46

SAMPLE REPORT: JAPAN April 2018 – (The data in the sample report may not be the latest data available in the service). COUNTRY ENERGY REPORT- SAMPLE Report Sample

SAMPLE REPORT: JAPAN April 2018 – (The data in the sample report may not be the latest data

available in the service).

COUNTRY ENERGY REPORT-SAMPLE

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 1

*Reproduction in whole or in part prohibited without written permission.

Table of contents

Table of contents ______________________________ 1

List of graphs & tables __________________________ 2

Overview ____________________________________ 4

Institutions and energy policy ____________________ 6

Energy companies ____________________________ 13

Energy supply ________________________________ 17

Energy prices ________________________________ 22

Energy consumption __________________________ 24

Issues and prospects __________________________ 30

Graphs & data files ___________________________ 36

Abbreviations ________________________________ 40

Glossary ____________________________________ 42

→

Report

Sample

World Energy Research

2 Energy Report Sample—Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved

*Reproduction in whole or in part prohibited without written permission.

List of graphs & tables

List of graphs

Graph 1: CO2-energy emissions (MtCO2) ----------------------------------------------------------------------------------------------------- 11

Graph 2: Installed electric capacity by source (2017, %) --------------------------------------------------------------------------------- 18

Graph 3: Gross power production by source (TWh) --------------------------------------------------------------------------------------- 19

Graph 4: Power generation by source (2017, %) ------------------------------------------------------------------------------------------- 19

Graph 5: Map of natural gas infrastructure -------------------------------------------------------------------------------------------------- 21

Graph 6: Gasoline & diesel prices (US$/l) ---------------------------------------------------------------------------------------------------- 22

Graph 7: Electricity prices for industry and households (US$c/kWh)------------------------------------------------------------------ 23

Graph 8: Gas prices for industry and households (US$c/kWh GCV) ------------------------------------------------------------------- 23

Graph 9: Consumption trends by energy source (Mtoe) --------------------------------------------------------------------------------- 24

Graph 10: Total consumption market share by energy (2017, %) ---------------------------------------------------------------------- 25

Graph 11: Final consumption market share by sector (2017, %) ----------------------------------------------------------------------- 25

Graph 12: Oil consumption (Mt) --------------------------------------------------------------------------------------------------------------- 26

Graph 13: Oil consumption breakdown by sector (2017, %) ---------------------------------------------------------------------------- 26

Graph 14: Electricity consumption (TWh) ---------------------------------------------------------------------------------------------------- 27

Graph 15: Electricity consumption breakdown by sector (2017, %) ------------------------------------------------------------------- 27

Graph 16: Natural gas consumption (bcm) -------------------------------------------------------------------------------------------------- 28

Graph 17: Gas consumption breakdown by sector (2017, %) --------------------------------------------------------------------------- 28

Graph 18: Coal and lignite consumption (Mt) ----------------------------------------------------------------------------------------------- 29

Graph 19: Coal and lignite consumption breakdown by sector (2017, %) ------------------------------------------------------------ 29

List of tables

Table 1: Economic indicators

• Population, GDP growth

• Imports & exports

• Inflation rate, exchange rate

• Energy security and efficiency indicators

• CO2 emissions

→

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 3

*Reproduction in whole or in part prohibited without written permission.

Table 2: Supply indicators

• Oil & Gas proven reserves

• Electric & refining capacity detailed by source

• Production by energy source

• Power production by source

• External trade by energy source

Table 3: Demand indicators

• Consumption / inhabitant and consumption trends

• Total consumption by energy source

• Final consumption by energy source and by sector

• Electricity consumption by sector

Table 4: Energy Balance

• Total energy balance

• Detailed energy balance by energy source

Table 5: Power Infrastructures

• Main power plant projects by energy, technology, status and operator

Table 6: Gas infrastructures and contracts

• Main gas plant projects

• Main LNG contracts

Report

Sample

World Energy Research

4 Energy Report Sample—Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved

*Reproduction in whole or in part prohibited without written permission.

Overview

Map Source: OCHA/ReliefWeb

Highlights

Despite the 2011 Fukushima disaster that has spurred many debates on nuclear energy, nuclear will remain a key pillar of the energy supply. Faced with volatile energy prices, the latest energy policy has made supply security, cost reduction, the environment and safety the top priorities. The Government is making progress in the liberalisation of the energy sector. Electricity generation is still dominated by a few vertically-integrated private companies. The top 10 utilities represent more than 75% of the power production market. The oil sector deregulation led to the restructuring of the companies via expansions and mergers of refineries to reduce the costs. The gas sector has many regional private players. Due to a lack of domestic resources and a highly-developed economy, Japan is among the world’s biggest importers of oil, gas and coal. The renewables capacity has also grown substantially in recent years, especially solar PV: the country ranks second in the world in terms of PV installed capacity. National oil prices follow international oil prices. Electricity prices are controlled by METI through an automatic adjustment mechanism. Energy intensity has been decreasing since 2000. The industry sector (including non-energy uses) is the largest energy consumer. Oil has the largest share in energy consumption. The country is facing pressure to reach its 2030 CO2 emissions and power mix targets, leading to tighter regulations for coal projects and the development of projects using CCS, whereas renewable energy projects are expected to grow rapidly in the near future. The gas import capacity is expected to increase since the Government is encouraging fuel switching to gas in the end-use sectors.

→

→

→

→

→

→

→

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 5

*Reproduction in whole or in part prohibited without written permission.

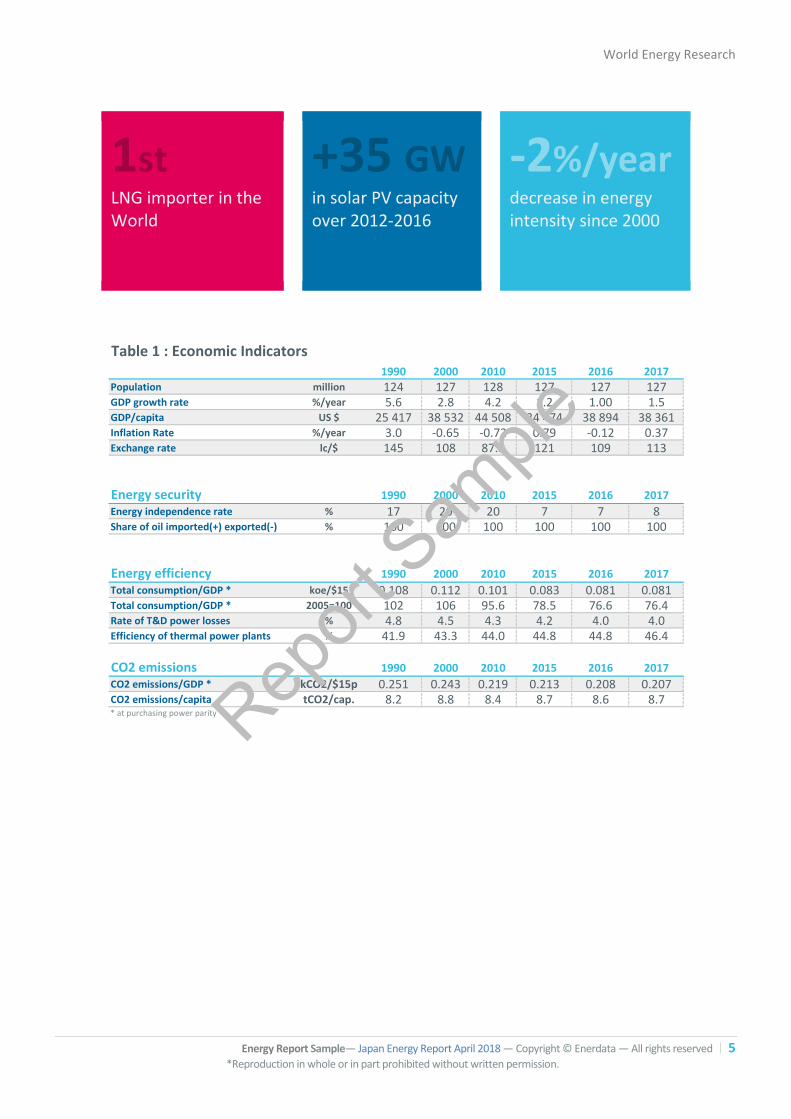

1st LNG importer in the World

+35 GW in solar PV capacity over 2012-2016

-2%/year decrease in energy intensity since 2000

Table 1 : Economic Indicators1990 2000 2010 2015 2016 2017

Population million 124 127 128 127 127 127GDP growth rate %/year 5.6 2.8 4.2 1.2 1.00 1.5GDP/capita US $ 25 417 38 532 44 508 34 474 38 894 38 361Inflation Rate %/year 3.0 -0.65 -0.72 0.79 -0.12 0.37Exchange rate lc/$ 145 108 87.8 121 109 113

Energy security 1990 2000 2010 2015 2016 2017

Energy independence rate % 17 20 20 7 7 8Share of oil imported(+) exported(-) % 100 100 100 100 100 100

Energy efficiency 1990 2000 2010 2015 2016 2017

Total consumption/GDP * koe/$15 0.108 0.112 0.101 0.083 0.081 0.081Total consumption/GDP * 2005=100 102 106 95.6 78.5 76.6 76.4Rate of T&D power losses % 4.8 4.5 4.3 4.2 4.0 4.0Efficiency of thermal power plants % 41.9 43.3 44.0 44.8 44.8 46.4

CO2 emissions 1990 2000 2010 2015 2016 2017

CO2 emissions/GDP * kCO2/$15p 0.251 0.243 0.219 0.213 0.208 0.207CO2 emissions/capita tCO2/cap. 8.2 8.8 8.4 8.7 8.6 8.7* at purchasing power parity Rep

ort Sam

ple

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 6

*Reproduction in whole or in part prohibited without written permission.

The residential electricity sector has been

open to competition since April 2016

Institutions and energy policy

Despite the 2011 Fukushima disaster that has spurred many debates on nuclear energy, nuclear will remain a key pillar of the energy supply.

Faced with volatile energy prices, the latest energy policy has made supply security, cost reduction, the environment and safety the top priorities.

The METI, Ministry of Economy, Trade and Industry, is in charge of the

energy sector through ANRE, Agency for Natural Resources and Energy.

ANRE has three departments: the Energy Conservation and Renewable

Energy Department, the Natural Resources and Fuel Department, and the

Electricity and Gas Industry Department.

EGC, Electricity and Gas Market Surveillance Commission, has been

implemented in 2015 to strengthen the monitoring of both markets.

The Strategic Energy Plan of Japan (2014) stipulates the main goals of the

country’s energy policy, based on the Basic Act on Energy Policy. It

designates nuclear power as an important long-term electricity source,

overturning the nuclear phase-out envisaged after the 2011 Fukushima

accident. The country will also seek to boost renewables. As of April 2018,

METI’s expert committee is finalising its long-term energy plan (to 2050)

proposal, which designates renewable energy sources and nuclear power

as major energy sources in the future, with an emphasis on advancing the

development of energy storage and hydrogen. The committee

recommended phasing-out and replacing inefficient coal-fired power

plants with gas power plants. METI aims to finalise the long-term energy

plan by summer 2018.

Electricity

ESCJ, Electric Power System Council of Japan, regulates the electricity

sector.

Under the Policy on the Electricity System Reform, the deregulation of the

retail market was launched in April 2016 and the residential sector was

open to competition. The unbundling of the power transmission and

→

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 7

*Reproduction in whole or in part prohibited without written permission.

Nuclear target: 20-22% of power mix in 2030

distribution activities is planned for April 2020. This market opening

reform ends the monopoly of the ten regional electricity companies and

aims to boost competition and lower prices, which are among the highest

in the world. Utilities have long been opposed to such a move, but the

Fukushima accident has weakened their lobbying power.

An Organization for Cross-regional Coordination of Transmission

Operators (OCCTO) was set up in 2015 to aggregate and evaluate the

electricity supply plans from various companies, to oversee the cross-

regional operation of supply/demand and the network, and to draw up

the rules of the network code and power bidding.

Since the full opening of the retail residential electricity market, the

number of electricity retailers has ballooned from the 10 vertically

integrated utilities to about 400 companies. Non-power utility retailers are

expected to account for more than 10% of Japan’s electricity consumption

soon. However, former regional monopolies still generate most of the

power, while new retail companies must purchase power from higher-cost

plants such as gas-fired power plants. In December 2016, the METI

announced that it plans to implement a baseload power market to

improve competition by ensuring equal access to cheap power supplies

for new retail companies. This new scheme is planned to start during the

fiscal year 2019-2020.

The Japan Electric Power Exchange (JPEX) was set up in 2003. Following a

request from METI, Japan’s nine major utilities have pledged to allocate at

least 10% of their sales for competitive bidding during the fiscal year

starting 1 April 2018. This volume (which was previously locked up in

bilateral agreements) will boost JPEX’s trading volume to exceed a 15%

share in Japan’s total domestic power demand during the same period.

Nuclear

The Energy White Paper (Annual Report on Energy), which was approved

by the Cabinet in 2014, calls for a nuclear revival. In 2015, the Government

released plans to achieve a 20-22% share of nuclear in the power mix by

2030. The government is expected to maintain this target nuclear share in

the next long-term energy plan, which it is finalising, as nuclear is

considered a major energy source for Japan’s future.

Following the Fukushima nuclear accident, a new nuclear regulatory

agency, the Nuclear Regulation Authority (NRA), was created in 2012. It

issued new nuclear safety rules that took effect in 2013. Since then, only 6

reactors have cleared NRA inspections and resumed operations, namely

Sendai-1 and 2, Ohi-3 (Kyushu Electric), Takahama-3 and 4, Genkai-3

Report

Sample

8 Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved *Reproduction in whole or in part prohibited without written permission.

The 4th Strategic Energy Plan

introduced full competition in the gas retail business in 2017

Energy efficiency target: 30% of energy savings by 2030

compared to 2006

(Kansai Electric). Shikoku Electric’s Ikata-3 also cleared inspection but was

ordered by the Hiroshima High Court to shut down until September 2018.

In addition, Kansai Electric’s Ohi-4 reactor and Kyushu Electric’s Genkai-4

reactor are scheduled for restart in May 2018.

In 2013, Japan created an authority dedicated to the dismantling of four

Fukushima nuclear units. The International Research Institute for Nuclear

Decommissioning (IRID) will be in charge of conceiving new technologies

and processes to clean up the nuclear site, including withdrawing spent

fuel.

Oil

Due to the lack of domestic resources, the energy policy incentivises

companies to pursue overseas exploration projects in order to secure the

supply.

Gas

The opening of the gas market took place in several phases: first for

customers consuming more than 217 mcm/year in 1994 and, after several

revisions, the threshold was lowered to 0.1 mcm/year in 2007. In 1999 the

law also introduced third party access to the gas transmission networks.

The government has implemented the full liberalisation of Japan’s gas

retail market since April 2017. Gas transmission and distribution networks

operated by the three largest gas suppliers, namely Tokyo Gas, Osaka Gas

and Toho Gas, will be transferred to companies that will become legally

separated in 2022, in order to open access to new entrants.

In 2014, Japan launched its LNG Futures market on the Japan OTC

Exchange (JOE) to bring more transparency to the spot deals and to lower

the price of LNG.

Energy efficiency

The Energy Efficiency Policy is governed by the Energy Conservation Law

(Rational Use of Energy Act, 1979), which was last amended in 2013. In

March 2018, the government approved a partial revision to the Rational

Use of Energy Act to establish a new evaluation system for inter-business

collaborations in energy conservation and to revise the energy

conservation classification of consignors in the goods transportation

sector. In 2006, the New National Energy Strategy, including the Energy

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 9

*Reproduction in whole or in part prohibited without written permission.

Renewable energy target: 10% of the primary energy

consumption by 2020

Conservation Frontrunner Plan, set the target to improve energy efficiency

by at least 30% by 2030 compared to 2006.

Energy efficiency standards, known as the “top-runner programme”, have

existed since 1998. They currently concern about 32 products and types of

equipment, including household and commercial electrical appliances,

lamps, road vehicles, heating and cooking appliances and industrial

electric equipment (e.g. motors, transformers), with up to 3 updates for

some of them. For passenger cars, the 2015 target represented an

increase of about 24% in average fuel efficiency compared to 2004 levels.

The vehicle efficiency targets are generally set at 5-year intervals, with the

government targeting an average passenger car fleet fuel economy of

20.3 km/l by 2020, a 24% increase from 2009 levels and a 19.6% increase

from the 2015 actual results.

In industry, and in the commercial sector since 2008, large companies are

obliged to name an “energy manager” who is responsible for the

implementation of an energy plan and who has to report statistics to the

METI.

In 2015, the METI announced plans to invest US$779m to finance the

implementation of energy efficiency devices, such as LED lamps or high-

efficiency boilers by SMEs and industries. In 2016, the government

introduced new energy efficiency benchmarks and standards for existing

and new thermal power plants, and revised the calculation method for

energy efficiency evaluation to promote the effective utilization of waste

heat.

Renewables

Under the Strategic Energy Plan of Japan, the country intends to supply

10% of its primary energy from renewables by 2020. In the government’s

proposed long-term energy plan, renewables are recognized as a major

energy source for Japan’s future. METI is expected to maintain the current

generation mix target share for renewables at 22-24% (including

hydropower) by 2030.

Feed-in tariffs (FITs) were introduced for solar PV (for surplus electricity

production only) in 2009. In 2011, FITs were extended to other

renewables. Since 2012, the new scheme applies to all generated

electricity. The scheme will be reviewed at least every three years and is

scheduled for a major review in 2020.

In 2015, the Government started to review the FiTs with the aim of

lowering them and to tackle grid instability (large share of solar) and the

Report

Sample

10 Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved *Reproduction in whole or in part prohibited without written permission.

improper use of guaranteed FiTs by some business owners (e.g. delaying

solar projects to take advantage of falling panel costs).

In 2012-2013, FiTs were among the highest in the world (twice the level of

Germany and over three times that of China for solar). The FiTs for non

residential solar PV systems >10 kW have been reduced several times

since 2013 to reflect declining costs and increasing utilization rates of solar

facilities. The latest reduction will apply to facilities certified in and after

April 2018, with the FiT dropping from Yen 21/kWh (US$19c/kWh) to Yen

18/kWh (US$16c/kWh). Current tariffs are, therefore, almost half the

initial levels set in July 2012 (Yen 40/kWh or US$36c/kWh). Since April

2017, non-residential PV projects > 2 MW are no longer eligible to FITs.

To boost offshore wind development, the METI introduced a specific FIT

for offshore wind in 2014. The FiT for offshore wind and small-scale wind

will remain at Yen 36/kWh (US$32c/kWh) and Yen 55/kWh (US$50c/kWh),

respectively, until FY 2019, while the FiT for large-scale (>20 kW) onshore

wind will decrease from Yen 21/kWh (US$19c/kWh) in FY 2017 to Yen

19/kWh (US$17c/kWh) in FY 2019. The FiT for repowering wind projects

will decreased from Yen 18/kWh (US$16c/kWh) in FY 2017 to Yen 16/kWh

(US$14c/kWh).

FITs for geothermal facilities are set for 15 years at US$28.2c/kWh

(>15 MW) and at US$43.4c/kWh (<15 MW). FITs for small and medium

hydropower are set at US$35c/kWh <200 kW), US$30c/kWh (between

200 kW and 1 MW) and US$25c/kWh (>1 MW), respectively, for 20 years

(from April 2015).

For biomass projects above 2 MW, the Yen 24/kWh (US$22c/kWh) tariff

will progressively fall to Yen 21/kWh (US$19c/kWh) from 1 September

2017 to FY 2019, while smaller installations will benefit from a tariff of Yen

24/kWh (US$22c/kWh).

In May 2016, the government revised the Act on Special Measures for

Renewable Energy, which includes changes in FiTs to promote a larger mix

of renewables, as the existing FiTs favoured solar PV. Since April 2017, FiTs

for large scale PV projects (non-residential >2 MW) have been shifted to a

tendering program initiated by METI. Under this “reverse auction system”,

companies will submit bids and compete to supply a fixed amount of

power to the utilities at the best possible costs. The bids will be accepted

from the lowest bid upwards until the capacity available at the auction is

completely allocated. Meanwhile, other renewables energies, i.e.

geothermal, hydro, and biomass, will benefit from a slightly more

favorable tariff framework.

Feed-in tariffs

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 11

*Reproduction in whole or in part prohibited without written permission.

GHG reduction target: 26% below 2013

levels by 2030

CO2

Japan met its Kyoto commitment to reduce its GHG emissions by 6% by

2008-2012 compared to the 1990 level. In 2017, Japan’s CO2 emissions

were 8% above the 1990 level (lower nuclear generation).

In its First NDC, Japan aims to reduce GHG emissions to 1.04 GtCO2eq by

fiscal year (FY) 2030, 26% below FY 2013 levels. In November 2016, the

country ratified the Paris Agreement on climate change.

Since the shutdown of most of the nuclear reactors after Fukushima and

the increase in thermal generation, Japan decided to scale back its 25%

reduction target for 2020 to 3.8% (compared to 2005 levels); this

translates into a 3% increase compared to the 1990 level. The long-term

goal, announced in 2008, is to reduce greenhouse gas emissions by 80%

by 2050 compared to 1990.

CO2 emissions from energy combustion peaked in 2013 following the

closure of nuclear reactors but have since declined slightly through to

2017.

GRAPH 1: CO2-ENERGY EMISSIONS (MtCO2)

0

200

400

600

800

1 000

1 200

1 400

The The Government announced in 2012 its intention to introduce a

national compulsory emissions trading scheme for large CO2 emitting

companies. However, in the face of strong opposition from industries, the

government scrapped the proposal and instead introduced the Feed-in

Tariff (FiT) scheme and a Global Warming Countermeasures tax (GW Tax),

which aims to limit energy-related CO2 emissions by placing a tax on fossil

fuel usage. Since April 2016, the GW Tax has been set at JPY 289/tCO2

(US$2.7/tCO2).

Emission trading scheme

Report

Sample

12 Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved *Reproduction in whole or in part prohibited without written permission.

In 2010, the Tokyo Metropolitan Government launched a mandatory cap

and trade scheme to reduce its GHG emissions by 25% by 2020 and 30%

by 2030 (compared with 2000). At the end of the first compliance period

(FY2010-2014), a 25% emission reduction was achieved; the second

compliance period started in 2015 and should last until 2019, with a

reduction target of 15-17% from base-year emissions. Japan’s fiscal year

(FY) runs between 1 April and 31 March.

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 13

*Reproduction in whole or in part prohibited without written permission.

JERA Integration of Tepco and

Chubu fossil fuel generation forms largest generator

Energy companies

The Government is making progress in the liberalisation of the energy sector.

Electricity generation is still dominated by a few vertically-integrated private companies. The top 10 utilities represent more than 75% of the power production market.

The oil sector deregulation led to the restructuring of the companies via expansions and mergers of refineries to reduce the costs.

The gas sector has many regional private players.

Electricity

The electricity sector is dominated by 10 regional, private companies (the

“Ten EPCOS”), vertically integrated and grouped together in the

Federation of Electric Power Companies (FEPC), and by J-Power (also

called EPDC), which until 2004 was a public company. The EPCOs’

monopoly in their region ended in April 2016 with the liberalization of the

retail electricity market: almost 400 companies are now registered to sell

electricity. The Ten EPCOS account for more than ¾ of the electricity

produced in Japan with the three largest - TEPCO, Kansai and Chubu -

representing about 60% of the installed capacity and sales of the Ten

EPCOS.

In October 2017, Tokyo Electric Power Company Holdings (Tepco) and

Chubu Electric Power Co received approval from the Japan Fair Trade

Commission (JTFC) to integrate their fossil fuel power plants under their

JERA Co joint venture. The biggest and third-biggest of Japan's power

utilities will combine their businesses in April-September 2019 to form a

company aggregating 68 GW of generation capacity.

TEPCO (Tokyo EPCO) currently has a capacity of over 67 GW (13 GW of

nuclear, 31 GW of LNG/LPG, 3.2 GW of coal, 11 GW of oil and 10 GW of

hydro, end of FY 2016). Prior to the Fukushima accident in 2011, its

nuclear capacity was 17.3 GW. The 6 Fukushima Daichi nuclear reactors

have now been permanently closed. TEPCO power generation has

→

Report

Sample

14 Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved *Reproduction in whole or in part prohibited without written permission.

decreased significantly, from 264 TWh in 2010 to 200 TWh in FY2016, and

its sales dropped to 242 TWh from 317 TWh in 2010 (FY2016: fiscal years

ending in March 2017). Following TEPCO’s nationalisation in 2012, the

Nuclear Damage Liability Facilitation Fund is now the company’s main

shareholder with a 54.69% stake. In December 2016, the government

announced that TEPCO could remain nationalized longer than initially

planned, but that the government would progressively reduce its

involvement in the management through the Nuclear Damage Liability

Facilitation Fund. The METI is also considering an alternative solution to

split TEPCO into "business operations" (power generation and retail sales)

and "Fukushima operations" (decommissioning operations and

compensation payment), with the latter entity remaining under public

control.

Kansai EPCO has a capacity of 36.6 GW and sales of 121.5 TWh (FY 2016).

Kansai has 11 nuclear reactors (9 GW). The company restarted operations

at Units 3 and 4 of the Takahama nuclear facility in June 2017 and the

Ohi-3 reactor in April 2018 (Ohi-4 is scheduled for May 2018).

Chubu EPCO has a capacity of 33 GW and sales of 122 TWh (FY2015).

The other companies are, in order of importance: Kyushu (29 GW, 79 TWh

of sales), Tohoku (19 GW, 74 TWh of sales), Chugoku (12 GW, 57 TWh of

sales), Hokuriku (8 GW, 28 TWh of sales), Hokkaido (8 GW, 27 TWh of

sales), Shikoku (6.3 GW, 30 TWh of sales), and Okinawa (2.1 GW, 7.8 TWh

of sales) (FY2016).

J-Power has a capacity of 17.8 GW (including affiliated companies), made

up of 8.8 GW thermal, 8.6 GW hydro, and 0.4 GW of wind (April 2017).

Total Sales in FY 2016 were 62.2 TWh. It was privatised in 2004 through

the sale by the State of 83% of its capital.

Japan Nuclear Fuel Ltd (JNFL) is a private venture led by the nation's ten

electric utilities to develop a "closed" nuclear fuel cycle. About 1/3 of the

capital will be contributed by TEPCO.

Nuclear Fuel Industries Ltd. has been Japan’s sole producer of nuclear fuel

since 1972. In 2009, Westinghouse Electric acquired a 52% stake in the

company from Furukawa Electric Co and Sumitomo Electric Industries,

which now hold the remaining 48% (24% each

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 15

*Reproduction in whole or in part prohibited without written permission.

JOGMEC was created in 2004 to help oil and gas companies to expand

overseas, mainly in E&P activities

Oil

Around thirty Japanese companies produce oil abroad and import it into

Japan. JOGMEC, Japan Oil, Gas and Metals National Corporation, supports

the oil and gas companies in conducting oil and gas exploration and

development efforts overseas and offshore Japan. JOGMEC provided

financial assistance to more than 50 companies for exploration activities.

In November 2016, the parliament adopted a bill allowing JOGMEC to

invest in foreign oil and gas companies. So far, the company was restricted

to supporting acquisitions of foreign natural resource assets by Japanese

companies. This should help Japan compete for global energy assets and

improve its energy supply. JOGMEC manages the national level petroleum

stockpiling.

To reduce costs, refineries are moving towards mergers and acquisitions.

JX Nippon Oil & Energy, Japan’s largest oil group with refineries with a

total capacity of 1.1 mb/d as of December 2016, integrated its business

with TonenGeneral on 1 April 2017 to form JXTG Nippon Oil & Energy.

The new company holds nearly 2 mb/d of refining capacity, controls half

of the Japanese gasoline market, and operates more than 14 000 retail

gasoline outlets in the country.

Until then, Tonen/General was one of the other large refiners (3 refineries

with a total capacity of 0.5 mb/d).

In 2015 Idemitsu Kosan and Showa Shell Sekiyu announced their merger

(acquisition by Idemitsu Kosan of 33.24% stake in Showa Shell Sekiyu, 6

refineries) to form the second largest oil refining company (0.8 mb/d),

controlling around 28% of the refining market. The integration of their key

businesses will be completed in spring 2018.

The remaining large refiner is Cosmo Oil (3 refineries with a total capacity

of 0.5 mb/d).

Gas

Three companies account for more than 80% of the gas supply: Tokyo Gas

(15.7 bcm of sales volume in FY 2016), Osaka Gas (8.7 bcm) and Toho Gas

(3.9 bcm). There are around 200 gas companies, 85% of which are private;

they are grouped together in the Japan Gas Association (JGA).

Inpex was set up to develop gas projects, in particular LNG imports to

Japan (about ¼ of total LNG imports). Initially, Inpex was public through

the 54% stake owned by JNOC, but the company was privatised in 2004.

Upstream

Downstream

Report

Sample

16 Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved *Reproduction in whole or in part prohibited without written permission.

Inpex holds shares in the LNG plant of Bontang and holds a 65% operating

interest in the Masela Abadi LNG project in Indonesia.

JERA, the joint venture of TEPCO and Chubu Electric, signed a Sales and

Purchase Agreement (SPA) in May 2016 with EDF Trading for the sale of

1.5 Mt of LNG over a 2.5-year period starting in June 2018.

Tokyo Gas and Kansai Electric signed a strategic cooperation agreement in

April 2016 to jointly source LNG on global markets. The two companies

will cooperate on LNG imports, especially from the Pluto LNG project in

Australia, as both have 15-year LNG import deals with that project

(1.5 Mt/year for Tokyo Gas and 1.75 Mt/year for Kansai Electric), as well

as from the Cove Point LNG project (20-year supply agreement for

1.4 Mt/year for Tokyo Gas and 0.8 Mt/year for Kansai Electric).

In April 2017, Tokyo Gas also partnered with Kyushu Electric to jointly

purchase LNG to reduce costs and enhance supply stability. The alliance

allows Kyushu Electric to offload its LNG contracted volumes following the

successful restart of its Sendai nuclear reactors and pending restart of its

Genkai nuclear reactors. The alliance also enables Tokyo Gas to defend

some of its market share from JERA.

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 17

*Reproduction in whole or in part prohibited without written permission.

Since 2013 4 nuclear units have

restarted and continued operating as of end-2017

Energy supply

Due to a lack of domestic resources and a highly-developed economy, Japan is among the world’s biggest importers of oil, gas and coal.

The renewables capacity has also grown substantially in recent years, especially solar PV: the country ranks second in the world in terms of PV installed capacity.

Resources

Japan has limited resources (around 6.2 Mt of oil and 29.3 bcm of gas in

2016) and fossil fuel production is very low compared to the demand.

ANRE estimates that the economically exploitable potential of renewable

energies amounts to 38-64 Mtoe/year (including 10-21 Mtoe of solar and

7-10 Mtoe of waste); the technical potential is estimated at

127 Mtoe/year.

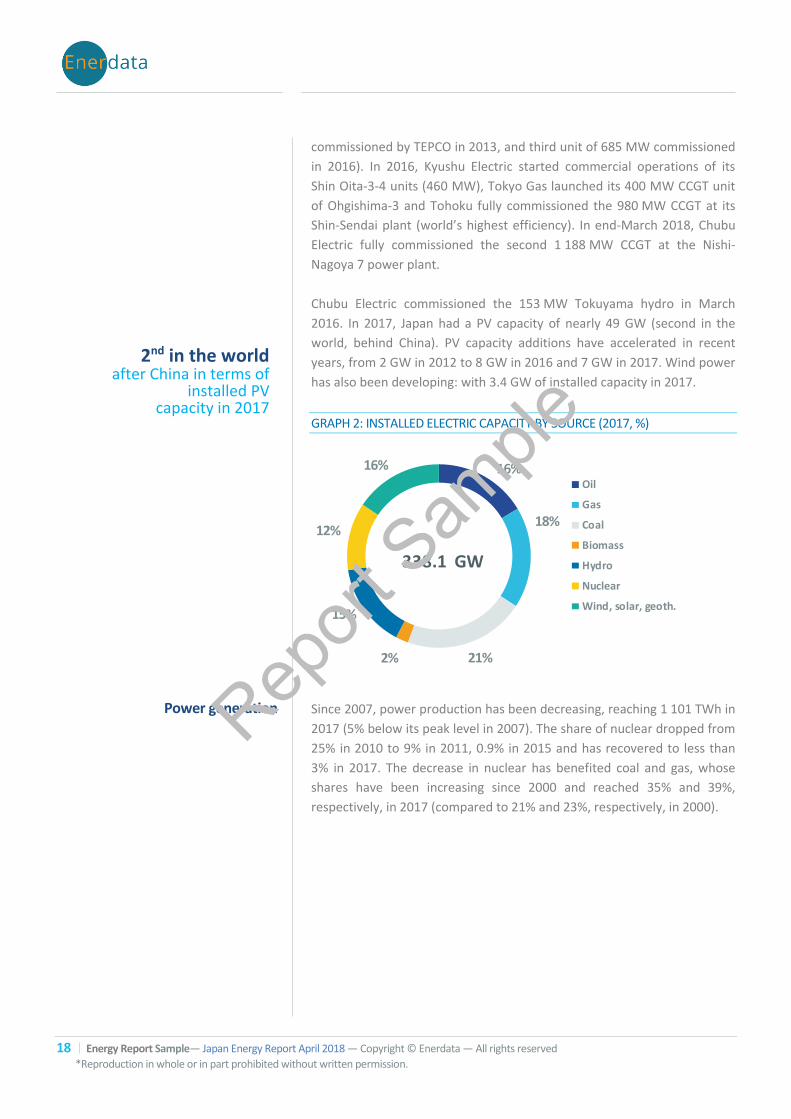

Electricity

The installed electricity capacity is 338 GW, including 40.3 GW of nuclear

energy and 50.2 GW of hydroelectricity. Thermal power plants account for

57% of the total capacity (end of 2017).

Following the Fukushima accident, all undamaged nuclear reactors were

placed offline for safety controls. Before the accident, there were

54 reactors spread over 17 plants. As of April 2018, 6 of the 42 operable

reactors have been restarted: the 890 MW units Sendai-1 and Sendai -2 by

Kyushu Electric in 2015, the 830 MW units Takahama-3 and Takahama-4

by Kansai Electric in 2017, and the 1 180 MW unit Ohi-3 by Kansai Electric

and the 1 180 MW unit Genkai-3 by Kyushu Electric in April 2018. The NRA

approved a lifetime extension for Takahama -1 and 2 in June 2016. This

approval will enable the reactors to operate until 2034 and 2035. It is the

first time that Japan has allowed a nuclear plant to operate beyond

40 years.

More than 7 GW of gas power capacity have been added to the network

since 2011, including four 576 MW units at the Joetsu CCGT LNG-fired

power station in the Niigata Prefecture (commissioned in 2012-2014 by

Chubu Electric), two new CCGT units in Kawasaki (the first unit of 500 MW

→

Installed capacity

Report

Sample

18 Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved *Reproduction in whole or in part prohibited without written permission.

2nd in the world after China in terms of

installed PV capacity in 2017

commissioned by TEPCO in 2013, and third unit of 685 MW commissioned

in 2016). In 2016, Kyushu Electric started commercial operations of its

Shin Oita-3-4 units (460 MW), Tokyo Gas launched its 400 MW CCGT unit

of Ohgishima-3 and Tohoku fully commissioned the 980 MW CCGT at its

Shin-Sendai plant (world’s highest efficiency). In end-March 2018, Chubu

Electric fully commissioned the second 1 188 MW CCGT at the Nishi-

Nagoya 7 power plant.

Chubu Electric commissioned the 153 MW Tokuyama hydro in March

2016. In 2017, Japan had a PV capacity of nearly 49 GW (second in the

world, behind China). PV capacity additions have accelerated in recent

years, from 2 GW in 2012 to 8 GW in 2016 and 7 GW in 2017. Wind power

has also been developing: with 3.4 GW of installed capacity in 2017.

GRAPH 2: INSTALLED ELECTRIC CAPACITY BY SOURCE (2017, %)

16%

18%

21%2%

15%

12%

16%Oil

Gas

Coal

Biomass

Hydro

Nuclear

Wind, solar, geoth.

338.1 GW

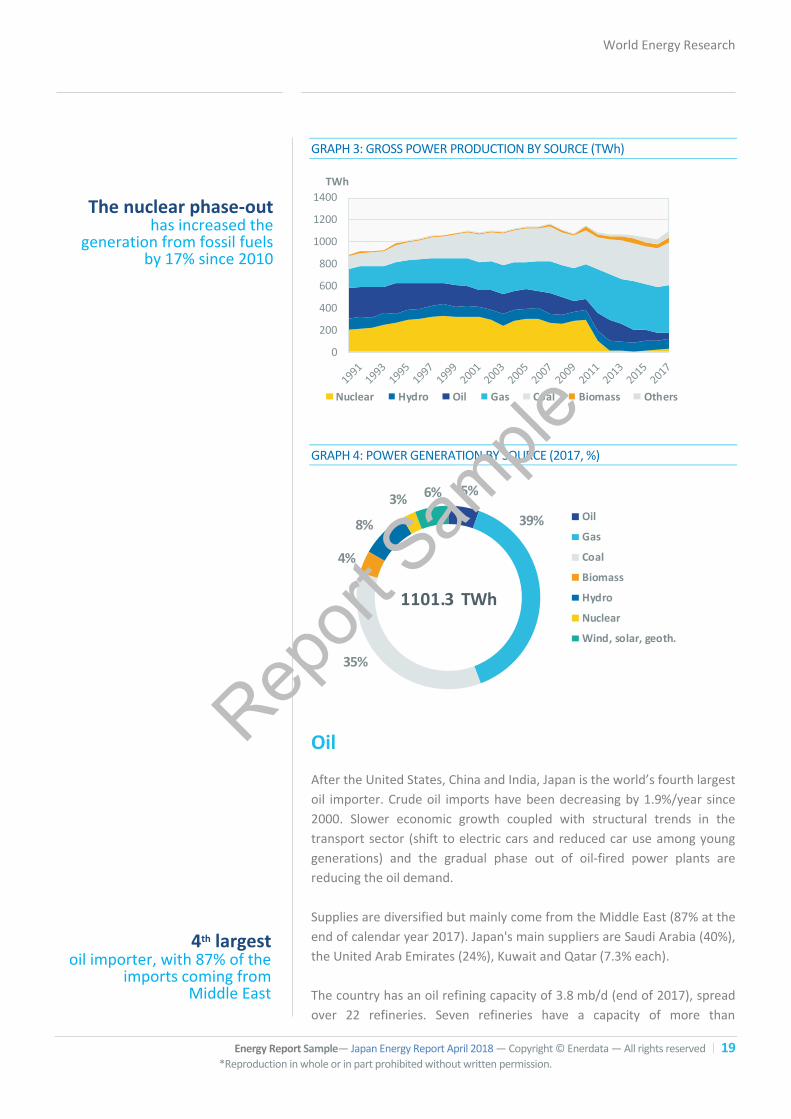

Since 2007, power production has been decreasing, reaching 1 101 TWh in

2017 (5% below its peak level in 2007). The share of nuclear dropped from

25% in 2010 to 9% in 2011, 0.9% in 2015 and has recovered to less than

3% in 2017. The decrease in nuclear has benefited coal and gas, whose

shares have been increasing since 2000 and reached 35% and 39%,

respectively, in 2017 (compared to 21% and 23%, respectively, in 2000).

Power generation Rep

ort Sam

ple

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 19

*Reproduction in whole or in part prohibited without written permission.

The nuclear phase-out has increased the

generation from fossil fuels by 17% since 2010

4th largest oil importer, with 87% of the

imports coming from Middle East

GRAPH 3: GROSS POWER PRODUCTION BY SOURCE (TWh)

0

200

400

600

800

1000

1200

1400

Nuclear Hydro Oil Gas Coal Biomass Others

TWh

GRAPH 4: POWER GENERATION BY SOURCE (2017, %)

5%

39%

35%

4%

8%

3% 6%

Oil

Gas

Coal

Biomass

Hydro

Nuclear

Wind, solar, geoth.

1101.3 TWh

Oil

After the United States, China and India, Japan is the world’s fourth largest

oil importer. Crude oil imports have been decreasing by 1.9%/year since

2000. Slower economic growth coupled with structural trends in the

transport sector (shift to electric cars and reduced car use among young

generations) and the gradual phase out of oil-fired power plants are

reducing the oil demand.

Supplies are diversified but mainly come from the Middle East (87% at the

end of calendar year 2017). Japan's main suppliers are Saudi Arabia (40%),

the United Arab Emirates (24%), Kuwait and Qatar (7.3% each).

The country has an oil refining capacity of 3.8 mb/d (end of 2017), spread

over 22 refineries. Seven refineries have a capacity of more than

Report

Sample

20 Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved *Reproduction in whole or in part prohibited without written permission.

Largest LNG importer: a total of 117 bcm of LNG

was imported in 2017

200 000 bbl/d, representing nearly half of the country’s capacity. In 2014,

JX Nippon Oil & Energy closed its Muroran Refinery (180 000 bbl/d) to

transform it into a petrochemical plant and Idemitsu Kosan closed its

Tokuyama refinery (120 000 bbl/d).

Gas

Japan is the world’s largest LNG importer. Imports increased rapidly

between 2010 and 2014 in order to compensate the drop in nuclear

production and supply gas power plants. However, imports have since

declined by 5% to 117 bcm in 2017. LNG imports represent more than one

third of the world’s total LNG trade.

The main LNG suppliers are Australia, Malaysia and Qatar (28%, 19% and

13%, respectively, in 2016). In 2016, significant imports also came from

Indonesia (9% - initially Japan's main supplier, but its market share is down

from 33% in 2000), Russia (8%) and the United Arab Emirates (6%).

Japan has secured a multitude of long-term LNG contracts, including

55 bcm/year from Australia, 24 bcm/year from Malaysia, 14 bcm/year

from Qatar, around 21 bcm/year from the US, 10 bcm/year from Russia

and 6 bcm/year from the United Arab Emirates. The total contracted

volume reached 160 bcm/year in 2017.

Japan has 40 operating LNG regasification terminals. The main recently

commissioned terminals are Hachinoe LNG (1 Mt/year) in 2015, Hitachi

LNG (1.7 Mt/year) in 2016 and Soma LNG (1 Mt/year) in March 2018.

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 21

*Reproduction in whole or in part prohibited without written permission.

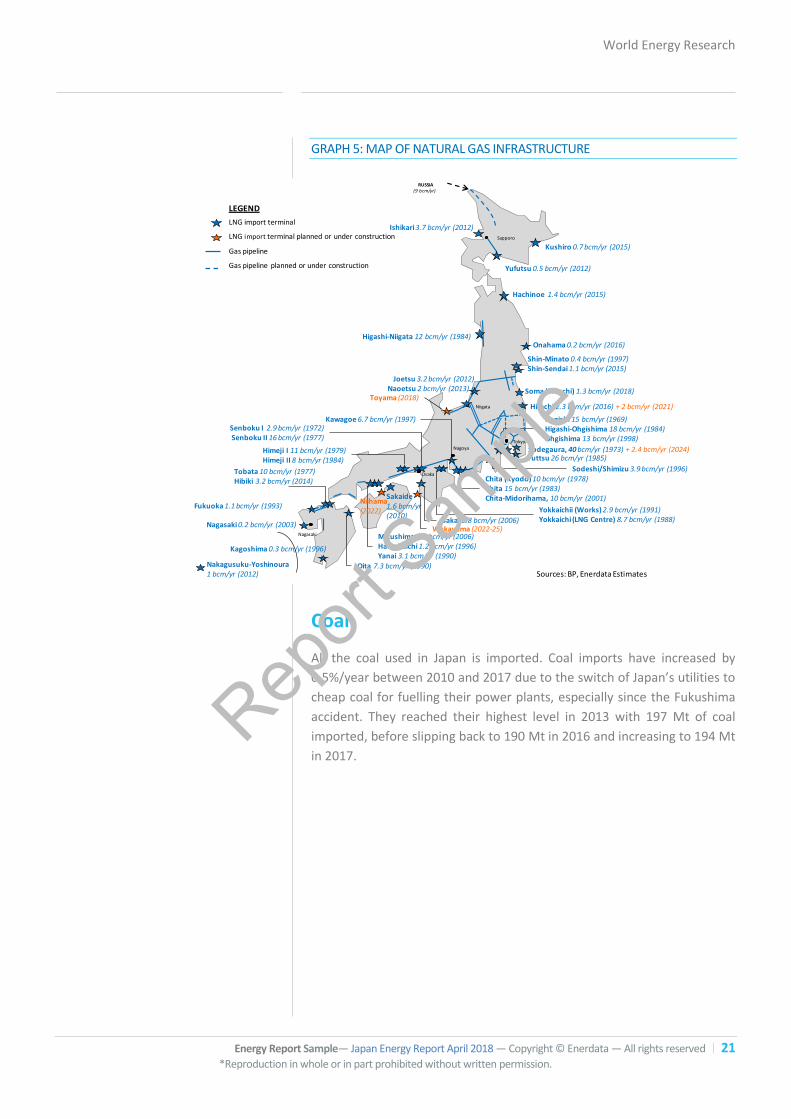

GRAPH 5: MAP OF NATURAL GAS INFRASTRUCTURE

Japan Gas Map

Tokyo

Nagoya

Nagasaki

Sapporo

Shin-Minato 0.4 bcm/yr (1997) Shin-Sendai 1.1 bcm/yr (2015)

Negishi 15 bcm/yr (1969)Higashi-Ohgishima 18 bcm/yr (1984)Ohgishima 13 bcm/yr (1998)

Sodegaura, 40bcm/yr (1973) + 2.4 bcm/yr (2024)

Sodeshi/Shimizu 3.9 bcm/yr (1996)

Chita (Kyodo) 10 bcm/yr (1978)Chita 15 bcm/yr (1983) Chita-Midorihama, 10 bcm/yr (2001)

Mizushima 5.8 bcm/yr (2006)Hatsukaichi 1.2 bcm/yr (1996)Yanai 3.1 bcm/yr (1990)

Kawagoe 6.7 bcm/yr (1997)

Yokkaichii (Works) 2.9 bcm/yr (1991)Yokkaichi (LNG Centre) 8.7 bcm/yr (1988)

Fukuoka 1.1 bcm/yr (1993)

Oita 7.3 bcm/yr (1990)

Higashi-Niigata 12 bcm/yr (1984)

Sakai 8.8 bcm/yr (2006)

RUSSIA(9 bcm/yr)

Sources: BP, Enerdata Estimates

Joetsu 3.2 bcm/yr (2012)Naoetsu 2 bcm/yr (2013) r

Wakayama (2022-25)

Sakaide1.6 bcm/yr(2010)

Hachinoe 1.4 bcm/yr (2015)

Ishikari 3.7 bcm/yr (2012)

Kagoshima 0.3 bcm/yr (1996)

Kushiro 0.7 bcm/yr (2015)

Yufutsu 0.5 bcm/yr (2012)

Futtsu 26 bcm/yr (1985)

Hitachi 2.3 bcm/yr (2016) + 2 bcm/yr (2021)Toyama (2018)

Nagasaki 0.2 bcm/yr (2003)

Soma (Shinchi) 1.3 bcm/yr (2018)

Himeji I 11 bcm/yr (1979)Himeji II 8 bcm/yr (1984)

Senboku I 2.9 bcm/yr (1972)Senboku II 16 bcm/yr (1977)

Tobata 10 bcm/yr (1977)Hibiki 3.2 bcm/yr (2014)

LNG import terminal

LNG import terminal planned or under construction

Gas pipeline

Gas pipeline planned or under construction

LEGEND

Niigata

Osaka

Onahama 0.2 bcm/yr (2016)

Nakagusuku-Yoshinoura1 bcm/yr (2012)

Niihama(2022)

Coal

All the coal used in Japan is imported. Coal imports have increased by

0.5%/year between 2010 and 2017 due to the switch of Japan’s utilities to

cheap coal for fuelling their power plants, especially since the Fukushima

accident. They reached their highest level in 2013 with 197 Mt of coal

imported, before slipping back to 190 Mt in 2016 and increasing to 194 Mt

in 2017.

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 22

*Reproduction in whole or in part prohibited without written permission.

Energy prices

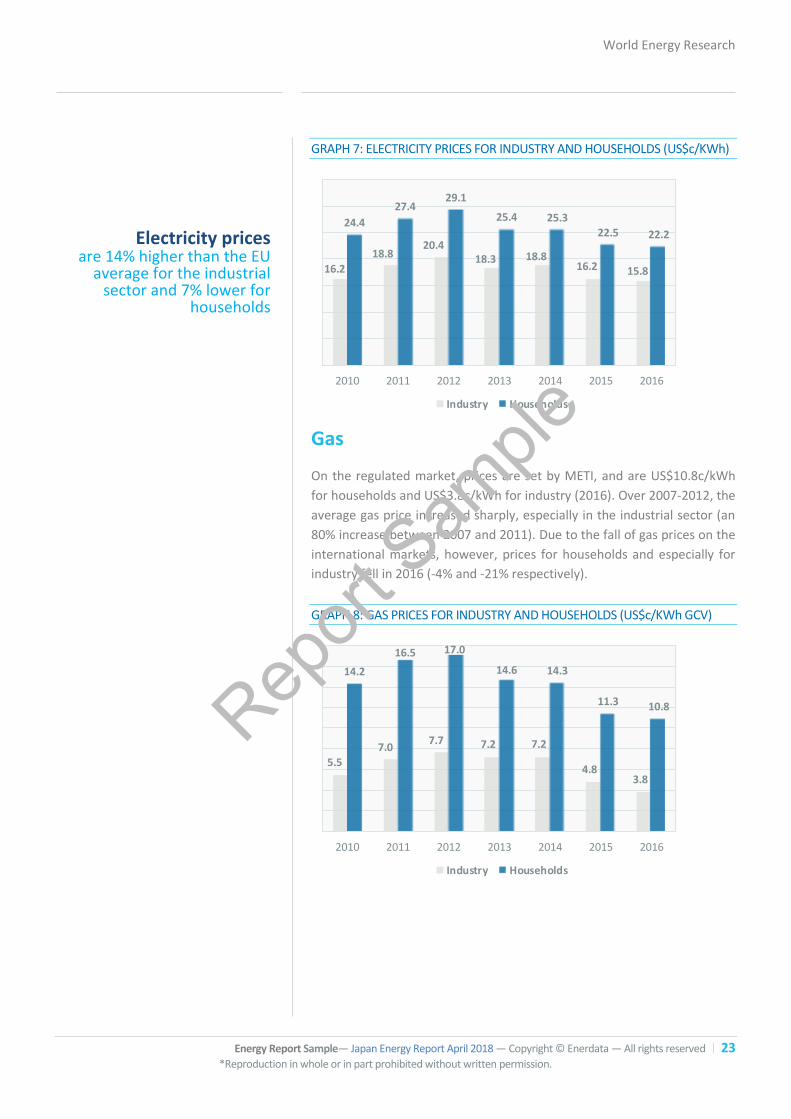

National oil prices follow international oil prices.

Electricity prices are controlled by METI through an automatic adjustment mechanism.

Oil

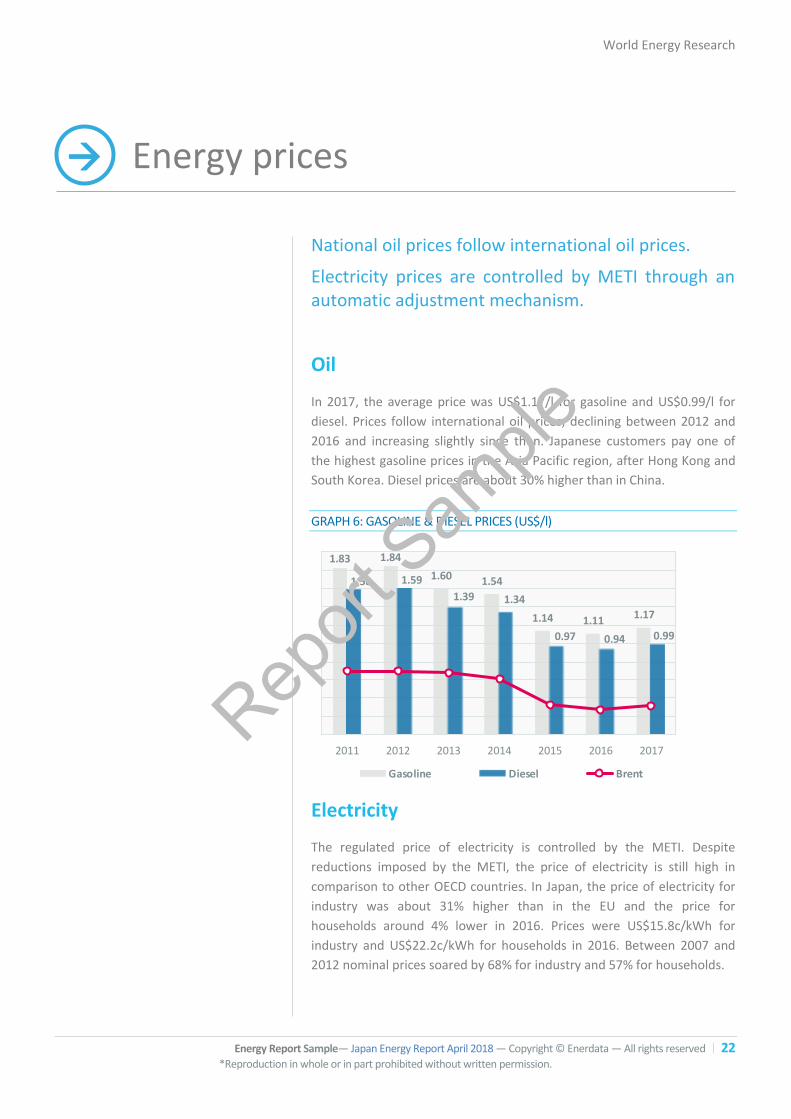

In 2017, the average price was US$1.17/l for gasoline and US$0.99/l for

diesel. Prices follow international oil prices, declining between 2012 and

2016 and increasing slightly since then. Japanese customers pay one of

the highest gasoline prices in the Asia Pacific region, after Hong Kong and

South Korea. Diesel prices are about 30% higher than in China.

GRAPH 6: GASOLINE & DIESEL PRICES (US$/l)

1.83 1.84

1.60 1.54

1.14 1.111.17

1.58 1.59

1.39 1.34

0.97 0.94 0.99

2011 2012 2013 2014 2015 2016 2017

Gasoline Diesel Brent

Electricity

The regulated price of electricity is controlled by the METI. Despite

reductions imposed by the METI, the price of electricity is still high in

comparison to other OECD countries. In Japan, the price of electricity for

industry was about 31% higher than in the EU and the price for

households around 4% lower in 2016. Prices were US$15.8c/kWh for

industry and US$22.2c/kWh for households in 2016. Between 2007 and

2012 nominal prices soared by 68% for industry and 57% for households.

→

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 23

*Reproduction in whole or in part prohibited without written permission.

Electricity prices are 14% higher than the EU

average for the industrial sector and 7% lower for

households

GRAPH 7: ELECTRICITY PRICES FOR INDUSTRY AND HOUSEHOLDS (US$c/KWh)

16.2

18.820.4

18.3 18.816.2 15.8

24.4

27.429.1

25.4 25.322.5 22.2

2010 2011 2012 2013 2014 2015 2016

Industry Households

Gas

On the regulated market, prices are set by METI, and are US$10.8c/kWh

for households and US$3.8c/kWh for industry (2016). Over 2007-2012, the

average gas price increased sharply, especially in the industrial sector (an

80% increase between 2007 and 2011). Due to the fall of gas prices on the

international markets, however, prices for households and especially for

industry fell in 2016 (-4% and -21% respectively).

GRAPH 8: GAS PRICES FOR INDUSTRY AND HOUSEHOLDS (US$c/KWh GCV)

5.5

7.07.7 7.2 7.2

4.83.8

14.2

16.5 17.0

14.6 14.3

11.3 10.8

2010 2011 2012 2013 2014 2015 2016

Industry Households

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 24

*Reproduction in whole or in part prohibited without written permission.

The share of nuclear dropped to zero in 2014,

from 16% in 2010

Energy consumption

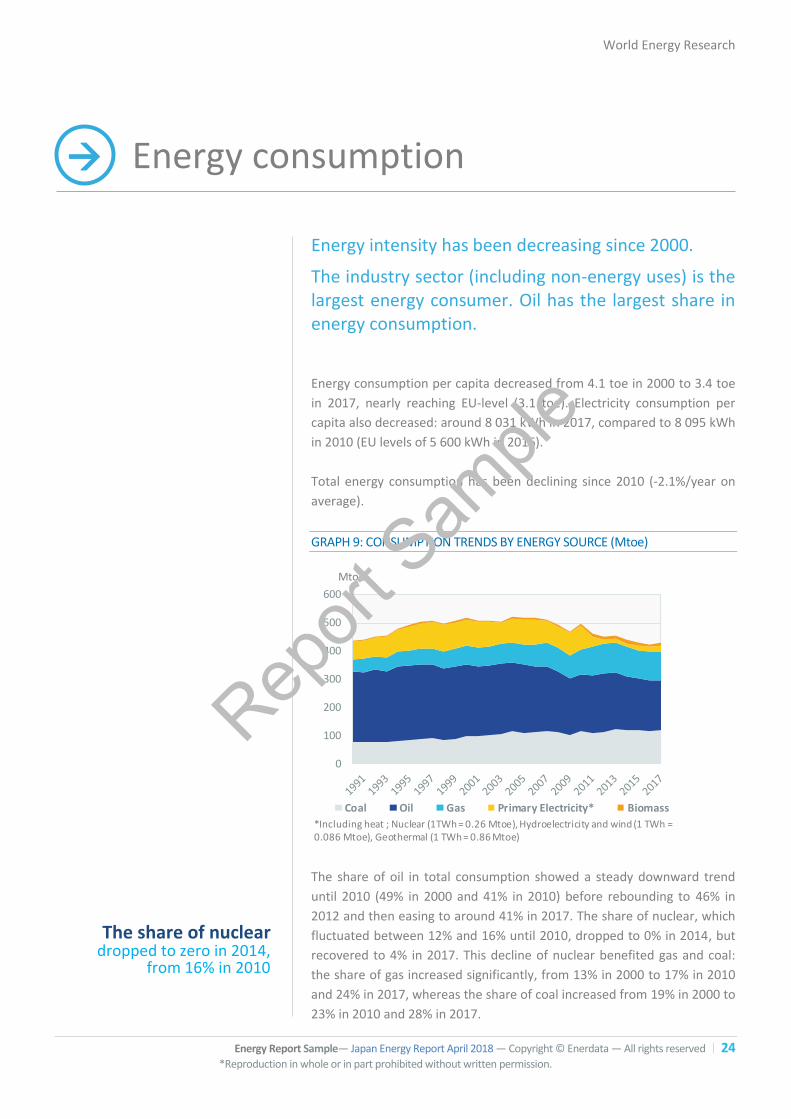

Energy intensity has been decreasing since 2000.

The industry sector (including non-energy uses) is the largest energy consumer. Oil has the largest share in energy consumption.

Energy consumption per capita decreased from 4.1 toe in 2000 to 3.4 toe

in 2017, nearly reaching EU-level (3.1 toe). Electricity consumption per

capita also decreased: around 8 031 kWh in 2017, compared to 8 095 kWh

in 2010 (EU levels of 5 600 kWh in 2016).

Total energy consumption has been declining since 2010 (-2.1%/year on

average).

GRAPH 9: CONSUMPTION TRENDS BY ENERGY SOURCE (Mtoe)

0

100

200

300

400

500

600

Coal Oil Gas Primary Electricity* Biomass

*Including heat ; Nuclear (1TWh = 0.26 Mtoe), Hydroelectricity and wind (1 TWh = 0.086 Mtoe), Geothermal (1 TWh = 0.86 Mtoe)

Mtoe

The share of oil in total consumption showed a steady downward trend

until 2010 (49% in 2000 and 41% in 2010) before rebounding to 46% in

2012 and then easing to around 41% in 2017. The share of nuclear, which

fluctuated between 12% and 16% until 2010, dropped to 0% in 2014, but

recovered to 4% in 2017. This decline of nuclear benefited gas and coal:

the share of gas increased significantly, from 13% in 2000 to 17% in 2010

and 24% in 2017, whereas the share of coal increased from 19% in 2000 to

23% in 2010 and 28% in 2017.

→

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 25

*Reproduction in whole or in part prohibited without written permission.

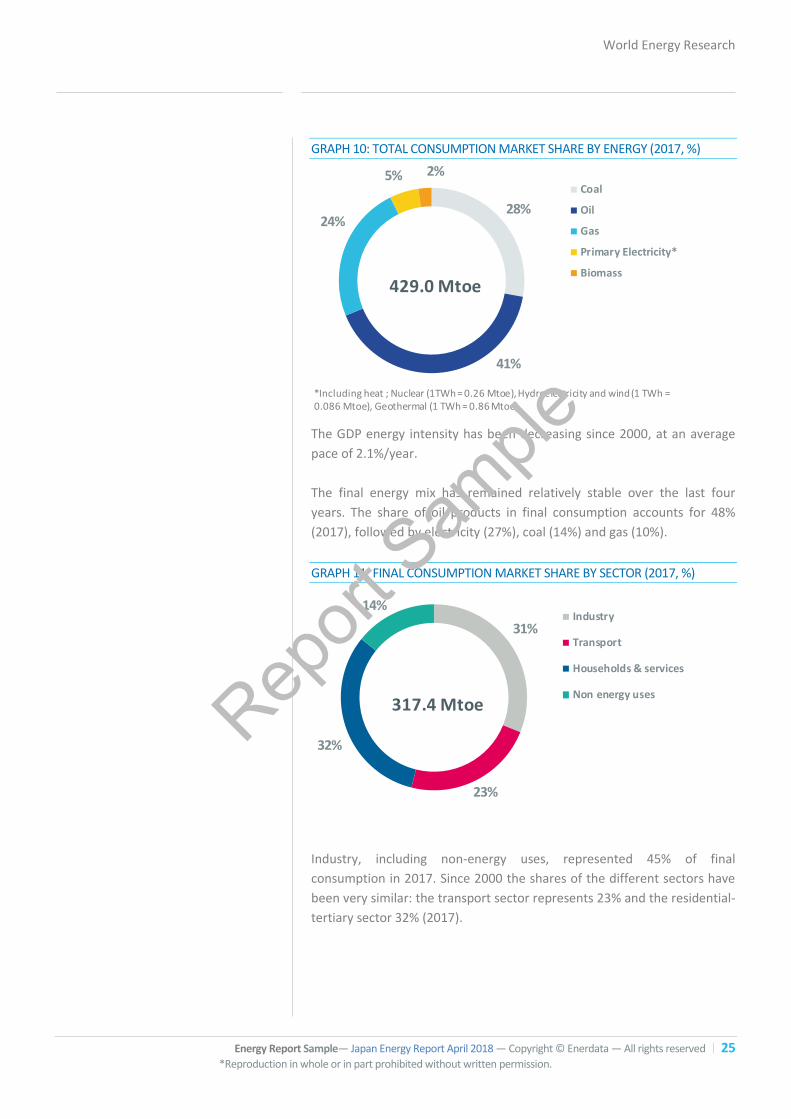

GRAPH 10: TOTAL CONSUMPTION MARKET SHARE BY ENERGY (2017, %)

28%

41%

24%

5% 2%Coal

Oil

Gas

Primary Electricity*

Biomass

*Including heat ; Nuclear (1TWh = 0.26 Mtoe), Hydroelectricity and wind (1 TWh = 0.086 Mtoe), Geothermal (1 TWh = 0.86 Mtoe)

429.0 Mtoe

The GDP energy intensity has been decreasing since 2000, at an average

pace of 2.1%/year.

The final energy mix has remained relatively stable over the last four

years. The share of oil products in final consumption accounts for 48%

(2017), followed by electricity (27%), coal (14%) and gas (10%).

GRAPH 11: FINAL CONSUMPTION MARKET SHARE BY SECTOR (2017, %)

31%

23%

32%

14%Industry

Transport

Households & services

Non energy uses317.4 Mtoe

Industry, including non-energy uses, represented 45% of final

consumption in 2017. Since 2000 the shares of the different sectors have

been very similar: the transport sector represents 23% and the residential-

tertiary sector 32% (2017).

Report

Sample

26 Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved *Reproduction in whole or in part prohibited without written permission.

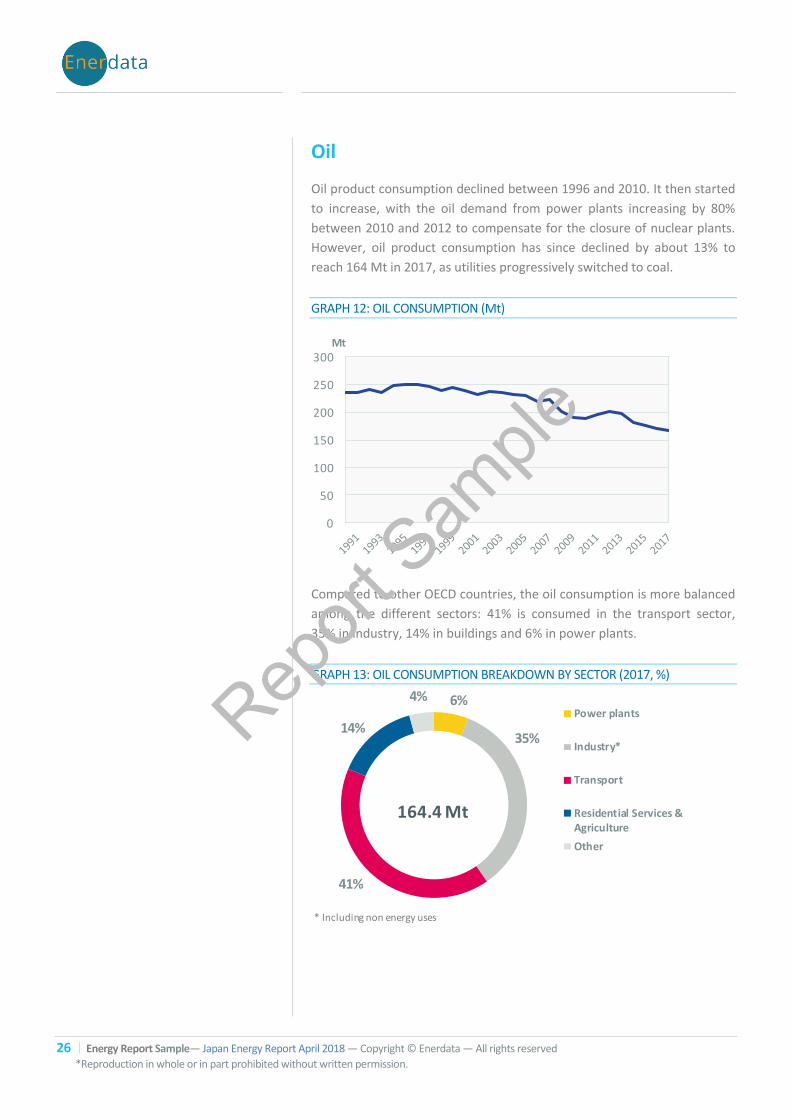

Oil

Oil product consumption declined between 1996 and 2010. It then started

to increase, with the oil demand from power plants increasing by 80%

between 2010 and 2012 to compensate for the closure of nuclear plants.

However, oil product consumption has since declined by about 13% to

reach 164 Mt in 2017, as utilities progressively switched to coal.

GRAPH 12: OIL CONSUMPTION (Mt)

0

50

100

150

200

250

300Mt

Compared to other OECD countries, the oil consumption is more balanced

among the different sectors: 41% is consumed in the transport sector,

35% in industry, 14% in buildings and 6% in power plants.

GRAPH 13: OIL CONSUMPTION BREAKDOWN BY SECTOR (2017, %) 6%

35%

41%

14%

4%Power plants

Industry*

Transport

Residential Services &Agriculture

Other

164.4 Mt

* Including non energy uses

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 27

*Reproduction in whole or in part prohibited without written permission.

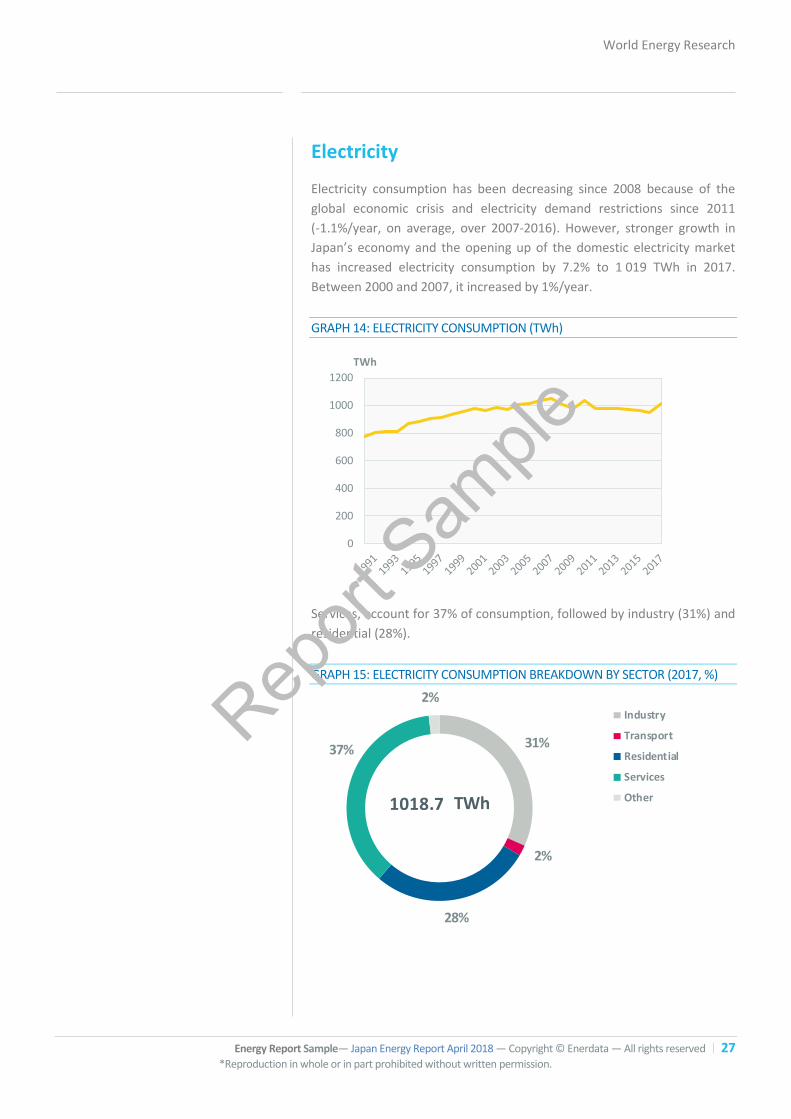

Electricity

Electricity consumption has been decreasing since 2008 because of the

global economic crisis and electricity demand restrictions since 2011

(-1.1%/year, on average, over 2007-2016). However, stronger growth in

Japan’s economy and the opening up of the domestic electricity market

has increased electricity consumption by 7.2% to 1 019 TWh in 2017.

Between 2000 and 2007, it increased by 1%/year.

GRAPH 14: ELECTRICITY CONSUMPTION (TWh)

0

200

400

600

800

1000

1200

TWh

Services, account for 37% of consumption, followed by industry (31%) and

residential (28%).

GRAPH 15: ELECTRICITY CONSUMPTION BREAKDOWN BY SECTOR (2017, %)

31%

2%

28%

37%

2%Industry

Transport

Residential

Services

Other1018.7 TWh

Report

Sample

28 Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved *Reproduction in whole or in part prohibited without written permission.

Natural gas

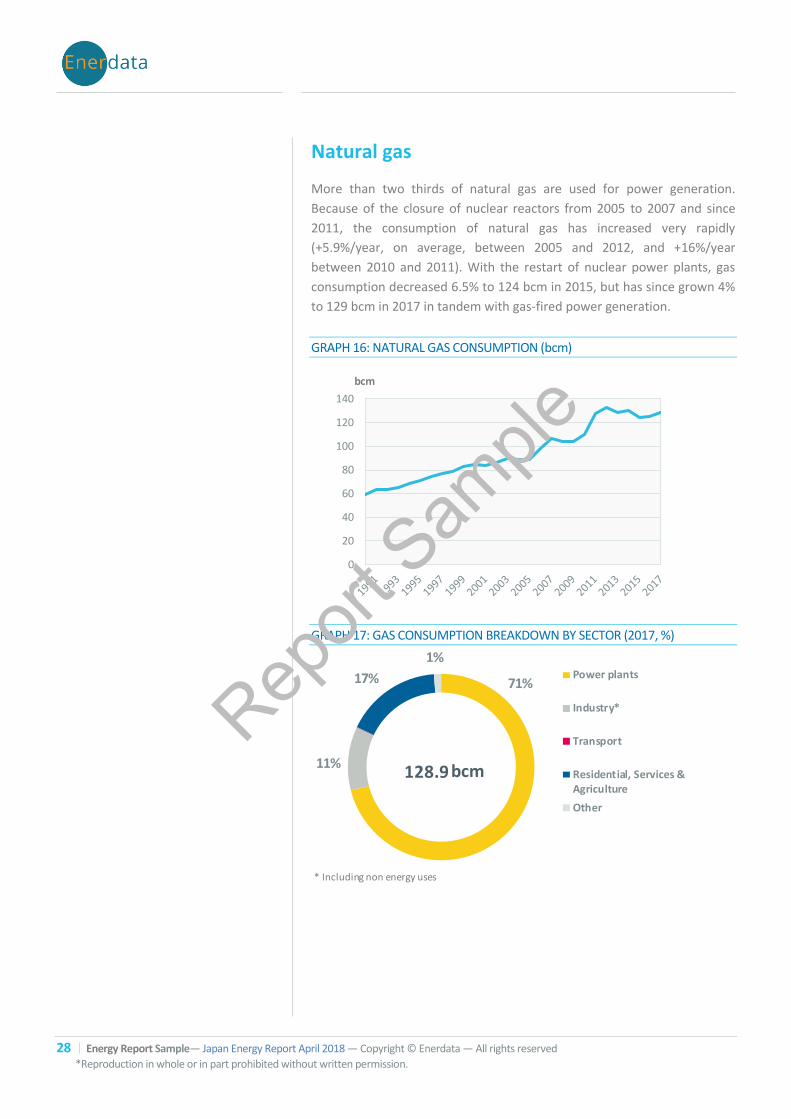

More than two thirds of natural gas are used for power generation.

Because of the closure of nuclear reactors from 2005 to 2007 and since

2011, the consumption of natural gas has increased very rapidly

(+5.9%/year, on average, between 2005 and 2012, and +16%/year

between 2010 and 2011). With the restart of nuclear power plants, gas

consumption decreased 6.5% to 124 bcm in 2015, but has since grown 4%

to 129 bcm in 2017 in tandem with gas-fired power generation.

GRAPH 16: NATURAL GAS CONSUMPTION (bcm)

0

20

40

60

80

100

120

140

bcm

GRAPH 17: GAS CONSUMPTION BREAKDOWN BY SECTOR (2017, %)

71%

11%

17%

1%Power plants

Industry*

Transport

Residential, Services &Agriculture

Other

128.9 bcm

* Including non energy uses

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 29

*Reproduction in whole or in part prohibited without written permission.

Coal

Coal consumption increased rapidly between 2000 and 2007 (3%/year)

but declined by 4.9%/year in 2008 and 2009. It has grown by around

2.2%/year since 2011 to 196 Mt in 2017, with most of the utilities

switching to this cheap fuel. Electricity production uses 61% of the coal

consumed, and the remainder is consumed by industry, mainly by the iron

and steel industry.

GRAPH 18: COAL AND LIGNITE CONSUMPTION (Mt)

0

50

100

150

200

250

Mt

GRAPH 19: COAL AND LIGNITE CONSUMPTION BREAKDOWN BY SECTOR (2017, %)

61%

35%

4%

Power plants

Industry*

Residential, Services &Agriculture

Other

196.0 Mt

* Including non energy uses

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 30

*Reproduction in whole or in part prohibited without written permission.

Issues and prospects

The country is facing pressure to reach its 2030 CO2 emissions and power mix targets, leading to tighter regulations for coal projects and the development of projects using CCS, whereas renewable energy projects are expected to grow rapidly in the near future.

The gas import capacity is expected to increase since the Government is encouraging fuel switching to gas in the end-use sectors.

Using its Global Energy Forecasting Model POLES, Enerdata foresees the

share of oil to account for 38% of the primary energy consumption by

2040, while the share of natural gas would be around 14% and the share

of coal around 10%. The remainder (37%) would be covered by nuclear,

renewables and biomass. METI is finalising the draft of its long-term

energy plan, which will prioritize nuclear and renewables as major energy

sources in Japan’s energy sector future.

Electricity

A Japanese consultative committee has backed governmental plans to

reach a 20-22% share of nuclear power in the power mix by 2030.

Renewable generation would account for 22% to 24% of the power mix

while coal would cover 26% of power generation. Gas is expected to

supply 27% by 2030. The target was formally approved by the Ministry of

Trade in 2015. It would be revised every three years and energy mix

targets could be changed if necessary. The energy mix targets are not

expected to differ greatly in METI’s long-term energy plan proposal.

Enerdata expects thermal generation to account for 61% of the power mix

by 2040, while renewables would grow to 20% (solar and wind). The

remainder would come from nuclear and hydro generation.

JERA announced in September 2016 that it would refurbish and operate

5.6 GW of thermal capacity by 2023. These capacities include "state-of-

the-art high-efficiency" projects: the Goi (3x780 MW) LNG-fired power

→

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 31

*Reproduction in whole or in part prohibited without written permission.

plant, the new Anegasaki (3x650 MW) LNG fired power plant and the

Yokosuka (2x650 MW) coal-fired power plant.

Since the Fukushima disaster in March 2011, only 6 of the 42 operable

reactors in Japan have cleared new regulatory safety standards

regulations and restarted operations. In December 2017, two units at

TEPCO’s Kashiwazaki-Kariwa passed safety inspections, but TEPCO has

struggled to obtain approval from the local government to resume

operations. High safety-related costs and rising opposition to restarting

existing nuclear plants have affected nuclear projects announced before

2011 and new nuclear commissionings remain hypothetical.

Two projects are currently under construction. Construction work has

resumed at Chugoku Electric’s Shimane 3 (1 325 MW), but the start year is

still unclear. Commissioning of J-Power’s Ohma (1 325 MW) has now been

shifted to 2024. Seven nuclear reactors are planned on 4 sites: Tsuruga

3&4 by Japco (2 x 1 500 MW), Kaminoseki 1&2 by Chugoku Electric

(2x1 320 MW), Higashi-Dori 1&2 by TEPCO (2x1 320 MW) and Hamaoka 6

by Chubu (1 380 MW).

Several power utilities have decided to decommission their nuclear

reactors, due to high investments required to upgrade them to the new

safety standards: Kansai Electric (Ohi-1 and 2), Japan Atomic Power

(Tsuruga-1), Kyushu Electric (Genkai-1), Chugoku Electric (Shimane-1),

Kansai Electric (Mihama-1 and Mihama-2), Shikoku Electric (Ikata-2).

In December 2016, the METI again revised its costs projections related to

Fukushima to Yen 21 500bn (US$188bn), which is two times higher than

the initial projections: decommissioning costs have soared from Yen

2 000bn to Yen 8 000bn (US$70bn), compensation payments to Yen

7 900bn (US$69bn) and the treatment and storage of contaminated soil to

Yen 5 600bn (US$49bn).

Meanwhile, three licence extensions enabling operations beyond 40 years

under revised regulation were granted by the NRA in 2016 to Takahama-1

and 2, and to the Mihama-3 nuclear power unit (780 MW). All units are

operated by Kansai Electric.

Due to fierce criticism from environmental groups, the Japanese

Government is considering tightening regulations on the approval of coal-

fired power projects, so that only the most efficient technologies

(including ultra-supercritical plants) would be approved. Japan plans to

adopt advanced technologies such as integrated gasification combined

cycle (IGCC) and to have them operational by 2020.

Nuclear projects

Coal power projects

Report

Sample

32 Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved *Reproduction in whole or in part prohibited without written permission.

Possible tightening of coal power plant

approvals due to pressure from

environmental groups

In 2013, in accordance with its “Comprehensive Special Business Plan”,

TEPCO invited bids for new power generation. The company is planning to

purchase a total of 2 600 MW of thermal power from other operators.

Power delivery should start between June 2019 and June 2021. In April

2016, TEPCO mothballed 12 gas and oil-fired power plants, totalling

4 061 MW, as part of its strategy to improve fuel efficiency in power

generation.

TEPCO is building two 540 MW coal-based IGCC power plants in

partnership with Joban Joint Power and Mitsubishi through the two joint-

ventures Nakoso IGCC Power GK and Hirono IGCC Power GK. The first

power plant is being built in the Hirono area by 2021, the second one is

being built within the premises of the Nakoso power plant by 2020.

J-POWER is constructing the 600 MW Takehara New 1 Ultra-supercritical

plant which is expected to start in 2020, and which will burn up to 10% of

wood.

Kyushu Electric is building the 1 000 MW Matsuura 2 Ultra-supercritical

plant, which is expected to be commissioned in 2019.

Chugoku Electric aims to build a 1 000 MW USC power plant, Misumi 2,

which is expected to be commissioned in 2022.

Chubu Electric is constructing the 650 MW Hitachinaka Kyodo power

plant, expected to be commissioned in 2020-2021.

Tohoku has started the construction of a new 950 MW gas-fired unit at its

Shin-Sendai plant. The company aims to start operating at half of the

capacity in mid-2016 and raise the output to full capacity in 2017.

Tokyo Gas is constructing the 400 MW Ohgishima 3 power plant which will

be commissioned in 2015.

TEPCO is constructing the 420 MW Kashima Group 7-3 which is expected

to start in 2015. TEPCO has received the finalised "Environmental impact

assessment results" for its Kawasaki II expansion project, involving the

construction of two 500 MW gas-fired CCGT units at the Kawasaki power

plant. The group plans to commission the units, currently under

construction, in July 2016 and July 2017, respectively.

Chubu Electric aims to build the 2 300 MW Nishi-Nagoya-7-1 & 7-2 CCGT

plant which is expected to be commissioned in 2017-2018. In 2013 Kyushu

Electric started building its 480 MW Shin Oita 3-4 CCGT power plant,

which is expected to start in 2016.

Gas power plants Rep

ort Sam

ple

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 33

*Reproduction in whole or in part prohibited without written permission.

Hokkaido Electric is planning the 1 600 MW Ishikariwan Shinko 1-2-3 CCGT

to be commissioned in stages over 2019-2029. Kobe Steel is planning the 1

200 MW Kobe Steel CCGT which is expected to start in 2019. Hokuriku

Electric-operated 400 MW Toyama Shinko CCGT is in the planning stage

and will be commissioned by 2018-2019.

Hokuriku Electric’s 400 MW Toyama Shinko CCGT is being built and

scheduled to start operations in November 2018.

Several CCGT are under construction, planned or in bid process:

Ishikariwan Shinko 1-2-3 (1 707 MW) by Hokkaido Electric (commissioning

in stages over 2019-2028); a 1 200 MW CCGT by Kobe Steel (expected to

start in 2019); a 1180 MW CCGT in the port of Soma is being planned by

Fukushima Gas Power (50.7% Japex, 49.3% Mitsui) (2x590 MW units, with

first unit to be commissioned in January 2020 and the second one in April

2020).

According to the METI, Japan has approved 87.4 GW worth of renewable

power projects since the introduction of feed-in tariffs in 2012.

Three pumped-storage projects are in the pipeline: the 1 880 MW

Kannagawa project being constructed by TEPCO and expected in 2019, the

200 MW Kyogoku-3 project by Hokkaido Electric (planned for 2023), And

the 400 MW Kazunogawa-3 project by TEPCO (planned for 2024.

According to a study by the Ministry of Environment in 2015, solar power

generation could increase to 78-128 TWh by 2030, out of a total

renewable power generation of 241-257 TWh, depending on energy

policies.

The main projects under construction are: the 231 MW Setouchi Solar

project developed by TOYO group that should be commissioned in 2019

and the 257.7 MW Sakuto project managed by Pacifico Energy planned for

2019.

According to the Japan Wind Power Association (JWPA), Japan has good

wind power potential, with average wind speeds of 6.5 m/s (onshore) and

7 m/s (up to 30 km offshore and less than 200m sea depth). In its wind

power roadmap to 2050, JWPA projects onshore and offshore wind power

capacities to reach 10 GW and 1 GW, respectively, by 2020, 27 GW

(onshore) and 9 GW (offshore) by 2030, and 38 GW (onshore) and 27 GW

(offshore) by 2050.

The New Energy and Industrial Technology Development Organisation

(NEDO) approved financial support through subsidies to two offshore wind

Hydropower projects

Gas power plants

Renewables

Solar power projects

Wind power projects

Report

Sample

34 Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved *Reproduction in whole or in part prohibited without written permission.

projects in January 2016: a 170 MW offshore wind park, developed by

Marubeni and Obayashi in the port of Noshiro by 2020, and a 104 MW

offshore wind park developed by Green Power Investment within the

Ishikari Bay by 2020.

Several wind plants are under consideration: Softbank is moving ahead

with plans for 150 MW Ibaraki offshore; Murakami City is bidding for

220 MW Iwafune (initially expected to start in 2025); and the 700 MW

Hibikinada offshore is being planned.

The city of Kitakyushu (Kyushu Island, Japan) has selected the Hibiki

consortium led by Kyuden Mirai (fully-owned renewable subsidiary of

Kyushu Electric), and including J-Power, Saibu Gas and engineering firm

Kyudenko to develop a Yen 175bn (US$1.5bn) offshore wind project near

the port of Kitakyushu.

Gas

To increase the LNG supply, several LNG regasification terminals are under

development, adding more than 4 bcm/year.

Tokyo Gas plans to add two LNG vaporisers in Hitachi by December 2018,

and the company announced that it plans to build a second LNG storage

tank by 2021, for a total capacity of 2 bcm/year.

In addition, the company plans to install two new vaporisers and a new

LNG storage tank at the Sodegaura LNG terminal by 2024 (2.4 bcm/year).

Japan and Russia have signed an MoU to promote Japanese firms'

participation in a project to build a terminal in Vladivostok (Russian far

east) for LNG for export to Japan. In 2014, the company decided to

reconsider the project feasibility and, while it has not advanced, the

possibility remains for an export terminal up to 10 Mt/year at some point

in the future.

Tokyo Gas, Japex and Nippon Steel & Sumikin Engineering completed a

preliminary feasibility study for a 1 500 km gas pipeline project, which

would import natural gas from Russia’s Sakhalin Island to Hokkaido and

then on to the Tokyo metropolitan area. The pipeline, which would be

50 cm to 76 cm in diameter, would be brought onshore near Kashima Port

in Ibaraki Prefecture and connected to Tokyo Gas’s pipeline network. It

would cost up to around US$6.5bn and could transport 25 bcm/year.

Gas pipelines

LNG projects

LNG projects

Report

Sample

World Energy Research

Energy Report Sample— Japan Energy Report April 2018 — Copyright © Enerdata — All rights reserved 35

*Reproduction in whole or in part prohibited without written permission.

Oil

The 4th Strategic Energy Plan recognises oil as an important energy

resource for the transportation, civilian and power sectors. According to

the Energy Committee of the Japanese government, oil demand is

expected to fall by 1.6%/year over FY2015-FY2020.

The unconventional oil revolution in the U.S. has prompted the Japanese

Government to promote policies that will increase the competitiveness of

the Japanese petrochemical industry. The energy efficiency and

production flexibility of the Japanese refineries need to be improved to

enable competition with the new refineries in Asia.

CO2 capture and storage

JGC Corporation has also received a contract from Japan CCS to construct

the core facilities at a CO2 capture and storage (CCS) technology

demonstration project. The site for the demonstration project is located

adjacent to an oil refinery in Tomakomai, Hokkaido, owned by Idemitsu

Kosan. The lump-sum turnkey contract calls for the engineering,

procurement, construction and commissioning work associated with

carbon dioxide capture facilities with a yearly capacity of 200 000 t/year of

CO2, as well as compression, transportation and injection facilities. The

value of the contract was not disclosed. Capture started with the pilot

project in March 2016 and is planned to operate for three years.

Toshiba Energy Systems and Solutions has started construction on Japan’s

first large-scale carbon capture project at its 50 MW Mikawa biomass

power plant. The project is scheduled for commercial operations in 2020

and aims to capture more than 500 tCO2/d.

Uranium

Japan Oil, Oil, Gas and Metals National Corp. (JOGMEC) and Navoi Mining

and Metallurgical Combinat (Uzbekistan) will conduct joint exploration for

uranium in Uzbekistan, with the aim of supplying Japan with nuclear fuel

in the case of the restart of nuclear plants. They will conduct joint

exploration for around 5 years and verify the amount and quality of

Uzbekistan’s uranium deposits. JOGMEC continues to undertake

exploration in the Navoi region. In May 2017, the company published a bid

for uranium exploration activities, including drilling works and analysis in

Uzbekistan. If Japan sees potential in mining high-quality uranium, it will

try to secure concession rights to both import it and export it to other

countries.

Report

Sample

Energy Statistics

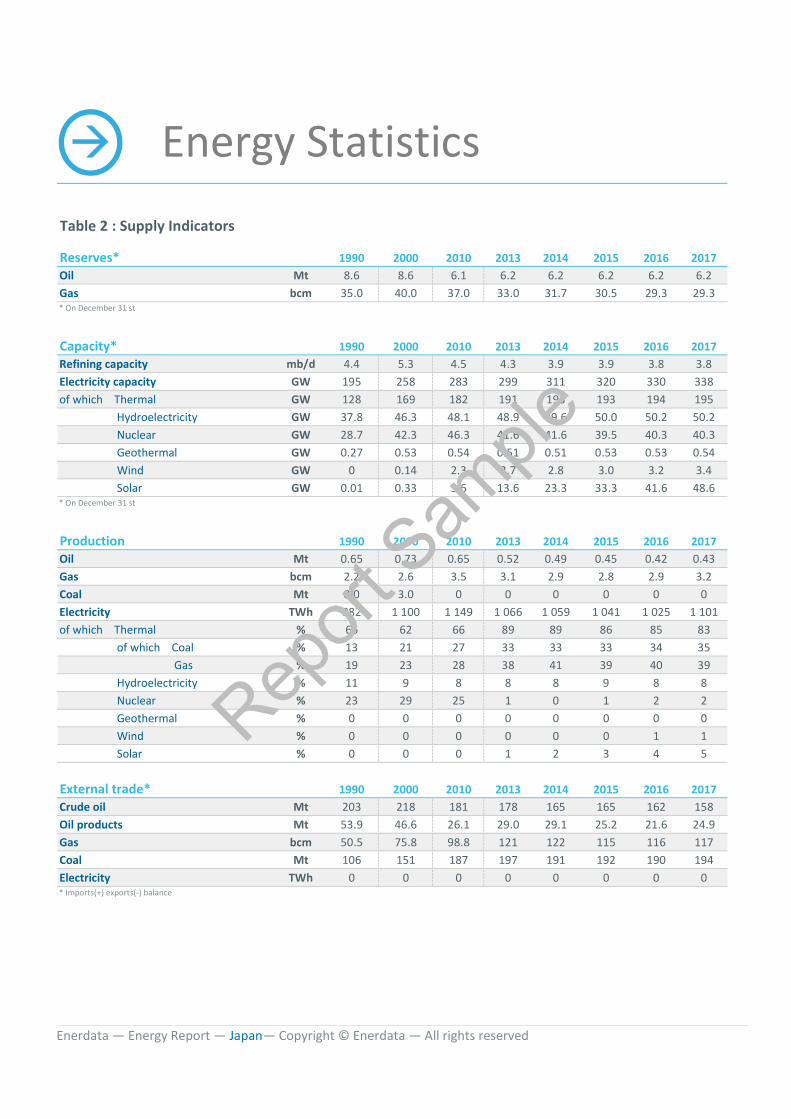

Table 2 : Supply Indicators

Reserves* 1990 2000 2010 2013 2014 2015 2016 2017Oil Mt 8.6 8.6 6.1 6.2 6.2 6.2 6.2 6.2Gas bcm 35.0 40.0 37.0 33.0 31.7 30.5 29.3 29.3* On December 31 st

Capacity* 1990 2000 2010 2013 2014 2015 2016 2017Refining capacity mb/d 4.4 5.3 4.5 4.3 3.9 3.9 3.8 3.8Electricity capacity GW 195 258 283 299 311 320 330 338of which Thermal GW 128 169 182 191 193 193 194 195 Hydroelectricity GW 37.8 46.3 48.1 48.9 49.6 50.0 50.2 50.2 Nuclear GW 28.7 42.3 46.3 41.6 41.6 39.5 40.3 40.3 Geothermal GW 0.27 0.53 0.54 0.51 0.51 0.53 0.53 0.54 Wind GW 0 0.14 2.3 2.7 2.8 3.0 3.2 3.4 Solar GW 0.01 0.33 3.6 13.6 23.3 33.3 41.6 48.6* On December 31 st

Production 1990 2000 2010 2013 2014 2015 2016 2017Oil Mt 0.65 0.73 0.65 0.52 0.49 0.45 0.42 0.43Gas bcm 2.2 2.6 3.5 3.1 2.9 2.8 2.9 3.2Coal Mt 8.0 3.0 0 0 0 0 0 0Electricity TWh 882 1 100 1 149 1 066 1 059 1 041 1 025 1 101of which Thermal % 66 62 66 89 89 86 85 83 of which Coal % 13 21 27 33 33 33 34 35 Gas % 19 23 28 38 41 39 40 39 Hydroelectricity % 11 9 8 8 8 9 8 8 Nuclear % 23 29 25 1 0 1 2 2 Geothermal % 0 0 0 0 0 0 0 0 Wind % 0 0 0 0 0 0 1 1 Solar % 0 0 0 1 2 3 4 5

External trade* 1990 2000 2010 2013 2014 2015 2016 2017Crude oil Mt 203 218 181 178 165 165 162 158Oil products Mt 53.9 46.6 26.1 29.0 29.1 25.2 21.6 24.9Gas bcm 50.5 75.8 98.8 121 122 115 116 117Coal Mt 106 151 187 197 191 192 190 194Electricity TWh 0 0 0 0 0 0 0 0* Imports(+) exports(-) balance

Enerdata — Energy Report — Japan— Copyright © Enerdata — All rights reserved

Report

Sample

Energy Statistics

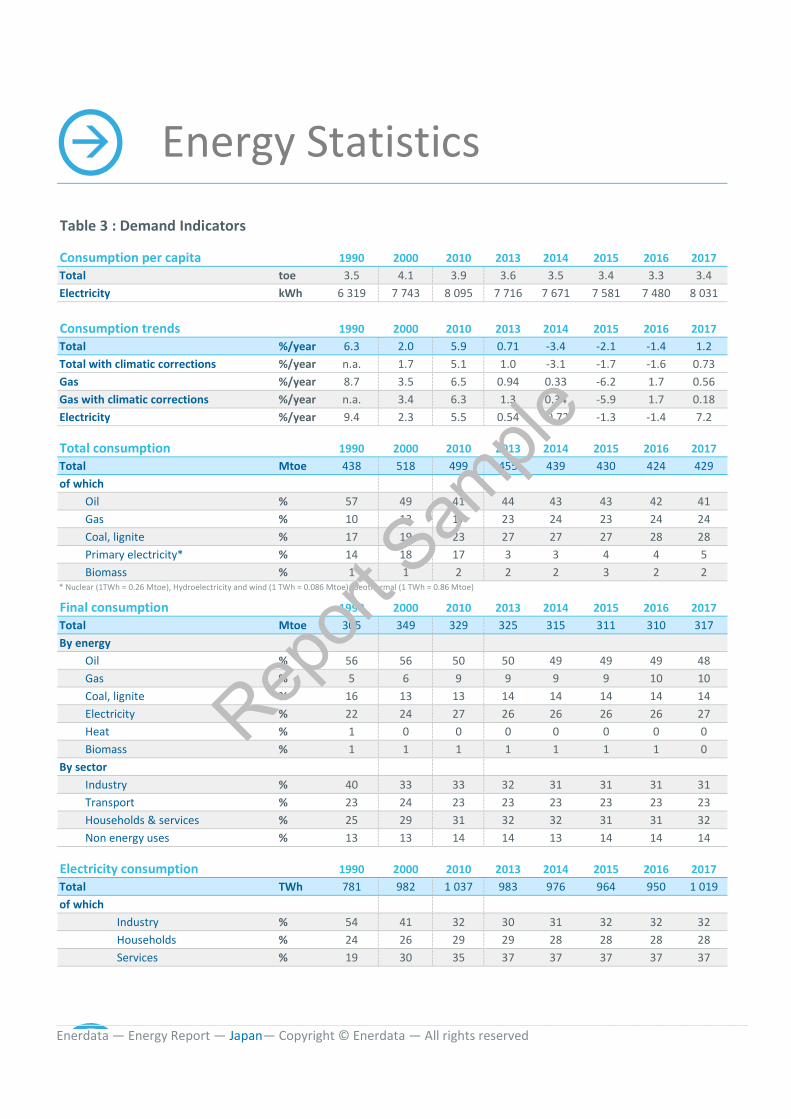

Table 3 : Demand Indicators

Consumption per capita 1990 2000 2010 2013 2014 2015 2016 2017Total toe 3.5 4.1 3.9 3.6 3.5 3.4 3.3 3.4Electricity kWh 6 319 7 743 8 095 7 716 7 671 7 581 7 480 8 031

Consumption trends 1990 2000 2010 2013 2014 2015 2016 2017Total %/year 6.3 2.0 5.9 0.71 -3.4 -2.1 -1.4 1.2Total with climatic corrections %/year n.a. 1.7 5.1 1.0 -3.1 -1.7 -1.6 0.73Gas %/year 8.7 3.5 6.5 0.94 0.33 -6.2 1.7 0.56Gas with climatic corrections %/year n.a. 3.4 6.3 1.3 0.34 -5.9 1.7 0.18Electricity %/year 9.4 2.3 5.5 0.54 -0.72 -1.3 -1.4 7.2

Total consumption 1990 2000 2010 2013 2014 2015 2016 2017Total Mtoe 438 518 499 455 439 430 424 429of which Oil % 57 49 41 44 43 43 42 41 Gas % 10 13 17 23 24 23 24 24 Coal, lignite % 17 19 23 27 27 27 28 28 Primary electricity* % 14 18 17 3 3 4 4 5 Biomass % 1 1 2 2 2 3 2 2* Nuclear (1TWh = 0.26 Mtoe), Hydroelectricity and wind (1 TWh = 0.086 Mtoe), Geothermal (1 TWh = 0.86 Mtoe)

Final consumption 1990 2000 2010 2013 2014 2015 2016 2017Total Mtoe 305 349 329 325 315 311 310 317By energy Oil % 56 56 50 50 49 49 49 48 Gas % 5 6 9 9 9 9 10 10 Coal, lignite % 16 13 13 14 14 14 14 14 Electricity % 22 24 27 26 26 26 26 27 Heat % 1 0 0 0 0 0 0 0 Biomass % 1 1 1 1 1 1 1 0By sector Industry % 40 33 33 32 31 31 31 31 Transport % 23 24 23 23 23 23 23 23 Households & services % 25 29 31 32 32 31 31 32 Non energy uses % 13 13 14 14 13 14 14 14

Electricity consumption 1990 2000 2010 2013 2014 2015 2016 2017Total TWh 781 982 1 037 983 976 964 950 1 019of which Industry % 54 41 32 30 31 32 32 32 Households % 24 26 29 29 28 28 28 28 Services % 19 30 35 37 37 37 37 37

Enerdata — Energy Report — Japan— Copyright © Enerdata — All rights reserved

Report

Sample

Energy Statistics

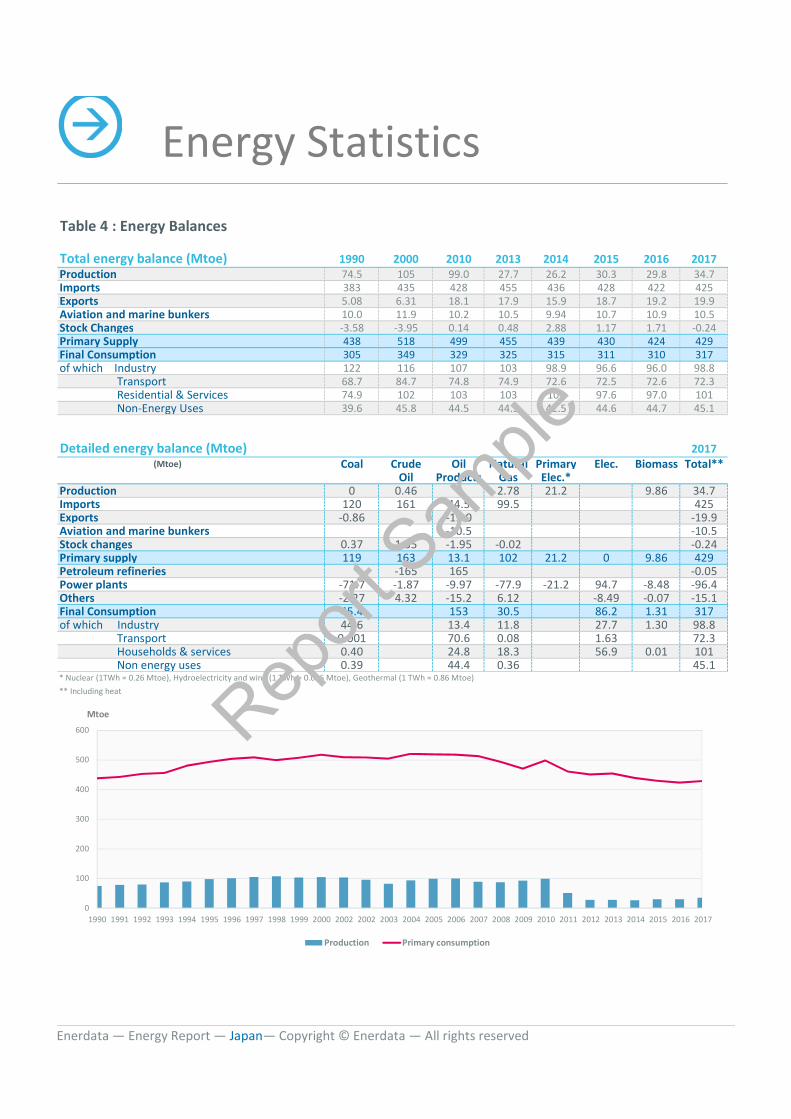

Table 4 : Energy Balances

Total energy balance (Mtoe) 1990 2000 2010 2013 2014 2015 2016 2017Production 74.5 105 99.0 27.7 26.2 30.3 29.8 34.7Imports 383 435 428 455 436 428 422 425Exports 5.08 6.31 18.1 17.9 15.9 18.7 19.2 19.9Aviation and marine bunkers 10.0 11.9 10.2 10.5 9.94 10.7 10.9 10.5Stock Changes -3.58 -3.95 0.14 0.48 2.88 1.17 1.71 -0.24Primary Supply 438 518 499 455 439 430 424 429Final Consumption 305 349 329 325 315 311 310 317of which Industry 122 116 107 103 98.9 96.6 96.0 98.8 Transport 68.7 84.7 74.8 74.9 72.6 72.5 72.6 72.3 Residential & Services 74.9 102 103 103 102 97.6 97.0 101 Non-Energy Uses 39.6 45.8 44.5 44.3 42.5 44.6 44.7 45.1

Detailed energy balance (Mtoe) 2017(Mtoe) Coal Crude Oil Natural Primary Elec. Biomass Total**

Oil Products Gas Elec.*Production 0 0.46 2.78 21.2 9.86 34.7Imports 120 161 44.5 99.5 425Exports -0.86 -19.0 -19.9Aviation and marine bunkers -10.5 -10.5Stock changes 0.37 1.35 -1.95 -0.02 -0.24Primary supply 119 163 13.1 102 21.2 0 9.86 429Petroleum refineries -165 165 -0.05Power plants -71.7 -1.87 -9.97 -77.9 -21.2 94.7 -8.48 -96.4Others -2.27 4.32 -15.2 6.12 -8.49 -0.07 -15.1Final Consumption 45.4 153 30.5 86.2 1.31 317of which Industry 44.6 13.4 11.8 27.7 1.30 98.8 Transport 0.001 70.6 0.08 1.63 72.3 Households & services 0.40 24.8 18.3 56.9 0.01 101 Non energy uses 0.39 44.4 0.36 45.1* Nuclear (1TWh = 0.26 Mtoe), Hydroelectricity and wind (1 TWh = 0.086 Mtoe), Geothermal (1 TWh = 0.86 Mtoe)** Including heat

0

100

200

300

400

500

600

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2002 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Production Primary consumption

Mtoe

Enerdata — Energy Report — Japan— Copyright © Enerdata — All rights reserved

Report

Sample

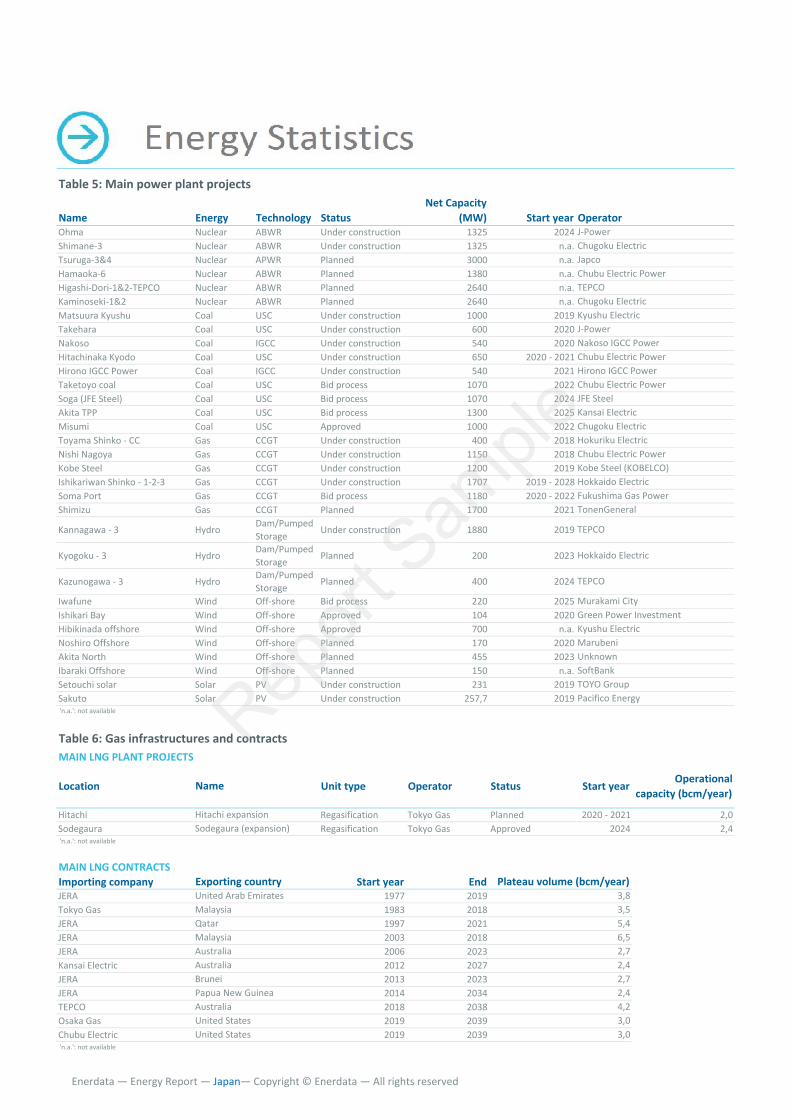

Name Energy Technology StatusNet Capacity

(MW) Start yearOhma Nuclear ABWR Under construction 1325 2024Shimane-3 Nuclear ABWR Under construction 1325 n.a.Tsuruga-3&4 Nuclear APWR Planned 3000 n.a.Hamaoka-6 Nuclear ABWR Planned 1380 n.a.Higashi-Dori-1&2-TEPCO Nuclear ABWR Planned 2640 n.a.Kaminoseki-1&2 Nuclear ABWR Planned 2640 n.a.Matsuura Kyushu Coal USC Under construction 1000 2019Takehara Coal USC Under construction 600 2020Nakoso Coal IGCC Under construction 540 2020Hitachinaka Kyodo Coal USC Under construction 650 2020 - 2021Hirono IGCC Power Coal IGCC Under construction 540 2021Taketoyo coal Coal USC Bid process 1070 2022Soga (JFE Steel) Coal USC Bid process 1070 2024Akita TPP Coal USC Bid process 1300 2025Misumi Coal USC Approved 1000 2022Toyama Shinko - CC Gas CCGT Under construction 400 2018Nishi Nagoya Gas CCGT Under construction 1150 2018Kobe Steel Gas CCGT Under construction 1200 2019Ishikariwan Shinko - 1-2-3 Gas CCGT Under construction 1707 2019 - 2028Soma Port Gas CCGT Bid process 1180 2020 - 2022Shimizu Gas CCGT Planned 1700 2021

Kannagawa - 3 Hydro Dam/PumpedStorage Under construction 1880 2019

Kyogoku - 3 Hydro Dam/PumpedStorage Planned 200 2023

Kazunogawa - 3 Hydro Dam/PumpedStorage Planned 400 2024

Iwafune Wind Off-shore Bid process 220 2025Ishikari Bay Wind Off-shore Approved 104 2020Hibikinada offshore Wind Off-shore Approved 700 n.a.Noshiro Offshore Wind Off-shore Planned 170 2020Akita North Wind Off-shore Planned 455 2023Ibaraki Offshore Wind Off-shore Planned 150 n.a.Setouchi solar Solar PV Under construction 231 2019Sakuto Solar PV Under construction 257,7 2019 'n.a.': not available

Location Unit type Operator Status Start year Operationalcapacity (bcm/year)

Hitachi Regasification Tokyo Gas Planned 2020 - 2021 2,0Sodegaura Regasification Tokyo Gas Approved 2024 2,4 'n.a.': not available

Importing company Start year EndJERA 1977 2019Tokyo Gas 1983 2018JERA 1997 2021JERA 2003 2018JERA 2006 2023Kansai Electric 2012 2027JERA 2013 2023JERA 2014 2034TEPCO 2018 2038Osaka Gas 2019 2039Chubu Electric 2019 2039 'n.a.': not available

Table 5: Main power plant projects

OperatorJ-PowerChugoku ElectricJapcoChubu Electric PowerTEPCOChugoku ElectricKyushu ElectricJ-PowerNakoso IGCC PowerChubu Electric PowerHirono IGCC PowerChubu Electric PowerJFE SteelKansai ElectricChugoku ElectricHokuriku ElectricChubu Electric PowerKobe Steel (KOBELCO)Hokkaido ElectricFukushima Gas PowerTonenGeneral

TEPCO

Hokkaido Electric

TEPCO