69

SAIA Consumer Education Projects Report: 2012/13 February 2014 # 112957

SAIA Consumer Education

Projects Report: 2012/13 February 2014

# 112957

Page | 2

Table of Content

1 Executive Summary ........................................................................................... 3

2 Introduction ........................................................................................................ 5 2.1 SAIA Consumer Education Strategy ............................................................. 5 2.2 SAIA Consumer Financial Education Programme Guidelines ....................... 6 2.3 Financial Sector Code ................................................................................... 9

3 2012/13 SAIA Consumer Education Initiative ................................................ 11 3.1 Teacher Development (iCount) Project ....................................................... 11 3.2 Community Radio Project............................................................................ 12

3.3 Funding ....................................................................................................... 13

4 Teacher Development (iCount) Project .......................................................... 14

4.1 The Project .................................................................................................. 14 4.2 The Research .............................................................................................. 18

4.3 The Research Findings ............................................................................... 21 4.4 Recommendations ...................................................................................... 51

5 Community Radio Project ............................................................................... 54 5.1 The Project .................................................................................................. 54 5.2 Project Background ..................................................................................... 54 5.3 The Project Context .................................................................................... 57

5.4 The Research .............................................................................................. 59

6 Project Impact (Ukhozi FM) ............................................................................. 61 6.1 Profile of Participants .................................................................................. 61

6.2 Main Findings .............................................................................................. 61 6.3 Conclusions................................................................................................. 63 6.4 Recommendations (Ukhozi FM) .................................................................. 63

7 Radio Sonder Grense (RSG) ........................................................................... 64 7.1 Findings ...................................................................................................... 64

7.2 Measurement of Radio Audience for RSG .................................................. 68 7.3 Recommendations (RSG FM) ..................................................................... 69

Page | 3

1 Executive Summary

Since the inception of the SAIA Consumer Education initiative in 2004, over R60

million has been spent on various consumer education projects aimed at creating

awareness on the importance of financial management as well as to increase the

consumers’ understanding of financial services and products. The SAIA Consumer

Education Initiative is considered to be one of the best industry-led initiatives that are

making a difference in the lives of South African consumers, particularly in the low-

income market. The initiative’s success is attributed to the commitment of SAIA

members, who even before the Financial Sector Code (FSC) was gazetted,

voluntarily contributed funds in recognition of the initiative’s its importance as a social

and business imperative.

For the 2012/13 SAIA Consumer Education Initiative, three projects were

implemented namely; The Teacher Development Project (iCount), Managing Your

Money (MYM) and the Radio Financial Literacy Project. As stipulated in the FSC

guidelines, all consumer financial education projects must be monitored and

evaluated for impact analysis. This was done through a baseline and endline survey

for both the Teacher Development and the Radio Financial Literacy Projects during

the campaign.

With regard to the MYM project, there was no impact study conducted during or after

the project, as this was a revision exercise for previous MYM material produced in

2008 for Grades 10, 11 and 12 for Maths Literacy teachers. The SAIA had partnered

with the Financial Services Board (FSB) on the MYM project in 2008 and due to its

success; the FSB requested that the material be revised to align it with the new

curriculum referred to as the Curriculum Assessment Policy Statement (CAPS),

introduced in schools in 2013. The material was revised by service provider, Bright

Media in consultation with officials from the Department of Basic Education. A total of

600 MYM resource files were printed and distributed to the provincial Heads of

Mathematical Literacy in all nine provinces to be used in schools.

In terms of the Teacher Development Project, this was a continuation of the 2011/12

iCount project, which focused on training Accounting subject school teachers in

Grade 10. This project was initially implemented at the request of the national

Department of Education (DBE) who had previously endorsed the MYM project, as

part of the Economic and Management Sciences (EMS) subjects for Grades 10 to

12. Due to the success of the iCount project in 2012, and for continuation purposes,

a decision was made to continue with the iCount project in 2013/14, focusing on

Grades 11 and 12. In this campaign, a total of 1,768 were trained through workshops

Page | 4

to teach learners the Accounting subject using material that was specifically

produced for them.

For the Radio Financial Literacy project, this was rolled out on two SABC Public

Broadcast Service (PBS) radio stations, namely; Radio Sonder Grense (RSG), which

broadcasts in Afrikaans and Ukhozi FM, which broadcasts in isiZulu. This project

entailed a 26 episode radio drama series in both languages, aimed at creating

awareness of financial products and services, the management of finances through

budgeting and saving, as well as to change behaviours and attitudes of consumers

with regard to financial management. Live call-in sessions were held after the

broadcast of each episode on both radio stations. With this interactive segment of

the project, voluntary experts drawn from SAIA member companies who were

proficient in Afrikaans and/or iSizulu participated in the call-in sessions to engage

with listeners and to answer questions. In total, the Radio project reached over two

million listeners (1, 86 million on Ukhozi FM and 155,000 on RSG).

The evaluations of both projects reveal that they were not only well received by the

intended audiences, but that there was also significant improvement in the

knowledge, understanding and change in attitude of the respondents. With regard to

the iCount project, teachers who attended the training workshops as well as their

learners said that the content was useful, particularly the inclusion of financial

literacy into the Accounting subject.

Similarly with the Radio Financial Literacy project, there was keen interest from

Ukhozi FM listeners, with respondents of the impact study recalling the content of the

episodes and making an effort to change how they manage their finances and risk. It

was revealed though that some respondents to the survey, particularly males, were

not happy with the programme’s timeslot as this was during the day when they did

not have access to the radio. A recommendation has been made to take cognisance

of that should we implement a similar project in the future.

With regard to RSG, the baseline survey initially revealed a negative response to the

programme, which necessitated a mid-term study to find out what the issue was. It

was noted that a significant number of RSG’s listeners were in the upper LSMs and

therefore did not find the information engaging. To rectify this, the service provider

worked closely with the SABC to develop programmes around the central drama to

reflect the needs of the listener base. This worked very well and the endline survey

reflected positive responses. However, these need to be considered in light of the

adjusted proportion of the upper LSM respondents.

Page | 5

2 Introduction

Consumer financial education continues to play a pivotal role in creating awareness

about sound financial management as well as in increasing consumer knowledge

and understanding of financial products and services. In the last few years, there has

been an increased focus on consumer financial education in light of the global

economic crisis, which left many people financially distressed. This, together with the

ever increasing financial choices that consumers have to make, the need for

knowledge to make informed decisions about their finances and lifestyles has

become even more relevant for consumers.

A recent national financial literacy survey conducted by the Human Sciences

Research Council (HSRC) indicates that many South Africans, particularly in the low-

income market make poor financial decisions due to a lack of financial management

skills, and continuously find themselves in the proverbial debt trap and the perpetual

cycle of poverty. Further exacerbating this problem is the lack of understanding of

the importance of risk management as an important pillar of financial management. It

is against this background that the South African Insurance Association (SAIA) has

since 2005 embarked on consumer education projects on behalf of the short-term

insurance industry.

Although members initially participated in the SAIA Consumer Education Initiative on

a voluntary basis, in 2009 the SAIA drafted a Consumer Education Strategy and

Guidelines, making it mandatory for members to contribute to the industry consumer

education project. This ensured that the collaborative initiative would continue

regardless of the Financial Sector Charter (now referred to as the Financial Sector

Code) being gazetted or not. For an update on the Financial Sector Code (FSC)

please see page 7 of this report.

2.1 SAIA Consumer Education Strategy

In terms of the strategy, participation in consumer education is a SAIA membership requirement.

All SAIA members are required to spend 0.2% of after tax profits on consumer education in the low-income market. (This percentage has since been revised following the gazetting of the FSC) to 0.4%.

A minimum of 0.1% (i.e. half of the 0.2% requirement) must be contributed to the SAIA industry initiative. The funds in this pool will be used by SAIA for generic consumer education, with an emphasis on short-term insurance.

Page | 6

SAIA members that wish to spend their remaining 0.1% on their own projects may do so.

SAIA members that do not wish to implement their own consumer education projects may contribute the full 0.2% to the SAIA industry initiative.

The SAIA will spend these funds in such a way that members will receive their points for consumer education on the FSC scorecard..

SAIA members that form part of conglomerate groups may choose to spend their 0.2% together with the other companies in their group. All spend should adhere to the SAIA Consumer Education standards and guidelines.

Such spend should be reported to the SAIA.

SAIA members that are granted exemption for the Access pillar in the Financial Sector Code may apply the SAIA membership requirement to spend the 0.2% of the after tax profits on consumer education.

Consumer education policies and guidelines should either be included in the general SAIA Code of Good Business Practice, or a Code for Consumer Education should be drafted.

2.2 SAIA Consumer Financial Education Programme Guidelines

The SAIA Consumer Education guidelines are premised on the definition of

financial education as defined by the Organisation for Economic Co-operation

and Development (OECD) as well as the FSC Consumer Education Standards.

This definition is also used by the industry’s regulator, the Financial Services

Board (FSB). According to the OECD, financial education is “the process by

which financial consumers/investors improve their understanding of financial

products, concepts and risks and, through information, instruction and/or

objective advice, develop the skills and confidence to become more aware of

financial risks and opportunities, to make informed choices, to know where to

go for help, and to take other effective actions to improve their financial well-

being”. Financial education therefore includes improving the levels of

knowledge, skills and attitudes that will lead to behaviour change.

Page | 7

Principles Providing financial education to consumers should form part of a financial

institution’s good governance and business practice in respect of their

relationship with their clients. This would include providing information,

appropriate disclosure and appropriate advice at point of sale according to any

relevant legislation, regulation and/or good practice, but also creating financially

aware and literate clients in the long term. The other principles are as follows:

Financial education should be provided in a fair and unbiased manner

and be non-discriminatory.

Programmes should be co-ordinated and fit into a sector and/or national

programme. Therefore, programmes should take cognisance of the

national consumer financial education framework / strategy as approved

by the FSB, and should seek to fit into this overall strategy. In addition,

programmes should seek to fit into the sector initiative and follow the

SAIA guidelines and FSC Standards.

Financial education programmes should provide context. For example,

should the target audience fall under the low income category and have

low levels of education, basic financial principles such as budgeting,

saving etc should provide a starting point. General principles regarding

insurance and specifically short-term insurance should provide the back-

drop for product information.

Financial education should be seen as a long-term commitment,

although short-term outcomes may be the starting point of a programme.

It should be seen as a continuous, on-going commitment towards clients

and potential clients.

Financial education programmes should be designed to meet the needs

of the target market and should take into account the general literacy

and financial literacy levels of the target market.

Financial education programmes and the outcomes of these

programmes should be shared at a general level in terms of the SAIA

requirements as well as a national framework or strategy to prevent

duplication and encourage learning.

Page | 8

Good Practices

Financial education programmes should be holistic, comprehensive and complementary.

Financial education could include generic financial literacy concepts, generic short-term insurance financial literacy concepts as well as general product information.

Objective information on risks and products and how these relate to the

needs of different target audiences should be encouraged.

A clear distinction should be made between financial education and

commercial information. Commercial financial information should be

disclosed as such and must fall outside of the consumer education spend

required by the SAIA of its members.

Financial education should be appropriate. The target audience should be

identified clearly. The message, content and delivery mechanisms used

should be aligned to the target audience. Information or education

provided should be simple and understandable. In South Africa, such

education should preferably be provided in the language/s best

understood by the target audience.

Financial education should have specific objectives.

Financial education should be monitored and assessed to ensure

appropriateness and impact.

Financial education should, if at all possible, attempt to create a link

between the consumer financial education and increased access to

financial services products.

Page | 9

2.3 Financial Sector Code

After a decade of protracted negotiations, the Financial Sector Code (previously

referred to as the Charter) was finally gazetted in November 2012 and was

officially launched to the financial sector in July 2013. However, the SAIA had

since inception of the consumer education initiative adhered to the FSC

consumer education requirements even when the Code was not in place.

This ensured that SAIA members would qualify for the points for consumer

education spend regardless of the Code being gazetted. New FSC standards

for consumer education have been agreed. Changes worth noting in the

consumer education standards include the following:

Target market:

The target market will include individuals earning less than R180,000 per

annum and 25% of funding should be used to reach rural areas.

New definitions:

‘Face-to-face’ initiatives have been replaced with ‘interactive’ initiatives

and can now also include other types of projects such as media projects

provided that interaction is possible between the target audience and the

facilitator.

‘Awareness’ projects will provide only basic information and will now be

strictly related to awareness creation only.

Funding percentage splits between different types of initiatives:

Up to 100% of funds can be spent on interactive projects and awareness

projects are capped at 40%.

The requirement for the financial sector to spend 0.2% of after tax profits on

consumer education has been increased to 0.25% for 2012. This percentage

will increase to 0.3% for 2013 and 0.4% for 2014. Strict requirements regarding

monitoring and evaluation, impact measurement as well as branding now form

part of the new FSC Consumer Education standards.

Page | 10

When considering projects for the 2012/13 consumer education initiative, the

Code was not yet in effect, however the following FSC Consumer Education

standards were taken into account.

Physical accessibility: Consumer education initiatives and

programmes must be offered and made available to all consumers of

FSC products and services at points of service or transaction.

Appropriateness: Consumer education initiatives and programmes

must meet the identified needs of consumers in the FSC target groups

with the aim of achieving the Code’s access goals. The outcomes of

FSC consumer education programmes must be measurable and be able

to contribute to the achievement of scoring points. Consumer education

must enable consumers to make more informed decisions about their

finances and lifestyles.

Affordability: Consumer education must be offered free of charge to the

consumer.

Simplicity: Consumer education initiatives and programmes must meet

the identified needs of consumers in the target groups with the aim of

achieving the Code’s Access goals. All consumer education materials

must meet the Code’s criteria for simplicity, being able to understand

and disclosure.

Non-discrimination: Consumer education materials must be freely

available in all languages. Suppliers must meet the FSC’s service

provider accreditation and BEE procurement criteria.

Page | 11

3 2012/13 SAIA Consumer Education Initiative

The mix of projects for the 2012/13 SAIA Consumer Education Initiative is a

continuation of the previous year’s projects. Due to the success of these projects and

to maintain consistency, a decision was made to continue with the Teacher

Development (iCount) project and the Radio Financial Literacy project. A request

was also made by the FSB to revise the Managing Your Money (MYM) material in

line with the Curriculum Assessment Policy Statement (CAPS). As this was just a

revision of material exercise, no impact study was conducted.

In the previous initiatives, the three projects addressed the financial skills gap in the

Living Standard Measurement (LSM) 1-8 as per the FSC requirement and also

enabled SAIA members to obtain points in accordance with the Code.

3.1 Teacher Development (iCount) Project

In 2011, the national Department of Basic Education (DBE) requested that the

schools’ project change focus from the Economic Management Sciences

(EMS) subjects previously done in 2010/11 and target the Accounting subject in

Grades 10 to 12. This intervention was initiated due to the lack of support for

Accounting at schools and based on the successful track record of Managing

your Money project for Mathematical Literacy.

The first phase of the iCount project was successfully implemented in the

2011/12 consumer education initiative in Grade 10. 2012/13 saw the

implementation of the second phase in Grades 10, 11 and 12 reaching over

69% of all teachers of the Accounting subject in the nine provinces. Lower LSM

consumers were targeted, and the profile of the recipients was aligned to the

Code’s requirements of over 70% Black.

The SAIA Consumer Education intervention in schools has an extensive track

record of success and impact and is one of the few government-industry

collaborations that make a demonstrable difference in content knowledge,

financial literacy indicators, classroom method and the use of the resources

provided. The resources content is aligned to the national curriculum financial

capability content. The service provider, Bright Media developed simple, clear,

educational materials through a collaborative process, with DBE officials being

involved at all levels.

Page | 12

3.2 Community Radio Project

The Radio Financial Literacy project which has proven successful over the last

three years was again implemented in the 2012/13 SAIA consumer education

initiative. The project is aimed at improving consumer knowledge, skills, and

attitudes and to develop behaviours which show critical and selective

engagement with financial products and to build the required knowledge to be

good life and risk managers. The financial education was delivered through a

radio “soap” drama programme on two public broadcast stations (RSG and

Ukhozi FM) through a series of 26 episodes on each station. Each episode was

followed immediately by a live call-in session with a topical short-term

insurance expert. The radio drama, as well as the follow up programme was

broadcast in Afrikaans and isiZulu, the languages of the respective radio

stations.

The anticipation was that the above mix of project would derive the

following results:

Measurable impact across a broad constituency.

Ability to reinforce education concepts applied in existing projects and to

expand consumer education to provide more focus on short-term

insurance product education.

Easy extension of the target market from Living Standards Measures

(LSM) 1-5 to include LSM 1- 8.

Building of relationships with existing suppliers with proven track records

for good delivery.

Managing Your Money (MYM) Project

The Managing Your Money project was a revision of previous MYM material in line with the Curriculum Assessment Policy Statement (CAPS), which was introduced in schools in 2013. The request to revise the material was made by the FSB who had partnered with the SAIA in a previous campaign. There was no impact study conducted for the MYM as the project was a revision of material exercise.

Page | 13

3.3 Funding

The final budget for the 2012/13 consumer education initiative was

R11 938 442,78. The total budget was made up of the pledged amount of

R9 895,879 from members, R900, 000 contributed by the FSB and R1 142, 563

from additional funds available from the previous year’s campaign interest.

The following funding proposal was approved.

Projects

Teacher Development (iCount) Project

SAIA funds R 6 805 087,07

Radio Financial Literacy Project

SAIA Funds R 2 566 595,00

FSB funds R 500 000,00

Managing Your Money

SAIA funds R 433 955,14

FSB funds R 400 000,00

Total expenditure R 10 705 637,21

The balance of R1 232 805,59 was added to the 2013/14 SAIA Consumer Education

campaign, including the accumulated interest.

Page | 14

4 Teacher Development (iCount) Project

4.1 The Project

The iCount project was first implemented in 2012 for Grade 10 learners

following a request by the Department of Basic Education (DBE) who had

identified Accounting as an area needing intervention. Due to its success and

for continuity reasons, the project was rolled out to Grades 11 and 12 in 2013.

A total of 1,768 teachers were trained in 2013 in all provinces through

workshops, bringing the total number of teachers who had undergone the

training (including those who trained in 2012) to 3,645.

Training Material

Each teacher received specialised training as well as a ready-to-use resource

pack for Accounting in Grades 10, 11 and 12. The Curriculum Assessment

Policy Statement (CAPS) aligned Grade 10 material was included in the pack to

ensure continuity in lessons. Two DVDs with 13 episodes each of Accounting

material was also given to the teachers. The full training resource pack

contained three high quality books of 56 colour pages each and two posters.

Accounting resources for teachers and learners

A total of 8,000 iCount resource files were printed and 8,000 DVD double packs

containing 26 episodes of Accounting material were delivered to the provinces.

These files contained 27,000 books based on the curriculum for Accounting

and teaching Financial Literacy. The files were distributed in classrooms of

schools most in need, as identified by the DBE.

Each resource file was professionally developed, published and printed to

contain the following elements:

One Grade 10 full colour resource book of 56 pages, aligned to the

CAPS document for Accounting.

One Grade 11 full colour resource book of 56 pages, aligned to the

CAPS document for Accounting.

One Grade 12 full colour resource book of 56 pages, aligned to the

CAPS document for Accounting.

Page | 15

One A2 sized poster, printed in full colour on the front reflecting the

Generally Accepted Accounting Principles (GAAP) with additional

Accounting terminology on the reverse side, as well as summaries of all

26 iCount episodes.

One A2 sized poster, printed in full colour on the front reflecting the

Steps to Financial Literacy principles, which are the core financial

capability indicators, expressed clearly in useable steps for learners and

teachers.

Two DVD disks in a pouch, which slots into the resource file, containing

all 26 of the iCount television episodes which include animation, live

action sequences with actors of 23 minutes in duration each – for use on

a computer or in a DVD machine. In addition, the DVD contains the

booklets in printable PDF format, the resources mentioned by the

curriculum such as the King Report and other resources for use in the

classroom.

The Adult Financial Capability Framework was used to develop the content,

reflecting the process model, including three broad elements of financial

capability, i.e. financial knowledge and understanding, financial skills and

competence, and financial responsibility. Quantitative and qualitative research

was conducted to assess the relevance, reach and impact of the project on

both financial capability and usefulness for the Accounting classroom.

Face to Face Workshops - Training in the nine (9) provinces:

Forty-four (44) teacher training workshops were successfully hosted (two

more than the contracted 42 workshops) reaching 1,768 educators in all

nine provinces.

The teachers were provided with resources to implement the iCount

project with their learners in classrooms.

This number was achieved despite the SADTU go-slow and strike action

at this time. Contingency plans were implemented and 10 workshops

were postponed and completed.

Page | 16

The workshop schedule was designed for each province ensuring that

reach and target audience of the project covered areas and schools

where the most need was, i.e. taking accounting learner performance

into consideration as well as alignment with any existing development

projects or programs such as the 'Underperforming Schools Project',

which were currently running in the provinces.

Nine meetings were held with provincial officials to discuss each

province's unique CAPS implementation plan and the alignment of the

SAIA Schools Project with this.

The date, time and venue for the workshops were discussed and

finalised once it was established which districts and/or schools would

participate.

The Educational District Officials also attended the workshops together

with accounting teachers. All iCount workshops were both opened and

closed by the relevant District Officials for the areas.

An iCount, audio visual DVD, episode was screened using a data

projector at 95% of the training workshops. The remaining 5% were

negatively affected by the lack of electricity or unforeseeable problems,

which could not be resolved.

Achievements

Developing financial literacy content for schools, publishing and printing 26,000

books in 8,000 files, organising a total of 44 workshops, which were

successfully conducted in all nine provinces during the first two school terms of

2013 summarises the project’s achievement.

A total of 1,768 attendees took part in the Accounting workshops. This

figure was attained despite two disruptive elements, namely the national

SADTU go-slow and strikes in the Eastern Cape, which took place

simultaneously. Due to constant monitoring of the media as well as

direct contact with the provincial Accounting co-ordinators, the situation

was monitored and the necessary contingency plans were implemented.

All workshop attendees filled out an evaluation form on completion of

each workshop. An independent research company conducted pre- and

post-intervention interviews with attendees. This qualitative and

Page | 17

quantitative information was data captured and analysed for insertion in

this final report.

All aspects of the training received a high majority rating of either

‘Excellent’ or ‘Good’, averaging out to an overall rating of ‘92% by all

attendees, for all aspects of the training. When including the ‘Average’

rating, 99% of all training delegates rated all aspects of the training as

between ‘Average’ – ‘Excellent’. This is a very positive aspect of the

training analysis as adult training is a much specialised field of expertise

due to the complex nature and varied expectations of trainees,

especially in the intricate field of education.

An overwhelmingly positive response has been received at provincial,

district and teacher level. Positive emails, telephone calls and SMS

messages poured in from the teachers on completion of the project.

A very important, achievement of this project is the potential reach that

each trained and resourced teacher has to improve the quality of their

learners’ educational experience. This reach covers both the in-class

experience through Accounting as well as the learners’ general financial

literacy to equip them to be better-informed consumers. Statistically, if

each trained teacher reaches an average of 50 – 60 Accounting learners

then 88,400 – 106,080 learners would have been reached through this

phase of the iCount project.

With CAPS training rolling out during the mid-year school holidays

(June/July) within most provinces, the teachers were excited to be in

possession of their first CAPS aligned resource. They also indicated that

they were less intimidated by the CAPS roll-out after experiencing the

lesson demonstration activities during the workshop as it made them feel

more at ease with CAPS and its implementation. The fact that the iCount

resource is CAPS aligned increases the likelihood of it being used in the

classroom as the teachers currently do not have any CAPS aligned

materials and they expressed their enthusiasm to use the iCount

materials as they now feel comfortable with the contents thereof.

Page | 18

Multimedia

The written and printed content was supplemented by audio-visual

content (episodes) in a multimedia pack, which was very well received.

Innovation

Two Knowledge Boxes were launched - one in in Gauteng, which was installed

at the Sci-bono Discovery Centre in Newtown, Johannesburg. A second one

was installed in Mthunzini in KwaZulu Natal. The Knowledge Box is an

interactive tool which teachers can use to receive updated resources by using a

USB memory stick, a memory card or a cell phone with Bluetooth to link to the

Knowledge Box. Using the high-tech touch screen, teachers browse through

valuable resources such as past exam papers, policy documents, lesson plans,

worksheets and the complete range of iCount resource books as well as the 26

multi-media episodes for Accounting teachers. These resources are updated on

a regular basis.

4.2 The Research

Objectives

The overall objective of the project was to evaluate the attitude of educators

and learners who had not been exposed to the iCount training workshop with a

view to conducting a future measurement of the impact, amongst educators

and learners who had recently been exposed to the iCount training.

Further objectives were to establish:

Initial evaluation of the learners’ own levels of financial literacy in terms

of their current level of knowledge, awareness, skills and impact of what

they have acquired in terms of financial literacy to date;

Evaluation of learner reaction to the training of their educators, both prior

and post the training received, positive and negative aspects;

Ascertain improved level of awareness and knowledge amongst learners

after their educators had been trained;

Page | 19

Determine response of learners to the educators who have been through

the training on the difference the learners now experience in their

understanding of financial literacy;

Identification of gaps in the training and recommendations for the future

of such programmes, focusing also on areas which learners feel that the

programme missed or areas where they feel they are lacking in terms of

financial literacy.

Develop a benchmark figure of a pre-workshop level of understanding of

accountancy principles against a first stage monitoring and evaluation

after one term’s work amongst learners whose educators had attended

the iCount workshops.

Overall Approach

The approach encompassed both a qualitative discussion with educators and

learners prior to the implementation of the training and educators attending the

training workshops. Learners in selected schools also completed quantitative

questionnaires to provide a baseline against which a second post training

impact study could be measured. In addition a control group of learners who

had not been taught by the trained educators was included in the study. The

study was conducted in Gauteng, amongst schools where educators had not

previously been trained on the iCount project, as well as in a control school

where educators were not trained at all.

Two training workshops were held in June 2013, one in Randfontein and one in

Dale Park, where about thirty educators completed the questionnaire in each

area. From amongst these educators, two schools were selected in each area

for participation in the study and fifty questionnaires were delivered to each

school. Ultimately three schools completed the questionnaires. Also included in

the study was a control school from the same area in Randfontein, so as to

provide a comparison of like with like in terms of learner background, etc. The

training was conducted just prior to the school holidays so the questionnaires

and the focus groups were conducted with students who were present doing

exams, mainly the Grade 12 pupils. The questionnaire was a self-completion

questionnaire, which was easy and quick to complete in order not to interfere

with the school day unduly.

Page | 20

Qualitative Stage

Two focus group discussions were held in June 2013 with educators, one in

Randfontein and one in Dale Park in Gauteng. Focus groups were held with

learners at three schools where educators had been trained and with learners

in a control school where the educators had received no iCount training.

Educators and learners at the workshops and at the selected participating

schools also completed a pre-training questionnaire.

All educators attending the training workshops were asked to complete a short

quantitative questionnaire. In each workshop, two educators were asked if they

would facilitate a quantitative study amongst their learners and an additional

control school, where no educator had received the iCount training. The

questionnaire was distributed amongst learners for a self-completion exercise.

This study forms the baseline, capturing information from educators and

learners prior to the educators receiving the training and prior to them providing

any input to the learners. The comparison is between user and non-user

schools and another endline study could be conducted amongst the same

educators and learners after the end of the third term. This is a further impact

study, and even beyond this, the matric results could be a further measure of

impact and change in knowledge skill and attitude. Each of the 1,768 attendees

of the workshops provided written assessment of the project, which was data

captured and analysed as part of the monitoring and evaluation.

Timing

The study was conducted in June 2013 with the non-trained school interviews

being conducted in July 2013.

Page | 21

The Research Findings

Research Limitations

Due to strike action, the timing for this study was very close to the exams and

school holidays so although it was possible to distribute the questionnaires to

the educators at the workshop for the learners to complete; only the Grade 12

learners were at school to complete this questionnaire. However this does

provide a unique opportunity to compare the matric results for these schools

when the results are available, to provide an additional layer of analysis of the

impact of the training. Of the four schools selected, only three managed to get

the learners to complete the questionnaires in time. It has been envisaged that

150 interviews would be completed with learners from the trained schools but

because of school closures, only 130 interviews were achieved.

Although it was possible to identify the non-participating school where the

educators were not trained in the Randfontein areas for direct comparison

purposes, it was only possible to conduct the study when the school reopened

in July. The overall objective of the project was to evaluate the attitude of

educators and learners who had not been exposed to the iCount training

workshop with a view to conducting a future measurement of the impact,

amongst educators and learners who had recently been exposed to the iCount

training.

Profile of the Educators and Learners

One hundred and sixty-four (164) learners took part in the study of which 36

participants amongst these learners were those with educators who did not

attend the iCount workshop; and 128 learners in schools where educators had

received training. Amongst the educators in the qualitative stage, 51 trained

educators were interviewed, 22 in Randfontein and 29 in Dale Park. Due to the

time period when the study was conducted, all the trained learners were in

Grade 12. Amongst the non-trained learners, 44% were in grade 11 and 56% in

Grade 12.The average number of learners taught per class/grade was as

follows: 39 in Grade 10, 34 in Grade 11 and 31 in Grade 12.

The Research Results

This is the baseline for this study, where the learners were tested before their

educators had a chance to put into practice any of the training or resources

Page | 22

they had received. The differences between the learners from schools where

educators attended the iCount training and those who had not are not

significant at the baseline stage. Full impact can only be measured when

implementation has an extended time for learning to be transferred as part of

the curriculum. By January 2014, impact will be able to be fully measured. The

following findings have relevance:

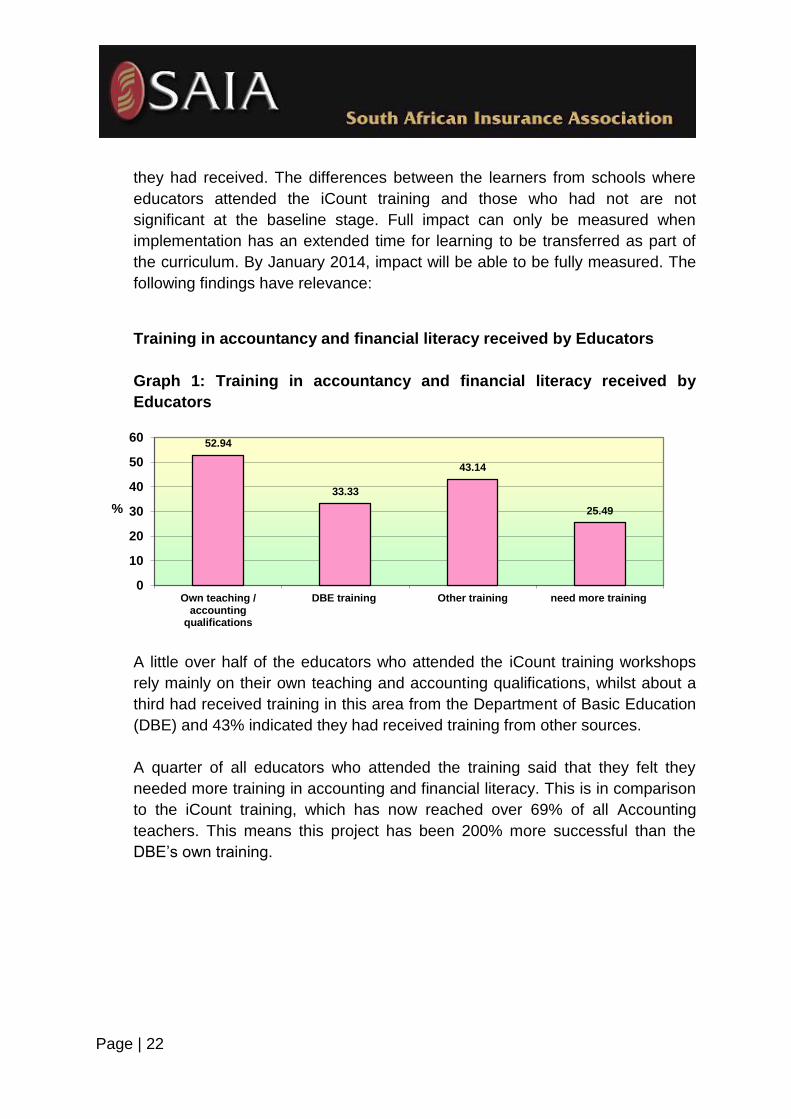

Training in accountancy and financial literacy received by Educators

Graph 1: Training in accountancy and financial literacy received by

Educators

A little over half of the educators who attended the iCount training workshops

rely mainly on their own teaching and accounting qualifications, whilst about a

third had received training in this area from the Department of Basic Education

(DBE) and 43% indicated they had received training from other sources.

A quarter of all educators who attended the training said that they felt they

needed more training in accounting and financial literacy. This is in comparison

to the iCount training, which has now reached over 69% of all Accounting

teachers. This means this project has been 200% more successful than the

DBE’s own training.

52.94

33.33

43.14

25.49

0

10

20

30

40

50

60

Own teaching /accounting

qualifications

DBE training Other training need more training

%

Page | 23

Resources currently utilised by Educators in facilitating Accounting and

financial literacy

Graph 2: Resources currently utilised by Educators

The main resource educators rely on is the textbook for Accounting for their

Grades, closely followed by past examination papers. All the educators used

textbooks and about 83% used past papers. Workbooks were used by 63% of

educators and 27% use DVDs of programmes on accounting and financial

literacy. About a third mentioned material and resources that they had made

and 14% use other materials as an aid in their lessons.

Educators have indicated that work books are needed for learners, that provide

exercises aligned with the text book material. This is to aid the learners in

putting into practice what they have learnt. A further problem that hinders

learning in Accounting is the lack of text books for learners. Educators also felt

that to enhance the subject and motivate their learners, the work books should

also include real life examples of businesses for the learners to work on.

Another area of perceived lack, particularly in teaching Accounting is that many

schools do not have computers for learners to use and work from. Educators

also find it extremely useful working with computers with projectors so that they

can pre-load accountancy information and present it to their learners.

Comments from some of the learners indicate that the resources do exist in

their schools but are used selectively and not always to the benefit of

accountancy learners.

100

62.75

33.33

82.35

27.45

13.73

0

10

20

30

40

50

60

70

80

90

100

Textbook Workbooks Resourcesmade myself

Past papers DVD / episodes Other

%

Page | 24

Educators need more training on following areas

Graph 3: Educators need more training on following areas

Educators were asked to indicate areas in which they needed more training and

significantly over half indicated that Risk Management was an area of greatest

need. This was followed by CAPS (47%), Accounting content in general (41%),

savings (41%) then Financial Literacy and Budgeting at 39%. Results from the

indicated levels of awareness of accountancy content indicate that educators

do need additional training in Risk Management, as they indicate here. In

addition, observed behaviour of educators in the training indicated that there is

sometimes a level of confusion and they actually need additional training in

some basic concepts such as how to work out compound and simple interest.

Another area of lack was in terms of understanding how business plans can be

used as a budget forecast for a business for the coming year and how

businesses need to use these plans to incorporate future development.

41.18

47.06

39.22 41.18 39.22

54.9

3.92

0

10

20

30

40

50

60

Acco

un

tin

gco

nte

nt

CA

PS

Fin

an

cia

l L

itera

cy

Sa

vin

gs

Bu

dg

eti

ng

Ris

k m

an

ag

em

en

t

Oth

er

Page | 25

Learner’s behaviour in income management

Graph 4: Learner’s behaviour in income management

A large percentage, 56%-58% of learners in schools with trained and non-

trained educators save their funds at home in a safe place, many referring to a

money box. This is a more convenient system for most learners who are often

at a distance from the local bank or post office, and require money to catch a

bus before they can access or deposit their funds. Therefore many prefer to

keep their money accessible, and without having to pay bank charges. About

59% of learners in “non-trained” and 42% of learners in “trained” schools say

they save their money in some form of bank account, be it a student account, a

savings account, an investment account or post office account.

Stokvel saving is practiced by 11%/7% of learners while 11%/13% of learners

said they use their income to develop their own small businesses. Some

learners save in both formal and informal systems. Significantly 11% of learners

in “non-trained schools” and 7% in trained schools also save their money in a

small insurance policy to cover things like cell phone insurance or other type of

insurance. A large proportion (58% “non-trained” and 44% “trained) of learners

say they use their funds for things they need such as airtime, clothes, books,

etc., and similarly a large group also lend to their families.

Moneybox

StudentA/c

Banksave a/c

PO savea/c

Investment a/c

StokvelSmall

insurancepolicy

Build OBUse forthings Ineed

Use forpleasure

lend tofamily

Non trained schools 56% 28% 22% 3% 8% 11% 11% 11% 58% 17% 61%

Trained schools 58% 10% 27% 3% 2% 7% 5% 13% 44% 9% 55%

56%

28% 22%

3% 8%

11% 11% 11%

58%

17%

61% 58%

10%

27%

3% 2% 7% 5%

13%

44%

9%

55%

0%

10%

20%

30%

40%

50%

60%

70%

Page | 26

Learners budgeting behaviour

Graph 5: Learners budgeting behaviour

In all, a reasonably high percentage of learners (72% “non-trained” and 69%

“trained” schools) indicated they know what money is available in their purse or

savings, and 42%-48% said they could use the information on what they had to

pay versus what they have coming in, to create a budget and plan what they

could save. Learners in the focus groups discussed budgeting and from their

comments they seem to grasp the whole concept of budgeting and the reason

for it in their own lives as well as in a business.

Knowmoney

available

Knowexpense

s

Knowincome

Calculate

balance

Calculate what Ican save

Plan topay &save

Writedownplan

Workwith plan

Non trained schools 72% 47% 28% 42% 50% 47% 58% 58%

Trained schools 69% 62% 37% 48% 63% 44% 37% 49%

72%

47%

28%

42%

50% 47%

58% 58%

69%

62%

37%

48%

63%

44%

37%

49%

0%

10%

20%

30%

40%

50%

60%

70%

80%%

Page | 27

Learner’s attitude towards saving

Graph 6: Learners attitude towards saving

Most learners (67% learners in non-trained schools and 75% in trained

schools), said they saved for what they needed now, followed closely by 69% -

59% who intend to save in the future. About 28% - 37% (“non-trained” and

“trained”) learners indicate that they save for the future, and 33%-41% save for

future education. Further, about 17% - 13% (“non-trained” and “trained”)

learners say they also save in a small insurance policy. This saving behaviour

is slightly higher amongst learners from schools where their educators have

attended an iCount training workshop. What is of note is the reasonably high

percentage of learners (42% “non-trained” and 38% trained) who indicate they

have not chosen their savings account indiscriminately but have discussed

terms and benefits to see what they are liable for and how they will benefit.

It must be said that the educator in the non-trained school, whilst not having

attended the iCount training had certainly attended other Financial Literacy

training courses and mathematics courses conducted by Bright Media in the

past and was very disappointed to have missed the iCount training.

Save forfuture

Save forwhat I need

Save forfuture

education

Save insmall

insurancepolicy

Save whenI can

Intend tosave infuture

Discussedterms &benefits

Non trained schools 28% 67% 33% 17% 58% 69% 42%

Trained schools 37% 71% 41% 13% 47% 59% 38%

28%

67%

33%

17%

58%

69%

42% 37%

71%

41%

13%

47%

59%

38%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Page | 28

Learners and Educators awareness & knowledge of financial and

accountancy

Practices

Learners in the focus group who were taking Accounting spoke about the value

of the subject to them and why they enjoy it.

Financial Literacy

The graphs below show the level of awareness and knowledge of Accounting

practices amongst Learners and Educators, at the school where the educators

have not received training in the iCount workshop (non-trained School) and at

schools where the educators have received this training (trained Schools).

Again it must be stressed that this is the baseline for this study, where the

learners have been tested before their educators have had a chance to put into

practise any of the training or resources they have received.

Graph 7: I know how to write a budget / savings plan - Learners

The majority of the learners in the “trained” schools, 52%, know very little whilst

11% didn’t answer this section at all. Nevertheless, about 38% said that they

knew quite a lot about this aspect. In contrast 44% of learners in the “non-

trained” school say they know a lot and 39% know something, whilst 17% said

it did not apply (i.e. didn’t know). Educators who received training in iCount are

comfortable with their level of knowledge about financial management, with

86% saying they know a lot while 14% know a little.

Applies a lot Applies a little Doesn't Apply

Non trained schools 44% 39% 17%

Trained schools 38% 52% 11%

44% 39%

17%

38%

52%

11%

0%

10%

20%

30%

40%

50%

60%

Page | 29

Graph 8a: I understand why I should save - Learners

The majority of the learners in both “trained” and “non-trained schools”, about

81%-82% say they do understand why they should save. Similarly in both types

of schools, 17% -13% say the statement applies a little, with very few (3% - 5%)

saying the statement does not apply.

Graph 8b: I understand why I should save - Educators

Trained educators were very confident in their knowledge of this aspect, with

94% saying they know a lot.

Applies a lot Applies a little Doesn't Apply

Non trained schools 81% 17% 3%

Trained schools 82% 13% 5%

81%

17%

3%

82%

13%

5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Applies a lot Applies a little Does not Apply

Educators 94% 6% 0%

94%

6% 0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Page | 30

Graph 9a: I control my spending so I can save what is left over - Learners

Almost two thirds of learners in “trained” schools where the educator had

attended the iCount training indicated that they control their spending to allow

them to save the balance, and close behind at 58%, were the learners from a

“non-trained” school where the educator had not attended the iCount training.

Graph 9b: I control my spending so I can save what is left over –

Educators

On the whole the majority of educators do try to control their spending in order

to save, with 73% saying this applies to them, with 27% saying it applies a little.

Applies a lot Applies a little Doesn't Apply

Non trained schools 58% 33% 8%

Trained schools 63% 29% 8%

58%

33%

8%

63%

29%

8%

0%

10%

20%

30%

40%

50%

60%

70%

Applies a lot Applies a little Does not Apply

Educators 73% 27% 0%

73%

27%

0% 0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Page | 31

Graph 10a: I ask about how much interest and costs are for any savings

plan - Learners

Again there is a similar profile for learners in both schools where their

educators had been trained at the iCount workshop as well as the school where

the educator had not been trained. The majority of the learners in the non-

trained schools, 39%, indicated that the statement, “I ask about how much

interest and costs are for any savings plan” applies to them a lot whilst 44%

said it applies to them a little, and 17% said it didn’t apply. Amongst learners

whose educators had attended the iCount training 34% said the statement

applied a lot and 45% a little over a fifth said it didn’t apply at all.

Graph 10b: I ask about how much interest and costs are for any savings

plan – Educators

Almost 70% of educators indicated that this statement applied to them a lot,

while a quarter said a little. 6% indicated this didn’t apply to them at all.

Applies a lot Applies a little Doesn't Apply

Non trained schools 39% 44% 17%

Trained schools 34% 45% 22%

39%

44%

17%

34%

45%

22%

0%

10%

20%

30%

40%

50%

Applies a lot Applies a little Does not Apply

Educators 69% 25% 6%

69%

25%

6%

0%

10%

20%

30%

40%

50%

60%

70%

Page | 32

Knowledge of Accountancy content

Graph 11a: I know and can explain the accounting cycle - Learners

When it comes to Accounting content knowledge levels drop somewhat. The

majority of the learners in both the “non-trained” and “trained” schools (50% -

58%) said that know very little about the Accounting cycle whilst 14%-16%

didn’t know at all. Nevertheless, about 36% of “non-trained” and 27% of

“trained” school learners said that they knew a lot about the Accounting cycle

and were able to explain it.

Graph 11b: I know and can explain the Accounting cycle – Educators

The majority of educators, 94%, were confident in their knowledge of this

aspect, with a mere 6% saying they only knew a little.

Applies a lot Applies a little Doesn't Apply

Non trained schools 36% 50% 14%

Trained schools 27% 58% 16%

36%

50%

14%

27%

58%

16%

0%

10%

20%

30%

40%

50%

60%

Applies a lot Applies a little Does not Apply

Educators 94% 6% 0%

94%

6% 0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Page | 33

Graph 14a: I know about compound interest and simple interest & know

how to calculate them – Learners

Knowledge of compound and simple interest is relatively high amongst both

groups, with 69% of “non-trained” school learners and 63% of “trained” school

learners indicating they know a lot about this aspect. A similar profile in both

groups (22% “non-trained” and 24% “trained”) indicated they know a little about

compound /simple interest, whilst 8% of “non-trained” and 13% of “trained

school learners say they know nothing, i.e. the statement doesn’t apply to them

at all.

Graph 14b: I know about compound interest and simple interest & know

how to calculate them – Educators

A little over 60% of educators indicated that they know a lot about compound

interest and 35% said they knew a little, while 4% said this does not apply to

them. This is important because it was noted in the training that in some

aspects of the Accounting content some educators seemed a little confused

about the difference between the two.

Applies a lot Applies a little Doesn't Apply

Non trained schools 69% 22% 8%

Trained schools 63% 24% 13%

69%

22%

8%

63%

24%

13%

0%

10%

20%

30%

40%

50%

60%

70%

Applies a lot Applies a little Does not Apply

Educators 61% 35% 4%

61%

35%

4%

0%

10%

20%

30%

40%

50%

60%

70%

Page | 34

Graph 15a: I know about income tax and why it is important to pay for

government services – Learners

Awareness of income tax was high amongst both groups but higher in the “non-

trained” school learners, at 69%, than amongst “trained” school learners, at

58%. Those who indicated they know a little were 22% amongst “non-trained”

school learners and 28% amongst “trained” school learners. Finally 8% “non-

trained” school learners and 14% “trained” school learners indicated they knew

nothing.

Graph 15b: I know about income tax and why it is important to pay for

government services – Educators

The majority of educators, 84%, were confident in their knowledge of income

tax, with only 16% saying they only knew a little about this.

Applies a lot Applies a little Doesn't Apply

Non trained schools 69% 22% 8%

Trained schools 58% 28% 14%

69%

22%

8%

58%

28%

14%

0%

10%

20%

30%

40%

50%

60%

70%

Applies a lot Applies a little Does not Apply

Educators 84% 16% 0%

84%

16%

0% 0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Page | 35

Graph 16a: I know how to calculate gross profit and net profit on sales –

Learners

Awareness of how to calculate gross profit and net profit on sales was

reasonably good amongst both groups but higher in the “non- trained” school

learners, at 53%, than amongst “trained” school learners, at 46%. Those who

indicated they know a little were about a quarter of “non-trained” school

learners and 38% amongst “trained” school learners. However almost a quarter

of the “non- trained” school learners indicated they didn’t know how to calculate

gross & net profit at all, while 17% of “trained” school learners indicated they

knew nothing of this aspect.

Graph 16b: I know how to calculate gross profit and net profit on sales –

Educators

The majority of educators, 96%, were confident in their ability to calculate gross

and net profit on sales, with only 4% saying they knew little about this.

Applies a lot Applies a little Doesn't Apply

Non trained schools 53% 25% 22%

Trained schools 45% 38% 17%

53%

25% 22%

45%

38%

17%

0%

10%

20%

30%

40%

50%

60%

Applies a lot Applies a little Does not Apply

Educators 96% 4% 0%

96%

4% 0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Page | 36

Graph 17a: I understand what a perpetual inventory system is – Learners

The majority of the learners in both the “non-trained” and “trained” schools

(50% - 45%) said that know very little about the perpetual inventory system

whilst 17%-29% didn’t anything know at all. However about a third of “non-

trained” and a quarter of “trained” school learners said that they knew a lot

about the perpetual inventory system.

Graph 17b: I understand what a perpetual inventory system is –

Educators

About three quarters of educators indicated that they knew a lot about the

perpetual inventory system, with 16% saying they know a little, while 8% said

they did not know.

Applies a lot Applies a little Doesn't Apply

Non trained schools 33% 50% 17%

Trained schools 26% 45% 29%

33%

50%

17%

26%

45%

29%

0%

10%

20%

30%

40%

50%

Applies a lot Applies a little Does not Apply

Educators 76% 16% 8%

76%

16%

8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Page | 37

Graph 18a: I know about creating a business plan as a budget and how to

work with a budget for a business – Learners

The majority of the learners in both the “non-trained” and “trained” schools

(53% - 52%) said that know very little about creating a business plan as a

budget and how to work with a budget for a business whilst 14%-16% didn’t

anything know at all.

However about a third of both “non-trained” and “trained” school learners said

that they knew a lot about creating a business plan as a budget and how to

work with a budget for a business.

Graph 18b: I know about creating a business plan as a budget and how to

work with a budget for a business – Educators

Creating a business plan as a budget and knowing how to work with a budget for

a business was an aspect that educators do not, on the whole feel very confident

about, with only 47% saying they know a lot and 45% saying they know a little

and 8% saying they know nothing about this aspect of Accounting.

Applies a lot Applies a little Doesn't Apply

Non trained schools 33% 53% 14%

Trained schools 32% 52% 16%

33%

53%

14%

32%

52%

16%

0%

10%

20%

30%

40%

50%

60%

Applies a lot Applies a little Does not Apply

Educators 47% 45% 8%

47% 45%

8%

0%

10%

20%

30%

40%

50%

Page | 38

Graph 19a: I know and can explain account reconciliation - Learners

Most of the learners in both the “non-trained” and “trained” schools (50% - 56%)

said that know very little about account reconciliation whilst 6% of “non- trained”

school learners and about a quarter of “trained” school learners didn’t anything

know at all. However about 44% of “non-trained” and a fifth of “trained” school

learners said that they knew a lot about account reconciliation.

Graph 19b: I know and can explain account reconciliation – Educators

About three quarters of the educators indicated they knew and could explain

account reconciliation, with almost a quarter saying they knew a little about this

and only 6% did not know.

Applies a lot Applies a little Doesn't Apply

Non trained schools 44% 50% 6%

Trained schools 20% 56% 24%

44%

50%

6%

20%

56%

24%

0%

10%

20%

30%

40%

50%

60%

Applies a lot Applies a little Does not Apply

Educators 73% 22% 6%

73%

22%

6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Page | 39

Graph 20a: I know about financial Accounts and financial statements that

you analyse to determine how well the company is financially – Learners

The majority of learners in “non-trained” schools, 56%, knew a lot about

financial Accounts and financial statements, with about a third saying they knew

a little and only 11% saying they know nothing. Conversely amongst the

“trained” school learners, the majority, 51%, said they only knew a little and a

little over a third said they knew a lot about financial accounts and financial

statements, with 14% saying they do not know.

Graph 20b: I know about financial accounts and financial statements that

you analyse to determine how well the company is financially – Educators

The majority of educators, 84%, indicated they know about financial accounts

and financial statements with only 12% saying they know a little and 4% saying

they know nothing.

Applies a lot Applies a little Doesn't Apply

Non trained schools 56% 33% 11%

Trained schools 35% 51% 14%

56%

33%

11%

35%

51%

14%

0%

10%

20%

30%

40%

50%

60%

Applies a lot Applies a little Does not Apply

Educators 84% 12% 4%

84%

12%

4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Page | 40

Graph 21a: I know how VAT is calculated and how to complete VAT

returns – Learners

Most of the learners in both the “non-trained” (50%) and “trained” (58%)

schools indicated they knew a lot about how VAT is calculated and how to

complete VAT returns. About 39% - 31% said they knew a little, whilst 11% in

both groups said they knew nothing.

Graph 21b: I know how VAT is calculated and how to complete VAT

returns – Educators

About three quarters of educators indicated they know a lot regarding VAT and

VAT returns with 18% saying they know a little and only 6% indicate they know

nothing.

Applies a lot Applies a little Doesn't Apply

Non trained schools 50% 39% 11%

Trained schools 58% 31% 11%

50%

39%

11%

58%

31%

11%

0%

10%

20%

30%

40%

50%

60%

Applies a lot Applies a little Does not Apply

Educators 76% 18% 6%

76%

18%

6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Page | 41

Graph 22a: I know that other threats to businesses are external risks

such as fire, floods or theft – Learners

Most of the learners in both the “non-trained” (56%) and “trained” (59%)

schools indicated they knew a lot about external risks to businesses such as

fire, floods or theft. About 39% - 28% said they knew a little, whilst 6%-13%

said they knew nothing.

Graph 22b: I know that other threats to businesses are external risks such

as fire, floods or theft – Educators

Amongst educators 67% were confident in their knowledge about external risks

to businesses such as fire, floods or theft, with 67% saying they know a lot as

opposed to 12% who said they knew a little. However, significantly, about a

quarter of educators said they knew nothing about this, indicating an area of

importance for future training.

Applies a lot Applies a little Doesn't Apply

Non trained schools 56% 39% 6%

Trained schools 59% 28% 13%

56%

39%

6%

59%

28%

13%

0%

10%

20%

30%

40%

50%

60%

Applies a lot Applies a little Does not Apply

Educators 67% 12% 22%

67%

12%

22%

0%

10%

20%

30%

40%

50%

60%

70%

Page | 42

Graph 23a: I know how to calculate operating expenses, operating profit

on sales – Learners

The majority of learners in “non-trained” schools, 47%, knew a lot about how to

calculate operating expenses, operating profit on sales with about 39% saying

they knew a little and 14% saying they know nothing. Conversely amongst the

“trained” school learners, the majority, 45%, said they only knew a little and a

little and 41% said they knew a lot about how to calculate operating expenses,

operating profit on sales, with 14% saying they do not know.

Graph 23b: I know how to calculate operating expenses, operating profit

on sales. – Educators

About three quarters of educators indicated they know a lot about how to

calculate operating expenses, operating profit on sales with 18% saying they

know a little and only 8% indicate they know nothing.

Applies a lot Applies a little Doesn't Apply

Non trained schools 47% 39% 14%

Trained schools 41% 45% 14%

47%

39%

14%

41% 45%

14%

0%

10%

20%

30%

40%

50%

Applies a lot Applies a little Does not Apply

Educators 75% 18% 8%

75%

18%

8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Page | 43

Graph 24a: I know how to calculate current ratio, acid test ratio, solvency

ratio on business to see if it can survive - Learners

Among both group, “non-trained” and “trained” school learners, about 47%-48%

indicated they know a lot about how to calculate current ratio, acid test ratio,

and solvency ratio on business to see if it can survive. However, about half of

“non-trained” school learners indicated that they knew little and 3% said they

knew nothing. Conversely 34% of “trained” learners knew little whilst 18% said

they knew nothing; an area in need of strengthening.

Graph 24b: I know how to calculate current ratio, acid test ratio and

solvency ratio on business to see if it can survive – Educators

About three quarters of educators knew a lot about how to calculate current

ratio, acid test ratio and solvency ratio on business to see if it can survive, with

18% saying they know a little and 8% who know nothing.

Applies a lot Applies a little Doesn't Apply

Non trained schools 47% 50% 3%

Trained schools 48% 34% 18%

47% 50%

3%

48%

34%

18%

0%

10%

20%

30%

40%

50%

Applies a lot Applies a little Does not Apply

Educators 75% 18% 8%

75%

18%

8%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Page | 44

Graph 25a: I know about values such as integrity and honesty, respect,

fairness that builds trust and how this affects a business amongst its

customers – Learners

Learners in both “non-trained” and “trained” schools are equally aware of the

importance of values such as integrity and honesty, respect, fairness that build

trust and how this affects a business amongst its customers, with 44% of both

groups saying they know a lot. However at least half of the “non- trained”

school learners say they know little about this and 6% know nothing. This

compares with 38% of “trained” school learners who know little and 18% who

know nothing. This is an area in need of strengthening.

Graph 25b: I know about values such as integrity and honesty, respect,

fairness that builds trust and how this affects a business amongst its

customers – Educators

Applies a lot Applies a little Doesn't Apply

Non trained schools 44% 50% 6%

Trained schools 44% 38% 18%

44%

50%

6%

44%

38%

18%

0%

10%

20%

30%

40%

50%

Applies a lot Applies a little Does not Apply

Educators 73% 18% 10%

73%

18%

10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Page | 45

Knowledge and awareness of insurance products

I understand what insurance does

Graph 26: Know and understand what Insurance does

Overall there is an increase in awareness of what insurance does, with 86%-

84% of learners in both iCount “non-trained” and “trained” schools knowing

what insurance does. The level of financial literacy awareness is higher, in

comparison to the previous study, because all the educators in all schools have

previously attended training, which incorporates financial literacy in all its

modules. Thus awareness of insurance, particularly amongst these Grade 12

learners is high.

In 2012, the results for this question were 63% amongst “non-trained” schools

and 74% amongst “trained” schools. These Grade 12 learners have now

probably been through two to three years of influence from educators trained in

financial literacy from attending previous courses in mathematics or Managing

your Money, and the long term effect can clearly be seen.The following table

shows the statements chosen by those who said yes, they knew what

insurance does.

Learners Educators

Non trained school 86%

Trained schools 84% 78%

86% 84% 78%

0%10%20%30%40%50%60%70%80%90%

100%

Page | 46

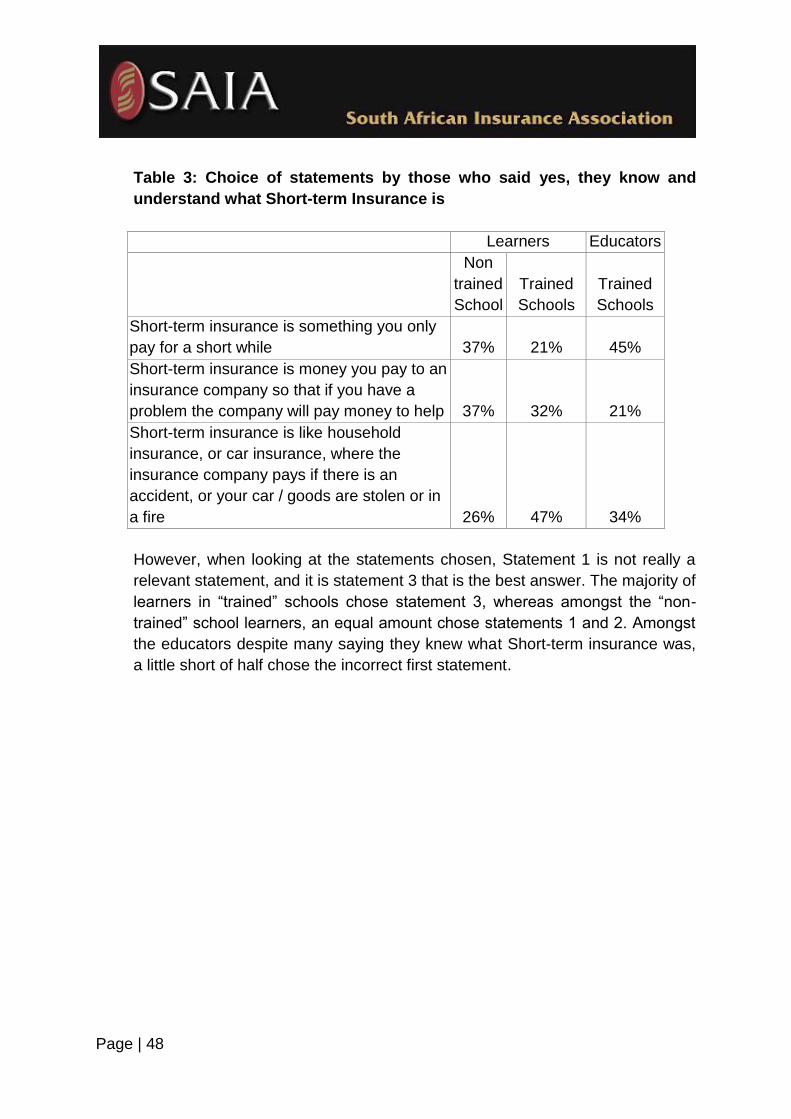

Table 1: Choice of statements by those who said yes, they know and

understand what Insurance does

Learners Educators

Non

trained

School

Trained

Schools

Trained

Schools

A plan to help people when they have

problems 35% 35% 50%

A structured savings plan to helps you save

for specific goals, like retirement etc 65% 65% 50%

The majority of learners in trained and non- trained schools chose statement

two, which focuses on a structured savings plan. However it seems that

learners are a little more au fait than their educators, who have a greater

proportion choosing the incorrect statement.

I understand what Educational Insurance does

Graph 27: Know and understand what Educational Insurance does

In total 61% of learners in non-trained schools and 73% of learners in trained,

said that they understood what Educational Insurance does.The statements

chosen by those who had said yes above, are listed in the table below.

Learners Educators

Non trained school 61%

Trained schools 73% 96%

61%

73%

96%

0%10%20%30%40%50%60%70%80%90%

100%

Page | 47

Table 2: Choice of statements by those who said yes, they know and

understand what Educational Insurance does

Learners Educators

Non

trained

School

Trained

Schools

Trained

Schools

Educational insurance is money you save

into an insurance policy so that when you

need it for tertiary education you have

something to help 77% 88% 98%

Education insurance is only worthwhile if you