24

STARTUP TAX STRATEGIES SAIDUDDIN & CO. ADVOCATES TAXATION, MANAGEMENT & COMPANY LAW CONSULTANTS

| Date post: | 30-Dec-2015 |

| Category: |

Documents |

| Upload: | kelley-oneal |

| View: | 216 times |

| Download: | 1 times |

STARTUP TAX STRATEGIES SAIDUDDIN & CO.ADVOCATES

TAXATION, MANAGEMENT & COMPANY LAW CONSULTANTS

PRESENTATION OVERVIEW What does tax mean to a Startup?

Which tax filings are due and when?

Under the Income Tax Laws. Under the Sales Tax Laws.

What do I need to do to get ready?

WHAT DOES TAX MEAN TO A START UP?

Everything including:

Whether to enter the market or not?

Payment structuring

Profitability

Compliances

WHICH TAX FILINGS ARE DUE AND WHEN?

Tax filings and due dates are driven by:

Business entity type (Sole Proprietorship, AOP & Company)

Where the business was formed and where it’s operating

The fiscal or calendar year end chosen for tax reporting

FIRST THINGS FIRST

What is the first thing that a Startup needs to do?

Set up a legal entity and get it self registered with both Federal and Provincial Tax Authorities

Before you register the entity it is mandatory to get yourself registered with the Federal Board of Revenue

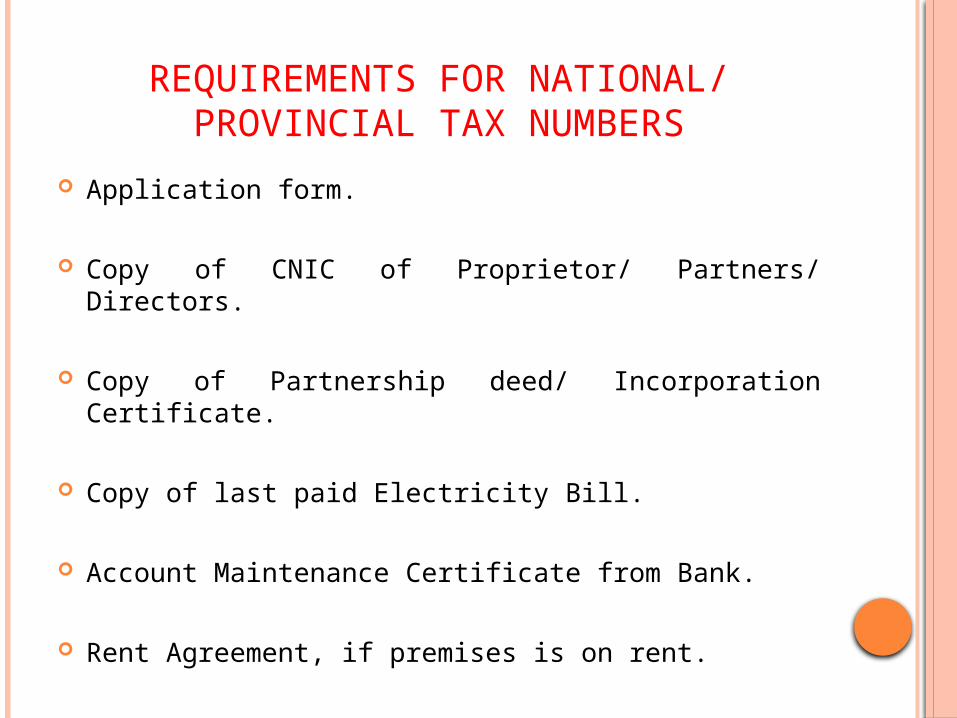

REQUIREMENTS FOR NATIONAL/ PROVINCIAL TAX NUMBERS

Application form.

Copy of CNIC of Proprietor/ Partners/ Directors.

Copy of Partnership deed/ Incorporation Certificate.

Copy of last paid Electricity Bill.

Account Maintenance Certificate from Bank.

Rent Agreement, if premises is on rent.

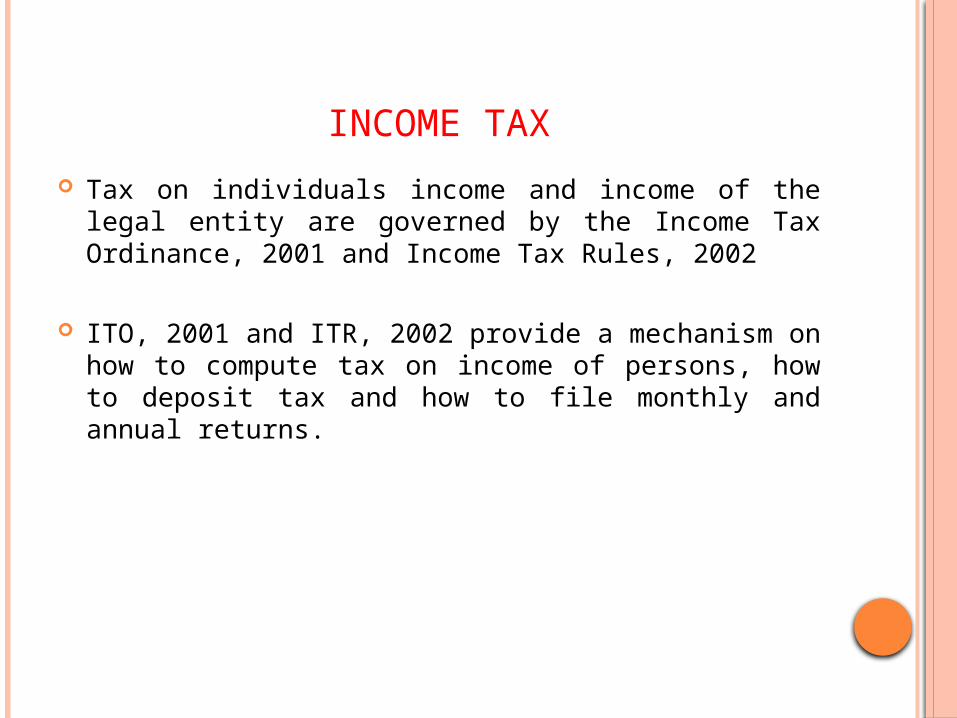

INCOME TAX

Tax on individuals income and income of the legal entity are governed by the Income Tax Ordinance, 2001 and Income Tax Rules, 2002

ITO, 2001 and ITR, 2002 provide a mechanism on how to compute tax on income of persons, how to deposit tax and how to file monthly and annual returns.

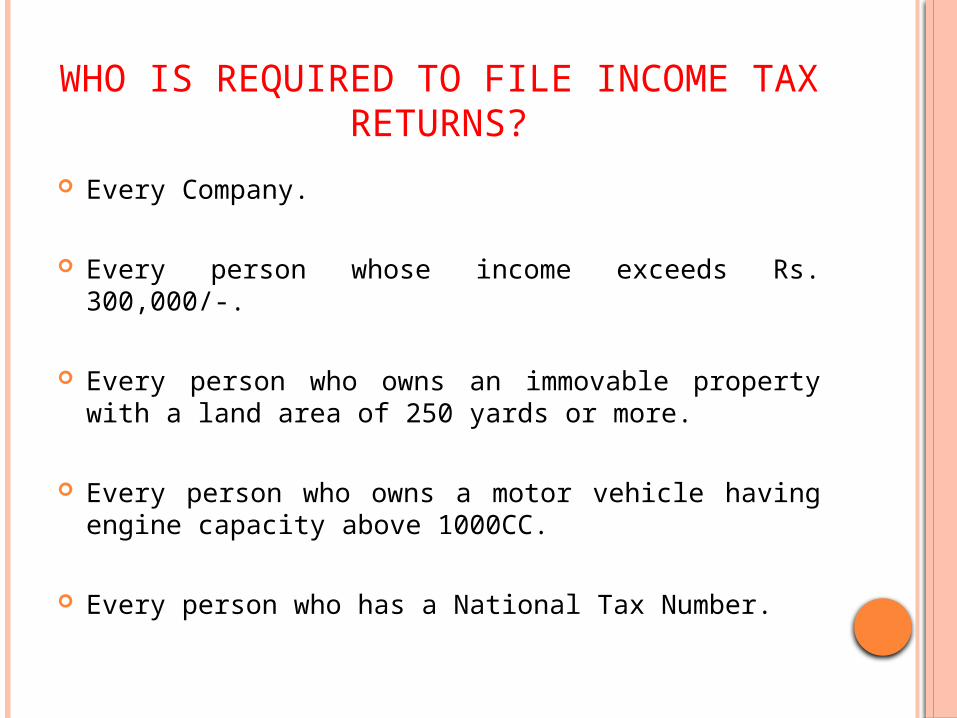

WHO IS REQUIRED TO FILE INCOME TAX RETURNS?

Every Company.

Every person whose income exceeds Rs. 300,000/-.

Every person who owns an immovable property with a land area of 250 yards or more.

Every person who owns a motor vehicle having engine capacity above 1000CC.

Every person who has a National Tax Number.

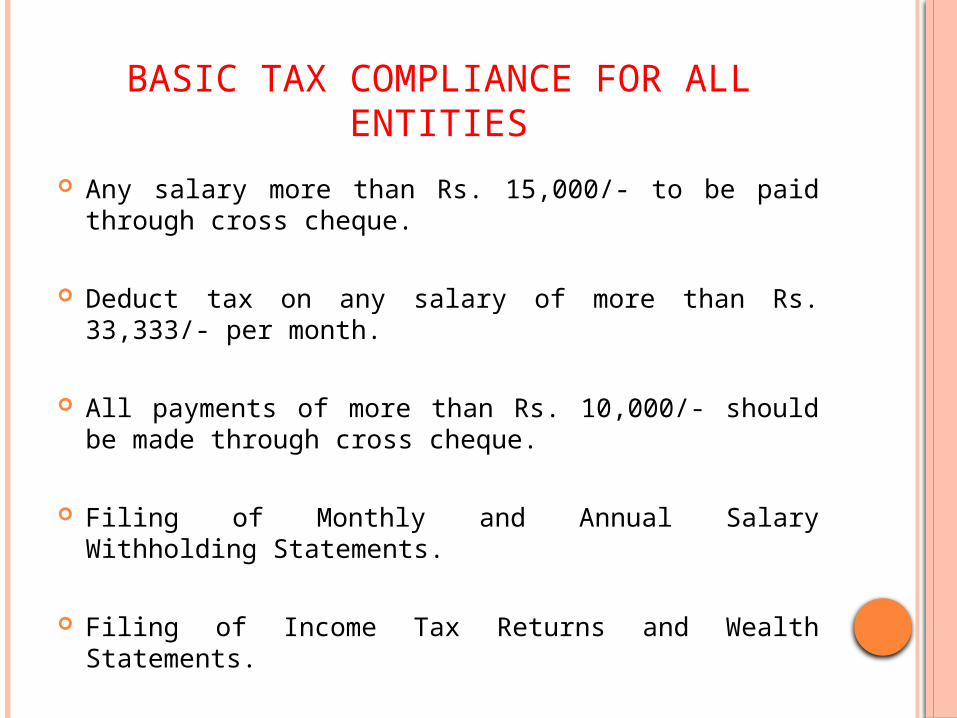

BASIC TAX COMPLIANCE FOR ALL ENTITIES

Any salary more than Rs. 15,000/- to be paid through cross cheque.

Deduct tax on any salary of more than Rs. 33,333/- per month.

All payments of more than Rs. 10,000/- should be made through cross cheque.

Filing of Monthly and Annual Salary Withholding Statements.

Filing of Income Tax Returns and Wealth Statements.

ADDITIONAL TAX COMPLIANCES

Sole Proprietorships and AoP’s having Annual Turnover of more than Rs. 50 million and Companies have to:

Deduct tax when making payments for services or supplies received.

Filing of monthly and annual withholding statements.

TAX YEAR AND TAX RATES

Tax Year is mostly from 1st July to 30th June unless a person opts for a Special Tax Year.

Progressive Tax Rates:

Salaried Individual: Between 0% and 30% Sole Proprietorship: Between 0% and 35% Association of Persons: Between 0% and 35% Small Company: 25% Company: 33%

(Income of Individuals and AoP if it is equal or less than Rs. 400,000/- is not chargeable to tax)

TAX ON SOLE PROPRIETORSHIP

Sole Proprietorship is taxed at a progressive rate on its taxable income i.e. total income of the person for the year reduced by the total of any deductible allowances.

The drawing of the Sole Proprietor during the tax year is not taxable.

Tax Rate: 0% to 35%

TAX ON AN AOP An AOP is taxed at a progressive rate on its taxable

income i.e. total income of the person for the year reduced by the total of any deductible allowances.

The drawings of the Partners of an AOP during the tax year are not taxable.

Tax Rate: 0% to 35%

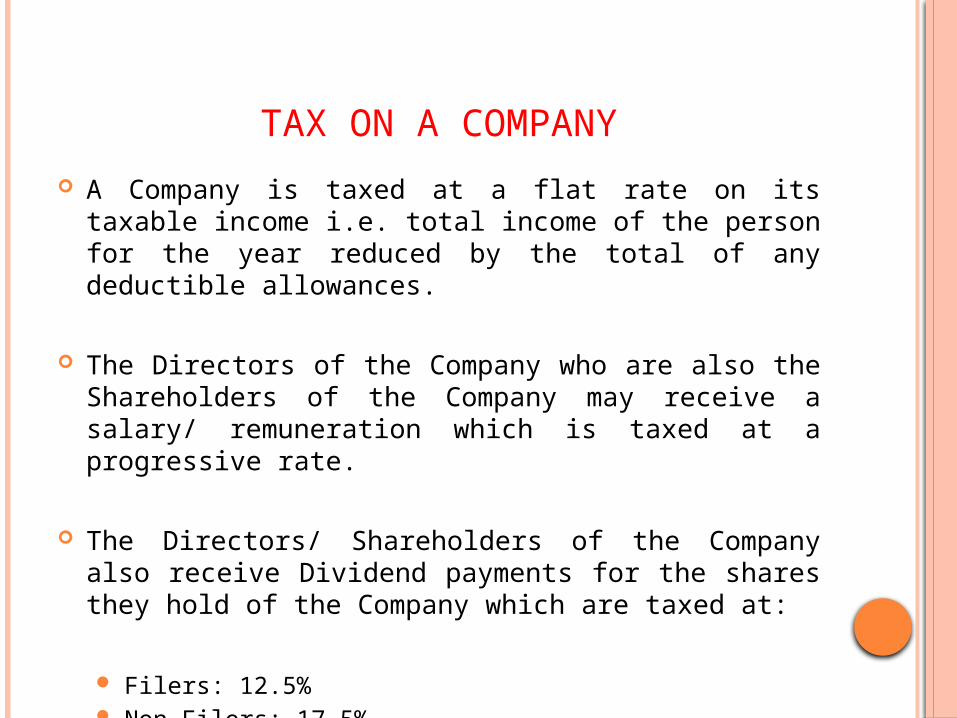

TAX ON A COMPANY

A Company is taxed at a flat rate on its taxable income i.e. total income of the person for the year reduced by the total of any deductible allowances.

The Directors of the Company who are also the Shareholders of the Company may receive a salary/ remuneration which is taxed at a progressive rate.

The Directors/ Shareholders of the Company also receive Dividend payments for the shares they hold of the Company which are taxed at:

Filers: 12.5% Non Filers: 17.5%

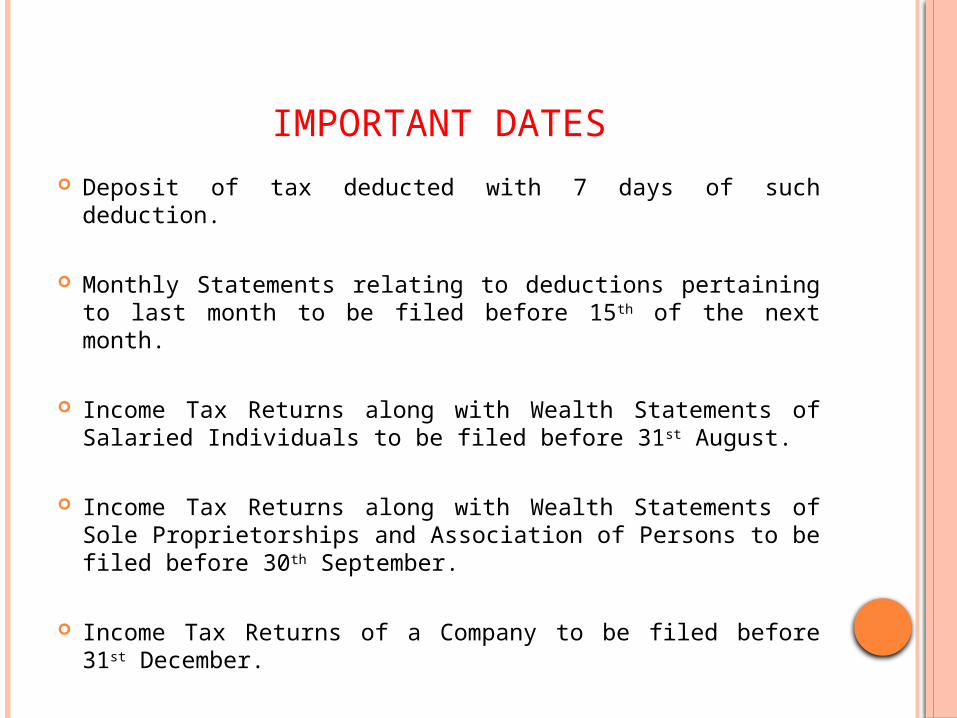

IMPORTANT DATES

Deposit of tax deducted with 7 days of such deduction.

Monthly Statements relating to deductions pertaining to last month to be filed before 15th of the next month.

Income Tax Returns along with Wealth Statements of Salaried Individuals to be filed before 31st August.

Income Tax Returns along with Wealth Statements of Sole Proprietorships and Association of Persons to be filed before 30th September.

Income Tax Returns of a Company to be filed before 31st December.

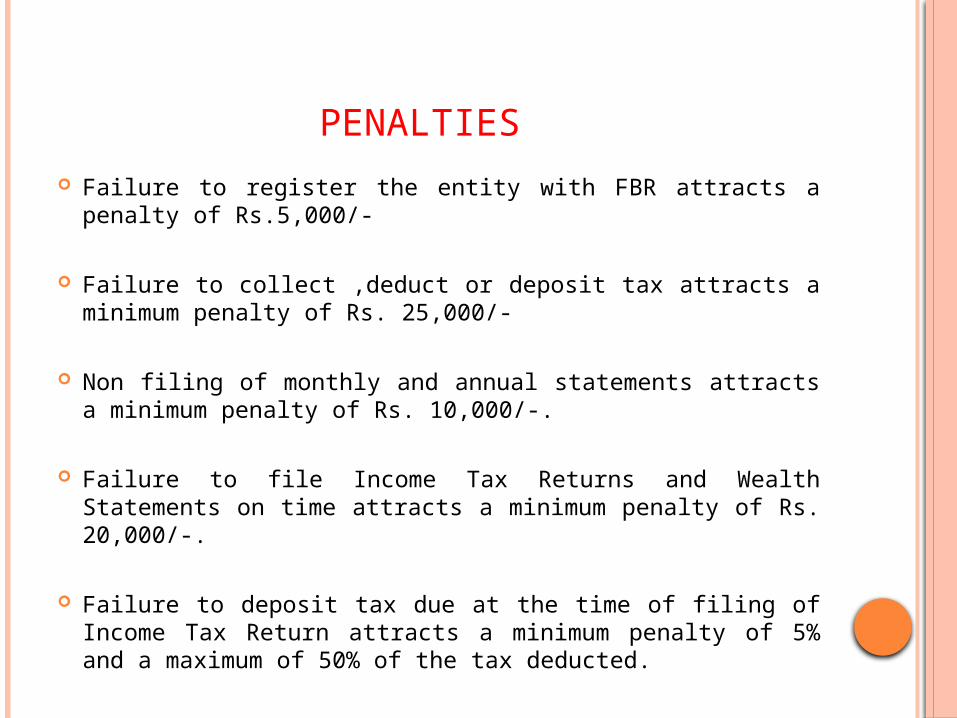

PENALTIES

Failure to register the entity with FBR attracts a penalty of Rs.5,000/-

Failure to collect ,deduct or deposit tax attracts a minimum penalty of Rs. 25,000/-

Non filing of monthly and annual statements attracts a minimum penalty of Rs. 10,000/-.

Failure to file Income Tax Returns and Wealth Statements on time attracts a minimum penalty of Rs. 20,000/-.

Failure to deposit tax due at the time of filing of Income Tax Return attracts a minimum penalty of 5% and a maximum of 50% of the tax deducted.

SALES TAX

Sales Tax on Goods is a Federal levy and is

governed by Sales Tax Act, 1990 and Sales Tax

Rules, 2006.

Sales Tax on Services is a Provincial levy and is

governed by:

Sindh Sales Tax on Services Act, 2011 & Sindh Sales Tax on

Services Rules, 2011.

Punjab Sales Tax on Services Act, 2012 & Punjab Sales Tax

Rules, 2012.

KPK Finance Act, 2013.

Islamabad Capital Territory (Tax on Services) Ordinance, 2001

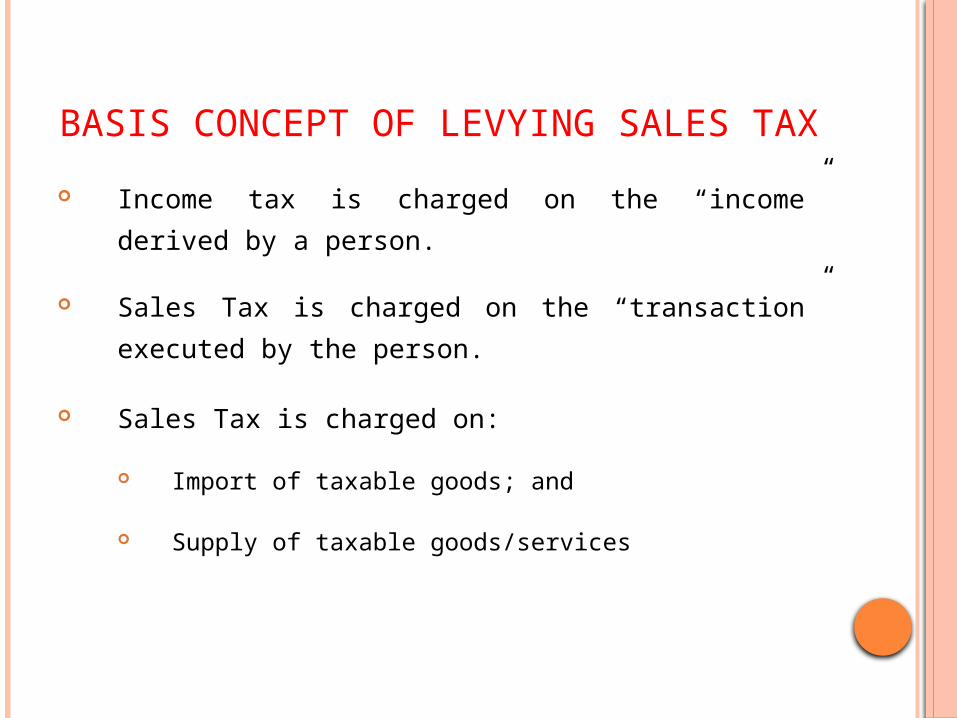

BASIS CONCEPT OF LEVYING SALES TAX

Income tax is charged on the “income” derived by a

person.

Sales Tax is charged on the “transaction” executed

by the person.

Sales Tax is charged on:

Import of taxable goods; and

Supply of taxable goods/services

INPUT AND OUTPUT TAX

When a person supplies goods or provide services,

sales tax is charged. This is called the “output tax”

Sales Tax paid at purchase of goods or acquiring of

services is called “input tax”.

The “output tax” is adjusted against the “input tax”

to arrive at the balance tax payable or refundable.

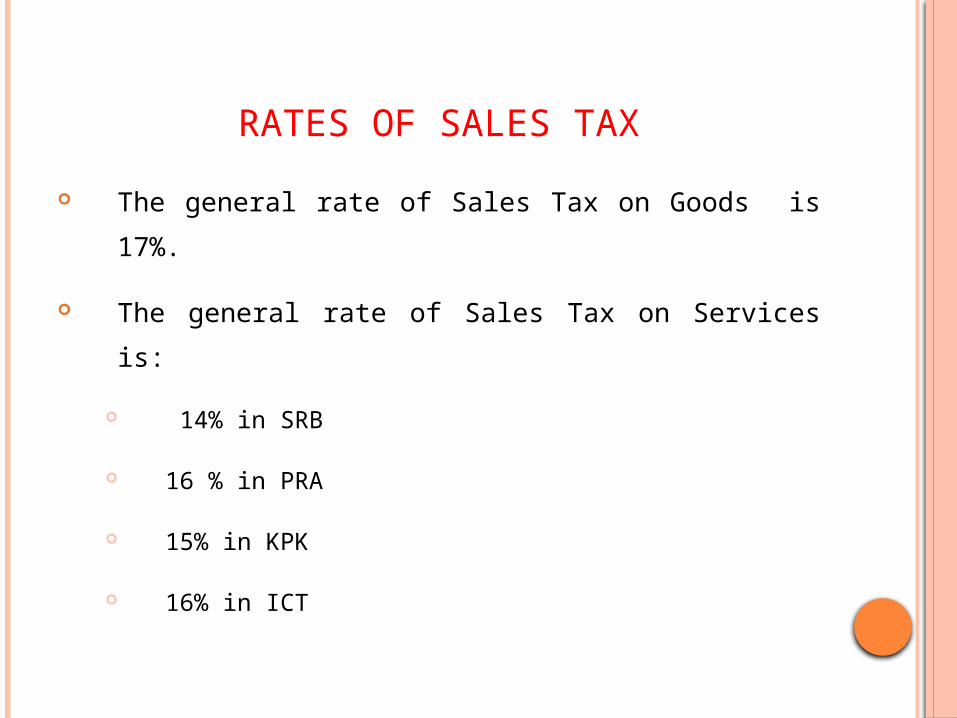

RATES OF SALES TAX

The general rate of Sales Tax on Goods is 17%.

The general rate of Sales Tax on Services is:

14% in SRB

16 % in PRA

15% in KPK

16% in ICT

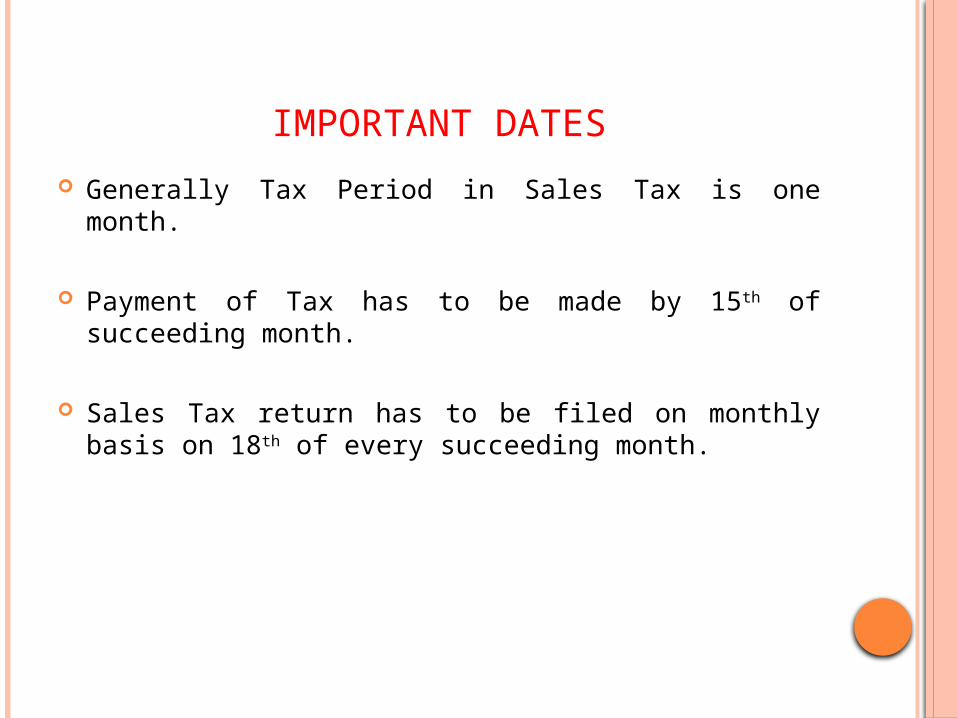

IMPORTANT DATES

Generally Tax Period in Sales Tax is one month.

Payment of Tax has to be made by 15th of succeeding month.

Sales Tax return has to be filed on monthly basis on 18th of every succeeding month.

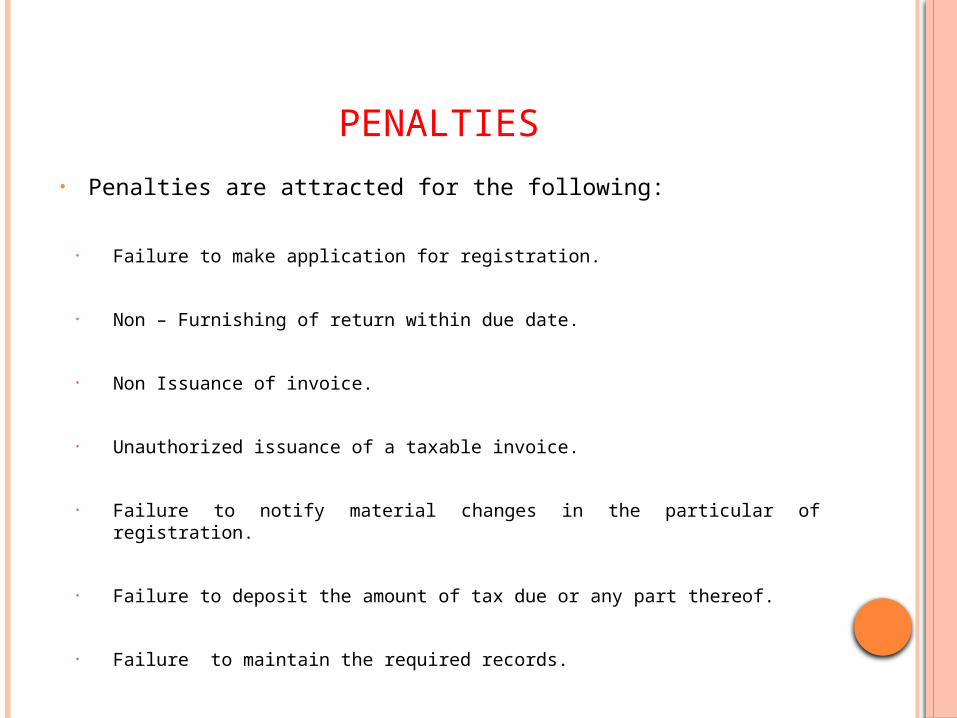

PENALTIES

• Penalties are attracted for the following:

• Failure to make application for registration.

• Non – Furnishing of return within due date.

• Non Issuance of invoice.

• Unauthorized issuance of a taxable invoice.

• Failure to notify material changes in the particular of registration.

• Failure to deposit the amount of tax due or any part thereof.

• Failure to maintain the required records.

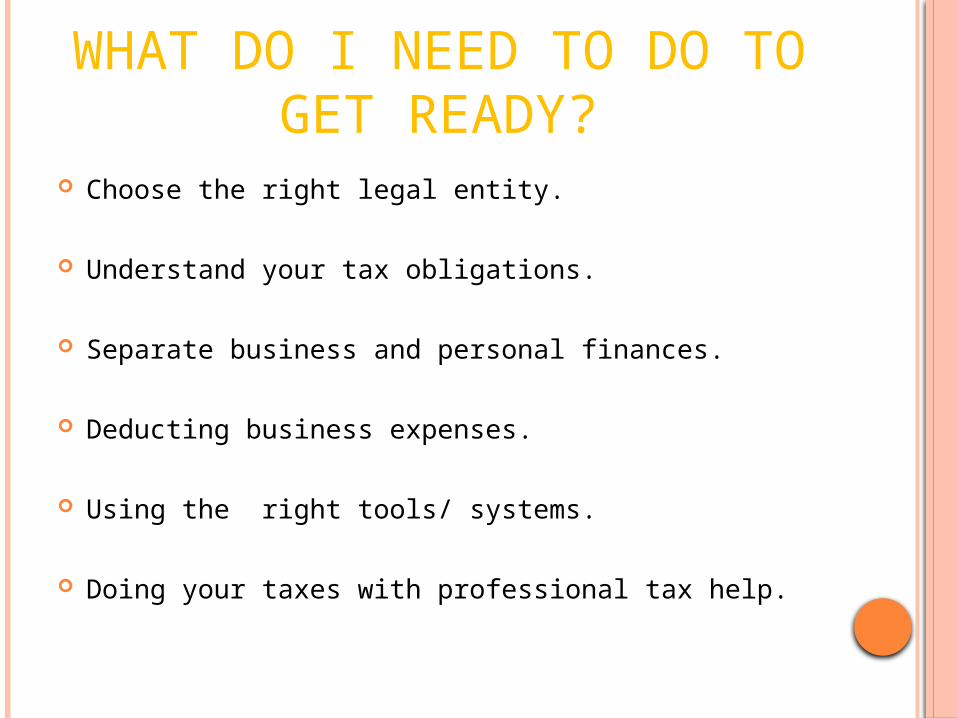

WHAT DO I NEED TO DO TO GET READY?

Choose the right legal entity.

Understand your tax obligations.

Separate business and personal finances.

Deducting business expenses.

Using the right tools/ systems.

Doing your taxes with professional tax help.

Thank You!

Any Questions?

Saiduddin & Co. 1st & 2nd Floor, Plot No-73C, Jami Commercial, 8th Street, Phase VII, DHA, Karachi