1. Right triangle PQR is to be constructed in the xy-plane so that the right angle is at P and PR is parallel to the x-axis. The x and y coordinates of P, Q and R are to be integers that satisfy the inequalities -4 <= x <= 5 and 6 <= y <= 16. How many different triangles with these properties could be constructed? (A) 110 (B) 1,100 (C) 9,900 (D) 10,000 (E) 12,100 Solution: No. of possible value for x=10 and y=11 1) information given is right angle at P, PR(ll) to x axis information inferred y coordinates of p and r is same. 2) PQ (llel) y therefore x coordinates of P and Q is same. For P x can be selected in 10 ways and y in 11 ways = 10*11 For R x in 9 ways and y in 1 way (as same of P) =9*1 For q x in 1 way and y in 10 ways (one already selected for P) =10*1 Total ways=10*11*9*10=9900 2. A password of a computer used five digits where they are from 0 and 9. What is the probability that the password solely consists ofprime numbers and zero? A 1/32 B 1/16 C 1/8 D 2/5 E ½ Solution: There are 10 possible options (0,1,2,3,4,5,6,7,8,9) for each digit. 5 of the options (0,2,3,5,7) are zero or prime. So, P(a given digit is zero orprime) = 5/10 = 1/2 A quick way is to look at this as an AND probability. P(all five digits are zero or prime) INTANGIBALE ASSSETS CAN BE TREATED IN THE SAME WAY AS FIXED ASSETS. THEY ARE NEEDED FOR OPERATION AND ARE ACQUIRED WITH ENTERPRISE FUNDS. EXAMPLE: PATENTS CAPITALIZED & MAY BE EXPENSED OVER A PERIOD OF TIME

Burn tables are CNC cutting torches, usually natural gas powered. Plasma and laser

cutting tables, and Water jet cutters, are also common. Plate steel is loaded on a table and the

parts are cut out as programmed. The support table is made of a grid of bars that can be

replaced. Some very expensive burn tables also include CNC punch capability, with a

carousel of different punches and taps. Fabrication of structural steel by plasma and laser

cutting introduces robots to move the cutting head in three dimensions around the material to

be cut.

the maximum output rate a process can achieve under ideal conditions” (Krajewski and Ritzman,

2003). The company believes that the CSI effectively communicates how well a process meets

customer specifications, and it provides more useful feedback to the production system. For

instance, a 65% of CSI in cutter operation was measured over a two-month period, which indicates

that only 65% of peak capacity was utilized to meet customer needs. In other words, 35% of

machine capacity was either wasted (due to setup, wait for material, maintenance, or breakdown) or

produced items that failed to meet customer specifications. The 65% of CSI was then used as a

baseline to measure the level of improvement made by this project. The goal (performance

outcome) established for this process was 80 percent of CSI, which was considered to be the

standard for world-class practice.

Once the measure and process capability for cutting operations was defined, the project

team proceeded to analyze the root cause of poor CSI performance. A Pareto analysis was nextperformed, and the team discovered that the cutter grinder accounted for 40% of machine

downtime on the cutting machines (Figure 3). The project team interviewed the operators and

found that, due to lack of proper lubrication of the blades, many cutting heads did not attain their

maximum life. Moreover, as the dull blades were removed for re-sharpening, cutter grinders

became idle and thus failed to keep up with the production schedule. Apparently, the dullness of the

blades caused substantial downtime at the cutters. Furthermore, a dull blade also resulted in many

defect-prone items including rough finish along the cutter lines and machine crash. In summary, the

root cause of poor CSI was found to be blade inefficiency, since it caused machine downtime and

defective cutter bodies.

Specifically, neither traditional unit cost reduction nor local operations productivity increase

was used to determine the improvement effort. Instead, the impact of the improvement on overall

quality of axle and system throughput was used to select the improvement project.

Figure 2 displays a simplified process flow of the Axle manufacturing. Following the TOC

approach, the project team first searched for the bottleneck by identifying operations associated

with large piles of inventory. Gear cutting operation was suspected to be the bottleneck. The

project team further interviewed the operators of the downstream operation, lapping, and

confirmed that lapping was constantly starving for competed ring set from the cutting operation.

Accordingly, cutting operation was determined to be the bottleneck and was chosen as the target

for improvement. Incorporating TOC concept into improvement process enabled the project team

to select a project that could increase the plant throughput and bottom-line performance.

(take in Figure 2)

Value analysis was first performed to determine the various activities in the cutter operation

that add both customer and operational value to the process (Table 1). The purpose of value

analysis is to streamline the value chain to reduce all non-value added waste in the system and to

look for ways to enhance high value-added activities. The machine cycle that includes the cutting

operation is both a customer and operational value-added activity. Improving the yield of a high-

value added activity such as blade cutting would increase the overall capacity of the plant.

Increasing the gear cutting capacity would have a positive impact on manufacturing system

throughput. This could be achieved through a reduction of hours required per gear set, which wouldin turn increase the capacity and remove the need for new capacity investments.

(take in Table 1)

After confirming gear cutters as the bottleneck, the project team initially discussed purchasing

additional cutting capacity. The company was using a solvent-cutting device, where the cutting head

was lubricated to increase the shelf life of the cutting blades. Newer technology in this process had

advanced to dry cutting, a significant increase in the life of the blade, thereby increasing the

capacity. However, with the capital constraints facing the plant, it was not feasible to upgrade to thedry cutting process. As suggested by the TOC concept, the team decided to “exploit” or maximize

the utilization of the current technology rather than make new capital investment in additional

cutting capacity. In other words, the team would proceed to investigate the current performance of

the solvent-based cutting machines and identifying ways to increase quality and throughput without

additional capital expenditures.

The business case for this project was initiated because of the eroding sales revenue, which

went down by 23% in 2000, while fixed expenses went up by as much as 22% within the same year.Management was faced with either shutting down the plant or eliminating the non-value added

processes to increase capacity without incurring new capital expenditures. The Axle facility had

some experience in successfully applying Six Sigma to its process improvement. After receiving

training on TOC, managers decided to combine TOC and Six Sigma to guide their improvement

effort. They felt that the concept of TOC could provide them with a focus on global system

improvement. With careful study and planning, an eight-member project team was formed. The

project team was composed of the plant manager, the controller, two six-sigma certified employees,

and four operators from the plant. One of the authors of this paper and a student team served as

external resources for the project. The team was charged with the responsibility of seeking process

improvement that would result in a minimum of $175,000 savings per year. This was the minimum

standard established by the plant for any major process improvement project. The team started by

reviewing the process map to determine possible bottlenecks in the process. Extensive interviews

were conducted, and an in-depth observation of the processes was undertaken to identify probable

causes of inefficiencies in the system. After the extensive investigation, the cutting process was

singled out as the likely bottleneck operation. The proposed integrated framework was adopted to

make the improvement. The various stages of the process implementation are discussed below.

Phase 1 of this integrated framework is identical to both strategies, and its purpose is to

identify current constraint(s) that block the improvement of global performance, such as meeting

customer needs or improving system throughput. Accordingly, a specific process is selected for

improvement. Phases 2 and 3 follow the spirit of TOC by exploring the capacity of the selected

process. Phase 2 measures the current performance of the process and identifies the root causes

needed to be corrected for improvement. The two phases of Six Sigma, measure and analyze, are

involved in this step. Once the root causes are confirmed, Phase 3 of the integrated approach

applies conventional Six Sigma strategy by using the key manufacturing, engineering, and statistical

techniques to remove root causes of the problem for making necessary process improvement. The

purpose is to best utilize the current capacity of the process without incurring additional capital

expenditures.

Phase 4 ensures the changes made in previous steps are properly supported by the rest of the

system. For example, managers may need to change policies and obtain buy-in from employees to

implement the changes. Training is often required for a revised process. Phases 5 and 6 are taken

from the TOC process. If the improvement of the selected process is insufficient to satisfy customer

needs or goals, managers have to consider various options (e.g., outsourcing and additional

investment) to raise the capacity of the process. Finally, managers must stay alert to the dynamic

nature of the manufacturing system and constantly monitor occurrence of new constraints.

Overall, when the integrated framework is applied to improve a specific process, these two

techniques seem to complement each other. The integration is made by combining the

management aspect of TOC and the engineering aspect of Six Sigma. Specifically, for firms that

apply Six Sigma, TOC provides a global perspective in identifying the constraints and examining

necessary changes to the rest of the systems. On the other hand, Six Sigma brings in the

perspectives of customer needs, performance measures, and engineering and statistical tools duringthe stages Theory of Constraints (TOC) was developed by Eliyahu M. Goldratt during the 1980s

(McMullen, 1998). The core idea of TOC is that every organization has at least one constraint that

prevents management from achieving the goal of the organization to a larger degree. Constraints

can be physical resources or policies. TOC develops a set of procedures and methodologies to

identify and optimize such constraints. For the purpose of continuous improvement, TOC uses a

systematic approach which consists of five focusing steps (Goldratt and Cox, 1992).

1. Identify the system’s constraint(s).

2. Decide how to exploit the system’s constraint(s).

3. Subordinate everything else to the above decision.

4. Elevate the system’s constraint(s).

5. If a constraint has been broken, go back to Step 1. Do not allow inertia to cause a

system’s constraint.

The implementation of Six Sigma strategy involves a series of steps specifically designed to

facilitate a process of continuous improvement. The strategy takes the key manufacturing,

engineering, and transactional processes of entire process through the five transformational phases

(Plotkin, 1999).

1. Define: Identify customer needs and a project suitable for Six-Sigma effort.

2. Measure: Determine what and how to measure the performance of the selected process.

3. Analyze: Understand and determine the variables that create quality variations.

4. Improve: Identify means to remove causes of defects and modify the process.

5. Control: Maintain the improvement.

The primary objective of the five-step process is to recognize critical customer requirements,

identify and validate the improvement opportunity, and upgrade the business processes. A

large number of companies have boosted their profitability, increased market share, and

improved customer satisfaction through the implementation of Six-Sigma. Companies such

as Allied Signal, General Electric, Sony, Texas Instruments, Bombadier, Crane Co.,

Lockheed Martin, and Caterpillar are beginning to dir

The swot anlysis of the Perpetual Inventory System is as under:

STREGTHS:

Accurate Reporti ng

Companies often experience more accurate financial reporting with a perpetualinventory system. Accountants update the general ledger after each inventorytransaction. This results in a general ledger account that closely mirrors the actual

physical inventory on hand. Owners and managers can then make quality decisions based on the accuracy of reporting inventory values. Multiple inventory types also

benefit from this method, as accountants accurately track each one through thegeneral ledger.

Electronic Management

Perpetual inventory systems often use electronic methods to record transactions. Anexample is the barcode system a clothing retailer uses when selling goods. Each scanrecords data that updates the company's inventory value. Accountants use thisinformation to balance the general ledger. Companies also use the data to order goodsusing a just-in-time system. Electronic ordering helps to prevent stock outs and lostsales.

WEAKNESSES:

Cost

Many perpetual inventory systems are expensive. The cost for these systems istwofold. The technology necessary to make the system work can be a major capitalexpense. Updating the system for new changes to the technology is also costly.Training employees to properly use the system is yet another expense. On theadministrative side, companies must find accountants who can work the system andmanage frequent changes to the general ledger.

Process

Perpetual inventory systems are often time-consuming. Electronic updates to acompany's general ledger may result in a need for account reconciliations.Accountants will often spend copious hours each week or month to reconcileinventory. Persistent errors can also cause further complications. Accountants need tocorrect errors and balance the inventory account prior to closing the company's books.Reporting inaccurate inventory figures can trigger an audit, resulting in potential

problems for the company.

Additional record-keeping Increase workload, increase in staff. Additional costs Staff

costs, costs of computer package to maintain inventory records.

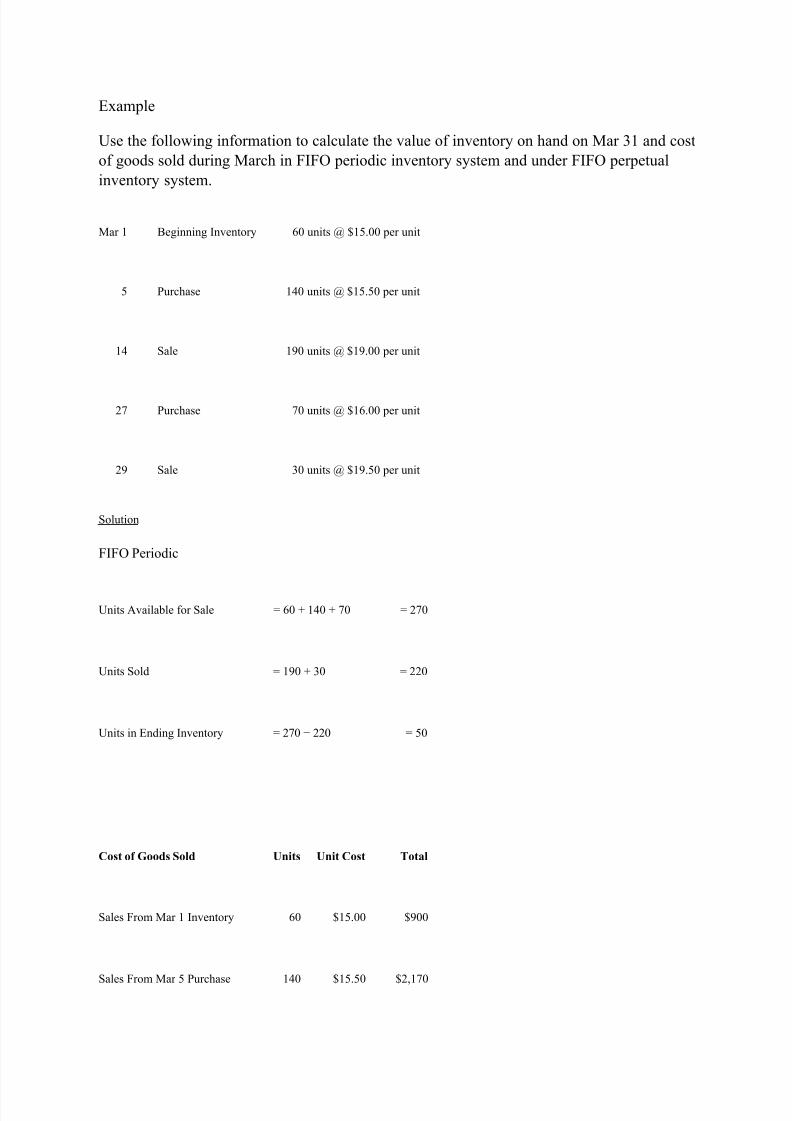

First-In, First-Out (FIFO) is one of the methods commonly used to calculate the value of

inventory on hand at the end of a period and the cost of goods sold during the period. This

method assumes that inventory purchased or manufactured first is sold first and newer

inventory remains unsold. Thus cost of older inventory is assigned to cost of goods sold and

that of newer inventory is assigned to ending inventory. The actual flow of inventory may not

exactly match the first-in, first-out pattern.

First-In, First-Out method can be applied in both the periodic inventory system and the

up-to-date inventory balance information and requiring a reduced level of physical inventory

counts. However, the calculated inventory levels derived by a perpetual inventory system

may gradually diverge from actual inventory levels, due to unrecorded transactions or theft,

so you should periodically compare book balances to actual on-hand quantities.

Perpetual inventory is by far the preferred method for tracking inventory, since it can yield

reasonably accurate results on an ongoing basis, if properly managed. The system works best

when coupled with a computer database of inventory quantities and bin locations, which is

updated in real time by the warehouse staff using wireless bar code scanners, or by sales

clerks using point of sale terminals. It is least effective when changes are recorded on

inventory cards, since there is a significant chance that entries will not be made, or will be

made incorrectly.

Balance sheets complete the sequence of accounts, showing the ultimate result of the entriesin the production, distribution and use of income, and accumulation accounts.Balance sheets and accumulation accounts form a group of accounts that are concerned withthe value of assets owned by institutional units or sectors, and their liabilities at particular

points in time and with the evolution of those values over time. Balance sheets measure thevalues of stocks and are compiled at the beginning and end of the accounting period. On theother hand, the accumulation accounts record the changes in the values of assets and

liabilities during the accounting period. They are flow accounts, whose entries depend on theamounts of economic or other activities that take place within a given period of time.In the balance sheets three categories of assets are distinguished:a) non-financial produced assets

b) non-financial non-produced assetsc) financial assets

(i) Periodic stock verification

(ii) Continuous stock verification

(i) Periodic stock verification: It refers to a system where physical stock verification isnormally done periodically, i.e., once or twice in a year. Under this method, value of stock isdetermined by physical counting of the stock on a particular date, usually at the end of theyear.

It is a simple and economical method of stock-taking and is adopted in small concerns. Thistype of verification is good only for the items which do not find place in the perpetualinventory records, e.g., works-in-progress, components and consumable stores at site etc. Butthere are many limitations of this method. Stores may' be closed down for a few days tofacilitate stock-taking. There is possibility of fraud] discrepancy, etc.

(ii) Continuous stock verification: This system comprises of counting and verifying i number

of items at random daily throughout the year so that all items of stores are verified several

times during the year. Notice of the particular stock to be verified each clay is given to thestore-keeper only on the date of actual verification.

As there is an element of surprise check in this system of stock-taking, effective control over the items of stores can be exercised. The system does not necessitate the closing down of the

stores to facilitate stock-taking. There is also less possibility of fraud and discrepancy, but themethod is expensive and is adopted by big concerns only.

The actual stock of material should not differ from the recorded stock under normalcircumstances. But-sometimes differences arise due to the following reasons:

(i) Breakage and wastage of materials due to improper handling.

(ii) Shrinkage and evaporation.

In earlier periods, non-continuous, or periodic inventory systems were more prevalent.Starting in the 1970s digital computers made possible the ability to implement a perpetualinventory system. This has been facilitated by bar coding and lately radio frequencyidentification (RFID) labeling which allows computer systems to quickly read and processinventory information as part of transaction processing.

Perpetual inventory systems can still be vulnerable to errors due to overstatements (phantominventory) or understatements (missing inventory) that can occur as a result of theft, breakage,scanning errors or untracked inventory movements, leading to systematic errors inreplenishment.

The ESA95 recommends the Perpetual Inventory Method (PIM) for the calculation of thestock of Fixed assets whenever direct information is missing (par. 6.04). The calculation of consumption of Fixed capital can be based on these stocks of assets. Besides net capital stock which appears in the Balance sheets can be derived within a PIM approach. In this paragraphthe basic principles of the PIM will be discussed. Using the PIM, gross capital stock iscalculated as the sum of gross fixed capital formation in Previous years, of which the servicelive is not yet expired. In the simplest case it is assumed that the total investment of a

particular asset does not deteriorate during the expected service life of that asset and isdiscarded as a whole after that period of time.

Becoming a preferred employer involves more than learning the characteristics of such an

organization, however—it also requires that you understand what top performers want and

value in a relationship with an employer. Interestingly, the answers to both questions are the

same.

To begin with, top-tier employers offer more than competitive pay and benefits. In fact, the

word "competitive" implies that you're simply matching what many other businesses are

providing. Even important additional elements, such as a good environment and open