22

Rising health spending but who benefits Presented by Sarina Fisher Centre for International Economics www.TheCIE.com.au 28 July 2015

| Date post: | 12-Aug-2015 |

| Category: |

Business |

| Upload: | informa-australia |

| View: | 98 times |

| Download: | 0 times |

Rising health spending but who benefits

Presented by Sarina Fisher

Centre for International Economics

www.TheCIE.com.au

28 July 2015

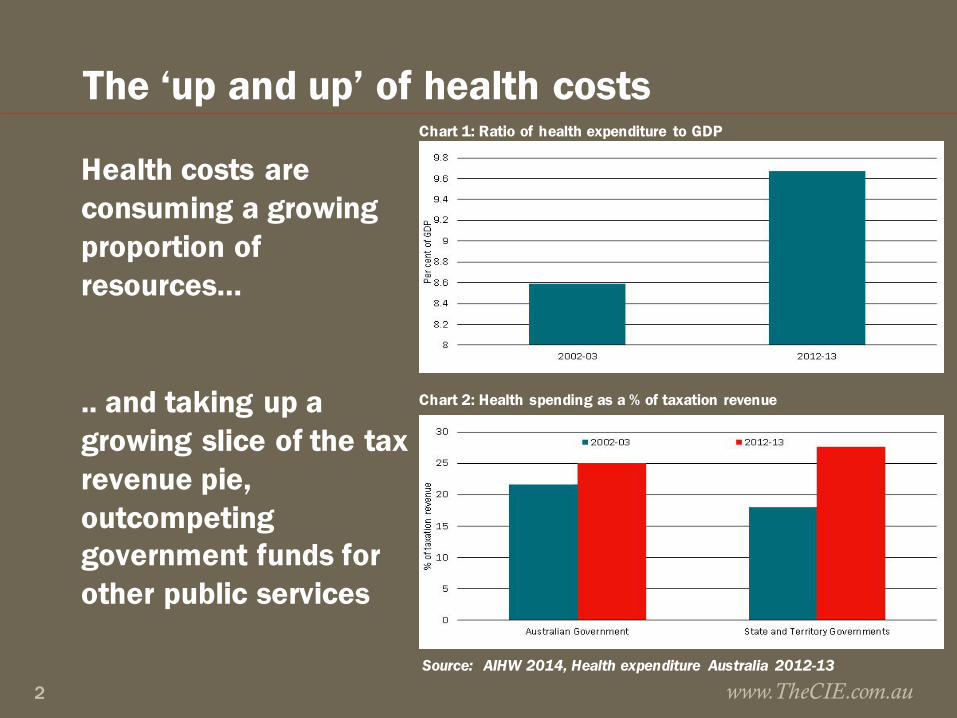

The ‘up and up’ of health costs

Health costs are consuming a growing proportion of resources…

.. and taking up a growing slice of the tax revenue pie, outcompeting government funds for other public services

www.TheCIE.com.au2

Chart 1: Ratio of health expenditure to GDP

Chart 2: Health spending as a % of taxation revenue

Source: AIHW 2014, Health expenditure Australia 2012-13

Dollar spend is rising and source of funds is changing, but little shift in spending profile

www.TheCIE.com.au3

0

20

40

60

80

100

120

140

160

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

$ billion

Capital expenditure Other recurrent Primary care Hospitals

5.3%

5.3%

20.3%

20.3%

36.3%

38.1%

35.9%

38.0%

Very little change in the distribution of total spending by area of expenditure

5.3%

5.3%

20.3%

20.3%

36.3%

38.1%

35.9%

38.0%

Very little change in the distribution of total spending by area of expenditure

$147.4bn in 2012-13

Health spending continued to rise, up

64%over the past decade

Source: AIHW health expenditure database

Chart 3: Total expenditure on health, constant prices

Chart 4: Health spending by source

www.TheCIE.com.au4

0

10

20

30

40

50

60

70

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

$ billion

Australian Government health expenditureState and Territory Government health expenditureNon-Government health expenditure

Average annual growth in spending per person2002-03 − 2007-08

Average annual growth in spending per person2008-09 − 2012-13

3.3 3.9 3.3 4.24.02.3

Consistent increase in non-Govt spending with growth in 2012-13 at a decade high

Source: AIHW health expenditure database

Everyone is spending more on hospitals■ Hospital spending accounts for 38% of health spending, but

takes the lions share of state and territory health budgets (70%), and is increasing as a share of non-government health spending (27%)

■ PHI’s hospital spending budget is increasingly making room for public hospital spending

■ Policy is driving up individual spending on hospitals. Following the 2008 increase in the MLS income threshold, growth in individual spending on hospitals has averaged 25%, compared to 6% for PHI and 4% for government

■ Individual spending on private hospitals has been strongest, averaging 31% p.a. over past 5 years, possibly reflecting the drift to exclusionary and excess/ co-payment products

www.TheCIE.com.au5

Chart 5: Spending on hospitals as a % of total funding by source

www.TheCIE.com.au6

Source: AIHW health expenditure database

37.0%

64.1%

25.2%

32.8%

69.5%

27.4%

AustralianGovernment

State andTerritoryGovernment

Non-Government

Outer rim = 2012-13 Inner rim = 2002-03

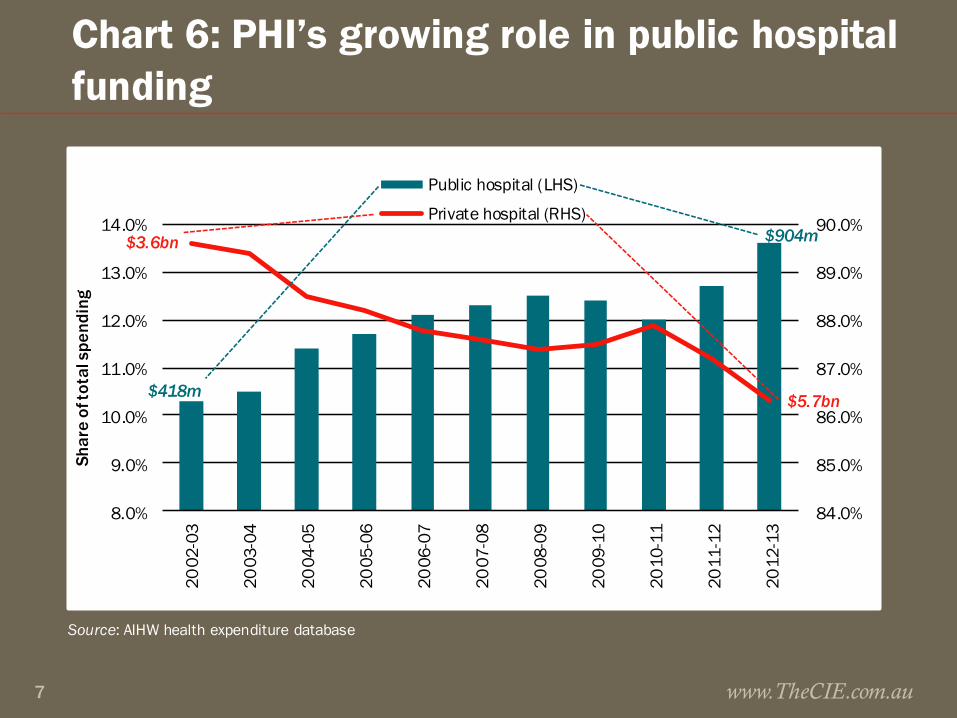

Chart 6: PHI’s growing role in public hospital funding

www.TheCIE.com.au7

Source: AIHW health expenditure database

84.0%

85.0%

86.0%

87.0%

88.0%

89.0%

90.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

Shar

e of

tota

l spe

ndin

g

Public hospital (LHS)

Private hospital (RHS)

$3.6bn

$5.7bn$418m

$904m

Key policy drivers impacting on individual health spend■ Medicare pays 75% of scheduled fee for private patients in

public/private hospital, and 85% of scheduled fee for a specialist, patients pay gap plus any above-schedule fee

■ 2010-11 Medicare levy introduced (1.5%). 1 July 2012 new income thresholds introduced with higher rates of the surcharge for high income earners

■ 1 July 2015, general patients pay $5 for each PBS prescription and $145.30 more to reach the safety net for concessional rate (lesser rises for concession card holders)

■ 1 July 2015, patients may pay (optional) $5 towards bulk billed standard GP consults and out-of-hospital pathology and imaging services. States and Territories allowed to introduce contributions for GP equivalent visits to EDwww.TheCIE.com.au8

Chart 7: Growth in private hospital funding, constant prices

www.TheCIE.com.au9

Source: AIHW health expenditure database

0

5

10

15

20

25

30

35

2002-03 –2007-08 2007-08 –2012-13

Ave

rage

ann

ual g

row

th in

hea

lth

spen

ding

per

per

son

(%)

Individuals PHI

$202m

$3.6bn$5.7bn

$1.5bn

ACTUALSPEND

PHI premium increases consistently above CPI because of benefits expenditure growth

www.TheCIE.com.au10

Source: Department of Health and ABS

0

1

2

3

4

5

6

7

8

2010 2011 2012 2013 2014 2015*

Annual % change

year to March 2015

Weighted average industry premium increase MBF Bupa CPI

Premium growth well above CPI

Source: Department of Health and ABS

Chart 9: Premium increases across the industry and for the largest PHIs

But as you would expect given growth in benefits expenditure

www.TheCIE.com.au11

Source: PHIAC

6 000

8 000

10 000

12 000

14 000

16 000

18 000

2009 2010 2011 2012 2013 2014

$

Chart 8: Hospital and General Treatment Benefits

Future cost of health care: … up some more

■ Currently >25% of Aust. Government spending is for health, age–related pensions and aged care

■ In GDP terms, Australian Government spending on health is forecast to rise the most in % of GDP terms, widening the spending gap between health and all other areas of Australian Government funding

www.TheCIE.com.au12

Health spending projections foretell ongoing pressure to share the funding burden

www.TheCIE.com.au13

Source: Commonwealth Treasury projections, Intergenerational Report 2015

0

1

2

3

4

5

6

2014-15 2024-25 2034-35 2044-45 2054-55

% of GDP

Health Aged careAge and service persions Other income supportEducation NDISPublic sector superannuation Defence

Health dominates spending growth

Chart 10: Projected Australian Government spending by category

Forecast spending confirms Govt emphasis on primary care, leaving increases in other spending to be met by non-Govt

■ No planned increase in real per person expenditure on the PHI rebate, which will be flat for next 15 years ($280 in 2014-15 to $283 in 2027-28

■ Medicare will growth the most from $855 to $1071 per person

■ Pharma spending to rise from $420 to $474 per person

■ Public hospital spending to rise from $647 to $680 per person

www.TheCIE.com.au14

Commonwealth prioritises primary care for growth spending

www.TheCIE.com.au15

Source: Treasury projections, International Report 2015.

0

200

400

600

800

1 000

1 200

Medicare services Pharmaceuticalspending

Funding for publichospitals

PHI rebate

2014-15 2027-28Strongest growth in

primary care and non-hospital interventions

Low and flat

Chart 11: Projected health spending per person, real terms

This signals wider purposeful shift away from hospital care to early intervention

■ Hospital and PHI funding increase only in line with population and CPI growth (CPI assumed to be < than premium ↑)

■ Medicare and pharmaceutical benefits increase in line with both CPI/population growth and non-demographic factors (in line with age based historical use patterns)

www.TheCIE.com.au16

Why are health costs rising like they are? .. mostly because of the things we do

■ Much talked about population ageing will fuel growth ■ Real health spending on 65+ to rise seven fold

■ Real health spending on 85+ to rise twelve fold

www.TheCIE.com.au17

■ But it is increasing demand for health services that really takes off

Chart 12: Australian Government spending on health: 2009-10 dollars

Source: Treasury projections, Intergenerational Report 2010

Most recent Treasury projections point to non-demographic factors driving health costs

■ Out to 2027-28 Treasury forecasts non-demographic factors will be the largest contributor (80%) to growth in real per person health spending

■ Ageing contributes just 10%■ Projected pharmaceutical benefits spending is four times

higher for 85+ years than the average person across all years

■ Projected public hospital spending is four times higher for 85+ years than the average person across all years

Source: Treasury projections from the 2015 Intergenerational Report www.TheCIE.com.au18

It is our needs, wants and options that are changing

■ Higher incomes bring increased preferences to consume more and/or better health services

■ Technology change increases demand and price (eg. Keyhole surgery is a better/more expensive way of treating same condition

■ Changes in disease rates (esp. chronic disease) increases demand for treatments

■ Wages growth >CPI leads to price growth in labour intensive industries, including hospitals and medical services

www.TheCIE.com.au19

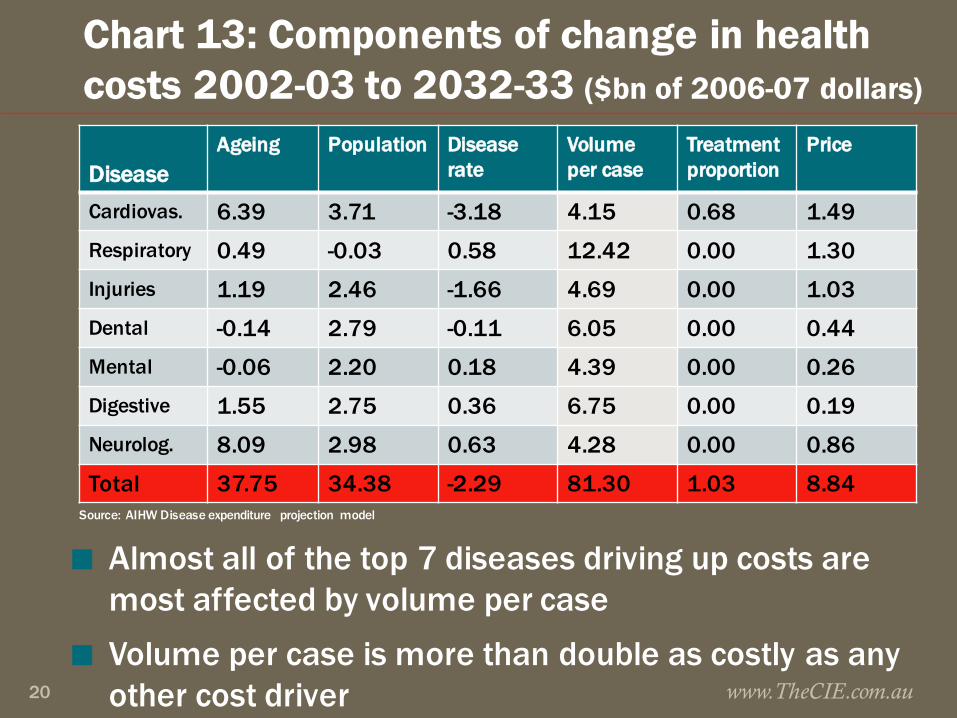

Chart 13: Components of change in health costs 2002-03 to 2032-33 ($bn of 2006-07 dollars)

DiseaseAgeing Population Disease

rateVolume per case

Treatment proportion

Price

Cardiovas. 6.39 3.71 -3.18 4.15 0.68 1.49Respiratory 0.49 -0.03 0.58 12.42 0.00 1.30Injuries 1.19 2.46 -1.66 4.69 0.00 1.03Dental -0.14 2.79 -0.11 6.05 0.00 0.44Mental -0.06 2.20 0.18 4.39 0.00 0.26Digestive 1.55 2.75 0.36 6.75 0.00 0.19Neurolog. 8.09 2.98 0.63 4.28 0.00 0.86

Total 37.75 34.38 -2.29 81.30 1.03 8.84

www.TheCIE.com.au20

■ Almost all of the top 7 diseases driving up costs are most affected by volume per case

■ Volume per case is more than double as costly as any other cost driver

Source: AIHW Disease expenditure projection model

Concluding thoughts..

■ Health spending pressure will make cost sharing inevitable, and price signals will increasingly be used to ration health services: look out for some rebalancing of the access vs quality compromise

■ Arguably unlikely to get additional Government sponsorship of PHI, policy momentum from sector likely to be to preserve the status quo

■ Can more be done to get more market signals into healthcare? Arguably yes, healthcare is very regulated but arguably mature enough to get equitable outcomes from greater market freedoms

www.TheCIE.com.au21