34

Second Quarter 2020 Earnings Review July 14, 2020 Citi | Investor Relations

Second Quarter 2020 Earnings Review

July 14, 2020

Citi | Investor Relations

Overview

2

Note:

(1) Preliminary. For additional information, please refer to Slide 32.

(2) Preliminary.

(3) Tangible Book Value per Share is a non-GAAP financial measures. For additional information, please refer to Slide 33.

Performance impacted by macro environment

– Despite a challenging environment, delivered solid revenue growth, expense control and

strong risk management

– Supported clients while maintaining credit discipline and balance sheet strength

– Credit reserve build primarily reflects deterioration in economic outlook and downgrades

in corporate loan portfolio

– Strong deposit growth across both Consumer and Institutional franchises

Strong capital and liquidity position

– Common Equity Tier 1 Capital Ratio of 11.5%(1)

– Liquidity Coverage Ratio of 117%(2)

– Tangible Book Value per Share increased 5% year-over-year to $71.15(3)

Priorities in this uncertain environment

– Operating from position of strength from capital, liquidity and balance sheet perspective

– Maintaining resources to support clients and employees, as well as broader economy

– Demonstrating operational resiliency as we manage through COVID-19 pandemic

– Focus on risk management and building a stronger company for the future

COVID-19 Response To Date – Supporting Our People, Clients & Communities

3

Employees Consumers Corporates Communities

• Committed more than

$100MM to date through Citi and Citi’s Foundation in

support of COVID-19-related community relief and

economic recovery efforts globally including:

― $25MM in initial

proceeds from Citi’s participation in SBA’s

Paycheck Protection Program to support

Community Development

Financial Institutions

― $4MM through Double the Good employee

donation campaign

• Announced $50MM facility to purchase loans from

Minority-Owned Depository Institutions

issued under SBA’s Paycheck Protection

Program

• Prudently extending credit

to corporate clients to support their liquidity

objectives and business needs in 2Q’20:

― $15B of draws on previously extended

credit facilities

― $18B of new credit facilities extended

― $26B of repayments on previous draws

• Facilitated $750B of

issuance in the debt and equity markets in 2Q’20,

driving repayments on previous draws

• Leveraging digital capabilities to assist clients

with supply chain management and liquidity

optimization

― In TTS, 20% increase in CitiDirect users and

strong growth in digital account openings

• Plan to participate in the Federal Reserve’s Main

Street Lending Program

• Slow and measured

reentry to site and rapid retreat where necessary

based on medical data and local conditions

• Enhanced flexibility and paid time off for colleagues

directly and indirectly impacted by COVID-19

• Additional health and well-

being resources

• Delivering virtual summer

internship program globally and guaranteed full-time

offers for those meeting minimum requirements in

hub locations

• In 1Q’20, provided > 75,000 colleagues globally with

special compensation, including $1,000 special

payment to eligible colleagues in US

• Extra cleaning and protective measures put in

place at our sites, branches and ATMs, and educating

our staff on preventive actions

• In the US, offering

comprehensive suite of customer relief treatments

across products:

― Credit Cards: provided assistance and relief

to ~2MM accounts, representing ~6% of

balances

― Mortgage: providedrelief to ~5% of

customers, representing ~7% of

balances

― Small Business: issued ~30K loans

totaling $3.4B through SBA’s Paycheck

Protection Program

• Similar programs in place in International GCB, in

line with local regulation

• Enhanced digital capabilities and servicing

2Q'20 1Q'20 %r 2Q'19 %r 1H'20 %r

Revenues $19,766 $20,731 (5)% $18,758 5% $40,497 8%

Operating Expenses 10,415 10,594 (2)% 10,500 (1)% 21,009 (0)%

Efficiency Ratio 52.7% 51.1% 56.0% 51.9%

Operating Margin 9,351 10,137 (8)% 8,258 13% 19,488 20%

Net Credit Losses 2,206 2,108 5% 1,963 12% 4,314 10%

Net ACL Build / (Release) 5,603 4,893 15% 111 NM 10,496 NM

Other Provisions 94 26 NM 19 NM 120 NM

Credit Costs 7,903 7,027 12% 2,093 NM 14,930 NM

EBT 1,448 3,110 (53)% 6,165 (77)% 4,558 (63)%

Income Taxes 131 576 (77)% 1,373 (90)% 707 (73)%

Effective Tax Rate 9% 19% 22% 16%

Net Income $1,316 $2,522 (48)% $4,799 (73)% $3,838 (60)%

Return on Assets 0.23% 0.49% 0.97% 0.36%

Return on Tangible Common Equity 2.9% 6.0% 11.9% 4.5%

EPS $0.50 $1.05 (52)% $1.95 (74)% $1.56 (59)%

Average Diluted Shares 2,084 2,114 (1)% 2,289 (9)% 2,103 (9)%

Average Assets ($B) $2,267 $2,080 9% $1,979 15% $2,173 11%

EOP Assets (Constant $B) 2,233 2,235 (0)% 1,957 14% 2,233 14%

EOP Loans (Constant $B) 685 726 (6)% 678 1% 685 1%

EOP Deposits (Constant $B) 1,234 1,193 3% 1,030 20% 1,234 20%

Citigroup – Summary Financial Results($MM, except EPS)

4

Note: Totals may not sum due to rounding. NM: Not meaningful. ACL: Allowance for Credit Losses. Constant dollar excludes the impact of foreign exchange translation into U.S.

dollars for reporting purposes and, as used throughout this presentation, is a non -GAAP financial measure. For a reconciliation of constant dollars to reported results, please

refer to Slide 34.

(1) Includes credit reserve build for loans and provision for credit losses on unfunded lending commitments.

(2) Includes provisions for credit losses on benefits and claims, HTM debt securities and other assets.

(3) Return on Tangible Common Equity (RoTCE) is a non-GAAP financial measure. For a reconciliation to reported results, please refer to Slides 33 and 34.

(1)

(3)

(2)

Global Consumer Banking

2Q'20 QoQ %r YoY %r 1H'20 %r

Revenues $7,339 (9)% (7)% $15,513 (2)%

North America 4,742 (9)% (5)% 9,966 0%

International 2,597 (8)% (12)% 5,547 (6)%

Expenses 4,013 (7)% (8)% 8,381 (4)%

North America 2,346 (7)% (10)% 4,882 (6)%

International 1,667 (5)% (4)% 3,499 (0)%

Operating Margin 3,326 (12)% (6)% 7,132 (1)%

Credit Costs 3,885 (19)% NM 8,716 NM

EBT (559) 45% NM (1,584) NM

Net Income $(396) 47% NM $(1,150) NM

Revenues $7,339 (9)% (7)% $15,513 (2)%

Retail Banking 2,836 (5)% (7)% 5,882 (3)%

Cards 4,503 (12)% (7)% 9,631 (2)%

Key Indicators (in Constant $B, except branches)

Branches 2,327 (0)% (3)% 2,327 (3)%

RB Average Deposits $302 6% 12% $296 10%

RB Average Loans 122 1% 6% 123 6%

Investment AUMs 187 11% 3% 187 3%

Cards Average Loans 150 (10)% (7)% 159 (2)%

Cards Purchase Sales 108 (15)% (23)% 236 (12)%

Note: Totals may not sum due to rounding. NM: Not meaningful. ACL: Allowance for Credit Losses. CECL: Current Expected Credit Losses. Constant dollar excludesthe

impact of foreign exchange translation into U.S. dollars for reporting purposes. For a reconciliation of constant dollars to reported results, please refer to Slide 34. 5

(Constant $MM)

• Revenues

– Down 7% YoY, driven by lower loan volumes and lower interest

rates across all regions, partially offset by strong deposit growth

• Expenses

– Down 8% YoY, driven by lower

volume-related expenses, reductions in marketing and other

discretionary spending, as well as efficiency savings, partially offset

by higher COVID-19 related expenses

• Credit Costs

– Up YoY, primarily reflecting net

ACL build of $2.0B driven by the impact of changes in economic

outlook under CECL

2Q'20 QoQ %r YoY %r 1H'20 %r

Revenues $4,742 (9)% (5)% $9,966 0%

Branded Cards 2,218 (5)% 1% 4,565 4%

Retail Services 1,402 (20)% (13)% 3,149 (4)%

Retail Banking 1,122 (1)% (3)% 2,252 (2)%

Expenses 2,346 (7)% (10)% 4,882 (6)%

Operating Margin 2,396 (11)% 2% 5,084 7%

Credit Costs 3,002 (23)% 100% 6,894 NM

EBT (606) 50% NM (1,810) NM

Net Income $(459) 50% NM $(1,369) NM

Key Indicators ($B, except branches, and as otherwise noted)

Branches 687 0% (0)% 687 (0)%

RB Average Deposits $173 7% 14% $167 11%

RB Average Loans 52 3% 9% 51 8%

Investment AUMs 69 12% 2% 69 2%

Branded Cards Average Loans 83 (11)% (7)% 88 (1)%

Branded Cards Purchase Sales 74 (14)% (21)% 160 (10)%

Retail Services Average Loans 46 (9)% (6)% 48 (3)%

Retail Services Purchase Sales 17 (6)% (25)% 35 (15)%

Active Digital Customers (MM) 20 0% 6%

Active Mobile Customers (MM) 13 1% 12%

North America Consumer Banking

Note: Totals may not sum due to rounding. NM: Not meaningful. ACL: Allowance for Credit Losses.

(1) Customers of all online and/or mobile services within the last 90 days through May 2020. For additional information, please refer to Slide 26.

(2) Customers of all mobile services (mobile apps or via mobile browser) within the last 90 days through May 2020. For additional information, please refer to Slide 26.

6

(1)

(2)

($MM)

• Revenues

– Down 5% YoY

– Branded Cards: Up 1% YoY, as a

favorable mix shift more than offset lower purchase sales and loan

volumes

– Retail Services: Down 13% YoY, reflecting lower average loans and

higher partner payments

– Retail Banking: Down 3% YoY, as lower deposit spreads more than

offset strong deposit growth and higher mortgage revenues

• Expenses– Down 10% YoY, driven by reductions

in marketing and other discretionary

spending, efficiency savings and lower volume-related expenses, partially

offset by COVID-19 related expenses

• Credit Costs

– NCLs grew 5% YoY, primarily

reflecting seasoning in Branded Cards portfolio

– Net ACL build of $1.5B, primarily

reflecting the impact of changes in economic outlook under CECL

• Revenues

– Latin America: Down 7% YoY, driven by lower cards purchase sales, a decline in

loan volumes and lower deposit spreads, partially offset by deposit growth

– Asia: Down 15% YoY, reflecting lower

cards purchase sales and lower deposit spreads, partially offset by strong deposit

growth

• Expenses

– Down 4% YoY, driven by efficiency savings and lower volume-related

expenses

• Credit Costs

– NCL rate of 1.79% vs. 1.81% in 2Q’19

– Net credit losses of $403MM down 1% YoY, primarily reflecting a decline in Latin

America

– Net ACL build of $461MM, primarily driven by the impact of changes in

economic outlook under CECL

2Q'20 QoQ %r YoY %r 1H'20 %r

Revenues $2,597 (8)% (12)% $5,547 (6)%

Latin America 1,050 (3)% (7)% 2,249 (3)%

Asia 1,547 (11)% (15)% 3,298 (8)%

Expenses 1,667 (5)% (4)% 3,499 (0)%

Latin America 604 (5)% (0)% 1,303 5%

Asia 1,063 (6)% (5)% 2,196 (3)%

Operating Margin 930 (13)% (23)% 2,048 (15)%

Credit Costs 883 1% NM 1,822 NM

EBT 47 (76)% (94)% 226 (86)%

Latin America 19 NM (93)% (38) NM

Asia 28 (88)% (95)% 264 (74)%

Net Income $63 (63)% (90)% $219 (82)%

Key Indicators (in Constant $B, except branches, and as otherwise noted)

Branches 1,640 (0)% (4)% 1,640 (4)%

RB Average Deposits $129 4% 10% $129 9%

RB Average Loans 70 (1)% 4% 71 5%

Investment AUMs 118 10% 4% 118 4%

Cards Average Loans 21 (10)% (9)% 23 (3)%

Cards Purchase Sales 18 (25)% (30)% 41 (17)%

Active Digital Customers (MM) 13 (0)% 13%

Active Mobile Customers (MM) 11 0% 22%

International Consumer Banking

7

Note: Totals may not sum due to rounding. NM: Not meaningful. ACL: Allowance for Credit Losses. Constant dollar excludes the impact of foreign exchange translation into U.S.

dollars for reporting purposes. For a reconciliation of constant dollars to reported results, please refer to Slide 34.

(1) Asia GCB includes the results of operations of GCB activities in certain EMEA countries for all periods presented.

(2) Customers of all online and/or mobile services within the last 90 days through May 2020. For additional information, please refer to Slide 26.

(3) Customers of all mobile services (mobile apps or via mobile browser) within the last 90 days through May 2020. For additional information, please refer to Slide 26.

(2)

(3)

(1)

(1)

(1)

(Constant $MM)

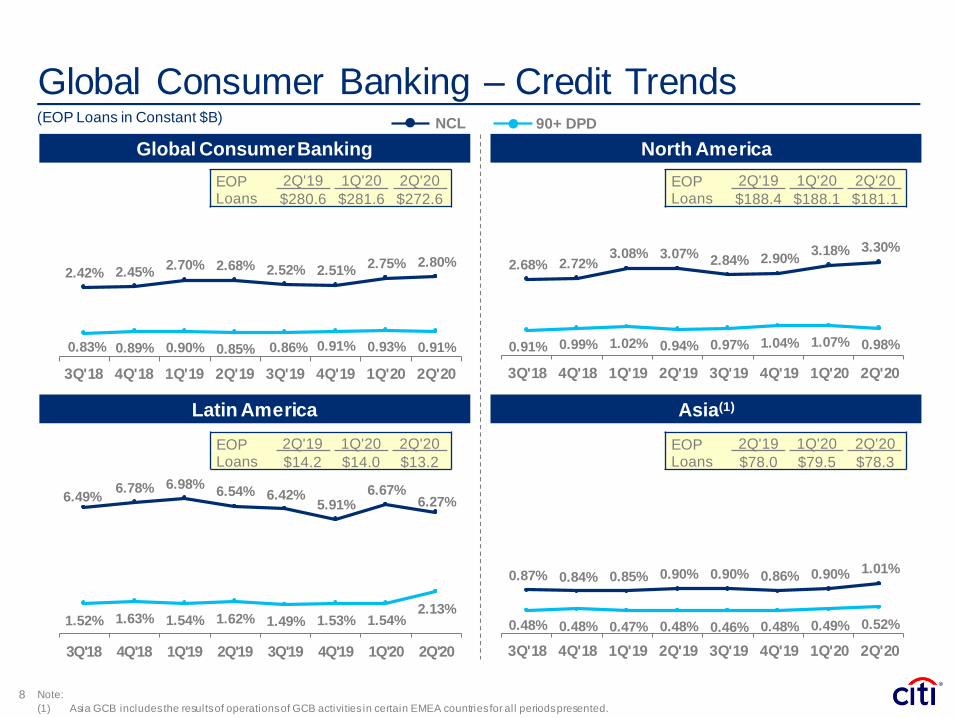

0.87% 0.84% 0.85% 0.90% 0.90% 0.86% 0.90% 1.01%

0.48% 0.48% 0.47% 0.48% 0.46% 0.48% 0.49% 0.52%

3Q'18 4Q'18 1Q'19 2Q'19 3Q'19 4Q'19 1Q'20 2Q'20

1.52% 1.63% 1.54% 1.62% 1.49% 1.53% 1.54%2.13%

6.49%6.78% 6.98%

6.54% 6.42%5.91%

6.67%6.27%

3Q'18 4Q'18 1Q'19 2Q'19 3Q'19 4Q'19 1Q'20 2Q'20

0.91% 0.99% 1.02% 0.94% 0.97% 1.04% 1.07% 0.98%

2.68% 2.72%3.08% 3.07%

2.84% 2.90%3.18% 3.30%

3Q'18 4Q'18 1Q'19 2Q'19 3Q'19 4Q'19 1Q'20 2Q'20

0.83% 0.89% 0.90% 0.85% 0.86% 0.91% 0.93% 0.91%

2.42% 2.45%2.70% 2.68% 2.52% 2.51%

2.75% 2.80%

3Q'18 4Q'18 1Q'19 2Q'19 3Q'19 4Q'19 1Q'20 2Q'20

NCL

Global Consumer Banking – Credit Trends

North AmericaGlobal Consumer Banking

Latin America Asia(1)

EOPLoans

2Q'19 1Q'20 2Q'20

$280.6 $281.6 $272.6

EOP Loans

2Q'19 1Q'20 2Q'20

$14.2 $14.0 $13.2

90+ DPD

EOPLoans

2Q'19 1Q'20 2Q'20

$78.0 $79.5 $78.3

EOPLoans

2Q'19 1Q'20 2Q'20

$188.4 $188.1 $181.1

Note:

(1) Asia GCB includes the results of operations of GCB activities in certain EMEA countries for all periods presented.

8

(EOP Loans in Constant $B)

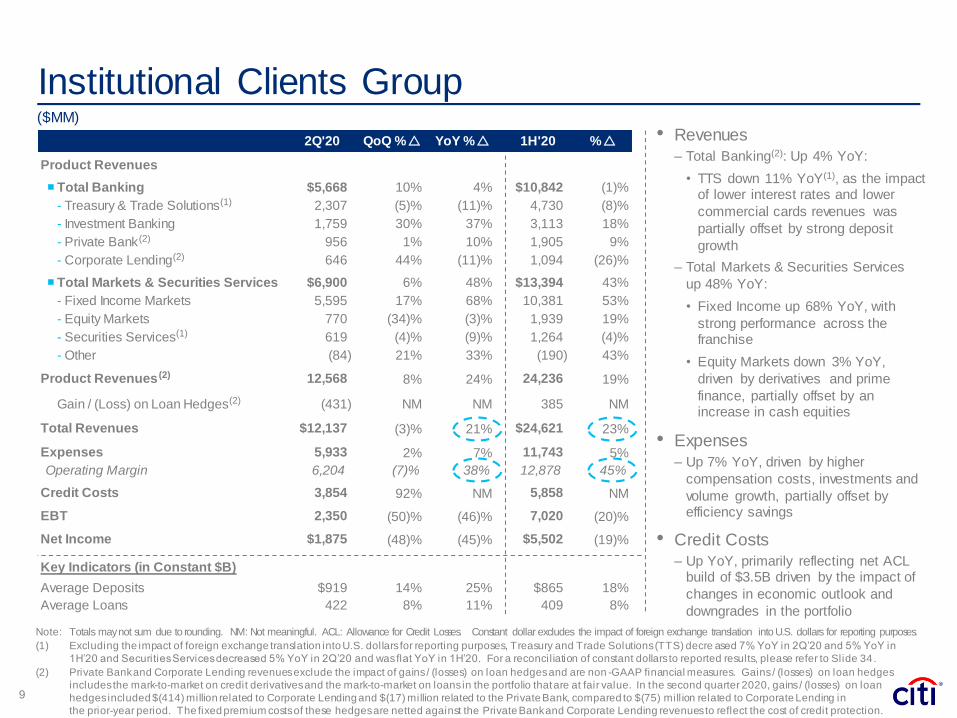

2Q'20 QoQ %r YoY %r 1H'20 %r

Product Revenues

Total Banking $5,668 10% 4% $10,842 (1)%

- Treasury & Trade Solutions 2,307 (5)% (11)% 4,730 (8)%

- Investment Banking 1,759 30% 37% 3,113 18%

- Private Bank 956 1% 10% 1,905 9%

- Corporate Lending 646 44% (11)% 1,094 (26)%

Total Markets & Securities Services $6,900 6% 48% $13,394 43%

- Fixed Income Markets 5,595 17% 68% 10,381 53%

- Equity Markets 770 (34)% (3)% 1,939 19%

- Securities Services 619 (4)% (9)% 1,264 (4)%

- Other (84) 21% 33% (190) 43%

Product Revenues 12,568 8% 24% 24,236 19%

Gain / (Loss) on Loan Hedges (431) NM NM 385 NM

Total Revenues $12,137 (3)% 21% $24,621 23%

Expenses 5,933 2% 7% 11,743 5%

Operating Margin 6,204 (7)% 38% 12,878 45%

Credit Costs 3,854 92% NM 5,858 NM

EBT 2,350 (50)% (46)% 7,020 (20)%

Net Income $1,875 (48)% (45)% $5,502 (19)%

Key Indicators (in Constant $B)

Average Deposits $919 14% 25% $865 18%

Average Loans 422 8% 11% 409 8%

• Revenues

– Total Banking(2): Up 4% YoY:

• TTS down 11% YoY(1), as the impact of lower interest rates and lower

commercial cards revenues was

partially offset by strong deposit

growth

– Total Markets & Securities Services

up 48% YoY:

• Fixed Income up 68% YoY, with

strong performance across the franchise

• Equity Markets down 3% YoY,

driven by derivatives and prime

finance, partially offset by an increase in cash equities

• Expenses

– Up 7% YoY, driven by higher

compensation costs, investments and

volume growth, partially offset by efficiency savings

• Credit Costs

– Up YoY, primarily reflecting net ACL build of $3.5B driven by the impact of

changes in economic outlook and

downgrades in the portfolio

Institutional Clients Group

9

($MM)

(2)

(2)

(2)

(1)

(1)

(2)

Note: Totals may not sum due to rounding. NM: Not meaningful. ACL: Allowance for Credit Losses. Constant dollar excludes the impact of foreign exchange translation into U.S. dollars for reporting purposes.

(1) Excluding the impact of foreign exchange translation into U.S. dollars for reporting purposes, Treasury and Trade Solutions (TTS) decre ased 7% YoY in 2Q’20 and 5% YoY in

1H’20 and Securities Services decreased 5% YoY in 2Q’20 and was flat YoY in 1H’20. For a reconciliation of constant dollars to reported results, please refer to Slide 34.

(2) Private Bank and Corporate Lending revenues exclude the impact of gains / (losses) on loan hedges and are non -GAAP financial measures. Gains / (losses) on loan hedges

includes the mark-to-market on credit derivatives and the mark-to-market on loans in the portfolio that are at fair value. In the second quarter 2020, gains / (losses) on loan

hedges included $(414) million related to Corporate Lending and $(17) million related to the Private Bank, compared to $(75) mill ion related to Corporate Lending in

the prior-year period. The fixed premium costs of these hedges are netted against the Private Bank and Corporate Lending revenues to reflect the cost of credit protection.

2Q'20 QoQ %r YoY %r 1H'20 %r

Revenues $290 NM (49)% $363 (65)%

Expenses 469 13% (2)% 885 (14)%

Credit Costs 164 (15)% NM 356 NM

EBT (343) 36% NM (878) NM

Income Taxes (178) 10% NM (376) NM

Net Income $(163) 54% NM $(514) NM

Corporate / Other

Note: Totals may not sum due to rounding. NM: Not meaningful.10

($MM)

• Revenues

– Down 49% YoY, reflecting the wind-down of legacy assets and

lower rate environment, partially offset by AFS gains and positive

marks on legacy securities

• Expenses

– Down 2% YoY, reflecting the wind-down of legacy assets,

partially offset by higher infrastructure costs and

incremental COVID-19 related expenses

3.40 2.89 3.13 2.214.82 4.90

0.90 1.22 0.841.21

1.14 1.47$4.29 $4.11 $3.97

$3.41

$5.96$6.37

1Q'19 2Q'19 3Q'19 4Q'19 1Q'20 2Q'20

10.54 10.42 10.54 10.50 10.22 9.61

0.86 1.24 0.77 1.13 1.11 1.47

$11.39 $11.66 $11.32 $11.63 $11.33 $11.08

2.72% 2.67% 2.56% 2.63%2.48%

2.17%

1Q'19 2Q'19 3Q'19 4Q'19 1Q'20 2Q'20

NIR

$(1.13)

$0.49

$(0.64)

$3.43

$0.49

$0.41 $3.91

Non-NIR

$(0.58)$(0.25)

Citigroup – Net Interest Revenue & Markets Revenue

(Constant $B)

2Q'20

QoQ r

11

2Q'20

YoY r

$2.25

Net Interest Revenue (NIR)

Markets(1) Revenue2Q'20

QoQ r

2Q'20

YoY r(Reported $B)

$0.23$0.35

$(0.81)$(0.61)

$0.25$0.33

$2.01$0.08

Citigroup NIM

Markets(1)

Ex-Markets

1H'20

YoY r

1H'20

YoY r

Note: Totals may not sum due to rounding. Excludes discontinued operations. Constant dollar excludesthe impact of foreign exchange translation into U.S. dollars for reporting

purposes. For a reconciliation of constant dollars to reported results, please refer to Slide 34.

NIM (%) includes the taxable equivalent adjustment (based on the U.S. federal statutory tax rate of 21% in all periods).

(1) Markets is defined as Fixed Income Markets and Equity Markets.

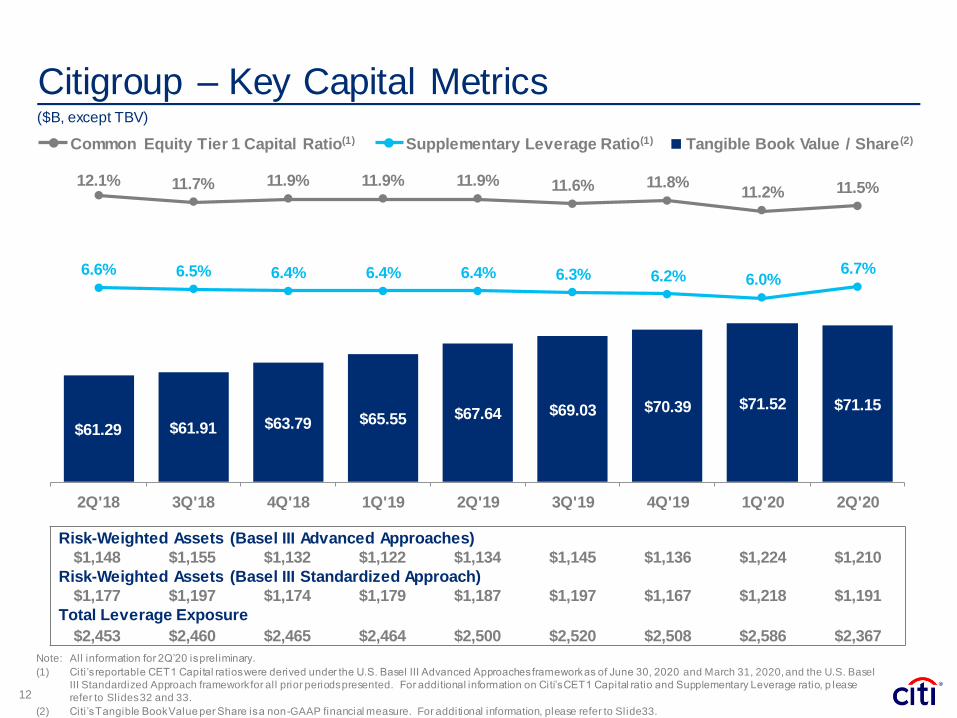

Citigroup – Key Capital Metrics

Note: All information for 2Q’20 is preliminary.

(1) Citi’s reportable CET1 Capital ratios were derived under the U.S. Basel III Advanced Approaches framework as of June 30, 2020 and March 31, 2020, and the U.S. Basel

III Standardized Approach framework for all prior periods presented. For additional information on Citi’s CET1 Capital ratio and Supplementary Leverage ratio, p lease

refer to Slides 32 and 33.

(2) Citi’s Tangible Book Value per Share is a non-GAAP financial measure. For additional information, please refer to Slide 33.

Common Equity Tier 1 Capital Ratio(1) Supplementary Leverage Ratio(1) Tangible Book Value / Share(2)

12

Risk-Weighted Assets (Basel III Advanced Approaches)

$1,148 $1,155 $1,132 $1,122 $1,134 $1,145 $1,136 $1,224 $1,210

Risk-Weighted Assets (Basel III Standardized Approach)

$1,177 $1,197 $1,174 $1,179 $1,187 $1,197 $1,167 $1,218 $1,191

Total Leverage Exposure

$2,453 $2,460 $2,465 $2,464 $2,500 $2,520 $2,508 $2,586 $2,367

$61.29 $61.91 $63.79 $65.55 $67.64 $69.03 $70.39 $71.52 $71.15

12.1% 11.7% 11.9% 11.9% 11.9% 11.6% 11.8%11.2% 11.5%

6.6% 6.5% 6.4% 6.4% 6.4% 6.3% 6.2% 6.0%6.7%

-5.0%

-3.0%

-1.0%

1.0%

3.0%

5.0%

7.0%

9.0%

11. 0%

13. 0%

2Q'18 3Q'18 4Q'18 1Q'19 2Q'19 3Q'19 4Q'19 1Q'20 2Q'20

40. 00

50. 00

60. 00

70. 00

80. 00

90. 00

100.00

($B, except TBV)

Conclusions

Note: GCB: Global Consumer Banking. ICG: Institutional Clients Group.

(1) Preliminary. For additional information on these measures, please refer to Slides 32 and 33.

(2) Preliminary. $900 billion of available liquidity resources including HQLA, additional unencumbered securities and available borrowing capacity at the FHLBs and Federal

Reserve Discount Window.

(3) Citi’s Tangible Book Value per Share is a non-GAAP financial measure. For additional information, please refer to Slide 33.

13

Operated well in challenging environment during 1H’20

– Results in GCB impacted by lower levels of activity due to COVID-19

– Solid client engagement across ICG and robust performance in Markets and Inv. Banking

– Delivered profitable first half despite ~$10.5B increase in credit reserves due to economic

outlook related to COVID-19

– Supported clients while maintaining credit discipline and balance sheet strength

Strong capital and liquidity position

– Common Equity Tier 1 Capital Ratio of 11.5%(1)

– Supplementary Leverage Ratio of 6.7%(1)

– Liquidity Coverage Ratio of 117%, with available liquidity of $900 billion(2)

– Tangible Book Value per share increased 5% year-over-year to $71.15(3)

Priorities in this uncertain environment

– Remain committed to serving clients, protecting employees and supporting economy

– Continue to demonstrate financial strength and operational resiliency

– Focus on risk management and building a stronger company for the future

Certain statements in this presentation are “forward-looking statements”

within the meaning of the rules and regulations of the U.S. Securities and

Exchange Commission (SEC). These statements are based on

management’s current expectations and are subject to uncertainty and

changes in circumstances. These statements are not guarantees of future

results or occurrences. Actual results and capital and other financial

condition may differ materially from those included in these statements due

to a variety of factors. These factors include, among others,

macroeconomic and other challenges and uncertainties related to the

COVID-19 pandemic, such as the extent and duration of the impact on

public health, the U.S. and global economies, financial markets and

consumer and corporate customers and clients, including economic

activity and employment, as well as the various actions taken in response

by governments, central banks and others, including Citi, and the

precautionary statements included in this presentation. These factors also

consist of those contained in Citigroup’s filings with the SEC, including

without limitation the “Risk Factors” section of Citigroup’s First Quarter

2020 Form 10-Q and Citigroup’s 2019 Form 10-K. Any forward-looking

statements made by or on behalf of Citigroup speak only as to the date

they are made, and Citi does not undertake to update forward-looking

statements to reflect the impact of circumstances or events that arise after

the date the forward-looking statements were made.14

Appendix

17. Citigroup Returns

18. Citigroup – LTM Efficiency Ratio and Expenses

19. Estimated FX Impact on Key P&L Metrics

20. CECL Details

21. Consumer Credit

22. ICG – Corporate Credit Exposure

23. ICG – Corporate Energy Exposure

24. ICG – Unfunded Corporate Energy Exposure

25. Regional Credit Portfolio

26. Consumer Drivers

27. Consumer Drivers (continued)

28. Institutional Drivers

29. Preferred Stock Dividend Schedule

30. Equity & CET1 Capital Drivers (QoQ)

31. Equity & CET1 Capital Drivers (YoY)

32. Common Equity Tier 1 Capital Ratio and Components

33. Supplementary Leverage Ratio; TCE Reconciliation

34. Adjusted Results and FX Impact Reconciliation

Table of Contents

16

Citigroup Returns

Note: Totals may not sum due to rounding. LTM’20: Last twelve months ending June 30, 2020.

(1) 2Q’20 represents 2Q’20 net income less 2Q’20 preferred dividends of $253 million. LTM’20 represents LTM’20 net income less L TM’20 preferred dividends of $1,094 million.

(2) Return on Assets (ROA) defined as annualized net income (before preferred dividends) divided by average assets.

(3) Tangible common equity (TCE) allocated to GCB and ICG based on estimated full year 2020 capital allocations. TCE is a non-GAAP financial measure. For additional

information on this measure, please refer to Slide 33.

Net Income

to Common

Average

GAAP

Assets

ROA(2)

(bps)

Average

Allocated

TCE(3) RoTCE

GCB $(0.4) $418 (38) $34 (4.7)%

ICG 1.9 1,756 43 87 8.6%

Corp / Other (0.4) 93 (70) 27 (6.2)%

Citigroup $1.1 $2,267 23 $149 2.9%

(1)

(1)

17

($B)

2Q’20 Returns

LTM’20 Returns

Net Income

to Common

Average

GAAP

Assets

ROA(2)

(bps)

Average

Allocated

TCE(3) RoTCE

GCB $1.9 $404 48 $34 5.6%

ICG 11.6 1,588 73 87 13.3%

Corp / Other (0.9) 95 23 28 (3.1)%

Citigroup $12.6 $2,086 66 $150 8.4%

(1)

(1)

2Q’20 1H’20 LTM’20

Operating Efficiency 52.7% 51.9% 54.1%

YoY r (bps) (328) (460) (254)

YoY r ex FX (bps) (316) (447) (248)

Note: LTM: Last Twelve Months.

Citigroup – LTM Efficiency Ratio and Expenses

18

$42.34 $42.32 $42.47 $42.24 $42.23 $42.43 $42.39 $42.28 $41.84 $41.50 $41.29 $41.44 $42.00 $42.01 $41.93

59.8%59.3% 59.2%

58.5%58.3% 58.2%

57.9% 57.7%57.4%

57.2%56.7% 56.7% 56.5%

55.0%

54.1%

4Q'16 1Q'17 2Q'17 3Q'17 4Q'17 1Q'18 2Q'18 3Q'18 4Q'18 1Q'19 2Q'19 3Q'19 4Q'19 1Q'20 2Q'20

LTM Efficiency Ratio and Expenses

($B)

Estimated FX(1) Impact on Key P&L Metrics

Note: Totals may not sum due to rounding.

(1) Impact of foreign exchange translation into U.S. dollars. Please also refer to Slide 34.

Year-over-Year Impact 2Q’20 1Q’20 4Q’19 3Q’19 2Q’19

Revenues $(0.4) $(0.3) $0.0 $(0.2) $(0.2)

Expenses (0.3) (0.2) 0.0 (0.2) (0.2)

Credit Costs (0.1) (0.0) 0.0 (0.0) (0.0)

Earnings Before Taxes $(0.1) $(0.1) $(0.0) $(0.1) $(0.1)

19

($B)

Balance

as of

12/31/19

CECL TransitionImpact

1Q’20 Build

1Q’20

FX /

Other(1)

Balance

as of

3/31/20

2Q’20 Build

2Q’20

FX /

Other(1)

Balance

as of

6/30/20

ACLL / Loans

as of

6/30/20

Cards $8.4 $4.5 $2.4 $(0.2) $15.1 $1.6 $0.0 $16.7 11.21%

All other GCB $1.2 $0.6 $0.4 $(0.2) $2.0 $0.4 $0.0 $2.4

Global Consumer Banking $9.6 $5.0 $2.8 $(0.4) $17.0 $2.0 $0.1 $19.1 7.00%

Institutional Clients Group $2.9 $(0.7) $1.3 $(0.0) $3.5 $3.4 $0.0 $6.8 1.71%

Corp / Other $0.3 $(0.1) $0.2 $(0.0) $0.3 $0.2 $(0.0) $0.5

Allowance for Credit Losses on Loans (ACLL) $12.8 $4.2 $4.3 $(0.5) $20.8 $5.5 $0.1 $26.4 3.89%

Allowance for Credit Losses on Unfunded Lending Commitments $1.5 $(0.2) $0.6 $(0.0) $1.8 $0.1 $(0.1) $1.9

Other(2) $0.0 $0.1 $0.0 $0.0 $0.1 $0.1 $(0.0) $0.2

Citigroup Allowance for Credit Losses $14.2 $4.1 $4.9 $(0.5) $22.8 $5.7 $0.0 $28.5

CECL Details

20

Note: Totals may not sum due to rounding.

(1) Includes the impact of foreign exchange translation, as well as other adjustments, on the opening balance and, in 1Q’20, the transition impact of the allowance for credit

losses, substantially all of which flows through OCI.

(2) Includes the allowance for held-to-maturity debt securities and other assets.

($B)

Allowance for Credit Losses

North America:

• Branded Cards: 10.1%

• Retail Services: 14.0%

($B) (%) 2Q'20 1Q'20 2Q'19 2Q'20 1Q'20 2Q'19

Korea 16.0 5.9% 4.0% 0.2% 0.2% 0.2% 0.7% 0.6% 0.6%

Hong Kong 12.8 4.7% 7.0% 0.1% 0.1% 0.0% 0.3% 0.2% 0.1%

Singapore 12.6 4.6% 2.0% 0.1% 0.1% 0.1% 0.3% 0.3% 0.3%

Australia 8.8 3.2% (8.8)% 0.7% 0.7% 0.8% 0.9% 0.8% 1.5%

Taiwan 7.8 2.9% (2.0)% 0.2% 0.2% 0.2% 0.4% 0.4% 0.3%

India 4.2 1.5% (4.4)% 1.5% 1.3% 1.2% 2.9% 2.0% 1.7%

Malaysia 3.7 1.4% (7.6)% 0.8% 1.2% 1.2% 0.9% 0.6% 0.4%

China 3.3 1.2% 12.3% 0.5% 0.4% 0.3% 1.2% 0.9% 0.6%

Thailand 2.6 1.0% 3.0% 1.6% 1.5% 1.4% 3.5% 3.2% 2.4%

Indonesia 0.7 0.3% (12.4)% 2.8% 2.0% 2.1% 6.5% 5.6% 6.3%

All Other 1.7 0.6% (0.6)% 1.9% 1.8% 1.4% 1.2% 3.7% 3.0%

Asia 74.2 27.2% 0.7% 0.5% 0.5% 0.4% 0.9% 0.8% 0.8%

Poland 1.9 0.7% (0.4)% 0.5% 0.5% 0.6% 1.3% 1.3% 1.4%

UAE 1.2 0.5% (14.6)% 2.5% 1.9% 1.5% 7.0% 4.8% 4.4%

Russia 0.8 0.3% (0.8)% 0.9% 0.6% 0.6% 2.6% 2.1% 1.9%

All Other 0.2 0.1% (22.6)% 2.0% 1.8% 1.2% 7.7% 5.0% 3.7%

EMEA 4.1 1.5% (6.3)% 1.2% 1.0% 0.9% 3.6% 2.8% 2.6%

Latin America 13.2 4.8% (7.2)% 2.1% 1.5% 1.5% 6.3% 7.0% 6.7%

Total International 91.5 33.6% (0.8)% 0.8% 0.7% 0.6% 1.8% 1.8% 1.8%

North America 181.1 66.4% (3.9)% 1.0% 1.1% 0.9% 3.3% 3.2% 3.1%

Global Consumer Banking 272.6 100.0% (2.9)% 0.9% 0.9% 0.8% 2.8% 2.7% 2.7%

Growth

YoY %

90+ DPD Ratio NCL Ratio2Q'20 Loans

Consumer Credit

21 Note: Totals may not sum due to rounding.

(Constant $B)

22

Region 2Q’20 1Q’20

North America 57% 57%

EMEA 24 25

Asia 12 12

Latin America 6 6

Total 100% 100%

ICG – Corporate Credit Exposure

Exposures Industry Composition – % of Portfolio

Geographic Distribution – % of Portfolio

Ratings Detail – % of Portfolio

Exposure Type 2Q’20 1Q’20

Direct outstandings(1) $359 $394

Unfunded lending commitments(2) 423 394

Total $782 $787

2Q’20 1Q’20

AAA / AA / A 49% 48%

BBB 31 33

BB / B 16 17

CCC or below 4 2

Total 100% 100%

Industry 2Q’20 1Q’20

Transportation & industrials 19% 19%

Autos 7 7

Transportation 4 4

Industrials 9 9

Private Bank 13 13

Consumer retail 11 10

Health 4 4

Technology, media and telecom 10 10

Power, chemicals, metals & mining 8 9

Banks and finance companies 7 8

Real estate 8 7

Energy and commodities 7 7

Public sector 3 3

Insurance 3 3

Asset managers and funds 3 3

Financial markets infrastructure 2 2

Securities firms 0 0

Other industries 2 1

Total 100% 100%

($B)

Note: 2Q’20 data is preliminary. Totals may not sum due to rounding. Data includes ICG excluding Private Bank delinquency managed portfolio in all periods.

(1) Includes drawn loans, overdrafts, bankers’ acceptances and leases.

(2) Includes unused commitments to lend, letters of credit and financial guarantees.

23

ICG – Corporate Energy Exposure

Energy / Energy-Related Exposure

Energy(1) Subsector Exposures

Geographic Distribution as of 2Q’20(2)

Ratings Detail

Note: 2Q’20 data is preliminary. Totals may not sum due to rounding. ICG: Institutional Clients Group. Reflects corporate credit exposures in the ICG.

(1) Includes energy-related exposures classified in other industries, primarily Public Sector and Transportation.

(2) Total exposure includes direct outstandings and unfunded commitments.

(3) E&P: Exploration and Production. RBL: Reserve-Based Lending. Services & Dril l ing includes Oil and Gas Equipment and Services, Oil and Gas Dril ling and Offshore Drill ing.

Funded Total Exposure(2)

2 2Q’20 1Q’20 2Q’20 1Q’20

AAA / AA / A 16 % 21 % 36 % 37 %

BBB 31 38 34 38

BB / B 33 30 21 19

CCC or below 20 10 10 7

Total 100 % 100 % 100 % 100 %

North America

57%

LATAM8% UK

14%

EMEA13%

Asia8%

Funded Total Exposure(2)

2Q’20 1Q’20 2Q’20 1Q’20

Energy $18.8 $19.3 $55.4 $55.4

Energy-Related(1) 3.4 3.2 5.8 5.4

Total $22.2 $22.5 $61.2 $60.8

(EOP in $B)

Funded

Total

Exposure(2)

2 2Q’20 1Q’20 2Q’20 1Q’20

Oil and Gas E&P(3) $6.0 $6.0 $15.2 $15.5

Memo: NA RBL(3) 2.9 3.1 4.9 5.6

Services and Drilling(3) 2.8 2.8 8.0 8.3

Refining 4.6 4.4 9.0 10.0

Midstream / Oil & Gas Storage & Transportation

2.4 2.6 8.5 7.8

Integrated Oil and Gas 5.1 5.5 17.9 16.7

Other 1.2 1.2 2.6 2.5

Total $22.2 $22.5 $61.2 $60.8

~82% of unfunded exposures as of 2Q’20 are investment grade

4.6% Funded Reserve Ratio

24

ICG – Unfunded Corporate Energy Exposure(1)

Facility Structure Ratings Detail

Subsector Ratings Detail

Key Takeaways 2Q’20

Note: 2Q’20 data is preliminary. Totals may not sum due to rounding. ICG: Institutional Clients Group. Preliminary.

(1) Represents unfunded commitments. Includes energy-related exposures classified in other industries, primarily Public Sector and Transportation.

(2) E&P: Exploration and Production. Services & Dril l ing includes Oil and Gas Equipment and Services, Oil and Gas Dril ling and Offshore Dril ling.

AAA /

AA / ABBB BB / B

CCC

or below

Total

Oil and Gas E&P(2) $2.9 $3.1 $2.7 $0.4 $9.1

Servicesand Drilling(2) 1.9 1.9 0.5 0.9 5.2

Refining 1.2 2.5 0.6 0.1 4.4

Midstream / Oil & Gas Storage & Transportation 1.9 3.4 0.6 0.1 6.1

Integrated Oil and Gas 9.9 2.2 0.7 – 12.8

Other 0.3 0.8 0.3 – 1.4

Total $18.2 $13.9 $5.5 $1.5 $39.0

(EOP in $B)

• Fronting exposure represents advances to borrowers on behalf of participating banks

• Letters of credit are generally short term and trade-related

• Exposures rated A or higher include, as an example, commercial paper backstops

• Generally protected by maintenance covenants; 48% of exposures are secured

AAA /

AA / ABBB BB / B

CCC

or below

Total

Fronting Exposure $5.1 – – – $5.1

Letters of Credit 1.9 2.4 0.9 0.1 5.3

Revolving Facility & Other 11.2 11.5 4.5 1.4 28.6

Total $18.2 $13.9 $5.5 $1.5 $39.0

A

B

C D

A

B

C

D

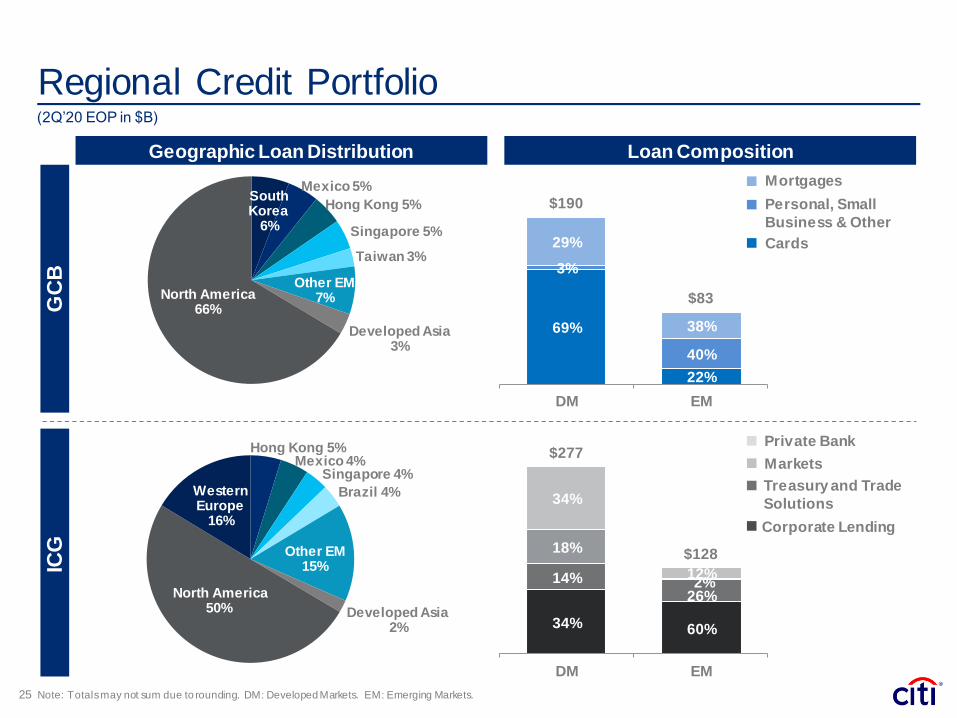

34% 60%

14%

26%

18%

2%

34%

12%

$277

$128

DM EM

69%

22%

3%

40%

29%

38%

$190

$83

DM EM

South Korea

6%

Mexico 5%

Hong Kong 5%

Singapore 5%

Taiwan 3%

Other EM7%

Developed Asia3%

North America66%

Regional Credit Portfolio

Hong Kong 5%Mexico 4%

Singapore 4%

Brazil 4%

Other EM15%

Developed Asia2%

North America50%

Western Europe

16%

GC

BIC

G

Geographic Loan Distribution Loan Composition

Note: Totals may not sum due to rounding. DM: Developed Markets. EM: Emerging Markets.

Markets

Treasury and Trade

Solutions

Corporate Lending

Mortgages

Cards

Personal, Small

Business & Other

25

Private Bank

(2Q’20 EOP in $B)

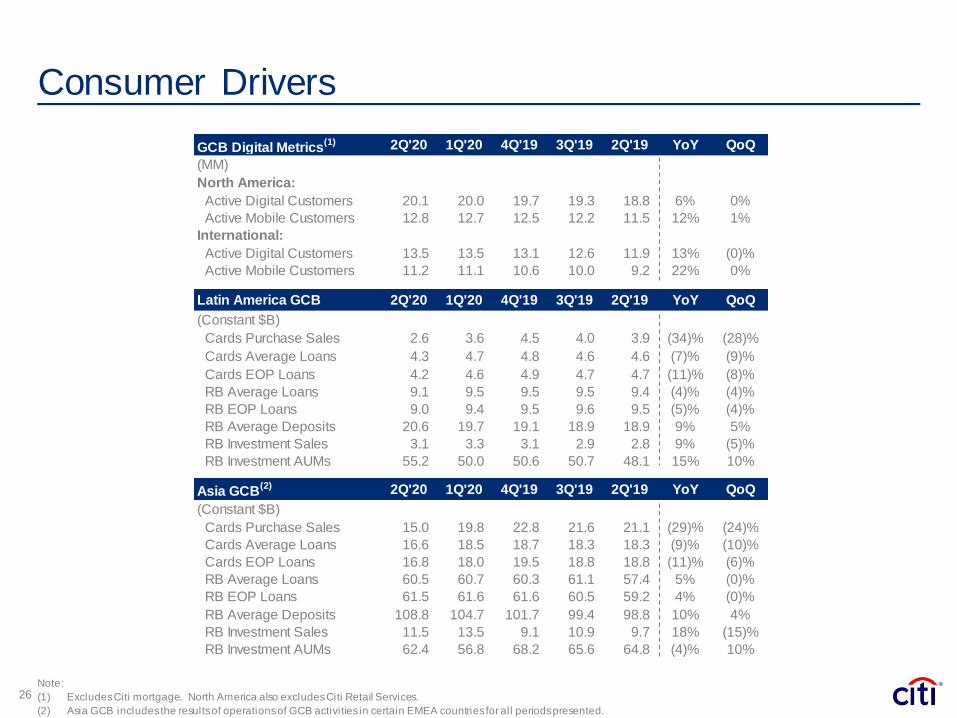

Asia GCB(2) 2Q'20 1Q'20 4Q'19 3Q'19 2Q'19 YoY QoQ

(Constant $B)

Cards Purchase Sales 15.0 19.8 22.8 21.6 21.1 (29)% (24)%

Cards Average Loans 16.6 18.5 18.7 18.3 18.3 (9)% (10)%

Cards EOP Loans 16.8 18.0 19.5 18.8 18.8 (11)% (6)%

RB Average Loans 60.5 60.7 60.3 61.1 57.4 5% (0)%

RB EOP Loans 61.5 61.6 61.6 60.5 59.2 4% (0)%

RB Average Deposits 108.8 104.7 101.7 99.4 98.8 10% 4%

RB Investment Sales 11.5 13.5 9.1 10.9 9.7 18% (15)%

RB Investment AUMs 62.4 56.8 68.2 65.6 64.8 (4)% 10%

Latin America GCB 2Q'20 1Q'20 4Q'19 3Q'19 2Q'19 YoY QoQ

(Constant $B)

Cards Purchase Sales 2.6 3.6 4.5 4.0 3.9 (34)% (28)%

Cards Average Loans 4.3 4.7 4.8 4.6 4.6 (7)% (9)%

Cards EOP Loans 4.2 4.6 4.9 4.7 4.7 (11)% (8)%

RB Average Loans 9.1 9.5 9.5 9.5 9.4 (4)% (4)%

RB EOP Loans 9.0 9.4 9.5 9.6 9.5 (5)% (4)%

RB Average Deposits 20.6 19.7 19.1 18.9 18.9 9% 5%

RB Investment Sales 3.1 3.3 3.1 2.9 2.8 9% (5)%

RB Investment AUMs 55.2 50.0 50.6 50.7 48.1 15% 10%

GCB Digital Metrics(1) 2Q'20 1Q'20 4Q'19 3Q'19 2Q'19 YoY QoQ

(MM)

North America:

Active Digital Customers 20.1 20.0 19.7 19.3 18.8 6% 0%

Active Mobile Customers 12.8 12.7 12.5 12.2 11.5 12% 1%

International:

Active Digital Customers 13.5 13.5 13.1 12.6 11.9 13% (0)%

Active Mobile Customers 11.2 11.1 10.6 10.0 9.2 22% 0%

Consumer Drivers

Note:

(1) Excludes Citi mortgage. North America also excludes Citi Retail Services.

(2) Asia GCB includes the results of operations of GCB activities in certain EMEA countries for all periods presented.

26

27.430.8

33.6

2Q'18 2Q'19 2Q'20

Consumer Drivers (continued)

E-Payment Penetration(4)

Note: LTM: Last Twelve Months.

(1) For additional information, please refer to footnote 1 on Slide 26.

(2) Agent contact rate defined as total agent handled calls divided by average total active accounts.

(3) E-statement penetration defined as total electronic statements divided by total statements (paper statements plus electronic statements).

(4) E-payment penetration defined as total electronic payments divided by total payments (paper payments plus electronic payments).

27

72% 75%78%

LTM'18 LTM'19 LTM'20

E-Statement Penetration(3)

Agent Contact Rate (2)

1.32 1.24

1.05

LTM'18 LTM'19 LTM'20

(20)%

47%50%

54%

LTM'18 LTM'19 LTM'20

~700 bps

~600 bps

Digital / Mobile Customers(1)

16.5

20.724.0

2Q'18 2Q'19 2Q'20

45%23%

Mobile CustomersDigital Customers(MM)

ICG 2Q'20 1Q'20 4Q'19 3Q'19 2Q'19 YoY QoQ

(Constant $B)

Average Deposits: 919 804 785 765 738 25% 14%

NA 481 402 392 374 351 37% 20%

EMEA 211 193 190 193 192 10% 9%

Latin America 40 34 33 31 30 30% 18%

Asia 187 176 170 166 164 14% 7%

EOP Deposits: 908 883 758 792 742 22% 3%

NA 472 445 374 393 356 33% 6%

EMEA 212 212 186 195 192 10% (0)%

Latin America 40 36 32 31 30 34% 10%

Asia 185 190 166 172 164 13% (3)%

Average Loans: 422 391 386 382 380 11% 8%

NA 215 196 191 189 188 14% 10%

EMEA 91 86 87 87 83 10% 5%

Latin America 43 36 36 36 38 15% 19%

Asia 73 73 72 70 72 1% 0%

EOP Loans: 404 435 384 392 386 5% (7)%

NA 203 224 191 191 191 6% (9)%

EMEA 88 95 85 92 86 2% (7)%

Latin America 42 41 36 36 37 14% 2%

Asia 71 75 72 73 72 (1)% (5)%

Institutional Drivers

Note: Totals may not sum due to rounding.28

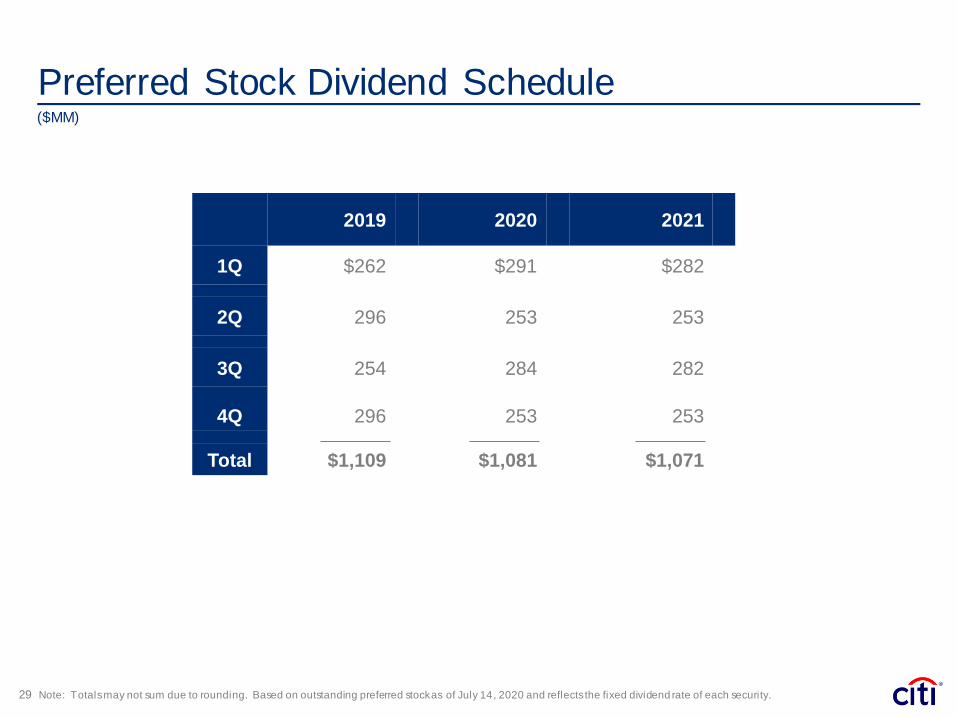

Preferred Stock Dividend Schedule

Note: Totals may not sum due to rounding. Based on outstanding preferred stock as of July 14, 2020 and reflects the fixed dividend rate of each security. 29

($MM)

2019 2020 2021

1Q $262 $291 $282

2Q 296 253 253

3Q 254 284 282

4Q 296 253 253

Total $1,109 $1,081 $1,071

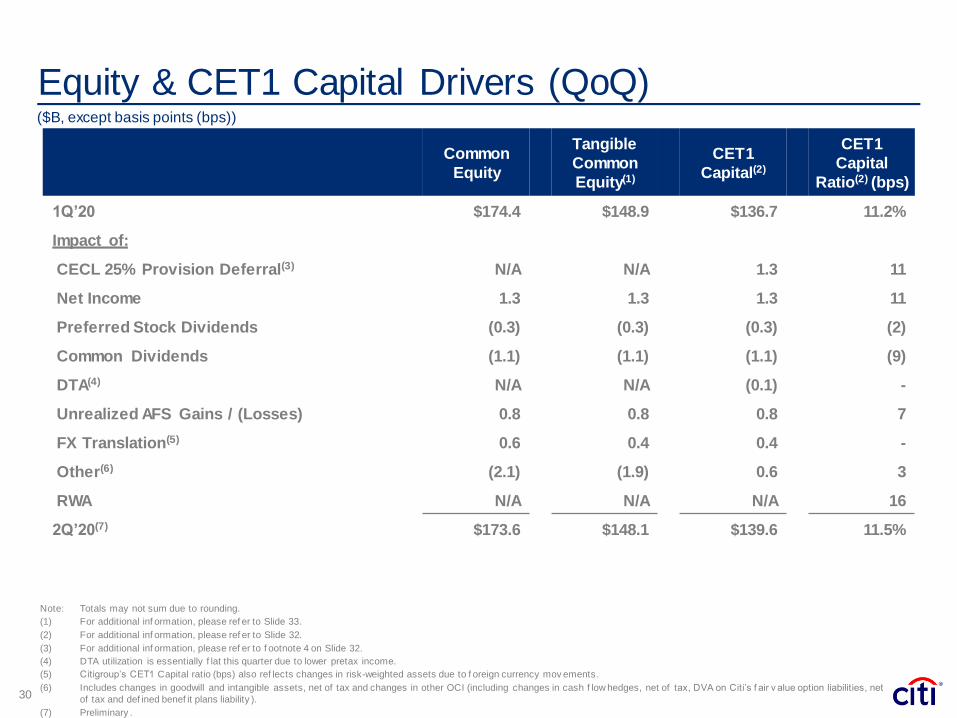

Equity & CET1 Capital Drivers (QoQ)

30

Note: Totals may not sum due to rounding.

(1) For additional inf ormation, please ref er to Slide 33.

(2) For additional inf ormation, please ref er to Slide 32.

(3) For additional inf ormation, please ref er to f ootnote 4 on Slide 32.

(4) DTA utilization is essentially f lat this quarter due to lower pretax income.

(5) Citigroup’s CET1 Capital ratio (bps) also ref lects changes in risk-weighted assets due to f oreign currency mov ements.

(6) Includes changes in goodwill and intangible assets, net of tax and changes in other OCI (including changes in cash f low hedges, net of tax, DVA on Citi’s f air v alue option liabilities, net

of tax and def ined benef it plans liability ).

(7) Preliminary .

($B, except basis points (bps))

Common

Equity

Tangible

Common

Equity(1)

CET1

Capital(2)

CET1

Capital

Ratio(2) (bps)

1Q’20 $174.4 $148.9 $136.7 11.2%

Impact of:

CECL 25% Provision Deferral(3) N/A N/A 1.3 11

Net Income 1.3 1.3 1.3 11

Preferred Stock Dividends (0.3) (0.3) (0.3) (2)

Common Dividends (1.1) (1.1) (1.1) (9)

DTA(4) N/A N/A (0.1) -

Unrealized AFS Gains / (Losses) 0.8 0.8 0.8 7

FX Translation(5) 0.6 0.4 0.4 -

Other(6) (2.1) (1.9) 0.6 3

RWA N/A N/A N/A 16

2Q’20(7) $173.6 $148.1 $139.6 11.5%

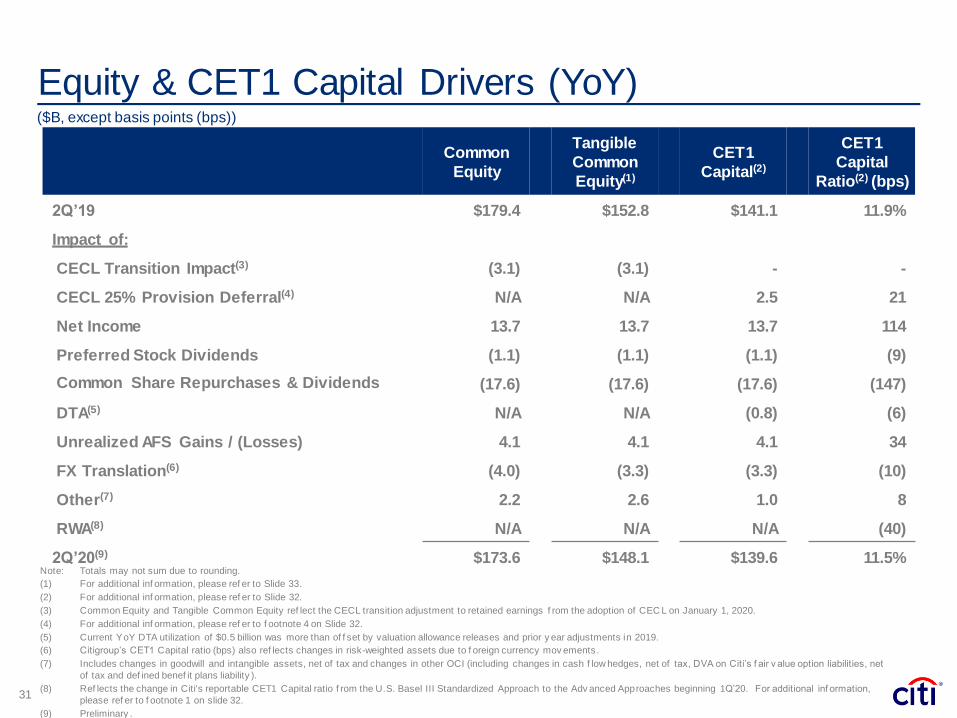

Equity & CET1 Capital Drivers (YoY)

31

($B, except basis points (bps))

Common

Equity

Tangible

Common

Equity(1)

CET1

Capital(2)

CET1

Capital

Ratio(2) (bps)

2Q’19 $179.4 $152.8 $141.1 11.9%

Impact of:

CECL Transition Impact(3) (3.1) (3.1) - -

CECL 25% Provision Deferral(4) N/A N/A 2.5 21

Net Income 13.7 13.7 13.7 114

Preferred Stock Dividends (1.1) (1.1) (1.1) (9)

Common Share Repurchases & Dividends (17.6) (17.6) (17.6) (147)

DTA(5) N/A N/A (0.8) (6)

Unrealized AFS Gains / (Losses) 4.1 4.1 4.1 34

FX Translation(6) (4.0) (3.3) (3.3) (10)

Other(7) 2.2 2.6 1.0 8

RWA(8) N/A N/A N/A (40)

2Q’20(9) $173.6 $148.1 $139.6 11.5%Note: Totals may not sum due to rounding.

(1) For additional inf ormation, please ref er to Slide 33.

(2) For additional inf ormation, please ref er to Slide 32.

(3) Common Equity and Tangible Common Equity ref lect the CECL transition adjustment to retained earnings f rom the adoption of CEC L on January 1, 2020.

(4) For additional inf ormation, please ref er to f ootnote 4 on Slide 32.

(5) Current YoY DTA utilization of $0.5 billion was more than of f set by valuation allowance releases and prior y ear adjustments in 2019.

(6) Citigroup’s CET1 Capital ratio (bps) also ref lects changes in risk-weighted assets due to f oreign currency mov ements.

(7) Includes changes in goodwill and intangible assets, net of tax and changes in other OCI (including changes in cash f low hedges, net of tax, DVA on Citi’s f air v alue option liabilities, net

of tax and def ined benef it plans liability ).

(8) Ref lects the change in Citi's reportable CET1 Capital ratio f rom the U.S. Basel III Standardized Approach to the Adv anced Approaches beginning 1Q’20. For additional inf ormation,

please ref er to f ootnote 1 on slide 32.

(9) Preliminary .

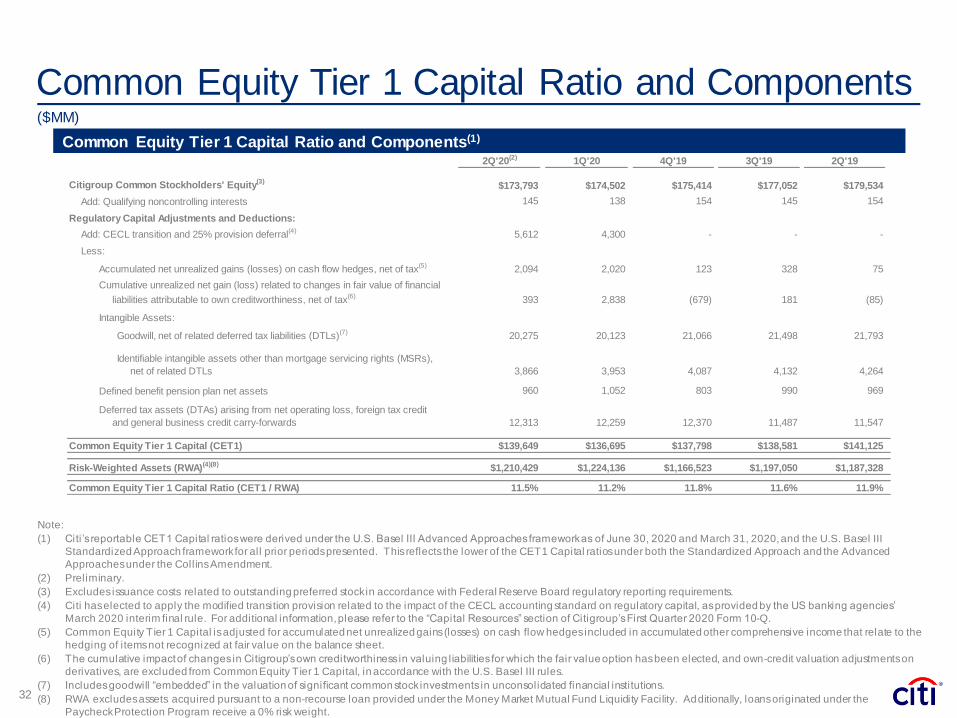

2Q'20(2) 1Q'20 4Q'19 3Q'19 2Q'19

Citigroup Common Stockholders' Equity(3) $173,793 $174,502 $175,414 $177,052 $179,534

Add: Qualifying noncontrolling interests 145 138 154 145 154

Regulatory Capital Adjustments and Deductions:

Add: CECL transition and 25% provision deferral(4) 5,612 4,300 - - -

Less:

Accumulated net unrealized gains (losses) on cash flow hedges, net of tax(5) 2,094 2,020 123 328 75

Cumulative unrealized net gain (loss) related to changes in fair value of financial

liabilities attributable to own creditworthiness, net of tax(6) 393 2,838 (679) 181 (85)

Intangible Assets:

Goodwill, net of related deferred tax liabilities (DTLs)(7) 20,275 20,123 21,066 21,498 21,793

Identifiable intangible assets other than mortgage servicing rights (MSRs),

net of related DTLs 3,866 3,953 4,087 4,132 4,264

Defined benefit pension plan net assets 960 1,052 803 990 969

Deferred tax assets (DTAs) arising from net operating loss, foreign tax credit

and general business credit carry-forwards 12,313 12,259 12,370 11,487 11,547

Common Equity Tier 1 Capital (CET1) $139,649 $136,695 $137,798 $138,581 $141,125

Risk-Weighted Assets (RWA)(4)(8) $1,210,429 $1,224,136 $1,166,523 $1,197,050 $1,187,328

Common Equity Tier 1 Capital Ratio (CET1 / RWA) 11.5% 11.2% 11.8% 11.6% 11.9%

Common Equity Tier 1 Capital Ratio and Components(1)

Note:

(1) Citi’s reportable CET1 Capital ratios were derived under the U.S. Basel III Advanced Approaches framework as of June 30, 2020 and March 31, 2020, and the U.S. Basel III

Standardized Approach framework for all prior periodspresented. This reflects the lower of the CET1 Capital ratios under both the Standardized Approach and the Advanced

Approaches under the Collins Amendment.

(2) Preliminary.

(3) Excludes issuance costs related to outstanding preferred stock in accordance with Federal Reserve Board regulatory reporting requirements.

(4) Citi has elected to apply the modified transition provision related to the impact of the CECL accounting standard on regulatory capital, as provided by the US banking agencies’

March 2020 interim final rule. For additional information, please refer to the “Capital Resources” section of Citigroup’s First Quarter 2020 Form 10-Q.

(5) Common Equity Tier 1 Capital is adjusted for accumulatednet unrealized gains (losses) on cash flow hedges included in accumulated other comprehensive income that relate to the

hedging of items not recognized at fair value on the balance sheet.

(6) The cumulative impact of changes in Citigroup’s own creditworthiness in valuing liabilities for which the fair value option has been elected, and own-credit valuation adjustments on

derivatives, are excluded from Common Equity Tier 1 Capital, in accordance with the U.S. Basel III rules.

(7) Includes goodwill “embedded” in the valuation of significant common stock investments in unconsolidated financial institutions.

(8) RWA excludes assets acquired pursuant to a non-recourse loan provided under the Money Market Mutual Fund Liquidity Facility. Additionally, loans originated under the

Paycheck Protection Program receive a 0% risk weight.

Common Equity Tier 1 Capital Ratio and Components

32

($MM)

2Q'20(1) 1Q'20 4Q'19 3Q'19 2Q'19

Common Stockholders' Equity $173,642 $174,351 $175,262 $176,893 $179,379

Less:

Goodwill 21,399 21,264 22,126 21,822 22,065

Intangible Assets (other than Mortgage Servicing Rights) 4,106 4,193 4,327 4,372 4,518

Tangible Common Equity (TCE) $148,137 $148,894 $148,809 $150,699 $152,796

Common Shares Outstanding (CSO) 2,082 2,082 2,114 2,183 2,259

Tangible Book Value Per Share (TCE / CSO) $71.15 $71.52 $70.39 $69.03 $67.64

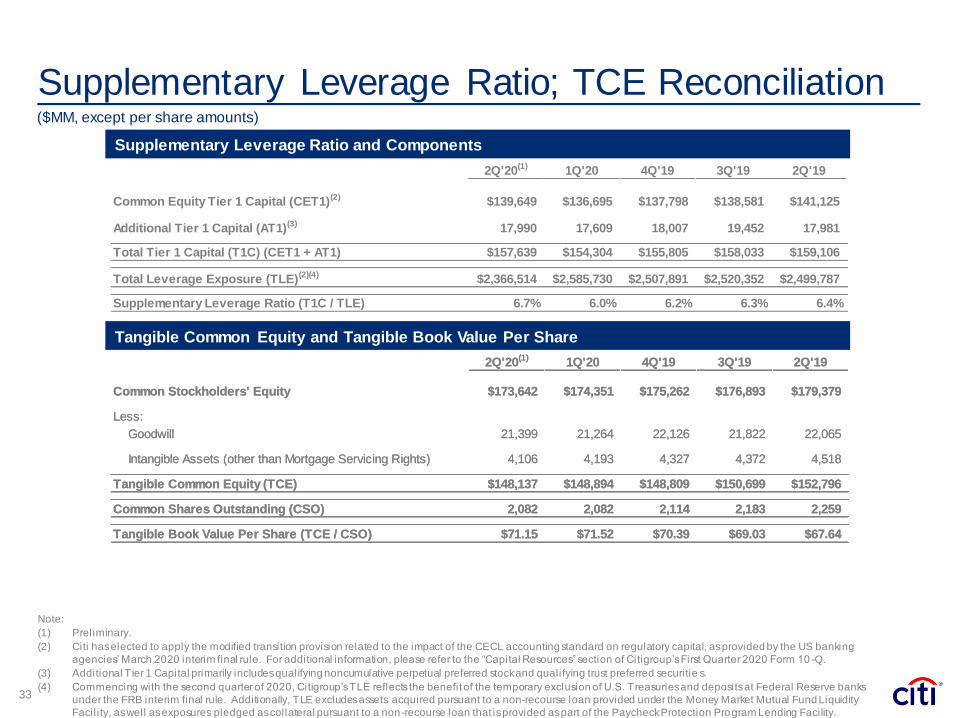

2Q'20(1) 1Q'20 4Q'19 3Q'19 2Q'19

Common Equity Tier 1 Capital (CET1)(2) $139,649 $136,695 $137,798 $138,581 $141,125

Additional Tier 1 Capital (AT1)(3) 17,990 17,609 18,007 19,452 17,981

Total Tier 1 Capital (T1C) (CET1 + AT1) $157,639 $154,304 $155,805 $158,033 $159,106

Total Leverage Exposure (TLE)(2)(4) $2,366,514 $2,585,730 $2,507,891 $2,520,352 $2,499,787

Supplementary Leverage Ratio (T1C / TLE) 6.7% 6.0% 6.2% 6.3% 6.4%

2Q'20(1) 1Q'20 4Q'19 3Q'19 2Q'19

Common Stockholders' Equity $173,642 $174,351 $175,262 $176,893 $179,379

Less:

Goodwill 21,399 21,264 22,126 21,822 22,065

Intangible Assets (other than Mortgage Servicing Rights) 4,106 4,193 4,327 4,372 4,518

Tangible Common Equity (TCE) $148,137 $148,894 $148,809 $150,699 $152,796

Common Shares Outstanding (CSO) 2,082 2,082 2,114 2,183 2,259

Tangible Book Value Per Share (TCE / CSO) $71.15 $71.52 $70.39 $69.03 $67.64

Supplementary Leverage Ratio and Components

Tangible Common Equity and Tangible Book Value Per Share

Supplementary Leverage Ratio; TCE Reconciliation

Note:

(1) Preliminary.

(2) Citi has elected to apply the modified transition provision related to the impact of the CECL accounting standard on regulatory capital, as provided by the US banking

agencies’ March 2020 interim final rule. For additional information, please refer to the “Capital Resources” section of Citigroup’s First Quarter 2020 Form 10 -Q.

(3) Additional Tier 1 Capital primarily includes qualifying noncumulative perpetual preferred stock and qualifying trust preferred securitie s.

(4) Commencing with the second quarter of 2020, Citigroup’s TLE reflects the benefit of the temporary exclusion of U.S. Treasuries and deposits at Federal Reserve banks

under the FRB interim final rule. Additionally, TLE excludes assets acquired pursuant to a non-recourse loan provided under the Money Market Mutual Fund Liquidity

Facility, aswell as exposures pledged as collateral pursuant to a non-recourse loan that is provided as part of the Paycheck Protection Program Lending Facility.

33

($MM, except per share amounts)

Citigroup 2Q'20 1Q'20 4Q'19 3Q'19 2Q'19 1Q'19 1H'20 1H'19

Reported Net Interest Revenue $11,080 $11,492 $11,997 $11,641 $11,950 $11,759 $22,572 $23,709

Impact of FX Translation - (160) (368) (326) (291) (367) (160) (657)

Net Interest Revenue in Constant Dollars $11,080 $11,332 $11,629 $11,315 $11,659 $11,392 $22,412 $23,052

Global Consumer Banking 2Q'20 1Q'20 2Q'19 1H'20 1H'19

Reported Retail Banking Revenues $2,836 $3,046 $3,202 $5,882 $6,308

Impact of FX Translation - (75) (155) - (229)

Retail Banking Revenues in Constant Dollars $2,836 $2,971 $3,047 $5,882 $6,079

Reported Cards Revenues $4,503 $5,128 $4,931 $9,631 $9,915

Impact of FX Translation - (39) (73) - (113)

Cards Revenues in Constant Dollars $4,503 $5,089 $4,858 $9,631 $9,802

International Consumer Banking 2Q'20 1Q'20 2Q'19 1H'20 1H'19

Reported Revenues $2,597 $2,950 $3,167 $5,547 $6,257

Impact of FX Translation - (115) (228) - (343)

Revenues in Constant Dollars $2,597 $2,835 $2,939 $5,547 $5,914

Reported Expenses $1,667 $1,832 $1,850 $3,499 $3,694

Impact of FX Translation - (68) (121) - (186)

Expenses in Constant Dollars $1,667 $1,764 $1,729 $3,499 $3,508

Reported Credit Costs $883 $939 $479 $1,822 $923

Impact of FX Translation - (62) (57) - (83)

Credit Costs in Constant Dollars $883 $877 $422 $1,822 $840

Reported Net Income $63 $156 $637 $219 $1,250

Impact of FX Translation - 13 (33) - (49)

Net Income in Constant Dollars $63 $169 $604 $219 $1,201

Citigroup 2Q'20 1Q'20 2Q'19 1H'20 1H'19

Reported Net Income $1,316 $2,522 $4,799 $3,838 $9,509

Less: Preferred Dividends 253 291 296 544 558

Net Income to Common Shareholders $1,063 $2,231 $4,503 $3,294 $8,951

Average TCE $148,516 $148,852 $152,193 $148,613 $151,821

RoTCE(1) 2.9% 6.0% 11.9% 4.5% 11.9%

Citigroup 2Q'20 1Q'20 2Q'19 1H'20 1H'19

Reported EOP Assets $2,233 $2,220 $1,988 $2,233 $1,988

Impact of FX Translation - 15 (32) - (32)

EOP Assets in Constant Dollars $2,233 $2,235 $1,957 $2,233 $1,957

Reported EOP Loans $685 $721 $689 $685 $689

Impact of FX Translation - 5 (10) - (10)

EOP Loans in Constant Dollars $685 $726 $678 $685 $678

Reported EOP Deposits $1,234 $1,185 $1,046 $1,234 $1,046

Impact of FX Translation - 8 (16) - (16)

EOP Deposits in Constant Dollars $1,234 $1,193 $1,030 $1,234 $1,030

Latin America Consumer Banking 2Q'20 1Q'20 2Q'19 1H'20 1H'19

Reported Revenues $1,050 $1,199 $1,320 $2,249 $2,592

Impact of FX Translation - (111) (193) - (266)

Revenues in Constant Dollars $1,050 $1,088 $1,127 $2,249 $2,326

Reported Expenses $604 $699 $704 $1,303 $1,377

Impact of FX Translation - (63) (97) - (132)

Expenses in Constant Dollars $604 $636 $607 $1,303 $1,245

Reported EBT $19 $(57) $321 $(38) $620

Impact of FX Translation - 12 (44) - (64)

EBT in Constant Dollars $19 $(45) $277 $(38) $556

Asia Consumer Banking(2) 2Q'20 1Q'20 2Q'19 1H'20 1H'19

Reported Revenues $1,547 $1,751 $1,847 $3,298 $3,665

Impact of FX Translation - (4) (35) - (77)

Revenues in Constant Dollars $1,547 $1,747 $1,812 $3,298 $3,588

Reported Expenses $1,063 $1,133 $1,146 $2,196 $2,317

Impact of FX Translation - (5) (24) - (54)

Expenses in Constant Dollars $1,063 $1,128 $1,122 $2,196 $2,263

Reported EBT $28 $236 $517 $264 $1,020

Impact of FX Translation - 3 (6) - (10)

EBT in Constant Dollars $28 $239 $511 $264 $1,010

Treasury and Trade Solutions 2Q'20 1Q'20 2Q'19 1H'20 1H'19

Reported Revenues $2,307 $2,423 $2,587 $4,730 $5,126

Impact of FX Translation - (38) (98) - (164)

Revenues in Constant Dollars $2,307 $2,385 $2,489 $4,730 $4,962

Securities Services 2Q'20 1Q'20 2Q'19 1H'20 1H'19

Reported Revenues $619 $645 $682 $1,264 $1,320

Impact of FX Translation - (12) (28) - (50)

Revenues in Constant Dollars $619 $633 $654 $1,264 $1,270

Adjusted Results and FX Impact Reconciliation

34Note: Totals may not sum due to rounding.

(1) RoTCE represents annualized net income available to common shareholders as a percentage of average TCE.

(2) Asia GCB includes the results of operations of GCB activities in certain EMEA countries for all periods presented.

($MM, except balance sheet items in $B)