24

Section 467 Rental Agreements January 21 2011 ABA Tax Section – Capital Recovery and Leasing

Section 467 Rental AgreementsJanuary 21 2011ABA Tax Section – Capital Recovery and Leasing

2

Disclaimer

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT ANY TAX ADVICE IN THIS COMMUNICATION IS NOT

INTENDED OR WRITTEN TO BE USED, AND INTENDED OR WRITTEN TO BE USED, AND

CANNOT BE USED, BY A CLIENT OR ANY OTHER CANNOT BE USED, BY A CLIENT OR ANY OTHER

PERSON OR ENTITY FOR THE PURPOSE OF (i) PERSON OR ENTITY FOR THE PURPOSE OF (i)

AVOIDING PENALTIES THAT MAY BE IMPOSED ON AVOIDING PENALTIES THAT MAY BE IMPOSED ON

ANY TAXPAYER OR (ii) PROMOTING, MARKETING ANY TAXPAYER OR (ii) PROMOTING, MARKETING

OR RECOMMENDING TO ANOTHER PARTY ANY OR RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.MATTERS ADDRESSED HEREIN.

3

Section 467Statutory Structure

Section 467 rental agreements Section 467 rental agreements defined asdefined as::

Agreements, written or oral, which provide for the use of Agreements, written or oral, which provide for the use of

tangibletangible property and are treated as leases for Federal property and are treated as leases for Federal

income tax purposes that have:income tax purposes that have:

Aggregate rent in excess of $250,000, AND EITHERAggregate rent in excess of $250,000, AND EITHER

Deferred or prepaidDeferred or prepaid rents, rents, OROR

Increasing or decreasingIncreasing or decreasing rentsrents

Note that any rental agreement that requires (or may require) Note that any rental agreement that requires (or may require)

contingent payments are generally deemed to have increasing or contingent payments are generally deemed to have increasing or

decreasing rents (subject to certain exceptions)decreasing rents (subject to certain exceptions)

4

Section 467Three Accrual Methods

Basic Method Basic Method –– Just Follow the Lease ProvisionsJust Follow the Lease Provisions

Proportional rental accrualProportional rental accrual

Constant rental accrualConstant rental accrual

5

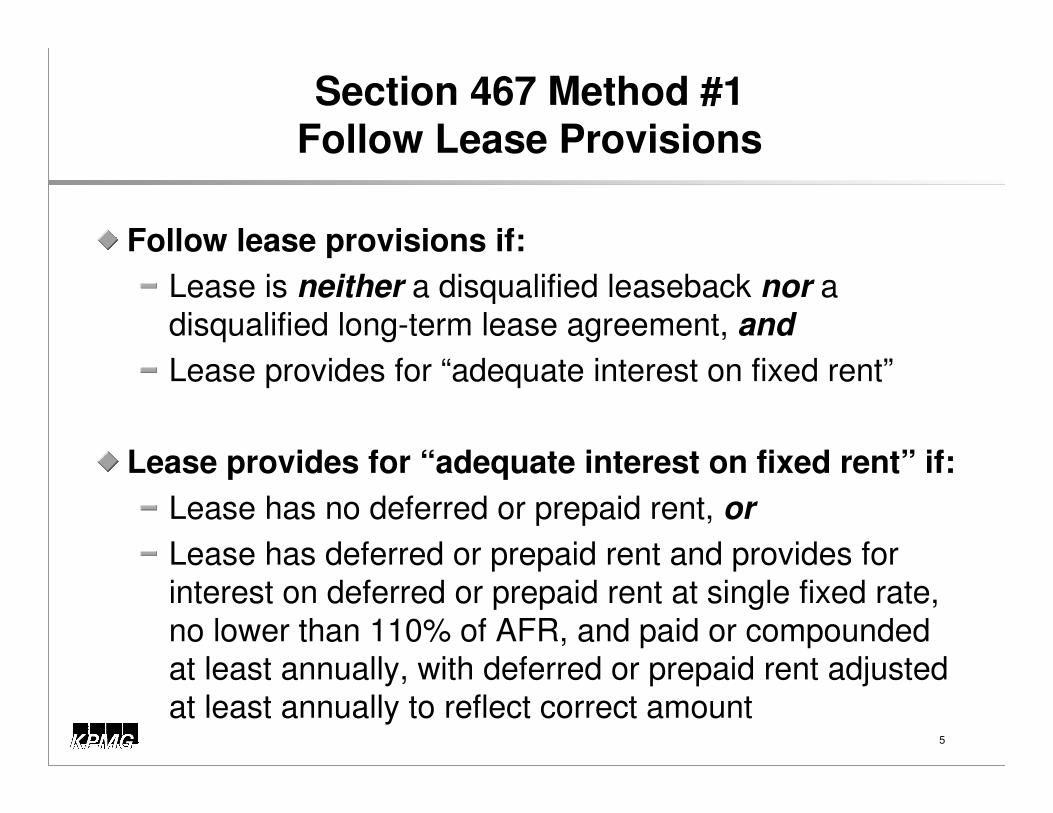

Section 467 Method #1Follow Lease Provisions

Follow lease provisions if:Follow lease provisions if:

Lease is Lease is neitherneither a disqualified leaseback a disqualified leaseback nornor a a

disqualified longdisqualified long--term lease agreement, term lease agreement, andand

Lease provides for Lease provides for ““adequate interest on fixed rentadequate interest on fixed rent””

Lease provides for Lease provides for ““adequate interest on fixed rentadequate interest on fixed rent”” if:if:

Lease has no deferred or prepaid rent, Lease has no deferred or prepaid rent, oror

Lease has deferred or prepaid rent and provides for Lease has deferred or prepaid rent and provides for

interest on deferred or prepaid rent at single fixed rate, interest on deferred or prepaid rent at single fixed rate,

no lower than 110% of AFR, and paid or compounded no lower than 110% of AFR, and paid or compounded at least annually, with deferred or prepaid rent adjusted at least annually, with deferred or prepaid rent adjusted

at least annually to reflect correct amountat least annually to reflect correct amount

Section 467 Method #1Follow Lease Provisions

Payment schedules are generally allocations of rent Payment schedules are generally allocations of rent

for section 467 purposesfor section 467 purposes

Use rent payment schedule if no separate rent Use rent payment schedule if no separate rent

allocation scheduleallocation schedule

For example For example –– rent holiday in payment schedule and no rent holiday in payment schedule and no separate rent allocation scheduleseparate rent allocation schedule

Zero rent allocated to rent holiday periodZero rent allocated to rent holiday period

Generally does not cause rental agreement to fail to allocate reGenerally does not cause rental agreement to fail to allocate rentnt

6

7

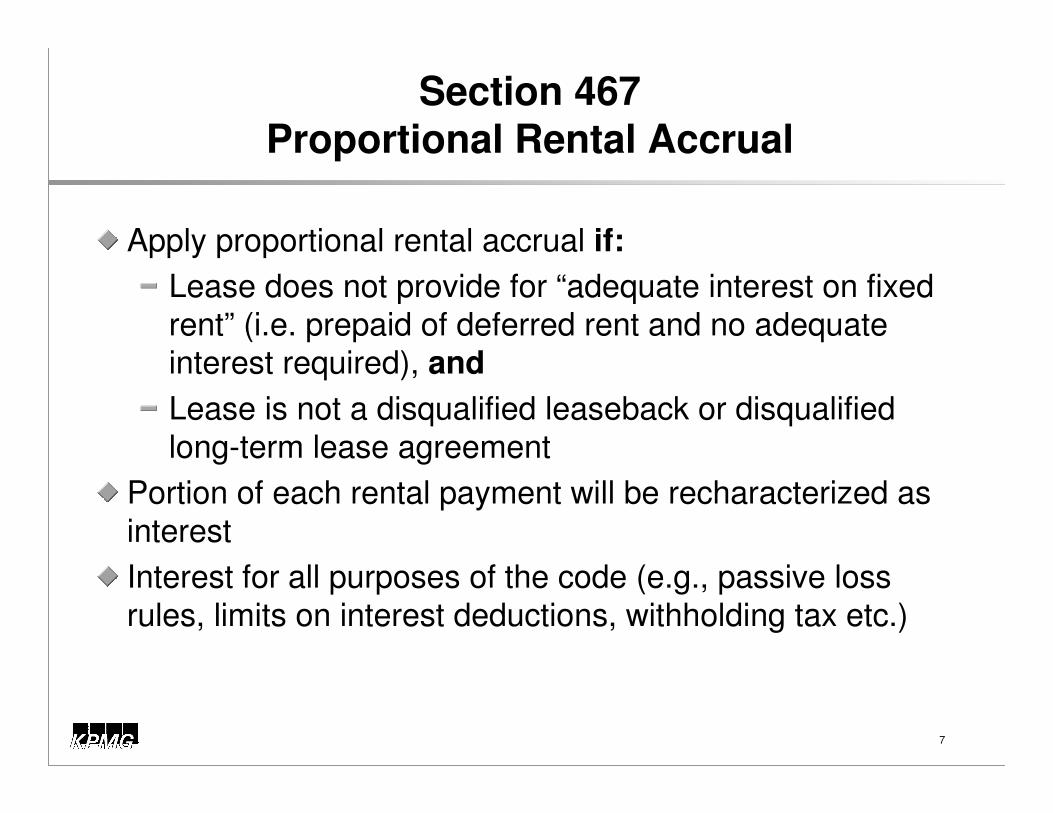

Section 467Proportional Rental Accrual

Apply proportional rental accrual Apply proportional rental accrual if:if:

Lease does not provide for Lease does not provide for ““adequate interest on fixed adequate interest on fixed

rentrent”” (i.e. prepaid of deferred rent and no adequate (i.e. prepaid of deferred rent and no adequate

interest required), interest required), andand

Lease is not a disqualified leaseback or disqualified Lease is not a disqualified leaseback or disqualified

longlong--term lease agreementterm lease agreement

Portion of each rental payment will be recharacterized as Portion of each rental payment will be recharacterized as

interestinterest

Interest for all purposes of the code (e.g., passive loss Interest for all purposes of the code (e.g., passive loss

rules, limits on interest deductions, withholding tax etc.)rules, limits on interest deductions, withholding tax etc.)

8

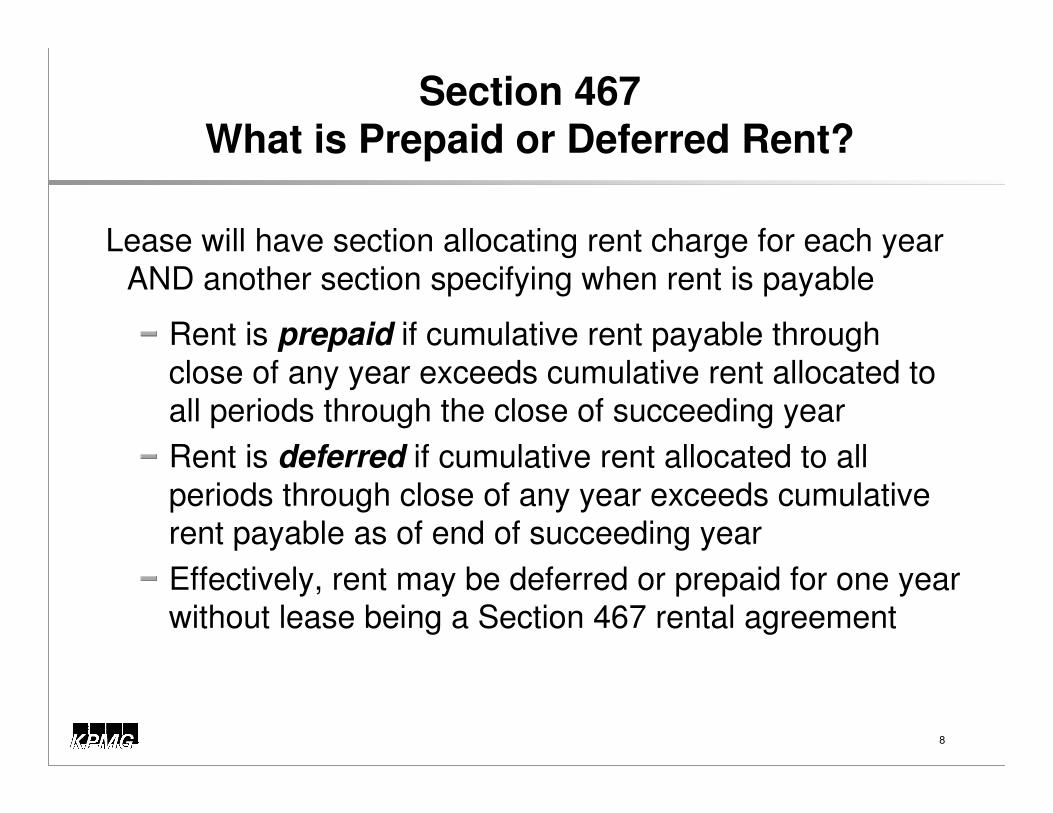

Section 467What is Prepaid or Deferred Rent?

Lease will have section allocating rent charge for each year Lease will have section allocating rent charge for each year

AND another section specifying when rent is payableAND another section specifying when rent is payable

Rent is Rent is prepaidprepaid if cumulative rent payable through if cumulative rent payable through

close of any year exceeds cumulative rent allocated to close of any year exceeds cumulative rent allocated to

all periods through the close of succeeding yearall periods through the close of succeeding year

Rent is Rent is deferreddeferred if cumulative rent allocated to all if cumulative rent allocated to all

periods through close of any year exceeds cumulative periods through close of any year exceeds cumulative rent payable as of end of succeeding yearrent payable as of end of succeeding year

Effectively, rent may be deferred or prepaid for one year Effectively, rent may be deferred or prepaid for one year

without lease being a Section 467 rental agreementwithout lease being a Section 467 rental agreement

9

Deferred Rent vs. Prepaid Rent

Deferred RentDeferred Rent

YearYearRent Rent

AllocatedAllocatedRent Rent

PayablePayable

11 $20$20 $0$0

22 $20$20 $15$15

33 $20$20 $20$20

44 $20$20 $30$30

55 $20$20 $35$35

Prepaid RentPrepaid Rent

YearYearRent Rent

AllocatedAllocatedRent Rent

PayablePayable

11 $20$20 $45$45

22 $20$20 $25$25

33 $20$20 $10$10

44 $20$20 $10$10

55 $20$20 $10$10

10

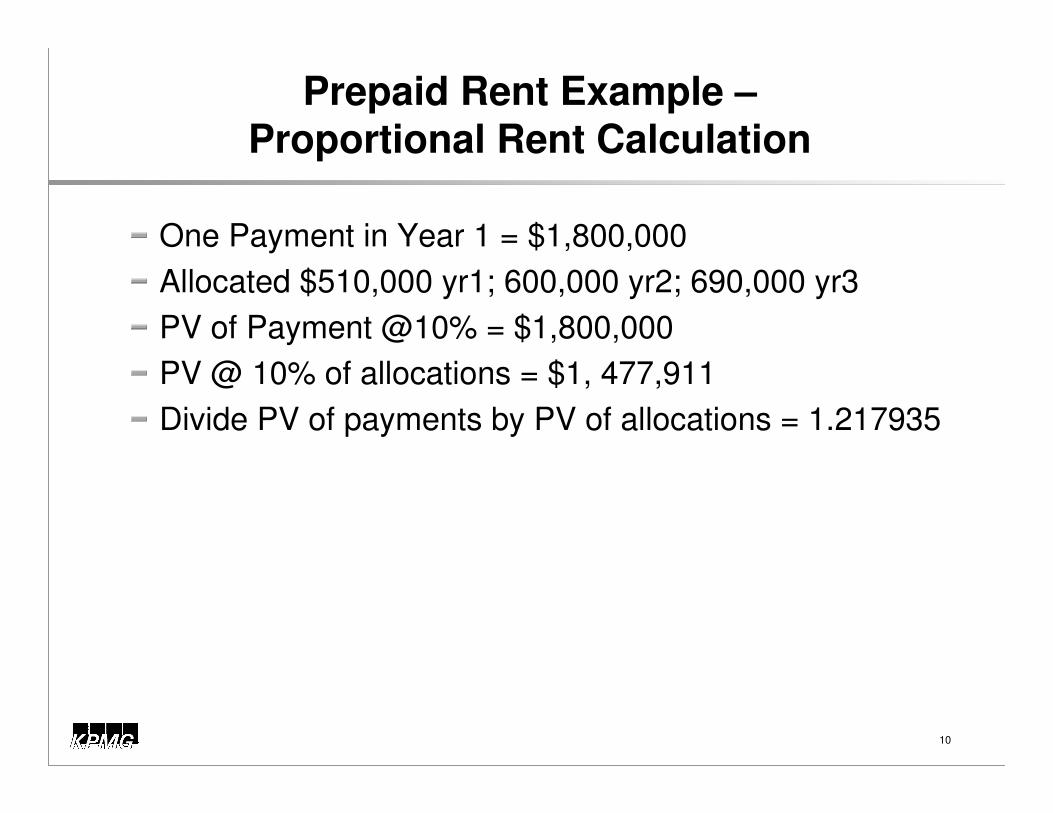

Prepaid Rent Example –Proportional Rent Calculation

One Payment in Year 1 = $1,800,000One Payment in Year 1 = $1,800,000

Allocated $510,000 yr1; 600,000 yr2; 690,000 yr3Allocated $510,000 yr1; 600,000 yr2; 690,000 yr3

PV of Payment @10% = $1,800,000PV of Payment @10% = $1,800,000

PV @ 10% of allocations = $1, 477,911PV @ 10% of allocations = $1, 477,911

Divide PV of payments by PV of allocations = 1.217935Divide PV of payments by PV of allocations = 1.217935

11

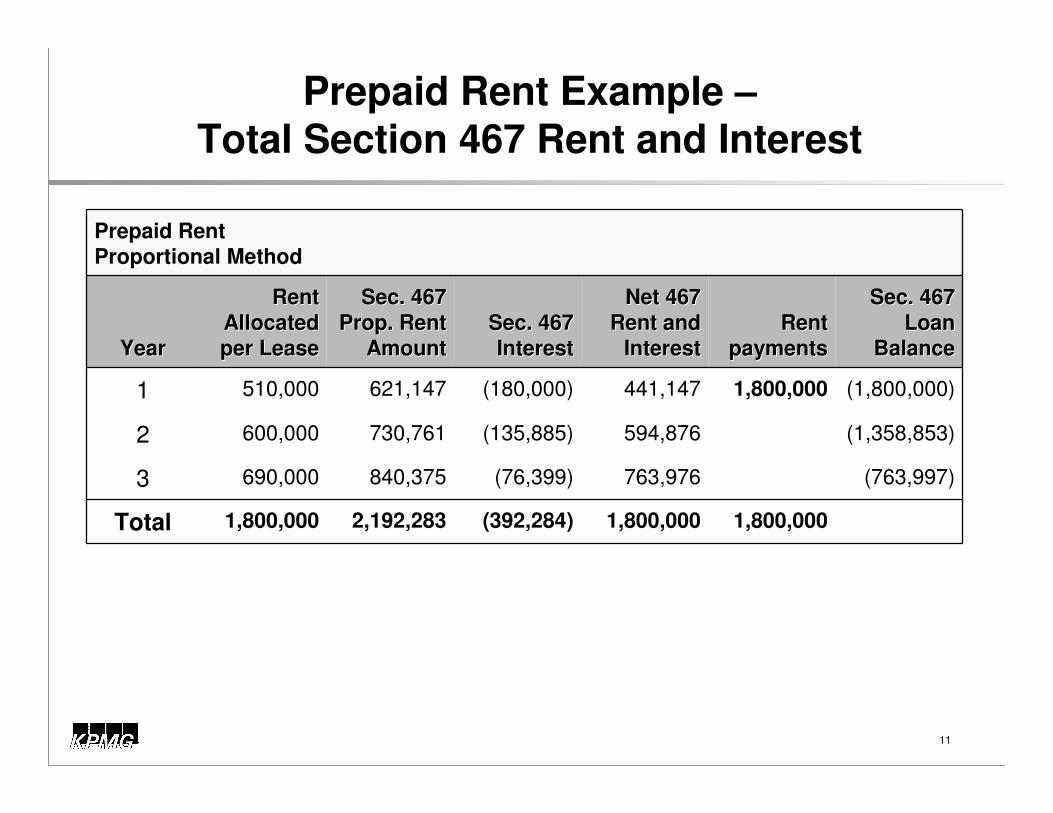

Prepaid Rent Example –Total Section 467 Rent and Interest

Prepaid Rent Prepaid Rent

Proportional MethodProportional Method

YearYear

Rent Rent

Allocated Allocated

per Leaseper Lease

Sec. 467 Sec. 467

Prop. Rent Prop. Rent

AmountAmountSec. 467 Sec. 467

InterestInterest

Net 467 Net 467

Rent and Rent and

InterestInterestRent Rent

paymentspayments

Sec. 467 Sec. 467

Loan Loan

BalanceBalance

11 510,000510,000 621,147621,147 (180,000)(180,000) 441,147441,147 1,800,0001,800,000 (1,800,000)(1,800,000)

22 600,000600,000 730,761730,761 (135,885)(135,885) 594,876594,876 (1,358,853)(1,358,853)

33 690,000690,000 840,375840,375 (76,399)(76,399) 763,976763,976 (763,997)(763,997)

TotalTotal 1,800,0001,800,000 2,192,2832,192,283 (392,284)(392,284) 1,800,0001,800,000 1,800,0001,800,000

12

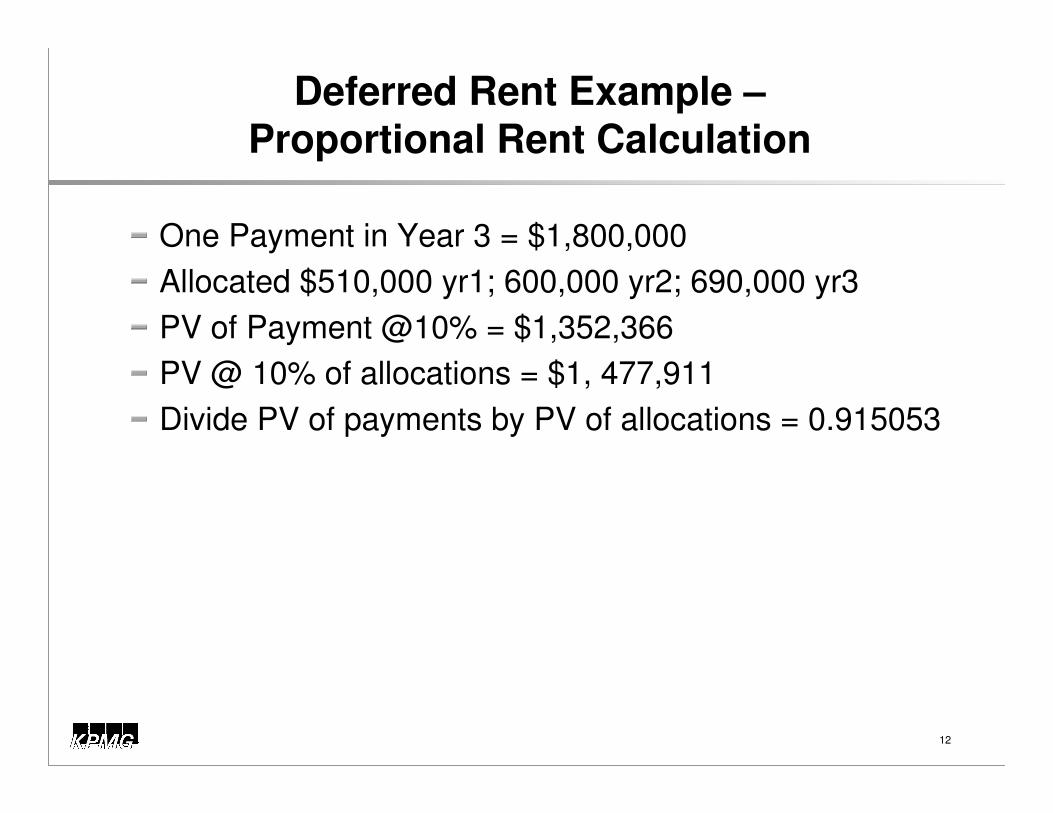

Deferred Rent Example –Proportional Rent Calculation

One Payment in Year 3 = $1,800,000One Payment in Year 3 = $1,800,000

Allocated $510,000 yr1; 600,000 yr2; 690,000 yr3Allocated $510,000 yr1; 600,000 yr2; 690,000 yr3

PV of Payment @10% = $1,352,366PV of Payment @10% = $1,352,366

PV @ 10% of allocations = $1, 477,911PV @ 10% of allocations = $1, 477,911

Divide PV of payments by PV of allocations = 0.915053Divide PV of payments by PV of allocations = 0.915053

13

Deferred Rent Example –Total Section 467 Rent and Interest

Deferred Rent Deferred Rent

Proportional MethodProportional Method

YearYear

Rent Rent

Allocated Allocated

per Leaseper Lease

Sec. 467 Sec. 467

Prop. Rent Prop. Rent

AmountAmountSec. 467 Sec. 467

InterestInterest

Net 467 Net 467

Rent and Rent and

InterestInterestRent Rent

paymentspayments

Sec. 467 Sec. 467

Loan Loan

BalanceBalance

11 510,000510,000 466,677466,677 466,677466,677

22 600,000600,000 549,031549,031 46,66746,667 595,698595,698 466,676466,676

33 690,000690,000 631,386631,386 106,237106,237 737,623737,623 1,800,0001,800,000 1,062,3741,062,374

TotalTotal 1,800,0001,800,000 1,647,0941,647,094 152,904152,904 1,800,0001,800,000 1,800,0001,800,000

14

Disqualified Leasebacks and Long-term Lease Agreements

LeasebackLeaseback

If tenant had an interest within 2 years of leasing from landlorIf tenant had an interest within 2 years of leasing from landlordd

LongLong--Term Lease AgreementTerm Lease Agreement

Lease term exceeds 75% of statutory recovery period of property;Lease term exceeds 75% of statutory recovery period of property;e.g., e.g.,

Specified statutory recovery period, Specified statutory recovery period, notnot depreciable life of assetdepreciable life of asset

For real property, statutory recovery period is 19 yearsFor real property, statutory recovery period is 19 years

Leaseback or LongLeaseback or Long--Term Lease Agreement is Term Lease Agreement is

disqualified ifdisqualified if::

AA principal purpose for providing increasing or decreasing rents principal purpose for providing increasing or decreasing rents is is the avoidance of Federal income tax, the avoidance of Federal income tax, andand

IRS decides to treat agreement as disqualifiedIRS decides to treat agreement as disqualified

15

Deferred Rent Example – Constant Rental Calculation

One Payment in Year 3 = $1,800,000One Payment in Year 3 = $1,800,000

PV of Payment @10% = $1,352,366PV of Payment @10% = $1,352,366

PV @ 10% of $1 assumed to be payable on the last day PV @ 10% of $1 assumed to be payable on the last day

of each accrual period = $2.486852of each accrual period = $2.486852

Divide PV of payments by PV of $1 =Divide PV of payments by PV of $1 =

Constant Rental Factor of $543,806Constant Rental Factor of $543,806

16

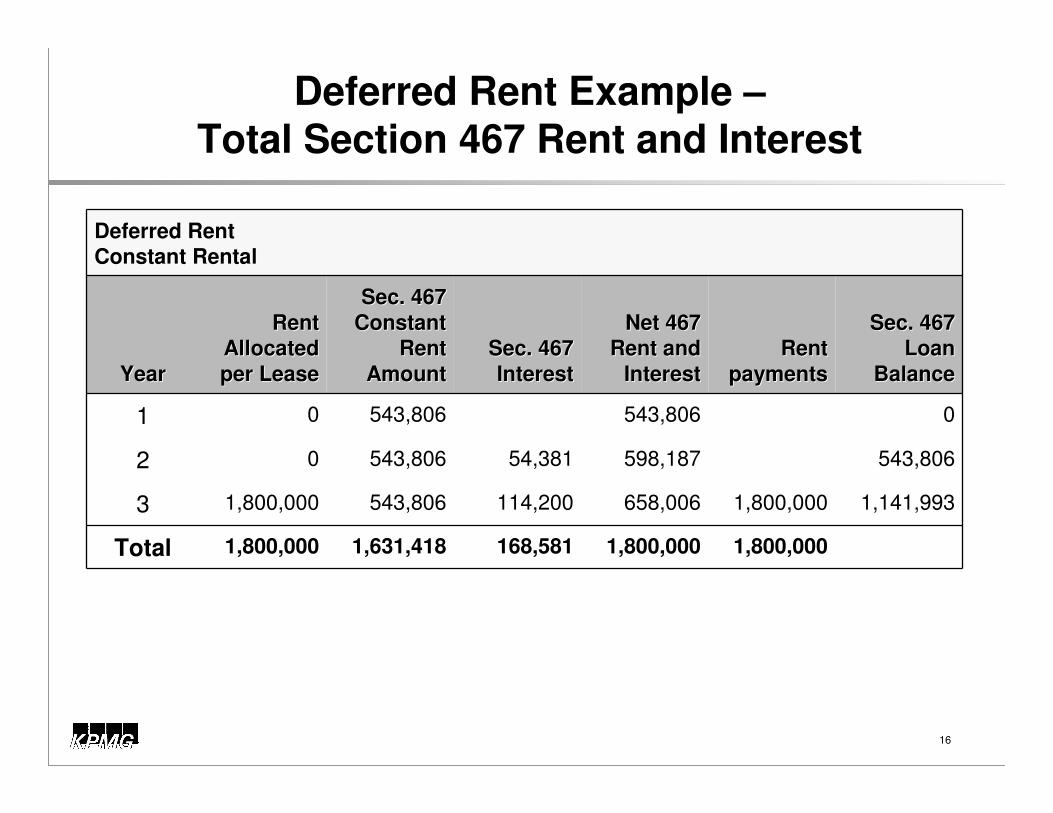

Deferred Rent Example –Total Section 467 Rent and Interest

Deferred Rent Deferred Rent

Constant RentalConstant Rental

YearYear

Rent Rent

Allocated Allocated

per Leaseper Lease

Sec. 467 Sec. 467

Constant Constant

Rent Rent

AmountAmountSec. 467 Sec. 467

InterestInterest

Net 467 Net 467

Rent and Rent and

InterestInterestRent Rent

paymentspayments

Sec. 467 Sec. 467

Loan Loan

BalanceBalance

11 00 543,806543,806 543,806543,806 00

22 00 543,806543,806 54,38154,381 598,187598,187 543,806543,806

33 1,800,0001,800,000 543,806543,806 114,200114,200 658,006658,006 1,800,0001,800,000 1,141,9931,141,993

TotalTotal 1,800,0001,800,000 1,631,4181,631,418 168,581168,581 1,800,0001,800,000 1,800,0001,800,000

17

“A” (not THE) Principal Purpose to Avoid Tax

Constant rental accrual does not apply unless rental Constant rental accrual does not apply unless rental agreement is disqualifiedagreement is disqualified

To be disqualified, agreement must have To be disqualified, agreement must have aa principal principal

purpose of tax avoidancepurpose of tax avoidance

How is the principal purpose test applied?How is the principal purpose test applied?

Agreement will be Agreement will be ““closely scrutinizedclosely scrutinized”” if reasonable to if reasonable to

expect expect ““significantsignificant”” difference between marginal tax rate difference between marginal tax rate

of lessor and lessee at some point during lease term.of lessor and lessee at some point during lease term.

Greater than 10% is significant, taking into account NOLs, crediGreater than 10% is significant, taking into account NOLs, credit t carryovers, AMT and partnership allocations.carryovers, AMT and partnership allocations.

18

Safe Harbors to Avoid Constant Rental Accrual Treatment

Increasing or decreasing rent is not considered to be Increasing or decreasing rent is not considered to be

motivated by tax avoidance where, inter alia:motivated by tax avoidance where, inter alia:

Rent allocated for each year is within Rent allocated for each year is within 10%10% of average annual rentof average annual rent

Where the rental agreement is a longWhere the rental agreement is a long--term agreement and at term agreement and at least 90% of property subject to agreement is real property, least 90% of property subject to agreement is real property, 15%15% variation allowedvariation allowed

If 10% test applies, eliminate free rent period < 3 months in If 10% test applies, eliminate free rent period < 3 months in making calculation if concession is at start of leasemaking calculation if concession is at start of lease

If 15% test applies, eliminate free rent period up to 24 months If 15% test applies, eliminate free rent period up to 24 months or 10% of the lease term if commercially reasonableor 10% of the lease term if commercially reasonable

Increase or decrease in rent attributable to a single rent holidIncrease or decrease in rent attributable to a single rent holiday for ay for one consecutive period if rent holiday is for 3 months or less aone consecutive period if rent holiday is for 3 months or less at t beginning of lease term, or does not exceed 24 months and is beginning of lease term, or does not exceed 24 months and is commercially reasonable in locality of use of propertycommercially reasonable in locality of use of property

19

Safe Harbors to Avoid Constant Rental Accrual Treatment

Safe Harbors (continued):Safe Harbors (continued):

Increase or decrease in rent attributable to a specified Increase or decrease in rent attributable to a specified

contingent rent provision, including:contingent rent provision, including:

A qualified percentage rents provision (rent equal to fixed A qualified percentage rents provision (rent equal to fixed percentage of lesseepercentage of lessee’’s sales receipts or sales)s sales receipts or sales)

An adjustment based on a reasonable price indexAn adjustment based on a reasonable price index

A provision requiring lessee to pay costs to a third partyA provision requiring lessee to pay costs to a third party

A provision requiring payment of late payment chargesA provision requiring payment of late payment charges

A tax indemnity provisionA tax indemnity provision

A variable interest rate provisionA variable interest rate provision

20

Section 467 and Lease Modifications

If a lease is If a lease is ““substantially modified,substantially modified,”” it is treated as a new it is treated as a new agreement made on the date of modificationagreement made on the date of modification

New determination must be made as to whether lease is a Section New determination must be made as to whether lease is a Section 467 rental agreement, and whether proportional rental accrual or467 rental agreement, and whether proportional rental accrual orconstant rental accrual applyconstant rental accrual apply

Safe harbors Safe harbors –– not a substantial modification if:not a substantial modification if:

Change in rent solely result of lessor refinancing debt incurredChange in rent solely result of lessor refinancing debt incurred to to acquire property,acquire property,

Change in rent in any rental period does not vary by more than 1Change in rent in any rental period does not vary by more than 1% % from original rent in that period, orfrom original rent in that period, or

Change in rent due to lesseeChange in rent due to lessee’’s obligations to pay thirds obligations to pay third--party costs party costs and certain other types of contingent paymentsand certain other types of contingent payments

Change in lessor or lessee generally not a substantial modificatChange in lessor or lessee generally not a substantial modificationion

21

Section 467 Recapture

If a lessor transfer property subject to a leaseback or longIf a lessor transfer property subject to a leaseback or long--term agreement (not disqualified) and the lease has some term agreement (not disqualified) and the lease has some

amount of backamount of back--loaded rent,loaded rent,”” the lessor must recapture as the lessor must recapture as

ordinary income an amount of gain on the sale equal to the ordinary income an amount of gain on the sale equal to the income it would have received if the lease had been income it would have received if the lease had been

subject to constant rental accrual over the income it subject to constant rental accrual over the income it actually reportedactually reported

Section 467 Method Changes

Automatic consent generally available for change to Automatic consent generally available for change to

use rent allocation methoduse rent allocation method

App. Sec. 20.01 of Rev. Proc. 2008App. Sec. 20.01 of Rev. Proc. 2008--52, as modified by Sec. 2.24 52, as modified by Sec. 2.24 of Rev. Proc. 2009of Rev. Proc. 2009--39 (automatic change # 136)39 (automatic change # 136)

Not applicable to taxpayers required to use constant rental accrNot applicable to taxpayers required to use constant rental accrual ual method or proportional rental accrual methodmethod or proportional rental accrual method

Must attach to Form 3115 copy of one of section 467 rental Must attach to Form 3115 copy of one of section 467 rental agreements to be covered by change (or at least rent allocation agreements to be covered by change (or at least rent allocation pages)pages)

No audit protection if IRS determines section 467 rental No audit protection if IRS determines section 467 rental agreement is disqualified leaseback or longagreement is disqualified leaseback or long--term agreementterm agreement

22

Section 467 Method Changes

Automatic consent (cont.)Automatic consent (cont.)

Generally see when taxpayers have been inadvertently Generally see when taxpayers have been inadvertently

following bookfollowing book

Taxpayer recognizes deferred rent on straightTaxpayer recognizes deferred rent on straight--line basis over line basis over term of rental agreement even though required to use rent term of rental agreement even though required to use rent allocation method under section 467allocation method under section 467

All other changes generally nonAll other changes generally non--automaticautomatic

Rev. Proc. 97Rev. Proc. 97--2727

Section 481(a) adjustment spread periodSection 481(a) adjustment spread period

Unfavorable (positive) adjustment Unfavorable (positive) adjustment –– 4 years4 years

Favorable (negative) adjustment Favorable (negative) adjustment –– 1 year1 year

23

Contact Information

Kevin Juran Kevin Juran –– KPMG LLP, 212 872KPMG LLP, 212 872--5826, 5826, [email protected]@kpmg.com

Natalie Tucker Natalie Tucker –– RSM McGladrey Inc., 904 680RSM McGladrey Inc., 904 680--7209, 7209, [email protected]@mcladrey.com

Glenn Johnson Glenn Johnson –– Ernst & Young LLP, 202 327Ernst & Young LLP, 202 327--6687, 6687, [email protected]@ey.com

Katherine Breaks Katherine Breaks –– KPMG LLP, 202 533KPMG LLP, 202 533--4578, [email protected], [email protected]

24