34

Earnings Call Presentation Q1, 2017 1 Saudi Arabian Mining Company (Ma’aden) Earnings Conference Call Q1 2017 May 7, 2017

Earnings Call Presentation Q1, 2017 1

Saudi Arabian Mining Company (Ma’aden) Earnings Conference Call Q1 2017

May 7, 2017

Earnings Call Presentation Q1, 2017 2

Walid Al-Hakim

Head Investor Relations

Earnings Call Presentation Q1, 2017 3

This presentation contains statements that are, or may be deemed to be, forward looking statements, including statements about the beliefs and expectations of Saudi Arabian Mining Company (the "Company"). These statements are based on the Company's current plans, estimates and projections, as well as its expectations of external conditions and events. Forward-looking statements involve inherent risks and uncertainties and speak only as of the date they are made. As a result of these risks, uncertainties and assumptions, a prospective investor should not place undue reliance on these forward-looking statements. A number of important factors could cause actual results or outcomes to differ materially from those expressed in any forward-looking statements. The Company is not obliged to, and does not intend to, update or revise any forward- looking statements made in this presentation whether as a result of new information, future events or otherwise. This communication has been prepared by and is the sole responsibility of the Company. It has not been reviewed, approved or endorsed by any financial advisor, lead manager, selling agent, receiving bank or underwriter retained by the Company. This communication is provided for information purposes only. In addition, because this communication is a summary only, it may not contain all material terms and this communication in and of itself should not form the basis for any investment decision. The information and opinions herein is believed to be reliable and has been obtained from sources believed to be reliable, but no representation or warranty, express or implied, is made with respect to the fairness, correctness, accuracy reasonableness or completeness of the information and opinions. There is no obligation to update, modify or amend this communication or to otherwise notify you if information, opinion, projection, forecast or estimate set forth herein, changes or subsequently becomes inaccurate. You are strongly advised to seek your own independent advice in relation to any investment, financial, legal, tax, accounting or regulatory issues discussed herein. Analyses and opinions contained herein may be based on assumptions that if altered can change the analyses or opinions expressed. Nothing contained herein shall constitute any representation or warranty as to future performance of any financial instrument, credit, currency, rate or other market or economic measure. Furthermore, past performance is not necessarily indicative of future results. The Company disclaims liability for any loss arising out of or in connection with your use of, or reliance on, this communication. These materials may not be published, distributed or transmitted and may not be reproduced in any manner whatsoever without the explicit consent of Ma’aden’s management. These materials do not constitute an offer to sell or the solicitation of an offer to buy the securities in any jurisdiction.

Forward looking statement

Earnings Call Presentation Q1, 2017 4

Khalid Al-Mudaifer

President & Chief Executive Officer

Earnings Call Presentation Q1, 2017 5

Solid performance in first quarter of 2017

Record

production

■ 71 K ounces of gold, up 61% vs Q1 2016

■ 369 K tonnes of alumina, up 5% vs Q1 2016

■ 228 K tonnes of primary aluminium, up 5% vs Q1 2016

■ 599 K tonnes of ammonia, up 97% vs Q1 2016

■ 721 K tonnes of ammonium phosphate fertilizer, up 9% vs Q1 2016

Outstanding cost

performance

Strong financial

performance

■ Sales SAR 2,717 mn, up 20% vs Q1 2016

■ EBITDA SAR 1,437 mn, up 52% vs Q1 2016

■ Net income SAR 341 mn, up 70%

■ Net cash from operation SAR 857 mn, up 137%

Growth projects

underway

■ Continued focus on efficiency, productivity and throughput

■ Reduced cash cost in all our products

■ Margins continue to increase with EBITDA margins higher

by ~17 basis points

■ Ammonia plant for Ma’aden Wa’ad Al Shamal (MWAS) entered commercial

operation on January 1, 2017

■ Remaining plants of MWAS project are on track for first production in Q2 2017

■ Feasibility of our new Mansourah / Massarah mines is being finalised

■ Feasibility study for the third phosphate project is progressing well

Strong operating performance, supportive market conditions, benefits of low cost operations

reflecting in healthier results

Earnings Call Presentation Q1, 2017 6

Margin improvement with price and volume increase

947 952 886

1,437

37% 41%

37%

53%

20%

25%

30%

35%

40%

45%

50%

55%

60%

0

200

400

600

800

1000

1200

1400

1600

Q2 2016 Q3 2016 Q4 2016 Q1 2017

EBITDA

EBITDA Margins

SA

R m

illio

n

Rebase t

o 1

00 a

s o

n 1

Mar

2016

Source: Bloomberg

Commodity price movement

EBITDA and margins

40.00

60.00

80.00

100.00

120.00

140.00

160.00

1-Mar-16 1-May-16 1-Jul-16 1-Sep-16 1-Nov-16 1-Jan-17 1-Mar-17

Aluminium Copper Gold DAP Ammonia Ma'aden share price

Earnings Call Presentation Q1, 2017 7

0

100

200

300

400

500

600

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 Jan-17

Avg. FOB, KSA DAP

Avg. FOB, ME Ammonia

Source: Ma’aden SBU analysis, CRU , FMB and FERTECON

■ In Q1 2017 DAP prices averaged ~US$355/tonne1 and ammonia price averaged ~US$ 285 / tonne2

■ Phosphate and ammonia prices recovered from lows of 2016, due to low exports from China & US, high demand in China,

Latin America, etc.

■ DAP demand from India is picking up but there are increasing exports from China on the back of firmer prices in Q1

■ Additional supplies expected in H1 2017 from MWAS and Morocco which may exert pressure on prices

■ Ammonia prices bounced back after a very weak Q4, on reduced supply from the Black Sea.

Firm phosphate market in Q1, but now showing signs of

weakness

DAP and Ammonia price movement (US$/t)

1 Tampa FOB Index, 2 Middle East FOB Index

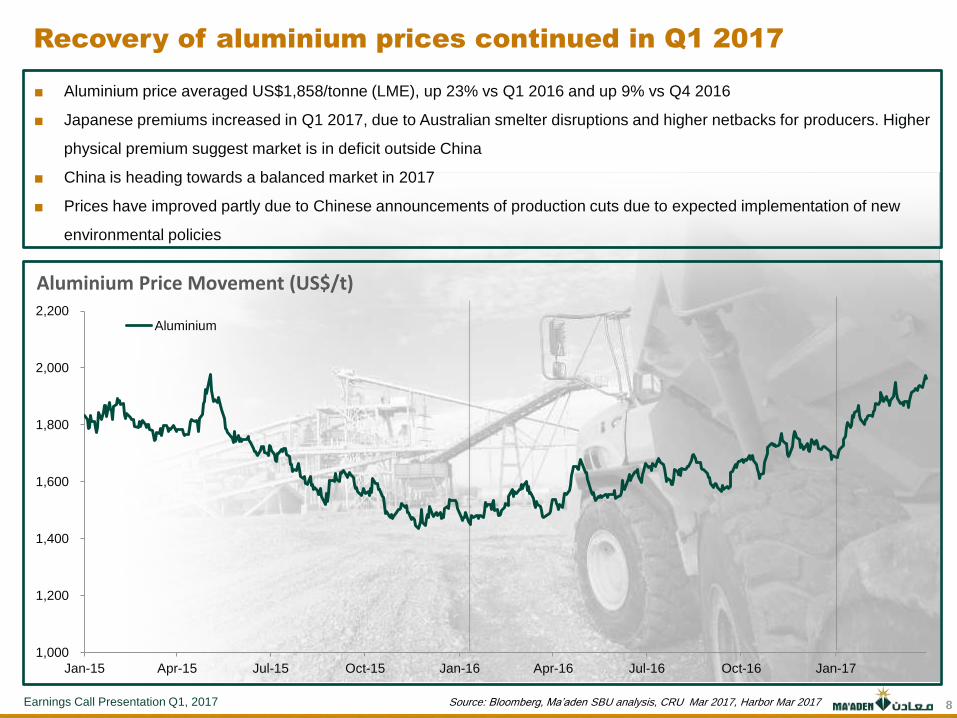

Earnings Call Presentation Q1, 2017 8

Recovery of aluminium prices continued in Q1 2017

■ Aluminium price averaged US$1,858/tonne (LME), up 23% vs Q1 2016 and up 9% vs Q4 2016

■ Japanese premiums increased in Q1 2017, due to Australian smelter disruptions and higher netbacks for producers. Higher

physical premium suggest market is in deficit outside China

■ China is heading towards a balanced market in 2017

■ Prices have improved partly due to Chinese announcements of production cuts due to expected implementation of new

environmental policies

Aluminium Price Movement (US$/t)

Source: Bloomberg, Ma’aden SBU analysis, CRU Mar 2017, Harbor Mar 2017

1,000

1,200

1,400

1,600

1,800

2,000

2,200

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 Jan-17

Aluminium

Earnings Call Presentation Q1, 2017 9

0.40

0.50

0.60

0.70

0.80

0.90

1.00

1.10

1.20

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16 Jul-16 Oct-16 Jan-17

Copper

Gold

Gold firm and copper is sustaining its recovery

Gold and copper price movement

Rebase t

o 1

as a

t 1 J

an 2

015

■ Gold and copper prices averaged US$1,221/ounce and US$ 5,855/tonne, up 3% and 25% respectively vs Q1 2016

■ World economic growth forecast, particularly Chinese structural reforms remain on track supporting the prices outlook

■ Production disruption at world’s three largest copper mines helped to support copper prices, despite financial market

weakness and industrial metals sell-off

■ Copper prices are expected to be driven by sustainability of Chinese demand into the second half of 2017 and US

infrastructure spending announcement

Source: Bloomberg, CRU Mar 2017, SBU secondary analysis

Earnings Call Presentation Q1, 2017

Additional reserves and resources added in phosphate and

copper business

0 500

KM

gold mine

copper mine

metallurgical bauxite mine

phosphate mine

low grade bauxite mine

Arabian

Shield

Ma’aden’s Total

Resources & Reserves1

461 Mt

288 Mt

210 Mt

16.5 Moz

4.3 Moz

P2O

5

Bau

xit

e

Go

ld

569 kt Co

pp

er

Minerals with potential for further

growth through exploration

HIGH

MEDIUM

bauxite, phosphate, gold,

copper, zinc

potash

1. Resources and reserves at December 2016

2. Resources for gold, phosphate and bauxite are stated inclusive of reserves

10

232 Mt

199 kt

Growth in Resources &

Reserves in 2016

Earnings Call Presentation Q1, 2017 11

Vision 2030 is of particular relevance to the mining

industry

Increased focus and expectation for the mining sector

Intensify exploration and development of mineral resources

Increase mining contribution to Saudi’s GDP to SAR97BN (USD26 BN) by 2020

creating 90,000 jobs

Simplify the licensing procedures for exploration and extraction

Increased ambition and support to develop Saudi economy

Raise competitiveness and productivity of national companies

Support large Saudi companies to expand globally into regional and global

leaders

Increase focus on sustainability and human capital

Strong focus on non-oil exports

Reduce pollution, promote optimal use of water, fight desertification

Grow local value chains

Attract and develop talent

Improve innovation and technology

11

Earnings Call Presentation Q1, 2017 12

And our strategy is aligned with the Vision to ensure we

build on the opportunity

▪ Focus on cost and productivity

▪ Operational, capital and

commercial excellence

▪ Profitability and returns in line with

international peers

▪ Best-in-class capabilities and

technology

▪ Leadership in sustainability, health,

safety and environment

▪ Grow in Saudi fertilizers,

aluminum, gold and base metals

▪ Grow in Saudi selected industrial

minerals

▪ Champion the development of the

Saudi mining sector

▪ Leverage world class selected

KSA deposits to be a world leader

▪ Grow globally in selected

commodities

Operational, capital, commercial

excellence and leading

sustainability

National mining

champion Global presence

12

Earnings Call Presentation Q1, 2017 13

Darren C. Davis

Chief Financial Officer

Earnings Call Presentation Q1, 2017 14

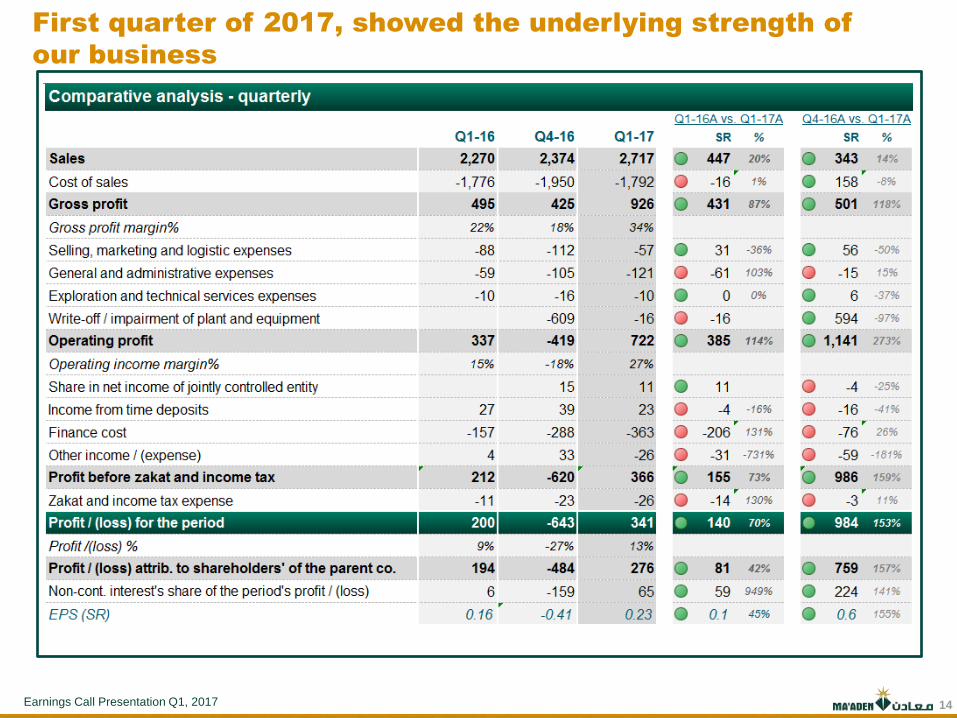

First quarter of 2017, showed the underlying strength of

our business

Earnings Call Presentation Q1, 2017

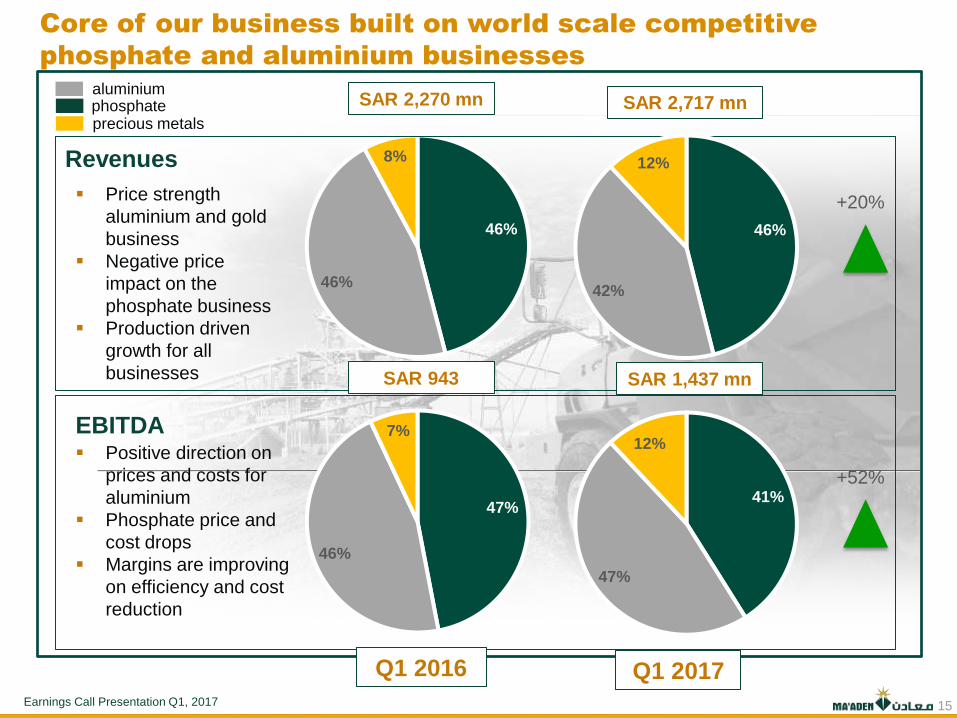

Core of our business built on world scale competitive

phosphate and aluminium businesses

46%

46%

8%

47%

46%

7%

Revenues

EBITDA

Price strength

aluminium and gold

business

Negative price

impact on the

phosphate business

Production driven

growth for all

businesses

Positive direction on

prices and costs for

aluminium

Phosphate price and

cost drops

Margins are improving

on efficiency and cost

reduction

aluminium phosphate precious metals

SAR 943

15

SAR 2,270 mn

Q1 2016

+20%

+52%

46%

42%

12%

SAR 1,437 mn

SAR 2,717 mn

Q1 2017

41%

47%

12%

Earnings Call Presentation Q1, 2017 16

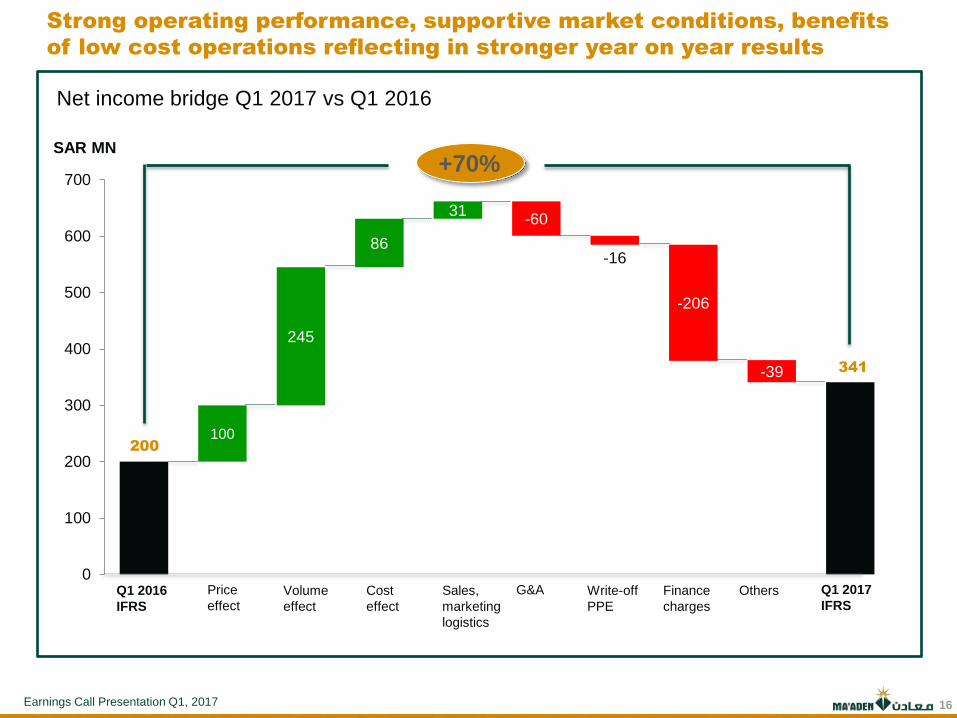

Strong operating performance, supportive market conditions, benefits

of low cost operations reflecting in stronger year on year results

Net income bridge Q1 2017 vs Q1 2016

100

245

86

31 -60

-16

-206

-39

0

100

200

300

400

500

600

700

200

341

Q1 2016

IFRS

Price

effect Volume

effect

Cost

effect

Sales,

marketing

logistics

G&A Write-off

PPE

Finance

charges

Others Q1 2017

IFRS

SAR MN +70%

Earnings Call Presentation Q1, 2017 17

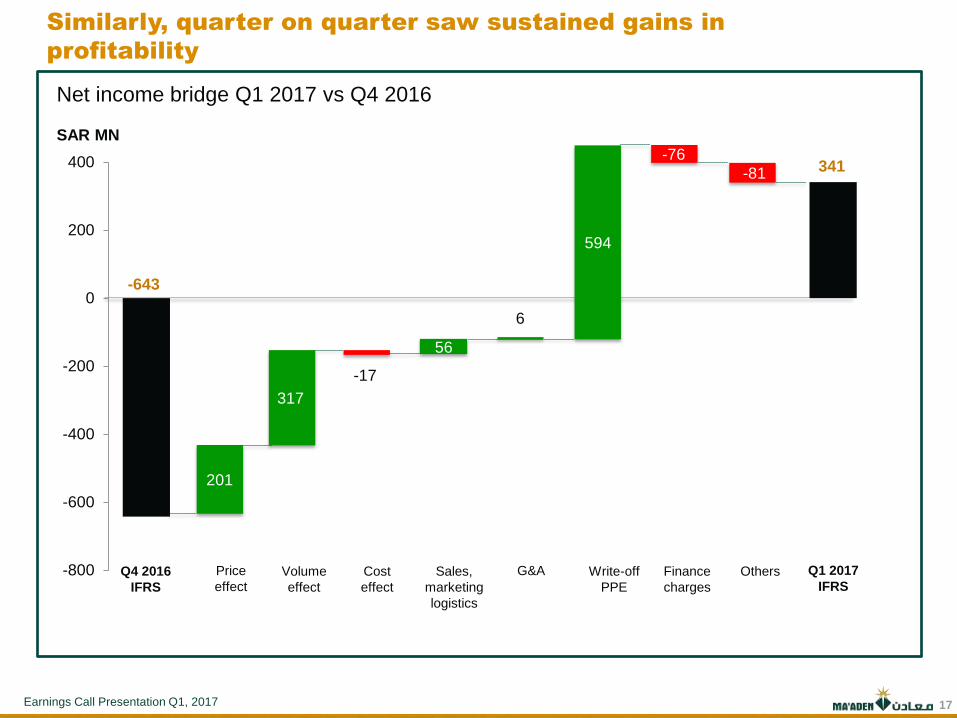

Similarly, quarter on quarter saw sustained gains in

profitability

Net income bridge Q1 2017 vs Q4 2016

Q4 2016

IFRS

Price

effect Volume

effect

Cost

effect

Sales,

marketing

logistics

G&A Write-off

PPE

Finance

charges

Others Q1 2017

IFRS

SAR MN

-17

56

6 594

-76

-81

594

201

317

-643

341

-800

-600

-400

-200

0

200

400

Earnings Call Presentation Q1, 2017 18

Operational performance

Earnings Call Presentation Q1, 2017 19

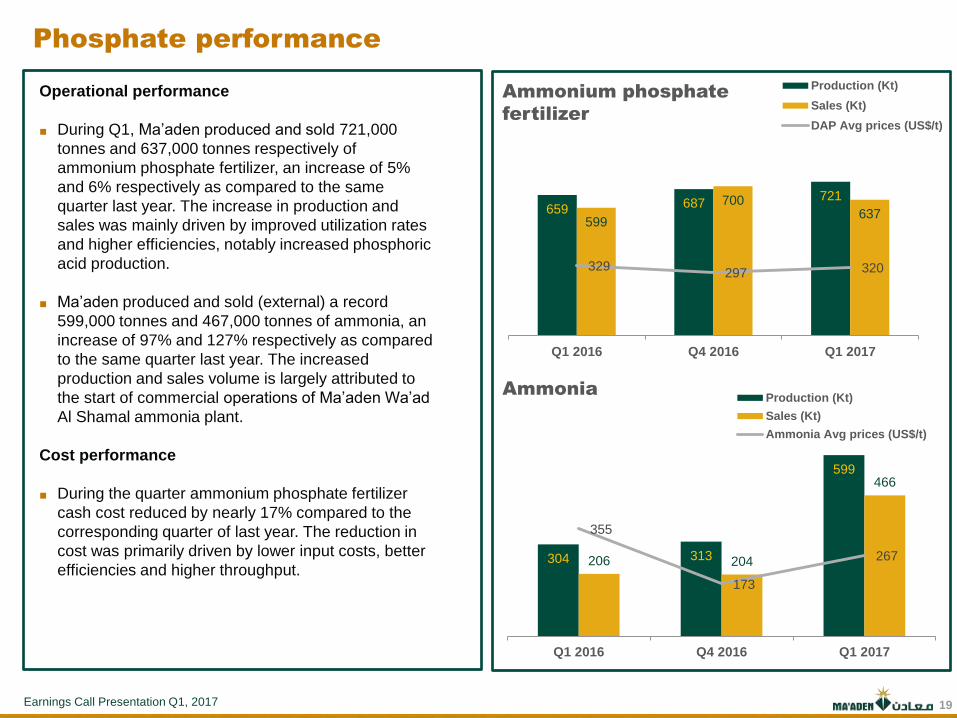

Phosphate performance

Operational performance

■ During Q1, Ma’aden produced and sold 721,000

tonnes and 637,000 tonnes respectively of

ammonium phosphate fertilizer, an increase of 5%

and 6% respectively as compared to the same

quarter last year. The increase in production and

sales was mainly driven by improved utilization rates

and higher efficiencies, notably increased phosphoric

acid production.

■ Ma’aden produced and sold (external) a record

599,000 tonnes and 467,000 tonnes of ammonia, an

increase of 97% and 127% respectively as compared

to the same quarter last year. The increased

production and sales volume is largely attributed to

the start of commercial operations of Ma’aden Wa’ad

Al Shamal ammonia plant.

Cost performance

■ During the quarter ammonium phosphate fertilizer

cash cost reduced by nearly 17% compared to the

corresponding quarter of last year. The reduction in

cost was primarily driven by lower input costs, better

efficiencies and higher throughput.

Ammonium phosphate

fertilizer

Ammonia

659 687 721

599

700 637

329 297 320

Q1 2016 Q4 2016 Q1 2017

Production (Kt)

Sales (Kt)

DAP Avg prices (US$/t)

304 313

599

206 204

466

355

173

267

Q1 2016 Q4 2016 Q1 2017

Production (Kt)

Sales (Kt)

Ammonia Avg prices (US$/t)

Earnings Call Presentation Q1, 2017 20

Aluminium performance

Operational performance

■ During the first quarter of 2017, Ma’aden produced

228,000 tonnes of primary aluminium, an increase of 5%,

compared to the same period of last year. The increase

was mainly due to increased production efficiency and

increased production from the recycling unit.

■ Ma’aden’s bauxite mine and alumina refinery operated

well. During Q1, Ma’aden produced 369,000 tonnes of

alumina, an increase of 5% compared to Q1 2016.

Ma’aden made its first external sales of 30,000 tonnes of

alumina in the last quarter.

Cost performance

■ During the quarter, our aluminium cash cost reduced

significantly, due to increased volumes, decreased fixed

costs through strong cost control measures, reduction in

some of the raw material consumptions, and lower input

costs, notably the lower price of alumina.

■ However, we see some headwinds with the prices of key

inputs such as caustic soda and coke prices increasing

Projects

■ The rolling mill operation continues to ramp up production

and is making gradual progress in penetrating the market

for can sheets in the Middle East region and beyond.

Primary aluminium

Corporate aluminium sales (Kt)

217 219

228

215 216

228

1,503 1,663

1,858

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

205

210

215

220

225

230

Q1 2016 Q4 2016 Q1 2017

Production (Kt)

Sales (Kt)

Avg LME prices (US$/t)

128

135

113

100

105

110

115

120

125

130

135

140

Q1 2016 Q4 2016 Q1 2017

Earnings Call Presentation Q1, 2017 21

44

64 71

40

64 70

1,192 1,182

1,200

800

850

900

950

1000

1050

1100

1150

1200

1250

0

10

20

30

40

50

60

70

80

Q1 2016 Q4 2016 Q1 2017

Production (Koz)

Sales (Koz)

Gold Avg prices (US$/oz)

Gold and Copper performance

Gold volumes

Copper volumes (Kt)

Operational performance

■ During the quarter, Ma’aden production of gold

increased by 61% to 71,000 ounces compared to the

same quarter last year. This was mainly due to

increased volumes from Ad Duwayhi mine, Ma’aden’s

largest gold mine, which was commercialized on April

1, 2016.

■ During the quarter, we produced 7,000 tonnes and sold

7,500 tonnes of copper concentrate. The Jabal Sayid

mine is progressing well in terms of reaching its full

production capability

Cost performance

■ Continued focus on cost has helped Ma’aden to

reduce its gold cash cost by 22% compared to the

same quarter last year. This is mainly attributed to

increased volumes and better efficiencies.

■ Jabal Sayid C1 cash cost performance continued to

improve through efficiency and higher throughput.

1 Ma’aden attributable production & sales @ 50%

4

8

7

5 5

7.5

0

1

2

3

4

5

6

7

8

9

Q1 2016 Q4 2016 Q1 2017

Production

Sales

Earnings Call Presentation Q1, 2017 22

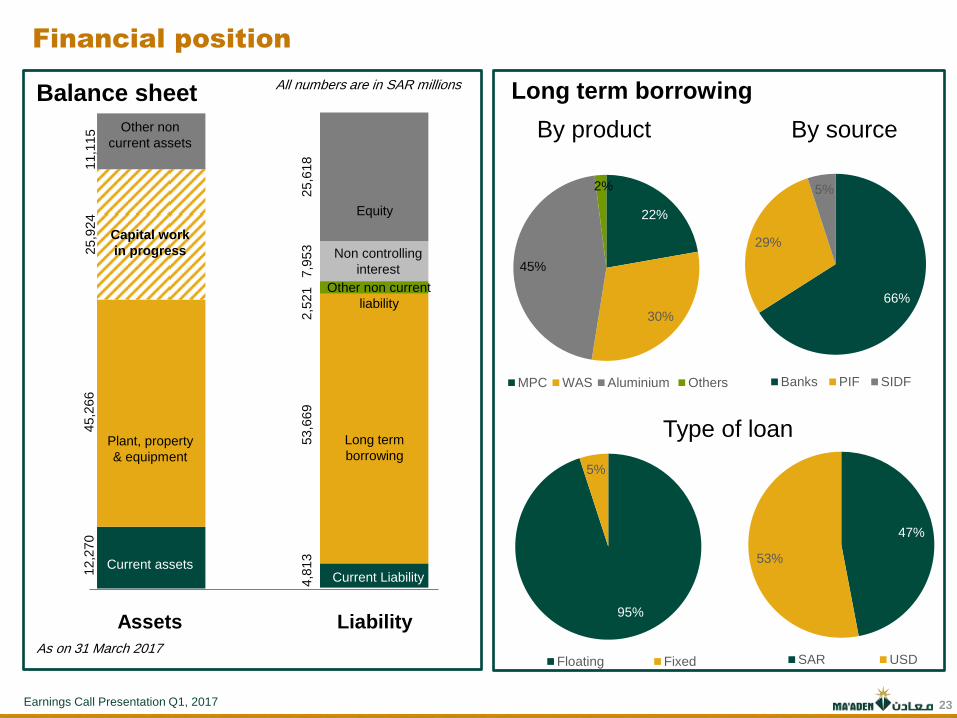

Financial position

Earnings Call Presentation Q1, 2017 23

All numbers are in SAR millions

4,8

13

53,6

69

2,5

21

7,9

53

25,6

18

Current Liability

22%

30%

45%

2%

MPC WAS Aluminium Others

66%

29%

5%

Banks PIF SIDF

Long term borrowing

By product By source

12,2

70

45,2

66

25,9

24

11,1

15

Capital work

in progress

Plant, property

& equipment

Current assets

Other non

current assets

Equity

Long term

borrowing

Other non current

liability

Assets Liability

As on 31 March 2017

Balance sheet

95%

5%

Floating Fixed

47%

53%

SAR USD

Type of loan

Financial position

Non controlling

interest

Earnings Call Presentation Q1, 2017 24

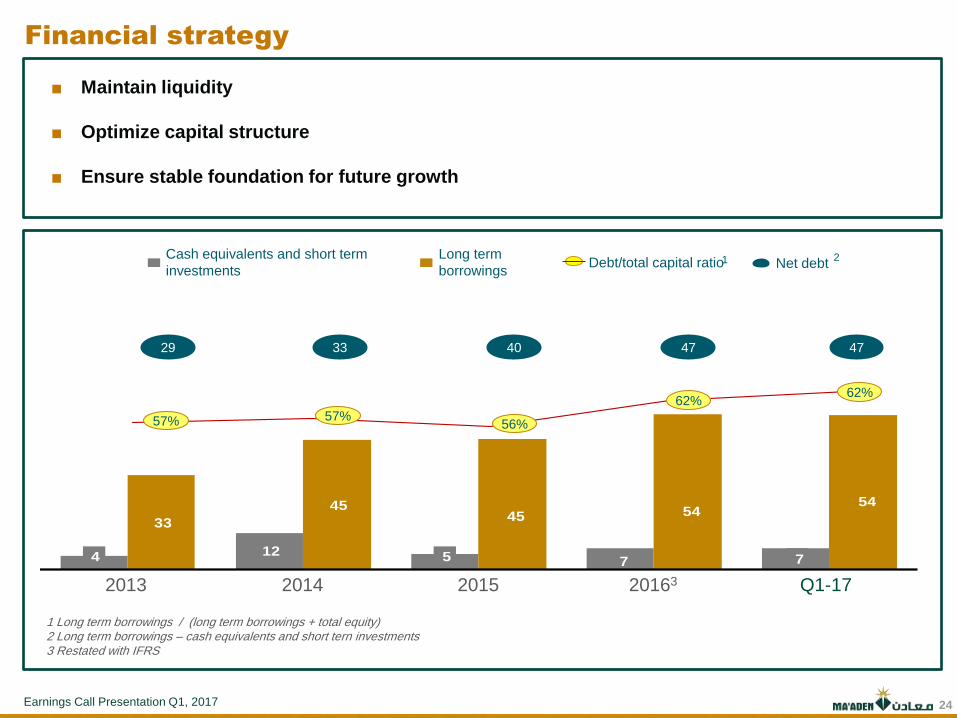

1 Long term borrowings / (long term borrowings + total equity) 2 Long term borrowings – cash equivalents and short tern investments 3 Restated with IFRS

Financial strategy

■ Maintain liquidity

■ Optimize capital structure

■ Ensure stable foundation for future growth

4 12 5 7 7

33

45 45 54

54

Cash equivalents and short term

investments

Long term

borrowings Debt/total capital ratio Net debt 1 2

57% 57% 56%

62% 62%

2013 2014 2015

29 33 40 47 47

Q1-17 20163

Earnings Call Presentation Q1, 2017 25

Summary

Leading position in fundamentally attractive commodities

Better overall price environment in Q1 2017 but some concerns for the balance of the

year, particularly in DAP

Underpinned outstanding cost performance

Strong cost performance allows us to see the full benefits of improved commodity prices

Record production in all our business first quarter 2017

Continued focus on volumes: ramping up new capacities and increasing throughput at existing

operations

Growth projects underway

Wa’ad Al Shamal on track and we have a good pipeline of new projects

Aligned to Vision 2030

Our strategy is set to contribute to, and benefit from, the Vision 2030 initiatives

Earnings Call Presentation Q1, 2017 26

Appendix

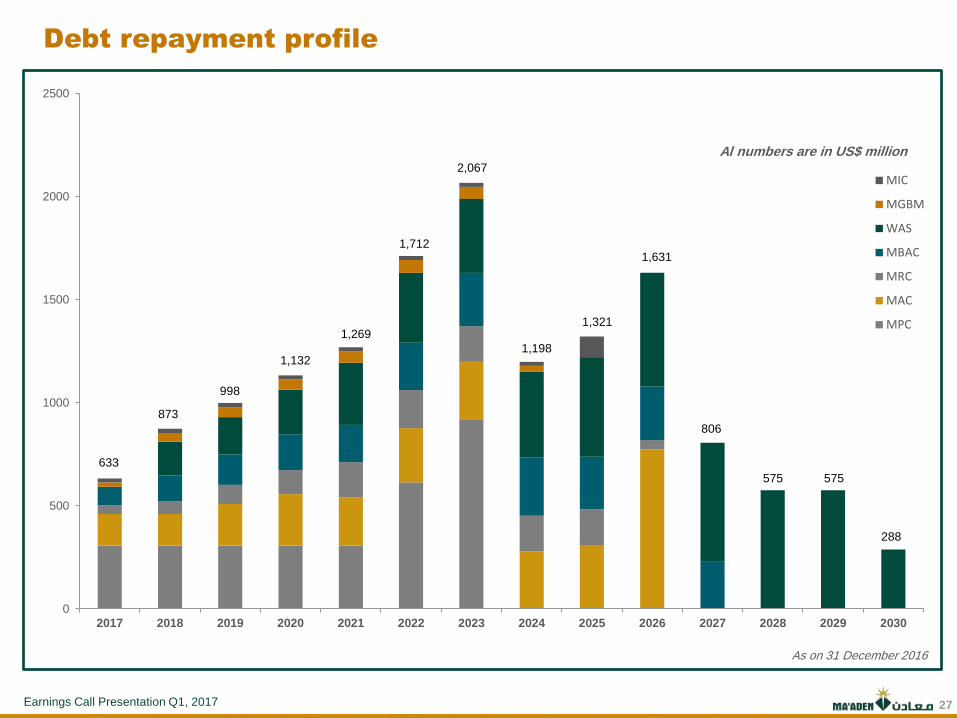

Earnings Call Presentation Q1, 2017 27

0

500

1000

1500

2000

2500

2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

MIC

MGBM

WAS

MBAC

MRC

MAC

MPC

633

873

998

1,132

1,269

1,712

2,067

1,198

1,321

1,631

806

575 575

288

Debt repayment profile

Al numbers are in US$ million

As on 31 December 2016

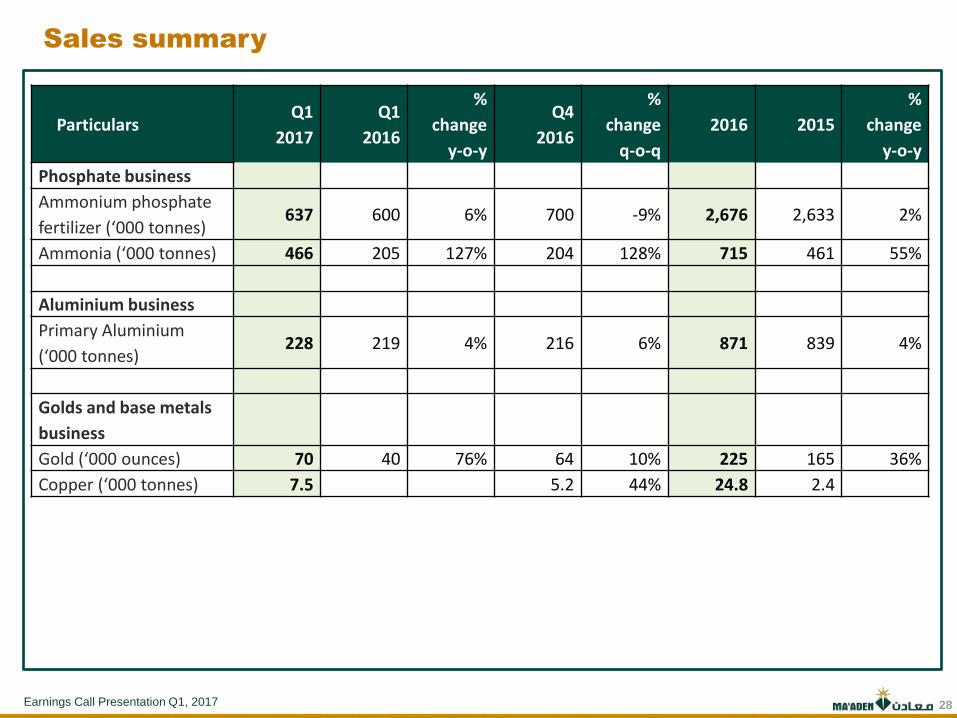

Earnings Call Presentation Q1, 2017 28

Particulars Q1

2017

Q1

2016

%

change

y-o-y

Q4

2016

%

change

q-o-q

2016 2015

%

change

y-o-y

Phosphate business

Ammonium phosphate

fertilizer (‘000 tonnes) 637 600 6% 700 -9% 2,676 2,633 2%

Ammonia (‘000 tonnes) 466 205 127% 204 128% 715 461 55%

Aluminium business

Primary Aluminium

(‘000 tonnes) 228 219 4% 216 6% 871 839 4%

Golds and base metals

business

Gold (‘000 ounces) 70 40 76% 64 10% 225 165 36%

Copper (‘000 tonnes) 7.5 5.2 44% 24.8 2.4

Sales summary

Earnings Call Presentation Q1, 2017 29

Saudi Arabian Mining Company (Ma’aden) IFRS Transition Impact on the Consolidated Financial Statements

May 7, 2017

Earnings Call Presentation Q1, 2017 30

IFRS transition from SOCPA to IFRS

IFRS transition

impact on

Ma’aden business

■ As per the Capital Market Authority (CMA) circular 7/5/7258/16 dated 18/11/1437H, referring to the

transition to the International Financial Reporting Standers (IFRS), with effect from January 1, 2017

Ma’aden has transitioned its financial reporting framework to comply with the International Financial

Reporting Standards (IFRS) as endorsed by SOCPA for financial reporting in the kingdom of Saudi

Arabia.

■ All of Ma’aden’s subsidiary companies have also transitioned to reporting under IFRS so as to enable us

to prepare our consolidated interim financial statements in accordance with IFRS

■ We have made all the adjustments required by IFRS, “First time adoption of international Financial

Reporting Standards “ to the standing balance sheet as of December 31, 2015 prepared in accordance

with SOCPA accounting standards and audited in accordance with International standards on Auditing

(“ISA”) endorsed by SOCPA.

■ The following slides summarize the key changes to our 2016 SOCPA financial statements as follows:

- the changes to retained earnings as at January 1, 2016 under IFRS against the retained earnings as

at December 31, 2015 as previously reported under SOCPA

- the changes in net income for the quarter ended December 31, 2016 under IFRS versus the net

income previously reported under SOCPA

- the changes in net income for the quarter ended March 31, 2016 under IFRS versus the net income

previously reported under SOCPA

■ For full details please refer to our consolidated interim financial statements for the quarter ended March

31, 2017

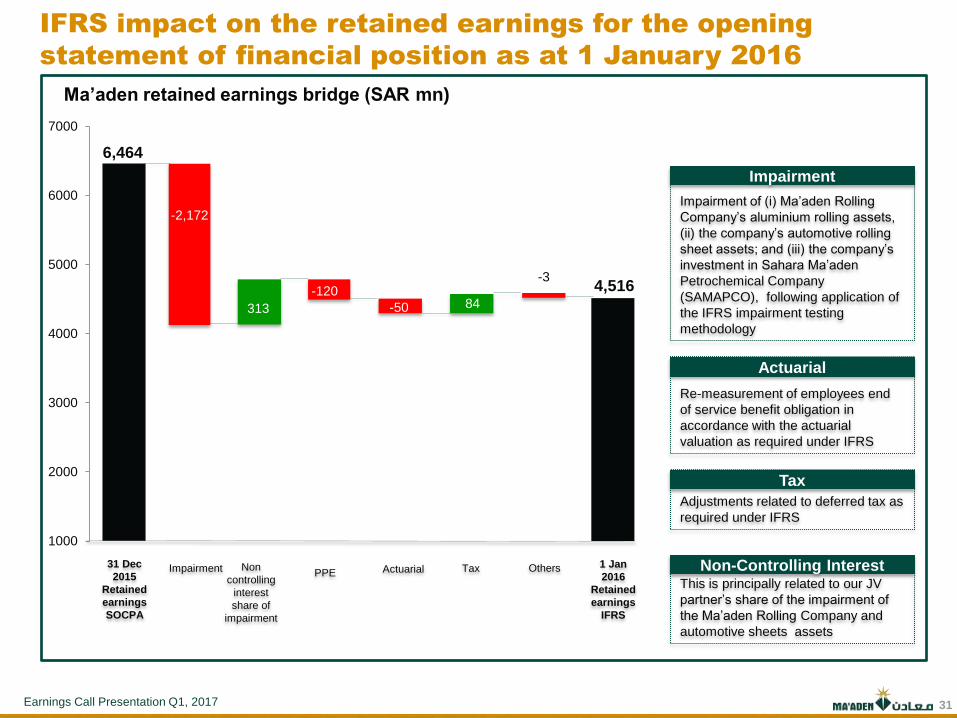

Earnings Call Presentation Q1, 2017 31

Ma’aden retained earnings bridge (SAR mn)

IFRS impact on the retained earnings for the opening

statement of financial position as at 1 January 2016

6,464

4,516

1000

2000

3000

4000

5000

6000

7000

-2,172

84

313

-3

31 Dec

2015

Retained

earnings

SOCPA

Impairment PPE Actuarial Tax Non

controlling

interest

share of

impairment

Others 1 Jan

2016

Retained

earnings

IFRS

Impairment of (i) Ma’aden Rolling

Company’s aluminium rolling assets,

(ii) the company’s automotive rolling

sheet assets; and (iii) the company’s

investment in Sahara Ma’aden

Petrochemical Company

(SAMAPCO), following application of

the IFRS impairment testing

methodology

Impairment

Re-measurement of employees end

of service benefit obligation in

accordance with the actuarial

valuation as required under IFRS

Actuarial

Adjustments related to deferred tax as

required under IFRS

Tax

This is principally related to our JV

partner’s share of the impairment of

the Ma’aden Rolling Company and

automotive sheets assets

Non-Controlling Interest

-120

-50 84

Earnings Call Presentation Q1, 2017 32

Re-measurements due to conversion to IFRS reporting

standard resulted to an increase in net loss by SR 620 mn

Net income/loss bridge of Q4 2016 SOCPA vs Q4 2016 IFRS

Due to the introduction of

componentization of

plant, property and

equipment, increased

the depreciation charge

Cost of sales

Re-measurement of

employees end of

service termination

benefit obligation in

accordance with the

actuarial valuation as

required under IFRS

Actuarial

Adjustments arising from

provisional pricing in gold

and aluminium business

Sales

Investment in SAMAPCO

was impaired on the date

of transition to IFRS,

which resulted in the

reversal of reported

equity share of loss for

Q4 2016 under IFRS

Share in net loss of JV

Adjustments related to

the deferred tax as

required under IFRS

applicable to non-

controlling interest

Others

Impairment of Ma’aden

Rolling Company’s

assets, following

adoption of IFRS

impairment methodology

Impairment

-23 -643

-700

-600

-500

-400

-300

-200

-100

0

Q4

2016

SOCPA

Net

loss

Sales Cost

of

sales

Actuarial Finance

cost Others Q4 2016

IFRS Net

loss

SAR MN

Impairment Share

in net

loss of

JV

-76

-5 -566

-23 17 29

3

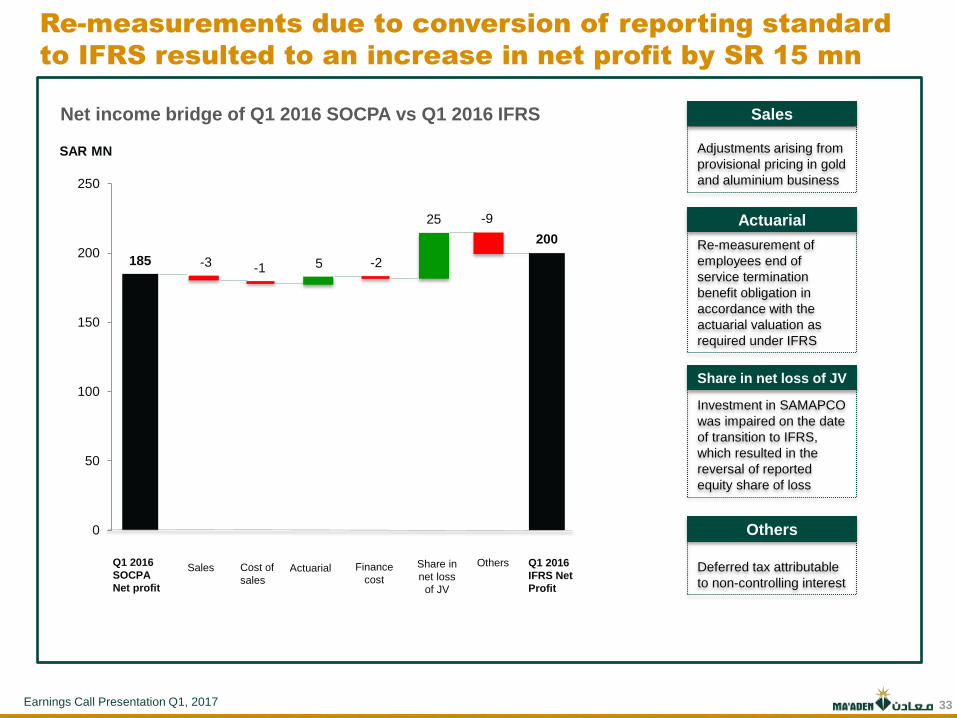

Earnings Call Presentation Q1, 2017 33

Adjustments arising from

provisional pricing in gold

and aluminium business

Sales

Investment in SAMAPCO

was impaired on the date

of transition to IFRS,

which resulted in the

reversal of reported

equity share of loss

Share in net loss of JV

Re-measurements due to conversion of reporting standard

to IFRS resulted to an increase in net profit by SR 15 mn

185

200

0

50

100

150

200

250

Q1 2016

SOCPA

Net profit

Sales Cost of

sales Actuarial

Finance

cost

Q1 2016

IFRS Net

Profit

SAR MN

Share in

net loss

of JV

Others

Net income bridge of Q1 2016 SOCPA vs Q1 2016 IFRS

Re-measurement of

employees end of

service termination

benefit obligation in

accordance with the

actuarial valuation as

required under IFRS

Actuarial

Deferred tax attributable

to non-controlling interest

Others

-3 -1 5 -2

25 -9

Earnings Call Presentation Q1, 2017 34

Thank You!

Copyright © 2016. Ma’aden . All rights reserved.