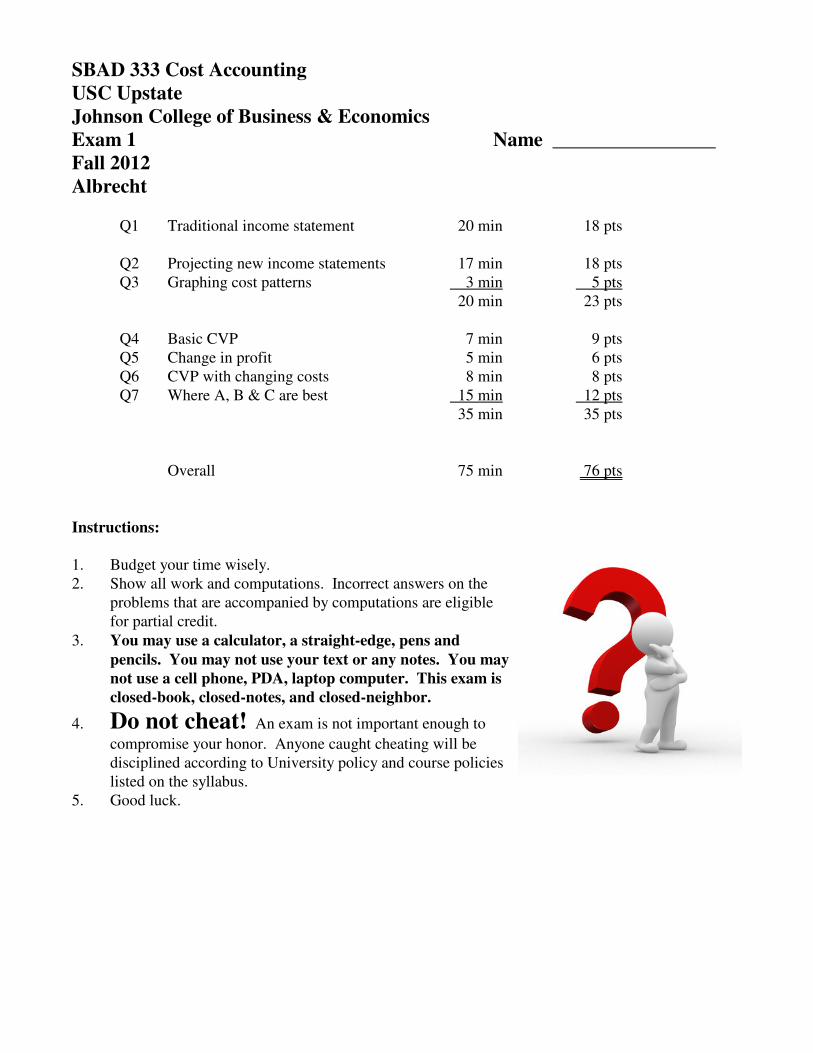

SBAD 333 Cost Accounting USC Upstate Johnson College of Business & Economics Exam 1 Name Fall 2012 Albrecht Q1 Traditional income statement 20 min 18 pts Q2 Projecting new income statements 17 min 18 pts Q3 Graphing cost patterns 3 min 5 pts 20 min 23 pts Q4 Basic CVP 7 min 9 pts Q5 Change in profit 5 min 6 pts Q6 CVP with changing costs 8 min 8 pts Q7 Where A, B & C are best 15 min 12 pts 35 min 35 pts Overall 75 min 76 pts Instructions: 1. Budget your time wisely. 2. Show all work and computations. Incorrect answers on the problems that are accompanied by computations are eligible for partial credit. 3. You may use a calculator, a straight-edge, pens and pencils. You may not use your text or any notes. You may not use a cell phone, PDA, laptop computer. This exam is closed-book, closed-notes, and closed-neighbor. 4. Do not cheat! An exam is not important enough to compromise your honor. Anyone caught cheating will be disciplined according to University policy and course policies listed on the syllabus. 5. Good luck.

Transcript

SBAD 333 Cost Accounting

USC Upstate

Johnson College of Business & Economics

Exam 1 Name

Fall 2012

Albrecht

Q1 Traditional income statement 20 min 18 pts

Q2 Projecting new income statements 17 min 18 ptsQ3 Graphing cost patterns 3 min 5 pts

20 min 23 pts

Q4 Basic CVP 7 min 9 ptsQ5 Change in profit 5 min 6 ptsQ6 CVP with changing costs 8 min 8 ptsQ7 Where A, B & C are best 15 min 12 pts

35 min 35 pts

Overall 75 min 76 pts

Instructions:

1. Budget your time wisely.2. Show all work and computations. Incorrect answers on the

problems that are accompanied by computations are eligiblefor partial credit.

3. You may use a calculator, a straight-edge, pens and

pencils. You may not use your text or any notes. You may

not use a cell phone, PDA, laptop computer. This exam is

closed-book, closed-notes, and closed-neighbor.

4. Do not cheat! An exam is not important enough to

compromise your honor. Anyone caught cheating will bedisciplined according to University policy and course policieslisted on the syllabus.

5. Good luck.

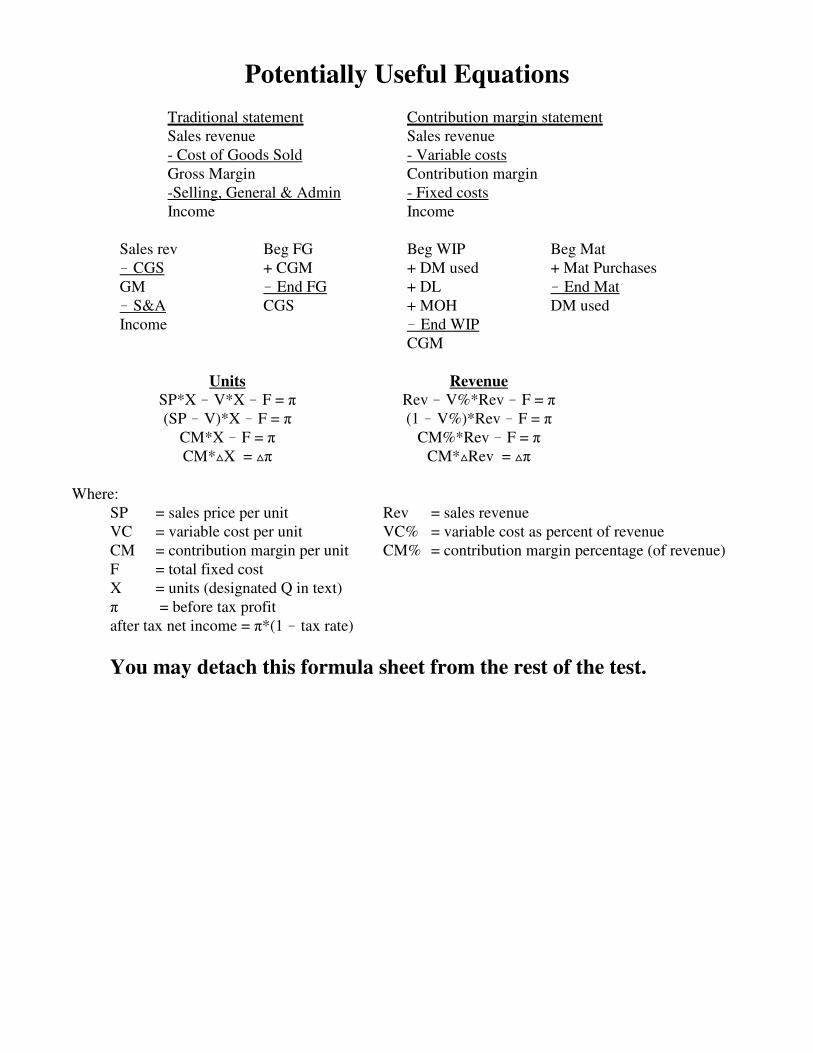

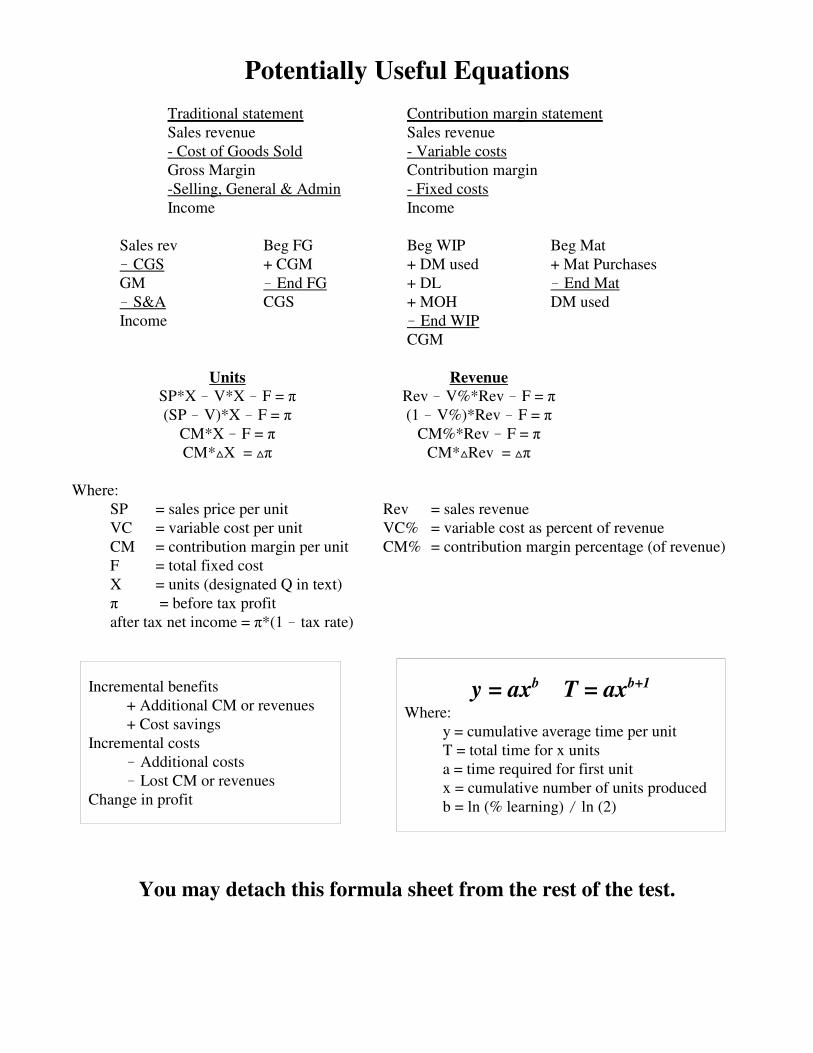

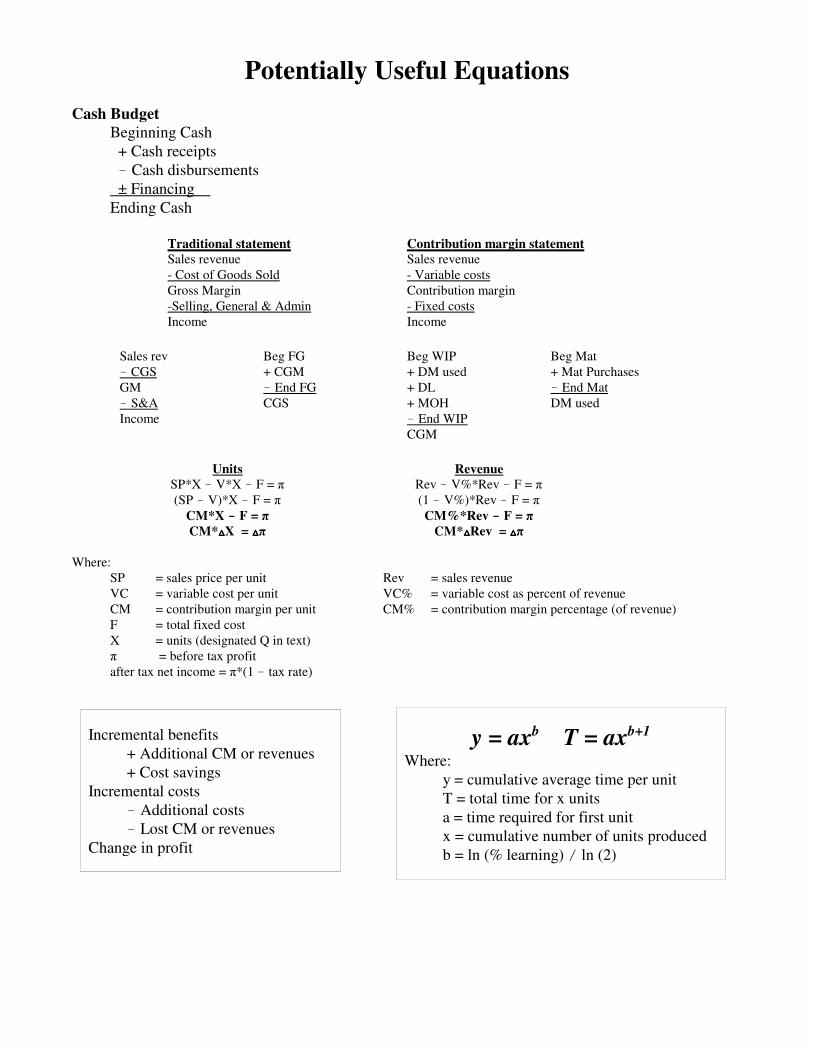

Potentially Useful Equations

Traditional statement Contribution margin statementSales revenue Sales revenue- Cost of Goods Sold - Variable costsGross Margin Contribution margin-Selling, General & Admin - Fixed costsIncome Income

Sales rev Beg FG Beg WIP Beg Mat! CGS + CGM + DM used + Mat PurchasesGM ! End FG + DL ! End Mat! S&A CGS + MOH DM usedIncome ! End WIP

CGM

Units Revenue

SP*X ! V*X ! F = π Rev ! V%*Rev ! F = π(SP ! V)*X ! F = π (1 ! V%)*Rev ! F = π

CM*X ! F = π CM%*Rev ! F = πCM*ªX = ªπ CM*ªRev = ªπ

Where:SP = sales price per unit Rev = sales revenueVC = variable cost per unit VC% = variable cost as percent of revenueCM = contribution margin per unit CM% = contribution margin percentage (of revenue)F = total fixed costX = units (designated Q in text)π = before tax profitafter tax net income = π*(1 ! tax rate)

You may detach this formula sheet from the rest of the test.

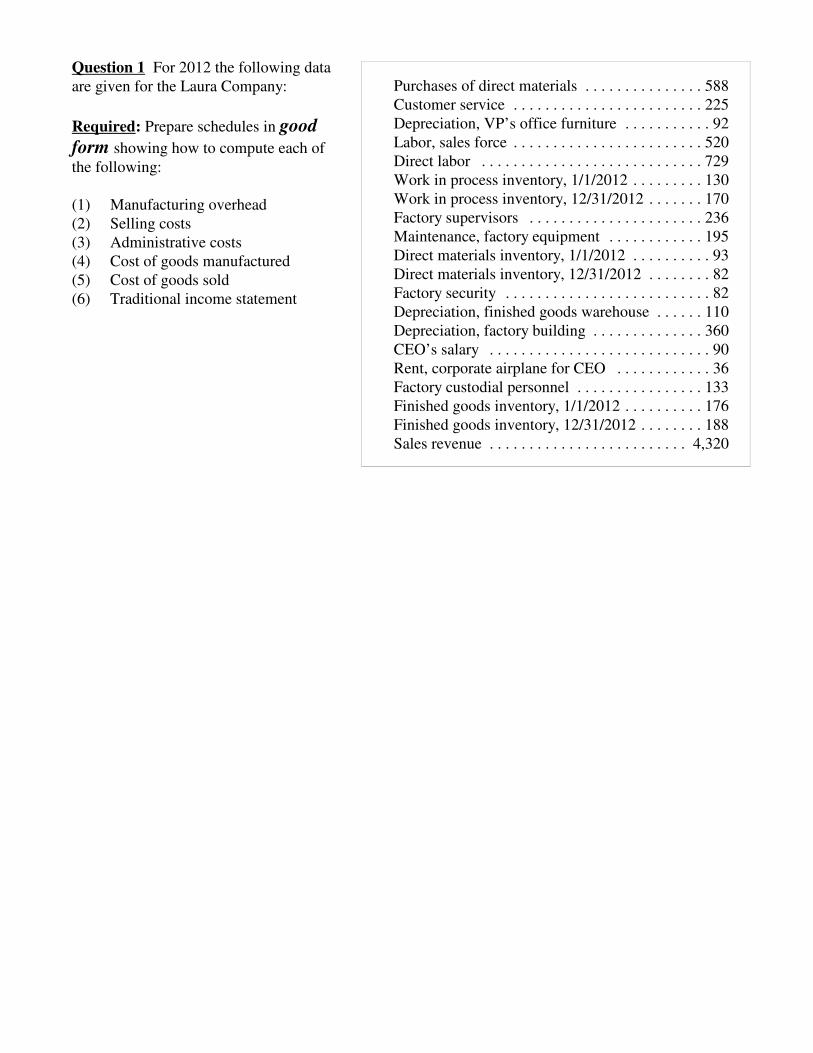

Question 1 For 2012 the following dataare given for the Laura Company:

Required: Prepare schedules in good

form showing how to compute each of

the following:

(1) Manufacturing overhead(2) Selling costs(3) Administrative costs(4) Cost of goods manufactured(5) Cost of goods sold(6) Traditional income statement

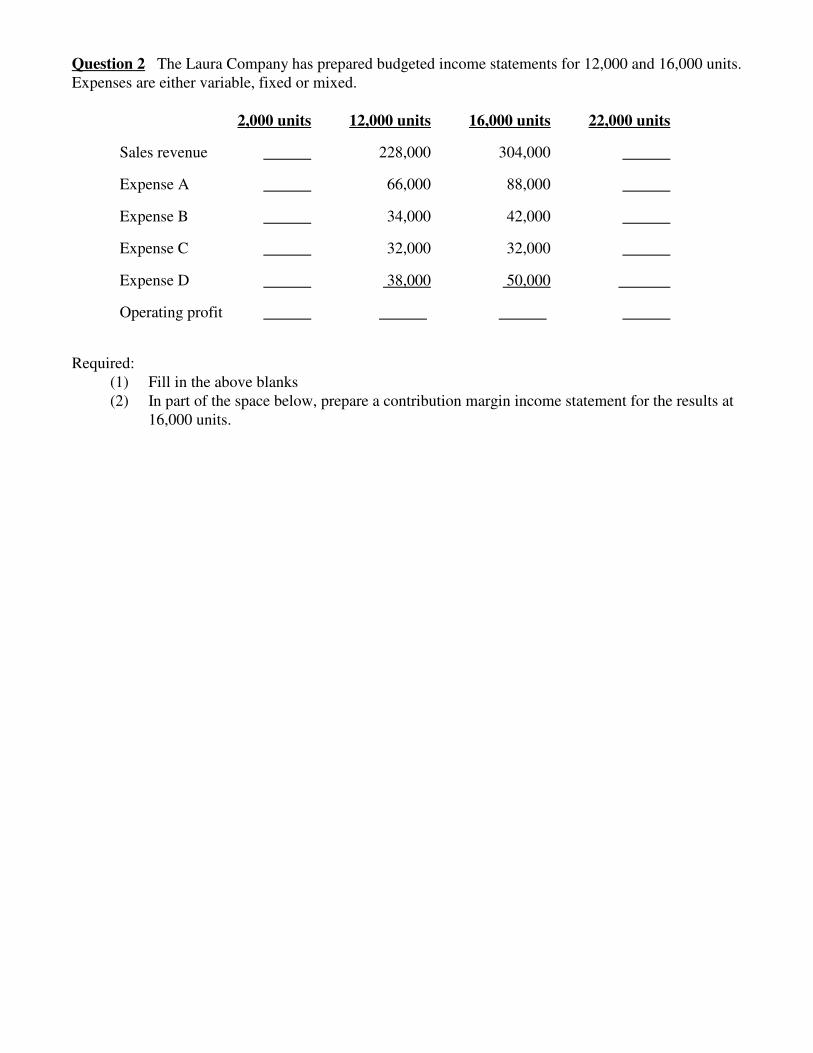

Question 2 The Laura Company has prepared budgeted income statements for 12,000 and 16,000 units. Expenses are either variable, fixed or mixed.

2,000 units 12,000 units 16,000 units 22,000 units

Sales revenue 228,000 304,000

Expense A 66,000 88,000

Expense B 34,000 42,000

Expense C 32,000 32,000

Expense D 38,000 50,000

Operating profit

Required:(1) Fill in the above blanks(2) In part of the space below, prepare a contribution margin income statement for the results at

16,000 units.

Question 3 The Nicolas Company incurs various types of costs. Create line graphs for the

following types of cost patterns on the graphs below. The lines do not need to be drawn to scale.

Your line graph should simply convey the proper shape of the line. The Y-axis (vertical) representstotal costs, the X-axis (horizontal) represents activity levels.

a. Cost of direct laborb. Initial fixed costs = $0. At 10,000 units, an investment in fixed cost of $20,000 is made.

For all units, the variable cost per unit is $3.

Question 4 The Chandler Company produces and sells super widgets. It projects the following revenueand costs for production and sales:

Sales price $17 per unitVariable cost $11 per unitFixed cost $68,532 total

Required:

(1) What is the break even point in units for Chandler's super widgets? Prepare a contributionmargin income statement to prove your answer.

(2) How many units in total are needed to generate a before tax profit of 20% of sales? Preparea contribution margin income statement to prove your answer.

(3) What is the change in profit going from 8,000 units to 12,200 units?

Clearly mark your answers with a circled number, Î, Ï, or Ð based on which part of the

question the answer is for.

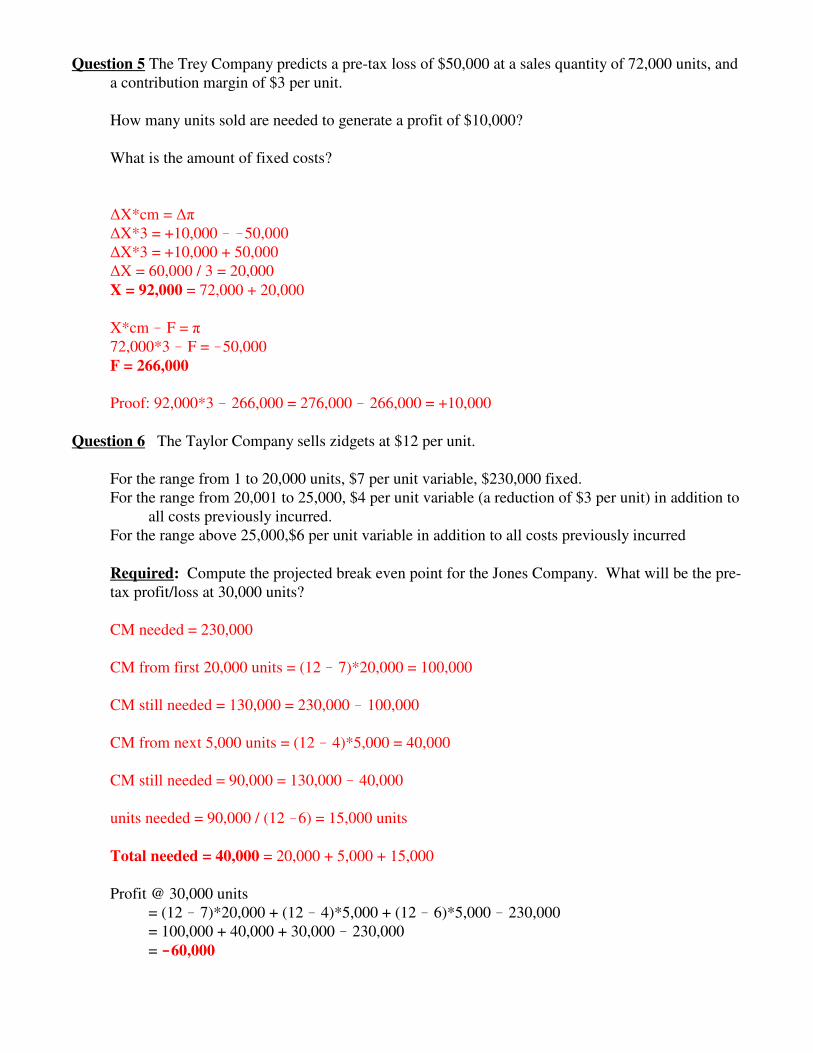

Question 5 The Trey Company predicts a pre-tax loss of $50,000 at a sales quantity of 72,000 units, anda contribution margin of $3 per unit.

How many units sold are needed to generate a profit of $10,000?

What is the amount of fixed costs?

Question 6 The Taylor Company sells zidgets at $12 per unit. The projectedcost structure varies depending on the relevant range.

For the range from 1 to 20,000 units, the cost structure for units producedand sold is expected to be $7 per unit variable, $230,000 fixed.

For the range from 20,001 to 25,000, the cost structure for units producedand sold is expected to be $4 per unit variable (a reduction of $3 perunit) in addition to all costs previously incurred.

For the range above 25,000, the cost structure for units produced and sold isexpected to be $6 per unit variable in addition to all costs previously incurred

Required: Compute the projected break even point for the Jones Company. What will be the pre-tax profit/loss at 30,000 units?

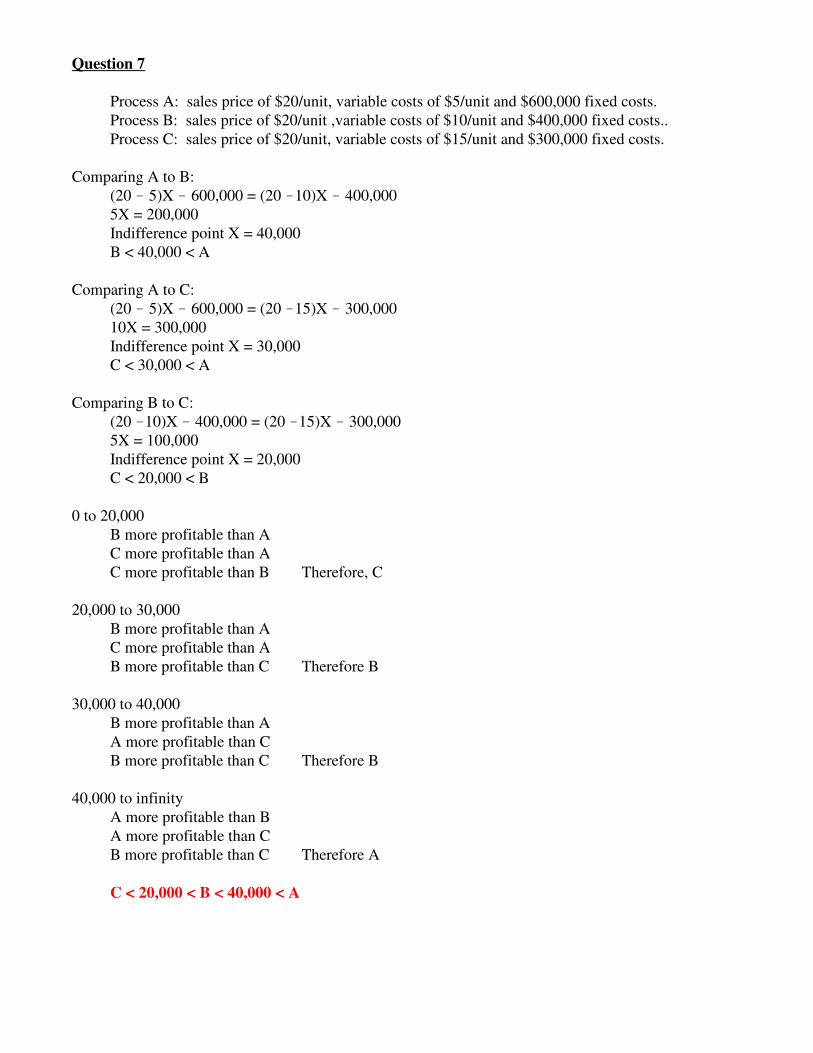

Question 7 The Jake Company is considering adopting one of three new processes to produce itsprimary product, Yidgets.

Process A: sales price of $20/unit, variable costs of $5/unit and $600,000 fixed costs.Process B: sales price of $20/unit ,variable costs of $10/unit and $400,000 fixed costs..Process C: sales price of $20/unit, variable costs of $15/unit and $300,000 fixed costs.

Required:

Which process is best at various parts of the relevant range? [Hint: you will need to computeindifference points between the various processes.]

SBAD 333 Cost Accounting

Exam 1

Fall 2012

Solutions

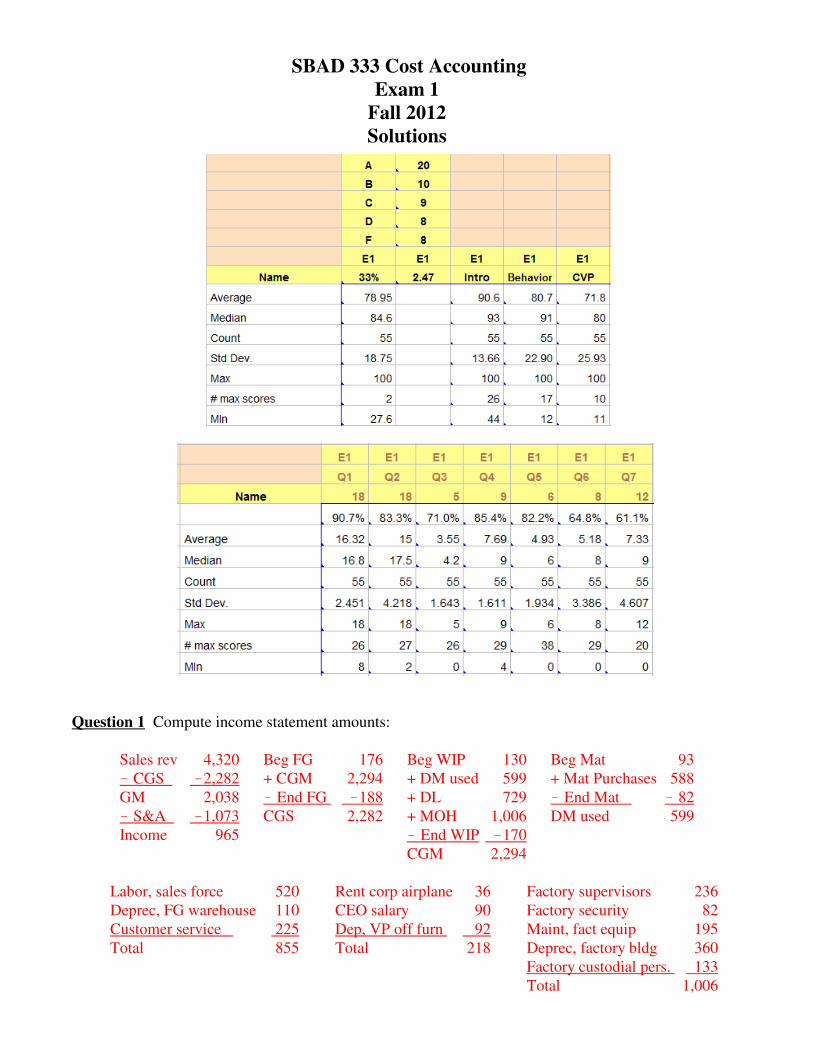

Question 1 Compute income statement amounts:

Sales rev 4,320 Beg FG 176 Beg WIP 130 Beg Mat 93! CGS !2,282 + CGM 2,294 + DM used 599 + Mat Purchases 588GM 2,038 ! End FG !188 + DL 729 ! End Mat ! 82! S&A !1,073 CGS 2,282 + MOH 1,006 DM used 599Income 965 ! End WIP !170

CGM 2,294

Labor, sales force 520 Rent corp airplane 36 Factory supervisors 236Deprec, FG warehouse 110 CEO salary 90 Factory security 82Customer service 225 Dep, VP off furn 92 Maint, fact equip 195Total 855 Total 218 Deprec, factory bldg 360 Factory custodial pers. 133

Total 1,006

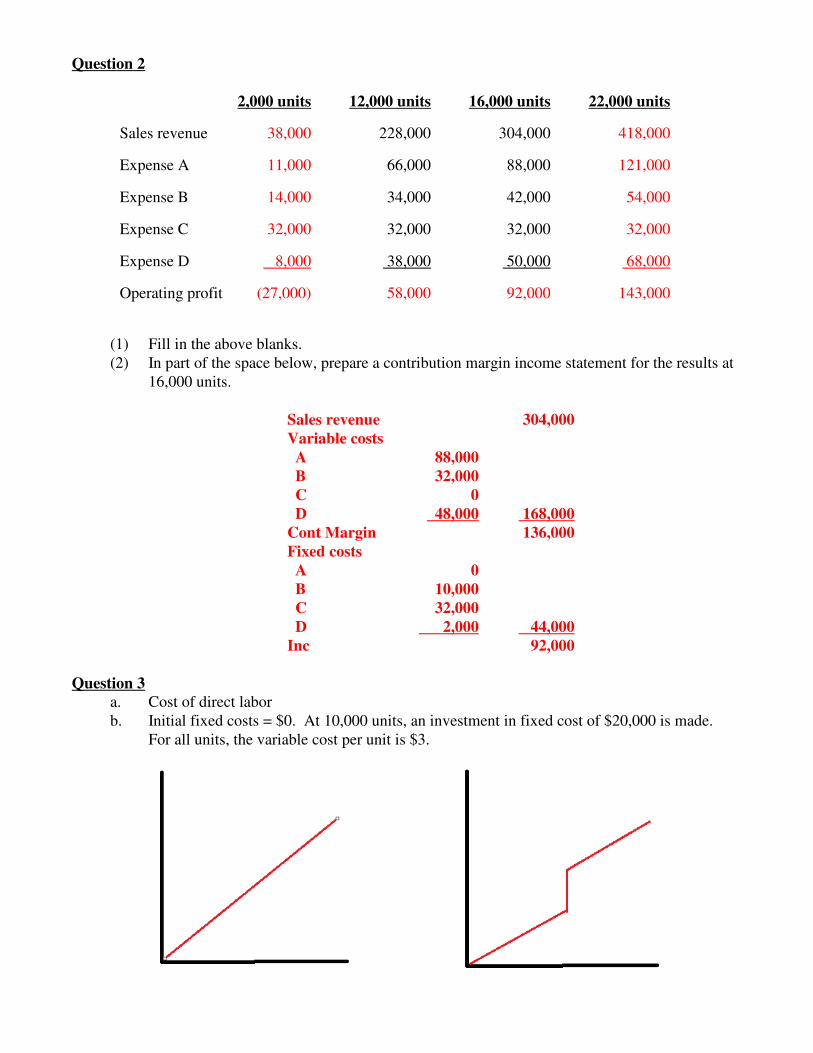

Question 2

2,000 units 12,000 units 16,000 units 22,000 units

Sales revenue 38,000 228,000 304,000 418,000

Expense A 11,000 66,000 88,000 121,000

Expense B 14,000 34,000 42,000 54,000

Expense C 32,000 32,000 32,000 32,000

Expense D 8,000 38,000 50,000 68,000

Operating profit (27,000) 58,000 92,000 143,000

(1) Fill in the above blanks.(2) In part of the space below, prepare a contribution margin income statement for the results at

16,000 units.

Sales revenue 304,000

Variable costs

A 88,000

B 32,000

C 0

D 48,000 168,000

Cont Margin 136,000

Fixed costs

A 0

B 10,000

C 32,000

D 2,000 44,000

Inc 92,000

Question 3

a. Cost of direct laborb. Initial fixed costs = $0. At 10,000 units, an investment in fixed cost of $20,000 is made.

For all units, the variable cost per unit is $3.

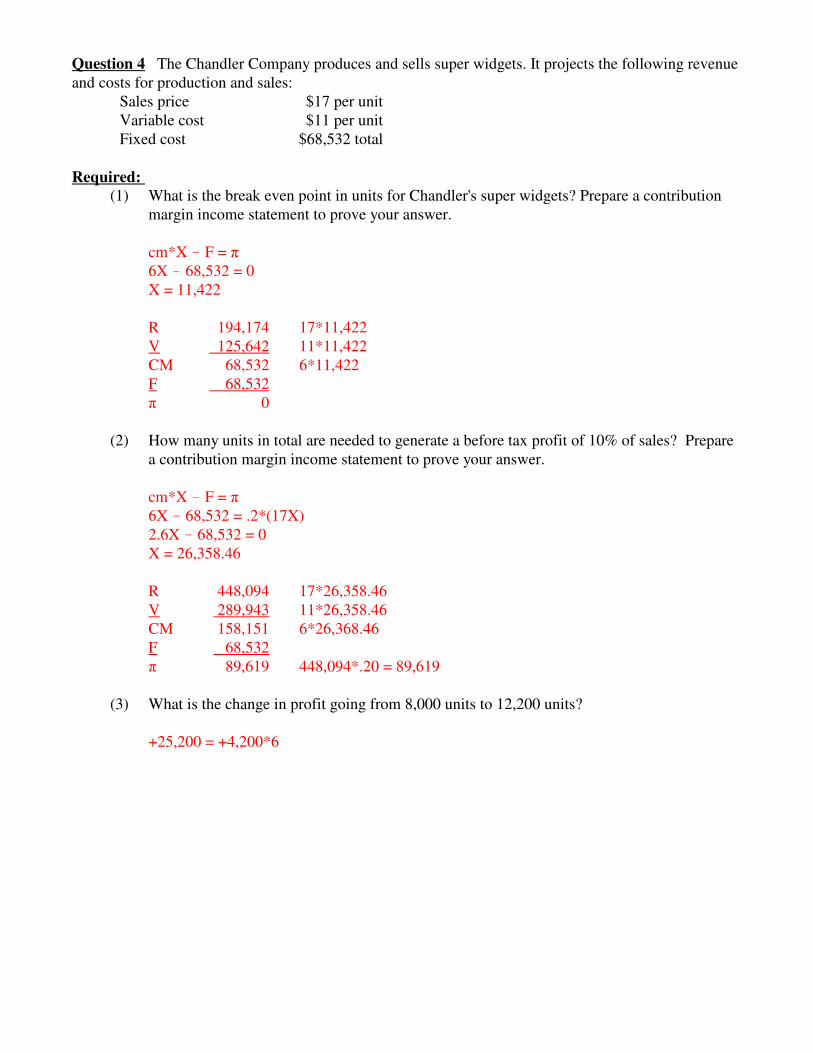

Question 4 The Chandler Company produces and sells super widgets. It projects the following revenueand costs for production and sales:

Sales price $17 per unitVariable cost $11 per unitFixed cost $68,532 total

Required:

(1) What is the break even point in units for Chandler's super widgets? Prepare a contributionmargin income statement to prove your answer.

cm*X ! F = π6X ! 68,532 = 0X = 11,422

R 194,174 17*11,422V 125,642 11*11,422CM 68,532 6*11,422F 68,532π 0

(2) How many units in total are needed to generate a before tax profit of 10% of sales? Preparea contribution margin income statement to prove your answer.

Question 6 The Taylor Company sells zidgets at $12 per unit.

For the range from 1 to 20,000 units, $7 per unit variable, $230,000 fixed. For the range from 20,001 to 25,000, $4 per unit variable (a reduction of $3 per unit) in addition to

all costs previously incurred.For the range above 25,000,$6 per unit variable in addition to all costs previously incurred

Required: Compute the projected break even point for the Jones Company. What will be the pre-tax profit/loss at 30,000 units?

CM needed = 230,000

CM from first 20,000 units = (12 ! 7)*20,000 = 100,000

CM still needed = 130,000 = 230,000 ! 100,000

CM from next 5,000 units = (12 ! 4)*5,000 = 40,000

Process A: sales price of $20/unit, variable costs of $5/unit and $600,000 fixed costs.Process B: sales price of $20/unit ,variable costs of $10/unit and $400,000 fixed costs..Process C: sales price of $20/unit, variable costs of $15/unit and $300,000 fixed costs.

Comparing A to B:(20 ! 5)X ! 600,000 = (20 !10)X ! 400,0005X = 200,000Indifference point X = 40,000B < 40,000 < A

Comparing A to C:(20 ! 5)X ! 600,000 = (20 !15)X ! 300,00010X = 300,000Indifference point X = 30,000C < 30,000 < A

Comparing B to C:(20 !10)X ! 400,000 = (20 !15)X ! 300,0005X = 100,000Indifference point X = 20,000C < 20,000 < B

0 to 20,000B more profitable than AC more profitable than AC more profitable than B Therefore, C

20,000 to 30,000B more profitable than AC more profitable than AB more profitable than C Therefore B

30,000 to 40,000B more profitable than AA more profitable than CB more profitable than C Therefore B

40,000 to infinityA more profitable than BA more profitable than CB more profitable than C Therefore A

C < 20,000 < B < 40,000 < A

SBAD 333 Cost Accounting by Albrecht

USC Upstate

Johnson College of Business & Economics

Exam 2 Name

Fall 2012

Q1 Change in profit 10 min 10 ptsQ2 CVP with changing costs 10 min 8 pts

15 min 16 pts

Q3 Continue or discontinue 10 min 14 ptsQ4 Special order 20 min 30 pts

30 min 44 pts

Q5 Learning curve–marginal blocks 10 min 8 ptsQ6 Learning curve–estimate parameters 15 min 15 pts

25 min 23 pts

Overall 65 min 77 pts

Instructions:

1. Budget your time wisely.2. Show all work and computations. Incorrect answers on

the problems that are accompanied by computations areeligible for partial credit.

3. You may use a calculator, a straight-edge, pens and

pencils. You may not use your text or any notes. You

may not use a cell phone, PDA, laptop computer. This

exam is closed-book, closed-notes, and closed-neighbor.

4. Do not cheat! An exam is not important enough to compromise your honor. Anyone

caught cheating will be disciplined according to University policy and course policies listed on thesyllabus.

5. Good luck.

Potentially Useful Equations

Traditional statement Contribution margin statementSales revenue Sales revenue- Cost of Goods Sold - Variable costsGross Margin Contribution margin-Selling, General & Admin - Fixed costsIncome Income

Sales rev Beg FG Beg WIP Beg Mat! CGS + CGM + DM used + Mat PurchasesGM ! End FG + DL ! End Mat! S&A CGS + MOH DM usedIncome ! End WIP

CGM

Units Revenue

SP*X ! V*X ! F = π Rev ! V%*Rev ! F = π(SP ! V)*X ! F = π (1 ! V%)*Rev ! F = π

CM*X ! F = π CM%*Rev ! F = πCM*ªX = ªπ CM*ªRev = ªπ

Where:SP = sales price per unit Rev = sales revenueVC = variable cost per unit VC% = variable cost as percent of revenueCM = contribution margin per unit CM% = contribution margin percentage (of revenue)F = total fixed costX = units (designated Q in text)π = before tax profitafter tax net income = π*(1 ! tax rate)

You may detach this formula sheet from the rest of the test.

Incremental benefits+ Additional CM or revenues+ Cost savings

Incremental costs! Additional costs! Lost CM or revenues

Change in profit

y = axb T = axb+1

Where:y = cumulative average time per unitT = total time for x unitsa = time required for first unitx = cumulative number of units producedb = ln (% learning) / ln (2)

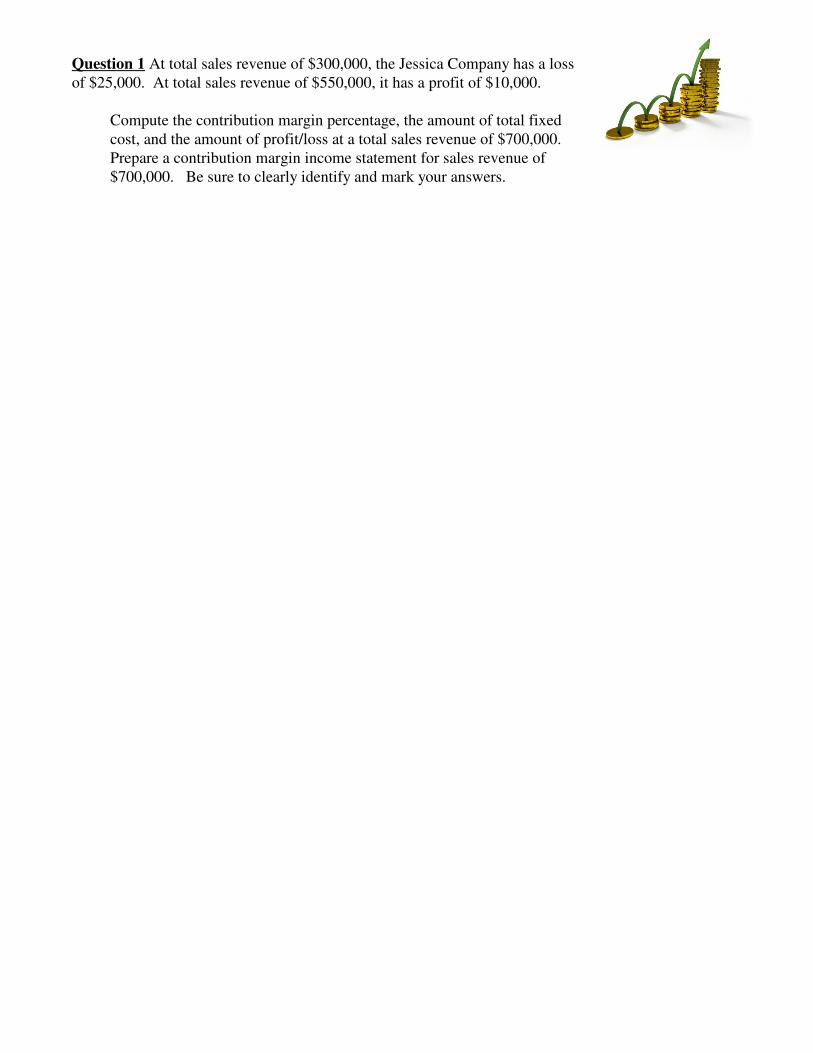

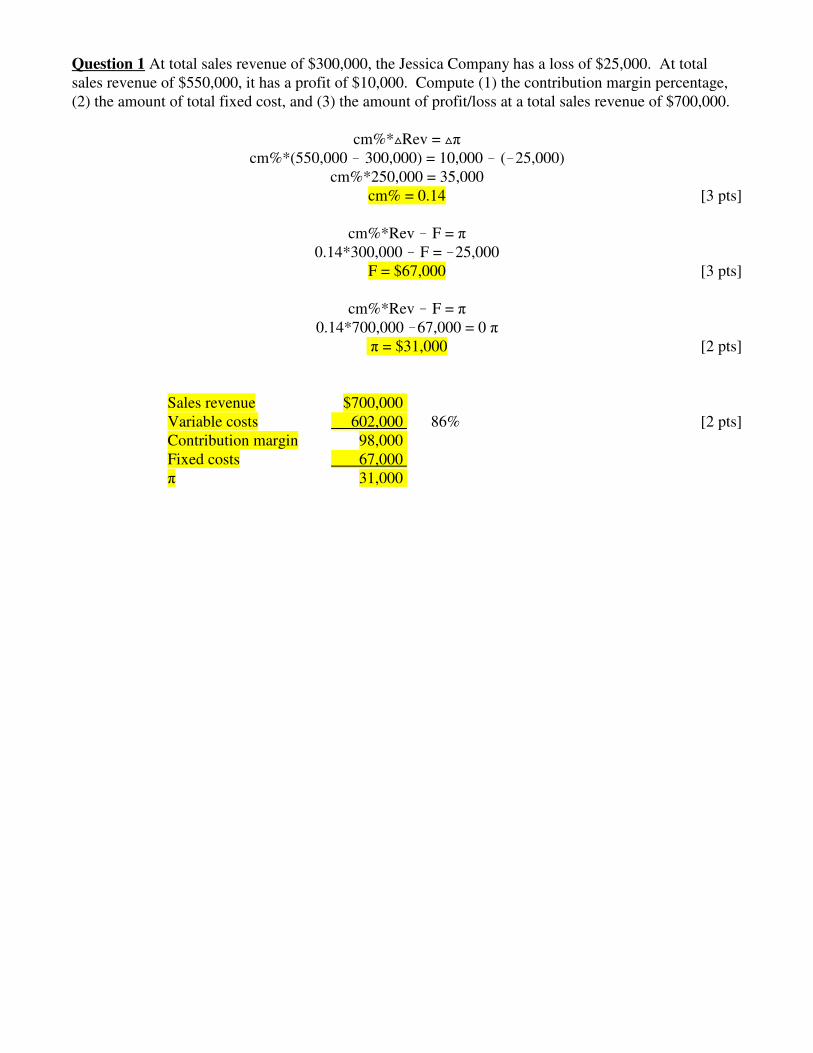

Question 1 At total sales revenue of $300,000, the Jessica Company has a lossof $25,000. At total sales revenue of $550,000, it has a profit of $10,000.

Compute the contribution margin percentage, the amount of total fixedcost, and the amount of profit/loss at a total sales revenue of $700,000. Prepare a contribution margin income statement for sales revenue of$700,000. Be sure to clearly identify and mark your answers.

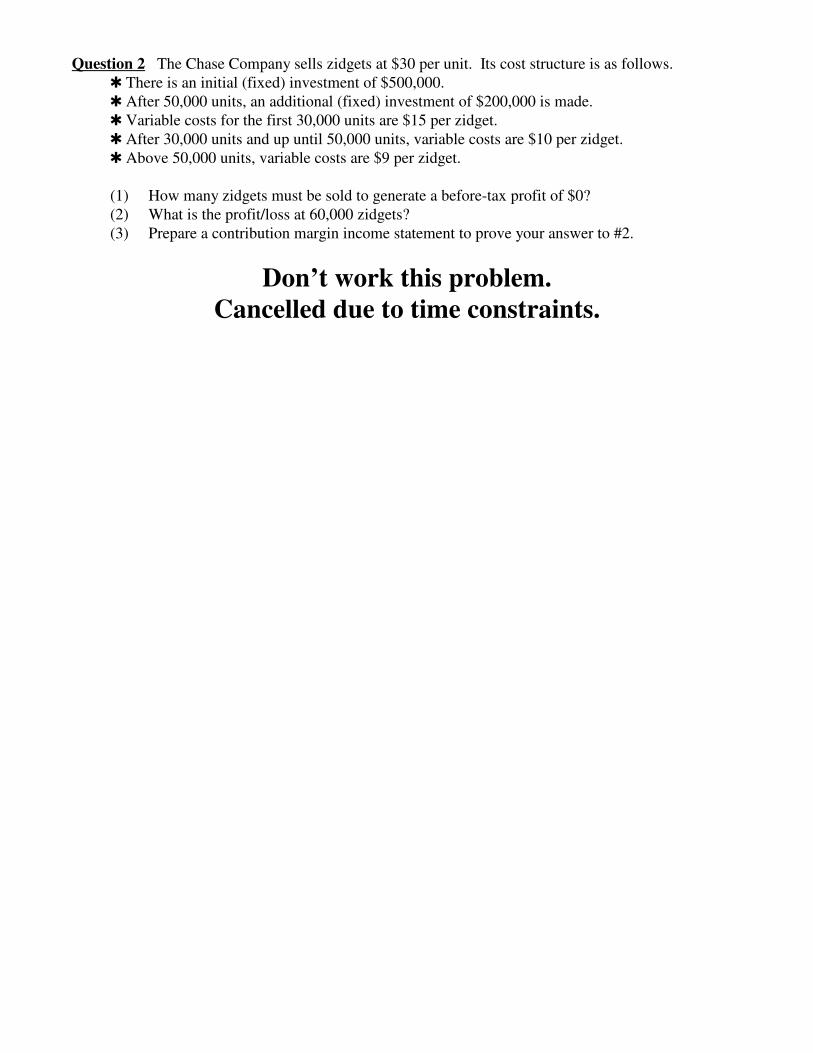

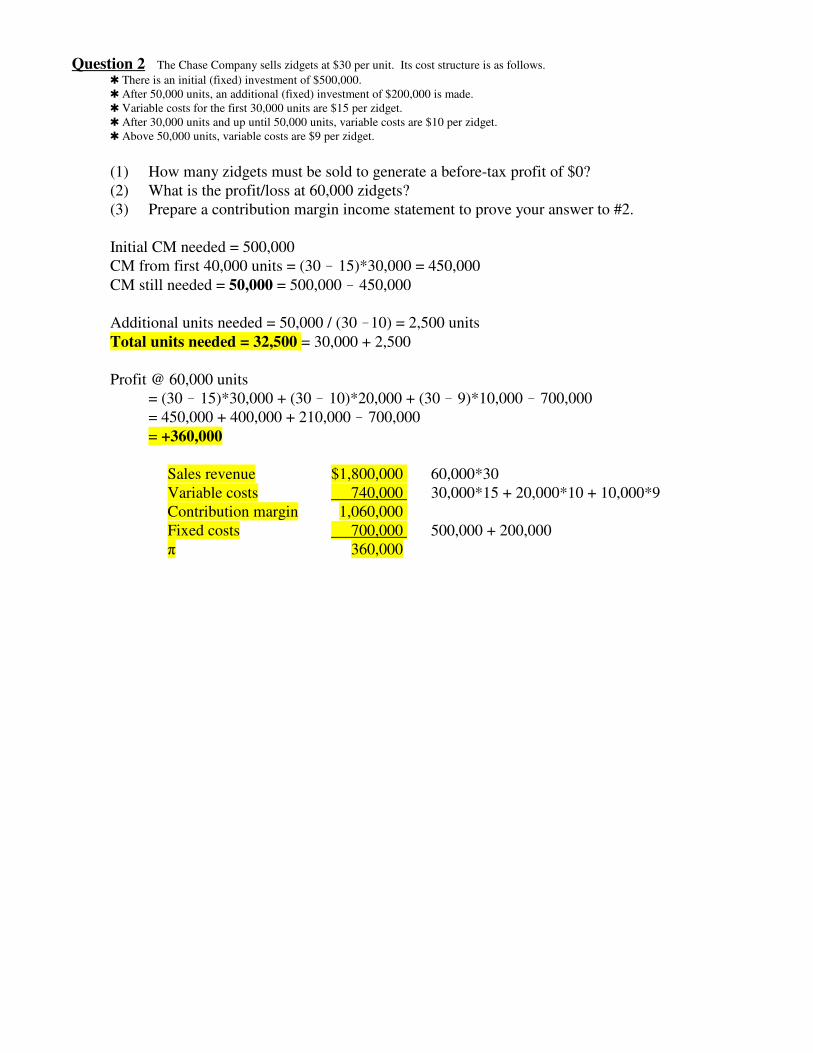

Question 2 The Chase Company sells zidgets at $30 per unit. Its cost structure is as follows. r There is an initial (fixed) investment of $500,000. r After 50,000 units, an additional (fixed) investment of $200,000 is made. r Variable costs for the first 30,000 units are $15 per zidget. r After 30,000 units and up until 50,000 units, variable costs are $10 per zidget. r Above 50,000 units, variable costs are $9 per zidget.

(1) How many zidgets must be sold to generate a before-tax profit of $0?(2) What is the profit/loss at 60,000 zidgets?(3) Prepare a contribution margin income statement to prove your answer to #2.

Don’t work this problem.

Cancelled due to time constraints.

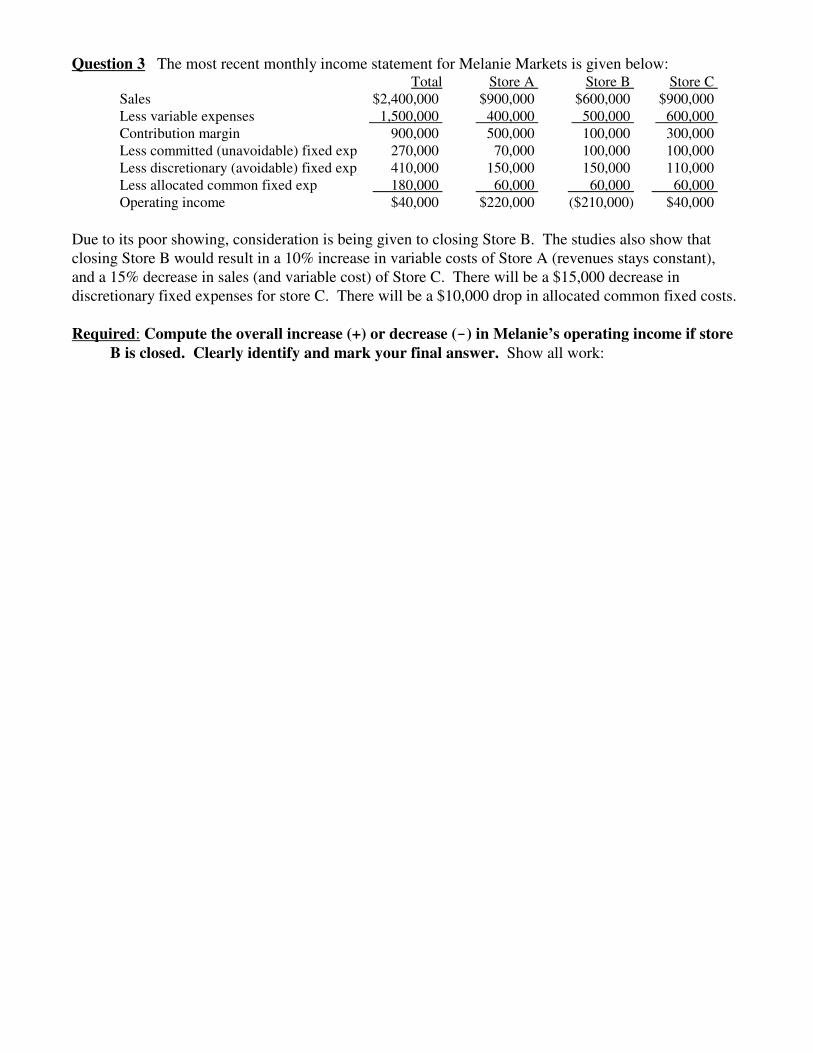

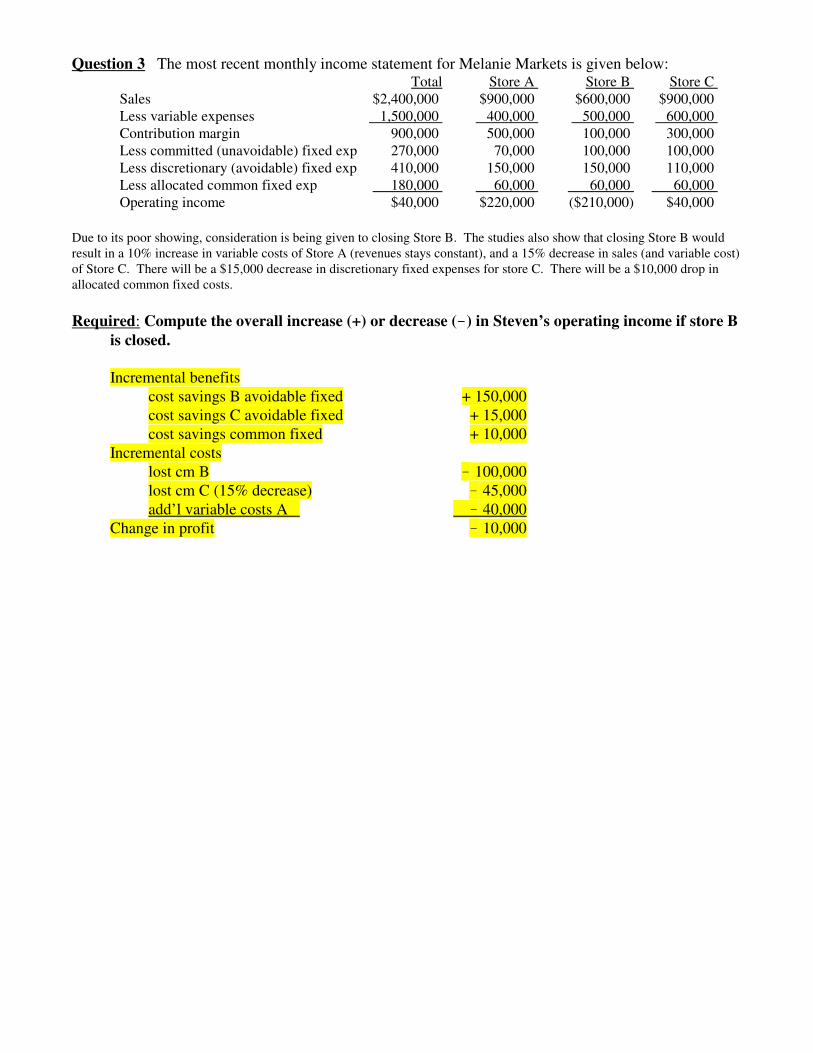

Question 3 The most recent monthly income statement for Melanie Markets is given below:Total Store A Store B Store C

Sales $2,400,000 $900,000 $600,000 $900,000 Less variable expenses 1,500,000 400,000 500,000 600,000 Contribution margin 900,000 500,000 100,000 300,000 Less committed (unavoidable) fixed exp 270,000 70,000 100,000 100,000 Less discretionary (avoidable) fixed exp 410,000 150,000 150,000 110,000 Less allocated common fixed exp 180,000 60,000 60,000 60,000 Operating income $40,000 $220,000 ($210,000) $40,000

Due to its poor showing, consideration is being given to closing Store B. The studies also show thatclosing Store B would result in a 10% increase in variable costs of Store A (revenues stays constant),and a 15% decrease in sales (and variable cost) of Store C. There will be a $15,000 decrease indiscretionary fixed expenses for store C. There will be a $10,000 drop in allocated common fixed costs.

Required: Compute the overall increase (+) or decrease (!!!!) in Melanie’s operating income if store

B is closed. Clearly identify and mark your final answer. Show all work:

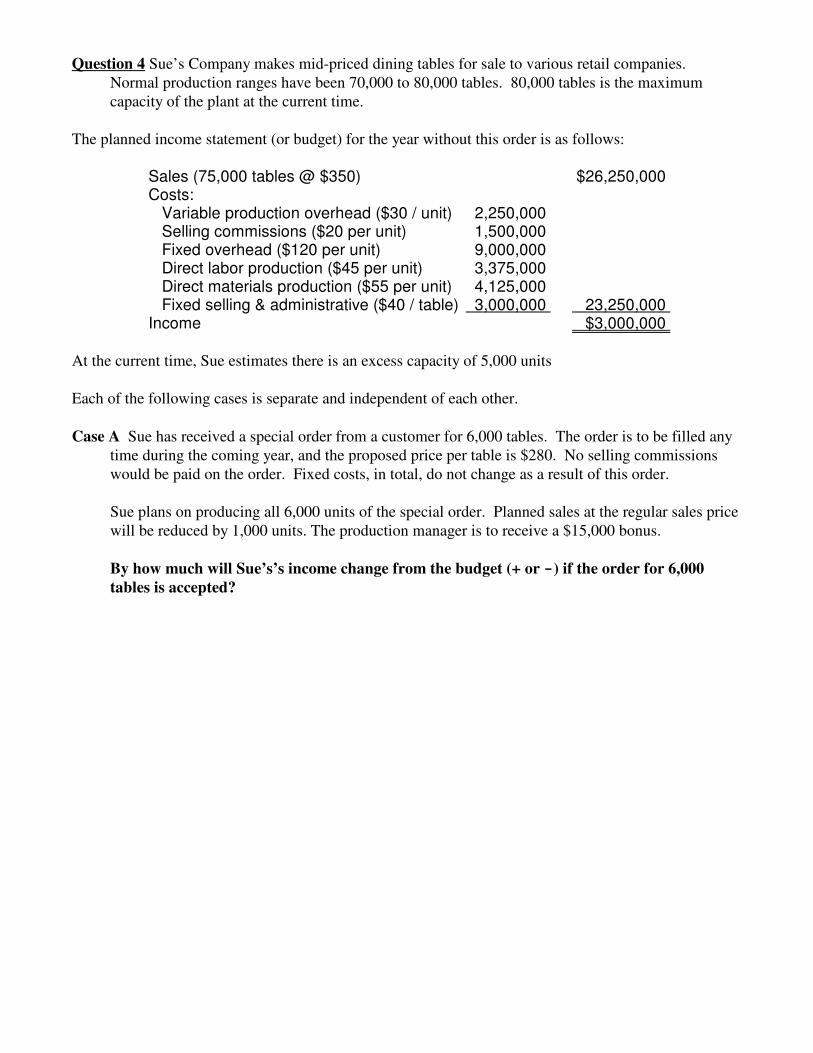

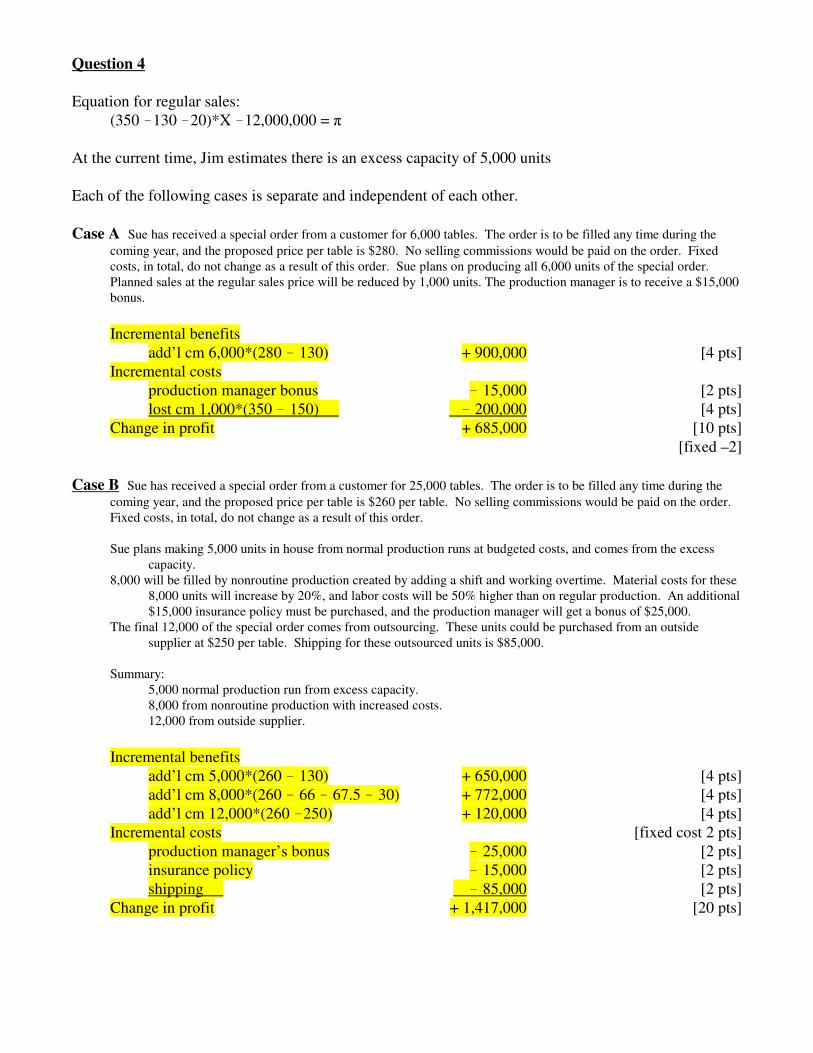

Question 4 Sue’s Company makes mid-priced dining tables for sale to various retail companies. Normal production ranges have been 70,000 to 80,000 tables. 80,000 tables is the maximumcapacity of the plant at the current time.

The planned income statement (or budget) for the year without this order is as follows:

Sales (75,000 tables @ $350) $26,250,000 Costs: Variable production overhead ($30 / unit) 2,250,000 Selling commissions ($20 per unit) 1,500,000 Fixed overhead ($120 per unit) 9,000,000 Direct labor production ($45 per unit) 3,375,000 Direct materials production ($55 per unit) 4,125,000 Fixed selling & administrative ($40 / table) 3,000,000 23,250,000 Income $3,000,000

At the current time, Sue estimates there is an excess capacity of 5,000 units

Each of the following cases is separate and independent of each other.

Case A Sue has received a special order from a customer for 6,000 tables. The order is to be filled anytime during the coming year, and the proposed price per table is $280. No selling commissionswould be paid on the order. Fixed costs, in total, do not change as a result of this order.

Sue plans on producing all 6,000 units of the special order. Planned sales at the regular sales pricewill be reduced by 1,000 units. The production manager is to receive a $15,000 bonus.

By how much will Sue’s’s income change from the budget (+ or !!!!) if the order for 6,000

tables is accepted?

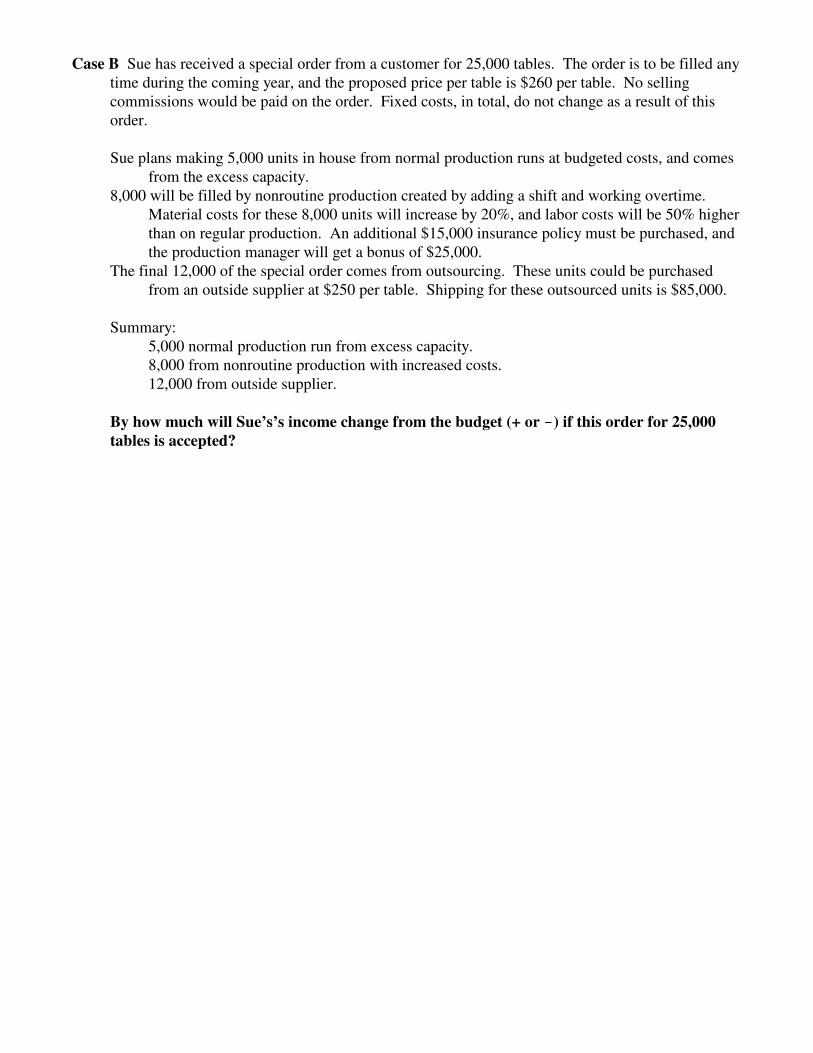

Case B Sue has received a special order from a customer for 25,000 tables. The order is to be filled anytime during the coming year, and the proposed price per table is $260 per table. No sellingcommissions would be paid on the order. Fixed costs, in total, do not change as a result of thisorder.

Sue plans making 5,000 units in house from normal production runs at budgeted costs, and comesfrom the excess capacity.

8,000 will be filled by nonroutine production created by adding a shift and working overtime. Material costs for these 8,000 units will increase by 20%, and labor costs will be 50% higherthan on regular production. An additional $15,000 insurance policy must be purchased, andthe production manager will get a bonus of $25,000.

The final 12,000 of the special order comes from outsourcing. These units could be purchasedfrom an outside supplier at $250 per table. Shipping for these outsourced units is $85,000.

Summary:5,000 normal production run from excess capacity.8,000 from nonroutine production with increased costs.12,000 from outside supplier.

By how much will Sue’s’s income change from the budget (+ or !!!!) if this order for 25,000

tables is accepted?

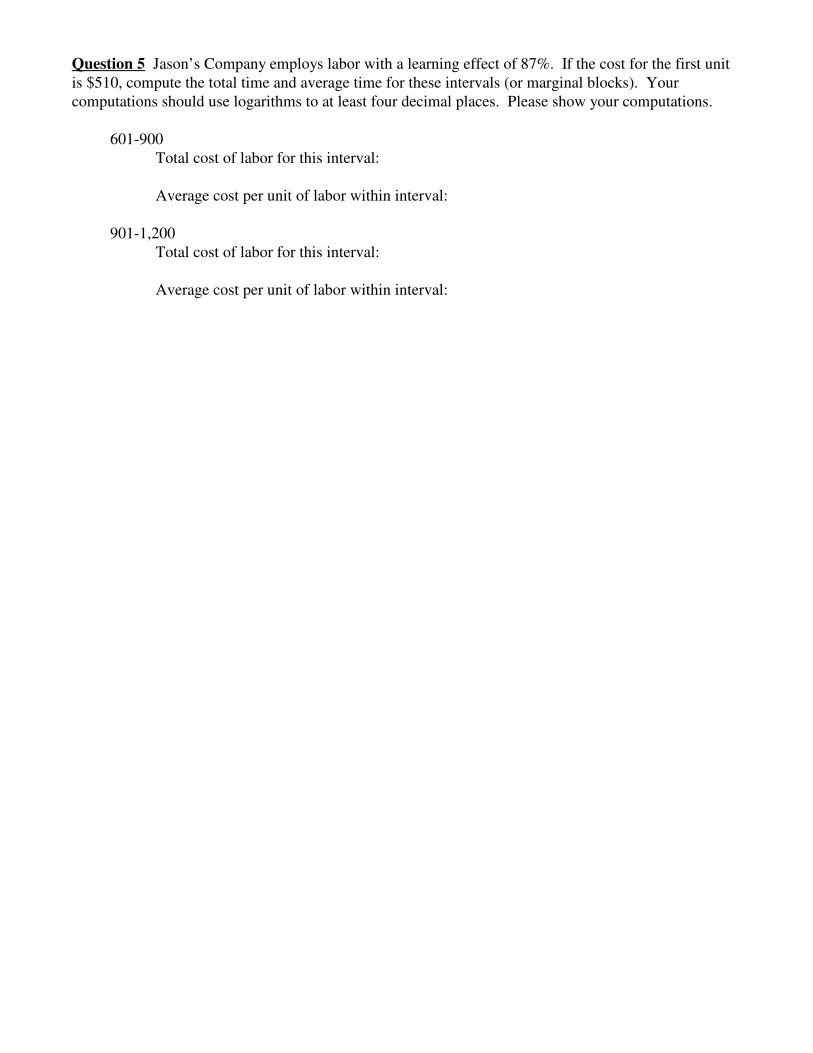

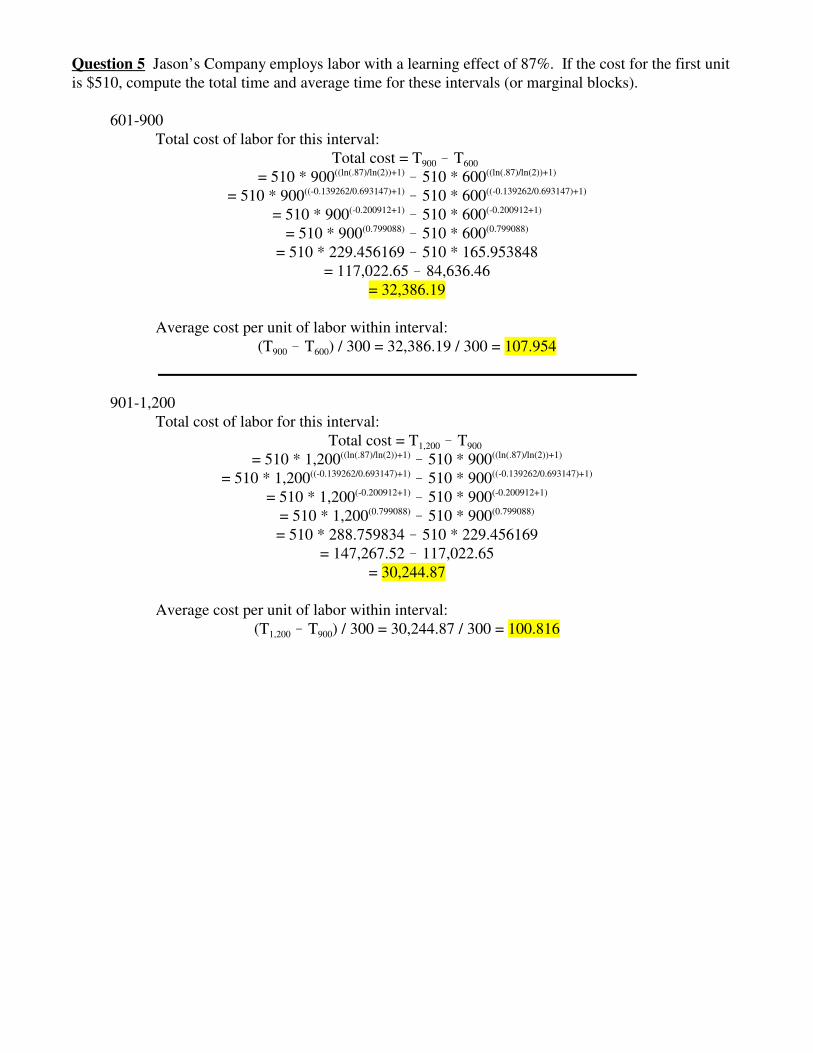

Question 5 Jason’s Company employs labor with a learning effect of 87%. If the cost for the first unitis $510, compute the total time and average time for these intervals (or marginal blocks). Yourcomputations should use logarithms to at least four decimal places. Please show your computations.

601-900Total cost of labor for this interval:

Average cost per unit of labor within interval:

901-1,200Total cost of labor for this interval:

Average cost per unit of labor within interval:

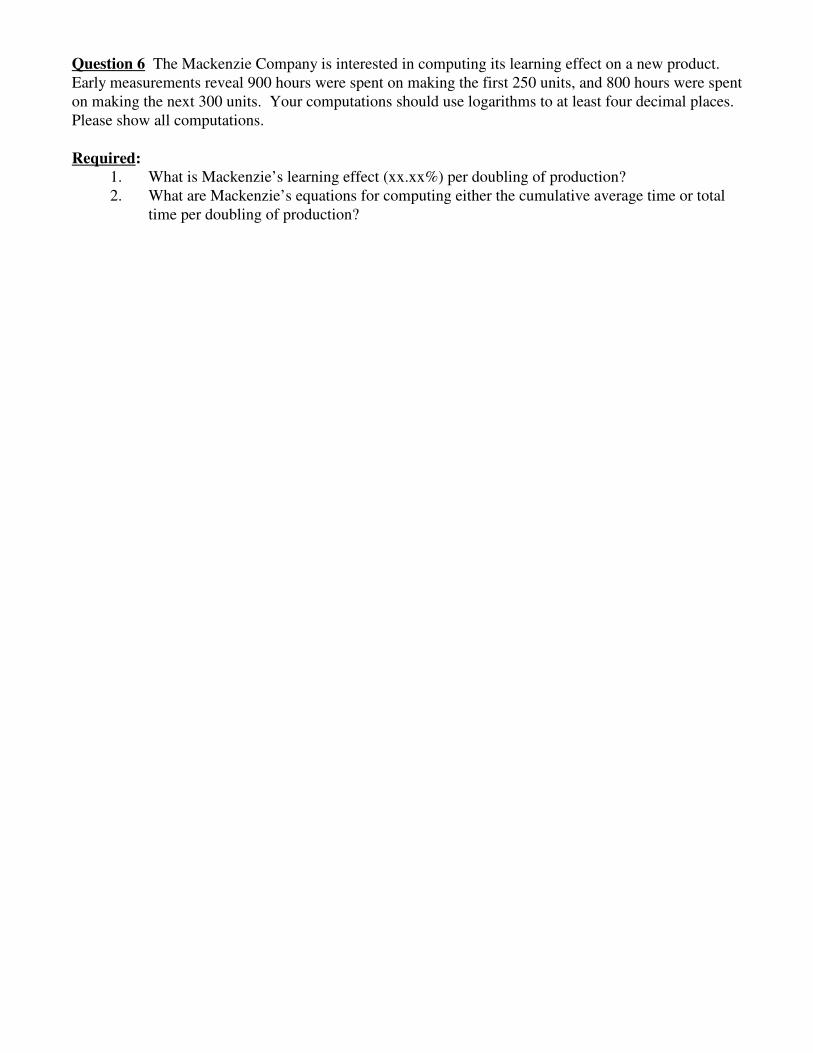

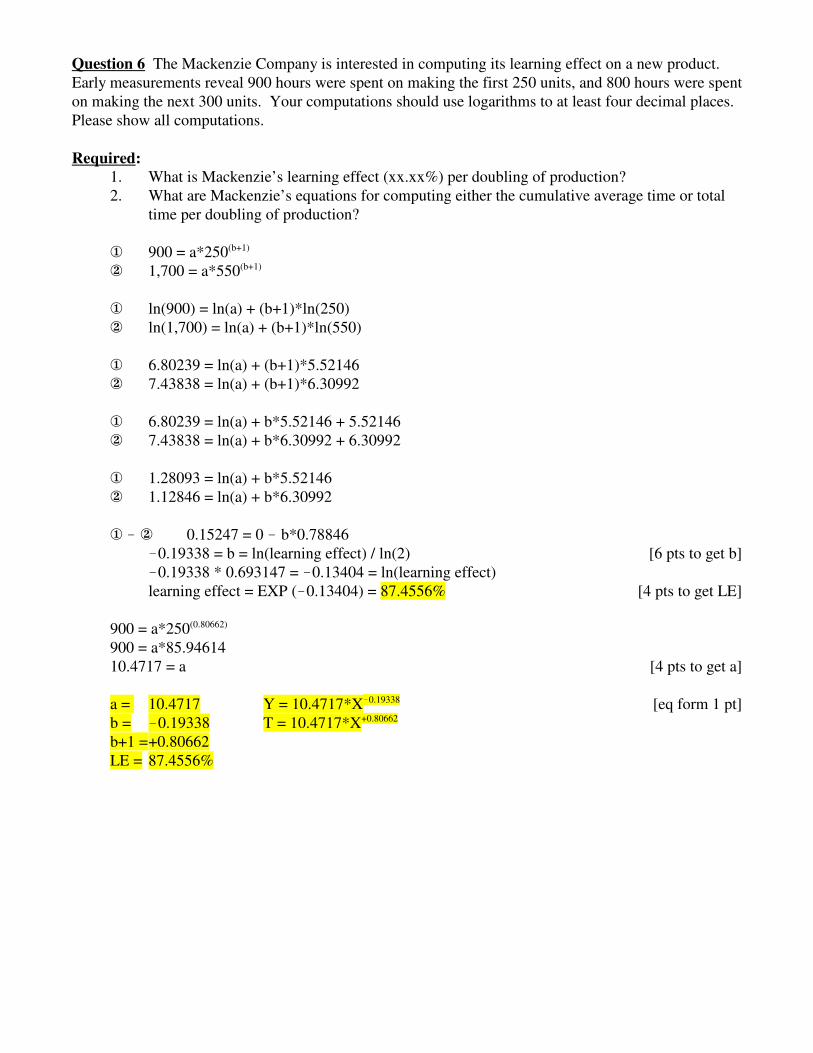

Question 6 The Mackenzie Company is interested in computing its learning effect on a new product. Early measurements reveal 900 hours were spent on making the first 250 units, and 800 hours were spenton making the next 300 units. Your computations should use logarithms to at least four decimal places. Please show all computations.

Required:

1. What is Mackenzie’s learning effect (xx.xx%) per doubling of production?2. What are Mackenzie’s equations for computing either the cumulative average time or total

time per doubling of production?

SBAD 333 Cost Accounting

Exam 2

Fall 2012

Solutions

Question 1 At total sales revenue of $300,000, the Jessica Company has a loss of $25,000. At totalsales revenue of $550,000, it has a profit of $10,000. Compute (1) the contribution margin percentage,(2) the amount of total fixed cost, and (3) the amount of profit/loss at a total sales revenue of $700,000.

Question 2 The Chase Company sells zidgets at $30 per unit. Its cost structure is as follows.

r There is an initial (fixed) investment of $500,000. r After 50,000 units, an additional (fixed) investment of $200,000 is made. r Variable costs for the first 30,000 units are $15 per zidget. r After 30,000 units and up until 50,000 units, variable costs are $10 per zidget. r Above 50,000 units, variable costs are $9 per zidget.

(1) How many zidgets must be sold to generate a before-tax profit of $0?(2) What is the profit/loss at 60,000 zidgets?(3) Prepare a contribution margin income statement to prove your answer to #2.

Initial CM needed = 500,000CM from first 40,000 units = (30 ! 15)*30,000 = 450,000

CM still needed = 50,000 = 500,000 ! 450,000

Additional units needed = 50,000 / (30 !10) = 2,500 units

Question 3 The most recent monthly income statement for Melanie Markets is given below:Total Store A Store B Store C

Sales $2,400,000 $900,000 $600,000 $900,000 Less variable expenses 1,500,000 400,000 500,000 600,000 Contribution margin 900,000 500,000 100,000 300,000 Less committed (unavoidable) fixed exp 270,000 70,000 100,000 100,000 Less discretionary (avoidable) fixed exp 410,000 150,000 150,000 110,000 Less allocated common fixed exp 180,000 60,000 60,000 60,000 Operating income $40,000 $220,000 ($210,000) $40,000

Due to its poor showing, consideration is being given to closing Store B. The studies also show that closing Store B wouldresult in a 10% increase in variable costs of Store A (revenues stays constant), and a 15% decrease in sales (and variable cost)of Store C. There will be a $15,000 decrease in discretionary fixed expenses for store C. There will be a $10,000 drop inallocated common fixed costs.

Required: Compute the overall increase (+) or decrease (!!!!) in Steven’s operating income if store B

is closed.

Incremental benefitscost savings B avoidable fixed + 150,000cost savings C avoidable fixed + 15,000cost savings common fixed + 10,000

Incremental costslost cm B ! 100,000lost cm C (15% decrease) ! 45,000add’l variable costs A ! 40,000

Change in profit ! 10,000

Question 4

Equation for regular sales:(350 !130 !20)*X !12,000,000 = π

At the current time, Jim estimates there is an excess capacity of 5,000 units

Each of the following cases is separate and independent of each other.

Case A Sue has received a special order from a customer for 6,000 tables. The order is to be filled any time during the

coming year, and the proposed price per table is $280. No selling commissions would be paid on the order. Fixedcosts, in total, do not change as a result of this order. Sue plans on producing all 6,000 units of the special order. Planned sales at the regular sales price will be reduced by 1,000 units. The production manager is to receive a $15,000bonus.

Incremental benefitsadd’l cm 6,000*(280 ! 130) + 900,000 [4 pts]

Case B Sue has received a special order from a customer for 25,000 tables. The order is to be filled any time during the

coming year, and the proposed price per table is $260 per table. No selling commissions would be paid on the order. Fixed costs, in total, do not change as a result of this order.

Sue plans making 5,000 units in house from normal production runs at budgeted costs, and comes from the excesscapacity.

8,000 will be filled by nonroutine production created by adding a shift and working overtime. Material costs for these8,000 units will increase by 20%, and labor costs will be 50% higher than on regular production. An additional$15,000 insurance policy must be purchased, and the production manager will get a bonus of $25,000.

The final 12,000 of the special order comes from outsourcing. These units could be purchased from an outsidesupplier at $250 per table. Shipping for these outsourced units is $85,000.

Summary:5,000 normal production run from excess capacity.8,000 from nonroutine production with increased costs.12,000 from outside supplier.

Incremental benefitsadd’l cm 5,000*(260 ! 130) + 650,000 [4 pts]add’l cm 8,000*(260 ! 66 ! 67.5 ! 30) + 772,000 [4 pts]add’l cm 12,000*(260 !250) + 120,000 [4 pts]

Question 5 Jason’s Company employs labor with a learning effect of 87%. If the cost for the first unitis $510, compute the total time and average time for these intervals (or marginal blocks).

Average cost per unit of labor within interval:(T1,200 ! T900) / 300 = 30,244.87 / 300 = 100.816

Question 6 The Mackenzie Company is interested in computing its learning effect on a new product. Early measurements reveal 900 hours were spent on making the first 250 units, and 800 hours were spenton making the next 300 units. Your computations should use logarithms to at least four decimal places. Please show all computations.

Required:

1. What is Mackenzie’s learning effect (xx.xx%) per doubling of production?2. What are Mackenzie’s equations for computing either the cumulative average time or total

Traditional statement Contribution margin statement

Sales revenue Sales revenue- Cost of Goods Sold - Variable costsGross Margin Contribution margin-Selling, General & Admin - Fixed costsIncome Income

Sales rev Beg FG Beg WIP Beg Mat! CGS + CGM + DM used + Mat PurchasesGM ! End FG + DL ! End Mat! S&A CGS + MOH DM usedIncome ! End WIP

CGM

Units Revenue

SP*X ! V*X ! F = π Rev ! V%*Rev ! F = π(SP ! V)*X ! F = π (1 ! V%)*Rev ! F = π

CM*X !!!! F = π CM%*Rev !!!! F = π

CM*ªªªªX = ªªªªπ CM*ªªªªRev = ªªªªπ

Where:SP = sales price per unit Rev = sales revenueVC = variable cost per unit VC% = variable cost as percent of revenueCM = contribution margin per unit CM% = contribution margin percentage (of revenue)F = total fixed costX = units (designated Q in text)π = before tax profitafter tax net income = π*(1 ! tax rate)

Incremental benefits+ Additional CM or revenues+ Cost savings

Incremental costs! Additional costs! Lost CM or revenues

Change in profit

y = axb T = axb+1

Where:y = cumulative average time per unitT = total time for x unitsa = time required for first unitx = cumulative number of units producedb = ln (% learning) / ln (2)

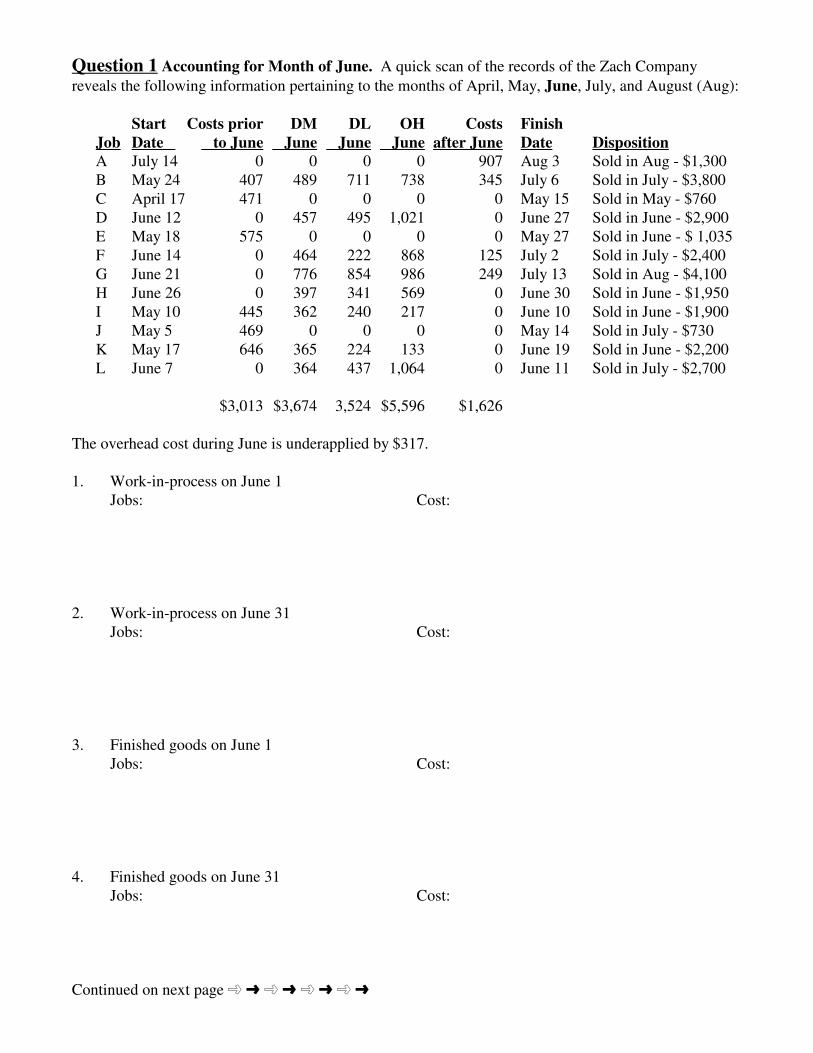

Question 1 Accounting for Month of June. A quick scan of the records of the Zach Company

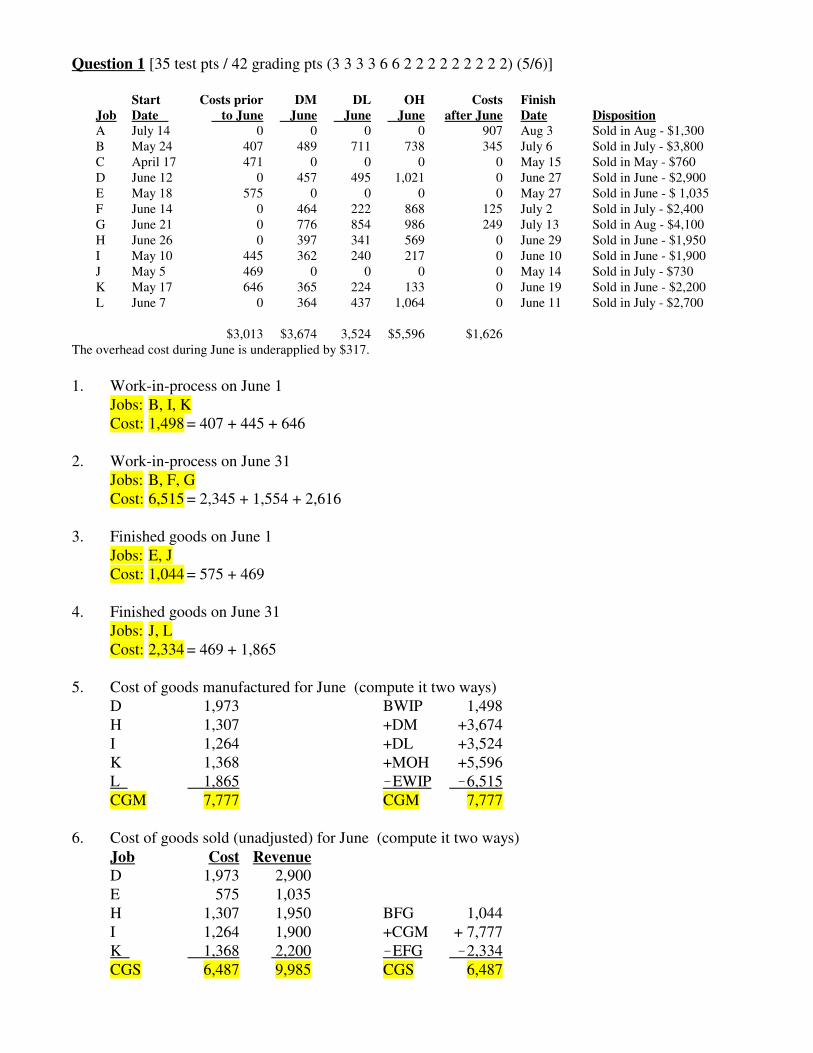

reveals the following information pertaining to the months of April, May, June, July, and August (Aug):

Start Costs prior DM DL OH Costs Finish

Job Date to June June June June after June Date Disposition

A July 14 0 0 0 0 907 Aug 3 Sold in Aug - $1,300B May 24 407 489 711 738 345 July 6 Sold in July - $3,800C April 17 471 0 0 0 0 May 15 Sold in May - $760D June 12 0 457 495 1,021 0 June 27 Sold in June - $2,900E May 18 575 0 0 0 0 May 27 Sold in June - $ 1,035F June 14 0 464 222 868 125 July 2 Sold in July - $2,400G June 21 0 776 854 986 249 July 13 Sold in Aug - $4,100H June 26 0 397 341 569 0 June 30 Sold in June - $1,950I May 10 445 362 240 217 0 June 10 Sold in June - $1,900J May 5 469 0 0 0 0 May 14 Sold in July - $730K May 17 646 365 224 133 0 June 19 Sold in June - $2,200L June 7 0 364 437 1,064 0 June 11 Sold in July - $2,700

$3,013 $3,674 3,524 $5,596 $1,626

The overhead cost during June is underapplied by $317.

1. Work-in-process on June 1Jobs: Cost:

2. Work-in-process on June 31Jobs: Cost:

3. Finished goods on June 1Jobs: Cost:

4. Finished goods on June 31Jobs: Cost:

Continued on next page ¸ º ¸ º ¸ º ¸ º

5. Cost of goods manufactured for June (compute it two ways)

6. Cost of goods sold (unadjusted) for June (compute it two ways)

7. How much was actually spent on overhead during June?

8. Cost of goods sold (adjusted) for June

9. Sales revenue for June

10. Gross margin for June

Continued on next page ¸ º ¸ º ¸ º ¸ º

11. Prepare the journal entry for the addition of all direct material to all jobs worked on during June

12. Prepare the journal entry for the addition of all manufacturing overhead to all jobs worked onduring June

13. Prepare the journal entry to account for all jobs completed during June

14. Prepare the journal entry for cost of goods sold for June.

15. Prepare the end of period entry to even up (or close out) the account for overhead.

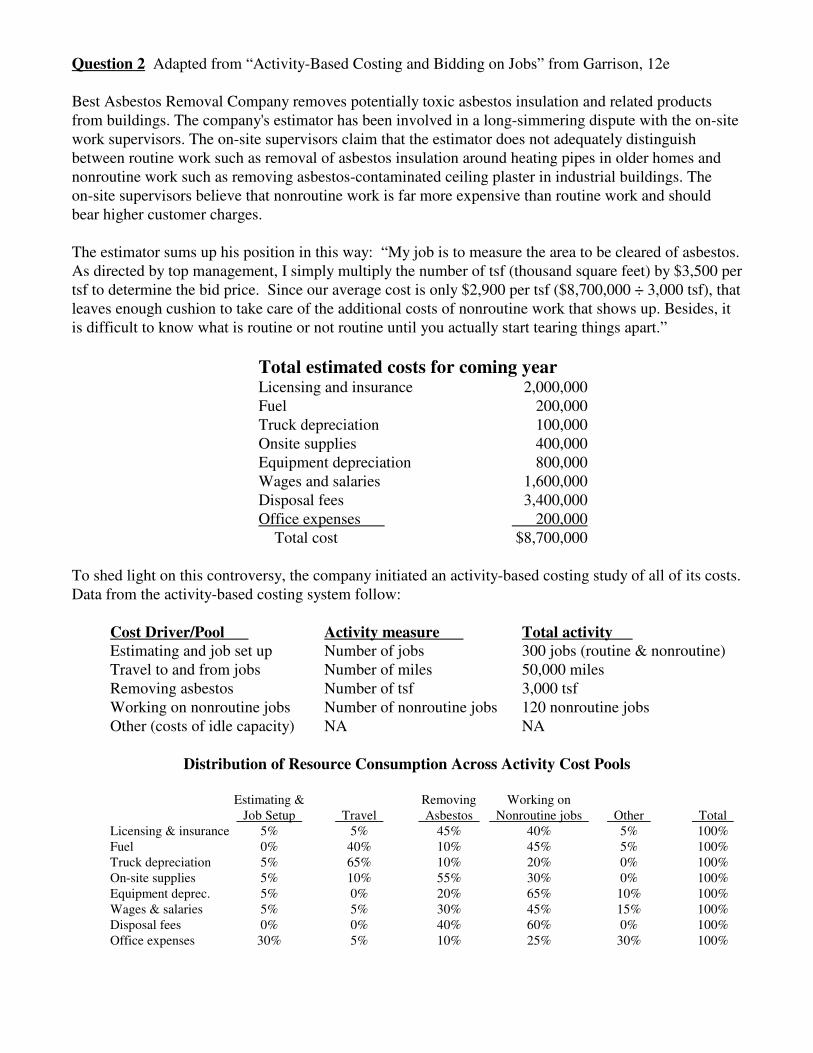

Question 2 Adapted from “Activity-Based Costing and Bidding on Jobs” from Garrison, 12e

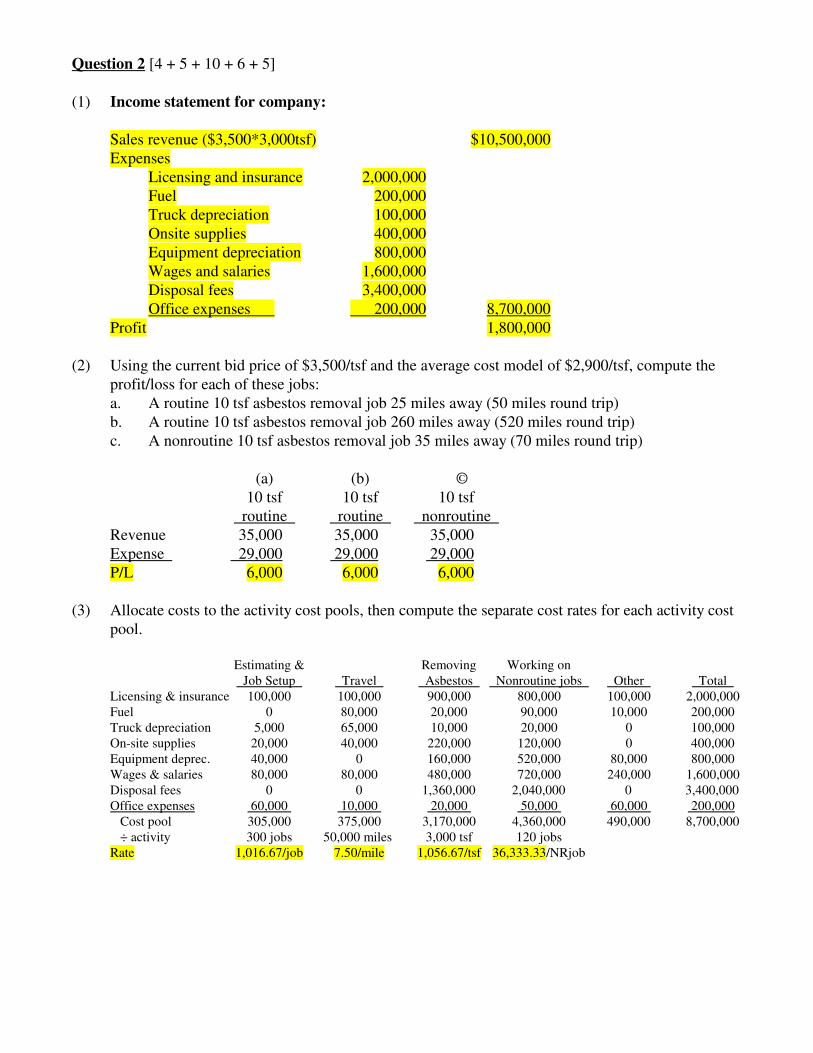

Best Asbestos Removal Company removes potentially toxic asbestos insulation and related productsfrom buildings. The company's estimator has been involved in a long-simmering dispute with the on-sitework supervisors. The on-site supervisors claim that the estimator does not adequately distinguishbetween routine work such as removal of asbestos insulation around heating pipes in older homes andnonroutine work such as removing asbestos-contaminated ceiling plaster in industrial buildings. Theon-site supervisors believe that nonroutine work is far more expensive than routine work and shouldbear higher customer charges.

The estimator sums up his position in this way: “My job is to measure the area to be cleared of asbestos.As directed by top management, I simply multiply the number of tsf (thousand square feet) by $3,500 pertsf to determine the bid price. Since our average cost is only $2,900 per tsf ($8,700,000 ÷ 3,000 tsf), thatleaves enough cushion to take care of the additional costs of nonroutine work that shows up. Besides, itis difficult to know what is routine or not routine until you actually start tearing things apart.”

Total estimated costs for coming yearLicensing and insurance 2,000,000Fuel 200,000Truck depreciation 100,000Onsite supplies 400,000Equipment depreciation 800,000Wages and salaries 1,600,000Disposal fees 3,400,000Office expenses 200,000 Total cost $8,700,000

To shed light on this controversy, the company initiated an activity-based costing study of all of its costs. Data from the activity-based costing system follow:

Cost Driver/Pool Activity measure Total activity

Estimating and job set up Number of jobs 300 jobs (routine & nonroutine)Travel to and from jobs Number of miles 50,000 milesRemoving asbestos Number of tsf 3,000 tsfWorking on nonroutine jobs Number of nonroutine jobs 120 nonroutine jobsOther (costs of idle capacity) NA NA

Distribution of Resource Consumption Across Activity Cost Pools

Estimating & Removing Working on Job Setup Travel Asbestos Nonroutine jobs Other Total

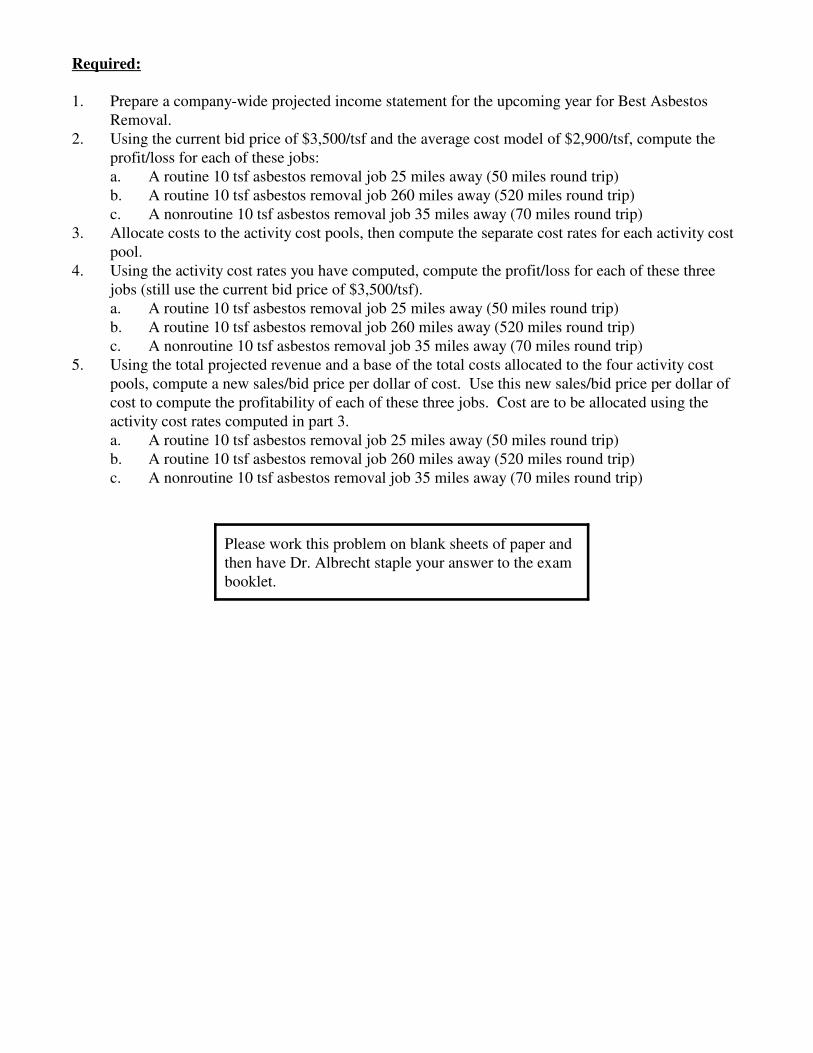

1. Prepare a company-wide projected income statement for the upcoming year for Best AsbestosRemoval.

2. Using the current bid price of $3,500/tsf and the average cost model of $2,900/tsf, compute theprofit/loss for each of these jobs:a. A routine 10 tsf asbestos removal job 25 miles away (50 miles round trip)b. A routine 10 tsf asbestos removal job 260 miles away (520 miles round trip)c. A nonroutine 10 tsf asbestos removal job 35 miles away (70 miles round trip)

3. Allocate costs to the activity cost pools, then compute the separate cost rates for each activity costpool.

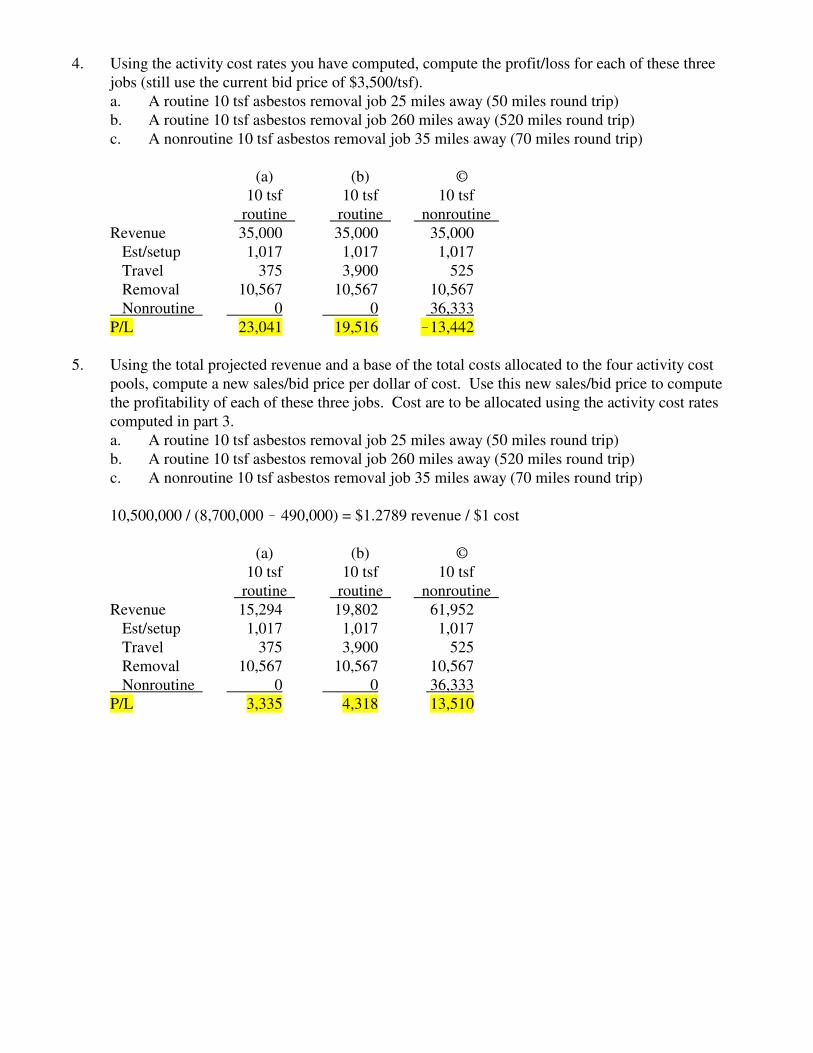

4. Using the activity cost rates you have computed, compute the profit/loss for each of these threejobs (still use the current bid price of $3,500/tsf).a. A routine 10 tsf asbestos removal job 25 miles away (50 miles round trip)b. A routine 10 tsf asbestos removal job 260 miles away (520 miles round trip)c. A nonroutine 10 tsf asbestos removal job 35 miles away (70 miles round trip)

5. Using the total projected revenue and a base of the total costs allocated to the four activity costpools, compute a new sales/bid price per dollar of cost. Use this new sales/bid price per dollar ofcost to compute the profitability of each of these three jobs. Cost are to be allocated using theactivity cost rates computed in part 3.a. A routine 10 tsf asbestos removal job 25 miles away (50 miles round trip)b. A routine 10 tsf asbestos removal job 260 miles away (520 miles round trip)c. A nonroutine 10 tsf asbestos removal job 35 miles away (70 miles round trip)

Please work this problem on blank sheets of paper andthen have Dr. Albrecht staple your answer to the exambooklet.

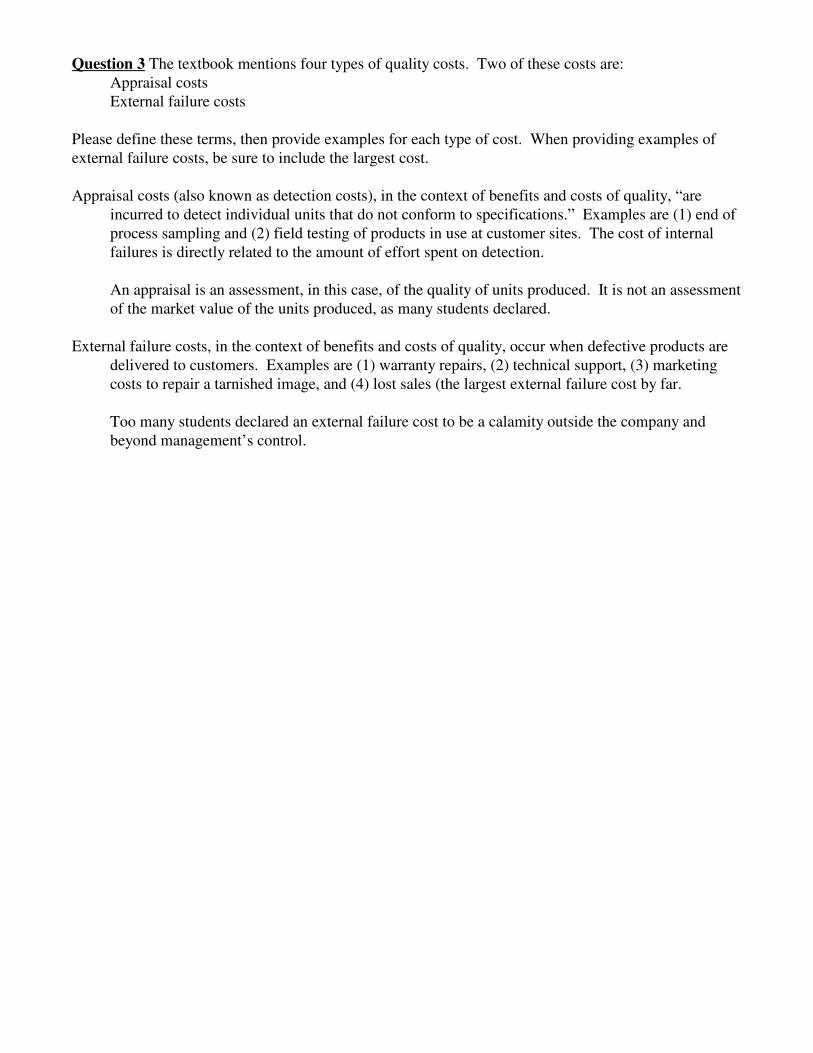

Question 3 The textbook mentions four types of quality costs. Two of these costs are:Appraisal costsExternal failure costs

Please define these terms, then provide examples for each type of cost. When providing examples ofexternal failure costs, be sure to include the largest cost.

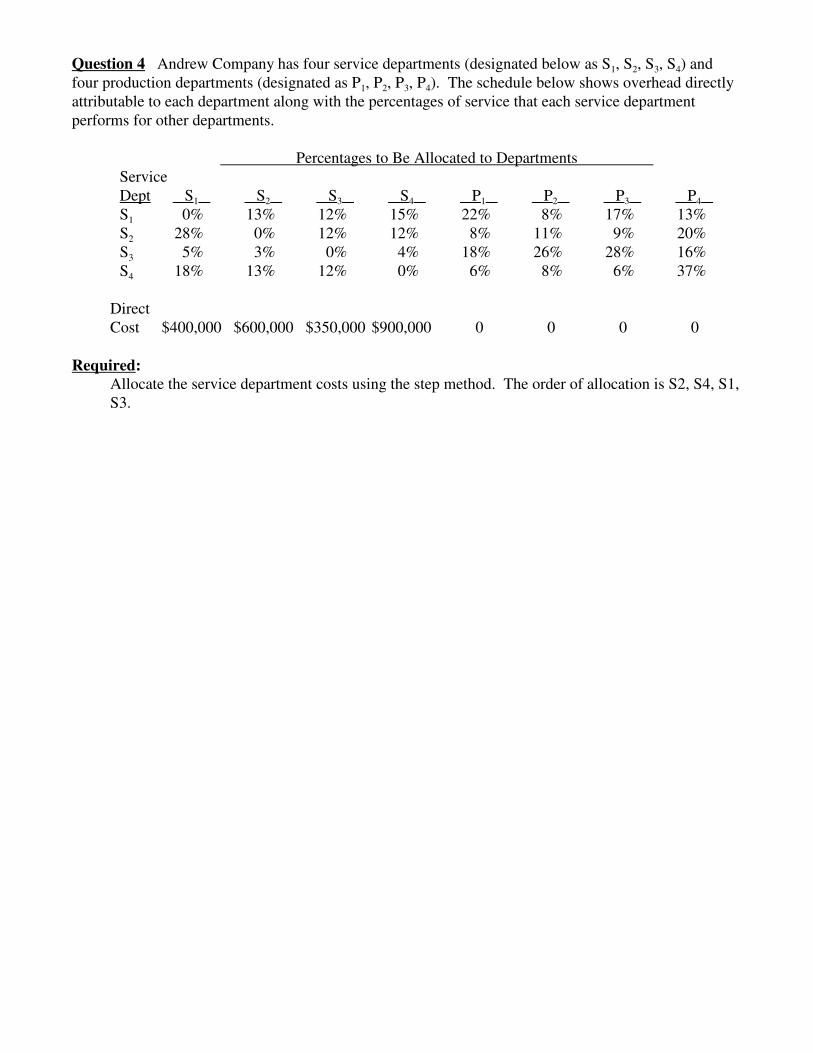

Question 4 Andrew Company has four service departments (designated below as S1, S2, S3, S4) andfour production departments (designated as P1, P2, P3, P4). The schedule below shows overhead directlyattributable to each department along with the percentages of service that each service departmentperforms for other departments.

Allocate the service department costs using the step method. The order of allocation is S2, S4, S1,S3.

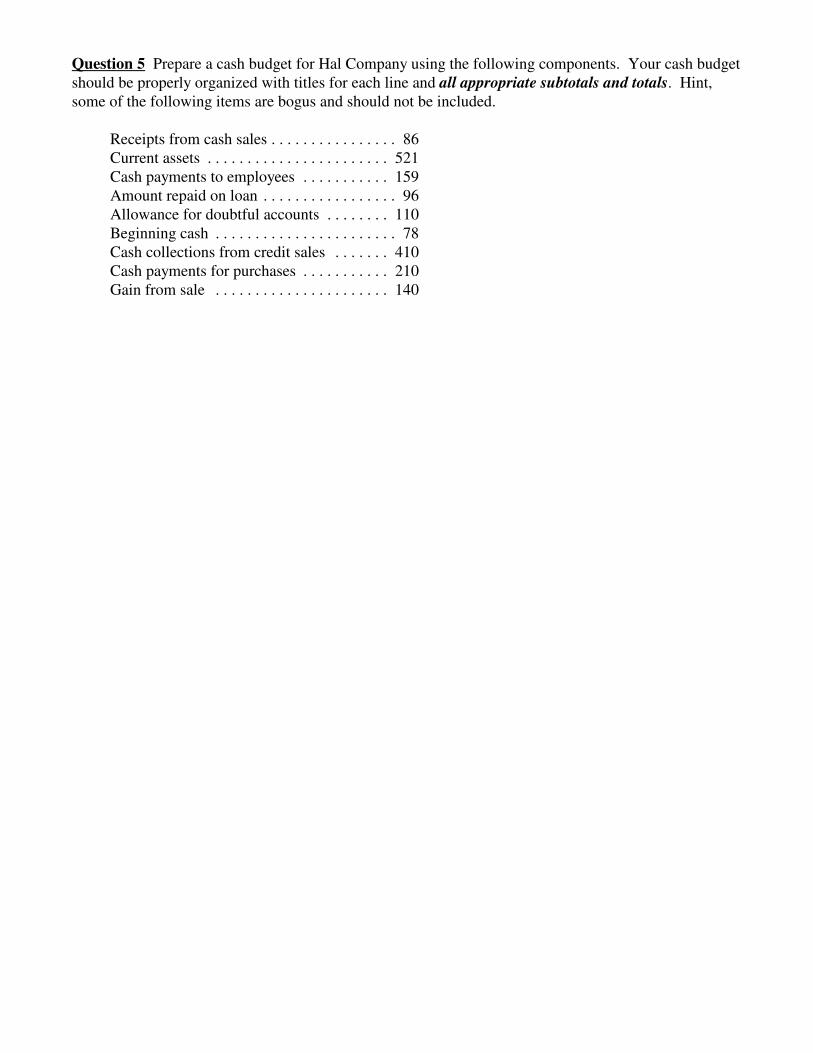

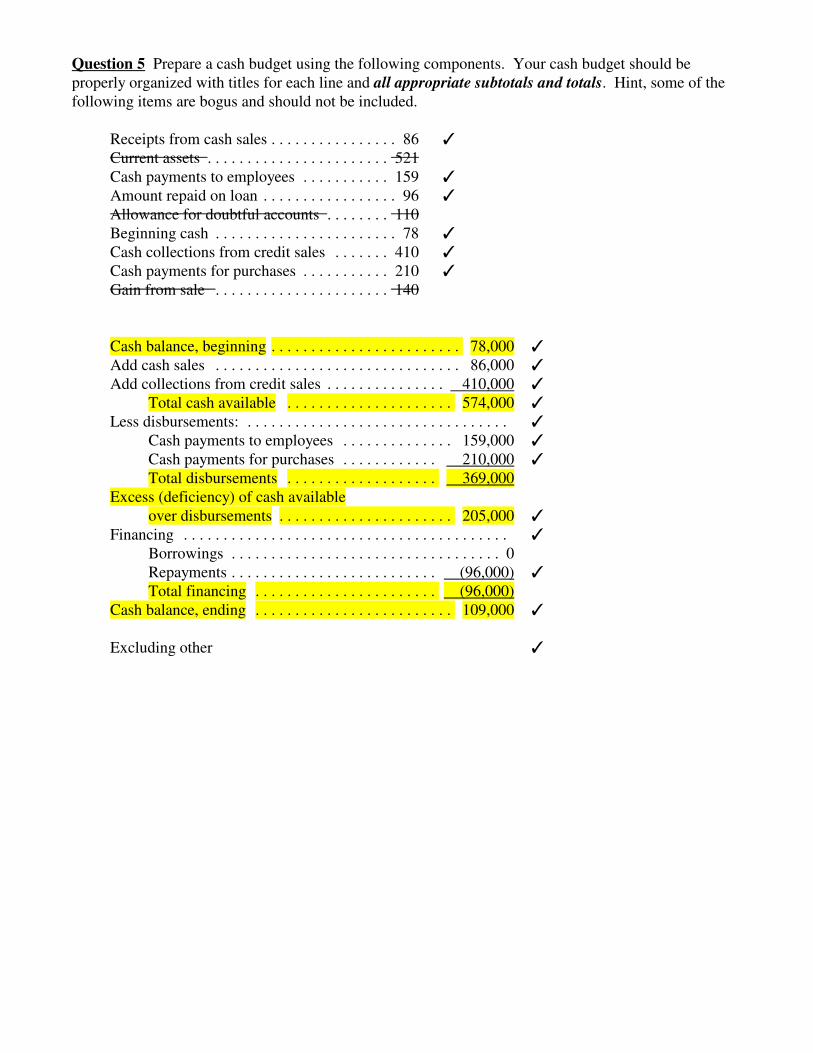

Question 5 Prepare a cash budget for Hal Company using the following components. Your cash budgetshould be properly organized with titles for each line and all appropriate subtotals and totals. Hint,some of the following items are bogus and should not be included.

Take home exam problem:You are to bring a solution to this problem to the final exam with you.

The following activities constitute cheating: (1) You are not to work with anyone else in any way,shape or form. (2) You are not to check answers. (3) Anything else that prevents your solutionfrom being completely and totally your work.

The following is allowed: (1) textbook, (2) notes, (3) HW and test solutions on course web page,(4) a financial calculator or spreadsheet.

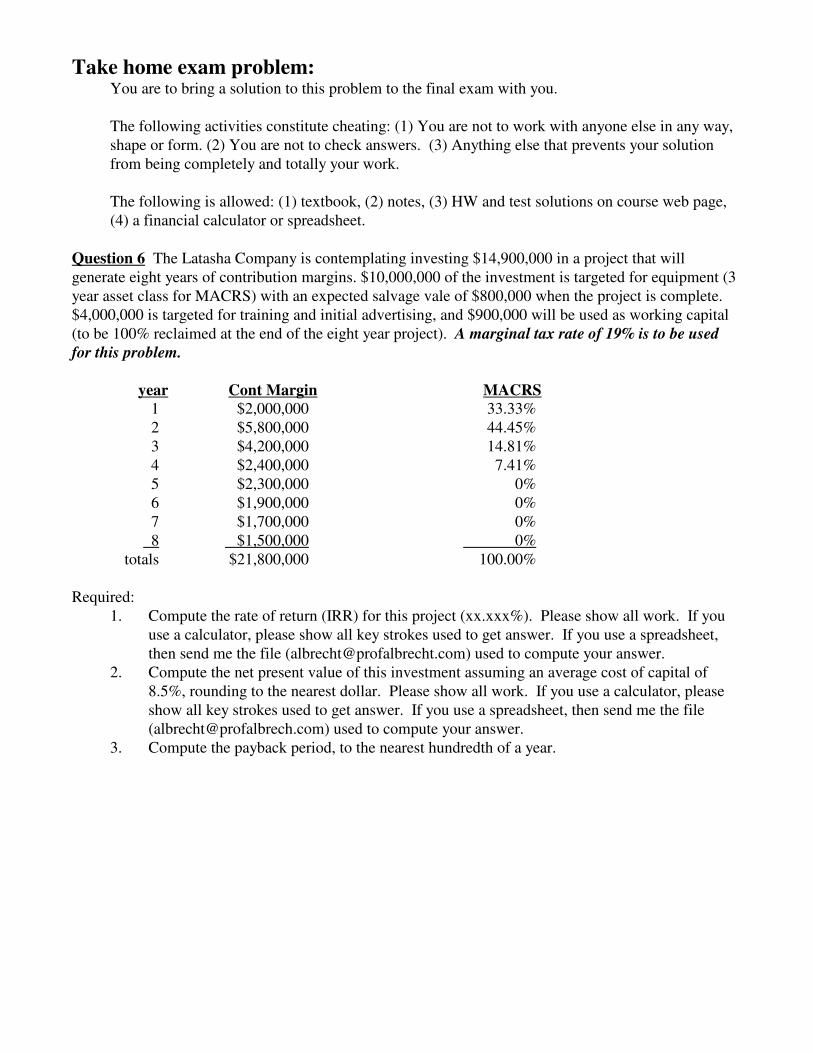

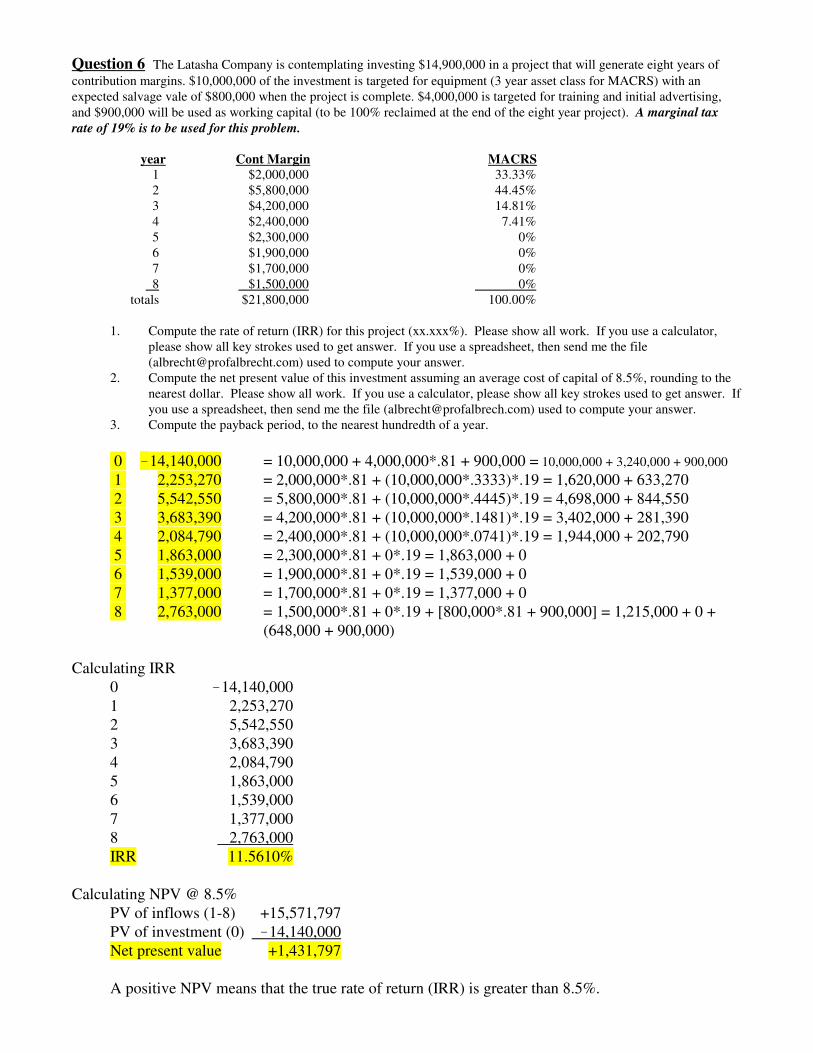

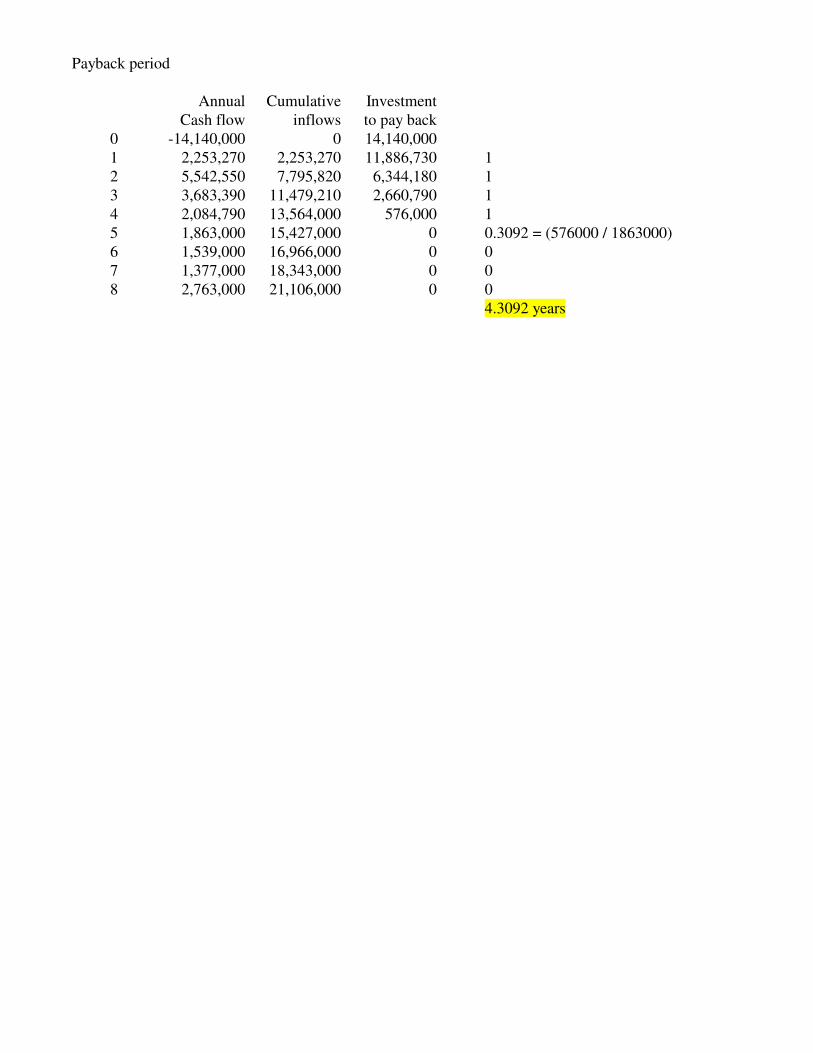

Question 6 The Latasha Company is contemplating investing $14,900,000 in a project that willgenerate eight years of contribution margins. $10,000,000 of the investment is targeted for equipment (3year asset class for MACRS) with an expected salvage vale of $800,000 when the project is complete.$4,000,000 is targeted for training and initial advertising, and $900,000 will be used as working capital(to be 100% reclaimed at the end of the eight year project). A marginal tax rate of 19% is to be used

Required:1. Compute the rate of return (IRR) for this project (xx.xxx%). Please show all work. If you

use a calculator, please show all key strokes used to get answer. If you use a spreadsheet,then send me the file ([email protected]) used to compute your answer.

2. Compute the net present value of this investment assuming an average cost of capital of8.5%, rounding to the nearest dollar. Please show all work. If you use a calculator, pleaseshow all key strokes used to get answer. If you use a spreadsheet, then send me the file([email protected]) used to compute your answer.

3. Compute the payback period, to the nearest hundredth of a year.

Job Date to June June June June after June Date Disposition

A July 14 0 0 0 0 907 Aug 3 Sold in Aug - $1,300B May 24 407 489 711 738 345 July 6 Sold in July - $3,800C April 17 471 0 0 0 0 May 15 Sold in May - $760D June 12 0 457 495 1,021 0 June 27 Sold in June - $2,900E May 18 575 0 0 0 0 May 27 Sold in June - $ 1,035F June 14 0 464 222 868 125 July 2 Sold in July - $2,400G June 21 0 776 854 986 249 July 13 Sold in Aug - $4,100H June 26 0 397 341 569 0 June 29 Sold in June - $1,950I May 10 445 362 240 217 0 June 10 Sold in June - $1,900J May 5 469 0 0 0 0 May 14 Sold in July - $730K May 17 646 365 224 133 0 June 19 Sold in June - $2,200L June 7 0 364 437 1,064 0 June 11 Sold in July - $2,700

$3,013 $3,674 3,524 $5,596 $1,626The overhead cost during June is underapplied by $317.

1. Work-in-process on June 1Jobs: B, I, KCost: 1,498 = 407 + 445 + 646

2. Work-in-process on June 31Jobs: B, F, GCost: 6,515 = 2,345 + 1,554 + 2,616

3. Finished goods on June 1Jobs: E, JCost: 1,044 = 575 + 469

4. Finished goods on June 31Jobs: J, LCost: 2,334 = 469 + 1,865

5. Cost of goods manufactured for June (compute it two ways)D 1,973 BWIP 1,498H 1,307 +DM +3,674I 1,264 +DL +3,524K 1,368 +MOH +5,596L 1,865 !EWIP !6,515CGM 7,777 CGM 7,777

6. Cost of goods sold (unadjusted) for June (compute it two ways)

7. How much was actually spent on overhead during June?actual= applied + underappliedactual = 5,596 + 317actual = 5,913

8. Cost of goods sold (adjusted) for June6,804 = 6,487 + 317

9. Sales revenue for June9,985

10. Gross margin for June3,181 = 9,985 ! 6,804

11. Prepare the journal entry for the addition of all direct material to all jobs worked on during June12. Prepare the journal entry for the addition of all manufacturing overhead to all jobs worked on

during June13. Prepare the journal entry for cost of goods manufactured during June14. Prepare the journal entry for cost of goods sold for June.15. Prepare the end of period entry for accounting for overhead.

During June Work-in-process 3,674Direct materials inventory 3,674

During June Work-in-process 5,596Manufacturing overhead control 5,596

June 30 Finished goods 7,777Work-in-process 7,777

June 30 Cost of goods sold expense 6,487Finished goods 6,487

June 30 Cost of goods sold expense 317Manufacturing overhead control 317

Licensing and insurance 2,000,000Fuel 200,000Truck depreciation 100,000Onsite supplies 400,000Equipment depreciation 800,000Wages and salaries 1,600,000Disposal fees 3,400,000Office expenses 200,000 8,700,000

Profit 1,800,000

(2) Using the current bid price of $3,500/tsf and the average cost model of $2,900/tsf, compute theprofit/loss for each of these jobs:a. A routine 10 tsf asbestos removal job 25 miles away (50 miles round trip)b. A routine 10 tsf asbestos removal job 260 miles away (520 miles round trip)c. A nonroutine 10 tsf asbestos removal job 35 miles away (70 miles round trip)

4. Using the activity cost rates you have computed, compute the profit/loss for each of these threejobs (still use the current bid price of $3,500/tsf).a. A routine 10 tsf asbestos removal job 25 miles away (50 miles round trip)b. A routine 10 tsf asbestos removal job 260 miles away (520 miles round trip)c. A nonroutine 10 tsf asbestos removal job 35 miles away (70 miles round trip)

5. Using the total projected revenue and a base of the total costs allocated to the four activity costpools, compute a new sales/bid price per dollar of cost. Use this new sales/bid price to computethe profitability of each of these three jobs. Cost are to be allocated using the activity cost ratescomputed in part 3.a. A routine 10 tsf asbestos removal job 25 miles away (50 miles round trip)b. A routine 10 tsf asbestos removal job 260 miles away (520 miles round trip)c. A nonroutine 10 tsf asbestos removal job 35 miles away (70 miles round trip)

Question 3 The textbook mentions four types of quality costs. Two of these costs are:Appraisal costsExternal failure costs

Please define these terms, then provide examples for each type of cost. When providing examples ofexternal failure costs, be sure to include the largest cost.

Appraisal costs (also known as detection costs), in the context of benefits and costs of quality, “areincurred to detect individual units that do not conform to specifications.” Examples are (1) end ofprocess sampling and (2) field testing of products in use at customer sites. The cost of internalfailures is directly related to the amount of effort spent on detection.

An appraisal is an assessment, in this case, of the quality of units produced. It is not an assessmentof the market value of the units produced, as many students declared.

External failure costs, in the context of benefits and costs of quality, occur when defective products aredelivered to customers. Examples are (1) warranty repairs, (2) technical support, (3) marketingcosts to repair a tarnished image, and (4) lost sales (the largest external failure cost by far.

Too many students declared an external failure cost to be a calamity outside the company andbeyond management’s control.

Question 4 Percentages to Be Allocated to Departments

Allocate the service department costs using the step method. The order of allocation is S2, S4, S1,S3.

Question 5 Prepare a cash budget using the following components. Your cash budget should beproperly organized with titles for each line and all appropriate subtotals and totals. Hint, some of thefollowing items are bogus and should not be included.

Question 6 The Latasha Company is contemplating investing $14,900,000 in a project that will generate eight years of

contribution margins. $10,000,000 of the investment is targeted for equipment (3 year asset class for MACRS) with anexpected salvage vale of $800,000 when the project is complete. $4,000,000 is targeted for training and initial advertising,

and $900,000 will be used as working capital (to be 100% reclaimed at the end of the eight year project). A marginal tax

1. Compute the rate of return (IRR) for this project (xx.xxx%). Please show all work. If you use a calculator,please show all key strokes used to get answer. If you use a spreadsheet, then send me the file([email protected]) used to compute your answer.

2. Compute the net present value of this investment assuming an average cost of capital of 8.5%, rounding to thenearest dollar. Please show all work. If you use a calculator, please show all key strokes used to get answer. Ifyou use a spreadsheet, then send me the file ([email protected]) used to compute your answer.

3. Compute the payback period, to the nearest hundredth of a year.