2 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Executive Summary

The Indian pharma sector had an exceptional performance with Nifty Pharma index delivering ~100% return in the last 18 months. But with covid-related tailwinds receding, we believe it’s time to refocus on the basics for the sector considering: i) challenging near-term US outlook as companies contend with high single-digit price erosion and crowded P-4 opportunities; ii) secondary data show IPM is recovering to normalcy, but sustained volume recovery is key; iii) a more prudent R&D approach, focus on profit-oriented growth, and debt and working

capital improvement would lift RoCE ~150bp annually; and iv) leaner balance sheets may spur inorganic moves.

Not on steroids, but the sector is trading at a six-year high, and therefore the next cycle makes a compelling case of bottom-up analysis. Greater divergence in stock performance would be visible and companies with efficient business models, de-risked approach

and more pronounced RoCEs and earnings growth are likely to fetch a premium. We anticipate a ‘revert to fundamentals’, and argue that stocks with greater branded footprint, a sticky US portfolio, diversified geographical presence and proven execution would outperform. Top

picks: SUNP: play on specialty; CIPLA: branded play with a sticky US portfolio; and AJP and ALKM: branded plays with proven execution.

Evolving business model to assist profitable growth

Even prior to the pandemic, the pharma industry had started showing signs of

recovery—cleaning up of balance sheets by aggressively retiring debt, cost-

optimisation programs and divestment of non-core assets. Most heartening though,

in our view, is realigning of capital allocation decisions and concentrating on areas

of strength—targeted investments in certain therapies (Sun Pharma:

oncology/derma; Cipla: respiratory; Lupin: respiratory/women’s health) or certain

businesses (Aurobindo and Dr. Reddy’s in injectables).

We particularly like the strategy that a few players such as Cipla have adopted—to

venture into specialty, which entails a small upfront payment and the rest is based

on milestones. This keeps balance sheet and P&L unharmed, even in case of an

adverse outcome.

We acknowledge innovation is critical to survive; the focus though is not on trying

to get a toehold in everything, but a foothold in preferred niches. On the whole, the

pharma sector is healthier than it was two years ago, but strong earnings

momentum is needed to keep the pharma rally going.

US: Targeted investments to ensure growth

Price erosion, innovator aggression and less profitable shared exclusivities are the

bugbears for Indian pharma players. But we note: i) ongoing drug shortages in the US

are near an all-time high, which should limit further price pressure (from high single-

digit level today); ii) US generic majors such as Teva, Amneal and Mylan have scaled

down their oral solids presence, focusing more on complex products and diversifying

outside the US; iii) several Para IV or limited competition opportunities should keep

the US ticking for Indian players; and iv) large players are exploiting M&A/partnerships,

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 5

Story in charts US generic pricing, which eased to mid-single digit, has reverted to high single-digit erosion

Source: IQVIA, Edelweiss Research

Drug shortages to keep price erosion under check

Source: FDA, Edelweiss Research

Sector RoCEs to improve ~340bps over FY21–23E

Source: Company, Edelweiss Research

Volume GR impacted before covid seeing revival

Source: AIOCD; Note: GR= growth

Acute therapies worst hit have started to recover

Source: AIOCD

0

25

50

75

100

125

-15

-7

1

9

17

25

Oct

-14

Feb-

15

Jun-

15

Oct

-15

Feb-

16

Jun-

16

Oct

-16

Feb-

17

Jun-

17

Oct

-17

Feb-

18

Jun-

18

Oct

-18

Feb-

19

Jun-

19

Oct

-19

Feb-

20

Jun-

20

Oct

-20

Feb-

21

Jun-

21

Gen

eric

YoY

pri

cing

cha

nge

Generic pricing FDA approvals

CAH expectes inflation to decelerate

FDA approvals ramp considerably

ABC states generic inflation has slowed significantly

MCK reduced FY17 inflation outlook to a range that includes zero

ClarusONE sourcingagreement announced

Endo: Consortiumpressure reason

for pricing pressure

Teva finalisesClarusONE contract

FDA approvals ramp further

Teva, Sandoz, Mylan announce portfolio

rationlisation

Generic Injectables help to offset

persistent deflation in generic Oral Solids

Erosion easing on demand shortages

Erosion to settle around high single digit

0

25

50

75

100

125

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

Au

g-2

1

No

s.

No. of ongoing drug shortages

5

10.4

15.8

21.2

26.6

32FY

13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY2

1E

FY2

2E

FY2

3E

(%)

RoCE (%) RoCE ex-domestic

RoCE bottomed to 11% (ex-domestic 6%) in FY20 from its peak of ~27% (ex-domestic 22%) in FY14

Increasing investments and declining profitability impacted RoCEs

RoCEs expected to increase ~340bs over FY21-23E

5.7 5.4 4.2 2.7 2.3 1.6

-5.4

4.59.0

2.3 4.12.1

-0.7

3.5 5.34.8

5.7

5.95.4

5.0

3.5

3.3

3.4 2.72.6

3.5

2.9

-6

-1

4

9

14

19

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9

FY2

0

FY2

1

Jul'2

1

Au

g'2

1

Volume GR Price GR New Introduction GR

-18

-7

4

15

26

37

FY1

9

FY2

0

FY2

1

Au

g'2

1

FY1

9

FY2

0

FY2

1

Au

g'2

1

FY1

9

FY2

0

FY2

1

Au

g'2

1

Anti-infective Respiratory Pain

Volume GR (%) Price GR (%) NI GR (%)

Pharmaceuticals

Edelweiss Securities Limited

6 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Sector debt to remain at comfortable levels

Source: Company, Edelweiss Research

Lower capex and high value launches to propel FCF

Source: Company, Edelweiss Research

Pharma index trading at 26.7x 1 year forward; ~20% premium to Nifty

Source: Bloomberg, Edelweiss Research

0

0.4

0.8

1.2

1.6

2

FY1

7

FY1

8

FY1

9

FY2

0

FY2

1E

FY2

2E

FY2

3E

FY2

4E

Sector Debt/EBITDA

-250

-150

-50

50

150

250

FY1

7

FY1

8

FY1

9

FY2

0

FY2

1E

FY2

2E

FY2

3E

FY2

4E

INR

bn

Sector FCF Capex

-15

5

25

45

65

85

Jan

-14

Oct

-14

Jul-

15

Ap

r-1

6

Jan

-17

Oct

-17

Jul-

18

Ap

r-1

9

Jan

-20

Oct

-20

Jul-

21

Nifty Index PE Nifty Pharma Index PE Relative Premium

Pharma index is trading at 26.7x (~20% premiumto Nifty)

Edelweiss Securities Limited

Pharmaceuticals

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 7

US: Prefer players with healthy pipeline

The bulk of investments in the US by Indian pharma players have gravitated towards complex generics and biosimilars as US generics market faced multiple headwinds over the last five years—commoditisation of oral solids, pricing pressure and intensifying competition, among others.

The complex opportunity looks promising, but Indian players have had a mixed bag so far. Meanwhile, sole exclusivities for the first-to-file in

the US for large opportunities are giving way to less profitable shared exclusivities, not to mention heightened aggression by innovators to hold onto their market shares.

Challenges aside, Indian players have opportunities to capture. We note: i) ongoing drug shortages in the US are at an all-time high, which should ensure price erosion does not breach into double-digits; ii) Indian pharma companies have started milking their investments and are present in several Para IV or limited competition areas in the near term and this should keep the US ticking for them; and iii) large players are exploiting M&A/partnerships, targeting selective therapy

areas/ delivery systems/product forms.

Overall, sector RoCEs, which bottomed out to 11% (ex-domestic 6%) in FY20 from peak of ~27% (ex-domestic 22%) in FY14, are likely to rise ~150bps annually. Furthermore, pharma players with cost arbitrage, especially those that are backward integrated and have successful FDA inspection track record, stand a better chance to succeed.

US – Balancing expectations

The US generics market has faced multiple headwinds in the last five years:

commoditisation of oral solids and buyer consolidation resulting in pricing pressure.

Top 8 Indian companies’ revenue in the US

Source: Company, Edelweiss Research

1000

1200

1400

1600

1800

2000

Q1

FY1

4

Q3

FY1

4

Q1

FY1

5

Q3

FY1

5

Q1

FY1

6

Q3

FY1

6

Q1

FY1

7

Q3

FY1

7

Q1

FY1

8

Q3

FY1

8

Q1

FY1

9

Q3

FY1

9

Q1

FY2

0

Q3

FY2

0

Q1

FY2

1

Q3

FY2

1

Q1

FY2

2

(USD

mn

)

Top 8 Indian companies US revenue

Average 8% YoY decline

Average 5% YoY increase

Pharma players with cost arbitrage,

especially those that are backward

integrated, healthy launch pipeline and have

successful FDA inspection track record,

stand a better chance to succeed.

Pharmaceuticals

Edelweiss Securities Limited

8 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

RoCE: Set to improve ~340bps over FY21–23E

Source: Company, Edelweiss Research

Complex generics – A mixed bag: While Indian pharma companies are trying to

move up the value chain and target complex/specialty opportunity, their success has

been a mixed bag so far- Successful: mesalamines, metformin XR, respiratory such

as albuterol, doxorubicin. Moderate success- gSuboxone; Setbacks- gNuvaring (GNP,

DRRD), gCopaxone (Biocon, DRRD), long acting injectables such as Sandostatin LAR,

Iron sucrose, Invega sustenna, Lupron depot.

Success in complex generics? A mixed bag so far

Drug Company

Successful Mesalamines Cadila

Metformin XR Sun Pharma, Lupin, Glenmark, ARBP, AJP, Granules

Albuterol Cipla, Lupin

Doxil liposome Sun Pharma, Dr. Reddy's, Cadila

Concerta Sun Pharma, Dr. Reddy's

Moderate success Suboxone Dr. Reddy's (18% market share)

Biosimilars Biocon

Non-so-successful Nuvaring Glenmark withdrew; Dr. Reddy's

Copaxone Dr. Reddy's, Biocon (CRL)

Sandostatin LAR Sun Pharma, Dr. Reddy's, Aurobindo

Lupron Depot Sun Pharma, Dr. Reddy's, Lupin, Aurobindo

Venofer (Iron Sucrose) Sun Pharma, Dr. Reddy's

Invega sustenna Dr. Reddy's, Aurobindo

Invega Trinza Dr. Reddy's

Source: Edelweiss Research

Indian pharma companies will continue to invest in building their respective

capabilities. In the last one and half year, the companies have started milking their

investments by identifying pocket of opportunities such as Para IV or differentiated

products with limited competition. This is evident from the recent filings/approvals:

Cipla (albuterol and Advair), Lupin (albuterol), Dr. Reddy’s (gCiprodex, gSuboxone,

Kuvan), Cadila (mesalamine) and Glenmark (gBrovana). This coupled with the key

near-term opportunities should keep the US ticking for Indian players.

5

10.4

15.8

21.2

26.6

32

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9

FY2

0

FY2

1E

FY2

2E

FY2

3E

(%)

RoCE (%) RoCE ex-domestic

RoCE bottomed to 11% (ex-domestic 6%) in FY20 from its peak of ~27% (ex-domestic 22%) in FY14

Increasing investments and declining profitability impacted RoCEs RoCEs expected to

increase ~340bs over FY21-23E

Edelweiss Securities Limited

Pharmaceuticals

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 9

Improving revenue mix to ease pricing pressure…

While oral solids continue to be key cogs due to their sheer volumes every year, the

approval of other product forms is fast catching up. Comparing the 2010–14 period

to 2019, while the oral solids approvals have increased ~75%, approvals for

injectables have shot up 105%, topicals by ~300% and ophthal by ~175%. Higher

complexity, R&D requirements and lower probability of success means that fewer

companies are going along this route. However, we expect new entrants over

coming years due to sticky revenue and better margin profile.

Approval pie changing rapidly

Source: FDA, PharmForward, Edelweiss Research

…and so for the Indian formulation players

Likewise, the pie of Indian formulators has also shifted toward complex generics.

They are targeting opportunities in topicals, injectables, derma and inhalation,

Eagle Pharma (settled for Feb 22 launch; unlimited

qty from Apr -22); May 2022 patent upheld in Dr.

Reddy's case

Amitiza Lubiprostone Mallinckro

dt/ Takeda 450 2HFY23 6

Par - launched AG in Jan-21; Sun (after Jan 23); Dr.

Reddy’s will be 6 years after Nov-16.

Source: Company, Edelweiss Research

Pharmaceuticals

Edelweiss Securities Limited

12 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Targeted acquisitions made by Indian players

Company Acquisition Access/Therapy Specialty/Complex/Generic

Sun Pharma Ocular Technologies Opthalmology Specialty

Insite vision Opthalmology Specialty

Pharmalucence Injectables Complex

Dusa Dermatology Specialty

Dr. Reddy's Habitrol (Novartis) OTC-Transdermal Complex

Aurobindo 4 brands from TL Pharma Biosimilar Complex

Spectrum Onco injectables Complex

Cipla Avenue Therepeutics IV Tramadol- Pain Complex

Pulmatrix Pulmazole - Respiratory Complex

Lupin Symbiomix Women’s Health Specialty

Celon Respiratory Complex

InspiRX Respiratory Complex

Laboratories Grin Ophthalmology Complex

Cadila Sentynl Pain Specialty

Glenmark Uno Ciclo (Biochimico) Hormonal Contraceptive Complex

Bouwer Bartlett Dermatology Complex

Source: Company, Edelweiss Research

Price erosion reverting to high single digit, but not to CY17 levels

We note management commentaries around increased price erosion, which was not

unexpected considering supply normalisation. On the positive side, ongoing drug

shortages in the US are near all-time highs, and that should keep price erosion within

10% as opposed to deeper cuts seen in 2016–18.

US generics players have also reduced their footprint over last three years—either

US contribution has fallen, or they have transitioned to other dosage forms that are

susceptible to minimal price erosion. US majors are gradually reducing their

footprint through product withdrawals and niche launches, and by moving away

from plain-vanilla products. This underpins the steeper decline in their US growth

than Indian counterparts.

Another factor is the rise in the US FDA’s approval rate since CY15 has directly

impacted prices of generic drugs. On top of it, consolidation in distributors &

pharmacies and formation of buying consortiums amplified the pricing pressure. The

top-3 generic purchasers command 90% share of generic purchases, whereas top 4

generic companies have a 38% USD share and 34% TRx share.

Immune to buyer consolidation threat: Wholesaler consolidation, which impacted

margins in 2017–18, has been largely digested with new emerging channels such as

Amazon yet to show any impact.

Big pharma pulling out: US continues to remain a key market for global generic players.

Indian pharma firms benefitted from portfolio rationalisation by key global generic

players; their market share thus shot up from ~38% in mid-2018 to ~45% by mid-2019.

Many global MNC players, owing to persistent pricing pressure in the US,

restructured their portfolios and exited many molecules with low profitability.

Mylan and Teva accounted for 75% of those withdrawals. To date, Mylan has

rationalised 350 SKUs. Recently, Viatris (Mylan + Upjohn) laid out plans to close,

downsize or divest up to 15 facilities – including the Morgantown plant, which

produces oral solids – as part of a restructuring exercise announced in 2019.

Global companies such as Teva, Hikma have

indicated that price erosion is along

expected lines and as seen during pre-covid

days, i.e. around mid-to-high single digits;

do not expect it to revert to double-digits

Edelweiss Securities Limited

Pharmaceuticals

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 13

US major generics performance

Source: Company, Edelweiss Research

NA: North America

…has resulted in aggravating drug shortages: While new drug shortages, i.e. new

cases added every year do not indicate there is a problem, we note the number of

ongoing shortages is higher. This indicates that previous years’ shortages are yet to

be addressed and would thus throw up opportunities.

The US FDA mentioned, for the first time, in 2019 that pricing dynamics in the

generic market lead to shortages and that this mechanism needs to be addressed.

The watchdog even recommended suppliers with consistent quality record should

get longer-term contracts at “fair value” from customers.

Covid-19 related disruptions further aggravated the shortages. But, with easing of

the situation, price erosion has reverted to mid-high single digit and is likely to

remain at those levels.

US generic pricing, which eased to mid-single digit, has reverted to high single-digit erosion

Source: IQVIA, Edelweiss Research

-16%

-12%

-8%

-4%

0%

4%

0

8

16

24

32

40

Teva Mylan SandozU

S/N

A a

s %

of

reve

nu

e

CY17-20 US/NA CAGR CY17-20 overall CAGR

US/NA - % of revenue (LHS)

0

25

50

75

100

125

-15

-7

1

9

17

25

Oct

-14

Feb

-15

Jun

-15

Oct

-15

Feb

-16

Jun

-16

Oct

-16

Feb

-17

Jun

-17

Oct

-17

Feb

-18

Jun

-18

Oct

-18

Feb

-19

Jun

-19

Oct

-19

Feb

-20

Jun

-20

Oct

-20

Feb

-21

Jun

-21

Gen

eric

Yo

Y p

rici

ng

chan

ge

Generic pricing FDA approvals

CAH expectes inflation to decelerate

FDA approvals ramp considerably

ABC states generic inflation has slowed significantly

MCK reduced FY17 inflation outlook to a range that includes zero

ClarusONE sourcingagreement announced

Endo: Consortiumpressure reason

for pricing pressure

Teva finalisesClarusONE contract

FDA approvals ramp further

Teva, Sandoz, Mylan announce portfolio

rationlisation

Generic Injectables help to offset

persistent deflation in generic Oral Solids

Erosion easing on demand shortages

Erosion to settle around high single digit

Pharmaceuticals

Edelweiss Securities Limited

14 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Number of ongoing drug shortages at all-time highs

Source: FDA, Edelweiss Research *as on 31 Aug 21

Approval trend picked up in later part of 2020

Source: FDA, Edelweiss Research

US FDA inspection cycle on a temporary hold

CY20 saw the lowest number of inspections in the wake of the covid-19-related

lockdowns. And the second covid wave in India is likely to push further the timelines

for physical inspection.

Recently, the US FDA issued guidelines detailing how it will conduct ‘voluntary

remote interactive evaluations’ (meaning: desktop audit) at pharma plants until the

time the covid-19 emergency declared by HHS stays in place. We believe the

guidelines intend to ease the FDA’s inspection backlog once the physical inspection

resumes while at the same time ensuring that compliant facilities are still able to

churn out new approvals. This puts the US FDA inspection cycle on a pause.

Inspection intensity to pick up from end-FY22…

We do not believe that existing warning letters/import alerts will be lifted after

remote evaluation as this may require a physical inspection. Hence, several Indian

plants that are due for inspections/re-inspections, including Torrent’s Dahej and

Indrad facilities, Lupin’s Goa, Mandideep and Pithampur plants, Cadila’s Moraiya,

Sun’s Halol, and Cipla’s Goa and Aurobindo’s Unit-7, among other plants may take

further time to clear. Once the covid cases ease and inspections outside the US

resume, we expect the intensity to pick up.

0

25

50

75

100

125

2013 2014 2015 2016 2017 2018 2019 2020 Aug-21N

os.

No. of ongoing drug shortages

130 167 201304 290 336 293

291

413429

539 520500

461

0

9

18

27

36

45

0

180

360

540

720

900

2014 2015 2016 2017 2018 2019 2020

(%)

No

s.

Indian cos. Others Share of India cos. (%)

Edelweiss Securities Limited

Pharmaceuticals

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 15

…but not a cause for concern – it’s a zero-sum game for the sector

The US FDA’s Centre for Drug Evaluation and Research (CDER) oversees prescription

and OTC drugs, including biological therapeutics and generic drugs. It is the body

also responsible for monitoring compliance and carrying out inspection at drug

manufacturing plants.

As Exhibit 13 shows, 2015–19 marked a ramp-up in FDA inspections in India. This

was a direct outcome of: i) capacity expansion during this period for the US markets

with companies such as Ajanta, Alembic, Cadila and Strides building new plants; ii)

GDUFA-2 regime saw more regular inspections with every plant getting inspected at

least once in two years and some inspected virtually almost every year; and iii)

India’s contribution to US generics (by volume) increased from ~33% to ~45%.

Rise in US FDA inspections in India: In line with contribution to US

2013 2014 2015 2016 2017 2018 2019 2020

India 114 102 206 176 152 203 230 76

China 86 96 133 165 126 119 117 2

Others 1532 1641 1547 1558 1389 1261 1152 279

Total 1732 1839 1886 1899 1667 1583 1499 357

India inspections (%) 7% 6% 11% 9% 9% 13% 15% 21%

Source: FDA, Edelweiss Research

Exhbit 14 shows Indian companies are gradually learning to meet the FDA’s

requirements. While we acknowledge that rising inspections have led to higher

number of Form 483s, the proportion of OAIs has actually gone down over the last

six years. That said, with the FDA tightening regulatory norms, the bar for the

industry has gone further up, but the Indian pharma industry is in pole position to

pass muster vis-à-vis peers.

Proportion of OAIs to Indian players down in last six years

Source: FDA

We also flag that while a Form 483/Warning Letter poses earnings risk for the

company in question, it can turn out to be earnings neutral—or in some cases even

earnings-accretive for the industry. In the past Cadila’s and Sun’s warning letters led

to larger-than-expected windfalls for Torrent and Alembic in gAbilify. Similarly, Ipca’s

import alert generated substantial sales for Cadila in HCQs and Sandoz’s issues at a

partner’s fill-finish plant helped Natco gain a lead in gCopaxone 40mg/ml.

0

5

10

15

20

25

30

0

50

100

150

200

250

2013 2014 2015 2016 2017 2018 2019 2020

OAI VAI NAI % of OAI (RHS)

Pharmaceuticals

Edelweiss Securities Limited

16 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

FDA’s remote 'evaluations': Sets out physical inspection timelines?

The US FDA has issued guidelines describing how it will conduct ‘voluntary remote

interactive evaluations’ (meaning: desktop audit) at pharma plants until the time the

covid-19 emergency declared by Health and Human Services (HHS) stays in place.

Policy applicability

The scope of this policy is fairly wide as it covers CGMP as well as follow-ups (post

483/WL) inspections. Remote evaluation will take place only when the FDA believes

it would help in assessing all risks related to the application (i.e. it can help in making

a final decision).

Pre-Approval or Pre-License Inspections: Only if there is no data integrity or any

other issue that requires a physical inspection.

Post-Approval Inspections: Only if the facility has an ‘acceptable inspection

history’ with no data integrity or any other issue that requires a physical

inspection.

Surveillance Inspections: To be determined based on established criteria for

normal CGMP inspections.

Follow-up Inspections: Completely facility dependant and will take into

considerations like data integrity and inspection history.

Bioresearch Monitoring Inspections: No data integrity; evaluation only if data can

be made available by company/plant that aids decision-making.

Key points to note

The FDA has categorically stated that remote interactive evaluations do not

replace inspections.

The FDA will not accept requests from companies to conduce remote

evaluations, but will determine itself the facilities that can be evaluated.

Companies/plants that qualify have to give their approval to the FDA to allow

them to conduct virtual evaluation.

The FDA will ask for records and documents prior to the remote evaluation.

The FDA will issue a list of observations, but will not issue a Form 483.

Observations must be responded to within 15 days.

Edelweiss Securities Limited

Pharmaceuticals

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 17

Biosimilars: No white knight

A crowded plain-vanilla generics market, uncertainty around complex generics and lack of M&A opportunities have led to global generic companies investing in biosimilars as the next growth engine. Strategically, biosimilars make the cut: high entry barriers, USD200bn market, limited competition and stickier revenue stream. However, faster-than-expected price erosion and lower-than-expected biosimilar penetration, especially in the US, have soured its commercial potential.

Current US regulations too do not favour interchangeability, and this has put generic players at a disadvantage to big pharma, which have a big salesforce, better traction with specialist doctors and larger portfolios of branded drugs that incentivise wholesalers.

The long-term opportunity in biosimilars notwithstanding, challenges at hand such as price erosion and the need to gain market share are real. Among Indian players, BIocon is head and shoulders above others. Aurobindo, Lupin and Dr. Reddy’s follow.

Market size and scale remain healthy

Eight out of world’s top-10 selling molecules are biologics and in the US ~45% of the

manufacturer net revenues (after discounts and rebates) are biologics, as per IQVIA.

Spending on biologics is increasing faster than small molecules—despite

competition from biosimilars, spending on biologics is expanding at a CAGR of 14%

versus. 2% for small molecules. Exhibit 15 shows that, barring trastuzumab, all other

molecules have shown healthy growth in recent quarters despite the covid impact.

While it is well known that large pharma companies (including US generics) are

developing biosimilars, they have collaborated with several relatively small players

such as Merck with Samsung, Teva with Celltrion and Amgen with Allergan. The

complexity and costs involved in marketing biosimilars, especially under the current

regulatory regime that doesn’t yet provide a pathway for interchangeability, is likely

to filter out smaller players in the marketing process. We expect innovators with a

biosimilar portfolio to continue developing and marketing their own products while

other players with smaller balance sheets could continue partnering to de-risk

potential failures.

Pharmaceuticals

Edelweiss Securities Limited

22 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Domestic – Too early to panic

Growth in the ~USD20bn domestic market had slowed to sub-10% (prior to covid) from 13.5% in 2015 and further bore the brunt of covid-19-led disruptions. A large part of domestic growth is pricing-led and an uptick in volume growth is still not visible.

Even before the lockdown was imposed, IPM volumes flagged, and we believe this issue may persist for a few more quarters before branded volume growth reverts to 2–4%. Disease profile in India, fewer

incentives for JanAushadi and enforcement of margin capping on trade generics should see a beginning of volume revival in brands.

While the covid-influenced drugs led to supernormal growth in Apr-21 and May-21, growth settled around 14% in June and July. Covid-influenced drugs are still playing a role, but recovery in therapies such as pain management and neuro shows other parts of IPM are also recovering. We expect price growth to remain steady and launches to help offset volume erosion. IPM would thus grow 10–11% for the next few years. However, NLEM expansion poses risk to the industry.

Volume revival critical in post-covid scenario

Volume growth had been tepid for several quarters even before covid-19. Industry

growth led by volumes is more sustainable in our view; hence, revival of volume

growth is critical.

The supernormal growth of 52% and 48% in Apr-21 and May-21, respectively, was largely

led by covid drugs as well as covid-influenced drugs such as insulins, anti-coagulants and

corticosteroids. Jun-21 and Jul-21 settled at ~14%, and August saw 18% growth.

Acute therapies drove the growth and chronic was subdued, growing in mid-single

digit. The analysis by AIOCD AWACS shows that IPM volume growth without covid-

influenced drugs stood at -0.7% in Jul-21.

IPM volume performance without covid drugs yet to recover

Contribution MAT July'21 Month July'21

Value GR (%) Unit GR (%) Value GR (%) Unit GR (%)

IPM 100% 12.8 4.2 13.7 4.9

With covid influence 37% 26.3 10.6 27.1 10.6

Without covid influence 63% 6.2 -0.7 7.1 -0.7

Source: AIOCD

Volumes were impacted even before covid

A deep-dive into IPM’s main growth drivers shows that: i) volume growth slowed by

~300bps largely due to penetration of unbranded generics and government push via

Jan Aushadhi; ii) pricing, while impacted by NPPA’s regulatory actions, has now

reverted to its 5% growth level; ii) new introductions (NI) slowed as approvals for

irrational combinations and new product innovations declined, impacting IPM

growth by ~200bps. While the risk of deceleration in pricing-led domestic growth

poses a challenge, we expect pricing growth to remain steady in the near term. The

volumes are expected to revert back to 2-4% as field force activity opens up and

patients take their elective surgeries.

Edelweiss Securities Limited

Pharmaceuticals

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 23

Volume and NI growth impacted even before lockdown

Source: AIOCD

Deciphering domestic growth in the aftermath of covid

Chronic therapies steady; acute can surprise positively

The overall IPM volumes further bore the brunt of covid-19-induced lockdown,

which led to restricted field force activity and postponement of elective surgeries.

This in turn dragged acute therapy growth, while chronic therapies continued to

perform well.

Growth of chronic therapies has been steady over the last four years, and we expect

it to continue to do well given rising incidence of chronic cases, molecules going off

patents, innovations and MNC introductions. On the other hand, the growth has

been lumpy in case of acute therapies and may surprise positively once the covid

situation eases.

Therapies such as anti-infective, gastro, vitamin and respiratory had significant

contribution from covid-influenced drugs, which led to strong double-digit growth

in revenues during the second covid wave. While covid influenced drugs continue to

aid volume growth, growth in therapies such as pain, neuro and ophthal show that

other parts of the IPM are seeing signs of revival.

Performance of top 10 therapies

MAT July'21 Month July'21

Value growth

(%)

Unit growth

(%)

Value growth

(%)

Unit growth

(%)

Covid

ratio

Anti-infective 21.3 0.7 30.2 16.8 73%

Cardiac 13.5 2.9 4.1 -4.3 23%

Gastro 17.9 11.7 19.6 9.8 64%

Anti-diabetic 6.8 1.9 3.3 -3.1 18%

Vitamin 21.5 13.9 10.5 -6.3 48%

Respiratory 3.2 -7.3 22.8 9.7 70%

Pain 11.9 8.4 24.1 16.9 32%

Derma 10.7 1.1 9.7 -5.6 3%

Neuro/CNS 7.8 1.8 8.2 0.0 3%

Gynaecological 10.8 5.3 15.4 6.5 13%

Source: AIOCD

MAT- Moving Annual Turnover

5.7 5.4 4.22.7 2.3 1.6

-5.4

2.3 4.1

2.1

-0.7

3.5 5.3

4.8

5.45.0

3.5

3.3

3.42.7

2.6

FY15 FY16 FY17 FY18 FY19 FY20 FY21

Volume GR Price GR New Introduction GR

13.414.5

9.8

5.3

9.1 9.7

2.1

Pharmaceuticals

Edelweiss Securities Limited

24 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Cardiovascular has been clocking an 11% CAGR over the past five years with 11.2%

growth as of MAT March 2021 and steady volume growth of about 5%. Major players

include Sun, Torrent, Lupin, USV and Glenmark. The anti-diabetic therapy accounts for

~10% of the IPM, or ~INR149bn. The therapy logged a ~17% CAGR over FY13–18 with

growth slowing to ~12%. This further came off to 6% in FY21, but is likely to pick up with

rising incidence of chronic cases. Major players include Abbott, Lupin, Sun and Sanofi.

Cardiac growth steady at ~11% over the years

Source: AIOCD

Anti-diabetic growth down from 11% to 6% in FY21

Source: AIOCD

Anti-infective is IPM’s largest therapy area, accounting for ~13% of the IPM. It is a seasonal

therapy that used to grow at 10–12%, but has moderated in recent times, and has settled

at mid to high single digit. Volume hit was worst seen in this therapy in the wake of low

incidence of anti-infective cases as people stayed indoors for most part of FY21.

Pain/analgesics account for ~6% of the IPM and has been clocking ~8% CAGR over

the past five years, with growth slowing to -2.7% as of MAT March 2021.

Vitamin/Mineral/Nutrients is a fast growing therapy, which could expand into a

tremendous opportunity with increasing diagnosis of vitamin deficiencies and an

overall focus on consumer health. The therapy accounts for ~9% of the IPM and has

been clocking a CAGR of ~8.5% over the past five years.

Worst volume hit seen in acute therapies; growth likely to recover as covid-19 situation eases

Tenofovir+Lamivudine+Dolutegravir 329 EmcureEmcure holds 99% of the

market; Cipla ~1%

Terbinafine 2,004 Sun Sebifin 248 2

GSK Zimig 152 3

Dr.Reddy Gris-ODT 140 4

Glenmark Ifin 98 6

Valganciclovir 46 Cipla Valgan 27 1

Major players

Pharmaceuticals

Edelweiss Securities Limited

30 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

Right capital allocation to drive returns

Soaring investments in complex generics/specialty and extended business costs during FY15–19 rendered US business of most Indian pharma companies almost non-profitable. RoCEs, which had reached north of 20% in 2015, sagged to 11% by FY19 with SUNP, LPC and TRP feeling the heat.

Prior to the pandemic, the pharma industry had already started showing signs of recovery—by dint of prudent capital allocation

decisions and concentrating on areas of strength, i.e. targeted investments in certain therapies (SUNP, Cipla, LPC, Alembic) or businesses (ARBP and DRRD in injectables).

We particularly like the strategy that only few players such as Cipla have adopted: to venture into specialty, which entails a small upfront payment and the rest is based on milestones, putting no pressure on balance sheet and P&L in case of an adverse outcomes.

Rationalising R&D spends; focus on improving productivity

As generics became a crowded space, Indian players started de-risking by moving up

the value chain. The significant amount of capital required to invest in augmenting

differentiated products or specialty led to R&D spends almost doubling over FY14–

19.

However, we note the recent shift in strategy of Indian drugs players, which involves

prioritising R&D spends towards focussed therapy areas and improving productivity

by leveraging R&D to sell products in multiple markets. Furthermore, companies are

relying on partnerships and joint ventures to finance R&D and commercialise

products: DRRD in 505b2 and biosimilars, ARBP in biosimilars, GNP in specialty

molecules. This strategic de-risking deal enables cost recovery and reduces future

R&D payouts while retaining some future upside benefits from successful filings and

commercialization.

Large players such as SUNP, LPC and DRRD commit over USD200mn in R&D

investments per annum, mainly towards specialty (wherein SUNP leads the pack)

and complex generics, primarily in injectables, respiratory, mesalamines and

transdermals. We expect biosimilars to constitute a notable share in the R&D pie

over coming years, particularly for ARBP, DRRD and CDH.

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 31

Focus remains on rationalising R&D investments

Company Comments on R&D

DRRD Focussing on creating global dossiers to leverage R&D to market same products across geographies, thus, improving productivity. Also, made a conscious decision to rationalise R&D spends on 505B2, evident from less number of products in the pipeline.

CIPLA With successful completion of gAdvair trials and filing, we expect R&D as % of sales to moderate going forward. However, the company will continue to invest meaningfully as the respiratory assets progress in clinical trials.

ARBP Only company to see significant increase in R&D, both in absolute and as % of sales as company gears itself to conduct biosimilar trials.

LPC "The focus today is on more complex products. Over the next several quarters, it will - tend to be a little lower, perhaps settling around the 8% range."

GNP Management intends to bring down R&D spends from 13% to 10% of sales in FY22. Scouting for partners for conducting phase 3 trials for certain molecules. Bulk of R&D comprises of innovative R&D and expect it to taper down.

CDH R&D to hover around 7–8% of revenue, with 60% on generics and rest divided between NCEs, biologics and vaccines.

Source: Company, Edelweiss Research

While we do not expect sector R&D to materially decline, the intensity of spends is

likely to moderate going forward commensurate with the increase in revenues.

Hence, we believe R&D as a percentage of sales would remain flat over the next

Divi’s is contracted to manufacture and supply molnupiravir API to Merck.

Molnupiravir is Merck and Ridgeback’s oral antiviral medication to treat Covid.

Interim analysis of Ph.3 shows molnupiravir reduced the risk of hospitalization or

death by approximately 50%; 7.3% of patients who received molnupiravir were

either hospitalized or died through Day 29 following randomization (28/385),

compared with 14.1% of placebo-treated patients (53/377).

Through Day 29, no deaths were reported in patients that received molnupiravir, as

compared to 8 deaths in patients that received placebo. An independent Data

Monitoring Committee has recommended that recruitment into the study be

stopped in consultation with the FDA early due to these positive results. Merck is

expected to seek US emergency use authorization. This could pave the way for the

Edelweiss Securities Limited

Pharmaceuticals

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 39

first covid treatment pill in the world. For now only antibody cocktails that have to

be given intravenously are approved for non-hospitalized patients.

According to Merck, US government has already placed orders for ~1.7mn doses at

~USD700/dose. Merck expects to produce at least 10mn doses in CY21 and even

more in CY22. Divi’s is contracted to supply API to Merck and our calculations

suggest it could add ~8-10% to Merck’s FY22 EPS.

Merck has also given licences to Sun, Cipla, Natco, Torrent, Dr. Reddy’s and Emcure

to sell molnupiravir in India and 100 low- and middle-income countries. Natco is

conducting its own trials in India while others are collaborating, and we expect trial

results soon.

We forecast ~10% EPS accretion to Divis’ FY23 earnings based on USD18/dose

realization and ~55% EBITDA margin.

Pharmaceuticals

Edelweiss Securities Limited

40 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

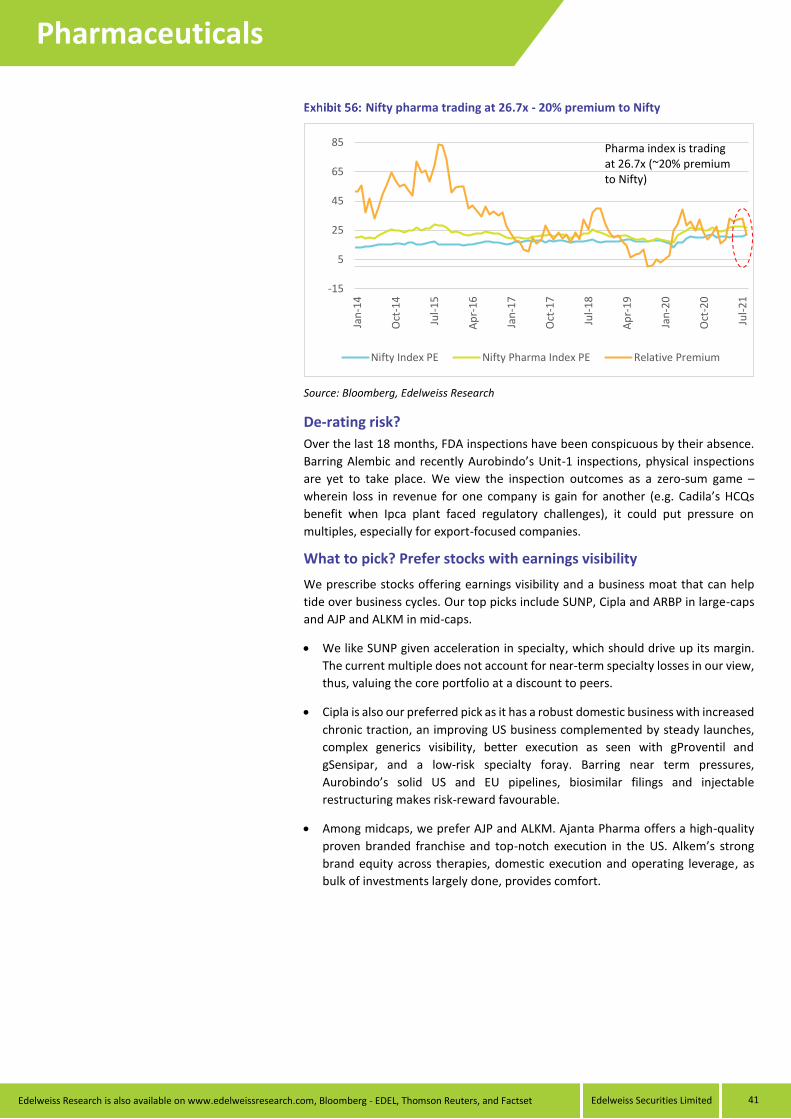

Valuations: Expensive but not prohibitive

The pharma sector has been in a sweet spot as it positioned itself quickly to grab opportunities in the covid-19-hit economy. Covid-19 pandemic – which led to best-ever quarters in terms of profitability – was a serendipitous event. Nifty Pharma is trading at ~27x PE and ~17x EV/EBITDA 1-year forward; they are six-year highs.

While sector RoCEs and RoEs are likely to improve 100–150bps annually hereon, we note RoEs are still lower than the peak seen in

FY14. And, the re-rating in the broader market has ensured pharma premium to Nifty stands at ~20%, which is below the 10-year average.

There are clear beneficiaries in the near term, and vaccine opportunity can have a long tail from exports and private markets, not to mention lack of clarity on the number and timing of doses, other covid-19 opportunity may fade over time.

We reiterate only stocks with diversified geographical presence, a quality launch pipeline, healthy balance sheet and earnings sustainability are likely to outperform the sector. We prefer SUNP, CIPLA and ARBP among large-caps, and AJP and ALKM in mid-caps.

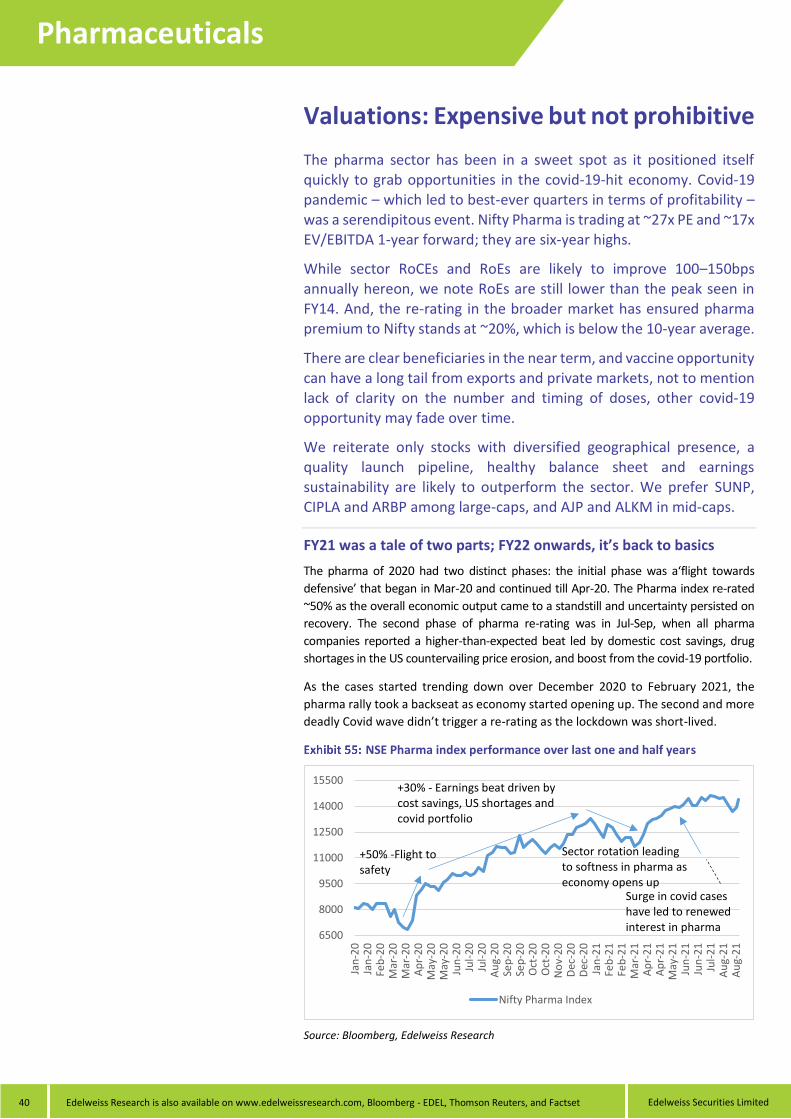

FY21 was a tale of two parts; FY22 onwards, it’s back to basics

The pharma of 2020 had two distinct phases: the initial phase was a‘flight towards

defensive’ that began in Mar-20 and continued till Apr-20. The Pharma index re-rated

~50% as the overall economic output came to a standstill and uncertainty persisted on

recovery. The second phase of pharma re-rating was in Jul-Sep, when all pharma

companies reported a higher-than-expected beat led by domestic cost savings, drug

shortages in the US countervailing price erosion, and boost from the covid-19 portfolio.

As the cases started trending down over December 2020 to February 2021, the

pharma rally took a backseat as economy started opening up. The second and more

deadly Covid wave didn’t trigger a re-rating as the lockdown was short-lived.

NSE Pharma index performance over last one and half years

Source: Bloomberg, Edelweiss Research

6500

8000

9500

11000

12500

14000

15500

Jan

-20

Jan

-20

Feb

-20

Mar

-20

Mar

-20

Ap

r-2

0M

ay-2

0M

ay-2

0Ju

n-2

0Ju

l-2

0Ju

l-2

0A

ug-

20

Sep

-20

Sep

-20

Oct

-20

Oct

-20

No

v-2

0D

ec-2

0D

ec-2

0Ja

n-2

1Fe

b-2

1Fe

b-2

1M

ar-2

1A

pr-

21

Ap

r-2

1M

ay-2

1Ju

n-2

1Ju

n-2

1Ju

l-2

1A

ug-

21

Au

g-2

1

Nifty Pharma Index

+50% -Flight to safety

+30% - Earnings beat driven by cost savings, US shortages and covid portfolio

Sector rotation leadingto softness in pharma as economy opens up

Surge in covid cases have led to renewed interest in pharma

Edelweiss Securities Limited

Pharmaceuticals

Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset 41

Nifty pharma trading at 26.7x - 20% premium to Nifty

Source: Bloomberg, Edelweiss Research

De-rating risk?

Over the last 18 months, FDA inspections have been conspicuous by their absence.

Barring Alembic and recently Aurobindo’s Unit-1 inspections, physical inspections

are yet to take place. We view the inspection outcomes as a zero-sum game –

wherein loss in revenue for one company is gain for another (e.g. Cadila’s HCQs

benefit when Ipca plant faced regulatory challenges), it could put pressure on

multiples, especially for export-focused companies.

What to pick? Prefer stocks with earnings visibility

We prescribe stocks offering earnings visibility and a business moat that can help

tide over business cycles. Our top picks include SUNP, Cipla and ARBP in large-caps

and AJP and ALKM in mid-caps.

We like SUNP given acceleration in specialty, which should drive up its margin.

The current multiple does not account for near-term specialty losses in our view,

thus, valuing the core portfolio at a discount to peers.

Cipla is also our preferred pick as it has a robust domestic business with increased

chronic traction, an improving US business complemented by steady launches,

complex generics visibility, better execution as seen with gProventil and

gSensipar, and a low-risk specialty foray. Barring near term pressures,

Aurobindo’s solid US and EU pipelines, biosimilar filings and injectable

restructuring makes risk-reward favourable.

Among midcaps, we prefer AJP and ALKM. Ajanta Pharma offers a high-quality

proven branded franchise and top-notch execution in the US. Alkem’s strong

brand equity across therapies, domestic execution and operating leverage, as

bulk of investments largely done, provides comfort.

-15

5

25

45

65

85

Jan

-14

Oct

-14

Jul-

15

Ap

r-1

6

Jan

-17

Oct

-17

Jul-

18

Ap

r-1

9

Jan

-20

Oct

-20

Jul-

21

Nifty Index PE Nifty Pharma Index PE Relative Premium

Pharma index is trading at 26.7x (~20% premiumto Nifty)

Pharmaceuticals

Edelweiss Securities Limited

42 Edelweiss Research is also available on www.edelweissresearch.com, Bloomberg - EDEL, Thomson Reuters, and Factset

We maintain the positive view on Ajanta Pharma (AJP) as it remains best placed to clock steady growth given: i) domestic business is backed by first-in-market products with a promising pipeline that would drive broad-based growth; ii) few, but profitable US launches; and iii) double-digit branded exports growth. Increased in-house production will lead to sustainable 30%+ EBITDA margin and tax

benefits will drive an FY21–24E revenue/EPS CAGR of 13%/17%.

AJP is our top pick in the mid-cap pharma space. Given ~65% branded mix, a stable domestic business and minimal price erosion, AJP deserves to trade at a premium. We value AJP at 27x FY23E EPS; retain ‘BUY’ with a TP of INR2,885 (earlier INR2,760) as we roll over to FY23E.

FINANCIALS (INR mn)

Year to March FY21A FY22E FY23E FY24E

Revenue 28,896 32,973 37,773 42,138

EBITDA 9,985 10,621 12,439 13,887

Adjusted profit 6,538 7,717 9,195 10,599

Diluted EPS (INR) 74.5 88.8 105.8 121.9

EPS growth (%) 47.0 19.1 19.2 15.3

RoAE (%) 23.4 23.6 23.8 23.2

P/E (x) 30.3 25.5 21.4 18.5

EV/EBITDA (x) 19.2 17.6 14.7 12.7

Dividend yield (%) 0.4 1.0 1.2 1.3

PRICE PERFORMANCE

Branded business provides stability; growth momentum to continue

We forecast a 13% revenue CAGR backed by structural recovery and growth

initiatives across therapies in India, and branded equity in Africa and Asia. AJP’s

branded play lends visibility and sustainability to its earnings while comparable

margins across India, Africa and Asia eliminate concentration risk. Moreover, its

growing trade generics portfolio complements its branded franchise. Also, with

deepening presence and scale-up of field force in select markets such as Iraq, the

Philippines, Uzbekistan, Africa and other geographies are expected to drive double-

digit growth. While the US will see fewer launches in FY22, market share expansion

in existing products and a few high-value launches like gChantix are likely to drive

20%+ CAGR. Given low US contribution, price erosion’s fallout would be minimal.

Capex completion to propel FCF 2.3x; return ratios impressive

AJP’s ~INR16.5bn investment over FY15–20 has potential to: i) expand sales 1.5x by

FY24; ii) bring down tax rate lower due to in-house manufacturing; and iii) lift FCF by

2.3x over FY21–24E. EBITDA margins have rebounded sharply from the FY20 trough,

and the company is confident of maintaining 30%+ margins. AJP has ~INR4bn in net

cash and enjoys superior returns ratios and asset turnover of ~30% and 2x,

respectively.

Explore:

Outlook and valuation: Attractive; maintain ‘BUY’

The company’s branded business, which accounts for ~65% of revenue, lends

visibility and sustainability to earnings growth. Despite a high FY21 base, we forecast

an FY21–24E EPS CAGR of ~17% driven by a steady operating performance across

businesses and operating leverage from new plants. Given higher branded

contribution, a stable domestic business and best-in- class returns metrics, we value

AJP at 27x FY23 EPS. Maintain ‘BUY/SO’ with a revised TP of INR2,885 (INR2,760

earlier) as we roll over the valuation to FY23E EPS. Key risks: delay in product

approvals, USFDA risk, NLEM and currency.

10

15

20

25

30

Sales Growth(%)

EPS Growth(%)

RoE(%)

PE(x)

Pharmaceuticals AJP IN EQUITY

38,000

42,600

47,200

51,800

56,400

61,000

1,500

1,680

1,860

2,040

2,220

2,400

Oct-20 Jan-21 Apr-21 Jul-21 Oct-21

AJP IN EQUITY Sensex

India Equity Research Pharmaceuticals October 4, 2021

We remain positive on Alkem (ALKM) based on: i) its strong brand equity, consistent market share gains and presence in fast-growing sub-therapies in India; ii) volume-driven growth, which is sustainable; iii) potential mid-teens CAGR and improved launches in the US driving profitability; and iv) uptick in margin for incremental business considering salesforce expansion is largely over.

Alkem remains one of our top pharma mid-cap space. We reckon growth led by sustained operating leverage and thus model in revenue/PAT CAGR of 14%/13% over FY21–24E. Maintain ‘BUY’ with a TP of INR4,600 (earlier INR4,060) as we roll over to FY23E EPS and raise the target to 27x due to stronger-than-expected sustainable recovery.

FINANCIALS (INR mn)

Year to March FY21A FY22E FY23E FY24E

Revenue 88,765 1,05,517 1,16,632 1,31,405

EBITDA 19,539 21,602 25,248 28,709

Adjusted profit 15,850 16,818 20,321 22,696

Diluted EPS (INR) 132.6 140.7 170.0 189.8

EPS growth (%) 40.5 6.1 20.8 11.7

RoAE (%) 23.4 21.1 21.9 21.1

P/E (x) 30.1 28.4 23.5 21.0

EV/EBITDA (x) 23.9 21.2 17.7 15.2

Dividend yield (%) 0.8 1.1 1.3 1.4

PRICE PERFORMANCE

Domestic remains on solid footing

Despite bearing the brunt of the first covid wave, Alkem has posted the sharpest

recovery, which could translate to a 24% spurt in domestic revenue in FY22. The

resilience underscores the brand equity of its domestic franchise and long-standing

relationships in the trade generics business. Even on high base, ALKM would clock

an 11% CAGR over FY22–24E since its therapies, other than anti-infective, are gaining

traction. With a sales force of ~10,500 for large sub-therapies, the company’s ability

to convert patients to own brands/therapies, not to mention pursuit of niche but

untapped therapies, should help it sustain above-industry growth.

US: Improving launch trajectory to drive profitable growth

The US business has been bolstered by limited competition launches such as gApriso

and gDuexis, and could witness FY23 onward other mesalamine launches along with

gPradaxa. In fact, ALKM’s US business has ramped up 3x over the last seven years;

we forecast a mid-teen revenue CAGR for FY21–24E driven by 12–15 launches in

FY22 and more than ten FY23 onwards. Unlike past, we expect its US profitability to

improve as sales grow on the back of improvement in launch quality. This would

improve margins from high single-digit to 14% by FY23.

Explore:

Outlook and valuation: Steady growth ahead; maintain ‘BUY’

Despite an exceptional FY21, Alkem can still post a 13% earnings CAGR through FY24

driven by a 14% revenue CAGR. The sharp recovery in its domestic business testifies

to its strong brand equity. A net-cash balance sheet, consistent FCF (1.7x over FY21)

and steady returns ratios instil additional comfort. We value Alkem at 27x FY23E EPS

(10% discount to Torrent) due to stronger-than-expected recovery, which is

sustainable in our view. This yields a fair value of INR4,600 (earlier INR4,060). Retain

‘BUY/SO’.

5

10

15

20

25

30

Sales Growth(%)

EPS Growth(%)

RoE(%)

PE(x)

Pharmaceuticals ALKEM IN EQUITY

38,000

42,600

47,200

51,800

56,400

61,000

2,550

2,845

3,140

3,435

3,730

4,025

Oct-20 Jan-21 Apr-21 Jul-21 Oct-21

ALKEM IN EQUITY Sensex

India Equity Research Pharmaceuticals October 4, 2021

We remain positive on Aurobindo Pharma (ARBP) as: i) barring near-term pressure, US pipeline looks solid; ii) injectables expansion is margin-accretive; iii) biosimilar filings would aid growth post-FY23; iv) gRevlimid adds to FY23–25E revenue stability; and v) EU pipeline of 250-plus launches can drive steady 9–10% growth.

ARBP is on the cusp of filing biosimilars, nasals, inhalers, transdermals, and depot injections. The prospects are bright, but entail high R&D outlay and execution risks. We argue our 16x FY23E EPS target captures the risk. Retain ‘BUY’ with a TP of INR990 (up from INR970) based on 16x core FY23E EPS and INR25/share for gRevlimid.

FINANCIALS (INR mn)

Year to March FY21A FY22E FY23E FY24E

Revenue 2,47,747 2,48,204 2,66,774 3,00,258

EBITDA 53,335 53,161 59,474 73,509

Adjusted profit 32,250 33,529 36,677 46,293

Diluted EPS (INR) 55.0 57.2 62.6 79.0

EPS growth (%) 12.6 4.0 9.4 26.2

RoAE (%) 27.5 14.3 13.7 15.1

P/E (x) 13.0 12.5 11.5 9.1

EV/EBITDA (x) 7.8 7.9 6.7 5.0

Dividend yield (%) 0.6 0.5 0.5 0.7

PRICE PERFORMANCE

US pipeline solid; injectables a clear priority

Near-term pressure from ertapenem competition and price erosion is likely to be

offset by a pipeline of ~170 pending ANDAs, 50 annual launches, gRevlimid and

injectable expansion. ARBP has a clear focus on growing the injectables business

from USD395mn at present to USD650–700mn over the next three years. While we

await the unveiling of depot injections, inhalers and transdermals, we see limited

risk to our mid-single-digit US growth estimates given low profit concentration.

Biosimilar and vaccine could provide potential upside

We are enthused by ARBP’s biosimilar investments. Two of the six biosimilars are

likely to be filed in the EU and the US before end-FY22. Biosimilars can add

INR60/share to fair value. We have not factored in the vaccine (covid and

pneumococcal) opportunity yet, implying further upside to our numbers.

Pushing all areas to improve Europe profitability

EU is likely to show margin improvement driven by: i) more products sourced from

low-cost base India; ii) ertapenem launch and expansion of penem block; iii) a

pipeline of 250-plus products including complex injectables for hospital setting that

will help offset price pressure; iv) 2 biosimilar filings; and v) Eugia oncology launches.

Explore:

Outlook and valuation: Risk-reward turning favourable; retain ‘BUY’

ARBP’s business is steady and with low-profit concentration. The biosimilars and

injectables expansion provides an additional push to high US base. gRevlimid

settlement offers cushion for its complex generics business to deliver. Our INR990

target price (up from INR970) is based on 16x FY23E core EPS and INR25/share from

gRevlimid. Maintain ‘BUY/SO’.

0

10

20

30

Sales Growth(%)

EPS Growth(%)

RoE(%)

PE(x)

Pharmaceuticals ARBP IN Equity

38,000

42,600

47,200

51,800

56,400

61,000

675

750

825

900

975

1,050

Oct-20 Jan-21 Apr-21 Jul-21 Oct-21

ARBP IN Equity Sensex

India Equity Research Pharmaceuticals October 4, 2021

We believe Biocon (BIOS) may underperform owing to: i) sub-par execution in biosimilars in the US and increased competition; and ii) surging R&D and high capex intensity. While interchangeability designation for its insulin products is welcome, we believe our 20% market share captures upside potential given innovator is likely to adopt different strategies to retain share. And given limited data

around vaccine type and strategy, we remain cautious on the vaccine deal with Serum Institute.

Meanwhile, we await evidence of a sustained uptick in market share and revenue. Our SoTP yield a DCF-based value of INR143/share for biosimilar. Maintain ‘REDUCE/SU’ with a target price of INR335.

Cadila Healthcare (CDH) is up against odds: i) Mounting US pricing pressure and impending mesalamine competition from H2FY22. ii) Awaiting approval and eventual execution on transdermals and injectables; iii) Sustainable domestic recovery not yet seen. iv) Limited market opportunity for ZyCov-D; v) Moraiya clearance.

We are building in a flat earnings CAGR over FY21–24 excluding gRevlimid. While the timing and extent of mesalamine erosion remains to be seen, potential earnings downside exists. Maintain ‘REDUCE’ with a target price of INR515 as we roll over the valuation to FY23E EPS. Our TP is based on 22x FY23E core EPS and INR30 from gRevlimid and Zy-CovD.

FINANCIALS (INR mn)

Year to March FY21A FY22E FY23E FY24E

Revenue 1,51,022 1,60,907 1,71,267 1,95,481

EBITDA 33,410 35,903 38,406 47,719

Adjusted profit 23,266 22,044 23,965 31,019

Diluted EPS (INR) 22.7 21.5 23.4 30.3

EPS growth (%) 58.5 (5.3) 8.7 29.4

RoAE (%) 18.3 15.9 15.3 17.3

P/E (x) 24.2 25.6 23.5 18.2

EV/EBITDA (x) 17.9 15.3 14.6 11.2

Dividend yield (%) 0.6 0.8 0.9 1.1

PRICE PERFORMANCE

US pressure rising; pipeline delivery critical

CDH’s current revenue stream is heavily dependent on its mesalamine franchise,

which contributes ~30% to profit in our view. With Asacol HD patent expiring in Nov-

21, Lialda peaking out and rising pricing pressure, it’s critical that transdermal and

injectable launches (including in-licensed ones with exclusivity) materialise. The

success hinges on Moraiya resolution, which remains uncertain. While opex savings

may lift margin in the near term, any delay in US launches would impact earnings.

Vaccines, biosimilars, specialty – All still evolving

In biosimilars, CDH aims to target EMs initially in a big way with pegfilgrastim,

trastuzumab and adalimumab (launched first biosimilar, viz., Pegfilgrastim in Russia).

This, we believe, may not move the needle. Besides, a late entry in developed

markets may limit the opportunity. In vaccines, UNICEF and PAHO tender markets

remain the key growth driver. Saroglitazar Magnesium is in trials in the US—phase

2b trials to begin for NASH indication and phase 2 completed for PBC.

Zy-CovD potential launch in October could add INR4–6 to EPS, in our view. But given

delayed approval, competitors already having approval and ramping up supplies,

market opportunity could be limited.

Explore:

Outlook and valuation: Risk-reward unfavourable; retain ‘REDUCE’

With Asacol HD patent expiring in Nov-21, mesalamine peaking out, US facing price

pressure and covid tailwinds now behind, the odds of flat earnings are high. We have

built in a flat earnings trajectory for FY21–24 (excluding gRevlimid) as US launches

from H2FY22 are likely to be set off by competition in mesalamine and price

pressure. While Zy-CovD can be ~25% accretive, market size may be limited due to

delayed launch. We continue to maintain ‘REDUCE’ with an unchanged TP of INR515.

Our TP is based on 22x FY23E core EPS and INR30 from gRevlimid and Zy-CovD.

-10

0

10

20

30

Sales Growth(%)

EPS Growth(%)

RoE(%)

PE(x)

Pharmaceuticals CDH IN Equity

38,000

42,600

47,200

51,800

56,400

61,000

375

435

495

555

615

675

Oct-20 Jan-21 Apr-21 Jul-21 Oct-21

CDH IN Equity Sensex

India Equity Research Pharmaceuticals October 4, 2021

Cipla remains among our ‘top picks’ in pharma based on: i) strong India business, ii) improved visibility in the US complex pipeline—gBrovana and gFosrenol in FY22, followed by gAdvair, gRevlimid and gAbraxane in FY23 that would potentially double US business by FY24; iii) focused cost control; and iv) a clearly delineated strategy, which allays concerns around investments and execution. Besides, with R&D likely

to rise slowly and much of opex savings looking sustainable, the base business margin of ~22% seems achievable.

Going forward, we expect the company to clock an EPS CAGR of 23% through FY24E. Maintain ‘BUY’ with a revised TP of INR1,140 (earlier INR1,100) as we roll forward to FY23E EPS.

FINANCIALS (INR mn)

Year to March FY21A FY22E FY23E FY24E

Revenue 1,91,596 2,15,232 2,35,579 2,69,662

EBITDA 42,524 48,700 59,120 69,536

Adjusted profit 24,049 29,951 37,657 44,836

Diluted EPS (INR) 29.8 37.2 46.7 55.6

EPS growth (%) 55.5 24.5 25.7 19.1

RoAE (%) 14.1 15.3 16.7 17.2

P/E (x) 33.0 26.5 21.1 17.7

EV/EBITDA (x) 18.2 15.7 12.6 10.4

Dividend yield (%) 0 0.5 0.5 0.5

PRICE PERFORMANCE

US execution promising; complex pipeline to drive growth

The company has achieved a market share of >15% in several molecules such as

gSensipar, gNexium and gPulmicort within 6–9 months of launch. The uptake in

gProventil has been promising so far, garnering ~16% share in the overall albuterol

market till Aug-21; the guidance of further market share gains is encouraging too.

While the first half of FY22 will be driven by base business recovery, H2 is likely to

see US gaining traction from launches such as gBrovana and gFosrenol. FY23 is likely

to be a big launch year with gAdvair, gAbraxane and gRevlimid all being multi-year

opportunities, followed by pipeline monetization beyond FY24.

Divi’s Laboratories (DIVI) is in a good position due to: i) volume ramp-up as a result of steady legacy molecules, new products and debottlenecking activities; ii) custom synthesis scale-up and diversified offerings such as contrast media and nutraceuticals; iii) operating leverage after full commercialisation of new capacities; and iv) China disruption—its key beneficiary. Besides, ~INR10bn incremental

Kakinada and Vishakhapatnam plant capex and molnupiravir opportunity would further help in sustaining growth momentum.

We increase our FY23E EPS by 10% to factor in molnupiravir opportunity. However, its current valuation prices in a 29% EPS CAGR for FY21–24E. ‘HOLD’ with a revised TP of INR5,410 (INR4,680 earlier).

FINANCIALS (INR mn)

Year to March FY21A FY22E FY23E FY24E

Revenue 69,694 88,733 1,11,173 1,30,465

EBITDA 28,599 38,253 49,185 58,204

Adjusted profit 19,875 27,703 35,904 42,569

Diluted EPS (INR) 74.9 104.4 135.3 160.4

EPS growth (%) 51.2 39.4 29.6 18.6

RoAE (%) 23.9 27.1 29.1 28.5

P/E (x) 64.5 46.3 35.7 30.1

EV/EBITDA (x) 43.8 32.8 25.3 21.1

Dividend yield (%) 0.4 0.6 0.8 0.9

PRICE PERFORMANCE

Growth engines laid out; expansion plans promising

The company has laid out six growth engines to enter the next phase of growth.

i) Backward integration of key molecules, focusing on expanding in profitable ones

such as mesalamine and cabidopa/levodopa. ii) Venturing into all sartans given no

NDMA issues. iii) Contrast media, wherein management believes it has just scraped

the surface. iv) Two long-term custom synthesis contracts. v) Large volume niche

molecules requiring specific technology expiring in 2023–25. vi) Key legacy generic

molecules to continue to grow at 10%. The aggressive INR25bn in capex over last

three years and ~INR10bn incremental capex in 1–2 years majorly towards the

Kakinada and Krishnapatnam port should be sufficient to meet its growth needs.

Even so, execution in contrast media and leadership in new molecules remains to

be seen.

Robust volumes; best-in-class margin and return ratios

DIVI’s focus on profitability, capital efficiency and investments in technology drove

its best-in-class gross/EBITDA margin of 67%/40%-plus and RoCE of 25%-plus.

Management is confident of maintaining it. China opportunities, aggressive capacity

expansion and backward integration make us confident of DIVI clocking an FY21–24E

revenue/earnings CAGR of 20%/25%.

Explore:

Outlook and valuation: Fully valued; maintain ‘HOLD’

We value DIVI at 40x earnings—a 50% premium to sector average considering its

best-in-class margins and returns ratios, strong cash flow and growth visibility—the

latter stemming from the company’s endeavours to capitalise on new opportunities.

We raise our FY23E EPS by 10% to factor in molnupiravir opportunity. Divis is the API

supplier to Merck and this being a branded product (USD700/10 pills), realizations

are likely to be quite handsome.

The stock is trading at 35.7x FY23E EPS, which fully captures the 29% EPS CAGR over

FY21-24E and potential benefit from capex. All in all, we retain ‘HOLD/SN’ with a

revised TP of INR5,410 (earlier INR4,680) while also rolling forward the valuation to

FY23E.

10

20

30

40

50

Sales Growth(%)

EPS Growth(%)

RoE(%)

PE(x)

Pharmaceuticals DIVI IN Equity

38,000

42,600

47,200

51,800

56,400

61,000

3,025

3,465

3,905

4,345

4,785

5,225

Oct-20 Jan-21 Apr-21 Jul-21 Oct-21

DIVI IN Equity Sensex

India Equity Research Pharmaceuticals October 4, 2021

We argue the road ahead for Dr. Reddy’s (DRRD) may not be smooth. i) Key launches are behind and launch momentum is fading. ii) Uncertainty around launch timelines of key products Sandostatin LAR, Levo, gCopaxone and gNuvaring; iii) High US contribution that is exposed to price pressure; iv) Domestic business remains in investment mode; acceleration awaited. v) The Sputnik opportunity is

shrinking, and its ramp-up is unlikely until domestic supplies builds up.

We await evidence of US pipeline monetization before turning positive again. Meanwhile, we keep ‘HOLD’ with a TP of INR5,150 (INR5,265 earlier) while rolling over to FY23E. TP breakdown: 25x core business, INR240/share from gRevlimid and INR32/share from Sputnik V.

FINANCIALS (INR mn)

Year to March FY21A FY22E FY23E FY24E

Revenue 1,89,722 2,23,099 2,52,347 2,90,567

EBITDA 44,682 48,189 65,105 85,427

Adjusted profit 23,679 29,785 42,436 57,409

Diluted EPS (INR) 142.9 179.7 256.1 346.4

EPS growth (%) (11.2) 25.8 42.5 35.3

RoAE (%) 10.5 16.1 19.7 22.2

P/E (x) 34.5 27.4 19.2 14.2

EV/EBITDA (x) 18.3 16.6 12.1 8.8

Dividend yield (%) 0.5 0.6 0.6 0.6

PRICE PERFORMANCE

US unlikely to surprise; launch momentum fading

Despite the launch of key assets, US has been underperforming due to rising pricing

pressure. DRRD’s market share is stagnant in existing products while uncertainty

persists on launch timelines for gRemodulin, sandostatin LAR, iron sucrose,

gCopaxone and gNuvaring. And since key US launches are behind, US is unlikely to

surprise. Furthermore, other lucrative launches are limited until gRevlimid in

H2FY23. DRRD is also looking to capitalise biosimilar opportunity with two in

advanced stages; this is likely to increase R&D spends. Fresenius’s potential US

pegfilgrastim launch is likely to gain traction only in FY23 post-Onpro-kind device

launch. We await evidence of investments fructifying and US pipeline monetization,

before turning positive again.

Domestic: In investment mode; acceleration awaited

DRRD is investing in new brands, OTC business (such as Celevida) in nutrition space,

rural areas and digital avenues. Management has indicated they would not shy away

from investing in India and Russia. However, domestic business is yet to reach pre-

covid levels. Opex in India and EMs, while welcome, are yet to bear fruit. Sputnik V

could add INR20/INR14 to FY22/23E EPS, but the opportunity is shrinking with delay

in supplies.

Explore:

Outlook and valuation: Not a smooth road ahead; maintain ‘HOLD’

Pipeline uncertainty, rising pricing pressure in the US, higher R&D and opex pose a

risk to our core earnings CAGR of 17% over FY21–24E. We reiterate ‘HOLD/SN’ with

a revised TP of INR5,150 (earlier INR5,265) while rolling forward the valuation to

FY23E. Our TP is based on 25x FY22E EPS and INR240 from gRevlimid NPV and INR46

from the Sputnik opportunity. We have reduced FY22/23E by 8%/5% to account for

lower Sputnik sales and US price erosion.

10

15

20

25

30

Sales Growth(%)

EPS Growth(%)

RoE(%)

PE(x)

Pharmaceuticals DRRD IN Equity

38,000

42,600

47,200

51,800

56,400

61,000

4,200

4,480

4,760

5,040

5,320

5,600

Oct-20 Jan-21 Apr-21 Jul-21 Oct-21

DRRD IN Equity Sensex

India Equity Research Pharmaceuticals October 4, 2021

We remain neutral on Glenmark as signs of operational improvement in core business await value unlocking in other parts. Domestic footprint is strong and US launch trajectory has improved, while GLS listing should help pare down debt. We await Ichnos fund-raising, NCE partnership and Ryaltris roll-out.

We forecast 8%/5% FY21–24 revenue/PAT CAGR. gSpiriva EU launch; gBrovana, theophylline in the US are likely to be partly offset by price erosion. While GLS proceeds would offset debt, debt repayment from organic cash flow proceeds is to be seen and with Ryaltris delay and no progress on Ichnos fund-raising, we reduce multiple marginally to 17x (from 18x). Maintain ‘HOLD’ with a TP of INR570 (from INR630).

FINANCIALS (INR mn)

Year to March FY21A FY22E FY23E FY24E

Revenue 1,09,440 1,22,107 1,26,199 1,36,061

EBITDA 20,845 22,486 22,315 24,281

Adjusted profit 9,393 9,717 9,649 10,796

Diluted EPS (INR) 33.3 34.4 34.2 38.3

EPS growth (%) 24.7 3.4 (0.7) 11.9

RoAE (%) 14.8 12.3 10.6 10.9

P/E (x) 15.3 14.8 14.9 13.4

EV/EBITDA (x) 9.4 8.0 7.8 7.0

Dividend yield (%) 0.5 0.5 0.5 0.5

PRICE PERFORMANCE

Still awaiting execution; awaiting triggers to play out in H2FY22

GNP’s core business promises aplenty: the company clocked >12% growth in key

therapies in India such as cardiac, anti-diabetic and respiratory driven by niche

launches and market penetration. Going forward, India is expected to clock double-

digit growth. Similarly, past couple of quarters have seen niche launches such as

gBrovana, theophylline and gQudexy, among others, but double-digit growth is

elusive as the company grapples with price erosion. gSpiriva is a promising launch,

but execution in the EU remains to be seen.

Specialty unlocking awaited

GNP has invested ~USD700m in its innovation business to date, and intends to raise

capital for Ichnos to fund the pipeline. While we note management’s efforts to

expand into NCEs, it has had limited success in partnering ISB 830, ISB 880 and ISC

17536. Before we turn positive, we await signs of better execution in the form of

gSpiriva and Ryaltris ramp-up in the EU, Ryaltris’s US approval and launch, and fund-

raising in Ichnos. While INR8bn from GLS proceeds is welcome, whether

management can generate enough organic FCF to pay off further debt remains to be

seen. Thus, while potential is aplenty, we await triggers to play out before turning

more positive on the stock.

Explore:

Outlook and valuation: Challenges persist; maintain ‘HOLD’

Though GNP is trading at a discount to peers, limited growth drivers and visibility on

free cash flow and a highly leveraged balance sheet limit upside potential. Hence,

we maintain ‘HOLD/SN’ with a revised TP of INR570 (17x Mar-2023E EPS; earlier

INR630).

0

10

20

30

Sales Growth(%)

EPS Growth(%)

RoE(%)

PE(x)

Pharmaceuticals GNP IN Equity

38,000

42,600

47,200

51,800

56,400

61,000

425

480

535

590

645

700

Oct-20 Jan-21 Apr-21 Jul-21 Oct-21

GNP IN Equity Sensex

India Equity Research Pharmaceuticals October 4, 2021