuned control.

MotorMotor Cycles CyclesFreight vehiclesFreight vehiclesCars Cars Sport Sport cars cars Convertibles Convertibles Limousines Limousines Class Class A A Class Class B B

n The slide shows the relationship between Controlling by Sales Order, Controlling by Order andControlling by Period.

n Complex make-to-order production could involve order-specific changes or complete redesigns ofproducts. The costs and revenues of such products must be planned and monitored in detail.

n Different methods are available for complex make-to-order production:

é Tracking costs directly on the sales order item (make-to-order)

é Using projects for complex production, such as in plant engineering (engineer-to-order)

n The inventories assigned to sales orders or projects are valuated in both cases. Because theseinventories are valuated, the actual costs on the sales order or work breakdown structure element donot result from the goods receipt for a purchase order or production order as with nonvaluatedinventories, but instead are incurred at withdrawal or delivery of the sales order inventory or projectinventory. The funds tied up in the inventories are reported in the Controlling Information System.

n You can plan the costs of manufacturing the material in a product cost estimate or a unit costestimate. You could specify the Costing method in the customizing. If you do not specify the costingmethod in customizing, then you choose the method when you call up costing.

n When product cost estimates are post processed with unit costing, the system does not save a costcomponent split. If the standard price is based on a post processed cost estimate, the system cannottransfer a cost component split to CO-PA.

W@X Y Z�[]\�^`_ Z ^ abX�Y c1Z [0d egf@W$h f3Wihkj�Y Y X�^6DOHV�2UGHU6DOHV�2UGHU 0DW� /DERU2+ 3URFHVV

3URGXFW

5DZ��2YHUKHDG

6HPL��5DZ��

6HPL���

�

n The sales order costing contains the detail of the cost estimate. All that is shown on the sales ordercost object is the cost of good sold (COGS), not the detail (itemization). With the sales order as acost object, the only actuals that post to the sales order are for the sales order delivery and invoice.The entire Cost of goods manufactured will be reported under one cost element, it will not displaythe itemization.

n Before the sales order BOM is completed, you can cost the sub-assemblies. This cost can be used tovalue the stock for these sub-assemblies.

n With the following menu path you can create a cost estimate for a sub-assembly:$FFRXQWLQJ��&RQWUROOLQJ��&RVW�2EMHFW�&RQWUROOLQJ��3URGXFW�&RVW�E\�6DOHV�2UGHU��0DVWHU'DWD�3ODQQLQJ��&UHDWH

n You can only use this function with valuated sales order stock.

l�m�n+prqsmwtuv�x�y�{�| x v�~��o���6'�2UGHU���������0DWHULDO�;�����SF

n You can transfer the planned costs, which are already calculated for the sub-assemblies, into thesales order cost estimate for the finished good. This improves performance significantly.

n Indicator determining whether the following requirements are allowed for the dependentrequirements of the material:

é Individual requirementsRequirement quantities of the dependent material are stated individually.

é Collective requirementsRequirement quantities of the dependent material are grouped together.

n The collective/individual requirement indicator applies to all lower level BOM components

n For each component with individual requirements, a separate order is created with lot-for-lot orderquantity (that is, orders created for different sales orders cannot be grouped together)

n You can maintain this indicator in the following places:

é In the material master record

é For the explosion type of the BOM item (in Customizing for Basic Data in the IMG activityDefine explosion types)

n The setting for the explosion type overrides that in the material master record.

n The definition of the condition type per requirement class allows you to determine differentcondition types for the different items of a sales and distribution. For example, you could carry outpricing for one item on the basis of a sales order pricing procedure, while the value of the sales orderpricing might only be forwarded statistically for another item in the same document. The sales ordercosting refers to the to the sales order item.

n If you do not store a condition type in the requirements class, then the condition type is determinedvia the sales document type. In this case, the condition type is valid for all sales document items ofthe sales document.

n In the standard version of the SD system, two condition types are provided for the cost transfer ofline items:

é EK01If you choose this condition type, the result of the sales order costing is first printed to the pricingscreen for the item. The value can be used as the basis for price computation.

é EK02If you choose this condition type, the result of the sales order costing is simply a statistical value,which you can compare with the price.

n If you are using assembly type 2 ("production order, network or service (stat. processing)” beforeRelease 4.5 the system copies the planned costs, which are calculated using the preliminary costestimate for the production order, to the SD conditions. You are unable to create a sales order costingfor the sales document item.

n Now you have the choice if the system copies the planned costs, which are calculated using thepreliminary cost estimate for the production order, to the SD conditions, or if the planned costs of asales order costing for the sales document item are transferred to the SD conditions.

n You control this feature in the requirement class.

n MRP (Material Requirement Planning) creates 2 production orders and 1 purchase order. Thisexample is only using the planned costs of the production order. There is no sales order estimate.The goods receipt for the raw material will be treated as valuated sales order stock, also. With multi-level structures, it would be recommended to cost the item on the sales order. Any components usingindividual requirements will also be valuated sales order stock.

n The goods receipt creates a debit to the valuated sales order stock. If price differences occur after theissue of the material (during invoice receipt), and if the price difference account is a cost element,then it could use the account assignment of the sale order item to post the price difference. This is thereason for the valuated sales order stock valuation class (Accounting View 1 of the material masterrecord).

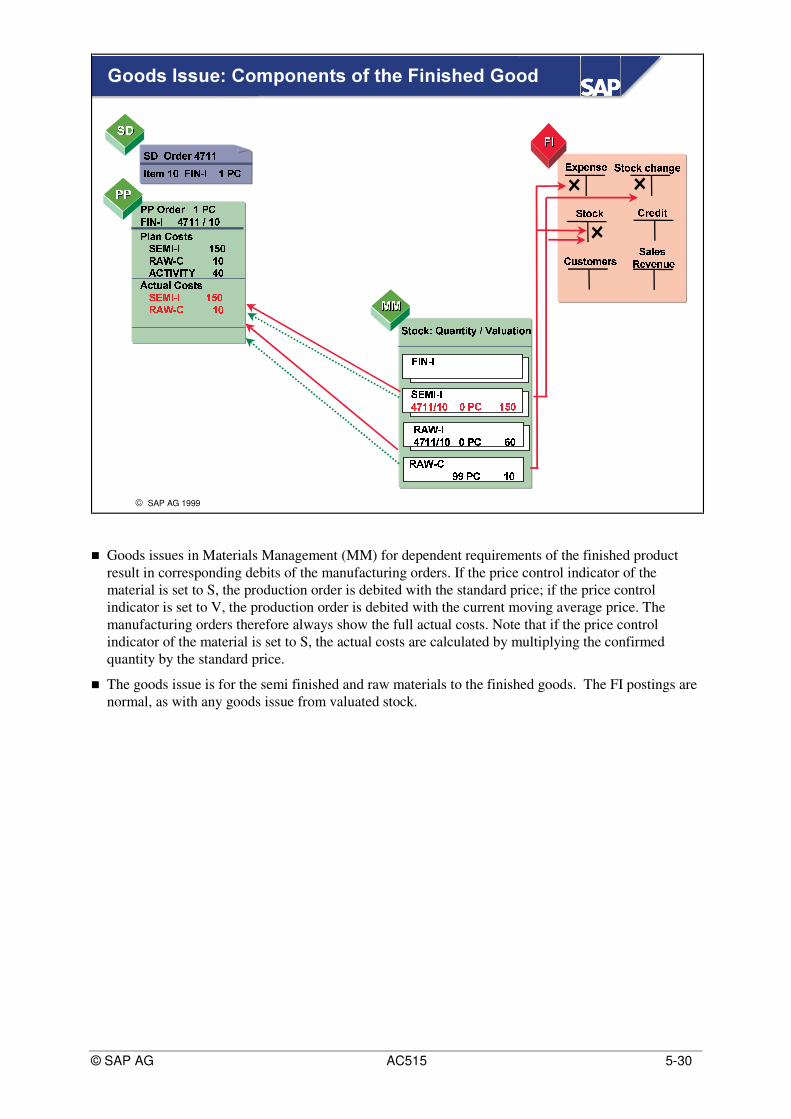

n Goods issues in Materials Management (MM) for dependent requirements of the finished productresult in corresponding debits of the manufacturing orders. If the price control indicator of thematerial is set to S, the production order is debited with the standard price; if the price controlindicator is set to V, the production order is debited with the current moving average price. Themanufacturing orders therefore always show the full actual costs. Note that if the price controlindicator of the material is set to S, the actual costs are calculated by multiplying the confirmedquantity by the standard price.

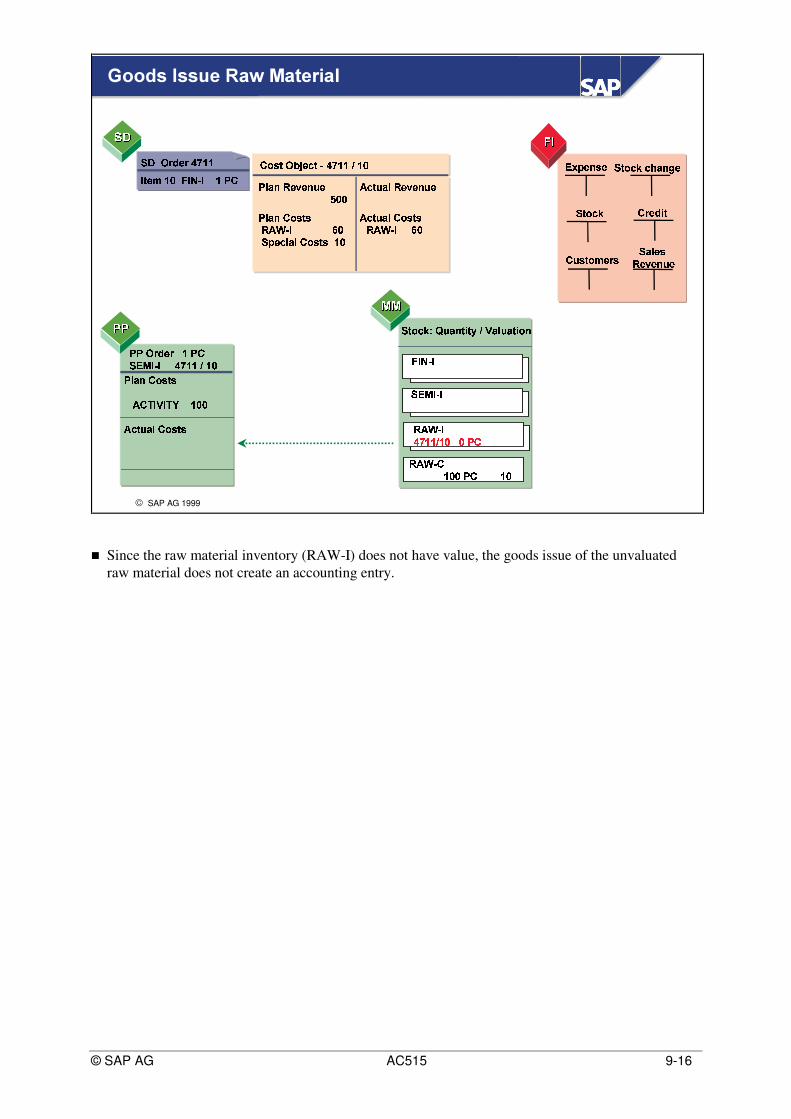

n The goods issue is for the semi finished and raw materials to the finished goods. The FI postings arenormal, as with any goods issue from valuated stock.

?Q��8����µ7wÝ`�;���1�!º�:!M�MbÁ1M�>� C E!� ¶ �NJ �!�1�%� TQ�%���%E�C ¶ ��J����!���

=%>�>� C E!��?@��8;��8 TQ�����%E1CI?3�!8%��8P�³�´���³ H >;> P!³ ´���³ H >�>��R%� �;� E!CI?@��8���8ÞMI>

������

���Ú����!��� º�:�M%M³ �4��DÛMI>ÜP!³ ´3�4³¼M � ?

n The sales order item is debited at the time of the goods issue for delivery to the customer. The cost ofsales is transferred to Financial Accounting with the goods issue posting.

?Q��8����µ7wÝ`�;���1�!º�:!M�MbÁ1M�>� C E!� ¶ �NJ �!�1�%� TQ�%���%E�C ¶ ��J����!���

=;>%>� C E!��?@��8;��8 TQ�����%E1CI?3�!8%��8P�³�´���³ H >;> P!³ ´���³ H >;>��R%� �;� E!CI?@��8���8ßMI>

¸2³ � H >;>

:RUN�LQ�3URFHVV*RRGV�LQ�7UDQVLW

������

���Ú����!��� º�:�M%M³ �4��DÛMI>ÜP!³ ´3�4³¼M � ?

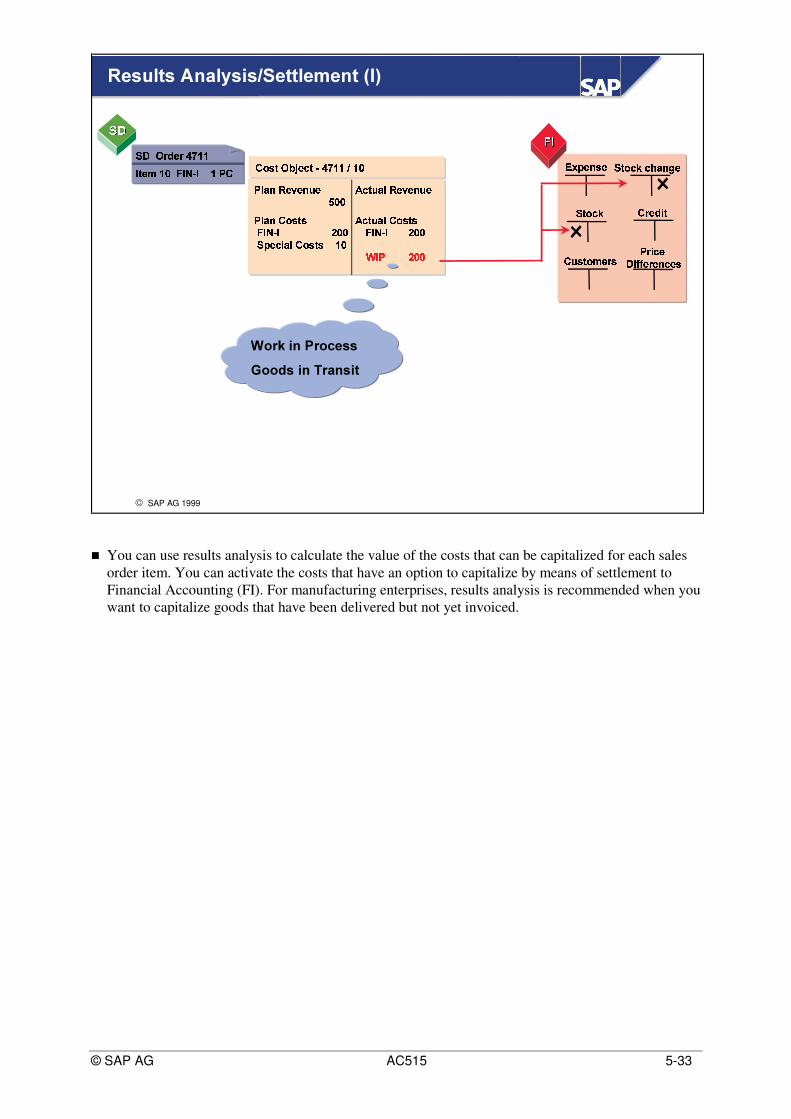

n You can use results analysis to calculate the value of the costs that can be capitalized for each salesorder item. You can activate the costs that have an option to capitalize by means of settlement toFinancial Accounting (FI). For manufacturing enterprises, results analysis is recommended when youwant to capitalize goods that have been delivered but not yet invoiced.

?Q��8����µ7wÝ`�;���1�!º�:!M�MbÁ1M�>� C E!� ¶ �NJ �!�1�%� TQ�%���%E�C ¶ ��J����!���

=;>%> =%>;>� C E!��?@��8;��8 TQ�����%E1CI?3�!8%��8P�³�´���³ H >%> P!³ ´���³ H >�>��R%� �;� E!CI?@��8���8àMN>

������

���Ú����!��� º�:�M%M³ �4��DÛMI>ÜP!³ ´3�4³¼M � ?

n The actual revenues are updated on the sales order item by the invoice.

n Billing invoices the customer for the goods and services delivered for a sales order. In Sales andDistribution, you create an invoice (billing document) on the basis of a reference document. In order-related billing, the reference document is the standard order or the delivery document with delivery-related billing.

n The data such as prices and quantities are transferred from the previous documents into the billingdocuments. The price can be calculated in the following ways:

é Using pricing on the basis of conditions (such as material or customer)

é On the basis of the incurred costs if you want to use resource-related billing

n When you enter a billing document, the system proposes a billing type depending on the referencedocument. The billing type determines the following:

é Which pricing procedure is used for account determination for Financial Accounting

é Whether the invoices are passed immediately to Financial Accounting

3URILW��6HJPHQWïBäNñ ä!å1ó%ä ÷�ø%øô é æ è&é!ù�ç�í�ò ä%æ ú ûIø

ü�ýSþüµýÉþÿ��ÿ��

ô é æ è������ ä ê�è�� � û�û��1û�ø� ò í åLïBäNñ ä!å1ó%ä � ê%è ó í�ò ï ä�ñ�ä�å!ó�ä

÷;ø%ø ÷%ø%ø� ò í å ô é æ è æ � ê�è ó í1ò ô é æ è æ� ��� � � ú;ø%ø ��� � � � ú;ø�øç ã%ä ê ö í!ò ô é æ è æàûNø � ��� � ú%ø%ø

ïBäIæ�ä!ð+ñ�ä;æ ûsøô ���kç ú!ûNø

������ç�� � ð�õ!ä�ð � û%û� è ä !ÛûIø"��� � � �¼û#� ô

n When a sales order item is finally billed, this means that no more revenue is expected for that salesorder item. Only debit memos and credit memos can be entered. For this reason you can normallycancel all capitalized inventories. In case of follow-up costs it is possible to create reserves.

ô é æ è������ ä ê�è�� � û�û��1û�ø� ò í åLïBäNñ ä!å1ó%ä � ê%è ó í�ò ï ä�ñ�ä�å!ó�ä

÷;ø%ø ÷%ø�ø� ò í å ô é æ è æ � ê�è ó í1ò ô é æ è æ� ��� � � ú;ø%ø ��� � � � ú�ø;øç ã%ä ê ö í!ò ô é æ è æàûNø � ð`ö ê ä�õ�ö ù�ù%$& ø� ò í å ô é æ è æ

ç á('�� � � ûN÷;øï� � � ô ûNø� ô�) � *�� )�+ ø� êNè ó í�ò ô é æ è æç á('�� � � ûN÷;øï� � � ô ûNø� ô�) � *�� )�+ ÷%ø� ú;ø%ø

�(� � ð�õ!ä�ðÙû�� ô��� � � � ,� û%û��&ûIø

� ò í å ô é æ è æï� � � � ÷%ø� ô-) � *-� )�+ ûNø;ø

� êsè ó í ò ô é æ è æï(� � � � .%ø� ô�) � *-� ),+ ûNú;ø

� ûI÷�ø

�(� � ð�õ ä1ðÂû�� ôç á('�� � � ,� û%û��&ûIø

/10/�0á â&ã%ä�å%æ�ä ç è�é1ê�ë$ê�ì%í å;î!ä

��ð�ö ê ä� ö ù�ù ä1ð+ä1å ê ä�æ

ô ð�ä�õ ö èç&è`é1ê�ë

3URILW��6HJPHQWï�äsñ!ä!å1ó�ä ÷;ø%øô é æ è&é!ù�ç�í1ò ä%æ ú%ø;ø

ü�ýÉþü�ýSþÿ��ÿ1�

ô ó�æ è`é !Lä ð�æ

������ç�� � ð�õ!ä�ð � û%û� è ä !ÛûIø"��� � � �¼û#� ô

2(32(3

4534�3

n In complex MTO-scenarios, it might make sense to collect the total production costs including pricedifferences on the level of the sales order item. In this case, you can define the price differenceaccount as a cost element and post the value to the sales order item when settlement to FI takesplace.

n In this case, make sure that variance categories are not settled from production order to CO-PA.

3URILW��6HJPHQWï�äIñ ä å1ó;ä ÷�øIøô é æ è1é!ù1ç í�ò ä%æ úIø�ø* í ð�ö í å ê ä6�1ö å1ö æ ì ûsø* í ð�ö í å ê ä ç ä5! ö ù ö å1ö æ ì87 ø

ü�ýSþüµý þÿ1�ÿ1�

� ò í å ô é æ è æç á('�� � � ûI÷�øï� � � ô ûNø� ô�) � *�� )�+ ø� êNè ó í�ò ô é æ è æç á('�� � � ûN÷;øï� � � ô ûNø� ô�) � *�� )�+ ÷%ø� ú;ø%ø

�(� � ð�õ!ä�ðÙû�� ô��� � � � ,� û%û��&ûIø

� ò í å ô é æ è æï� � � � ÷;ø� ô�) � *�� )�+ ûNø;ø

� êNè ó í�ò ô é æ è æï9� � � � .%ø� ô�) � *-� ),+ ûIú�ø

� ûs÷;ø

�(� � ð�õ!ä�ðÙû�� ôç á('#� � � ,� û%û��&ûIø

ÿ#ÿÿ$ÿ

2:32(3

4534�3

ô ó�æ è�é !�ä!ð�æ

n Because the manufacturing orders contain the full actual costs for the production of the materialmanufactured by the manufacturing order, you can calculate variances at the level of themanufacturing orders and settle them to CO-PA.

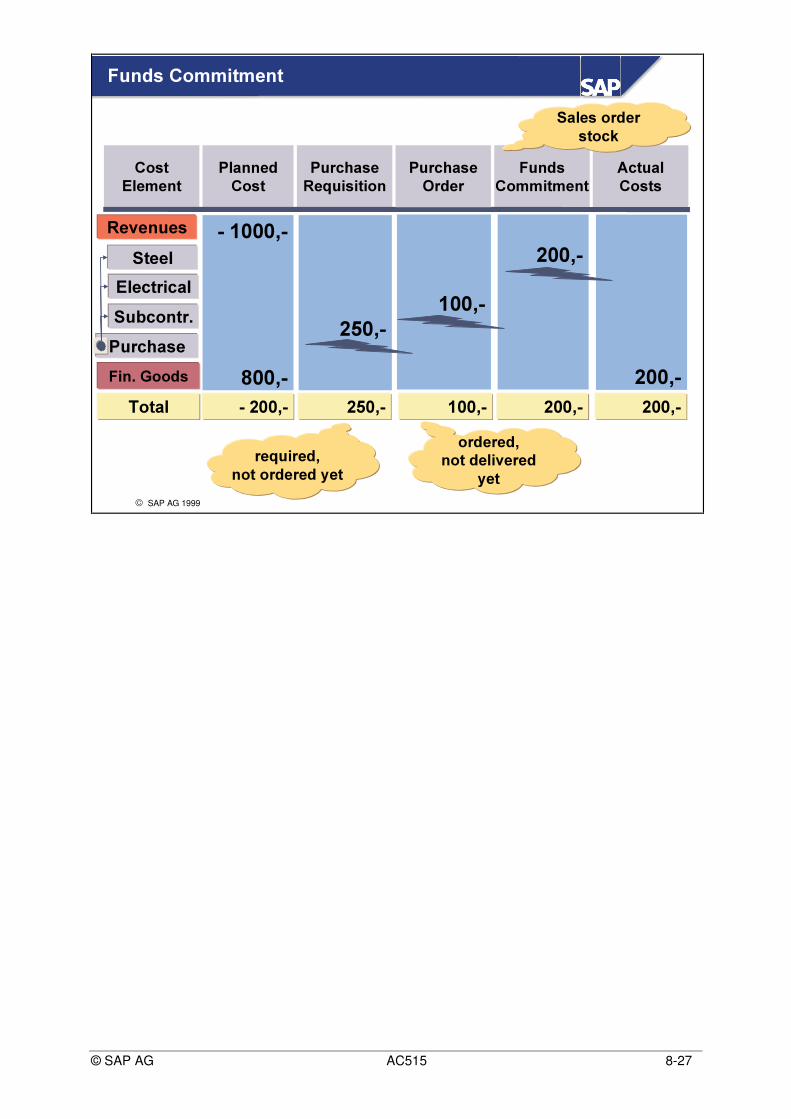

l &RQWUDFWXDO�FRPPLWPHQWV�ZKLFKUHVXOWV�LQ�DFWXDO�FRVWV; 3XUFKDVH�5HTXLVLWLRQ; 3XUFKDVH�2UGHUV

l &DSLWDOL]HG�FRVWV�LQ�WKH�YDOXDWHGVDOHV�RUGHU�VWRFN

n Commitments show you the contractual or planned commitments that do not yet affect accounting(no expenses yet) but that will result in actual costs at a later time. This allows you to analyze theeffects on cost accounting of purchase orders for sales document items.

n In addition, you can view the funds commitment in the valuated sales order inventory on the salesorder item as statistical actual data in the Product Cost Controlling Information System if the salesorder item carries costs and revenues.

n Unlike unvaluated sales order stock, a goods receipt in valuated sales order stock leads to actualcosts on the relevant Controlling objects (SD document item, WBS element). In order to be able todisplay the committed funds on the sales order stock in the Controlling information system, thesystem would need to read the corresponding segments in the material master.

n If the purchase requisitions are created by the MRP-run, the commitments for these purchaserequisitions are not updated.

<&=�=�?@BA9C DXWD�Y�?R>S Y D R>S =�P�? =�PZK @N[ P%?<\J�P S @N[�P]K ^_Y(C [9O(OHK�O�V

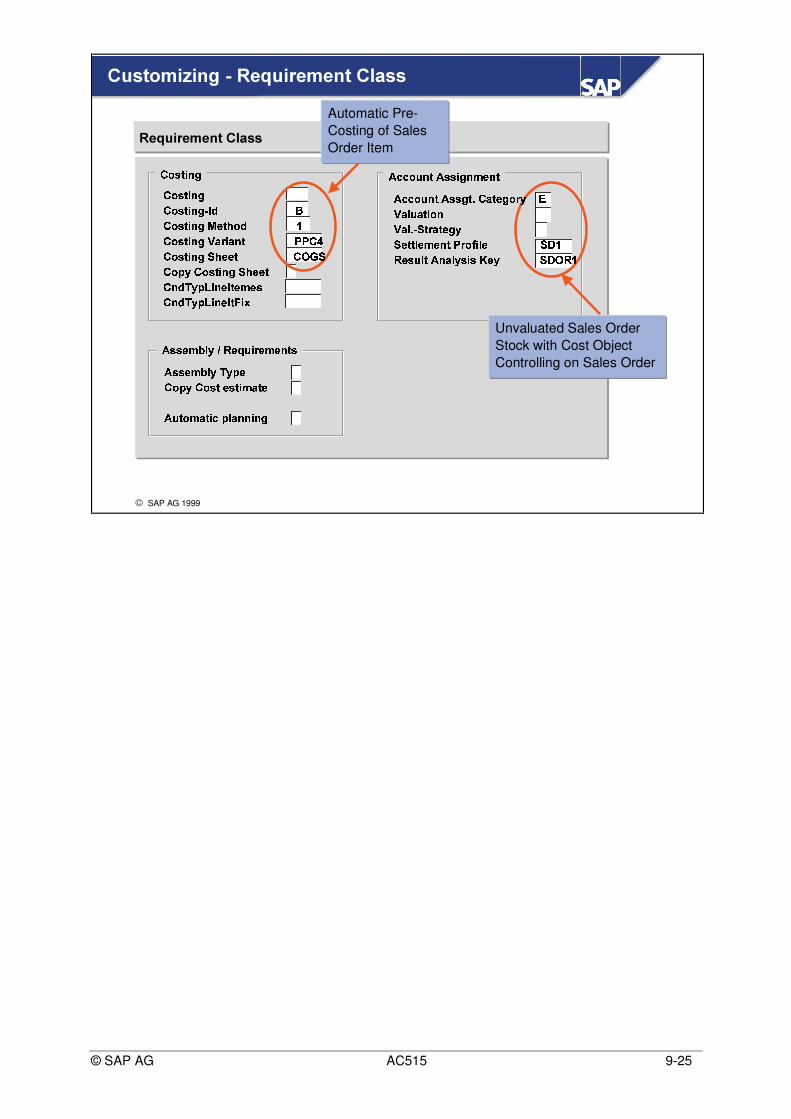

<�^�^ S JHO�P(<>=5=HK V1O:@N?9O�P5HTXLUHPHQW�&ODVV

RTS =�PZK�OVRTS =�PZK�OVH`%a b cRTS =�PZK�OV_d6?�PUe S b fRTS =�PZK�OVFg�[(LZK [9O�P h1h RjiRTS =�PZK�OVlkTe�?�?5P RTm�n kRTS Y5D RTS =�PUK�O:VlkTe�?�? PR Ob(W:D�Y9o9K O�?9a PQ?@N=R Ob(W:D�Y9o9K O�?9a PUp9K q

Automatic Pre-Costing of SalesOrder Item

<�^5^ S J9O�P:<>=�=:VP]r R [�Ps?�V S L�Dutg�[(C J[5PZK S O dg�[(C r `vk1PZLM[�Ps?�VDk-?5PMP]C ?�@l?(O�P�hjL S(w K�C ? k�xTfGj? =HJ9C P%=6<\O�[9C D�=HK =_yj?,D k�x m G>f

Valuated Sales OrderStock with Cost ObjectControlling on Sales Order

<&=�=�?@BA9C DXWD�Y�?R>S Y D R>S =�P�? =�PZK @N[ P%?<\J�P S @N[�P]K ^_Y(C [9O(OHK�O�V

<�^�^ S JHO�P(<>=5=HK V1O:@N?9O�P

�

5HTXLUHPHQW�&ODVV

This indicator controls whether

l the preliminary costing for the manufacturingorder should be used for assembly processing

l a sales order costing can be created

n This indicator is only relevant if you are using assembly type 2 ("production order, network orservice (stat. processing)").

é If you don’t set this indicator the system copies the planned costs, which are calculated using thepreliminary cost estimate for the production order, to the SD conditions. You are then unable tocreate a sales order costing for the sales document item.

é If you set this indicator, you can create a sales order costing for the sales document item, which isthen copied to the conditions. The planned costs, created using the preliminary cost estimate forthe production order, are not copied into the SD conditions.

n The following examples explain where it is appropriate to create a sales order costing for assemblytype 2:

é A cost component split has been stored for sales order costing using the product costing methodbut it is not available for the preliminary costing estimate of a production order (because thesystem only creates a cost component split dynamically for the production order display). Copyingthe cost component split based on sales order costing to Profitability Analysis (CO-PA) is usefulif you are working with a valuated sales order stock and the standard price is based on the salesorder costing (also see Valuation with standard price).

é When you use the nonvaluated sales order stock, the preliminary cost estimate does not deliver thecomplete planned costs to the assembly order. To receive the complete planned costs, it makessense to calculate the sales order costing and transfer this to the SD conditions.

<&=�=�?@BA9C DXWD�Y�?R>S Y D R>S =�P�? =�PZK @N[ P%?<\J�P S @N[�P]K ^_Y(C [9O(OHK�O�V

<�^�^ S JHO�P(<>=5=HK V1O:@N?9O�P

Transfer of thetotal cost

tjy-�:f

Transfer of thefixed cost part

5HTXLUHPHQW�&ODVV

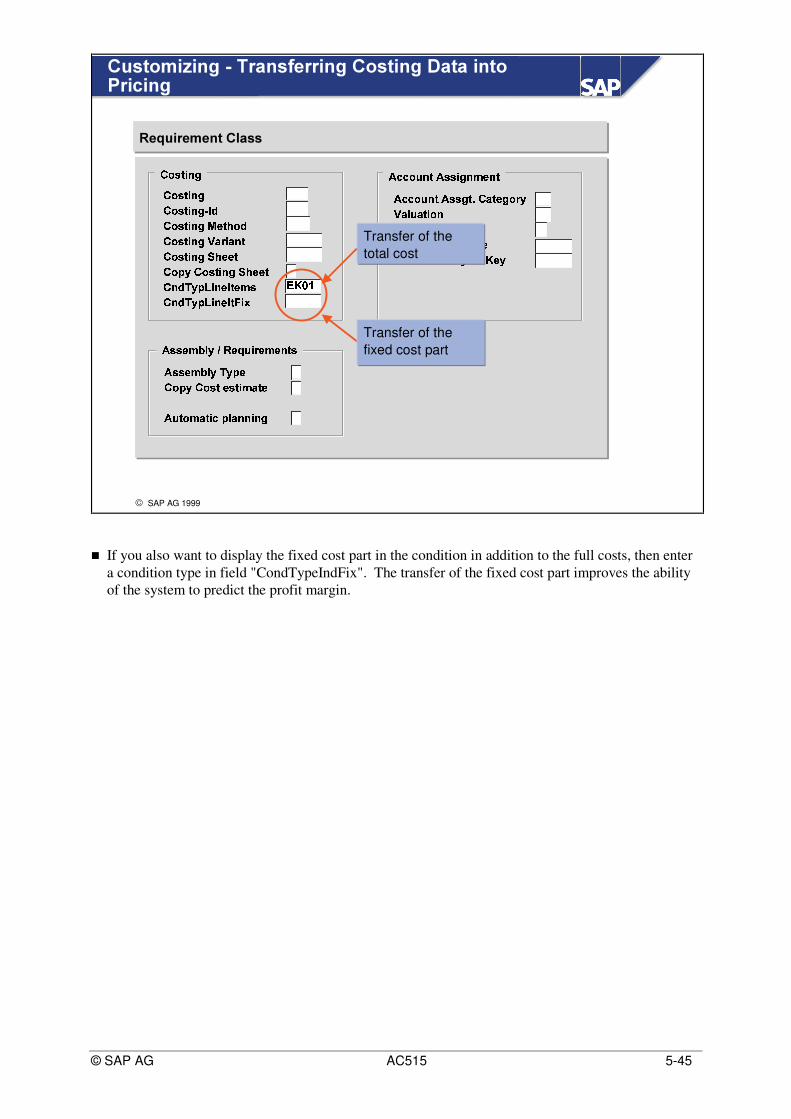

n If you also want to display the fixed cost part in the condition in addition to the full costs, then entera condition type in field "CondTypeIndFix". The transfer of the fixed cost part improves the abilityof the system to predict the profit margin.

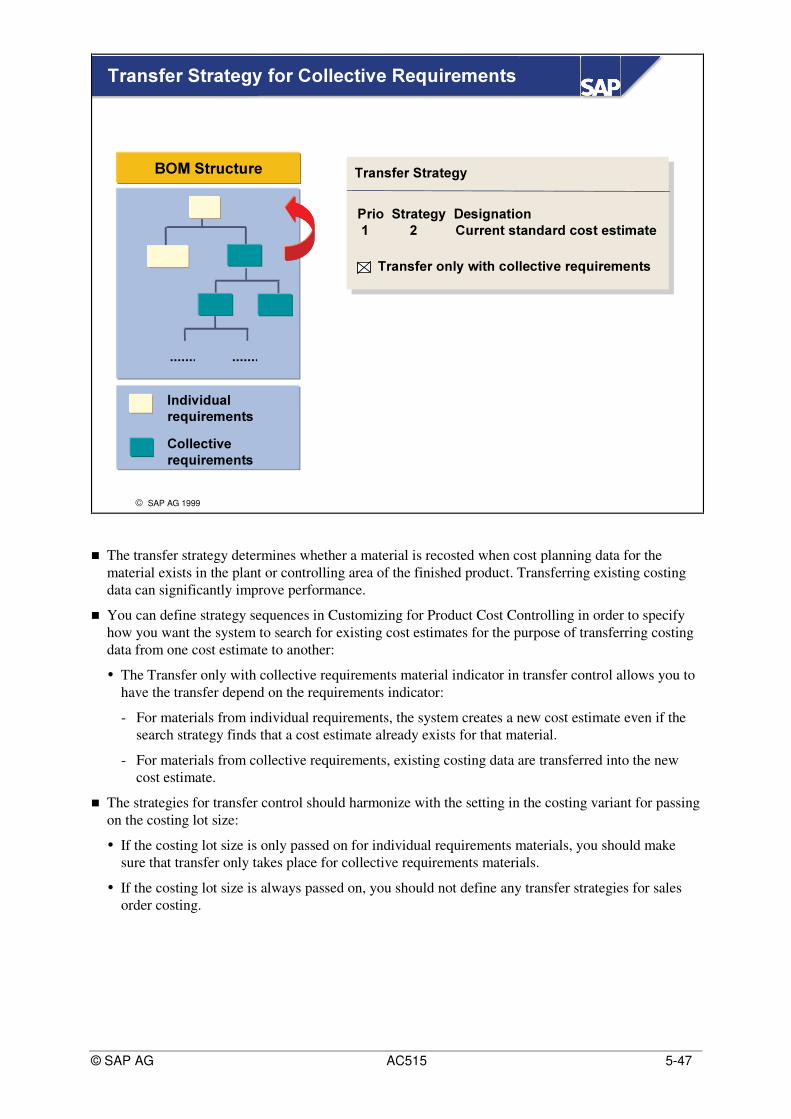

n The transfer strategy determines whether a material is recosted when cost planning data for thematerial exists in the plant or controlling area of the finished product. Transferring existing costingdata can significantly improve performance.

n You can define strategy sequences in Customizing for Product Cost Controlling in order to specifyhow you want the system to search for existing cost estimates for the purpose of transferring costingdata from one cost estimate to another:

é The Transfer only with collective requirements material indicator in transfer control allows you tohave the transfer depend on the requirements indicator:

- For materials from individual requirements, the system creates a new cost estimate even if thesearch strategy finds that a cost estimate already exists for that material.

- For materials from collective requirements, existing costing data are transferred into the newcost estimate.

n The strategies for transfer control should harmonize with the setting in the costing variant for passingon the costing lot size:

é If the costing lot size is only passed on for individual requirements materials, you should makesure that transfer only takes place for collective requirements materials.

é If the costing lot size is always passed on, you should not define any transfer strategies for salesorder costing.

Transfer only with collective requirements material

Strategy Sequence Fiscal Year Periods ... 12Current standard cost estimate

Single-Plant Cross-Plant

¢ �(���:�]� �Q� � �����9��]�1�}�Pass on Lot size Only with individual requirement

...

Performance Recommendation:

Pass on the lot size only with individualrequirements and use a transfer control,which searches for existing costestimates for collective requirements

n A costing variant contains control parameters for calculating the planned costs of a sales documentitem. From the sales document item you branch to the costing functions.

n Performance recommendation: Pass on the lot size only for individual requirements and use atransfer control, which searches for existing cost estimates for collective requirements.

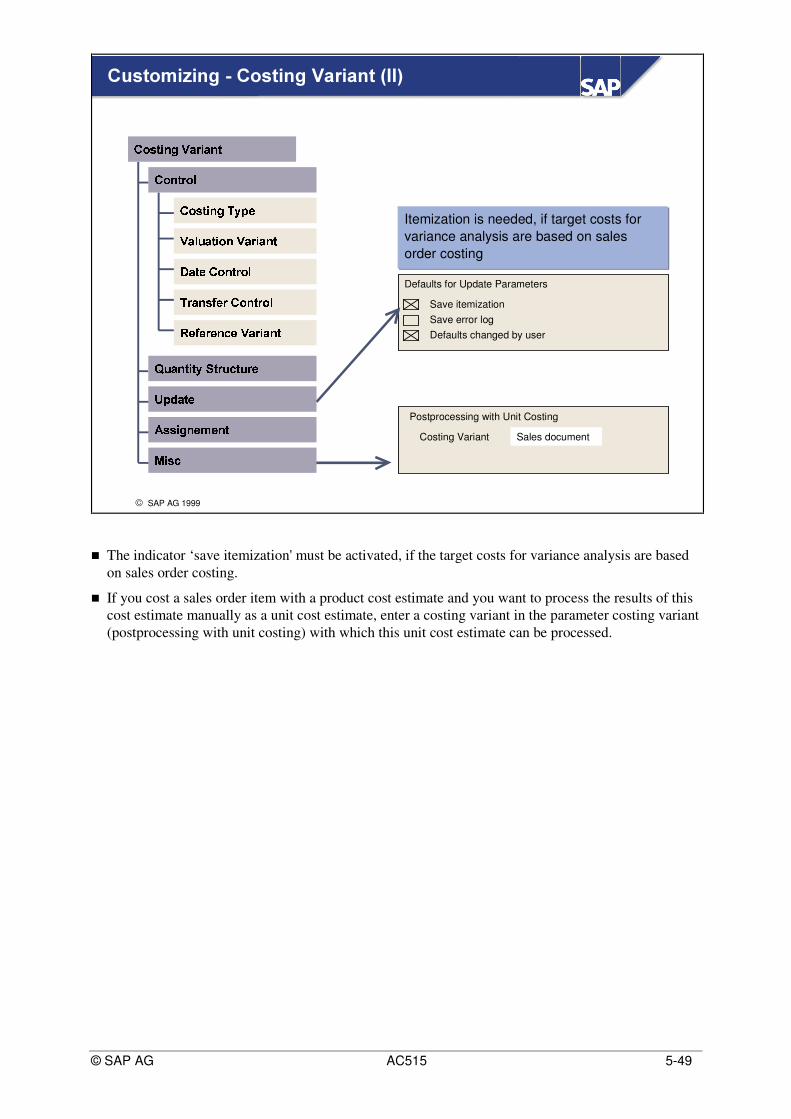

Save itemizationSave error logDefaults changed by user

¢ �(���:�]� �Q� � �����9��]�1�}�

Itemization is needed, if target costs forvariance analysis are based on salesorder costing

Postprocessing with Unit Costing

Costing Variant�z� � �

Sales document

n The indicator ‘save itemization' must be activated, if the target costs for variance analysis are basedon sales order costing.

n If you cost a sales order item with a product cost estimate and you want to process the results of thiscost estimate manually as a unit cost estimate, enter a costing variant in the parameter costing variant(postprocessing with unit costing) with which this unit cost estimate can be processed.

<#^5PUK ~[�PM? R�S @BY S O�?(O�P%=R>S =�P R ?:O�Ps?9Lm LQb9?9LHd\[9O[�V9?�@X?:O�PR>S @_@zK PU@l?(O�P1d\[(O�[V(?@l?(O�Ph-L S:w K P:<�O[(C D�=HK =<�^ PUK ~�K PQD_A[5=�?b RTS =�P]K OVh�L S:w K P R ?9O5Ps?9L<�^�^ S J9O�PUK�OVh�L S £ ?^5PQ=k�[9C ?5= m L%b(?9LM=¤¥r ^ S @_@zK P1@l[(O�[V:?:@N?9O�P

RTS =�P m A £ ?^ PM=

f R>S @BY S O�?(O�PH[^ PUK ~:?f R>S @BY S O�?(O�PH[^ PUK ~:?f8<�^5P}K ~:?i h-L S:w K P(<�O�[9C D�=9K =�¦<�^5P}K ~�K PQDBA�[�=�?�b R�S =�P]K O�V

This indicator controlswhether commitmentsare updated

For balance sheet accountsthe cost element type 90 isdefined

&RVW�(OHPHQWV�IRU�%DODQFH�6KHHW�$FFRXQW

&RVW�(OHPHQW � ¨%ú;ø�ø;ø

n The committed funds on the sales order stock not only need to be displayed, but must have interestcalculated for them as well, especially in projects. Therefore the information on the committed fundsneeds to be available up-to-date on a daily basis. But this information cannot be taken from thematerial master, and thus needs to be updated in Controlling under the value type 11 Statistical actualfor all goods movements for sales order stock. To this end, cost elements are created with the costelement category 90 statistical balance sheet account for the relevant statistical balance sheetaccounts.

n Note: Before an inventory account may be created as a statistical cost element, the inventory accountmust be already identified for MM Account determination for the Inventory posting (BSX process).

At the conclusion of this exercise, you will be able to:

• Understand the quantity and value flow in make-to-order with salesorder controlling using discrete manufacturing.

• Check the control data of the sales order item.

• Determine which material will be produced or purchased specificallyfor the sales order.

• Create production orders and purchase orders to fulfill the sales ordersrequirements.

• Create a delivery and invoice for the sales order item.

• Analyze the relevant accounting and controlling documents.

In your plant 1000, the finished product T-F1## is produced. The masterdata has already been maintained but is to be verified. You will create asales order for material T-F1## and execute material requirementsplanning for your sales order. You will then create production orders anda purchase order for the individual requirements materials and completethe necessary postings (goods issues, goods receipts, confirmations) inthe system to produce the product T-F1##. At the end of this exercise,you will create a partial delivery to the customer.

1-1 Start by creating a sales order for the finished good T-F1##.

1-1-1 Create a sales order for the material T-F1##:

Use the following data:Order type: 25�(standard order)Sales organization: ����Distribution channel: ��Division: ��

Sold-to party: ����PO number: ����Material: 7�)���Order quantity: �� piecesChoose (QWHU.Accept the delivery date proposal.

What results analysis key and costing sheet were transferred into the salesorder? How were the defaults for the costing sheet and results analysis keytransferred to the sales order item?

1-2 Review the BOM (listed below) for T-F1##. Complete the following questions byreviewing the material master setting for the individual/collective requirementsindicator for the BOM components.

1-2-1 Which sub assemblies will be produced specifically for the sales orderrequirement?

1-2-3 Change the individual/collective requirements indicator for Material7�7����� so that this component will be purchased specifically for the salesorder.

1-3 Execute material requirement planning for your sales order. Save the results for allcomponents.

1-4 From the evaluations menu, go to the stock requirements list for 7�%���, plant1000, and display the planning result.

1-4-1 The list will show the planned order created to fulfill the dependentrequirement of your sales order requirement for T-F1##. Convert thisplanned order to a production order.

1-4-2 Display the assignment data for the production order. Is the productionorder assigned to the sales order?

1-5 Review the stock requirements list for 7�7���. A purchase requisition was createdto support the sales order requirement.

1-5-1 Convert the purchase requisition into a purchase order. Use purchasingorganization 1000, vendor 1000, purchase group 010 and company code1000. The price is 50 UNI.

1-5-2 Save your purchase order and record the purchase order number. If thepop-up 32�RI�WRGD\�DOUHDG\�H[LVWV appears, proceed with the button 1HZ3XUFKDVH�2UGHU�___________________________________________________________

1-5-3 Go to the information system for Product Cost by Sales Order and reviewthe commitment report for your sales order. Check whether thecommitment for the purchase order was updated on the corresponding salesorder item

1-6 From inventory management, process the goods receipt for material 7�7��� andreview the valuated special stock report.

1-6-1 Process the goods receipt:

Menu path:/RJLVWLFV��0DWHULDOV�0DQDJHPHQW��,QYHQWRU\�0DQDJHPHQW��*RRGV5HFHLSW��)RU�3XUFKDVH�2UGHU��32�QXPEHU�NQRZQ

Now enter the following data:Purchase Order: \RXU�SXUFKDVH�RUGHU�QXPEHUChoose (QWHU

Set the OK flag for the purchase order position.

Choose: 6DYH

1-6-2 From the valuated special stock report, determine if the material T-T4## isshown as valuated special stock.

1-7 Proceed with the manufacturing of material 7�%����

1-7-1 Issue material T-T4## to the production order for T-B3##. Use movementtype 261, plant 1000, storage location 0001. Is there an accountingdocument created for the transaction?

1-7-2 Return to production control menu. Enter the production confirmation (timeticket based) for the last operation, confirm a quantity of 10 and increase theproposed activity quantity to 2 hours. Save the final confirmation.

1-7-3 Go to the information system and display the actual costs for the productionorder. Was the production order credited for the goods receipt of T-B3##?How was the value of the goods receipt determined?

1-9 Proceed with the manufacturing of material 7�)����

1-9-1 Post the material issue to the production order for T-F1##. Use movementtype 261, plant 1000, storage location 0001

1-9-2 Return to the production control menu. Enter a partial confirmation for theproduction order for T-F1##. Confirm only a quantity of 5 and save thepartial confirmation.

1-9-3 Go to valuated special stock display for material T-F1##. Is the goodsreceipt for production confirmation of 5 ea displayed as sales order stock?What is the total stock quantity and stock value for valuated sales orderstock of T-F1##?

1-10 5 of the ordered 10 pumps are now available for delivery.

1-10-1 Create a sales delivery for the 5 pumps.

Use the following data:Shipping Point: ����Delivery Date: WRGD\¶V�GDWH�SOXV����GD\VSales Order: QXPEHU�RI�\RXU�VDOHV�RUGHURecord the delivery number.

1-1 Start by creating sales orders for the finished good T-F1##.

1-1-1 Create a sales order for the material T-F1##:

Menu path:/RJLVWLFV�Å�6DOHV�DQG�'LVWULEXWLRQ�Å�6DOHV�Å2UGHU�Å�&UHDWH

Enter the following data:Order type: 25����6WDQGDUG�RUGHU�Sales organization: ����Distribution channel: ��Division: ��Choose (QWHU.

Now enter the following data:Sold-to party: ����PO number: ����Material: 7�)���Order quantity: �� piecesChoose (QWHU.Accept the delivery date proposal by selecting the button 'HOLYHU\�3URSRVDO

1-1-2 Check the following control data of the sales order item.

What item category does the item have?

(found on tabstrip Sales)

7$1���6WDQGDUG�,WHP�What results analysis key and costing sheet were transferred into the salesorder? How were the defaults for the costing sheet and results analysis keytransferred to the sales order item?

To verify the results analysis key and the costing sheet, which are assignedthrough the requirements class, select the following menu path:*RWR��,WHP��$FFRXQW�$VVLJQPHQW

What requirements type was determined for the sales order item?(From sales overview, select tabstrip 3URFXUHPHQW)&2���0DNH�WR�2UGHU��ZLWK�&RQWUROOLQJ�E\�6DOHV�2UGHU

1-1-3 Save the sales order and record the sales order number:

1-2 Review the BOM (listed below) for T-F1##. Complete the following questions byreviewing the material master setting for the individual/collective requirementsindicator for the BOM components.

1-2-1 Which subassemblies will be produced specifically for the sales orderrequirement for T-F1##?

Material: 7�%���Choose (QWHU. In the dialog box, select 053��Choose (QWHU. In the dialog box, make the following entry:Plant: ����Choose (QWHU.

From the MRP4 view of the material master, determine the entry forindividual/collective requirements for each subassembly (Material:T-B1##, T-B2##, T-B3##, T-B4##). Since T-B3## has a blank indicator, itwill use the setting of the next higher assembly.

1-2-2 Which materials will be issued from anonymous stock?

T-B1##, T-B2## and T-B4## have the collective requirement indicator,which determines that these subassemblies will be issued to the productionorder from anonymous stock.

1-2-3 Change the individual/collective requirements indicator for material 7�7���so that this component will be purchased specifically for the sales order.

For the Material T-T4## you need to set the individual/collectiverequirements indicator to blank (or 1). Then, T-T4## will follow the samecontrol that is established for T-B3##. MRP will generate a purchaserequisition for T-T4## to support the sales requirement for T-F1##.

7�)���

7�%���1

7�%���1

7�%���1

%20�IRU�SURGXFW�7�)���

7�7���1

7�7���1

7�7���1

7�%���1

...

1-3 Execute material requirements planning for your sales order. Save the results for allcomponents.

Menu path:/RJLVWLFV��3URGXFWLRQ��053��3ODQQLQJ��6LQJOH�,WHP��6DOHV�2UGHU

Enter your sales order number and item 10. Press enter TWICE. Save the MRPresult for T-F1##. When you receive the window for 1H[W�6WRSSLQJ�3RLQW, selectSURFHHG�ZLWKRXW�VWRSSLQJ, then cRQWLQXH.