Page 1

2 April 2019

Salt Lake Potash (ASX: SO4) Speculative Buy

Price Target $1.21

Colin McLelland Contact: 0439 412 537

Security Details

Ordinary Shares 204.6m

Unlisted Performance Shares 17.5m

Unlisted Options & Perf’ Rights 32.9m

Market Capitalisation (m, undil.) $116.6m

Cash & equivalents (31/12/2018) $12.0m

Share Price (1/04/2019) $0.57

52 week high/low $0.620/$0.425

Share Price Graph

Directors

Ian Middlemas Chairman Tony Swiericzuk MD &CEO Clint McGhie CFO and Company Sec. Mark Pearce Non‐Executive Director Bryn Jones Non‐Executive Director

Major Shareholders

Lombard Odier Asset Mgt. Ltd. 11.6% Ian Middlemas 5.7% Fidelity (various) 5.0% JP Morgan Asset Mgt. 4.2%

Investment Highlights

• Salt Lake Potash (SO4) enjoys a capex advantage through its ability to use unlined evaporation ponds and the infrastructure available in the Goldfields region. The location of the Goldfields Salt Lakes Project (GSLP) also suggests an opex advantage over competitors with more remote projects.

• SO4 has a (relatively) new MD and has strengthened its development team with three senior appointments – all ex-FMG, as is the MD.

• Despite the July 2018 release of the Scoping Study into a Demonstration Plant at Lake Way, we can’t make the economics work at that scale and we assume a production level of 200ktpa as per the Lake Wells Stage 1 Scoping Study. SO4 has confirmed it is “reviewing a larger scale scenario”, with technical results expected in the current half. SO4 is currently constructing the initial ponds at Lake Way.

• We note the MD’s performance rights are all based around 200ktpa levels – something the 50ktpa Demonstration Plant does not envisage. The recent appointment of executives from FMG means SO4 now has in-house experience of “continuous” development. We would be very surprised if the executives had been appointed to oversee a Demonstration scale development.

• SO4 has now demonstrated it can produce salts from both Lake Wells and Lake Way, and has demonstrated SOP production from Lake Wells salts, with Lake Way SOP production pending.

• SO4 now has MOUs in place with Mitsubishi Corporation (Mitsubishi, April 2018) and Sinofert Holdings Limited (Sinofert, October 2018). In both cases the MOU agreements include the provision of strategic advice on marketing - key, in our view.

• We maintain coverage on Salt Lake Potash (SO4) with a Speculative Buy recommendation and a revised NPV based Price Target of $1.21/share, subject to review as the development pathway is clarified.

Page 2

Salt Lake Potash Ltd.

Taylor Collison Limited 2 | P a g e

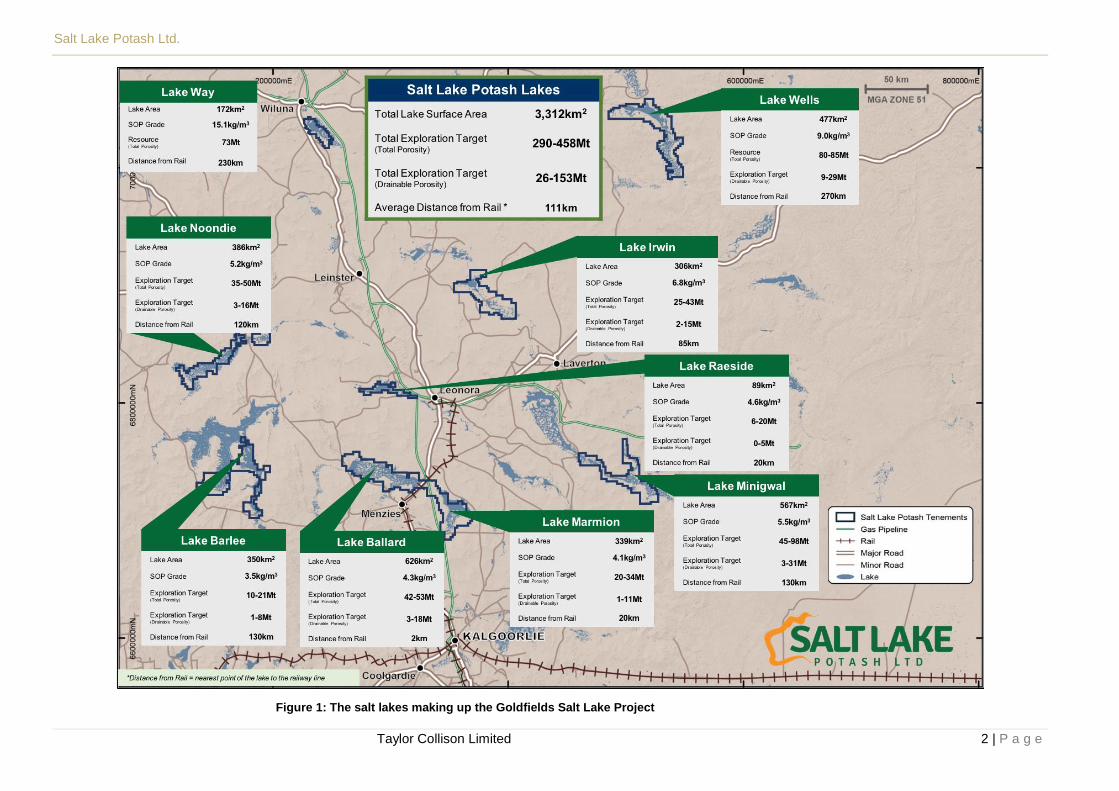

Figure 1: The salt lakes making up the Goldfields Salt Lake Project

Page 3

Salt Lake Potash Ltd.

Taylor Collison Limited 3 | P a g e

Goldfields Salt Lakes Project (GSLP)

The Goldfields Salt Lakes Project is made up of multiple salt lakes, as shown in Figure 1 on the previous

page. Most salt lakes within the GSLP benefits from the infrastructure advantage of its location in the

Goldfields Region. Existing infrastructure includes:

• the Goldfields Highway,

• the Great Central Road,

• the Goldfields Gas Pipeline,

• multiple railheads (Malcolm, Leonora, Menzies and Kookynie), and

• access to ports at Geraldton, Freemantle (rail access) and Esperance (rail access).

The diversification benefits of having access to multiple export ports should not be under-estimated,

particularly for a single commodity Company.

As a concrete example of the infrastructure advantage of its location, SO4 intends to use excess power

available at the Wiluna Gold Mine power plant at Lake Way, whereas Kalium Lakes (ASX KAL) has

estimated A$39m in capex for the extension of a gas pipeline and the construction of a power station for

its Beyondie project.

The GSLP is a highly scaleable resource, and there appears strong potential to develop an integrated

project sourcing brine from multiple salt lakes within the project. We model production at a rate of

approximately 600ktpa by 1H 2030 from just two of the salt lakes within the portfolio. However, at that

level, SO4 would be producing what is approximately 9% of the current global SO4 market. Given the

Company’s cost curve position, it should be able to gain that market share by displacing higher cost

producers (as a worst case). The key challenge, and the key risk in our view, will be establishing demand

for the product without the excessive initial discounting that would conflict with SO4’s positioning of its

SOP as a premium product in the marketplace.

Historically, SO4’s focus was on Lake Wells (just one of the salt lakes within the broader GSLP), with a

Scoping Study released in August 2016. Early in 2018, post the signing of an MOU with Blackham

Resources (ASX BLK), the development effort appears to have been re-focused on Lake Way (again, just

one of the salt lakes in the broader GSLP), with a Scoping Study on a Demonstration Plant at Lake Way

released in July 2018.

With the development experience recently added to SO4’s management team, we expect the Company

is now less risk averse and is prepared to manage any issues that may arise from a move straight to larger

scale development. We can’t make the economics of a Demonstration Plant at Lake Way work and we

model a ramp up to a 200ktpa straight away (over two years) at the Lake Way operation for this reason.

Beyond initial development at Lake Way, we await clarity on the development pathway for an integrated

SOP operation, potentially drawing on the resource of any, or all, of the salt lakes in the GSLP. Two

priorities outside of Lake Wells and Lake Way include Lake Ballard ( which the rail line crosses) and Lake

Irwin, which is substantially closer to the railhead than Lake Wells.

Brine grade is also significant. Higher grade requiring lower volumes of brine to be pumped and

evaporated. Lake Way is a stand-out for initial development with a grade of 15.1kg/m3. After that, things

are less clearcut. With a maximum average resource grade in the Exploration Target (JORC Exploration

Targets are required to present a range) of greater than 8kg/m3, Lake Irwin makes a strong case for future

development and, given its location, it may be developed as a brine source ahead of Lake Wells.

Page 4

Salt Lake Potash Ltd.

Taylor Collison Limited 4 | P a g e

The Lake Wells Scoping Study demonstrated that capital intensity for expansions is lower than the capital

intensity to build the initial plant capacity. It is possible that this could see an integrated development

following the initial development of Lake Way, in preference to the development of Lake Wells. Despite

the relatively advanced status of studies at Lake Wells, we are now not confident that Lake Wells will be

the next development undertaken within the broader GSLP project.

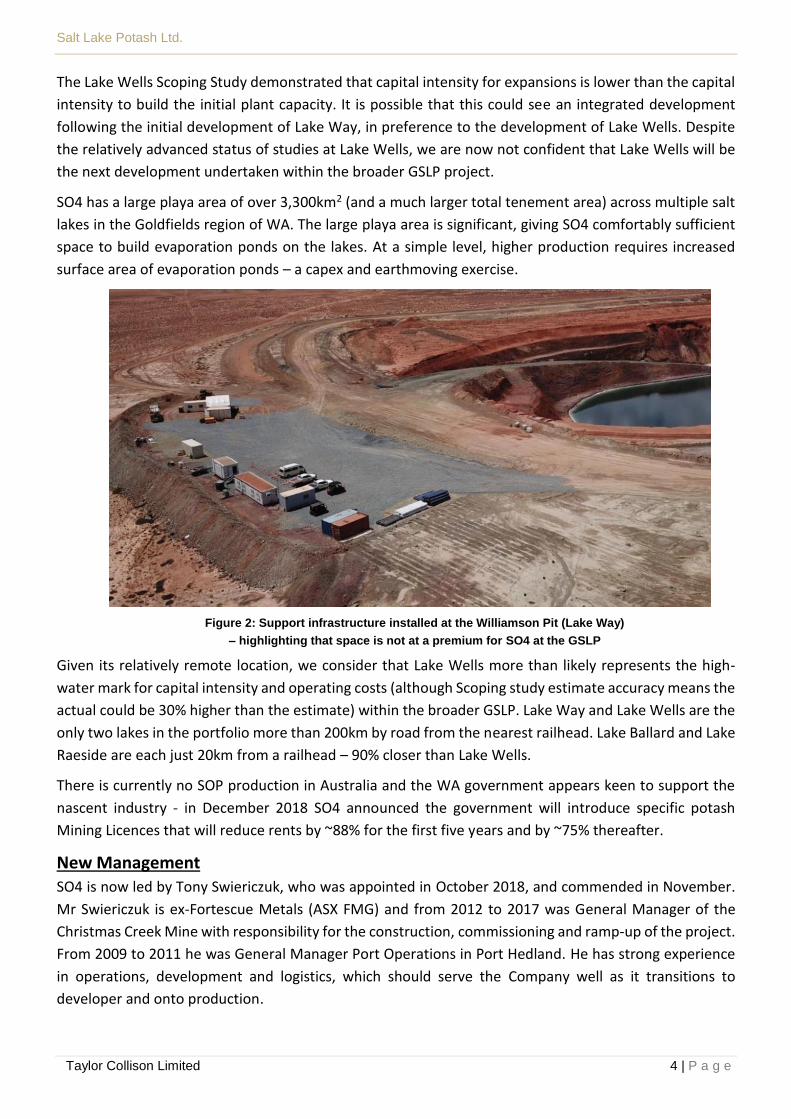

SO4 has a large playa area of over 3,300km2 (and a much larger total tenement area) across multiple salt

lakes in the Goldfields region of WA. The large playa area is significant, giving SO4 comfortably sufficient

space to build evaporation ponds on the lakes. At a simple level, higher production requires increased

surface area of evaporation ponds – a capex and earthmoving exercise.

Figure 2: Support infrastructure installed at the Williamson Pit (Lake Way)

– highlighting that space is not at a premium for SO4 at the GSLP

Given its relatively remote location, we consider that Lake Wells more than likely represents the high-

water mark for capital intensity and operating costs (although Scoping study estimate accuracy means the

actual could be 30% higher than the estimate) within the broader GSLP. Lake Way and Lake Wells are the

only two lakes in the portfolio more than 200km by road from the nearest railhead. Lake Ballard and Lake

Raeside are each just 20km from a railhead – 90% closer than Lake Wells.

There is currently no SOP production in Australia and the WA government appears keen to support the

nascent industry - in December 2018 SO4 announced the government will introduce specific potash

Mining Licences that will reduce rents by ~88% for the first five years and by ~75% thereafter.

New Management SO4 is now led by Tony Swiericzuk, who was appointed in October 2018, and commended in November.

Mr Swiericzuk is ex-Fortescue Metals (ASX FMG) and from 2012 to 2017 was General Manager of the

Christmas Creek Mine with responsibility for the construction, commissioning and ramp-up of the project.

From 2009 to 2011 he was General Manager Port Operations in Port Hedland. He has strong experience

in operations, development and logistics, which should serve the Company well as it transitions to

developer and onto production.

Page 5

Salt Lake Potash Ltd.

Taylor Collison Limited 5 | P a g e

Transportation costs are a significant operational impost on potash projects, having been estimated at

30% and 25% of FOB costs in SO4’s two Scoping Studies to date. Mr Swiericzuk’s experience in optimising

logistics is likely to prove every bit as valuable to SO4 shareholders as his experience in overseeing

development and ramp-up of projects.

In addition, FMG’s Christmas Creek mine used to pump ~45GL of water annually in managing the water

table to enable successful iron ore mining, giving Mr Swiericzuk valuable experience in water

management.

Market the Key Risk – but we model greater scale at Lake Way

We see relatively low resource risk for the GSLP despite the early stage of resource definition. Similarly,

while exact capital and operating costs remain uncertain, we do not see them as the key risk for the GSLP,

particularly given the development experience the Company has now acquired, through the bolstering of

the Senior Executive team in December 2018.

Sulphate of Potash (SOP) is a premium fertiliser product, and SO4 will be a relatively small entrant

(initially) to that global market. The Company may be marketing the first SOP produced in Australia. In

our view, marketing is the key risk for SO4. Successfully establishing a market presence and establishing

its product as a known market entity should significantly de-risk the greater GSLP.

In this regard, the importance of the MOU’s with Mitsubishi Corporation (Mitsubishi, April 2018) and

Sinofert Holdings Limited (Sinofert, October 2018) should not be under-estimated. In both cases, the MOU

agreements include the provision of strategic advice on marketing. Each (non-binding) agreement gives

the counter-party rights to up to 50% of the SOP production from SO4’s Demonstration Plant at Lake Way,

and, in the case of Sinofert, this extends to 50% of all production from the GSLP.

Despite the need to establish market credibility, the Lake Wells Scoping Study highlights the value upside

of greater scale. We cannot make the economics of the Demonstration Plant work, and have effectively

transplanted Stage 1 of the Lake Wells Scoping Study results to Lake Way. We highlight that the MD’s

performance rights and Stage 1 of the Lake Wells Scoping Study were based around 200ktpa, not the

50ktpa envisaged for the Lake Way Demonstration Plant.

Not only does the Demonstration Plant make no sense economically, the MD is not incentivised to pursue

it. Indeed, a current review process to consider a “larger scale scenario” at Lake Way is underway, with

technical results of the review anticipated to be released towards the end of JunQ19.

Page 6

Salt Lake Potash Ltd.

Taylor Collison Limited 6 | P a g e

Fertilizer Basics

The six macronutrients required by plants are: nitrogen; phosphate; potassium; sulphur; calcium, and

magnesium. There are no substitutes for these. Sulphate of Potash, (SOP, also known as Potassium

Sulphate - K2SO4) contains two of the six macronutrients required by plants (potassium and sulphur).

Testing (and real-world practice) has shown that crop yields increase with application of SOP, as can be

seen (with tomatoes) in the photo below:

Figure 3: Impact of fertilizer application rates (Source: Potash Ridge – Feb ’17 Investor Presentation)

Muriate of Potash (MOP, also known as potassium chloride - KCL) contains 46% chloride, while SOP

contains 18% sulphur and has almost no chloride. SOP is a premium product used principally for specialty

crops such as fruits, vegetables and tree nuts: products where taste and appearance are just as important

as yield.

While MOP and SOP are both potassium fertilizers, SOP is a premium fertilizer and is priced accordingly.

It also has a smaller global market (~1/10th the size) with differing supply and demand dynamics to those

exhibited in the larger MOP market. It appears an under-supplied market.

Globally, the Mosaic Company (NYSE: MOS) was, until recently, the leader in potash production (although

focussed on MOP) with 2018 production of 8.8 million tonnes and with 2019 guidance of 9.0-9.4 million

tonnes. Mosaic has a stated potash production capacity of 11 million tonnes and is forecasting global

production of 69m (MOP) in 2019. In January 2018, Potash Corp of Saskatchewan completed its merger

with Agrium, creating Nutrien, now the largest global producer of potash (again MOP focussed). Nutrien

is guiding for 2019 potash production of 13-13.4 million tonnes and expects a global market of 67-69

million tonnes. In comparison, SO4 sizes the global SOP market at approximately 7mt in 2019.

SOP is also most suitable for regions affected by high salinity soils. When chloride concentration in the

soil solution increases, plants take it up on the account of essential anionic nutrients, especially nitrate.

High concentrations of chloride may cause toxic effects and even crop failures. Even where crops are not

immediately damaged, sustained use of MOP degrades soils over time through the accumulation of salt.

100lb/acre 200lb/acre 300lb/acre

Page 7

Salt Lake Potash Ltd.

Taylor Collison Limited 7 | P a g e

Figure 4: Fruit leaves exhibiting salt damage (Source: Potash Ridge – Feb ’17 Investor Presentation)

As the world population grows and arable land per capita falls, demand for fertiliser is expected to

increase. There is also a relationship between country GDP and fertiliser use, with higher GDP leading to

higher fertiliser use. As such, the demand picture for SOP appears robust.

Secondary processing In addition to primary production, MOP can be upgraded to SOP through the Mannheim Process (energy

and emissions intensive as well as expensive), a process that involves the addition of sulphuric acid to

MOP in a Mannheim furnace to produce SOP and a hydrochloric acid by-product.

Figure 5: The secondary processing inputs and outputs

(Source: Potash Ridge – Feb ’17 Investor Presentation)

The production of hydrochloric acid as a by-product is important. Where demand for HCL is weaker than

demand for SOP, the disposal of excess HCL is a significant complication that prevents there from being a

straight arbitrage between the price of MOP and SOP. As a result, the price of SOP is largely determined

by the economics of high value crops rather than the input cost of MOP.

Page 8

Salt Lake Potash Ltd.

Taylor Collison Limited 8 | P a g e

The cost curve below highlights the split nature of operations. Primary SOP production dominates the

lower end of the cost curve, before a sharp jump in costs as secondary processing becomes the means of

production. High cost production is generally from China, but also includes some European production.

Figure 6: The SOP cost curve (Source: SO4 Company presentation)

There is no widely accepted spot price series to follow for either SOP or MOP. However, recent transaction

prices are made available on various subscription services. Prices vary with quality, but SO4 quotes a

current price range of US$500-650/t for SOP and approximately US$300/t for MOP, implying a simplistic

(rather than-value-in use) premium for SOP over MOP of US$200-350$/t.

The Mining Process

Unlike many mining operations, the production of SOP from brines appears a simple process (there is no

doubt much technical work behind this apparent simplicity). The engineering value add behind brine

extraction and evaporation pond design would appear to be in the minimisation of pumping

requirements, and therefore power consumption (6% of operating costs in the Lake Way Demonstration

Plant Scoping Study). Given sufficient space exists, construction of solar evaporation ponds appears

largely an earthmoving exercise.

Once the ponds are in equilibrium, the time taken from brine entering the system to being harvested as

a salt, should be around nine months for SO4. The entire process uses off-the-shelf equipment and even

where specialized equipment (such as an amphibious excavator) is used, it is readily available.

Page 9

Salt Lake Potash Ltd.

Taylor Collison Limited 9 | P a g e

Figure 7: The SOP production process

Brine is pumped from trenches and/or bores into a series of solar evaporation ponds which see the

concentration of potassium increased to around 8-9%, but with chloride levels remaining high. Potassium

double salts are then mechanically harvested, in a process the Lake Wells Scoping Study estimated would

take70 days (20 days for draining and drying the salts, 50 days for harvesting)

The harvested salts are subsequently fed into a processing plant, where they are crushed and milled and

dissolved back into potassium rich liquor (using a circulating potassium rich intermediate brine). The

resulting thickened salt slurry solution is converted to schoenite in a sulphate solution at ambient

temperatures. The liquor then passes through a flotation stage and the chloride is floated off. Heating the

resultant schoenite slurry to 48 degrees Celsius sees the crystallisation of the schoenite to SOP. The SOP

is then filtered, dried and packed. Final product format (powder, granulated etc) is about meeting

customer requirements and maximising product revenue, and SO4 is still evaluating this. Regardless, it

will be using readily available equipment used widely in the sugar industry.

The industry wide average for SOP is a range of K2O of 50-52%, with NaCl ranging from 0.3% - 1.0%. SO4

has demonstrated it can produce a very high quality SO4 product. SO4’s current expectations are for K2O

at around 53% with a very low NaCl content at 0.1%. SO4 needs to do more work to understand if it will

be rewarded for such a high-quality product, or if projected returns are improved by targeting production

of a lower specification product at a lower unit cost.

SO4 has already demonstrated an ability to produce high quality SOP from salts produced at Lake Wells.

Pilot plant production of SOP from salts produced at Lake Way is currently underway at the SRC (finalising

the Company’s process flowsheet, prior to sign-off).

The Lake Wells Scoping Study anticipated production of 200ktpa SOP, produced from shallow, low cost,

trenches and bores and subsequently by deeper (120m) bores for production of 400ktpa SOP. Trenches

are simply dug with an excavator with an example design shown in the Lake Way Demonstration Plant

Scoping Study.

Page 10

Salt Lake Potash Ltd.

Taylor Collison Limited 10 | P a g e

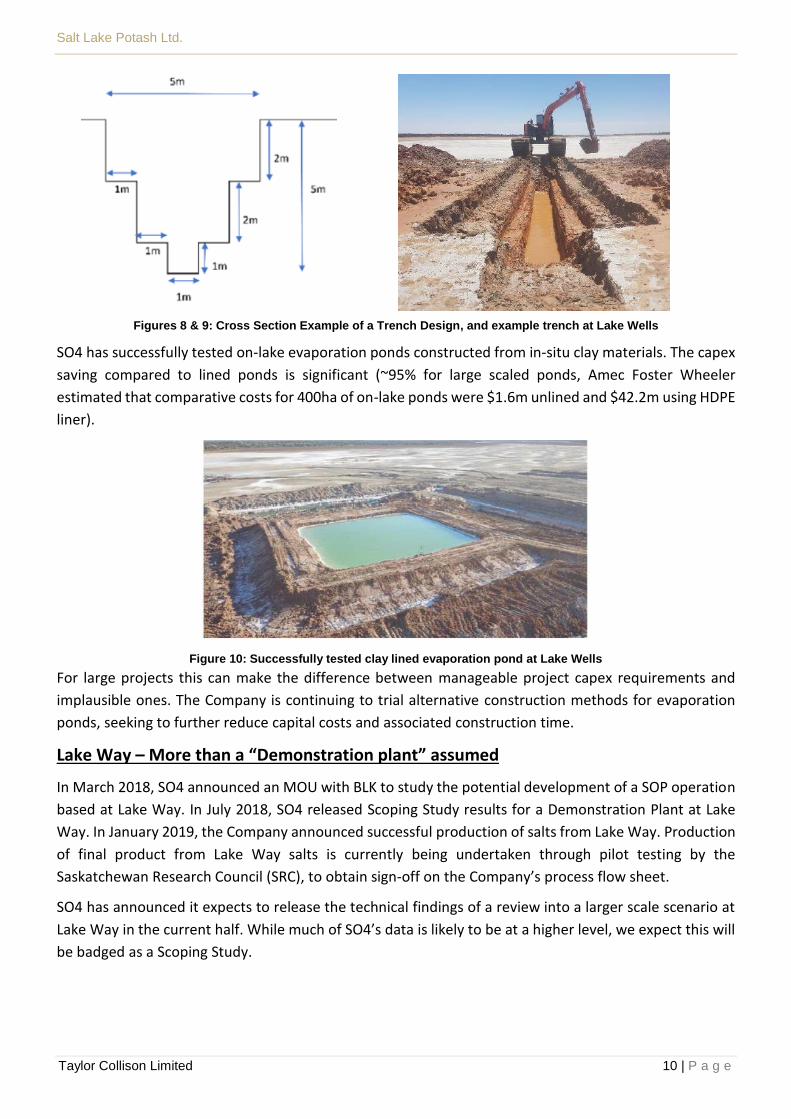

Figures 8 & 9: Cross Section Example of a Trench Design, and example trench at Lake Wells

SO4 has successfully tested on-lake evaporation ponds constructed from in-situ clay materials. The capex

saving compared to lined ponds is significant (~95% for large scaled ponds, Amec Foster Wheeler

estimated that comparative costs for 400ha of on-lake ponds were $1.6m unlined and $42.2m using HDPE

liner).

Figure 10: Successfully tested clay lined evaporation pond at Lake Wells

For large projects this can make the difference between manageable project capex requirements and

implausible ones. The Company is continuing to trial alternative construction methods for evaporation

ponds, seeking to further reduce capital costs and associated construction time.

Lake Way – More than a “Demonstration plant” assumed

In March 2018, SO4 announced an MOU with BLK to study the potential development of a SOP operation

based at Lake Way. In July 2018, SO4 released Scoping Study results for a Demonstration Plant at Lake

Way. In January 2019, the Company announced successful production of salts from Lake Way. Production

of final product from Lake Way salts is currently being undertaken through pilot testing by the

Saskatchewan Research Council (SRC), to obtain sign-off on the Company’s process flow sheet.

SO4 has announced it expects to release the technical findings of a review into a larger scale scenario at

Lake Way in the current half. While much of SO4’s data is likely to be at a higher level, we expect this will

be badged as a Scoping Study.

Page 11

Salt Lake Potash Ltd.

Taylor Collison Limited 11 | P a g e

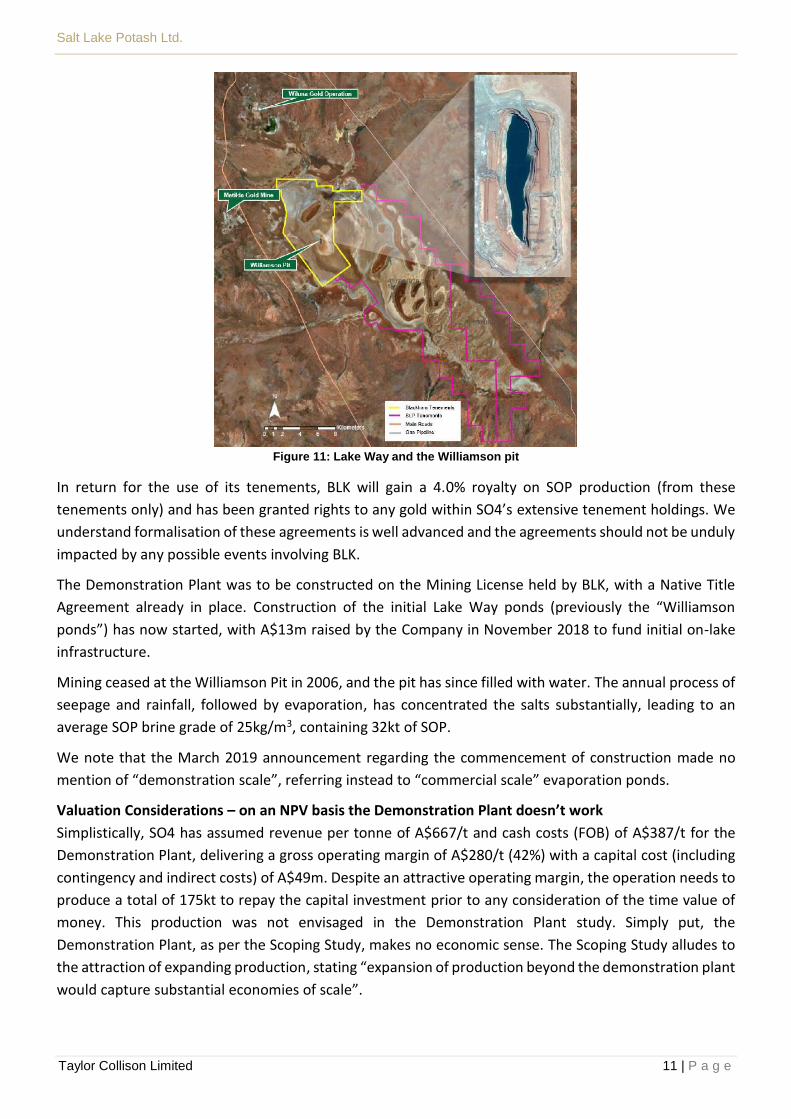

Figure 11: Lake Way and the Williamson pit

In return for the use of its tenements, BLK will gain a 4.0% royalty on SOP production (from these

tenements only) and has been granted rights to any gold within SO4’s extensive tenement holdings. We

understand formalisation of these agreements is well advanced and the agreements should not be unduly

impacted by any possible events involving BLK.

The Demonstration Plant was to be constructed on the Mining License held by BLK, with a Native Title

Agreement already in place. Construction of the initial Lake Way ponds (previously the “Williamson

ponds”) has now started, with A$13m raised by the Company in November 2018 to fund initial on-lake

infrastructure.

Mining ceased at the Williamson Pit in 2006, and the pit has since filled with water. The annual process of

seepage and rainfall, followed by evaporation, has concentrated the salts substantially, leading to an

average SOP brine grade of 25kg/m3, containing 32kt of SOP.

We note that the March 2019 announcement regarding the commencement of construction made no

mention of “demonstration scale”, referring instead to “commercial scale” evaporation ponds.

Valuation Considerations – on an NPV basis the Demonstration Plant doesn’t work

Simplistically, SO4 has assumed revenue per tonne of A$667/t and cash costs (FOB) of A$387/t for the

Demonstration Plant, delivering a gross operating margin of A$280/t (42%) with a capital cost (including

contingency and indirect costs) of A$49m. Despite an attractive operating margin, the operation needs to

produce a total of 175kt to repay the capital investment prior to any consideration of the time value of

money. This production was not envisaged in the Demonstration Plant study. Simply put, the

Demonstration Plant, as per the Scoping Study, makes no economic sense. The Scoping Study alludes to

the attraction of expanding production, stating “expansion of production beyond the demonstration plant

would capture substantial economies of scale”.

Page 12

Salt Lake Potash Ltd.

Taylor Collison Limited 12 | P a g e

If SO4 were able to achieve the A$241/t cash cost estimated for the Lake Wells Stage 1 operation (2016

Scoping Study) the gross operating margin would improve by 52% to A$425/t. Given the recent

development skills added by the Company, we expect this opportunity to prove compelling, and it is what

we model, pending further information becoming available.

The Scoping Study announcement suggests the Demonstration Plant is intended to run for between one

to three years (varies between “12-24 months” and “2-3 years”). We would need to model several years

longer than this to deliver even a break-even NPV for the Demonstration Plant our assumed SOP price of

US$500/t and a 10% discount rate. High depreciation charges mean the project is unlikely to deliver

accounting profits at the envisaged scale – hence (in our view) the review into “a larger scale scenario”

for Lake Way, and our decision to assume planned Lake Wells Stage 1 scale production will occur at Lake

Way first.

We see the real value of the Demonstration Plant as in the proof of concept, and the ability to gain market

acceptance for the end product without resorting to substantial initial discounting, together with the

possible proof that partially lined ponds are not needed for harvest ponds. Value is not in the continued

operation of the project at this smaller scale. Pending SO4’s findings from its review into a larger scale

operation, we currently assume ramp up to a 200ktpa rate by DecH2022.

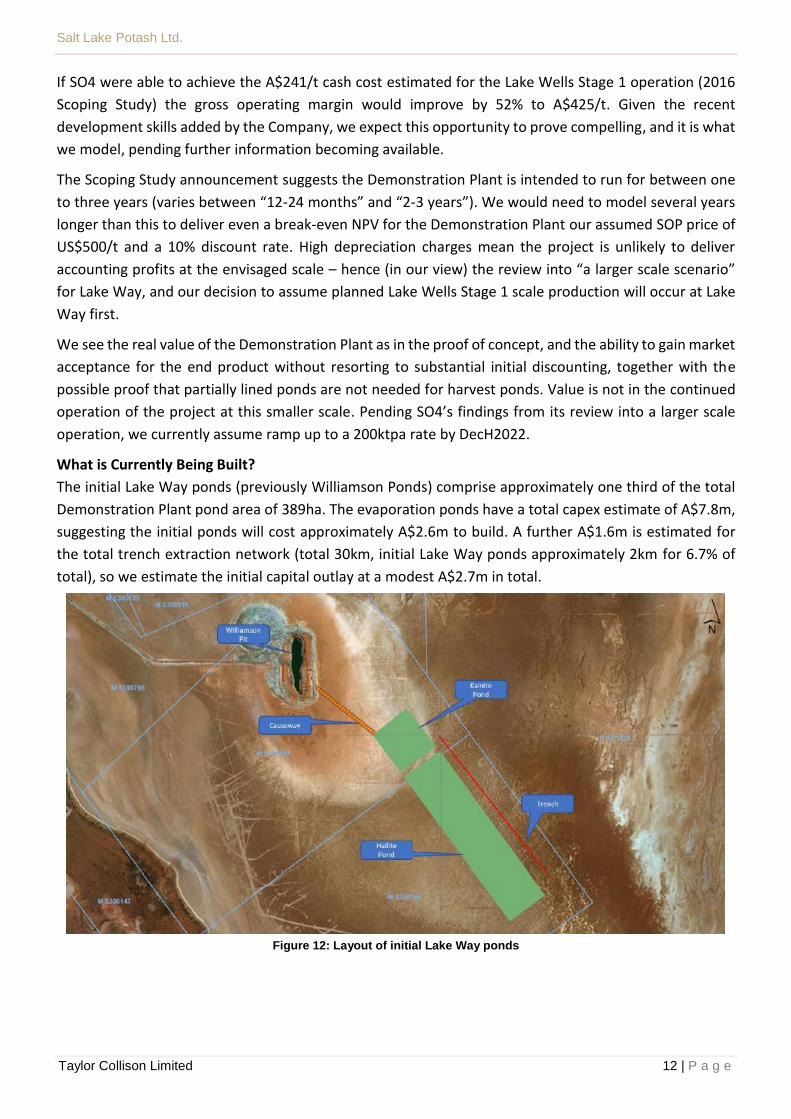

What is Currently Being Built?

The initial Lake Way ponds (previously Williamson Ponds) comprise approximately one third of the total

Demonstration Plant pond area of 389ha. The evaporation ponds have a total capex estimate of A$7.8m,

suggesting the initial ponds will cost approximately A$2.6m to build. A further A$1.6m is estimated for

the total trench extraction network (total 30km, initial Lake Way ponds approximately 2km for 6.7% of

total), so we estimate the initial capital outlay at a modest A$2.7m in total.

Figure 12: Layout of initial Lake Way ponds

Page 13

Salt Lake Potash Ltd.

Taylor Collison Limited 13 | P a g e

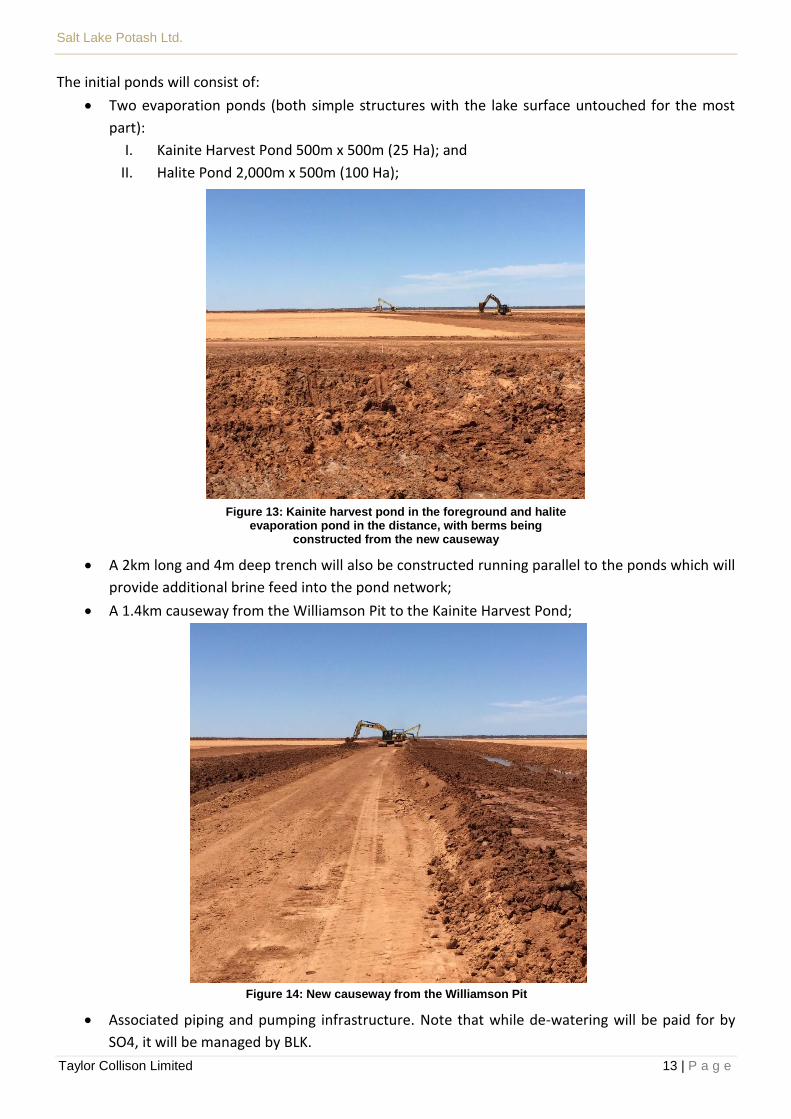

The initial ponds will consist of:

• Two evaporation ponds (both simple structures with the lake surface untouched for the most

part):

I. Kainite Harvest Pond 500m x 500m (25 Ha); and

II. Halite Pond 2,000m x 500m (100 Ha);

Figure 13: Kainite harvest pond in the foreground and halite evaporation pond in the distance, with berms being

constructed from the new causeway

• A 2km long and 4m deep trench will also be constructed running parallel to the ponds which will

provide additional brine feed into the pond network;

• A 1.4km causeway from the Williamson Pit to the Kainite Harvest Pond;

Figure 14: New causeway from the Williamson Pit

• Associated piping and pumping infrastructure. Note that while de-watering will be paid for by

SO4, it will be managed by BLK.

Page 14

Salt Lake Potash Ltd.

Taylor Collison Limited 14 | P a g e

Timing

SO4 has committed to dewatering the Williamson Pit by 30 June 2019 – a process expected to take 76

days to complete. SO4 is aiming to have the initial Lake Way ponds ready to accept brine by 9 April 2019.

While the high-grade brine in the Williamson pit should reduce the timeline for production of salts, the

production of saleable end product at a commercial scale at Lake Way is not imminent. The Scoping Study

estimated 9-12 months would be needed for fabrication and installation of the process plant. Assuming a

decision is taken when the Feasibility Study is expected to be complete, SO4 expected to commission the

plant in early 2020, using stockpiled salts. The longest lead items required have a lead time of

approximately nine months.

Given the published timeline for commissioning, we expect further studies are close to the critical path

for development. We model first sales in JunH2021 with production of 27kt of SOP assumed in the half.

We assume a continued ramp up to a 200ktpa rate in the DecH2022. A Stage 2 expansion at Lake Way

may offer lower capital intensity than the initial development of Lake Wells (as may another lake

altogether), hence our emerging uncertainty around the development timeline for Lake Wells.

Capital and Operating Costs

The Scoping Study for the Demonstration Plant estimated capital costs at A$48.9m (including indirects

and contingency) and operating costs at A$387/t, including a 4% royalty to BLK. Given the expected

lifespan our modelling of this scenario delivers a negative NPV. You would not build it. However, our site

visit highlighted that SO4 are rapidly developing at Lake Way, and the Company has recently acquired

significant development experience.

SO4 has estimated a “whole of lake” resource for Lake Way (73mt) that is approximately 90% of the low

end of the exploration target for Lake Wells (80-85mt) on a drainable basis. Given that:

• the resource scale (8.2mt drainable) is there to support a larger operation,

• the economics of a small operation don’t work, and

• the Company has said it is reviewing a larger operation

we have effectively transferred the Stage 1 production levels, capital and operating costs from the Lake

Wells Scoping Studs to Lake Way, in our modelling. We have added the 4% BLK royalty to these costs for

production from within the BLK tenements (492kt assumed). Pre this royalty, we assume the following

production and costs at Lake Way:

Demonstration Plant Our Model

Annual Production (tpa) – steady state 50,000 200,000

Capital Cost* A$49m A$224m

Operating Cost** A$387/t A$241/t

* Capital Costs based on an accuracy of -10%/+30%.

**Operating Costs based on an accuracy of ±30% including transportation & handling (FOB) but before royalties and depreciation. Private

royalty of 4% payable on production from BLK tenements

Clearly, there is risk involved in this approach, but we do not expect the Demonstration Plant to be built

as per the Scoping Study. It makes no economic sense. We await clarification from the Company on the

development pathway and timeline at Lake Way, and for other lakes making up the broader GSLP.

Page 15

Salt Lake Potash Ltd.

Taylor Collison Limited 15 | P a g e

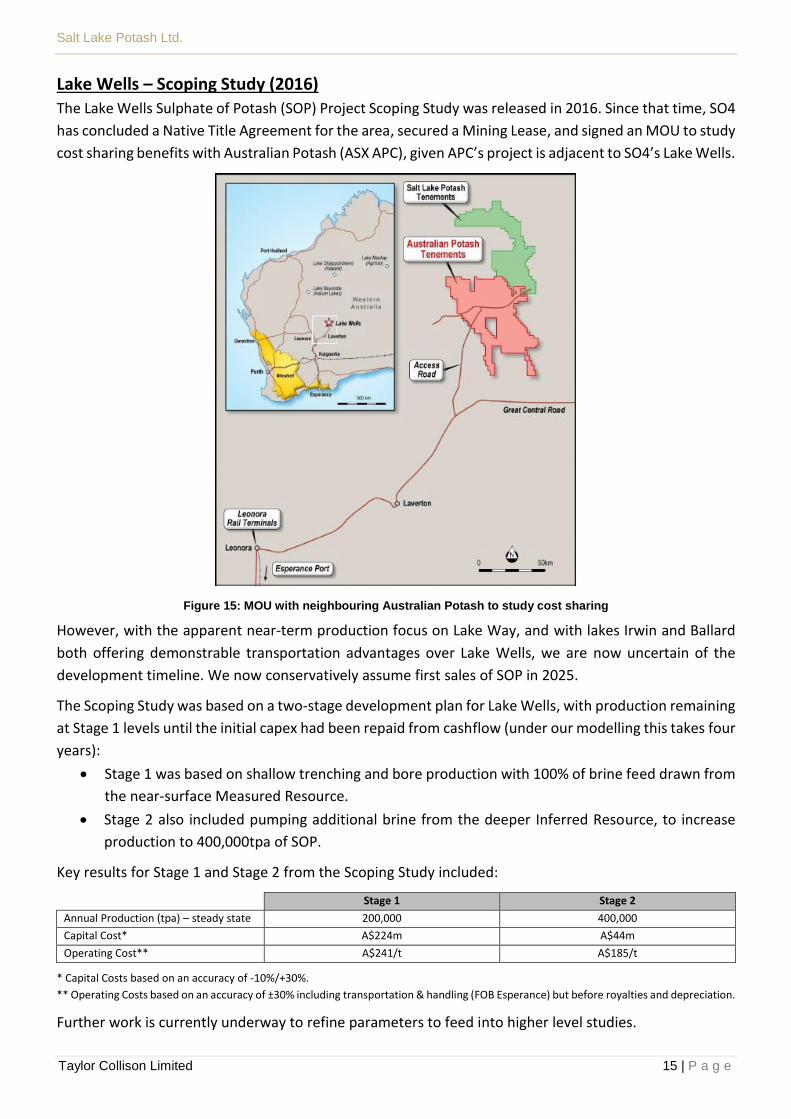

Lake Wells – Scoping Study (2016)

The Lake Wells Sulphate of Potash (SOP) Project Scoping Study was released in 2016. Since that time, SO4

has concluded a Native Title Agreement for the area, secured a Mining Lease, and signed an MOU to study

cost sharing benefits with Australian Potash (ASX APC), given APC’s project is adjacent to SO4’s Lake Wells.

Figure 15: MOU with neighbouring Australian Potash to study cost sharing

However, with the apparent near-term production focus on Lake Way, and with lakes Irwin and Ballard

both offering demonstrable transportation advantages over Lake Wells, we are now uncertain of the

development timeline. We now conservatively assume first sales of SOP in 2025.

The Scoping Study was based on a two-stage development plan for Lake Wells, with production remaining

at Stage 1 levels until the initial capex had been repaid from cashflow (under our modelling this takes four

years):

• Stage 1 was based on shallow trenching and bore production with 100% of brine feed drawn from

the near-surface Measured Resource.

• Stage 2 also included pumping additional brine from the deeper Inferred Resource, to increase

production to 400,000tpa of SOP.

Key results for Stage 1 and Stage 2 from the Scoping Study included:

Stage 1 Stage 2

Annual Production (tpa) – steady state 200,000 400,000

Capital Cost* A$224m A$44m

Operating Cost** A$241/t A$185/t

* Capital Costs based on an accuracy of -10%/+30%.

** Operating Costs based on an accuracy of ±30% including transportation & handling (FOB Esperance) but before royalties and depreciation.

Further work is currently underway to refine parameters to feed into higher level studies.

Page 16

Salt Lake Potash Ltd.

Taylor Collison Limited 16 | P a g e

At this stage of study, we would typically assume capital costs at the upper end of the stated study

accuracy (i.e.+30%). However, given SO4 has entered into a cost sharing agreement with neighbouring

APC we are comfortable that the risk to capital (Stage 1 (200ktpa) A$223.7m, Stage 2 (400ktpa) A$43.9m)

and operating costs (Stage 1 A$240.84/t, Stage 2 A$185.10/t) is likely on the downside in this instance.

Given Lake Wells is on the North East extremity of the GSLP it would appear that this project should

represent the worst-case scenario in terms of capital intensity and operating costs for development and

operation of the other salt lakes in the GSLP.

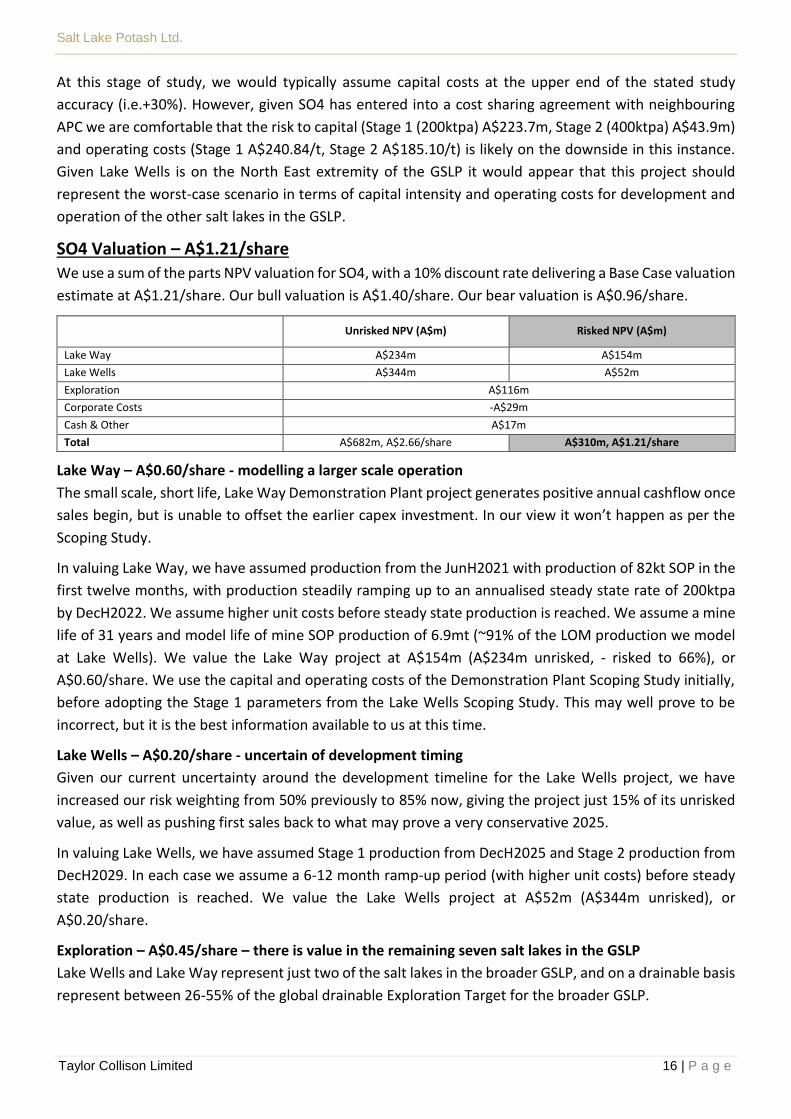

SO4 Valuation – A$1.21/share

We use a sum of the parts NPV valuation for SO4, with a 10% discount rate delivering a Base Case valuation

estimate at A$1.21/share. Our bull valuation is A$1.40/share. Our bear valuation is A$0.96/share.

Unrisked NPV (A$m) Risked NPV (A$m)

Lake Way A$234m A$154m

Lake Wells A$344m A$52m

Exploration A$116m

Corporate Costs -A$29m

Cash & Other A$17m

Total A$682m, A$2.66/share A$310m, A$1.21/share

Lake Way – A$0.60/share - modelling a larger scale operation

The small scale, short life, Lake Way Demonstration Plant project generates positive annual cashflow once

sales begin, but is unable to offset the earlier capex investment. In our view it won’t happen as per the

Scoping Study.

In valuing Lake Way, we have assumed production from the JunH2021 with production of 82kt SOP in the

first twelve months, with production steadily ramping up to an annualised steady state rate of 200ktpa

by DecH2022. We assume higher unit costs before steady state production is reached. We assume a mine

life of 31 years and model life of mine SOP production of 6.9mt (~91% of the LOM production we model

at Lake Wells). We value the Lake Way project at A$154m (A$234m unrisked, - risked to 66%), or

A$0.60/share. We use the capital and operating costs of the Demonstration Plant Scoping Study initially,

before adopting the Stage 1 parameters from the Lake Wells Scoping Study. This may well prove to be

incorrect, but it is the best information available to us at this time.

Lake Wells – A$0.20/share - uncertain of development timing

Given our current uncertainty around the development timeline for the Lake Wells project, we have

increased our risk weighting from 50% previously to 85% now, giving the project just 15% of its unrisked

value, as well as pushing first sales back to what may prove a very conservative 2025.

In valuing Lake Wells, we have assumed Stage 1 production from DecH2025 and Stage 2 production from

DecH2029. In each case we assume a 6-12 month ramp-up period (with higher unit costs) before steady

state production is reached. We value the Lake Wells project at A$52m (A$344m unrisked), or

A$0.20/share.

Exploration – A$0.45/share – there is value in the remaining seven salt lakes in the GSLP

Lake Wells and Lake Way represent just two of the salt lakes in the broader GSLP, and on a drainable basis

represent between 26-55% of the global drainable Exploration Target for the broader GSLP.

Page 17

Salt Lake Potash Ltd.

Taylor Collison Limited 17 | P a g e

We attribute a nominal Exploration Value of A$116m (A$0.45/share), set as 20% of the Lake Wells and

Lake Way valuations combined, as a proxy for the inherent value in the potential integrated development

of the broader GSLP.

Corporate Costs – (A$0.11/share) – a long life impost

Given the long life we assume at Lake Way scoping study we model ongoing corporate costs to 2056,

leading to a corporate impost of A$29m (A$0.11/share) on our valuation for the Company.

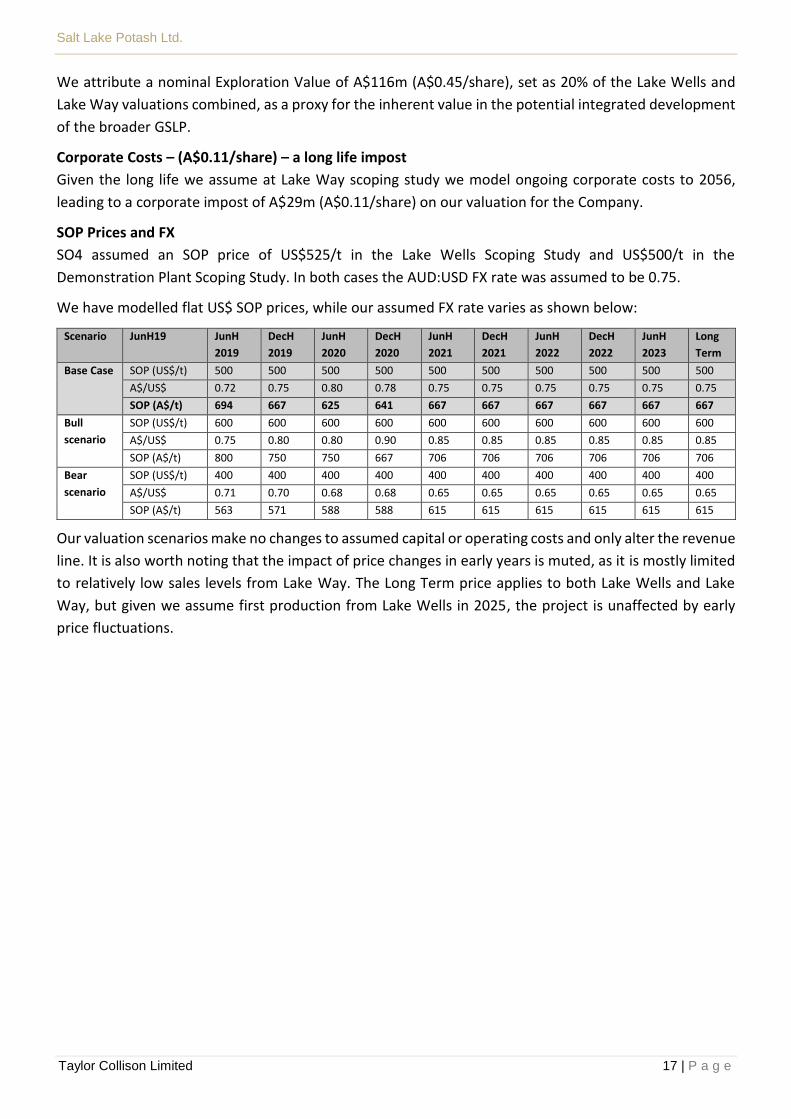

SOP Prices and FX

SO4 assumed an SOP price of US$525/t in the Lake Wells Scoping Study and US$500/t in the

Demonstration Plant Scoping Study. In both cases the AUD:USD FX rate was assumed to be 0.75.

We have modelled flat US$ SOP prices, while our assumed FX rate varies as shown below:

Scenario JunH19 JunH

2019

DecH

2019

JunH

2020

DecH

2020

JunH

2021

DecH

2021

JunH

2022

DecH

2022

JunH

2023

Long

Term

Base Case SOP (US$/t) 500 500 500 500 500 500 500 500 500 500

A$/US$ 0.72 0.75 0.80 0.78 0.75 0.75 0.75 0.75 0.75 0.75

SOP (A$/t) 694 667 625 641 667 667 667 667 667 667

Bull

scenario

SOP (US$/t) 600 600 600 600 600 600 600 600 600 600

A$/US$ 0.75 0.80 0.80 0.90 0.85 0.85 0.85 0.85 0.85 0.85

SOP (A$/t) 800 750 750 667 706 706 706 706 706 706

Bear

scenario

SOP (US$/t) 400 400 400 400 400 400 400 400 400 400

A$/US$ 0.71 0.70 0.68 0.68 0.65 0.65 0.65 0.65 0.65 0.65

SOP (A$/t) 563 571 588 588 615 615 615 615 615 615

Our valuation scenarios make no changes to assumed capital or operating costs and only alter the revenue

line. It is also worth noting that the impact of price changes in early years is muted, as it is mostly limited

to relatively low sales levels from Lake Way. The Long Term price applies to both Lake Wells and Lake

Way, but given we assume first production from Lake Wells in 2025, the project is unaffected by early

price fluctuations.

Page 18

Salt Lake Potash Ltd.

Taylor Collison Limited 18 | P a g e

Funding risk

SO4 remains unfunded for development of the Lake Wells project, the GSLP or even completion of the

full Demonstration Plant, as studied, at Lake Way. Typically, we would assume a nominal capital raising,

diluting our valuation for a greater number of shares to fund expected capex.

SO4 had A$12.0m in cash at the end of 2018 and forecast expenditure of A$5.5m in MarQ2019. There is

no evidence that SO4 expects to slow its capital burn rate, meaning the company will likely need further

funding towards, or shortly after, the end of JunQ2019.

In this instance, with SO4 owning 100% of the projects and with the Lake Wells Scoping Study estimating

first quartile operating costs at scale, we assume other sources of funding - such as offtake funding, pre-

payments or joint ventures may be available.

Given no market ability to hedge production, we would expect any project debt to be provided by non-

bank lenders, but would expect SO4’s predicted bottom quartile positioning on the industry cost curve to

give debt providers a great deal of comfort. We note ASX listed Kalium Lakes (ASX KLL) has secured A$74m

of debt from the Northern Australia Infrastructure Fund (NAIF) and agreed terms for a further A$102m

from German KfW IPEX-Bank. This A$176m of debt represents 81.5% of the proposed Stage 1 project

capex for its Beyondie project in the Northern Territory.

However, at this stage, SO4 remains unfunded and more conservative investors may choose to await

greater clarity around the funding solution.

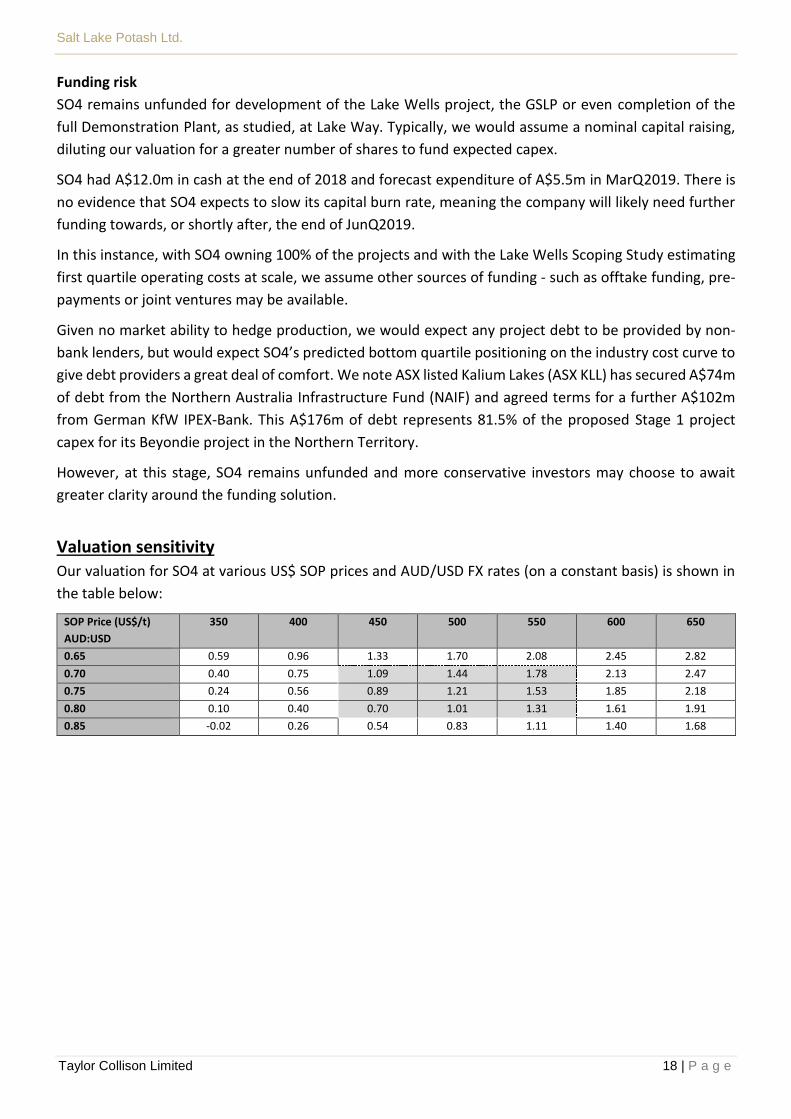

Valuation sensitivity

Our valuation for SO4 at various US$ SOP prices and AUD/USD FX rates (on a constant basis) is shown in

the table below:

SOP Price (US$/t)

AUD:USD

350 400 450 500 550 600 650

0.65 0.59 0.96 1.33 1.70 2.08 2.45 2.82

0.70 0.40 0.75 1.09 1.44 1.78 2.13 2.47

0.75 0.24 0.56 0.89 1.21 1.53 1.85 2.18

0.80 0.10 0.40 0.70 1.01 1.31 1.61 1.91

0.85 -0.02 0.26 0.54 0.83 1.11 1.40 1.68

Page 19

Salt Lake Potash Ltd.

Taylor Collison Limited 19 | P a g e

GSLP - Resource

SO4 has published JORC resource estimates for Lake Wells and Lake Way and has published Exploration

Targets for a further seven of the lakes in the GSLP (as well as Lake Wells on a drainable basis).

Note JORC Resource estimates are calculated on the assumption that it never rains again. The 9mm of

rain received by the site the day prior to our site visit exposes this assumption for the fallacy it is. The

resource estimate assumes a finite resource at a point in time, whereas in reality, rainfall and associated

lake recharge will add to the resource somewhat over time.

Lake Wells - JORC Resource Classification Bulk Volume

(million m3)

Porosity Brine Volume

(million m3)

Average SOP (K2SO4)

Concentration

(kg/m3)

In situ K2SO4

Tonnage (Mt)

Measured 5,427 0.464 2,518 8.94 23

Indicated 775 0.464 359 8.49 3

Inferred* 18,521 0.368 6,275 -2,015* 8.68 54 – 59

Total 24,723 0.392 9,154 – 9,691 8.74 80 -85

*Using Porosities of 0.22 – 0.30 for the Fractured Siltstone Aquifer (aircore drilling prevented porosity analysis of an intact sample)

The Mineral Resource Estimate at Lake Wells totals 80-85 million tonnes of SOP. The Mineral Resource

estimate is based on an average thickness of 52m. The brine pool remains open at depth and laterally in

a number of areas.

Lake Way – “Whole of Lake” JORC Resource

SO4 previously (July 2018) published a resource for Lake Way based solely on the Blackham tenements

(55km2) to a depth of just 6m. SO4 has now released an updated “whole of lake” resource for Lake Way

(an additional 87km2). Just using the Measured and Indicated resource categories for the drainable (rather

than the far higher stored) resource would deliver the following mine lives at Lake Way:

• Demonstration Plant 50,000tpa – 64 years (164 years using total drainable resource)!

• 200,000tpa – 16 years (41 years using total drainable resource)

• 400,000tpa – 8 years (20 years using total drainable resource)

Classification Bulk Volume

(million m3)

Porosity Brine Volume

(million m3)

Average SOP

(K2SO4)

Concentration

(kg/m3)

In situ K2SO4

Tonnage (Mt)

Measured (Williamson Pit) 1.26 NA 25.5 0.03

Measured (Lake) 1,060 43% 456 15.4 6.9

Indicated (Paleochannel) 686 40% 274 13.6 3.7

Inferred 10,216 40% 4,096 15.2 62.2

Total 11,963 4,826 73

Page 20

Salt Lake Potash Ltd.

Taylor Collison Limited 20 | P a g e

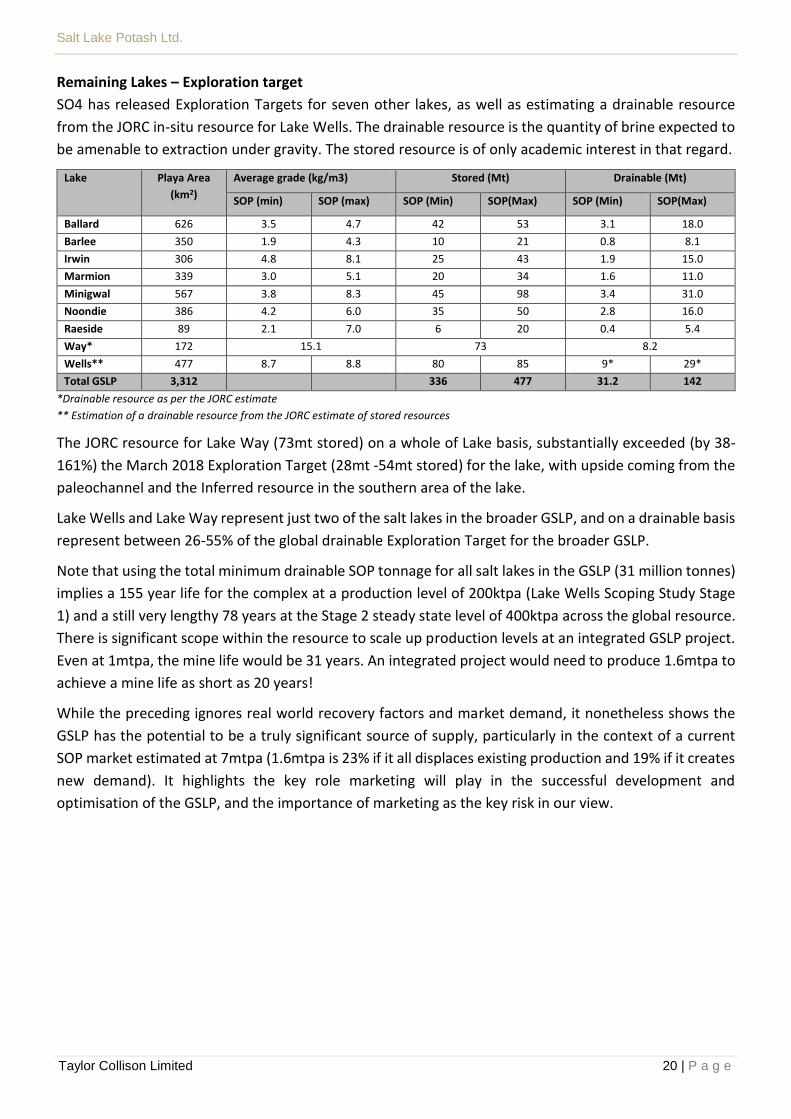

Remaining Lakes – Exploration target

SO4 has released Exploration Targets for seven other lakes, as well as estimating a drainable resource

from the JORC in-situ resource for Lake Wells. The drainable resource is the quantity of brine expected to

be amenable to extraction under gravity. The stored resource is of only academic interest in that regard.

Lake Playa Area

(km2)

Average grade (kg/m3) Stored (Mt) Drainable (Mt)

SOP (min) SOP (max) SOP (Min) SOP(Max) SOP (Min) SOP(Max)

Ballard 626 3.5 4.7 42 53 3.1 18.0

Barlee 350 1.9 4.3 10 21 0.8 8.1

Irwin 306 4.8 8.1 25 43 1.9 15.0

Marmion 339 3.0 5.1 20 34 1.6 11.0

Minigwal 567 3.8 8.3 45 98 3.4 31.0

Noondie 386 4.2 6.0 35 50 2.8 16.0

Raeside 89 2.1 7.0 6 20 0.4 5.4

Way* 172 15.1 73 8.2

Wells** 477 8.7 8.8 80 85 9* 29*

Total GSLP 3,312 336 477 31.2 142

*Drainable resource as per the JORC estimate

** Estimation of a drainable resource from the JORC estimate of stored resources

The JORC resource for Lake Way (73mt stored) on a whole of Lake basis, substantially exceeded (by 38-

161%) the March 2018 Exploration Target (28mt -54mt stored) for the lake, with upside coming from the

paleochannel and the Inferred resource in the southern area of the lake.

Lake Wells and Lake Way represent just two of the salt lakes in the broader GSLP, and on a drainable basis

represent between 26-55% of the global drainable Exploration Target for the broader GSLP.

Note that using the total minimum drainable SOP tonnage for all salt lakes in the GSLP (31 million tonnes)

implies a 155 year life for the complex at a production level of 200ktpa (Lake Wells Scoping Study Stage

1) and a still very lengthy 78 years at the Stage 2 steady state level of 400ktpa across the global resource.

There is significant scope within the resource to scale up production levels at an integrated GSLP project.

Even at 1mtpa, the mine life would be 31 years. An integrated project would need to produce 1.6mtpa to

achieve a mine life as short as 20 years!

While the preceding ignores real world recovery factors and market demand, it nonetheless shows the

GSLP has the potential to be a truly significant source of supply, particularly in the context of a current

SOP market estimated at 7mtpa (1.6mtpa is 23% if it all displaces existing production and 19% if it creates

new demand). It highlights the key role marketing will play in the successful development and

optimisation of the GSLP, and the importance of marketing as the key risk in our view.

Page 21

Salt Lake Potash Ltd.

Taylor Collison Limited 21 | P a g e

ASX-listed Potash Brine Developers

Salt Lake Potash

(SO4)

Australian

Potash

(APC)

Kalium Lakes

(KLL)

Agrimin

(AMN)

Reward

Minerals

(RWD)

Market Cap’. A$117m A$31m A$92m A$99m A$16m

Net Cash (as at

31/12/2018)

A$12.0m A$5.4m* A$5.3m A$10.4m A$3.2m

Project Name Lake Way

Demonstration

Lake Wells Lake Wells Beyondie Mackay SOP Lake

Disappointment

Status of Project Ongoing Pre - Feasibility DFS Underway BFS Complete DFS

Underway

DFS Underway

Steady state

production

50ktpa Stg 1 :200ktpa

Stg 2: 400ktpa

Stg 1: 150ktpa

Stg 2: 300ktpa

(yr 6)

Stg 1: 90ktpa

Stg 2:180ktpa

426ktpa 408ktpa

Mine Life (years) 2-3 (artificially

limited)

20+ 20 30+ 20 23

Initial Capex A$49m Stg 1 A$224m

Stg 2: A$44m

Stg1: A$175m

Stg 2: A$163m

Stg 1: A$216m**

Stg 2: A$125m

A$545m*** A$451m

Operating Cost

(C1)

A$387/t Stg 1: A$241/t

Stg 2: A$185/t

Stg 1: A$368/t

Stg 2: A$339/t

Stg 1: A$224/t

Stg 2: A$182/t

A$296/t*** A$335/t

Capital Intensity

A$/t SOP

A$980/t Stg 1: A$1,120/t

Stg 2: A$670/t

Stg 1: A$1,167/t

Stg 2: A$1,126/t

Stg 1: A$2,400/t

Stg 2: A$1,894/t

A$1,230/t*** A$1,105/t

*Includes A$4.2m gross proceeds from 2019 rights issue

**Debt funding now organised with A$74m approved from NAIF (20/2/19) and agreed terms for a further A$102m from German

KfW IPEX-Bank (19/3/19)

***Converted from USD at an exchange rate of (AUD/USD) = 0.75

Aspirational SOP production from these ASX listed juniors (other than SO4) amounts to 1.3mtpa, or

approximately 19% of the current global market (ignoring whether the ratio between proposed capex and

current market capitalisation suggests development is likely).

This again highlights the importance of marketing in SO4’s development plans. SO4’s position on the cost

curve means it can afford to gain market share by undercutting incumbent suppliers, but the Company

wants to compete on quality not on price. Gaining market share at the premium price desired is the key

risk in our view.

Page 22

Salt Lake Potash Ltd.

Taylor Collison Limited 22 | P a g e

Directors and Management

Ian Middlemas

Chairman

Mr Middlemas is a Chartered Accountant, a member of the Financial Services Institute of Australasia and

holds a Bachelor of Commerce degree. He worked for a large international Chartered Accounting firm

before joining the Normandy Mining Group where he was a senior group executive for approximately 10

years. He has had extensive corporate and management experience, and is currently a Director with a

number of publicly listed companies in the resources sector.

Tony Swiericzuk

Chief Executive Officer

Mr Swiericzuk is a Mining Engineer with outstanding credentials as a builder and operator of mining

projects, having recently been General Manager of the Christmas Creek Mine from 2012 to 2017. He

oversaw the construction, commissioning and ramp-up of this project from 15Mtpa to 60Mtpa in his initial

two year period, then proceeded to optimise the operation and help drive FMG to become the world’s

lowest cost iron ore producer.

In his initial years at FMG Mr Swiericzuk was General Manager Port Operations in Port Hedland and

managed the ramp up from 20Mtpa to 60Mtpa from 2009 to 2011.

Bryn Jones

Non-Executive Director

Mr Jones is a Chemical Engineer with over 20 years management experience in industrial processing in

commercial and mining operations around the world, including potash and phosphate projects.

Mark Pearce

Non-Executive Director

Mr Pearce is a Chartered Accountant and is currently a Director of several listed companies that operate

in the resources sector. He has had considerable experience in the formation and development of listed

resource companies and has worked for several large international Chartered Accounting firms. Mark is

also a Fellow of the Governance Institute of Australia and a Fellow of the Financial Services Institute of

Australasia.

Clint McGhie

Chief Financial Officer & Company Secretary

Mr McGhie is an experienced Chartered Accountant and Company Secretary who commenced his career

at a large international accounting firm and has since been involved with a number of ASX and AIM listed

exploration and development companies operating in the resources sector, including Apollo Minerals

Limited, Berkeley Energia Limited and Sovereign Metals Limited. Mr McGhie is also an Associate Member

of the Governance Institute of Australia (Chartered Secretary), and a Fellow of the Financial Services

Institute of Australasia.

Page 23

Salt Lake Potash Ltd.

Taylor Collison Limited 23 | P a g e

Disclaimer The following Warning, Disclaimer and Disclosure relate to all material presented in this document and should be read before making any

investment decision.

Warning (General Advice Only): Past performance is not a reliable indicator of future performance. This report is a private communication

to clients and intending clients and is not intended for public circulation or publication or for the use of any third party, without the approval

of Taylor Collison Limited ABN 53 008 172 450 ("Taylor Collison"), an Australian Financial Services Licensee and Participant of the ASX Group.

TC Corporate Pty Ltd ABN 31 075 963 352 (“TC Corporate”) is a wholly owned subsidiary of Taylor Collison Limited. While the report is based

on information from sources that Taylor Collison considers reliable, its accuracy and completeness cannot be guaranteed. This report does

not take into account specific investment needs or other considerations, which may be pertinent to individual investors, and for this reason

clients should contact Taylor Collison to discuss their individual needs before acting on this report. Those acting upon such information and

recommendations without contacting one of our advisors do so entirely at their own risk.

This report may contain “forward-looking statements". The words "expect", "should", "could", "may", "predict", "plan" and other similar

expressions are intended to identify forward-looking statements. Indications of and guidance on, future earnings and financial position and

performance are also forward looking statements. Forward-looking statements, opinions and estimates provided in this report are based on

assumptions and contingencies which are subject to change without notice, as are statements about market and industry trends, which are

based on interpretations of current market conditions. Any opinions, conclusions, forecasts or recommendations are reasonably held at the

time of compilation but are subject to change without notice and Taylor Collison assumes no obligation to update this document after it has

been issued. Except for any liability which by law cannot be excluded, Taylor Collison, its directors, employees and agents disclaim all liability

(whether in negligence or otherwise) for any error, inaccuracy in, or omission from the information contained in this document or any loss

or damage suffered by the recipient or any other person directly or indirectly through relying upon the information.

Disclosure: Analyst remuneration is not linked to the rating outcome. Taylor Collison may solicit business from any company mentioned in

this report. For the securities discussed in this report, Taylor Collison may make a market and may sell or buy on a principal basis. Taylor

Collison, or any individuals preparing this report, may at any time have a position in any securities or options of any of the issuers in this

report and holdings may change during the life of this document.

The preparation of this report was funded by ASX in accordance with the ASX Equity Research Scheme. This report was prepared by Taylor

Collison and not by ASX. ASX does not provide financial product advice. The views expressed in this report do not necessarily reflect the views

of ASX. No responsibility or liability is accepted by ASX in relation to this report.

Analyst Interests: The Analyst(s) may hold the product(s) referred to in this document, but Taylor Collison Limited considers such holdings

not to be sufficiently material to compromise the rating or advice. Analyst(s)’ holdings may change during the life of this document.

Analyst Certification: The Analyst(s) certify that the views expressed in this document accurately reflect their personal, professional opinion

about the financial product(s) to which this document refers.

Date Prepared: March 2019

Analyst: Colin McLelland BE, GDAFI, MBA

Release Authorised by: David Cutten