Unit 11.4 Double Entry AccountingTopic 4: Analysis of transactions

In Topic 4 we move on to analysing transactions, covering the Syllabus (p. 15): ‘Transaction analysis chart’. This Topic covers:• Using charts to analyse changes in transactions.• Preparing ledger accounts.• Using tables to prepare ledger accounts.• Differentiating between two ledger formats.• Using correct methods of balancing, in preparation for the Trial Balance.Analysis charts appear in template form.

Transactions take place daily in the lives of all businesses. No business stands still. The assets, liabilities and equity are always changing because of the transactions that are constantly occurring. This means that values in the accounting equation also change.

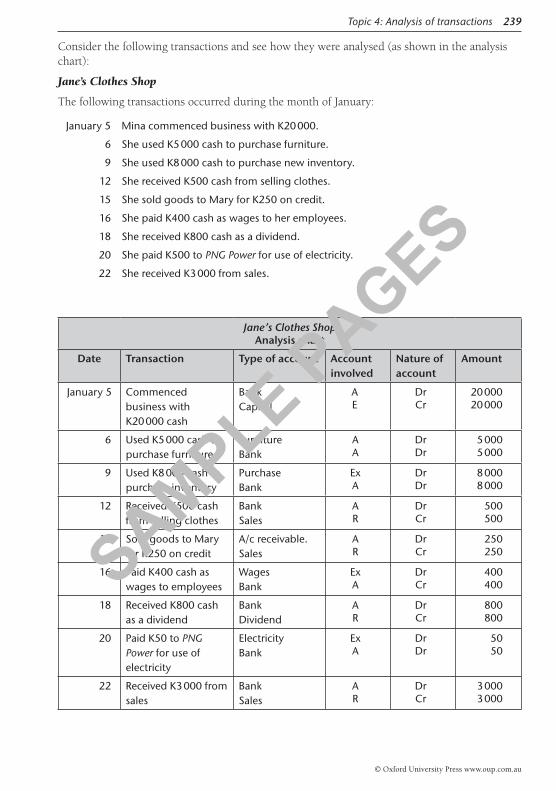

Transactions need to be recorded in the journals, analysed and posted to a ledger. We are studying the analysis of transactions because correct analysis is one of the most important processes in accounting. We will revisit the accounting rules to help us with analysis. We will use the analysis chart (see p. 259) to show our analysis.

How to analyse transactionsThe definition of a ‘transaction’ in accounting is an exchange of two things, but the accounting definition makes the assumption that the two things are of equal value; so for accounting purposes it is assumed that in any transaction the value received is equal to the value parted with.

The accounting definition is easiest to understand in terms of buying and selling, where the assumption is that the value of goods or services received is equal to the amount of cash given in exchange for those goods and services. It doesn’t matter if you think you have got a bargain, and gained more than you gave away; in accounting for the transaction, it is always assumed that the equal money value of the goods or services is equal to the cash paid in return. If you pay rent, for example, the accounting assumption is that the value of the rent to you is the same as the money you paid. In credit transactions, goods and services are received or given away while money is received or repaid later. Both situations represent transactions that must be recorded in the journals, analysed and posted.

To analyse transactions, we need to understand that each transaction has a double effect. We need to correctly identify this double effect in order to show it correctly in the analysis chart.

Example AEach of the following transactions has a double effect: a debit and a credit. Think about each transaction and identify the double effect of each one:a. Paying wages to employees.b. Receiving money from the sale of some goods.c. Paying for a telephone bill.d. Taking money as drawings from the business.e. Purchasing some goods on credit, to be sold.f. Paying for a transport service.g. Obtaining a loan from a bank.h. Receiving money for a service performed.

23_SAV_ACC11_78898_TXT_PPS.indd 237 12/08/13 9:44 AM

i. Making payments to repay a bank loan.j. Selling goods on credit.k. Receiving interest from the bank.Transactions a, b, e:a. Paying wages to employees is a transaction that has a double effect:

i. Wages are an expense, which has a debit nature. Expenses have been increased, so the debit side of the wages account is increased.

ii. Money would have been taken from the bank to pay wages to the employee and so the cash at bank, an asset, is decreased. The credit side of cash at bank has been decreased.

b. Receiving money from sales is a transaction that has a double effect:i. Sales – receiving money is revenue, which has a credit nature; the credit side of the

sales account is increased.ii. Money received was deposited into the bank account; cash at bank is an asset, so

the debit side of the cash at bank account is decreased.c. Purchasing goods on credit is a transaction that has a double effect:

i. Goods or stock purchased is an asset, which has a debit nature; the debit side of the inventory account is increased.

ii. The purchase of goods or stock on credit is a liability, which has a credit nature; the credit side of the credit purchased account is decreased.

So we can say that for every transaction, two accounts are involved. One of these accounts has a credit nature while the other has a debit nature. Discuss the other examples as a class with your teacher, and identify the double effect of each. Remember, when thinking about debits and credits, don’t think in terms of addition or subtraction – instead, think in terms of increases and decreases.

Unit 11.4 Activity 4A: The effects of transactionsIdentify and name the double effect for each of the following transactions:

1. Paying a telephone bill.

2. Taking money as drawings from the business.

3. Paying for a transport service.

4. Obtaining a loan from a bank.

5. Receiving money for a service performed.

6. Making payments to settle a bank loan.

7. Selling goods on credit.

8. Receiving cash from sales.

9. Purchasing furniture with cash.

10. Purchasing goods for resale on credit.

11. Taking goods from the business for your own use.

AnalysisAn analysis chart shows how a transaction is analysed and helps us determine the account to which it should be posted (whether as a debit and a credit) on ledgers.

23_SAV_ACC11_78898_TXT_PPS.indd 238 12/08/13 9:44 AM

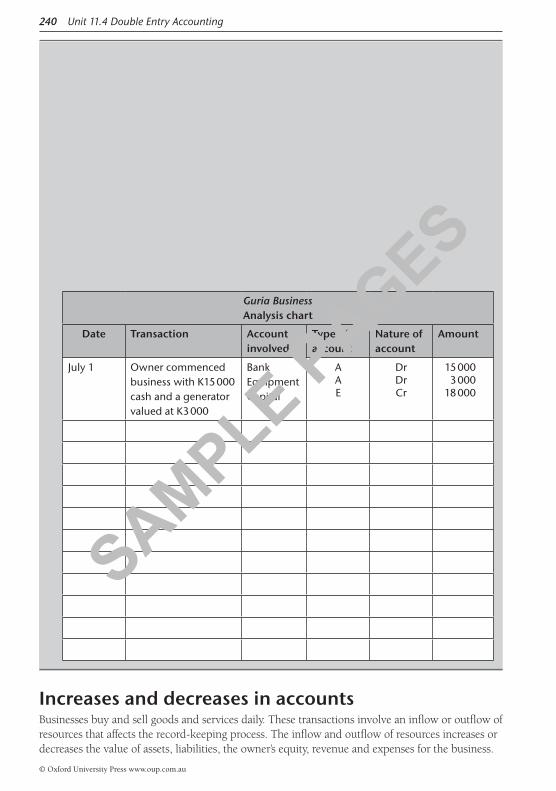

Unit 11.4 Activity 4B: Using the analysis chart1. Use the analysis chart shown below to show your analysis of the following transactions for

Guria Business for the month of July.

July 1 Owner commenced business with K15 000 cash and a generator valued at K3 000.

3 Used K3 000 cash to buy office furniture.

6 Used K5 000 cash to purchase stock.

10 Received K300 from the sale of goods.

13 Paid K400 cash as wages to employees.

17 Paid K200 for electricity.

20 Received K400 from the sale of goods.

23 Owner introduced further K5 000 cash into the business.

25 Purchased equipment for K2 500 with cash.

Guria Business Analysis chart

Date Transaction Account involved

Type of account

Nature of account

Amount

July 1 Owner commenced business with K15 000 cash and a generator valued at K3 000

BankEquipmentCapital

AAE

DrDrCr

15 0003 000

18 000

Increases and decreases in accountsBusinesses buy and sell goods and services daily. These transactions involve an inflow or outflow of resources that affects the record-keeping process. The inflow and outflow of resources increases or decreases the value of assets, liabilities, the owner’s equity, revenue and expenses for the business.

23_SAV_ACC11_78898_TXT_PPS.indd 240 12/08/13 9:44 AM

To analyse the performance of a business, all transactions need to be carefully recorded and correctly posted to journals and ledgers. There are several rules to remember, that will help you to correctly identify the account for a transaction and determine whether the account will be posted as a debit or credit on a ledger.

Rule 1: An increase to an account is recorded on the same side as the nature of the account.

Rule 2: A decrease to an account is recorded on the opposite side to the nature of the account

• An asset has a debit nature. If there is an increase in an asset account, then it is a debit.• A liability has a credit nature. If there is an increase in a liability account, then it is a credit.• An equity or proprietorship account has a credit nature. If there is an increase in the owner’s

equity account then it is a credit.• Revenue has a credit nature. If there is an increase in revenue then it is a credit.• An expense has a debit nature. If there is an increase in an expense then it is a credit.

• Assets have a debit nature. If there is a decrease in an asset account then it is a credit.• Liabilities have a credit nature. If there is a decrease in a liability account then it is a debit.• Equity or proprietorship has a credit nature. If there is a decrease in the owner’s equity

account then it is a debit.• Revenue has a credit nature. If there is a decrease in a revenue account then it is a debit.• Expense has a debit nature. If there is a decrease in an expense account then it is a credit.

The following tables summarise the above:

Table I

Account Increase Decrease

Assets Debit Credit

Liabilities Credit Debit

Equity or proprietorship Credit Debit

Revenue Credit Debit

Expenses Debit Credit

Table II

Account Debit Credit

Assets Increase Decrease

Liabilities Decrease Increase

Equity or proprietorship Decrease Increase

Revenue Decrease Increase

Expenses Increase Decrease

You need to be familiar with the above rules so that you can use them to analyse each transaction correctly and post it correctly to the ledger.

23_SAV_ACC11_78898_TXT_PPS.indd 241 12/08/13 9:44 AM

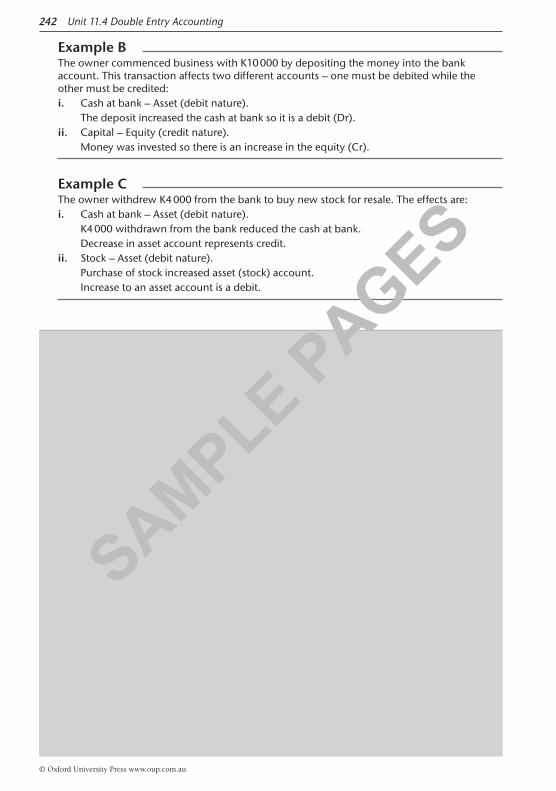

Example BThe owner commenced business with K10 000 by depositing the money into the bank account. This transaction affects two different accounts – one must be debited while the other must be credited:i. Cash at bank – Asset (debit nature).

The deposit increased the cash at bank so it is a debit (Dr).ii. Capital – Equity (credit nature).

Money was invested so there is an increase in the equity (Cr).

Example CThe owner withdrew K4 000 from the bank to buy new stock for resale. The effects are:i. Cash at bank – Asset (debit nature).

K4 000 withdrawn from the bank reduced the cash at bank.Decrease in asset account represents credit.

ii. Stock – Asset (debit nature).Purchase of stock increased asset (stock) account.Increase to an asset account is a debit.

Unit 11.4 Activity 4C: More about transactions1. Insert the correct words:

a. An asset has a ______________ ______________ nature.

b. A liability has a ______________ nature.

c. Owner’s equity has a ______________ nature.

d. Debit is always on the ______________ side.

e. Credit is always on the ______________ side.

f. An increase to an account is recorded on the ______________ side as the ______________ of the account.

g. A decrease to an account is recorded on the ______________ side to the ______________ of the account.

2. Following are some examples of increases and decreases in accounts. Write the account and state whether it is an increase or a decrease (the first two have been done for you):

a. A bank loan was obtained from the bank. Increase in liability.

b. Money was paid to the employees as fortnightly wages. Increase in expense.

c. A certain amount of money was withdrawn from the bank.

d. The business sold its furniture.

e. The business received a dividend.

f. The business purchased new furniture on credit.

g. The owner made a further investment.

h. The business paid cash wages to the employees.

i. The business received a discount on goods purchased with cash for resale.

j. The business purchased a computer on credit from Datec.

23_SAV_ACC11_78898_TXT_PPS.indd 242 12/08/13 9:44 AM

3. Show the two effects for each transaction in question 2 above (the first two have been done for you):

a. Bank loan

i. A bank loan is a liability and is a credit. The bank loan increases liability and is a credit (Cr).

ii. A bank loan obtains an increase in the cash at bank and is a Debit (Dr)

b. Money paid to the employees as fortnightly wages.

i. Wages are an expense and are a debit. Paying wages increases expenses – Asset (Dr).

ii. Money was withdrawn from the bank, leading to a decrease in the cash at bank (asset) and is a credit (Cr).

c. A certain amount of money was withdrawn from the bank.

d. The business sold its furniture.

e. The business received a dividend.

f. The business purchased new furniture on credit.

g. The owner made a further investment.

h. The business paid cash wages to the employees.

i. The business received a discount on goods purchased with cash for resale.

j. The business purchased a computer on credit from Datec.

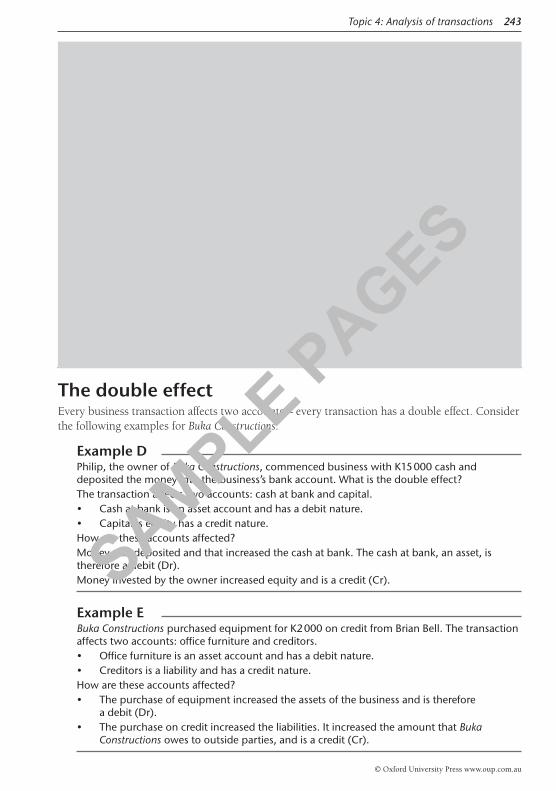

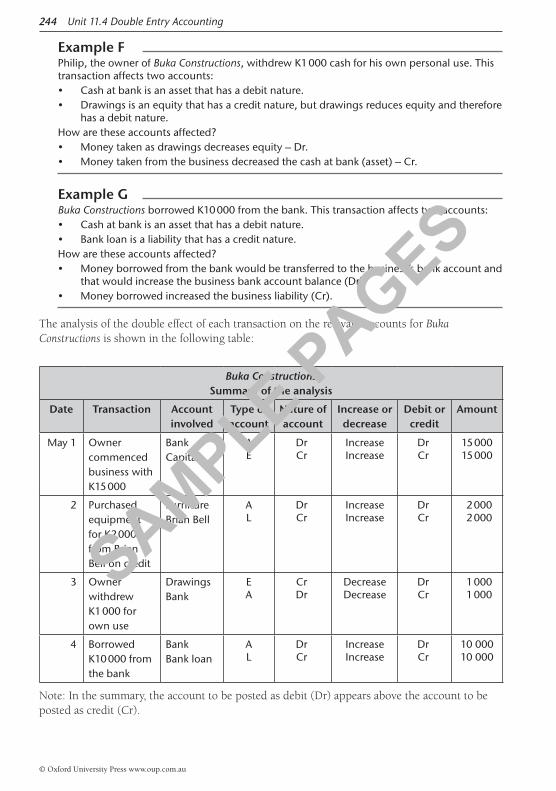

The double effectEvery business transaction affects two accounts – every transaction has a double effect. Consider the following examples for Buka Constructions.

Example DPhilip, the owner of Buka Constructions, commenced business with K15 000 cash and deposited the money into the business’s bank account. What is the double effect?The transaction affects two accounts: cash at bank and capital.• Cash at bank is an asset account and has a debit nature.• Capital is equity has a credit nature.How are these accounts affected?Money was deposited and that increased the cash at bank. The cash at bank, an asset, is therefore a debit (Dr).Money invested by the owner increased equity and is a credit (Cr).

Example EBuka Constructions purchased equipment for K2 000 on credit from Brian Bell. The transaction affects two accounts: office furniture and creditors.• Office furniture is an asset account and has a debit nature.• Creditors is a liability and has a credit nature.How are these accounts affected?• The purchase of equipment increased the assets of the business and is therefore

a debit (Dr).• The purchase on credit increased the liabilities. It increased the amount that Buka

Constructions owes to outside parties, and is a credit (Cr).

23_SAV_ACC11_78898_TXT_PPS.indd 243 12/08/13 9:44 AM

Example FPhilip, the owner of Buka Constructions, withdrew K1 000 cash for his own personal use. This transaction affects two accounts:• Cash at bank is an asset that has a debit nature.• Drawings is an equity that has a credit nature, but drawings reduces equity and therefore

has a debit nature.How are these accounts affected?• Money taken as drawings decreases equity – Dr.• Money taken from the business decreased the cash at bank (asset) – Cr.

Example GBuka Constructions borrowed K10 000 from the bank. This transaction affects two accounts:• Cash at bank is an asset that has a debit nature.• Bank loan is a liability that has a credit nature.How are these accounts affected?• Money borrowed from the bank would be transferred to the business’s bank account and

that would increase the business bank account balance (Dr).• Money borrowed increased the business liability (Cr).

The analysis of the double effect of each transaction on the relevant accounts for Buka Constructions is shown in the following table:

Buka Constructions Summary of the analysis

Date Transaction Account involved

Type of account

Nature of account

Increase or decrease

Debit or credit

Amount

May 1 Owner commenced business with K15 000

BankCapital

AE

DrCr

IncreaseIncrease

DrCr

15 00015 000

2 Purchased equipment for K2 000 from Brian Bell on credit

FurnitureBrian Bell

AL

DrCr

IncreaseIncrease

DrCr

2 0002 000

3 Owner withdrew K1 000 for own use

DrawingsBank

EA

CrDr

DecreaseDecrease

DrCr

1 0001 000

4 Borrowed K10 000 from the bank

BankBank loan

AL

DrCr

IncreaseIncrease

DrCr

10 00010 000

Note: In the summary, the account to be posted as debit (Dr) appears above the account to be posted as credit (Cr).

23_SAV_ACC11_78898_TXT_PPS.indd 244 12/08/13 9:44 AM

Further analysisHere are three different transactions for Wabag Stationery in the month of June, with an explanation for each one showing how it can be analysed.

June 15 Wabag Stationery purchased a computer for K3 200 on credit from Wabag Information Technology Services.

A computer is an asset; when purchased it increased Wabag Stationery’s assets.

It was bought on credit and that increased Wabag Stationery’s liabilities.

17 K200 interest was received.

The money was deposited and increased the cash at bank (asset).

Interest is revenue – interest received increases revenue.

18 The owner of Wabag Stationery invested a further K15 000 cash.

The K15 000 was paid into the bank that increased the cash at bank (asset).

The amount invested is capital that increased the owner’s equity.

21 The business paid K3 200 to settle its account with Wabag Information Technology Services.

Amount of K3200 paid to Wabag Information Technology Services decreased Wabag Stationery’s liabilities.

The amount of K3200 taken from the bank reduced cash at bank, which is an asset.

Wabag Stationery Summary of the analysis

Date Transactions Account involved

Type of account

Nature of account

Increase or decrease

Debit or

credit

Amount

June 15 Purchase computer for K3 200 on credit from Wabag Information Technology Services

ComputerWabag ITS

AL

DrCr

IncreaseIncrease

DrCr

3 2003 200

17 Received K200 interest

BankInterest

AR

DrCr

IncreaseIncrease

DrCr

200200

18 Owner invested further capital of K15 000 cash

BankCapital

AE

DrCr

IncreaseIncrease

DrCr

15 00015 000

21 Repaid K3 200 to settleaccount with Wabag ITS

Wabag ITSBank

LA

CrDr

DecreaseDecrease

DrCr

3 2003 200

Following is an analysis chart for the four transactions described above:

Note: In the summary, an account to be posted as a debit (Dr) appears above an account to be posted as a credit (Cr).

23_SAV_ACC11_78898_TXT_PPS.indd 245 12/08/13 9:44 AM

SummaryThere is a double effect to every business transaction: one account is debited while another is credited. This double entry system ensures that the accounting equation remains in balance. Accounts that have a debit nature are shown on the left of the ledger, while those that have a credit nature are shown on the right of the ledger.

The following questions can be used as guidelines for analysing transactions correctly:

1. Which two accounts are affected by the transaction?2. Are the accounts asset, liability or equity?3. Is the nature of the account involved Dr or Cr?4. Is the ledger increasing or decreasing?5. Which side of the ledger account is changing?6. What is the amount of this change?

Here are four different transactions for Oro Kai Bar for the month of June. Study the analysis chart and understand how each transaction was analysed.

June 4 Owner purchased furniture for K600 cash.

7 Business purchased furniture for K800 on credit from Lae Co.

10 Owner withdrew K600 cash for own use.

15 Business paid K500 cash as wages to employees

18 Business paid K180 cash for electricity.

Oro Kai Bar Analysis chart

Date Transactions Account involved

Type of account

Nature of account

Increase or decrease

Debit or credit

Amount

June 4 Bought furniture for K600 cash

FurnitureBank

AssetAsset

DrDr

IncreaseDecrease

DrCr

600600

23_SAV_ACC11_78898_TXT_PPS.indd 249 12/08/13 9:44 AM

Obtained equipment for K7 000 on lease from Mt Hagen Hardware Supplies Ltd

Equipment Asset Dr Increase Dr 7 0007 000

Revenue and expensesYou have learnt how to analyse transactions involving Balance Sheet items: assets, liabilities, equity and proprietorship. The purpose is to give you practice in analysing transactions, which are then ready for the next step in the process: posting onto the ledger.

Revenue and expenses are the next two elements that are part of the accounting process, but they are considered revenue statement items. Since revenue and expenses are accounts that are part of the accounting process, they are included in the accounting equation as such.

A + Ex = L + E + R

A = Assets These have a debit nature.Ex = Expenses

L = LiabilitiesThese have a credit nature.E = Equity

R = Revenue

Revenue: money received from the sale of goods or services and from other sources such as interest on funds deposited at the bank or on money lent to other people, and dividends received for being a shareholder.

23_SAV_ACC11_78898_TXT_PPS.indd 251 12/08/13 9:44 AM

Expenses: the costs involved in running the business. There is an outflow of charges and cash from the business to cover expenses; for example, purchases, wages, bank charges, advertising and insurance.

• Expenses accounts have a debit nature.• Revenue accounts have a credit nature.

The rules on increasing and decreasing accounts for assets, liabilities and equity or proprietorship also apply to both revenue accounts and expenses accounts.

• Increases to accounts are recorded on the same side as the nature of the account.• Decreases to accounts are recorded on the opposite side to the nature of the account.

Using the rules:

• An increase to an expense account is a debit.• A decrease to an expense account is a credit.• An increase to a revenue account is a credit.• A decrease to a revenue accounts is a debit.

Consider these transactions for Timas Trade Stoa that involve revenue or expense accounts:

June 4 Timas Trade Stoa sold goods and received K2 000.

June 12 Paid wages to employees for K500 cash.

Which two accounts are affected by each of these transactions?

June 4 i. Goods sold (ie sales) earn revenue. Sale increases revenue and is a credit.

ii. The money received would be deposited in the bank account; this would increase the cash at bank, which is an asset and is therefore a debit.

June 12 i. Wages (expenses). These increase expenses and are therefore a debit.

ii. Cash at bank (an asset). Money was taken from the bank; this decreased the cash at bank, which in turn reduced assets.

The above transactions are presented in the following analysis chart:

Timas Trade Stoa Analysis chart

Date Transaction Account involved

Type of account

Nature of account

Increase or decrease

Debit or credit

Amount

June 4 Sold goods worth K2 000

BankSales

AssetRevenue

DrCr

IncreaseIncrease

DrCr

2 0002 000

12 Paid wages to employees for K500

WagesBank

ExpenseAsset

DrDr

IncreaseDecrease

DrCr

500500

23_SAV_ACC11_78898_TXT_PPS.indd 252 12/08/13 9:44 AM

Unit 11.4 Activity 4F: Business accounts 1. These are various accounts for Highlands Coffee Exporters. Write each under its correct

heading as a Balance Sheet item or a Profit Statement item: a. Wages b. Rent c. Accounts payable d. Electricity e. Sales f. Cash at bank g. GST h. Interest i. Bank loan j. Inventory k. Purchases l. Equipment m. Interest on bank loan n. Drawings o. Bank overdraft p. Accounts receivable q. Advertising r. Bank charges s. Capital t. Dividend received u. Lease v. Investment – shares

Highlands Coffee Exporters

Balance sheet items Profit statement items

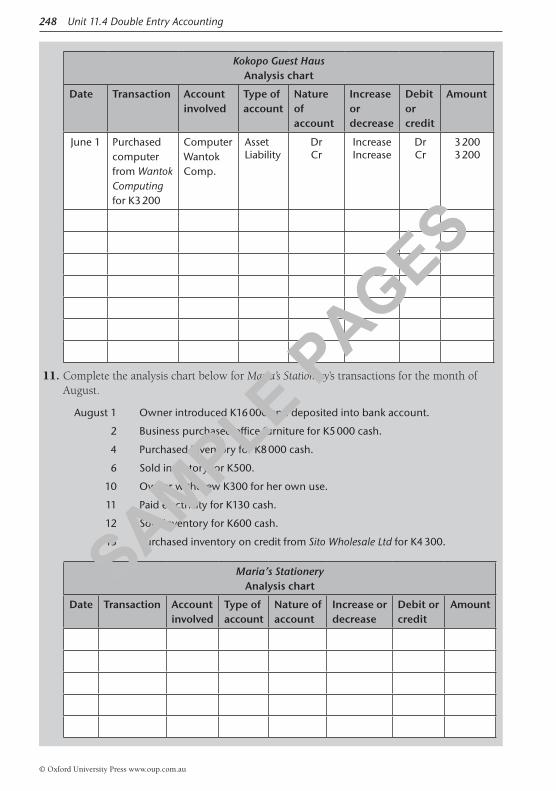

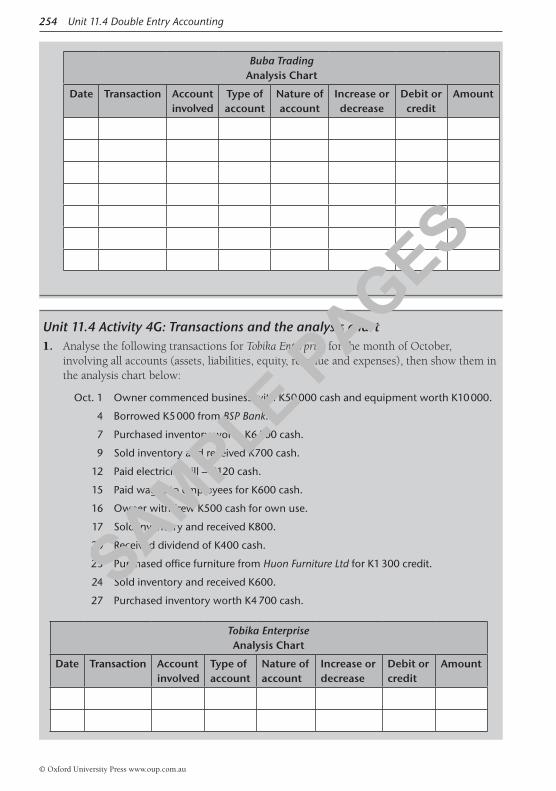

2. Analyse the following transactions for Buba Trading, involving all accounts (assets, liabilities, equity, revenue and expenses) for the month of May, then show them in the analysis chart below:

March 2 Sold goods and received K800.

3 Purchased new inventory for K2 500 cash.

7 Received dividend of K600 from Ok Tedi Mining.

12 Sold goods and received K1 200.

14 Paid wages to employees for K500.

15 Paid electricity for K200 cash.

16 Sold goods and received K1 000.

23_SAV_ACC11_78898_TXT_PPS.indd 253 12/08/13 9:44 AM

We have covered the main concepts in analysing transactions that involve all five accounting concepts. Now you should be able to use your skills to analyse transactions that satisfy the following equation:

Drawings is one of the proprietorship accounts. Proprietorship accounts have a credit nature. Since drawings decreases proprietorship or equity, it is a debit. That is why this account appears on the left-hand side of the equation.

Study the analysis below for Tobias Trading to help you to complete a similar exercise for Guria Trading (p. 258).

Below are transactions for Tobias Trading for the month of January. The analysis for these transactions is shown as an example on page 257.

January 3 Owner commenced business with K12 000 cash, which was deposited into bank account.

5 Borrowed K5 000 from the bank.

6 Purchased new stock for K9 500 on credit from Sito Wholesale.

7 Purchased new office furniture for K1 200 cash.

8 Purchased cash register on credit from Brian Bell for K1 300.

9 Sold inventory and received K500 cash.

10 Paid electricity bill – K80 cash.

11 Paid K120 cash for installing telephone.

15 Sold goods and received K1 000 cash.

23_SAV_ACC11_78898_TXT_PPS.indd 255 12/08/13 9:44 AM

20 Paid K9 500 cash to Sito Wholesale to settle account.

21 Purchased new stock on credit from Sito Trading for K2 400.

22 Business received K680 cash as dividend.

25 Sold goods for K260 to Jane on credit.

27 Page K600 cash as wages to employees.

28 Sold goods and received K1 600.

29 Petty cash for K100.

30 Repaid bank loan of K500 cash.

Owner took K2 000 cash from the business for his own use.

You should notice the following from the analysis:

• Any amount shown as an increase has a plus (+) sign.• Any amount shown as a decrease has minus (–) sign.• At the end of the month the amounts in each account are added or subtracted to determine

the balance for that account.• The totals of all the debit columns are added together to determine the total debit.• The totals of all the credit columns are added wholesale to determine the total credit:• This will show whether Debit (Dr) equals Credit (Cr).

23_SAV_ACC11_78898_TXT_PPS.indd 256 12/08/13 9:44 AM

Unit 11.4 Activity 4I: The analysis chart – Nambawan Klos Stoa1. Use the analysis Forms 3 & 4 to analyse the following transactions for Nambawan Klos Stoa

for the month of July:

July 1 Owner commenced business by introducing K14 000 cash.

2 Owner secured a bank loan for K6 000.

4 Purchased cash register for K1 200 cash.

5 Purchased new stock for K1 800 on credit from Pacific Imports Pty Ltd.

7 Sales K1 300.

9 Made part payment of rent K1 000.

12 Paid Telikom K199 for modem.

13 Sales of K1 000.

16 Further investment of K8 000.

18 Part payment to Pacific Imports Pty Ltd of K1 000.

21 Paid wages to employees – K800.

25 Sales – K2 700.

26 Drawings – K2 000 cash.

23_SAV_ACC11_78898_TXT_PPS.indd 260 12/08/13 9:44 AM

Unit 11.4 Activity 4J: Analysis of transactions – multiple choice1. Purchasing goods on credit for resale is a transaction that has a double effect. One of the

accounts is accounts payable. What is the other account?

A. Cash at bank.

B. Accounts receivable.

C. Stock (or inventory).

D. Expenses.

2. Tim received a dividend of K700 from his business. What is the double effect of this transaction?

A. Dividend and cash at bank.

B. Dividend and revenue.

C. Dividend and expense.

D. Cash at bank and equity.

3. A business made a cash payment to the Post Courier to run an advertisement in the newspaper. The transaction has a double effect; one of the accounts is cash at bank. What is the other account?

A. Accounts payable – Post Courier.B. Accounts receivable – Post Courier.C. Expenses – advertising.

D. Liabilities – advertising.

4. Which of the following represents a debit?

A. Increase in liability.

B. Increase in equity.

C. Decrease in expense.

D. Decrease in revenue.

5. Which of the following represents a debit?

A. Decrease in expenses.

B. Increase in assets.

C. Increase in revenue.

D. Increase in equity.

6. Jane made a payment of K400 to PNG Power for the use of electricity by her business. The transaction has a double effect. Identify the accounts and answers for a. and b.:

a. Which account would be posted as a credit?

A. Electricity for K400.B. Cash at bank for K400.

C. Inventory for K400.

D. Drawings for K400.

b. Which account would be posted as a debit?

A. Electricity for K400.B. Cash at bank for K400.

C. Inventory for K400.

D. Drawings for K400.

23_SAV_ACC11_78898_TXT_PPS.indd 262 12/08/13 9:44 AM