Developments of Credit Demand and Supply in Armenian Banking System Hayk Sargsyan The Central bank of Armenia, 6 V. Sargsyan, 0010, Yerevan, Armenia Narek Sargsyan The Central bank of Armenia, 6 V. Sargsyan, 0010, Yerevan, Armenia

Transcript

Developments of Credit Demand and Supply in Armenian Banking

System

Hayk Sargsyan

The Central bank of Armenia, 6 V. Sargsyan, 0010, Yerevan, Armenia

Narek Sargsyan

The Central bank of Armenia, 6 V. Sargsyan, 0010, Yerevan, Armenia

Outline

• The Research Question

• Literature Review

• Introduction to Armenian Banking System

• The Theoretical Model

• The Used Dataset

• Empirical Approach and the Results

• Summary and Conclusions

• Future

Outline

• The Research Question

• Literature Review

• Introduction to Armenian Banking System

• The Theoretical Model

• The Used Dataset

• Empirical Approach and the Results

• Summary and Conclusions

• Future

The Research Question

• Is financial intermediary in Armenian bankingsystem explained by the fundamentals?

– The recent developments in Armenian bankingsystem give rise to different debates about thisproblem, so the following research aims clear upthis question

Some Views

• IMF Mission to Armenia in 2007 led byMs. Marta Castello-Branco

– The recent increase in the financial intermediation is apositive development for Armenian economy and theCentral bank of Armenia should encourage this trend,meanwhile it should further provide high prudentialstandards for banks to keep efficient risk management andtransparency

Some Views

• Financial Sector Assessment Program (FSAP (2012))

– Armenia has still low level of financial intermediary, in terms of lowcredit to GDP ratio, and there are a numerous opportunities toincrease the financial intermediary in Armenia which will havereasonable contribution to economic growth of this country

– The main disturbing factors are underdeveloped marketinfrastructures, especially outside the capital city Yerevan, complicatedprocedures relating to the collateral for loans, high level ofintermediation spreads, underdeveloped capital markets, and finallylow share of non-banking sector

Some Views

• Head of EBRD Yerevan Resident Office,Mark Davis

– In response to the question about the possible effects ofthe Central bank`s decision about the increase in the levelof minimum capital requirement since 2017, he answeredthat this will result to the possible increase in capital inflowto Armenian banking system, hence the financialdeepening, and this effect should be welcomed

Some Views

• However, recently we can observe a common fear that financialintermediation in Armenia has already exceeded the payable demand andfurther deepening may bring to the increase of risk in the banking system

• The supporters of this view claim that

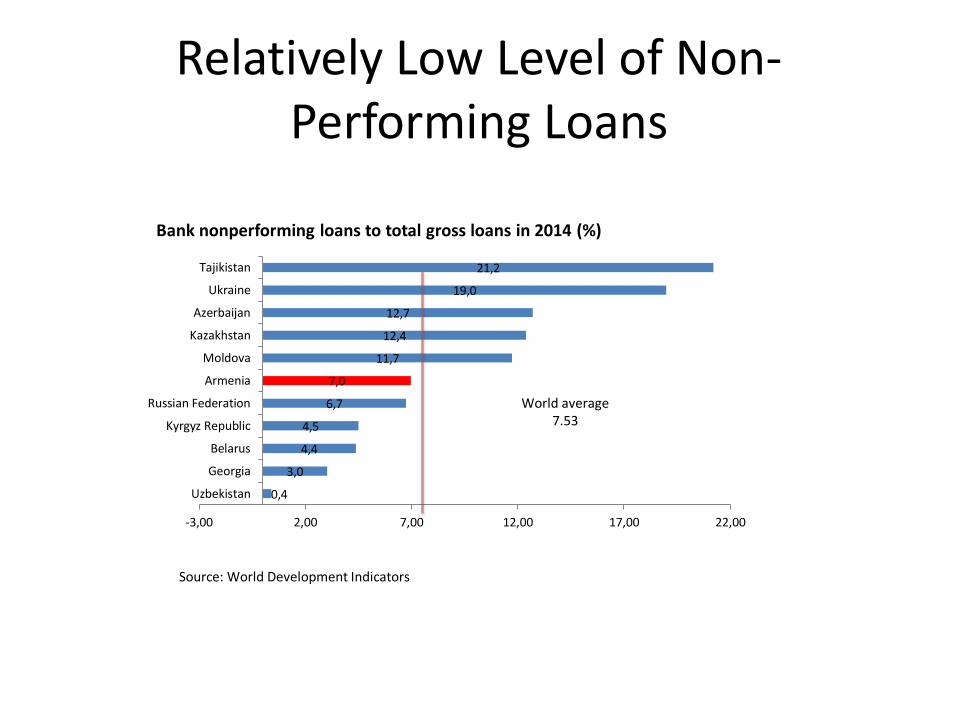

– During the recent five years NPL in Armenia was always growing andcompared with 2010 it increased approximately three times and was about9.13% in 2015

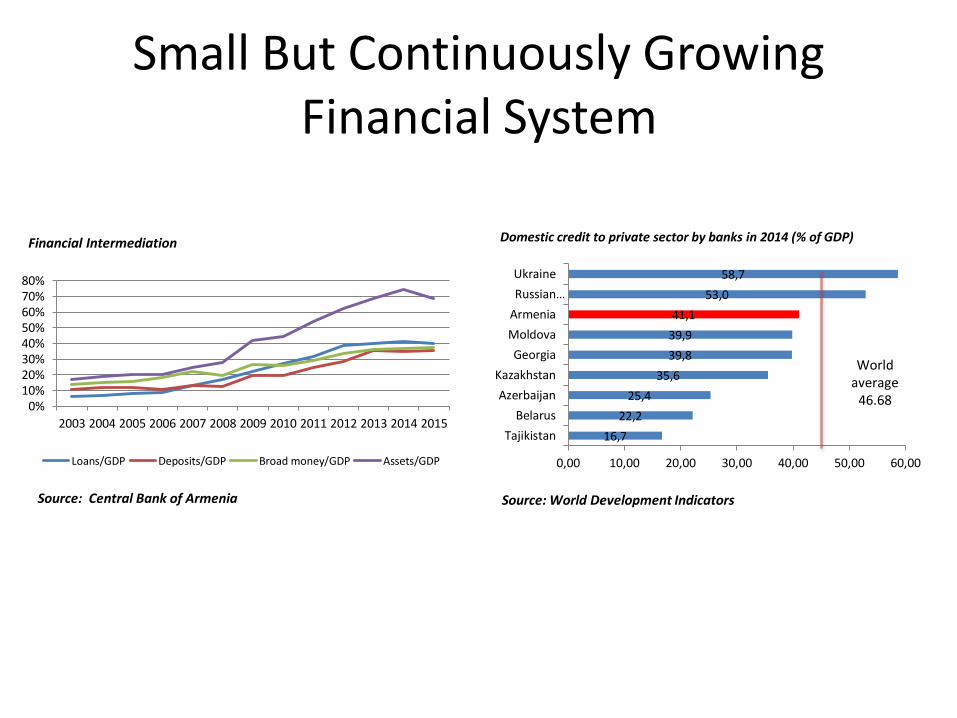

– Armenia has already high financial intermediation ratio, compared to itsneighbors; according to the WB, in 2014 the share of domestic credit to privatesector by banks was about 41.08%, and with this number Armenia was thethird country among the CIS countries, staying behind only from Russia andUkraine

Outline

• The Research Question

• Literature Review

• Introduction to Armenian Banking System

• The Theoretical Model

• The Used Dataset

• Empirical Approach and the Results

• Summary and Conclusions

• Future

Literature Review

• Melitz J and Pardue M., «The Demand and Supply of Commercial Bank Loans», Journal of Money, Credit and Banking, Vol. 5, No. 2 (May, 1973), pp. 669-692

• Panagopoulos Y. and Spiliotis A., «The Determinants of Commercial Banks' Lending Behavior: Some Evidence for Greece», Journal of Post Keynesian Economics, Vol. 20, No. 4 (summer, 1998), pp. 649-672

• Calza A., C. Gartner and J. Sousa, «Modeling the demand for loans to the private sector in the euro area» Working paper No. 55

• Aoki S., T. Hasegawa and S. Watanabe, (2009) “Supply and Demand Factors of Stagnant Bank Lending in the U.S. and Europe: Comparison with Japan’s Post-Bubble Period “. Bank of Japan Review

• Plašil M., Radkovský Š. and Řežábek P., (2013). Modelling Bank Loans to Non-financial Corporations. Czech National Bank / Financial Stability Report 2012/2013

Outline

• The Research Question

• Literature Review

• Introduction to Armenian Banking System

• The Theoretical Model

• The Used Dataset

• Empirical Approach and the Results

• Summary and Conclusions

• Future

Introduction to Armenian Banking System

• Armenian financial system consists of mainly bankingsector with 22 commercial banks (about 89%), smallinsurance sector, and insignificant capital markets

• More than the half of the banking sector assetsbelongs to the foreign capital, originating from Russia,France, UK, Cyprus and Kazakhstan

• Among the foreign owners we can also find manyinternational organizations, like EBRD, IFC, KFW, orOPEC Fund for International Development

Small But Continuously Growing Financial System

16,7

22,2

25,4

35,6

39,8

39,9

41,1

53,0

58,7

0,00 10,00 20,00 30,00 40,00 50,00 60,00

Tajikistan

Belarus

Azerbaijan

Kazakhstan

Georgia

Moldova

Armenia

Russian…

Ukraine

Domestic credit to private sector by banks in 2014 (% of GDP)

Bank nonperforming loans to total gross loans in 2014 (%)

Source: World Development Indicators

World average7.53

Stable Banking System

Capital adequacy

Assets quality

Yield

Liquidity

Interest rate risk

Foreign exchange risk

Banking system stability map

2014 2015

Source: Central Bank of Armenia

Outline

• The Research Question

• Literature Review

• Introduction to Armenian Banking System

• The Theoretical Model

• The Used Dataset

• Empirical Approach and the Results

• Summary and Conclusions

• Future

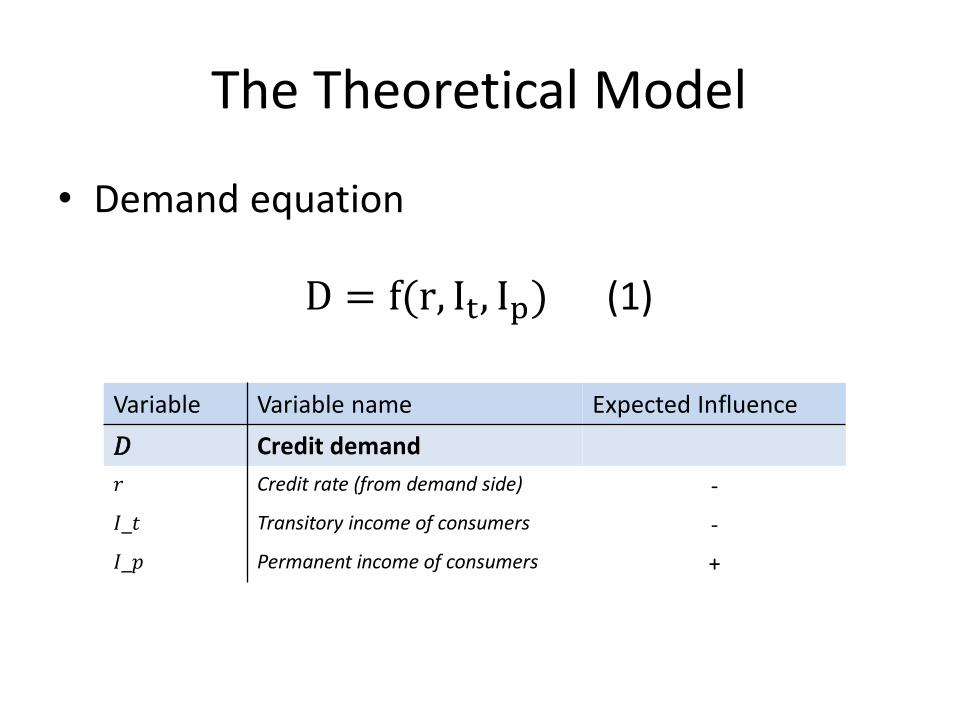

The Theoretical Model

• Demand equation

D = f(r, It, Ip) (1)

Variable Variable name Expected Influence

𝐷 Credit demand

𝑟 Credit rate (from demand side) -

𝐼_𝑡 Transitory income of consumers -

𝐼_𝑝 Permanent income of consumers +

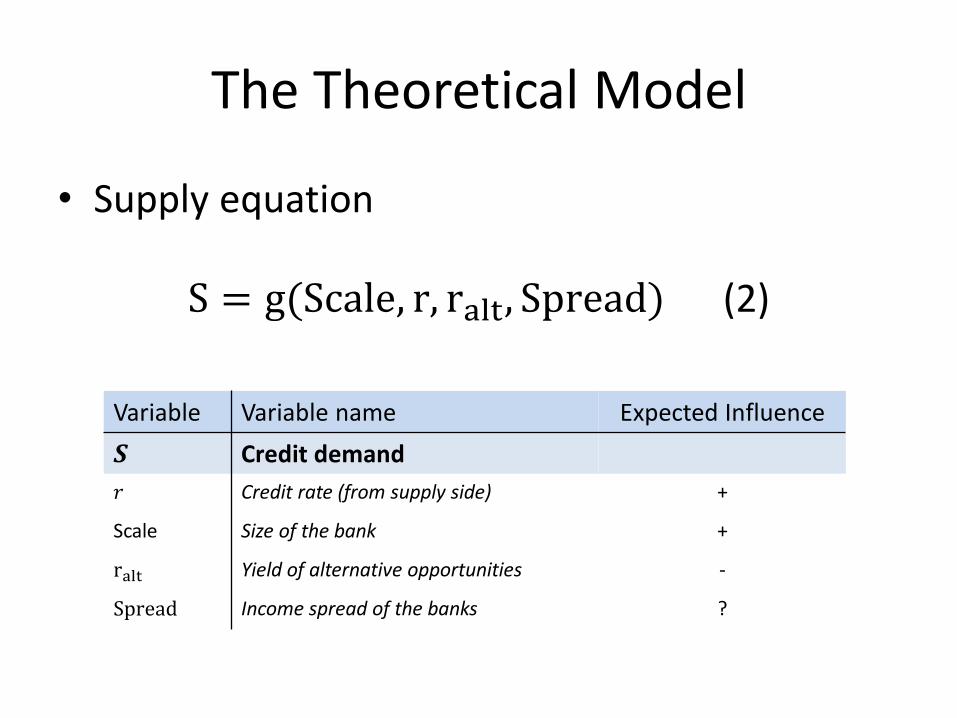

The Theoretical Model

• Supply equation

S = g(Scale, r, ralt, Spread) (2)

Variable Variable name Expected Influence

𝑺 Credit demand

𝑟 Credit rate (from supply side) +

Scale Size of the bank +

ralt Yield of alternative opportunities -

Spread Income spread of the banks ?

Outline

• The Research Question

• Literature Review

• Introduction to Armenian Banking System

• The Theoretical Model

• The Used Dataset

• Empirical Approach and the Results

• Summary and Conclusions

• Future

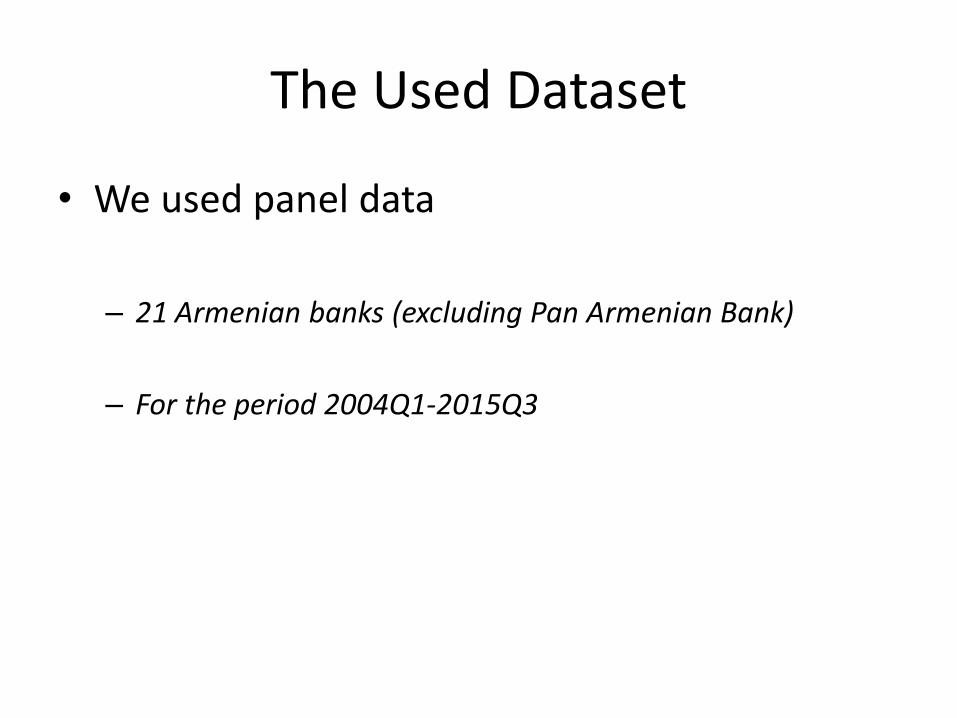

The Used Dataset

• We used panel data

– 21 Armenian banks (excluding Pan Armenian Bank)

– For the period 2004Q1-2015Q3

The Dependent Variable(Credit Volume)

• Dependent variable in both the equations is the actual levels of total loanvolume in billion AMD (stock, monthly average) given by the particularbank during the given period

0

100

200

300

2004q1 2007q1 2010q1 2013q1 2016q1date

Total loan volume in billion AMD (stock, monthly average) mean_loan_vol

loan_vol

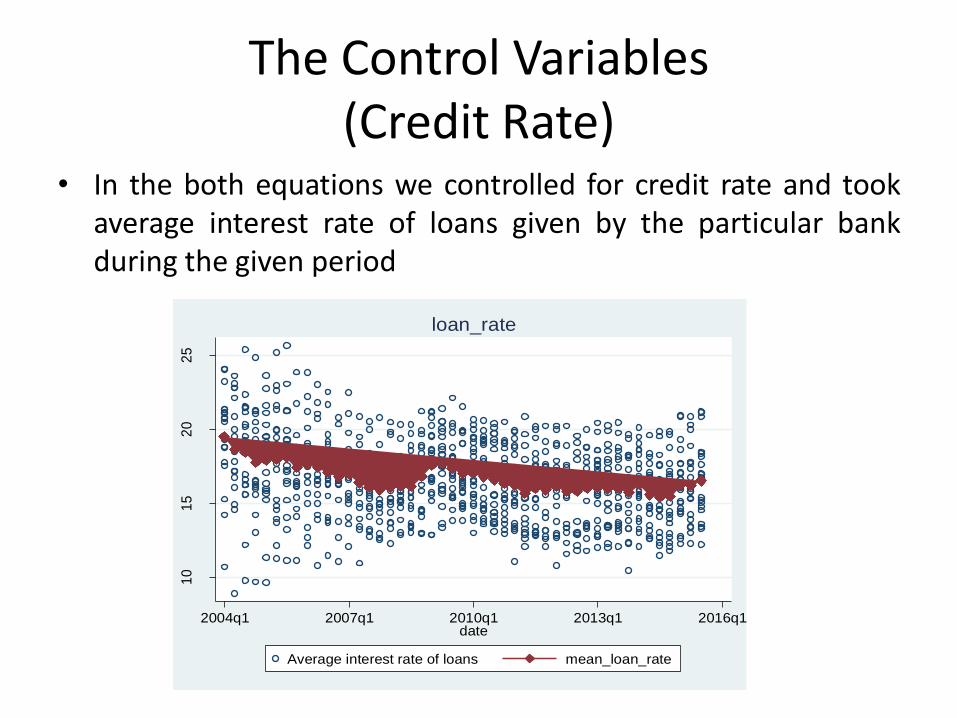

The Control Variables(Credit Rate)

• In the both equations we controlled for credit rate and tookaverage interest rate of loans given by the particular bankduring the given period

10

15

20

25

2004q1 2007q1 2010q1 2013q1 2016q1date

Average interest rate of loans mean_loan_rate

loan_rate

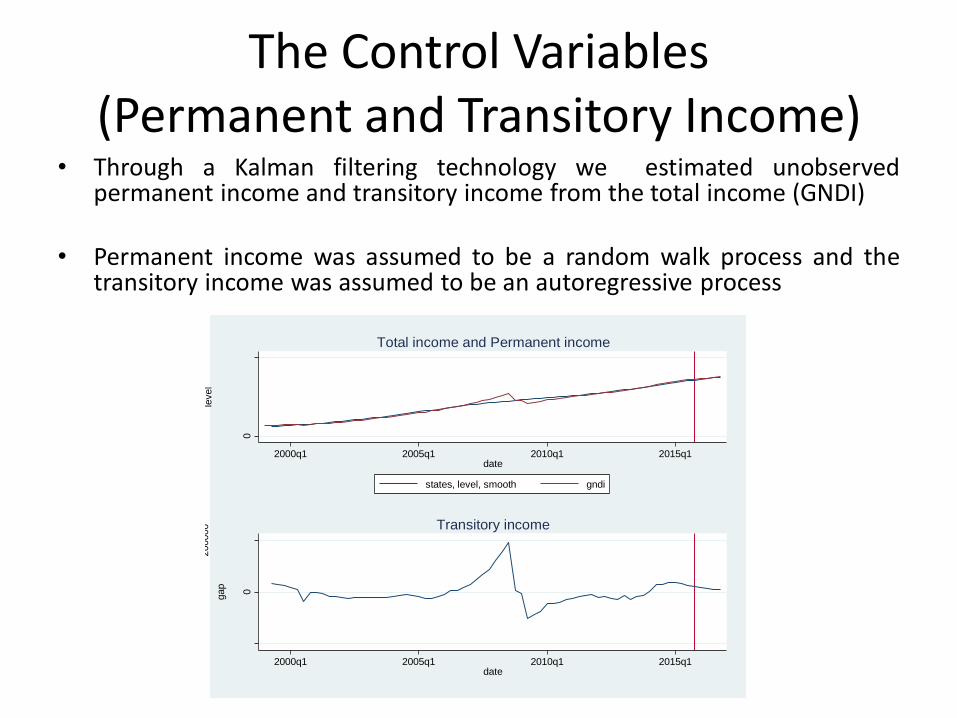

The Control Variables(Permanent and Transitory Income)

• Through a Kalman filtering technology we estimated unobservedpermanent income and transitory income from the total income (GNDI)

• Permanent income was assumed to be a random walk process and thetransitory income was assumed to be an autoregressive process

0

2000000

level

2000q1 2005q1 2010q1 2015q1date

states, level, smooth gndi

Total income and Permanent income

-200000

0

200000

gap

2000q1 2005q1 2010q1 2015q1date

Transitory income

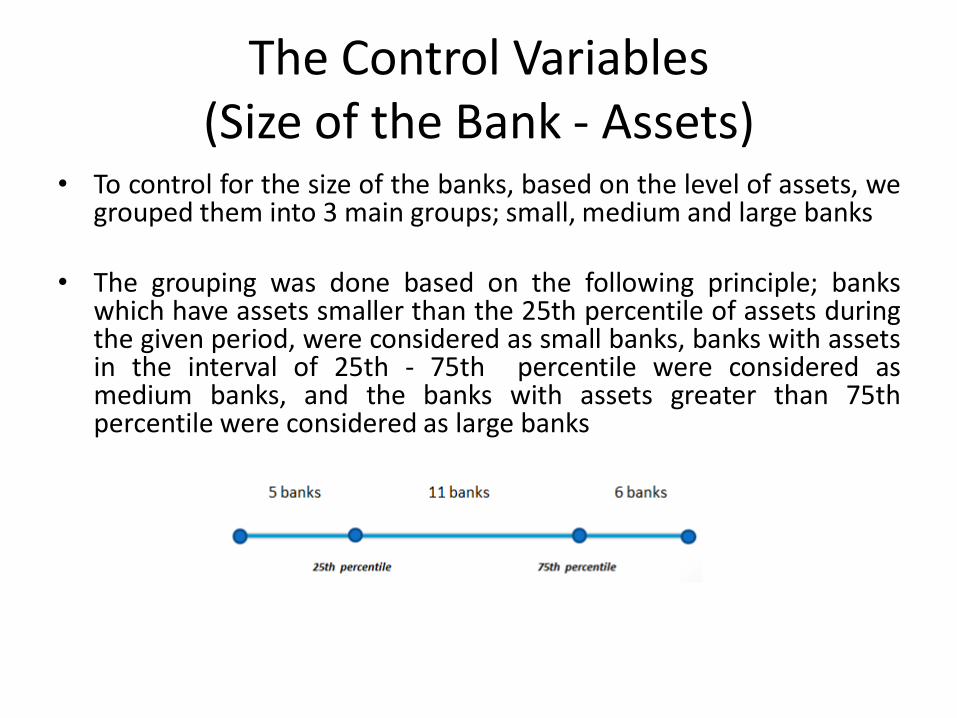

The Control Variables(Size of the Bank - Assets)

• To control for the size of the banks, based on the level of assets, wegrouped them into 3 main groups; small, medium and large banks

• The grouping was done based on the following principle; bankswhich have assets smaller than the 25th percentile of assets duringthe given period, were considered as small banks, banks with assetsin the interval of 25th - 75th percentile were considered asmedium banks, and the banks with assets greater than 75thpercentile were considered as large banks

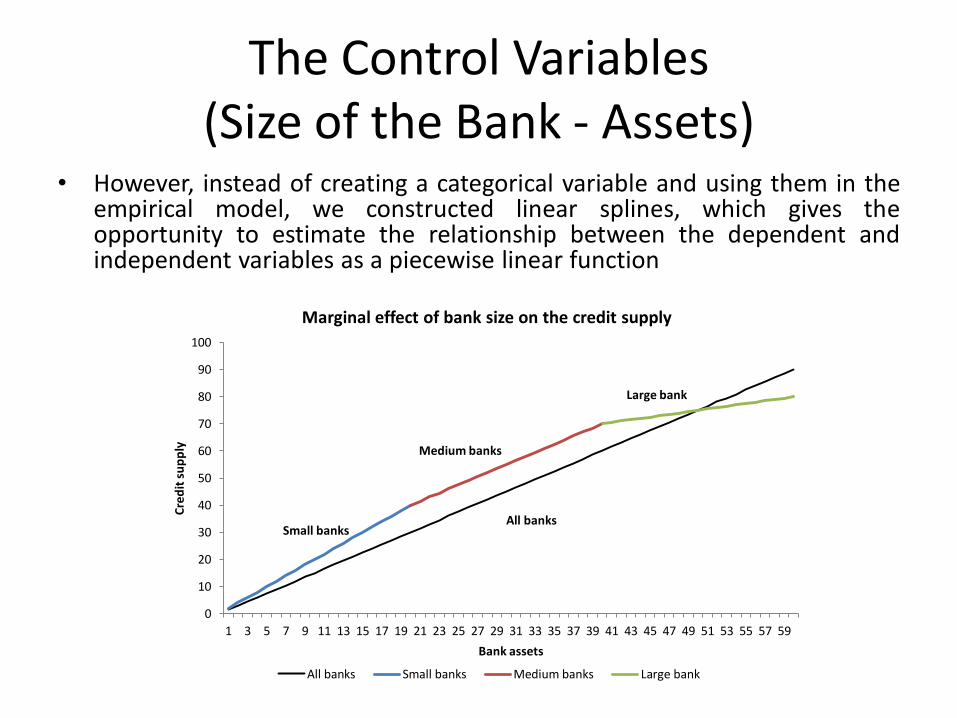

The Control Variables(Size of the Bank - Assets)

• However, instead of creating a categorical variable and using them in theempirical model, we constructed linear splines, which gives theopportunity to estimate the relationship between the dependent andindependent variables as a piecewise linear function

The Control Variables(Alternative Opportunity Rate)

• As an alternative opportunity rate we tookgovernment treasury bills rate4

.00

6.0

08

.00

10.0

01

2.0

01

4.0

0r_

alt

2003q1 2006q1 2009q1 2012q1 2015q1date

GT rates

Regime switch

Sharpe appreciation of AMD

Sharpe depreciation of AMD

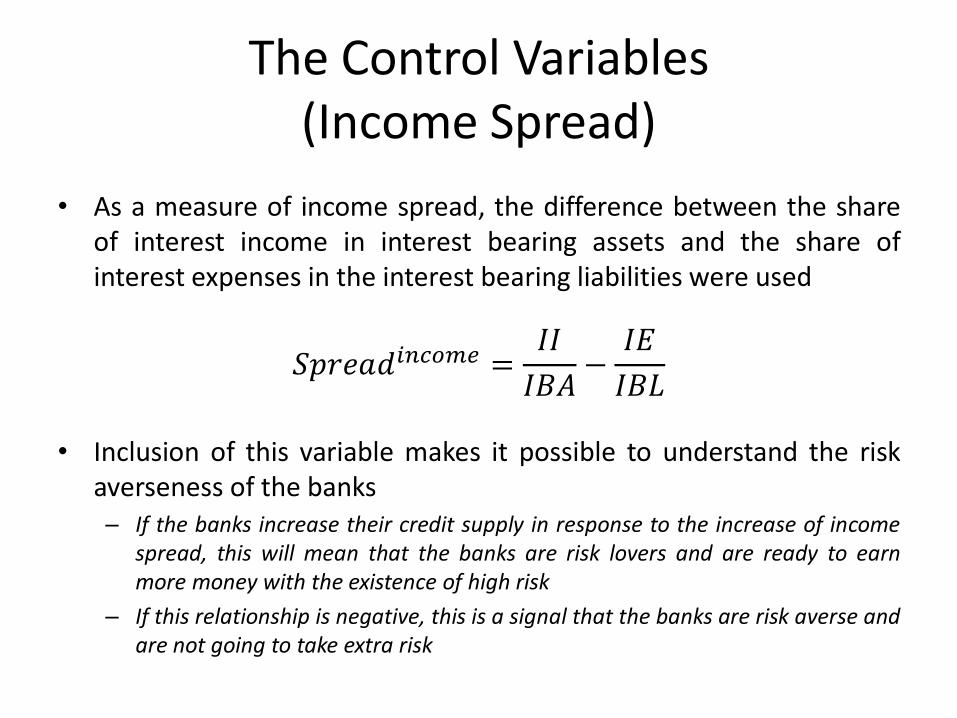

The Control Variables(Income Spread)

• As a measure of income spread, the difference between the shareof interest income in interest bearing assets and the share ofinterest expenses in the interest bearing liabilities were used

𝑆𝑝𝑟𝑒𝑎𝑑𝑖𝑛𝑐𝑜𝑚𝑒 =𝐼𝐼

𝐼𝐵𝐴−

𝐼𝐸

𝐼𝐵𝐿

• Inclusion of this variable makes it possible to understand the riskaverseness of the banks– If the banks increase their credit supply in response to the increase of income

spread, this will mean that the banks are risk lovers and are ready to earnmore money with the existence of high risk

– If this relationship is negative, this is a signal that the banks are risk averse andare not going to take extra risk

The Control Variables(Income Spread)

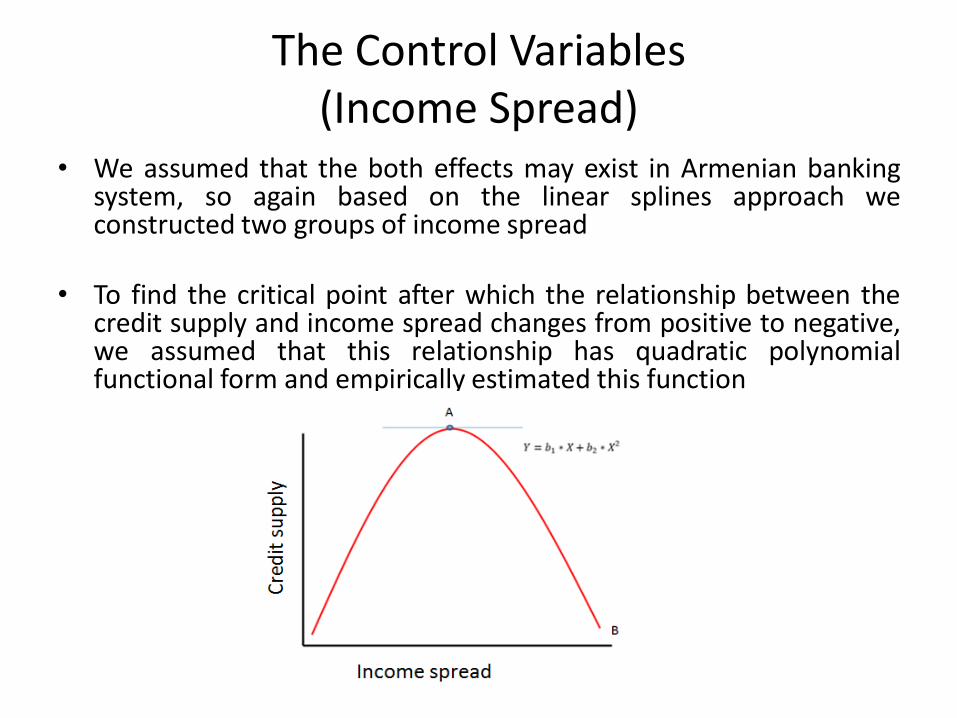

• We assumed that the both effects may exist in Armenian bankingsystem, so again based on the linear splines approach weconstructed two groups of income spread

• To find the critical point after which the relationship between thecredit supply and income spread changes from positive to negative,we assumed that this relationship has quadratic polynomialfunctional form and empirically estimated this function

Outline

• The Research Question

• Literature Review

• Introduction to Armenian Banking System

• The Theoretical Model

• The Used Dataset

• Empirical Approach and the Results

• Summary and Conclusions

• Future

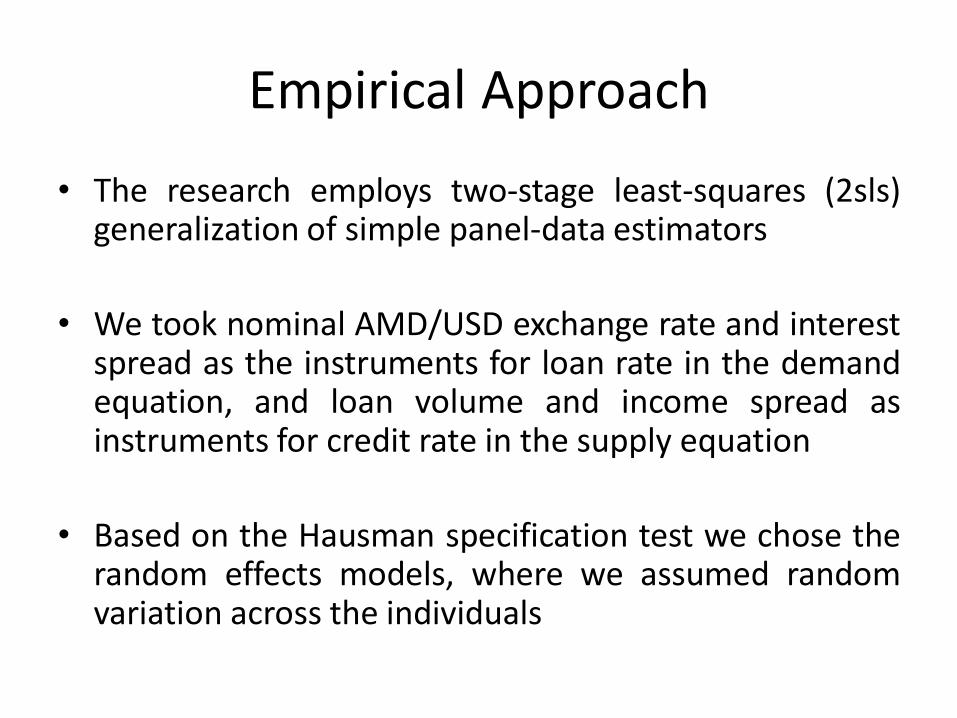

Empirical Approach

• The research employs two-stage least-squares (2sls)generalization of simple panel-data estimators

• We took nominal AMD/USD exchange rate and interestspread as the instruments for loan rate in the demandequation, and loan volume and income spread asinstruments for credit rate in the supply equation

• Based on the Hausman specification test we chose therandom effects models, where we assumed randomvariation across the individuals

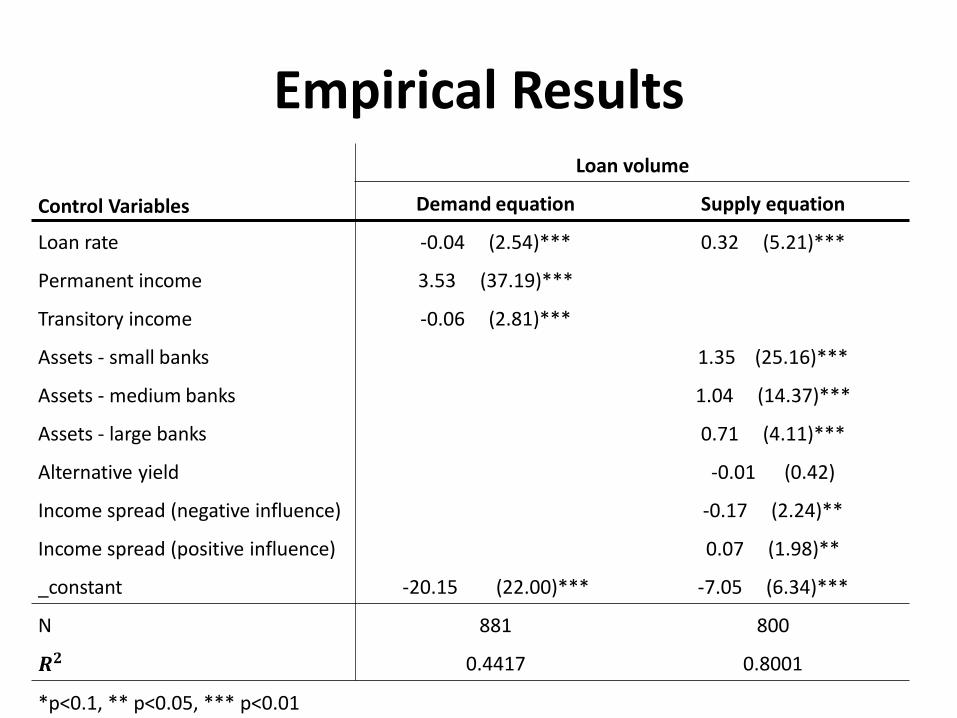

Empirical ResultsLoan volume

Control Variables Demand equation Supply equation

Loan rate -0.04 (2.54)*** 0.32 (5.21)***

Permanent income 3.53 (37.19)***

Transitory income -0.06 (2.81)***

Assets - small banks 1.35 (25.16)***

Assets - medium banks 1.04 (14.37)***

Assets - large banks 0.71 (4.11)***

Alternative yield -0.01 (0.42)

Income spread (negative influence) -0.17 (2.24)**

Income spread (positive influence) 0.07 (1.98)**

_constant -20.15 (22.00)*** -7.05 (6.34)***

N 881 800

𝑹𝟐 0.4417 0.8001

*p<0.1, ** p<0.05, *** p<0.01

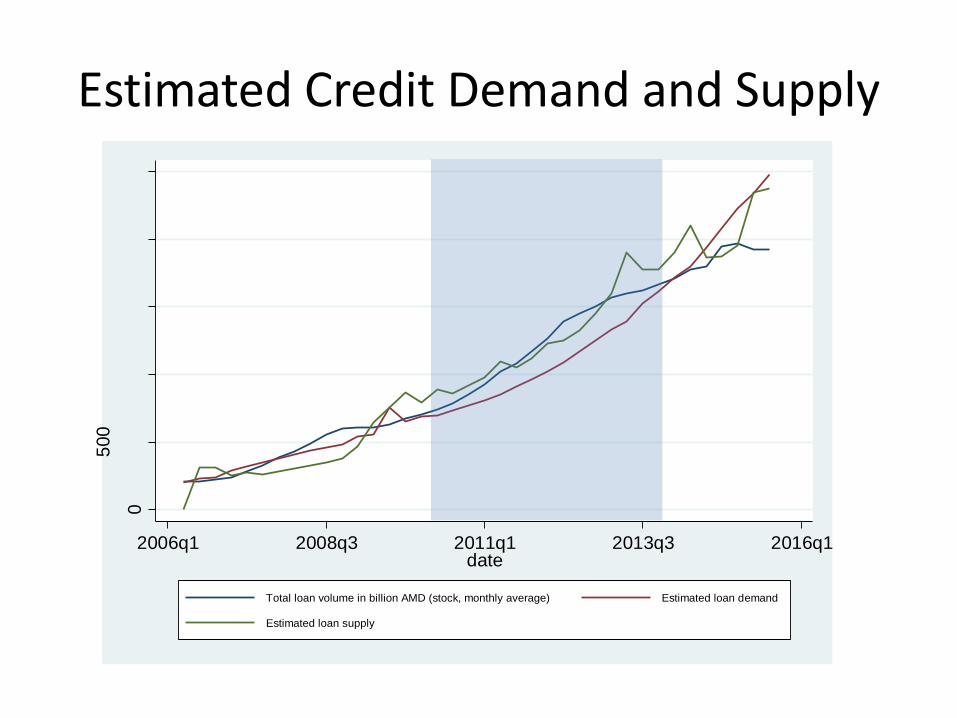

Estimated Credit Demand and Supply0

500

100

01

50

02

00

02

50

0

2006q1 2008q3 2011q1 2013q3 2016q1date

Total loan volume in billion AMD (stock, monthly average) Estimated loan demand

Estimated loan supply

Outline

• The Research Question

• Literature Review

• Introduction to Armenian Banking System

• The Theoretical Model

• The Used Dataset

• Empirical Approach and the Results

• Summary and Conclusions

• Future

Summary and Conclusions

• From the empirical model we found that credit rates have statistically significantpositive effect on the credit supply and statistically significant negative effect onthe credit demand, meanwhile, the response of bank loans` supply is much biggerthan the response of demand

• From the demand equation we found that permanent income has positiveinfluence and transitory income has negative influence on the changes of creditdemand. Both the effects are statistically significant; however the effect ofpermanent income is much stronger than the effect of transitory income

• From the supply equation three different statistically significant effects were foundfor different groups of banks for assets on the credit supply

• Another interesting result is that banks do not respond to the changes ofgovernment treasury bill`s rate, which can be a signal of weak monetary policytransmission mechanism

• Finally, we found that banks respond positively to the increase in income spreaduntil the optimal point after which the response changes and the increase ofincome spread decreases the credit supply

Summary and Conclusions

• Having estimated the credit supply and demand it waspossible to compare the historical developments of creditdemand and supply with the actual bank loans

• The comparison enabled us to understand when thefinancial intermediary in Armenia complied with thedemand and supply explained by the fundamentals

• This result has very important implications and may serveas crucial policy recommendations. We got strong empiricalresults and believe that they will have important policyimplications as during the recent years in Armenia manyexperts dispute about the level of financial intermediary

Outline

• The Research Question

• Literature Review

• Introduction to Armenian Banking System

• The Theoretical Model

• The Used Dataset

• Empirical Approach and the Results

• Summary and Conclusions

• Future

Future

• Today we are testing the model as aforecasting tool to be used by the Centralbank of Armenia during the macro financialpolicy analyses

• Based on the testing results minor changes inthe model specification may be possible