25

Scarce resources: Making production decisions when resources are tight. Choosing among products. Setting production schedules

Scarce resources:

Making production decisions when resources are tight.

Choosing among products.Setting production schedules

Agenda

• Reichard Maschinen GmbH written analysis

• Contribution approach - recap

• A more in-depth look at scarce resource decisions

• Group work: Information Technology, Inc.

Reichard Maschinen GmbH Written Analysis

• A 10% assignment. Maximum of five pages (not including exhibits).

• Be sure you have downloaded the instructions for the write-up.

• Cover memo - a page or two.• Analysis: computations and reasoning• Cover page, but no slick or stiff covers• Typed, double-spaced, 12-point font.

Reichard Maschinen Written Analysis

Decisions1. Whether or not to manufacture plastic rings.

2. Alternative schedules for launching plastic rings.

3. Strategic implications of ring decision and effect on demand in both short- and long-run.

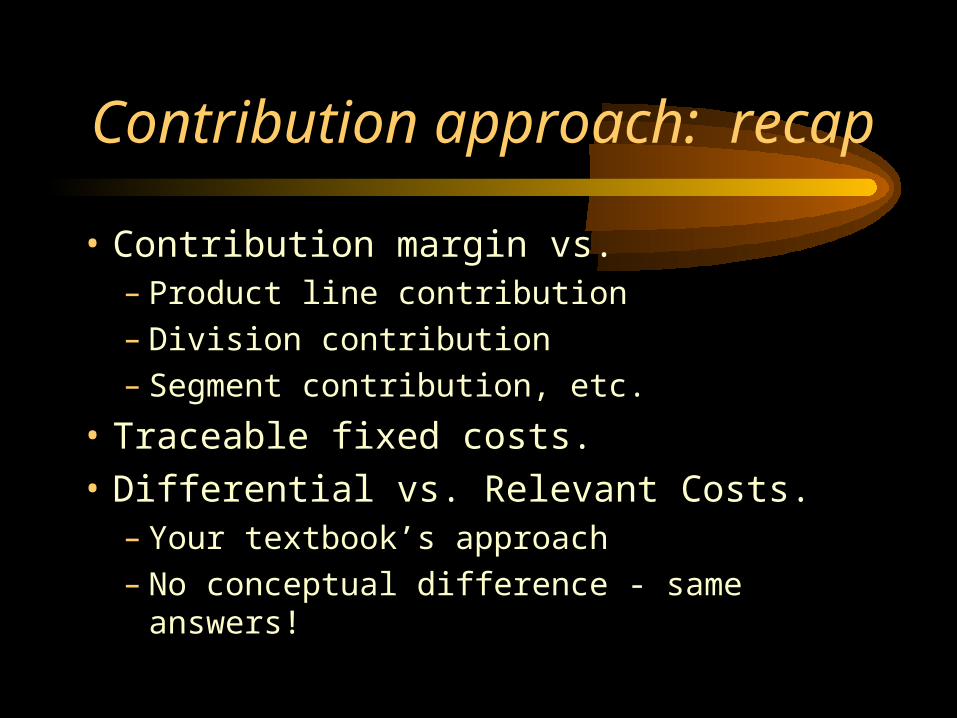

Contribution approach: recap

• Contribution margin vs.– Product line contribution– Division contribution– Segment contribution, etc.

• Traceable fixed costs.• Differential vs. Relevant Costs.

– Your textbook’s approach– No conceptual difference - same answers!

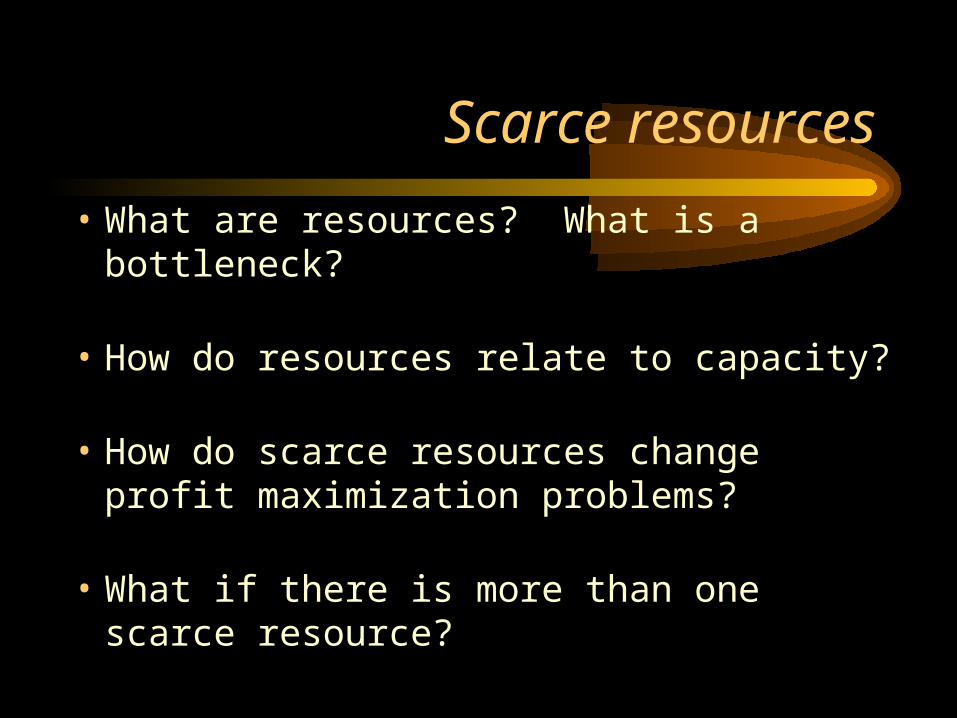

Scarce resources• What are resources? What is a bottleneck?

• How do resources relate to capacity?

• How do scarce resources change profit maximization problems?

• What if there is more than one scarce resource?

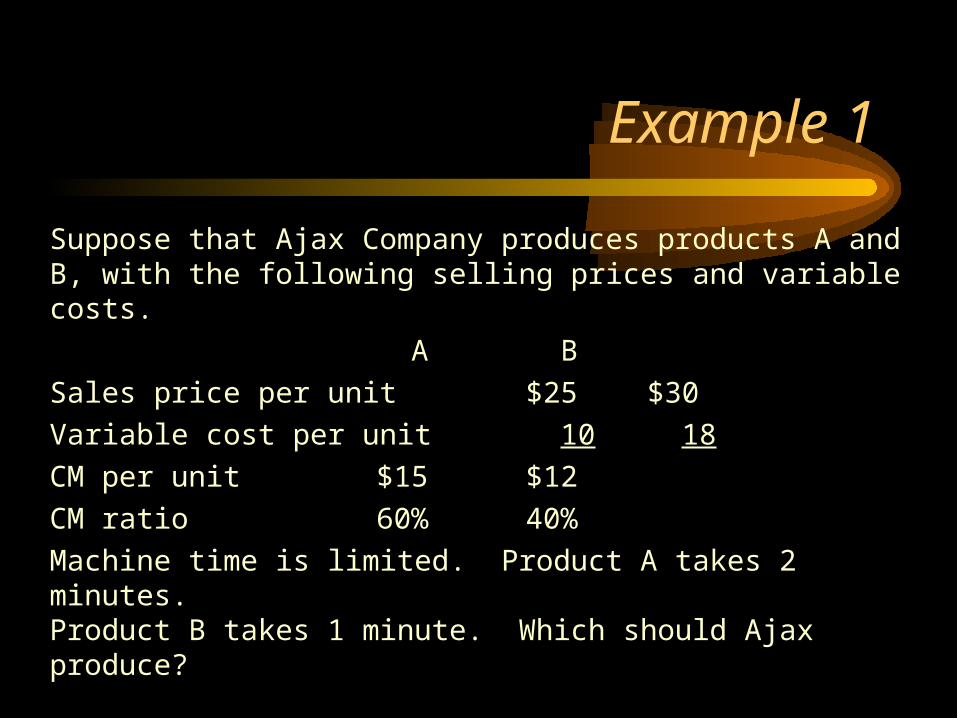

Example 1

Suppose that Ajax Company produces products A and B, with the following selling prices and variable costs.

A BSales price per unit $25 $30Variable cost per unit 10 18CM per unit $15 $12CM ratio 60% 40%Machine time is limited. Product A takes 2 minutes.Product B takes 1 minute. Which should Ajax produce?

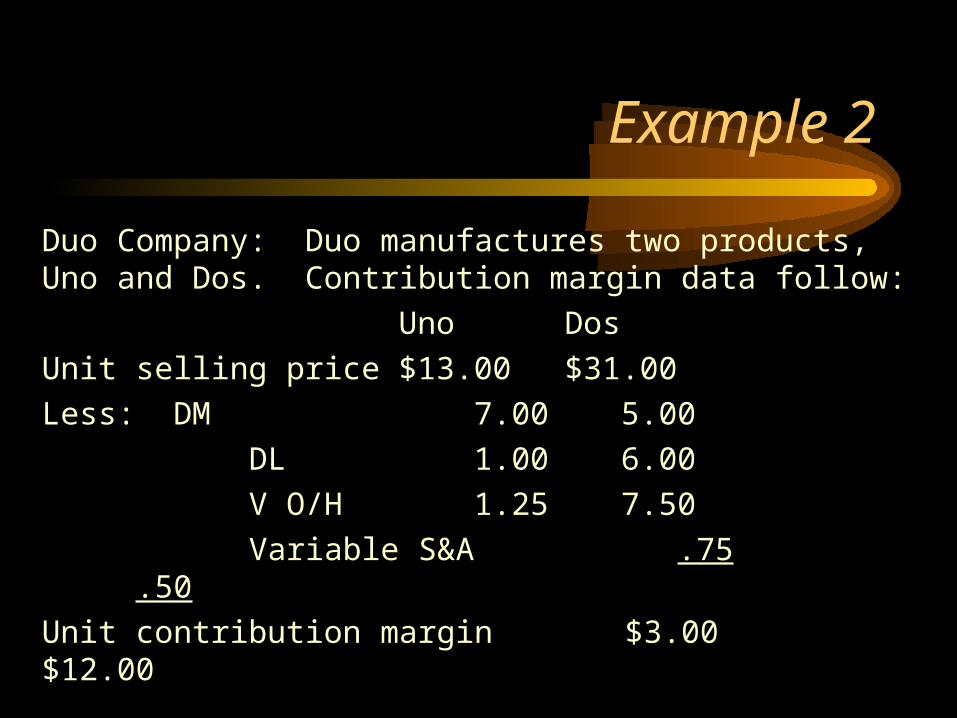

Example 2

Duo Company: Duo manufactures two products, Uno and Dos. Contribution margin data follow:

Uno DosUnit selling price $13.00 $31.00Less: DM 7.00 5.00 DL 1.00 6.00 V O/H 1.25 7.50 Variable S&A .75 .50Unit contribution margin $3.00 $12.00

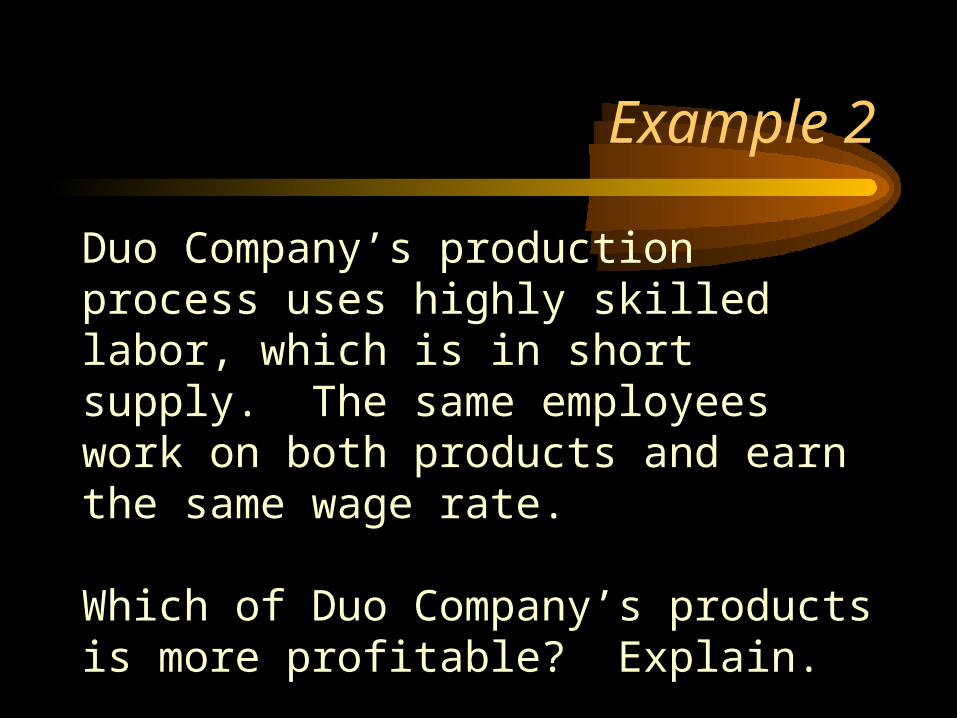

Example 2

Duo Company’s production process uses highly skilled labor, which is in short supply. The same employees work on both products and earn the same wage rate.

Which of Duo Company’s products is more profitable? Explain.

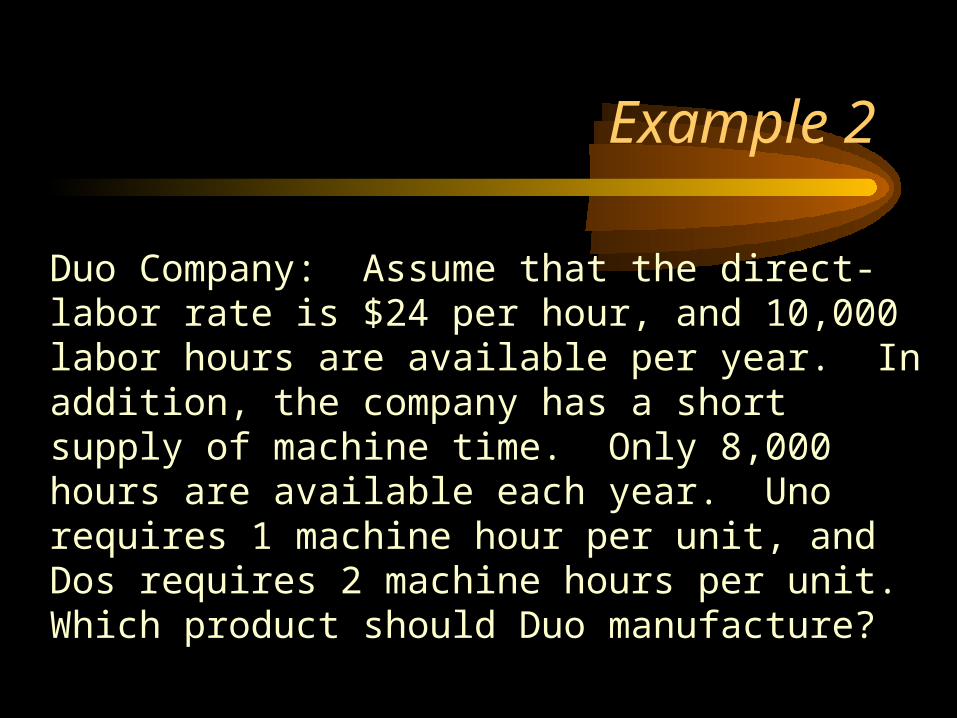

Example 2

Duo Company: Assume that the direct-labor rate is $24 per hour, and 10,000 labor hours are available per year. In addition, the company has a short supply of machine time. Only 8,000 hours are available each year. Uno requires 1 machine hour per unit, and Dos requires 2 machine hours per unit.Which product should Duo manufacture?

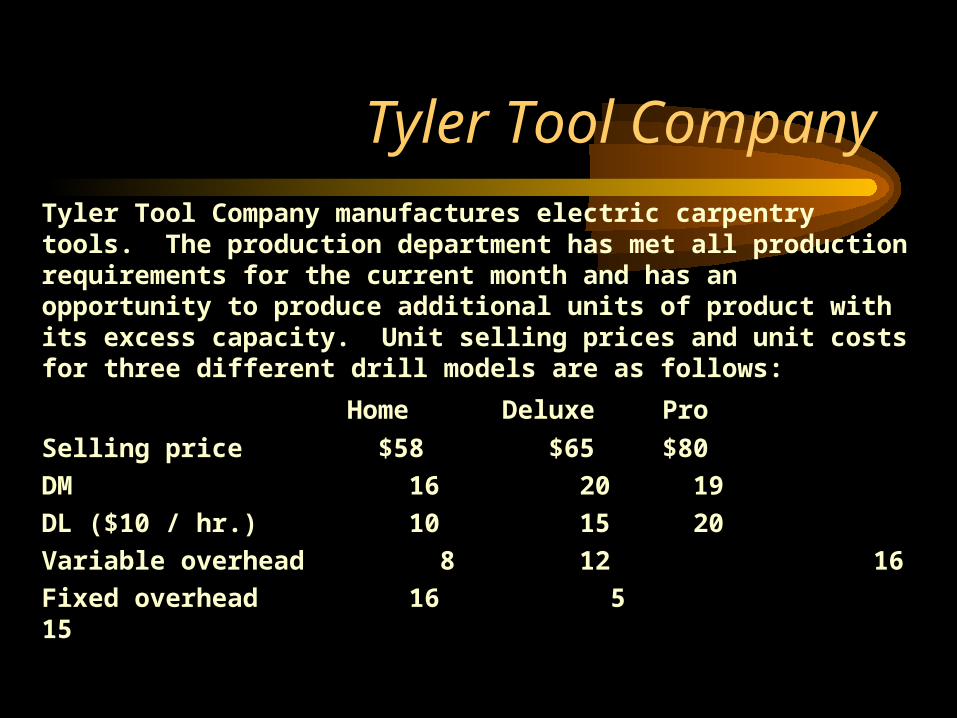

Tyler Tool CompanyTyler Tool Company manufactures electric carpentry tools. The production department has met all production requirements for the current month and has an opportunity to produce additional units of product with its excess capacity. Unit selling prices and unit costs for three different drill models are as follows:

Home Deluxe ProSelling price $58 $65 $80DM 16 20 19DL ($10 / hr.) 10 15 20Variable overhead 8 12 16Fixed overhead 16 5 15

Tyler Tool Company

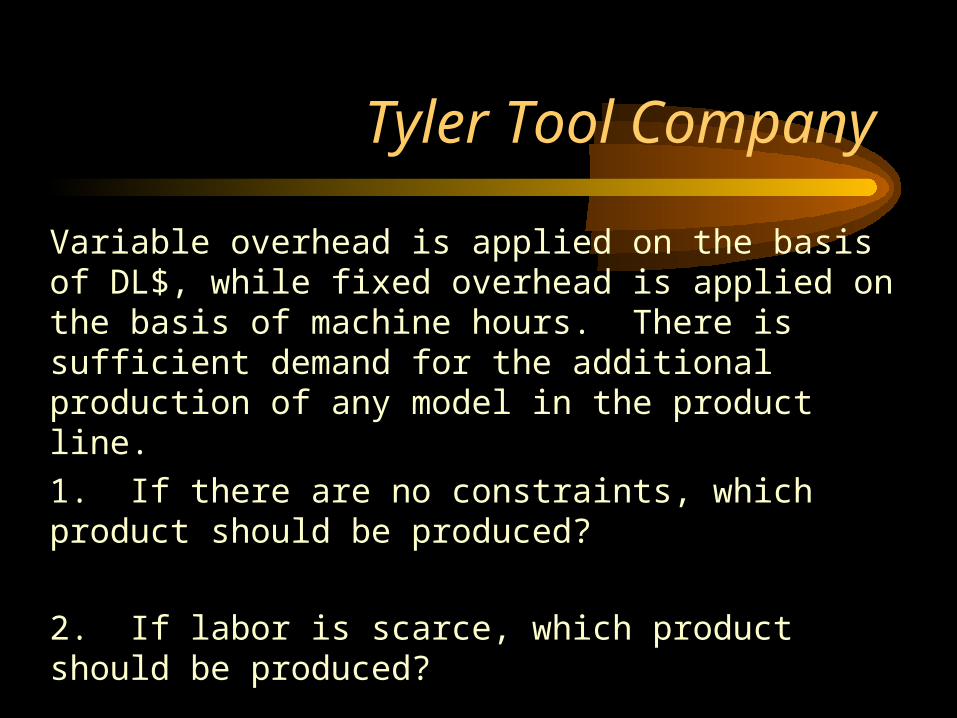

Variable overhead is applied on the basis of DL$, while fixed overhead is applied on the basis of machine hours. There is sufficient demand for the additional production of any model in the product line.1. If there are no constraints, which product should be produced?

2. If labor is scarce, which product should be produced?

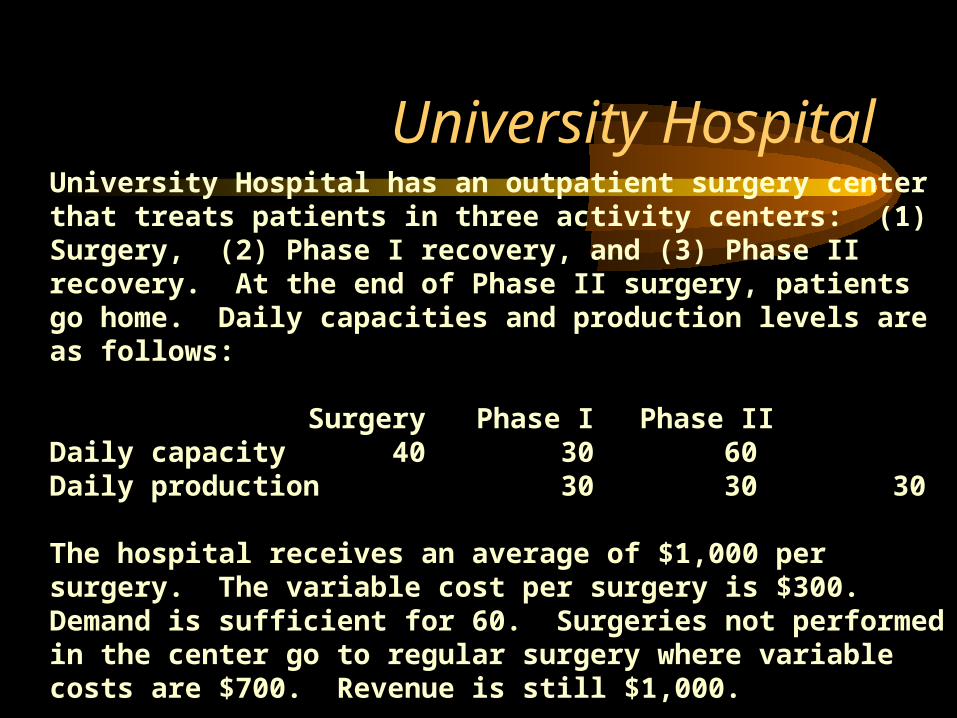

University HospitalUniversity Hospital has an outpatient surgery center that treats patients in three activity centers: (1) Surgery, (2) Phase I recovery, and (3) Phase II recovery. At the end of Phase II surgery, patients go home. Daily capacities and production levels are as follows:

Surgery Phase I Phase IIDaily capacity 40 30 60Daily production 30 30 30

The hospital receives an average of $1,000 per surgery. The variable cost per surgery is $300. Demand is sufficient for 60. Surgeries not performed in the center go to regular surgery where variable costs are $700. Revenue is still $1,000.

University Hospital

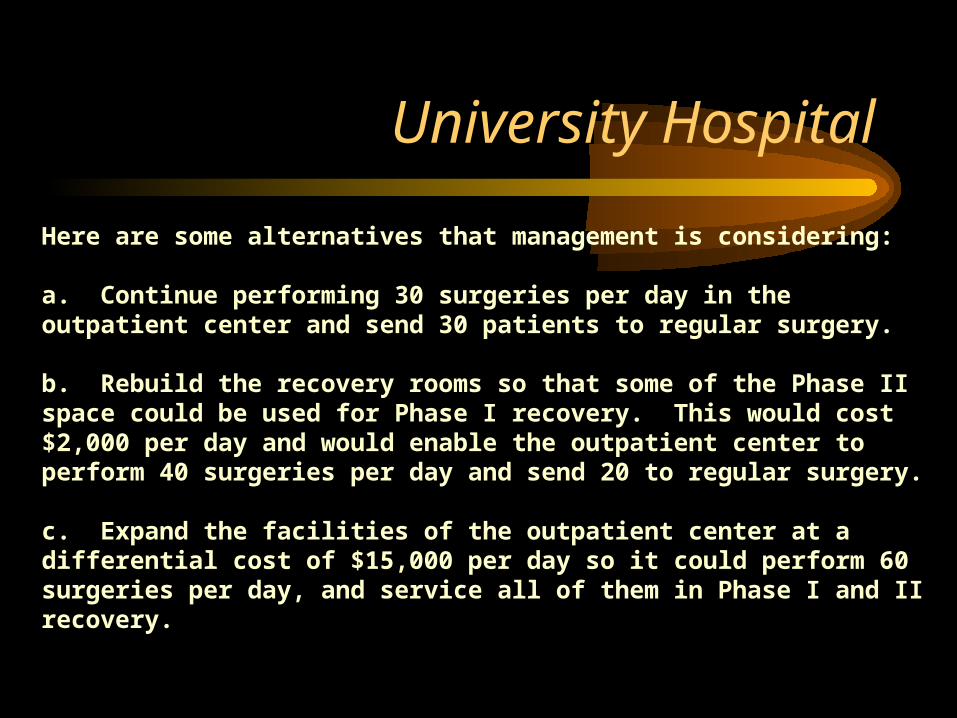

Here are some alternatives that management is considering:

a. Continue performing 30 surgeries per day in the outpatient center and send 30 patients to regular surgery.

b. Rebuild the recovery rooms so that some of the Phase II space could be used for Phase I recovery. This would cost $2,000 per day and would enable the outpatient center to perform 40 surgeries per day and send 20 to regular surgery.

c. Expand the facilities of the outpatient center at a differential cost of $15,000 per day so it could perform 60 surgeries per day, and service all of them in Phase I and II recovery.

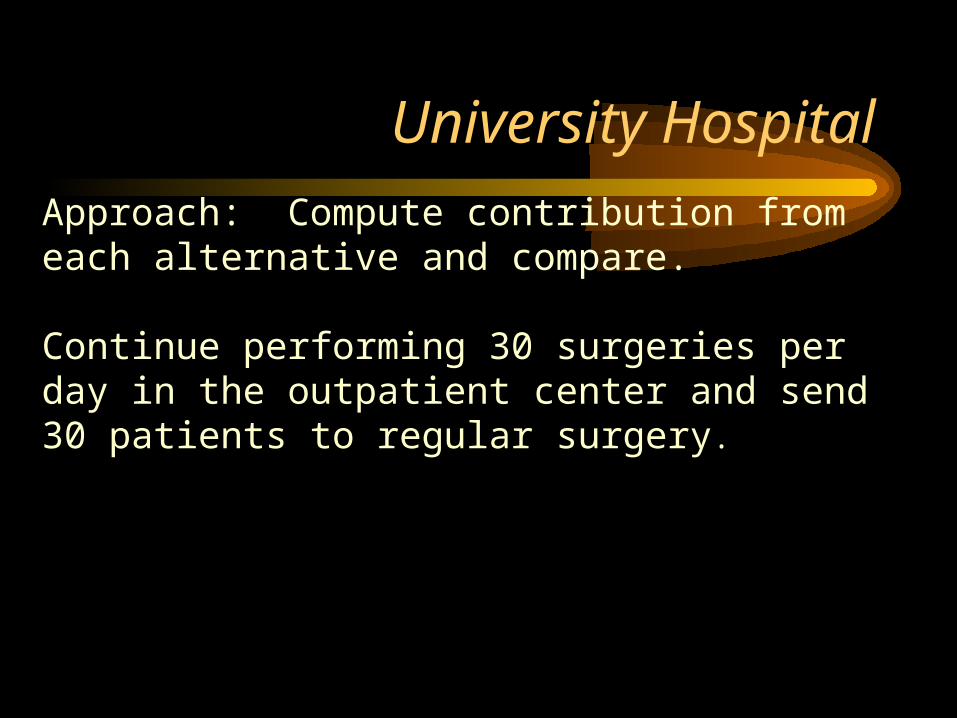

University HospitalApproach: Compute contribution from each alternative and compare.

Continue performing 30 surgeries per day in the outpatient center and send 30 patients to regular surgery.

University Hospital

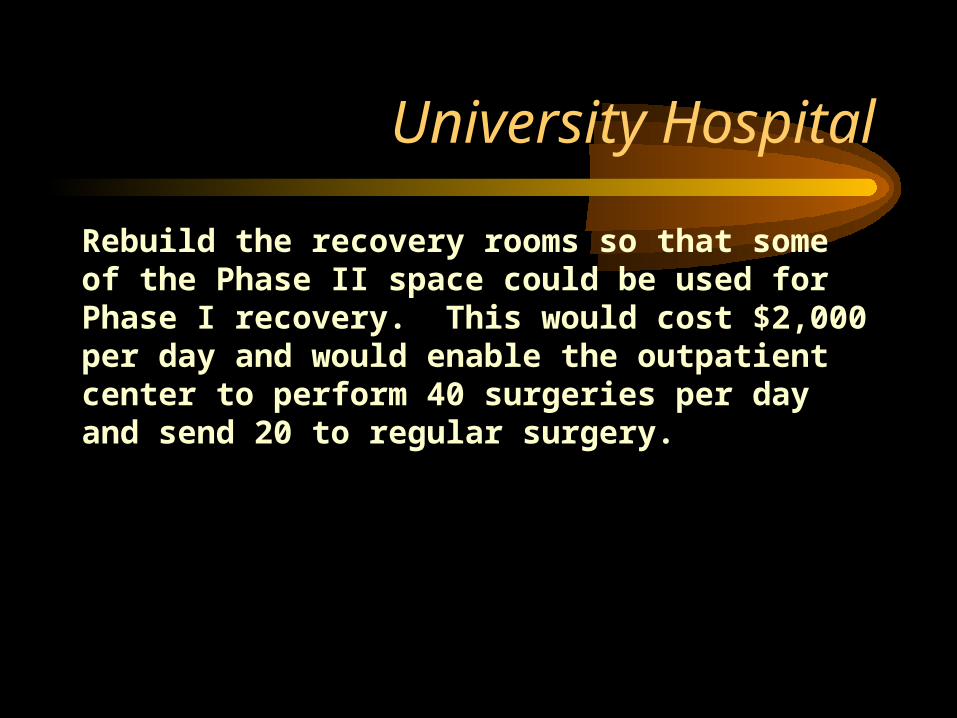

Rebuild the recovery rooms so that some of the Phase II space could be used for Phase I recovery. This would cost $2,000 per day and would enable the outpatient center to perform 40 surgeries per day and send 20 to regular surgery.

University Hospital

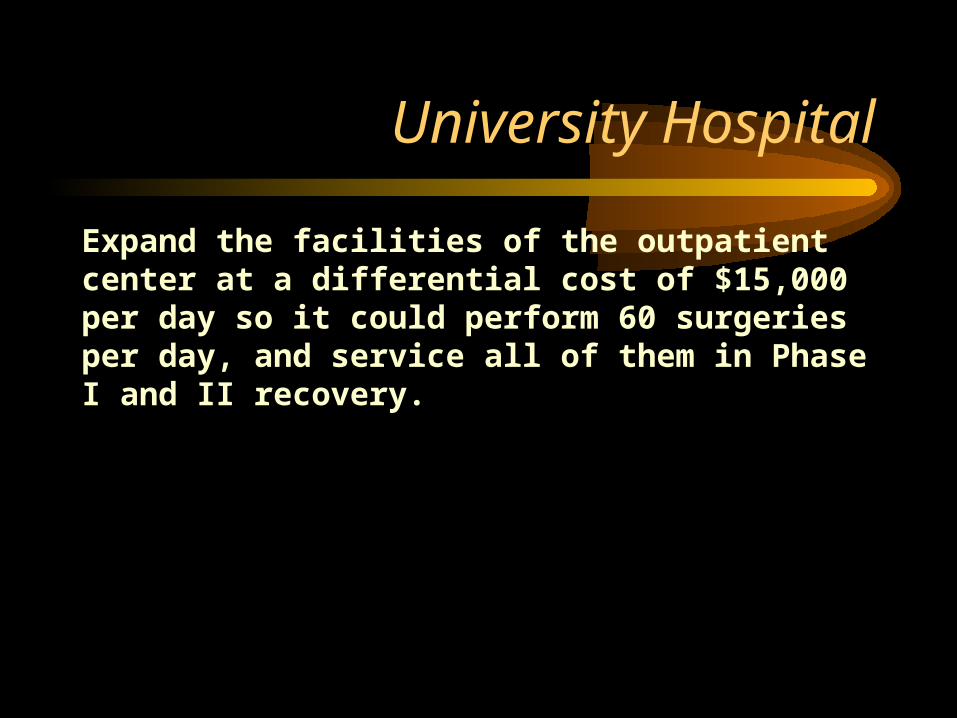

Expand the facilities of the outpatient center at a differential cost of $15,000 per day so it could perform 60 surgeries per day, and service all of them in Phase I and II recovery.

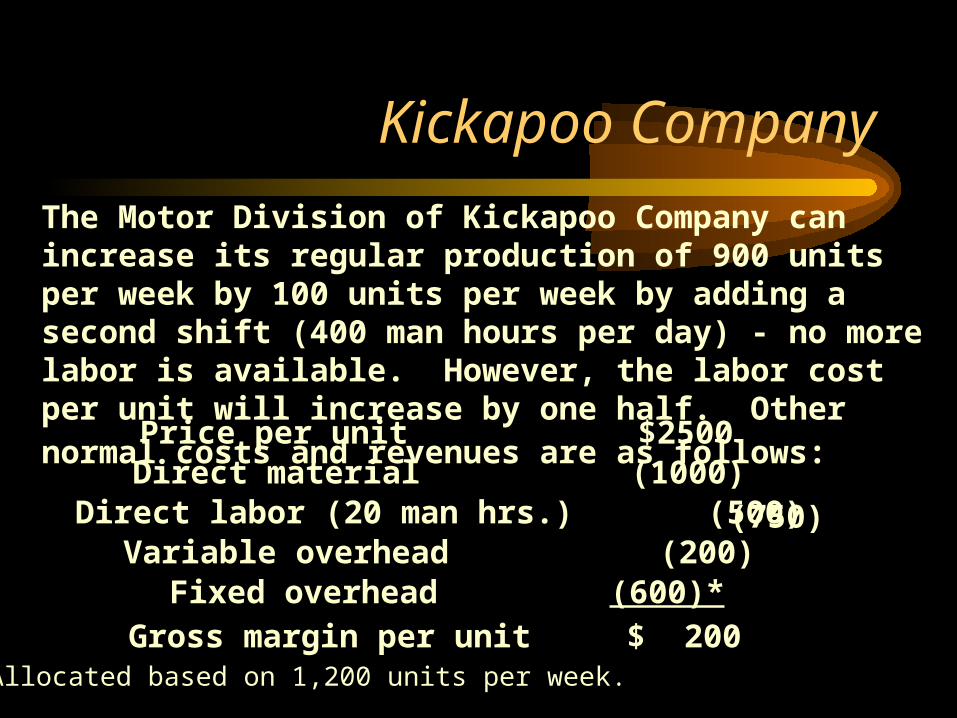

Kickapoo CompanyThe Motor Division of Kickapoo Company can increase its regular production of 900 units per week by 100 units per week by adding a second shift (400 man hours per day) - no more labor is available. However, the labor cost per unit will increase by one half. Other normal costs and revenues are as follows:

Price per unit $2500Direct material (1000)Direct labor (20 man hrs.) (500)Variable overhead (200)Fixed overhead (600)*Gross margin per unit $ 200

*Allocated based on 1,200 units per week.

(750)

Kickapoo Company

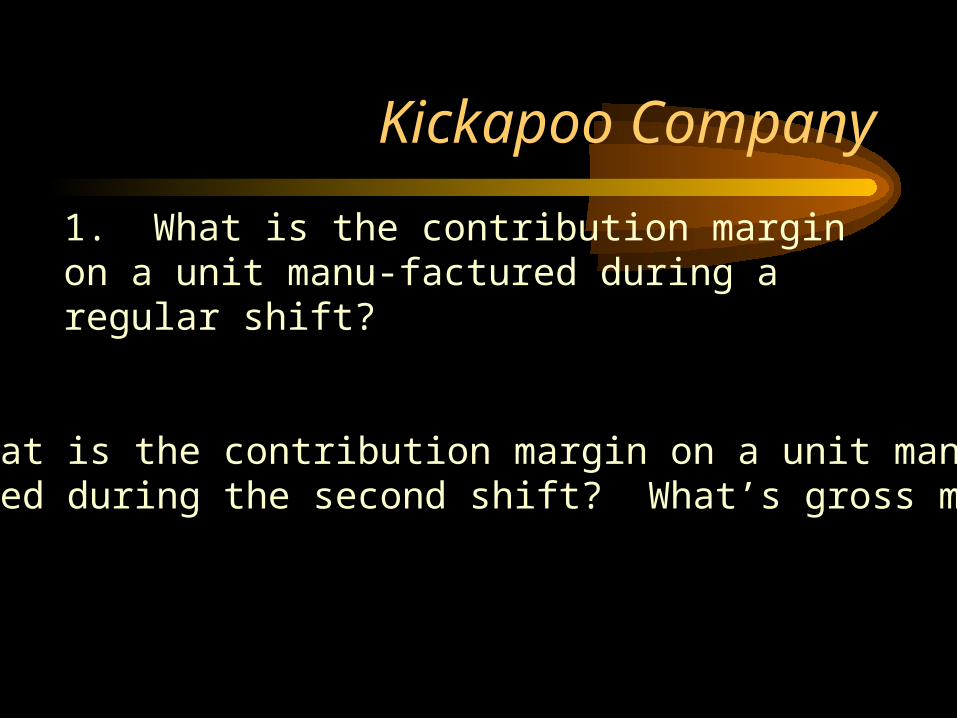

1. What is the contribution margin on a unit manu-factured during a regular shift?

2. What is the contribution margin on a unit manu-factured during the second shift? What’s gross margin?

Kickapoo Company: Motor Division Profit

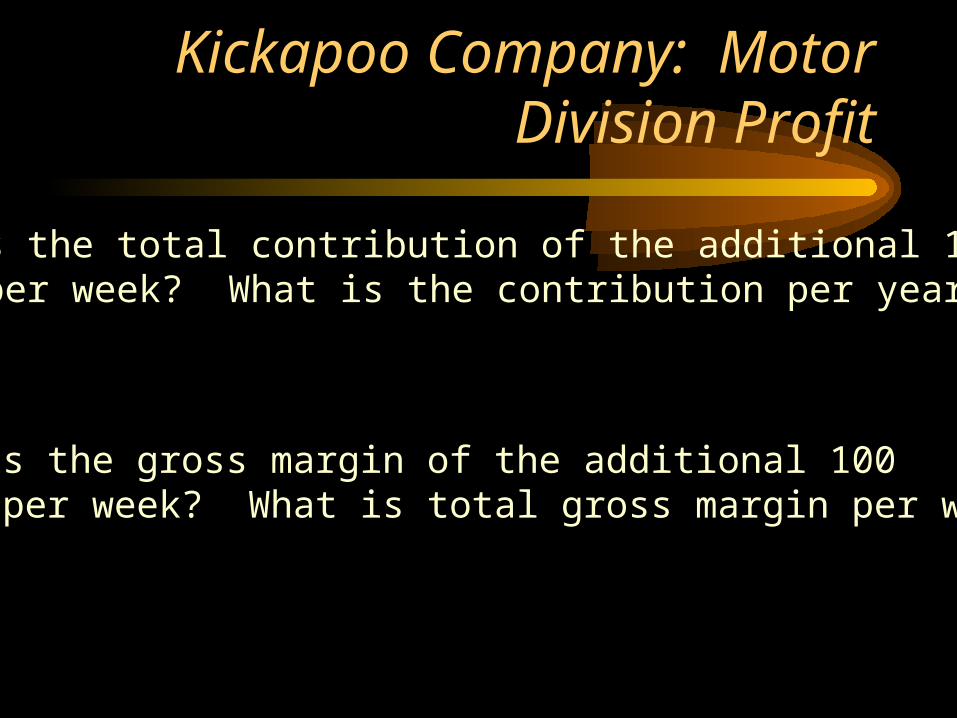

What is the total contribution of the additional 100units per week? What is the contribution per year?

What is the gross margin of the additional 100units per week? What is total gross margin per week?

Kickapoo Company: Company Profits

What is Kickapoo’s annual reported gross margin fromMotor’s product at normal production?

Kickapoo Company: Company Profit

What is Kickapoo’s annual income from Motor’s productwith the 100 unit per week increase?

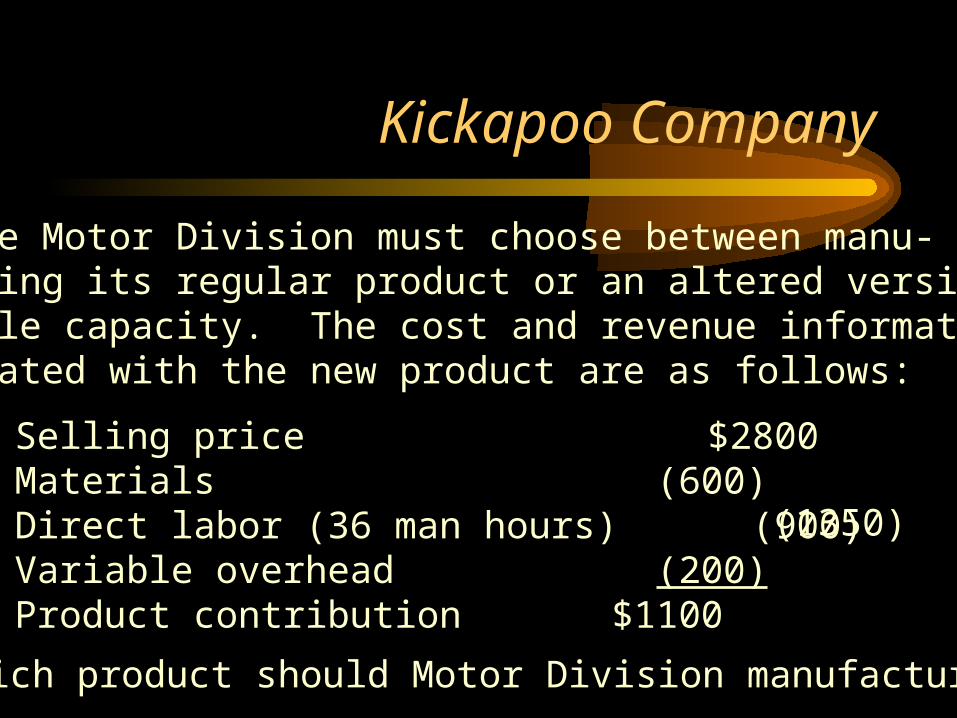

Kickapoo Company

Suppose Motor Division must choose between manu-facturing its regular product or an altered version usingits idle capacity. The cost and revenue informationassociated with the new product are as follows:

Selling price $2800Materials (600)Direct labor (36 man hours) (900)Variable overhead (200)Product contribution $1100

Which product should Motor Division manufacture?

(1350)

Kickapoo Company

Group work: Information Technology, Inc.

Answer questions (1) and (2) in your groups andhand in your answers at the end of the hour.

The best answer to part (2) requires a little creativethinking.