Section 4(c)(8) of the BHC Act (Mortgage Banking—Derivative Commitments to Originate and Sell Mortgage Loans) Section 3071.0 3071.0.1 INTERAGENCY ADVISORY ON ACCOUNTING AND REPORTING FOR COMMITMENTS TO ORIGINATE AND SELL MORTGAGE LOANS On May 3, 2005, the Federal Reserve and the other federal financial institution regulatory agen- cies 1 (the agencies) issued an Interagency Advisory on Accounting and Reporting for Com- mitments to Originate and Sell Mortgage Loans. 2 (See SR-05-10.) The advisory provides guidance on the appro- priate accounting and reporting for commit- ments to— • originate mortgage loans that will be held for resale, and • sell mortgage loans under mandatory-delivery and best-efforts contracts. Commitments to originate mortgage loans that will be held for resale are derivatives and must be accounted for at fair value on the bal- ance sheet by the issuer. All loan-sales agree- ments, including both mandatory-delivery and best-efforts contracts, must be evaluated to deter- mine whether the agreements meet the defini- tion of a derivative under Statement of Financial Accounting Standards No. 133, ‘‘Accounting for Derivative Instruments and Hedging Activities,’’ as amended by Statement of Financial Account- ing Standards No. 149, ‘‘Amendment of State- ment 133 on Derivative Instruments and Hedg- ing Activities’’ (collectively, FAS 133). A financial institution should also account for loan- sales agreements that meet the definition of a derivative at fair value on the balance sheet. The advisory discusses the characteristics that should be considered in determining whether mandatory-delivery and best-efforts contracts are derivatives and the accounting and regula- tory reporting treatment for both commitments to originate mortgage loans that will be held for resale and those loan-sales agreements that meet the definition of a derivative. The advisory also addresses the guidance that should be consid- ered in determining the fair value of derivatives. The advisory provides additional guidance on the application of FAS 133. Financial institu- tions, including those that are not required to file reports with the Securities and Exchange Com- mission (SEC), are expected to follow the guid- ance in SEC Staff Accounting Bulletin No. 105, ‘‘Application of Accounting Principles to Loan Commitments’’ (SAB 105). 3 A financial institution is expected to account for and report derivative loan commitments and forward loan-sales commitments as derivatives in accordance with generally accepted account- ing principles (GAAP), which include the use of valuation techniques that are reasonable and supportable in the determination of fair value. An institution’s failure to account for and report derivative loan commitments and forward loan- sales commitments in regulatory reports in accordance with GAAP may be an unsafe and unsound practice. 3071.0.1.1 Accounting and Reporting 3071.0.1.1.1 Accounting Policies Well-managed financial institutions have writ- ten and consistently applied accounting policies for commitments to originate mortgage loans that will be held for resale and to sell mortgage loans under mandatory-delivery and best-efforts contracts, including approved valuation method- ologies and procedures to formally approve changes to those methodologies. The method- ologies should be reasonable, objectively sup- ported, and fully documented. Procedural disci- pline and consistency are key concepts in any valuation-measurement technique. Institutions should ensure that internal controls, including effective independent review or audit, are in place to provide integrity to the valuation pro- cess. Institutions’ practices should, therefore, reflect these concepts to ensure the reliability of their valuations of derivative loan commitments and forward loan-sales commitments. 3071.0.1.1.2 Derivative Loan Commitments A financial institution should account for deriva- 1. The agencies are the Board of Governors of the Federal Reserve System, the Federal Deposit Insurance Corporation, the National Credit Union Administration, the Office of the Comptroller of the Currency, and the Office of Thrift Supervi- sion. 2. The guidance in the interagency advisory is also in- tended to apply to financial-statement reporting by bank hold- ing companies. 3. Staff accounting bulletins (SABs) summarize the views of the SEC’s staff regarding the application of generally accepted accounting principles. BHC Supervision Manual January 2006 Page 1

Transcript

Section 4(c)(8) of the BHC Act (Mortgage Banking—DerivativeCommitments to Originate and Sell Mortgage Loans) Section 3071.0

3071.0.1 INTERAGENCY ADVISORYON ACCOUNTING AND REPORTINGFOR COMMITMENTS TO ORIGINATEAND SELL MORTGAGE LOANS

On May 3, 2005, the Federal Reserve and theother federal financial institution regulatoryagen-cies1 (the agencies) issued an InteragencyAdvisory on Accounting and Reporting for Com-mitments to Originate and Sell MortgageLoans.2 (See SR-05-10.)

The advisory provides guidance on the appro-priate accounting and reporting for commit-ments to—

• originate mortgage loans that will beheld forresale, and

• sell mortgage loans under mandatory-deliveryand best-efforts contracts.

Commitments to originate mortgage loansthat will be held for resale are derivatives andmust be accounted for at fair value on the bal-ance sheet by the issuer. All loan-sales agree-ments, including both mandatory-delivery andbest-efforts contracts, must be evaluated to deter-mine whether the agreements meet the defini-tion of a derivative under Statement of FinancialAccounting Standards No. 133, ‘‘Accounting forDerivative Instruments and Hedging Activities,’’as amended by Statement of Financial Account-ing Standards No. 149, ‘‘Amendment of State-ment 133 on Derivative Instruments and Hedg-ing Activities’’ (collectively, FAS 133). Afinancial institution should also account for loan-sales agreements that meet the definition of aderivative at fair value on the balance sheet.

The advisory discusses the characteristics thatshould be considered in determining whethermandatory-delivery and best-efforts contractsare derivatives and the accounting and regula-tory reporting treatment for both commitmentsto originate mortgage loans that will be held forresale and those loan-sales agreements that meetthe definition of a derivative. The advisory alsoaddresses the guidance that should be consid-ered in determining the fair value of derivatives.

The advisory provides additional guidance on

the application of FAS 133. Financial institu-tions, including those that arenot required to filereports with the Securities and Exchange Com-mission (SEC), are expected to follow the guid-ance in SEC Staff Accounting Bulletin No. 105,‘‘Application of Accounting Principles to LoanCommitments’’ (SAB 105).3

A financial institution is expected to accountfor and report derivative loan commitments andforward loan-sales commitments as derivativesin accordance with generally accepted account-ing principles (GAAP), which include the use ofvaluation techniques that are reasonable andsupportable in the determination of fair value.An institution’s failure to account for and reportderivative loan commitments and forward loan-sales commitments in regulatory reports inaccordance with GAAP may be an unsafe andunsound practice.

3071.0.1.1 Accounting and Reporting

3071.0.1.1.1 Accounting Policies

Well-managed financial institutions have writ-ten and consistently applied accounting policiesfor commitments to originate mortgage loansthat will be held for resale and to sell mortgageloans under mandatory-delivery and best-effortscontracts, including approved valuation method-ologies and procedures to formally approvechanges to those methodologies. The method-ologies should be reasonable, objectively sup-ported, and fully documented. Procedural disci-pline and consistency are key concepts in anyvaluation-measurement technique. Institutionsshould ensure that internal controls, includingeffective independent review or audit, are inplace to provide integrity to the valuation pro-cess. Institutions’ practices should, therefore,reflect these concepts to ensure the reliability oftheir valuations of derivative loan commitmentsand forward loan-sales commitments.

3071.0.1.1.2 Derivative LoanCommitments

A financial institution should account for deriva-1. The agencies are the Board of Governors of the Federal

Reserve System, the Federal Deposit Insurance Corporation,the National Credit Union Administration, the Office of theComptroller of the Currency, and the Office of Thrift Supervi-sion.

2. The guidance in the interagency advisory is also in-tended to apply to financial-statement reporting by bank hold-ing companies.

3. Staff accounting bulletins (SABs) summarize the viewsof the SEC’s staff regarding the application of generallyaccepted accounting principles.

BHC Supervision Manual January 2006Page 1

tive loan commitments at fair value on the bal-ance sheet, regardless of the manner in whichthe intended sale of the mortgage loans will beexecuted (e.g., under a best-efforts contract, amandatory-delivery contract, or the institution’sown securitization). An institution should reporteach fixed, adjustable, and floating derivativeloan commitment as an ‘‘ other asset’’ or an‘‘ other liability’’ in their regulatory reports basedupon whether the individual commitment has apositive (asset) or negative (liability) fair value.4

With respect to floating derivative loan com-mitments, because the interest rate on such acommitment ‘‘fl oats’’ on a daily basis with mar-ket interest rates, the fair value of a floatingderivative loan commitment approximates zeroas long as the creditworthiness of the borrowerhas not changed. However, as with other deriva-tive loan commitments, an institution must reportthe entire gross notional amount of floatingderivative loan commitments in its regulatoryreports.

Commitments to originate mortgage loansthat will be held for investment purposes andcommitments to originate other types of loansare not within the scope of FAS 133 and, there-fore, are not accounted for as derivatives.5 Aninstitution should report the unused portion ofthese types of commitments, which are not con-sidered derivatives, as ‘‘ unused commitments’’in its regulatory reports.

3071.0.1.1.3 Forward Loan-SalesCommitments

A financial institution should account for for-ward loan-sales commitments for mortgage loansas derivatives at fair value on the balance sheet.Each forward loan-sales commitment should bereported as an ‘‘ other asset’’ or an ‘‘ other liabil-ity’’ based upon whether the individual commit-ment has a positive (asset) or negative (liability)fair value.6

3071.0.1.1.4 Netting of Contracts

For balance-sheet-presentation purposes, FAS133 does not provide specific guidance onfinancial-statement presentation.7 A financialinstitution may not offset derivatives with nega-tive fair values (liabilities) against those withpositive fair values (assets), unless the criteriafor ‘‘ netting’’ under GAAP have been satis-fied.8 In addition, an institution may not offsetthe fair value of forward loan-sales commit-ments against the fair value of derivative loancommitments (the pipeline) or mortgage loansheld for sale (warehouse loans). Rather, forwardloan-sales commitments must be accounted forseparately at fair value, and warehouse loansmust be accounted for at the lower of cost or fairvalue (commonly referred to as ‘‘ LOCOM’’ )9

with certain adjustments to the cost basis of theloans if hedge accounting is applied.

3071.0.1.1.5 Hedge Accounting

A financial institution should follow the guid-ance in FAS 133 when applying hedge account-ing to its mortgage banking activities. If theFAS 133 qualifying criteria are met, an institu-tion may apply—

• fair-value hedge accounting in a hedgingrelationship between forward loan-sales com-mitments (the hedging instrument) and fixed-rate warehouse loans (the hedged item), or

• cash-flow hedge accounting in a hedgingrelationship between forward loan-sales com-

4. When preparing Reports of Condition and Income (CallReports) and the Consolidated Financial Statements for BankHolding Companies (BHC reports), fixed, adjustable, andfloating derivative loan commitments should not be reportedas unused commitments in Schedule RC-L, Derivatives andOff-Balance Sheet Items (Schedule HC-1 for bank holdingcompanies), because such commitments are to be reported asderivatives in this schedule.

5. See FAS 133, paragraph 10(i).6. Regardless of whether the underlying mortgage loans

will be held for investment or for resale, commitments topurchase mortgage loans from third parties under either

mandatory-delivery contracts or best-efforts contracts arederivatives if, upon evaluation, the contracts meet the defini-tion of a derivative under FAS 133. An institution shouldreport its loan-purchase commitments that meet the definitionof a derivative at fair value on the balance sheet.

7. That is, FAS 133 does not provide specific guidancewhere, in the financial statements, the fair value of derivativesor the changes in the fair value of derivatives should beclassified and presented on the financial statement.

8. When an institution has two (or more) derivatives withthe same counterparty, contracts with positive fair values andnegative fair values may be netted if the conditions set forth inFASB Interpretation No. 39, ‘‘ Offsetting of Amounts Relatedto Certain Contracts’’ (FIN 39), are met. Those conditions areas follows: (1) each of the parties owes the other determinableamounts; (2) the reporting party has the right to set off theamount owed with the amount owed by the other party;(3) the reporting party intends to set off; and (4) the right ofsetoff is enforceable at law. In addition, without regard to thethird condition, fair-value amounts recognized for derivativecontracts executed with the same counterparty under a masternetting arrangement may be offset.

9. See Statement of Financial Accounting Standards No.65, ‘‘Accounting for Certain Mortgage Banking Activities’’(FAS 65), paragraph 4.

Mortgage Banking—Derivative Commitments to Originate and Sell Mortgage Loans 3071.0

BHC Supervision Manual January 2006Page 2

mitments (the hedging instrument) and theforecasted sale of the warehouse loans and/orthe loans to be originated under derivativeloan commitments (the forecastedtransaction).10

If a financial institution does not apply hedgeaccounting, either because the FAS 133 hedgecriteria are not met or the institution chooses notto apply hedge accounting, forward loan-salescommitments should be treated as nonhedgingderivatives. If hedge accounting is not applied,an institution will account for its warehouseloans at the lower of cost or fair value. Becausenonhedging forward loan-sales commitmentsare accounted for at fair value through earnings,such an approach causes volatility in reportedearnings if the fair value of the warehouse loansincreases above their cost basis. In this situa-tion, the volatility is a result of recognizing thefull amount of any decline in the fair value ofthe forward loan-sales commitments in earningswhile not adjusting the carrying amount of thewarehouse loans above their cost basis.

3071.0.1.1.6 Income-Statement Effect

Unless cash-flow hedge accounting is applied, afinancial institution should include the periodicchanges in the fair value of derivative loancommitments and forward loan-sales commit-ments in current-period earnings. An institutionshould report these changes in fair value ineither ‘‘ other non-interest income’’ or ‘‘ othernon-interest expense,’’ but not as trading rev-enue, in their regulatory reports. However, aninstitution’s decision as to whether to report thechanges in fair value in its regulatory reports inan income or expense line item should be con-sistent with its presentation of these changes inits general-purpose external financial statements(including audited financial statements)11 andshould be consistent from period to period.

3071.0.1.2 Valuation

3071.0.1.2.1 Fair Value

FAS 133 indicates that the guidance in State-ment of Financial Accounting Standards No.107, ‘‘ Disclosures About Fair Value of Finan-cial Instruments’’ (FAS 107), should be fol-

lowed in determining the fair value of deriva-tives.12 That guidance provides that quoted marketprices are the best evidence of the fair value offinancial instruments. However, when quotedmarket prices are not available, which is typi-cally the case for derivative loan commitmentsand forward loan-sales commitments, estimatesof fair value should be based on the best infor-mation available in the circumstances (e.g., valu-ation techniques based on estimated expectedfuture cash flows). When expected future cashflows are used, they should be the institution’sbest estimate based on reasonable and support-able assumptions and projections.

Estimates of fair value should consider pricesfor similar assets or similar liabilities and theresults of valuation techniques to the extentavailable in the circumstances. In the absence of(1) quoted market prices in an active market,(2) observable prices of other current markettransactions, or (3) other observable data sup-porting a valuation technique, the transactionprice represents the best information availablewith which to estimate fair value at the incep-tion of an arrangement.

A financial institution should not recognizean unrealized gain or loss at inception of aderivative instrument unless the fair value ofthat instrument is obtained from a quoted mar-ket price in an active market or is otherwiseevidenced by comparison to other observablecurrent market transactions or based on a valua-tion technique incorporating observable marketdata.13 Based on this guidance, derivative loancommitments generally would have a zero fairvalue at inception.14 However, subsequentchanges in the fair value of a derivative loancommitment must be recognized in financialstatements and regulatory reports (e.g., changesin fair value attributable to changes in marketinterest rates).

When estimating the fair value of derivativeloan commitments and those best-efforts con-tracts that meet the definition of a derivative, a

10. See FAS 133, paragraphs 20–21, and related FAS 133guidance for hedging instruments, hedged items, and fore-casted transactions that qualify for fair-value and cash-flowhedge accounting.

11. See footnote 7.

12. See FAS 133, paragraph 17.13. See footnote 3 in Emerging Issues Task Force Issue

No. 02-3 (EITF 02-3), ‘‘ Issues Involved in Accounting forDerivative Contracts Held for Trading Purposes and ContractsInvolved in Energy Trading and Risk Management Activi-ties.’’

14. If a potential borrower pays the lender a fee uponentering into a derivative loan commitment (e.g., a rate-lockfee), there is a transaction price, and the lender should recog-nize the derivative loan commitment as a liability at inceptionusing an amount equal to the fee charged to the potentialborrower.

Mortgage Banking—Derivative Commitments to Originate and Sell Mortgage Loans 3071.0

BHC Supervision Manual January 2006Page 3

financial institution should consider predicted‘‘ pull-through’’ (or, conversely, ‘‘ fallout’’ ) rates.A pull-through rate is the probability that aderivative loan commitment will ultimately resultin an originated loan. Some factors that may beconsidered in arriving at appropriate pull-through rates include (but are not limited to) theorigination channel (which may be either inter-nal [retail] or external [wholesale or correspon-dent, to the extent the institution rather than thecorrespondent closes the loan]),15 current mort-gage interest rates in the market versus theinterest rate incorporated in the derivative loancommitment, the purpose of the mortgage (pur-chase versus refinancing), the stage of comple-tion of the underlying application and under-writing process, and the time remaining until theexpiration of the derivative loan commitment.Estimates of pull-through rates should be basedon historical information for each type of loanproduct adjusted for potential changes in marketinterest rates that may affect the percentage ofloans that will close. An institution should notconsider the pull-through rate when reportingthe notional amount of derivative loan commit-ments in regulatory reports but, rather, mustreport the entire gross notional amount.

3071.0.1.2.2 SAB 105

In March 2004, the SEC issued SAB 105 toprovide guidance on the proper accounting anddisclosures for derivative loan commitments.SAB 105 is effective for derivative loan com-mitments entered into after March 31, 2004.SAB 105 indicates that the expected future cashflows related to the associated servicing of loansshould not be considered in recognizing deriva-tive loan commitments. Incorporating expectedfuture cash flows related to the associated ser-vicing of the loan essentially results in theimmediate recognition of a servicing asset. Ser-vicing assets should only be recognized whenthe servicing asset has been contractually sepa-rated from the underlying loan by sale or securi-tization of the loan with servicing retained.16

Further, no other internally developed intangibleassets (such as customer-relationship intangibleassets) should be recognized as part of deriva-tive loan commitments. Recognition of suchassets would only be appropriate in a third-partytransaction (for example, the purchase of aderivative loan commitment either individually,in a portfolio, or in a business combination).

3071.0.1.3 Standard-Setter Activities

Financial institutions should be aware that theSEC or the Financial Accounting StandardsBoard (FASB) may issue additional fair-value,measurement, or recognition guidance in thefuture (e.g., a fair-value measurement state-ment). To the extent that additional guidance isissued, institutions must also consider the guid-ance in developing fair-value-estimate method-ologies for derivative loan commitments andforward loan-sales commitments as well as mea-suring and recognizing such derivatives.

3071.0.1.4 Changes in Accounting forDerivative Loan Commitments andLoan-Sales Agreements

Financial institutions should follow AccountingPrinciples Board Opinion No. 20 (APB 20),‘‘Accounting Changes,’’ 17 if a change in theiraccounting for derivative loan commitments,best-efforts contracts, or mandatory-delivery con-tracts is necessary. APB 20 defines various typesof accounting changes and addresses the report-ing of corrections of errors in previously issuedfinancial statements. APB 20 states, ‘‘ Errors infinancial statements result from mathematicalmistakes, mistakes in the application of account-ing principles, or oversight or misuse of factsthat existed at the time the financial statementswere prepared.’’

For regulatory reporting purposes, a financialinstitution must determine whether the reasonfor a change in its accounting meets the APB 20definition of an accounting error. If the reasonfor the change meets this definition, the errorshould be reported as a prior-period adjustmentif the amount is material. Otherwise, the effectof the correction of the error should be reportedin current earnings.

If the effect of the correction of the error is

15. If an institution commits to purchase a loan that will beclosed by a correspondent in the correspondent’s name, theinstitution would have a loan-purchase commitment ratherthan a derivative loan commitment. See footnote 6.

16. See Statement of Financial Accounting Standards No.140 (FAS 140), ‘‘Accounting for Transfers and Servicing ofFinancial Assets and Extinguishments of Liabilities,’’ para-graph 61.

17. Effective December 15, 2005, APB 20 will be replacedby FASB Statement No. 154, ‘‘Accounting Changes and ErrorCorrections—A Replacement of APB Opinion No. 20 andFASB Statement No. 3.’’

Mortgage Banking—Derivative Commitments to Originate and Sell Mortgage Loans 3071.0

BHC Supervision Manual January 2006Page 4

material, a financial institution should also con-sult with its primary federal regulatory agencyto determine whether any of its prior regulatoryreports should be amended. If amended regula-tory reports are not required, the institutionshould report the effect of the correction of theerror on prior years’ earnings, net of applicabletaxes, as an adjustment to the previously reportedbeginning balance of equity capital. For the CallReport, the institution should report the amountof the adjustment in Schedule RI-A, item 2,‘‘ Restatements due to corrections of materialaccounting errors and changes in accountingprinciples,’’ with an explanation in ScheduleRI-E, item 4.

The effect of the correction of the error onincome and expenses since the beginning of theyear in which the error is corrected should bereflected in each affected income and expenseaccount on a year-to-date basis beginning in thenext quarterly income statement (Call Report) tobe filed and not as a direct adjustment to retainedearnings.

3071.0.1.5 Definitions of Terms Used inthe Advisory

3071.0.1.5.1 Derivative LoanCommitment

The term derivative loan commitment refers to alender’s commitment to originate a mortgageloan that will be held for resale. Notwithstand-ing the characteristics of a derivative set forth inFAS 133, these commitments to originate mort-gage loans must be accounted for as derivativesby the issuer under FAS 133 and include, butare not limited to, those commonly referred toas interest-rate-lock commitments.

In a derivative loan commitment, the lenderagrees to extend credit to a borrower undercertain specified terms and conditions in whichthe interest rate and the maximum amount of theloan18 are set prior to or at funding. Under theagreement, the lender commits to lend funds toa potential borrower (subject to the lender’sapproval of the loan) on a fixed- or adjustable-rate basis, regardless of whether interest rateschange in the market, or on a floating-rate basis.In a typical derivative loan commitment, theborrower can choose to—

• ‘‘ lock in’’ the current market rate for a fixed-rate loan (i.e., a fixed derivative loancommitment),

• ‘‘ lock in’’ the current market rate for anadjustable-rate loan that has a specified for-mula for determining when and how the inter-est rate will adjust (i.e., an adjustable deriva-tive loan commitment), or

• wait until a future date to set the interest rateand allow the interest rate to ‘‘fl oat’’ withmarket interest rates until the rate is set (i.e., afloating derivative loan commitment).

Derivative loan commitments vary in term andexpire after a specified time period (e.g., 60days after the commitment date). Additionally,derivative loan commitments generally do notbind the potential borrower to obtain the loan,nor do they guarantee that the lender will approvethe loan once the creditworthiness of the poten-tial borrower has been determined.

3071.0.1.5.2 Forward Loan-SalesCommitment

The term forward loan-sales commitment refersto either (1) a mandatory-delivery contract or(2) a best-efforts contract that, upon evaluationunder FAS 133, meets the definition of aderivative.

3071.0.1.5.3 Mandatory-DeliveryContract

A mandatory-delivery contract is a loan-salesagreement in which a financial institution com-mits to deliver a certain principal amount ofmortgage loans to an investor at a specifiedprice on or before a specified date. If the institu-tion fails to deliver the amount of mortgagesnecessary to fulfill the commitment by the speci-fied date, it is obligated to pay a ‘‘ pair-off’’ fee,based on then-current market prices, to theinvestor to compensate the investor for the short-fall. Variance from the originally committedprincipal amount is usually permitted, but typi-cally may not exceed 10 percent of the commit-ted amount.

All loan-sales agreements must be evaluatedto determine whether they meet the definition ofa derivative under FAS 133.19 A mandatory-

18. In accordance with the ‘‘ Background Information andBasis for Conclusions’’ in Statement of Financial AccountingStandards No. 149 (FAS 149), the notional amount of aderivative loan commitment is the maximum amount of theborrowing. See FAS 149, paragraph A27.

19. See FAS 133, paragraph 6, for the characteristics of afinancial instrument or other contract that meets the definitionof a derivative.

Mortgage Banking—Derivative Commitments to Originate and Sell Mortgage Loans 3071.0

BHC Supervision Manual January 2006Page 5

delivery contract has a specified underlying (thecontractually specified price for the loans) andnotional amount (the committed loan-principalamount), and requires little or no initial netinvestment. Additionally, a mandatory-deliverycontract requires or permits net settlement or theequivalent thereof as the institution is obligatedunder the contract to either deliver mortgageloans or pay a pair-off fee (based on the then-current market prices) on any shortfall on thedelivery of the committed loan-principal amount.Since the option to pay a pair-off fee accom-plishes net settlement, it is irrelevant as towhether the mortgage loans to be delivered areconsidered readily convertible to cash.20 Basedon these characteristics, a mandatory-deliverycontract meets the definition of a derivative atthe time an institution enters into the commitment.

3071.0.1.5.4 Best-Efforts Contract

The term best-efforts contract refers to a loan-sales agreement in which a financial institutioncommits to deliver an individual mortgage loanof a specified principal amount and quality to aninvestor if the loan to the underlying borrowercloses. Generally, the price the investor will paythe seller for an individual loan is specified priorto the loan being funded (e.g., on the same daythe lender commits to lend funds to a potentialborrower). A best-efforts contract that has all ofthe following characteristics would meet thedefinition of a derivative:

• an underlying (e.g., the price the investor willpay the seller for an individual loan is speci-fied in the contract)

• a notional amount (e.g., the contract specifiesthe principal amount of the loan as an exactdollar amount or as a principal range with adeterminable maximum amount)21

• requires little or no initial net investment (e.g.,no fees are exchanged between the seller andinvestor upon entering into the agreement, ora fee that is similar to a premium on otheroption-type contracts is exchanged)

• requires or permits net settlement or the equiva-

lent thereof (for example, the seller is contrac-tually obligated to either (1) deliver the loanto the investor if the loan closes or (2) pay apair-off fee, based on then-current marketprices, to the investor to compensate the in-vestor if the loan closes and is not delivered.Since the option to pay a pair-off fee accom-plishes net settlement, it is irrelevant as towhether the loan to be delivered is consideredreadily convertible to cash.).

3071.0.1.5.5 Master Agreement

A financial institution may enter into one ofseveral types of arrangements with an investorto govern the relationship between the institu-tion and the investor and set the parametersunder which the institution will deliver indi-vidual mortgage loans through separate best-efforts contracts. Such an arrangement mightinclude, for example, a master agreement or anumbrella contract. These arrangements mayspecify an overall maximum principal amountof mortgage loans that the institution may deliverto the investor during a specified time period,but generally they do not specify the price theinvestor will pay for individual loans. Further,while these arrangements may include pair-off-fee provisions for loans to be sold under indi-vidual best-efforts contracts covered by thearrangements, the seller is neither contractuallyobligated to deliver the amount of mortgagesnecessary to fulfill the maximum principal amountspecified in the arrangement nor required to paya pair-off fee on any shortfall. Because thesearrangements generally either do not have aspecified underlying or determinable notionalamount or do not require or permit net settle-ment or the equivalent thereof, the arrangementstypically do not meet the definition of a deriva-tive. As discussed above, an individual best-efforts contract governed by one of thesearrangements may, however, meet the definitionof a derivative.

As the terms of individual best-efforts con-tracts and master agreements or umbrella con-tracts vary, a financial institution must carefullyevaluate such contracts to determine whetherthe contracts meet the definition of a derivativein FAS 133.

20. See FAS 133, paragraph 57(c)(1), for a description ofcontracts that have terms that implicitly or explicitly requireor permit net settlement.

21. The use of a maximum amount as the notional amountof a best-efforts contract is consistent with the loan-commitment discussion in the ‘‘ Background Information andBasis for Conclusions’’ in FAS 149. See FAS 149, paragraphA27.

Mortgage Banking—Derivative Commitments to Originate and Sell Mortgage Loans 3071.0

BHC Supervision Manual January 2006Page 6

3071.0.1.6 Example of the Accountingfor Commitments to Originate and SellMortgage Loans22

3071.0.1.6.1 ABC Mortgage FinancialInstitution (Best-Efforts Contracts and NoApplication of Fair-Value HedgeAccounting)

The following simplified example was devel-oped to provide a financial institution that has alimited number of derivative loan commitmentsgeneral guidance on one approach that may beused to value such commitments.23 This exam-ple also illustrates the regulatory reportingrequirements for derivative loan commitmentsand forward loan-sales commitments.

The guidance in this example is for illustra-tive purposes only, as there are several ways thata financial institution might estimate the fairvalue of its derivative loan commitments. Asecond approach to valuing derivative loan com-mitments is described in Derivative Loan Com-mitments Task Force Illustrative Disclosures onDerivative Loan Commitments, a practice aiddeveloped by staff of the American Institute ofCertified Public Accountants (AICPA) and atask force comprising representatives from thefinancial services, mortgage banking, and publicaccounting communities.24 As indicated in thebody of the interagency advisory, a financialinstitution must consider the guidance in FAS133, FAS 107, EITF 02-3, and SAB 105 inmeasuring and recognizing derivative loan com-mitments and forward loan-sales commitments.In addition, an institution should be aware thatthe SEC or FASB may issue additional guidancein the future that may alter certain aspects ofthis example.

3071.0.1.6.1.1 Background

ABC Mortgage Financial Institution (ABC) en-ters into fixed, adjustable, and floating deriva-

tive loan commitments to originate mortgageloans that it intends to sell. The institutionaccounts for the commitments as derivativefinancial instruments as required under FAS133.

ABC enters into best-efforts contracts with amortgage investor under which it commits todeliver certain loans that it expects to originateunder derivative loan commitments (i.e., thepipeline) and loans that it has already originatedand currently holds for sale (i.e., warehouseloans). ABC and the mortgage investor agree onthe price that the investor will pay ABC for anindividual loan with a specified principal amountprior to the loan being funded. Once the pricethat the mortgage investor will pay ABC for anindividual loan and the notional amount of theloan are specified, and ABC is obligated todeliver the loan to the investor if the loan closes,the contract represents a forward loan-sales com-mitment. Under FAS 133, ABC accounts forthese forward loan-sales commitments asderivative financial instruments.

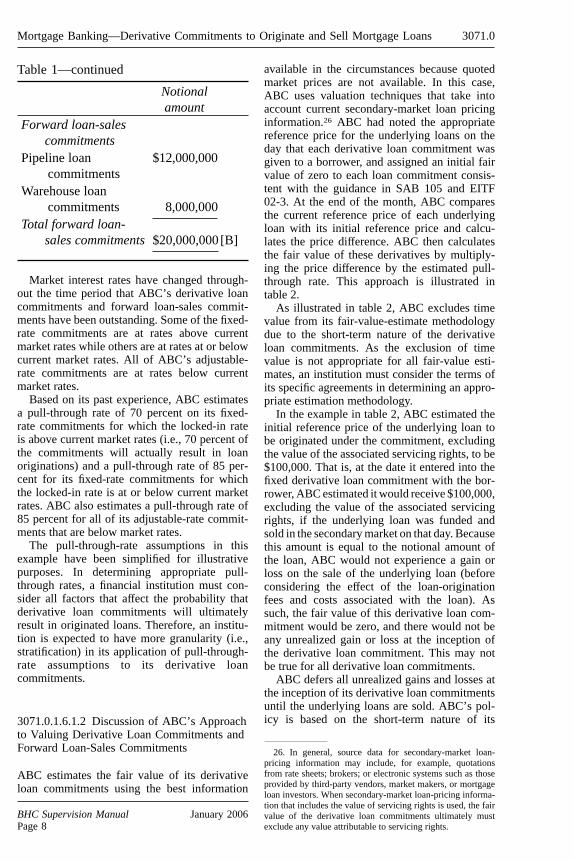

On December 31 of a given year, the notionalamounts of ABC’s mortgage banking derivativeloan commitments and forward loan-sales com-mitments are as follows:

Table 1—Notional Amounts of DerivativeLoan Commitments and ForwardLoan-Sales Commitments

Notionalamount

Derivative loancommitments

Fixed-ratecommitments

$ 8,500,000

Adjustable-ratecommitments 1,500,000

Floating-ratecommitments

2,000,000

Total derivative loancommitments $12,000,000 [A]2522. This example uses the definitions and concepts pre-

sented in the body of the Interagency Advisory on Accountingand Reporting for Commitments to Originate and Sell Mort-gage Loans (the interagency advisory). Refer to the inter-agency advisory for clarification of the terms and conceptsused in this example.

23. Estimating fair values when quoted market prices areunavailable requires considerable judgment. Valuation tech-niques using simplified assumptions may sometimes be used(with appropriate disclosure in the financial statements) toprovide a reliable estimate of fair value at a reasonable cost.See FAS 107, paragraphs 60–61.

24. The practice aid is available at www.aicpa.org/download/members/div/acctstd/Illustrative_Disclosure_on_Derivative_Loan_Commitments.pdf.

25. Alpha references in table 1 and the text of this examplerefer to the ‘‘ Reference’’ column in table 3.

Mortgage Banking—Derivative Commitments to Originate and Sell Mortgage Loans 3071.0

BHC Supervision Manual January 2006Page 7

Table 1—continued

Notionalamount

Forward loan-salescommitments

Pipeline loancommitments

$12,000,000

Warehouse loancommitments 8,000,000

Total forward loan-sales commitments $20,000,000 [B]

Market interest rates have changed through-out the time period that ABC’s derivative loancommitments and forward loan-sales commit-ments have been outstanding. Some of the fixed-rate commitments are at rates above currentmarket rates while others are at rates at or belowcurrent market rates. All of ABC’s adjustable-rate commitments are at rates below currentmarket rates.

Based on its past experience, ABC estimatesa pull-through rate of 70 percent on its fixed-rate commitments for which the locked-in rateis above current market rates (i.e., 70 percent ofthe commitments will actually result in loanoriginations) and a pull-through rate of 85 per-cent for its fixed-rate commitments for whichthe locked-in rate is at or below current marketrates. ABC also estimates a pull-through rate of85 percent for all of its adjustable-rate commit-ments that are below market rates.

The pull-through-rate assumptions in thisexample have been simplified for illustrativepurposes. In determining appropriate pull-through rates, a financial institution must con-sider all factors that affect the probability thatderivative loan commitments will ultimatelyresult in originated loans. Therefore, an institu-tion is expected to have more granularity (i.e.,stratification) in its application of pull-through-rate assumptions to its derivative loancommitments.

ABC estimates the fair value of its derivativeloan commitments using the best information

available in the circumstances because quotedmarket prices are not available. In this case,ABC uses valuation techniques that take intoaccount current secondary-market loan pricinginformation.26 ABC had noted the appropriatereference price for the underlying loans on theday that each derivative loan commitment wasgiven to a borrower, and assigned an initial fairvalue of zero to each loan commitment consis-tent with the guidance in SAB 105 and EITF02-3. At the end of the month, ABC comparesthe current reference price of each underlyingloan with its initial reference price and calcu-lates the price difference. ABC then calculatesthe fair value of these derivatives by multiply-ing the price difference by the estimated pull-through rate. This approach is illustrated intable 2.

As illustrated in table 2, ABC excludes timevalue from its fair-value-estimate methodologydue to the short-term nature of the derivativeloan commitments. As the exclusion of timevalue is not appropriate for all fair-value esti-mates, an institution must consider the terms ofits specific agreements in determining an appro-priate estimation methodology.

In the example in table 2, ABC estimated theinitial reference price of the underlying loan tobe originated under the commitment, excludingthe value of the associated servicing rights, to be$100,000. That is, at the date it entered into thefixed derivative loan commitment with the bor-rower, ABC estimated it would receive $100,000,excluding the value of the associated servicingrights, if the underlying loan was funded andsold in the secondary market on that day. Becausethis amount is equal to the notional amount ofthe loan, ABC would not experience a gain orloss on the sale of the underlying loan (beforeconsidering the effect of the loan-originationfees and costs associated with the loan). Assuch, the fair value of this derivative loan com-mitment would be zero, and there would not beany unrealized gain or loss at the inception ofthe derivative loan commitment. This may notbe true for all derivative loan commitments.

ABC defers all unrealized gains and losses atthe inception of its derivative loan commitmentsuntil the underlying loans are sold. ABC’s pol-icy is based on the short-term nature of its

26. In general, source data for secondary-market loan-pricing information may include, for example, quotationsfrom rate sheets; brokers; or electronic systems such as thoseprovided by third-party vendors, market makers, or mortgageloan investors. When secondary-market loan-pricing informa-tion that includes the value of servicing rights is used, the fairvalue of the derivative loan commitments ultimately mustexclude any value attributable to servicing rights.

Mortgage Banking—Derivative Commitments to Originate and Sell Mortgage Loans 3071.0

BHC Supervision Manual January 2006Page 8

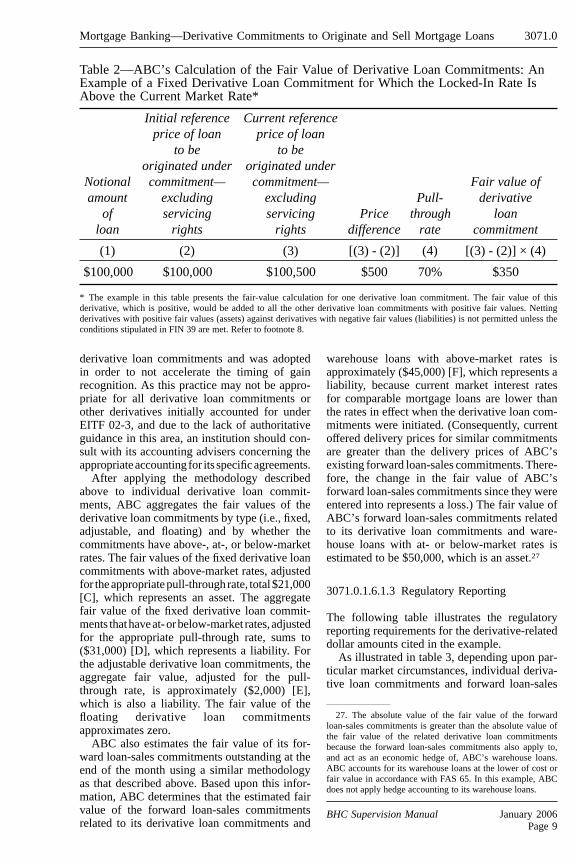

Table 2—ABC’s Calculation of the Fair Value of Derivative Loan Commitments: AnExample of a Fixed Derivative Loan Commitment for Which the Locked-In Rate IsAbove the Current Market Rate*

Notionalamount

ofloan

Initial referenceprice of loan

to beoriginated undercommitment—

excludingservicing

rights

Current referenceprice of loan

to beoriginated undercommitment—

excludingservicing

rightsPrice

difference

Pull-through

rate

Fair value ofderivative

loancommitment

(1) (2) (3) [(3) - (2)] (4) [(3) - (2)] × (4)

$100,000 $100,000 $100,500 $500 70% $350

* The example in this table presents the fair-value calculation for one derivative loan commitment. The fair value of thisderivative, which is positive, would be added to all the other derivative loan commitments with positive fair values. Nettingderivatives with positive fair values (assets) against derivatives with negative fair values (liabilities) is not permitted unless theconditions stipulated in FIN 39 are met. Refer to footnote 8.

derivative loan commitments and was adoptedin order to not accelerate the timing of gainrecognition. As this practice may not be appro-priate for all derivative loan commitments orother derivatives initially accounted for underEITF 02-3, and due to the lack of authoritativeguidance in this area, an institution should con-sult with its accounting advisers concerning theappropriateaccounting for its specificagreements.

After applying the methodology describedabove to individual derivative loan commit-ments, ABC aggregates the fair values of thederivative loan commitments by type (i.e., fixed,adjustable, and floating) and by whether thecommitments have above-, at-, or below-marketrates. The fair values of the fixed derivative loancommitments with above-market rates, adjustedfor the appropriate pull-through rate, total $21,000[C], which represents an asset. The aggregatefair value of the fixed derivative loan commit-ments thathaveat-orbelow-market rates, adjustedfor the appropriate pull-through rate, sums to($31,000) [D], which represents a liability. Forthe adjustable derivative loan commitments, theaggregate fair value, adjusted for the pull-through rate, is approximately ($2,000) [E],which is also a liability. The fair value of thefloating derivative loan commitmentsapproximates zero.

ABC also estimates the fair value of its for-ward loan-sales commitments outstanding at theend of the month using a similar methodologyas that described above. Based upon this infor-mation, ABC determines that the estimated fairvalue of the forward loan-sales commitmentsrelated to its derivative loan commitments and

warehouse loans with above-market rates isapproximately ($45,000) [F], which represents aliability, because current market interest ratesfor comparable mortgage loans are lower thanthe rates in effect when the derivative loan com-mitments were initiated. (Consequently, currentoffered delivery prices for similar commitmentsare greater than the delivery prices of ABC’sexisting forward loan-sales commitments. There-fore, the change in the fair value of ABC’sforward loan-sales commitments since they wereentered into represents a loss.) The fair value ofABC’s forward loan-sales commitments relatedto its derivative loan commitments and ware-house loans with at- or below-market rates isestimated to be $50,000, which is an asset.27

3071.0.1.6.1.3 Regulatory Reporting

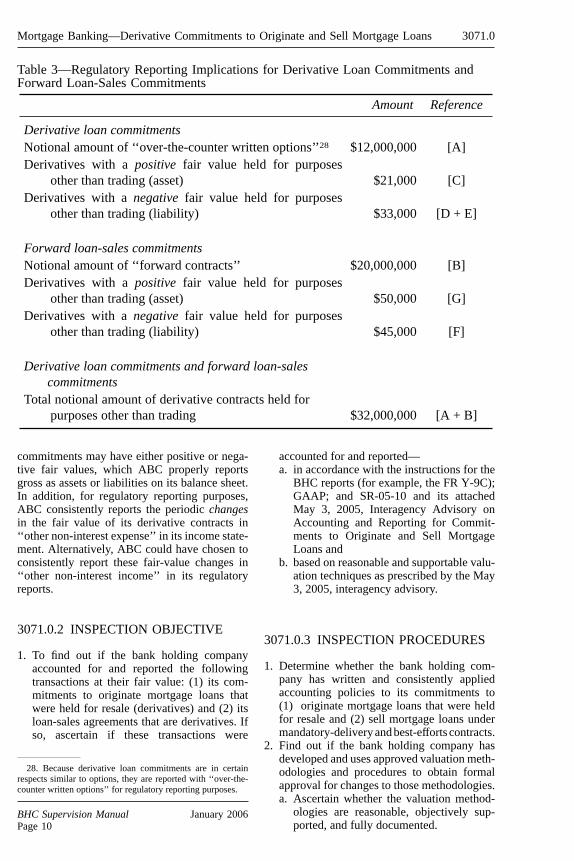

The following table illustrates the regulatoryreporting requirements for the derivative-relateddollar amounts cited in the example.

As illustrated in table 3, depending upon par-ticular market circumstances, individual deriva-tive loan commitments and forward loan-sales

27. The absolute value of the fair value of the forwardloan-sales commitments is greater than the absolute value ofthe fair value of the related derivative loan commitmentsbecause the forward loan-sales commitments also apply to,and act as an economic hedge of, ABC’s warehouse loans.ABC accounts for its warehouse loans at the lower of cost orfair value in accordance with FAS 65. In this example, ABCdoes not apply hedge accounting to its warehouse loans.

Mortgage Banking—Derivative Commitments to Originate and Sell Mortgage Loans 3071.0

Derivative loan commitmentsNotional amount of ‘‘ over-the-counter written options’’ 28 $12,000,000 [A]Derivatives with a positive fair value held for purposes

other than trading (asset) $21,000 [C]Derivatives with a negative fair value held for purposes

other than trading (liability) $33,000 [D + E]

Forward loan-sales commitmentsNotional amount of ‘‘ forward contracts’’ $20,000,000 [B]Derivatives with a positive fair value held for purposes

other than trading (asset) $50,000 [G]Derivatives with a negative fair value held for purposes

other than trading (liability) $45,000 [F]

Derivative loan commitments and forward loan-salescommitments

Total notional amount of derivative contracts held forpurposes other than trading $32,000,000 [A + B]

commitments may have either positive or nega-tive fair values, which ABC properly reportsgross as assets or liabilities on its balance sheet.In addition, for regulatory reporting purposes,ABC consistently reports the periodic changesin the fair value of its derivative contracts in‘‘ other non-interest expense’’ in its income state-ment. Alternatively, ABC could have chosen toconsistently report these fair-value changes in‘‘ other non-interest income’’ in its regulatoryreports.

3071.0.2 INSPECTION OBJECTIVE

1. To find out if the bank holding companyaccounted for and reported the followingtransactions at their fair value: (1) its com-mitments to originate mortgage loans thatwere held for resale (derivatives) and (2) itsloan-sales agreements that are derivatives. Ifso, ascertain if these transactions were

accounted for and reported—a. in accordance with the instructions for the

BHC reports (for example, the FR Y-9C);GAAP; and SR-05-10 and its attachedMay 3, 2005, Interagency Advisory onAccounting and Reporting for Commit-ments to Originate and Sell MortgageLoans and

b. based on reasonable and supportable valu-ation techniques as prescribed by the May3, 2005, interagency advisory.

3071.0.3 INSPECTION PROCEDURES

1. Determine whether the bank holding com-pany has written and consistently appliedaccounting policies to its commitments to(1) originate mortgage loans that were heldfor resale and (2) sell mortgage loans undermandatory-delivery and best-efforts contracts.

2. Find out if the bank holding company hasdeveloped and uses approved valuation meth-odologies and procedures to obtain formalapproval for changes to those methodologies.a. Ascertain whether the valuation method-

ologies are reasonable, objectively sup-ported, and fully documented.

28. Because derivative loan commitments are in certainrespects similar to options, they are reported with ‘‘ over-the-counter written options’’ for regulatory reporting purposes.

Mortgage Banking—Derivative Commitments to Originate and Sell Mortgage Loans 3071.0

BHC Supervision Manual January 2006Page 10

b. Determine if the bank holding companyhas internal controls, including an effec-tive independent review or audit, in placethat give integrity to the valuation process.

3. If the bank holding company issues fixed-,adjustable-, and floating-rate derivative loancommitments or forward loan-sales commit-ments, review an adequate sample that evi-dences the full coverage of these types oftransactions.a. Ascertain if these transactions were prop-

erly reported on the balance sheet as an‘‘ other asset’’ or an ‘‘ other liability,’’ basedon whether the individual commitmenthas a positive (asset) or negative (liabil-ity) fair value in accordance with theinstructions for the BHC reports.

b. Determine if the floating-rate derivativeloan commitments and other derivativeloan commitments were reported at theirentire gross notional amount in the BHC’sreports (such as the FR Y-9C).

c. Find out if the balance sheet correctlypresents accounts for all such transac-tions, including the netting of contracts,the application of hedge accounting tomortgage banking activities, the valuationof derivatives, and any material or otheraccounting changes for derivative loancommitments and loan-sales agreements.Also determine if the bank holding com-pany complies with the May 3, 2005,Interagency Advisory on Accounting and

Reporting for Commitments to Originateand Sell Mortgage Loans and with GAAP.

d. Ascertain if periodic changes in the fairvalue of derivative loan commitments andforward loan-sales commitments arereported in current-period earnings as either‘‘ other non-interest income or ‘‘ non-interest expense, as appropriate.

4. Report to the central point of contact orexaminer-in-charge any failure by the bankholding company’s management to follow(1) the bank holding company’s accountingand valuation policies for its commitments tooriginate mortgage loans that are held forresale and its commitments to sell mortgageloans, (2) the instructions for the Consoli-dated Financial Statement for Bank HoldingCompanies, (3) the May 3, 2005, interagencyadvisory, or (4) GAAP.

5. When additional inspection scrutiny isneeded—based on the examination’s find-ings; the supervisory concerns discussed insection 3071.0; the February 23, 2003, Inter-agency Advisory on Mortgage Banking (seeSR-03-4 and its attachment); and the May 3,2005, Interagency Advisory on Accountingand Reporting for Commitments to Originateand Sell Mortgage Loans (see SR-05-10 andits attachment)—consider using the compre-hensive mortgage banking examination pro-cedures in the appendix section A.2040.3 ofthe Commercial Bank Examination Manual.

Mortgage Banking—Derivative Commitments to Originate and Sell Mortgage Loans 3071.0

BHC Supervision Manual January 2006Page 11

Section 4(c)(8) of the BHC Act (Activities Related to ExtendingCredit) Section 3072.0

In 1997, the Board amended Regulation Y toinclude ‘‘activities related to extending credit’’in section 225.28(b)(2), which includes the fol-lowing permissible nonbanking activities:

Section No.1. real estate and personal property

appraising 3270.02. arranging commercial real estate

equity financing 3220.03. check-guaranty services 3320.04. collection agency services 3330.05. credit bureau services 3340.06. asset-management, servicing, and

collection activities 3084.07. acquiring debt in default 3104.08. real estate settlement services1 3072.8

1. Real estate settlement services do not include providingtitle insurance as principal, agent, or broker.

BHC Supervision Manual July 2006Page 1

Section 4(c)(8) of the BHC Act Real Estate Settlement ServicesSection 3072.8

In 1997, the Board incorporated real estate ser-vicing into section 225.28(b)(2) as one of theactivities related to extending credit. (See 12C.F.R. 225.28(b)(2)(viii).) Real estate settle-ment services do not include providing titleinsurance as principal, agent, or broker. Previ-ously, the Board had approved the activity byBoard order. In the order, the Board found thatreal estate settlement services consist of—

1. reviewing the status of the title in the titlecommitment, resolving any exceptions to thetitle, and reviewing the purchase agreementto identify any requirements that need to becomplied with;

2. verifying payoffs on existing loans securedby the real estate and verifying the amount ofand then calculating the prorating of specialassessments and taxes on the property;

3. obtaining an updated title insurance commit-ment to the date of closing; preparing therequired checks, deeds, and affidavits; andobtaining any authorization letters needed;

4. establishing a time and place for the closing,conducting the closing, and ensuring that allparties properly execute all appropriate docu-ments and meet all commitments;

5. collecting and disbursing funds for the par-ties, holding funds in escrow pending satis-faction of certain commitments, and prepar-ing the HUD settlement statement, the deedof trust, mortgage notes, the Truth-in-Lending statement, and purchaser’s affida-vits; and

6. recording all of the documents required underlaw. (See 1990 FRB 1058.)

3072.8.1 REAL PROPERTYEXCHANGE TRANSACTIONS UNDERSECTION 1031 OF THE INTERNALREVENUE CODE

A request submitted to the Board on behalf of abank holding company (BHC) requested anadvisory opinion pursuant to section 225.27 ofRegulation Y (12 C.F.R. 225.27). The BHC wasproposing the acquisition of a subsidiary (the1031 exchange subsidiary) that provided ser-vices to customers seeking to make exchangesof real property pursuant to section 1031 of theInternal Revenue Code (1031 exchangetransactions).

Section 1031 of the Internal Revenue Codeprovides a U.S. taxpayer with deferral of gainwhen the taxpayer exchanges his or her property

for another property of a ‘‘like kind.’’ In a‘‘forward’’ 1031 exchange transaction, the tax-payer first sells his or her existing property andlater purchases a replacement property.1 In orderto complete a forward 1031 exchange transac-tion successfully, a taxpayer must satisfy certainconditions in section 1031 of the Internal Rev-enue Code and the U.S. Treasury regulationsthat implement section 1031. For example, in aforward 1031 exchange transaction, at the clos-ing of the sale of the initial property, the pro-ceeds of the sale must be held by an individualor entity otherwise unrelated to the transaction(the qualified intermediary). In addition, the tax-payer engaging in the forward 1031 exchangetransaction may not receive the sale proceedsduring the period in which a replacement prop-erty is identified (up to 45 days) and acquired(up to 180 days). In this request, the BHC wasproposing to acquire a subsidiary that would actas a qualified intermediary in forward 1031exchange transactions involving real property.

The 1031 exchange subsidiary would engagein several activities in order to facilitate forward1031 exchange transactions. First, the subsidi-ary would provide its customer with documentsrelated to theexchange toensure that theexchangequalified as a valid forward 1031 exchangetransaction. Specifically, the subsidiary wouldprovide an exchange agreement, an assignmentagreement, and a notice. The exchange agree-ment is a contract between the customer and thesubsidiary that, among other features, notes therequirements for the successful completion ofthe transaction. The assignment agreement trans-fers from the customer to the subsidiary certainresponsibilities for the sale of the initial prop-erty and the receipt of sales proceeds in order toensure that the customer does not ‘‘construc-tively receive’’ the proceeds of the initial prop-erty sale for tax purposes. These responsibilitiesmay include taking the transitory title to theinitial property and replacement property as theyare transferred from seller to buyer. The noticeinforms the purchaser of the initial property thatthe transaction is part of a forward 1031 exchangetransaction; it helps establish that the mecha-

1. In a ‘‘reverse’’ 1031 exchange transaction, the taxpayerfirst purchases a replacement property and later sells his or herproperty. The proposal did not include the provision of ser-vices to customers seeking to make reverse 1031 exchangetransactions.

BHC Supervision Manual July 2006Page 1

nism for the forward 1031 exchange transactionis in place at the time of the sale.

Second, the 1031 exchange subsidiary wouldinvest the proceeds of the sale of the initialproperty on behalf of the customer until thecustomer acquired the replacement property.The proceeds would be invested at the discre-tion of the subsidiary but would typically bedeposited into deposit accounts at the BHC’ssubsidiary state-chartered commercial bank.2 Thesubsidiary would also transfer the necessaryfunds to the appropriate party to effect the cus-tomer’s purchase of the replacement property. Ifthe customer does not identify a replacementproperty or purchase the replacement propertywithin the required time periods set forth insection 1031 of the Internal Revenue Code orU.S. Treasury regulations implementing section1031, the proceeds of the sale of the initialproperty would be transferred to the customer. Itwas represented that the subsidiary would act ina fiduciary capacity in holding, investing, anddisbursing the customer’s funds and that a state-chartered nondepository trust company wouldbe allowed to engage in the activities of thesubsidiary.

The 1031 exchange subsidiary (1) would notparticipate in negotiating the terms of the real

property sale and purchase transactions that con-stitute the forward 1031 exchange transactionand (2) would not assist the customer in locatinga buyer of the initial property or a seller of thereplacement property. The requestor also assertedthat the proposed services are permissible non-banking activities for BHCs under section225.28(b) of Regulation Y (12 C.F.R. 225.28(b)).

In view of all the facts of the record, Boardstaff opined that the proposed activities of the1031 exchange subsidiary would be permissiblereal estate settlement services under section225.28(b)(2)(viii) of Regulation Y (12 C.F.R.225.28(b)(2)(viii)); would be trust company func-tions under section 225.28(b)(5) of RegulationY (12 C.F.R. 225.28(b)(5)); and would be finan-cial advisory services, including tax-planningand tax-preparation services, under section225.28(b)(6) of Regulation Y (12 C.F.R.225.28(b)(6)).3

The opinion is limited to the activities relat-ing to the 1031 exchange transaction describedin the opinion and in the correspondenceexchanged between the requestor and Boardstaff. See the Board staff’s February 9, 2006,legal interpretation.

2. The BHC’s commercial bank subsidiary also may be alender with respect to real properties involved in the 1031exchange transaction. Any lending relationship between thebank and the customer would depend on the ability of thecustomer and the loan transaction to meet the bank’s standardunderwriting terms and conditions.

3. The Office of the Comptroller of the Currency (OCC)authorized national banks to provide a wide range of servicesto facilitate their customers’ 1031 exchange transactions. SeeOCC Interpretive Letter No. 880 (December 16, 1999) andOCC Corporate Decision No. 2001–30 (October 10, 2001).

Section 4(c)(8) of the BHC Act Real Estate Settlement Services 3072.8

BHC Supervision Manual July 2006Page 2

Section 4(c)(8) of the BHC Act(Education-Financing Activities) Section 3073.0

A bank holding company applied for the Board’sapproval under section 4(c)(8) of the Bank Hold-ing Company Act (BHC Act) and section 225.23of Regulation Y to expand the student-loan-servicing activities of its nonbank subsidiary.The activities would consist of—

1. providing student-loan authorities (the author-ity) with regular reports that include informa-tion in the aggregate and by individual lend-ers concerning the volume of loans beingserviced for the authority and the volume ofloans outstanding;

2. preparing projections for approval by theauthority of student loans to be purchasedand commitments to be issued in the future,based on the volume of loans being servicedandcommitmentsoutstanding,consistentwiththe amount of funds available to the author-ity as the result of its sale of bonds;

3. advising eligible lenders, borrowers, and otherinterested parties of the authority’s student-loan-purchase program, including the criteriaused by the authority in purchasing studentloans and the extent to which the authoritywill be purchasing loans in the future basedon the availability of funds; and

4. meeting regularly with the authority to adviseit of the nonbank subsidiary’s efforts in con-nection with the student-loan activities.

Under no circumstances would the nonbanksubsidiary be authorized to bind the authority orits bank trustee to commit to purchase or actu-

ally to purchase student loans from eligiblelenders.

The proposed activities were regarded as beingequivalent to the activities of a mortgage bank-ing subsidiary of a bank holding company,authorized under section 225.28(b)(1) of Regu-lation Y, with respect to acquiring and servicingmortgage loans for institutional investors or inconnection with the secondary-mortgage mar-ket. The activities proposed and currently con-ducted by the applicant, to the extent that theywere different from the services performed byany institution that services loans for others,were perceived as being different only in thatthey related to servicing student loans for agovernmental authority. Banks and their non-bank subsidiaries generally provide comprehen-sive loan-acquisition and -servicing ‘‘packages’’for investors in mortgage and other loans. Thebank holding company’s nonbank subsidiarywas the nation’s largest servicer of studentloans, and was thus particularly well equippedto perform the proposed expanded services.

In addition to determining that the proposedactivities were closely related to banking toapprove the application, the Board had to con-clude that the proposed activities would producebenefits to the public that would outweigh anypossible adverse effects, such as unsound bank-ing practices, unfair competition, conflicts ofinterests, or undue concentration of resources.The Board made that conclusion in addition todetermining that the balance of public interestfactors that it is required to consider under sec-tion 4(c)(8) of the BHC Act was favorable.Accordingly, the application was approved onJuly 1, 1985 (1985 FRB 725).

BHC Supervision Manual December 1998Page 1

Section 4(c)(8) of the BHC Act(Servicing Loans) Section 3080.0

A bank holding company or its subsidiary mayengage in the activity of servicing loans or otherextensions of credit for either affiliated compa-nies or for persons or institutions not affiliatedwith the holding company. The service willoften be carried on as an additional activity of acredit-extending subsidiary, such as a mortgagecompany, where the loan serviced was origi-nated by the subsidiary and subsequently sold toan investor. A servicing company provides thecollection vehicle through receipt and disburse-ment of funds for investors who may not pos-sess the resources to accomplish the activity.The purpose of servicing is to keep a sound loanin good standing for a passive investor. Theservicing company’s remuneration is usuallybased upon a percentage of the outstanding bal-ance of the loan.The traditional servicing arrangement arises

from the normal business of a mortgage com-pany. The company grants extensions of creditto qualified borrowers and subsequently pack-ages and sells these loans, normally withoutrecourse, to individuals or institutional investorswho contract the collection of the credit to themortgage company. The company may also pur-chase mortgages or other extensions of credit inthe open market with the intention of resellingthe credit and retaining the servicing or cansimply purchase servicing portfolios (12 C.F.R.225.132). The collection itself is basically abookkeeping function.Servicing loans for others is relatively risk-

free to the company when the credits are soldwithout recourse to investors. A credit whichhas been soldwith recourse represents an unusualcircumstance and should, therefore, be reviewedin detail. The serviced loans will generally behigh quality mortgages which are in turn pur-chased from the company by passive investorsdesiring a fixed rate of return on their funds.The risk to a servicing company lies in itsportfolio of unsold loans, or its ‘‘warehouse.’’The risk is two-fold: (1) the loan may not be ofhigh enough quality to attract an investor so thatthe servicing company will have to continue tocarry the credit for its own account, and (2) theloan was made at an interest rate which is belowcurrent market rates. In the latter case, the ser-vicing company must either sell the loan at adiscount or continue to hold the credit for itsown account. In either case, the loan is treatedas an asset of the company and involves creditrisk.The inspection of a servicing company, or a

servicing department of a credit-extending sub-

sidiary, should focus on adequacy of documen-tation and controls, and on the quality and mar-ketability of thewarehoused loans. The examinershould obtain a past due report for the portfolioand note in the inspection report significantcredits which are past due together with theperiod of delinquency, the type of loan, and theasset classification, if any. The nature of theservicing business is such that the number ofpast dues should be small because loans areonly warehoused for a short period of time untilthey can be sold to an investor. As a rule, a pastdue loan or a current loan which has been ware-housed for more than several months is indica-tive of some problem with the credit. Each loanshould be evaluated to determine the reason ithas not been sold.During periods of rising long-term interest

rates, the warehouse portfolio becomes subjectto the risk that a loan may not be marketable,except at a discount, because of its relativelylow yield. This affects both the servicer’s incomeand liquidity.In the case of the parent company acting as a

servicer, the inspection should also determinewhether the activity is being carried on underthe proper exemption. A bank holding companymay act as a servicer under section 4(c)(8) ofthe Act or under the provisions of sections4(a)(2) and/or 4(c)(1) of the Act. If carried onunder Section 4(a)(2) of the BHC Act, the hold-ing company is limited to servicing loans onlyfor its own account or its banking and nonbank-ing subsidiaries. If carried under Section4(c)(1)(C) of the BHC Act, the bank holdingcompany is limited to servicing loans only forits own account or its banking subsidiaries.Finally, the income of the company should be

subject to scrutiny. A servicing company shouldbe a profitable business. The servicer receives afee based upon a percentage of the outstandingbalance of the loan. In the early years of thepayback period, the fee should significantlyexceed the cost of the service, and becausemuch of the portfolio will be refinanced eitherprior to its maturity or prepaid, the fee incomeshould be sufficient to cover the servicer’s costplus profit. The reason for poor earnings in thisactivity is generally either inefficiency in thecollection area, failure to attain the breakevenpoint of servicing volume, or the inability toturnover the warehouse portfolio often enoughto maintain new fee generation. In the event that

BHC Supervision Manual December 1992Page 1

the servicer is unprofitable, the examiner shoulddetermine the reasons and clearly set them forthin the inspection report.The servicing arrangement is of a fiduciary

nature and as such it gives rise to certain contin-gent liabilities. In the situation where the ser-vicer is not fully and properly discharging itsservicing responsibilities in accordance with theservicing agreement, the holder of the servicednotes might bring legal claims against the ser-vicer. The inspection process should directattention to this area including a review of theservicing agreement and verification that theservicer is fulfilling its obligations. Manage-ment should be reminded of the significant lossexposure which can result from improper atten-tion to its fiduciary responsibilities.

3080.0.1 INSPECTION OBJECTIVES

1. To determine that internal controls areadequate to administer effectively the servicingof the loan portfolio.

2. To determine the level of exposure tocredit risk of loans held for the firm’s ownaccount.3. To determine if the firm’s earnings are

sufficient so as not to be a burden on the parentor subsidiary bank.

3080.0.2 INSPECTION PROCEDURES

1. Review the balance sheet to determine thevolume of credits held for the firm’s own accountand evaluate their asset quality.2. Review internal controls and evaluate their

adequacy.3. Review earnings and appraise the impact

on the parent and bank subsidiaries.4. Review servicing agreements and evaluate

the potential or contingent risks to which thefirm is exposed in the event of failure by aborrower to service its loan properly.5. Determine whether mortgage servicing

rights are recorded as an asset and whether theyare being amortized over the average life of theloans being serviced.

Section 4(c)(8) of the BHC Act (Servicing Loans) 3080.0

BHC Supervision Manual December 1992Page 2

Section 4(c)(8) of the BHC Act (Asset-Management,Asset-Servicing, and Collection Activities) Section 3084.0

A bank holding company may engage undercontract with a third party in the management,servicing, and collection1 of the types of assetsthat an insured depository institution may origi-nate and own. The company cannot engage inreal property management or real estate broker-age services as part of these services. See Regu-lationY,section225.28(b)(2)(vi).Providedbeloware some initial historical examples of Boardorders that involve asset-management servicesrelated to this nonbanking activity. The commit-ments and conditions provided for within theBoard orders should not be considered to becurrently applicable.

3084.0.1 ASSET-MANAGEMENTSERVICES TO CERTAINGOVERNMENTAL AGENCIES ANDUNAFFILIATED FINANCIALINSTITUTIONS WITH TROUBLEDASSETS

Three bank holding companies (the applicants)applied for the Board’s approval under section4(c)(8) of the BHC Act to engage de novo inprovidingasset-managementservices to theReso-lution Trust Corporation and the Federal DepositInsurance Corporation, and generally to unaffili-ated financial institutions with troubled assets.The applicants committed to conduct theseactivities under the same terms and conditionsas set out in 1988 FRB 771.

The commitments and conditions of this orderrequired that (1) the asset-management activi-ties would be provided to the banks and savingsassociations, (2) the applicant would obtain theBoard’s approval before providing asset-management services for pools of assets thatwere not originated or held by financial institu-tions and their affiliates, (3) the applicant wouldcause its asset-management subsidiary to estab-lish procedures to preserve the confidentiality ofinformation obtained in the course of providingasset-management services, and (4) neither theapplicant nor its management subsidiary wouldtake title to the assets managed by the asset-management subsidiary.

The applications of these holding companieswere approved by a Board order on Decem-ber 24, 1990 (1991 FRB 124). Two additional

orders about providing asset-management ser-vices were approved on March 25, 1991 (1991FRB 331 and 334).

3084.0.2 ASSET-MANAGEMENTSERVICES FOR ASSETSORIGINATED BY NONFINANCIALINSTITUTIONS

Two bank holding companies (the applicants)applied jointly for the Board’s approval undersection 4(c)(8) of the BHC Act to engage denovo in collection-agency activities pursuant toRegulation Y through a joint venture. The Boardconcluded that the collection activities werepermissible.

The bank holding companies also applied forthe Board’s approval to engage in asset-management, asset-servicing, and collectionactivities through a nonbank of the joint venturelocated in New Jersey. The subsidiary wouldprovide asset-management services to the Reso-lution Trust Corporation (RTC) and the FederalDeposit Insurance Corporation (FDIC). It wouldalso provide these services to unaffiliated third-party investors that purchase pools of assetsassembled by the RTC or the FDIC. Under theproposal, neither the applicants nor this non-bank subsidiary would acquire an ownershipinterest in the assets that they manage or in theinstitutions for which they provide the asset-management services. The applicants furthercommitted that they would not provide realproperty management or real estate brokerageservices as part of the proposed activities.

The Board previously determined that, withincertain parameters, providing asset-managementservices for assets originated by financial institu-tions (banks, savings associations, and creditunions) and their bank holding company affili-ates is an activity closely related to banking (see1991 FRB 331, 334 and section 3600.15.3). Theapplicants proposed to conduct all asset-management activities subject to the same con-ditions as in the Board orders previously cited.

The applicants proposed to engage in asset-management activities for assets originated bynonfinancial institutions as well as by financialinstitutions. These assets include real estate,consumer, and other loans; equipment leases;and extensions of credit. Assets of nonfinancialinstitutions include pension funds, leasing com-

1. Asset-management services include acting as agent inthe liquidation or sale of loans and collateral for loans, includ-ing real estate and other assets acquired through foreclosureor in satisfaction of debts previously contracted.

BHC Supervision Manual June 1999Page 1

panies, finance companies, and investment com-panies formed to engage in asset-managementactivities. The managed assets would be limitedto the types of assets that financial institutionshave the authority to originate. The Board con-cluded that the applicants would have the exper-tise to engage in managing these types of assets,

regardless of the originating entity. The Boardalso determined that the proposal was consistentwith the asset-management proposals approvedin its prior orders. The Board concluded that theapplicants’ proposed activities are closely relatedto banking and approved the order on December21, 1992. (1993 FRB 131)

Section 4(c)(8)—(Asset-Management, Asset-Servicing, and Collection Activities) 3084.0

BHC Supervision Manual June 1999Page 2

Section 4(c)(8) of the BHC Act(Receivables) Section 3090.0

Two nonbanking activities authorized undersection 4(c)(8) of the BHC Act, per RegulationY in section 225.28(b)(1), are the discount pur-chasing of a client’s accounts receivables (fac-toring) and the establishment of a revolving

credit facility secured by an assignment ofaccounts receivable (accounts receivable financ-ing). These activities date back to Board ordersissued in 1951. See sections 3090.1 and 3090.2.

BHC Supervision Manual December 1997Page 1

Section 4(c)(8) of the BHC Act(Factoring) Section 3090.1

3090.1.1 INTRODUCTION

Factoring is the discount purchasing of the cli-ent’s accounts receivable invoices for goods thathave been manufactured and shipped. Factoringdiffers from accounts receivable financing inthat the factor assumes the credit risk of collect-ing payment from the recipient of the goods.The principal advantage of factoring is that theclient is assured of the collection of the pro-ceeds of its sales, regardless of whether thefactor is paid.

A factor generally offers four basic services:(1) credit investigation and approval; (2) buyingthe client’s accounts receivable at a discount(generally between .75 and 1.5 percent) aftershipment of the goods to which there is nosubsequent claim, just a claim against theinvoices; (3) bookkeeping in the form of postingaccounts; and (4) advancing funds in the formof an ‘‘open account’’ when there could be30 days between shipment and payment. Thelater allows the client to replenish inventoryloans for working capital or expansion.

Maturity factoring and advance factoring arethe basic techniques of the industry. In maturityfactoring, an average maturity due date is com-puted for the receivables purchased during aperiod and the client receives payment on thatdate. Advance factoring uses the same computa-tions, however, the client has the option of tak-ing advance payments equal to a percentage ofthe balance due at any timeprior to the com-puted average maturity due date. The unad-vanced balance, sometimes called the ‘‘client’sequity,’’ is payable on demand at the due date.

The factor’s balance sheet reflects the pur-chases as ‘‘factored receivables’’ and the liabili-ties as ‘‘due to clients.’’ Usually the due toclients balance will be significantly less than thefactored receivables balance because of pay-ments and advances to the clients. The incomestatement will show factoring commissions,which represent the discount on the receivablespurchased. Interest income for advances on thedue to client balances may or may not be aseparate line item.

The factor is a pivoting point between thebuyer and the seller. The buyer must pay or allparties lose. Also the seller must have a reputa-tion for delivering quality merchandise. The fac-tor must know the business well enough toaccount for sudden increases in returns for out-of-specification merchandise or for merchandiseof low quality. If the seller does not performadequately, payment for the goods may not be

forthcoming, and if bankruptcy threatens theseller, buyers may hold back their futurepurchases.