16

1 School Financing Information July 27, 2010

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 1/16

1

School Financing Information

July 27, 2010

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 2/16

2

School Construction Financinghttp://www.doe.virginia.gov/support/facility_construction/literary_fund_loans/funding_options.pdf

School Construction Financing Options~ . Fm

L ocal Public School D ivisions

January 2008

Virginia Public Schoo l Authority

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 3/16

3

School Construction Financing

•

•

•

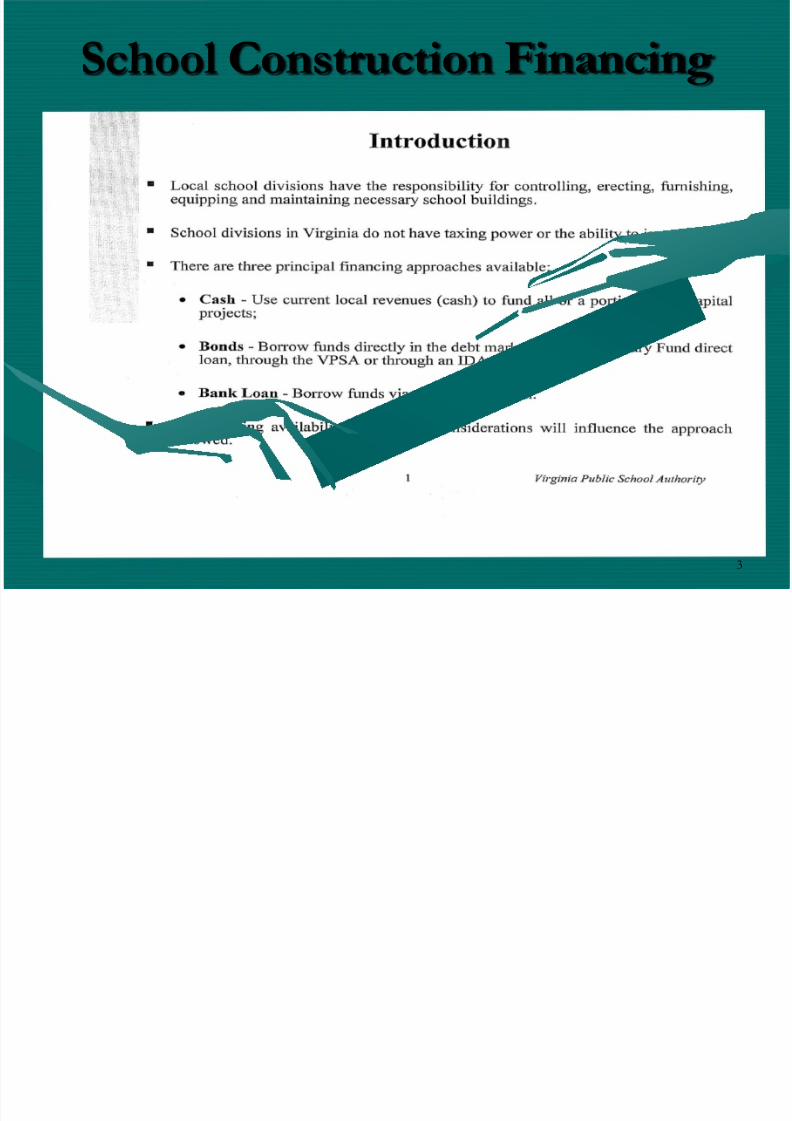

Introduction

Local school d iv isions have the responsibility for controlling, erecting, furnishing,equipping and maintaining necessary school buildings .

Schoo l divisions in Virginia do not have taxing power or th e ability to issue debt.

There are three principa l financing approaches available:

• Cash - Use current local revenues (cash) to fund a ll or a portion of the capitalprojects;

• Bonds - Borrow funds directly in th e debt market or with a Literruy Fund directloan, tlu'ough th e VPSA or through an IDA; or

• Bank Loan - Borrow funds via a direct bank loan .

Cost, funding availability and t iming considerations will influence th e approachfollowed.

1 Virginia Pu b lic Schoo l Au thority

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 4/16

4

School Construction Financing

~ ;

Financing Options

lti I. General Obligation Debt (GO) - Secured by the full faith and credit of

an issuer with taxing power.

f· .~ :J. - : ~ • Direct Local Goverrunent Borrowing: Issue and sell GO bonds directly in

either the public or private markets (may require voter approval to secure

GO pledge);

,::. ~ , ;

• L iterary Fund Direct Loan: For qualified projects bon'ow at below marketinterest t"ates from the fund, administered by the Department of E ducation.

o Projects up to $7.5 million; $20 million ca p by locality

o Interest rates are derived from th e loca l composite index of ability to pay,an d

o Subject to availability of funds.

• Virginia Public School Authority (VPSA): Borrow indirectly through th epooled bond or subsidy programs of the VPSA.

2 Virginia Public School Au/hOl·ity

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 5/16

5

School Construction Financing

Financing Options (cont'd)

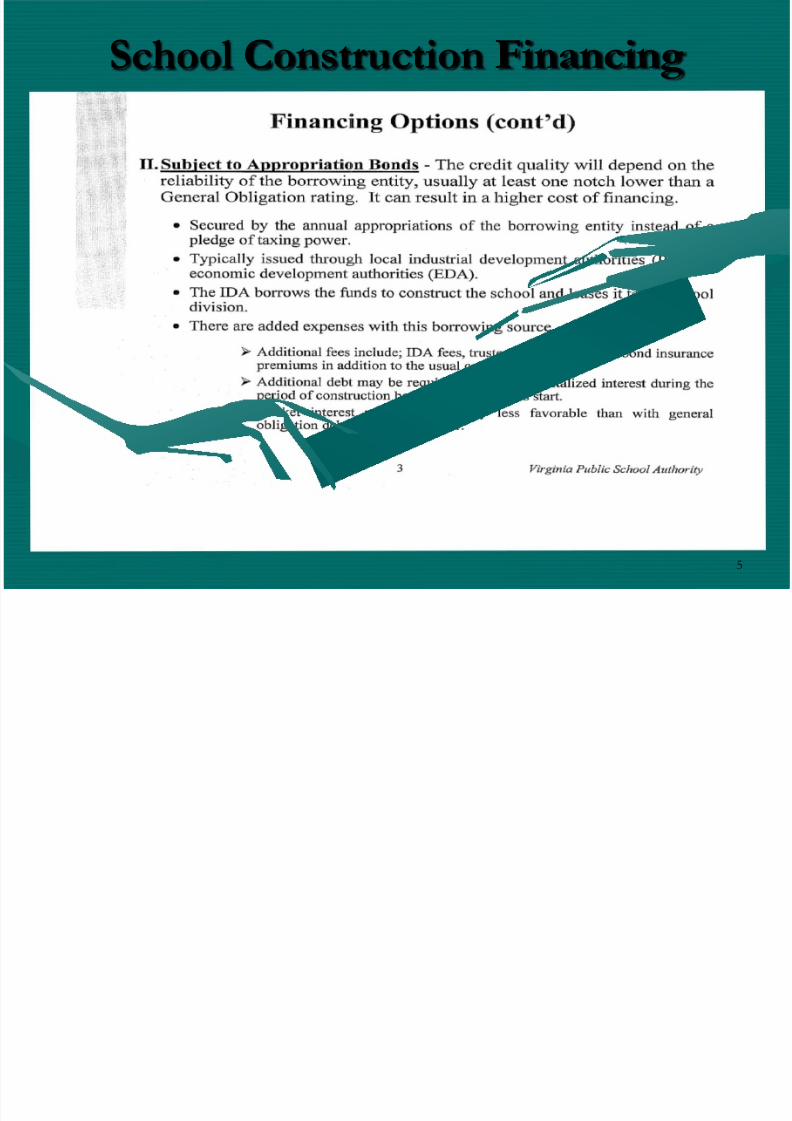

II. Subject to Appropriation Bonds - The credit qua lity will depend on the

reliability of the borrowing entity, usually at least one notch lower than aGeneral Obligation rating. I t can result in a h igher cost of financing.

• Secured by the annual appl"Opriations of the borrowing entity instead o f apledge o f taxing power.

• Typically issued through local industrial development authorities (IDA) OT

economic development authorities (EDA).• The IDA borl"Ows the funds to construct the school and leases it to the school

division.

• There ar e added expenses with this borrowing source.

}» Additional fees include; IDA fees, trustee fees and possibly bond insurancepremiums in addition to the usual costs of issuance.

}» Additional debt may be required to provide capitalized interest during th e

period o f construction before lease payments start.

}» Market interest rates are generally les s favorable than with generalobligation debt of the same issuer.

3 Virginia Public School Authority

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 6/16

6

School Construction Financing

Virginia Public School AuthorityIntroduction

• The Virginia Public School Authority ("VPSA") , established in 1962, is a bond

bank which pwvides low-cost :fmancing o f capital pwjects for primary an d

secondary public schools in Virginia localities.

• Pwvides financing to localities through th e sale of bonds. With th e proceeds

of it s bonds, the VPSA purchases general obligation bonds from localities.

• Assists localities through -

o Pooled bond program;

o Interest rate subsidy program for projects on the Board o f Education's

First Priority Waiting list (the "L ist");

o Stand alone bond pwgram; and,

o Educational Technology Notes.

4 Virginia Public School Authority

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 7/16

7

School Construction Financing

"

Pooled Bond ProgralDKey Features For Local Participants

• VPSA can finance all types o f real and personal property for public schools

including land, buildings and equipment.

• Under the State Constitution, local issuers of general obligation school bonds

are not required to obtain voter approval for bonds sold to the VPSA .

• VPSA's "double-A plus" bond rating provides very attractive interest rates for

participating localities.

• Semi-Annual SpringlFall bond issues have scheduled debt servIce in the

subsequent fiscal year to conform to local budgetary cycles.

5 Virginia Public Schoo l Authority

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 8/16

8

School Construction FinancingPooled Bond Program

Key Features For Local Participants (cont'd)

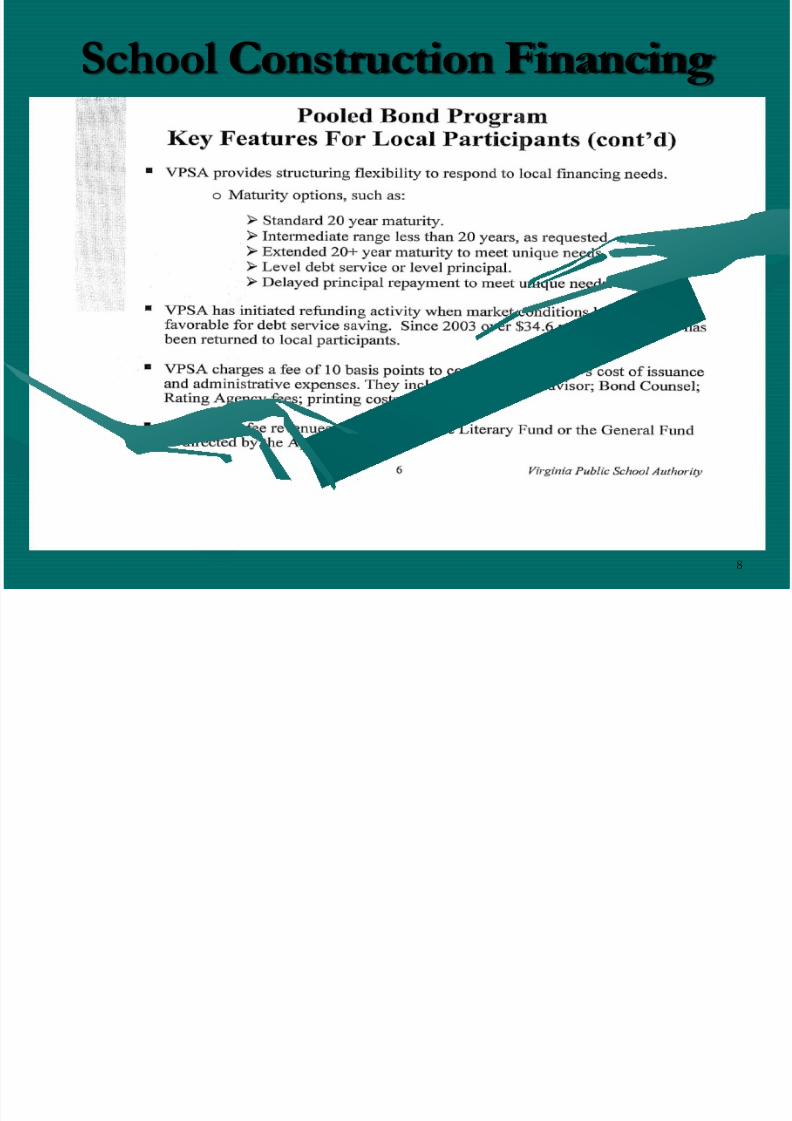

• VPSA provides str ucturing flexibility to respond to local Imancing needs.

o Maturity options, such as :

~ Standard 20 year maturity.

~ Intermediate range less than 20 years, as requested.

~ Extended 20+ year maturity to meet unique needs.

~ Leve l debt service or level principal.

~ Delayed principal repayment to meet unique needs.

• VPSA has initiated refunding activity when market conditions have beenfavorable for debt service saving . Since 2003 over $34 .6 million in savings hasbeen returned to local participants.

• VPSA charges a fee of 10 basis points to cover the Authority's cost o f issuanceand administrative expenses. They include: Financial Advisor; Bond Counsel;Rating Agency fees; printing costs; etc.

• Any excess fee revenues revert back to the Literary Fund or the General Fundas directed by th e Appropriation Act .

6 Virginia Public School Authority

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 9/16

9

School Construction Financing

•."

., ,,I •

••

•

•

•

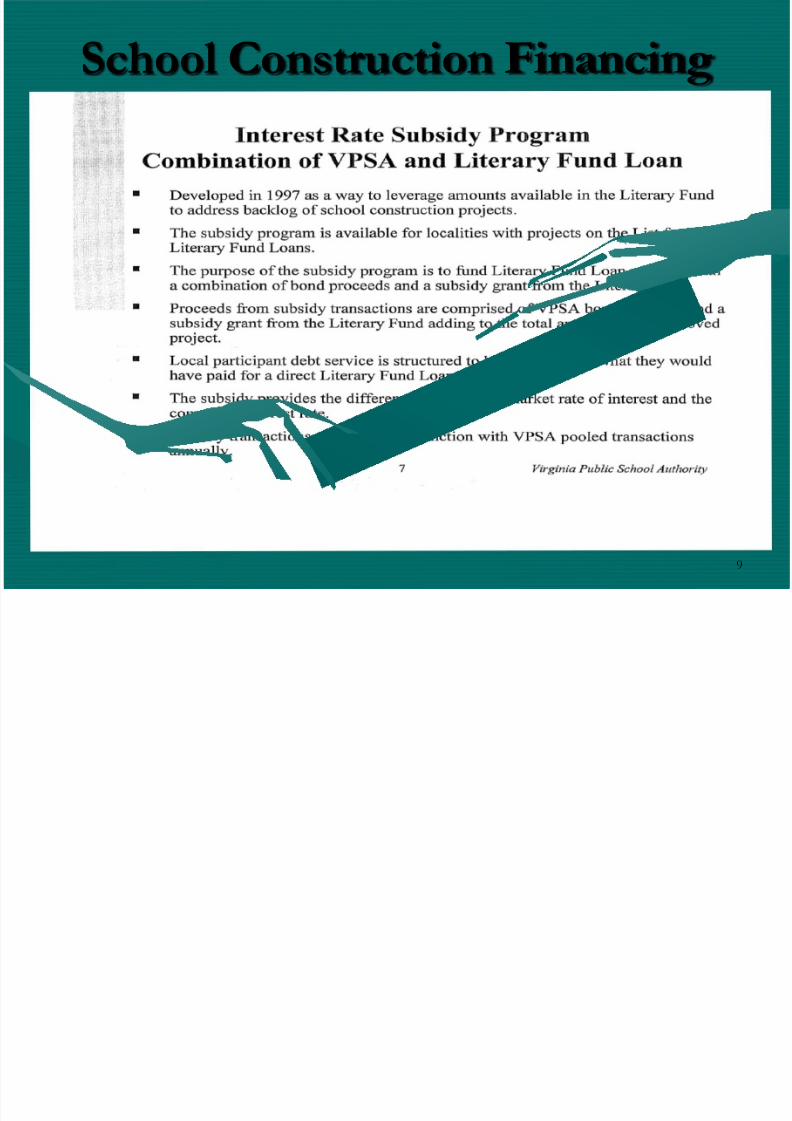

Interest Rate Subsidy Progr amCombination of VPSA and Literary Fund Loan

Developed in 1997 as a way to leverage amou nts available in the LiteralY Fundto address backlog of schoo l construction projects .

The subsidy program is available for localities with projects on the List for direct

Literary Fund Loans .

The purposeof

the subsidy program is to fund Literary Fund Loan requests witha combination of bond proceeds and a subsidy grant from the Literary Fund.

Proceeds from subsidy transactions ar e comprised ofVPSA bond proceeds and asubsidy grant fi·om th e Literary Fund adding to the total amount of th e approved

project .

Local participant debt service is structured to be equivalent to what they would

have paid for a direct Literary Fund Loan.

T he subsidy provides the difference between the market rate of interest and the

composite interes t rate .

Subsidy transactions are held in conjunction with VPSA pooled transactions

annually .

7 Virgin ia P ublic School Au thority

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 10/16

10

School Construction Financing

, ' ~ , ~ ; •

.,-

';

Interest Rate Subsidy Prog ram

Combination ofVPSA and Literary Fund Loan (cont'd)

• Advantages:

• Bon-ow for school construction at below market interest ra tes, Le_ Literary

Fund loan rates typically of2% - 4%.

• A subsidy loan does not count toward the $20 million outstanding LiteraryFund cap per locality .

• Funds can be expended in accordance with the more flexible VPSA guidelines

fo r school capital expenditures.

• Item 135 o f the 2007 Approp riation Act for the 2006-2008 biennirun authorized theVPSA to provide interest rate subsidies to localities on the List_

• $15 .0 million available in fiscal year 2007 - $105.7 million of projects funded

on the List; and

• $20_0 million available in fiscal year 2008 - $149.9 million of projects fundedon the List.

8 Virg in ia Public Sc hoo l Autho rity

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 11/16

11

School Construction Financing

Other Sources:

• Rural Development Funds – Not usually

available for schools and Montgomery

County does not qualify

• FEMA – collapse does not meet FEMA

threshold

• Actions by State or Federal Elected Officials

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 12/16

12

County Debt

Montgomery County , o ; ; , ~ ~ ~ ! c o c J " ; ; , . , . Virginia r l \ l . . . , j Analysis of Proposed QSCB P rojec ts ~ ~ 0 ~ , " . 4 ~ on Debt Capacity and / : ~ ~ e ~ Debt Affordabi l i ty .- .

Apri l 26, 2010

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 13/16

13

County Debt

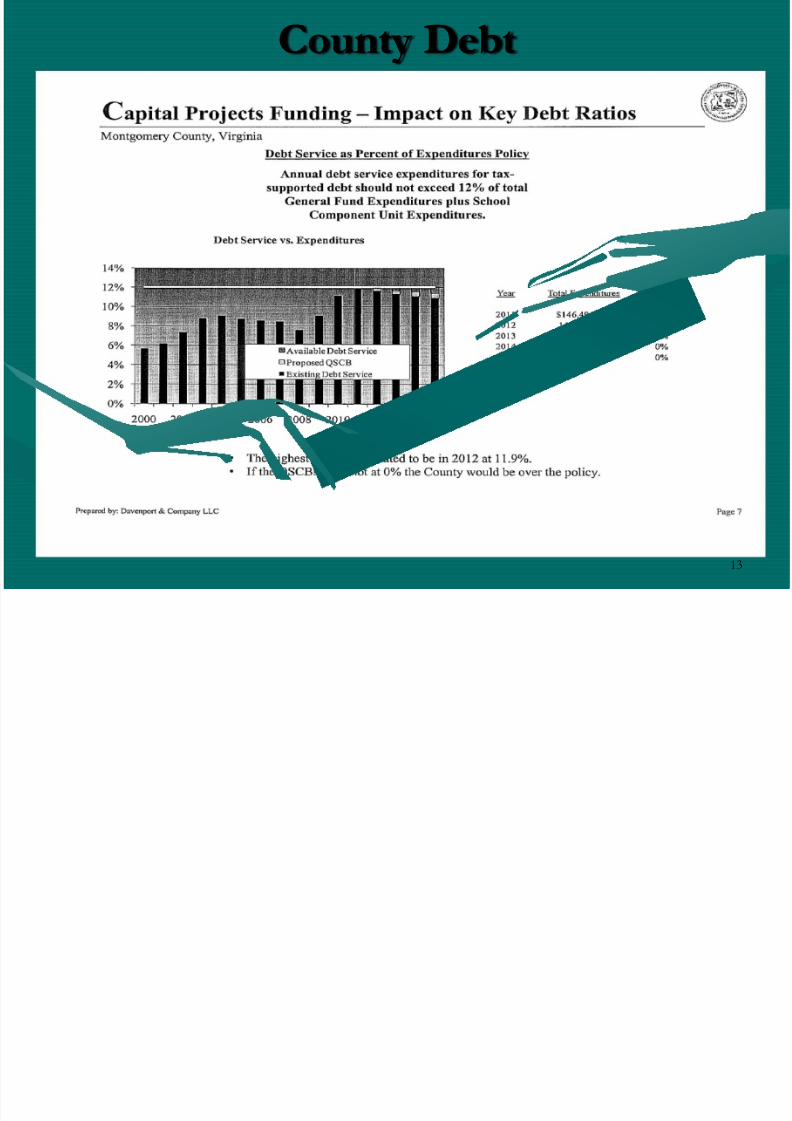

Capital Projects Funding - Impact on Key Debt Ratios

Montgomery County, Virginia

14%

12%10%

8%

6%

4%

2%

Q1Yo

Debt Service as Percent of Expenditures Policy

Annua l debt service expenditures fo r tax-

supported debt sbould no t exceed 12 % oftotal

Genera l Fund Expenditures plus School

Component Unit Expenditures.

Debt Service vs. Expenditures

Year

2011

201 2

201 3

201 4

201 5

2000 2002 2004 2006 2008 2010 2012 2014

The highest point is estimated to be in 2012 at 11.9% ,

Total Expenditures

S 146,49 6 ,555

146,49 6 ,55 5

146,496 ,555

146 .49 6 .555

146 ,49 6, 55 5

If the QSCBs were no t at 0% the County wou ld be over the policy,

Prepared by: Davenport & Company LLC

% Growth

0%

0%

0%

0%

Page 7

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 14/16

14

County Debt

Future Debt CapacityMontgo mery County, Virginia

Future Debt Caoacity

2011 2012 2013

Debt vs . AV 65,364,628 15,276 ,43 1 15 ,875,606

Debt Service vs. E ~ p e D d i t u r e s 2. 108.620 1.73 4 .700 7.080,533

DS to Expenditures - Cumu lative 2,108.620 3.84 3 ,320 10,923,853

2014

15,945,783

7.837.309

18,761 ,162

2015

16,384,404

10.778,400

29,539,562

» Using a 20 -year stTucture Debt Service vs . Expenditure is th e limiting factor. If the

growth in the budget slows further, the capacity will shrink.

» This assumes 0% growth 2012-2015 .

Prc:pared by: Oavenpon &: Company LLC

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 15/16

15

County Debt

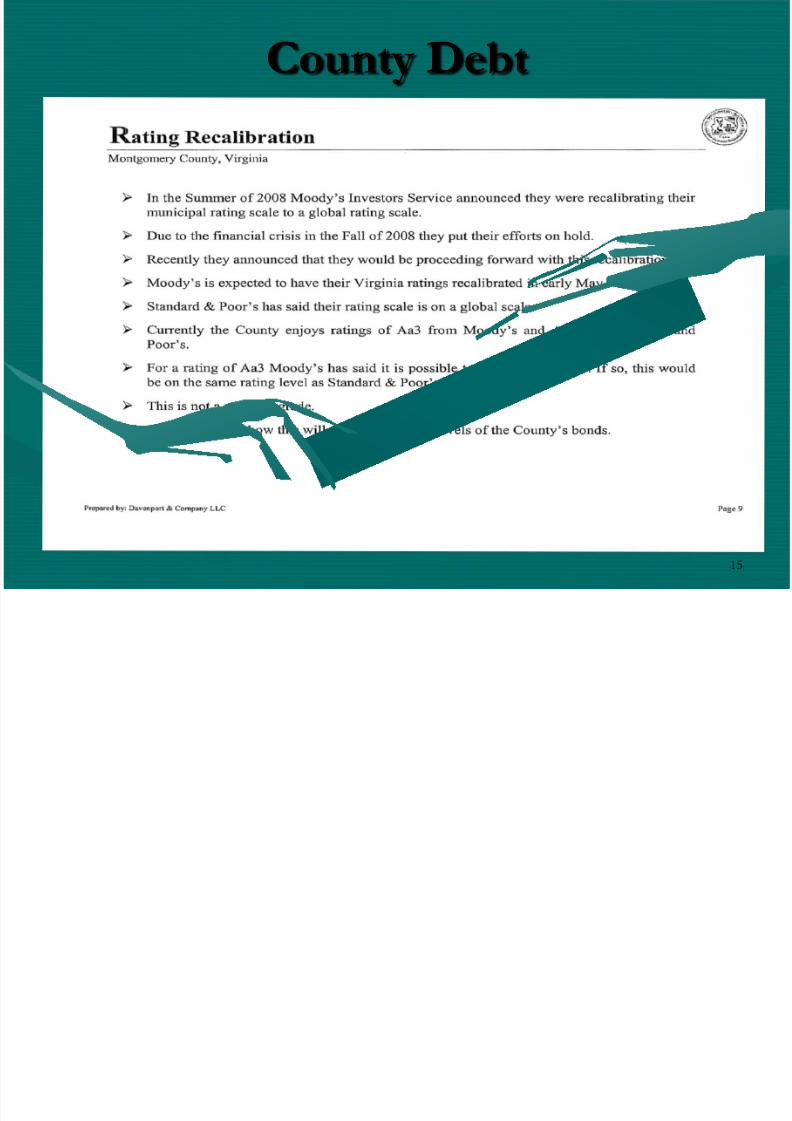

Rating RecalibrationMontgomery County, Virg inia

» In the Sununer of2008 Moody's Investors Service announced they were recalibrating their

municipal rating scale to a globa l rating scale.

» Due to the financial crisi s in the Fall of 2008 they put their effol1:s on hold.

» Recently they arul0wlced fuat they would be proceeding forward with this recalibration.

» Moody ' s is expected to have fueir Virginia ratings recalibrated in early May.

» Standard & Poor ' s has said their rating scale is on a global scale.

» Currently fue County enjoys ratings o f Aa3 from Moody's an d AA from Standard and

Poor's.

» For a rating of Aa3 Moody ' s has said it is possible to move up to a Aa2 . I f so , fuis would

be on th e same rating level as Standard & Poor 's .

» This is not a rating upgrade.

» I t is still unclear how tlus will affect fue trading le vels o f th e County's bonds .

Prep3rcd by: OGvc:npon & Company LLC Page 9

8/7/2019 SB School Financing Options Power Point) July 27 2010 (2)

http://slidepdf.com/reader/full/sb-school-financing-options-power-point-july-27-2010-2 16/16

16

School Financing Information

July 27, 2010