Page 1

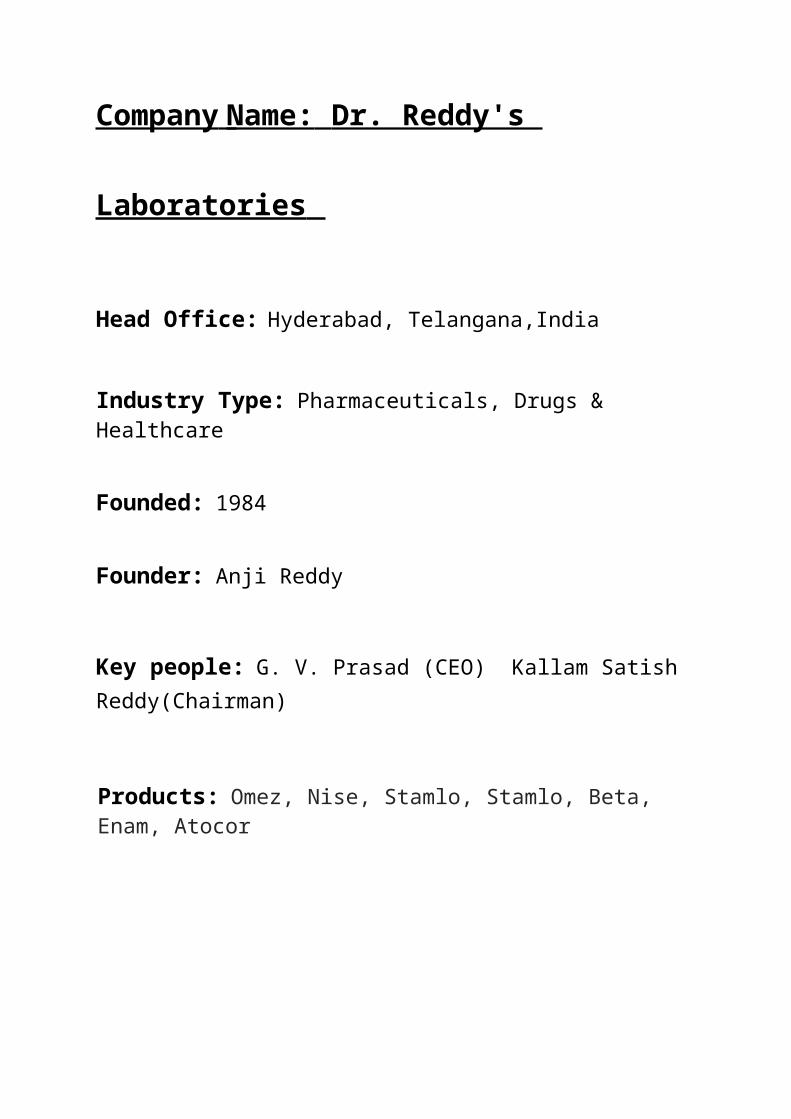

Company Name: Dr. Reddy's Laboratories

Head Office: Hyderabad, Telangana,India

Industry Type: Pharmaceuticals, Drugs & Healthcare

Founded: 1984

Founder: Anji Reddy

Key people: G. V. Prasad (CEO) Kallam Satish Reddy(Chairman)

Products: Omez, Nise, Stamlo, Stamlo, Beta, Enam, Atocor

Page 2

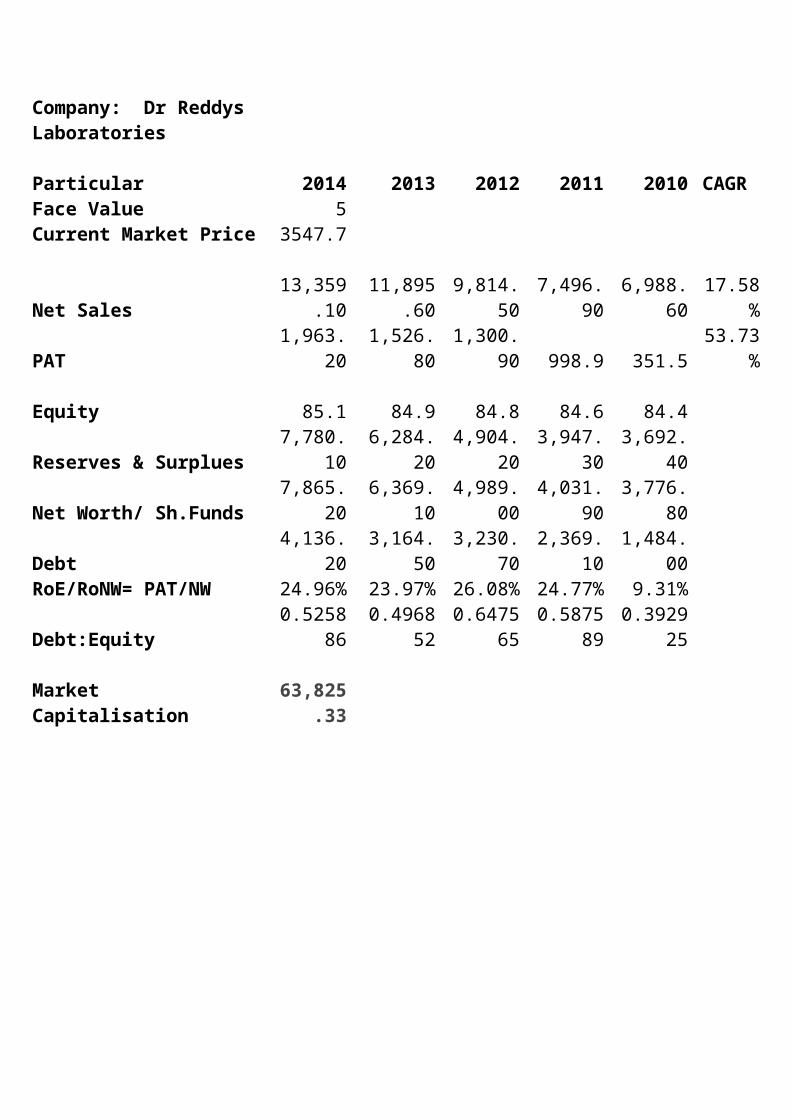

Company: Dr Reddys Laboratories Particular 2014 2013 2012 2011 2010 CAGRFace Value 5 Current Market Price 3547.7

Net Sales 13,359.1011,895.6

0 9,814.50 7,496.90 6,988.60 17.58%PAT 1,963.20 1,526.80 1,300.90 998.9 351.5 53.73% Equity 85.1 84.9 84.8 84.6 84.4 Reserves & Surplues 7,780.10 6,284.20 4,904.20 3,947.30 3,692.40 Net Worth/ Sh.Funds 7,865.20 6,369.10 4,989.00 4,031.90 3,776.80 Debt 4,136.20 3,164.50 3,230.70 2,369.10 1,484.00 RoE/RoNW= PAT/NW 24.96% 23.97% 26.08% 24.77% 9.31%

Debt:Equity 0.525886 0.496852 0.647565 0.5875890.39292

5 Market Capitalisation 63,825.33

Page 3

Fundamental Analysis

Page 4

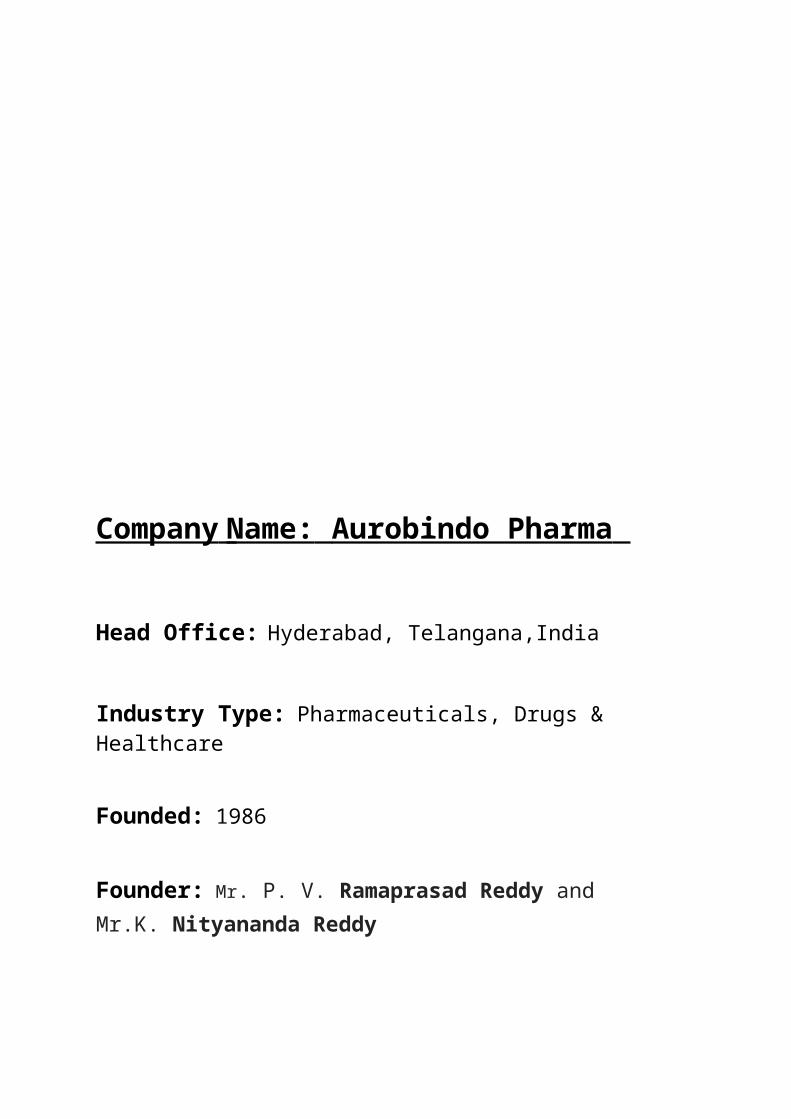

Company Name: Aurobindo Pharma

Head Office: Hyderabad, Telangana,India

Industry Type: Pharmaceuticals, Drugs & Healthcare

Founded: 1986

Founder: Mr. P. V. Ramaprasad Reddy and Mr.K. Nityananda Reddy

Key people: Dr. M. Sivakumaran, Mr. Madanmohan Reddy, Mr. Govind, Mr. Arvind Vasudeva,

Products: Formulation, Active Pharmaceutical Ingredient, Organic Intermediates

Page 5

Fundamental AnalysisCompany:Aurobindo Pharma

Particular 2014 2013 2012 2011 2010 CAGR

Face Value 1

Current Market Price 1415.35

Net Sales 8,099.79 5,855.32 4,627.40 4,384.80 3,604.27 22.44%

PAT 1,169.07 291.4 -124.14 563.06 563.08 20.04%

Equity 29.15 29.12 29.11 29.11 27.86

Reserves & Surplues 3,721.00 2,576.64 2,310.54 2,415.72 1,801.22

Net Worth/ Sh.Funds 3,750.15 2,605.76 2,339.65 2,444.83 1,829.08

Debt 3,633.92 3,384.38 2,572.84 2,414.35 2,154.56

RoE/RoNW= PAT/NW 31.17% 11.18% -5.31% 23.03% 30.78%

Debt:Equity 0.969007 1.298807 1.099669 0.987533 1.177947

Market Capitalisation 42,413.35

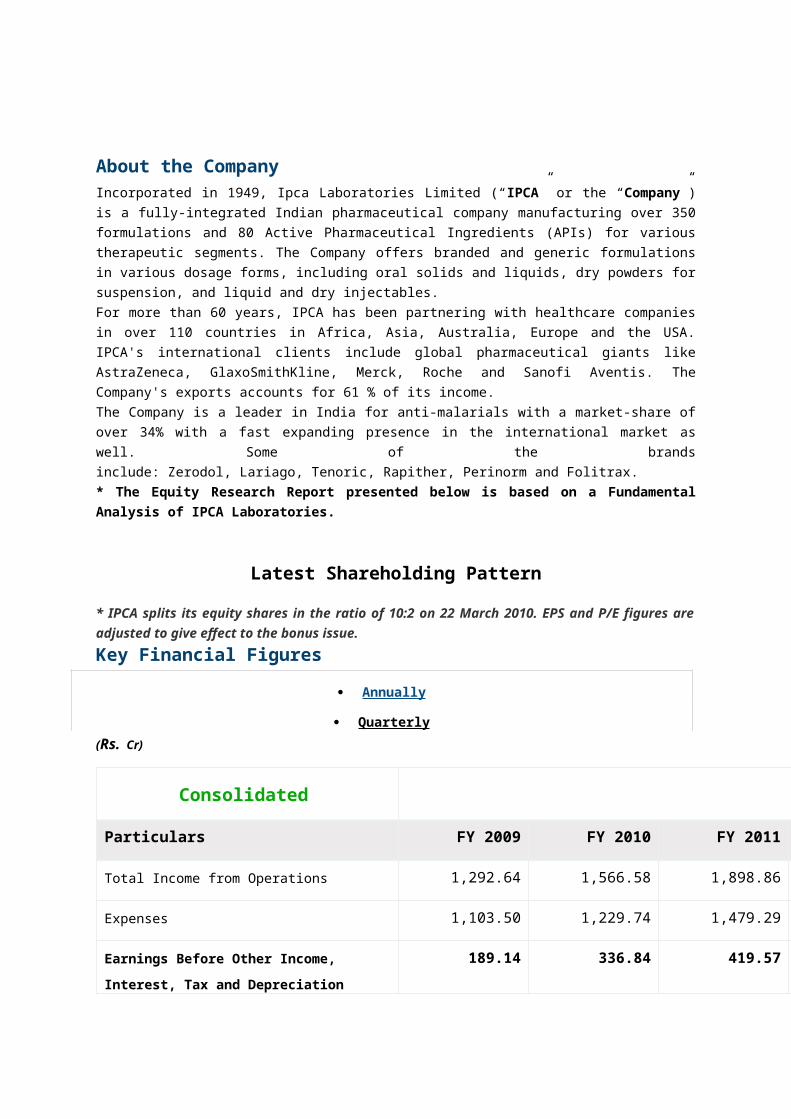

About the Company

Aurobindo Pharma Limited (“Aurobindo Pharma” or the “Company”) was set up in the year 1986 and is a leading manufacturer of Active Pharmaceutical Ingredients (APIs) and finished dosage formulations. The Company has presence in key therapeutic segments such as neurosciences, cardiovascular, anti-retrovirals, anti-diabetics, gastroenterology and cephalosporins.

The Company has robust product portfolio spread over major product areas encompassing anti-retroviral, antibiotics, gastroenterologicals, anti-diabetics and anti-allergics. Its range of formulations include sterile injectables, orally disintegrating tablets, combination generics, immediate release generics, liquids/dry syrups and lyophilized sterile injectables.

Aurobindo Pharma features among the top 10 companies in India in terms of consolidated revenues. APL’s formulations and APIs are exported to over 125 countries across the globe with more than 70 % of its revenues derived from international operations.

Page 6

* The Equity Research Report presented below is based on a Fundamental Analysis of Aurobindo Pharma.

Latest Shareholding Pattern

Key Financial Figures

Annually

Quarterly

(Rs. Cr)

Consolidated

Particulars FY 2009 FY 2010 FY 2011

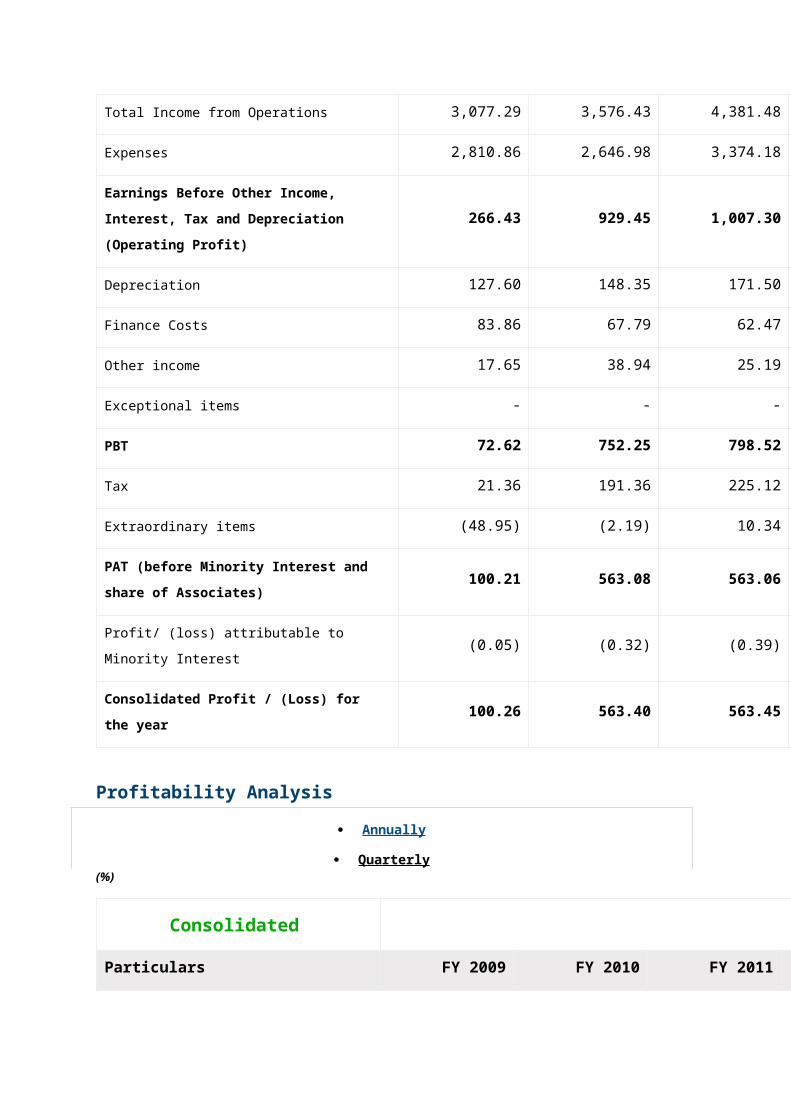

Total Income from Operations 3,077.29 3,576.43 4,381.48

Expenses 2,810.86 2,646.98 3,374.18

Earnings Before Other Income, Interest, Tax and

Depreciation (Operating Profit)266.43 929.45 1,007.30

Depreciation 127.60 148.35 171.50

Finance Costs 83.86 67.79 62.47

Other income 17.65 38.94 25.19

Exceptional items - - -

PBT 72.62 752.25 798.52

Tax 21.36 191.36 225.12

Page 7

Extraordinary items (48.95) (2.19) 10.34

PAT (before Minority Interest and share of

Associates)100.21 563.08 563.06

Profit/ (loss) attributable to Minority Interest (0.05) (0.32) (0.39)

Consolidated Profit / (Loss) for the year 100.26 563.40 563.45

Profitability Analysis

Annually

Quarterly (%)

Consolidated

Particulars FY 2009 FY 2010 FY 2011

Operating Profit Margin Ratio 8.66 25.99 22.99

Net Profit Margin Ratio 3.26 15.75 12.86

Operating profit margin is a measurement of the proportion of a company’s revenue that is left over

after paying for production costs such as raw materials, salaries and administrative costs. Net profit

margin is arrived at by deducting non operating expenses such as depreciation, finance costs and

taxes out of operating profit and shows what is left for the shareholders as a percentage of net sales.

Together these ratios help in understanding the cost and profit structure of the firm and analysing

business inefficiencies. Profitability Ratios

Key Balance Sheet Figures(Rs. Cr)

Sources of Funds / Liabilities

Particulars FY 2009 FY 2010 FY 2011

Page 8

Share Capital 26.88 27.86 29.11

Reserves & Surplus 1,214.38 1,801.22 2,415.72

Net worth (shareholders funds) 1,241.26 1,829.08 2,444.83

Minority Interest 3.15 4.33 9.12

Long term borrowings 2,332.97 2,154.56 523.35

Current liabilities 570.05 707.99 2,768.49

Other long term liabilities and provisions - - 3.09

Deferred Tax Liabilities 79.04 95.35 123.40

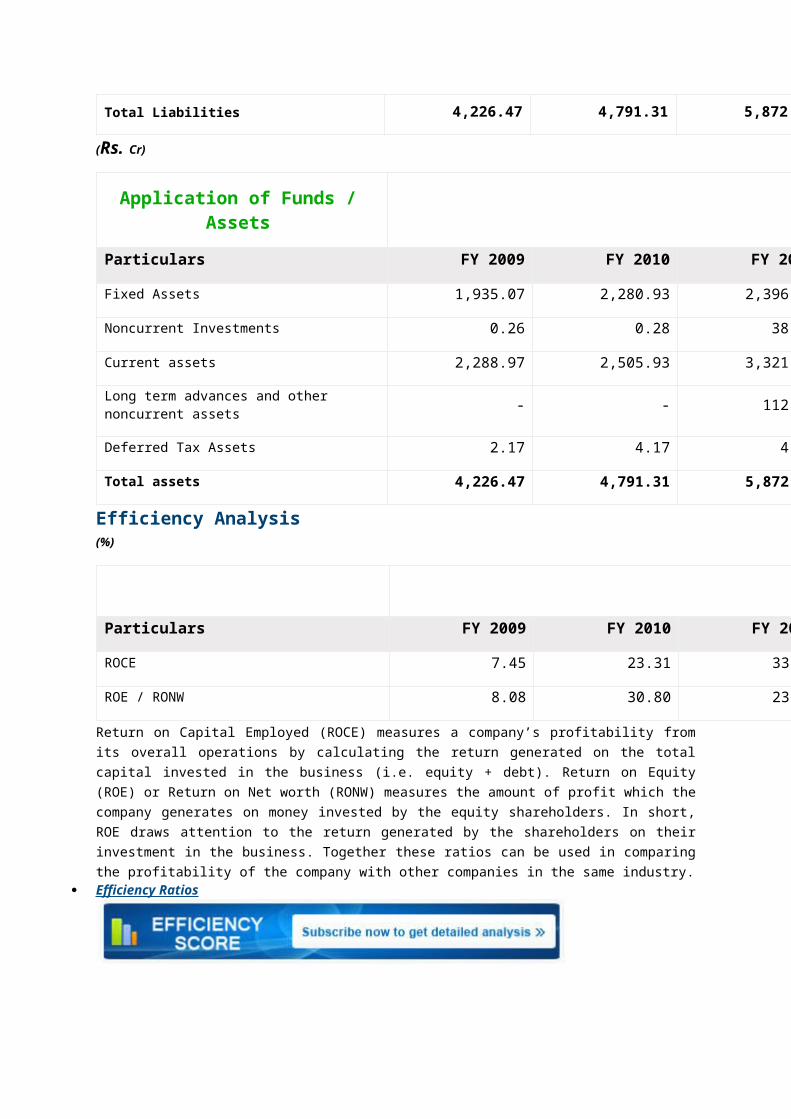

Total Liabilities 4,226.47 4,791.31 5,872.28

(Rs. Cr)

Application of Funds / Assets

Particulars FY 2009 FY 2010 FY 2011

Fixed Assets 1,935.07 2,280.93 2,396.02

Noncurrent Investments 0.26 0.28 38.49

Current assets 2,288.97 2,505.93 3,321.18

Long term advances and other noncurrent assets - - 112.24

Deferred Tax Assets 2.17 4.17 4.35

Total assets 4,226.47 4,791.31 5,872.28

Efficiency Analysis(%)

Particulars FY 2009 FY 2010 FY 2011

ROCE 7.45 23.31 33.94

ROE / RONW 8.08 30.80 23.05

Return on Capital Employed (ROCE) measures a company’s profitability from its overall operations by

calculating the return generated on the total capital invested in the business (i.e. equity + debt).

Page 9

Return on Equity (ROE) or Return on Net worth (RONW) measures the amount of profit which the

company generates on money invested by the equity shareholders. In short, ROE draws attention to

the return generated by the shareholders on their investment in the business. Together these ratios

can be used in comparing the profitability of the company with other companies in the same industry. Efficiency Ratios

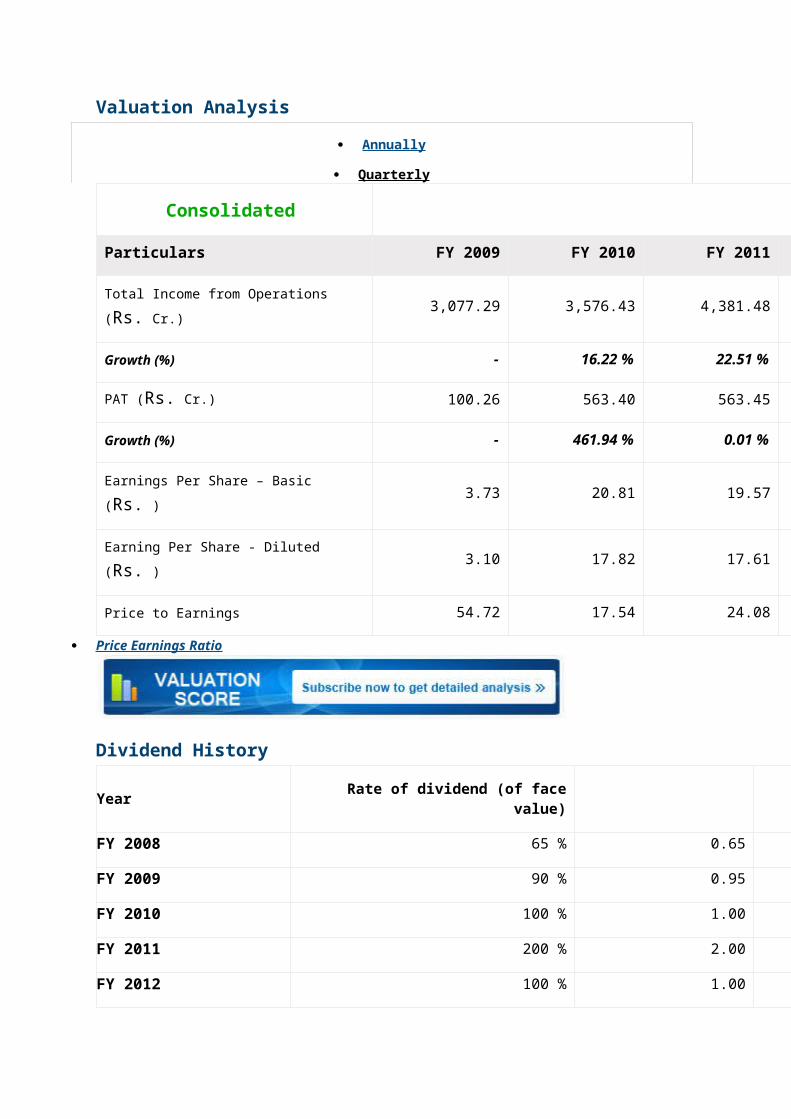

Valuation Analysis

Annually

Quarterly

Consolidated

Particulars FY 2009 FY 2010 FY 2011

Total Income from Operations (Rs. Cr.) 3,077.29 3,576.43 4,381.48

Growth (%) - 16.22 % 22.51 %

PAT (Rs. Cr.) 100.26 563.40 563.45

Growth (%) - 461.94 % 0.01 %

Earnings Per Share – Basic (Rs. ) 3.73 20.81 19.57

Earning Per Share - Diluted (Rs. ) 3.10 17.82 17.61

Price to Earnings 54.72 17.54 24.08

Price Earnings Ratio

Dividend History

Year Rate of dividend (of face value) Rs.

FY 2008 65 % 0.65

FY 2009 90 % 0.95

FY 2010 100 % 1.00

FY 2011 200 % 2.00

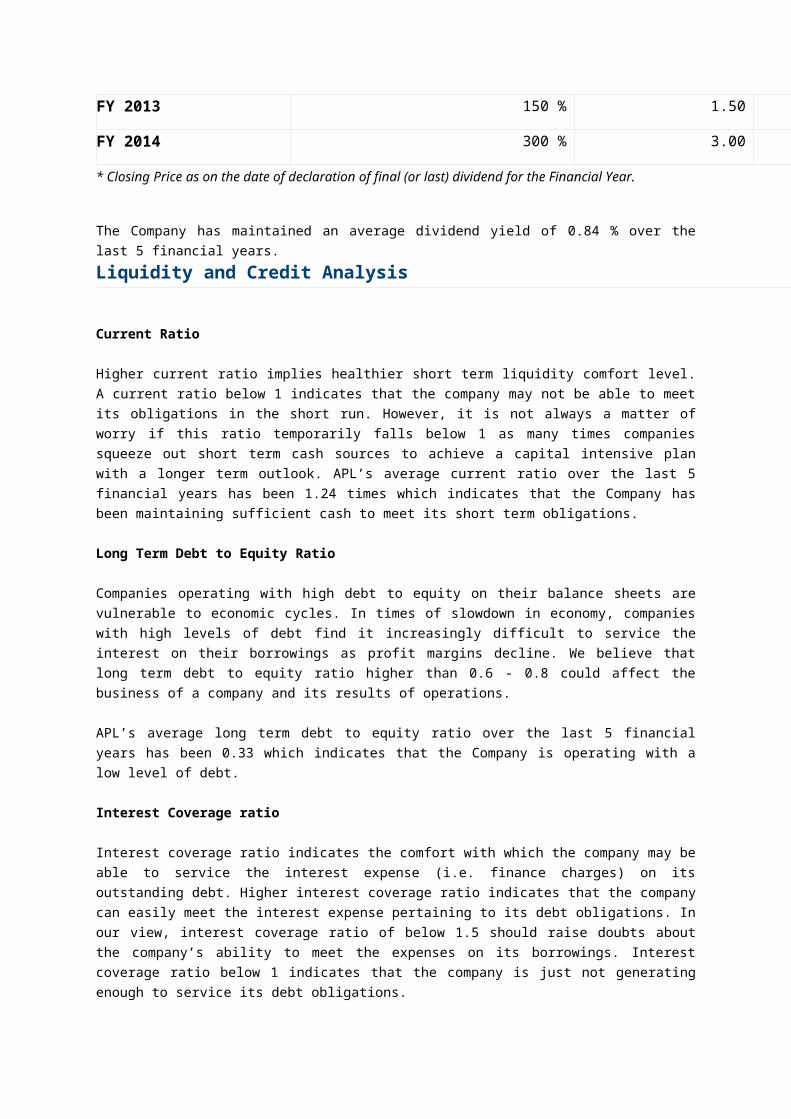

Page 10

FY 2012 100 % 1.00

FY 2013 150 % 1.50

FY 2014 300 % 3.00

* Closing Price as on the date of declaration of final (or last) dividend for the Financial Year.

The Company has maintained an average dividend yield of 0.84 % over the last 5 financial years.

Liquidity and Credit Analysis

Current Ratio

Higher current ratio implies healthier short term liquidity comfort level. A current ratio below 1

indicates that the company may not be able to meet its obligations in the short run. However, it is not

always a matter of worry if this ratio temporarily falls below 1 as many times companies squeeze out

short term cash sources to achieve a capital intensive plan with a longer term outlook. APL’s average

current ratio over the last 5 financial years has been 1.24 times which indicates that the Company has

been maintaining sufficient cash to meet its short term obligations.

Long Term Debt to Equity Ratio

Companies operating with high debt to equity on their balance sheets are vulnerable to economic

cycles. In times of slowdown in economy, companies with high levels of debt find it increasingly

difficult to service the interest on their borrowings as profit margins decline. We believe that long term

debt to equity ratio higher than 0.6 - 0.8 could affect the business of a company and its results of

operations.

APL’s average long term debt to equity ratio over the last 5 financial years has been 0.33 which

indicates that the Company is operating with a low level of debt.

Interest Coverage ratio

Interest coverage ratio indicates the comfort with which the company may be able to service the

interest expense (i.e. finance charges) on its outstanding debt. Higher interest coverage ratio

indicates that the company can easily meet the interest expense pertaining to its debt obligations. In

our view, interest coverage ratio of below 1.5 should raise doubts about the company’s ability to meet

the expenses on its borrowings. Interest coverage ratio below 1 indicates that the company is just not

generating enough to service its debt obligations.

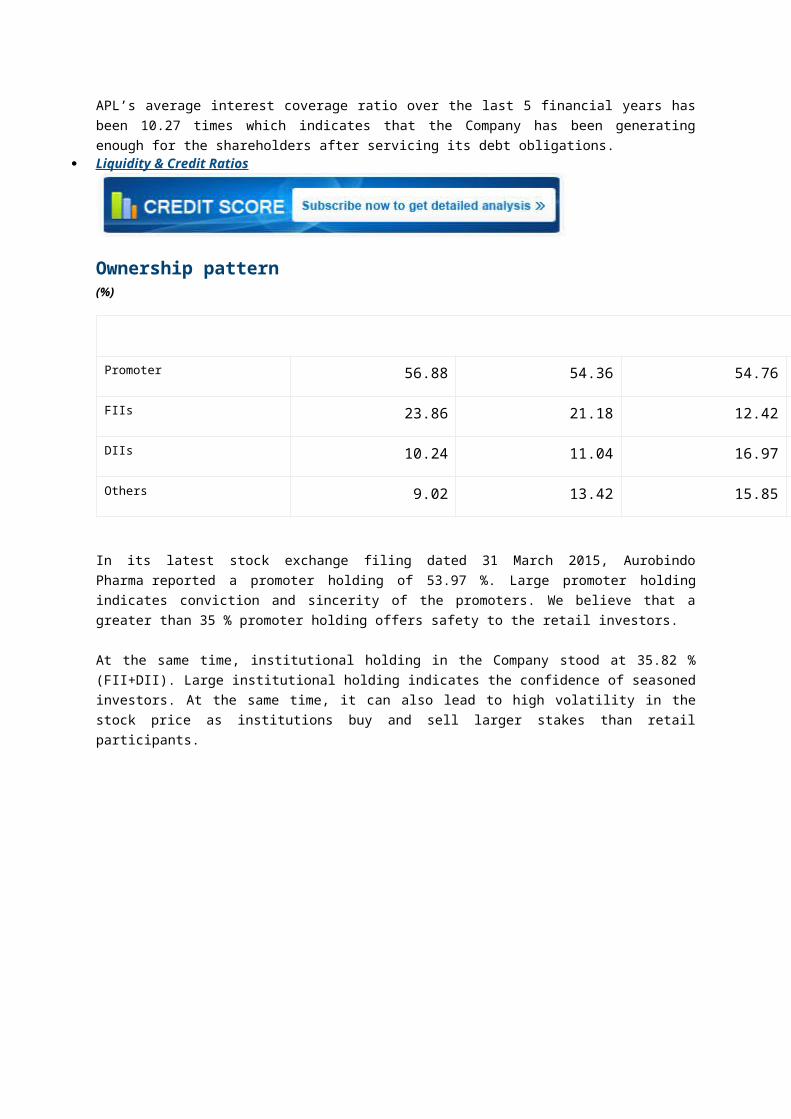

APL’s average interest coverage ratio over the last 5 financial years has been 10.27 times which

indicates that the Company has been generating enough for the shareholders after servicing its debt

obligations. Liquidity & Credit Ratios

Page 11

Ownership pattern(%)

Shareholding March 2010 March 2011 March 2012

Promoter 56.88 54.36 54.76

FIIs 23.86 21.18 12.42

DIIs 10.24 11.04 16.97

Others 9.02 13.42 15.85

In its latest stock exchange filing dated 31 March 2015, Aurobindo Pharma reported a promoter

holding of 53.97 %. Large promoter holding indicates conviction and sincerity of the promoters. We

believe that a greater than 35 % promoter holding offers safety to the retail investors.

At the same time, institutional holding in the Company stood at 35.82 % (FII+DII). Large institutional

holding indicates the confidence of seasoned investors. At the same time, it can also lead to high

volatility in the stock price as institutions buy and sell larger stakes than retail participants.

Page 12

Company Name: Ipca Laboratories

Head Office: Mumbai, India

Industry Type: Pharmaceuticals

Founded: 19 October 1949

Founder: K.B. MehlaDr. N.S. Tibrawala

Key people: Prem Chand Godha, MD, Mr. AK Jain, JMD

Products:Pharmaceuticals, drugs, Atenolol(antihypertensive) Chloroquine Phosphate (anti-malarial), Furosemide (diuretic), Hydroxychloroquine Sulphate (NSAID)

Page 13

Fundamental AnalysisCompany: Ipca Laboratories Particular 2014 2013 2012 2011 2010 CAGRFace Value 2 Current Market Price 698.65

Net Sales 3,281.77 2,813.12 2,370.09 1,975.341,621.9

319.27

PAT 478.2 324.6 276.2 262.31 203.5423.81

Equity 25.24 25.24 25.23 25.14 25.04 Reserves & Surplues 1,934.42 1,528.54 1,228.78 1,026.45 839.84 Net Worth/ Sh.Funds 1,959.66 1,553.78 1,254.01 1,051.59 864.88 Debt 437.94 523.35 531.54 530.32 454.01 RoE/RoNW= PAT/NW 24.40% 20.89% 22.03% 24.94% 23.53%

Debt:Equity0.22347

80.33682

40.42387

20.50430

3 0.52494 Market Capitalisation 8,664.20

About the CompanyIncorporated in 1949, Ipca Laboratories Limited (“IPCA” or the “Company”) is a fully-integrated Indian

pharmaceutical company manufacturing over 350 formulations and 80 Active Pharmaceutical

Ingredients (APIs) for various therapeutic segments. The Company offers branded and generic

formulations in various dosage forms, including oral solids and liquids, dry powders for suspension,

and liquid and dry injectables.

Page 14

For more than 60 years, IPCA has been partnering with healthcare companies in over 110 countries

in Africa, Asia, Australia, Europe and the USA. IPCA's international clients include global

pharmaceutical giants like AstraZeneca, GlaxoSmithKline, Merck, Roche and Sanofi Aventis. The

Company's exports accounts for 61 % of its income.

The Company is a leader in India for anti-malarials with a market-share of over 34% with a fast

expanding presence in the international market as well. Some of the brands

include: Zerodol, Lariago, Tenoric, Rapither, Perinorm and Folitrax.

* The Equity Research Report presented below is based on a Fundamental Analysis of IPCA

Laboratories.

Latest Shareholding Pattern

* IPCA splits its equity shares in the ratio of 10:2 on 22 March 2010. EPS and P/E figures are

adjusted to give effect to the bonus issue.

Key Financial Figures

Annually

Quarterly

(Rs. Cr)

Consolidated

Particulars FY 2009 FY 2010 FY 2011

Total Income from Operations 1,292.64 1,566.58 1,898.86

Expenses 1,103.50 1,229.74 1,479.29

Earnings Before Other Income, Interest, Tax and

Depreciation (Operating Profit)189.14 336.84 419.57

Depreciation 39.66 46.74 55.79

Finance Costs 31.80 26.38 31.40

Other income 0.64 2.54 8.31

Exceptional items - - -

PBT 118.32 266.26 340.69

Tax 23.25 62.72 78.38

Page 15

Extraordinary items - - -

PAT (before Minority Interest and share of

Associates)95.07 203.54 262.31

Profit/ (loss) attributable to Minority Interest (0.38) (0.20) (0.08)

Share of profit / (loss) of Associates (5.35) (1.62) (0.43)

Consolidated Profit / (Loss) for the year 100.80 205.36 262.82

Profitability Analysis

Annually

Quarterly (%)

Consolidated

Particulars FY 2009 FY 2010 FY 2011

Operating Profit Margin Ratio 14.63 21.50 22.10

Net Profit Margin Ratio 7.80 13.11 13.84

Operating profit margin is a measurement of the proportion of a company’s revenue that is left over

after paying for production costs such as raw materials, salaries and administrative costs. Net profit

margin is arrived at by deducting non operating expenses such as depreciation, finance costs and

taxes out of operating profit and shows what is left for the shareholders as a percentage of net sales.

Together these ratios help in understanding the cost and profit structure of the firm and analysing

business inefficiencies. Profitability Ratios

Key Balance Sheet Figures(Rs. Cr)

Sources of Funds / Liabilities

Page 16

Particulars FY 2009 FY 2010 FY 2011

Share Capital 24.99 25.04 25.14

Share application money pending allotment 0.03 0.01

Reserves & Surplus 606.30 839.84 1,026.45

Net worth (shareholders funds) 631.32 864.89 1,051.59

Minority Interest (0.38) (0.58) (0.66)

Long term borrowings 459.36 454.52 194.62

Current liabilities 216.18 209.70 578.53

Other long term liabilities and provisions - - 7.00

Deferred Tax Liabilities 65.11 79.30 80.73

Total Liabilities 1,371.59 1,607.83 1,911.81

(Rs. Cr)

Application of Funds / Assets

Particulars FY 2009 FY 2010 FY 2011

Fixed Assets 591.20 676.13 793.97

Noncurrent Investments 41.17 32.54 40.68

Current assets 739.22 899.16 1,036.80

Long term advances and other noncurrent assets - - 40.36

Goodwill on consolidation (net) - -

Total assets 1,371.59 1,607.83 1,911.81

Efficiency Analysis(%)

Particulars FY 2009 FY 2010 FY 2011

ROCE 17.35 25.54 33.67

Page 17

ROE / RONW 15.97 23.74 24.99

Return on Capital Employed (ROCE) measures a company’s profitability from its overall operations by

calculating the return generated on the total capital invested in the business (i.e. equity + debt).

Return on Equity (ROE) or Return on Net Worth (RONW) measures the amount of profit which the

company generates on money invested by the equity shareholders. In short, ROE draws attention to

the return generated by the shareholders on their investment in the business. Together these ratios

can be used in comparing the profitability of the company with other companies in the same industry. Efficiency Ratios

Valuation Analysis

Annually

Quarterly

Consolidated

Particulars FY 2009 FY 2010 FY 2011

Total Income from Operations (Rs. Cr.) 1,292.64 1,566.58 1,898.86

Growth (%) - 21.19 % 21.21 %

PAT (Rs. Cr.) 100.80 205.36 262.82

Growth (%) - 103.73 % 27.98 %

Earnings Per Share – Basic (Rs. ) 7.89 16.44 20.96

Earning Per Share - Diluted (Rs. ) 7.8 16.41 20.95

Price to Earnings 8.33 16.41 14.39

Price Earnings Ratio

Dividend History

Year Rate of dividend (of face value) Rs.

FY 2008 80 % 1.60

Page 18

FY 2009 110 % 2.20

FY 2010 150 % 3.00

FY 2011 160 % 3.20

FY 2012 160 % 3.20

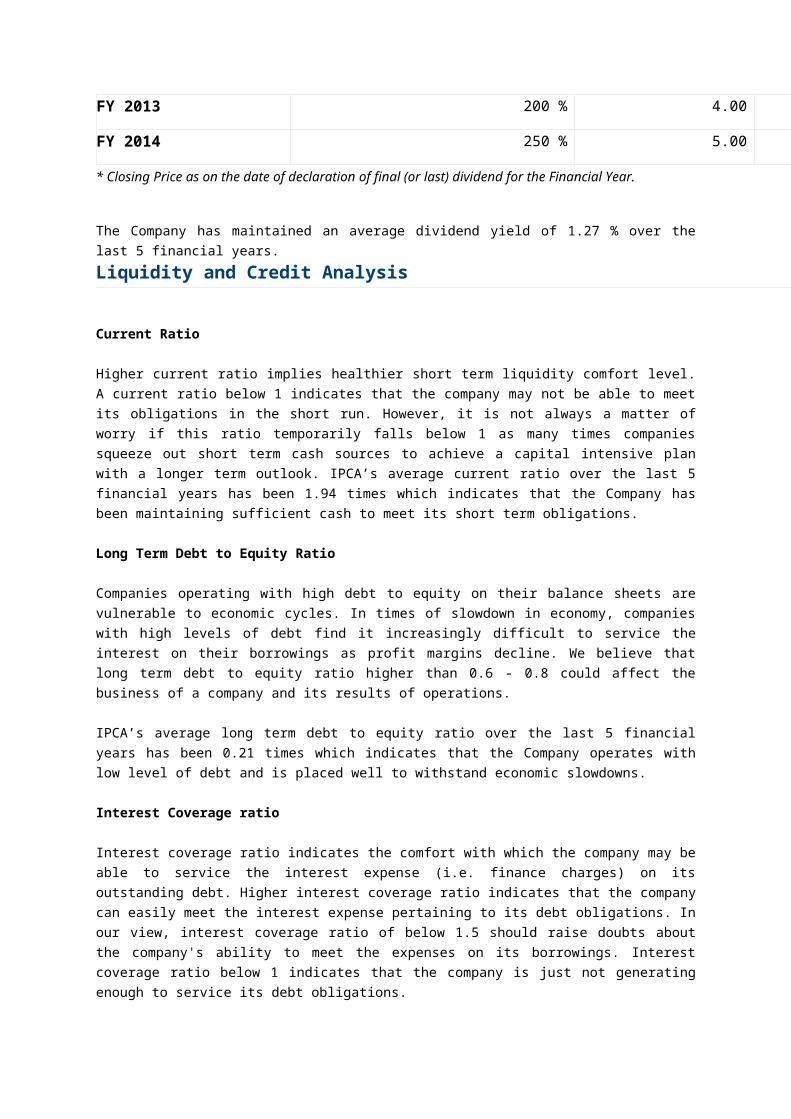

FY 2013 200 % 4.00

FY 2014 250 % 5.00

* Closing Price as on the date of declaration of final (or last) dividend for the Financial Year.

The Company has maintained an average dividend yield of 1.27 % over the last 5 financial years.

Liquidity and Credit Analysis

Current Ratio

Higher current ratio implies healthier short term liquidity comfort level. A current ratio below 1

indicates that the company may not be able to meet its obligations in the short run. However, it is not

always a matter of worry if this ratio temporarily falls below 1 as many times companies squeeze out

short term cash sources to achieve a capital intensive plan with a longer term outlook. IPCA’s average

current ratio over the last 5 financial years has been 1.94 times which indicates that the Company has

been maintaining sufficient cash to meet its short term obligations.

Long Term Debt to Equity Ratio

Companies operating with high debt to equity on their balance sheets are vulnerable to economic

cycles. In times of slowdown in economy, companies with high levels of debt find it increasingly

difficult to service the interest on their borrowings as profit margins decline. We believe that long term

debt to equity ratio higher than 0.6 - 0.8 could affect the business of a company and its results of

operations.

IPCA’s average long term debt to equity ratio over the last 5 financial years has been 0.21 times

which indicates that the Company operates with low level of debt and is placed well to withstand

economic slowdowns.

Interest Coverage ratio

Interest coverage ratio indicates the comfort with which the company may be able to service the

interest expense (i.e. finance charges) on its outstanding debt. Higher interest coverage ratio

indicates that the company can easily meet the interest expense pertaining to its debt obligations. In

our view, interest coverage ratio of below 1.5 should raise doubts about the company's ability to meet

the expenses on its borrowings. Interest coverage ratio below 1 indicates that the company is just not

generating enough to service its debt obligations.

Page 19

IPCA’s average interest coverage ratio over the last 5 financial years has been 17.26 times which

indicates that the Company has been generating enough for the shareholders after servicing its debt

obligations.

Company Name: Divis Laboratories

Head Office: Hyderabad

Industry Type: Pharmaceuticals

Founded: 1990

Founder: Dr. Murali K Divi

Key people: Mr N. V. Ramana, Executive Director, Mr Madhusudana Rao Divi, Director, Mr. Kiran S Divi, Director (Business Development)

Products: Active Pharmaceutical Ingredients (APIs) & Intermediates for Generics

Page 20

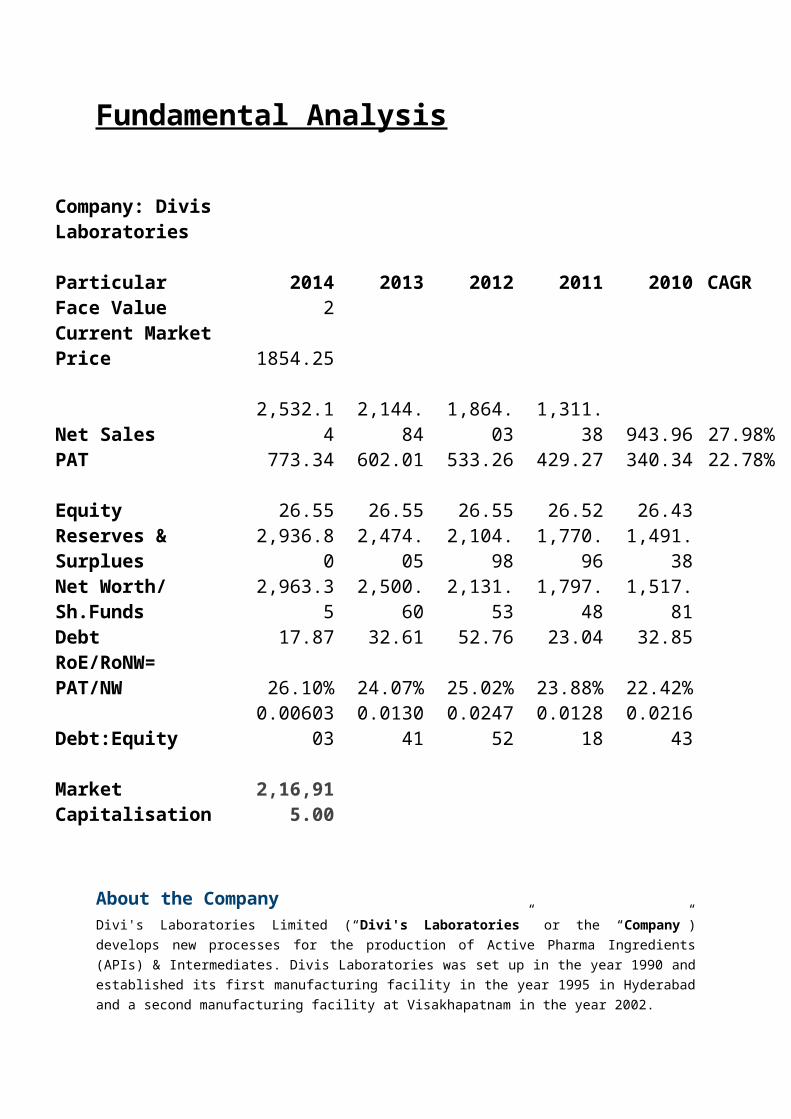

Fundamental Analysis

Company: Divis Laboratories Particular 2014 2013 2012 2011 2010 CAGRFace Value 2 Current Market Price 1854.25 Net Sales 2,532.14 2,144.84 1,864.03 1,311.38 943.96 27.98%PAT 773.34 602.01 533.26 429.27 340.34 22.78% Equity 26.55 26.55 26.55 26.52 26.43 Reserves & Surplues 2,936.80 2,474.05 2,104.98 1,770.96 1,491.38 Net Worth/ Sh.Funds 2,963.35 2,500.60 2,131.53 1,797.48 1,517.81 Debt 17.87 32.61 52.76 23.04 32.85 RoE/RoNW= PAT/NW 26.10% 24.07% 25.02% 23.88% 22.42% Debt:Equity 0.0060303 0.013041 0.024752 0.012818 0.021643

Market Capitalisation 2,16,915.0

0

About the CompanyDivi's Laboratories Limited (“Divi's Laboratories” or the “Company”) develops new processes for the

production of Active Pharma Ingredients (APIs) & Intermediates. Divis Laboratories was set up in the

year 1990 and established its first manufacturing facility in the year 1995 in Hyderabad and a second

manufacturing facility at Visakhapatnam in the year 2002.

The Hyderabad plant comprises of 13 multi-purpose production blocks While the Visakhapatnam site

has 14 multipurpose production blocks. The Company's product portfolio comprises of two broad

segments i) Generic APIs (Active Pharma Ingredients) and Nutraceuticals and ii) Custom Synthesis of

APIs, intermediates and specialty ingredients for innovator pharma giants.

The Company operates predominantly in export markets and has a broad product portfolio under

generics and custom synthesis. Exports constituted around 90% of gross sales in FY 2013 r as

against 89% in the previous year. Exports to advanced markets comprising Europe and America

accounted for 77% of business.

Page 21

* The Equity Research Report presented below is based on a Fundamental Analysis of Divis

Laboratories.

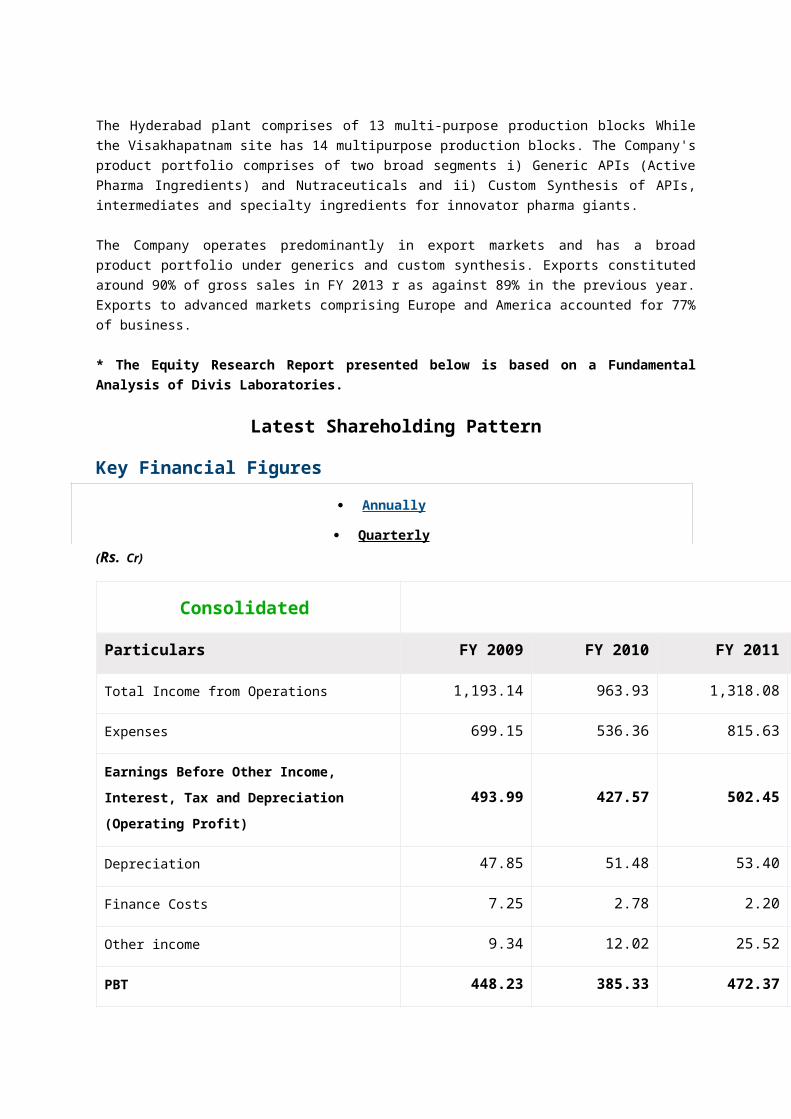

Latest Shareholding Pattern

Key Financial Figures

Annually

Quarterly

(Rs. Cr)

Consolidated

Particulars FY 2009 FY 2010 FY 2011

Total Income from Operations 1,193.14 963.93 1,318.08

Expenses 699.15 536.36 815.63

Earnings Before Other Income, Interest, Tax and

Depreciation (Operating Profit)493.99 427.57 502.45

Depreciation 47.85 51.48 53.40

Finance Costs 7.25 2.78 2.20

Other income 9.34 12.02 25.52

PBT 448.23 385.33 472.37

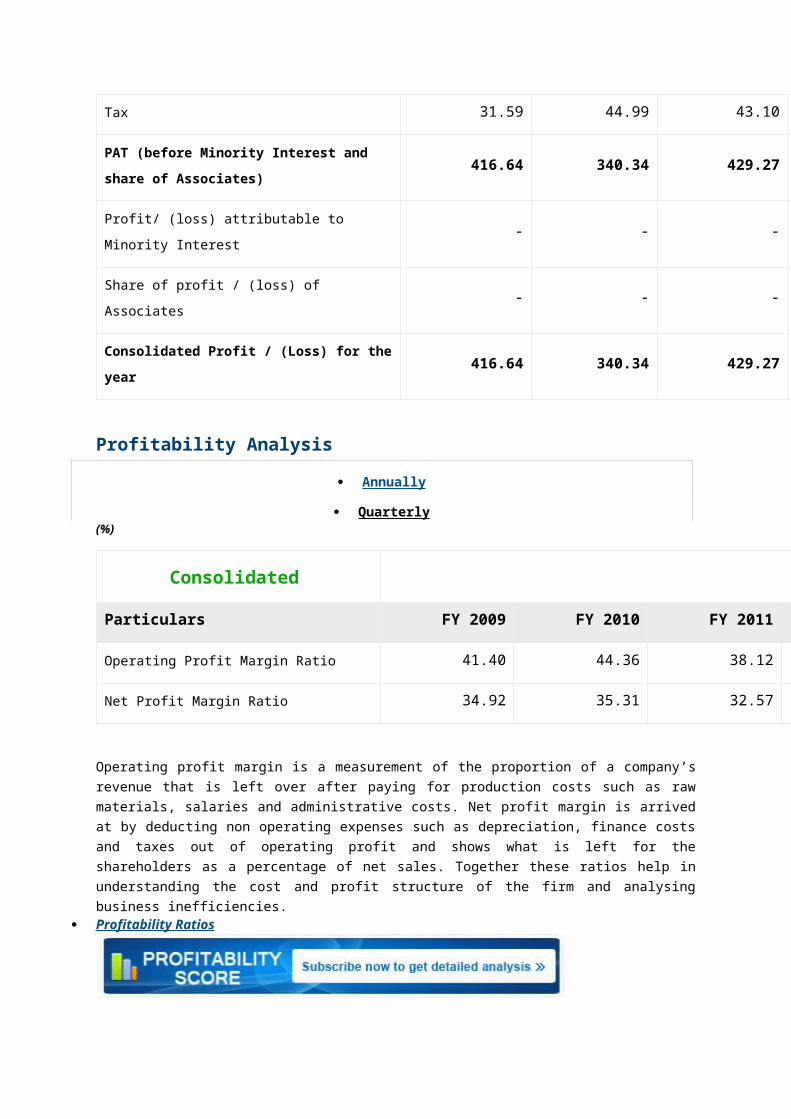

Tax 31.59 44.99 43.10

PAT (before Minority Interest and share of

Associates)416.64 340.34 429.27

Profit/ (loss) attributable to Minority Interest - - -

Share of profit / (loss) of Associates - - -

Consolidated Profit / (Loss) for the year 416.64 340.34 429.27

Profitability Analysis

Annually

Page 22

Quarterly (%)

Consolidated

Particulars FY 2009 FY 2010 FY 2011

Operating Profit Margin Ratio 41.40 44.36 38.12

Net Profit Margin Ratio 34.92 35.31 32.57

Operating profit margin is a measurement of the proportion of a company’s revenue that is left over

after paying for production costs such as raw materials, salaries and administrative costs. Net profit

margin is arrived at by deducting non operating expenses such as depreciation, finance costs and

taxes out of operating profit and shows what is left for the shareholders as a percentage of net sales.

Together these ratios help in understanding the cost and profit structure of the firm and analysing

business inefficiencies. Profitability Ratios

Key Balance Sheet Figures(Rs. Cr)

Sources of Funds / Liabilities

Particulars FY 2009 FY 2010 FY 2011

Share Capital 12.95 26.43 26.52

Reserves & Surplus 1,228.43 1,491.38 1,770.96

Net worth (shareholders funds) 1,241.38 1,517.80 1,797.48

Long term borrowings 52.64 32.85 4.92

Current liabilities 211.01 260.79 409.90

Other long term liabilities and provisions - - 12.43

Deferred Tax Liabilities 43.22 47.41 50.04

Page 23

Total Liabilities 1,548.25 1,858.85 2,274.78

(Rs. Cr)

Application of Funds / Assets

Particulars FY 2009 FY 2010 FY 2011

Fixed Assets 609.37 613.59 694.27

Noncurrent Investments 171.80 441.28

Current assets 767.08 803.99 1,540.71

Long term advances and other noncurrent assets - - 39.80

Total assets 1,548.25 1,858.85 2,274.78

Efficiency Analysis(%)

Particulars FY 2009 FY 2010 FY 2011

ROCE 38.17 27.57 27.88

ROE / RONW 33.56 22.42 23.88

Return on Capital Employed (ROCE) measures a company’s profitability from its overall operations by

calculating the return generated on the total capital invested in the business (i.e. equity + debt).

Return on Equity (ROE) or Return on Net Worth (RONW) measures the amount of profit which the

company generates on money invested by the equity shareholders. In short, ROE draws attention to

the return generated by the shareholders on their investment in the business. Together these ratios

can be used in comparing the profitability of the company with other companies in the same industry. Efficiency Ratios

Valuation Analysis

Annually

Quarterly

Consolidated

Particulars FY 2009 FY 2010 FY 2011

Page 24

Total Income from Operations (Rs. Cr.) 1,193.14 963.93 1,318.08

Growth (%) - (19.21 %) 36.74 %

PAT (Rs. Cr.) 416.64 340.34 429.27

Growth (%) - (18.31 %) 26.13 %

Earnings Per Share – Basic (Rs. ) 32.19 26.12 32.42

Earning Per Share - Diluted (Rs. ) 31.87 26.06 32.41

Price to Earnings 14.96 26.06 20.85

Price Earnings Ratio

Dividend History

Year Rate of dividend (of face value) Rs.

FY 2008 200 % 4.00

FY 2009 300 % 6.00

FY 2010 300 % 6.00

FY 2011 500 % 10.00

FY 2012 650 % 13.00

FY 2013 750 % 15.00

FY 2014 1,000 % 20.00

* Closing Price as on the date of declaration of final (or last) dividend for the Financial Year.

The Company has maintained an average dividend yield of 0.98 % over the last 5 financial years.

Liquidity and Credit Analysis

Current Ratio

Higher current ratio implies healthier short term liquidity comfort level. A current ratio below 1

indicates that the company may not be able to meet its obligations in the short run. However, it is not

always a matter of worry if this ratio temporarily falls below 1 as many times companies squeeze out

Page 25

short term cash sources to achieve a capital intensive plan with a longer term outlook. DIVISLAB’s

average current ratio over the last 5 financial years has been 3.50 times which indicates that the

Company is comfortably placed to pay for its short term obligations.

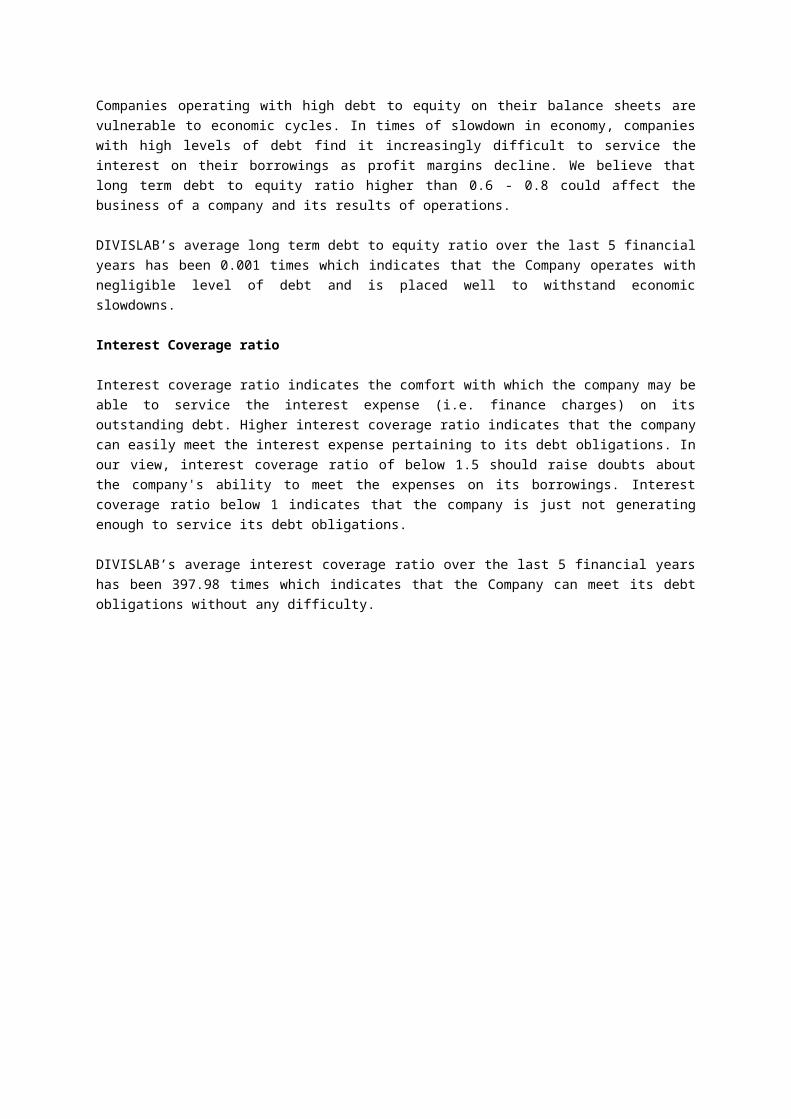

Long Term Debt to Equity Ratio

Companies operating with high debt to equity on their balance sheets are vulnerable to economic

cycles. In times of slowdown in economy, companies with high levels of debt find it increasingly

difficult to service the interest on their borrowings as profit margins decline. We believe that long term

debt to equity ratio higher than 0.6 - 0.8 could affect the business of a company and its results of

operations.

DIVISLAB’s average long term debt to equity ratio over the last 5 financial years has been 0.001 times

which indicates that the Company operates with negligible level of debt and is placed well to withstand

economic slowdowns.

Interest Coverage ratio

Interest coverage ratio indicates the comfort with which the company may be able to service the

interest expense (i.e. finance charges) on its outstanding debt. Higher interest coverage ratio

indicates that the company can easily meet the interest expense pertaining to its debt obligations. In

our view, interest coverage ratio of below 1.5 should raise doubts about the company's ability to meet

the expenses on its borrowings. Interest coverage ratio below 1 indicates that the company is just not

generating enough to service its debt obligations.

DIVISLAB’s average interest coverage ratio over the last 5 financial years has been 397.98 times

which indicates that the Company can meet its debt obligations without any difficulty.

Page 26

Company Name: Alembic Pharmaceuticals

Head Office: Vadodara , Gujarat ,INDIA

Industry Type: Pharmaceuticals

Founded: 1907

Founder: Mr.Chirayu R. Amin

Key people: Pranav Amin, shaunak amin

Products: Pharmaceutical substances and Intermediates

Page 27

Fundamental Analysis

Company:Alembic Pharmaceuticals Particular 2014 2013 2012 2011 2010 CAGRFace Value 2 Current Market Price 679 Net Sales 2,056.12 1,863.22 1,520.35 1,466.39 1,192.35 14.59%PAT 282.72 235.51 165.25 130.13 85.39 34.89% Equity 37.7 37.7 37.7 37.7 37.7 Reserves & Surplues 846.94 637.87 465.24 357.3 259.03 Net Worth/ Sh.Funds 884.64 675.57 502.94 395 296.73 Debt 238.5 77.65 140.64 234.32 327.9 RoE/RoNW= PAT/NW 31.96% 34.86% 32.86% 32.94% 28.78% Debt:Equity 0.269601 0.11494 0.279636 0.593215 1.105045 Market Capitalisation 14,347.95

About the CompanyEstablished in 1907, Alembic Pharmaceuticals Limited ("Alembic" or the "Company") is one of the

leading pharmaceutical company in India. The Company develops, manufactures and markets

pharmaceutical products, pharmaceutical substances and Intermediates. Alembic is the market leader

in the segment of anti-infective drugs in India.

The Company's manufacturing facilities are located in Vadodara and Baddi in Himachal Pradesh. The

plant at Vadodara has the largest fermentation capacity in India. The Panelav facility houses the API

and formulation manufacturing (both US FDA approved) plants. The plant at Baddi, Himachal Pradesh

manufactures formulations for the domestic and non-regulated export market.

* The Equity Research Report presented below is based on a Fundamental Analysis of Alembic

Pharmaceuticals Limited.

Latest Shareholding Pattern

Key Financial Figures

Annually

Quarterly

(Rs. Cr)

Page 28

Consolidated

Particulars FY 2011 FY 2012 FY 2013

Total Income from Operations 1,202.04 1,466.39 1,519.34

Expenses 1,041.79 1,245.98 1,267.38

Earnings Before Other Income, Interest, Tax and

Depreciation (Operating Profit)160.25 220.41 251.96

Depreciation 29.59 33.65 34.97

Finance Costs 23.89 26.21 14.57

Other income 0.08 0.44 3.93

PBT 106.85 160.99 206.35

Tax 21.46 30.85 41.10

PAT (before Minority Interest and share of

Associates)85.39 130.14 165.25

Share of profit / (loss) of Associates - - -

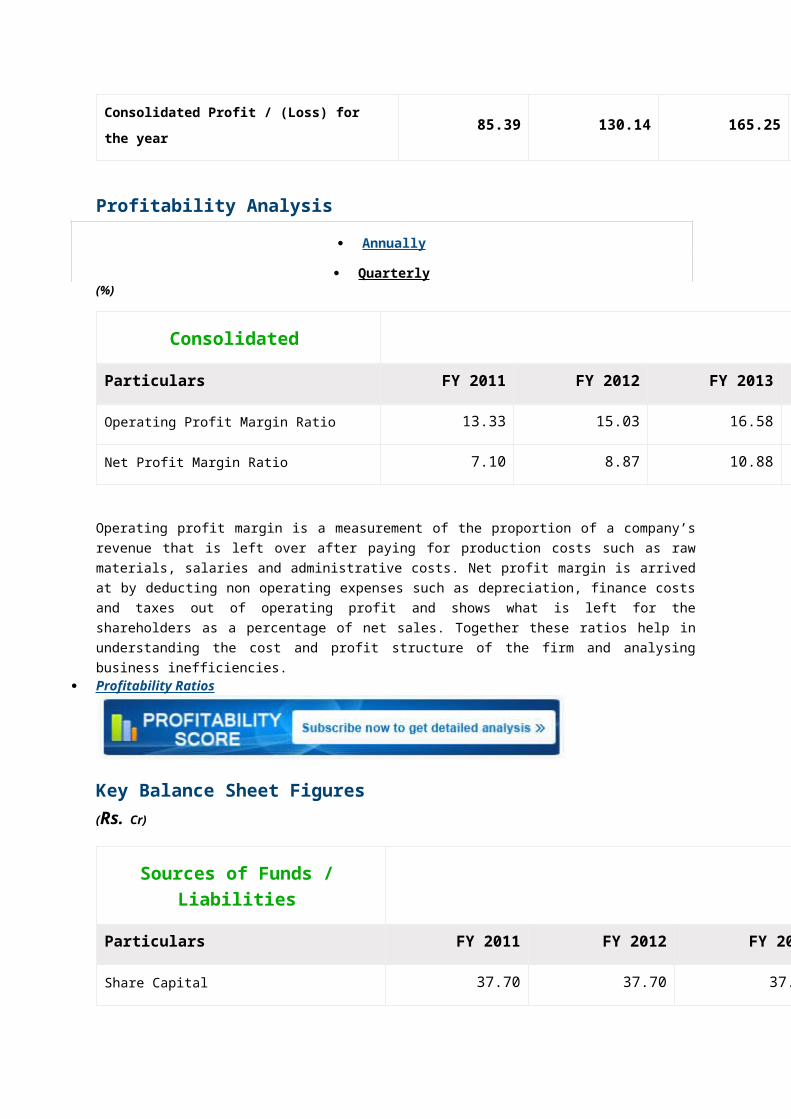

Consolidated Profit / (Loss) for the year 85.39 130.14 165.25

Profitability Analysis

Annually

Quarterly (%)

Consolidated

Particulars FY 2011 FY 2012 FY 2013

Operating Profit Margin Ratio 13.33 15.03 16.58

Net Profit Margin Ratio 7.10 8.87 10.88

Page 29

Operating profit margin is a measurement of the proportion of a company’s revenue that is left over

after paying for production costs such as raw materials, salaries and administrative costs. Net profit

margin is arrived at by deducting non operating expenses such as depreciation, finance costs and

taxes out of operating profit and shows what is left for the shareholders as a percentage of net sales.

Together these ratios help in understanding the cost and profit structure of the firm and analysing

business inefficiencies. Profitability Ratios

Key Balance Sheet Figures(Rs. Cr)

Sources of Funds / Liabilities

Particulars FY 2011 FY 2012 FY 2013

Share Capital 37.70 37.70 37.70

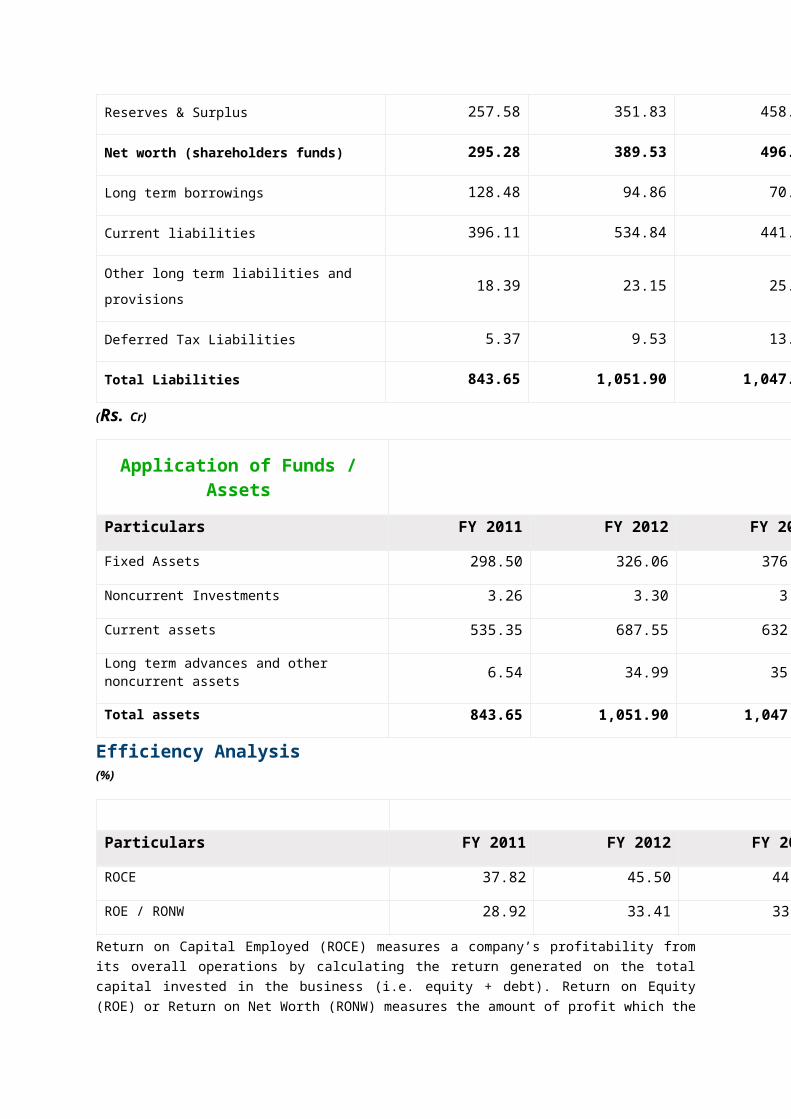

Reserves & Surplus 257.58 351.83 458.54

Net worth (shareholders funds) 295.28 389.53 496.25

Long term borrowings 128.48 94.86 70.53

Current liabilities 396.11 534.84 441.63

Other long term liabilities and provisions 18.39 23.15 25.52

Deferred Tax Liabilities 5.37 9.53 13.90

Total Liabilities 843.65 1,051.90 1,047.82

(Rs. Cr)

Application of Funds / Assets

Particulars FY 2011 FY 2012 FY 2013

Fixed Assets 298.50 326.06 376.48

Noncurrent Investments 3.26 3.30 3.30

Current assets 535.35 687.55 632.16

Page 30

Long term advances and other noncurrent assets 6.54 34.99 35.88

Total assets 843.65 1,051.90 1,047.82

Efficiency Analysis(%)

Particulars FY 2011 FY 2012 FY 2013

ROCE 37.82 45.50 44.45

ROE / RONW 28.92 33.41 33.30

Return on Capital Employed (ROCE) measures a company’s profitability from its overall operations by

calculating the return generated on the total capital invested in the business (i.e. equity + debt).

Return on Equity (ROE) or Return on Net Worth (RONW) measures the amount of profit which the

company generates on money invested by the equity shareholders. In short, ROE draws attention to

the return generated by the shareholders on their investment in the business. Together these ratios

can be used in comparing the profitability of the company with other companies in the same industry. Efficiency Ratios

Valuation Analysis

Annually

Quarterly

Consolidated

Particulars FY 2011 FY 2012 FY 2013

Total Income from Operations (Rs. Cr.) 1,202.04 1,466.39 1,519.34

Growth (%) - 21.99 % 3.61 %

PAT (Rs. Cr.) 85.39 130.14 165.25

Growth (%) - 52.00 % 26.98 %

Earnings Per Share – Basic (Rs. ) 4.53 6.90 8.77

Earning Per Share - Diluted (Rs. ) 4.53 6.90 8.77

Price to Earnings 10.13 7.09 11.88

Page 31

Price Earnings Ratio

Dividend History

Year Rate of dividend (of face value) Rs.

FY 2012 70 % 2.00

FY 2013 125 % 2.00

FY 2014 150 % 2.00

* Closing Price as on the date of declaration of final (or last) dividend for the Financial Year.

The Company has maintained an average dividend yield of 2.00 % over the last 3 financial years.

Liquidity and Credit Analysis

Current Ratio

Higher current ratio implies healthier short term liquidity comfort level. A current ratio below 1

indicates that the company may not be able to meet its obligations in the short run. However, it is not

always a matter of worry if this ratio temporarily falls below 1 as many times companies squeeze out

short term cash sources to achieve a capital intensive plan with a longer term outlook.

Alembic's average current ratio over the last 5 financial years has been 1.41 times which indicates

that the Company is comfortably placed to pay for its short term obligations.

Long term Debt to Equity Ratio

Companies operating with high long term debt to equity on their balance sheets are vulnerable to

economic cycles. In times of slowdown in economy, companies with high levels of debt find it

increasingly difficult to service the interest on their borrowings as profit margins decline. We believe

that long term debt to equity ratio higher than 0.6 - 0.8 could affect the business of a company and its

results of operations.

Alembic's average long term debt to equity ratio over the last 5 financial years has been 0.18 times

which indicates that the Company operates with close to zero debt and is placed well to withstand

economic slowdowns.

Interest Coverage Ratio

Interest coverage ratio indicates the comfort with which the company may be able to service the

interest expense (i.e. finance charges) on its outstanding debt. Higher interest coverage ratio

Page 32

indicates that the company can easily meet the interest expense pertaining to its debt obligations. In

our view, interest coverage ratio of below 1.5 should raise doubts about the company’s ability to meet

the expenses on its borrowings. Interest coverage ratio below 1 indicates that the company is just not

generating enough to service its debt obligations.

Alembic's average interest coverage ratio over the last 5 financial years has been 59.05 times which

indicates that the Company can meet its debt obligations without any difficulty.