12

SECOND QUARTER 2018 PHILIPPINE REPORT CONSTRUCTION MARKET QUARTERLY UPDATE

SECOND QUARTER 2018

PHILIPPINE REPORTCONSTRUCTION MARKETQUARTERLY UPDATE

TABLE OF CONTENTS

The Lerato Tower 3Makati City

MARKET SUMMARY 1

The Philippine Economy 1

Foreign Direct Investments 2

Philippine Construction 3

CONSTRUCTION MARKET ACTIVITY 4

Construction Market 5 Activity Cycle

COMMODITY PRICE TRENDS 6

Metal Prices 6

Steel Reinforcements 6

Crude Oil Prices 6

MATERIAL PRICE TRENDS 7

Retail Price Index 7

Currency Exchange Rates 7

CONSTRUCTION PRICES 8

PROFESSIONAL SERVICES 9

1Rider Levett Bucknall | Construction Market Quarterly Update 2018 Second Quarter

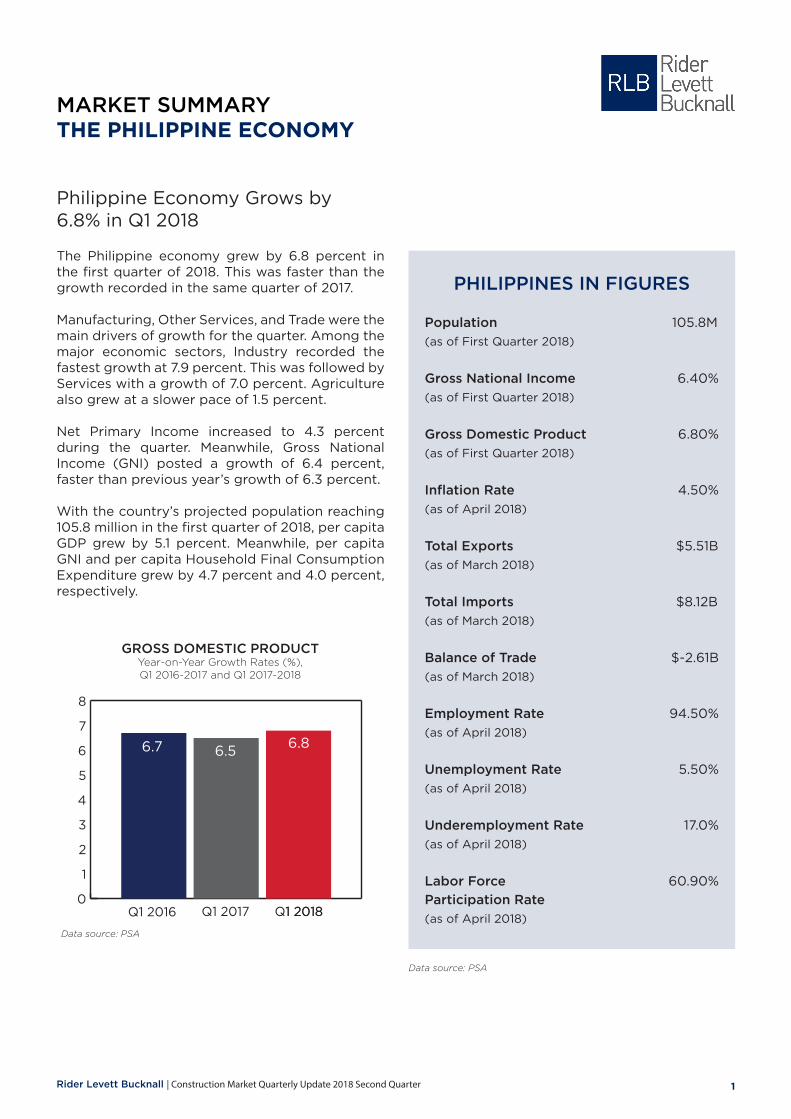

The Philippine economy grew by 6.8 percent in the first quarter of 2018. This was faster than the growth recorded in the same quarter of 2017.

Manufacturing, Other Services, and Trade were the main drivers of growth for the quarter. Among the major economic sectors, Industry recorded the fastest growth at 7.9 percent. This was followed by Services with a growth of 7.0 percent. Agriculture also grew at a slower pace of 1.5 percent.

Net Primary Income increased to 4.3 percent during the quarter. Meanwhile, Gross National Income (GNI) posted a growth of 6.4 percent, faster than previous year’s growth of 6.3 percent.

With the country’s projected population reaching 105.8 million in the first quarter of 2018, per capita GDP grew by 5.1 percent. Meanwhile, per capita GNI and per capita Household Final Consumption Expenditure grew by 4.7 percent and 4.0 percent, respectively.

Philippine Economy Grows by 6.8% in Q1 2018

GROSS DOMESTIC PRODUCTYear-on-Year Growth Rates (%), Q1 2016-2017 and Q1 2017-2018

MARKET SUMMARYTHE PHILIPPINE ECONOMY

PHILIPPINES IN FIGURES

Population 105.8M

(as of First Quarter 2018)

Gross National Income 6.40%

(as of First Quarter 2018)

Gross Domestic Product 6.80%

(as of First Quarter 2018)

Inflation Rate 4.50%

(as of April 2018)

Total Exports $5.51B

(as of March 2018)

Total Imports $8.12B

(as of March 2018)

Balance of Trade $-2.61B

(as of March 2018)

Employment Rate 94.50%

(as of April 2018)

Unemployment Rate 5.50%

(as of April 2018)

Underemployment Rate 17.0%

(as of April 2018)

Labor Force 60.90%

Participation Rate

(as of April 2018)Data source: PSA

Data source: PSA

0

1

2

3

4

5

6

7

8

6.7 6.56.8

Q1 2016 Q1 2017 Q1 2018Q1 2018

2 Construction Market Quarterly Update 2018 Second Quarter | Rider Levett Bucknall

MARKET SUMMARYFOREIGN DIRECT INVESTMENTS

Total foreign investments (FI) approved in the first quarter of 2018 by the seven investment promotion agencies (IPAs), namely: Board of Investments (BOI), Clark Development Corporation (CDC), Philippine Economic Zone Authority (PEZA), and Subic Bay Metropolitan Authority (SBMA) as well as the Authority of the Freeport Area of Bataan (AFAB), BOI-Autonomous Region of Muslim Mindanao (BOI-ARMM), and Cagayan Economic Zone Authority (CEZA) amounted to PhP 14.2 billion. This was 37.9 percent lower compared with the PhP 22.9 billion approved in the same period last year.

Among the top investing counries, during the quarter, Japan topped with PhP 7.9 billion accounting for 55.3 percent of the total FI commitments. United Kingdom and Netherlands came in second and third pledging PhP 1.5 billion and Php 878.5 million, or 10.9 percent and 6.2 percent of the total approved FI, respectively.

Manufacturing bested all other industries as it stands to receive 64.1 percent of total FI pledges or PhP 9.1 billion. Administrative and Support Service Activities came in second with investment commitments valued at PhP 1.80 billion, or 12.7 percent of the total FI. Real Estate Activities followed with PhP 1.81 billion, or 12.6 percent of the total FI.

In terms of location, majority of the approved foreign investments in the first quarter of 2018 would be intended to finance projects in CALABARZON amounting to PhP 7.4 billion or 52.0 percent. This was followed by the National Capital Region with PhP 3.2 billion or 22.5 percent, and Northern Mindanao with PhP 1.6 billion or 11.5 percent.

Approved investments of foreign and Filipino nationals in the first quarter of 2018 grew by 52.3 percent, nearly PhP 185.0 billion from PhP 121.5 billion in the same period last year. Filipino nationals shared PhP 170.8 billion worth of investments pledges or 92.3 percent of the total approved investments during the quarter.

Foreign and Filipino projects approved by the seven IPAs in the first quarter of 2018 are expected to generate 33,704 jobs. This is 38.4 percent lower compared with previous year’s projected employment. Out of these anticipated jobs, 66.9 percent or 22,535 jobs would come from projects with foreign interest.

Committed FI Reached P14.2B in Q1 2018

TOTAL APPROVED FOREIGN INVESTMENT BY COUNTRY

OF INVESTORFirst Quarter 2018

TOTAL APPROVED FOREIGN INVESTMENT BY INDUSTRY

First Quarter 2018

Data source: PSA

Data source: PSA

Japan 55.3%

UK

10.9%

Netherlands

6.2%

Singapore 4.0%

USA

3.9%

China (PROC) 3.0%

South Korea 2.8%

Australia

2.3%

Taiwan

2.2%

Manufacturing 64.1%

Admin and Support 12.7%

Real Estate

12.6%

3Rider Levett Bucknall | Construction Market Quarterly Update 2018 Second Quarter

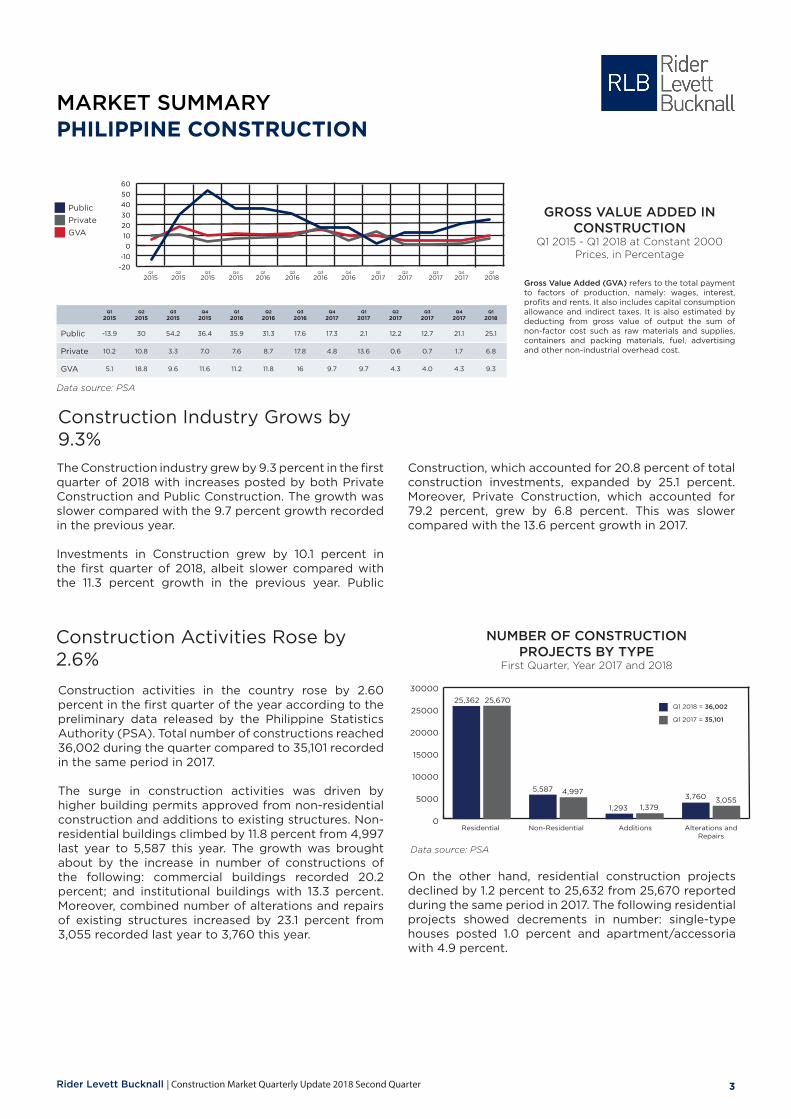

Construction Industry Grows by 9.3%

MARKET SUMMARYPHILIPPINE CONSTRUCTION

Construction activities in the country rose by 2.60 percent in the first quarter of the year according to the preliminary data released by the Philippine Statistics Authority (PSA). Total number of constructions reached 36,002 during the quarter compared to 35,101 recorded in the same period in 2017.

The surge in construction activities was driven by higher building permits approved from non-residential construction and additions to existing structures. Non-residential buildings climbed by 11.8 percent from 4,997 last year to 5,587 this year. The growth was brought about by the increase in number of constructions of the following: commercial buildings recorded 20.2 percent; and institutional buildings with 13.3 percent. Moreover, combined number of alterations and repairs of existing structures increased by 23.1 percent from 3,055 recorded last year to 3,760 this year.

Construction Activities Rose by 2.6%

On the other hand, residential construction projects declined by 1.2 percent to 25,632 from 25,670 reported during the same period in 2017. The following residential projects showed decrements in number: single-type houses posted 1.0 percent and apartment/accessoria with 4.9 percent.

The Construction industry grew by 9.3 percent in the first quarter of 2018 with increases posted by both Private Construction and Public Construction. The growth was slower compared with the 9.7 percent growth recorded in the previous year.

Investments in Construction grew by 10.1 percent in the first quarter of 2018, albeit slower compared with the 11.3 percent growth in the previous year. Public

Construction, which accounted for 20.8 percent of total construction investments, expanded by 25.1 percent. Moreover, Private Construction, which accounted for 79.2 percent, grew by 6.8 percent. This was slower compared with the 13.6 percent growth in 2017.

Gross Value Added (GVA) refers to the total payment to factors of production, namely: wages, interest, profits and rents. It also includes capital consumption allowance and indirect taxes. It is also estimated by deducting from gross value of output the sum of non-factor cost such as raw materials and supplies, containers and packing materials, fuel, advertising and other non-industrial overhead cost.

GROSS VALUE ADDED IN CONSTRUCTION

Q1 2015 - Q1 2018 at Constant 2000 Prices, in Percentage

NUMBER OF CONSTRUCTION PROJECTS BY TYPE

First Quarter, Year 2017 and 2018

Q1

2015Q2

2015Q3

2015Q4

2015Q1

2016Q2

2016Q3

2016Q4

2017Q1

2017Q2

2017Q3

2017Q4

2017Q1

2018

Public -13.9 30 54.2 36.4 35.9 31.3 17.6 17.3 2.1 12.2 12.7 21.1 25.1

Private 10.2 10.8 3.3 7.0 7.6 8.7 17.8 4.8 13.6 0.6 0.7 1.7 6.8

GVA 5.1 18.8 9.6 11.6 11.2 11.8 16 9.7 9.7 4.3 4.0 4.3 9.3

Data source: PSA

Data source: PSA

Q4

2017Q3

2017Q2

2017Q1

2017Q4

2016Q3

2016Q2

2016Q1

2016Q4

2015Q3

2015Q2

2015Q1

2015

Public

Private GVA

-20

-10

0

10

20

30

40

50

60

Q1

2018

0

5000

10000

15000

20000

25000

30000

25,362 25,670

5,587 4,997

1,293 1,379

3,760 3,055

Q1 2018 = 36,002

Q1 2017 = 35,101

Residential Non-Residential Additions Alterations andRepairs

4 Construction Market Quarterly Update 2018 Second Quarter | Rider Levett Bucknall

MARKET SUMMARYPHILIPPINE CONSTRUCTION

CONSTRUCTION MARKET ACTIVITY

TOP 5 REGIONS WITH THE HIGHEST NUMBER OF

CONSTRUCTION PROJECTSFirst Quarter 2018

DISTRIBUTION OF CONSTRUCTION PROJECTS BY REGIONFirst Quarter 2018

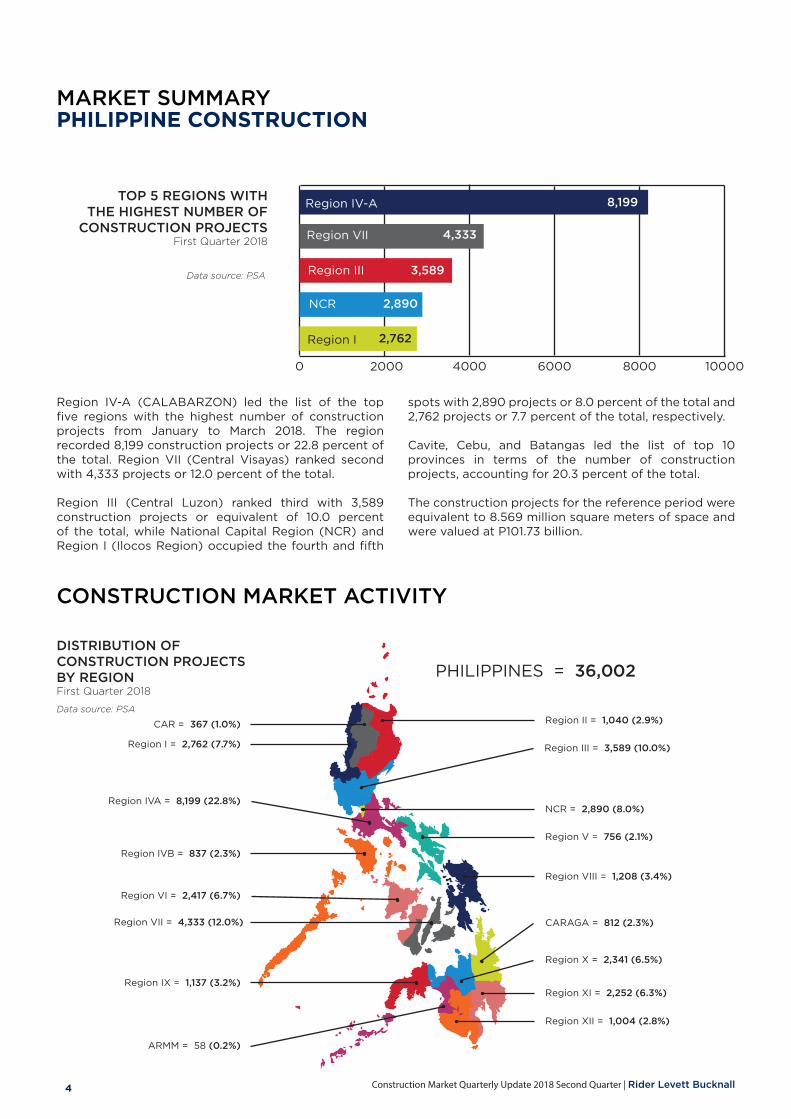

Region IV-A (CALABARZON) led the list of the top five regions with the highest number of construction projects from January to March 2018. The region recorded 8,199 construction projects or 22.8 percent of the total. Region VII (Central Visayas) ranked second with 4,333 projects or 12.0 percent of the total.

Region III (Central Luzon) ranked third with 3,589 construction projects or equivalent of 10.0 percent of the total, while National Capital Region (NCR) and Region I (Ilocos Region) occupied the fourth and fifth

spots with 2,890 projects or 8.0 percent of the total and 2,762 projects or 7.7 percent of the total, respectively.

Cavite, Cebu, and Batangas led the list of top 10 provinces in terms of the number of construction projects, accounting for 20.3 percent of the total.

The construction projects for the reference period were equivalent to 8.569 million square meters of space and were valued at P101.73 billion.

Data source: PSA

Data source: PSARegion II = 1,040 (2.9%)CAR = 367 (1.0%)

Region I = 2,762 (7.7%)

Region IVA = 8,199 (22.8%)

Region IVB = 837 (2.3%)

Region VI = 2,417 (6.7%)

Region VII = 4,333 (12.0%)

Region IX = 1,137 (3.2%)

ARMM = 58 (0.2%)

Region III = 3,589 (10.0%)

NCR = 2,890 (8.0%)

Region V = 756 (2.1%)

Region VIII = 1,208 (3.4%)

CARAGA = 812 (2.3%)

Region X = 2,341 (6.5%)

Region XI = 2,252 (6.3%)

Region XII = 1,004 (2.8%)

PHILIPPINES = 36,002

0 4000 6000 8000 10000

Region IV-A 8,199

Region VII 4,333

Region III 3,589

NCR 2,890

Region I 2,762

2000

5Rider Levett Bucknall | Construction Market Quarterly Update 2018 Second Quarter

CONSTRUCTION MARKET ACTIVITYCONSTRUCTION MARKET ACTIVITY CYCLE

RLB CONSTRUCTION MARKET ACTIVITY CYCLEFirst Quarter

Activity within the construction industry traditionally has been subject to volatile cyclical fluctuations.

The RLB Construction Sector Activity Cycle represents the construction development activity cycle. The chart below shows the relative level of activity for various sectors of the construction industry in each RLB Philippines’ main and satellite offices in the country.

Each sector is categorised by three positions within the cycle; Peak, Mid and Trough. Within each position, activity is further defined by either declining or growing within that sector.

The “up” and “down” arrows highlight the current status within the three positions of the cycle by means of the three colours identified in the cycle diagram below.

MID

GR

OW

TH

PEAK

TROUGH

DE

CL

INE

KEY CITIES HOUSES APARTMENTS OFFICES INDUSTRIAL RETAIL HOTEL

METRO MANILA

CLARK

SUBIC

LAGUNA

ILOILO

BACOLOD

BOHOL

CEBU

CAGAYAN DE ORO

DAVAO

6 Construction Market Quarterly Update 2018 Second Quarter | Rider Levett Bucknall

COMMODITY PRICE TRENDS

METAL APR2017

MAY2017

JUN2017

JUL2017

AUG2017

SEP2017

OCT2017

NOV2017

DEC2017

JAN2018

FEB2018

MAR2018

APR2018

Copper 5,684 5,600 5,720 5,985 6,486 6,577 6,808 6,827 6,834 7,066 7,007 6,799 6,852

Aluminum 1,921 1,913 1,885 1,903 2,030 2,096 2,131 2,097 2,080 2,210 2,182 2,069 2,255

Steel 657 646 635 635 658 689 677 673 689 717 750 DATA NOT AVAILABLE

DATA NOT AVAILABLE

METAL APR2017

MAY2017

JUN2017

JUL2017

AUG2017

SEP2017

OCT2017

NOV2017

DEC2017

JAN2018

FEB2018

MAR2018

APR2018

Rebar 502 497 498 509 530 579 581 576 598 616 632 DATA NOT AVAILABLE

DATA NOT AVAILABLE

METAL APR2017

MAY2017

JUN2017

JUL2017

AUG2017

SEP2017

OCT2017

NOV2017

DEC2017

JAN2018

FEB2018

MAR2018

APR2018

Crude Oil 52.2 49.9 46.2 47.7 49.9 53 54.9 59.9 61.2 66.2 63.5 64.2 68.8

METAL PRICESApril 2017 - April 2018

Data Source: World Bank and MEPS

STEEL REINFORCEMENTSApril 2017 - April 2018

Description: Rebar (conrete reinforcing bars) (Japan) producers’ export contracts (3 to 12 months terms) fob mainly to Asia, US Dollars per Tonne.

CRUDE OIL PRICESApril 2017 - April 2018

Description: Crude Oil (petroleum), simple average of three spot prices; Dated Brent, West Texas Intermediate, and the Dubai Fateh, US Dollars per Barrel

METAL PRICES

STEEL REINFORCEMENTS

CRUDE OIL PRICES

0

1000

2000

3000

4000

5000

6000

7000

8000

400

500

600

700

800

40

50

60

70

80

7Rider Levett Bucknall | Construction Market Quarterly Update 2018 Second Quarter

MATERIAL PRICE TRENDS

MATERIALS APR2017

MAY2017

JUN2017

JUL2017

AUG2017

SEP2017

OCT2017

NOV2017

DEC2017

JAN2018

FEB2018

MAR2018

APRIL2018

Carpentry 157.2 157.2 157.2 157.2 158.1 158.5 158.6 159.0 159.1 159.3 159.5 161.3 162.8

Electrical 209.0 208.9 208.9 209.0 209.7 210.3 209.8 211.0 211.1 211.2 210.9 211.3 211.7

Masonry 195.5 195.4 195.4 198.2 199.1 199.4 199.0 199.5 199.5 200.1 200.3 201.0 201.5

Painting 189.0 189.0 189.5 189.9 191.0 191.0 191.0 190.9 190.7 191.0 191.1 191.8 191.9

Plumbing 169.7 169.7 169.5 169.8 169.7 169.9 170.3 170.4 170.6 170.9 170.5 171.5 172.0

Tinsmithry 146.0 146.3 146.3 146.3 146.7 146.7 146.7 147.1 147.2 147.5 147.9 148.0 148.2

Miscellaneous 289.7 289.8 292.6 295.1 298.8 301.5 304.7 307.6 310.9 312.2 312.9 313.9 313.3

CURRENCYUNITS PER USD

UNIT APR2017

MAY2017

JUN2017

JUL2017

AUG2017

SEP2017

OCT2017

NOV2017

DEC2017

JAN2018

FEB2018

MAR2018

APR2018

PhilippinePeso ₱ 1 49.7 49.87 50.47 50.58 51.17 51.07 51.80 50.37 49.92 51.42 52.03 52.20 52.00

SingaporeDollar $ 1 1.4 1.38 1.38 1.36 1.36 1.36 1.36 1.35 1.34 1.31 1.33 1.31 1.32

UK PoundSterling £ 1 1.29 1.28 1.3 1.31 1.29 1.33 1.32 1.34 1.35 1.42 1.40 1.41 1.37

AustralianDollar $ 1 0.75 0.75 0.77 0.8 0.79 0.78 0.77 0.76 0.78 0.81 0.80 0.80 0.80

CanadianDollar $ 1 1.37 1.35 1.30 1.25 1.25 1.25 1.29 1.29 1.26 1.23 1.30 1.30 1.28

JapaneseYen ¥ 1 111.25 110.95 111.94 110.55 110.5 112.66 113.15 112.00 112.90 108.84 107.32 106.19 109.31

Korean Won ₱ 1 1,130.10 1,123.90 1,139.60 1,119.10 1,122.80 1,146.70 1,125.00 1,082.40 1,071.40 1,071.50 1,071.00 1,066.50 1,076.20

ThailandBaht ₱ 1 34.62 34.08 33.98 33.31 33.21 33.37 33.22 32.62 32.66 31.36 31.46 31.22 31.51

NetherlandsEuro ₱ 1 1.09 1.12 1.14 1.17 1.18 1.18 1.16 1.18 1.20 1.25 1.22 1.23 1.21

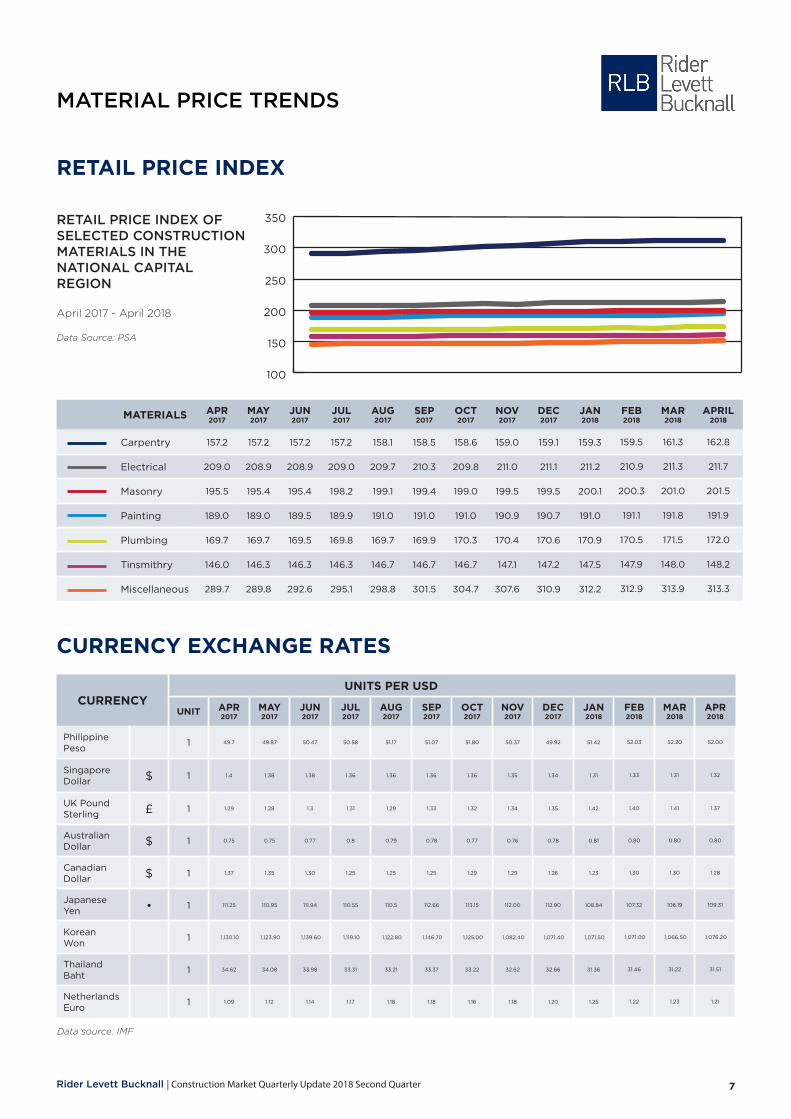

RETAIL PRICE INDEX OF SELECTED CONSTRUCTION MATERIALS IN THE NATIONAL CAPITAL REGION

April 2017 - April 2018

Data Source: PSA

RETAIL PRICE INDEX

CURRENCY EXCHANGE RATES

Data source: IMF

100

150

200

250

300

350

8 Construction Market Quarterly Update 2018 Second Quarter | Rider Levett Bucknall

DEVELOPMENT TYPE LOW HIGH

OFFICE TOWERS PHP/m2

10 - 35 Storeys (NCR) 37,100 54,700

10 - 35 Storeys (Province) 27,700 34,600

OFFICE FIT-OUT

OPEN PLANNED PHP/m2

Computer Areas 18,100 20,900

Executive Areas and Front of House

32,800 37,800

Insurance Office, Government Departments

18,100 20,900

Major Company Headquarters 27,100 31,400

Solicitors, Financiers 27,100 31,400

OFFICE FIT-OUT

FULLY PARTITIONED PHP/m2

Computer Areas 21,500 25,000

Executive Areas and Front of House

38,600 44,400

Insurance Office, Government Departments

21,500 25,000

Major Company Headquarters 33,100 38,100

Solicitors, Financiers 27,100 33,100

OFFICE REFURBISHMENT PHP/m2

Office Typical Floor 42,600 49,000

Office Core Upgrade (excluding life Modernization)

32,700 38,600

WORKSTATION PHP/ea

Call Centre 42,200 48,500

Executive 131,000 151,000

Secretarial 60,300 69,300

Technical Staff 82,700 95,100

DEVELOPMENT TYPE LOW HIGH

RESIDENTIAL PHP/m2

Hi-End Residential Building 38,700 71,600

Mid-End Residential Building 31,600 47,800

Low-End Residential Building 30,600 36,700

Rowhouse ( 1 - 4 storeys) 42,100 49,900

Duplex 29,700 39,400

Single Detached 35,000 62,400

CLUBHOUSE PHP/m2

Clubhouse (Premier) 136,000 307,000

Clubhouse (Secondary) 54,200 71,700

HOTEL FIT-OUT PHP/Room

Three Star 2,930,000 3,250,000

Four Star 4,170,000 4,800,000

Five Star 5,880,000 6,480,000

HOTELS incl. FF&E PHP/m2

Five (5) Star 85,000 100,000

Villas 112,000 148,000

RETAIL PHP/m2

Retail Strip (NCR) 50,000 66,200

Shopping Malls (NCR) 38,400 69,400

Shopping Malls (Province) 31,300 56,500

INSTITUTIONAL PHP/m2

Schools 40,500 49,600

Hospitals with FF&E 36,700 55,500

INDUSTRIAL PHP/m2

Commissary 52,700 67,300

BPO PHP/m2

With Fit-out Works 37,700 53,200

Without Fit-out Works 28,100 47,600

CONSTRUCTION PRICES

9Rider Levett Bucknall | Construction Market Quarterly Update 2018 Second Quarter

PROFESSIONAL SERVICES

QUANTITY SURVEYING

¥ Full Quantity Surveying from start of project to finish¥ Budgetary Estimates and Cost Estimate Preparation¥ Preparation of Priced Bills of Quantities¥ Bid Documentation, Bidding and Award of Contracts¥ Contract Documentation and Administration¥ Project Cost Control¥ Financial, Physical and Quality Audit of Construction¥ Contractual Advice¥ Contractual Claims Preparation and Adjudication¥ Dispute Management¥ Builders Quantities Preparation¥ Replacement Cost Estimates¥ Assistance in Arbitration, and/or Litigation¥ Secondment of Staff

PROJECT MANAGEMENT / CONSTRUCTION MANAGEMENT

¥ Project / Construction Management and Supervision¥ Value Engineering Services¥ Project Close-out Services¥ Quality Assurance and Quality Control (QA/QC) Services

SPECIAL SERVICES

¥ Financial Audit of Construction¥ Physical Audit of Construction¥ Quality Audit of Construction¥ Verification of Loan Amounts¥ Verification of Monies Spent¥ Contractual Advice¥ Contractual Claims Preparation and Adjudication¥ Builders Quantities Preparation¥ Replacement Cost Estimates after Disaster; Fire; Typhoon etc.¥ Expert Witness in Arbitration, and/or Litigation¥ Secondment of Staff

Disclaimer: While Rider Levett Bucknall Philippines, Inc. has endeavoured to ensure the accuracy of the information and materials (the “Materials”)

herein, it does not warrant its accuracy, adequacy, completeness or reasonableness and expressly disclaims liability for any errors in, or omissions

therefrom. Rider Levett Bucknall Philippines, Inc. shall not be liable for any damages, loss or expense whatsoever arising out of or in connection

with the use or reliance on the Materials. The Materials are provided for general information only. Professional advice should be obtained for your

particular factual situation before making any decision. The Materials may not, in any medium, be reproduced, published, adapted, altered or

otherwise used in whole or in part in any manner without the prior written consent of Rider Levett Bucknall Philippines, Inc.

MAIN OFFICE:Building 3, Corazon Clemeña Compound, No. 54 Danny Floro Street, Bagong Ilog, Pasig City, 1600 PhilippinesT: +63 2 687 1075 / 470 0642 F: 570 4025E:[email protected]; [email protected]

STA. ROSA, LAGUNA OFFICE:Unit 201, Brain Train Center, Lot 11 Block 3, Sta. Rosa Business Park, Greenfield, Brgy. Don Jose, Sta. Rosa City, Laguna, 4026 Philippines M: + 63 922 806 7507E: [email protected]

CEBU OFFICE:Suite 602, PDI Condominium, Archbishop Reyes Ave. corner J. Panis Street, Banilad,Cebu City, 6014 PhilippinesT: +63 32 268 0072 E:[email protected]

DAVAO OFFICE:6th Floor, Units 15 & 19, Metro Lifestyle Complex Corner F. Torres Street & E. Jacinto ExtensionDavao City, 8000 Philippines T: +63 82 222 5315 M: +63 917 550 7013E: [email protected]

CAGAYAN DE ORO OFFICE:Rm. 702, 7th Floor, TTK Tower, Don Apolinar Velez Street, Bgy. 19 Cagayan De Oro City, 9000 PhilippinesT: +63 88 850 4105 M: +63 917 860 0207 E: [email protected]; [email protected]

BACOLOD OFFICE:2nd Floor, Mayfair Plaza,Lacson cor. 12th Street, Bacolod CityNegros Occidental, 6100 PhilippinesT: +63 34 432 1344 E:[email protected] BOHOL OFFICE:Cascajo, Panglao Island, Bohol, 6340 PhilippinesT: +63 977 852 9548E:[email protected]

ILOILO OFFICE:2nd Floor (Door 21), Uy Bico Building, Yulo Street, Iloilo City Proper, Iloilo, 5000 PhilippinesT: +63 33 320 0945E:[email protected]

SUBIC OFFICE:The Venue Bldg. Unit 418, Lot C-5, Commercial Area, Subic Bay Gateway Park, Phase 1, Subic Bay Freeport Zone, ZambalesM: +63 917 517 3962

CLARK OFFICE:Units 202-203 Baronesa Place Bldg., Mc Arthur Hi-way Dau, Mabalacat City, PampangaM: +63 918 965 3891

A Quarterly Publication from the Research and Development of:

Rider Levett Bucknall Philippines, Inc.

10 Construction Market Quarterly Update 2018 Second Quarter | Rider Levett Bucknall