Financial Overview Heinie Werth Market and Product Philosophy Anton Gildenhuys Operations Hennie de Villiers Distribution, Sanlam Life Strategy Lizé Lambrechts Financial Overview Heinie Werth Financial Overview Financial Overview Heinie Heinie Werth Werth

Transcript

Financial Overview Heinie Werth

Market and Product Philosophy Anton Gildenhuys

OperationsHennie de Villiers

Distribution, Sanlam Life Strategy Lizé Lambrechts

Financial Overview

Heinie Werth

Financial OverviewFinancial Overview

HeinieHeinie WerthWerth

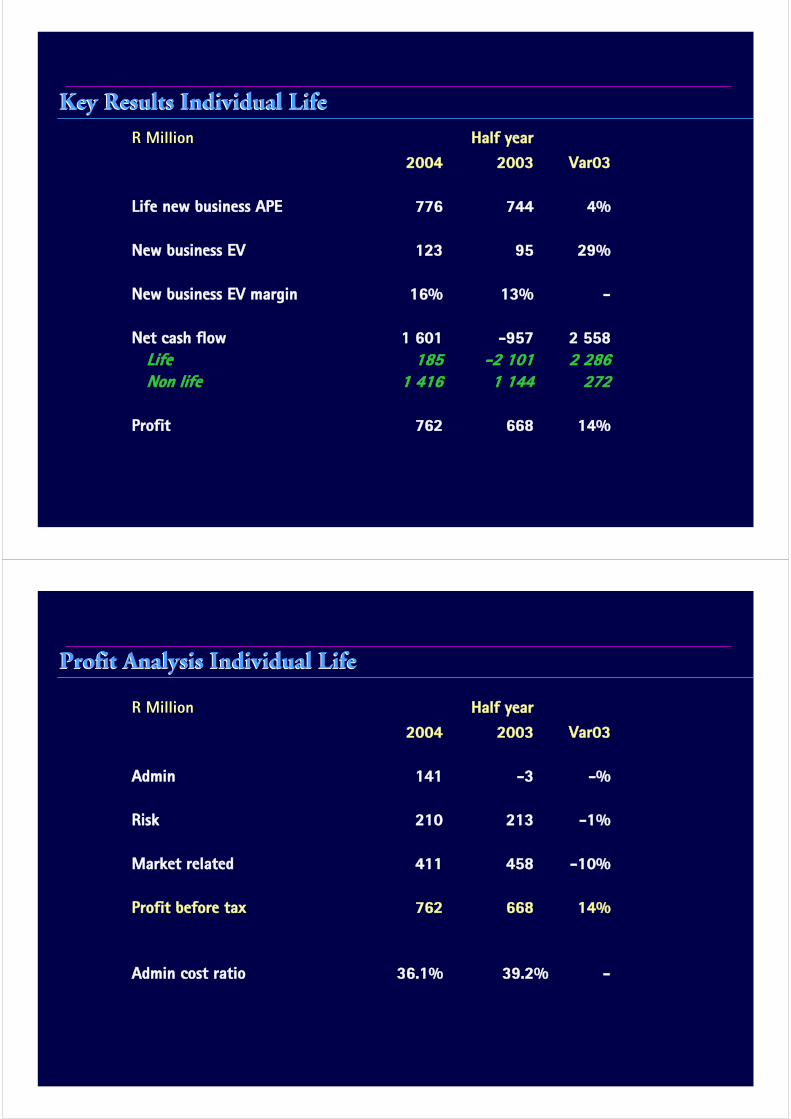

R Million Half year

2004 2003 Var03

Life new business APE 776 744 4%

New business EV 123 95 29%

New business EV margin 16% 13% -

Net cash flow 1 601 -957 2 558

Life 185 -2 101 2 286

Non life 1 416 1 144 272

Profit 762 668 14%

Key Results Individual LifeKey Results Individual Life

R Million Half year

2004 2003 Var03

Admin 141 -3 -%

Risk 210 213 -1%

Market related 411 458 -10%

Profit before tax 762 668 14%

Admin cost ratio 36.1% 39.2% -

Profit Analysis Individual LifeProfit Analysis Individual Life

6 Year Trend — Admin costs Individual Life6 Year Trend — Admin costs Individual Life

800

1 000

1 200

1 400

1 600

1 800

2 000

2000 2001 2002 2003 2004

R'm Actual 2000 base

R Million Half year

Total costs — 2003* 1 026

Add Inflation (5.4%) 55

Add MIA 37

Potential costs — 2004 1 118

Less Net savings -121

Total costs — 2004* 997

2004 estimated annual savings

- effective 285

- annualised 300

* Costs = admin costs plus other sales remuneration

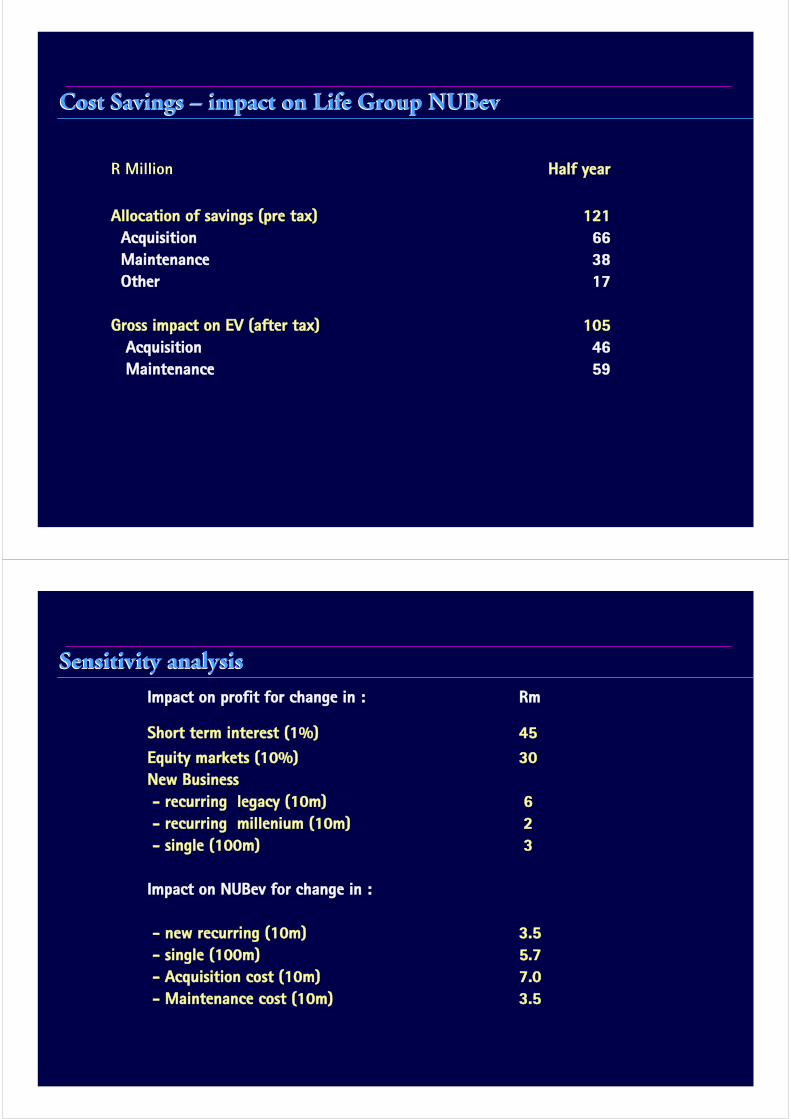

Recon of Cost Savings — Life GroupRecon of Cost Savings — Life Group

R Million Half year

Allocation of savings (pre tax) 121

Acquisition 66

Maintenance 38

Other 17

Gross impact on EV (after tax) 105

Acquisition 46

Maintenance 59

Cost Savings — impact on Life Group NUBevCost Savings — impact on Life Group NUBev

Impact on profit for change in : Rm

Short term interest (1%) 45

Equity markets (10%) 30

New Business

- recurring legacy (10m) 6

- recurring millenium (10m) 2

- single (100m) 3

Impact on NUBev for change in :

- new recurring (10m) 3.5

- single (100m) 5.7

- Acquisition cost (10m) 7.0

- Maintenance cost (10m) 3.5

Sensitivity analysisSensitivity analysis

Market and Products

Anton Gildenhuys

Market and ProductsMarket and Products

Anton Anton GildenhuysGildenhuys

Market segmented focusMarket segmented focus

Success in each market segment dependent on:

• Market potential

• Client contact

• Advice model

• Distribution model

• Marketing

• Product support

• Product design

• Client service

• Segment profitability (result of all the above)

Market segmented focusMarket segmented focus

Market segmented teams responsible for:

• Aligning components

• Allocating resources to areas that will yield maximum result

Product StrategyProduct Strategy

QualityQualityInnovationInnovation

PricePrice

Product StrategyProduct Strategy

InnovationInnovation

Some Sanlam firstsSome Sanlam firsts

• Offshore asset swaps (1995)

• Structured products (1997)

• New generation, unitised, flexible savings; Stratus (2000)

• Endowment / RA payable anywhere in world (2001/2)

• Liquid offshore fund of hedge funds (2002)

• Tax & Forex Amnesty product (2003)

• 7 Year Guaranteed Endowment (2004)

Some innovations in the past yearSome innovations in the past year

• ALSI40 Highest level locker

• Highest monthly value locked in

• ALSI40 tracker over 6 year term

• Subject to cap over term of product (120%)

• Escalating guarantee investment

• Cliquet

• 5 Year term

• LEAD Fund of hedge funds

• South African hedge funds

Product StrategyProduct Strategy

PricePrice

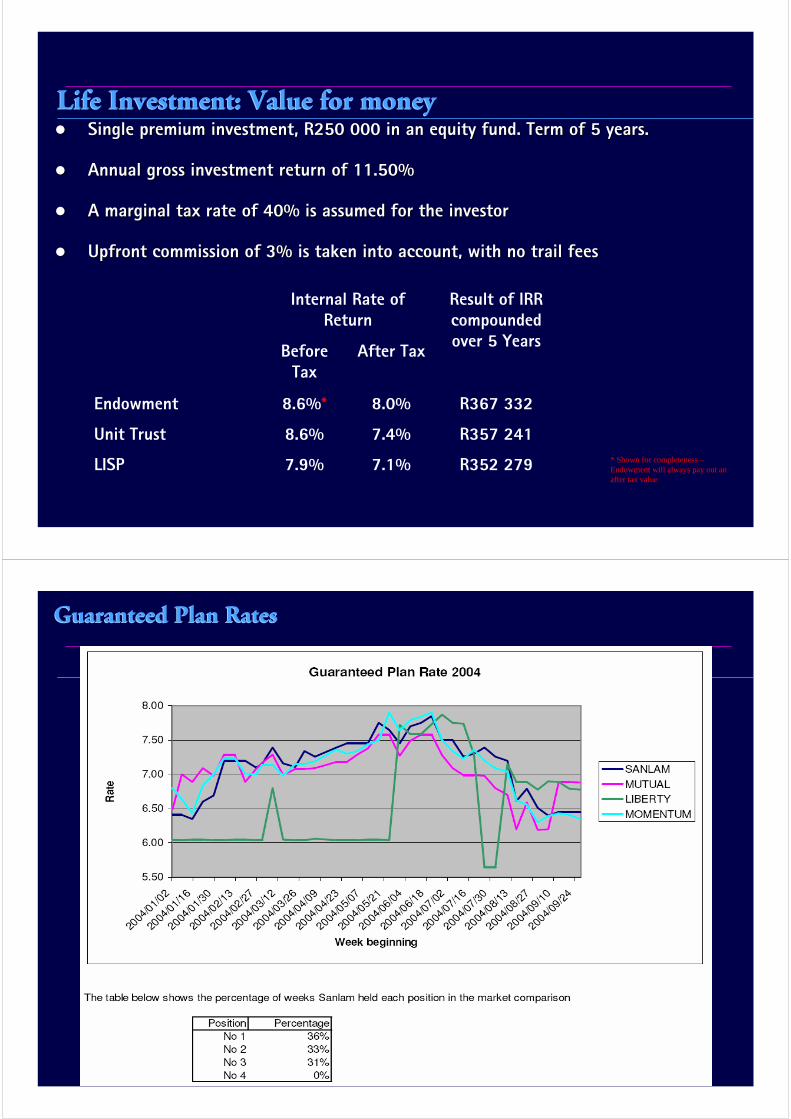

Life Investment: Value for moneyLife Investment: Value for moneySingle premium investment, R250 000 in an equity fund. Term of 5Single premium investment, R250 000 in an equity fund. Term of 5 years.years.

Annual gross investment return of 11.50%Annual gross investment return of 11.50%

A marginal tax rate of 40% is assumed for the investorA marginal tax rate of 40% is assumed for the investor

Upfront commission of 3% is taken into account, with no trail feUpfront commission of 3% is taken into account, with no trail feeses

R352 279

R357 241

R367 332

Result of IRR

compounded

over 5 Years

7.1%7.9%LISP

7.4%8.6%Unit Trust

8.0%8.6%*Endowment

After TaxBefore

Tax

Internal Rate of

Return

* Shown for completeness –Endowment will always pay out an after tax value

Guaranteed Plan RatesGuaranteed Plan Rates

Product StrategyProduct Strategy

QualityQuality

Quality productsQuality products• Client focused

• Value for money

• Real benefits — integrity

• Benefit design appropriate to needs of client

• Examples

Matrix : Underwritten for life. No need to notify Sanlam if

• Change in occupation

• Part time activities

• Change from smoker to non-smoker

Funeral products. Premiums guaranteed for policy term

Stratus savings products. Focus on value for money

• Minimum premiums

• Transparency of charges

The road aheadThe road ahead

• Comprehensive product set — increase share of wallet:

Mortgages

Other

• Innovate regularly:

International products

Structured products, e.g. ALSI40 locker, Escalating guarantee

Risk product rider benefits

• Focus on core products:

Best of breed

Huge leveraging opportunity

• Package advice within product

Lifetime options

Sim.sense

Sanlam Life Operations

Hennie de Villiers

Sanlam Life OperationsSanlam Life Operations

HennieHennie de de VilliersVilliers

Operations’ GoalsOperations’ Goals

• To provide value for money to clients

• To be the service provider of choice for our clients and

intermediaries

• To retain existing business

• To grow administration profit

• To provide innovative needs driven IT & business solutions

• SME and SMME (entrepreneurs and small businesses)

• We exclude the mass markets

How will we win?How will we win?

•

Goals and Aspirations

Client centricity

Market segment

focus

New and alternative sources of

profit

• Outstanding execution

• High performance organisation and employer of choice

• Success friendly environment

• Cost management/operational effectiveness and efficiency

• Alliance and network management

• Brand awareness

Dominant

distribution

Issue : ABSA penetration

• relationship / service at regional level

• Data brokers and Business Bank

• Products

• Progress this year

Distribution actionsDistribution actions

Issue : Entry Level Market

• Expand SGS to 500 advisors

• Broker channel

• direct marketing

• Structural growth

• UB/BFS

Distribution actionsDistribution actions

Issue : Gauteng Market share

• BSO concept

• Develop black broker networks

• Gauteng Agency Initiative

• Rebuild Gauteng broker region

• Appoint black advisers

Distribution actionsDistribution actions

Issue : Low productivity

• Performance management

• Review incentives

• Sales support

• Remuneration more variable

• Manage as a business on transfer price basis

Distribution actionsDistribution actions

Issue : Affluent Market

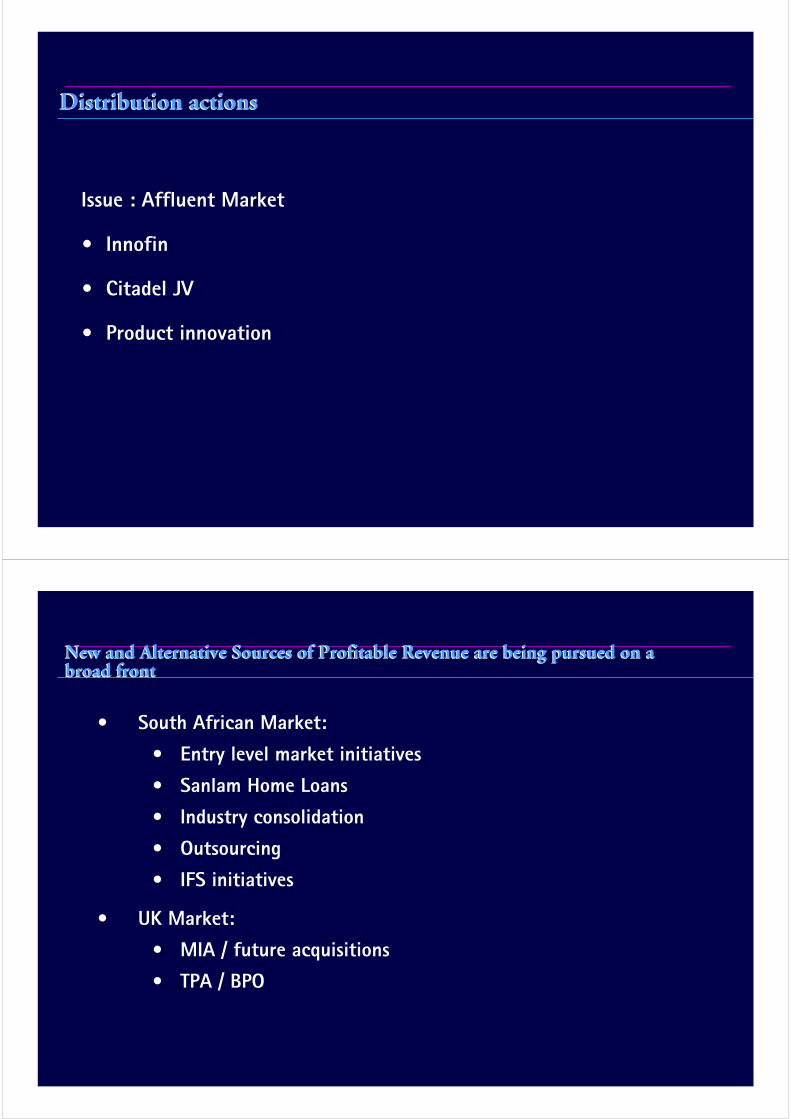

• Innofin

• Citadel JV

• Product innovation

Distribution actionsDistribution actions

New and Alternative Sources of Profitable Revenue are being pursued on a broad frontNew and Alternative Sources of Profitable Revenue are being pursued on a broad front